ABSTRACT

Introduction:Research has shown the negative impacts of climate change on the economy and how the state of the environment has been a complex global challenge. Prior studies have suggested immediate actions to avoid any unforeseen circumstances for all living things on Earth. Previous research has also supported all kinds of sustainability efforts as resolutions to address the deterioration of climate change caused by business activities. Originality: There is a need for companies to start acting and assigning employees to mitigate carbon emitted by corporations. This study is motivated by the lack of empirical evidence that examines how corporate carbon governance influences better carbon performance of organizations and authorizes organizations to implement and embed carbon accounting. Objective: This study used evidence from Malaysia to explore this subject matter and examined the association between carbon governance and carbon performance of corporations. The research also investigated the mediation effect of carbon accounting with respect to carbon governance and carbon performance. Findings: It is revealed that carbon governance had no significant influence on an organization’s carbon performance although carbon accounting implementation positively influenced carbon performance. The findings imply that despite its insignificance, carbon accounting remains a vital matter to be deployed by organizations for better carbon emission mitigation.

Introduction

Although companies have primarily focused on financial performance in the past, accountability toward environmental impact is expected in lieu of the current climate crisis. For a few decades, both aspects of the international and local community have been struggling to discover an appropriate strategy for corporations to take responsibility to reduce greenhouse gases (GHGs) emissions, especially carbon dioxide (CO2). Carbon dioxide emissions are mainly contributed by industrial activities (Van Der Hoeven Citation2011). Hazardous impacts of climate change include deteriorating the environment and poor effects on the economy. As posited by Adedeji et al. (Citation2020), financial indicators are no longer measured by performance alone; hence, there is a need to implement balanced, non-financial measures for organizations to meet their strategic objectives. Boards of directors are now expected to assess and manage the impacts of climate change. Thus, integration of carbon governance in a corporate strategy should implement carbon accounting which should improve firm performances financially and environmentally. Nevertheless, there have been limited attempts to investigate how carbon governance could affect the carbon performance of corporations. Thus, this study explored the relationship between carbon governance and carbon performance by using carbon accounting as a mediator in Malaysian organizations. The worsening trend of CO2 emissions appears to have no immediate improvement. The sustainability efforts initiated currently have led to the perception that objectively measuring CO2 emissions is costly and complex, which causes corporate organizations to become skeptical of such efforts. The major challenge faced by organizations is that the immediate conversion of their activities into an advanced sustainable action in handling the organizations’ carbon footprint issues. Mainly when companies are by this time comfortable with the traditional management approach; habitual power usage inefficiency and organization hesitant toward sustainability cause the increase in CO2 that leads to the greenhouse effect. Besides the familiarity with traditional technology utilization, little is known about carbon accounting in Malaysia. Prior studies are prescriptive and focus mostly on one environmental management accounting tool or managerial aspect, as well as the impacts on the economic benefits. The consequences were that most Malaysian companies have no instant motivation to practice sustainability focusing on CO2 organizational matters. On the other hand, although these sustainability efforts are doubtful, and awareness of climate change is relatively low in Malaysia, carbon mitigation efforts are increasingly gaining dynamism.

Generally, it has been recorded that when an organization’s top management has higher awareness and concern for environmental wellbeing they are more likely to prioritize the company’s management of CO2. Based on a survey by Bakar et al. (Citation2017), 80% of the organizations studied were concerned about the negative impacts of carbon emissions on the environment. The top management must obtain the company’s complete carbon impact information so that it can support the carbon reduction and competitive strategy of an organization (Schaltegger and Csutora Citation2012). Boards of directors also are expected to consider the interests of various stakeholders. Shareholders tend to focus on economic returns on investment, but stakeholders that are not financially oriented may ask that more action is to be taken for environmental protection and social welfare. Within resource limitations, boards of directors must reconcile the conflicting interests of these two major groups (Luo and Tang Citation2020). According to legitimacy and stakeholder theories, firms with high-quality carbon governance tend to be more stakeholder-oriented and more aware of legitimacy issues arising from climate change and thus motivated to improve their carbon performance to meet societal expectations or various potentials.

Past studies have found a significant moderation effect on an environmental system and company performance. Many other studies were done by exploring the direct relationship between carbon strategy and financial performance such as Ganda (2017); Lee, (2012); Lewandowski, (2017); Yunus, Elijido-Ten, and Abhayawansa (Citation2016) but very few studies investigated the antecedents of carbon accounting system implementation and the role of carbon accounting as a mediator in the association between independent variables and dependent variables. A study conducted by Spencer et al. (2013) investigated the linkages between commitment by top management in environmental 76 sustainability and environmental performance with the implementation of a sophisticated environmental information system as a mediator. Solovida and Latan (2016) found a significant positive effect between environmental strategies through the use of Environmental Management Accounting (EMA) as a mediator in improving companies’ environmental performance. A study that investigates the mediation effects of carbon accounting is very scarce. Due to the scarcity and the gap, there is a need to examine the effects of carbon accounting system implementation as a mediator because instead of focusing on the external influences, a study should focus on organization definite influences such as strategy that could potentially encourage the adoption of carbon accounting and hence improve company’s performance.

Previous studies have found significant influences between carbon mitigation efforts and organizations’ performances; Gallego-Álvarez et al. (2015) investigated the carbon emission impacts on financial and operational performance. Likewise, Chakrabarty and Wang (2013) analyzed the linkages among the mitigation of carbon and financial performance. Meanwhile, Rokhmawati, Sathye, and Sathye (2015) investigated the effects of GHG emission, environmental, and social performance on financial performance. Based on the literature review, few studies have primarily concentrated on the impact of environmental strategies on a company’s financial performance; however, research that specifically examines the impact of corporate carbon strategies on carbon performance is exceedingly rare. Few studies have examined the effects of carbon performance on financial performance, such as studies by Lewandowski (2017) and Rahman, Rasid, and Basiruddin (2014). Therefore, there is an urge to firstly find out what is the manner of the companies in employing their carbon strategies, are they doing well with their carbon performance and how they ensure their carbon performance is 77 superior and under control, before they can see the superiority of carbon performance impacting on a better financial performance. The environmental performance of a corporation is a multidimensional construct. Its definitions and measurement methods are seemed to likely affect empirical results (Guenther & Hoppe, 2014). According to Guenther and Hoppe (2014), a corporate environmental performance that includes corporate carbon performance is measured based on these four ways; reporting scheme (Andrew & Cortese, 2011), emission scope (Lee, 2012), indicator specification (Hoffman & Busch, 2008), and perspective of measurement (Olson, 2010).

