Abstract

This study aims to assess academics’ comprehension of the relevance of international financial reporting standards (IFRS) integration, as well as its implications on how IFRS are included into accounting curricula and academics’ awareness of these plans. This research also sought to examine the impact of academics’ plans to include IFRS into the curriculum. These statistics were submitted by 119 academics teaching at the undergraduate level in the accounting departments of Yemeni University. The findings indicate that academics’ expertise has a positive impact on their IFRS integration objectives. The data indicate that while stakeholders have a substantial and positive impact on IFRS integration and academic objectives, this effect is not uniform.

1. Introduction

The accounting industry was not exempt from changes in the financial and corporate sectors. Instead, it saw a real improvement in terms of global norms (Russell et al., Citation2000). The International Financial Reporting Standards (IFRS) have been a topic of research in various regions, including Africa and Europe. Studies conducted by (O Cualain & Tawiah, Citation2023; Tawiah, Citation2019; Tawiah & Boolaky, Citation2020) have provided valuable insights into the challenges and opportunities of implementing IFRS in different regions, as well as the role of enforcement in ensuring their effective adoption. Experts in the field of accounting and academia agree that there is a widening gulf between what students learn and what professionals really do (Hayek et al., Citation2013; Nassar & Al-Khadash Osama, Citation2013). Universities require a framework to assist them design a course of study that can support graduate students as they start their transition to a professional qualification curriculum because they anticipate accounting education to deliver a regular and consistent stream of courses. Educational and professional institutions are needed to adapt to any changes and stay current due to the increasing accounting standards, rules, and practices. However, given the global tendency to embrace IFRS, students who do not understand IFRS as learning outcomes would surely leave the competitive market (Abou-El-Sood & Ghoniem, Citation2021; Russell et al., Citation2000; Sayed Ahmad & Zalzali, Citation2022).

In the context of Yemen, most instruction at Yemeni institutions is given in an old-fashioned manner, with professors giving lectures and students taking notes. The majority of exam questions for students still require them to memorize information, with little focus on their ability to analyze or solve problems (World Bank, Citation2010). Regarding the accounting education in Yemen, there are three categories in accounting education: (1) a four-year bachelor’s program following secondary school, (2) a two-year diploma program at a commercial institute, and (3) professional certificates. To become a professionally designated Yemeni Certified Public Accountant (YCPA), an individual must complete a four-year undergraduate accounting degree at a post-secondary institution, three to four years of work experience, one to two years for holders of a master’s degree in accounting, and six months after graduation for holders of a doctorate in accounting, with the exception of those who have taught accounting and auditing at one of the universities. Additionally, a national professional examination is required.Footnote1 According to the work of the Yemeni Certified Public Accountants Association (YCPAA) and the Licensing Committee of the Ministry of Industry and Commerce, Yemen has taken the first step toward IFRS adoption. On 1 January 2020, Cabinet Decision No. 51 of 2019 was issued regarding the adoption and application of IFRS, International Auditing Standards (IAS), and international rules and ethics in the Republic of Yemen.Footnote2 In addition, Yemen is an Associate member of the IFAC through the Yemeni Association of Certified Public Accountants (YACPA), which will have a significant impact on the reshaping of accounting education in Yemen (IFAC, Citation2021).

However, there is a lack of research on accounting education in Yemen and other underdeveloped countries. Several studies have been conducted in (Al-Absy, Citation2015; Al-Hattami, Citation2021; Al-Mujtaba & Al-Mawry, Citation2018)., with some focus on addressing concerns about International Financial Reporting Standards (IFRS) (Al-Absy, Citation2015). Al-Absy found that 41.5% of respondents believed it would take more than 10 years for Yemen to implement IFRS, while 58.6% said it would take 3 to 10 years, suggesting that IFRS is not included in the curriculum. Al-Absy recommended that the Yemeni Certified Public Accountants Association (YCPAA) and government officials carefully consider how to apply IFRS in Yemen. However, his study was limited to 48 Yemeni postgraduate accounting students enrolled in public institutions in Malaysia, which is a small sample. By contrast, this study focuses on selecting a model that considers suitable and relevant participants and a representative sample of notable and leading colleges across Yemen.

