ABSTRACT

The aim is to investigate the value basis of Socially Responsible Retirement Investments (SRRI) in a study of Swedish pension investors in the age range 18 to 65 years (N=1005). Logistic regression analyses were performed with self-reported SRRI choice as dependent variable and different levels of values as independent variables. On a higher level of analyses, self-transcendent values, especially universalism (e.g., equality, protecting the environment, and social justice), have the most important influences on SRRI choice. In contrast, on a lower-level analysis, SRRI choice is influenced by self-enhancement values with high priority for authoritarian power and low priority for wealth. The three-level analysis of values (self-transcendence vs self-enhancement value orientation, motivational domain, and value) questions the contradiction between dimension poles of values and the structuring of values in interrelated motivational domains. The results thereby clarify some previous findings and increase the understanding of the value basis of SRRI.

1. Introduction

It is argued that any future change towards sustainable development must include corporations taking their environmental, social and ethical responsibilities (e.g. Friedman and Miles Citation2001). One way for private investors to exert pressure on corporations to do so is through investments in funds that not only focus on financial returns but that also focus on societal values. Socially responsible investment (SRI) refers to investment practices that in addition to financial aspects include environmental and social concerns (Sparkes Citation2001; Sparkes and Cowton Citation2004; Dijk-de and Nijhof Citation2015). Other terms with similar or identical meaning as SRI include ethical investment, responsible investment, sustainable investment and impact investment (Dumas and Louche Citation2016; Apostolakis, Dijk et al. Citation2018; Apostolakis, van Dijk et al. Citation2018; Agrawal and Hockerts Citation2021).

Several studies have compared risk-adjusted returns of SRI to conventional stock investments (e.g. Orlitzky, Schmidt, and Rynes Citation2003; Margolis Citation2008; Haan, Dam, and Scholtens Citation2012; Friede, Busch, and Bassen Citation2015; Chang-Soo Citation2019). The main conclusion to be drawn from this body of research is that SRI has no financial penalty. Yet, SRI funds only amount to a small share of the total investments in funds (EUROSIF Citation2018, Citation2021). There are several potential reasons for this. Firstly, knowledge about SRI is fairly limited among the general public. Secondly, people, in general, may not be concerned about long-term consequences, neither to themselves nor to others (Waygood Citation2011). But even if people were, they may doubt (1) that SRI yields good financial returns and (2) that SRI will deliver on its (implicit) promise of preserving the environment and improving social conditions. Finally, even though the number of SRI funds in the market is growing, there are still few with sector specialization.

The aim of the present study is to gain a deeper understanding of the value-based motives that drives SRI choice by pension savers. Retirement funds represent an increasingly larger share of private investors’ investments in the stock market (Eurosif Citation2018). Due to its long-term investment horizon, retirement savings ought to constitute a particularly promising field for increasing SRI’s market share. Globally, pension assets amount to about 36 trillion USD (Statista Citation2020). Retirement assets vary significantly from country to country and are driven by cultural, demographic, economic and political factors (Statista Citation2020). In this paper, we report data for Sweden.

1.1. The Swedish case

This study is limited to the Swedish premium pension system which is the part of the pension for which the individual citizen has the mandate to choose how they want to invest their pension savings. In total, the pension assets are estimated to represent about 20% of all portfolio assets in Sweden and almost half of the savings of the Swedish households (Insurance Sweden Citation2019; Swedish Pensions Agency Citation2020).

In 2000 the pension market in Sweden was deregulated in order to promote competition in a previously protected market and to allow citizens to themselves choose among a large number of different equity and interest-bearing funds. About 2.5% of an individual’s income was set aside for the so-called premium-pension funds. Individuals have the freedom to choose up to five of these funds in which to invest their premium pension. The purpose is to give citizens the opportunity to benefit from the value development of a fund portfolio they construct themselves. If an active selection is not made, the money is invested in a governmental-managed default fund that invests in a variety of markets and industries in order to guarantee risk-adjusted financial returns. During the data collection, the default fund was not labeled as a SRI fund (Swedish Pensions Agency Citation2020).

