?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Sustainable Production Forest Management is a priority forest policy in Laos in which forest management plans need to be produced for each Production Forest Area (PFA). The forest management plan is very important for the sustainable use of forest resources in a PFA. It determines harvesting rotation cycles, annually allowed sustainable cuts of timber for each compartment, and identifies areas for conservation, restoration and rehabilitation in each PFA. This study examines the economic feasibility of the implementation of forest management operations in Xaibouathong Forest Management Area (FMA) in Khammouan Province with a 15-year cutting cycle. Data and information on Government cost norms, fees, and timber prices associated with the development and implementation of forest management plans, volumes and timber species harvested from three sub-forest management areas (Sivilai, Kengchone, and Phakong) of Xaibouathong FMA were collected and analyzed by using benefit-cost analysis. The results of this study showed that the current production forest management operation in Xaibouathong FMA is not economically feasible. Most of the sub-forest management areas costs outweigh its benefits because most of commercial tree species harvested in the three Sub-FMAs are lesser use species with low market price. Further study is needed to identify the real costs associated with the development and implementation of forest management plans when the Government permits logging operations in other production forest areas.

Introduction

The Lao People’s Democratic Republic (Lao PDR classifies its forests into three categories for the purpose of management, protection, development and utilization, namely: Protection Forests, Conservation Forests and Production Forests. Production Forests are areas covering natural forests and planted forests designated for the supply of wood and None Timber Forest Products (NTFPs) as commodities to satisfy the requirements of national socio-economic development and people’s livelihoods. The Government of Laos has declared 51 Production Forest Areas (PFAs) covering a total area of 3.1 million hectare throughout the country (PMO Citation2006a, Citation2006b, Citation2008). Based on government regulations (PMO Citation2002; GOL 2019), the management of PFAs shall involve the following six main activities conducted at different times in the management cycle ().

Table 1. Sequence of forest management operation with 15 years cutting cycle.

Each forest management operation has a different objective and involves sub-activities as follows:

Forest management plan development: In order to develop a FMP, a forest management inventory is conducted to collect information on land use, tree volume, tree species, NTFP and other socio-economic information of each Sub-FMA. This information is used to develop FMPs. A management plan covers productive zones, restoration zones, and conservation zones. Each zone has a different management objective. In the productive zones that has timber stock volume of more than 70 cubic meter per ha, the management plan focuses on the harvesting cycle over a period of time, typically 15 years in lowland areas and 20 years in upland areas (DOF 2006). The restoration zones that have timber stocking volume less than 70 cubic meter per ha, focus on assisting natural regeneration by applying silvicultural practices i.e. enrichment planting, tending, etc. The conservation zones focus on management of certain kinds of high conservation value forests (HCVF) such as: village protected areas, riparian buffer zones, wildlife habitats, etc.

Timber harvesting plan development: The main objective of a timber harvesting plan development is to reduce the costs for harvesting such as tree felling, skidding, transporting and forest road construction. In order to develop a timber harvesting plan, a pre-harvest inventory (PHI) is conducted to collect forest resources information needed for timbers harvest planning and forest regeneration (DOF 2006).

Tree marking list: The objective of tree marking is to guide logging unites to fell trees in accordance with logging regulations and to minimize damages to the forest ecosystem.

Logging operation including timber sale and benefit sharing: Logging operation is strictly followed a timber harvesting plan which comprises tree felling, skidding, transporting, log scaling and grading. Logs harvested from production forests shall go through an open bidding process and Money obtained from timber auctions is shared among stakeholders (PS 2012).

Post-harvesting Inventory: The main objective of postharvesting activities is to facilitate the natural regeneration in the logging site and to protect the environment, in particular avoiding stream and river siltation. This involves focusing on three main areas: (1) an assessment of harvesting performance, (2) an assessment of environmental impacts, and (3) an assessment of regeneration and the need for silvicultural treatments.

Timber stocking survey: The main objective of the survey is to evaluate the status of forest stocking volumes by using systematic-line-plots of 5% sampling intensity.

