ABSTRACT

Covid-19 recovery efforts via public and private finance should not support assets and companies that are incompatible with the Paris Agreement. Yet even before the current crisis, there was a lack of agreement about what investor portfolio or bank loan book alignment with climate change outcomes actually means, and what assets are (in)compatible with different carbon budgets and global warming thresholds. We need to clarify this urgently and embed it within decision-making frameworks. Assessing (in)compatibility with a warming threshold should take account of carbon lock-in. We also need to develop appropriate confidence levels for measuring (in)compatibility. The state of (in)compatibility changes under different circumstances and targets for alignment should be set in a way that explicitly acknowledges these uncertainties. A portfolio with a lower confidence level would be less desirable than one with the same level of alignment and a higher level of confidence.

Introduction

There are growing efforts to ensure that post Covid-19 recovery efforts are supportive of the transition to a net zero carbon economy and for stimulus and bailouts to be aligned with the ambitions of the Paris Agreement. But all this enthusiasm and interest will come to nothing for the climate unless stimulus and bailout finance provided by governments, as well as private finance, are aligned with climate objectives. We must guard against deploying public finance or encouraging private finance in a way that supports assets and companies that are incompatible with Paris. This would build up climate risk and is essentially robbing Peter to pay Paul.

Even before the current crisis, there was a lack of agreement about how finance actually contributes to the realisation of the Paris Agreement. There remains a poor understanding of what investor portfolio or bank loan book alignment with climate change outcomes actually means, and what assets are (in)compatible with different carbon budgets and global warming thresholds. We need to clarify this urgently and embed it within decision-making frameworks to ensure we do not undermine long term climate outcomes through misdirected Covid-19 recovery capital allocations.

(In)compatibility with Paris at the right level of confidence

Whether an individual asset or a company’s or portfolio’s constituent assets are (in)compatible with a global carbon budget for a Paris Agreement aligned warming threshold (i.e. a ‘well-below 2°C’ carbon budget) depends on how much of the global budget is left and how much of this is allocated to the sector in which the asset(s) is/are located. It also depends on anticipated utilisation of the asset(s)and its/their carbon efficiency.

These complexities are smoothed over in current attempts to set targets for asset, company, or portfolio (in)compatibility with the Paris Agreement, such as Science-based Targets (SbTs). For example:

Targets are set assuming carbon budgets are fixed, and targets are set for assets, companies, or portfolios without regard to the fact that the remaining carbon budget will depend on what peers do and how our scientific understanding of the climate system improves.

Targets are often straight-line from the present until 2050, assuming progress happens linearly and that each change is of equal difficulty. We know that early reductions may be much easier than later ones.

Targets focus on tracking changes in annual carbon intensity or emissions and ignore Committed Cumulative Carbon Emissions (CCCEs) or ‘carbon lock-in’, the fact that assets already operational or planned commit us to future emissions and result in path dependency.

A better approach for assessing (in)compatibility with a warming threshold must therefore take account of carbon lock-in and the interactions between the stock of carbon in the atmosphere and the annual flows, acknowledging that to achieve any warming threshold requires net zero emissions globally and across all sectors.

Carbon Lock-in Curves (CLICs) resolve these issues by objectively assessing the carbon budget implications of current and planned assets. CLICs create a way to order, optimise, and represent portfolios of assets based on their committed emissions or future ‘carbon lock-in’. Cumulative committed emissions across assets are compared to carbon budgets to determine which assets are (in)compatible with a given budget.

CLICs are built on a methodological approach that combines the concept of CCCEs with the concept of marginal abatement cost (MAC) curves. CCCEs are an estimate of the emissions that will result from an asset over the remainder of its expected lifetime (Davis and Socolow Citation2014; Pfeiffer et al. Citation2016, Citation2018). MAC curves provide a method of comparing specific abatement actions (Kesicki and Strachan Citation2011). MAC curves calculate the cost of specific abatement actions relative to a business-as-usual baseline. These abatement actions are then ranked using an estimate of the unit cost of emissions abated, thus providing a way of comparing the relative merit of each action (Huang, Luo, and Chou Citation2016).

