?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The random inspection of the China Securities Regulatory Commission (CSRC) is an important policy for practicing “standardizing regulatory behavior and innovating management modes”. This study investigates how CSRC’s random affect capital market information efficiency from the perspective of stock price synchronicity. Using a sample of China’s non-financial A-share firms from 2013 to 2019, we find that random inspections significantly reduced the stock price synchronicity of inspected firms. Random inspections could increase the probability of releasing management earnings forecasts, media coverage and investor attention, and thereby improve information efficiency. Further study finds that the effect of random inspections on stock price synchronicity is stronger for non-state controlled firms, districts with more listed firms, and districts with more transparent government. This study enriches the literature on the consequences of random inspections and extends our knowledge of the relationship between regulatory innovations and the information efficiency of the capital market.

1. Introduction

The report to the 20th National Congress of the Communist Party of China (CPC) stressed the construction of a high-level socialist market economy, which requires the market to play a decisive role in resource allocation and the government to play a better role in regulating the market. The better role of the government aims to improve and promote the decisive role of the market in resource allocation. The government should strive to ‘guarantee fair competition, strengthen market supervision, and maintain market order’ to enhance the efficiency of resource allocation of the market.

Since the 18th CPC National Congress, there has been a continuous transformation of the government’s functions. The 19th CPC National Congress put forward that the government needs to transform its functions, streamline administration and delegate powers, innovate regulatory methods, and enhance its credibility and enforcement ability. The 20th CPC National Congress states that the government needs to transform its functions, optimise the accountability system and organisational structure, promote the legalisation of institutions, functions, authorities, procedures, and responsibilities, and enhance the efficiency and credibility of government administration. The State Council has implemented the random inspection system since 2015 to standardise government regulation and innovative management modes. In the capital market, the CSRC’s random inspection has shown significant regulation effects, such as improving information disclosure quality (Liu et al., Citation2021) and standardising corporate operations (Teng et al., Citation2022). These findings suggest that the CSRC’s random inspection is a practice of the better regulatory role of government, contributing to the improvement of security regulation efficiency. This is consistent with the theoretical statement that a competent government provides space and premise for an efficient market (Lu & Wang, Citation2021).

An unanswered question is whether the CSRC’s random inspection can enhance the efficiency of resource allocation of the capital market. Information serves as a foundational determinant of capital market resource allocation efficiency, with higher information efficiency leading to higher resource allocation efficiency. This study explores the impact and mechanisms of the CSRC’s random inspection on capital market information efficiency, regarding stock price synchronicity. Based on a sample of Chinese A-share non-financial listed firms from 2013 to 2019, this paper uses a difference-in-difference (DID) model to empirically investigate how the CSRC’s random inspection affects capital market information efficiency. The results find that the CSRC’s random inspection significantly decreases the stock price synchronicity, suggesting that the CSRC’s random inspection promotes more firm-specific information entering stock prices and thus improves the capital market information efficiency. The mechanism tests show that the CSRC’s random inspection significantly increases the management earnings forecast, the media coverage, and the investor attention, which can accelerate the heterogeneous information content of stock prices and thus decrease the stock price synchronicity. Further study finds that the effect of the CSRC’s random inspection on the stock price synchronicity is relatively weak in SOEs, indicating a more pronounced effect for non-SOEs. The effect is strengthened by the number of listed firms within a district, indicating the CSRC’s random inspection could alleviate the resource constraint of securities supervision and improve security regulation efficiency. Finally, the effect is found to be strengthened by government transparency, revealing that the effect of random inspection depends on a high-transparent government.

This paper studies how the random inspection system influences capital market information efficiency by investigating the impact and mechanisms of the CSRC’s random inspection on stock price synchronicity. The paper enriches the research on the effectiveness and consequences of the random inspection system and provides evidence for the interaction between the competent government and the efficient market. The contributions of this paper are as follows:

First, this paper enriches the research on the consequence of the random inspection system. Kong et al. (Citation2021) and Huang et al. (Citation2020) theoretically discussed how the random inspection system generates a regulatory effect on product quality. Liu and Wang (Citation2021) investigated the accounting information quality random inspection carried out by the Ministry of Finance and found it could restrain earnings management. Teng et al. (Citation2022) studied the market reaction to the CSRC’s random inspection and demonstrated the effectiveness of the random inspection from the regulatory effect on corporate decisions and the deterrent effect on corporate violation behaviours. Existing studies also explored CSRC’s random inspection on accounting firms (Wen et al., Citation2020; Zhang et al., Citation2022) and on listed firms (Ban et al., Citation2022; Liu & Shen, Citation2021; Liu et al., Citation2021, Citation2022), and found significant impacts on the stock price crash risk, accounting information quality, and company violation. Stock price synchronicity is an important aspect that reflects the capital market information efficiency. This paper expands on the consequences of the CSRC’s random inspection by showing its impact and mechanisms on stock price synchronicity.

Second, this paper extends the study on the relationship between government regulation and capital market information efficiency from the perspective of the CSRC’s random inspection. China’s socialist market economy pursues the organic integration of the competent government and the efficient market. On the one hand, the government would, through its visible hand, stabilise stock price fluctuations (Teng et al., Citation2020). On the other hand, government behaviour, such as securities market system construction (You et al., Citation2007), security violation punishment (Gu et al., Citation2016), capital market liberalisation (Zhong & Lu, Citation2018), and industrial policy (Chen & Yao, Citation2018), could reduce stock price synchronicity and thus improve the capital market efficiency. The existing literature mainly investigates the determinants of stock price synchronicity from information disclosure, corporate governance, and information intermediaries. This paper focuses on the role of government regulation and studies the CSRC’s random inspection. It shows how this regulation innovation improves capital market information efficiency by revealing more firm-specific information and providing new evidence on the interaction between the competent government and the efficient market.

The remainder of the paper is organised as follows. Section 2 introduces the literature review and hypothesis development. Section 3 presents the research design. Section 4 reports empirical results. Section 6 summarises the conclusions and implications.

