?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The rapid surge in large-scale land acquisitions (LSLAs) has been triggered by the convergence of food, financial and environmental crises in the late 2000s. Since the 2008 commodity price spike, several Asian countries have become preferential targets for LSLAs carried out by foreign companies and governments. The rising interest in Asian farmlands and natural resources arose in a complex set of political transitions and socioeconomic dynamics that have shaped the whole continent in the last decades. This study relies on a dataset built on different data sources, from 2003 to 2021 for a total of 14,724 million hectares involved in LSLAs in Asia. The southeastern region is the most targeted one, with Indonesia and the Philippines as the principal host countries. The main investors are intraregional and, especially in private or stock-exchange listed companies, are from China and Malaysia, who intend to produce palm oil or rubber. Results partially confirm the initial hypothesis, showing that the endowment of land and water resources in host countries is positively related to the amount of land acquired. Findings also show that investors are looking for free market areas, with low trade barriers and low fiscal pressure, where the protection of workers’ rights is lower than that in their homeland.

KEYWORDS:

1. INTRODUCTION

The rapid surge in large-scale land acquisitions (LSLAs) triggered by the convergence of food, financial and environmental crises in the late 2000s has led to a renewed interest in social and rural studies in understanding how overseas farmland investments could shape the trajectories of agrarian change in the world.

Initial concerns raised by media, institutions and NGOs about the implications of a massive land use change driven by the new wave of investments in least developed countries (GRAIN, Citation2008; Oxfam, Citation2011) prompted scholars to focus on the negative effects of LSLAs, reporting adverse impacts on local food security, human rights violations and resource depletion that still constitute the main concern of critical literature (Abdallah et al., Citation2022; De Schutter, Citation2011 Müller et al., Citation2020). At the same time, as the wave of land acquisitions was unfolding rapidly in the first years following the commodity price spike of 2008, the development of global stakeholders’ networks has led to a better understanding of the main features of the so-called ‘new global land rush’ (Edelman et al., Citation2013). An LSLA is defined as a transnational or domestic land acquisition or lease ‘typically covering an area of 200 hectares (ha) or more’ (De Maria et al., Citation2023, p. 1). In this regard, data reported by Land Matrix show that the early areas of debate paid excessive attention towards the activity of ‘finance-rich, resource-poor’ (Borras & Franco, Citation2010) countries like China and the Gulf States purchasing large tracts of farmland in the developing world, underestimating the role played by investors from developed economies (Bräutigam & Zhang, Citation2013).

Building on theoretical assumptions that have interpreted the rapid surge of LSLAs as a ‘top-down phenomenon’ (Fairbairn, Citation2013; Wolford et al., Citation2013) where the state acts as the key player in regulating access to land and natural resources (Ribot & Peluso, Citation2003), studies have assessed, with various results, the influence of the institutional and legal framework at the target site in attracting LSLAs from foreign investors. Moreover, the same contributions also show the importance of environmental, climate and socioeconomic variables, both on the host and on the investor side, in shaping the flows of LSLAs (Arezki et al., Citation2015; Conigliani et al., Citation2018; Giovannetti & Ticci, Citation2016; Mazzocchi et al., Citation2021). However, to the best of our knowledge, no study has already assessed how specific features at the country level could be determinants of LSLAs in Asia, a continent that accounts for 15% of the global area interested in LSLAs, according to Land Matrix data.Footnote1

Since the 2008 commodity price spike, several Asian countries have become preferential targets for LSLAs carried out by foreign companies and governments. The rising interest in Asian farmlands and natural resources arose from a complex set of political transitions and socioeconomic dynamics that have shaped the whole continent in the last decades. The collapse of the Soviet bloc, the rise of China as a global power and the subsequent growing geopolitical relevance of the Indo-Pacific have resulted, for many Asian nations, in a redefinition of the development strategies followed until then. A renewed global quest for farmlands triggered by the convergence of multiple crises has been perceived by several Asian governments not only as a chance to improve the agricultural sector and boost economic growth, but also as a means of reasserting the authority of the central state on the country, especially where ethnic and religious divisions have produced, over the centuries, situations of legal pluralism (Debonne et al., Citation2019). However, along with the influence of governments’ macroeconomic and institutional policies on the development of land investments, case studies also report the crucial impact of existing social, environmental and climate features on the implementation of LSLAs in Asian countries (Baird, Citation2019; Debonne et al., Citation2019; Schönweger & Messerli, Citation2015).

While most of the literature related to LSLAs in Asia has extensively focused on single topics or individual case studies, to the best of our knowledge no research has yet been undertaken on an analysis of how specific national features could be determinants of LSLAs in this continent. Our hypothesis is that investors may be influenced in their investment choices by a broad range of factors – both on the target and on the investor side – including environmental features related to climate change (CC), which is considered to have a major role in shaping the flows of LSLAs (Davis et al., Citation2015; Mazzocchi et al., Citation2021). Thus, following an approach related to economic geography, the influence on the implementation of LSLAs in Asia could be related to environmental and economic features both of the host and investor countries, taking the perspective within the literature outlined by Lay and Nolte (Citation2018). More specifically the analysis of the factors at play as determinants of LSLAs in Asia is developed through a gravity model analysis, an approach already employed in LSLA literature (Arezki et al., Citation2015; De Maria, Citation2015; Giovannetti & Ticci, Citation2016; Hirsch et al., Citation2020; Lay & Nolte, Citation2018; Mazzocchi et al., Citation2021; Olayinka, Citation2018).

The paper is organised as follows. Section 2 reviews existing literature regarding LSLAs determinants. Section 3 presents the methodology and data used in the study. Section 4 shows and discusses the results and Section 5 draws conclusions.

2. LITERATURE REVIEW ON THE DETERMINANTS OF LSLAs

The issue of which factors shape the global flows of LSLAs is recognised by scholars as an important gap in the literature (Hirsch et al., Citation2020; Mazzocchi et al., Citation2021; Messerli et al., Citation2014). In recent years scholars have investigated how specific economic, social, institutional and environmental features, both at the target and the investor side, may influence the global flows of LSLAs. These researches involve both quantitative and qualitative approaches.

To date, studies committed to assessing the determinants of LSLAs have focused on factors previously assessed as predictors of foreign direct investments (FDI) between two countries (Arezki et al., Citation2015; Conigliani et al., Citation2018; Olayinka, Citation2018). Concerning this research approach, Lay and Nolte (Citation2018, p. 81) warn that the determinants of LSLAs are more specific than those for FDI, because ‘the quest to secure access to food and energy resources is believed to play a major role in such acquisitions, while market-seeking factors may be less important’. However, in literature, most of the variables included in the econometric models for the analysis of LSLAs and FDI overlap and prove to be significant predictors not only for the latter but also for the former.

Among the potential determinants of the LSLA flows investigated, studies agree in assessing the availability of arable land with agricultural potential in host countries as a strong predictor of land investments (Giovannetti & Ticci, Citation2016; Mazzocchi et al., Citation2018; Mazzocchi et al., Citation2021). Moreover, Arezki et al. (Citation2015) and Lay and Nolte (Citation2018) affirm that investor countries with poor fertile lands at the domestic level are more likely to invest abroad for food production, while in the analysis developed by Mazzocchi et al. (Citation2021) investors’ land endowment is not a significant parameter in driving the flow of LSLAs. While the aforementioned studies stress that investors are looking for lands with agricultural potential, in their analysis Hirsch et al. (Citation2020) assess the yield gap as a minor factor in driving LSLAs.

