?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Over the past few decades, there has been a sharp increase in interest by investment professionals to become more socially responsible with regards to their decision making relating to their choice of investments and overall make-up of their portfolios. This paper conducts various tests to establish a link between Corporate Social Responsibility (CSR) and Corporate Financial Performance (CFP). This paper adds a strategic management element by establishing various frameworks that corporations can include in the decision-making process and includes CSR and Environmental, Social and Governance (ESG) principles when making investment decisions. The sample chosen for this paper includes the iShares MSCI KLD 400 Social exchange traded fund (ETF), iShares Core S&P 500 ETF as well as firms that follow the Principles for Responsible Investing (PRI). Overall, there is no evidence to suggest that ethical ETFs outperform conventional ETF's however PRI following firms outperform those who do not follow the guidelines.

1. Introduction

There is an ever-growing trend towards the inclusion of Environmental, Social and Governance (ESG) considerations in the discussion of corporate sustainable responsibility (CSR) within the finance sector, especially for asset and fund managers. Such considerations include: improved access to debt financing, lower cost of capital through lower perceived risk’ and the impact of increased shareholder value on the ability to raise capital through debt and equity markets (Hopwood, Unerman, and Fries Citation2010), impacting access to both debt and equity finance for firms. To understand the overall significance of how incorporating ESG considerations within the financial markets has grown, we use the United Nations’ Principles for Responsible Investment initiative as a lens for analysis.

The PRI were designed to provide a common framework to help encourage financial companies to incorporate environmental, social and governance (ESG) criteria into their investment decision making and by adopting these principles – that were launched by the United Nations in 2006 – institutions can look to implement CSR. On a societal level, this initiative aims to promote a more stable and sustainable financial system (UN PRI Citation2015) and whilst there is no mandatory requirement for professional organisations to adopt the PRI, the number of signatories has increased from slightly more than 100 in 2006 to more than 2,701 in 2020 representing over $80 trillion in assets.

Key aspects of the initiative include responsible and sustainable decision-making but specifically, the disclosure on ESG issues into ownership policies and practices and ensuring that all signatories and members of the initiative are working together to enhance their effectiveness of implementing the six governing principles. But this is not possible just from the market and financial system, responsible investors who feel empowered to support and invest in institutions who incorporate ESG issues will strengthen and expand their core work and lead to responsible investors pursuit of long-term value and meaningful impact.

There is also evidence to suggest that the reputational benefits of environmental innovation and CSR performance can increase the market value of the firm as well as bringing operational benefits to financial performance (Quinche-Martín and Cabrera-Narváez Citation2020). For example, better environmental performance can improve revenue through better access to certain markets, differentiating products, diminishing costs through better risk management and relations with external stakeholders that can lower the cost of material, energy, cost of capital and labour (Semenova and Hassel Citation2008; Guoyou et al. Citation2013; Amber and Lanoie Citation2008).

Thus, it is very much in the firms’ interest to look into increasing CSR and ESG practices as much as possible to see direct benefits on Return on Asset (ROA), Return on Equity (ROE) and Market Value (MV), as well as indirect benefits such as a greater reputation which can boost revenue and add a greater level of importance within the market for the firm. As a result of this, it is also in the interest of the academic community to further investigate and explore the relationship between the social responsibility of firms and their financial performance.

Global warming, climate change and environmental degradation issues have increased public scrutiny regarding the role of firms as actors and agents that are part responsible for such issues. Corporate commitment to sustainability is increasingly evidenced by firms’ participation in voluntary risk assessment and reporting initiatives such as: The UN's Global Compact (UNGC), the FTSE4 Good Indices, the Global Reporting Initiative (GRI), the Dow Jones Sustainability Index (DJSI) or through the compliance to International Standards Organisations certification such as ISO 144001 and ISO 26000 (Kimbro Citation2013).

The ISO standards are a collection of quality management criteria with the sole purpose to ensure organisations meet the needs of customers and other stakeholders whilst operating within a regulatory framework. Adhering to such standards can result in increased CSR and therefore positively impact CFP. For the purpose of this paper, we will be defining Exchange-traded funds as financial innovations that may be considered as part of the index financial instruments category, together with stock index derivatives (Marszk and Lechman Citation2020).

This paper presents two frameworks, allowing firms to decide whether they are proactive or reactive with regards to the introduction of sustainable, ESG-leaning policies and practices and whether this results in them being labelled a sustainability champion or deviant. The paper uses a series of regression analyses to evaluate the financial monthly returns of 900 firms that use ESG metrics and subscribe to the sustainable initiatives such as the PRI against comparable firms that do not over a 10-year period. The paper also includes a variety of previous literature on the ever-growing topic of sustainable investment and the prospects of future research, as well as discussing how sustainability can be included in the capital budgeting process.