1.2. Theory

This study follows up on Jansson et al. (Citation2014) in investigating the role of values for choice of SRRI (Socially Responsible Retirement Investment) by private investors. Our point of departure is Schwartz’s theory of universal values (Schwartz and Bielsky Citation1987; Schwartz Citation1992; Krystallis, Vassallo, and Chryssohoidis Citation2012). The theory that for decades has dominated value research identifies 56 values organized in ten so-called motivational domains. Values and motivational domains are located in a two-dimensional space defined by the dimensions ‘openness to change’ versus ‘conservation’ and ‘self-transcendence’ versus ‘self-enhancement’. The first dimension that contrasts the poles ‘openness to change’ and ‘conservation’ captures the conflict between motivational domains emphasizing readiness for change (i.e. self-direction and stimulation) and motivational domains emphasizing resistance to change (i.e. security and conformity/tradition). The second dimension that contrasts ‘self-enhancement’ and ‘self-transcendence’ captures the conflict between motivational domains emphasizing the pursuit of one’s own interests, relative success and dominance over others (i.e. achievement and power) versus motivational domains emphasizing concern for the welfare and interests of others (i.e. universalism and benevolence). The motivational domains are the following:

Achievement. Self-enhancement values related to personal success through demonstrating competence according to social standards (e.g. ambitious).

Power. Self-enhancement values related to social status and prestige, control or dominance over people and resources (e.g. wealth).

Benevolence. Self-transcendent values related to preservation and enhancement of the welfare of people with whom one is in frequent personal contact (e.g. forgiving).

Universalism. Self-transcendent values related to understanding, appreciation, tolerance and protection for the welfare of all people and for nature (e.g. protecting the environment).

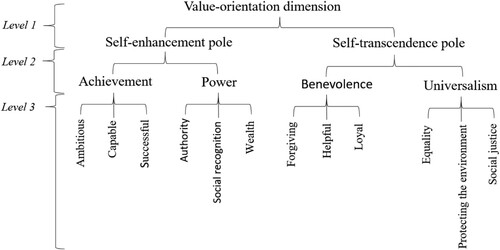

As motivated below, in this study a three-level analysis of values related to SRRI choice was performed referring to (1) the two poles self-enhancement values versus self-transcendent values, (2) the four motivational domains (e.g. achievement, power, benevolence and universalism) and (3) the individual values included in Schwartz’ value survey (SVS) shown in .

Figure 1. The three levels of values: (1) The poles of the value-orientation dimension self-enhancement versus self-transcendence, (2) the motivational domains, and (3) the values. Note: The values at the third level are limited to those measured in the present study.

1.3. Previous research

Previous research in Sweden has identified different segments of investors. Some private SR (socially responsible) investors are primarily driven by altruistic motives, while others are primarily driven by financial motives (Nilsson Citation2009). According to Beal, Goyen, and Phillips (Citation2005), SR investors have three different motives: (1) superior financial return, (2) non-wealth return and (3) contributions to social change. No other study than that of Jansson et al. (Citation2014) cited above seems to have applied Schwartz’s (Citation1992) theory to identify the value basis of SRRI. Jansson et al. (Citation2014) concluded that SRRI is positively associated with self-transcendent values but also with beliefs about long-term financial benefits.

According to Hancock (Citation2005), SR investors are less self-focused and more globally conscious than conventional investors. In Schwartz’s (Citation1992) theory, this implies that compared to conventional investors, SR investors have a higher priority of self-transcendence values and a lower priority of self-enhancement values. Other characteristics of SR investors are high education, being well-informed about financial markets and being active information seekers and deliberative decision makers (Getzner and Grabner-Kräuter Citation2004; Hancock Citation2005; Nilsson Citation2008; Wins and Zwegel Citation2016; Rossi et al. Citation2019).

Even if most previous studies related to SRI focused on the self-transcendence values (e.g. Jansson et al. Citation2014; Jansson and Biel Citation2014), studies of socially responsible consumption have included self-enhancement values. The main conclusion from these studies is that socially responsible consumption (e.g. of ecological food or fair-trade products) is positively related to self-transcendence values and negatively related to self-enhanced values (e.g. Grunert and Juhl Citation1995; Ladhari and Tchetgna Citation2015).

Several studies of socially responsible consumption have also analyzed values on the three different levels. Grunert and Juhl (Citation1995) found that both motivational domains (i.e. universalism and benevolence) influence socially responsible consumption, while Ladhari and Tchetgna (Citation2015) found that only universalism influences socially responsible consumption. On the third level of analysis, Grunert and Juhl (Citation1995) found that protecting the environment and social justice were salient values subordinate to universalism that influence socially responsible consumption, while forgiving was a salient value subordinate to benevolence. Furthermore, Ladhari and Tchetgna (Citation2015) found that equality and social justice were salient values subordinate to universalism that positively influence socially responsible consumption, while social recognition was a salient value subordinate to power that negatively influences socially responsible consumption. These studies illustrate that an analysis of values related to socially responsible retirement investments (SSRI) may gain from a three-level analysis of values, including value orientation dimension, motivational domain and value.