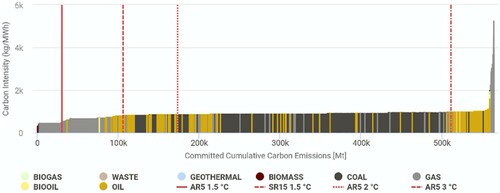

N.B. To improve rendering, assets with the same efficiency are aggregated and plotted as one. Therefore, each bar may represent the CCCEs of many individual assets. Power generating assets are ordered by asset efficiency (carbon intensity (kg/MWh)). The vertical lines represent the global carbon budget allocated to the global power sector for each warming scenario.

plots a global CLIC and shows all current and planned thermal power stations in the world ordered by carbon efficiency.

Figure 1. A global CLIC with all current and planned power assets.

The database of power generating units that has been used to build the CLIC consists of unique units merged from the Platts World Electric Power Plants Database (Q4, 2019), Global Energy Monitor’s Global Coal Plant Tracker (Q2 2019) and the World Resources Institute’s (WRI) Global Power Plant Database (Q2 2019). This merged database is a comprehensive dataset providing detailed information about power generating units globally. It consists of 84,433 emitting power units spread across 226 unique countries/regions, of these emitting power units 77,610 are operating, and 6,823 are either planned or under construction.

A CLIC plots the CCCE for each asset ordered by a particular ranking method (e.g. plant efficiency, marginal cost, plant age). The width of each column represents the CCCEs and the ordering variable is plotted on the y-axis. The carbon budgets are then plotted as a vertical line. Assets that are on the left of these vertical carbon budget lines are compatible with that carbon budget, given various assumptions, whereas assets that fall to the right of these budget lines are incompatible with the carbon budget for a given warming threshold.

Global carbon budgets are allocated to sectors Integrated Assessment Models on an industry fair-share basis. Caldecott, McCarten, and Triantafyllidis (Citation2018) developed CLICs for initial use in the power sector. The approach can be applied to any emitting asset, whether in the power sector or elsewhere, including but not limited to agriculture, automotive, aviation, cement, chemicals, healthcare, iron & steel, IT, mining, oil & gas, real estate, road & rail, and shipping.

The construction of global CLICs to assess Paris (in)compatibility for different sectors requires: (1) a global carbon budget for a Paris aligned warming threshold, (2) a proportion of this global carbon budget allocated to each sector, (3) assumptions of asset-level utilisation and efficiency (to calculate asset-level CCCEs within each sector), and (4) an ordering method (e.g. by marginal cost, age, efficiency, or some combination) for assets to see which assets are at or below the carbon budget line for a given Paris aligned warming threshold.

Trusted third parties can provide key assumptions and standardised metrics for 1–4 above. Computing the analysis consistently across all sectors with emitting assets is not particularly challenging if these assumptions and standardised metrics are provided. The main impediment is the availability of consistent asset-level data (3), as well as related data on marginal costs (4) that could be used for certain ordering approaches.

These data challenges are far from insurmountable and have already been largely addressed in some sectors (such as power). For sectors that currently lack good asset-level data, much of this data will be held by companies for their own assets.

We can also secure this data in different ways. Asset-level data resides in many different locations: it exists in existing company disclosures to financial markets, regulators, and government agencies (in multiple jurisdictions and in different languages); in voluntary disclosures; in existing proprietary and non-proprietary databases; in public and private research institutions; and in academic research. The challenge is finding the relevant sources, integrating the data, cleaning the data, and then of course making the data available for analysis. In addition, there is significant and exciting potential for new data from ‘big data’ and remote sensing to complement these existing datasets. We have never been in a better position to observe assets and what is going on in listed and non-listed companies at low cost, even if companies do not want to disclose.

