ABSTRACT

In the Credit Lyonnais case, the CJEU concluded that the proportion of input VAT deduction on mixed-use goods and services is to be calculated by taking into account the output supplies carried out by establishments located within the same territory only. This interpretation of the VAT Directive leads to a different treatment of domestic and foreign branches and is, hence, questionable in the light of the freedom of establishment. This paper analyses the impact of the fundamental freedoms on VAT law in general and possible reasons behind the interpretation chosen by the Court in the Credit Lyonnais case more specifically.

KEYWORDS:

1. About this paper

When enacting secondary law, the EU legislature is bound by EU primary law including, amongst other provisions, the fundamental freedoms. The same holds true for the CJEU when interpreting secondary law. Nevertheless, in the Credit Lyonnais case the CJEU ruled, via an interpretation of Articles 173 et seq of the VAT Directive,Footnote1 that the proportion of input VAT to be allowed as a deduction on mixed-use goods and services is to be calculated on a territorial basis. This interpretation of the VAT Directive leads to different treatment of domestic and foreign branches and is, hence, questionable in the light of the freedom of establishment. As the Court accepts this discriminatory effect—without discussing it in further detail—the Credit Lyonnais case reveals its somewhat lenient attitude as regards the implications of the freedoms in the area of VAT. The aim of this paper is to assess the potential conflict between the interpretation chosen in the Credit Lyonnais case and the freedom of establishment and the legitimacy of this interpretation in the light of the ‘rule of reason’ developed by the CJEU. As the CJEU jurisprudence on the compatibility of VAT law measures with the fundamental freedoms is rather limited, a major part of the paper addresses whether and to what extent the extensive jurisprudence on direct tax can be transposed to VAT law and to the specific case at hand.

The paper will start with a summary of the judgment in the Credit Lyonnais case including the background to the case and further implications arising from the judgment (Section 2). Sections 3–4 will be dedicated to a thorough analysis of the fundamental freedoms aspect of the case. When analysing why the CJEU accepts the potentially discriminatory treatment as being in line with the goals of the internal market, several elements have to be considered: First and foremost, one might question whether the different level of harmonisation in VAT law, as compared to direct tax law, is of relevance when evaluating the effects of the fundamental freedoms (Section 3). Second, one has to keep in mind that not every difference in treatment between a domestic and a cross-border situation is prohibited by the fundamental freedoms. In this respect, one might question: whether the territorial approach leads to a restriction on the freedom of establishment at all (Section 4.2); whether domestic and foreign branches are objectively comparable when it comes to input VAT deduction (Section 4.3); and whether there might be a justification for the different treatment which is pursued and implemented by the VAT Directive in a proportional and coherent manner (Section 4.4). In the last section, a conclusion on the main findings is presented (Section 5).

2. The Credit Lyonnais case

2.1. Input VAT deduction

Deduction of input VAT is a core principle of the system of VAT in the European Union which aims to ensure complete neutrality of taxation of all economic activities.Footnote2 Based on the general rules of the EU VAT Directive, a taxable person is entitled to deduct input VAT if the goods or services to which that input VAT relates are used for the purposes of taxed transactions carried out either in the same Member State (Article 168) or in another state. The latter scenario is subject to the additional requirement that the output transactions would be eligible for deduction had they occurred in the territory of the state where the input VAT is due (Article 169(a)). The calculation of the deductible input VAT in the case of goods and services used for both taxed transactions and exempt transactions (‘mixed-use’ goods or services) is regulated in Article 173 of the VAT Directive, according to which ‘only such proportion of the VAT as is attributable to the [taxed] transactions shall be deductible’. This deductible proportion (often also referred to as the ‘recovery ratio’ or ‘pro rata deduction’) should be calculated ‘for all the transactions carried out by the taxable person’. Article 174 of the VAT Directive clarifies the method to be used for this pro rata calculation: the numerator is the ‘total amount … of turnover per year attributable to transactions in respect of which VAT is deductible’. The denominator consists of the ‘total amount … of turnover per year’ including transactions eligible for deduction and those not eligible for deduction. Article 173(2) of the VAT Directive grants the Member States the option to introduce a number of derogations to the pro rata calculation; amongst others the Member States may ask for a separate recovery ratio for different business sectors or they may disregard insignificant amounts of input VAT. It should be noted that according to settled CJEU case law out-of-scope transactions (that is non-economic activities) are not to be included in the pro rata calculation based on Article 174.Footnote3 Hence, when using the term ‘pro rata calculation’ or ‘recovery ratio’ in this paper, this refers to the apportionment of input VAT between taxed and exempt transactions only.

The legal basis for input VAT deduction set out in Articles 167 et seq of the VAT Directive does not explicitly deal with whether the recovery ratio for mixed-use goods and services is to be calculated on a world-wide or a territorial basis. Instead, the wording refers generally to the ‘taxable person’, ‘all the transactions’ (Article 173) and to the ‘total amount … of turnover’ (Article 174). The term ‘fixed establishment’ is not used. In relation to output VAT, the Court ruled in the FCE Bank case, handed down in 2006, that a fixed establishment is not a separate taxable person and there cannot therefore be any taxable transactions between the head office and other establishments of the same legal entity (single-entity approach), even in a cross-border situation.Footnote4 Against this background, scholars have argued that a global recovery ratio is more appropriate.Footnote5 However, the practice of the Member States in this area has been diverse for many years.Footnote6 In 2013, a French court asked the CJEU whether the output supplies of fixed establishments located in other Member States or in third countries have to be taken into account when calculating the recovery ratio for the domestic head office according to Articles 17 and 19 of the Sixth Directive (now Articles 173 and 174 of the VAT Directive). This case is known as the Credit Lyonnais case and was decided by the Court on 12 September 2013.

2.2. CJEU: territorial approach

Advocate General Cruz Villalón considered that it should be up to the individual Member States to decide whether or not to permit companies to include the output supplies of foreign branches in the recovery ratio calculation of a head office.Footnote7 The Court did not follow this proposal. It concluded that Member States are prohibited from allowing companies to take into account the output supplies of foreign fixed establishments when calculating the recovery ratio of their domestic head office. The CJEU based this result on three arguments: First and foremost, it pointed out that the system for input VAT deduction falls within ‘the scope of the national VAT legislation to which an activity or transaction must be linked for tax purposes.’Footnote8 This assumption is supported by (i) the several options available for the Member States in Article 17(5)(3) of the Sixth VAT Directive (now Article 173(2) of the VAT Directive), and (ii) the system laid down in the Eighth Council Directive 79/1072/EEC and the Thirteenth Council Directive 86/560/EEC, both making the method of repayment of VAT, by deduction or by refund, conditional upon the existence of a fixed establishment.Footnote9 In the light of this systematic background, taking into account the turnover of foreign branches would ‘seriously [jeopardise] the rational allocation of the spheres of application of national legislation in VAT matters’.Footnote10 Second, including the output supplies of a foreign branch would, according to the Court, not guarantee better observance of the principle of neutrality in all cases. Taking into account the turnover of foreign branches could even serve to increase the recovery ratio, albeit some of the acquisitions may not have any connection with the activities carried out by those establishments.Footnote11 Third, the Court argued that including the output supplies of foreign branches would impair the effectiveness of the provisions of Articles 5(7)(a) and 6(3) of the Sixth VAT Directive (now Articles 18(a) and 27 of the VAT Directive) as those provisions grant the Member States ‘certain discretion’ with respect to their tax policy choices.Footnote12 In order to avoid distortion of competition, these provisions give the Member States the right to treat the in-house creation of goods and the in-house supply of services as taxable transactions, if the taxable person does not have a full right to input VAT deduction.Footnote13

Although the CJEU explicitly ruled on the recovery ratio calculation of a domestic head office only, the same interpretation of Articles 173 et seq of the VAT Directive will consequently also apply to fixed establishments.Footnote14 Based on the reasoning given by the Court, any establishment (head office or fixed establishment) has to calculate its recovery ratio on a territorial per-country basis excluding output supplies carried out by establishments in other countries.

