?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This research investigates the factors influencing Corporate Environmental Performance (CEP) using S&P 500 firm-level data spanning 2001-2022. Drawing on existing literature, the study argues that corporate environmental performance (CEP) is positively affected by certain corporate characteristics. Specifically, the study reveals that CSR-linked compensation, the presence of a CSR committee, disclosure policies, and environmental targets are positively associated with CEP. Furthermore, the study shows that the inclusion of independent directors and female board members can also lead to higher CEP scores. Additionally, the findings indicate that analyst coverage and network size are positively linked to CEP. Robustness tests, including 2SLS, subsample analysis, and alternative measures, provide further support for the primary conclusions. The study's results contribute to the growing body of research on the importance of corporate characteristics in promoting sustainable business practices.

1. Introduction

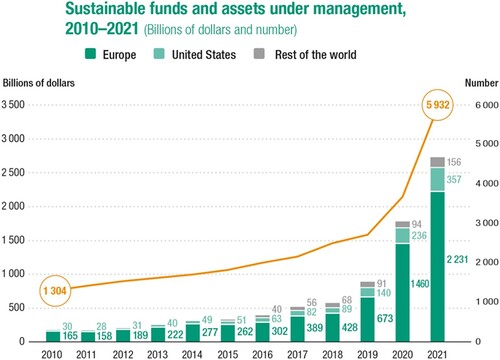

Environmental sustainability is a critical issue facing society, and corporate environmental performance (CEP) plays a significant role in achieving sustainable development goals. In recent decades, sustainable funds and assets under management have increased dramatically.Footnote1 Also, CEP has become a significant concern for investors and stakeholders who are increasingly demanding that companies take environmental responsibility seriously. Moreover, they are increasingly aware of the importance of environmental performance in terms of long-term sustainability and risk management. Therefore, understanding the factors that influence CEP is vital for promoting sustainable development.

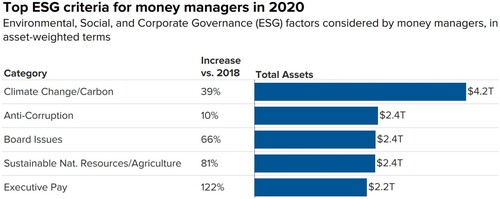

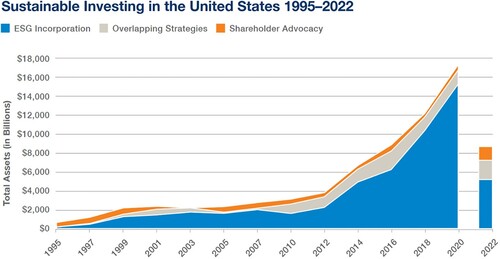

In the U.S. setting, sustainable investment has jumped in recent years (see Figure A2). The U.S. market has seen a growing trend in corporate environmental investment. One of the main drivers of corporate environmental investment in the U.S. is the growing demand from consumers and investors for environmentally sustainable products and services. In response to this growing demand, U.S. firms have increased their investment in environmental initiatives. Likewise, there are increasing concerns for top ESG criteria for money managers about climate risk, sustainable development, and executive pay (Figure A3).

Previous studies have shown that CEP can positively affect a firm’s financial performance, leading to increased investment and improved stock performance (i.e. Jo and Harjoto Citation2011). Corporate environmental performance is essential for understanding the factors that drive firms to adopt and implement environmentally sustainable practices. In other words, gaining insights into how CEP affects financial performance can help firms to attract investors and achieve long-term profitability. In this sense, firms need to urgently establish effective environmental management strategies, reduce environmental risks and impacts, and enhance environmental performance.

Despite the breadth of this literature, relatively less attention appears to have been given to the comprehensive analysis of factors that affect CEP. Besides, the benefits of having a higher proportion of independent directors and female board members also need further investigation. This study aims to narrow the gap and missing part of the literature by conducting a comprehensive examination of the determinants of environmental performance and investments from a variety of aspects. This study offers incremental contributions, and it diverges from the existing literature. Moreover, this study highlights the unique aspects such as the focus on CSR-linked compensation, the role of a CSR committee, disclosure policies, environmental targets, and the influence of board composition on CEP. Most importantly, this is the first paper that covers all these elements, which aims to underscore the distinctive contributions of the study and how it extends and enriches the current understanding of the factors influencing environmental performance.

Specifically, the primary objective of this study is to investigate the determinants of corporate environmental performance (CEP) and assess its effect on financial performance. In addition to the primary objective, this study has several additional aims. These include examining the impact of CSR-linked compensation schedules for executives (H1), assessing the influence of CSR committees, disclosure practices, and CSR strategies on CEP (H2 and H3), and investigating the roles of independent directors and female board members in shaping CEP and reducing agency costs (H4 and H5). These additional aims are expected to enrich this study and tend to provide a more comprehensive analysis of CEP's determinants and implications for businesses and stakeholders.

To fill the gap, this study begins by testing the preliminary prediction that firms should enjoy an environmental benefit (greater environmental score and emission score) on implementing the CSR-linked compensation schedule as an executive incentive. Importantly, this study then extends the argument to propose and test the more refined prediction that establishing CSR committees, disclosure, and strategies can also have a positive effect on CEP. Further investigation on the benefits of having independent directors and female board members is conducted. Differentiated from the previous literature, this study uses score value for CSR-linked compensation, CSR committee, disclosure, and other environmental targets while existing studies use dummy variables.

Of direct relevance, these factors then manifest in the relative benefits of reduced agency costs, more efficient financing and investing decisions, and enhanced monitoring. Noted from existing studies that, information asymmetry is mitigated when companies have established committees and strategies. These internal bodies also play a monitoring role. Further, the risk-shifting problem (managers make risky investment decisions that maximize equity shareholder value at the expense of debtholders’ interests) is relatively less severe in firms with more independent and female directors.

The study uses a sample of 11,032 firm-level observations during the period 2001–2022 across 24 industries of 11 sectors (GIC standard) in the U.S. setting. The environmental score (Escore) is employed as the primary measure of CEP, and the emission score (Emission) as the secondary measure for robustness purposes. Several groups of variables of interest are examined such as CSR-linked compensation incentives, CSR committee, disclosure, strategy, environmental Targets, as well as the appearance of independent directors and female board members.

In detail, this study tends to interpret these aspects as providing support for the argument about CEP. The risk of environmental misconduct and risk-taking investment are both lower, and agency costs are reduced through enhanced monitoring, and hence as formalized in the first hypothesis of the positive association between CER and CSR-linked compensation incentive. Importantly, incentive in hand does not necessarily mean the executives will generate great environmental performance, and executives can still propose risky projects. Therefore, CSR committees, Disclosure, Environmental Targets, and other strategies are also vital internal support functions. Next, to directly test H2, this study focuses exclusively on the environmental committee, team, and other CSR-related bodies that potentially benefit the corporate environmental performance.

Further, to test H3 companies with CSR-related Targets such as emission targets, and water and waste targets, can outperform these without the schedule about environmental performance. Additionally, the positive impact of more independent directors and female board members should not be neglected, and thereby the benefits arising from this aspect should be of the same importance. Hence, as formalized in the fourth hypothesis, H4a, the proportion of independent directors is positively related to environmental performance; H4b, the higher the proportion of female corporate board members, the greater CEP. In H5, other potential factors such as analyst coverage and networking size have been investigated.