There are existing collaborative efforts, such as the GeoAsset ProjectFootnote1, that aim to, ‘make accurate, comparable, and comprehensive asset-level data tied to ownership publicly available across key sectors and geographies’. In a way that is analogous to what the Human Genome Project achieves, they aim to produce universally trusted, transparent, and verifiable datasets of every asset in the global economy.

Efforts to provide key assumptions and standardised metrics, particularly for allocating global carbon budgets to sectors, and asset-level utilisation and efficiency numbers, can be enhanced by greater collective efforts. These efforts are a pre-requisite for much more accurate and robust measurement of (in)compatibility with the Paris Agreement.

But we also need to enhance our understanding of confidence levels associated with measuring (in)compatibility. As we have seen, we can assess whether an asset (or a group of assets at the company- or portfolio-level) are (in)compatible with a given carbon budget. This is a binary state: given certain assumptions asset(s) are either compatible or incompatible with a given carbon budget associated with a warming threshold.

The state of (in)compatibility could change under different circumstances (or given different assumptions). For example, if the size of sectoral carbon budgets reduce due to changes in our scientific understanding of the climate system, more assets will become incompatible. Or if assets are utilised less than previously thought due to falling demand and keeping all other factors constant, then more assets will be compatible. Or if more polluting assets prematurely close, then the remaining assets will have more budget between them, and more will be compatible.

We should set targets in a way that explicitly acknowledges these uncertainties (or sensitivities). For example, targets could be set as follows: in 2025 X% of my investment portfolio’s assets will be compatible with Y carbon budget with Z confidence level. Z could represent +/- some range of carbon budget uncertainty or be some other measure of confidence.

The key thing is that whatever the confidence level it would quantify simply how resilient your asset(s) or portfolio(s) level of Paris alignment is/are to changes to your asset(s) usage and efficiency, the sector(s) carbon budget, and the global carbon budget.

A portfolio that has X% of Paris alignment, but a much lower confidence level would be less desirable than one with the same level of alignment and a higher level of confidence. It also opens the prospect of third parties, including government and regulators, requiring certain levels of confidence in current and future levels of firm or financial institution Paris alignment.

It would then not be sufficient simply to say I will meet X target by X year, you have to be clear about how robust that target it, in terms of how likely it is for X% of your assets in a sector(s) is/are compatible with a given carbon budget.

This approach – carbon lock-in approaches plus confidence levels for given targets – has a number of benefits:

Honesty – it makes clear that some types of asset or ways of utilising an asset can never be compatible with a given carbon budget. It is mathematically impossible, or it is only possible under heroic assumptions about what other assets in the same sector or other sectors do and the availability of negative emission technologies. Under current approaches that track annual emissions, these truths are hidden. It also makes clear that a point could be reached where every asset and portfolio is incompatible (i.e. nothing is compatible) with a given carbon budget. It brings the need for collective action to deliver Paris home.

Ratchet – there is an in-built ratchet within the target. Meeting a 50% compatibility target for the power sector in 2025 with the same confidence level is harder than a 50% compatibility target in 2020. This is because all things being equal, there is less of a carbon budget to go around. This demonstrates and internalises the importance of early action.

Comparability – while levels of ambition, e.g. X% of my firm’s assets will be compatible with a Paris aligned carbon budget by 2025, 2030, 2035 and so on, can vary by firm and portfolio, they are easy to compare. If the same basic assumptions are used consistently and/or if the assumptions are disclosed, transparent comparisons are straightforward.

Scalability – Targets can be set for all assets across multiple sectors or be set for assets in specific sectors and target stringency can also vary sector by sector. For example, ‘ … in 2025 X% of my firm’s assets across all sectors we have exposure to will be compatible with Y carbon budget with a confidence level of Z’. Alternatively, ‘ … in 2025 X% of my firm’s assets in the [power][mining][shipping][…] sector[s] will be compatible with Y carbon budget with a confidence level of Z.’

