ABSTRACT

This paper investigates how investment funds behave in line with European Union (EU)'s Sustainable Finance Disclosure Regulation (SFDR). The SFDR requires investment funds to take a clear position with respect to sustainability objectives, aiming at addressing the threats of greenwashing. However, we still do not know whether investment funds are managed accordingly. We frame our study within the organizational category theory, using Morningstar Direct data to analyze the category of investment funds declaring sustainability objectives – SFDR Article 9– and a control group with no sustainability objectives – SFDR Article 6. We assess how investment managers are financially incentivized to achieve either sustainability or financial objectives. The analysis evidences unexpected results: investment funds that self-select into opposite categories have incentives to behave similarly from both the financial and sustainability perspectives. Our results show that European investment funds hardly distinguish the attributes of sustainability meanings across opposite categories, reflecting category fuzziness.

1. Introduction

Over time, financial markets have increasingly integrated sustainability practices within investment activities. In the recent years, sustainable development became a dogma for business and financial actors, raising doubts about the reliability of their sustainability claims, which spread the dangerous phenomenon of greenwashing, or impact washing (Harji and Jackson Citation2012; Findlay and Moran Citation2019). To overcome this issue, from March 2021, the European Union adopted a set of regulations to guide financial actors toward proper sustainability strategies. In particular, the Sustainable Finance Disclosure Regulation 2019/2088 (SFDR) is a cornerstone framework that requires financial operators to declare their products’ positioning with respect to the overarching framework of the EU Taxonomy for sustainable activities (Schütze and Stede Citation2021). The SFDR indeed defines some categories into which financial products must fall, ranging from the one containing initiatives with no sustainability considerations to the one covering initiatives with a specific and intentional sustainability objective.

However, very few studies (Becker, Martin, and Walter Citation2022; Bengo, Boni, and Sancino Citation2022) have so far investigated the impact of SFDR on the actual behaviour of financial actors. Therefore, our objective is to understand whether the perimeter defined by the SFDR effectively drives investment funds to allocate resources depending on the different positioning they declare with respect to sustainability objectives. We do this by analysing how management fees – i.e. the managers’ financial incentives – are linked to the sustainability strategy that investment funds state in their declaration of compliance to the SFDR. Leveraging on organisational category theory, we study the behaviour of funds declaring a membership within two categories introduced by the SFDR: the Article 6 category, i.e. funds declaring no sustainability practices, and the Article 9 category, i.e. funds with explicit sustainability objectives. We retrieve the data for the analysis from the Morningstar Direct database.

We find that for both Article 6 and Article 9 funds there is a positive relationship between financial performances and management fees, as well as between sustainability performances and management fees; essentially, investment funds that claim to belong to two opposite positionings show that managers’ financial incentives are similarly influenced by financial and sustainability performances. Our results can therefore be explained through organisational category theory. Organisational categories have been used as a framework to clarify how entities group with others within specific socially accepted schemas depending on predetermined and shared features, values, and characteristics (Durand and Paolella Citation2013; Glynn and Navis Citation2013; Negro, Koçak, and Hsu Citation2010). Category theory has been already applied in the context of sustainability issues to explain how firms belonging to the same category – i.e. B Corps – differently promote their affiliations, showing diverse levels of distinctiveness within the same category (Gehman and Grimes Citation2017). Since the SFDR defines a predetermined set of attributes and features that aims at distinguishing members that adopt sustainability objectives from those that do not, our results contribute to demonstrate that the European financial industry is currently subject to category fuzziness with respect to sustainability issues (Kovács and Hannan Citation2015; Zhao and Han Citation2020): this means that, despite a stated and formalised distinction with legal relevance, members of different categories are incentivised to behave without distinctions.

Accordingly, our work exploits category theory to evidence the criticalities that a fuzzy financial market may face, suggesting proactive actions for policymakers to adjust the functioning of the Regulation. We hope that our work can help policymakers take effective measures to prevent greenwashing, thus ensuring transparency on sustainability issues in financial markets.

2. Literature review

2.1. The context

10 March 2021, set the date on which the Sustainable Finance Disclosure Regulation (SFDR) 2019/2088 of the European Union came into force, after being adopted on 27 November 2019, by the European Parliament and Council (European Parliament Citation2019). As the Article 1 of the SFDR states,

this Regulation lays down harmonised rules for financial market participants and financial advisers on transparency with regard to the integration of sustainability risks and the consideration of adverse sustainability impacts in their processes and the provision of sustainability-related information with respect to financial products

The purpose of the SFDR is to require financial players to formally declare their degree of compliance to ESG (Environmental, Social, Governance) disclosure and reporting obligations, in an effort to prevent greenwashing – or impact washing – phenomena, which have become increasingly widespread in recent years. Greenwashing is defined as a misleading practice that identifies participants of financial markets as irresponsible and unsustainable with respect to their claims (Cadman Citation2011). Essentially, actors that declare sustainability objectives without behaving in accordance with their achievement are considered greenwashers (de Freitas Netto et al. Citation2020). Actors accused of greenwashing face the threats of bad reputation with respect to the general audience, a condition that may lead to market exclusion, sanctions, and entering lawsuits (Laufer Citation2003; Torelli, Balluchi, and Lazzini Citation2020).

