?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This study is relevant since the formation of methodologies to improve the efficiency of innovative leasing-based companies is vital since the leasing form of financing are significant in updating the fixed assets of small and medium enterprises. The aim is to create an original leasing tool to improve the efficiency of innovative companies. The study uses comparative analysis, economic and mathematical modeling of synthesis, and graphical methods of data processing. Methodology to use leasing tools to improve the efficiency of innovative enterprises are presented. The result is the method of calculating lease payments for operating leasing regarding both the method of calculating depreciation based on the sum of years and the amounts of insurance payments for financial and property insurance. This method allows those who uses operational leasing to vary the indicators that form the lease payment through a variable coefficient of the depreciable part of the leasing property.

Introduction

Arising at all stages of the reproduction cycle, innovations differ in typology, origin, purpose, degree of novelty, subject-content structure, level of distribution, and impact on economic processes.

Thus, innovative activity is not a single act of introducing innovation, but a purposeful system of measures for the development, implementation, mastering, production, diffusion, and commercialization of innovations. Innovative activity can be represented as a process of creativity and creating innovation. It is implemented as a maximum of innovative alternatives, innovative needs and entrepreneurial efforts.

The complexity of the innovation process gives special complexity to the methods and techniques of innovation management: innovative processes as an object of management possess uncertainty, multivariance, and are inherently probabilistic (stochastic). In turn, this determines the specifics of the methodology and organization of innovation management. Driven by innovation, structural transformation of the economy are also involved in the system of innovation management objects (Khoreva Citation2017).

Innovation activity consists of a number of activities that make up a single logical chain. Each link of this chain and each stage of this activity are subject to their own logic of development, laws and content. Together, scientific research, R&D and engineering, investment, financial, commercial and production activities are subordinate to one common goal: the creation of innovation. Therefore, innovation can not be reduced to just one of the components but should be considered as a set (Barykina et al. Citation2017).

In order to examine the components of innovation, one should refer to the definition and data of Federal State Statistics Service (Rosstat).

According to Rosstat, innovation is the activity related to the transformation of ideas (usually, results of scientific research and development or other achievements of science and technology) into either technologically new or improved products or services introduced on the market, or new or enhanced processes or methods of producing (or transferring) services used in practice. Innovation involves a whole range of scientific, technological, organizational, financial, and commercial activities, and they lead to innovation in their entirety only (Gazman Citation2017).

At the same time, innovative products, works and services include the ones that are new or technologically modified over the past three years.

Innovations include the following components:

– technological innovations as the final result of innovative activity. It is embodied either in a new or improved product or service introduced in the market or a new/improved process or method of producing (transferring) services used in practice;

– product innovations that include developing and implementing technologically new and significantly improved products;

– process innovations that include developing and implementing technologically new or significantly improved production methods, including transmission methods;

Experts say there are two types of technological innovations in industrial production and the service sector: product and process innovations.

The introduction of a new product (service) is that radical product innovation, the intended application of which, as well as its functional characteristics, properties, design, or used materials and components, significantly differ from previously produced products (services). Such innovations can be based on fundamentally new technologies or on a combination of existing technologies in their new application.

Technological improvement of a product/service affects an existing product the quality or cost of which have been significantly improved by using more efficient components and materials, or by partially changing one or several technical subsystems (for complex products).

Process innovations are usually aimed at improving the efficiency of production or transfering the existing products. Besides, it may also be intended for the production and delivery of technologically new or improved products that are not produced or delivered using conventional production methods.

– marketing innovations. These are already implemented new or significantly improved marketing methods that cover significant changes in the design and packaging of goods, works and services, their presentation and promotion in the sales market; formation of new pricing strategies;

– organizational innovations. It is the implementation of a new method in running a business, organizing jobs, or organizing external relations (DeGraba Citation1994).

This analysis and the study of laws on innovation in certain RF regions revealed that the objects of innovation are not only products (services) and processes, but also technologies. This study suggests the following definition of innovation. Innovative activity is a system of measures to create and implement objects of innovative activity (new or improved types of products(services), new or improved technology and new or improved processes) to make a profit or other useful result, to achieve competitive advantages, and to ensure sustainable development of the enterprise (Szymańska et al. Citation2015).

Materials and methods

Technological innovations include not only product and process innovations but also innovations in technology.

According to Rosstat statistics, innovative activity has several types as follows.

research and development;

tool preparation and organization of production covering the purchase of production equipment and tools, their adjustment, as well as in the procedures, methods and standards of production and quality control necessary to make a new product, the application of a new technological process and new technology;

production design, engineering and other developments, which do not belong to scientific research and development, of new products, services and methods of their production (transfer), new production processes, including the preparation of plans and drawings provided for the definition of production procedures, technical specifications, performance characteristics necessary to create the concept, development, production and marketing of new products, processes, technologies, and services;

purchase of materialized technologies: machines and equipment technologically related to the implementation of technological and other innovations;

purchase of non-materialized technologies, i.e. patents, licenses (contracts) for the use of inventions, industrial designs, utility models, disclosure of know-how, as well as technological services;

purchase of software for the implementation of technological innovations;

staff training and retraining for the introduction of technological innovations;

marketing research.