Nevertheless, according to Al-Mujtaba and Al-Mawry (Citation2018), the quality of Yemeni accounting education has been hampered and underestimated due to the country’s failure to comply to worldwide norms of accounting education. To do so, he zeroed in on how the presence of foreign auditing companies in Yemen might affect efforts to bring academic institutions there up to international standards in accounting education. He surveyed educators and auditors in the field of accounting to get a sense of how IFRS is now being taught in classrooms and how much academic institutions plan to embrace it in the future. In order to ascertain if Yemen’s accounting curriculum meets IT industry standards, Al-Hattami (Citation2021) also polled graduate students. He discovered that the accounting curriculum does not reflect what the market expects. He affirms that adding proper information technology in the accounting curriculum may assist in meeting the demands of the IT job market and giving students a thorough grasp of the sector.

One of the most significant current discussions in accounting education research is the incorporation of IFRS into accounting curricula. Recent years have witnessed growing academic interest in the integration of IFRS, especially in countries that have recently adopted IFRS. However, few studies have focused on the status of the IFRS curriculum in the context of developing countries. The study will provide a road map to the academics, professional, and all stakeholders in to take a leap forward for further improvement to incorporate IFRS into accounting curriculum. Thus, this study makes an important contribution to the field of accounting education, providing fresh insight into the context of Yemen. Thus, it has become necessary to align accounting education curricula with IFRS due to the fast growth and adoption of IFRS (IFRS). Given all that has been said thus far, this research concludes that there aren’t enough studies about IFRS and accounting education in Yemen, therefore it aims to fill that gap. The accounting academics of Yemen, a developing nation, is the subject of this research. Therefore, the primary goal of this research is to (1) assess the effect of academics’ knowledge of IFRS integration into the accounting curriculum. (2) Examine the effect of academics being aware of their plans. (3) To determine how academics’ plan would affect how IFRS is incorporated into the accounting curriculum. (4) Assess the effect of stakeholder support on academics’ plans, awareness, and IFRS incorporation into the accounting curriculum. In the context of Yemen as a developing nation, this study adds to the body of research already done on IFRS incorporation in accounting education. Additionally, it might be claimed that this study has applications for accounting professors in Yemeni colleges, supporting the claim that it is unique research.

The study found that Academic awareness has a positive impact on the implementation of International Financial Reporting Standards (IFRS) in the accounting curriculum. However, despite the high level of academic preparation and activity, the intentions of academicians regarding IFRS have little influence on its incorporation into the accounting curriculum at Yemeni institutions, indicating the need for more action. The study also finds that stakeholder support and academic goals have negligible effects on IFRS integration, but stakeholder assistance has a significant influence on academic awareness. The demographic factors revealed that over half of the respondents lacked professional certification, highlighting the need for more professional credentials among academics. The study concludes that more work is needed to integrate IFRS into Yemen’s accounting curriculum. This research emphasizes the importance of IFRS integration in accounting curricula for producing qualified graduates, and the implications of this study can be applied to other developing countries in the Middle East. Overall, this research emphasizes the importance of IFRS integration in accounting curricula for producing qualified graduates in Yemen and other developing countries in the Middle East. The implications of this study can be applied to decision-makers, professionals, corporations, and academics. Although there are limitations to this study, it provides a solid foundation for developing a plan to adopt IFRS in the accounting curriculum. The results of this research might also have a big impact on decision-makers, professionals, corporations, and academics.

Finally, this work is divided into five important parts from section two to section six in addition to this introduction. In part two, we offer an overview of the literature pertinent to the work here and develop the hypothesis. The research model and study technique are provided in section three. The results of the study questions are presented in section four after an analysis of the collected data. The discussion of the study’s key results will take place in section five. The study’s primary conclusions and consequences are outlined in section six, along with its limitations and a possible direction for further research.

2. Literature review and hypothesis development

2.1. Awareness of academicians of integrating IFRS into the curriculum

The necessity for accounting education to be coupled with the creation of a single set of accounting standards that will serve as the basis for the industry’s common language has been motivated by the ever-increasing business circumstances in international financial markets (Puri & Singh, Citation2021). The introduction of IFRS has some ramifications for how IFRS is taught in colleges and other institutional settings. In order to reflect on IFRS adoption in the teaching process and the accounting curriculum, all stakeholders should be aware of these difficulties and their repercussions. The perception of academics, students, and audit professionals is often measured in research (Folashade et al., Citation2016; Joshi et al., Citation2008; Rivera-Valentin & North Central University, Citation2017; Sugahara, Citation2013; Zhu et al., Citation2011). Academicians have been the subject of a lot of earlier studies (Atabey et al., Citation2014; Carvalho & Bruno, Citation2013; Dong et al., Citation2019; Natoli et al., Citation2020; Rivera-Valentin & North Central University, Citation2017; Sugahara, Citation2013; Zhu et al., Citation2011). Zhu et al. (Citation2011) discovered that a number of factors, including academic staff characteristics, institutional factors, teachers’ perceptions of IFRS implementation in the US, and practical difficulties, all have a significant impact on how much time and effort instructors spend discussing IFRS in introductory accounting courses.