2.3. Arguments for a global approach

There are a number of reasons for questioning the interpretation chosen by the CJEU. First, the wording suggests a different approach: the second sentence of Article 173(1) of the VAT Directive stipulates that input VAT deduction shall be based on ‘all the transactions carried out by the taxable person’. Moreover, in this regard Article 169(a) of the VAT Directive, clarifies that, in principle, output supplies carried out in other Member States also have to be considered.

In addition to the wording of the Directive, there are also systematic arguments supporting a global recovery ratio approach. According to the FCE Bank case, the head office and any fixed establishment(s) are regarded as one single taxable person. Hence, a fixed establishment cannot carry out taxable supplies itself.Footnote15 As the wording of the Directive does not include an express statement either for the output side (Article 9) or for the input side (Articles 167 et seq), when it comes to the status of a fixed establishment, one could argue that the inherent system of the VAT Directive should provide a similar result for both areas.Footnote16 In this respect the Eighth Council Directive 79/1072/EEC and the Thirteenth Council Directive 86/560/EEC cannot convincingly support a different result for the input side. The CJEU itself has established in the Daimler and Widex case that it is not the existence of a fixed establishment, but the provision of taxable supplies that determines the method of repayment of VAT (by deduction or by refund).Footnote17

Furthermore, the solution adopted by the Court in Crédit Lyonnais suggests that the system for input VAT deduction including the calculation of the recovery ratio is always strictly limited to one country, but that is not true: under Article 169(a) of the VAT Directive, supplies carried out abroad generate a right to input VAT deduction under certain conditions.Footnote18 Even more importantly, one has to keep in mind that in a situation where a branch does not make any taxable supplies in the Member State where it is located, the head office is nevertheless entitled to ask for a refund of input VAT based on Directive 2008/9/EC (the former Eighth Council Directive 79/1072/EEC) or the Thirteenth Council Directive 86/560/EEC.Footnote19 Hence, the EU VAT system clearly also links input VAT with output supplies carried out in foreign territories.Footnote20 Moreover, the solution adopted by the Court may lead to non-deductible input VAT even though the services or goods are used for an economic activity. This result is questionable in the light of the neutrality principle and the aim of the input VAT deduction rules.Footnote21

The most important reason (as regards this paper), however, is that interpreting the VAT Directive such that Member States are prohibited from including output supplies carried out by foreign establishments (head office or fixed establishment) when calculating the recovery ratio of the resident establishment (head office or fixed establishment) may also lead to an infringement of the freedom of establishment.

2.4. Territorial approach: an interpretation in conflict with the freedom of establishment?

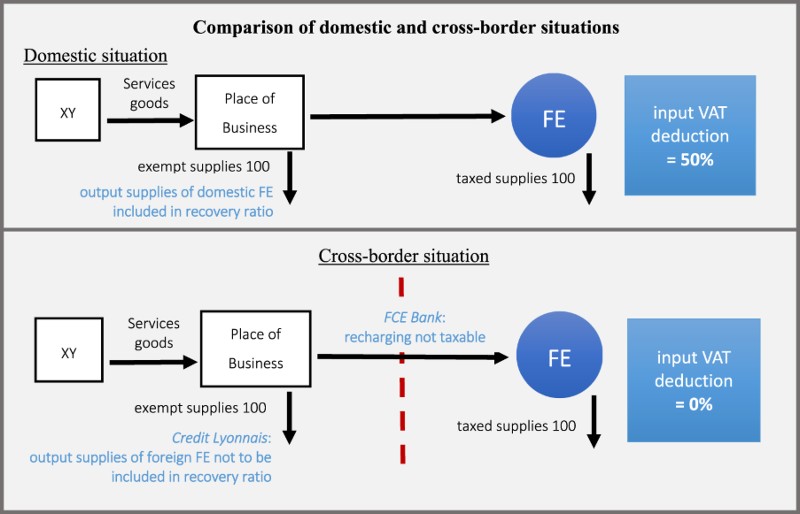

The potential infringement of the freedom of establishment as a consequence of the interpretation chosen by the Court in the Credit Lyonnais case can be illustrated by the following simplified example:

A company consists of a place of business and one fixed establishment. The place of business carries out exempt supplies in the amount of 100 (e.g. letting of real estate for residential purposes, Article 135(1)(l)). The fixed establishment conducts taxed supplies in the amount of 100 (e.g. letting of real estate for touristic purposes, Article 135(2)(a)). The place of business acquires a computer which is used for accounting purposes for both activities in equal parts (mixed-use good).

If the fixed establishment and the place of business are located in the same Member State, the result will be as follows: the recovery ratio based on Article 174 of the VAT Directive is to be calculated by using the taxed supplies (100) in the numerator and the total turnover (200) in the denominator. Hence, the taxable person will have a right of deduction of 50% of the input VAT charged for the computer.

If one adds a border between the place of business and the fixed establishment the result is different. According to the Credit Lyonnais case, the head office is not allowed to take into account the taxed output supplies of the foreign fixed establishment when calculating the recovery ratio. Moreover, according to the FCE Bank case, the recharging of costs between the place of business and the fixed establishment is not a taxable transaction and cannot therefore increase the numerator. Based on the interaction of the Credit Lyonnais and the FCE Bank cases, the result in the cross-border situation is as follows: since the place of business carries out exempt supplies only, the numerator is zero. Hence, the taxable person does not have any right to deduct the input VAT on the cost of the computer, although it is—similarly to the purely domestic situation—partly (one half) used for taxable output supplies. To sum up: if the output supplies of a foreign fixed establishment are not tax exempt, excluding those output supplies leads to a lower recovery ratio for the head office compared to conducting the same output supplies via a domestic fixed establishment.Footnote22

The two situations—carrying out supplies via a domestic and a foreign fixed establishment—are treated differently purely due to the border. A lower recovery ratio leads to higher VAT costs for the taxable person. These additional costs might deter a business from setting up a branch in another Member State. Hence, the interpretation of the VAT Directive chosen by the CJEU in the Credit Lyonnais case arguably leads to an infringement of the freedom of establishment.Footnote23 Note, that this argument is valid with respect to entities operating from multiple locations in the European Union and EEA Member States only, since third-country establishments are not covered by the freedom of establishment.

Since, based on the hierarchy of norms, secondary law must be in line with primary law, the Court has constantly emphasised that Directive provisions must be interpreted in the light of the fundamental freedoms.Footnote24 More precisely, if the wording of an instrument of secondary EU law is open to more than one interpretation, ‘preference should be given to the interpretation which renders the provision consistent with the EC Treaty [now TFEU] rather than to the interpretation which leads to its being incompatible with the Treaty’. Footnote25 In the light of these obligations, the interpretation of the VAT Directive in the Credit Lyonnais case may reveal some important aspects with respect to the effects of the fundamental freedoms in the area of VAT. Although the parties to the proceedings argued that the Directive had to be interpreted consistently with the treaty freedoms,Footnote26 the CJEU did not explicitly deal with the different treatment of domestic and foreign branches caused by its interpretation and the potential implications for the freedom of establishment. With respect to whether a territorial or global recovery ratio is to be preferred, the wording of the EU VAT Directive (Articles 173 et seq) is doubtlessly open to more than one interpretation.Footnote27 Based on the wording of the Directive provisions and their systematic context, it would definitely have been possible for the Court to have argued for a global recovery ratio, which would thereby have avoided any potential conflict with the freedom of establishment. The Court did not choose that interpretation which suggests that the CJEU is of the opinion that a different treatment of domestic and foreign branches with respect to the input VAT recovery ratio is compatible with the freedom of establishment.