The implementation of these types of innovative activities depends on the company's innovation strategy aimed at:

creating a completely new market segment;

creating a product or solution that is a far cry from the existing ones on the market;

creating a product with higher utility and value for consumers;

creating a product that is attractive to the target market;

creating new processes or improving the existing ones, etc.

An analysis of the scientific studies of Professor Cristiano Antonelli shows that direction and rate of technological change in the global economy exhibit contrasting trends. Since the end of the XX century, the rate of technical change measured by productivity growth has been stronger if its direction is more labor-intensive. This puzzling finding can be explained using an interpretative framework that integrates the induced technological change and localized knowledge approaches with the Schumpeterian creative response. It is hypothesized that the globalization of both product and financial markets induces a creative response based on localized knowledge which accounts for the new knowledge- and labor-intensive direction of technological change that is more effective and productivity- enhancing than capital-intensive innovations. The empirical evidence shows that a variety of processes have affected the rate and the direction of technological change in the global economy. It should be noted that since the beginning of the 21st century, total factor productivity (TFP) has increased at faster rates in several of the advanced countries where the labor share has increased. (Antonelli and Feder Citation2020).

This study focuses on the leasing form of financing since leasing is one of the most popular methods of improving the efficiency of innovative companies in the Russian Federation.

The leasing agreement has long been successfully used in countries with developed market (competitive) economies. Leasing is primarily understood as renting machines, equipment, vehicles, and industrial facilities. The leasing agreement is understood both from an economic and legal points of view. From an economic point of view, a leasing agreement is a credit transaction and a type of investment activity. From a legal point of view, a leasing contract is an independent contract that has certain components of civil law institutions, such as sales, rent, credit, and so on. For example, in the United States, the legal nature of a lease agreement is recognized as a lease. Therefore, the problem of defining it for the U.S. lawyers is reduced to the problem of distinguishing a leasing agreement from similar agreements, for example, from a sale with deferred payments (IQ Decision Citation2019).

As described by Ion Ionascu and Mihaela Ionascu the classical definition, a lease is a contract that gives the right to use an asset (the underlying) for a certain period of time in exchange for consideration. In a lease transaction, the lessee controls the use of the underlying during the term of the lease and has the obligation to return the leased asset to the lessor at the end of the lease term (IFRS 16, BC 28, according to IFRS (2016)). In the leasing model, it is the right to use an asset that is acquired (rights to use property, industrial equipment and plant, cars, aircrafts, office equipment, etc. – goods called generic fixed assets or tangible assets) in return for lease payments, with the option of buying the asset that was the subject of the lease at a residual value which takes into account previous lease payments. From this point of view, leasing is considered as an alternative to other sources of finance – equity and debt and can take several forms: operating lease, the finance lease and lease-back (Ionașcu and Ionașcu Citation2018).

Leasing in foreign countries is an established tool for the development of the country's economy. Today, it is easy to spot a trend common to all Western companies (Barykina and Velm Citation2019).

Organizations focus on their main activities freeing themselves from excess property. This allows companies to choose more flexible approaches to the current state of economy.

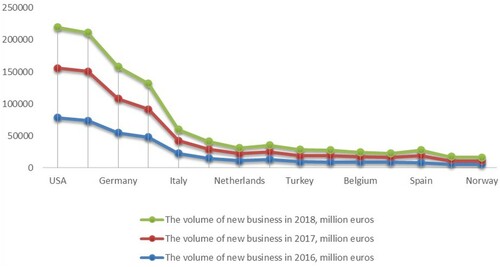

Consider the positions of foreign countries in the leasing market in .

Figure 1. Positions of foreign countries in the leasing market (mln EUR) (Leading financial technologies Citation2018).

Despite the economic crises of many countries, leasing is gaining momentum, but this is more typical for developed countries. The largest market share in the development of the global leasing business belongs to three key regions: North America, Europe and Asia.

According to the White Clarke Global-2018 statistics, the state of the leasing industry in the leading countries of the world shown in reveals the rating of countries for the development of new leasing business for the last three years (2016–2018). The leasing industry continues to grow significantly, which means that companies are introducing new and innovative forms and methods of financing equipment around the world. shows significant growth in Europe and America, which account for about 50%.

The reason for the widespread use of leasing in developed countries is a number of advantages it proposes:

The leasing company can get financing at lower rates or offer more favorable financial terms;

leasing involves one hundred percent financing of the investment project and does not require immediate start of payments. Lease payments usually start after the property is delivered to the lessee;

possible reduction of currency risk by fixing the interest rates on leasing;

the risk of equipment obsolescence falls entirely on the lessor. The lease provider has the ability to constantly update their equipment;

fixed lease rates;

tax benefits for leasing may be greater than similar benefits for capital expenditures at the expense of own funds.

In the Russian Federation, the development rate of the leasing market lags behind the needs of the economy, so the demand for such services is not fully met. However, the future development of leasing is more likely to be positive, since time is the key factor.