Previous research of Schwartz values and SRRI (Jansson et al. Citation2014) and SRI (Jansson and Biel Citation2014) have only considered the highest level of values – the value orientation dimension. Since the two lower levels of values have contributed new insights regarding socially responsible consumption (Grunert and Juhl Citation1995; Ladhari and Tchetgna Citation2015), we consider it to be promising to apply a three-level analysis of the relation of values to SRRI choice.

1.4. Hypotheses

Similar to previous studies (e.g. Jansson et al. Citation2014; Jansson and Biel Citation2014) on values and their relation to SRI, this study only includes the value-orientation dimension self-enhancement versus self-transcendent but not the dimension openness to change versus conservation. It has been found in studies of consumers’ socially responsible decision making that the value-orientation dimension self-enhancement versus self-transcendent is more relevant to consider than the value-orientation dimension openness to change versus conservation (Stern et al. Citation1999; Kaiser, Hübner, and Bogner Citation2005). Furthermore, previous SRI research has only investigated the self-transcendence pole and not the self-enhancement pole of this dimension. Jansson and Biel (Citation2014) and Jansson et al. (Citation2014) assumed that a high degree of self-transcendence implies a low degree of self-enhancement and vice versa. Since a deeper analysis of values successfully has been applied to understand socially responsible consumption (Grunert and Juhl Citation1995; Ladhari and Tchetgna Citation2015), we extend the data analyses in Jansson et al. (Citation2014) to include also the lower levels of values not reported before.

This study differs from, and as such expands, previous research regarding three important aspects. Firstly, it includes both self-transcendence and self-enhancement motivational domains while Jansson and Biel (Citation2014) and Jansson et al. (Citation2014) only included the self-transcendence motivational domains. Secondly, this study analyzes SRRI in relation to the three levels of values; value-orientation dimension, motivational domain and individual value. Jansson and Biel (Citation2014) and Jansson et al. (Citation2014) only included the first level (i.e. the self-transcendence motivational domains). Thirdly, in contrast to this study’s exclusive focus on values, the previous studies had a less inclusive perspective of what factors influence SRRI.

This study does not primarily aim to propose a model that fully explains SRRI. Rather, the aim is to contribute to a more detailed analysis of the value basis of SRRI choice based on Schwartz’s (Citation1992) value theory. A three-level analysis of values related to SRRI would reveal which values are the most salient in higher levels of motivational domains and if there are contradictory values within this category, which might reduce or eliminate its influence. This should increase the understanding of the value basis of SRRI beyond current knowledge and thereby to accurately construct models that better help predict and influence SRRI.

Based on Schwartz’s (Citation1992) theory as well as the previous research on values related to SRI and socially responsible consumption cited above, we expect that self-transcendent motivational domains, especially universalism but also benevolence, are positively associated with SRRI. We expect this since such values are related to enhancement of others by transcendence of selfish interests and global consciousness. Thus, we formulate the following hypothesis:

H1. Self-transcendent motivational domains and values are positively associated with SRRI.

We also expect that the importance of self-enhancement motivational domains, especially power, is negatively associated with SRRI, since these reflect self-focus and individualistic interests instead of global consciousness and collectivistic interests. Thus, we formulate the following hypothesis:

H2. Self-enhancement motivational domains and values are negatively associated with SRRI.

We only propose these two hypotheses at the value-orientation level. The analyses of the values at the lower levels are exploratory.

2. Method

2.1. Participants

A random sample of 3,500 Swedish residents between 18 and 65 years of age was obtained from the official taxpayer register. A paper-and-pencil survey including a free-reply envelope was distributed by regular mail in 2012. After two reminders, 1,005 usable surveys were received corresponding to a response rate of 28.7%. The sample consisted of 50.5% men. The mean age was 51.3 years (SD = 11.7), 41.8% had a university degree and 31.8% had a monthly income above SEK 30,000. Compared to the Swedish population in the same age range (Statistics Sweden Citation2020), the sample was somewhat overrepresented by men and older residents (mean age 41.3 years in the population). Further, the sample was slightly higher educated (33.8% university degree in the population). The income distribution did not differ importantly from the population. Among the 1,005 participants, 68 stated that they actively choose to invest their premium pension in SR funds.

2.2. Measures

Twelve items from the Schwartz’s (Citation1992) value survey were selected; six were classified as self-enhanced values and six were classified as self-transcendent values (). Participants rated each value on 5-point scales ranging from 1 (nothing I strive to achieve in my life at all) to 5 (something I very much strive to achieve in my life).

Table 1. The three levels of values (value-orientation dimension poles, motivational domains, and values).

SRRI choice was measured by a single item: ‘I have actively selected premium-pension funds based on ethical, social, and environmental aspects’. The variable was dummy coded (1 = Yes, 0 = No).