Capex – Capex decisions matter. Planned assets and their impact on future carbon lock-in are not ignored but are explicitly factored in. This forward-looking aspect to this approach is critical for appraising (in)compatibility.

Seeing objectively at any given time what percentage of assets are (in)compatible with Paris and at what level of confidence, would be a powerful tool for encouraging and tracking alignment. If the data is available, there are no reasons, other than processing costs and reporting burdens, why these calculations cannot be updated regularly, perhaps even monthly or quarterly.

Conclusion and recommendations

These different aspects of public finance should ensure that their investment portfolios and loans books are increasingly compatible with Paris carbon budgets:

Infrastructure finance – the role of public financing in different stages of infrastructure projects, from development through to operation. Many countries have very well-established infrastructure banks, including KfW in Germany, Caisse des Dépôts in France, BNDES in Brazil, and the China Development Bank.

Business finance – the role of public financing in supporting company growth and development, from start-ups and SMEs through to large multinational enterprises.

Personal finance – enabling individuals to borrow for education/skills or home investments that provide public and private goods, e.g. energy efficiency.

Export credit – government guarantees and loans provided by Export Credit Agencies (ECAs) to help companies export goods and services.

Insurance – supporting insurance provision, particularly for risks that are uninsurable or prohibitively expensive to insure through private markets.

Development finance – delivering combinations of the above through Multilateral Development Banks (MDBs) and Development Finance Institutions (DFIs) focused on developing and emerging economies.

Public finance should be a first mover in the adoption of financial practices for Paris alignment. Public financial institutions also have a role to play in supporting private finance deliver the capital required to implement Paris, and the role of public balance sheets has significantly increased as a result of 2020 pandemic. These issues and changes merit an urgent review of the role of public finance and public financial institutions in Paris alignment. Failure to do so will mean we fail to secure alignment and will result in carbon lock-in and stranded assets on public sector balance sheets.

While central banks and financial supervisors have shown significant and growing interest in climate-related risks, they have shown much less interest in Paris alignment. The focus of the Network of Central Banks and Supervisors for Greening the Financial System (NGFS) has primarily been on micro-prudential supervision, and to a lesser extent macro-prudential supervision, followed by monetary policy and financial conduct.

Perhaps the area that has most overlapped with Paris alignment from a NGFS perspective has been growing concern about greenwashing and the mis-selling that could result. The UK Financial Conduct Authority has recently warned that, ‘[greenwashing] could undermine confidence in the green finance sector, leading to unsatisfied demand, reduced participation and competition and insufficient investment in the transition’ (FCA Citation2019, 27).

Financial supervisors should be much stricter at authorising and monitoring such product and fund claims. The proposals outlined here would help to address these greenwashing challenges.

There are also potential levers central banks and supervisors could pull to ensure private finance aligns with Paris, including:

Capital charges for finance provided to incompatible assets. This would go beyond aligning capital charges with climate-related risk and would overlay carbon budget considerations onto the setting of risk weights.

Targets for portfolio and loan book Paris (in)compatibility. Supervisors could ask firms to disclose voluntary targets or they could set mandatory ones. If targets were introduced, they should set out the ultimate destination in terms of the percentage of assets that will be compatible with Paris aligned global warming thresholds for every 5-year period starting in 2020 up to 2050 for a given confidence level. For voluntary target setting, supervisors could require standardised levels of confidence, as well as common metrics and assumptions, to ensure comparability. Supervisors could consider requiring quarterly or even monthly reporting for all supervised firms.

Risk budgeting is used to guide Asset-Liability Matching (ALM) and Strategic Asset Allocation (SAA). Supervisors could require that carbon budgets be factored into these processes, which would allow institutions to determine the most efficient use of a given carbon budget allocated to their institution. This carbon budget would need to take account of carbon lock-in (see previous sections) and could be introduced voluntarily or compulsorily.