Thus, greenwashing spreads in conditions of unregulated contexts. The financial context has been facing an enormous growth in the direction of sustainable development over the last decade, without this being much controlled by external bodies such as regulators and institutions. Literature evidences that financial actors have already attempted to exploit the sustainability or impact label for mere marketing purposes (Harji and Jackson Citation2012; OECD Citation2019; Findlay and Moran Citation2019), with the objective of better positioning their products in a market where showing sustainable attributes is increasingly central (Busch et al. Citation2021).

Since late 2020, the arrival of the SFDR has led existing investment funds to undergo an intense rebranding process. Data available on Morningstar Direct as of February 2021 show that 256 funds were rebranded by adding terms such as sustainable, ESG, impact, or green to their names; in the first quarter of 2021 alone, just before SFDR came into force, there were already 127 rebranded funds (see Morningstar press release issue to date). This trend emphasised the risk that many financial market participants might simply rename their products with words indicating sustainability purposes, while maintaining their usual operating methods.

Accordingly, the need to adopt the SFDR emerged to solve such issues and evidenced the necessity to formalise how financial market participants shape and manage financial products integrating sustainability factors, which are defined by the SFDR as ‘environmental, social and employee matters, respect for human rights, anti-corruption and anti-bribery matters’. However, the approaches implemented by financial operators may consider sustainability through different approaches.

2.2. Distinguishing typologies of sustainability approaches in financial markets

Financial practices that incorporate ESG aspects into their decision-making processes are typically identified with the term sustainable finance. After several decades of predominance of the Freidmanian vision, according to which businesses are sustainable only if they increase profits for their shareholders, the early 1970s saw the first appearance of sustainable finance, intended as a practice that also addresses aspects of social and/or environmental sustainability (Friede, Busch, and Bassen Citation2015). However, sustainable finance really took off only in the new millennium, in response to the growing need for resources coping with social and environmental crises.

The current prevailing sustainable finance approach is ESG investing, which interprets sustainability as a means of mitigating potential risks arising from social and environmental issues that may negatively affect financial performance (Friede, Busch, and Bassen Citation2015). Within this context, some market participants consider the adoption of ESG criteria with a more proactive approach: in addition to the exclusion of harmful sectors, they consider sustainability factors when selecting investments; for this purpose, investors can leverage on many ESG ratings, which set thresholds to guide investments selection, excluding the ones with little ESG potential.

We are also observing an innovative way of looking at sustainable finance, rooted in the proactive desire to achieve transformative social and environmental change through the allocation of financial resources. This approach is known as impact investing, which regards ‘investments made into companies, organisations, and funds, with the intention to generate measurable social and environmental impact, alongside a financial return’ (Mudaliar, Pineiro, and Bass Citation2016). The term impact investing was coined in 2007 at a meeting organised by the Rockefeller Foundation, to describe ‘a range of activities that participants perceived as distinctive from established practices of socially responsible and ethical investment’ (Findlay and Moran Citation2019). In the last few years, impact investments escalated from being a niche populated only by few pioneers to being an appealing capital allocation strategy for mainstream finance players. Impact investing initiatives are based on exclusionary criteria and aim to achieve higher ESG performances than their peers, as ESG investing approaches do; however, they also require the investment approach to follows pre-determined sustainability objectives (Bugg-Levine and Emerson Citation2011). Thus, impact investing differs from ESG investing approaches because it intentionally defines and pursues measurable social and/or environmental objectives, which guide investment management practices.

Although the attractiveness of impact investing is undoubtedly a positive trend in finance, markets face challenges in trying to rigorously distinguish it from ESG investing and traditional for-profit approaches. Many critical issues emerged when it became evident that this investment strategy lacks a solid theoretical and methodological conceptualisation (Calderini, Chiodo, and Michelucci Citation2018), leading to various interpretations of the boundaries within which an investment initiative can constitute impact investing (Harji and Jackson Citation2012; Busch et al. Citation2021). Despite this, operators of different nature and purpose have continued to refer to their initiatives as impact investing, making it virtually impossible to distinguish attempts at greenwashing from the genuine intentionality in creating transformative social and environmental impact. The recent trend of investment funds to add impact, green or ESG labels to their denominations provides an example of how difficult it is to distinguish consistent impact investors from deceptive ones; we argue that this phenomenon that requires in-depth analysis and action.

2.3. How SFDR interprets different typologies of sustainability approaches

The SFDR’s aim is to define a top-down mechanism supporting financial markets’ participants in their interpretations of sustainability issues. The SFDR is relevant for two main reasons: first, all financial market participants operating in the EU must comply with it; second, it provides a series of useful definitions – i.e. sustainability factors, sustainable investment, sustainability risk – and a list of obligations that financial actors must fulfil, both at the organisation and individual product level. In particular, regarding individual products, financial entities are required to disclose which article of the SFDR – from Article 6 to Article 9 – each of their products complies to (European Parliament Citation2019). Such articles reflect an increasing emphasis on sustainability factors.