According to other scholars, water availability in host countries also plays a key role in driving the flows of farmland acquisitions (Giovannetti & Ticci, Citation2016; Mazzocchi et al., Citation2018). In fact, precipitations are positively correlated to LSLAs, increasing the amount of land acquired by external investors (Hirsch et al., Citation2020; Mazzocchi et al., Citation2021).

Although several target countries have enacted laws intended to preserve the environment, studies assess that forests and protected areas are among the preferential targets of LSLAs (Mazzocchi et al., Citation2021; Messerli et al., Citation2014), with the share of land left to forests being a driver in land acquisitions in Africa (Conigliani et al., Citation2018; Tulone et al., Citation2022). For example, Messerli et al. (Citation2014, p. 449) identify ‘remote forestlands with lower population density’ as one of the preferential landscapes for investors. Moreover, Woods (Citation2015) describes cases in Myanmar where constraints on forests have not been respected, making forested areas a target of land acquisitions.

Assessing the link between natural resources endowment and investors’ interest requires us to consider the ways CC could have affected the global flow of LSLAs. The quest for fertile lands, water and forested areas could be a consequence of climate extremes such as droughts, floods and wildfires that have affected agricultural output in potential investor countries and, therefore, have prompted governments and corporations to outsource their food and energy production. Therefore, Davis et al. (Citation2015) suggest an active role with CC driving farmland acquisitions in developing countries. Mazzocchi et al. (Citation2021) develop a gravity model employing variables related to natural resources endowment, climate disasters, the presence of protected areas and CO2 emissions, both for investors and host countries, in order to assess how climate and environmental factors may drive the flow of LSLAs. In addition to the positive relationship between land and water resources endowment – including precipitations – in target countries and LSLAs, the authors have found a negative influence with climate disasters, showing that investors have limited interest in developing projects in countries affected by the consequences of CC. Similarly, according to the analysis, the level of CO2 emissions in host countries negatively influences the amount of land acquired; therefore, it is possible to assert that investors are less willing to invest in countries where the levels of emissions are high.

Along with environmental and climate variables, some works investigate the role of the institutional, social and cultural context in driving LSLAs. Cultural and geographical proximities are identified as important factors in shaping the flow of investments: a common language and a former colonial relationship between two countries are assessed as two strong predictors, positively related to land investments, while the distance between investor and host is negatively related (Arezki et al., Citation2015; De Maria, Citation2015; Hirsch et al., Citation2020; Lay & Nolte, Citation2018; Mazzocchi et al., Citation2021; Olayinka, Citation2018; Raimondi & Scoppola, Citation2018).

Low population in the host country is a parameter often associated with land investments (Nolte et al., Citation2016) but, according to Messerli et al. (Citation2014), the geographical distribution of land deals depends on the interaction between population density and land use and cover. Other authors (Mazzocchi et al., Citation2021) investigate the role of women in sub-Saharan countries, observing that the level of political involvement of women in public institutions in host countries is negatively related to the amount of land acquired by external investors. This suggests that an improvement of women’s rights in target countries could improve the domestic debate on LSLAs, especially in countries where women’s participation in social and political life is still an unsolved problem.

Studies show mixed and contrasting results about the ways the rule of law, property rights protection and the quality of institutions influence the flows of LSLAs. Arezki et al. (Citation2015) and Giovannetti and Ticci (Citation2016) recognise a negative relationship between protection of land rights and LSLAs, arguing that a weak land tenure is a condition that attracts investments in the country. This situation is often linked with a general weakness in the rule of law, where high levels of corruptibility and a selective law enforcement could be preferential features for foreign investors (Arezki et al., Citation2015; De Maria, Citation2015; Dell'Angelo et al., Citation2017; Giovannetti & Ticci, Citation2016; Lay & Nolte, Citation2018; Nkansah-Dwamena & Yoon, Citation2022). However, Olayinka (Citation2018) finds that a weak institutional framework could be unfavourable for investors and Conigliani et al. (Citation2018) assess government integrity and a low level of violence in host countries as variables positively related to LSLAs. Moreover, in sub-Saharan Africa Nkansah-Dwamena and Yoon (Citation2022) find that LSLAs occur in countries with a low level of political stability.

Finally, literature focused on GDP per capita found it is often negatively related in host countries with the land deal size, while the unemployment rate is positively related (De Maria, Citation2015). Investors seem to be more likely to start projects in countries that fail to supply the domestic demand for food, a proxy of the food security of a state. In fact, in sub-Saharan Africa it has been observed that there is a positive relation between the amount of external debt of the host country and the size acquired by foreign investors, as well as between the national rate of cereal import and the LSLAs size (Tulone et al., Citation2022). In the same area, the level of FDI net inflows of the host countries is positively related to LSLAs, while the days required to start a business and the cost of a business start-up are negatively related to the amount of land acquired, showing the importance of a conducive business environment in potential host countries in influencing the flows of LSLAs (Nkansah-Dwamena & Yoon, Citation2022).

Concerning a qualitative analysis approach, a study carried out by Sändig (Citation2021) was made using a sample of research that provide insights into how southern rural communities have contested agricultural LSLAs. The sample was restricted to articles that document instances of resistance to LSLAs, finding six main issues related to the contesting actions compared in the sample of papers reviewed. They are: tactics, used by communities to face LSLAs; grievances, namely issues arising from the coercion imposed by LSLAs; benefits, representing the promised benefits of LSLA projects for the society; political opportunities and constraints, including the legal constraints and land tenure issue; community ties and resources, concerning the community solidarity and the participation of local leaders in contentions; framing, related to various framing processes playing a role in facilitating opposition against LSLAs. The primary impetus behind the contention arises from significant grievances over LSLAs, primarily stemming from economic losses, as well as environmental and cultural damage. This aligns with the findings of Schoneveld (Citation2017) indicating that instances of positive benefits from LSLAs in the African continent have been infrequent and have seldom outweighed the associated negative impacts. Another example is given by Adam and Agegnehu (Citation2023) who have studied the issue of contract farming in Ethiopia, as an alternative way to LSLAs, highlighting the lack of institutional intervention in regulating this process. Other scholars (Notess et al., Citation2020) using a qualitative approach have studied communities land formalisation in different countries, as land tenure and land property rights are among the major problems emerging from LSLAs.

Summarising, literature has produced contrasting figures about the role of land tenure security and the quality of institutions in attracting foreign investors both using quantitative and qualitative analysis. However, there is a wider consensus in assessing the endowment of land, water and forests as features positively related to the amount of land acquired, stressing the importance of natural resources in the quest for overseas farmlands. In addition, CC could play a key role in the future because studies show that countries affected by natural disasters are less attractive for investors.