When analysing why the Court went down this route, different arguments can be advanced and these will be separately analysed in Sections 3 and 4. First, the different level of harmonisation in VAT law, as compared to direct tax law, may have influenced the Court. In this respect, the CJEU case law to date on the compatibility of VAT law measures with the fundamental freedoms will be scrutinised (Section 3). Second, one has to keep in mind that not every difference in treatment between a domestic and a cross-border situation is prohibited by the fundamental freedoms. Different treatment might be permissible where it does not restrict a freedom (Section 4.2), if the domestic and cross-border situation are not objectively comparable (Section 4.3) or if there is a legitimate and proportionate justification for the different treatment (Section 4.4).

3. Fundamental freedoms in VAT: general remarks

3.1. Secondary law and fundamental freedoms

Compared to the extensive and ever growing case law on the effects of the fundamental freedoms in the area of direct tax law, the number of cases dealing with the effects of the fundamental freedoms in the area of VAT is extremely low. As at the end of 2017, about three cases had been brought to the CJEU dealing with the compatibility of the VAT Directive with the fundamental freedoms,Footnote28 and about three cases dealing with the compatibility of domestic VAT rules with the fundamental freedoms.Footnote29

The limited number of cases decided by the CJEU in this area can be explained by the different levels of harmonisation. VAT—in contrast to direct taxes—has been harmonised by the VAT Directive to a great extent. The VAT Directive removes many obstacles to the free flow of goods and services in the internal market. Hence, there is less scope for taxpayers and courts to identify potential infringements of the freedoms.

The different level of harmonisation is also of major importance when evaluating the effects of the fundamental freedoms in VAT. Due to the exhaustive harmonisation it will be the Directive and the EU legislature which is confronted with the violation of the freedoms in the majority of cases, not the Member States’ domestic law and domestic legislatures. This may include differences with respect to the standard of evaluation when applying the rule of reason (‘judicial self-restraint’). In the Credit Lyonnais case, the Court had to interpret the VAT Directive and thereby take into account primary law. In such a scenario the case law on the compatibility of secondary law with the fundamental freedoms seems of greater relevance.

According to prevailing opinion and settled case law, the EU legislature—although not formally stated in the wording of the Treaties—is also bound by EU primary law, especially the fundamental freedoms enshrined therein.Footnote30 The number of cases where the Court has had to deal with the question of whether a Directive is invalid due to an infringement of primary law, is, however, very limited compared to the overall amount of its case law.Footnote31 However, the CJEU can not be held responsible for the limited number of cases, as the Court cannot initiate action of its own accord but is primarily dependent on the initiative of national courts and the Commission. As a rule, the CJEU presumes that EU legislation is lawful and will analyse its compatibility with primary law only when specifically asked to do so.Footnote32 As the number of cases on the compatibility of secondary law with primary law is limited, it is also no surprise that the number of cases where the Court has found a provision of a directive to be incompatible with the fundamental freedoms is also very low.Footnote33

When looking at the few cases it has considered so far, the CJEU seems to apply a less strict standard when analysing whether the EU legislature has infringed the fundamental freedoms as compared to the standard it applies when domestic legislatures are alleged to have infringed them.Footnote34 In the Rewe-Zentral case in 1984, the Court emphasised that the ‘Community institutions have a discretion in particular with regard to the possibility of proceeding towards harmonization only in stages and of requiring only the gradual abolition of unilateral measures adopted by the Member States.’Footnote35 This formula has been confirmed several times and is to be considered as settled case law.Footnote36 The Court has emphasised this ‘harmonisation-in-stages’ argument in particular in the area of tax law: the harmonisation of tax measures

is generally difficult … because they require the competent Community institutions to draw up, on the basis of diverse and complex national provisions, common rules in harmony with the aims laid down by the Treaty and … , as is the case in fiscal matters, the unanimous agreement of the [Members of the Council].Footnote37

It should be noted though, that this discussion on a ‘judicial self-restraint’ as regards secondary law in the area of tax law has gained and will gain even more importance in future years. Driven by the OECD BEPS project, since 2016 the European Union has adopted a number of secondary law measures raising potential conflicts with EU primary law, primarily in the area of direct taxes.Footnote40 The most prominent example is the Anti-Tax Avoidance Directive (ATAD) which includes six specific measures to fight profit shifting and base erosion by multinationals.Footnote41 Many of these measures have been criticised by scholars as being in conflict with the fundamental freedoms as interpreted by the CJEU.Footnote42 Hence, the CJEU will most likely be given the possibility to develop further and refine its approach. However, as the date by which the Member States must implement the ATAD is the beginning of 2019 or for some measures even as late as 2022/2024, it will take some years until referrals from domestic courts on this subject will reach the CJEU.

3.2. VAT directive and fundamental freedoms

Against this background, it is less of a surprise that, both in direct tax and in VAT law, it has thus far never happened that the CJEU has invalidated a provision of secondary law (in particular a directive) based on an infringement of the fundamental freedoms.Footnote43 In the event of potential conflict, the Court either tries to interpret secondary law in line with the freedoms (or other primary law provisions)Footnote44 or emphasises the need to harmonise in stages.Footnote45 As regards VAT, the potential invalidity of a directive provision due to an infringement of the fundamental freedoms or closely linked primary law provisions was discussed in three cases. In all three of these cases, the Court used different methods to avoid declaring the provision in question invalid: in the Schul case, handed down in 1982, the Court made use of extensive interpretation methods in order to avoid a conflict between the Sixth VAT Directive and Article 110 of the TFEU (formerly Article 95 EEC-Treaty).Footnote46 In the Kieffer and Thill case, handed down in 1997, the Court found the obligation to report intra-EU supplies to be justified by the need to promote the completion of the EU internal market and the need for statistical data. Thereby, the Court also explicitly referred to the ‘harmonisation-in-stages’ argument.Footnote47 Finally, in the Schmelz case, handed down in 2010,Footnote48 the Court applied a less stringent proportionality test in favour of the EU legislature compared to its direct tax case law approach without using the ‘harmonisation-in-stages’ reasoning explicitly (see in more detail Section 4.4.3.3).

To sum up, the jurisprudence on the compatibility of VAT Directive provisions with the fundamental freedoms is very limited and does not give much guidance. Nevertheless, the case law indicates—in line with the case law on other secondary law—that the Court applies a less stringent standard when evaluating whether secondary law is in line with primary law compared to the standard it applies to evaluating the Member States’ domestic law. The methodological approach used to achieve this result, however, differs from case to case.

4. Applying the fundamental freedoms to the Credit Lyonnais case

4.1. The non-discrimination test

The fundamental freedoms preclude Member States from treating cross-border situations less favourably than domestic situations, ‘unless such a difference in treatment concerns situations which are not objectively comparable or is justified by overriding reasons in the public interest’.Footnote49 When evaluating whether a discriminatory treatment is permissible, the justification must also meet the proportionality principle, thus the domestic measure ‘must be appropriate to the objective pursued, and must not go beyond what is necessary to attain that objective’.Footnote50 Based on this formula, there are three main possible arguments for why the interpretation by the CJEU in the Credit Lyonnais case does not lead to an infringement of the freedom of establishment: First, one could argue that there is no disadvantage and hence no discrimination is present; second, one might question and deny the objective comparability of the situations; and third, one or more valid ground(s) of justification could allow the discriminatory treatment to subsist.