From an accounting perspective, carbon performance is mostly measured and results from corporate carbon emission data obtained through either voluntary or mandatory reporting. From another perspective, environmental engineering studies are correspondingly relevant to carbon performance as well. Engineering research has deeply discussed carbon emissions and carbon reduction efforts by integrating engineering tools to measure carbon performance, such as Building Information Modeling (BIM) or MyCREST in Malaysia (Ohueri et al., 2019). Besides BIM and MyCREST, an integrated carbon accounting and mitigation (INCAM) studied by Hashim, Ramlan, and Wang (Citation2017) is discussed under the engineering perspective instead of accounting. The research done in the engineering field discusses further carbon performance and its measurements using engineering tools, unlike carbon performance in accounting. Consequently, it is important to see how an organization’s carbon performance is discussed from an accounting perspective. Based on literature review, accounting research does discuss carbon performance, but its measurement by companies is still lacking and not comprehensively discussed based on accounting views compared to engineering research. Although considerable attention on carbon dioxide emissions has increased in the last decade, there is no indication of the existence of the management decision circumstances related to carbon accounting, which are particularly supported by academic and professional literature on carbon accounting (Zvezdov & Schaltegger, 2015). In the review of over 800 environmental management accounting publications, carbon accounting is acknowledged as one of the most debated subjects (Schaltegger, Gibassier, & Zvezdov, 2013). A review by Ascui (2014) and Stechemesser and Guenther (2012) on the wider area of carbon accounting delivered a comprehensive overview of the literature. Case studies conquered the extension of literature and evidence that various companies have discovered, if not much, some potential benefits of carbon accounting (Ascui & Lovell, 2012). Most of the carbon accounting research were not published under management accounting journal rather, several of carbon accounting studies were published under the Journal of Engineering, Journal of Environmental Science and Policy, Journal of Science and Technology, Journal of Applied Energy, Journal of Innovation and Strategy, and so on. A study by Ascui (2014) reveals that carbon management accounting has remained largely under-researched despite being highly discussed. In this study, parallel with the global literature on carbon accounting, carbon accounting research in Malaysia that discusses at an organizational level is under research. This situation leads to the weak theoretical foundation of carbon accounting in Malaysia, and the consequences of carbon accounting are still unclear and inconsistent.

Based on the highlighted issues, this study explored the relationship between carbon governance and carbon performance of Malaysian organizations with carbon accounting as the mediator. To address this issue, research questions raised were: (i) does carbon governance positively influence the implementation of carbon accounting?; (ii) does carbon accounting positively influence carbon performance?; and (iii) does carbon accounting mediate the relationship between carbon governance and carbon performance? Subsequently, these research objectives are to be achieved; (i) To explore the influence of carbon governance on the implementation of carbon accounting; (ii) To explore the influence of carbon accounting implementation on carbon performance, and (iii) to analyze the mediating effect of carbon accounting on the relationships between corporate carbon strategies and carbon performance. This study significantly provides further insights into the importance of having carbon governance in organizations as one of the organizational carbon strategies in support of the organizational CO2 emission mitigation effort. Furthermore, as carbon accounting serves as a mediator that mediates the relationship between carbon governance and carbon performance, this insight contributes to the richness of the management accounting literature in the context of carbon accounting implementation and sustainable development.

Background

Industrialization is the fundamental cause of CO2 emissions (Van Der Hoeven Citation2011), supported by a reluctance to adopt green technology and to maintain the usual business activities have driven CO2 levels to increase. Because of that, accountants are presumably able to help concerned organizations deal with organizational CO2 emissions by employing carbon accounting. As measuring, recording, and communicating are the accounting principles, carbon accounting refers to a process that facilitates carbon emission measurement and monitoring that will eventually motivate better performance. Thus, accountants play an important role in carbon accounting establishment and operation. Carbon accounting deals with professional responsibilities. Organizations must take action to help reduce greenhouse gas emissions because CO2 emissions mitigation is a massive task that requires extensively synchronized resolutions. Environmental degradation caused by carbon emissions affects business operations in every country and region across the globe. Thus, carbon accounting is needed in various aspects. Systematically, carbon accounting provides tools to quantify carbon emissions and help organizations make informed-decisions regarding mitigation strategies. The information generated from carbon accounting could enhance carbon performance superiority. Economically, provided with the right guidance, carbon accounting can simply help identify which business activities consume much energy, which is the starting point to help reduce the energy and resources used. This aspect signifies how carbon accounting assists organizations to attain a superior carbon performance and also proves that carbon accounting does improve carbon performance (Alrazi and Husin Citation2016). When a company has achieved an improved carbon performance, the carbon transparency verified will develop trust and loyalty among the stakeholders. Environmentally, carbon accounting implementation helps organizations become more environmentally mindful by taking carbon emissions and mitigation efforts into their accounts. This move fundamentally creates a real change that contributes to the achievement of Sustainable Development Goals (SDG).

Unfortunately, most of the economic production forms will continue to contribute to pollution. Transforming conventional customs and behaviors that are detrimental to the environment into more environmentally friendly approaches requires a substantial understanding of its surroundings and influences (Daud, Mohamed, and Abas Citation2015). Thus, in implementing carbon accounting practices in organizations, companies must understand the need to mitigate a company’s CO2 emissions; as well as the factors that influence a certain amount of emissions. From a carbon accounting practice perspective, a company needs necessary internal mechanisms such as carbon governance to support the implementation of a carbon mitigation system. According to Motzer (Citation2020), there are few ways to achieve successful corporate carbon performance and reporting; firstly, to define carbon accounting boundaries to concentrate on and which part of business activities that significantly emit CO2. Secondly, to determine the consumption values, especially when robust energy consumption values are fundamental for reliable measurement and calculation of CO2 emissions. Carbon accounting, therefore, plays a vital role in measuring reliable values of CO2 emissions. Thirdly, to develop appropriate carbon strategies (as such carbon governance) according to the organization’s needs. Besides the importance of CO2 emissions’ hard facts and figures, companies’ CO2 emission mitigation or environmental efforts shall also be reflected in the corporate strategy that they have embedded. Therefore, this study appropriately focuses on the context of carbon governance and carbon performance with the support of carbon accounting that these threefold-variables have become critical in the current business sphere, especially when they are basically interdependent.