Financial products declaring their compliance to Article 6 are characterised by the absence of sustainability goals. For these products, it is required to provide ‘transparency on the integration of sustainability risks’ and a clear explanation of the motivations in the case the product in question does not consider sustainability risks to be relevant. Article 7 instead advocates for higher ‘transparency of adverse sustainability impacts at financial product level’, requiring a detailed and convincing explanation in case adverse impacts are not accounted for. The SFDR then goes on to cover financial products that, although at different levels, consider sustainability as one of their distinctive features: Article 8 calls for ‘transparency of the promotion of environmental or social characteristics in pre-contractual disclosures’, requiring product managers to declare how these characteristics are achieved and what methodology is used to measure them. Finally, Article 9 concerns products with an intentional sustainability objective, thus demanding ‘transparency of sustainable investments in pre-contractual disclosures’; it is therefore necessary to indicate how the investment contributes to achieving the stated sustainability objective and to explain how this latter differs from a traditional market objective. Consequently, financial initiatives that fall within the boundaries of impact investing should be included in Article 9.

Considering the SFDR’s purpose and structure, we believe it constitutes a fundamental instrument for deepening the actual validity of investors’ claims with respect to their contribution to sustainability issues. As the SFDR aims to clearly distinguish actors who define themselves outside a sustainability scope – Article 6 – from those who intentionally define and pursue sustainability objectives – Article 9 –, our objective is to investigate the reliability of investment funds’ claims and explain their behaviour in light of the SFDR framework.

3. Theoretical framework

The way in which the European Union has drafted the SFDR can be explained through the theoretical framework of organisational categories. They are defined as conceptual systems that gather organisations based on shared characteristics (Navis and Glynn Citation2010). Moreover, an organisational category considers a socially construed segment of organisations that have a mutual understanding of the symbols, resources, and attributes that define the assessment of the membership (Gehman and Grimes Citation2017).

The compliance to EU’s SFDR, which imposes actors to indicate a specific positioning among a pool of choices, serves as a relevant example of the symbolic resources that distinguish different category memberships. Kennedy, Lo, and Lounsbury (Citation2010) highlighted that organisational categories differ in the extent to which they have positive appeal and straightforward meaning; they argued that it is more likely for organisations to affiliate in categories that have appeal both for the relevant and clear meaning.

Sustainability is becoming widely appealing for financial actors because it is a new trajectory of innovation, it can provide solid reputation in the market, and it is a source of interesting returns. Accordingly, actors are increasingly attracted by the possibility to position themselves as ‘sustainable’. However, category membership should be a coherent choice that balances the features of the organisation itself and the attribute scheme that the category exhibits (Negro, Koçak, and Hsu Citation2010). Accordingly, some studies emphasise the role of institutional actors in defining the meaning of certain categories (Gehman and Grimes Citation2017; Sine, David, and Mitsuhashi Citation2007).

Thus, although categories can emerge from a mechanism of social acceptance and shared attributes (Negro, Koçak, and Hsu Citation2010; Pontikes Citation2012), in some circumstances institutional actors such as the European Union are able to provide immediate legitimacy to a financial regulation defining a set of social codes able to easily drive financial actors towards a coherent membership. The institutionalisation of categories is a mechanism that facilitates consensus and helps the achievement of social agreements (Durand and Thornton Citation2018). As it normally occurs through the usual repetition and identification – at the community level (Tolbert and Zucker Citation1996) – of a pattern of practices that becomes related to a category of organisation members, literature mostly refers to categories that become institutionalised with a bottom up-process (Durand and Thornton Citation2018; Hsu Citation2006). Conversely, extant literature in neo institutional theory suggests that organisations can be subject to their larger institutional environment to be inscribed in certain organisational categories (Anteby Citation2010; Jourdan, Durand, and Thornton Citation2017; Meyer and Rowan Citation1977). In this scenario, organisations instantiate logics that the relevant audiences comprehend from an institutional intervention, that is, independent of the sensemaking of social schemes and features that may occur from a bottom-up perspective (Durand and Thornton Citation2018; Hsu Citation2006).

Accordingly, in case of top-down mechanisms of category institutionalisation, the social agreement with respect to the categorisation process should be taken for granted and endorsed to avoid members incurring penalisation from the central institution and bad reputation judgements. As a matter of fact, the European Union uses sanctions such as financial charges, fees, or block of investment activities for financial actors that reveal sustainability features that are misaligned with their positioning in the Regulation. For these reasons, we expect from our analysis that category members correctly affiliate themselves to the institutionally defined category.

However, literature reports that organisational categories may be characterised by fuzziness. Category fuzziness occurs when members can be hardly distinguished across categories (Kovács and Hannan Citation2015), evidencing an incorrect correspondence between the characteristics the members exhibit and those that they are supposed to consider from the socially accepted schemes (Vergne and Wry Citation2014; Zhao and Han Citation2020). Category fuzziness leads to negative judgement from the relevant audience to members, posing the categories institutionalisation process at risk (Bogaert, Boone, and Carroll Citation2010). The context of the financial industry serves as a relevant example of category fuzziness as it generally struggles to recognise reliable sustainability practices, raising concerns in discerning actors that exploit sustainability as a marketing signal from those that pursue a substantial and transformative approach to social impact generation. As the SFDR defines a point of no return that establishes clear indications for fighting greenwashing, members should be incentivised to properly interpret the Regulation imposed by the European Union to avoid misleading behaviours that may incur in accusations of greenwashing, and consequent reputational and pecuniary sanctions.