3. METHODOLOGY

3.1. Conceptual framework

Previous research intended to assess the determinants of LSLAs have employed different empirical methods, such as unilateral regression models (Conigliani et al., Citation2018; Mazzocchi et al., Citation2018) and network analysis (Interdonato et al., Citation2020). However, an increasing number of studies have investigated LSLA drivers by implementing a gravity model (Arezki et al., Citation2015; De Maria, Citation2015; Giovannetti & Ticci, Citation2016; Hirsch et al., Citation2020; Lay & Nolte, Citation2018; Mazzocchi et al., Citation2021; Olayinka, Citation2018), a tool traditionally applied in economic research to study the flows of FDI between countries. According to De Maria (Citation2015), the structural analogies between the framework of bilateral investment flows assessed in FDI literature and the inherent nature of land markets make gravity models the most suitable approach in assessing the determinants of LSLAs. Building on De Maria’s arguments and on existing studies, the present work develops a gravity model in order to assess the determinants of LSLAs in Asian countries.

3.2. Dependent variable description

In this research, the size of land deals in hectares between pairs of host and investor countries was chosen as the dependent variable in the gravity model. This is an approach followed by other studies that have assessed the determinants of LSLAs (De Maria, Citation2015; Hirsch et al., Citation2020; Mazzocchi et al., Citation2021), while other authors have employed the number of deals as the dependent variable (Arezki et al., Citation2015; Lay & Nolte, Citation2018). The dependent variable was calculated on the basis of a raw dataset of 2486 global land deals which occurred from 2003 to 2021, in any implementation and negotiation status and involving a surface of more than 200 hectares, for a total of 95,788 million ha.Footnote2 Data were provided by the platform Land Matrix, which has been recognised as one of the most reliable sources in monitoring the global development of LSLAs (Conigliani et al., Citation2018; Lay & Nolte, Citation2018; Petrescu et al., Citation2020; Scoones et al., Citation2013). For each deal reported in the database, Land Matrix specifies the host country, the nationality of the investors and the deal size.

Building on the original dataset, the study considered only the deals occurring in Asian countries, thereby excluding the ones taking place in other continents.

For the identification of countries belonging to Asia, this study relies on the United Nations publication ‘Standard Country or Area Codes for Statistical Use’ originally published as Series M, No. 49 and now commonly referred to as the M49 standard.Footnote3 This classification is slightly different from the one provided by Land Matrix, and it also includes Kazakhstan and Uzbekistan, which Land Matrix classifies as Eastern European countries.Footnote4

The new Asian LSLAs dataset, made up of 563 deals for a total of 14,724 million hectares involved in land acquisitions, constituted the basis for further elaborations. In detail, the dependent variable includes all the possible investor country–host Asian country combinations, both the occurred deals and the non-occurred deals (potential combinations) for a total of 2835. Thus, the database includes zeros, as further explained in Section 3.4.

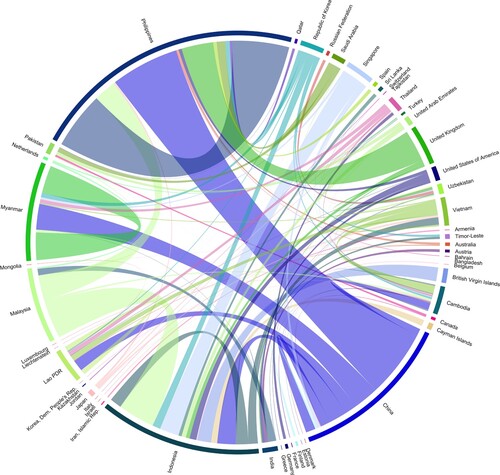

According to Land Matrix data, the most targeted region in Asia is the southeast, accounting for 90% of the land deal sizes negotiated in the whole continent.

represents a chord diagram plot which depicts cumulative LSLA flows between countries. The main host countries are the Philippines and Indonesia, followed by Myanmar, Laos and Cambodia. However, the southeastern region also contains important net investors, such as Malaysia, which seeks lands, especially in Indonesia, and, to a lesser extent, in the Philippines, and Singapore, who is also active in Indonesia. The main regional investor, however, is China, which operates especially in the Philippines and in Myanmar but also in Laos, Cambodia and Indonesia. To a lesser degree, the Republic of Korea and Saudi Arabia are also regional net investors. Extra-Asian companies have a limited role in the continent; among them, data show relevant flows from the United States to Indonesia, India and the Philippines. A special case is represented by Vietnam, a net host country which, however, has an active role in purchasing lands in Indonesia and Cambodia.

Figure 1. LSLAs flows between investors countries and host countries in Asia (all signed deals) in 2000–2022 period from our database.

In the cases of multilateral deals involving a plurality of investors from different countries, the whole size of the deal was attributed to every host-investor pair involved. This approach undoubtedly increases the numbers at play; however, studies employing, as dependent variable, not the size but the number of deals is likely to smooth out the wide differences existing in the actual surfaces involved by the reported deals, equating investments that, in reality, affect quite different areas. Considering these reasons and the aim of assessing which factors influence the magnitude of LSLA flows, the size of land deals has been chosen as the dependent variable.

3.3. Independent variables, descriptions and data sources

In line with previous studies on LSLA determinants discussed in Section 2, the present work assesses the role of socioeconomic, political, institutional, environmental and climate factors in driving farmland investments in Asia. shows the potential explanatory variables included in the analysis, which were obtained from different sources and divided into three groups: the Gravity Model variables group, the Socio-political variables group and the Environmental variables group.

Table 1. Variables description.

The explanatory variables were sourced from various databases, including the Index of Economic Freedom by Miller et al. (Citation2019), CEPII GeoDist, Faostat, Millennium Development Goals Indexes (MDGI), United Nations Statistics Division (UNSD) and the Terrestrial Air Temperature and Precipitation: 1900–2006 Gridded Monthly Time Series, version 1.01 (Dell et al., Citation2012). The ‘Terrestrial Air Temperature and Precipitation: 1900–2006 Gridded Monthly Time Series’ database offers mean precipitation, serving as an explanatory variable associated with climate change (CC) in our model.