The research sheds direct light and makes several key contributions to the literature. At a higher level, it provides new and direct evidence confirming the benefits for firms to establish CSR-linked compensation, committee, disclosure, and environmental targets as well as having more independent and female board members concerning environmental investment and performance. As described above, these benefits are argued to arise from several factors, including higher incentives for executives. Secondly, increased monitoring by CSR bodies such as committees and auditors, and thirdly a less severe risk-shifting problem when more independent and female board members have. As such, the results provide potential insights into the underlying drivers of CEP. Thus, this study represents an important step forward in understanding the role that different environmental targets, incentives, and compensation schedules play in sustainable development, most notably around environmentally sensitive industries.

The remainder of this paper proceeds as follows. Section 2 discusses the theoretical background, summarizes the literature, and develops hypotheses. Section 3 discusses the empirical methodology and describes the sample data. Section 4 presents the empirical results and finally, Section 5 concludes the study.

2. Hypothesis and related literature

2.1. Theoretical backgrounds

Previous literature on agency theory posits that organizations need to consider the interests of all stakeholders, including shareholders, employees, customers, and the wider community (i.e. Eisenhardt Citation1989). This study aligns with this theory by examining how certain corporate characteristics, such as CSR-linked compensation and the presence of a CSR committee, contribute to improved CEP, reflecting a commitment to broader stakeholders. In addition, this study fits the agency theory because it aims to address the principal-agent relationship within corporations and the need for mechanisms to align the interests of executives (agents) with those of shareholders (principals). This study draws on agency theory by exploring the impact of CSR-linked compensation on CEP. This reflects the notion that aligning executive compensation with CSR goals creates incentives for executives to prioritize environmental performance, aligning their interests with those of shareholders interests.

Further, the corporate governance theory (see. Williamson Citation1988; Bhagat and Bolton Citation2008; John, Litov, and Yeung Citation2008) also guides the exploration of the impact of board composition on CEP. The inclusion of independent directors and female board members is informed by the belief that diverse and independent governance structures contribute positively to sustainable and responsible corporate behavior. Moreover, prior studies have focused on firm's resources and capabilities drive its competitive advantage. This study examines how certain corporate resources, such as environmental targets and disclosure policies, contribute to superior CEP.

2.2. CSR-related executive compensation incentives

Research suggests that companies with CSR-linked compensation incentives are likely to have greater corporate environmental performance. CSR-linked executive compensation incentives are significantly associated with higher environmental scores. A study by Wang et al. (Citation2015) finds that CSR-linked compensation incentives positively influence corporate environmental responsibility. They suggested that such incentives motivate employees to adopt environmentally responsible practices and create a culture of sustainability within the organization. Companies with such incentives are more likely to adopt environmentally responsible practices as part of their overall CSR strategy. Further, Radu and Smaili (Citation2022) examine the effect of the CSR committee and CSR-linked executive compensation on CSR performance. The study finds that both the presence of a CSR committee and CSR-linked executive compensation positively influence CSR performance, suggesting that alignment and monitoring mechanisms can enhance CSR outcomes. Moreover, Bai, Sarkis, and Dou (Citation2016) show that firms with CSR-linked compensation incentives are more likely to engage in environmental management and disclose environmental information.

Furthermore, Cordeiro and Sarkis (Citation2008) investigate the effectiveness of explicit contracting in linking CEO compensation to environmental performance. The study suggests that explicit contracting can effectively align CEO compensation with environmental performance, leading to improved environmental outcomes. Besides, Al-Shaer, Albitar, and Liu (Citation2023) suggest that CEOs with greater power tend to receive higher compensation linked to corporate environmental responsibility. Companies with a greater emphasis on CSR and sustainability in their compensation schemes tend to achieve higher CEP. Environmental performance is positively associated with executive compensation, indicating that firms reward executives for improving environmental outcomes (Berrone and Gomez-Mejia Citation2009).

Callan and Thomas (Citation2014) find that the specific measure of compensation used can influence the relationship between CEO compensation and performance outcomes, highlighting the importance of considering different compensation metrics. Likewise, Deckop, Merriman, and Gupta (Citation2006) find that CEO pay structure, specifically the proportion of equity-based compensation, positively influences corporate social performance, indicating that aligning CEO incentives with social objectives can enhance social performance. Moreover, there is evidence that financial incentives positively influence CSR performance, and there are learning effects that enhance the relationship between CSR performance and incentives over time (Derchi, Zoni, and Dossi Citation2021).

Therefore, companies with CSR-linked compensation incentives are likely to have greater corporate environmental performance due to the motivation provided to employees and executives to engage in environmentally responsible practices, and the positive influence of such incentives on employee behavior, organizational culture, and CSR strategy. Hence, this study proposes the following hypothesis.

H1: Ceteris paribus, there is a positive association between corporate environmental performance (CEP) and CSR-linked executive compensation incentives.

2.3. CSR-related committee, disclosure, and strategy

Previous literature indicates that companies with a dedicated CSR committee are likely to perform better environmentally. Specifically, Gond et al. (Citation2017) find that companies with CSR committees are likely to adopt environmental standards and engage in environmental reporting. CSR committees could catalyze environmental action within companies. indicate that the presence of CSR committees positively influences ESG performance. Baraibar-Diez and Odriozola (Citation2019) highlight the importance of dedicated committees in driving sustainable practices. Likewise, Elmaghrabi (Citation2021) provides evidence suggesting that CSR committee attributes, such as expertise and independence, positively influence CSR performance, highlighting the importance of effective committee composition.

In another vein, several studies have found that companies that engage in CSR reporting tend to have better environmental performance. For example, Clarkson et al. (Citation2008) find that firms with better environmental performance tend to disclose more information about their environmental practices. Likewise, a previous study found a positive relationship between CSR disclosure and environmental performance. Firms with higher levels of environmental disclosure tend to have better environmental performance (Orlitzky, Schmidt, and Rynes Citation2003). In addition, Gond et al. (Citation2017) indicate that corporations with higher levels of CSR disclosure have a higher likelihood to adopt environmental standards and engage in environmental reporting. They argue that CSR disclosure could act as a signal of a company's environmental commitment and could influence stakeholder perceptions. Additionally, Al-Tuwaijri, Christensen, and Hughes Li (Citation2004) use a simultaneous equations approach to analyze the relationships among environmental disclosure, environmental performance, and economic performance. The study provides empirical evidence supporting a positive association between environmental disclosure and both environmental and economic performance.

These studies suggest that CSR disclosure can be an important driver of corporate environmental performance. By providing transparency and accountability, CSR disclosure can encourage companies to improve their environmental practices and policies and communicate their environmental performance to stakeholders. Moreover, CSR reporting has been found to positively influence environmental performance by enhancing stakeholder engagement, improving internal decision-making processes, and promoting a culture of sustainability within the company (Cormier and Magnan Citation1999). The quality of CSR reporting matters. Firms that provide more comprehensive, transparent, and credible CSR reports tend to have better CEP than those that provide incomplete or inconsistent information. Based on these, this study proposes the second hypothesis as below.

H2: Ceteris paribus, companies achieve better environmental performance in the presence of a CSR committee, CSR disclosure, audit team, and strategy.