2. Literature review and hypothesis development

2.1. Random inspection of CSRC

The State Council released the Notice of the General Office of the State Council on promoting the Random Inspections and Regulating the Interim and Post-Event Supervision in July 2015. Since then, CSRC has been actively implementing random inspections in securities regulation, to standardise real-time and post-event supervision. The CSRC’s random inspection has been fully implemented since 2016. Listed firms are important targets of the CSRC’s random inspection. According to the List of Matters Subject to Random Inspection of CSRC (2015, 2021), the CSRC supervises and inspects information disclosure and corporate governance of listed firms. The selection of firms for random inspections is mainly determined through drawing lots and lottery. The CSRC conducts random selections in March, April, and May, while on-site inspections mostly occur between September and November (Teng et al., Citation2022).

The promulgation and implementation of the CSRC’s random inspection are significantly informative to the market (Teng et al., Citation2022). The CSRC’s random inspections of listed firms have regulatory and governance effects, such as curbing earnings management (Liu et al., Citation2021; Teng et al., Citation2022), improving information disclosure quality (Liu et al., Citation2021), and enhancing internal control quality (Teng et al., Citation2022). The CSRC’s random inspection also generates a deterrent effect on violations, increasing the probability of violation detection (Liu & Shen, Citation2021), and reducing the likelihood of subsequent violations by listed firms (Ban et al., Citation2022; Teng et al., Citation2022). Furthermore, the CSRC’s random inspection also affects audit risk (Liu & Shen, Citation2021) and auditing conservatism (Liu et al., Citation2022).

The CSRC could also conduct a joint inspection of listed firms and their engaged auditing firms. The study by Wen et al. (Citation2020) revealed that the random inspection of accounting firms can enhance their customers’ financial reports quality, thus reducing the stock price crash risk. Zhang et al. (Citation2022) found that the random inspection of accounting firms contributes to strengthening branch office management, improving internal controls, and thereby reducing auditing opinion shopping.

2.2. Stock price synchronicity

There are two theoretical views on stock price synchronicity. The information efficiency view holds that the fluctuations in stock prices deviating from the market average returns stem from firms’ specific information. A lower degree of stock price synchronicity indicates a higher level of specific information embedded in the stock price, thereby reflecting a higher level of capital market information efficiency (Jin & Myers, Citation2006; Morck et al., Citation2000; Roll, Citation1988). The information efficiency view is widely studied in China, the literature has explored the roles of investors (Bian et al., Citation2022; Luo et al., Citation2021), media (Huang & Guo, Citation2014), analyst (Yi et al., Citation2019; Zhu et al., Citation2007), financial reporting regime (Jin, Citation2010; Wang & Li, Citation2019), and government (Chen & Yao, Citation2018; Gu et al., Citation2016; You et al., Citation2007; Zhong & Lu, Citation2018) in determining stock price synchronicity. These studies conclude that enhancing investor protection and improving information transparency help to reduce stock price synchronicity, thus, enhancing capital market information efficiency.

According to the irrational behaviour view, factors such as market noise, speculative bubbles, and investor cognitive biases contribute to the fluctuations in stock prices. For firms with opaque information, amplified market noise increases the uncertainty surrounding their fundamentals (Zhou, Citation2014). Consequently, speculative trading activities drive stock price volatility, subsequently reducing stock price synchronicity (Dasgupta et al., Citation2010). In this context, stock price synchronicity serves as a positive reflection of capital market information efficiency (Lee & Liu, Citation2011; West, Citation1988; Xu et al., Citation2013).

With the continuous improvement of institutions in China’s capital market, the inverse association between stock price synchronicity and market information efficiency has become increasingly recognised (You et al., Citation2007). More and more studies support the information efficiency perspective and find that stock price synchronicity is predominantly determined by firm-specific information. We thereby suppose stock price synchronicity serves as a negative reflection of capital market information efficiency in this study.

2.3. Hypothesis development

From the information efficiency perspective, stock price fluctuations are driven by firm-specific information. We expect that the CSRC’s random inspection improves capital market information efficiency and therefore reduces stock price synchronicity.

Firstly, The CSRC’s random inspection reveals firm-specific information. Once a firm is selected for random inspection, the CSRC will conduct comprehensive on-site inspections, focusing on various facets, such as the authenticity, accuracy, completeness, timeliness, and fairness, of information disclosure, the compliance of corporate governance practices, the formalisation in exercising of shareholder rights and control by major shareholders or ultimate controllers, the standardisation of accounting procedures and financial management, and so on. If deficiencies or problems are detected in any of these areas, the CSRC mandates listed firms to rectify problems and submit rectification reports on time. Throughout this process, pertinent regulatory documents and rectification reports are promptly disclosed, which helps reveal firm-specific information and therefore lowers stock price synchronicity. The study of Teng et al. (Citation2022) shows significant market reactions when listed firms are targeted for inspection, indicating that the CSRC’s random inspections effectively unveil firm-specific information to the market.

Secondly, the CSRC’s random inspection could improve information disclosure. Prior research has shown that low earnings management (Lu & Shen, Citation2011) and high information disclosure quality (Choi et al., Citation2019; Peterson et al., Citation2015) increase the firm-specific information content in stock prices, decreasing stock price synchronicity. The random inspection wields effective regulatory power derived from governmental authority, exerting substantial governance influence over the financial reporting quality of the inspected firms. After CSRC’s random inspections, both accrual and real earnings management of inspected firms significantly decrease (Liu et al., Citation2021; Teng et al., Citation2022), and information disclosure quality improves (Teng et al., Citation2022). Furthermore, the random inspection may also augment the ‘quantity’ of information disclosure. In addition to the information disclosed during the inspection and rectification process, the random inspection enhances the internal control of inspected firms (Teng et al., Citation2022), contributing to increased voluntary information disclosure levels (Khlif et al., Citation2021). As documented by Gassen et al. (Citation2020), information disclosure and information intermediaries not only augment the quantity of firms’ public information relative to overall market information but also reduce investors’ information acquisition costs, mitigating adverse selection issues, and thereby diminishing the stock price synchronicity.