Consistent with the literature on determinants of LSLA assessed by gravity models (Arezki et al., Citation2015; Lay & Nolte, Citation2018), our study incorporates the following factors (Gravity Model group): the agricultural area of the country (agricultural land), the cropland area of the country (cropland area), the arable area of the country (arable area), the GDP of the country (total, per capita, growth rate), the existence of a historical colonial relationship between hosts and investors (colony), and a common official language (language) between hosts and investors. These factors have been previously identified as positively correlated with the amount of land acquired in a country (De Maria, Citation2015; Lay & Nolte, Citation2018; Mazzocchi et al., Citation2021). This group also incorporates the distance between hosts and investors (distance), a variable that has been observed to have a negative relationship with the extent of LSLAs (Arezki et al., Citation2015). Gross domestic product (GDP) per capita can serve as an indicator to assess how wealthier countries, considering per capita values, are more inclined to participate in LSLAs (Mazzocchi et al., Citation2021). Additionally, it can be utilised to examine the impact of the host country's market size on land acquisitions. The Socio-political group comprises factors linked both to the issue of the social sustainability of LSLAs, a concept represented, for example, by the variables labour freedom, property rights, population and variables related to the political economic environment, such as public debt, government integrity, fiscal health, unemployment rate and tariff rate. These variables are usually included in analysis assessing LSLAs drivers for their influence demonstrated in literature, although with different intensity and meaning, according to the different context and models applied. For instance, in our model the unemployment rate of a host country could serve as an indicator of the potential number of individuals interested in employment opportunities in new investment projects. For investors, it also provides insights into the overall level of well-being in a country (Mazzocchi et al., Citation2021). The public debt variable can serve as a proxy for the fragility of a state, potentially indicating a propensity for investment in countries with higher levels of public debt by investors. Regarding the tariff rate, LSLAs are more likely to occur in countries where investors perceive a favourable return on their investment. For instance, legal regimes have an impact on the likelihood of LSLAs (Carter et al., Citation2017); thus, our hypothesis is that the higher the tariff rate, the lower the amount of LSLAs in a host country. The issue of property rights is undoubtedly one of the most investigated variables in determining LSLA drivers (Notess et al., Citation2020). While some authors found that countries with limited protections of local population land tenure rights were more targeted by land acquisitions (Giovannetti & Ticci, Citation2016), other researchers suggest that this relationship does not consistently exist (Mazzocchi et al., Citation2021). We hypothesise that in Asian regions this variable can be relevant in influencing LSLAs. In fact, while at national level, governments have fostered or halted foreign farmland investments according to specific political or economic purposes, the ‘fragmented sovereignty’ that distinguishes several Asian countries (Kenney-Lazar, Citation2019; Lund, Citation2011) still requires investors to interact with different layers of power in order to implement their projects successfully. For example, Lu and Schonweger (Citation2019) report the case of seven Chinese companies that failed to obtain the lands granted by the Laotian central government because they didn’t manage to interact successfully with local authorities that exercise the actual control on land access. A situation of fragmented sovereignty, thus, heavily affects the proper management of LSLAs, thereby influencing the outcomes of the investments on the livelihoods and food security of local communities. As for the variable government integrity, Conigliani et al. (Citation2018) and Mazzocchi et al. (Citation2021) assessed government integrity and a low level of violence in host countries as variables positively correlated to LSLAs, although in some countries, especially in Africa, a high level of corruption can foster LSLAs (Agboola et al., Citation2023; Mazzocchi et al., Citation2018).

The environmental variables group includes factors related to the impact of the environmental and climate conditions on the decision of investors to acquire land in a specific country. They are: annual freshwater withdrawals, renewable internal freshwater resources, protected areas in a country, temperature change and precipitation. Specifically, temperature and precipitation are recognised as major drivers of climate change (CC), and the period chosen (1900–2006) is considered as significant and reliable for analysis (Dell et al., Citation2012).Footnote5

3.4. Econometric specification

In order to address the scope of our paper, LSLAs between host and investor countries from 2003 to 2021 are explored by implementing gravity model specifications. These specifications have already been largely used in empirical analyses of bilateral trade flows, acquisitions, strategic alliances and foreign direct investments (see, for instance, Duarte et al., Citation2018; Hirsch et al., Citation2020; Mazzocchi et al., Citation2021; Owen & Yawson, Citation2013; Shahriar et al., Citation2019; Yotov, Citation2022).

We built a bilateral database of land deals considering all the investor country–host Asian country pairs included in Land Matrix. The final bilateral land deal database consists of 2,835 possible investor country–host Asian country combinationsFootnote6 with 563 completed land deals for a total of 14,724 million hectares and it includes 133 investor countries and 21 host Asian countries. Thus, in our analysis, thanks to the gravity model approach, all the variables have been tested both on the investor countries’ side and on the host countries’ side, as can be seen in .

Table 3. PPML estimation gravity models.

A testable gravity equation is typically formulated by taking the natural logarithm of both sides of the multiplicative version of the gravity model (Burger et al., Citation2009). Traditional literature has relied on ordinary least squares (OLS) for estimating these log-normal gravity specifications. More recently, Santos Silva and Tenreyro (Citation2006) proposed the use of Poisson estimators, which are capable of handling heteroscedasticity and are considered a ‘promising choice for estimating gravity equations’. These authors recommended the adoption of a Poisson-pseudo maximum likelihood (PPML) estimator. This approach has garnered widespread approval in the literature (e.g., Arezki et al., Citation2015; Arvis & Shepherd, Citation2013; Haberly & Wojcik, Citation2015).

Exploring our dependent variable in more detail, we found that it is skewed to the right due to the presence of an excess of zeros and overdispersed with the variance greater than the mean: 2272 observations are zero observations and only 563 are non-zeros.

According to Santos Silva and Tenreyro (Citation2006) and Lay and Nolte (Citation2018), Poisson estimators have been used to study bilateral flows. Specifically, the PPML specification is a robust substitute for the standard log-linear model which can handle heteroscedasticity and is considered an efficient method for the estimation of gravity equations. Moreover, PPML specification can be used to analyse continuous data and to address two data issues characterising the distribution of LSLAs across country pairs – zero inflation and overdispersion (Haberly & Wojcik, Citation2015).

We regressed the sum in hectares of all land acquired (yi,j) by players of the investor country (j) in the host country (i) registered in the Land Matrix database including characteristics of the gravity model (GM), a set of socio-political variables (SP) from host country and investor country, a group of environmental variables (ENV) from host country and investor country, as well as an error term . Thus, we obtained the following PPML gravity model equation:

We used the ‘gravity’ package in the R 4.2.1 software to estimate the PPML gravity model.

4. RESULTS AND DISCUSSION

4.1. Descriptive statistics

shows the descriptive statistics for the variables included in the model, comparing host and investor countries.

Table 2. Descriptive statistics.

In few cases, i.e. agricultural land, cropland, GDP and population, the maximum value of the host country variable matches with the one of the investor country variables, because it refers to China, which is both host and investor. The same goes for temperature change variable, which is referred to Mongolia.

In general, LSLAs are developed by richer and less populous countries, as shown by GDP per capita and population variables, with a lower endowment of lands and water resources, as confirmed by the average values of agricultural land, cropland, arable land and the water-related variables. At first glance, this seems to strengthen the narrative of a land rush driven by resource-poor and finance-rich countries (Borras & Franco, Citation2010).

On the socioeconomic side, quite surprisingly investors show a lower average value of labour freedom than the hosts value. However, the higher value of deviation standard for investors is due to the inclusion of countries from sub-Saharan Africa and Latin America, which present very low values of labour freedom. These countries have been included in the model as possible investors but are not investing in Asia. On the hosts’ side, the higher average value is affected by the presence of countries like Kazakhstan, Mongolia and Malaysia that have good values of labour freedom but account together, according to Land Matrix data, for less than 2% of the total land deals size.

Temperature change average value is higher for investors countries, thereby corroborating the hypothesis of Davis et al. (Citation2015), which suggest the active role of climate change in driving overseas farmland investments.

A value of 0.6 is set as the threshold to consider potential high correlation between the explanatory variables. No correlation beyond the set threshold exists between the independent variables.

4.2. Gravity model results and discussion

shows the results of the gravity model, reporting the variables that have been found statistically significant in at least one of the models.