2.4. CSR targets and environmental performance

Prior studies show that companies with higher CSR Targets tend to have greater corporate environmental performance. For example, Maas (Citation2018) investigates whether the inclusion of corporate social performance targets in executive compensation contributes to CSP. The findings suggest that the presence of CSP targets positively influences CSP, which shows that linking executive compensation to social performance can drive improved social outcomes. Kolk and Pinkse (Citation2008) show that firms with formal environmental management systems (EMS) are likely to set and achieve environmental targets. CSR targets help firms identify and prioritize environmental issues and motivate them to take action to address these issues.

Furthermore, studies have shown that firms with emission targets tend to achieve better CEP compared to those without targets. Having a clear goal or target can provide companies with a sense of direction and motivation to reduce their emissions and improve CEP. Christmann and Taylor (Citation2006) find that companies with environmental management systems (EMS) tend to have higher levels of innovation related to environmental performance. It also helps them to monitor and track their progress toward achieving their targets. In a recent study, Liu (Citation2023) indicates that adopting green innovation not only reduces firm volatility and credit risk but also improves both firm value and emission performance. Therefore, setting emission targets can signal to stakeholders, such as investors and customers, that the company is committed to reducing its environmental impact.

Diversity and inclusion initiatives have been gaining increasing attention in the corporate world. Literature has indicated that diversity targets are associated with a greater focus on social and environmental issues, leading to more sustainable business practices and policies (Adams and Ferreira Citation2009). Diversity targets promote a culture of inclusivity and encourage the participation of all employees in environmental decision-making processes. Thus, setting and achieving CSR targets can be an important driver of corporate environmental performance. By providing a clear focus and direction for environmental action, CSR targets can motivate companies to improve their environmental performance and achieve better outcomes. Hence, H3 is proposed as below,

H3: Ceteris paribus, corporates established CSR-related Targets such as emission targets, water, and diversity targets, are likely to outperform these without the Targets about CEP.

2.5. Board composition: independent directors and female board members

Companies with more independent directors and female board members are likely to achieve greater corporate environmental performance. Independent directors on boards can act as a check on management and help to ensure that companies are adopting environmentally responsible practices. Board independence is positively associated with corporate social responsibility, including environmental responsibility. Diverse boards are more likely to engage in socially responsible practices (Harjoto, Laksmana, and Lee Citation2015). Further, Byron and Post (Citation2016) indicate that having women on boards is associated with better corporate social performance. Haque (Citation2017) finds that board characteristics, such as board size and board independence, and the adoption of sustainable compensation policies positively influence carbon performance, indicating their role in driving environmental outcomes.

Likewise, corporate governance mechanisms, such as board independence and board size, positively influence executive compensation for CSR, indicating the role of governance in incentivizing CSR activities (Hong, Li, and Minor Citation2016). Firms with more independent directors are likely to have greater corporate environmental performance due to their diverse perspectives, expertise, and ability to act as a check on management. Hence, H4a is proposed as follows.

H4a: Ceteris paribus, the proportion of independent directors is positively related to environmental performance.

Previous studies have shown that gender diversity on boards is positively associated with corporate environmental performance (i.e. Westphal and Milton Citation2000). The researchers also suggest that female board members can bring a different perspective and greater attention to social and environmental issues. Likewise, Adams and Ferreira (Citation2009) present that gender diversity on boards is positively associated with CEP, including environmental responsibility. It is likely that gender-diverse boards tend to have environmental committees and engage in environmental reporting (Cahan et al. Citation2016). In a similar vein, Ben-Amar, Chang, and McIlkenny (Citation2017) find that greater board gender diversity is associated with stronger corporate response to sustainability initiatives, suggesting that gender diversity can enhance sustainability practices. In addition, Birindelli, Iannuzzi, and Savioli (Citation2019) analyze the impact of women leaders on environmental performance in banks. The study provides evidence supporting a positive relationship between gender diversity in leadership positions and improved environmental performance, emphasizing the importance of women leaders in driving sustainability. Hence, this study proposes H4b as below.

H4b: Ceteris paribus, the higher the proportion of female board members, the greater the environmental performance.

2.6. Additional factors

Analyst coverage: Luo and Bhattacharya (Citation2009) indicate a positive association between analyst coverage and corporate environmental performance. The presence of more analysts can lead to greater pressure from institutional investors for better environmental performance, as analysts provide information to these investors. Firms with greater analyst coverage tend to have better corporate governance practices, which can also lead to better CEP. This is because good corporate governance practices can facilitate the adoption of environmentally responsible policies and practices.

Similarly, Albuquerque, Koskinen, and Zhang (Citation2019) show that firms with better corporate governance are more likely to adopt environmentally responsible practices and to have better environmental performance. A study by Marquis and Qian (Citation2014) finds that firms with greater analyst coverage are likely to have better social and environmental performance, as analysts tend to focus on firms’ social and environmental responsibility in addition to financial performance. Therefore, firms with more analyst coverage have a higher likelihood to perform better environmentally due to greater scrutiny, pressure from institutional investors, and better corporate governance practices.

Network sizes: larger companies are more likely to invest in environmental initiatives due to their larger resource base, greater public scrutiny, and the need to manage reputational risks. In addition, larger firms tend to have more resources available to invest in environmental performance improvement initiatives. Based on these, this study proposes H5 as below.

H5: Ceteris paribus, analyst coverage, and larger networking size have a positive impact on corporate environmental performance.

3. Data and methodology

3.1. Methodology

3.1.1. Models

This study employs the following empirical models to test the hypotheses. This study estimates ordinary least squares (OLS) regression as in EquationEquation (1)(1)

(1) for all hypotheses. Specifically, the association between environmental performance and CSR-linked compensation incentives (H1). H2 is related to the impact of the CSR committee on environmental performance, and H3 investigates the relationship between environmental scores and environmental Targets. H4 is related to Board composition and the investigation of other factors is in H5. This study expects the coefficients of the variables of interest to be positive, suggesting these factors have a positive impact on environmental performance. All regression models incorporate the year and industry fixed effects and cluster at the firm level. Variables and proxies are discussed in the following section.

(1)

(1) where CEP – corporate environmental performance is measured using the environmental score and emission score in the primary analysis. Factor represents a vector of the variable of interests that has a detrimental effect on CEP: CSR-linked compensation, CSR committee, disclosure, environmental Targets, independent director, female board member, analyst coverage, and network size. The X and Z are vectors of firm-level variables to control for additional financial (X) and board characteristics (Z) identified within the literature as influencing CEP. The FE represents the inclusion of year, industry-fixed effects. The specific variables included as controls are discussed in detail below. The model is run using OLS with standard errors clustered at the firm level. Based on H1 – H5, this study expects the coefficient on Factor to be positive (i.e. β1 < 0).