Thirdly, the CSRC’s random inspection could decrease stock price synchronicity by increasing media and investor attention. As an integral component of public enforcement, random inspection of CSRC generates positive externalities and strengthens the role of social monitoring. The random inspection emphasises the importance of information disclosure and accepting social monitoring to foster regulatory collaboration. In terms of execution effectiveness, prior research has demonstrated that the CSRC’s random inspection enhances the supervisory role of auditors (Liu & Shen, Citation2021; Liu et al., Citation2022). Furthermore, the CSRC’s random inspection elicits media and investor attention to the inspected firms, prompting market participants to unveil, disseminate, and exploit firm-specific information. Studies by Dong and Ni (Citation2014) and Zhang et al. (Citation2022) found an inverse relationship between media attention and stock price synchronicity, revealing that firms with higher levels of media attention experience decreased synchronicity. Greater investor attention can also facilitate more firm-specific information into the stock price (Andrei & Hasler, Citation2015) and lower the stock price synchronicity as a result of information exchange on social media platforms (Zheng et al., Citation2022) and online searches (Hu et al., Citation2021).

In summary, the CSRC’s random inspection can reveal more firm-specific information. It may also facilitate firm-specific information reflected in stock prices by improving the quality and quantity of information disclosure, as well as increasing media and investor attention. Consequently, CSRC’s random inspection leads to a reduction in stock price synchronicity and enhances capital market information efficiency.

Based on the information efficiency view, we propose the following hypothesis:

H1:

The CSRC’s random inspection reduces the stock price synchronicity.

3. Research design

3.1. Models and variables

To empirically examine the effect of CSRC’s random inspection on stock price synchronicity, we follow Teng et al. (Citation2022), Liu and Shen (Citation2021), and Wen et al. (Citation2020) and construct a time-varying DID model as shown in Equationequation (1)(1)

(1) :

where SYN is stock price synchronicity which is calculated according to Gul et al. (Citation2010), Wang and Li (Citation2019), and Zhao et al. (Citation2020), using Equationequations (2)(2)

(2) and (Equation3

(3)

(3) ):

where ri,w represents the weekly return of firm i in week w of a year, rm,w is the weekly market return (the CSI 300 Index) in week w of a year, rk,w is the weekly value-weighted industry return of industry k in week w of a year. After excluding observations with trading weeks less than 26 within a year, we regress each firm’s annual data using Equationequation (2)(2)

(2) to obtain the model goodness of fit (R2). We then calculate the stock price synchronicity (SYN) of each firm based on Equationequation (3)

(3)

(3) .

In Equationequation (1)(1)

(1) , Post_Inspection is a dummy variable representing the post-period of random inspection. Referring to the design of Teng et al. (Citation2022) and Liu and Shen (Citation2021), Post_Inspection equals 1 for inspected firms during the year of inspection and subsequent years, and 0 during other years. For the non-inspected firms, Post_Inspection remains 0 throughout the sample period. The coefficient of Post_Inspection, β1, measures the impact of CSRC’s random inspection on stock price synchronicity. Following Gul et al. (Citation2010), Wang and Yu (Citation2013), and Gu et al. (Citation2016), we control for weekly return variance of the industry (Var_Ind) and a set of firm-level variables, including weekly return skewness (Skewness), weekly return kurtosis (Kurtosis), differential of monthly average turnover rate (Dtn), accounting transparency (AbsDacc), asset size (LSize), leverage ratio (LLev), return on assets (LROA), growth rate (LGrowth), institutional investor ownership percentage (LShare_Insti), ownership type (LSOE), analyst coverage (LAnalyst), shareholding percentage of the largest shareholder (LShare_Top1), board size (LBoard_Size), board independence (LBoard_Indep), CEO-Chair duality (LDual), and auditing quality (LBig4).Footnote1

Variable definitions are shown in .

Table 1. Variable definitions.

3.2. Sample selection and data source

The random inspection system was launched nationwide by the State Council in 2015, and the CSRC initiated inspections on listed firms in 2016. The study period therefore covers three years surrounding 2016, i.e. from 2013 to 2019. Moreover, firms that have already undergone inspections by local CSRC bureaus in the past three years are excluded from re-inspection. For example, as outlined in the Implementation Plan for Random On-site Inspections of Listed Companies by the Beijing Securities Regulatory Bureau in 2016, the following entities shall not be the objects of random inspection: entities with preliminary evidence or clues of suspected illegal activities under investigation, entities subject to legal cases and inspections initiated within the previous year, and entities had been randomly inspected by the Beijing Securities Regulatory Bureau within the past three years. To mitigate the potential impact of duplicate inspections, we end the sample period by 2019. The research sample thus consists of A-share non-financial listed firms, excluding those under enforcement investigation, resulting in a final dataset comprising 17,607 firm-year observations. We winsorise all continuous variables at their 1% and 99% percentiles. The list of listed firms subjected to random inspection of CSRC is hand-collected from the websites of local CSRC bureaus. Data for other variables are extracted from the Wind and CSMAR databases.

4. Empirical results

4.1. Descriptive statistics

reports the descriptive statistics of the main variables, including correlation coefficients, number of observations, means, standard deviations, minimum values, and maximum values. The highest correlation coefficient is −0.55 between board size (LBoard_Size) and board independence (LBoard_Indep). Asset size (LSize) and leverage (LLev) also exhibit a significant correlation, with a coefficient of 0.50. The remaining variables show correlation coefficients within a reasonable range, suggesting there are no severe multicollinearity issues in the model. The statistics of variables are all within a reasonable range. The correlation between SYN and Post-Inspection is −0.05 and statistically significant at the 1% level, indicating reduced stock price synchronicity after the CSRC’s random inspection, thus providing preliminary evidence for H1.

Table 2. Descriptive statistics.