For these reasons, because of the SFDR, we hypothesise that the institutionalisation of categories leads financial actors to position within the category that is mostly coherent with their approach to sustainability. We assess proper category membership and category institutionalisation building on the extant impact investing literature that analyses the financial remuneration and incentives of managers in investment funds with respect to their sustainability objectives (Geczy et al. Citation2021).

Geczy and colleagues (Citation2021) indeed evidenced that in case of funds with sustainability objectives, managers have higher payrolls than their peers working in traditional for-profit funds, because they manage not only financial returns, but also sustainability returns out of their investment activities. Essentially, considering the baseline of higher payrolls, managers of fund with sustainability objectives should not associate financial incentives based on the selection of assets generating higher financial performance, as this could increase the risk of mission drift and of losing the focus on social impact (Ebrahim, Battilana, and Mair Citation2014). Instead, the same managers should get higher financial incentives as they define a portfolio of assets generating higher sustainability performance. Literature reports that the fund managers’ financial incentives are expressed in terms of management fees (Giambona and Golec Citation2009), for which we acknowledge its association with the risk components of the funds (Golec Citation1992), and its delicate role when funds should achieve sustainability objectives. A recent study points out that some funds claiming sustainability objectives require no management fees as a mechanism to disincentivise portfolio focusing primarily on financial returns (Zeidan Citation2022).

Therefore, since the top-down mechanism of institutionalising categories penalises category fuzziness, members of an organisational category should be encouraged to behave in accordance with the peculiar characteristics of that category, and disincentivised to divert from them. Consequently, in the European financial context of adherence to the SFDR, an organisational category including members that declare sustainability objectives should align management fees to a portfolio of assets that generate relevant sustainability performances, and skew management fees from financial performances. Thus, we test the following hypotheses:

Hypothesis 1: The financial performance of an investment fund belonging to a category that fosters sustainability objectives is negatively related to the managers’ financial incentives.

Hypothesis 2: The sustainability performance of an investment fund belonging to a category that fosters sustainability objectives is positively related to the managers’ financial incentives.

4. Data and methodology

4.1. Research design

To investigate our hypotheses, we perform the data collection through the Morningstar Direct software, as it offers the possibility to classify investment funds according to the SFDR guidelines. Accordingly, we create two distinct datasets characterised respectively by European investment funds that, to date, are classified as Article 9 funds (i.e. with intentional sustainability objectives) and Article 6 funds (with no sustainability objectives). The Article 9 database contains 3717 records, whereas the Article 6 database consists of 49059 records.

Our research design considers management fees as a proxy for the behaviour of investment funds. Management fees reflect the internal mechanisms of financial incentives that managers define on top of their investment activities, and generally are a stable characteristic of the fund over time, measured as the percentage managers earn out of the total net assets under management (Giambona and Golec Citation2009). Extant scholars already investigated management fees as a mechanism to assess the reliability of different sustainability approaches (Liang, Sun, and Teo Citation2021), also to identify potential agency problems that may lead to greenwashing practices. Thus, the commitment of the managers to achieve high sustainability performances is a fundamental discriminator between different sustainable finance strategies. To be compliant to the Article 9 positioning within the SFDR, managers of funds claiming sustainability objectives should be incentivised to build a portfolio of assets generating higher sustainability performances than portfolios of assets generating financial performances. On the contrary, in order to comply with Article 6, fund managers should have a stronger incentive to invest in highly profitable assets, regardless of sustainability performance.

Accordingly, the literature argues that the remuneration and incentive structure of managers can be an effective indicator of an organisation’s efforts to generate social and environmental impact (Geczy et al. Citation2021). Previous literature has shown that impact investors seem inclined to provide their capital to highly impactful but less profitable entities, thus sacrificing part of their financial return to achieve a higher impact return (Bugg-Levine and Emerson Citation2011). However, considering the increasing differentiation between ESG and impact investing strategies imposed by the SFDR and the threats of greenwashing practices, this perspective may require specific investigations.

4.2. Characteristics of the sample

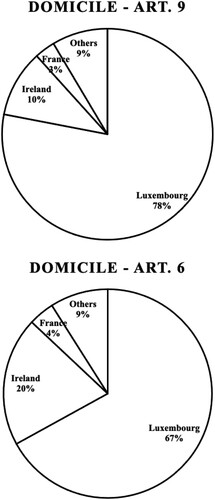

We provide a geographical localisation considering both the funds’ domicile and their investment area, as well as their internal structure of asset classes. Regarding the geographical domicile in , both databases show a prevalence of funds located in Luxembourg, followed by Ireland and France.

Figure 1. Investment funds by Domicile

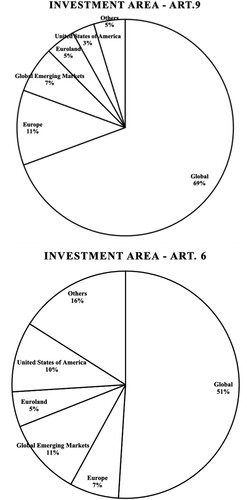

In terms of investment area, – i.e. the geographical regions in which the funds’ investments are concentrated – highlights that both categories reveal a preference for the entire Global Area, followed by Europe, Global Emerging markets, Euroland and the USA.