Rivera-Valentin and North Central University (Citation2017). find that participants had the impression that IFRS education was relevant but unprepared, and they had no plans to teach IFRS-related material. Similarly (Sugahara, Citation2013), showed that the majority of Japanese accounting academics held the opinion that the International Education Standards (IES) had little to no influence on accounting instruction. Additionally, few academics are aware of how to get beyond these barriers to global convergence. Atabey et al. (Citation2014) shed light on the amount of expertise maintained by accounting academics and recent developments in the IFRS implementation process. They demonstrate that academics consider IFRS adoption and mandated implementation to be necessities rather than alternatives. On the other hand, roughly 67 percent of participants said that it was challenging to explain the differences between IFRS and Turkish accounting standards. In the context of China, Dong et al. (Citation2019) investigated the learning approaches of IFRS among 402 Chinese undergraduates registered as ACCA students through a survey. The Association of Chartered Certified Accountants (ACCA) provides education programs for many accounting students in China to learn IFRS. This study emphasizes the significance of teaching and learning IFRS for global accounting convergence. Furthermore, Natoli et al. (Citation2020) investigate the perceptions of Chinese accounting students on the learning environment factors that influence students’ learning techniques. The researchers surveyed 497 accounting students over the age of 20 years at two Chinese institutions. The results indicated that teaching quality, defined goals, and standards were substantially connected to an in-depth learning method.

Alzeban (Citation2016) investigated the challenges that academics and educators face while instructing students. He wanted to gain an understanding of the challenges that accounting educators encounter when attempting to instruct students on IFRS material as well as the effects that various factors (teacher attitude, department size, workload, institution type, teaching experience, and materials) have on the amount of time that is spent instructing students on IFRS material in undergraduate accounting programs. He demonstrates that instructors’ time spent studying IFRS is influenced by both the attitudes of the professors and the accessibility of IFRS resources. Carvalho and Bruno (Citation2013) investigate the effect of the adoption of International Financial Reporting Standards (IFRS) on Brazilian accounting education. This study investigates the change from Brazil’s old accounting model to a principles-based approach, which presents issues for accounting instructors and undergraduate students. It also describes how IFRS adoption influences Brazil’s accounting and auditing certification processes. Overall, this study contributes to the body of knowledge by underlining the necessity of incorporating new teaching approaches to satisfy the changing needs of the accounting profession, in light of IFRS adoption.

Nonetheless, other studies have contrasted the views of academics and professionals (Mah’d & Mardini, Citation2020; Rezaee et al., Citation2010). Rezaee et al. (Citation2010), for instance, claim that effective convergence to a set of globally accepted accounting standards will benefit the majority of respondents as well as all stakeholders, including standard setters. According to Sugahara (Citation2013), Rivera-Valentin and North Central University (Citation2017), Atabey et al. (Citation2014), and Zhu et al. (Citation2011), Academicians were the focus of this research because they are more directly connected to concerns about curricula and student challenges. Therefore, it may be assumed that;

H1:

Academics’ awareness regarding IFRS has a significant effect on IFRS integration into accounting curricula.

H2:

Academics ’ awareness of IFRS integration has a significant impact on their plans to integrate IFRS into accounting curricula.

2.2. Academic plans

If there are no plans for what, when, and how, there won’t be any IFRS integration. Few scholars, nevertheless, have concentrated on this subject. Black (Citation2012) provided a comprehensive historical analysis of the occasions that resulted in the present route agenda. The proposed works should consider their professional background, evaluate how contemporary works fit with those principles, and add to the body of knowledge in accounting education given that research drives changes in accounting education. Successful course integration depends on the effectiveness of the instructors, the viability of the methodology, and the availability of the resources (Patro & Gupta, Citation2012). Wong and Wong (Citation2013) found that the vast majority of the 300 Hong Kong business students they surveyed were eager to learn about IFRS and were aware of its advantages. Additionally, Carmona and Trombetta (Citation2010) build on best practices to give a particular method for incorporating IFRS into the curricula of higher education institutions in the United States. They learned that the idea behind their suggestion was that the focus of accounting education should change from teaching constantly evolving regulations to focusing on the strategic and financial underpinnings of accounting operations. Input from academics on IFRS inclusion techniques is sought for this project. Thus, we postulate the following:

H3:

Academics plans regarding IFRS have a significant impact on IFRS integration into the accounting curricula.