Implementation of forest management operations with 15 years cutting cycle requires financial support to implement the six main activities. Although, the costs associated with these activities are determined by Government cost norms, the economic feasibility of implementing forest management activities is unclear and has yet to be studied. Therefore, the aim of this study is to determine the economic feasibility of the implementation of forest management operations with a 15-year cutting cycle in a selected production forest. The results of this study will provide substantial information in developing a policy framework that could promote sustainable production forest management toward achievement of the Lao PDR’s Sustainable Development Goals.

Materials and methodology

Study area and design

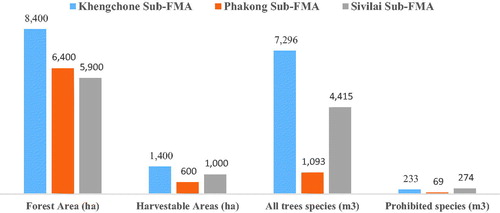

The study area is confined to the Xaibouathong FMA of Dong Phousoy Production Forest in Khammuan Province in the central region of Laos. It is located in between 17° 07′ and 17° 33′ N latitude and 105° 14′ and 105° 31′ E longitude. The total area of the Xaibouathong FMA is 31,700 ha. divided into three Sub-FMAs, namely: Sivilai (8,950 ha), Kengchone (12,400 ha), and Phakong (10,350 ha). The forest area of the Sivilai, Kengchone and Phakong is 66% (5,900 ha), 67% (8,400 ha), and 62% (6,400 ha), respectively. The remaining area being under non-forest comprising of residential areas, agriculture land, water bodies, wetlands etc.

Data collection and sources

Based on its objectives, this study collected data on the major costs of implementing production forest management activities for the three (3) Sub-FMAs with a 15-year cutting cycle from 2007 to 2022, comprising: forest management inventory, pre-harvesting inventory, tree marking activities, harvesting operations, postharvesting inventory, forest regeneration, log measuring and grading, and log transport permits. The logging costs include trees felling, timber bucking and skidding and log transportation from logs landing I to log landing II. The government set cost norms for technical services, management operations and fees for different tree species (). The timber species and volumes in each Sub-FMA () were derived from four sources, namely (1) forest management plans, (2) timbers harvesting plans, (3) tree marking lists, and (4) the log lists recorded in the Provincial Agriculture and Forestry Office of Khammouan Province. Timber prices vary from species to species, whether for domestic use or for export and for sawn or round wood. Since 2007, the Government of Laos has banned the export of sawn and round wood, so the price of timber used in this study is based on the price for domestic use ().

Table 2. The cost of the implementing forest management activities.

Table 3. Timber species and volumes (15 years) of the three Sub-FMAs.

Table 4. Timber prices.

Data analysis

The analytical framework for data analysis is shown in . The net benefits incurred from 2007 to 2022 for the three (3) Sub-FMAs were estimated by subtracting the cost of implementing forest management activities presented in from the revenue derived from timber species, volumes, and price presented in and , respectively. The economic returns from the investment in sustainable production forest management system of Xaibouathong FMA with a single rotation or a 15-year cutting cycle were analyzed using cost benefit analysis tools. This involved the usual investment criteria of Net Present Value (NPV), Internal Rate of Return (IRR), and Benefit-Cost Ratio (BCR) (Brown and Cambell Citation2003).

Figure 1. Flow chart of the analytical framework.

The NPV expresses the difference between the discounted present value of future benefits and the discounted present value of future cost. If NPV > 0, it means the investment benefits are greater than its costs, but if NPV < 0 or minus, it means the investment cannot be profitable as per formula below:

(1)

(1)

The Internal Rate of Return (IRR) is to make the discount rate at which the NPV becomes ‘0’. It means if the IRR is greater than cost of financing the project (IRR ≥ the interest rate), the investment should be accepted, but if the IRR is less than the cost of finance (IRR < r), the investment should be rejected. The IRR can be calculated as the following formula:

(2)

(2)

The Benefit-Cost Ratio is the way of comparing the present value of a project’s costs with the present value of a project’s benefits. If BCR ≥ 1 that means the investment project should be accepted, but if BCR < 1 that means the project should be rejected or the project will be unprofitable. The BCR can be calculated as the following formula:

(3)

(3)

where Bt is the benefit of timber sale in year t; Ct is the cost of the implementing forest management activities in year t; n is the number of years of the investment; r is the interest rate (discount rate) using 10%, 12.5%, and 15% based on prevailing loan rates of the Agricultural Promotion Bank of Laos (Agricultural Promotion Bank Citation2019), and (1 + r)t is discount factor for year t.