Figure 2. Investment funds by Investment area

Regarding asset class orientation, shows that most funds have an equity orientation, followed by fixed income and allocation.

Table 1. Investment funds by Global Broad Category Group – SFDR Article 9.

Again, the results from suggest some correspondence among the two databases. This preliminary and descriptive analysis shows a similarity between the funds of the two databases with respect to the variables considered.

Table 2. Investment funds by Global Broad Category Group – SFDR Article 6.

4.3. Description of the variables

We select a set of variables that cover specific characteristics of the sample in order to perform our analyses. Such variables are collected in together with the description provided on the Morningstar Direct software:

Table 3. Variables considered in the analysis.

5 Results

5.1. Descriptive statistics

In the following , we show the descriptive statistics for the variable Management Fees and the set of variables included in our model, respectively within the databases of Article 9 and Article 6 funds. The findings suggest that, on average, Article 9 funds pay lower management fees than Article 6 funds.

Table 4. Management fee descriptive statistics.

, on the other hand, summarises the percentages of funds in the databases belonging to the different Sustainability Rating categories.

Table 5. Funds by sustainability rating.

The results show a greater percentage of Article 9 funds belonging to higher levels of the Sustainability Rating. In fact, almost three quarters of the Article 9 funds (72.83%) belong to the two classes with the highest level of sustainability, while for Article 6 just over 30% of funds belong to the highest classes. Moreover, for Article 9 only about 5% of funds belong to the two worst classes from the point of view of sustainability, while for Article 6 the percentage is over 27%.

and 7 show the set of variables we include in our research design, respectively for Article 9 and Article 6 funds.

Table 6. Set of variables – SFDR Article 9.

Table 7. Set of variables – SFDR Article 6.

On average, Article 9 funds show a higher level of Financial Return and lower Fund Age with respect to Article 6 funds.

provides the percentages of funds in both databases that belong to the different Sector categories.

Table 8. Sector categories – SFDR Articles 9 and 6.

In this case, we find a difference between the two databases: for Article 6, there is a clear prevalence of Multisector funds (68.63%), followed at a considerable distance by the Sensitive and Cyclical sectors, while the Defensive one maintains a marginal presence at around 2%; in contrast, for Article 9 two categories are in clear majority – Sensitive and Multisector – while the Cyclical and Defensive ones are much less represented.

To verify that our analysis on Article 9 and Article 6 funds is relevant, we test for the significant difference between the two datasets with respect to their sustainability performances. Accordingly, we perform a t-test on the Sustainability Rating variable. The outcome of the t-test is summarised in the following .

Table 9. Outcome of the t-test,

Thanks to the t-test, we demonstrate that the difference between the average Sustainability Rating of the two databases is statistically significant. Accordingly, since the aim of our analysis is to answer our initial research question and determine the accuracy of the hypotheses formulated, we analyse the relationship between Management Fees– which represents the dependent variable – and two of the most relevant characteristics of investment funds, i.e. their financial performance and their level of sustainability. We take as the reference variables of such dimensions respectively the Financial Return and the Sustainability Rating, in line with the data provided by Morningstar Direct: these constitute the main independent variables of our models. We choose to isolate the effect of the two main independent variables in order to study them independently and more accurately. This implies the need to create, for each database, two different regression models, containing only one of the two main independent variables, plus a set of control variables.

5.2. Correlations

We check for multicollinearity between the independent variables of our models. We do this by constructing a correlation matrix in which we show the Pearson correlation values for each pair of variables; and present the matrices.

Table 10. Correlation Matrix for the database of SFDR Article 9 funds.

Table 11. Correlation Matrix for the database of SFDR Article 6 funds.

None of the pairs of variables present collinearity problems: we therefore include all selected independent variables in the final regression model.

5.3. Regressions

We present the most relevant results of the two models in and 13. We show for each independent variable the estimate, the p-value – represented by the number of asterisks in which p < 0.1 = *; p < 0.05 = **; p < 0.01 = *** – and, in brackets, the standard error.

Table 12. Results of Model 1.

In , the analysis shows that the main independent variable, Financial Return, is positively correlated with Management Fees and is highly significant for Article 9 funds. This result conflicts with Hypothesis 1, and shows that funds categorised in Article 9 with higher financial performances tend to have higher financial incentives. In Model 1, all variables are statistically significant except for Sector Sensitive and Fund Age. In particular, we find that Article 9 funds evidence a positive correlation of Manager Average Tenure and NAV with the Management Fees. For funds with sustinability objectives, asset values and the tenure of managers tend to influence the management fees. With regard to Article 6 funds, the analysis provides similar results with respect to the one conducted on Article 9; also in this case, the main independent variable, Financial Return, is statistically significant and positively related to the Management Fees. Differently from Article 9 funds, the age of the fund is statistically significant and influences the management fees.