2.3. Stakeholders and IFRS

Binh et al. (Citation2017) investigated how stakeholders influence the creation and implementation of accounting curriculum at a Vietnamese state-owned institution. They revealed that the government had little influence on accounting education; nevertheless, professional accounting groups and businesses had the most influence over curriculum development. Moreover, Szmanda (Citation2018) discovered that there are several potentials in active learning policies, such as settled learning, including stakeholders in promoting IFRS training at universities, and increasing respect and understanding for process convergence.

Moving further, stakeholders might design accounting and delivery strategies coursework that encourages the use of active learning policies as part of the established learning model (Arnseth, Citation2008; James et al., Citation2003; Szmanda, Citation2018). The disparity in IFRS education and knowledge may reveal a concealed gap in preparation among associated stakeholders and local institutions. Nwaiwu and Macgregor (Citation2018) revealed that there are no variations in preparedness for adoption between academics and practitioners. Furthermore, improving IFRS education among firms, academics, and Japanese stakeholders is critical to ensuring effective implementation (Rivera-Valentin & North Central University, Citation2017). In this context, the current research investigated academics’ perceptions on the support responsibilities of stakeholders such as governmental institutions, appropriate authorities, and the corporate sector. As a result, it is possible to speculate that;

H4:

Stakeholder support has a significant impact on academic plans for IFRS integration into accounting curricula.

H5:

Stakeholder support has a significant impact on academic awareness.

H6:

Stakeholder support for IFRS integration has a significant impact on accounting curricula.

3. Methodology

A quantitative analytical approach was used in this research to explore the important correlations between variables. A questionnaire was used to gather data from Yemeni universities. The data were further analysed using SPSS software and partial least squares structural equation modeling (PLS-SEM).

3.1. Survey instrument and measurement

Previous research was used to develop methods for assessing the variables. The survey questionnaire included 27 indicators for assessing academic awareness, academic planning, stakeholder support, and IFRS incorporation in the accounting curriculum. The inclusion of IFRS into the accounting curriculum is the independent variable. Six questions were used and altered to assess IFRS integration created by IES2 IFAC (Citation2019), while five items were adopted and adapted from KPMG and AAA (2014) to measure academics’ goals using two latent variables (course type and faculty members preparation). The authors created eight questions to assess stakeholder support.

3.2. Sampling and data collection

3.2.1. Sampling

Yemen has 42 universities with accounting departments, consisting of 12 public and 30 private universities. J. F. Hair et al. (Citation2021) recommend that researchers consider power tables (Cohen, Citation1992). According to the table proposed by Cohen, J A regarding the sample size recommendation in PLS-SEM for a statistical power of 80%, the sample size was determined by considering R2 (0.10,0.25,0.50, and 0.70) at any significant level of the structural model at 1%, 5%, and 10%. It was assumed that 80% of the commonly used level of statistical power (Cohen, Citation1992) and the maximum number of arrows point to a construct in the PLS path model. In this study, there were six arrows pointing to the construct in the structural model. To achieve a statistical power of 80% for detecting R2 values of at least 0.25, 80 participants were required (Cohen, Citation1992). However, the sample selected in this study consisted of 119 participants, which is above the minimum sample size.

3.2.2. Data collection

Several studies have given questionnaires to students (Folashade et al., Citation2016; Patro & Gupta, Citation2012; Rich et al., Citation2012; Santos & Clayton Quilliam, Citation2013; Wong & Wong, Citation2013). Academics working in accounting departments in Yemeni universities were chosen as targeted respondents for the questionnaire (Alzeban, Citation2016; Julieth et al., Citation2016; Sugahara, Citation2013) because they are most familiar with the teaching process and the state of the IFRS curriculum. The first of the six sections in the questionnaire structure for this study was devoted to gathering data from respondents. With the third section, Measure, including FRS in the accounting curriculum, the second component was created to gauge academics’ awareness of the incorporation of IFRS in the accounting curriculum. We evaluate academics’ suggestions to add IFRS to the accounting curriculum in the fourth segment. In the fifth section, we assess stakeholder support for IFRS integration in the accounting curriculum. A total of 119 participants representing nine public universities and five private universities were selected. A total of 119 responses out of 179 were used to compile the data. A 67 percent response rate was recorded in the data collected.