3.1.2. Endogeneity test: two stage least square

This study adopts the 2SLS (Two-Stage Least Squares) method to analyze the determinants of CEP aiming to eliminate endogeneity. Endogeneity occurs when there is a bidirectional relationship between the dependent variable (environmental performance) and the independent variables (i.e. CSR-linked compensation), and this can lead to biased estimates of the coefficients of the independent variables. The 2SLS approach involves using an instrumental variable (IV) to address endogeneity. In this study, the standard deviation of Board Age is employed as the IV for the variables of interest (i.e. CSR-linked compensation, committee, targets, etc.). The choice of Board Age standard deviation as an IV suggests an attempt to address endogeneity concerns by selecting a variable that is theoretically related to CSR but is unlikely to be directly correlated with the error term in the environmental performance equation. Likewise, the rationality of choosing board age standard deviation as an IV suggests that the age diversity or homogeneity of board members can affect CSR strategies and targets.

Further, this instrument captures the diversity of perspectives and experiences within the board. For instance, a more diverse board, in terms of age, tends to bring a wider range of views on CSR issues, which leads to more comprehensive and effective CSR strategies. Besides, older board members are more inclined to advocate for robust CSR governance mechanisms. Therefore, using this IV, the relationship between the dependent variables (CEP) and the independent variable (variable of interest) can be estimated without the influence of endogeneity. In this study, the strength of the instrument, as indicated by the weak instrument test (See Panel C), provides confidence in its ability to isolate the variation in CSR strategies and targets that is unrelated to other potential determinants of environmental performance.

First stage regression as specified in Equation (2):

(2)

(2) where AgeBoard is the standard deviation of board member age as the instrumental variable. The other variable explanations are the same as Equation (1). The model is run using the 2SLS-first stage with standard errors clustered at the firm level. Based on H1 – H5, this study expects the coefficient on AgeBoard to be significant (i.e. β1 < 0 or >0), meaning that the instrumental variable has a strong relationship with the endogenous variables.

Second stage regression as specified in Equation (3):

(3)

(3) where Factor(instrumented) represents a vector of the variable of interests that has a detrimental effect on CEP. Different from EquationEquation (1)

(1)

(1) , these variables are instrumented by AgeBoard (instrumental variable). The other variable explanations are the same as Equationequation (1)

(1)

(1) . The model is run using the 2SLS-second stage with standard errors clustered at the firm level. Based on H1 – H5, this study expects the coefficient on Factor to be positive (i.e. β1 < 0) as the baseline OLS regression.

3.1.3. Subsample test

This study adopts two subsample tests to further explore the relationship between variables in a subset of the data. The first investigation focuses on any difference in the determinate effect on the CEP pre- and post-GFC. Second, this study investigates whether there is any difference in environmentally sensitive industries. This allows this study to examine whether the relationship between the determinants and CEP is stronger for companies within a certain period, industries, and with certain characteristics. The subsample analysis on these subsets of data helps to find whether the relationship holds across all subgroups or whether there are variations in the strength of the relationship.

3.1.4. Alternative measures and other considerations

For further robust checks, this study adopts dummy variables that have been used in previous studies to confirm the generalization of the results. In the main regression, this study uses a score value instead of a dummy variable because a score value can provide more granular information about the level or degree of a variable being measured. A score value can reflect the magnitude, intensity, or extent of a phenomenon or behavior, while a dummy variable only indicates the presence or absence of a characteristic. For example, if a dummy variable is employed to indicate whether a company has a carbon reduction target, it will only provide information about whether the company has a target. However, if a score value is estimated to represent the company's carbon reduction target, it can provide information about the specific target that the company has set and the degree to which the company is achieving that target.

3.2. Variables and proxies

3.2.1. Proxies of environmental performance

i) Environmental score

Following the previous literature (i.e. Chouaibi, Rossi, and Zouari Citation2019), in this study, environmental score (EScore) is used as the proxy for corporate environmental performance (CEP) as it provides a comprehensive measure of a company's sustainability performance. Also, it provides a standardized and comparable measure of sustainability performance across companies, industries, and regions, facilitating cross-sectional and longitudinal analyses.

ii) Emission score

This study uses the emission score (Emission) as the second proxy for CEP because greenhouse gas emissions are one of the most widely used and well-understood measures of a company's environmental impact. Measuring a company's emissions can provide insight into its environmental performance, as it reflects its contribution to climate change and air pollution.

3.2.2. Key variables of interest

This study uses six key variables of interest as below. First, CSR-linked compensation incentives (Compensation) are rewards offered to employees for achieving sustainability goals set by the company to motivate employees to work towards socially responsible business practices, benefiting both the company and the environment. This variable captures the extent to which executive compensation is linked to CSR initiatives. This study posits that aligning executive incentives with CSR goals is likely to enhance environmental performance. Second, the CSR committee (Committee) is a group of individuals within a company responsible for developing and implementing socially responsible initiatives. A CSR committee can improve environmental performance by setting environmental goals, implementing sustainable practices, and monitoring progress toward achieving those goals, ensuring that the company operates in an environmentally responsible manner. Third, CSR disclosure (Disclosure) refers to the process of publicly reporting a company's social, environmental, and ethical performance. This helps stakeholders evaluate a company's commitment to CSR and hold it accountable for its actions. CSR disclosure can improve environmental performance by increasing transparency, promoting accountability, and encouraging companies to adopt sustainable practices. Likewise, firms with robust disclosure policies tend to exhibit a higher level of commitment to sustainability. This study expects a positive relationship between disclosure policies and CEP.

Environmental Targets are specific goals set by organizations to reduce their environmental impact. These targets may include reducing emissions, conserving resources, improving waste management, or adopting sustainable practices to promote environmental stewardship. In addition, having measurable goals related to environmental performance is associated with improved outcomes. This study anticipates a positive association between the presence of environmental targets and CEP. Fifth, the independent director (Independent director) is a member of a company's board of directors who is not affiliated with the company, its management, or its shareholders, providing an unbiased perspective and oversight. Lastly, the Female board member (Female Board) serves on a company's board of directors, contributing to the diversity of perspectives, and promoting gender equality and representation in corporate leadership. This study argues that diverse and independent boards are more likely to consider a range of perspectives, leading to improved corporate decision-making, including decisions related to environmental performance.

3.2.3. Instrumental variable (IV)

As discussed above, an appropriate instrument should be relevant, exogenous, and exclusive. In this case, the standard deviation of board age satisfies these criteria, as it is exogenous to the environmental performance and relevant for CSR strategies and targets. Prior studies have also used board age (Age Board) as an instrument variable in examining the relationship between corporate governance and environmental performance (Tantalo and Priem Citation2016). Cheng, Ioannou, and Serafeim (Citation2019) find that the standard deviation of board age was a strong and significant instrument for CSR disclosure. Similarly, Eccles, Ioannou, and Serafeim (Citation2014) use the standard deviation of board age as an instrument for CSR-linked compensation and find a positive impact on environmental performance. Therefore, the standard deviation of board age is a suitable and reliable instrument for examining the impact of CSR-related practices on CEP.

3.2.4. Control variables

Following the previous literature (i.e. Dyck et al. Citation2019; McGuinness, Vieito, and Wang Citation2017; Nofsinger, Sulaeman, and Varma Citation2019; Waddock and Graves Citation1997; Chouaibi, Rossi, and Zouari Citation2019), this study controls several firm financial and board character variables. This allows the study to isolate the effect of a specific variable of interest on environmental performance while holding other factors constant and helps to ensure that any observed relationship between the variables is not simply due to chance or the influence of other factors.