As Hypothesis 1 suggests that the more investment funds self-select in categories requiring the definition of sustainability objectives, the less they should align management fees with financial returns, the results from Model 1 instead indicate that investment funds tend to align management fees with their financial returns regardless of their positioning with respect to the SFDR. This is coherent for purely profit-oriented funds – Article 6 –, but inconsistent for those that intentionally decide to also pursue sustainability objectives – Article 9. Our analysis reveals that Article 6 and Article 9 funds seem to behave similarly with respect to their system of financial incentives, regardless of their positioning with respect to sustainability strategies and to the SFDR framework.

summarises the results valid to test for Hypothesis 2. In Model 2, for Article 9 funds, the outcome of the regression model demonstrates that the main independent variable, the Sustainability Rating, is positively correlated with Management Fees and is statistically significant. This result confirms Hypothesis 2: funds with sustainability objectives have higher financial incentives when they allocate financial resources to assets presenting higher sustainability performances.

Table 13. Results of Model 2.

Interestingly, for Article 6 funds, we find similar results also in this case. Even funds with no sustainability objectives receive higher financial incentives when they structure portfolios of assets with higher sustainability performances, suggesting that Article 6 funds are incentivised to behave in a similar manner to Article 9 ones.

Hypothesis 2 stated that the more investment funds define sustainability objectives, the more they should align management fees with sustainability performance, and the results of Model 2 show Article 9 funds confirming our predictions. However, also Article 6 funds tend to align management fees with their sustainability performance. Therefore, also with regard to sustainability performance, Article 6 and Article 9 funds seem to be incentivised to adopt the same behaviour, regardless of their different positioning with respect to sustainability strategies and the SFDR framework.

6. Discussion

The aim of the paper was to analyse how European investment funds are incentivised to behave according to their sustainability claims. We considered the innovations brought by the SFDR to study the extent to which the Regulation stimulates actors claiming sustainability objectives to internally arrange in order to pursue them. To achieve this, we used Morningstar Direct to create two datasets of Article 6 funds and Article 9 funds for respectively assessing how fund managers are financially incentivised to achieve both financial and sustainability performances. Considering that Article 6 funds comprise financial products with no sustainability objectives, and Article 9 funds gather financial products with intentional sustainability objectives, we framed our reasoning around organisational category theory to explain potential differences. Our results show that funds self-selecting within the two opposite groups are incentivised to behave in a remarkably similar way on both the financial and sustainability side. Accordingly, our results offer the following potential contributions.

First, our study evidences that, despite the innovation brought by the SFDR, the European financial market context is still characterised by ambiguity and category fuzziness. Article 6 funds and Article 9 funds express two types of categories that oblige financial products to self-discriminate against sustainability goals; our results show that besides a façade of distinct memberships, when we investigate the internal structure of incentives, such distinction is no longer valid. Managers from both type of funds exhibit higher financial incentives for portfolios of assets presenting the same schema of financial and sustainability performances. Extant literature indicates that category fuzziness recalls organisations that span multiple market categories (Bogaert, Boone, and Carroll Citation2014; Vergne and Wry Citation2014). Previous studies investigated fuzziness in the financial context, showing conflicting results (Shen, Li, and Tolbert Citation2021). In particular, scholars considered the investment portfolio as the unit of analysis to disentangle fuzziness, evidencing that investors may prefer ventures that are related to ‘fuzzy’ categories because they can benefit from cross-pollination and distant knowledge sources. However, fuzziness may also reduce the consensus from the relevant audience as it creates confusion and ambiguity (Cudennec and Durand Citation2022; Hsu, Hannan, and Koçak Citation2009). We contribute to the literature of category fuzziness taking the perspective of the funds’ internal structure, evidencing that management strategies span across multiple categories: with respect to financial performances, they claim membership to Article 9, but behave as Article 6 funds. On the other hand, with respect to sustainability performances, they claim membership to Article 6, but they behave exactly like Article 9 funds.

Second, such perspective of category fuzziness in the financial context poses concerns for greenwashing practices. As funds are increasingly adding terms such as ‘sustainable’, ‘ESG’, ‘impact’, or ‘green’ to their denominations, our results show that sustainability claims are frequently linked to a fund conduct that does not necessarily differ from that of purely for-profit funds. Essentially, our work suggests that such practices of relabelling may potentially mask a behaviour that is not in line with the actual achievement of sustainability objectives. Accordingly, category fuzziness may open potential research avenues deepening on the determinants of such fuzziness in financial contexts. As categories exhibit fuzziness when members straddle the boundaries (Negro, Hannan, and Rao Citation2011), our results suggest that the SFDR currently presents loose boundaries and is therefore unable to fulfil its ultimate objective of transparency on sustainability claims. We argue that the determinants of such fuzziness are to be sought mainly on two fronts: the varying maturity of sustainable finance in European countries and the approach of European and national policymakers towards sustainability issues.

Indeed, the sustainable finance industry is at different stages of growth in the various European countries and the expertise of market players is consequently very diverse (Ahlström and Monciardini Citation2022). We thus suggest greater efforts to be put in place by European and national institutions to standardise the knowledge base on sustainability concepts that financial actors need to acquire in order to position themselves correctly and intentionally pursue impact objectives. We also recommend that policymakers clarify how sustainability risks and impact outcomes should be accounted for at each level (from Article 6–9). A preliminary alignment between the information to be disclosed and the main impact measurement frameworks currently available could help funds understand what information they are actually willing to share (Bengo, Boni, and Sancino Citation2022). This may allow them to self-position in the most appropriate category from the beginning, thus avoiding category fuzziness.