The survey also included questions about age (years), gender (dummy coded: 1 = female, 0 = male), educational attainment (dummy coded: 1 = university degree, 0 = no university degree) and income (dummy coded: 1 => SEK 30,000 per month, 0 =< SEK 30,000 per month).5

2.3. Data analyses

Firstly, SRR and non-SRR investors were compared through independent-samples t-tests and χ2-tests. The t-tests were used to compare the two groups on the three levels of values and age, while the χ2-tests were used to compare the groups on gender, educational level and income. Secondly, three logistic regression analyses were performed to analyze the impact of values on SRRI choice at the three levels of values. The impact of values was analyzed on each level after controlling for age, gender, educational level and income. Previous research has found that SR investors was characterized by young age, being female, high education and high income (Getzner and Grabner-Kräuter Citation2004; McLachlan and Gardner Citation2004; Hancock Citation2005; Nilsson Citation2008; Wins and Zwegel Citation2016), although the income findings are mixed (Experian UK Citation2005; Pasweark and Riley Citation2010).

Table 2. Independent-samples t-tests on three levels of values as a comparison between socially responsible retirement (SRR) investors and non-SRR investors.

3. Results

3.1. Comparing SRR investors and non-SRR investors

shows the results of independent-samples t-tests performed to compare the 2 value-orientation dimension poles (i.e. self-enhancement values versus self-transcendent values), the 4 motivational domains and the 12 values. There was no statistically significant difference (p > .05) in self-enhancement values between SRR and non-SRR investors. However, the differences were significant (p < .05 and p < .01) for authority and wealth, two values subordinate to the power motivational domain of self-enhancement. There was also a significant difference in self-transcendent values between SRR and non-SRR investors (p < .001) and significant differences for both self-transcendent motivational domains, benevolence and universalism (p < .01 and p < .001). Further, there were significant differences for forgiving and loyalty (p < .01 and p < .05), subordinate to benevolence and for equality, protecting the environment and social justice (p < .001), subordinate to universalism.

3.2. A three-level analysis of values

shows mean ratings and standard deviations for each value as well as aggregated for the motivational domain (achievement, power, benevolence and universalism) and for self-enhancement and self-transcendent values. Cronbach’s alphas >.70 indicate that the reliability is satisfactory for all the aggregated measures except for Power (α = .61). Pearson correlations between the value variables and point-biserial correlations with SRRI choice are also reported.

Table 3. Means (M), standard deviations (SD), reliability (Cronbach´s α), and Pearson correlations of value-orientation dimension poles, motivational domains, and values, and point-biserial correlations with choice of socially responsible retirement investment (SRRI).

3.1.1. Level 1: the impact of self-enhancement and self-transcendence values on SRRI choice

A logistic regression analysis was performed to assess the impact on the SSRI choice of self-enhancement and self-transcendence values. The model was statistically significant, χ²(2, N = 1005) = 13.33, p < .001, indicating that it distinguishes between SRR investors and non-SRR investors. The model explained 3.4% of the variance in SRRI choice and correctly classified 93.3% of the respondents. As shown in , only self-transcendence values have a significant effect (p < .05). The odds ratio is 2.39, implying that the odds of the choice of SRRI increased by 139% per unit of increase on the self-transcendent value scale.Footnote1

Table 4. Results of logistic regression analyses of value-orientation dimension poles.

In an additional logistic regression analysis, the control variables age, gender, educational level and income explained 3.4% of the variance in the SRRI choice (Model 2 in ). After the entry of self-enhancement and self-transcendent values, the total variance explained was 5.7%, χ² (6, N = 993) = 22.00, p < .001. The value variables thus explained an additional 2.3%. In this model (Model 3 in ), only educational level (odds ratio 1.96) and self-transcendent values (odds ratio 2.37) were statistically significant (p < .05).

3.1.2. Level 2: the impact of motivational domain on SRRI choice

A second logistic regression analysis was performed to assess the impact on SRRI choice of the four motivational domains (i.e. achievement, power, benevolence and universalism). The model was statistically significant, χ² (4, N = 1005) = 17.05, p < .01, indicating that it distinguishes between SRR and non-SRR investors. It explained 4.4% of the variance and correctly classified 93.2% of the respondents. As shown in , only universalism was statistically significant (p < .05). The odds ratio was 2.53 (153% increase in the odds of the choice of SRRI per unit of increase on the universalism scale).

Table 5. Results of logistic regression analyses of motivational domains.