4.2. No disadvantage?

In the scenario illustrated in Section 2.4, the calculation of input VAT based on a territorial recovery ratio doubtlessly leads to a disadvantage in the cross-border situation compared to the domestic situation. The business suffers higher non-deductible VAT costs caused by the location of the fixed establishment abroad. However, excluding the output supplies of a foreign fixed establishment does not necessarily result in a negative effect, but may work in both ways: to the detriment and the benefit of the taxable person. A per-country recovery ratio calculation leads to a disadvantage if the foreign establishment as a stand-alone has a higher recovery ratio than the head office. By contrast, an advantage for the business occurs if, on a stand-alone basis, the foreign establishment has a lower recovery ratio than the head office. As it depends on the facts in each case, one could argue that an interpretation of the Directive’s provisions in favour of a territorial recovery ratio is not discriminatory as such.Footnote51

However, this argument is not convincing if one looks at the direct tax jurisprudence. According to settled case law on direct taxation, a disadvantage for one taxpayer cannot be offset by advantages created by the same legislation for other taxpayers.Footnote52 For example, in the Lakebrink case, the dispute concerned whether the exclusion of foreign negative income when calculating the tax rate for resident persons was in line with the fundamental freedoms. The Luxembourg Government argued that the disadvantage suffered by Mr and Mrs Lakebrink was compensated for by the fact that, overall, the Luxembourg measure was more favourable for non-residents as compared to residents because it took no account of foreign income, whether negative or positive. The Court clearly rejected this argument: the fact that a legislative measure places non-residents at a disadvantage ‘cannot be compensated for by the fact that in other situations that same legislation does not discriminate between non-residents and residents’.Footnote53 Continuing along this line of reasoning, the Court also acknowledged in the Lidl Belgium case that the lack of a right to deduct the losses generated by a foreign permanent establishment, subject to the exemption method in the applicable double tax treaty, as compared to domestic permanent establishments, amounted to a restriction on the freedom of establishment. The fact that the disputed discriminatory effect only existed in loss and not profit situations, did not prevent the CJEU from requiring justification for the different treatment.Footnote54 Moreover, the Court made clear in the Talotta case that, even if the domestic legislation is beneficial in the vast majority of cases and only creates a hindrance to the fundamental freedoms under very specific circumstances, this does not detract from the fact that the individual case falls within the non-discrimination test. Footnote55 To sum up, the Court usually focuses on the individual situation in isolation when analysing whether legislation establishes an obstacle to the internal market.Footnote56 Based on this settled case law, the fact that a territorial recovery ratio may turn out to be more favourable to some businesses conducting cross-border activities should not rule out the obligation to carry out a justification and proportionality analysis for those individual situations where the same legislation creates obstacles to the exercise of the fundamental freedoms.Footnote57

It is worth noting though, that all the CJEU cases mentioned above dealt with Member States’ domestic legislation, not harmonised Union measures. Hence, it can not be ruled out that the CJEU might be willing to apply a more lenient approach as regards provisions in the VAT Directive (see Section 3). The result in the Credit Lyonnais case might even support such an assumption. Such a compensatory approach, however, should be rejected for its generality, since it goes against the rationale of an internal market. Advantages for some taxpayers can not take away a disadvantage for other taxpayers caused by the same legislation. Distortional effects on their decisions will still be in place. A tax measure leading to discriminatory effects for some taxpayers can only be permissible if the discriminatory effect can be justified by a legitimate reason in the public interest.Footnote58

4.3. Lack of comparability?

4.3.1. Reasoning in Credit Lyonnais

Another argument to explain the result of the CJEU may rest with the lack of comparability. It is settled case law that discrimination arises ‘through the application of different rules to comparable situations’.Footnote59 Hence, if two situations are not ‘objectively comparable’, the CJEU tends to stop its analysis and accepts a different treatment as being in line with the fundamental freedoms.Footnote60 One could try to argue that the situations of a domestic and a foreign fixed establishment are not objectively comparable when it comes to input VAT deduction and, hence, they need not be treated equally. This seems to be the approach followed by Advocate General Cruz Villalón who emphasised that ‘[a] company which has its principal establishment and branches in a single Member State is not, with regard to the objective system established by the Sixth Directive 77/388, in the same situation as a company which has branches in other Member States’.Footnote61 Some statements by the Court seem to build on the same reasoning.Footnote62

4.3.2. Direct tax jurisprudence

The comparability test has gained importance in direct tax jurisprudence since 2013.Footnote63 Nevertheless, scholars and Advocates General have rightly been critical of the fact that the exact criteria for evaluating comparability are still blurred.Footnote64 According to ‘settled case-law’Footnote65 the ‘aim’ of the disputed measure forms the basis for the comparability analysis.Footnote66 In a growing number of cases—in particular in the practically important areas of dividend taxation and loss utilisation—the CJEU also refers to the (non-)existence or (non-)exercise of taxing jurisdiction in relation to a certain undertaking.Footnote67

With respect to domestic and foreign permanent establishments, until 2008, the CJEU had implicitly confirmed their comparability without giving a detailed reasoning.Footnote68 This approach, however, seems to have been overruled by the Timac Agro case handed down in 2015. In Timac Agro, the Court had to deal with the question whether losses generated by foreign permanent establishments and domestic permanent establishments have to enjoy the same tax treatment under German income tax law; in particular whether Germany is obliged to take into account ‘final’ losses. The Court applied a restrictive approach. To the surprise of academic commentatorsFootnote69 the reasoning was based on the lack of comparability: the Court held that

in principle, permanent establishments situated in a Member State other than the Member State concerned are not in a situation comparable to that of resident permanent establishments in relation to measures laid down by that Member State in order to prevent or mitigate the double taxation of a resident company’s profits.Footnote70

4.3.3. Relevance for VAT

As regards the aim of the provisions on input VAT deduction, it is rather difficult to infer any relevant difference in the situations discussed in Credit Lyonnais. Articles 167 et seq of the VAT Directive deal with one of the core principles of the EU VAT system: achieving neutrality by avoiding VAT costs for businesses, insofar as the input costs are used for taxed output supplies. This aim of achieving neutrality through input VAT deduction applies equally to businesses with domestic branches and businesses with foreign branches. In both scenarios, the taxable person may use the goods or services for taxed output supplies and, hence, would like to benefit from input VAT deduction.Footnote73

However, a difference in the situations may be identified when focusing on the taxing jurisdiction as the criterion for comparability. One may argue that in the cross-border scenario the state where the input VAT is due has no right to tax the corresponding output supplies for which the input costs are used. In other words: following this argument, input VAT deduction would be possible only if the input VAT costs are used for taxed output supplies in the same territory and, hence, generate VAT revenue for the respective Member State. However, as the VAT Directive does not follow such a symmetric system and does not link input VAT deduction and output supplies coherently to the territory of the same Member State (see Section 2.3), this reasoning seems not to be very persuasive.

Also, from a methodological point of view, better arguments speak in favour of accepting comparability. Relying on the lack of taxing jurisdiction at the comparability level of the analysis leads to a major unsystematic overlap with the justification level.Footnote74 In contrast to evaluating these arguments at the level of justification, using them to deny comparability, however, implies a significant deficiency: the measure is not subject to the proportionality test.Footnote75 The argument based on (non-)existing taxing jurisdiction should, hence, be tested at the justification level only.

4.4. Justification

A third possible basis for arguing that a territorial recovery ratio does not infringe the freedom of establishment could rest with the justification grounds. One could in particular think of those justification grounds which have already been accepted in the direct tax jurisprudence: safeguarding the balanced allocation of taxing rights, safeguarding the coherence of the tax system, safeguarding the effectiveness of fiscal supervision and combating abuse. Moreover, one could also try to justify the different treatment for reasons of administrative practicability. This argument has not yet been very successful in direct tax law, but could potentially have a broader scope in VAT.