On the other hand, we contend that policymakers at the European and national level should put sustainability issues at the centre of their agendas and ask the financial world’s leaders to do the same. At the moment, policymakers are struggling to properly distinguish values, norms and features that characterise what is sustainable from what is not. However, sustainability issues are becoming incredibly urgent and will require serious attention from governments in the short term. We thus encourage political figures to improve their knowledge of sustainability topics and grasp the importance of sustainable development as the most crucial innovation lever for the European financial system. We hope that our research will inspire scholars to increase the focus on social and environmental sustainability from a policy perspective; an interesting avenue for future research could include an exploration of the extent to which sustainability-related skills of European policymakers and government officials are relevant compared to their finance-based competences.

With this work, our objective is essentially to stimulate European authorities to make fine-grained modifications to the SFDR. Besides the adjustments to the Regulation, and the definition of more straightforward boundaries, the European financial market needs a more severe monitoring mechanism of the managers’ financial incentives with respect to the self-adopted positioning in terms of sustainability objectives. The commitment of the management to allocate resources to assets generating higher sustainability performances is a crucial step to avoid greenwashing, helping funds to comply with regulatory frameworks and to deliver significant social and environmental impact.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Ahlström, H., and D. Monciardini. 2022. “The Regulatory Dynamics of Sustainable Finance: Paradoxical Success and Limitations of EU Reforms.” Journal of Business Ethics 177 (1): 193–212.

- Anteby, M. 2010. “Markets, Morals, and Practices of Trade: Jurisdictional Disputes in the U.S. Commerce in Cadavers.” Administrative Science Quarterly 55: 606–638.

- Becker, M. G., F. Martin, and A. Walter. 2022. “The Power of ESG Transparency: The Effect of the new SFDR Sustainability Labels on Mutual Funds and Individual Investors.” Finance Research Letters. Article 102708.

- Bengo, I., L. Boni, and A. Sancino. 2022. “EU Financial Regulations and Social Impact Measurement Practices: A Comprehensive Framework on Finance for Sustainable Development.” Corporate Social Responsibility and Environmental Management, 1–11.

- Bogaert, S., C. Boone, and G. R. Carroll. 2010. “Organizational Form Emergence and Competing Professional Schemata of Dutch Accounting, 1884-1939.” In Categories in Markets: Origins and Evolution (Research in the Sociology of Organizations, Vol. 31), edited by G. Hsu, G. Negro, and Ö Koçak, 115–150. Bingley: Emerald Group Publishing Limited.

- Bugg-Levine, A., and J. Emerson. 2011. Impact Investing: Transforming how we Make Money While Making a Difference. Hoboken: John Wiley & Sons.

- Busch, T., P. Bruce-Clark, J. Derwall, R. Eccles, T. Hebb, A. Hoepner, C. Klein, et al. 2021. “Impact Investments: A Call for (re)Orientation.” SN Business & Economics 1 (33): 1–13.

- Cadman, T. 2011. “Evaluating the Governance of Responsible Investment Institutions: An Environmental and Social Perspective.” Journal of Sustainable Finance & Investment 1: 20–29.

- Calderini, M., V. Chiodo, and F. V. Michelucci. 2018. “The Social Impact Investment Race: Toward an Interpretative Framework.” European Business Review 30 (1): 66–81.

- Cudennec, A., and R. Durand. 2022. “Valuing Spanners: Why Category Nesting and Expertise Matter.” Academy of Management Journal.

- de Freitas Netto, S. V., M. F. F. Sobral, A. R. B. Ribeiro, and G. B. da Luz Soares. 2020. “Concepts and Forms of Greenwashing: A Systematic Review.” Environmental Sciences Europe 32: 19.

- Durand, R., and L. Paolella. 2013. “Category Stretching: Reorienting Research on Categories in Strategy, Entrepreneurship, and Organization Theory.” Journal of Management Studies 50 (6): 1100–1123.

- Durand, R., and P. Thornton. 2018. “Categorizing Institutional Logics, Institutionalizing Categories: A Review of Two Literatures.” Academy of Management Annals 12: 2.

- Ebrahim, A., J. Battilana, and J. Mair. 2014. “The Governance of Social Enterprises: Mission Drift and Accountability Challenges in Hybrid Organizations.” Research in Organizational Behavior 34: 81–100.

- European Parliament. 2019. “Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on Sustainability-Related Disclosures in the Financial Services Sector (Text with EEA Relevance).” Official Journal of the European Union 317 (1): 1–16.

- Findlay, S., and M. Moran. 2019. “Purpose-washing of Impact Investing Funds: Motivations, Occurrence and Prevention.” Social Responsibility Journal 15 (7): 853–873.

- Friede, G., T. Busch, and A. Bassen. 2015. “ESG and Financial Performance: Aggregated Evidence from More Than 2000 Empirical Studies.” Journal of Sustainable Finance & Investment 5 (4): 210–233.

- Geczy, C., J. S. Jeffers, D. K. Musto, and A. M. Tucker. 2021. “Contracts with (Social) Benefits: The Implementation of Impact Investing.” Journal of Financial Economics 142 (2): 697–718.

- Gehman, J., and M. Grimes. 2017. “Hidden Badge of Honor: How Contextual Distinctiveness Affects Category Promotion among Certified B Corporations.” Academy of Management Journal 60 (6): 2294–2320.