In the Russian Federation, there is a number of factors that hinder the development of the leasing business. The general reasons include (Nechaev and Antipina Citation2015):

contradictions in the leasing legislation regarding the subject of leasing;

low awareness of business entities about all available advantages of leasing operations;

unwillingness of financial and credit institutions to carry out additional work on introducing leasing operations (preference is given to lending);

the difficulty of predicting the leasing percentage, as well as the leasing premium;

lack of specialists who are aware of the intricacies of leasing operations;

weak development of secondary equipment markets.

The specific reasons are:

lack of sufficient available funds for long-term investments, the main part of which is accumulated in the European part of the country;

the weakness of local leasing companies, as well as the reluctance of large Russian leasing companies to move to the regions of the country due to the complexity of risk assessment, especially when working in ‘narrow’ market segments;

‘fictional’ leasing: some regional leasing companies are in-house companies of large corporations and are established to minimize taxes;

weak participation of regional authorities in the development of leasing business in specific regions.

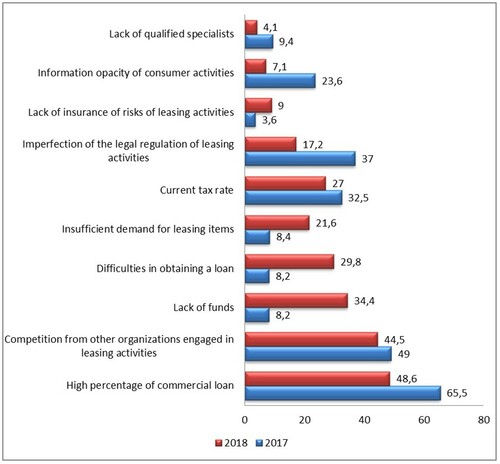

The factors that negatively affect the activities of organizations in financial leasing for 2017 to 2018 are shown in .

Figure 2. Factors that negatively affect the activities of organizations in financial leasing (RAEX rating agency Citation2020).

Analyzing the factors shown in it should be noted that in comparison with 2017, in 2018, the negative indicators that directly affect the economic situation in the country have increased. Namely, it is high percentage of lack of financial resources and getting a loan. Based on this, the demand for leasing items decreased from 8.4% to 21.6%. State support measures would solve this situation and could become the most effective for the sustainable development of the process of industrial modernization using leasing.

The main goal of financial leasing management is to minimize the flow of payments for servicing each leasing operation. One of the main disadvantages of leasing that reduces its economic efficiency is the low level of methodological elaboration of calculating lease payments.

Another factor that hinders economic growth is the depreciation of fixed assets of organizations in Russia. The process of updating them is financed mainly by retained profits of enterprises and is constrained by a lack of available debt capital. Leasing as an alternative financing mechanism can play an important role in fulfilling this strategic task facing the Russian economy, like in re-equipping the fixed assets of industrial enterprises.

Having compared the development of the Russian and American leasing markets, it becomes clear that the United States is a leader in leasing operations. In the Russian Federation, operational leasing is developing at the moment. There are no flexible payment patterns, leasing is not focused on the activities of large banks, there is almost no state support, while all the listed leasing criteria have long been developed and applied in America. Also, there are no sanctions in the United States. Every year, the American leasing market shows an average growth of 5–10% in aviation and other areas of leasing. In the Russian Federation, only transport leasing is stable. Macroeconomic and foreign policy factors influence the dynamics of leasing development in the RF (Dogan Citation2016).

In Europe, the market value is much bigger than the Russian one. Of course, the Russian leasing market is also trying to develop at full speed, doing everything possible to attract new customers. At the same time, this sphere perfectly survived the crisis and quickly recovered, continuing its victorious march. The volume of new business is constantly growing, but, unfortunately, this is not enough to even approach the European level.

Next, this paper compares the international and Russian leasing practices in .

Table 1. Comparison of leasing practices in the Russian Federation and abroad.

In North America, Europe and other foreign countries, leasing is actively developing in construction and commercial real estate. In some countries, it covers residential real estate. Leasing operations in these sectors are subject to additional tax incentives, which arouse the interest of lessors. Leasing of aircraft and helicopters, ships and barges, lifting and transport equipment, computer equipment, medical equipment, and large industrial equipment is rapidly developing in foreign countries. The feature of leasing in France is that land plots can be leased, while in Russia land plots and other natural objects cannot. Currently, the Russian Federation has a highly developed agricultural leasing industry. The other industries are involved in leasing but are not developed as well as abroad. For the development of leasing of all industries, first of all, they need state support for the entire industry of the Russian Federation

It should be noted that in the context of current economic state and financial instability, the formation and development of industrial enterprises, attracting credit funds or other modern methods of investment do not always have a positive result due to increased rates. Leasing becomes the most rational and efficient way out. When comparing a loan, rent, or lease, only the amount of payments and interest rates are taken into account. This is not decisive in determining the benefits of a particular form of financing. In leasing, is it possible to significantly save and reduce the tax burden, the amount of which would remain for a long time after the termination of all payments under the contract (Hogarth Citation2012).

There are many methods for leasing operations, such as Thanawath Niyamosoth suggested mathematical model is formulated and a numerical procedure is developed for finding the optimal period of preventive maintenance actions and the optimal size of buffer stock to minimize the total expected costs considering both a lessor and a lessee over a lease period.