Theoretical literature review

Resource-based theory

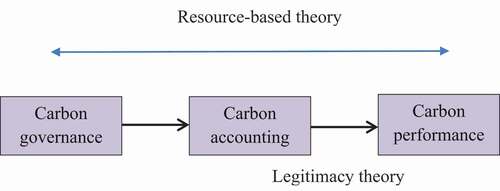

The resource-based view (RBV) of a company and the resultant resource-based theory (RBT) provides essential contexts in explaining and predicting the company’s competitive advantage basis and performance (Barney, Ketchen, and Wright Citation2011). The Resource-based View (RBV) theory is an important idea in strategy as it suggests the potential to explain sustained competitive advantage, which is the process of delivering long-run abnormal returns to shareholders (Toms and Carter Citation2010). RBV perspective highlights the superiority of performance generated from organizational ability to create a valuable strategy that allows the utilization of unique corporate resources and capabilities (Wahyuni and Ratnatunga Citation2015). Therefore, RBT theory is the overarching theory that covers and explains the whole strategy-system-performance framework of this study and is parallel in the context of this study where carbon accounting practice or its system is considered as a new resource of a company which by implying resource-based theory (RBT), it highlights how these intangible resources and capabilities could improve company’s performance.

The resource-based theory explains the relationship between carbon governance and carbon accounting that each company differs in terms of operations and resources. As a result, by having carbon accounting system, company is considered as distinct from others in terms of operation.

Legitimacy theory

Legitimacy theory emphasizes that organizations constantly attempt to be assumed as operating within the norms and values of their respective societies. Particularly, organizations strive to be viewed by external parties or stakeholders as being legitimate. Hence, legitimacy theory reflects on how a company should act responsibly in addressing societal concerns. According to Deegan (Citation2002), the legitimacy theory suggests that a corporation complies to disclosures to attain expectations from the community and it recognizes the fact that organizations are tied to the social contract in which they decide to perform within the norms of their respective societies, and suggests that organizations disclose their environmental activities as a legitimate way to meet societal expectations and thus to gain or maintain their legitimacy (Kalu, Buang, and Aliagha Citation2016). According to Ghomi and Leung (Citation2013), legitimacy is a resource needed by companies to survive. Legitimacy is a dynamic resource that continuously evolves. In this study, legitimacy theory suggests that as companies are supposed to be under more scrutiny regarding carbon footprint emissions, companies need to contribute in terms of producing carbon performance to legitimize operations. At the same time, they are aware of and use the government’s carbon initiatives due to the social pressure on companies, hence leading increases in companies’ involvement in carbon alleviation through disclosure of voluntary carbon and carbon performance. The legitimacy theory explains the relationship between carbon accounting and carbon performance as legitimacy theory supports the disclosure of organizational environmental acts to legitimize the organizational behavior.

Based on the research framework presented in , carbon governance is the independent variable, carbon accounting is the mediator and carbon performance is the dependent variable.

Figure 1. Research framework

Carbon governance

Carbon governance is an organizational management capability that is concerned with a company’s involvement in carbon activities and how the risks and opportunities relate to carbon mitigation, how they are dealt with, and the resulting governance mechanisms (Tang and Luo Citation2014). Legitimacy and stakeholder theories emphasize that good governance structures are effective in protecting the interests of multiple stakeholders in which can impact the corporate environmental performance positively (Nguyen et al. Citation2021). Very little is known about these forms of governance, not just in the carbon accounting field, but also in broader accounting areas (Bebbington, Kirk, and Larrinaga Citation2012). Organizational involvement that aims to educate the company’s workforce about carbon emissions or efforts to mitigate climate change is called carbon governance. Similar to corporate governance that acts as the monitoring mechanism to ensure that an entity has proper checks and controls in place (Ong et al. Citation2019), carbon governance acts as a corporation’s mechanism to monitor carbon emissions. Carbon governance involves organizational carbon involvement, aiming for the participation and cooperation of the whole workforce in the struggle to mitigate climate change (Tang and Luo Citation2014). Thus, carbon governance in this study refers to the combination of the top management roles and the employees’ involvement in carbon accounting matters as a whole (generally refers to as organizational involvement); it shows that it is crucial for everyone in an organization to play their part and show collaborative efforts in making the strategies successful.

Carbon governance consists of strategies that make the top management accountable and engaged in a subject matter. Carbon governance is directed at decision-makers in an organization, usually those in the position to convince the organization to choose an appropriate setting that will comply with operations on a long-term duration. Top management and strategic management might need a company’s carbon impact information that is fairly aggregated and could support the reduction of CO2 and competitive strategy of organizations (Schaltegger and Csutora Citation2012). Depending on diverse organizational levels, a company can assign accountability roles and responsibilities to staff. Consequently, the knowledge and awareness of climate change may be distributed to all employees at all levels, promoting a climate-friendly culture. Companies can also offer monetary or non-monetary incentives in their efforts to engage all staff in the process of carbon emission reduction (Backman, Verbeke, and Schulz Citation2015). Moreover, when a company assigns carbon emission responsibility to employees of different levels, it allows the top management to obtain carbon information and measure carbon emissions for each part of the company. Most companies utilize carbon information and predict the range of emissions in the whole organization to gain operationalization efficiency. This is paralleled with the findings that claim that when members of top management are consistently involved and have extra awareness of risks and opportunities related to climate change, they tend to participate in more activities that increase competitive advantages (Damert, Paul, and Baumgartner Citation2017).

Carbon performance

Carbon performance reduces the absolute amount of discharges into the environment (an absolute reduction of greenhouse gas (GHG) emissions) and improves efficiencies or intensities by reducing emissions per kilogram of product or functional unit of a company (Schaltegger and Csutora Citation2012). Carbon performance is extremely hard to measure because it is a new area in the accounting industry, and it involves the association between climate change science and professional accounting practice (Gibassier and Schaltegger Citation2015). A few studies have explicitly examined governance characteristics that are dedicated to climate governance. These include the level of management responsibility for climate change issues, frequency, and time horizon of risk reporting at the board of directors’ level, and the presence of executive incentives linked to carbon performance (Bui, Houqe, and Zaman Citation2019). Currently, the carbon performance reports by the board of directors are ambiguous and thus make it difficult to come up with carbon-related decisions.