Financials: Firm size is controlled as it can influence a company's ability to implement sustainable practices and policies, as larger firms may have greater resources to invest in sustainability initiatives (Dyck et al. Citation2019). Leverage and cash holding can impact a company's ability to finance and invest in sustainable projects, and firms with higher levels of leverage may face greater pressure from stakeholders to manage ESG risks (Jensen Citation2010). A company with a high growth rate may face more pressure to prioritize short-term financial performance over long-term ESG goals. Firms with higher levels of tangible assets may face greater ESG risks related to resource depletion or pollution. Finally, ROA is included because firms that enjoy higher profitability tend to have greater slack resources, which often leads to a greater likelihood of making investments in environmental initiatives (Waddock and Graves Citation1997).

Board characteristic: Following the previous literature (McGuinness, Vieito, and Wang Citation2017), this study controls for several board characteristic variables. Boards play a crucial role in shaping a company's environmental strategy. Board size and CEO dualism are important control variables to be considered when examining the determinants of corporate environmental performance. Smaller boards may be more effective in implementing environmental policies, while CEO dualism (when the CEO also serves as the board chair) may hinder accountability and oversight. These variables can provide valuable insights into the role of corporate governance in promoting sustainability and responsible environmental practices.

Year-fixed and Industry-fixed effects: ESG performance may be influenced by factors such as changes in regulation, technological advancements, or shifts in societal values. Further, different industries have different levels of ESG risk or opportunity, and companies within the same industry may face similar challenges or opportunities related to ESG issues. Therefore, incorporating the year-fixed and industry-fixed effects allows this study to examine the relationship between the variables of interest and ESG performance while accounting for the effects of industry.

The Cluster at the firm level: The environmental performance of companies over multiple years may have multiple observations for each company. This study controls for clustered data at the firm level, which accounts for any within-firm correlation in the data. In other words, it ensures that the statistical analysis accurately reflects the fact that multiple observations are made on the same firms and that these observations may be correlated. This helps to improve the accuracy of standard errors and hypothesis tests.

3.3. Sample selection

To conduct the examination, this study constructs a comprehensive dataset that includes S&P 500 firm-level observations over the period 2001–2022 across 24 industries of 11 sectors (GIC standard). The dependent variables environmental scores and emission scores, and other variables of interest such as CSR-linked compensation data, and environmental targets are obtained from the Refinitive Eikon database. This study collects board-relevant data such as board size, number of independent directors, CEO duality, female board members, and board network from the BoardEx database. The financial controls are extracted from WRDS Compust North America. Lastly, the ESG data, board-relevant data, and financial controls are combined to generate a preliminary sample of 11,032 U.S. firm-level observations.

This study focuses on S&P 500 companies for the following reasons. Firstly, the S&P 500 is a widely recognized stock market index that includes 500 large-cap companies in the United States. These companies collectively represent a significant portion of the U.S. economy, and their environmental performance can have significant impacts on the environment and society. Secondly, many investors use the S&P 500 as a benchmark for investment performance. By analyzing the CEP of S&P 500 companies, investors can better understand the environmental risks and opportunities associated with their investments and make more informed investment decisions. The environmental performance of S&P 500 companies has implications for promoting sustainability, mitigating environmental risks, and making informed investment and policy decisions.

4. Empirical results

4.1. Descriptive statistics

Panel A presents descriptive statistics for the primary variables. These variables are important for understanding the extent to which firms are engaging in socially and environmentally responsible practices, as well as their overall level of sustainability.

Table 1. Descriptive statistics of key variables.

The mean value for the environmental score is 42.65, with a standard deviation of 29.49. Similar results are presented for the emission score and ESG score. The first set of variables relates to CSR, results suggest that firms vary widely in their level of engagement with CSR practices, with some firms demonstrating a high level of commitment and others demonstrating very little. The next set of variables relates to environmental targets. The mean values for these variables range from 12.92 to 44.65, with standard deviations ranging from 32.20 to 41.24. Again, this suggests that there is significant variation across firms in terms of their environmental performance, with some firms demonstrating a high level of sustainability and others lagging. As revealed, the pattern is relatively similar for CSR factors and environmental targets.

Panel B shows the firm-level financial and board character controls. The sample size for all the variables is over 9000. The mean value for firm size is 9.45 with a standard deviation of 1.68, indicating that the sample firms are of similar sizes and financial standing. For ROA, the mean is 0.10 with a standard deviation of 0.10, and the values range from −0.05 to 0.26. The minimum and maximum cash holding values in the sample are 0.01 and 0.29, respectively. This implies that, on average, the sample firms have a moderate level of cash reserves and are moderately leveraged. The mean growth rate is 8.69, which suggests that the firms in the sample are experiencing some growth, albeit not at a high rate.

Panel C reports the mean values of key variables by 24 GIC industries. The mean values of these variables vary across industries. There are noticeable variations in the mean values of the variables across industry sectors. For instance, the automobile industry has the highest mean EnvtScore and Emission, while the real estate industry has the lowest. The household and personal industry has the highest mean ESGScore, Compensation, Committee, Disclosure, Strategy, TargetsE, IndepDirect, and FemaleBoard, while the retailing industry has the lowest. Finally, the transportation industry has the highest frequency, while the telecommunication industry has the lowest.

Panel A presents the Pearson correlation matrix of key variables.Footnote2 The results reveal a significant correlation between the variables of interest and the dependent variables, namely the Environmental score, emission score, and ESG score. These correlations surpass the 0.7 threshold, which aligns with the study's anticipated goal of identifying a strong positive association among these variables. When assessing the correlations among the variables of interest (Compensation, Committee, Disclosure, Target, etc.), most fall within the range of 0.2 to 0.4, indicating a relatively low level of correlation and the absence of multicollinearity concerns.

Table 2. Correlation matrix and multicollinearity test.

In Panel B, the Variance Inflation Factor (VIF) test was performed to assess multicollinearity among the independent variables.Footnote3 In this study, VIF values range from 2 to 4 (18 out of 20 variables), indicating very low levels of multicollinearity. Consequently, all variables have VIF values below 10, suggesting the absence of multicollinearity issues. The overall findings from both the Pearson correlation matrix and VIF test suggest that there is no multicollinearity issue within the scope of this study. The proxies of the determinants have a significant positive impact on the CEP and there is no multicollinearity issue between the variables of interest.

4.2. Regression analysis

reports the results of the OLS regression analysis examining the relationship between the CSR factors and the measures of CEP. The results from Models 1 to 5 indicate that CSR-linked executive compensation incentives have a significant positive effect on both environmental and emission scores (coefficient = 0.167 and 0.081). This implies that firms are more likely to improve their environmental performance when their executives’ compensation is linked to CSR activities. Similarly, in Models 2 and 6, the existence of a CSR committee has a significant positive impact on both measures of CEP. Firms with a CSR committee in place are more likely to adopt green practices. In addition, CSR disclosure is also positively associated with both environmental and emission scores. Finally, CSR strategy has a significant positive effect on both environmental and emission scores. The results suggest that firms need to consider not only financial performance but also environmental performance.

Table 3. Compensation, committee, disclosure, and CEP.