The proposed model gives better solutions than those where the maintenance cost to the lessor and the production inventory cost to the lessee are minimized separately (Niyamosoth and Pathumnaku Citation2018).

Athanasios Andrikopoulos and Raphael N. Markellos have developed a model of the dynamic interaction between price fluctuations in the leasing and car sales markets. The model involves a differentiated game between several competing types of firms that offer differentiated products for promising agents (European Federation of Leasing and Car Rental Associations).

Besides the leasing form of financing, the objective of the system to improve the efficiency of enterprises s to develop policies, procedures and methods that allow for planning and timely control of costs (Andrikopoulos and Markellos Citation2015).

Project cost management processes include the following:

Cost estimation – the process required to develop approximate values for the resources required to perform project operations.

Developing an expense budget – the process required to sum up estimates of the cost of individual operations or work packages to estimate the baseline by cost.

Cost management – influencing the factors that cause cost deviations and managing changes to the project budget.

Cost management is based on the cost management plan. It is a document that sets the format and defines operations and criteria for planning, structuring, and managing the project cost. A cost management plan is developed at an initial stage of project planning and defines a framework for each of the three cost management processes to ensure their efficiency and consistency (Weber Citation2014).

The cost management plan can be formal or informal, very detailed or generalized, depending on the requirements of the project participants. The cost management plan is contained in or is an auxiliary plan in the project management plan.

The plan covers only the processes related to estimating the cost of work and resources when preparing the justification and developing the project plan, i.e. the processes of cost estimation and developing the project budget. The cost management process belongs to the project implementation stage and is not considered within the framework of this study. Thus, when developing a cost management plan, two processes are implemented: cost estimation and development of the budget of expenditures.

Results

The need to consider foreign practices in implementing innovations in small business is determined by the fact that currently in the Russian Federation there are significant disparities between large, medium and small businesses. Moreover, they exist despite the fact that their interaction is based not only on mutual interests but also common goals. There are currently two niches in the global market where Russian companies feel quite confident: the first is energy resources and related products. The second is the production of goods that are more complex and of higher quality than the Chinese analogues, but at a price, lower than the European one and are produced in small innovative companies (Andreeva and Nechaev Citation2013).

In foreign countries, small and medium-sized businesses represent the main sphere of employment of the population, contribute to the development of innovative potential, search and implementation of new forms of production activities, as well as sales and financing. It is the innovation which is one of the main factors that allows getting specific benefits.

Foreign practices in an innovative small business can be divided into the following fields:

practices of state regulation;

practices of the creation of additional jobs;

practices of reducing administrative barriers;

practices of engaging universities;

experience in export-oriented business.

Small businesses are forced to constantly compete for their markets with large domestic and foreign capital. Small businesses need an effective support and incentive mechanism because of their instability and vulnerability, especially at the formation stage and during crisis periods of economic development. Therefore, it is necessary to improve the state regulation of small businesses in the Russian Federation in:

Creating a competitive environment;

Creating conditions for a steadily developing supply of goods and services produced on the basis of innovation;

Stimulating and generating demand for innovative products;

Forming organizational and market infrastructure of entrepreneurship.

Ensuring social orientation of the formation and development of small businesses:

Providing state support in financing companies.

The practices of developing countries show that the main methodological requirements for organizing state support of small business are non-concentration of resources at the disposal of one person. Also, there is a the need to highlight the areas of small innovative businesses that have priority from the viewpoint of public interest and to create them particularly favorable conditions for development. It is recommended to widely use the program-oriented approach in Russia. It involves implementing various targeted programs to support small innovative businesses at the federal and regional levels.

The foreign practices of such countries as the United States, Canada, Italy, Argentina, and Brazil also demonstrates that it is possible to efficiently combine a simplified tax system for individual entrepreneurs and family businesses with a tax system for certain types of activities in the form of unified tax on imputed income.

In total, in Western Europe, more than 20% of investments in production assets are currently made through leasing financing. At the same time, up to 80% of the leasing business in Western Europe is located in the U.K., Germany, Italy, and France. The transition to market development in Hungary, the Czech Republic, Slovakia, and other Eastern European countries (as well as the CIS countries) opened up new opportunities for leasing business.

Some Western European countries like Great Britain, Germany, and Denmark, have not adopted special legislation on leasing, but implement it within the framework of ordinary commercial law. Apart, France, Portugal and Sweden have special legislation that specifies mainly the rights of the lessor and their relationship with the producers of the leased property.

Being a specific form of economic relations, leasing is reflected in a legal document that covers the necessary instructions, the law of trusts, the contract of sale, the amount of the lease payment, and other aspects.

France, Belgium, and Italy stick to the concept of an economic owner, while Great Britain, Ireland, the Netherlands, and the United States support the concept of a legal owner. In addition, some Western European countries occupy an intermediate position in legal terms, having elements that are characteristic of both one and other legal systems in their legislation.

State regulation of leasing activities in each country has its own peculiarities. Where leasing is a specific function of banks (Italy, France), state authorities not only regulate banking activities but also exercise control over leasing. In the U.K. and Germany, banks control only the part of leasing operations that are carried out by their subordinate structures. In France, all leasing activities are strictly regulated by the state on a par with banks. In other countries, the management of leasing activities is significantly simplified compared to banking operations (Destan Citation2017).