In the final model shown in where the control variables are included, only educational level (odds ratio 1.94) and universalism (odds ratio 2.62) were statistically significant (p < .05). The total variance explained by the model was 7.0%, χ² (8, N = 993) = 27.17, p < .001. The motivational domains thus explained an additional 3.6% (Model 2 in and ).

3.1.4. Level 3: the impact of values on SRRI choice

A final logistic regression analysis was performed to assess the impact on the SRRI choice of the twelve values. The model was statistically significant, χ² (12, N = 1005) = 31.93, p < .001, indicating that it distinguishes between SRRI investors and non-SRR investors. The model explained 8.0% of the variance and correctly classified 93.2% of the respondents. As shown in , only authority and wealth have significant effects. Authority had an odds ratio of 1.42. This corresponds to an increase of the odds of the SRRI choice by 42% per unit of increase on the authority scale. The odds ratio for wealth was 0.64, thus implying a 36% decrease in the odds of the SRRI choice per unit of increase on the wealth scale.

Table 6. Results of logistic regression analyses of values.

In the final model (Model 2 in ) with the control variables included, gender (odds ratio 1.92), educational level (odds ratio 1.86), authority (odds ratio 1.46) and wealth (odds ratio 0.61) were statistically significant (p < .05). The total explained variance in SRRI choice was 11.0%, χ² (16, N = 993) = 43.17, p < .001. The twelve values thus explained an additional 7.6% (Model 2 in and ).

4. Discussion

As hypothesized, we found that SRRI choice is associated with broad self-transcendent values. This was expected since such values are related to the enhancement of others by transcendence of selfish interests and a global consciousness. Our results in this respect confirm the findings of previous research investigating self-transcendent values in relation to SRRI (Jansson et al. Citation2014), in relation to SRI in general (Hancock Citation2005) and in relation to socially responsible consumption (Grunert and Juhl Citation1995; Ladhari and Tchetgna Citation2015).

The motivational domain benevolence did, however, not show any relationship with SRRI choice. This is inconsistent with Grunert and Juhl (Citation1995) who found a positive relation between benevolence and socially responsible consumption (i.e. of ecologic food or fair-trade products). These differences could depend on that the previous finding is based on bivariate analyses, while our study featured multivariate analyses. If we only conduct a bivariate analysis (see ), the results would be consistent with Grunert and Juhl’s (Citation1995) results. The two self-transcendent motivational domains are positively correlated (r = .69) resulting in that benevolence did not have a significant effect on SRRI choice (p < .05) if universalism is controlled. It is also conceivable that self-transcendent values related to family and friends (i.e. benevolence) may better explain the consumption of ecological food and fair-trade products than SRRI choice.

Also inconsistent with Grunert and Juhl (Citation1995) and Ladhari and Tchetgna (Citation2015), any significant relationship was not found between protecting the environment and SRRI choice or between social justice and SRRI choice. Protecting the environment and social justice may be more relevant for the consumption of ecologic food and fair-trade products compared to SRRI choice. SRR investors may furthermore have different views of the social impact they want their choice of funds to have. Investing in a socially responsible fund related to equality and social justice may not attract investors who want to promote ecological sustainability. Previous research (Beal, Goyen, and Phillips Citation2005; Nilsson Citation2009; Zwegel, Wins, and Klein Citation2019) have shown that socially responsible investors are not a homogeneous group regarding their needs and motives.

Contrary to previous research, we did not find a negative association between self-enhancement motivational domains and SRRI choice (Hancock Citation2005), and there was no negative association between the power and SRRI choice. This is surprising as we would have expected that power in terms of authority, social recognition and wealth would have a negative effect on SRRI choice. Our regression analysis of values () indicates that values in the motivational domain power influence SRRI choice in two opposite directions; authority being positively associated, and wealth being negatively associated with SRRI choice. The positive association between authority and SRRI choice contrasts with the negative relationship found by Grunert and Juhl (Citation1995) for socially responsible consumption. Authority may be more relevant for SRRI choice than consumption of ecologic food and fair-trade products. This value is defined as the right to lead and command in order to control people and resources (Schwartz Citation1992). In the present context, it may be associated with responsibility and a positive attitude towards the regulation of the financial system to protect societal values rather than as an indicator of a self-enhancement value orientation. It may even be perceived to be in contrast to neo-liberalism and a totally free and unregulated market. Further research needs to show if authority only is related to SRRI choice or if it is related to deliberate choices of pension funds in general.