4.4.1. Balanced allocation of taxing rights

4.4.1.1. Reasoning in Credit Lyonnais

One of the arguments used by the CJEU to support its interpretation of Article 173 of the VAT Directive would suggest that the Court was implicitly relying on a justification linked to the balanced allocation of taxing rights. The Court highlighted:

Since the methods of calculation of the proportion constitute a fundamental element of the deduction system, account cannot be taken, in calculating the proportion applicable to the principal establishment of a taxpayer established in a Member State, of the turnover of all of the taxable person’s fixed establishments in the other Member States, without seriously jeopardising both the rational allocation of the spheres of application of national legislation in VAT matters and the rationale of the aforesaid proportion.Footnote76

4.4.1.2. Direct tax jurisprudence

The justification ground of safeguarding the balanced allocation of taxing rights originally stems back to the landmark decision in Marks and Spencer on cross-border loss utilisation handed down in 2005Footnote78 and has been gaining importance year on year since then. It has been accepted as valid justification in three main scenarios:Footnote79 utilisation of foreign losses,Footnote80 exit tax measures,Footnote81 and anti-profit shifting measures.Footnote82 In allowing this justification ground, the Court seems to accept that there is an internationally accepted tax policy for direct tax law systems as well as for international tax agreements and that the Member States are permitted to rely on such common principles when designing their tax systems and allocating taxing rights between them.Footnote83 In particular, the Court acknowledges that Member States follow the territoriality principle and that they may also take measures to defend taxation in line with this principle.Footnote84 According to the Court, a balanced allocation of taxing powers ‘might make it necessary to apply to the economic activities of companies established in one of those States only the tax rules of that State in respect of both profits and losses’.Footnote85 Hence, Member States can take measures required for ‘safeguarding the symmetry between the right to tax profits and the right to deduct losses’.Footnote86 Based on these arguments, Member States are permitted to deny the offset of foreign losses if they cannot tax profits from the same undertaking.Footnote87 As the Lidl Belgium and Timac Agro cases show, the Court applies this line of reasoning particularly in relation to foreign permanent establishments subject to the exemption method in a double tax treaty.Footnote88

4.4.1.3. Relevance for VAT

General Remarks: The justification based on the need to safeguard a balanced allocation of taxing rights between states has to be seen against the background that direct tax law is not exhaustively harmonised. In contrast to VAT, EU law does not contain any binding rules on the allocation of taxing rights when it comes to the taxation of income. Hence, the CJEU accepts that Member States make their own tax policy decisions including the signing of tax treaties with other states and that they may also take measures to defend taxation in line with these decisions. By contrast, in the area of VAT the connecting factors for allocating taxing rights on one transaction are harmonised by the VAT Directive (mainly by the place of supply rules). Member States are, in general, not free in their tax policy decisions nor are they free to agree on bi- or multilateral treaties amongst each other in this respect. Double taxation should not occur. Hence, at first sight there is nothing that may be defended by the Member States in a similar manner to the direct tax area.Footnote89 Moreover, the reasoning on balanced allocation of taxing rights in direct tax law is, ultimately, based on the territoriality principle which is an internationally recognised principle in the area of direct tax law. As regards VAT, the relevance of the territoriality principle is, however, more than questionable. The allocation of taxing rights between states in the area of VAT, in particular in the European Union, follows the destination and neutrality principles which do not seem to have any similarities with the territoriality principle in direct tax law. The justification based on safeguarding a balanced allocation of taxing rights between states is, hence, difficult to transpose to VAT.

However, although the VAT Directive establishes a very exhaustive harmonisation of the law following the destination and neutrality principle, there are still areas where the Member States enjoy a certain degree of discretion and where they can make their own tax policy decisions.Footnote90 Discretionary power in particular exists where the VAT Directive provides options for the Member States.Footnote91 In those areas there might be room for justification on the basis of safeguarding the balanced allocation of taxing rights or on similar grounds labelled with another terminology.

Options when designing input VAT deduction: When taking a closer look at the legal basis in the VAT Directive, the system for input VAT deduction as stipulated in Articles 167 et seq of the VAT Directive leaves the Member States a margin of discretion by providing several optionsFootnote92 which was also pointed out by the Advocate General and the Court in Credit Lyonnais.Footnote93 Moreover, the right to deduct input VAT is to a great extent linked to exemptions, since input VAT deduction is possible only if the corresponding output transactions are subject to tax. Member States enjoy rather large discretion when implementing exemptionsFootnote94 and the number and scope of exemptions varies from Member State to Member State. This might also speak in favour of a territorial approach when it comes to input VAT deduction.

However, neither of these aspects of tax sovereignty should be able to justify the exclusion of output transactions carried out by a foreign establishment when calculating the recovery ratio of a domestic establishment. It is true that the rules on input VAT deduction grant a margin of discretion to the Member States. Nonetheless, it is unclear why this should prevent them from calculating the recovery ratio in a non-discriminatory way. The fact that Member States may choose to implement different options does not prevent them from applying the same rules and limitations to businesses operating purely domestically and to businesses operating across borders. In fact, in relation to VAT, the Court itself constantly requires Member States to exercise any discretion given by the secondary legislation in line with the principle of neutrality.Footnote95 None of the options for input VAT deduction provided by the Directive seems to have any specific legal or practical restriction when implemented for businesses with multiple locations. For example Article 173(2)(b) of the VAT Directive—an option which was highlighted by the Court in Credit Lyonnais—grants the Member States the possibility of requiring the taxable person to determine a separate pro rata deduction for each sector of his business and to keep separate accounts for each sector. There is no reason why this requirement cannot be implemented and applied to businesses with only one location and those with multiple locations on an equal level.

Furthermore, tax sovereignty with respect to exemptions has already been addressed by the EU legislature: According to Article 169(a) of the VAT Directive the Member State where input VAT is due is required to grant an input VAT deduction only if the linked output supplies taxable abroad would entitle the taxpayer to an input VAT deduction under its domestic law as well.Footnote96 Hence, Member States’ sovereignty when designing exemptions is upheld. A refusal to consider transactions carried out by foreign establishments when calculating the recovery ratio for input VAT seems to go beyond what is necessary to achieve this aim.

Options in Articles 18(a) and 27 of the VAT Directive: In Credit Lyonnais, the Court also highlighted other provisions in the VAT Directive granting discretion to the Member States. According to the Court, the obligation to take into account supplies carried out via foreign establishments in the pro rata calculation ‘is liable to impair the effectiveness of Articles 5(7)(a) and 6(3) of the Sixth Directive which grant Member States certain discretion while mitigating the effects of their choices in relation to taxation policy’.Footnote97 Both provisions mentioned are nowadays to be found—without substantial amendmentFootnote98—in Articles 18(a) and 27 of the VAT Directive. These provisions grant the Member States the right to tax in-house production of goods and services (‘insourcing’), if acquiring the same supplies from third parties (‘outsourcing’) would lead to non-deductible input VAT. In making this statement, the Court seems to be of the opinion that both optional provisions—when exercised by a Member State—would lead to a separate-entity approach in a cross-border situation and more precisely, grant Member States the right to tax supplies carried out between different fixed establishments of the same taxable person located in different states.Footnote99 If one follows this interpretation of Articles 18(a) and 27, the refusal to allow a global pro rata calculation seems reasonable at first sight. Applying a global pro rata calculation at the input level could indeed interfere with such a domestic policy decision. The Member State would be forced to apply a single-entity approach on the input side although it has exercised the option for a separate-entity approach in Articles 18(a) and 27 for the output side. Since the EU legislature did not provide any special rules for self-supplies based on Articles 18(a) and 27 within the pro rata calculation in Article 173, applying these rules to scenarios where a Member State has availed itself of the option in Articles 18(a) and 27 leads to an unsystematic result:Footnote100 the business would have to take into account the same added value twice in the numerator and/or denominator.Footnote101

However, whether this systematic problem and lack of specific rules in the Directive may justify the discriminatory treatment which arises from a strict territorial approach when interpreting Article 173 of the VAT Directive is questionable. First, even by denying a global pro rata deduction this systematic problem cannot be avoided. If a Member State makes use of the option in Article 27, the mismatch between the input and output side also occurs in purely domestic scenarios; this is the case if two establishments of the same taxable person located in the same Member State exchange services or, even more remarkably, if one establishment produces goods or services in-house for its own use. It would only be possible to completely avoid this problem if the Court were to require the Member States to implement a pro rata calculation per establishment or per business unit (not per country). This is, however, not what the Court seems to argue in Credit Lyonnais.