The laws of Italy, the United States, and France provide special requirements for the leasing mechanism. Leasing agreements are subject to registration in the judicial authorities in order to notify certain persons, provided by law, about the owner of the property being leased, etc.

The practices show that specific legislation does not determine the development of leasing: it is the country's macroeconomic conditions that dominate, as well as state support for investment activities and leasing as its important form. The most favorable conditions for the leasing market are created in the U.K., Germany, Ireland, Norway, and the United States. For example, in Ireland, to encourage leasing, the leasing companies are provided with government subsidies, are granted the ability to use the accelerated depreciation regime and other benefits, which have had a beneficial effect on the leasing market. As a result, Ireland has become a world center for aircraft leasing. There is an international center for financial services and other enterprises.

Treating leasing as a circular business model for sustainable development, involving the sale of a service and the recirculation of the good (Ghisellini, Cialani, and Ulgiati Citation2016; Guldmann Citation2016; Korhonen, Honkasalo, and Seppälä Citation2018), brings novelty to the fact that the producer or the supplier, who remains the owner of the asset throughout its useful life, attempts to control the leased assets at the end of the (first) use period for the renewal, refurbishment, remanufacturing of the product and recycling of the materials. So, within product-service systems, such as leasing and renting, a company offers the customer access to the product, but retains the property, and at the end of the life of the asset, the lessor recovers it for remanufacturing or recycling as raw materials, thus diminishing the impact on the natural environment. Therefore, in a leasing transaction, the ownership of the asset is split into two components: the legal property that remains with the producer/supplier, which is the “legal owner of the underlying asset” (IFRS 16, BC 22) and the economic ownership, which is transferred to the lessee (the user) in exchange for a series of payments. Thus, leasing becomes an alternative to the traditional “buy and own” model (Lewandowski Citation2016).

There are countries where certain restrictions prevent the development of leasing. For example, in Greece, leasing of real estate, trucks and buses is prohibited, and depreciation rates, which are regulated by the state, are also an obstacle. International Accounting Standards Committee (IASC) has developed some standards for leasing accounting, which are adopted by Belgium, Great Britain, Greece, Ireland, the Netherlands, the United States, Japan, and other countries. They are based on economic ownership of leased property. However, some Western European countries, as well as the European Union Commission and the European Leasing Organization, stick to the legal right to own leased property. Due to differences in property ownership, accounting systems and methods for calculating depreciation and taxes differ, since, according to the economic concept, the property should be accounted for on the lessee's balance sheet, and according to the legal concept, on the lessor's balance sheet.

North America has strengthened its position as the world's largest leasing market by new business volume. In this region, the U.S.A. is a key participant in leasing transactions, having almost a third of the global volume of new leasing business and sales of equipment (SOE).

The U.S. and Europe are vying for a high ranking in the global market: the U.S. accounts for 37.9%, while Europe accounts for 31.5% of the world's volume. The North American continent has strengthened its positions as the world's largest leasing company by new business volume. The United States is a key participant in leasing transactions, accounting for almost a third of the global volume of new leasing business and sales of equipment (SOE).

The U.K. and Germany take in second and third places in the world and dominate in Europe. The asset funding market in the U.K. showed strong results in 2015, with the U.K. industry capturing EUR 76,882 million in new business, thus demonstrating significant growth rates compared to 2017 and manifesting it as a strong position after the U.S. in the world rating. Germany shows growth in 2015 and loses it by 3.42% in 2016–2017. The leasing policy of German industries is one of the most developed in the world in terms of cars (58%) and trailers and trucks (16%), occupying the main types of leased property.

France continues to hold the fourth place in the world rating, despite the reduced growth in 2016-2017.

Italy ranks fifth in the rating with a volume of EUR 18028 million for 2017. Sweden is the sixth with its volume of EUR 12313 million.

In general, members of the European Union of Leasing and Finance Organizations recorded an impressive consolidated increase in new business of about 10%. Another growth worth noting for the past three years, according to statistics of the countries, include Netherlands, Poland, Switzerland, Belgium, Denmark, Spain, Austria, and Norway (Organization of Economic Cooperation and Development).

However, there are countries where the leasing industry has negative dynamics, for example, Africa. This is due to the continent's poverty, as well as the constant socio-political conflicts in the region.

The nature of the development of leasing activities in the world is currently determined by two main trends: increasing competition between creditors and world economic and financial globalization (Washburn Citation2017).

The state in the United States encourages the creation of venture capital firms and research centers. According to the National Science Foundation of the United States, the most efficient research centers and venture capital firms can be fully or partially funded from the federal budget for the first five years. The National Science Foundation of the United States plays an important role in investing in small firms, as it not only lends to innovative companies, but also provides grants – the gratuitous grant-in-aid (Sourrouille Citation2012).

Small businesses account for an increasing share of research and development (R&D) companies. Italy is the leader in the number of small and medium-sized R&D enterprises: it accounts for 65% of the total number of companies. Greece and Ireland have 50%, Norway – 48%. The smallest share of small and medium research enterprises is in Japan (7%). The OECD average is 17%. Firms with fewer than 50 employees in R&D counts are up to 20% in New Zealand, Norway, Greece, Australia, and Ireland. The common trend is the smaller is the country's economy, the greater is the share of R&D work performed by small and medium enterprises.