Our finding of a negative association between wealth and SRRI choice is consistent with Grunert and Juhl (Citation1995) who found a negative association between priority of wealth and socially responsible consumption. To invest in sustainable pension funds can be an expression of future beliefs and expectations beyond higher financial returns. Since many SR investors primarily invest for other reasons than financial returns (Beal, Goyen, and Phillips Citation2005; Nilsson Citation2009), it seems plausible and in agreement with previous research that the SRR investors on average prioritize wealth less than non-SRR investors do (Apostolakis et al. Citation2018b). Yet, the finding seems to be contrary to the positive relation between financial motives and SRRI choice found by Jansson et al. (Citation2014). The difference may be explained by use of different measurement instruments. Jansson et al. (Citation2014) measured financial motives through beliefs of risks and returns related to SRRI rather than the importance of such beliefs on SRRI. SRR investors may thus believe that SRRI has a good risk-adjusted financial return, even if they perceive wealth (in terms of material possessions and money) as less important than non-SRR investors (Beal, Goyen, and Phillips Citation2005; Nilsson Citation2009). It may be the case that the relatively higher education and knowledge among the SRR investors make them concerned about social, ethical and environmental aspects, rather than economic aspects?

We finally note that the results are inconsistent with Schwartz’s value theory (Schwartz and Bielsky Citation1987; Schwartz Citation1992). One inconsistency concerns the contradictory relation between the two poles of self-enhancement values and self-transcendent values. The results indicate that SRRI is associated with a high level of self-transcendent values but still at an intermediate level associated with self-enhancement values. Another inconsistency is that the interrelations between power values are questioned since authority and wealth are contradictory. Conceivably, authority related to SRRI reflects the self-transcendent motivational domains of universalism (e.g. ‘lead and command’ in order to protect the environment and achieve social justice) although it theoretically is related to self-enhancement in terms of the motivational domain power. Yet, being the first study of this kind, further research is needed to investigate the relation of SRRI to the lowest level of values.

5. Conclusions and limitations

In contrast to previous SRRI research, we analyzed three levels of values. At the first level, we found that SRRI choice is associated with self-transcendent values rather than self-enhancement values which are in line with our hypothesis. At the second level, we found that self-transcendent values are related to the universalism rather than the benevolence motivational domain. This may imply that SRR investors strive to contribute to the goodness of people and nature in general rather than exclusively to family and relatives. This is in line with our expectation since the investment in SRR funds is perceived to contribute to the well-being of society in general rather than solely to family, friends and acquaintances.

At the third level, we found that SRRI choice is positively associated with authority and negatively associated with wealth. This means that SRRI choice depends on self-enhancement values of power () rather than self-transcendent values of universalism. These finding was unexpected and are inconsistent with Schwartz’s value theory (Schwartz Citation1992) and previous empirical findings in studies of socially responsible consumption (Grunert and Juhl Citation1995). According to the theory as well as our empirical results, authority and wealth are related, but they influence SRRI choice in opposite directions. SRRI choice may be perceived as a more strategic decision compared to other socially responsible behaviors (e.g. consuming ecologic food and fair-trade products). An authoritarian inclination may furthermore be understood as a right to lead and command society in a socially responsible direction reflected in the active choice of retirements funds. However, the inclination for achieving wealth in terms of money and material possessions may correspond to more typical self-interest aspects of power and self-enhancement values in general. In concluding, our study indicates that socially responsible investors prioritize wealth lower than other investors do and are therefore less motivated by financial returns. Therefore, SRRI choice is a way of striving to dominate people and resources for the well-being of others (i.e. social responsibility) rather than gaining wealth for oneself.

Overall, it can be concluded that values at a lower level provide a better explanatory model of SRRI. But more importantly, it can be conjectured that the influences on SRRI of higher levels of values (e.g. value-orientation and motivational domain) are not always justified. This is an important observation since in previous SRRI research only higher level of values has been used. The problem becomes clearest with regard to the motivational domain power at the second level of values. Reliability of the measure (Cronbach's alpha) is relatively high for power at the second level, but power does still not have much impact on SRRI choice. At the third level of values, authority and wealth (both subsumed to power) have impacts in opposite directions, which explains that power itself does not impact on SRRI choice. This is a key finding, as the motivational domain power needs to be analyzed more deeply to provide adequate guidance related to SRRI.

A limitation is that in our sample (N = 1005) only 68 participants reported that they actively chose SRRI. In further research, a higher representation of SRR investors would be desirable since this would increase statistical power.Footnote2 Another related limitation is that we rely on self-reported choices of SRRI, instead of observing whether the respondents have actually chosen SRRI. Such measurements have a number of possible caveats, including influences of social desirability responses and memory errors (Baumesiter, Vohs, and Funder Citation2007). On the other hand, we were in this study only interested in people who themselves make an active choice to invest their pension money in socially responsible funds. It is possible that some SRRI choices are made by people who have not themselves made an active choice. It would be interesting in future research to distinguish active from passive SRRI. Comparative analyses between SRR investors and other active and conscious retirement investors would furthermore be desirable. Another interesting comparison would be between SRR and SR investors to determine the role of time horizon.