The base model employs control variables, namely distance, GDP per capita both for hosts and investors, agricultural land both for host and investors, language, latitude and longitude of host countries. Models 2 and 3 add two sets of explanatory variables to the base model, respectively the socio-political and the environmental ones. Finally, in the full model are introduced all the explanatory variables.Footnote7 The addition of the predictors improves the explanatory power of the model: the R-squared suggests that the full model fits 48% of the variation in the data. We incorporated numerous explanatory variables into our analysis, necessitating a thorough examination of the issue of collinearity. We included only those variables in the models that exhibited correlation values significantly below the designated threshold of 0.6, as suggested by O’Brien (Citation2007). To address potential multicollinearity concerns among the explanatory regressors, we separately introduced three sets of these variables into the regression models (Mod. 1, Mod. 2 and Mod. 3) to assess any changes in their sign and magnitude relative to the full model (Mod. 4). Our analysis revealed no apparent signs of bias resulting from multicollinearity. Furthermore, we assessed the presence of multicollinearity (refer to ) by calculating the variance inflation factors (VIFs) and observed that multicollinearity was not problematic, as the VIFs remained below the recommended threshold of five, as per O’Brien (Citation2007), for Mods. 1, 2, and 3, with only a slight increase above five observed in Mod. 4.

Distance between investor and host countries has a negative effect on LSLA size, thereby confirming findings of previous studies which assess the crucial role of the geographical proximity between investors and host countries (Arezki et al., Citation2015; De Maria, Citation2015; Hirsch et al., Citation2020; Lay & Nolte, Citation2018; Mazzocchi et al., Citation2021; Olayinka, Citation2018; Raimondi & Scoppola, Citation2018). Moreover, longitude of the host countries is positively related to the size of investments, suggesting that the further the host is from Greenwich, i.e. Europe, the higher the interest is in investing in that country. These two findings seem to contradict each other; however, they are explained by the fact, outlined in Section 3.1, that the most targeted countries in Asia are placed in the southeastern region (the farthest from Greenwich) where investors are mainly intraregional, such as China, Malaysia, Singapore and Vietnam. While other studies observe that the presence of a common language between host and investors is positively related to the size of land acquired (De Maria, Citation2015; Hirsch et al., Citation2020; Lay & Nolte, Citation2018; Mazzocchi et al., Citation2021; Raimondi & Scoppola, Citation2018), in this study the parameter (language) is not statistically significant.

Moreover, several variables related to the economic and institutional context are strongly related to the amount of land acquired. GDP per capita is an influencing factor of land acquisitions, both on the host and the investor side. On the host side, the negative relation assessed in this study is consistent with findings in previous research (De Maria, Citation2015; Mazzocchi et al., Citation2021). On the investor side, the positive relation confirms the figures provided by Land Matrix data, that shows richer countries as the main active actors in the land rush. The tariff rate of host country result suggests that investors preferentially target countries with low trade barriers, in order to export the goods produced. A context of an open market, maybe with preferential trade agreements in force, is thus positively related to the land acquisition size. The prospect of high return on investments also explains the negative effect of a high tax burden as % of GDP on the amount of land acquired. In line with literature affirming that higher corporate income tax rates discourage inward FDI (Haberly & Wojcik, Citation2015), a lower fiscal pressure in the host country is positively related with land acquisitions by foreign investors. This seems in contrast with another result of the gravity, namely the positive relation between inflation rate in host country and the dependent. Literature on FDI is quite conflicting on how inflation in potential recipient developing countries affects investments inflows. While several studies claim that a high inflation rate is negatively related to FDI not only because it erodes the return of the investment, but also because it is a symptom of political and macroeconomic instability, making investors less likely to invest in that country (Demirhan & Masca, Citation2008; Mustafa, Citation2019; Vasileva, Citation2018), other studies find that a moderate rate of inflation can be perceived by potential investors as a sign of economic stability and market opportunity (Adhikary, Citation2017; Lee et al., Citation2021; Nguyen, Citation2020). In line with the second group of studies, the present work proposes that an under-control inflation rate could be perceived by foreign investors as an increasing openness to market by the region and a business opportunity.

Among the socioeconomic parameters, the level of labour freedom in investor countries is significant and has a slight positive effect on the land deal size. As shown in and explained in Section 4.1, investor countries present a lower mean value and a higher standard deviation value of labour freedom than the corresponding ones of host countries, due to the inclusion of African nations – having very low levels of this parameter (Miller et al., Citation2019) – in the group of potential investor countries. In addition, the higher mean value of labour freedom in host countries is influenced by the inclusion of Kazakhstan, Malaysia and Mongolia, with high levels of this variable but accounting together for less than 2% of the total land deals size (Land Matrix, Citation2022). Building on these considerations, the greater the labour rights protection in investor countries the greater the likelihood that investors outsource the production. Labour emerged as one of the most significant issues in the LSLAs debate (Li, Citation2011) and also in the Asian regions. Although in some cases LSLAs resulted in a shift from independent agricultural production towards employment in agricultural labour (Anti, Citation2021), recent evidence shows a limited global effect of LSLAs in creating stable jobs (Gyapong, Citation2020; Lay et al., Citation2021) and the importance of migrants and temporary workers in the implemented projects (Baird, Citation2019; Li, Citation2011; Zhan & Scully, Citation2018).

Results also confirm the importance of land and water endowment in driving LSLAs flows, in accordance with other studies (Giovannetti & Ticci, Citation2016; Lay & Nolte, Citation2018; Mazzocchi et al., Citation2018; Mazzocchi et al., Citation2021; Messerli et al., Citation2014; Müller et al., Citation2020; Nolte et al., Citation2016; Olayinka, Citation2018). On the host side, the availability of land with agricultural potential (agricultural land variable) could work as a major driver of acquisitions, attracting the so-called ‘finance-rich, resource-poor’ (Borras & Franco, Citation2010) countries. However, the positive correlation between agricultural land in investor countries and land deal size seems to contradict the narrative of a land rush driven only by rich countries who lack lands and natural resources. This finding may be explained by several reasons. First of all, land has been treated as a financial asset which has featured in speculative investments; the financial crisis that has triggered the new wave of acquisitions has induced investors from the financial sector to target cheaper overseas land as an inflation hedge strategy (Fairbairn, Citation2014). Another reason that partially explains the finding lies in the strong presence of regional investors in the Asian context, especially in the southeastern region. As already discussed in Section 3.2, countries with a large endowment of agricultural land like Malaysia, Vietnam and China are, to different degrees, both target and investor countries. Another reason could be found in the so-called phenomenon of ‘water grabbing’, closely linked to the one of LSLAs. Thus, water could be the key driver for land acquisition and the reasons that influence the flows of LSLAs to specific countries (Anseeuw et al., Citation2012; Mehta et al., Citation2012; Theesfeld, Citation2018; Woodhouse, Citation2012). This hypothesis is corroborated by the positive relation that the present study finds between precipitation in host countries, which is an indicator of water availability, and the dependent variable (Hirsch et al., Citation2020; Mazzocchi et al., Citation2021; Olayinka, Citation2018). The greater the water availability in host countries, the higher the overall size of land acquired. Finally, in line with previous research (Mazzocchi et al., Citation2021; Messerli et al., Citation2014), protected areas in host countries is a factor positively related to LSLAs deal size, suggesting that, in general, target nations have enacted laws intended to protect forests and other natural landscapes.

5. CONCLUSIONS

In recent years scholars have assessed which factors have shaped the flows of farmland investments in the last decade. The present work develops a gravity model analysis intended to assess the determinants of LSLAs in Asia, contributing to this line of research for a region that has been little investigated yet.