However, the incorporation of climate change issues at the board level strongly indicates an organization’s commitment to addressing climate change. An indication of this commitment is whether boards monitor carbon emissions and carbon performance (Prado-Lorenzo and Garcia-Sanchez Citation2010). Carbon disclosure (the report of carbon performance to third parties) is more aligned under intense carbon performance conditions. Under the guidance of the board, high-performing companies tend to disclose more CO2 information to signal strong performance and differentiate themselves from other companies (Qian and Schaltegger Citation2017). This is because robust climate governance indicates heightened concern about climate change issues and discloses truthful carbon performance to shareholders and stakeholders, so they are not misled by the carbon information provided (Bui, Houqe, and Zaman Citation2019). Despite the notable climate-related regulations and initiatives, it can be seen clearly that there is a lack of progress in designing and enforcing firm-specific policies and guidelines that can help policymakers to observe not only process-oriented carbon performance but also the actual carbon performance at a firm-level (Haque and Ntim Citation2020). Since board members oversee disclosure policies, it can be expected that when the management provides extensive disclosure, it would mean its successful contribution to the organization’s good carbon performance which in turn would reduce carbon in organizations with strong climate governance (Alrazi, De Villiers, and Van Staden Citation2015)

Carbon accounting

In general, the greenhouse gas accounting concept could be used for accounts that include various greenhouse gases; only when carbon dioxide emissions are mentioned, and carbon accounting is used (Schaltegger and Csutora Citation2012). The importance of carbon accounting is that many disciplines are obliged to work together to solve these complex sustainability problems, particularly corporate CO2 emissions. The main purpose of carbon accounting was to mitigate carbon footprints by measuring and monitoring a company’s carbon emission level in which carbon accounting principally focuses on carbon emissions (Gibassier and Schaltegger Citation2015). Even though carbon footprint mitigation must be a company’s principal concern, the first proactive mitigation action must be by managers. Thus, for the realistic reduction of carbon, the use of carbon accounting may substantially help managers make the right decisions for organizations. There is a need for an internal and external supporting mechanism to develop an accounting system that captures and copes with climate change issues.

Regarding carbon-related accounting, a company needs necessary internal mechanisms to create such a system. These internal mechanisms include financial and non-financial resources such as the organization’s management systems, organizational leadership, and governance. In this study, a carbon accounting or carbon accounting system that captures carbon-related information generated from a corporate carbon strategy is considered the link between corporate carbon strategies (carbon governance) and corporate carbon performance. Appropriate integration of carbon accounting is needed in a company to manage its carbon strategies properly, and a further link to the organizational goals, which are carbon performance and reduction. In the absence of an appropriate integration of carbon accounting, the measurement of carbon performance might be inaccurate.

Empirical literature review and hypotheses development

Corporate governance is used as the monitoring instrument to ensure checks and controls are properly in position. Corporate governance encourages fairness, accountability, and transparency within an entity (Parul et al. Citation2017). Thus, companies with good corporate governance may enjoy a better corporate image and earn shareholders’ trust. With a better corporate image and increased confidence, companies would gain better access to scarce and limited resources and funds which in turn provides companies with improved growth and the ability to continue operations. Similarly, it also applies to carbon governance, where it acts as the monitoring mechanism to ensure proper monitoring and control over carbon footprint matters. A further study by Yunus, Elijido-Ten, and Abhayawansa (Citation2016) observed the influential decision factors that were used to adopt carbon management strategies within companies. It was found that the existence and implementation of an environmental management system in an organization; comprising an environmental committee, board size, and board independence; significantly and positively impacted a company’s decision to adopt a carbon management strategy. Likewise, Larrinaga (Citation2014) posited that the fundamental rationale is based on prescriptive forms of carbon governance where companies would be more accountable for carbon emissions. The use of resource-based logic is directed toward understanding why some firms persistently outperformed others in terms of carbon performance, which in turn led to competitive advantage. Therefore, underpinned by the resource-based theory that considers distinct organizational operations and resources, the following hypothesis (H) was proposed:

H1: Carbon governance positively influences the implementation of carbon accounting.

By highlighting the close interplay between environmental management accounting and environmental performance the belief that is strengthened in this study is that when carbon accounting, also known as a carbon accounting system, is implemented by an organization it significantly improves a company’s carbon performance. The association between carbon accounting and carbon performance research remains scarce, especially from the Malaysian perspective. Tang and Luo (Citation2014) study is the only study that empirically examined the relationship between carbon accounting system and carbon emission mitigation adopted by an organization. The study confirmed a positive correlation between carbon accounting systems and carbon mitigation variables based on the findings. However, the study did not pay attention to the carbon accounting system’s features in collecting and processing financial and environmental information for internal management. In this study, the relationship between carbon accounting and an organization’s carbon performance is associated with the legitimacy theory that proposes an organization’s behavior should be concerned with the values and beliefs of the social paradigm within which the organization operates (Suchman Citation1995). Consequently, a company tends to disclose information regarding its carbon emissions to legitimize the organization’s actions and behaviors. Given the strategic significance of carbon accounting implementation in carbon-sensitive organizations, this issue should be appropriately addressed and investigated. Therefore, owing to that purpose, underpinned by the legitimacy theory, the following hypothesis was developed:

H2: Implementation of carbon accounting positively influences carbon performance.

The board’s function in establishing carbon governance is to ensure a sound carbon policy and provide insights regarding carbon accounting implementation. Carbon accounting is one of the board of directors’ responsibilities as they have the power to develop the overall carbon strategy, deploy carbon accounting, and prioritize carbon actions in mitigating emissions and generating superior carbon performance. Nevertheless, it cannot be presumed that carbon accounting and accountability are always consistent with the objectives of an organization. Due to the possible conflicts between organizational objectives and carbon accounting implementation, constant tension will happen between carbon management and the existing organizational culture where profit – usually becomes the prime objective (Tang Citation2014). However, decision-making needs to involve the participation of top-level carbon accounting. It is principally useful when the degree of uncertainty is high, and the stakeholders show inconsistent concern. Therefore, reinforced by resource-based theory literature and stakeholder theory, the following hypothesis was proposed:

H3: Carbon accounting mediates the relationship between carbon governance and carbon performance.