4.2. The CSRC’s random inspection and stock price synchronicity

We use Equationequation (1)(1)

(1) to examine the impact of random inspection of CSRC on stock price synchronicity, and the results are reported in . Column 1 of shows the results of the baseline model, and the coefficient of Post_Inspection is −0.066 at a 5% significance level. Economically speaking, the stock price synchronicity of inspected firms decreases by 0.066 relative to firms that were not inspected, which is approximately 44% of the sample mean. These findings verify the significant reduction in stock price synchronicity due to the CSRC’s random inspection and support H1. To address the potential regional bias, column 2 of includes the interactive fixed effects of Province*Year. The results show that the coefficient of Post_Inspection remains negative and statistically significant. These results support the information efficiency view that the CSRC’s random inspection facilitates the integration of firm-specific information into the stock price, leading to a decrease in stock price synchronicity and an improvement in capital market information efficiency.

Table 3. The CSRC’s random inspection and stock price synchronicity.

4.3. Robustness tests

4.3.1. Parallel trend test

The empirical study employing a DID model requires satisfying the parallel trend assumption. To examine the parallel trend, we introduce dummy variables for the current year (Current) and the three years before and after (Before3, Before2, Before1, After1, After2, and After3) the CSRC’s random inspection. The empirical results are presented in . The results show that coefficients for Before3, Before2, and Before1 are all statistically insignificant, while those for Current, After1, After2, and After3 are all significantly negative. This suggests that before the random inspection, the stock price synchronicity of inspected and uninspected firms exhibited parallel trends. However, after the inspection, the stock price synchronicity of the inspected firms significantly decreased compared to the uninspected firms.

Table 4. The parallel trend test.

graphically presents the results of the parallel trends test. As shown, before the random inspection, the coefficients for Before3, Before2, and Before1 do not significantly differ from zero, while the coefficients for Current, After1, After2, and After3 are all significantly negative. These results confirm the parallel trend assumption.

Figure 1. The parallel trend.

4.3.2. Alternative measurements for stock price synchronicity

Drawing on Li et al. (Citation2014) and Huang and Jiang (Citation2022), we adopt synchronicity (SYN_Factor) and idiosyncratic volatility (IV_Factor) calculated based on the CAPM three-factor model as alternative indicators of stock price synchronicity. A higher value of SYN_Factor indicates a higher level of stock price synchronicity, whereas a higher value of IV_Factor indicates a lower level of stock price synchronicity. The calculation processes are presented in Equationequations (4)(4)

(4) -(Equation6

(6)

(6) ):

The robustness test results for the alternative dependent variables are presented in . In column (1) of , using SYN_Factor as the dependent variable, the coefficient of Post_Inspection is shown to be −0.052 with a 1% significance level, indicating that the CSRC’s random inspection significantly reduces stock price synchronicity. In column (2) of , using IV_Factor as the dependent variable, the coefficient of Post_Inspection is 0.059, significant at the 1% level, suggesting that the random inspection significantly increases the stock price idiosyncratic volatility, thereby reducing stock price synchronicity.

Table 5. Alternative measurements for stock price synchronicity.

4.3.3. Using a matching sample

The CSRC randomly inspects listed firms at a relatively low frequency. To address potential biases arising from the sample size differences between inspected and non-inspected firms, we conduct a robustness test using a matching sample. Specifically, we use the Propensity Score Matching (PSM) method to identify non-inspected firms that closely resemble the inspected firms in terms of asset size (LSize), leverage ratio (LLev), and return on investment (LROA) within the same province and year. The matched sample is then employed to conduct the DID empirical analysis. The results are presented in . Columns (1)-(3) of display the results using SYN, SYN_Factor and IV_Factor, respectively. The coefficients of Post_Inspection are −0.066, −0.045, and 0.036, respectively, all of which are statistically significant. The results from the PSM-DID analysis buttress the main findings.

Table 6. Using matching sample.

4.3.4. Placebo test

Adhering to the design of a random inspection system, the selection process by the CSRC is random. This provides us with an exogenous setting to conduct the DID empirical analysis. We conduct a placebo test to further check the robustness of our results. Specifically, an equivalent number of firms are randomly chosen as virtual inspected firms, while other firms are classified as non-inspected firms in 2016, 2017, 2018, and 2019. The placebo sample is then utilised for testing Equationequation (1)(1)

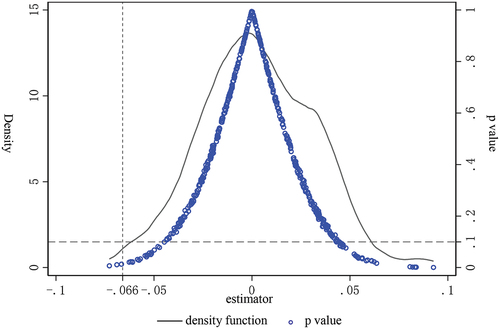

(1) and the procedure is repeated 500 times. The distribution of the 500 DID coefficients of Post_Inspection and their respective p-values are depicted in . As illustrated, the coefficients based on the placebo sample exhibit a normal distribution with a mean of zero, and most p-values are above 0.1, indicating that most of the regression coefficients are not statistically significant. The findings illustrated in from the placebo test confirm that the observed reduction in stock synchronicity can indeed be attributed to the CSRC’s random inspection.

Figure 2. The placebo test.

4.4. Mechanism tests

The above empirical results indicate that the CSRC’s random inspection could facilitate the integration of more firm-specific information into the stock price, thereby reducing stock price synchronicity and enhancing capital market information efficiency. As important participants in the capital market, firms, media, and investors play crucial roles in this process. Higher levels of corporate information disclosure, increased media coverage, and more proactive searching of company information by investors can result in greater inclusion of firm-specific information in stock prices. Therefore, we examine the mechanisms through which random inspection of CSRC reduces stock synchronicity from the perspectives of improving corporate information disclosure (i.e. the release of management earnings forecasts), enhancing media attention, and increasing investor attention. The results are reported in .

Table 7. Mechanism tests.