There is a wide variation in the level of government funding for R&D among the OECD countries. In Australia, Portugal, Hungary, and Italy, small and medium enterprises receive 2/3 or more of their R&D funding. In Australia, more than 50% of funds go to companies with fewer than 50 employees. On the contrary, in France, the United States, Germany, the United Kingdom, and Turkey, the state orders usually go to large firms.

Small and medium enterprises in the OECD countries are the main generator of jobs; they cover from 95 to 98% of the employed population in different countries. In 25 European countries, 23 million businesses with fewer than 50 employees give jobs to 66% of those employed in the private sector. In Italy, Portugal and Spain, small and medium enterprises account for the majority in the manufacturing sector (75% or more). Small businesses (up to 50 employees) account for more than 50% in Italy and Spain. This figure is significantly lower in Slovakia (15%), Germany and Ireland (22%).

It should be noted that due to the development of innovation, the export orientation of small and medium businesses in developed countries has increased. The reasons are as follows (Barykina et al. Citation2018):

First, there is a trend to involve small businesses in international technology transfer and investment exports. In Italy during the 1990s, the number of small business investors increased four-fold and reached 44.7% of the total number of Italian investors.

Second, the role of small businesses in foreign economic relations has increased towards the increasing intra-industry specialization of production. Many small businesses specialize in manufacturing and supplying various nodes, parts, and components to large companies, especially in the automobile industry, aircraft industry, and electronics. The share of supplies of small producers in Japan and France is from 20 to 50% of all manufactures goods.

Third, e-commerce is developing rapidly throughout the world. For small businesses, this form has become particularly attractive for lower costs, since it reduces the costs for the traditional methods of transmitting information, as well as the speed of its acquisition.

However, it should be noted that export potential of small businesses is not fully realized. Among the reasons that hinder the growth of small business exports are the lack of information on foreign market conditions, insufficient transparency of the export organization mechanism, monopolization and official red tape when promoting goods and services for export, ignorance of the requirements for the quality and standards of exported products, and insufficient number of trading houses and representative structures of small businesses abroad.

Tax policy is a powerful tool for stimulating innovation policy and increasing the sources of financing. When implementing innovative projects, tax liabilities are decreased through both direct reduction and the use of an indirect mechanism involving the application of deferred or installment tax payments, which is a hidden form of credit. Tax regulation methods are numerous and dynamic. The main ones are:

change in the total of tax revenues;

replacing some methods or forms of taxation with others;

differentiation of tax rates;

changes in benefits and discounts, their reorientation to their function, objects and payers (full or partial tax exemption, deferred payment or debt relief and refund of paid amounts).

It seems that to increase the efficiency of innovative projects, it is advised to:

extend the tax exemption in terms of VAT or introduce a reduced VAT rate to all companies that implement projects using various sources of financing, in particular, the leasing form of financing;

include the use of tax holidays for several years on profits from the implementation of innovative projects;

to introduce other income tax benefits (Nechaev and Antipina Citation2014).

Currently, the nature of international leasing development is determined by two main directions: globalization and increasing international competition in the financial sector. Competition is also intensifying within the leasing industry itself, leading to lessors looking for new competitive prerogatives. This is manifested in the cost differentiation of leasing products, rendering additional services, the consolidation of companies in order to find new areas, and creating new leasing offers.

Allocation of operational leasing is of practical importance since it allows companies of different parties to enter into a contract on mutually beneficial terms, taking into account their direct needs. At the same time, in order to strengthen and develop international relations and create the most favorable regulatory regime for leasing and development, it is expedient to consolidate the choice of applicable law. This legislative position would create the most favorable regime for regulating such agreements in practice.

The transition to operational leasing announces the beginning of the third stage of leasing. At this stage, lessors really need to take a risk regarding the residual value of the leased asset. The emergence of a secondary market for leasing objects (in the context of the financial and economic crisis) requires a transition to this stage. Since the lessor has difficulties in selling the equipment (transferring it to the next lessee) at the end of the lease term, this requires the activities in reselling the equipment returned to the lessor at the end of the lease term. As soon as the packaging is removed from the equipment, its cost falls by 20%, and for the first three months of use, it loses 30%.

Working with new types of risks makes lessors explore the market more actively, use more sophisticated methods in leasing marketing, be more careful about planning cash flows, and pay more attention to long-term multi-variant planning. The level of management of the leasing company rises to a higher level. Most Western European countries find themselves at the mentioned stage of development.

Thus, analyzing the experience of the leading world powers, it becomes clear that leasing plays an important role in the activities of companies. It has a huge impact on the economic growth of the country. Its role is especially noticeable in the transition period of economic development.

Next, it is advisable to present a financial instrument for improving innovative companies in order to increase their efficiency.

A method for calculating lease payments for operational leasing, taking into account the method of calculating depreciation on the sum of the number of years and including the calculation of the amounts of insurance payments for financial and property insurance may serve as such instrument.