Second, it should be noted that Articles 18(a) and 27 of the VAT Directive do not refer either to fixed establishments or to cross-border situations. Based on the historical materialsFootnote102 and also confirmation by the Court,Footnote103 the aim of Article 18(a) is to prevent partly exempt businesses from gaining a competitive advantage via in-house construction of goods. For businesses carrying out exempt output transactions, the self-production of goods or the in-house supply of services, without recourse to third parties, is more favourable as it avoids additional input VAT costs. Hence, businesses conducting exempt activities which need to buy the same goods or services externally are at a disadvantage. In this respect Article 18(a) steps in: In order to achieve neutrality of the choice of organisational structures (insourcing or outsourcing), Member States may treat the self-production of goods as a supply of goods made for consideration within the meaning of the Directive, thereby triggering input VAT costs for the in-house producing business as well.Footnote104 Article 27 mirrors for services, the self-supply rule for goods. Although historical materials do not provide any explicit link between these two provisions, according to prevailing opinion, which is backed up by the similarities in their wording, both provisions serve the same aim.Footnote105 Moreover, in the Credit Lyonnais case the Court referred to both provisions in one breathFootnote106 which proves their parallels. Seen from this teleological background, neither of these provisions is aimed at establishing a separate-entity approach for fixed establishments or at allocating taxing rights between states.Footnote107

The context of the VAT Directive even suggests that both provisions are primarily targeted at purely domestic situations: first, since the cross-border transfer of goods is already covered by Article 17, there is no need to apply Article 18(a) to cross-border scenarios. Second, applying both provisions, in particular Article 27, to cross-border scenarios raises problems of accumulation of VAT:Footnote108 since Article 27 is optional and the Court grants discretionary power to Member States with respect to optional provisions,Footnote109 Member States may use the option in a different way or not at all. If one Member State has exercised the option but the other Member State involved has not, this could lead to a double burden of VAT or no taxation at all.Footnote110 If it is only the state of the fixed establishment using the in-house service that has exercised the option in Article 27, that state will levy VAT on the self-supply, but the state where the fixed establishment rendering the service is located may not allow systematic input VAT deduction for input costs necessary to provide the in-house services.Footnote111 This ends up in a double burden of VAT which could only be solved by extensive interpretation methods as applied in the Schul case.Footnote112 In the inverse scenario, non-taxation is also difficult to tackle using the existing instruments.Footnote113 The lack of specific provisions in the VAT Directive for solving these neutrality problems suggests that the EU legislature was not addressing cross-border situations when enacting Articles 18(a) and 27. Against this background, the reference to Articles 18(a) and 27 of the VAT Directive in the Credit Lyonnais case is confusing, as the Court seems to give a different meaning to each of these provisions from that which their teleological, historic and systematic background would suggest.

‘Symmetry’: Nevertheless, although the reference by the CJEU to the options stipulated in Articles 167 et seq and Articles 18(a) and 27 of the VAT Directive is not convincing, in the light of the more recent developments in the direct tax law jurisprudence it might still be possible to justify the Court’s approach on the basis of safeguarding a balanced allocation of taxing powers between states. In particular, one could try to transfer the increasingly used set phrase on ‘symmetry’ by analogy to the Credit Lyonnais case. As already mentioned in connection with the comparability level of the analysis (see Section 4.3), unlike in a purely domestic situation, in the case of an entity with multiple locations, the state where the input VAT is due might have no right to tax the corresponding output supplies for which the input costs are used.Footnote114 This has echoes of the constellation discussed in the K and Timac Agro cases on loss utilisation, where the Court accepted the non-deductibility of foreign losses as part of a ‘logical symmetry’.Footnote115

Still, there are good arguments against accepting the balanced allocation of taxing rights between states as a valid justification ground for the different treatment of domestic and foreign branches when calculating the recovery ratio for input VAT. The reasoning in the loss utilisation cases in direct tax law is, ultimately, based on the territoriality principle.Footnote116 As already highlighted previously, the allocation of taxing rights between states in the area of VAT, however, builds on other underlying principles, namely the destination and neutrality principles. Especially with respect to input VAT deduction, the VAT Directive does clearly not follow a territorial approach. Based on the neutrality principle, the linking of input VAT to output supplies taxable in another country is not detrimental to the right to input VAT deduction as such (see Section 2.3). Hence, the context of the VAT Directive significantly weakens this line of reasoning and should render the discriminatory measure disproportionate.

4.4.2. Coherence of the tax system

4.4.2.1. Reasoning in Credit Lyonnais

Another possible justification which does not appear in the reasoning of the judgment, but which is worth evaluating, is one based on the coherence of the tax system. The argument might be as follows: as the territorial recovery ratio works to the detriment and to the benefit of the taxable person, the business will not only suffer a disadvantage, but benefit from an advantage in previous or subsequent years. Hence, the territorial approach reflects a coherent system. However, in view of the direct tax jurisprudence, whether this argument is persuasive is again rather questionable.

4.4.2.2. Direct tax jurisprudence

Nowadays, the coherence argument has two manifestations in direct tax law: The original argument stemming from the Bachmann judgmentFootnote117 requires a ‘direct link’ between an advantage and a disadvantage in the hands of the same taxpayerFootnote118 and with respect to the same tax.Footnote119 For example, in Bachmann the Court accepted the non-deductibility of contributions to non-resident insurance companies as being in line with the fundamental freedoms, since—in contrast to those made by resident insurance companies—the subsequent payments by the non-resident insurance companies to the same taxpayer could not be taxed.Footnote120 Under this approach, coherence requires that the advantage is actually offset by a disadvantage in the hands of the same taxpayer (factual direct link)Footnote121 and that the domestic provision itself ‘establishes a relationship’ between both elements (legal direct link).Footnote122

The new manifestation of the justification ground of ‘coherence’—which has arisen since the year 2010 mainly in the area of loss utilisation—requires the same advantageous and disadvantageous element, but it is no longer seen as necessary that the disputed benefit will indeed be neutralised (i.e. no factual direct link required). Rather, the Court seems to regard it as sufficient if the law establishes a coherent link in theory, without analysing whether the advantage will actually be offset by a corresponding disadvantage in an individual case.Footnote123 In particular the K case on foreign loss utilisation follows this new line of reasoning.Footnote124 However, in other judgments handed down after the K case, the Court is still explicitly asking for a factual direct link.Footnote125 In all cases where the ‘new’ meaning of coherence pops up, the Court has additionally referred to the argument on safeguarding the balanced allocation of taxing rights between states.Footnote126 Hence, the most convincing way to solve the conflict between the diverging lines of jurisprudence is to regard the reasoning on safeguarding the balanced allocation of taxing rights between states as key in those cases.Footnote127 In order to establish a systematic approach, references to ‘coherence’ in this paper should be read as referring to the traditional meaning of the concept.Footnote128

4.4.2.3. Relevance for VAT

The coherence argument is not specifically linked to direct tax law. Although the CJEU has never yet done so, there is room to apply this justification also in relation to VAT. However, in the author’s opinion, the justification based on safeguarding the coherence of the tax system cannot be relied on in the case at hand. The ‘coherence’ concept as it stemmed from the Bachmann case requires a strict correlation between an advantage and a disadvantage with respect to the same taxpayer. This requirement is not met here: The prohibition on including the supplies carried out by foreign establishments when calculating the recovery ratio for input VAT may lead to an advantage or to a disadvantage for the business in question depending on the specific situation in each separate tax period. It is not certain that the disadvantage (lower recovery ratio due to ignoring the taxable supplies carried out by the foreign establishment) will be offset by an advantage (higher recovery ratio due to ignoring the exempt supplies carried out by the foreign establishment).Footnote129 What is more, Article 173 of the VAT Directive does not establish any link between these two situations. Hence, there is neither a legal nor a factual direct link. The taxable person (e.g. Credit Lyonnais) may suffer a disadvantage only and never benefit from an advantage, e.g. if the foreign establishment does not carry out any exempt supplies at any time (or vice versa). Hence, the different treatment acceptable under the interpretation of the Court in the Credit Lyonnais case cannot be justified by the need to safeguard the coherence of the VAT system.Footnote130

4.4.3. Ensuring the effectiveness of fiscal supervision

4.4.3.1. Reasoning in Credit Lyonnais

Another justification which might play a role in the given case and in VAT in general is the need to safeguard the effectiveness of fiscal supervision. If a taxable person conducts business in various different countries through fixed establishments, a global recovery ratio would bring with it the need to include output supplies made in a great number of states. All this data may not be easy to verify. Hence, one might argue that a territorial recovery ratio is necessary to ensure effective fiscal supervision.