Research design and methodology

The research purpose is descriptive as it gains a precise profile of events, persons, or situations. The research strategy was via a questionnaire survey that was related to the deductive research approach. The questionnaire is appropriate as it used standardized data collection from a sizable population in a highly economical way, allowing easy comparison. The research population comprised Standard and Industrial Research Institute of Malaysia (SIRIM) International Organization for Standardization (ISO) 14,001 certified companies in Malaysia. This research adopted the census sampling method and considering the entire population of all 586 ISO 14,001 certified Malaysian companies granted by SIRIM. The research instrument and the structured questionnaire mostly included rating questions where the Likert-style rating was frequently used (Saunders, Lewis, and Thornhill Citation2016). Questionnaire items were adapted from the past and relevant carbon strategy and carbon accounting research, but some questions were altered to fit this research’s objectives adequately. Questionnaires used to collect data probability dictated that the respondents would either respond or refuse to respond to the questionnaires given; thus, the sample size was affected by the choice of the statistical analysis method. Using the census sampling method, which considers the total number of companies in the population, a total of 136 valid survey questionnaires (response rate of 23.2%) were used for data analysis. presents the useable questionnaires for data analysis;

Table 1. Useable Questionnaires

Hair et al. (Citation2010) indicated that structural equation modeling (SEM) results tend to be sensitive to sample size, and suggested that a minimum of 100 and a maximum of 200 cases should be presented for SEM analysis. Model assessments are subjected to partial least square-structural equation modeling (PLS-SEM) analysis, where the structural model (inner model) is assessed by a modeling path via Smart PLS version 3.2.7.

Diverse multivariate inferential data analysis methods have been used in accounting research to test model fitness and hypotheses developed in this research include partial correlations, linear regression, SEM, and PLS. SEM is convenient for testing and developing theories containing multiple equations, encompassing dependent associations where a hypothesized dependent variable becomes an independent variable in a subsequent dependent relationship (Hair et al. Citation2010). One of the SEM characteristics is that it includes both measurement and structural models. The model measurement determines correlations between observed and latent variables, while the structural model tests the correlations between latent variables and incorporated and identified measurement error variances. Structure equation models (SEMs) convey flexibility in testing the model and tolerate the use of multiple predictors and criterion variables, construct latent (unobservable) variables, observe variables model errors in measurement, and test mediation and moderation relationships in a single model (Hair et al. Citation2010). Denscombe (Citation2014) contended that the validity of quantitative research could be assured in the accuracy of causal relationships and interpretations between variables through PLS-SEM analysis.

The structural model assesses the predictive capability of the model and the linkages between constructs specified by the underpinning theory. According to Hair et al. (Citation2014), the structural model in PLS-SEM is measured based on experiential criteria determined by the model’s predictive capabilities. The complete bootstrapping procedure with 5000 sub-samples via PLS-SEM analysis was executed to determine the significance level of hypothesized paths. It can be used to compute a standard error of each model parameter. Depicted on the standard error, the significance of each parameter can be determined using t-values. The bootstrapping procedure executed given the statistical objective of PLS-SEM is to show the significance of the structural model relationships. Bootstrapping is a non-parametric method for assessing the path coefficient precision, and the procedure generates standard errors and t-values for investigating the statistical significance of the path coefficients (Hair, Ringle, and Sarstedt Citation2011). The β values, commonly in the range between 0.20 and 0.30 are considered significant. The empirical t-value needs to be significant at a certain confidence level (P-value) to support the hypothesized relationship, or it may be otherwise. Parameters with the presence of t-value greater than 1.96 indicate 95% confidence level (p < 0.05) and with t-value greater than 2.58 indicate 99% confidence level (p < 0.01) (Hair et al. Citation2014).

Empirical results and discussion

shows the demographic profiles of companies selected for this study. As discussed earlier, there were 136 companies selected. Companies between the ages of 21 to 40 represented the most with 67.7% (n = 92). Furthermore, small and medium-sized companies stood out the most with 69% (n = 69). Among the industrial sectors studied, other sectors showed the highest percentage (n = 31, 22.8%) where the respondents stated engineering, technology, transportation and automotive, finance, manufacturing, infrastructure, commercial, materials, consulting, operation and maintenance, authority, and government agencies. Among the observations studied, 94 companies (69.1%) were local and stood out the most in terms of the companies’ ownership. As for the sampled companies’ emission scope, companies with scope 1 emissions (all direct emissions) displayed the highest rank with 50% (n = 68) in this study.

Table 2. Demographic profiles

Findings in show the path of carbon governance (CG) and carbon accounting (CA) (CG > CA), whereby carbon governance had no effects on carbon accounting (standardized β = 0.053, p > 0.05). This proved that H1 is unsupported. Contrary to the prediction, carbon governance did not play a role as a strategy in implementing carbon accounting in organizations. The non-significant result is consistent with the study by Damert, Paul, and Baumgartner (Citation2017), where they found that carbon governance did not affect carbon reduction activities.

Table 3. Direct path coefficient result

Little is known about the form of governance in carbon accounting, and it is recommended that companies follow prescriptive forms of carbon governance, where they would be made more accountable for the usage of carbon (Larrinaga Citation2014). The literature has done little to comprehend the role of governance in CO2 emissions (Abid Citation2016). Few studies have explicitly examined the characteristics of governance committed to climate governance (Bui, Houqe, and Zaman Citation2019). Nevertheless, in terms of carbon accounting implementation, the non-significant result showed that the benefits of carbon governance did not produce the expected achievement.

When the board establishes carbon governance, it is anticipated that carbon accounting is securely implemented, thus ensuring a sound carbon policy. There is no doubt that the board of directors of an organization has the ultimate responsibility and influence to develop carbon strategies, and set carbon reduction targets. The board of directors also help to establish a carbon policy and abide by it, utilize specific necessary resources, and prioritize the importance of carbon emission mitigation. Overall, it can be said that good carbon governance is supposed to sustain the use of resources through carbon accounting and strategies, oversee CA implementation, support, and prioritize CO2 mitigation.