The results reported in suggest that CSR targets have a positive and significant effect on corporate environmental performance (CEP), as measured by the environmental score and emission score. The positive coefficients observed for Emission targets, Energy targets, Water targets, and Diversity targets across both environmental and emission scores are highly consistent with the literature. Firms that adopt water conservation practices have better environmental performance (Sutantoputra, Lindorff, and Johnson Citation2012). Particularly, it is observed that larger firms tend to have more resources and capabilities, which allows them to invest in and implement environmentally friendly practices. In addition, the positive coefficients for ROA in several models suggest that firms with higher profitability exhibit better environmental performance. Besides, firms with higher cash reserves have the financial flexibility to invest in environmentally sustainable practices. The results also indicate that rapidly growing firms may face challenges in simultaneously managing growth and implementing sustainability initiatives. Furthermore, larger boards can bring diverse perspectives and expertise, enhancing the governance mechanisms that drive sustainability.

Table 4. CSR Targets and Corporate Environmental Performance (CEP).

presents that independent directors and female board members have a positive impact on corporate environmental performance. The results suggest that having independent directors and female board members on the board can help firms set and achieve CSR targets related to environmental performance. Gender diversity on boards is positively associated with innovative output, as well as with better financial performance. These findings are consistent with the prior literature that the presence of independent directors and female board members is associated with enhanced corporate social and environmental responsibility. Therefore, independent directors bring diverse perspectives and stronger oversight, contributing to more sustainable business practices. Likewise, female board members have been linked to a greater focus on environmental and social issues. The positive relationships observed in the results contribute to the growing body of literature emphasizing the role of board composition in promoting corporate environmental performance.

Table 5. Independent director, female board member, and CEP.

The results from Panel A show that CSR practices have a significant positive effect on CEP. These findings are consistent with previous studies on CSR and environmental performance (Kolk and Pinkse Citation2008; Jizi et al. Citation2014). Overall, the findings suggest that implementing CSR practices can have a positive impact on CEP, which can lead to better financial performance and corporate reputation. Therefore, firms should consider adopting these practices to improve their environmental performance and enhance their competitiveness. These results reinforce the existing understanding that organizations with robust CSR practices, diverse boards, and a focus on environmental strategy tend to exhibit superior environmental performance. Additionally, the positive impact of independent directors and female board members on CEP supports the literature's argument that board diversity contributes to sustainable business practices.

Table 6. Overall effect and other determinants of CEF.

Panel B also reports significant positive relationships between analyst coverage and networking size with CEP. Greater analyst coverage and networking size are associated with higher environmental and emission scores, which are consistent with previous research that highlights the importance of external stakeholders in shaping corporate environmental practices, including analysts and network size (Hoepner, Oikonomou, and Scholtens Citation2016; Christmann and Taylor Citation2006).

4.3. Robustness test

4.3.1. 2SLS endogeneity test

Panel A reports the first stage results of 2SLS regression. The instrument variable, board age standard deviation, has a significant negative association with all factor variables. Age difference means different experiences and thoughts, and greater communication barriers, which hinder the implementation of CSR strategies (Friedman and Miles Citation2002). This finding is consistent with the argument that older board members are not sensitive to social and environmental issues and are less likely to prioritize CSR concerns (Ho and Taylor Citation2007).

Table 7. Endogeneity Test: 2SLS regression (Instrument variable = board age standard deviation).

Panel B presents results for the second stage of 2SLS analysis. The results indicate that there is a positive relationship between the CSR-related determinants (instrumented) and CEP, which is consistent with the hypothesis and prior research. Specifically, the positive coefficients for CSR-related compensation, CSR committee, CSR disclosure, targets, independent directors, and female board members in the environmental score align with theoretical expectations. These results suggest that CSR practices positively influence corporate environmental performance. Moreover, this study provides further support for the positive impact of CSR-related determinants on CEP. Overall, the results suggest that firms should consider implementing CSR practices to improve environmental performance.

In Panel C, the post-estimation tests for the 2SLS analysis reveal a robust instrumental variable (IV) in the form of board age standard deviation. The weak instrument test demonstrates its strength across various dependent variables related to corporate environmental performance, with consistently low p-values and higher values in Wald F statistics. In addition, the overidentification tests indicate no issues with an excess of instruments, while under-identification tests reject the null hypothesis, confirming the relevance of the instruments used (higher LM statistics values and p-value = 0). Importantly, the Durbin chi2 and Wu-Hausman F tests suggest that the endogeneity problem has been addressed using the 2SLS regression method.

4.3.2. Sub-sample tests

Panel A conducts a sub-sample test to analyze the effect of determinants of corporate environmental performance (CEP) pre- and post-the-global financial crisis (GFC). It allows this study to assess whether the GFC had a significant impact on the studied variables, providing valuable insights into the temporal dynamics of the phenomenon under investigation and its potential implications for policy and decision-making. Additionally, this approach tends to capture potential shifts or changes in the relationship, which can contribute to a more comprehensive understanding of the topic.

Table 8. Sub-sample test.

The results suggest that the GFC had a significant impact on the relationship between some determinants and CEP. These findings are consistent with previous studies that suggest the GFC had a significant impact on the relationship between corporate social responsibility (CSR) and financial performance. For instance, Du, Bhattacharya, and Sen (Citation2015) finds that the GFC had a significant negative impact on the relationship between CSR and financial performance in the banking industry. Overall, the results suggest that the impact of determinants on CEP may change over time, particularly during periods of economic crisis. Therefore, companies need to adapt their CSR strategies to changing economic conditions to maintain their environmental performance.

In Panel B, the results of this subsample analysis are consistent with prior research that environmental performance is positively related to CSR-related practices in environmentally sensitive industries. Besides, CSR-linked executive compensation incentives, CSR committees, and CSR disclosure are important factors in improving environmental performance in these industries. In addition, gender diversity on boards is positively related to environmental performance in environmentally sensitive industries.

4.3.3. Alternative measures and other considerations

Panel A uses Dummy variables as the alternative measures of the independent variables (score values are used in the baseline Models). The sample is divided into two groups Model 2 (firms with CSR-linked compensation incentives) and Model 3 (without). Consistent results have been found across different Models. The results indicate that the presence of CSR-linked executive compensation incentives is significantly associated with higher environmental scores, consistent with the agency theory perspective that links executive compensation to environmental performance. The presence of a CSR committee and CSR reporting is also positively related to environmental performance, indicating that corporate governance and disclosure practices can enhance the firm's environmental performance (Darnall et al. Citation2010). Firms should consider implementing various CSR practices and disclosing information to improve their environmental performance and satisfy stakeholders’ expectations.

Table 9. Alternative measures and other considerations.

Panel B adopts the ESG score to test the validity of the results. Since the environmental score is the constitution of the ESG score. The findings should be generalized to the ESG score. Theoretically, great environmental performance also improves the overall ESG score. In Models 1 and 2, the results are aligned with the baseline regression and support the hypothesis. In Panel B Model 4, consistent results have been found that firms with CSR-linked compensation incentives are more likely to engage in environmental innovation.

4.4. Discussion

Several corporate characteristics play a crucial role in influencing Corporate Environmental Performance (CEP). Notably, CSR-linked compensation, the presence of a CSR committee, disclosure policies, environmental targets, inclusion of independent directors, and female board members all exhibit positive associations with CEP. The magnitudes of these coefficients highlight the strength and direction of these relationships. For instance, a positive coefficient for CSR-linked compensation suggests that firms tying executive compensation to CSR initiatives experience higher CEP. This reinforces the idea that economic incentives are effective in driving environmental responsibility.