In additional studies, we suggest that the other value-orientation dimension of Schwartz’s (Citation1992) value theory (i.e. openness to change versus conservation) should be included, as a reasonable hypothesis is that people open to change (versus being conservative) are more willing to consider social responsibility in their financial decision making.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1 The formula is 100(OR-1) % where the odds ratio OR is the ratio of the odds of choosing SRRI over the odds of not choosing SRRI.

2 Statistical power is primarily influenced by sample size. Yet, the statistical power of independent-samples t-tests decreases if sample sizes differ.

References

- Agrawal, A., and K. Hockerts. 2021. “Impact Investing: Review and Research Agenda.” Journal of Small Business & Entrepreneurship 33 (2): 153–181.

- Apostolakis, G., G. V. Dijk, R. J. Blomme, F. Kraanen, and A. P. Papadopoulos. 2018. “Predicting Pension Beneficiaries’ Behaviour When Offered a Socially Responsible and Impact Investment Portfolio.” Journal of Sustainable Finance & Investment 8 (3): 213–241.

- Apostolakis, G., G. van Dijk, F. Kraanen, and R. J. Blomme. 2018. “Examining Socially Responsible Investment Preferences: A Discrete Choice Conjoint Experiment.” Journal of Behavioral and Experimental Finance 17: 83–96.

- Baumesiter, R. F., K. D. Vohs, and D. C. Funder. 2007. “Psychology as the Science of Self-Reports and Finger Movements: Whatever Happened to Actual Behavior?” Perspecitives on Psychological Science 2 (4): 396–404.

- Beal, D., M. Goyen, and P. Phillips. 2005. “Why DO WE Invest Ethically?” The Journal of Investing 14 (3): 66–78.

- Chang-Soo, K. 2019. “Can Socially Responsible Investments be Compatible with Financial Performance? A Meta-Analysis.” Asia-Pacific Journal of Financial Studies 48 (1): 30–64.

- Dijk-de, M. v. G., and A. H. J. Nijhof. 2015. “Socially Responsible Investment Funds: A Review of Research Priorities and Strategic Options.” Journal of Sustainable Finance & Investment 5 (3): 178–204.

- Dumas, C., and C. Louche. 2016. “Collective Beliefs on Responsible Investment.” Business & Society 55 (3): 427–457.

- EUROSIF. 2018. “2018 SRI Study Launch.” Accessed July 2, 2021. www.eurosif.org.

- EUROSIF. 2021. “EUROSIF Report 2021: Fostering investor impact.” Accessed January 3, 2021. www.Eurosif.org.

- Experian UK. 2005. Financial Strategy Segments - The Consumer Classification of Financial Behaviour in the UK. Nottingham: Mori Financial Services.

- Friede, G., T. Busch, and A. Bassen. 2015. “ESG and Financial Performance: Aggregated Evidence from More than 2000 Empirical Studies.” Journal of Sustainable Finance & Investment 5 (4): 210–233.

- Friedman, A. L., and S. Miles. 2001. “Socially Responsible Investment and Corporate Social and Environmental Reporting in the UK: An Exploratory Study.” The British Accounting Review 33 (4): 523–548.

- Getzner, M., and S. Grabner-Kräuter. 2004. “Consumer Preferences and Marketing Strategies for “Green Shares” – Specifics of the Austrian Market.” The International Journal of Bank Marketing 22: 260–278.

- Grunert, S. C., and H. J. Juhl. 1995. “Values, Environmental Attitudes, and Buying of Organic Foods.” Journal of Economic Psychology 16: 39–62.

- Haan, M. d., L. Dam, and B. Scholtens. 2012. “The Drivers of the Relationship Between Corporate Environmental Performance and Stock Market Returns.” Journal of Sustainable Finance & Investment 2 (3–4): 338–375.

- Hancock, J. 2005. An Investoŕs Guide to Ethical & Socially Responsible Investment Funds. London: Kogan Page.

- Insurance Sweden. 2019. “Pensioner utgör en stor del av hushållens sparande.” May 10. Accessed July 2, 2021. www.pensioner-utgor-en-stor-del-av-hushallens-sparande/ (in Swedish).

- Jansson, M., and A. Biel. 2014. “Investment Institutions’ Beliefs About and Attitudes Toward Socially Responsible Investment (SRI): A Comparison Between SRI and Non-SRI Management.” Sustainable Development 22 (1): 33–41.