2. Literature review

Since the introduction of the concept of sustainable development by the report from the World Commission of Environment and Development in 1987, more companies have become aware of their responsibility in this matter (Peeters Citation2003). Various studies have empirically examined the relationship between corporate social responsibility and financial performance in terms of quantifiable returns, however there seems to be no consensus in the relevant literature in terms of direction (Przychodzen and Przychodzen Citation2015). It is vital to compare, contrast and highlight the differences in the literature concerning CSR and CFP, their realised implications as well as evaluate the literature of the subjects. It is critical to compare and contrast competing themes and studies on CSR as it is very difficult to define and can be prone to conceptual stretching, that is when a concept becomes distorted and the original concept does not fit the new cases. Scholtens (Citation2008), Margolis and Walsh (Citation2001), Ingio and Albareda (Citation2019), and Miralles-Quiros, Miralles-Quiros, and Nogueria (Citation2019) all state that it is very difficult to measure the sustainability of firms for this very reason. However, throughout this paper, the following two definitions of CSR can be considered and used interchangeably as a benchmark and reference point:

CSR is perceived as situations where organisations undertake social initiatives in support of the communities within which they operate, which goes beyond their interests as well as the requirements of law (Marszałek and Uryzsek Citation2020).

A business approach that creates long-term shareholder value by embracing opportunities and managing risks deriving from economic, environmental and social developments (DJSI Citation2012).

The table below shows a plethora of related studies on the issue of CSR and the implications it can have on CFP with the majority of academics finding that there is a positive correlation between a firm acting in a more sustainable manner and their overall financial performance. Statman and Glushkov in their 2009 paper found that when considering the Capital Asset Pricing Model (CAPM) and Fama-French three factor model that sustainability orientated innovation has a positive impact on both the financial performance as well as increasing competition within the market, highlighting that it influences on both a strategic and financial level. Clark, Feiner, and Viehs (Citation2015), found in their study of the cost of capital in American firms over a 26-year period that in 90% of cases, sustainability lowers the Weighted Average Cost of Capital (WACC) for a firm therefore, increasing the scope and access a corporation has to debt and equity markets. However, not all studies find the same results and whilst this paper extensively assesses the impact on Exchange Traded Funds, the impact is not limited to simply ETFs. Starks and Bialkowski in their 2016 study which reviewed the returns of mutual funds over a 12-year period noted that there was no difference between the Alphas of sustainably responsible and conventional mutual funds. It is also noted that sustainable investment performance is heterogenous worldwide, but there is a promising opportunity for investors to obtain superior adjusted returns in certain regions while incorporating sustainable investment practices (Cunha et al. Citation2019).

3. Methodology and data

This paper uses exchange traded funds (ETF) data collected by the KLD Research & Analytics group, the S&P 500 ETF as well as firms that follow the Principle for Responsible Investment strategies and those comparable firms who do not. Our final sample compromises of 900 firms, the data was collected over a 10-year period using monthly returns and although daily returns would have been preferred, due to the number of firms over that length of time, monthly was more suitable due to time and data restrictions.

Firms that appeared in both of the indexes were jettisoned from the sample size to ensure greater validity of the results. The main differentiating point being that some of the firms in the S&P 500 ETF may be considered as ‘sin stocks’ with poor ESG ratings so would not meet the requirements for the KLD 400 ETF. The variables used as proxies of financial performance were as follows: Total Return, Return on Equity, P/E Ratio, Market Value and Beta. A dummy variable was used to account for the difference throughout the years, the results of which are not shown due to constraints on space. All regressions were completed at the 90, 95 and 99% confidence intervals for validity checks and robustness regressions were also done to test the validity.

Correlation analysis and VIF tests were undergone to investigate the strength of the independent variables chosen and to test for multicollinearity. The VIF test results showed that there is no issue with multicollinearity as they are all <10, hence the regression using the variables as the predictor were not correlated with any other variable.

The model can be expressed with the following regression equation:

where: TR = Total Return; β1 = Natural log of Market Value; β2 = Natural log of P/E; β3 = Return on Equity; β4 = Beta;βYD is the dummy variable to represent the regression period (2009–2019)

4. ESG and investor impact

Many investors are attracted to sustainable investing due to their altruistic motives (Hartzmark and Sussman Citation2017; Riedl and Smeets Citation2017), the notion that investing their money in assets in ones which both aim to provide positive financial returns and also makes a positive impact in the wider world is something that is of great benefit to an increasing number of investors. As a result of this, banks and asset managers are catering to both these requirements, if not expectations by offering an increased amount of investment products where the apotheosis of their existence is on sustainability, responsibility and bringing about positive change (Kölbel et al. Citation2020).