This method is based on the method of calculating depreciation on the sum of the number of years, taking into account the amounts of insurance payments for financial and property insurance. The formation of lease payments occurs through a variable depreciation coefficient that changes the values of indicators.

It is necessary to distinguish between the concepts of the standard useful life of fixed assets and efficient use. The standard useful life is different due not only to physical deterioration, but also to functional depreciation, and the influence of other manufacturers of specific fixed assets in specific industries. Therefore, the term of transferring fixed assets to operational leasing is of great importance for both the lessor and the lessee. The term of transfer of fixed assets is important for the lessee since the lessee should purchase the leased property for the period when the efficiency of its use is maximum: it would give the maximum profit from its use. In turn, for the lessor, the term of transferring fixed assets is also of great importance, since the lessor can use the leasing property for re-transfer but to another lessee until they reach the full functional depreciation of this leasing property.

It is necessary to calculate the coefficient of the depreciable part of the leased property for operational leasing (KA), which would determine the depreciable cost of the leased property that is carried as an asset:(3.1)

(3.1) where η – the average value of the efficient use of fixed production assets; τ – the standard useful life of fixed production assets.

This study proposes a mathematical model for calculating the lease payment for each year for operational leasing using the method of calculating depreciation on the sum of the number of years that takes into account the insurance process.(3.2)

(3.2) where Π – the cost of the leased property to calculate the lease payments for operational leasing; m – the number of years until the end of the period depreciation during the operational leasing; N – the number of years of depreciation in operational leasing; α – the interest rate on the loan; β – is the interest rate of the commission; D – the amount of the additional service determined by the leasing contract; n – the amount of lease payments; γ – VAT rate; Ψ – the percentage of insurance in financial risk insurance; λ – the percentage of the guarantee in property risks insurance.

The model is presented as follows:(3.3)

(3.3) where t – year of the lease agreement; Q – term of the lease agreement.

This method is an efficient tool that allows contractors to use operational leasing to change the indicators that form the lease payment, taking into account the main types of leasing insurance through a variable coefficient of the depreciable part of the leased property.

Discussion

The main goal of financial leasing management in terms of attracting loan capital is to minimize the flow of payments for servicing each leasing operation. One of the main disadvantages of leasing that reduces its economic efficiency is the low level of methodological elaboration of calculating lease payments.

This work included the presentation of the problems that hinder the development of leasing in the Russian Federation and ways to resolve them in .

Table 2. Leasing problems and ways to resolve them.

When determining the method for calculating lease payments, one cannot ignore the current state of the Russian leasing market. Reduced access to financing, reduced customer solvency, a general decline in business activity and demand for leasing services as a result of reduced government funding for lessee companies, limited interaction with foreign businesses due to the situation on the foreign exchange market are the main risks that can cause serious damage to leasing companies both for ongoing projects and for the future ones.

However, in order to take a leading position in the leasing market in the future, it is possible to identify the focus areas. Thus, in the context of negative macroeconomic trends, the leasing market of the Russian Federation is stagnating due to low investment demand from major clients and the collapse of a number of investment projects. The current industry and product structure of the market would change in the medium term. The small and medium business segment also shows significant growth rates. The need to develop leasing in the Russian Federation, including the formation of the leasing market, is predetermined by the unfavorable state of the equipment stock and insufficient investment activity. The success of any leasing company depends on whether this organization is able to change and improve its performance. Optimization is important not only because it would reduce costs, but also because it would reduce the time for reviewing the inquiries. In other words, it would improve the quality of customer service and increase their satisfaction.

Conclusion

Despite the existing financial and technical problems, foreign suppliers of industrial equipment and various types of equipment show significant interest in the Russian market. The main activity of such companies is expected to be the export of equipment. To minimize risks in these transactions, it is advised to use modern advanced financial technologies.

When using leasing, Russian companies get a number of advantages that are unobtainable in other forms of financing for the modernization of production. Along with the fact that leasing is often almost the only available financing tool in cases of insufficient financing for equipment purchase, it provides a number of free benefits in the interests of all leasing participants, which makes it more attractive and affordable.

The main fear of transferring financial leasing agreements to operational ones is the deterioration of the customers’ solvency and the lack of state support for leasing companies. Therefore, the extension of regulation to operational leasing is not promising in the Russian Federation.

The state does not have the ability to finance every organization that needs to update production. Thus, organizations have to think independently about updating and replenishing non-current assets in order to remain competitive in the market.

References

- Andreeva, E. S., and A. S. Nechaev. 2013. “The Mechanism of an Innovative Development of the Industrial Enterprise.” World Applied Sciences 27 (13 A): 21–23.

- Andrikopoulos, Athanasios, and Raphae N Markellos. 2015. “Dynamic Interaction Between Markets for Leasing and Selling Automobiles.” Journal of Banking & Finance 50 (2015): 260–270. doi: https://doi.org/10.1016/j.jbankfin.2014.01.032

- Antonelli, Cristiano, and Christophe Feder. 2020. “The New Direction of Technological Change in the Global Economy.” Structural Change and Economic Dynamics 52: 1–12. doi: https://doi.org/10.1016/j.strueco.2019.09.013

- Barykina, Y. N., A. S. Nechaev, and N. V. Puchkova. 2017. “Analysis of Articles of Fixed Assets Renewal of Russian Business Enterprises.” In Advances in Economics, Business and Management Research. Proceedings of the International Conference on Trends of Technologies and Innovations in Economic and Social Studies, 551–556.