4.4.1. Improving corporate information disclosure

We argue that the CSRC’s random inspection induces firms to disclose more fundamental information, thereby enabling the inclusion of greater firm-specific information into stock prices. To examine this mechanism, we investigate whether the CSRC random inspection promotes the disclosure of management earnings forecasts. Management earnings forecasts contain significant informational content (Waymire, Citation1984). To test the impact of the CSRC random inspection on the probability of disclosing management earnings forecasts, we use a logit model and introduce a dummy variable, IfMEF (indicating whether the company releases management earnings forecasts). We also test the mediating effect of IfMEF. The results are presented in columns (1)-(3) of . Column (1) shows that the coefficient of Post_Inspection is significantly positive at the 10% level, indicating that the CSRC’s random inspection significantly increases the probability of management earnings forecasts. Columns (2) and (3) show the empirical results when introducing the mediating variable. In each column, Post_Inspection is significantly negative, and the result of IfMEF on SYN is also significantly negative, suggesting that management earnings forecasts significantly reduce stock price synchronicity. The results of the mediating effect test at the bottom of the table demonstrate that the interaction between Post_Inspection and IfMEF significantly contributes to decreasing stock price synchronicity, suggesting that management earnings forecasts play a mediating role.

4.4.2. Enhancing media attention

Listed firms inspected by the CSRC will attract more media coverage. This implies that the CSRC’s random inspection enhances media attention, leading to stock prices reflecting more firm-specific information and ultimately contributing to a reduction in stock price synchronicity (Huang & Guo, Citation2014). With the advancements in modern information technology, online media has emerged as a dominant medium for information dissemination and acquisition. We therefore use the natural logarithm of the number of online financial news articles (MediaAtten) to measure media attention. Results in columns (4)-(6) of show the mechanism test. Column (4) reveals that the coefficient of Post_Inspection on MediaAtten is significantly positive, indicating that the CSRC’s random inspection significantly increases media attention. Results in columns (5) and (6) show the results when including the mediating variable. In each column, Post_Inspection is significantly negative, and the result of MediaAtten on SYN is also significantly negative, suggesting that media attention significantly reduces stock synchronicity. In column (6), after including the mediating variable, the impact of Post_Inspection is relatively diminished compared to column (5), indicating a mediating effect of MediaAtten (Preacher & Hayes, Citation2004). The test of the mediating effect at the bottom demonstrates that media attention plays a significant mediating role in the impact of the CSRC’s random inspection on reducing stock price synchronicity.

4.4.3. Increasing investor attention

The CSRC’s random inspection not only increases media attention but also could attract investors’ attention towards inspected firms, thereby incorporating firm-specific information into stock prices. We refer to Drake et al. (Citation2012) and Feng (Citation2014) and use investor web search volume (InvAtten) as a measure of investor attention. Columns (7)-(9) in present the results. The results in column (7) reveal that the coefficient of Post_Inspection on InvAtten is significantly positive, indicating that the CSRC’s random inspection significantly increases investor attention. Columns (8) and (9) show that Post_Inspection is significantly negative in each column, and the results of InvAtten on SYN are also significantly negative, suggesting that investor attention significantly reduces stock synchronicity. In column (9), after including the mediating variable, the impact of Post_Inspection is relatively reduced compared to column (8), indicating a mediating effect of InvAtten (Preacher & Hayes, Citation2004). The results of the mediating effect test at the bottom demonstrate that investor attention plays a significant mediating role in the impact of random inspection of CSRC in reducing stock price synchronicity.

In summary, the CSRC’s random inspection significantly promotes the release of management earnings forecasts and increases media and investor attention, resulting in more firm-specific information incorporated into stock prices and reducing stock price synchronicity.

4.5. Further analysis

4.5.1. Ownership type (SOEs and non-SOEs)

The effect of the CSRC’s random inspection on stock price synchronicity may vary across firms with different ownership types. On one hand, political connections may weaken the effectiveness of CSRC regulatory enforcement (Correia, Citation2014), suggesting that the inherent political affiliations of state-owned enterprises (SOEs) may dampen the regulatory effect of CSRC’s random inspection. On the other hand, CSRC’s random inspection primarily focuses on the regulatory compliance of listed firms. SOEs face stricter regulatory supervision, leading to more standardised corporate governance practices compared to non-SOEs. Therefore, the regulatory effect of the CSRC’s random inspection may be stronger for non-SOEs. A related study by Liu et al. (Citation2021) found that the effect of CSRC’s random inspection on accrual and real earnings management is significant only in non-SOEs. Based on the above analysis, we expect a stronger effect of CSRC’s random inspection on reducing stock price synchronicity for non-SOEs.

presents the moderating effect of ownership nature. Columns (1)-(3) show the results using SYN, SYN_Factor, and IV_Factor as dependent variables, respectively. The results in columns (1) and (2) show that coefficients of Post_Inspection*LSOE are both significantly positive, suggesting a stronger impact of CSRC’s random inspection on reducing stock price synchronicity for non-SOEs. The result in column (3) shows that the coefficient of Post_Inspection*LSOE is significantly negative, also indicating a stronger effect of CSRC’s random inspection for non-SOEs. The results in demonstrate that, compared to SOEs, the random inspection of CSRC can lower stock price synchronicity for non-SOEs.

Table 8. Further analysis of ownership type.

4.5.2. Number of listed firms within a district

The CSRC’s random inspection helps alleviate the regulatory inefficiency problem caused by enforcement resource constraints. As a result, the effectiveness of the random inspection is expected to be stronger when the CSRC faces greater resource constraints. This is evidenced by Teng et al. (Citation2022) who show that when the CSRC faces greater resource constraints, the effects of the CSRC’s random inspection on enhancing company information disclosure quality, improving internal control quality, and suppressing illegal and irregular behaviours are stronger. We anticipate that the impact of the CSRC’s random inspection on stock price synchronicity will be stronger when the CSRC faces greater resource constraints.