To disseminate the questionnaire, the researchers chose a sample of academicians teaching at the undergraduate level in Yemeni institutions based on their academic and practical contact with their colleagues. Google Forms was used to conduct the surveys. A total of 119 replies were received, representing 13 institutions:93% of public universities and 7% of private universities. The final data were statistically analyzed using SPSS 20 and Smart PLS-SEM 03Data Analysis and Findings

3.3. Profile of respondents

Table (panel B) reveals that the bulk of the sample was male (96.6%), whereas just 3.4% of the sample consisted of females. The low participation of women in the survey conducted in Yemen can be attributed to several factors. First, the low representation of women in the accounting profession and education in Yemen, a patriarchal and conservative society, has resulted in fewer women being eligible to participate in the survey. Additionally, accessing female respondents has been a challenge as they are less likely to respond to online surveys or share their contact information with strangers. The low participation of women in the survey could have a significant impact on the generalizability of the results, given that the views and experiences of females may differ from those of their male counterparts. Therefore, it is important to address this gap in future research by implementing different methods and strategies to increase the response rates of female respondents.

Table 1. Participants’ demographic information

47.9 percent were between the ages of 40 and 49, 38.7 percent were between the ages of 30 and 39, and 13.4 percent were older than 49. The qualifications in panel C reveal that the sample consists of three levels: bachelor’s, master’s, and Ph.D., with 47.9 percent of the sample holding a Ph.D., 35.3 percent holding a master’s, and 16.7 percent holding a bachelors. Panel E represents the years of experience of the sample’s members. It reveals that 6–10 years of experience account for the biggest proportion of the sample (28.6 percent), while 1–5 years account for 23.5 percent of the sample. Experience between 16- and 20 years accounts for 21% of all participants, whereas experience between 16 and 20 years and above 20 years accounts for 18.5% and 8.4%, respectively.

Panel F represents academic participants’ experience in teaching about IFRS, while Panel G represents academic participants’ experience in applying IFRS in the real world. As can be seen in Panel F, 82.4 percent of respondents hold some sort of teaching certification. To the contrary, 17.6% of the people surveyed lacked IFRS-related teaching competence, which likely contributed to the inclusion of IFRS in IFRS. There was an abundance of IFRS expertise among panelists G, with around 67.2% possessing hands-on experience. Yet, 32.8% have no real-world experience, which might increase the gap between theory and practice. Professionally certified and academically credentialed respondents are broken down into five distinct groups in Panel H. (accountants, YCPA, CMA, ACCA, and others).

3.4. Descriptive analysis

The descriptive data for academic activities indicated a mean score of 3.16 (SD = 0.94). This demonstrated a modest amount of academic planning in relation to academic engagement. Attending scientific seminars or introductory IFRS workshops has the highest mean value, showing that academics give greater attention to plans for attending scientific seminars or introductory IFRS workshops. Academics’ preparedness as a component of academic plans indicated a mean score of 3.99 (SD = 0.60), suggesting a high degree of academic preparation and favorable perception among academicians about academicians’ readiness. The total mean score for IFRS integration in Table is 3.18 (SD = 0.67), suggesting a modest degree of IFRS integration. Applying accounting principles to transactions and other events had the greatest level, with a mean of 3.83; applying (IFRSs) or other applicable standards to transactions and other events, as well as Interpreting reports that contain non-financial facts and information, had the lowest mean.

According to course type and academic preparation, academic awareness was evaluated. shows that the overall mean score for course type is 3.20 (SD = 0.81), indicating a modest degree of academic understanding of course type. The university’s independent training courses are determined by the highest mean score. In contrast, the preparations of faculty members yielded an aggregate mean score of 3.92 (SD = 0.70). This demonstrates a high degree of academic sensitivity about the training of faculty members. A mean score of 3.55 (SD = 0.86) for stakeholder support indicated good stakeholder support. The highest support was reported for the Yemeni Association of Certified Public Accountants (YACPA) with a mean of 4.02, indicating that (YACPA) played a significant role in supporting universities for IFRS integration. The lowest support was reported for the Ministry of Higher Education and Scientific Research with a mean of 3.11, indicating that the Ministry has a moderate level of supporting universities for IFRS integration.