First, in recent years several Asian countries have become preferential targets for LSLAs carried out by foreign companies and governments and this fact is confirmed by our results in terms of economic and financial variables, where it emerges that target countries with low trade barriers and a lower fiscal pressure are preferred: in fact, in a context of the open market, perhaps with preferential trade agreements in force, land acquisitions are easier. Second, along the economic aspect, in contexts where ethnic and religious divisions have produced, over the centuries, situations of legal pluralism with multiple overlapping land claims, governments have seen LSLAs as a means of reasserting the authority of the central state on the country. These situations, which have developed in different ways from one country to another, have produced a multitude of social systems whose productive, institutional and legal peculiarities have played a key role in shaping LSLAs on the ground and the outcomes of these investments on local production systems. According to the results, this situation in host countries is accompanied by the fact that investor’s countries with high labour rights protection are more prone to outsource the production in Asian countries.

Lastly, the rising interest in Asian farmlands and natural resources arose in a complex set of political transitions and socioeconomic dynamics that have shaped the whole continent in the last few decades. Our findings, in terms of environmental factors influencing LSLAs, state that investors direct their interest towards water-rich countries, thereby confirming that the so-called ‘land grabbing’ is also, if not above all, a ‘water grabbing’. Thus, the endowment of land and natural resources is a significant factor in driving LSLAs to Asian countries.

Although we find that examining this dataset has provided valuable insights into the determinants of LSLAs in Asia, it also imposes limitations on our analysis. The first consideration concerns the low transparency that characterises the phenomenon of LSLAs and, consequently, the scarce information on the real negotiation and implementation status of the reported deals, as well as on the area actually involved. However, as explained in previous sections, Land Matrix has been recognised as the most reliable source to analyse LSLAs. Second, our analysis does not consider regional variations within states. This omission could be significant, especially concerning land and water resources, as investors might acquire land in specific, water-rich and fertile regions of a country. Moreover, another limitation is that the database only collects land deals contracting 200 hectares or more, without including the land deals regarding areas under this threshold. However, as just defined, LSLAs are considered to be international and local land transactions usually encompassing an expanse of 200 hectares (ha) or greater, thus limiting the approximation.

Further analysis could extend this branch of research to regions so far little investigated which nevertheless are gaining increasing importance as the deals are being implemented, i.e., Latin America and Eastern Europe.

AUTHOR CONTRIBUTION STATEMENT

Conceptualisation, C.M., L.Z. and L.O.; methodology, L.O., C.M.; software, L.O.; validation C.M. and L.O.; writing – original draft preparation, L.Z.; writing – review and editing, C.M., L.O., L.Z.

All authors have read and agreed to the published version of the manuscript.

ETHICS STATEMENT

The authors of this research declare that the study was conducted with strict adherence to ethical principles. In the design, execution, and documentation of this research, care was taken to ensure that no human or animal subjects were involved at any stage.

DATA AVAILABILITY STATEMENT

The datasets generated during and/or analysed during the current study are available from the corresponding author on reasonable request.

DISCLOSURE STATEMENT

No potential conflict of interest was reported by the author(s).

Notes

1 Land Matrix, Accessed 19 August 2022, https://landmatrix.org/map.

2 Land Matrix, Accessed 19 August 2022, https://landmatrix.org/list/deals.

3 UNSD, ‘Standard country or area codes for statistical use (M49)’, Accessed 2 September 2022, https://unstats.un.org/unsd/methodology/m49/.

4 Land Matrix, Accessed 19 August 2022, https://landmatrix.org/map.

5 We utilised Dell's version of the database. For a comprehensive description of the database, refer to Dell et al. (Citation2012).

6 We included all the countries mapped in the Land Matrix database vers. 2022.

7 The original dataset includes 2835 observations. Due to missing data in some key explanatory variables the regression models can report different observations numbers, as can be seen in .

REFERENCES

- Abdallah, A., Ayamga, M., & Awuni, J. A. (2022). Impact of land grabbing on food security: Evidence from Ghana. Environment, Development and Sustainability, https://doi.org/10.1007/s10668-022-02294-7

- Adam, A. G., & Agegnehu, A. W. (2023). Contract farming as an alternative to large-scale land acquisition and promoting inclusive and responsible agricultural investment: Evidences from Ethiopia. Corporate Social Responsibility and Environmental Management, 30(6), 2840–2851. https://doi.org/10.1002/csr.2519

- Adhikary, B. K. (2017). Factors influencing foreign direct investment in South Asian economies, a comparative analysis. South Asian Journal of Business Studies, 6(1), 8–37. https://doi.org/10.1108/SAJBS-10-2015-0070

- Agboola, A. O., Amidu, A. R., Olapade, D. T., & Odebode, A. A. (2023). Transnational large-scale land investments in developing economies: What role do formal institutions play? Land Use Policy, 134, 106924. https://doi.org/10.1016/j.landusepol.2023.106924

- Anseeuw, W., Lay, J., Messerli, P., Giger, M., & Taylor, M. (2012). Creating a public tool to assess and promote transparency in global land deals: The experience of the Land Matrix. The Journal of Peasant Studies, 40(3), 521–530. https://doi.org/10.1080/03066150.2013.803071

- Anti, S. (2021). Land grabs and labor in Cambodia. Journal of Development Economics, 149, 102616. https://doi.org/10.1016/j.jdeveco.2020.102616

- Arezki, R., Deininger, K., & Selod, H. (2015). What drives the global “land rush”? The World Bank Economic Review, 29(2), 207–233. https://doi.org/10.1093/wber/lht034

- Arvis, J. F., & Shepherd, B. (2013). The poisson quasi-maximum likelihood estimator: A solution to the ‘adding up’problem in gravity models. Applied Economics Letters, 20(6), 515–519. https://doi.org/10.1080/13504851.2012.718052

- Baird, I. G. (2019). Problems for the plantations: Challenges for largescale land concessions in laos and Cambodia. Journal of Agrarian Change, 20(3), 387–407. https://doi.org/10.1111/joac.12355

- Borras, S., & J. Franco. 2010. Towards a broader view of the politics of global land grab: Rethinking land issues, reframing resistance. ICAS Working Paper Series No. 001.