Gunny and Hermis (Citation2020) argued that an increased number of listed firms within the district leads to a stronger regulatory burden, diminishing the effectiveness of government enforcement. We follow Teng et al. (Citation2022) and measure the level of resource constraints faced by the CSRC using the number of listed firms within the jurisdiction of the local securities regulatory authority (ProvNum). We focus on the interaction term between Post_Inspection and ProvNum, and the Province*Year fixed effect is included in the empirical model to control for potential regional differences. reports the results. In column (1), with SYN as the dependent variable, the coefficient of Post_Inspection*ProvNum is negative but statistically insignificant. In column (2), with SYN_Factor as the dependent variable, the coefficient of Post_Inspection*ProvNum is significantly negative at the 5% level. In column (3), with IV_Factor as the dependent variable, Post_Inspection*ProvNum is shown to be significantly positive at the 1% level. The overall results in indicate that more listed firms within a district lead to a stronger effect of the CSRC’s random inspection on reducing stock price synchronicity. This also suggests that random inspection can enhance securities regulation efficiency.

Table 9. Number of listed firms within a district.

4.5.3. Government transparency

The random inspection system mandates the government to ‘disclose the regulatory information and form regulatory synergy’. This indicates that increased government transparency can enhance the effectiveness of the random inspection. Wang and Ma (Citation2017) showed that lower government transparency exacerbates information asymmetry, incentivising government agencies to conceal violations and misconduct. Thus, higher government transparency could facilitate information sharing among government regulatory departments and enhance the efficiency of random inspection. In addition, government information disclosure generates significant externalities, as greater transparency provides the public with expanded access to information resources. This empowers market participants to utilise government information for learning, research, and decision-making (He, Citation2020). Consequently, government transparency could strengthen the effectiveness of the random inspection and could also encourage market participants to actively seek information about inspected firms, thereby incorporating more specific information into stock prices. We thus expect that higher government transparency will lead to a more pronounced effect of the CSRC’s random inspection on stock price synchronicity.

To examine the moderating effect of government transparency, we use the Government Transparency Index (GovTrans) published by Nie et al. (Citation2018) to measure the level of government transparency in different provinces. The index captures the extent of the administrative information disclosure and fiscal transparency. We introduce the interaction term of GovTrans and Post_Inspection in Equationequation (1)(1)

(1) and control the Province*Year fixed effect to mitigate potential regional variations. The empirical results are presented in , where column (1), (2) and (3) uses SYN, SYN_Factor, and IV_Factor as dependent variables respectively. Coefficients of Post_Inspection*GovTrans are all significantly negative in columns (1) and (2), indicating that higher government transparency enables the effect of the CSRC’s random inspection. In column (3), Post_Inspection*ProvNum is significantly positive at the 1% level. The overall findings from suggest that the effect of the CSRC’s random inspection on stock price synchronicity is more pronounced in provinces with higher government transparency.

Table 10. Government transparency.

5. Conclusion

The CSRC’s random inspection is an important practice in the capital market in transforming government functions, innovating government administration modes, regulating law enforcement behaviour, and improving the role of government. These, eventually, contribute to the enhanced resource allocation efficiency of the capital market. This study examines the impact and mechanisms of the CSRC’s random inspection on capital market information efficiency from the perspective of stock synchronicity. Based on a sample of non-financial listed firms in the Chinese A-share market from 2013 to 2019, we find that the CSRC’s random inspection significantly reduces stock price synchronicity. This suggests that the random inspection promotes the incorporation of firm-specific information into the stock price and improves the capital market information efficiency. The underlying mechanisms include increased release of management earnings forecasts and heightened attention from the media and investors. Furthermore, we find that the effect of the random inspection is stronger for non-state-controlled listed firms, regions with a higher number of listed firms, and regions with higher government transparency.

The policy implications of this study highlight the importance of a better combination of competent government and efficient markets, as a manifestation of China’s socialist market economy. By introducing the innovative regulatory approach of random inspection, the regulatory efficiency of the CSRC can be improved, thereby increasing the capital market information efficiency. To further enhance the regulatory effect of the CSRC’s random inspection, it becomes imperative to improve government transparency and government information disclosure. This, in turn, will stimulate greater attention from market participants such as the media and investors, consequently promoting the positive spill-over effect of the random inspection on social supervision.

Acknowledgments

This study was supported by the National Natural Science Foundation of China [Grant No. 72102244], 2022 Guangdong Provincial Social Science Planning Foundation Special Project on Major Basic Theory Research [Grant No. GD22ZDZGL02], and 2022 The Educational Department of Liaoning Province Basic Research Project [Grant No. LJKMR20221586].

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1 Teng et al. (Citation2022) found a significant negative market reactions when firms are inspected by the CSRC. Our results remain unchanged after controlling for the cumulative abnormal returns within one day before and after the CSRC’s random inspection announcement. We acknowledge this valuable insight from anonymous reviewers.

References

- Andrei, D., & Hasler, M. (2015). Investor attention and stock market volatility. The Review of Financial Studies, 28(1), 33–72. https://doi.org/10.1093/rfs/hhu059

- Ban, X., Jiang, Y. B., & Xu, C. X. (2022). Can the random inspection system of China securities regulatory commission restrain corporate violations? Modern Finance and Economics-Journal of Tianjin University of Finance and Economics, 42(10), 93–113. in Chinese. https://doi.org/10.19559/j.cnki.12-1387.2022.10.006

- Bian, S. B., Chen, Y., & Wang, X. X. (2022). Can high-quality interaction improve the stock market pricing efficiency? Evidence from SSE E-interaction. China Economic Quarterly, 22(3), 749–772. in Chinese. https://doi.org/10.13821/j.cnki.ceq.2022.03.02

- Chen, D. H., & Yao, Z. Y. (2018). Will government behavior definitely increase stock price synchronicity? Empirical evidence from China’s industrial policies. Economic Research Journal, 53(12), 112–128. in Chinese.