- Barykina, Y. N., N. V. Puchkova, and M. S. Budaeva. 2018. “Аnalysis of Innovation Activity Financing Methods in Russian Economy.” In RPTSS 2018 International Conference on Research Paradigms Transformation in Social Sciences, 120–127.

- Barykina, Y. N., and M. V. Velm. 2019. “Improvement of Methods and Forms of Investment of Innovative Activity.” Advances in Social Science, Education and Humanities Research, 793–796.

- DeGraba, P. 1994. “No Lease is Short Enough to Solve the Time Inconsistency Problem.” Journal of industrial economics 42 (4): 361–374. doi: https://doi.org/10.2307/2950443

- Destan, Halit Akbulut. 2017. “The Effects of Operating Leases Capitalization on Financial Statements and Accounting Ratios: A Literature Survey.” In Business Administration, Galatasaray University, edited by Mehmet Huseyin Bilgin, 3–10. Istanbul: Springer International Publishing AG.

- Dogan, Figen Gunes. 2016. “Non-cancellable Operating Leases and Operating Leverage.” European Financial Management 22 (4): 576–612. doi: https://doi.org/10.1111/eufm.12069

- Gazman, V. D. 2017. “Overcoming Stereotypes in Leasing.” Voprosy Ekonomiki 2 (2017): 136–151. doi: https://doi.org/10.32609/0042-8736-2017-2-136-152

- Ghisellini, P., Catia C. Cialani, and S. Ulgiati. 2016. “A Review on Circular Economy: The Expected Transition to a Balanced Interplay of Environmental and Economic Systems.” Journal of Cleaner Production 114 (7): 11–32. doi: https://doi.org/10.1016/j.jclepro.2015.09.007

- Guldmann, E. 2016. Best Practice Examples of Circular Business Models. Copenhagen: The Danish Environmental Protection Agency.

- Hogarth, J. Ryan. 2012. “The Role of Climate Finance in Innovation Systems.” Journal of Sustainable Finance and Investment 2 (3-4): 257–274. Accessed February 9, 2020. https://www.tandfonline.com/doi/full/https://doi.org/10.1080/20430795.2012.742637.

- IFRS 16 Leases Effects Analysis International Financial Reporting Standard. January 2016.

- Ionașcu, I., and M. Ionașcu. 2018. “Business Models for Circular Economy and Sustainable Development: The Case of Lease.” Transactions. Amfiteatru Economic 20 (48): 356–372.

- IQ Decision. 2019. Biznes i finansy. Accessed February 9, 2020. https://iqdecision.com/category/novosti/biznes-i-finansyi.

- Khoreva, I. V. 2017. “Current State and Prospects of Leasing Finance Development.” Economics 5: 82–86.

- Korhonen, J., A. Honkasalo, and J. Seppälä. 2018. “Circular Economy: The Concept and its Limitations.” Ecological Economics 143 (C): 37–46. doi:https://doi.org/10.1016/j.ecolecon.2017.06.041

- Leading financial technologies. “Global Leasing Report 2018”. Accessed February 9, 2020. https://www.whiteclarkegroup.com/videos/global-leasing-report-video-2018.

- Lewandowski, M. 2016. “Designing the Business Models for Circular Economy – towards the Conceptual Framework.” Sustainability 8 (1): 1–28. doi: https://doi.org/10.3390/su8010043

- Nechaev, A., and O. Antipina. 2014. “Taxation in Russia: Analysis and trends.” Economic Annals-XXI 1-2 (1): 73–77.

- Nechaev, A., and O. Antipina. 2015. “Tax Stimulation of Innovation Activities Enterprises.” Mediterranean Journal of Social Sciences 6 (1S2): 42–47.

- Niyamosoth, Thanawath, and Supachai Pathumnaku. 2018. “Joint Determination of Preventive Maintenance and Buffer Stock for a Production Unit under Lease.” Journal of Industrial Engineering and Management 11 (3): 497–512. doi: https://doi.org/10.3926/jiem.2578

- RAEX. Analytics (rating agency). Accessed February 9, 2020. https://raex-a.ru.

- Sourrouille, Diego M. 2012. “Leasing in the Middle East and Northern Africa (MENA) Region: A preliminary assessment.” Financial Flagship p. 16.

- Szymańska, Aleksandra, Stijn van Puyvelde, and Marc Jegers. 2015. “Capital Structure of Social Purpose Companies – a Panel Data Analysis.” Journal of Sustainable Finance and Investment 5 (4): 234–254. doi: https://doi.org/10.1080/20430795.2015.1089829.

- Washburn, Kevin. 2017. “Explaining the Modernized Leasing and Right-of-Way Regulations for Indian Lands.” Legal Studies Research Paper Series Research Paper No. 2017-10.

- Weber, Olaf. 2014. “The Financial Sector's Impact on Sustainable Development.” Journal of Sustainable Finance and Investment 4: 1. doi:https://doi.org/10.1080/20430795.2014.887345.