The findings are consistent with the existing literature and theoretical expectations. Numerous studies have emphasized the positive impact of CSR-related practices on environmental performance. The positive association between CSR-linked compensation, CSR committee presence, disclosure policies, and environmental targets with CEP aligns with the broader literature that advocates for the importance of corporate governance and strategic initiatives in fostering sustainability. Moreover, the positive relationships observed with the inclusion of independent directors, female board members, analyst coverage, and network size echo the literature on the role of diverse and informed governance structures in promoting environmentally responsible behavior. These results extend the theoretical foundations that posit a connection between corporate characteristics and sustainable business practices.

5. Conclusion

This study examines the determinants of corporate environmental performance by investigating a variety group of factors: ranging from CSR-linked compensation incentives, CSR committees and strategies, environmental targets, and board structure. Following the literature, this study posits that great environmental performance interests the alignment of management and shareholders. For corporations that implement CSR-linked compensation incentives, the executives are likely to perform better environmentally. In addition to this, establishing CSR committees and strategy, environmental Targets, and increased involvement by shareholders manifest in the relative benefits of reduced information asymmetry, more efficient financing and investing decisions, and enhanced monitoring, and thus ultimately better environmental performance.

Companies can benefit financially from better environmental performance. For example, investments in energy efficiency and renewable energy can lead to cost savings over the long term. Additionally, companies with better environmental performance may have an advantage in attracting socially responsible investors and customers, which can also benefit the company financially. The interest alignment of management and shareholders concerning environmental performance can help drive investments and decision-making that prioritize environmental considerations. This can benefit the company financially while also contributing to the achievement of environmental goals. Moreover, corporates seeking to enhance their environmental performance should consider adopting CSR-linked compensation, establishing CSR committees, implementing robust disclosure policies, and setting explicit environmental targets. Additionally, the results suggest that diversifying board composition and increasing analyst coverage can contribute positively to CEP.

This study offers important practical implications for policymakers, investors, organizations, and other stakeholders. Investors are increasingly concerned about corporate ESG performance, which might pressure organizations to strive for their environmental goals. In addition, the findings can help policymakers develop effective policy measures that promote environmental sustainability and ensure compliance by businesses (Kolk and Pinkse Citation2008). Organizations can also use this information to benchmark their environmental performance against their peers identify areas for improvement and develop more effective strategies and management practices that help to improve their sustainability performance. Finally, other stakeholders can also advocate for changes in corporate behavior that contribute to a more sustainable future (Lozano and Huisingh Citation2011).

In summary, this study holds significant economic meaning and contributes to the understanding of corporate sustainability. The results offer insights into the economic benefits of environmental responsibility and promote long-term profitability. Furthermore, the study's findings can inform businesses on how to develop tailored environmental management strategies, ultimately fostering sustainable practices that align with financial success and stakeholder expectations, making it a valuable resource for companies striving for both economic and environmental sustainability. In aggregate, the factors that affect CEP are important for promoting sustainable development, meeting stakeholder expectations, developing effective environmental policies, attracting investors, achieving long-term profitability, reducing environmental risks and impacts, and crafting customized environmental management strategies. For future research, the study provides a foundation for further exploration of the nuanced relationships between specific corporate characteristics and environmental performance. It also opens avenues for investigating the effectiveness of different governance mechanisms in driving sustainable practices.

Acknowledgements

The author would like to thank the anonymous reviewers for taking the necessary time and effort to review the manuscript. I sincerely appreciate all your valuable comments and suggestions, which helped us in improving the quality of the manuscript.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 see Figure A1 Sustainable funds and assets under management 2010–2021.

2 In the realm of correlation analysis, a general rule of thumb is as follows: a correlation coefficient exceeding 0.7 typically indicates a strong correlation, while values falling within the range of 0.3 to 0.7 are indicative of a moderate correlation. Conversely, correlations below 0.3 are considered weak.

3 A higher VIF indicates a greater likelihood of multicollinearity, with values exceeding 10 signifying significant multicollinearity. Multicollinearity is not a concern when the value is below 10.

References

- Adams, R.B., and D. Ferreira. 2009. Women in the boardroom and their impact on governance and performance. Journal of Financial Economics 94, no. 2: 291–309.

- Al-Shaer, H., K. Albitar, and J. Liu. 2023. CEO power and CSR-linked compensation for corporate environmental responsibility: UK evidence. Review of Quantitative Finance and Accounting 60: 1025–63.

- Al-Tuwaijri, S.A., T.E. Christensen, and K.E. Hughes Li. 2004. The relations among environmental disclosure, environmental performance, and economic performance: A simultaneous equations approach. Accounting, Organizations and Society 29: 447–71.

- Albuquerque, R., Y. Koskinen, and C. Zhang. 2019. Corporate social responsibility and firm risk: Theory and empirical evidence. Management Science 65, no. 10: 4451–69.

- Bai, C., J. Sarkis, and Y. Dou. 2016. Corporate sustainability development in China: Review and analysis. Journal of Cleaner Production 127: 1–17.

- Baraibar-Diez, E., and M.D. Odriozola. 2019. Csr Committees and Their Effect on ESG Performance in UK, France, Germany, and Spain. Sustainability 11, no. 18: 5077.

- Ben-Amar, W., M. Chang, and P. McIlkenny. 2017. Board gender diversity and corporate response to sustainability initiatives: Evidence from the carbon disclosure project. Journal of Business 142, no. 2: 369–83.

- Berrone, P., and L.R. Gomez-Mejia. 2009. Environmental performance and executive compensation: an integrated agency-institutional perspective. Academy of Management Journal 52, no. 1: 103–26.

- Bhagat, S., and B. Bolton. 2008. Corporate governance and firm performance. Journal of Corporate Finance 14, no. 3: 257–73.

- Birindelli, G., A.P. Iannuzzi, and M. Savioli. 2019. The impact of women leaders on environmental performance: Evidence on gender diversity in banks. Corporate Social Responsibility and Environmental Management 26, no. 6: 1485–99.

- Byron, K., and C. Post. 2016. Women on boards of directors and corporate social performance. A meta-analysis. Corporate Governance: An International Review 24: 428–42.

- Cahan, S.F., C. De Villiers, D.C. Jeter, V. Naiker, and C.J. Van Staden. 2016. Are CSR disclosures value relevant? Cross-country evidence. European Accounting Review 25, no. 3: 579–611.

- Callan, S.J., and J.M. Thomas. 2014. Relating CEO compensation to social performance and financial performance: Does the measure of compensation matter? Corporate Social Responsibility and Environmental Management 21, no. 4: 202–27.

- Cheng, B., I. Ioannou, and G. Serafeim. 2019. Corporate social responsibility and access to finance. Strategic Management Journal 40, no. 5: 781–802.

- Chouaibi, Y., M. Rossi, and G. Zouari. 2019. The effect of corporate social responsibility and the executive compensation on implicit cost of equity: Evidence from French ESG Data. Sustainability 11, no. 23: 6707.

- Christmann, P., and G. Taylor. 2006. Firm self-regulation through international certifiable standards: Determinants of symbolic versus substantive implementation. Journal of International Business Studies 37, no. 6: 863–78.