Results

shows the flow of the costs, revenues and net benefits for the three (3) sub-FMAs from 2007 to 2022. In 2007, net benefits are negative for all three (3) Sub-FMAs, because there is no revenue from timbers sale. The net benefits of Kengchone and Sivilai Sub-FMA became positive from 2008 to 2018 and 2021, respectively, while net benefits of Phakong Sub-FMA shows a negative value over the cutting cycle with a total negative value of nearly USD −59,000 (or USD −4,000/year). Although, the Kengchone Sub-FMA shows a positive net benefit with an annual average nearly USD 3100 from 2008 to 2018 (or 7.7% of the annual operation cost), the negative value in 2007 and from 2019 to 2022 causes net benefit over 15- year cutting cycle are negative of nearly USD −6,700. The result of Sivilai Sub-FMA shows positive net benefits from 2008 to 2021. Although, there are some negative net benefits occurred in 2007 and 2022, the annual benefit arises from nearly 13% of the annual operation cost between 2008 and 2015 to nearly 56% between 2016 and 2021. As a result, the net benefit over 15-year cutting cycle is positive at nearly USD 108,600 (or USD 7200/year). The major factors affecting the annual benefit for the three Sub-FMAs are annual volumes and timber species harvested from each compartment. If annual volumes and high economic value timber species harvested from each compartment are less, the annual revenue from timber sale will be less and making benefit change annually.

Table 5. The flow of the costs, revenues and net benefits for the three Sub-FMAs from 2007 to 2022.

shows the result of the Benefit-Costs Analysis for the three Sub-FMAs, using the discounted rate at 10%, 12.5%, and 15%. This result indicates that the NPV of Kengchone and Phakong is negative; while Sivilai sub-FMA is positive. Although, the NPV of Sivilai Sub-FMA is positive, the negative NPVs of Kengchone and Phakong cause the overall NPV of Xaibouathong FMA to be negative.

Table 6. The benefit-cost analysis of xaibouathong FMA.

Discussion

The results of the analyses indicated that the size of forest areas, harvestable areas, volume of harvested trees and volume of high economic tree species or prohibited species are the major factors affecting the NPV of the three (3) Sub-FMAs (). The forest management, preharvesting, and postharvesting inventories are calculated based on the areas (USD/ha). If the forest area of Sub-FMA and harvestable area are large, the cost of the inventory will be more. If volume of harvested trees and volume of high economic tree species or prohibited species are less, the revenue from timber sale will be less. The forest area of Kengchone Sub-FMA is 8400 ha, larger than other two (2) sub-FMAs. Although, the total timber volume harvested is higher than others, most of them are controlled species with low market price. As a result, forest management operation costs outweigh its benefits resulting to NPV < 0. Similar to Phakong, the total forest area is 6,400 ha. but harvestable area is very small at only 9% of the total area (or 600 ha). Moreover, the commercial tree species harvested is very low or 3% of the total volume resulting to NPV < 0. In contrast, the forest area of Sivilai is smaller than the others, but the proportion of harvestable area and volume with high economic value tree species is higher than the others. As a result, the net present value is greater than zero (NPV > 0).

Figure 2. The major factors affecting the NPV of the three (3) Sub-FMAs.

In addition, the forest management system and government cost norm for implementing forest management activities are other important factors affecting the NPV.