Table 2. Statistics of descriptive

3.5. Structure equation modelling results

This research utilised a reflective-formative model of a hierarchical latent variable. To estimate the hierarchical latent variable model (Becker et al., Citation2012; Sarstedt et al., Citation2019), which does not need an equal amount of indicators from the LOCs, a disjoint two-stage procedure was used. Because higher-order constructions in the second stage are formative, Becker et al. (Citation2012) used a disjoint two-stage with mode B for higher-order constructs. The two-stage method is advantageous because it estimates a simple model for higher-level analysis without requiring lower-order components (Becker et al., Citation2012). Using PLS-SEM, the two-stage technique calculates the latent variable scores, allowing for the estimation of lower-order latent variable scores (Chin, Citation1998; Lohmöller, Citation1989; Tenenhaus et al., Citation2005).

3.5.1. The evaluation of first-order measurement models

To estimate low-order constructions in the first step, a two-stage technique is used. The scores of the latent variables of the low-order constructs were then employed as formative indicators of the high-order constructs (Mode B)) (Becker et al., Citation2012; Sarstedt et al., Citation2019). This second-order formative construct is directly impacted by the exogenous construct and influences the final endogenous variable (see Figure ). Indicators were used to assess the four latent variables of the low-order constructs. As demonstrated in Tables , based on the requirements of the reflective measurement model, all lower-order components fulfilled all relevant criteria of internal consistency, convergent validity, and discriminant validity.

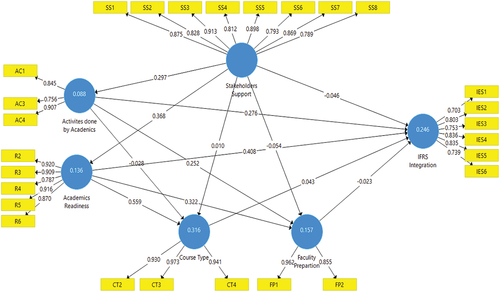

Figure 1. Measurement model (Low order construct), SS= Stakeholder Support, AC= Activities done by academicians, R= Academicians Readiness, CT= Course Type, FP= Faculty members preparation, IES= IFRS Integration.

Table 3. Reliability and convergent validity analysis

Table 4. Correlations of discriminant validity

In the evaluation of the reflective measurement model, the indicator loadings are (J. F. Hair et al., Citation2019). The factor loading refers to “the amount to which each item in the correlation matrix connects with the specified main component (Pett et al., Citation2003). Table demonstrates that the majority of measurement indicator factor loadings were over the 0.7 criterion (J. F. Hair et al., Citation2011, Citation2019; Leguina, Citation2015). Typically, Jöreskog (Citation1971) was used to determine the internal consistency dependability. Composite reliability in exploratory research is acceptable if the values are between 0.60 and 0.70, fair to excellent for values between 0.70 and 0.90, and troublesome for values of 0.95 and above (Drolet and Morrison Citation2001; Diamantopoulos et al., Citation2012). According to Table , the composite dependability statistics vary between 0.877 and 0.964%. Cronbach’s alpha findings are reported in Table . The range of Cronbach’s alpha was from 0.944 to 0.801. Both measures of dependability statistics exceeded the required.70 level (J. F. Hair et al., Citation2011, Citation2019; Henseler et al., Citation2009). Cronbach’s alpha and composite reliability were used to demonstrate concept validity (CR) (See Figure ).

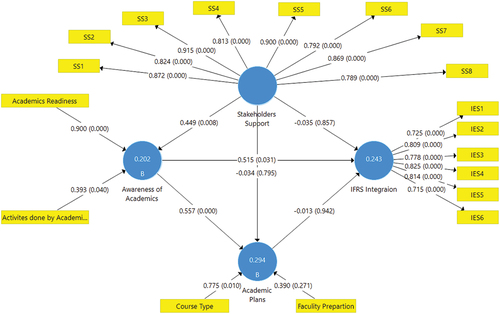

Figure 2. Structural Model - Hypotheses Testing Results, SS= Stakeholder Support, AC= Activities done by academicians, R= Academicians Readiness, CT= Course Type, FP= Faculty members Preparation, IES= IFRS Integration..

3.5.2. Convergent validity

“Convergent validity is the degree of agreement between various measures of the same idea. The premise is that two or more measurements of the same object should have greater covariance if they are reliable measures of the concept (Bagozzi et al., Citation1991. when the AVE value was equal to or higher than the suggested value of 0.50 (Claes & Larcker, Citation2018). Table AVE figures demonstrate that all constructions’ AVE values were more than 0.5, ranging from 0.608% to 0.8999%. It was determined that the measurements of all 11 first-order constructs had good degrees of convergent validity. In conclusion, after eliminating (AC2, CT1, FP3, and R1), the outer loadings of all 11 indicators for constructs met the first condition for convergent validity.