- Bräutigam, D., & Zhang, H. (2013). Green dreams: Myth and reality in China’s agricultural investment in Africa. Third World Quarterly, 34(9), 1676–1696. https://doi.org/10.1080/01436597.2013.843846

- Burger, M., Van Oort, F., & Linders, G. J. (2009). On the specification of the gravity model of trade: Zeros, excess zeros and zero-inflated estimation. Spatial economic analysis, 4(2), 167–190. https://doi.org/10.1080/17421770902834327

- Carter, S., Manceur, A. M., Seppelt, R., Hermans-Neumann, K., Herold, M., & Verchot, L. (2017). Large scale land acquisitions and REDD+: a synthesis of conflicts and opportunities. Environmental Research Letters, 12(3), 035010. https://doi.org/10.1088/1748-9326/aa6056

- CEPII. (2015). Institutional Profiles Database III, Paris. Retrieved January 11, 2024, from http://www.cepii.fr/institutions/EN/ipd

- Conigliani, C., Cuffaro, N., & D'Agostino, G. (2018). Large-scale land investments and forests in Africa. Land Use Policy, 75, 651–660. https://doi.org/10.1016/j.landusepol.2018.02.005

- Davis, K. F., Yu, K., Rulli, M. C., Pichdara, L., & D'Odorico, P. (2015). Accelerated deforestation driven by large-scale land acquisitions in Cambodia. Nature Geoscience, 8(10), 772–775. https://doi.org/10.1038/NGEO2540

- Debonne, N., van Vliet, J., & Verburg, P. (2019). Future governance options for large-scale land acquisition in Cambodia: Impacts on tree cover and tiger landscapes. Environmental Science and Policy, 94, 9–19. https://doi.org/10.1016/j.envsci.2018.12.031

- Dell, M., Jones, B. F, & Olken, B. A. (2012). Temperature shocks and economic growth: Evidence from the last half century. American Economic Journal: Macroeconomics, 4(3), 66–95. http://doi.org/10.1257/mac.4.3.66

- Dell'Angelo, J., D'Odorico, P., Rulli, M. C., & Marchand, P. (2017). The tragedy of the grabbed commons: Coercion and dispossession in the global land rush. World Development, 92, 1–12. https://doi.org/10.1016/j.worlddev.2016.11.005

- De Maria, M. (2015). Trading the untradeable: A gravity model for large-scale land acquisitions. Paper presented at the “World bank conference on land and poverty”, The World Bank, Washington DC, 23–27 March 2015.

- De Maria, M., Robinson, E. J. Z., & Zanello, G. (2023). Fair compensation in large-scale land acquisitions: Fail or fail? World Development, 170, 106338. https://doi.org/10.1016/j.worlddev.2023.106338

- Demirhan, E., & Masca, M. (2008). Determinants of Foreign Direct Investment flows to developing countries: A cross-sectional analysis. Prague Economic Papers, 17(4), 356–369. https://doi.org/10.18267/j.pep.337

- De Schutter, O. (2011). How not to think of land-grabbing: Three critiques of large-scale investments in farmland. The Journal of Peasant Studies, 38(2), 249–279. https://doi.org/10.1080/03066150.2011.559008

- Duarte, R., Pinilla, V., & Serrano, A. (2018). Factors driving embodied carbon in international trade: A multiregional input–output gravity model. Economic Systems Research, 30(4), 545–566. https://doi.org/10.1080/09535314.2018.1450226

- Edelman, M., Oya, C., & Borras, S. (2013). Global land grabs: Historical processes, theoretical and methodological implications and current trajectories. Third World Quarterly, 34(9), 1517–1531. https://doi.org/10.1080/01436597.2013.850190

- Fairbairn, M. (2013). Indirect dispossession: Domestic power imbalances and foreign access to land in Mozambique. Development and Change, 44(2), 335–356. https://doi.org/10.1111/dech.12013

- Fairbairn, M. (2014). ‘Like gold with yield’: Evolving intersections between farmland and finance. The Journal of Peasant Studies, 41(6), 777–796. https://doi.org/10.1080/03066150.2013.873977

- Faostat. (2019). Retrieved January 11, 2024, from http://www.fao.org/faostat/en/#home

- Giovannetti, G., & Ticci, E. (2016). Determinants of biofuel-oriented land acquisitions in Sub-Saharan Africa. Renewable and Sustainable Energy Reviews, 54, 678–687. https://doi.org/10.1016/j.rser.2015.10.008

- GRAIN. (2008). The 2008 landgrab for food and financial security. Retrieved August 11, 2022, from https://grain.org/article/entries/93-seized-the-2008-landgrab-for-food-and-financial-security.

- Gyapong, A. Y. (2020). How and why large scale agricultural land investments do not create long-term employment benefits: A critique of the ‘state’ of labour regulations in Ghana. Land Use Policy, 95, https://doi.org/10.1016/j.landusepol.2020.104651

- Haberly, D., & Wojcik, D. (2015). Tax havens and the production of offshore FDI: An empirical analysis. Journal of Economic Geography, 15(1), 75–101. https://doi.org/10.1093/jeg/lbu003

- Hirsch, C., Krisztin, T., & See, L. (2020). Water resources as determinants for foreign direct investments in land. A gravity analysis of foreign land acquisitions. Ecological Economics, 170, 106516. https://doi.org/10.1016/j.ecolecon.2019.106516

- Interdonato, R., Bourgoin, J., Grislain, Q., Zignani, M., Gaito, S., & Giger, M. (2020). The parable of arable land: Characterizing large scale land acquisitions through network analysis. PLoS ONE, 15(10), e0240051. https://doi.org/10.1371/journal.pone.0240051

- Kenney-Lazar, M. (2019). Relations of sovereignty: The uneven production of transnational plantation territories in Laos. Transactions of the Institute of British Geographers, 45(2), 331–344. https://doi.org/10.1111/tran.12353

- Land Matrix. (2022). Retrieved January 11, 2024, from http://www.landmatrix.org

- Lay, J., Anseeuw, W., Eckert, S., Flachsbarth, I., Kubitza, C., Nolte, K., & Giger, M. (2021). Taking stock of the global land rush: Few development benefits, many human and environmental risks. Analytical Report III. Bern Open Publishing, https://doi.org/10.48350/156861

- Lay, J., & Nolte, K. (2018). Determinants of foreign land acquisitions in low- and middle-income countries. Journal of Economic Geography, 18(1), 59–86. https://doi.org/10.1093/jeg/lbx011

- Lee, H.-S., Chernikov, S. U., & Nagy, S. (2021). Motivations and locational factors of FDI in CIS countries: Empirical evidence from South Korean FDI in Kazakhstan, Russia, and Uzbekistan. Regional Statistics, 11(4), 79–100. https://doi.org/10.15196/RS110404

- Li, T. M. (2011). Centering labor in the land grab debate. The Journal of Peasant Studies, 38(2), 281–298. https://doi.org/10.1080/03066150.2011.559009

- Lu, J., & Schonweger, O. (2019). Great expectations: Chinese investment in Laos and the myth of empty land. Territory, Politics, Governance, 7(1), 61–78. https://doi.org/10.1080/21622671.2017.1360195

- Lund, C. (2011). Fragmented sovereignity: Land reform and dispossession in Laos. Journal of Peasant Studies, 38(4), 885–905. https://doi.org/10.1080/03066150.2011.607709

- Mazzocchi, C., Orsi, L., & Sali, G. (2021). Environmental, climate and socio-economic factors in large-scale land acquisitions (LSLAs). Climate Risk Management, 32, 100316. https://doi.org/10.1016/j.crm.2021.100316

- Mazzocchi, C., Salvan, M., Orsi, L., & Sali, G. (2018). The determinants of large-scale land acquisitions (LSLAs) in Sub-Saharan Africa (SSA): A case study. Agriculture, 8(12), 194. https://doi.org/10.3390/agriculture8120194

- Mehta, L., Veldwisch, G. J., & Franco, J. (2012). Introduction to the special issue: Water gabbing? Focus on the (re)appropriation of finite water resources. Water Alternatives, 5(2), 193–207.