Presently, most sustainable investment funds either exclude firms operating in harmful industries, i.e. ‘Sin stocks’ such as tobacco, firearms and gambling industries or focus on companies that historically performed well on ESG metrics. The work of Kölbel et al. focuses extensively on the work of financial return for the sophisticated sustainable investor. Assume that a social or environmental parameter P depends on other variables on the size and level of the company activity Ac. Company activity can refer to both a company's every day operations and to its products, services and consumers and the wider market in which they operate in. Then company impact, Ic is the marginal change in parameter P per unit of company activity Ac, integrated over the level of company activity. Equation (1) can look at the investors impact of a sustainable asset at a single moment in time, Equation (2) shows the same result over a longer investment horizon.

(1)

(1)

(2)

(2)

The work of Kölbel et al. aim to prove that through the equations, and in fundamentally different ways, investors can achieve investor impact. First, by growing the level of company activity; second by improving the quality of company activity. This is also supported in the current trends and requirements by the ESG-conscious investor on a company's behaviour, ensuring that the firm is compliant with various standards and voluntary frameworks – such as being compliant with the various ISO requirements and ensuring that the firm is not engaging in any activity that can compromise their status as a sustainability champion – a characterisation that will be discussed later in this paper.

5. Sustainability frameworks

Whilst it is of paramount importance to consider the impact that CSR and ESG can have on financial performance, it is of equal importance to discuss the strategic, qualitative means by which a firm can achieve such returns. By increasing reputation for corporate sustainability within the market place, firms can come to expect greater returns, as discussed in the literature review. Below are two corporate sustainability frameworks of which firms can utilise to evaluate whether they are proactive or reactive corporations in the arena of CSR – whether they are agenda setters or agenda followers and leverage their position to attract inward investment. The second corporate sustainability framework is an adaptation of Bowman's Citation1996 Strategy Clock, which allows the firm to explore the options associated with acting in a more sustainable manner. Strategic decisions which are made shape the image and reputation of the company, impacting their overall Perceived Sustainability Value (PSV) and Perceived Sustainability Value Dimensions (PSVD), which are characterised by four value dimensions which shall be discussed in this part of the paper.

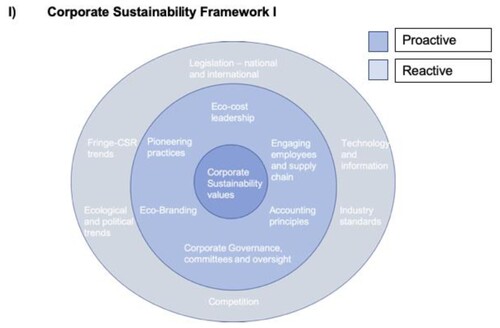

is a suggestive framework divided into two distinct categories that the management board of a firm can engage in order to become more sustainable based around the over-arching theme of corporate sustainability values. The first stage, proactive, are conscious actions that the firm can engage in order to act more sustainably, pioneer sustainability in the industry, help set trends within the sector and to better enhance the overall reputation of the firm. Such engagements include eco-cost leadership and management, one of the key competitive forces among the majority of prevailing enterprises (Biernacki Citation2015). Schatsky found in his study of executive sustainability involvement that 21% of the boards directly approve and oversee such objectives, 17% of vice presidents (VP) or senior VP and 62% of C-level executive actively review such policies.

Figure 1. Corporate sustainability framework I. Source: own work.

The second phase, reactive, focuses on indirect agents, actors and powers that the firm has to act in response to and contains actions and policies that may be out of their control. For example, the firm will have to directly respond to local and international governing bodies policies and legislation that will affect their eco-performance and policies. As a result of this, firms can seek to enhance their commitment to becoming proactive by enforcing high levels and standards to CSR commitment and strive to be the following three with regards to corporate social responsibility:

Industry leaders;

Agenda setters;

Government influencers and advisors on the topics and sub-topics.

The framework provides an insight into the scope of the vast number of variables that the contemporary firm has to be aware of with regards to how they go about their own business with regards to setting trends, agendas and influencing governments through CSR policy. Furthermore, they too are bound by such actors to confirm to their legislation that can constrain their own activities which may jeopardise their possibilities to act in a way in order to deliver a profit to their shareholders whilst appeasing stakeholders ().

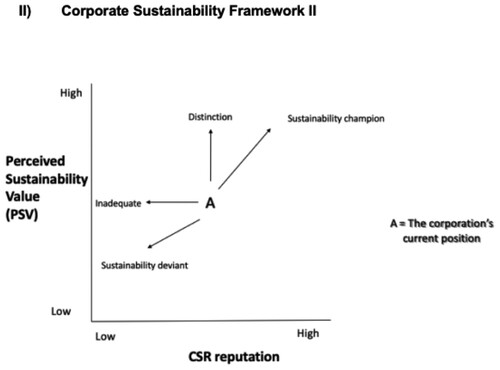

Figure 2. Corporate sustainability framework II. Source: own work adapted from Bowman's Strategy Clock.