- Choi, J. H., Choi, S., Myers, L. A., & Ziebart, D. (2019). Financial statement comparability and the informativeness of stock prices about future earnings. Contemporary Accounting Research, 36(1), 389–417. https://doi.org/10.1111/1911-3846.12442

- Correia, M. M. (2014). Political connections and SEC enforcement. Journal of Accounting and Economics, 57(2), 241–262. https://doi.org/10.1016/j.jacceco.2014.04.004

- Dasgupta, S., Gan, J., & Gao, N. (2010). Transparency, price informativeness, and stock return synchronicity: Theory and evidence. Journal of Financial and Quantitative Analysis, 45(5), 1189–1220. https://doi.org/10.1017/S0022109010000505

- Dong, Y., & Ni, C. (2014). Does limited attention constrain investors’ acquisition of firm‐specific information? Journal of Business Finance & Accounting, 41(9–10), 1361–1392. https://doi.org/10.1111/jbfa.12098

- Drake, M. S., Roulstone, D. T., & Thornock, J. R. (2012). Investor information demand: Evidence from Google searches around earnings announcements. Journal of Accounting Research, 50(4), 1001–1040. https://doi.org/10.1111/j.1475-679X.2012.00443.x

- Feng, X. N. (2014). Does investors have information acquisition ability? Evidence from management earning forecast in China. China Economic Quarterly, 13(3), 1065–1090. in Chinese. https://doi.org/10.13821/j.cnki.ceq.2014.03.013

- Gassen, J., Skaife, H. A., & Veenman, D. (2020). Illiquidity and the measurement of stock price synchronicity. Contemporary Accounting Research, 37(1), 419–456. https://doi.org/10.1111/1911-3846.12519

- Gul, F. A., Kim, J.-B., & Qiu, A. A. (2010). Ownership concentration, foreign shareholding, audit quality, and stock price synchronicity: Evidence from China. Journal of Financial Economics, 95(3), 425–442. https://doi.org/10.1016/j.jfineco.2009.11.005

- Gunny, K. A., & Hermis, J. M. (2020). How busyness influences SEC compliance activities: Evidence from the filing review process and comment letters. Contemporary Accounting Research, 37(1), 7–32. https://doi.org/10.1111/1911-3846.12507

- Gu, X. L., Xin, Y., & Teng, F. (2016). Does external enforcement actions have governance effect? Discussion on the duality of stock price synchronicity indicators. Nankai Business Review, 19(5), 41–54. in Chinese. https://doi.org/10.3969/j.issn.1008-3448.2016.05.005

- He, Z. T. (2020). Publishing administrative illegal information as reputation penalty: Logical proof and system design. Administrative Law Review, 124(6), 78–89. in Chinese.

- Huang, J., & Guo, Z. R. (2014). News media coverage and capital market pricing efficiency: An analysis based on stock price synchronicity. Journal of Management World, 5, 121–130. in Chinese. https://doi.org/10.19744/j.cnki.11-1235/f.2014.05.010

- Huang, B., & Jiang, H. D. (2022). Investors’ lottery-like preference and synchronicity in stock prices: Evidence from China’s stock markets. Nankai Economic Studies, 6, 182–200. in Chinese. https://doi.org/10.14116/j.nkes.2022.06.010

- Huang, S. S., Qian, S. P., & He, J. Y. (2020). An experimental study on the regulatory effect of “double random and one open” food industry. Journal of Nanjing University of Finance and Economics. 1, 64–73. in Chinese. CNKI:SUN:NJJJ.0.2020-01-007

- Hu, Y., Li, X., Goodell, J. W., & Shen, D. (2021). Investor attention shocks and stock co-movement: Substitution or reinforcement? International Review of Financial Analysis, 73, 101617. https://doi.org/10.1016/j.irfa.2020.101617

- Jin, Z. (2010). New accounting standard, accounting information quality and stock price synchronicity. Accounting Research, (7), 19–26. https://doi.org/10.3969/j.issn.1003-2886.2010.07.003

- Jin, L., & Myers, S. C. (2006). R2 around the world: New theory and new tests. Journal of Financial Economics, 79(2), 257–292. https://doi.org/10.1016/j.jfineco.2004.11.003

- Khlif, H., Samaha, K., & Amara, I. (2021). Internal control quality and voluntary disclosure: does CEO duality matter? Journal of Applied Accounting Research, 22(2), 286–306. https://doi.org/10.1108/JAAR-06-2020-0114

- Kong, Q. S., Zhang, Q., Yang, H. X., & Wen, D. C. (2021). Product quality supervision model of random inspections. Chinese Journal of Management Science, 29(3), 80–89. in Chinese. https://doi.org/10.16381/j.cnki.issn1003-207x.2018.1128

- Lee, D. W., & Liu, M. H. (2011). Does more information in stock price lead to greater or smaller idiosyncratic return volatility? Journal of Banking & Finance, 35(6), 1563–1580. https://doi.org/10.1016/j.jbankfin.2010.11.002

- Li, B., Rajgopal, S., & Venkatachalam, M. (2014). R2 and idiosyncratic risk are not interchangeable. The Accounting Review, 89(6), 2261–2295. https://doi.org/10.2308/accr-50826

- Liu, H. X., Li, J. Z., & Ma, Y. B. (2022). CSRC’s random inspection and audit quality: Quasi natural experiment based on the on-site inspection of listed companies by CSRC. Auditing Research, 2, 94–106. in Chinese. https://doi.org/10.3969/j.issn.1002-4239.2022.02.011

- Liu, Y. Y., Lu, J. W., & Ning, C. (2021). Can CSRC random inspection improve the accounting information quality of listed companies. Journal of Shanxi University of Finance & Economics, 43(12), 111–126. in Chinese. https://doi.org/10.13781/j.cnki.1007-9556.2021.12.009

- Liu, J. Y., & Shen, Y. J. (2021). Regulatory effect of CSRC’s random inspection: Spillover or substitution? From the perspective of stock exchanges and auditors. Auditing Research, 4, 77–87. in Chinese. https://doi.org/10.3969/j.issn.1002-4239.2021.04.009

- Liu, G. Q., & Wang, D. (2021). How does government accounting supervision affect earnings management: Quasi natural experiment based on the inspection program of accounting information quality of Ministry of Finance. Journal of Management World, 37(5), 157–169. in Chinese. https://doi.org/10.19744/j.cnki.11-1235/f.2021.0071

- Luo, Q., Wu, N. Q., Su, Y. Y., & Yu, T. Q. (2021). Investor earnings optimism and manager’s catering: Evidence from social media sentiment analysis. China Industrial Economics, 11, 135–154. in Chinese. https://doi.org/10.19581/j.cnki.ciejournal.2021.11.008

- Lu, Y., & Shen, X. L. (2011). Information content of stock prices and earnings management: Evidence from the Chinese stock markets. Journal of Financial Research, 12(1), 131–146. in Chinese.