3.5.3. Discriminant validity

“Discriminant Validity is the degree to which measurements of diverse concepts may be distinguished.” If two or more ideas are distinct, then their respective valid metrics should not correlate excessively (Bagozzi et al., Citation1991). Discriminant validity is achieved when the square root of the AVE for a concept exceeds its correlation with all other constructs (Claes & Larcker, Citation2018). Table demonstrates that the association between the construct square root of AVE and all other constructs is stronger than that of the construct square root of AVE. Consequently, it offers robust evidence for the creation of discriminant validity.

In addition, the HTMT is based on a correlation calculation between components. Based on the HTMT ratio, discriminant validity was determined. However, the threshold of 0.90 proposed by Henseler et al. (Citation2015). Table demonstrates that the HTMT ratio of all constructs was less than the needed threshold of 0.90, establishing discriminant validity.

Table 5. Discriminant validity—HTMT

In brief, four indications (AC2, CT1, FP3, and R1) were eliminated at this stage. All of the aforementioned findings imply that all evaluation requirements for the low-order measurement models were fulfilled, hence establishing the reliability, convergent validity, and discriminant validity of all measures (Sarstedt et al., Citation2019).

3.5.4. High-order measurement model evaluation

3.5.4.1. Validating high order construct

The study’s higher-order construct, academicians’ awareness, was derived from two lower-order constructs, academicians’ IFRS-related actions and academicians’ preparedness. In addition, the IFRS-related academic plan was a higher-order construct built on two lower-order constructs: course type and academic preparation for IFRS. In the second step, they were employed as indicators to measure the high-order latent variable (Sarstedt et al., Citation2019). Redundancy analysis, outer weights, outer loadings, and VIF were assessed to demonstrate the validity of higher-order formative conceptions.

As convergent validity needs formative constructs, we undertake a redundancy analysis to demonstrate convergent validity (Chin, Citation1998). We incorporated a single item that reflects the core of academics’ awareness and academic goals in order to undertake redundancy analysis (Cheah et al., Citation2018). According to Sarstedt et al. (Citation2022), the correlation between formative measured constructs and reflective measured items should be greater than or equal to 0.7008. This study reveals path coefficients of 0.824 and 0.967 for the academicians’ awareness and academic plans constructs, which are above the acceptable threshold of 0.708. Consequently, convergent validity was shown. Examine the formative model for collinearity difficulties. When VIF values exceed five, collinearity concerns exist (J. F. Hair et al., Citation2021). All VIF readings were less than the suggested threshold of 5 in the current investigation (Sarstedt et al., Citation2016). The statistical significance and significance of the outer weight were then evaluated. Significant outside weights were discovered in Table (Sarstedt et al., Citation2016). The outside weights of the faculty members’ preparation were negligible, but their outer loading was much over 0.50; hence, the indicator should be viewed as absolutely significant, as opposed to moderately significant. Consequently, faculty members’ preparations are often preserved (Hair et al., Citation2019) In addition, Table demonstrates that outer loadings were found to be greater than 0.50 for each of the lower-order constructs (Sarstedt et al., Citation2019), with the exception of the outer loadings of academic activities, which were slightly below 0.5; however, its outer weights were significant, so the indicator should be interpreted as relatively significant. Therefore, academicians’ activities would largely be preserved (J. Hair et al., Citation2017). In this manner, higher-order formative conceptions are progressively validated. Since all conditions were satisfied, the HOC’s legitimacy was proven.

Table 6. Higher order construct validity

3.6. Structural model (inner model) assessment

3.6.1. Hypotheses testing

The evaluation of stage two outcomes concludes with a discussion of the structural model. The study demonstrates that the other structural model assessment outcomes (e.g., significance and relevance for path coefficients, Q2, PLS predict) support the predicted link to validate the offered hypotheses (Sarstedt et al., Citation2019).

H1 examines whether academic knowledge has a substantial impact on the incorporation of IFRS into the accounting curriculum. The findings indicate that the knowledge of academics has a considerable and favorable effect on the incorporation of IFRS into the accounting curriculum. (B = 0.515, t = 2.159, p < 0.05). H1 is thus supported. In addition, H2 examines whether academics’ knowledge has a substantial impact on their intentions for IFRS incorporation into the accounting curriculum. The findings indicate that academics’ knowledge of IFRS has a considerable and beneficial effect on the incorporation of IFRS into the accounting curriculum. (B = 0.557, t = 5.141, p < 0.001). H2 is thus supported. Moreover, H3 determines if academic plans concerning IFRS have a major impact on the incorporation of IFRS into accounting courses. The findings indicate that academic strategies addressing IFRS have little effect on the incorporation of IFRS into the accounting curriculum (B = −0.013, t = 0.073, p > 0.05). Therefore, H3 was unsupported. Moreover, H4 evaluates the impact of stakeholder support on academic strategies for IFRS incorporation into the accounting curriculum. The findings indicate that the influence of stakeholder support on academic plans for IFRS integration in the accounting curriculum is negligible. (B = −0.034, t = 0.259, p > 0.05). Therefore, H4 is unsupported.