Governance is a proxy for voice and accountability, government effectiveness, the rule of law, and regulatory authority, and all are measured in a percentile rank (Abid Citation2016). However, in this context, carbon accounting as an accounting system is independent of carbon governance as a strategy. It is believed that an effective accounting system is able to segregate the carbon governance and performance. Economic benefits are definite priorities for organizations, so when carbon governance becomes operational, carbon management may disrupt the main organizational objectives. This may place pressure on organizational and managerial culture since carbon resources may interfere with the main objective of profitability and a company becomes ambivalent toward carbon accounting. Besides, the insignificant results show that Malaysia’s carbon governance does not play a crucial role in mitigating and controlling companies’ carbon activities. Although carbon accounting could help the board enforce carbon strategies, the findings of this study revealed that carbon governance is unlikely to influence the implementation of carbon accounting.

Subsequently, the direct path of carbon accounting (CA) and carbon performance (CP) (CA > CP) shows that carbon accounting has a significant positive effect on carbon performance (standardized β = 0.751, p < 0.01). Thus, H2 is supported. The crucial component of carbon accounting is the determination of carbon performance (Hashim, Ramlan, and Wang Citation2017). This finding is consistent with the statement that the focal point of carbon accounting is to determine its carbon performance. This could be due to the organization’s effort to implement carbon accounting at the organization’s strategic level leading to superior carbon performance.

In the current situation, CO2 is not only threatening the environment but companies too because companies are subjected to the risks of penalty or legal fines due to improper CO2 management. Thus, when companies apply carbon accounting to strategy ways to reduce CO2 they are more likely to gain improved carbon performance. Intrinsically, carbon performance might be strengthened and improved by implementing carbon accounting. Carbon accounting is indeed advantageous in providing accurate CO2 information via measuring and monitoring processes and, by achieving reduction targets and motivating better performances.

Depending on an organization’s CO2 reduction practices, there are many ways corporations can assess carbon performance; also, by assessing carbon performance a company shows its commitment to environmental issues. If companies improve their carbon performance, perceptively, it could reduce the industry carbon emission index (CEI), promote cleaner production, reduce carbon footprints of the industry, and generate goodwill by demonstrating their CO2 reduction efforts. These significant findings between carbon accounting and carbon performance prove that improved carbon accounting could drive better corporate carbon performance. Furthermore, it is necessary to improve carbon performance that responds to various stakeholders’ needs and further create transparency for stakeholders who require legitimate information to compare corporate performances between companies over time. presents the paths, the hypotheses, and the results of standard beta (β) and the effect size (f2) that measures the impact of CG and CA as exogenous constructs on CA and CP endogenous constructs accordingly.

Table 4. Direct effect path coefficient assessment

R2 is a measure of predictive accuracy, and its magnitude explains an effective combination of exogenous latent variables in each specific endogenous variable and is calculated as squared correlation (Hair et al. Citation2014). R2 results are generated from the complete bootstrapping procedure based on 5,000 sub-samples. The value of R2 ranges from 0 to 1, where a higher value indicates greater and better predictive accuracy. The results in indicate that the model’s predictive accuracy (R2) for the model in this study was substantial.

Table 5. Coefficient of determination (R2)

Effect size (f2) is the measure of the impact of a specific exogenous construct on an endogenous construct. It is an assessment of R 2 magnitude changes when a specific exogenous construct is omitted from the model. shows the result of effect size (f2) and reports that the exogenous paths to endogenous constructs are small and medium f2.

Table 6. Effect size (f2)

The predictive relevance (Q2) measured by the Stone-Geisser Q2 value is an addition to estimating the magnitude of predictive accuracy (R2) and calculated through a blindfolding procedure in PLS-SEM for endogenous variables with reflective scales. The Q2 represents a criterion for evaluation of the cross-validated predictive relevance of the PLS path model to assess the quality of the model. The values of Q2 range within 0 to 1 and a value greater than zero (Q2 > 0) indicates the predictive relevance of exogenous latent variables for the endogenous latent variables in the model (Hair et al. Citation2014). shows the blindfolding results of Q2 presented with the values of endogenous latent variables; carbon accounting (Q2 = 0.594), carbon governance (Q2 = 0.368), and carbon performance (Q2 = 0.549).

Table 7. The level of Q2.

Based on the mediation analysis presented in , carbon accounting mediates the relationship between carbon governance and carbon accounting. Carbon accounting functions as a complete mediator comparable to a catalyst that operationalizes carbon strategies and actualizes better carbon performance in a company. Nonetheless, the findings show that there is no mediation effect on carbon governance, carbon accounting, and carbon performance (CG > CA > CP), with (standardized β = 0.040, p > 0.1). Thus, H3 is unsupported. This was consistent with Larrinaga’s (Citation2014) that stated that there was nothing that could prove the formation of governance in carbon accounting. This study’s findings showed that carbon accounting performed as a weak mediator between carbon governance and carbon performance.

Table 8. Mediation analysis results

The effectiveness of carbon governance in mitigating carbon emissions depends on the governance characteristics such as CO2 emissions, extra concern about the impacts on companies and the environment, and being proactive in practicing green initiatives. The board of directors is expected to successfully manage and supervise the management team to improve the long-term values of a company because strong carbon governance shows assertiveness in carbon management. On the contrary, the results revealed that carbon accounting was unlikely to support carbon governance as a strategy to improve carbon performance. This might be due to internal organizational conflict of interests, such as the desire to make a profit, or a company’s lack of commitment to reducing carbon. These issues affect the decision to fully implement carbon accounting. Thus, carbon accounting does not become the enabler of carbon governance’s role in enhancing and improving carbon performance. The insignificant mediation effect on this relationship might also be affected by the insignificance of direct relations (CG > CA). presents the paths, the hypothesis, and the results of standard beta (β) and the effect size (f2) that measures the impact of CG constructs on CA and CP constructs.

Table 9. Mediation path coefficient assessments

Summary and discussion

For the direct relationship, the findings indicated that contrary to the prediction, carbon governance was found non-significant to carbon accounting, indicating that carbon governance did not influence the implementation of carbon accounting in a firm. Conversely, the direct relationship between carbon accounting and carbon performance showed significant results.