- Lu, F. C., & Wang, S. K. (2021). A well-functioning government from the perspective of history and practice: Based on the socialist political economics with Chinese characteristics. Journal of Management World, 37(9), 77–90. in Chinese. https://doi.org/10.19744/j.cnki.11-1235/f.2021.0138

- Morck, R., Yeung, B., & Yu, W. (2000). The information content of stock markets: Why do emerging markets have synchronous stock price movements? Journal of Financial Economics, 58(1), 215–260. https://doi.org/10.1016/S0304-405X(00)00071-4

- Nie, H. H., Han, D. L., Ma, L., & Zhang, N. D. Y. (2018). Ranking of government and business relations of Chinese cities (2017). National Academy of Development and Strategy, Renmin University of China. in Chinese. http://nads.ruc.edu.cn/zkcg/ndyjbg/c9ad75bec3024ec0bb24e4fc6b7d3c14.htm

- Peterson, K., Schmardebeck, R., & Wilks, T. J. (2015). The earnings quality and information processing effects of accounting consistency. The Accounting Review, 90(6), 2483–2514. https://doi.org/10.2308/accr-51048

- Preacher, K. J., & Hayes, A. F. (2004). SPSS and SAS procedures for estimating indirect effects in simple mediation models. Behavior Research Methods, Instruments, & Computers, 36(4), 717–731. https://doi.org/10.3758/BF03206553

- Roll, R. (1988). R2. The Journal of Finance, 43(3), 541–566. https://doi.org/10.1111/j.1540-6261.1988.tb04591.x

- Teng, F., Xia, X., & Xin, Y. (2022). CSRC’s random inspections and standard operations of listed companies. Journal of World Economy, 45(8), 109–132. in Chinese. https://doi.org/10.19985/j.cnki.cassjwe.2022.08.007

- Teng, F., Xin, Y., Shu, Q., & Xu, L. P. (2020). The helping hand: Stock price crash risk and government subsidy. Accounting Research, (6), 49–60. in Chinese. https://doi.org/10.3969/j.issn.1003-2886.2020.06.004

- Wang, M. Z., & Li, D. (2019). New audit reporting and stock price synchronicity. Accounting Research, (1), 86–92. in Chinese. https://doi.org/10.3969/j.issn.1003-2886.2019.01.013

- Wang, H. J., & Ma, X. L. (2017). Government transparency, media supervision, and government audit performance: Empirical evidence from provincial board data. Journal of Nanjing Audit University, 14(3), 86–94. in Chinese.

- Wang, Y., & Yu, L. (2013). State-owned bank loan and stock price synchronicity. China Journal of Accounting Studies, 1(2), 91–113. https://doi.org/10.1080/21697221.2013.809503

- Waymire, G. (1984). Additional evidence on the information content of management earnings forecasts. Journal of Accounting Research, 22(2), 703–718. https://doi.org/10.2307/2490672

- Wen, H., Gao, H., Chen, S. C., & Xiao, J. L. (2020). Administrative supervision over audit firms and stock price crash risk: Evidence from CSRC’s random inspection. Systems Engineering-Theory & Practice, 40(11), 2769–2783. in Chinese.

- West, K. (1988). Dividend innovations and stock price volatility. Econometrica, 56(1), 37–61. https://doi.org/10.2307/1911841

- Xu, N. H., Yu, S. Y., & Yi, Z. H. (2013). Herding behavior of institutional investors and the risk of stock price crash risk. Journal of Management World, 7, 31–43. in Chinese. https://doi.org/10.19744/j.cnki.11-1235/f.2013.07.004

- Yi, Z. H., Yang, S. Z., & Chen, Q. Y. (2019). Could analysts reduce stock price synchronicity: A textual analysis based on analyst report. China Industrial Economics, 1, 156–173. in Chinese. https://doi.org/10.19581/j.cnki.ciejournal.2019.01.009

- You, J. X., Zhang, J. S., & Jiang, W. (2007). Institution building, firm-specific information and the synchronicity of stock prices: A R2 based perspective. China Economic Quarterly, (1), 189–206. in Chinese. CNKI:SUN:JJXU.0.2007-01-010

- Zhang, G., Chen, S., Zhang, P., & Lin, X. (2022). Does the random inspection reduce audit opinion shopping? China Journal of Accounting Studies, 10(4), 528–548. https://doi.org/10.1080/21697213.2022.2143685

- Zhang, Y. L., Cui, H. T., Li, Q., & Bai, Q. C. (2022). Study on the influence of media attention on stock pricing efficiency. Review of Investment Studies, 41(9), 143–158. in Chinese.

- Zhao, T. J., Li, C., & Zhang, B. S. (2020). Industrial network and the information efficiency of capital market: An evidence based on stock price synchronicity. Accounting Research, (10), 136–149. in Chinese.

- Zheng, J. D., Lv, X. L., Lv, B., & Guo, F. (2022). Information interaction on social media platforms and capital market pricing efficiency: Evidence from big data of stock message board. Journal of Quantitative & Technological Economics, 39(11), 91–112. in Chinese. https://doi.org/10.13653/j.cnki.jqte.2022.11.005

- Zhong, Q. L., & Lu, Z. F. (2018). Can market liberalization improve the stock price informativeness? Evidence from Shanghai-Hong Kong stock connect. Journal of Management World, 34(1), 169–179. in Chinese. https://doi.org/10.2139/ssrn.3483638

- Zhou, J. (2014). Corporate governance, institutional ownership, and stock price synchronicity. Journal of Financial Research, 8, 146–161. in Chinese. CNKI:SUN:JRYJ.0.2014-08-010

- Zhu, H. J., He, X. J., & Tao, L. (2007). Can securities analysts improve the efficiency of capital market in China. Journal of Financial Research, (2), 110–121. in Chinese. CNKI:SUN:JRYJ.0.2007-02-010