Second, corporate sustainability framework, an adaptation of Bowman's Citation1996 Strategy Clock, has been established to include the options embedded in acting more sustainably for the firm. Strategic decisions which are made shape the image and reputation of the company, this impacts their overall Perceived Sustainability Value (PSV) and are characterised by the four Perceived Sustainability Value Dimensions (PSVD), detailed below:

Sustainability Champion

In this dimension, firms can become more sustainable through product, system and management innovations and structural changes as this embeds professionalism and paradigm-shifting thought processes. This relates back to the idea of the firm being proactive in their decision-making regarding CSR issues, engaging employees outside of board/senior levels of management and truly being the industry leaders by setting the agenda and industry standards. Companies that can be classified as sustainability champions include: Chr. Hansen Holding A/S, Kering SA, Neste Corporation and GlaxoSmithKline Plc based on a variety of factors including their carbon productivity score, CEO-average work pay ratio, percentage of women on boards and percentage of ‘clean’ revenues (Forbes Citation2019). As a result of this widely accepted label as leaders of sustainability within the industry, they can expect to see increased inward investment from ESG-investors as they are already shown to be and demonstrating the skills associated with the ‘ideal-sustainable investment’, e.g. the eco-cost leadership, subscription and adoption of ISO requirements and PRI methods and the distinct lack of interest to engage in behaviour that may deter the sustainable investor.

(II) Distinction

Firms can be classified as fitting into the distinction dimension if they show continuous dedication to sustainability via incremental improvement and changes implemented by a CSR-compliant board and engaged workforce. Firms characterised by distinction excel in reacting to the policies made by external actors and agents but are yet to pioneer their own proactive policies. Firms within this dimension are seen as pivotal companies with regards to implementing CSR policies and the employees are aware of the values that the firm has surrounding the issue.

(III) Inadequate

Companies within this dimension fall behind on CSR levels and standards as a whole, characterised more so by profit and resourced driven and will meet legal minimum requirements for CSR implementation with minimal desire or will to be proactive in their governance and policies. Firms in this dimension are associated with what socially responsible investors would refer to as ‘Sin stocks’, i.e. gambling, tobacco and firearms companies. Inadequate firms can move North or ideally, North West on the framework by engaging in sustainable practices, engaging the employees in more processes and establish sustainability committees within the enterprise.

(IV) Sustainability Deviant

Firms here show no palpable effort made or desire from management to increase CSR reputation or policies, the firm will meet legal requirements but struggle to not only be proactive in their approach, but would find it hard to cope reacting to the policies of governments, international bodies, NGOs, pressure groups and the overall general consensus and standards of corporate social responsibility. Companies are typically forced into this position based on industry requirements such as mining, chemicals and primary metal firms and fear that acting more sustainably can negatively impact profits.

6. Incorporating sustainability into the capital budgeting process

We have considered CSR from strategic management perspective through the two frameworks how firms can embed CSR into their corporate culture and identity. However, capital budgeting methods of businesses and how corporate sustainability can be included in accounting decisions must also be considered by the ethical firm. There is evidence to suggest that traditionally accepted and analytics frameworks and tools such as the Net Present Value (NPV), Discounted Cash Flow (DCF) and Internal Rate of Return (IRR) do not favour and perhaps even ‘punish’ sustainable investments (Hopwood Citation2009).

Capital budgeting techniques have evolved significantly during the past 20 years or so. Academic research suggests that before the 1980s, firms seldom used DCF and NPV methods; however, by the turn on the millennium, 75% of surveyed firms stated that they use both of these approaches to evaluating investments and capital budgeting decisions (Graham and Harvey Citation2001; Moore and Reichart Citation1983). Frequently used capital budgeting methods are constructed in ways that indeed can create bias against the selection of sustainable alternatives in capital selection (Kimbro Citation2013). Specifically, certain benefits and gains that may arise from sustainable projects might require larger investments which in turn, can require longer payback periods in order to develop a positive cash flow – dependent on the investment horizon and rate of return determined, this result can be undesirable to the investor.

It can be argued that discounting NPV techniques incorrectly assume that the advantages of future biodiversity preservation and ‘natural capital’ conservation will decrease in future years. In other words, it will be wrong to assume that the future benefits of a sustainable investment will be less valuable than the present benefits of conservation as the application of the discount techniques apply. As a result of this, the sustainability NPV method can be established and practiced to include ESG and CSR matters into the decision-making process.