As for the mediation effect of carbon accounting, the relationship between carbon governance and carbon performance showed non-significant results, whereby carbon accounting exerted a full mediation effect on the relationship. The findings are in contrast to the prediction, in the relationship between carbon governance and carbon performance; the non-significant results indicated that carbon accounting did not exert its mediation effect on this relationship. Furthermore, this means that carbon accounting did not support the operationalization role of carbon governance in improving carbon performance. Nonetheless, this study offered insight into management practices, particularly to ISO 14,001 certified companies and other companies that utilize environmental management systems. Companies should strategically structure their carbon management in their organizational practices since carbon strategies develop a readiness to implement carbon accounting. This in turn helps to create better carbon performance of an organization, where managers are mindful of carbon reduction practices. Supported by these findings, this study provides empirical proof and a fundamental understanding of carbon accounting in Malaysia.

The operationalization aspect of carbon accounting in organizations must be fully understood at the managerial level. Employees expect managers to understand the basics of carbon accounting and hence seize opportunities to improve carbon capabilities and performance. When managers are equipped with knowledge and understanding of carbon accounting they readily guide their employees. They can point out carbon presence, organizational responsibility, and the importance of carbon accounting in organizations, and encourage the involvement of the whole organization to be aware of carbon issues and target environmental improvement.

Furthermore, ISO 14,001 EMS-certified companies should understand the importance of a carbon accounting manager rather than just a general manager, especially when organizational carbon matters certainly need to be handled by an expert. Based on the survey responses, only a few surveys were answered by respondents with specific carbon or GHGs background. Accordingly, having a carbon accounting manager who possesses the ability to recognize carbon issues in the company could probably bridge the gap through strategic carbon responsiveness, commitment, and motivation. In conclusion, this study filled the gap in the literature by explaining carbon accounting consequences in Malaysian companies and clarifying the need to successfully implement carbon accounting.

Additionally, an identified limitation of this study is that it did not investigate organizations’ culture and whether they are carbon-emissions conscious or whether green-culture had been embedded and adapted into the company. One of the factors that encourage companies to be environmental-friendly and sustainability-based comes from within a company. The same level of intrinsic motivation is needed from companies to practice carbon-related strategies, systems, and performances. As posited by Renwick, Redman, and Maguire (Citation2013), organizational culture is among the top motivational factors that support environmental management and enhance environmental performance. Thus, there is a need to integrate sustainability and carbon-conscious culture in organizations to initiate, facilitate, and sustain the practice of carbon accounting in firms. Therefore, future studies should investigate whether green culture is already embedded in organizations since green culture awareness in organizations determines the extent of CO2 mitigation. Organizational culture is one of the motivational factors that support and encourage companies to practice carbon accounting and continuously mitigate CO2. Thus, culture should be investigated in future studies as it influences companies to practice sustainability. Future studies should also include different contexts based on different countries, regions, cultural backgrounds, environmental forces, and economic stances.

Acknowledgments

This work was supported by the Grant number 6303806-10601 (SPE/UPM) and FRGS/1/2020/SS01/MMU/02/4.

Disclosure Statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abid, M. 2016. “Impact of Economic, Financial, and Institutional Factors on CO2 Emissions: Evidence from Sub-Saharan Africa Economies.” Utilities Policy 1–13. doi:https://doi.org/10.1016/j.jup.2016.06.009.

- Adedeji, B. S., T. S. Ong, M. U. H. Uzir, and A. B. A. Hamid. 2020. “Corporate Governance and Performance of Medium-sized Fi Rms in Nigeria: Does Sustainability Initiative Matter?” Corporate Governance: The International Journal of Business in Society 20 (3): 401–427. doi:https://doi.org/10.1108/CG-09-2019-0291.

- Alrazi, B., C. De Villiers, and C. J. Van Staden. 2015. “A Comprehensive Literature Review On, and the Construction of A Framework For, Environmental Legitimacy, Accountability and Proactivity.” Journal of Cleaner Production 102: 44–57. doi:https://doi.org/10.1016/j.jclepro.2015.05.022.

- Alrazi, B., and N. M. Husin. 2016. “Institutional Governance Framework for Determining Carbon-related Accounting Practices: An Exploratory Study of Electricity Generating Companies in Malaysia.” IOP Conference Series: Earth and Environmental Science 32 (1). doi:https://doi.org/10.1088/1755-1315/32/1/012063.

- Backman, C. A., A. Verbeke, and R. A. Schulz. 2015. “The Drivers of Corporate Climate Change Strategies and Public Policy : A New Resource-Based View Perspective.” Business and Society 1–31. doi:https://doi.org/10.1177/0007650315578450.

- Bakar, N. A., H. Abdullah, F. W. Ibrahim, and M. R. M. Jali. 2017. “Green Economy: Evaluation of Malaysian Company Environmental Sustainability.” International Journal of Energy Economics and Policy 7 (2): 139–143. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85017648231&partnerID=40&md5=7c9713dd6d545154d7f06dc2c128ea2f

- Barney, J. B., D. J. Ketchen, and M. Wright. 2011. “The Future of Resource-based Theory: Revitalization or Decline?” Journal of Management 37 (5): 1299–1315. doi:https://doi.org/10.1177/0149206310391805.

- Bebbington, J., E. A. Kirk, and C. Larrinaga. 2012. “The Production of Normativity: A Comparison of Reporting Regimes in Spain and the UK.” Accounting, Organizations and Society 37 (2): 78–94. doi:https://doi.org/10.1016/j.aos.2012.01.001.

- Bui, B., M. N. Houqe, and M. Zaman. 2019. “Climate Governance Effects on Carbon Disclosure and Performance.” The British Accounting Review 52 (2): 100880. doi:https://doi.org/10.1016/j.bar.2019.100880.

- Damert, M., A. Paul, and R. J. Baumgartner. 2017. “Exploring the Determinants and Long-term Performance Outcomes of Corporate Carbon Strategies.” Journal of Cleaner Production 160: 123–138. doi:https://doi.org/10.1016/j.jclepro.2017.03.206.

- Daud, Z. M., N. Mohamed, and N. Abas. 2015. “Public Knowledge of Climate Change: Malaysia‘s Perspective.” The 2nd International Conference on Human Capital and Knowledge Management. KL, Malaysia. 11/2/105-13/2/2015

- Deegan, C. 2002. “Introduction: The Legitimising Effect of Social and Environmental Disclosures - a Theoretical Foundation.” Accounting, Auditing & Accountability Journal 15 (3): 282–311. doi:https://doi.org/10.1108/09513570210435852.