4.4.3.2. Direct tax jurisprudence

In an internal EU direct tax context, the justification based on ensuring effective fiscal supervision and the difficulties in verifying information is in general not accepted by the Court.Footnote131 The CJEU has emphasised in settled case law that EU taxpayers ‘should not be excluded a priori from providing relevant documentary evidence’.Footnote132 Moreover, the Court has also pointed out that the Member States may make use of the means provided by the Directive on Administrative Cooperation 2001/116/EU (DAC) to ask for information and cooperation from the financial authorities of other Member States to verify whether the data provided by the taxpayer is correct.Footnote133 In the ELISA case the CJEU emphasised that even if it may be impossible to request cooperation by foreign authorities (due to factual or legal limitations), this cannot justify a categorical refusal to grant a tax benefit.Footnote134

4.4.3.3. Relevance for VAT

Based on the existing legal framework as regards the cooperation between financial authorities for VAT purposes, the justification ground that the different treatment is required to ensure the effectiveness of fiscal supervision will—compared to the internal EU situation in direct taxes—play only a limited role in the VAT area.Footnote135 Exchange of information and cooperation of Member States’ financial authorities for VAT purposes is provided by Regulation No 904/2010/EU.Footnote136 Based on this comparable legal framework, the jurisprudence on direct tax law can be transposed to VAT: the Member States can either ask the taxpayer to provide all necessary information and/or make use of the mutual assistance procedures under the Regulation as a less restrictive means of achieving the objective of fiscal supervision. In the Schul case, the Court has already applied a similar line of reasoning to a VAT case.Footnote137 In the light of the recent case WebMindLicences, it might be even harder for Member States to rely on the justification of ensuring fiscal supervision in VAT law than it is in direct tax law. Whereas the CJEU has held that the Member States are not obliged to make use of the DAC in direct tax law in order to receive information from other Member States,Footnote138 the Court acknowledged in WebMindLicences that Regulation No 904/2010/EU sets up an obligation for Member States to send requests for information to other Member States under specific circumstances.Footnote139

Admittedly, the Schmelz case handed down in 2010 adds some confusion. In dispute in Schmelz was whether the limitation of the exemption for small businesses in Article 287 of the VAT Directive to resident persons was in line with the fundamental freedoms. The Court acknowledged that it ‘is not at all easy’ for the host Member State to effectively supervise the activities of non-resident businesses as all documents relating to their economic activity will be kept at the foreign place of establishment.Footnote140 Due to the lack of formality obligations on small businesses (exemption from formalities based on Articles 213–271), the Regulation is not of any help to the authorities since the home Member State will not have any information available either. The host Member State can only get the necessary information by subjecting the small business to information provision obligations which would, however, be contrary to the aim of the exemption under dispute.Footnote141 This outcome is surprising and also differs from the opinion provided in the case by Advocate General Kokott.Footnote142 Less restrictive measures are available in order to attain the objectives expressed out. Even though this would bring additional formalities for the taxable person, it seems—in line with the Schul and ELISA jurisprudence—more convincing to allow the taxable person to decide himself whether the benefits provided by the exemption offset the costs caused by additional evidential burdens.Footnote143

Quite apart from these criticisms, the situation in the Schmelz case was a very special one due to the specific aim of the provision under dispute. Hence, the Schmelz reasoning should not be applied to the discriminatory issue at hand. With respect to businesses with multiple locations within the European Union, the business can be required to provide all necessary information for calculating the recovery ratio and this can also be verified by relying on Regulation No 904/2010/EU. There is, as a rule, no legal or practical limitation to the exchange of information. Based on the Schul case and the direct tax jurisprudence, the categorical denial of the tax benefit in the cross-border situation should, hence, not be considered to meet the proportionality test.

4.4.4. The need for administrative simplification

4.4.4.1. Reasoning in Credit Lyonnais

Another argument—which was not addressed by the Court itself, but was mentioned in passing by the Advocate GeneralFootnote144—to justify the different treatment of domestic and foreign establishments might be the need for practicability and simplification of the rules. A calculation of the recovery ratio for the purposes of Article 173 of the VAT Directive on an EU-wide or global basis implies complexity and administrative burdens both for the taxable person and the financial authorities.Footnote145 In the case of an entity with fixed establishments in various Member States, output supplies subject to different domestic VAT systems would have to be verified. Based on settled CJEU case law, the right to input VAT deduction for cross-border operating businesses is subject to a double limitation: meaning every output supply has to be analysed separately to see whether it entitles the taxpayer to an input VAT deduction both in the Member State where the supplies are made and in the Member State where the input VAT is due. Only if the output supplies qualify as taxable transactions in both states, is input VAT deductible and the supplies can be included in the numerator of the pro rata formula.Footnote146 Hence, the Member State of the establishment where the input VAT is due would need to verify the character of every output supply and also would have to learn about the tax treatment of those output supplies in the other Member States. Since Member States enjoy a rather far reaching discretion when it comes to exemptions, this double test would call—particularly in the case of multinational banks or insurance companies—for a lot of resources in terms of people and time and would also be subject to the risk of errors.Footnote147 Different languages and legal traditions as well as changes to the domestic law are only a few obstacles to mention.Footnote148

4.4.4.2. Direct tax jurisprudence

Considerations of an administrative burden and practicability nature have traditionally not been accepted by the Court as justification for a more burdensome tax treatment of cross-border situations.Footnote149 For example, the Court has held that higher social security contributions for workers who transfer their residency abroad cannot be justified by reasons of simplification or difficulties of a technical nature.Footnote150 At the same time, it should be noted that, outside the tax area, the Court has already accepted in several cases that Member States are permitted to introduce ‘rules which are easily managed and supervised’ when pursuing legitimate objectives (e.g. road safety, environmental protection).Footnote151 There is no objective reason why direct and indirect tax law should make an exception to this principle. Hence, simplification measures which help the tax authorities in managing the huge number of taxpayers and assessments they have to deal with could be in line with the fundamental freedoms.

The most prominent examples in the direct tax area implicitly supporting this conclusion are the X and Sopora cases.Footnote152 In the X case, the dispute concerned whether the collection means of withholding at source rather than an assessment procedure violated the fundamental freedoms. Withholding at source allows for the efficient and swift collection of taxes for a large number of taxpayers having only a very limited connection to the domestic territory. However, it also brings with it an administrative burden for a person who is not the actual taxpayer (the recipient of the service). The Court found that collection by withholding was justified by the need to ensure the efficient collection of taxes and did not go beyond what is necessary to achieve the aim.Footnote153 Amongst other arguments, the Court highlighted that direct collection from the non-resident service provider ‘would give rise to a significant administrative burden for the tax authorities responsible for the service recipient in view of the large number of services provided on an ad hoc basis’.Footnote154 Hence, the practicability of the tax collection mechanism was upheld by the Court, even though an assessment might have been less onerous both for the person withholding the tax as well as for the actual taxpayer and even though the Member States could have relied upon the Tax Collection DirectiveFootnote155 to enforce taxes on non-resident taxpayers.Footnote156

In the Sopora case, the Court followed a comparably lenient approach in favour of simplification. The Netherlands granted a 30% tax allowance to non-resident workers who had their main residence more than 150 km away from the Dutch border. Non-residents living closer to the Dutch border (in particular German and Belgian residents) were excluded from this benefit, but had to supply evidence of any extraterritorial expense incurred. The 30% tax allowance (reflecting compensation in respect of extraterritorial expenses) and the 150 km limitation (reflecting those situations where daily commuting is not feasible) were simplification measures designed to allow easy and efficient administration. By referring to its settled case law in the non-tax areaFootnote157 the Court was reluctant to find a violation of the fundamental freedoms: according to the Court these criteria set by the Netherlands, even though ‘necessarily approximate in nature, cannot … [of themselves] amount to indirect discrimination or an impediment to the free movement of workers’. The Court made one exception: discrimination could exist if the Dutch rules ‘were systematically to give rise to a net overcompensation in respect of the extraterritorial expenses actually incurred’.Footnote158 Hence, as long as the criteria (in this case 30% and 150 km) reflected reality in most cases and were not arbitrarily chosen, the Member State was allowed to apply them, even though a limited number of non-residents might suffer a disadvantage compared to non-residents of other Member States. This case law on direct taxes confirms that the need for a practicable and efficient system with respect to the huge number of taxpayers allows for measures of administrative simplification.Footnote159