In order to calculate the potential costs associated with each risky category of a project; the probability that each risk could materialise should be estimated – this is called the sustainability cost NPV. The potential cost of each risk is multiplied by its expected return to calculate the expected value associated with risk as it is critical to estimate when the risk may arise and the impact that may have on the end return of a project. For example, in the case of PPE the probability of risk materialising is as the asset gets older and depreciates in value. Once the sustainability NPV per project is calculated, aggregate the collective NPVs of all sustainability risks, subtract the sustainability NPV from the NPV calculation of each capital alternative to get the realised NPV which factors both sustainability, risk and timing.

Figure 1 Net Present Value (NPV) formula:

where: CF = Cash flow at point t; r = Discount rate or return from alternative investments; t = Time period

Considering sustainability in the accounting and capital budgeting processes can be seen as a proactive measure that firms can undergo which influences their sustainability levels, reputation, reduces the cost of capital and increase efficiency. Referencing the quantitative analysis too, it can be argued that firms who undergo such practices may financially outperform those who do not. Therefore, it is not only in the interest of the wider society and environment to consider such sustainable and ecological activities, but in the interest of the corporation too.

8. Development of the hypotheses

Our quantitative approach tests the relationship and significance between corporate social responsibility and financial performance in exchange traded funds (ETFs). The paper explores financial benefit of Principles for Responsible Investing (PRI) guidelines, by testing the relationship between ethical and financial performance. Murray et al. (Citation2006), Miralles-Quiros, Miralles-Quiros, and Nogueria (Citation2019) find a positive relationship between corporate social responsibility, sustainable exchange traded funds and corporate financial performance. Brammer, Brooks, and Pavelin (Citation2006), Plinke and Knorzer (Citation2006) found that the returns for socially responsible investment exchange traded funds are worse off than that of conventional funds. This paper uses the total return as the measure of financial performance and the null and alternate hypothesis are stated below.

The below hypotheses were the result of a culmination of following up from various academic studies that research the impact of sustainability and following ethical guidelines and principles on financial performance. Scholars have noted a positive correlation between firms who follow sustainable-drive initiatives such as the UN's Global Compact (UNGC), the FTSE4 Good Indices, Down Jones Sustainability Index (DJSI) or through the compliance to International Standards Organisations Certification such as ISO 144001 and ISO 26000 and overall financial performance (Kimbro Citation2013).

As a means analysing the uncertainty of the models and regressions, a robustness test was undergone to test the sensitivity of each variables and to increase the validity of inferences. The purpose of the robustness check was to explore how certain fundamental regression coefficient estimates behave when the regression arrangement is revised by adding or removing regressors.

H10: Ethical ETFs returns are no different from the returns of conventional funds.

H20: Returns will be higher for firms that follow PRI guidelines.

9. Results

The below table shows the descriptive statistics for firms in the KLD 400, S&P 500 ETFs as well as firms that are and are not PRI-signatories. The purpose of this table is to include the variables used to assess the normality of the data ().

Table 1. Descriptive statistics.

The table below shows statistical evaluation of the relationship of each variable for all four regressions. It shows that across all variables used, ln (MV) had the highest correlation with total return ().

Table 2. Correlation analysis.

The same regressions were done on STATA using the robustness check to see if the results still hold and assess for outliers. As a whole, the results either stayed the same or explained the variable better, increasing the validity of the regressions ().

Table 3. Summary of robustness regression results.

Market Value is a strong predictor (t = 2.839) for the KLD ethical ETF whereas a moderate predictor for the S&P 500 ETF (t = 0.742). This shows that the firms in the ethical ETF as a whole, have a higher MV than those in the other ETF and is a strong indicator of total return for the former, but not the latter. The P/E ratio is a weak indicator for both the ethical and conventional fund, (t = 0.361) and (t = 0.374) respectively at the 99% confidence interval which could be due to the reason that both ETFs consist of firms in differing sectors, at different stages in the product life cycle and/or more focused on other metrics. This also explains the similar results found in the ROE analysis.

The Beta is a strong predictor (t = 2.60), comparable to the Market Value, for the KLD ETF at the 99% confidence interval as well as for the S&P500 ETF (t = 0.99). This is indicative of the nature of the Beta as a measure of risk therefore, having a significant impact of the firm's ability to make profit and total return. The R-squared results, whilst appearing quite low, are in line with the pre-existing literature and research on the issue referenced in so are as expected and considered reasonable. Simply put, ethical exchange traded funds are typically categorised by less risk and the regression shows that the returns are different from that of conventional exchange traded funds, therefore null hypothesis H10, is rejected.

The third and fourth regression gauges whether the total returns are different based on companies who abide by the Principle for Responsible Investing (PRI) guidelines versus those who do not. The Market Value is a strong predictor (t = 0.70) at the 90% confidence interval for the PRI abiding firms as oppose to those who do not follow their guidelines (t = 0.274), because firms who typically follow external, voluntary guidelines may be larger multi-national firms who follow such guidelines for reputational increase hence its extra weight on overall total revenue.