- Messerli, P., Giger, M., Dwyer, M. B., Breu, T., & Eckert, S. (2014). The geography of large-scale land acquisitions: Analysing socio-ecological patterns of target contexts in the global South. Applied Geography, 53, 449–459. https://doi.org/10.1016/j.apgeog.2014.07.005

- Millennium Development Goals Indicators (MDGI). (2019). Retrieved January 11, 2024, from https://millenniumindicators.un.org/unsd/mdg/Metadata.aspx?IndicatorId=0&SeriesId=660

- Miller, T., Kim, A. B., & Roberts, J. M. (2019). 2019 index of economic freedom. The Heritage Foundation.

- Müller, M. F., Penny, G., Niles, M. T., Ricciardi, V., Chiarelli, D. D., Davis, K. F., Dell'Angelo, J., D'Odorico, P., Rosa, L., Rulli, M. C., & Mueller, N.D. (2020). Impact of transnational land acquisitions on local food security and dietary diversity. Proceeding of the National Academy of Sciences of the United States of America, 118(4), e2020535118. https://doi.org/10.1073/pnas.2020535118

- Mustafa, A. (2019). The relationship between foreign direct investment and inflation: Econometric analysis and forecasts in the case of Sri Lanka. Journal of Politics and Law, 12(2), 44–52. https://doi.org/10.5539/jpl.v12n2p44

- Nguyen, C. H. (2020). Labor force and foreign direct investment: Empirical evidence from Vietnam. Journal of Asian Finance, Economics and Business, 8(1), 103–112. https://doi.org/10.13106/jafeb.2021.vol8.no1.103

- Nkansah-Dwamena, E., & Yoon, H. (2022). Why is sub-Saharan Africa an attractive destination to foreign land grabbers? Evidence from country characteristics. African Development Review, 34(2), 280–292. https://doi.org/10.1111/1467-8268.12632

- Nolte, K., Chamberlain, W., & Giger, M. (2016). International land deal for agriculture. Fresh insights from the Land Matrix: Analytical report II. In Cde/CIRAD/GIGA/University of Pretoria. Bern Open Publishing. https://doi.org/10.7892/boris.85304.

- Notess, L., Veit, P., Monterroso, I., Sulle, E., Larson, A., Gindroz, A. S., Quaedvlieg, J., & Williams, A. (2020). Community land formalization and company land acquisition procedures: A review of 33 procedures in 15 countries. Land Use Policy, 110, 104461. https://doi.org/10.1016/j.landusepol.2020.104461

- O’Brien, R. M. (2007). A caution regarding rules of thumb for variance inflation factors. Quality & Quantity, 41(5), 673–690. https://doi.org/10.1007/s11135-006-9018-6

- Olayinka, I. K. (2018). The determinants of large-scale land investments in Africa. Land Use Policy, 75, 180–190. https://doi.org/10.1016/j.landusepol.2018.03.039

- Owen, S., & Yawson, A. (2013). Information asymmetry and international strategic alliances. Journal of Banking and Finance, 37(10), 3890–3903. https://doi.org/10.1016/j.jbankfin.2013.06.008

- Oxfam. (2011). Land and power. The growing scandal surrounding the new wave of investment in land. Retrieved August 11, 2022, from https://policy-practice.oxfam.org/resources/land-and-power-the-growing-scandal-surrounding-the-new-wave-of-investments-in-l-142858/.

- Petrescu, D. C., Hartel, T., & Petrescu-Mag, R. M. (2020). Global land grab: Toward a country typology for future land negotiations. Land Use Policy, 99, 104960. https://doi.org/10.1016/j.landusepol.2020.104960

- Raimondi, V., & Scoppola, M. (2018). Foreign land acquisitions and institutional distance. Land Economics, 94(4), 517–540. https://doi.org/10.3368/le.94.4.517

- Ribot, J. C., & Peluso, N. L. (2003). A theory of access. Rural Sociology, 68(2), 153–181. https://doi.org/10.1111/j.1549-0831.2003.tb00133.x

- Sändig, J. (2021). Contesting large-scale land acquisitions in the Global South. World Development, 146, 105581. https://doi.org/10.1016/j.worlddev.2021.105581

- Schoneveld, G. C. (2017). Host country governance and the African land rush: 7 reasons why large-scale farmland investments fail to contribute to sustainable development. Geoforum; Journal of Physical, Human, and Regional Geosciences, 83, 119–132. https://doi.org/10.1016/j.geoforum.2016.12.007

- Schönweger, O., & Messerli, P. (2015). Land acquisition, investment, and development in the Lao coffee sector: Successes and failures. Critical Asian Studies, 47(1), 94–122. https://doi.org/10.1080/14672715.2015.997095

- Scoones, I., Hall, R., Borras, S., White, B., & Wolford, W. (2013). The politics of evidence: Methodologies for understanding the global land rush. Journal of Peasant Studies, 40(3), 469–483. https://doi.org/10.1080/03066150.2013.801341

- Shahriar, S., Kea, S., & Qian, L. (2019). Determinants of China’s outward foreign direct investment in the Belt & Road economies: A gravity model approach. International Journal of Emerging Markets, 15(3), 427–445. https://doi.org/10.1108/IJOEM-03-2019-0230

- Silva, J. S., & Tenreyro, S. (2006). The log of gravity. The Review of Economics and Statistics, 88(4), 641–658. https://doi.org/10.1162/rest.88.4.641

- Theesfeld, I. (2018). From land to water grabbing: A property rights perspective on linked natural resources. Ecological Economics, 154, 62–70. https://doi.org/10.1016/j.ecolecon.2018.07.019

- Tulone, A., Galati, A., Pecoraro, S., Carroccio, A., Siggia, D., Virzì, M., & Crescimanno, M. (2022). Main intrinsic factors driving land grabbing in the African countries’ agro-food industry. Land Use Policy, 120, 106225. https://doi.org/10.1016/j.landusepol.2022.106225

- United Nation Statistics Division (UNSD). (2017). Standard country or area codes for statistical use (M49). Retrieved September 2, 2022, from https://unstats.un.org/unsd/methodology/m49/.

- United Nation Statistics Division (UNSD). (2018). Retrieved January 11, 2024, from https://unstats.un.org/home/

- Vasileva, I. (2018). The effect of inflation targeting on foreign direct investment flows to developing countries. Atlantic Economic Journal, 46(4), 459–470. https://doi.org/10.1007/s11293-018-9594-6

- Wolford, W., Borras, S., Hall, R., Scoones, I., & White, B. (2013). Governing global land deals: The role of the state in the rush for land. Development and Change, 44(2), 189–210. https://doi.org/10.1111/dech.12017

- Woodhouse, P. (2012). Foreign agricultural land acquisitions and the visibility of water resource impacts in Sub-Saharan Africa. Water Alternatives, 5(2), 208–222.

- Woods, K. (2015). Commercial agriculture expansion in Myanmar: Links to deforestation, conversion timber and land conflicts. Forest Trends Report Series.

- Yotov, Y. V. (2022). On the role of domestic trade flows for estimating the gravity model of trade. Contemporary Economic Policy, 40(3), 526–540. https://doi.org/10.1111/coep.12567

- Zhan, S., & Scully, B. (2018). From South Africa to China: Land, migrant labor and the semi-proletarian thesis revisited. The Journal of Peasant Studies, 45(5-6), 1018–1038. https://doi.org/10.1080/03066150.2018.1474458