- Clarkson, P., Y. Li, G. Richardson, and F. Vasvari. 2008. Revisiting the relation between environmental performance and environmental disclosure: An empirical analysis. Accounting, Organizations and Society 33, no. 4-5: 303–27.

- Cordeiro, J.J., and J. Sarkis. 2008. Does explicit contracting effectively link CEO compensation to environmental performance? Business Strategy Environment 17, no. 5: 304–317.

- Cormier, D., and M. Magnan. 1999. Corporate environmental disclosure strategies: Determinants, costs and benefits. Journal of Accounting, Auditing & Finance 14, no. 4: 429–51.

- Darnall, N., I. Henriques, and P. Sadorsky. 2010. Adopting proactive environmental strategy: The influence of stakeholders and firm size.Journal of Management Studies 47: 1072–1094.

- Deckop, J.R., K.K. Merriman, and S. Gupta. 2006. The effects of CEO pay structure on corporate social performance. Journal of Management 32, no. 3: 329–42.

- Derchi, G.B., L. Zoni, and A. Dossi. 2021. Corporate social responsibility performance, incentives, and learning effects. Journal of Business Ethics 173: 617–41.

- Du, S., C.B. Bhattacharya, and S. Sen. 2015. Corporate social responsibility, multi-faceted job-products, and employee outcomes. Journal of Business Ethics 131: 319–35.

- Dyck, A., K.V. Lins, L. Roth, and H.F. Wagner. 2019. Do institutional investors drive corporate social responsibility? International evidence. Journal of Financial Economics 131, no. 3: 693–714.

- Eccles, R.G., I. Ioannou, and G. Serafeim. 2014. The impact of corporate sustainability on organizational processes and performance. Management Science 60, no. 11: 2835–57.

- Eisenhardt, K.M. 1989. Agency theory: An assessment and review. Academy of Management Review 14, no. 1: 57–74.

- Elmaghrabi, M.E. 2021. CSR committee attributes and CSR performance: UK evidence. Corporate Governance 21, no. 5: 892–919.

- Friedman, R., and S. Miles. 2002. Developing stakeholder theory. Journal of Management Studies 39, no. 1: 1–21.

- Gond, J.P., A. El Akremi, V. Swaen, and N. Babu. 2017. The psychological microfoundations of corporate social responsibility: A person-centric systematic review. Journal of Organizational Behavior 38, no. 2: 225–46.

- Haque, F. 2017. The effects of board characteristics and sustainable compensation policy on carbon performance of UK firms. British Accounting Review 49, no. 3: 347–64.

- Harjoto, M., I. Laksmana, and R. Lee. 2015. Board diversity and corporate social responsibility. Journal of Business Ethics 132, no. 4: 641–60.

- Ho, L., and M. Taylor. 2007. An empirical analysis of triple bottom-line reporting and its determinants: Evidence from the United States and Japan. Journal of International Financial Management and Accounting 18, no. 2: 123–50.

- Hoepner, A.G., I. Oikonomou, and B. Scholtens. 2016. The effects of corporate and country sustainability characteristics on the cost of debt: An international investigation. Journal of Business Finance and Accounting 43, no. 1-2: 158–90.

- Hong, B., Z. Li, and D. Minor. 2016. Corporate governance and executive compensation for corporate social responsibility. Journal of Business Ethics 136, no. 1: 199–213.

- Jensen, M.C. 2010. Value maximization, stakeholder theory, and the corporate objective function. Journal of Applied Corporate Finance 22 (1): 32–42.

- Jizi, M.I., A. Salama, R. Dixon, and R. Stratling. 2014. Corporate governance and corporate social responsibility disclosure: Evidence from the US banking sector. Journal of Business Ethics 125, no. 4: 601–15.

- Jo, H., and M.A. Harjoto. 2011. Corporate governance and firm value: The impact of corporate social responsibility. Journal of Business Ethics 103, no. 3: 351–83.

- John, K., L. Litov, and B. Yeung. 2008. Corporate governance and risk-taking. The journal of finance 63, no. 4: 1679–728.

- Kolk, A., and J. Pinkse. 2008. A perspective on multinational enterprises and climate change: Learning from “an inconvenient truth"? Journal of International Business Studies 39, no. 8: 1359–78.

- Liu, L. 2023. Green innovation, firm performance, and risk mitigation: evidence from the USA. Environment, Development and Sustainability, 1–22. https://doi.org/10.1007/s10668-023-03632-z.

- Lozano, R., and D. Huisingh. 2011. Inter-linking issues and dimensions in sustainability reporting. Journal of Cleaner Production 19, no. 2–3: 99–107.

- Luo, X., and C.B. Bhattacharya. 2009. The debate over doing good: Corporate social performance, strategic marketing levers, and firm-idiosyncratic risk.Journal of Marketing 73 (6): 198–213.

- Maas, K. 2018. Do corporate social performance targets in executive compensation contribute to corporate social performance? Journal of Business Ethics 148, no. 3: 573–85.

- Marquis, C., and C. Qian. 2014. Corporate social responsibility reporting in China: Symbol or substance? Organization Science 25, no. 1: 127–48.

- McGuinness, P.B., J.P. Vieito, and M. Wang. 2017. The role of board gender and foreign ownership in the CSR performance of Chinese listed firms. Journal of Corporate Finance (Amsterdam, Netherlands) 42: 75–99.

- Nofsinger, J.R., J. Sulaeman, and A. Varma. 2019. Institutional investors and corporate social responsibility. Journal of Corporate Finance 58: 700–25.

- Orlitzky, M., F.L. Schmidt, and S.L. Rynes. 2003. Corporate social and financial performance: A meta-analysis. Organization Studies 24, no. 3: 403–41.

- Radu, C., and N. Smaili. 2022. Alignment versus monitoring: An examination of the effect of the CSR committee and CSR-linked executive compensation on CSR performance. Journal of Business Ethics, Springer 180 (1): 145–63.

- Sutantoputra, A.W., M. Lindorff, and E.P. Johnson. 2012. The relationship between environmental performance and environmental disclosure. Australasian Journal of Environmental Management 19, no. 1: 51–65.

- Tantalo, C., and R.L. Priem. 2016. Value creation through stakeholder synergy. Strategic Management Journal 37, no. 2: 314–29.

- Waddock, S.A., and S.B. Graves. 1997. The corporate social performance–financial performance link. Strategic Management Journal 18, no. 4: 303–19.

- Wang, H., L. Tong, R. Takeuchi, and G. George. 2015. Corporate social responsibility: An overview and new research directions. Academy of Management Journal 58, no. 2: 557–76.

- Westphal, J.D., and L.P. Milton. 2000. How experience and network ties affect the influence of demographic minorities on corporate boards.Administrative Science Quarterly 45 (2): 366–398.

- Williamson, O.E. 1988. Corporate finance and corporate governance. The Journal of Finance 43, no. 3: 567–91.

Appendices

Appendix 2.1. Figures

Figure A1. Sustainable funds and assets under management 2010–2021. Source: UNCTAD, based on Morningstar data

Figure A2. Sustainable investment in the United States 1995–2022. Source: US SIF Foundation. Assets under management in 2022 represent US SIF’s new modified methodology.

Figure A3. Top ESG Criteria for Money Managers in 2020. Source: US SIF Foundation