The intercept and t-stats for P/E are quite similar for both groups of firms and are insignificant, this may be because the data collected was on a monthly basis and P/E may be better considered on a daily basis for more statistical significance. ROE was a significant influencer (t = 0.980) for the PRI abiding firms as this is by the nature of the ROE, in comparison to non-abiding firms (t = 0.0662).

10. Conclusion and implication of study

The impact and importance of corporate social responsibility is one that has been on the rise for the past few decades and does not look set to slow down with regards to how corporations should respond to climate change, prevailing trends and public outcry concerning the role that businesses have in contributing to environmental issues. This is explained by the fact that financial institutions have witnessed a large shift in investors’ demands and preferences with regards to the sustainability of their investments, which has led to a sharp increase in the amount of socially responsible investment funds (Munoz-Torres et al. Citation2004).

This growth has been driven by increased investors awareness of CSR, a plethora of financial products available to them (O’Rourke Citation2003) and by ever-increasing regulation on the issue (Albareda, Lozano, and Ysa Citation2007), as well as the growing mass of academic literature stating that generally the returns on SRI/ethical investing do not differ greatly from those on more conventional investments (Guerard Citation1997; Hutton, D’Antion, and Johnsen Citation1998; Bellow Citation2012; Statman Citation2000; Vermeier, Van de Velde, and Corten Citation2005). United with the fact that almost 90% of Fortune 500 companies employ ethical practices (Kotler and Lee Citation2004), we can see that there is a critical juncture in the point whereby firms are very much accepting of such practices.

Thus, leading to the point of how firms can engage in such practices if it is indeed the norm and ‘in-trend’ to engage with. The sustainability frameworks aimed to offer some guidance with regards to how firms can consider their CSR/ESG positions internally and compare to the industry and competitors as well as offering suggestions with regards to how they can change their position to the one they desire. This can be done by being both proactive and reactive as well as making the attempt to move to the position of the sustainability champion or completing any North West movement on Framework II.

The sample chosen included firms who abide by the Principles for Responsible Investing guidelines as well as comparable firms who do not follow such guidelines over the period 2009–2019 using monthly returns as the measurement. It also considered the overall financial performance of PRI firms against those who are not, the results were similar for both regressions which is in line with the current academic work on voluntary sustainable guidelines affecting performance. For this regression, total return was used as the dependent variable as a main driver of profitability whereas P/E ratio, ROE, MV and the Beta were used as the independent variables to test the relationship and how much they influence total return.

Overall, the regressions proved that there is no inherent financial benefit to being sustainable, however it is important to state that there are numerous non-financial benefits to acting in a sustainable manner such as increased reputation, feel-good factor of being eco-aware, increased access to debt and equity financing and perhaps better credit ratings and overall contribution to a better environment. However, the aforementioned frameworks should supply an understanding of where the firm is, the capabilities they have, and what is required by them in order to become more sustainable and the associated benefits of doing so.

11. Further study considerations

Future research could look into the role that unsustainable practices are being increasingly built into the workings of the financial world. As previously stated, the role of Bitcoin, blockchain and generally Fintech is very much being incorporated into the list of financial products that big institutions are offering to their clients. With the former of the three being high unsustainable, it is important to question how big corporations and professional services firms are going to adjust when there is an upsurge of two conflicting trends: the need to become more sustainable parallel with the want to offer cutting-edge innovative products. Ultimately, there will have to be a trade-off and whether that rests with the prioritising profits or sustainability will impact the firms position in both of the frameworks put forward.

Similar to this, there should be a greater academic focus on the influence ESG scores have on the financial performance of exchange traded funds too, as ESG scores are having an increasing influence on investment decision making. From a strategic perspective, more work can be done to consider the application of sustainability frameworks into firms typically associated with being highly unsustainable.

Whilst this paper has analysed the returns of over 900 firms and the impact that sustainability can have on financial performance and the strategic behavioural variables that can allow for sustainability to further be included in the company's ethos, it is important to discuss and consider how the structure of an institution will impact both their decision-making abilities and their inherent interest and need to consider further including ESG metrics into the firm's mantra. For example, a company that is hoping to seek funds through an IPO may be more interested in how their ESG behaviour will impact the markets valuation of the firm than a Partnership that whilst operating on a global level, are held accountable to the Partners rather than a plethora of shareholders. Further work on a company's capital and business structure on their desire to consider ESG metrics into the decision-making process would be of great significance to the field and one that would hold great value.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Albareda, L., J. Lozano, and T. Ysa. 2007. “Public Policies on Corporate Social Responsibility of Governments in Europe.” Journal of Business Ethics 74 (4): 391–407.