- Denscombe, M. 2014. The Good Research Guide: For Small-scale Social Research Projects. 5th ed. Maindenhead: Open University Press.

- Ghomi, Z. B., and P. Leung. 2013. “An Empirical Analysis of the Determinants of Greenhouse Gas Voluntary Disclosure in Australia.” Accounting and Finance Research 2 (1): 110–127. doi:https://doi.org/10.5430/afr.v2n1p110.

- Gibassier, D., and S. Schaltegger. 2015. “Carbon Management Accounting and Reporting in Practice.” Sustainability Accounting, Management and Policy Journal 6 (3): 340–365. doi:https://doi.org/10.1108/SAMPJ-02-2015-0014.

- Hair, J., T. Hult, C. Ringle, and M. Sarstedt. 2014. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). Thousand Oaks, CA: Sage Publications.

- Hair, J. F., W. C. Black, B. J. Babin, and R. E. Anderson. 2010. Multivariate Data Analysis. 7th ed. Upper Saddle River: Prentice Hall.

- Hair, J. F., C. M. Ringle, and M. Sarstedt. 2011. “PLS-SEM: Indeed a Silver Bullet.” Journal of Marketing Theory and Practice 19 (2): 139–152. doi:https://doi.org/10.2753/MTP1069-6679190202.

- Haque, Faizul, and Collins G. Ntim. 2020. “Executive compensation, sustainable compensation policy, carbon performance and market value.” British Journal of Management 31, no. 3: 525-546.

- Hashim, H., M. R. Ramlan, and Y. C. Wang. 2017. “A New Framework for Carbon Accounting and Mitigation for Greening the Industry.” Malaysia Sustainable Cities Program, Working Paper Series, 1–18.

- Kalu, J. U., A. Buang, and G. U. Aliagha. 2016. “Determinants of Voluntary Carbon Disclosure in the Corporate Real Estate Sector of Malaysia.” Journal of Environmental Management 182: 519–524. doi:https://doi.org/10.1016/j.jenvman.2016.08.011.

- Larrinaga, C. 2014. “Carbon Accounting and Carbon Governance.” Social and Environmental Accountability Journal 34 (1): 1–5. doi:https://doi.org/10.1080/0969160X.2014.889788.

- Luo, L., and Q. Tang. 2020. “Corporate Governance and Carbon Performance: Role of Carbon Strategy and Awareness of Climate Risk.” Accounting & Finance 1–44. doi:https://doi.org/10.1111/acfi.12687.

- Motzer, T. 2020. “Five Steps to Successful Corporate Carbon Footprint and CDP Reporting.” https://sphera.com/blog/5-steps-to-successful-corporate-carbon-footprint-and-cdp-reporting/

- Nguyen, Thi HH, Mohamed H. Elmagrhi, Collins G. Ntim, and Yue Wu. 2021. “Environmental performance, sustainability, governance and financial performance: Evidence from heavily polluting industries in China.” Business Strategy and the Environment.

- Ong, T. S., Y. H. Ng, B. H. Teh, N. F. Kasbun, and J. H. Kwan. 2019. “The Relationship between Corporate Governance Attributes and Environmental Disclosure Quality of Malaysian Public Listed Companies.” Asian Journal of Accounting and Governance 12: 1–12.

- Parul, K., K. Neha, K. G. Sunil, and R. K. Sharma. 2017. “Impact of Corporate Governance and Financial Parameters on Profitability of the BSE 100 Companies.” The IUP Journal of Corporate Governance 16 (1): 7–26.

- Prado-Lorenzo, J. M., and I. M. Garcia-Sanchez. 2010. “The Role of the Board of Directors in Disseminating Relevant Information on Greenhouse Gases.” Journal of Business Ethics 97 (3): 391–424. doi:https://doi.org/10.1007/s10551-010-0515-0.

- Qian, W., and S. Schaltegger. 2017. “Revisiting Carbon Disclosure and Performance: Legitimacy and Management Views.” The British Accounting Review xxx: 1–15. doi:https://doi.org/10.1016/j.bar.2017.05.005.

- Renwick, D. W. S., T. Redman, and S. Maguire. 2013. “Green Human Resource Management: A Review and Research Agenda*.” International Journal of Management Reviews 15: 1–14. doi:https://doi.org/10.1111/j.1468-2370.2011.00328.x.

- Saunders, M., P. Lewis, and A. Thornhill. 2016. Research Methods for Business Students. Seventh ed. England: Pearson Education Limited.

- Schaltegger, S., and M. Csutora. 2012. “Carbon Accounting for Sustainability and Management. Status Quo and Challenges.” Journal of Cleaner Production 36: 1–16. doi:https://doi.org/10.1016/j.jclepro.2012.06.024.

- Suchman, M. C. 1995. “Managing Legitimacy: Strategic and Institutional Approaches.” Academy of Management Review 20 (3): 571–610. doi:https://doi.org/10.5465/amr.1995.9508080331.

- Tang, Qingliang. “Framework for and the Role of Carbon Accounting in Corporate Carbon Management Systems: A Holistic Approach.” Research Methods & Methodology in Accounting eJournal (2017): n. pag.

- Tang, Q., and L. Luo. 2014. “Carbon Management Systems and Carbon Mitigation.” Australian Accounting Review 24 (1): 84–98. doi:https://doi.org/10.1111/auar.12010.

- Toms, S., and C. Carter. 2010. “Value, Profit and Risk: Accounting and the Resource-Based View of the Firm.” Accounting, Auditing & Accountability Journal 23 (5): 647–670. doi:https://doi.org/10.1108/09513571011054927.

- Van Der Hoeven, M. 2011. “CO2 Emissions from Fuel Combustion Highlights.” International Energy Agency 1–134. doi:https://doi.org/10.1787/co2_fuel-2011-en.

- Wahyuni, D., and J. Ratnatunga. 2015. “Carbon Strategies and Management Practices in an Uncertain Carbonomic Environment – Lessons Learned from the Coal-face.” Journal of Cleaner Production 96: 397–406. doi:https://doi.org/10.1016/j.jclepro.2014.01.095.

- Yunus, S., E. Elijido-Ten, and S. Abhayawansa. 2016. “Determinants of Carbon Management Strategy Adoption.” Managerial Auditing Journal 31 (2): 156–179. doi:https://doi.org/10.1108/MAJ-09-2014-1087.