In a similar way to how the Senior Managers Regime (SMR) is now used in the UK for climate-related risk management (see Bank of England Citation2019), Paris alignment could be added to this framework. This would create clear supervisory oversight and accountability of senior executive management.

Central banks and supervisors, together with policymakers and researchers, should work on these and other related ideas to understand their pros, cons, and delivery challenges. Some potential questions for the research community include: at what level should capital charges be set to make a material difference and how would capital charges set for climate incompatibility interact with those set for climate-related risk? How could carbon budgets be factored into ALM and SAA, are there analogous cases of values-based factors being included in such processes, and what could we learn from them? Can existing SMRs be used to integrate environmental and social objectives? If not, what changes in legislation or regulation are required and if so, where has this happened, and what can we learn?

Assessing (in)compatibility with Paris will also require researchers from a range of disciplines and subdisciplines to collaborate to understand and resolve a number of gaps. This includes resolving missing, out-of-date, or inaccurate data, particularly at the asset-level, and assumptions and metrics that can become standardised to ensure comparability. The latter is especially important for determining confidence levels associated with (in)compatibility. To drive adoption we also need to identify and deploy the most effective ways to communicate such metrics so that they are meaningful and intuitive for users.

These and other research questions have compelling pathways to impact and were mission critical before Covid-19. The crisis and the post-crisis recovery, given the sheer scale of stimulus and bailouts, requires us to accelerate work on them. To do the work both quickly and effectively we need to deepen nascent collaborative efforts between researchers, finance practitioners, policymakers, and regulators.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

References

- Bank of England. 2019. Supervisory Statement | SS3/19: Enhancing Banks’ and Insurers’ Approaches to Managing the Financial Risks from Climate Change.

- Caldecott, B. L., M. McCarten, and C. Triantafyllidis. 2018. Carbon Lock-in Curves and Southeast Asia: Implications for the Paris Agreement. Accessed January 2 2019. https://www.smithschool.ox.ac.uk/research/sustainable-finance/publications/Carbon-Lock-in-Curves-and-Southeast-Asia.pdf.

- Davis, Steven J, and Robert H Socolow. 2014. “Commitment Accounting of CO2 Emissions.” Environmental Research Letters 9 (8), 084018. doi: https://doi.org/10.1088/1748-9326/9/8/084018

- FCA. 2019. FS19/6: Climate Change and Green Finance: Summary of Responses and Next Steps. London. Accessed April 12 2020. https://www.fca.org.uk/publication/feedback/fs19-6.pdf.

- Huang, S. K., K. Luo, and K. Chou. 2016. “The Applicability of Marginal Abatement Cost Approach: A Comprehensive Review.” Journal of Cleaner Production 127: 59–71. doi: https://doi.org/10.1016/j.jclepro.2016.04.013

- Kesicki, F., and N. Strachan. 2011. “Marginal Abatement Cost (MAC) Curves: Confronting Theory and Practice.” Environmental Science & Policy 14 (8): 1195–1204. doi: https://doi.org/10.1016/j.envsci.2011.08.004

- Pfeiffer, A., C. Hepburn, A. Vogt-Schilb, and B. Caldecott. 2018. “Committed Emissions From Existing and Planned Power Plants and Asset Stranding Required to Meet the Paris Agreement.” Environmental Research Letters 13 (5). doi: https://doi.org/10.1088/1748-9326/aabc5f

- Pfeiffer, Alexander, Richard Millar, Cameron Hepburn, and Eric Beinhocker. 2016. “The ‘2°C Capital Stock’ for Electricity Generation: Committed Cumulative Carbon Emissions From the Electricity Generation Sector and the Transition to a Green Economy.” Applied Energy 179 (1st October 2016): 1395–1408. doi: https://doi.org/10.1016/j.apenergy.2016.02.093