- Jansson, M., J. Sandberg, A. Biel, and T. Gärling. 2014. “Should Pension Fund’s Fiduciary Duty be Extended to Include Social, Ethical and Environmental Concerns? A Study of Beneficiaries’ Preferences.” Journal of Sustainable Finance & Investment 4 (3): 213–229.

- Kaiser, F. G., G. Hübner, and F. X. Bogner. 2005. “Contrasting the Theory of Planned Behavior with the Value-Belief-Norm Model in Explaining Conservation Behavior.” Journal of Applied Social Psychology 35 (10): 2150–2170.

- Krystallis, A., M. Vassallo, and G. Chryssohoidis. 2012. “The Usefulness of Schwart’s Values Theory in Understanding Consumer Behaviour Towards Differentiated Products.” Journal of Marketing Management 28 (11-12): 1438–1463.

- Ladhari, R., and N. Tchetgna. 2015. “The Influence of Personal Values on Fair Trade Consumption.” Journal of Cleaner Production 87: 469–477.

- Margolis, J. 2008. “Do Well by Doing Good? Don’t Count on It.” Harvard Business Review 86 (1): 19–20.

- McLachlan, J., and J. Gardner. 2004. “A Comparison of Socially Responsible and Conventional Investors.” Journal of Business Ethics 52 (1): 11–25.

- Nilsson, J. 2008. “Investment with a Conscience: Examining the Impact of Pro-Social Attitudes and Perceived Financial Performance on Socially Responsible Investment Behavior.” Journal of Business Ethicss 83 (2): 307–325.

- Nilsson, J. 2009. “Segmenting Socially Responsible Mutual Fund Investors: The Influence of Financial Return and Social Responsibility.” International Journal of Bank Marketing 27 (1): 5–31.

- Orlitzky, M., F. L. Schmidt, and S. L. Rynes. 2003. “Corporate Social and Financial Performance: A Meta-Analysis.” Organization Studies 24 (3): 403–441.

- Pasweark, W. R., and M. E. Riley. 2010. “It´s a Matter of Principle: The Role of Personal Values in Investment Decisions.” Journal of Business Ethics 93 (2): 237–253.

- Rossi, M., D. Sonsone, A. van Soest, and C. Torricelli. 2019. “Household Preferences for Socially Responsible Investments.” Journal of Banking and Finance 105: 107–120.

- Schwartz, S. H. 1992. “Universals in the Content and Structure of Values: Theoretical Advances and Empirical Tests in 20 Countries.” Advances in Experimental Social Psychology 25: 1–65.

- Schwartz, S. H., and W. Bielsky. 1987. “Toward a Universal Psychological Structure of Human Values.” Journal of Personality and Social Psychology 53 (3): 550–562.

- Sparkes, R. 2001. “Ethical Investments: Whose Ethics, Which Investment?” Business Ethics: A European Review 10 (3): 194–205.

- Sparkes, R., and C. J. Cowton. 2004. “The Maturing of Socially Responsible Investment: A Review of the Developing Link with Corporate Social Responsibility.” Journal of Business Ethics 52 (1): 45–57.

- Statista. 2020. “Retirement Assets Worldwide – Statistics & Facts.” April 3. Accessed July 2, 2021. www.statista.com/topics/5170/retirement-assets-worldwide.

- Statistics Sweden. 2020. “Population Statistics.” Accessed July 2, 2021. www.scb.se/en/findingstatistics/statistics-by-subjectarea/population/populationcom-position/population-statistics/.

- Stern, P. C., T. Dietz, T. Abel, G. A. Guagnano, and L. Kalof. 1999. “A Value-Belief-Norm Theory of Support for Social Movements: The Case of Environmentalism.” Human Ecology Review 6: 81–97.

- Swedish Pensions Agency. 2020. “Vad innebär fondsparande i premiepensionen?” May 12. Accessed July 15, 2020. www.pensionsmyndigheten.se/forsta-din-pension/valjoch-byt-fonder/fondsparande (In Swedish).

- Waygood, S. 2011. “How do the Capital Markets Undermine Sustainable Development? What Can be Done to Correct This?” Journal of Sustainable Finance & Investment 1 (1): 81–87.

- Wins, A., and B. Zwegel. 2016. “Comparing Those Who Do, Might and Will Not Invest in Sustainable Funds: A Survey among German Retail Fund Investors.” Business Research 9 (1): 51–99.

- Zwegel, B., A. Wins, and C. Klein. 2019. “On the Heterogeneity of Sustainable and Responsible Investors.” Journal of Sustainable Finance and Investment 9 (4): 282–294.