- Amber, S., and P. Lanoie. 2008. “Does It Pay to Be Green? A Systematic Overview.” Academy of Management Perspectives 22 (4): 45–62.

- Bellow, E. 2012. “Corporate Social Responsibility and Organisations Innovation Strategy.” Journal of Strategic Innovation and Sustainability 8 (2): 37–45.

- Benijts, T. 2008. “Measuring Corporate Sustainability.” Journal of Corporate Citizenship 2008 (32): 29–42.

- Berrone, P., J. Surroca, and J. Tribo. 2007. “Corporate Ethical Identity as a Determinant of Firm Performance: A Test of the Mediating Role of Stakeholder Satisfaction.” Journal of Business Ethics 76 (1): 35–53.

- Biernacki, M. 2015. “Environmental Life Cycle Costing (LCC) In the Aspect of Cost Management in The Company.” University of Szczecin Faculty of Economic Sciences and Management Journals 77: 305–312.

- Bowman, C., and S. Segal-Horn. 1996. “Strategic Management Business Process Reengineering: A Multi-Disciplinary Approach.”

- Brammer, S., C. Brooks, and S. Pavelin. 2006. “Corporate Social Performance and Stock Returns: UK Evidence from Disaggregate Measures.” Journal of Financial Management 35: 97–116.

- Clark, G. L., A. Feiner, and M. Viehs. 2015. “From the Stockholder to the Stakeholder: How Sustainability Can Drive Financial Outperformance.” Accessed 14 August 2019. https://doi.org/10.2139/ssrn.2508281.

- Cochran, P. L., and R. A. Wood. 1984. “Corporate Social Responsibility and Financial Performance.” Academy of Management Journal 27: 1.

- Cunha, F., E. M. de Oliveira, R. J. Orsato, M. C. Klotzle, F. L. Cyrino Oliveira, and R. G. G. Caiado. 2019. “Can Sustainable Investments Outperform Traditional Benchmarks? Evidence from Global Stock Markets.” Business Strategy and the Environment 29 (2): 682–697.

- Dow Jones Sustainability Indexes, DJSI. 2012. DJSI Annual Review 2012 – Results. Accessed 3 August 2020. http://www.sustainability-index.com.

- Forbes article: “The Most Sustainable Companies in 2019.” Accessed August 13, 2019. https://www.forbes.com/sites/karstenstrauss/2019/01/22/the-most-sustainable-companies-in-2019/

- Giese, G., L.-E. Lee, D. Melas, Z. Nagy, and L. Nishikawa. 2019. “Foundations of ESG Investing: How ESG Affects Equity Valuation, Risk, and Performance.” The Journal of Portfolio Management 45 (5): 69–83.

- Graham, J., and C. Harvey. 2001. “The Theory and Practice of Corporate Finance: Evidence from the Field.” Journal of Financial Economics 60: 187–243.

- Guerard, J. B. 1997. “Additional Evidence on the Cost of Being Socially Responsible in Investing.” Journal of Investing 6 (4): 31–34.

- Guoyou, Q., Z. Saixing, T. Chiming, Y. Haitao, and Z. Hailiang. 2013. “Stakeholders Influences on Corporate Green Innovation Strategy: Case Study of Manufacturing Firms in China.” Journal of Corporate Social Responsibility & Environmental Management 2: 1–14.

- Hart, S., and G. Ahuja. 1996. “Does it Pay to Be Green? An Empirical Examination of the Relationship Between Emission Reduction and Firm Performance.” Business Strategy and the Environment 5 (1): 30–37.

- Hartzmark, S. M., and A. B. Sussman. 2017. Do Investors Value Sustainability? A Natural Experiment Examining Ranking and Fund Flows. https://www.ssrn.com/abstract=3016092.

- Hopwood, A. 2009. “The Economic Crisis and Accounting: Implications for the Research Community.” Accounting, Organisations and Society 36 (6-7): 797–802.

- Hopwood, A., J. Unerman, and J. Fries. 2010. Accounting for Sustainability: Practical Insights, 1–44. London: Earthscan.

- Hutton, R. B., L. D’Antion, and T. Johnsen. 1998. “Socially Responsible Investing: Growing Issues and New Opportunities.” Business and Society 37 (3): 281–305.

- Ingio, E. A., and L. Albareda. 2019. “Sustainability Orientated Innovation Dynamics: Levels of Dynamic Capabilities and Their Path-Dependent and Self-Reinforcing Logics.” Technological Forecasting & Social Change 139: 334–351.

- Kimbro, M. B. 2013. “Integrating Sustainability in Capital Budgeting Decisions.” In Corporate Sustainability’. Part of the CSR, Sustainability. Part of the CSR, Sustainability, Ethics & Governance Series, 103–114. London: Springer Link Publications. doi:10.1007/978-3-642-37018-2.