- Giambona, E., and J. Golec. 2009. “Mutual Fund Volatility Timing and Management Fees.” Journal of Banking & Finance 33 (4): 589–599.

- Glynn, M. A., and C. Navis. 2013. “Categories, Identities, and Cultural Classification: Moving Beyond a Model of Categorical Constraint.” Journal of Management Studies 50 (6): 1124–1137.

- Golec, J. H. 1992. “Empirical Tests of a Principal-Agent Model of the Investor-Investment Advisor Relationship.” Journal of Financial and Quantitative Analysis 27 (1): 81–95.

- Harji, K., and E. T. Jackson. 2012. Accelerating Impact – Achievements, Challenges and What’s Next in Building the Impact Investing Industry. New York: E.T. Jackson & Associates Ltd. and Rockefeller Foundation.

- Hsu, G. 2006. “Jacks of all Trades and Masters of None: Audiences’ Reactions to Spanning Genres in Feature Film Production.” Administrative Science Quarterly 51: 420–450.

- Hsu, G., M. T. Hannan, and Ö Koçak. 2009. “Multiple Category Memberships in Markets: An Integrative Theory and two Empirical Tests.” American Sociological Review 74 (1): 150–169.

- Jourdan, J., R. Durand, and P. Thornton. 2017. “The Price of Admission: Organizational Deference as Strategic Behavior.” American Journal of Sociology 123: 1.

- Kennedy, M. T., J. Lo, and M. Lounsbury. 2010. “Category Currency: Meaning Change and the Dynamics of Market Categories.” Research in the Sociology of Organizations 31: 369–397.

- Kovács, B., and M. T. Hannan. 2015. “Conceptual Spaces and the Consequences of Category Spanning.” Sociological Science 2: 252–286.

- Laufer, W. S. 2003. “Social Accountability and Corporate Greenwashing.” Journal of Business Ethics 43 (3): 253–261.

- Liang, H., L. Sun, and M. Teo. 2021. “Greenwashing: Evidence from Hedge Funds. Available at SSRN 3610627.

- Meyer, J. W., and B. Rowan. 1977. “Institutionalized Organizations: Formal Structure as Myth and Ceremony.” American Journal of Sociology 83 (2): 340–363.

- Mudaliar, A., A. Pineiro, and R. Bass. 2016. Impact Investing Trends: Evidence of a Growing Industry. New York, NY: Global Impact investing Network.

- Navis, C., and M. A. Glynn. 2010. “How New Market Categories Emerge: Temporal Dynamics of Legitimacy, Identity, and Entrepreneurship in Satellite Radio, 1990–2005.” Administrative Science Quarterly 55 (3): 439–471.

- Negro, G., M. T. Hannan, and H. Rao. 2011. “Category Reinterpretation and Defection: Modernism and Tradition in Italian Winemaking.” Organization Science 22 (6): 1449–1463.

- Negro, G., Ö Koçak, and G. Hsu. 2010. “Research on Categories in the Sociology of Organizations.” In Categories in Markets: Origins and Evolution (Research in the Sociology of Organizations, Vol. 31), edited by G. Hsu, G. Negro, and Ö Koçak, 3–35. Bingley: Emerald Group Publishing Limited.

- OECD. 2019. Social Impact Investment 2019: The Impact Imperative for Sustainable Development. Paris: OECD Publishing.

- Pontikes, E. G. 2012. “Two Sides of the Same Coin: How Ambiguous Classification Affects Multiple Audiences’ Evaluations.” Administrative Science Quarterly 57 (1): 81–118.

- Schütze, F., and J. Stede. 2021. “The EU Sustainable Finance Taxonomy and its Contribution to Climate Neutrality.” Journal of Sustainable Finance & Investment, 1–33. doi:10.1080/20430795.2021.2006129.

- Shen, X., H. Li, and P. S. Tolbert. 2021. “Converging Tides Lift All Boats: Consensus in Evaluation Criteria Boosts Investments in Firms in Nascent Technology Sectors.” Organization Science.

- Sine, W. D., R. J. David, and H. Mitsuhashi. 2007. “From Plan to Plant: Effects of Certification on Operational Start-up in the Emergent Independent Power Sector.” Organization Science 18 (4): 578–594.

- Tolbert, P. S., and L. G. Zucker. 1996. “The Institutionalization of Institutional Theory.” In Handbook of Organization Studies, edited by S. R. Clegg, W. N. Nord, and C. Hardy, 175–190. Thousand Oaks, CA: Sage.

- Torelli, R., F. Balluchi, and A. Lazzini. 2020. “Greenwashing and Environmental Communication: Effects on Stakeholders’ Perceptions.” Business Strategy and the Environment 29 (2): 407–421.

- Vergne, J. P., and T. Wry. 2014. “Categorizing Categorization Research: Review, Integration, and Future Directions.” Journal of Management Studies 51 (1): 56–94.

- Zeidan, R. 2022. “Obstacles to Sustainable Finance and the covid19 Crisis.” Journal of Sustainable Finance & Investment 12 (2): 525–528.

- Zhao, M., and J. Han. 2020. “Tensions and Risks of Social Enterprises’ Scaling Strategies: The Case of Microfinance Institutions in China.” Journal of Social Entrepreneurship 11 (2): 134–154.