Forest management system

Based on production forest management regulations, the cutting intensity is very low due to the short rotation (15 years). In addition, most PFAs in Laos are secondary forests which have undergone logging in past decades. Most of the high economic value species were harvested and only species with low market demand are left. Therefore, to improve economic feasibility, the harvest cycle should be increased based on tree growth rate, yield information and stocking volume. As a comparison, forests in Malaysia, the forests are classified into 3 broad forest types, namely: dry inland forest or dipterocarp forest, peat swamp forest and mangrove forest and are managed under two different management systems, namely selective management with a 30 year or uniform or modified system with a 55-year rotation. Under the former system, cutting regimes are based on predetermined stocking and residual stand, while under the latter management system all trees down to 45 cm diameter breast height (dbh) are removed in one single felling (Jusoff and Taha Citation2008).

Government cost norms

Although, the Government regulates the cost norms for different management operations, real cost for each operation should be used instead. The Government sets timber prices according to domestic market demand which it varies from year to year, but instead timber process should be set based on real data from auctions. In addition, all costs related to forest management operations including forest management inventory, preharvesting inventory, tree marking, postharvesting assessment, harvesting operation, forest regeneration, log measurement and grading, and log transport permits should be reassessed in order to make recommendation to Government on how to improve their cost norm calculations.

Conclusion

Sustainable Production Forest Management Systems play a vital role not only in contributing to national economic development, but also in generating income for rural people. By analyzing the costs of forest management operations and timber sales data from various sources for Kengchone, Phakong, Sivilai Sub-Forest Management Areas, the study has illustrated that current production forest management operations in Xaibouathong FMA are not economically feasible. Most of the sub-forest management areas costs outweigh its benefits because most of the three (3) sub-FMAs are secondary forests which have undergone logging in past decades, volumes and timber species harvested from all sub-FMAs are low and most on them are lesser use species with low market price. To help ensure the economic feasibility of this system, the cost of the implementing forest management activities should be reassessed based on the actual implementation and improve the forest management system to increase harvesting rotation cycles, cutting intensity and cutting limit based on tree growth rate, yield information and stocking volume. In addition, market price for lesser use species should be improved in order to increase the revenue from timber sale. The same study is needed to identify the real costs associated with the development and implementation of forest management plans when the Government permits logging operations in other production forest areas.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Agricultural Promotion Bank. 2019. Interest rate for agricultural sector [Internet]; [cited 2019 October 16]. Available from: https://www.apb.com.la/interestrate.php.

- Brown RPC, Cambell HF. 2003. Benefit-cost analysis "Financial and economic appraisal using spreadsheets. The United States of America: New York: Cambrigde University Press.

- Department of Forestry 2006. Guideline on sustainable production forest management planning. Vientiane Capital.

- Department of Forestry 2012. Report on the assessment of forest cover and land use during 1992–2010. Vientiane Capital.

- Government of Lao PDR. 2012. Presidential decree on fees and service cost no. 003. Vientiane Capital (in Laos).

- Government of Lao PDR. 2019. Law on forestry No.64/NA. Vientiance Capital.

- Jusoff K, Taha D. s H D H. 2008. Sustainable forest management parties and environmental protection in Malaysia. WSEAS Transact Environ Develop. 4(3):191–199.

- Ministry of Industry and Commerce. 2014. Notice on Royalty of the Logs at Landing II and the Royalty for logs export to foreign countries for 2013–2014. Vientiane Capital.

- Ministry of Industry and Commerce (MOIC). 2010. Notice on Royalty of the Logs at Landing II for 2009–2010. Vientiane Capital.

- President of the State. 2012. Decree No. 001: benefit sharing from timber sales from production forest management systems. Vientiane Capital.

- Prime Minister Office. 2002. Decree No. 59: sustainable management of production forest area. Vientiane Capital.

- Prime Minister Office. 2006a. Decree No. 27: establishment of 8 national production forest areas. Vientiane Capital.

- Prime Minister Office. 2006b. Decree No. 321: establishment of 29 national production forest areas. Vientiane Capital.

- Prime Minister Office. 2008. Decree No. 270: establishment of 14 national production forest areas. Vientiane Capital.