4.4.4.3. Relevance for VAT

This jurisprudence may be of great relevance in the area of VAT. In the field of VAT, tax administrations are also confronted with a huge number of taxpayers and assessments. Hence, simplification measures are necessary to guarantee practicability and efficiency of the tax system and tax collection. Since VAT is, in contrast to direct taxes, also directly linked to the EU’s financial interestsFootnote160—which has recently been emphasised in a number of cases by the CJEUFootnote161—justification based on the need for practicability and simplification in order to ensure efficient collection of taxes may gain even more importance in VAT. The importance of efficient VAT collection is also visible in the rather strict approach the Court applies when addressing cases of abuse and evasion under the VAT Directive.Footnote162 In the words of the Court, a Member State is ‘under an obligation to take all legislative and administrative measures appropriate for ensuring collection of all the VAT due on its territory and for preventing evasion’.Footnote163 Such efficient tax collection for VAT can be achieved only if measures for administrative simplification are accepted—at least to some extent. If the Court imposes a duty on the Member States to ensure VAT collection, it should also allow them to use practical and feasible means to fulfil this duty.

If one applies this line of reasoning to the Credit Lyonnais case, there might be good arguments to justify the exclusion of output supplies conducted by foreign establishments when calculating the recovery ratio for input VAT deduction. A territorial recovery ratio is definitely much easier to manage for businesses and the financial authorities. A global recovery ratio would in many cases require complex evaluations and calculations to be carried out by the businesses and the financial authorities. As the Court continues to take into account the need for administrative simplification when evaluating the proportionality of discriminatory measures in other fields of law, an extension of this jurisprudence to the area of tax law—particularly to VAT—would also be consequent.Footnote164

5. Conclusion

In the Credit Lyonnais case the CJEU decided that the recovery ratio for services and goods used both for transactions for which input VAT deduction is allowed and for transactions for which input VAT deduction is not allowed as stipulated in Article 173 of the VAT Directive has to be calculated on a territorial basis. This interpretation leads to a different treatment of domestic and foreign branches and is, hence, questionable in the light of the freedom of establishment. Since the wording of Article 173 is doubtlessly open to more than one interpretation, the Court needs to take into account primary law and in particular the freedom of establishment when interpreting this provision. Although the compatibility with the freedoms was raised by the parties to the proceedings, the Court missed an opportunity to address and clarify the effects of the fundamental freedoms in VAT law.

Since the Court nevertheless implicitly accepts the restriction on the freedom of establishment to be in line with EU primary law, the judgment confirms the tendency of the Court to apply a more lenient standard when evaluating the effects of the fundamental freedoms on EU secondary law in general and the VAT Directive specifically. The Court did not disclose the arguments on which it relied when accepting the different treatment of domestic and foreign establishments to be in line with the internal market. The reasoning adopted by the CJEU in Credit Lyonnais, however, supports the view that the Court was either of the opinion that domestic and foreign establishments are not objectively comparable when it comes to input VAT deduction or that the different treatment was justified in the case by the need to safeguard the balanced allocation of taxing rights between Member States. Hence, the Credit Lyonnais case reveals that when ruling field of VAT, the CJEU may be attempting to follow the trend towards respecting tax borders, territoriality and tax sovereignty that it has developed in its recent direct tax jurisprudence. However, in the light of the different context applying in VAT, this reasoning is not coherent and, thus, not convincing. In contrast to direct tax law, the allocation of taxing rights between states is harmonised in EU VAT. This harmonised system based on the VAT Directive does not follow a territoriality principle and does also not implement a territorial approach as regards input VAT deduction.

Although the arguments relied on by the Court are worthy of criticism, the result achieved in the Credit Lyonnais case may still be reasonable. A global pro rata calculation taking into account all establishments worldwide would involve a lot of complexity and be administratively burdensome for businesses as well as tax authorities, which probably would also offset any neutrality benefits connected to it. Hence, the need to ensure the practicability and simplicity of the VAT system and tax collection might serve as a valid justification ground for a discriminatory treatment. Since VAT is linked to the EU budget and VAT collection has to cope with a huge number of taxpayers and assessments, in the author’s opinion this ‘new’ justification ground will gain importance in the CJEU case law in the area of VAT in future years, whether expressly or by implication.

The VAT Directive contains a vast number of provisions that establish a different—more burdensome—treatment for cross-border situations as compared to domestic situations.Footnote165 In the light of the jurisprudence so far and as highlighted by the Credit Lyonnais case, most of these provisions seem to be in line with the fundamental freedoms. Nevertheless, it would be interesting to see more cases going to the CJEU on the compatibility of secondary EU law with primary EU law. In the light of the BEPS project and the drive for harmonisation that it has prompted, the limits set by primary EU law on the EU legislature when enacting secondary law will be of increasing relevance in the coming years.

Acknowledgements

The author would like to thank Univ.-Prof. Dr. DDr. H. C. Michael Lang, Prof. Dr. Servatius van Thiel, and the two experts conducting the double-blind peer review for their valuable comments on the paper.

Disclosure statement

No potential conflict of interest was reported by the authors.

Notes

1 Council Directive 2006/112/EC on the common system of value added tax, L 347/1.

2 See, inter alia, Cases C-488/07, Royal Bank of Scotland, EU:C:2008:750, para 15; C-388/11, Crédit Lyonnais, EU:C:2013:541, para 27.

3 Cases C-108/14 and C-109/14, Larentia + Minerva, EU:C:2015:496, paras 26–27 and the case law cited. The determination of the methods for apportioning input VAT between economic and non-economic activities is at the discretion of the Member States, however, when exercising that discretion they must have regard to the aims and logic of the Directive (Cases C-437/06, Securenta, EU:C:2008:166, para 39; C-496/11, Portugal Telecom, EU:C:2012:557, para 42).

4 Case C-210/04, FCE Bank, EU:C:2006:196.

5 Cf Christian Amand, ‘VAT Grouping, FCE Bank and Force of Attraction—The Internal Market is Leaking’ (2007) International VAT Monitor 242; Casper Bjerreegaard Eskildsen, ‘Pro Rata Deduction by Entities Established in Several VAT Jurisdictions’ (2012) International VAT Monitor 28; Thomas Ecker, ‘VAT Deductions’ in Michael Lang & et al. (eds) ECJ – Recent Developments in Value Added Tax (Linde, 2014) 354–356; Sebastian Pfeiffer, ‘VAT grouping from a European Perspective’ IBFD online, Reviewed 31 July 2015, Section 10.4.4.3.2.1.

6 See in more detail Charlene Herbain, ‘The Journey of Branches into VAT Schizophrenia’ (2013) World Journal of VAT/GST Law 207; see also the examples mentioned by Amand (n 5).

7 Case C-388/11, Crédit Lyonnais, EU:C:2013:120, Opinion of AG Cruz Villalón.

8 Crédit Lyonnais (n 2) para 30.

9 Ibid, para 33.

10 Ibid, para 35.

11 Ibid, paras 37–38.

12 Ibid, para 39.

13 See on these provisions in more detail Section 4.4.1.3.

14 Herbain (n 6) 208; Ecker (n 5) 355.

15 FCE Bank (n 4).

16 See also the arguments by the taxpayer in Crédit Lyonnais (n 2), para 17; see in detail on this argument, Crédit Lyonnais, Opinion of AG Cruz Villalón (n 7), points 33–41.