- Kölbel, J. F., F. Heeb, F. Paetzold, and T. Busch. 2020. “Can Sustainable Investing Save the World? Reviewing the Mechanisms of Investor Impact.” Journal title 33 (4): 554–574.

- Kotler, P., and N. Lee. 2004. Corporate Social Responsibility: Doing the Most Good for Your Company and Your Cause. Hoboken, NJ: Wiley Publishing.

- Margolis, J. D., and J. P. Walsh. 2001. People and Profits: The Search for a Link Between a Company’s Social and Financial Performance. Hove: Psychology Press.

- Marszałek, A. K., and A. K. Uryzsek. 2020. “CSR and Socially Responsible Investing Strategies in Transitioning and Emerging Economies.” IGI Global. doi:10.4018/978-1-7998-2193-9.

- Marszk, A., and E. Lechman. 2020. “Exchange-Traded Funds on European Markets: Has Critical Mass been Reached? Implications for Financial Systems.” Entropy 22 (6): 686. doi:10.3390/e22060686.

- Miralles-Quiros, J. L., M. M. Miralles-Quiros, and J. M. Nogueria. 2019. “Diversification Benefits of Using Exchange-Traded Funds in Compliance To The Sustainable Development Goals.” Business, Strategy & the Environment 28 (1): 244–255.

- Moore, J., and A. Reichart. 1983. “An Analysis of The Financial Management Techniques Currently Employed by Large U.S. Corporations.” Journal of Business, Finance & Accounting 10 (4): 623–645.

- Munoz-Torres, M. J., M. A. Fernandez, and R. B. Franch. 2004. “The Social Responsibility Performance of Ethical and Solidarity Funds: An Approach to the Case of Spain.” Business Ethics: A European Review 13 (2–3): 200–218.

- Murray, A., D. Sinclair, D. Power, and R. Gray. 2006. “Do Financial Markets Care About Social and Environmental Disclosure? Further Evidence and Exploration from the UK.” Accounting, Auditing and Accountability Journal 19 (2): 228–255.

- O’Rourke, A. 2003. “A New Politics of Engagement: Shareholder Activism for Corporate Social Responsibility.” Business Strategy & the Environment 12 (4): 227–239.

- Patten, D. M. 1991. “Exposure, Legitimacy, and Social Disclosure.” Journal of Accounting and Public Policy 10: 297–308.

- Peeters, H. 2003. “Sustainable Development and the Role of the Financial World.” The World Summit on Sustainable Development, 241–274.

- Plinke, E., and A. Knorzer. 2006. “Sustainable Investment and Financial Performance: Does Sustainability Compromise the Financial Performance of Companies and Investment Funds?” 1 (10): 232–241.

- Przychodzen & Przychodzen. 2015. “Relationships Between Eco-Innovation and Financial Performance – Evidence from Publicly Traded Companies in Poland and Hungary.” Journal of Cleaner Production 90: 253–263.

- Quinche-Martín, F. L., and A. Cabrera-Narváez. 2020. “Exploring the Potential Links Between Social and Environmental Accounting and Political Ecology.” Social and Environmental Accountability Journal 40 (1): 53–74. doi:10.1080/0969160X.2020.1730214.

- Riedl, A., and P. Smeets. 2017. “Why do Investors Hold Socially Responsible Mutual Funds?” Journal of Finance 72 (6): 2505–2550. doi:10.1111/jofi.12547.

- Scholtens, B. 2008. “Stakeholder Relations and Financial Performance.” Sustainable Development 16 (3): 137–140.

- Semenova, L., and L. Hassel. 2008. “The Value Relevance of Environmental and Social Performance”, 1–19.

- Starks, L., and J. Białkowski. 2016. “SRI Funds: Investor Demand, Exogenous Shocks and ESG Profiles.” Working Papers in Economics 16/11, University of Canterbury, Department of Economics and Finance, 1-48.

- Statman, M. 2000. “Behavioural Portfolio Theory.” The Journal of Financial and Quantitative Analysis 3 (2): 127–151.

- Statman, M., and D. Glushkov. 2009. “The Wages of Social Responsibility.” Financial Analysts Journal 4 (65): 33–46. CFA Publication.

- United Nations. 2015. Principles for Responsible Investing Annual Report 2015. Accessed 8 October 2020. https://www.unpri.org/about-the-pri/annual-report-2015/710.article.

- Vermeier, W., E. Van de Velde, and F. Corten. 2005. “Sustainable and Responsible Performance.” The Journal of Investing 13 (3): 94–101.

- Waddock, S. A., and S. B. Graves. 1997. “The Corporate Social Performance-Financial Performance Link.” Strategic Management Journal 18 (4): 303–319.

- Webley, S., and E. More. 2003. Does Business Ethics Pay? 1–10. London: Institute of Business Ethics.