H5 investigates if assistance from stakeholders has a major impact on academic awareness. The findings demonstrated that stakeholder support has a substantial and favorable effect on academic awareness. (B = 0.449, t = 2.638, p < 0.05). H5 is thus supported. Finally, H6 investigates whether stakeholder support has a substantial impact on the incorporation of IFRS into accounting courses. The findings indicate that the influence of stakeholder support on the incorporation of IFRS within the accounting curriculum is negligible. (B = −0.035, t = 0.180, p > .0.05). Therefore, H6 is unsupported.

3.6.2. Predictive relevance of the model

While R2 measures the model’s predictive power inside the sample (Rigdon, Citation2012), Q2 calculates the model’s predictive power outside the sample (Galit & Koppius, Citation2011; Shmueli, Citation2010). R2 estimates the variation that is explained by each endogenous construct, and so is a measure of the model’s explanatory ability (Galit & Koppius, Citation2011). R2 is also known as in-sample predictive capacity (Rigdon, Citation2012). R2 scores varied from 0 to 1, with higher values suggesting a larger capacity for the explanation. R2 values of 0.75, 0.50, and 0.25 might be regarded as considerable, moderate, and weak, respectively (J. F. Hair et al., Citation2011; Henseler et al., Citation2009). Table reveals that academic plans (0.294), academic awareness (0.202), and IFRS integration (0.243) show limited predictive power within the sample. In some research, an R2 value as low as 0.10 is deemed adequate (Raithel et al., Citation2012).

Table 7. Structural model – hypotheses testing

In addition, the Q2 of Construct Cross validated Redundancy demonstrated the prediction accuracy of the route model (Geisser, Citation1974; Stone, Citation1974). Q2 values greater than 0, 0.25, and 0.50, respectively, imply modest, medium, and substantial predictive importance (J. F. Hair et al., Citation2019). Table reveals that academic plans (0.137), academic awareness (0.058), and IFRS integration (0.116) imply that the predictive significance of the PLS-path model is modest. The standard root means square residual (SRMR) may also be used as a measure of fit. A number less than 0.10 or 0.08 is deemed acceptable (Li Tze & Bentler, Citation2009). The findings revealed that the SRMR value was 0.085, which was less than the minimum value of 0.10, suggesting a satisfactory model fit (J. F. Hair et al., Citation2019).

Table 8. Model goodness, predictive relevance, and model fit

PLS predict-based was used to evaluate the predictive capacity of the model by calculating the root mean squared error (RMSE) and the mean absolute error (MAE). PLS predict evaluates the prediction error for all endogenous construct indicators (J. F. Hair et al., Citation2019). Comparing PLS-SEM analysis against the naive LM benchmark in terms of RMSE and MAE values demonstrates the predictive potential of the model (Danks & Ray, Citation2018; Shmueli et al., Citation2019). Table demonstrates that all indicators in the PLS-SEM study had greater RMSE prediction errors than the naive LM benchmark, indicating a strong predictive potential. Thus, the model’s predictive validity was demonstrated.

Table 9. Prediction relevance of the model

4. Discussion

One of the most significant current discussions in accounting education research is the incorporation of the International Financial Reporting Standards (IFRS) into accounting curricula. While there has been growing academic interest in the integration of IFRS, especially in countries that have recently adopted the standards, few studies have focused on the status of the IFRS curriculum in the context of developing countries. This study makes an important contribution to the field of accounting education by providing fresh insights into the context of Yemen. Academics were the focus of this research since they are crucial to the accounting education process input (Alzeban, Citation2016; Julieth et al., Citation2016; Sugahara, Citation2013). This study demonstrates that academic awareness has a substantial and favorable effect on the incorporation of IFRS into the accounting curriculum. This finding is consistent with that of Atabey et al. (Citation2014), who determined that academic knowledge may serve as a starting point for implementing IFRS in accounting education. In addition, IFRS-related academic activities are modest in size, indicating that further activities are necessary. A high level of academic readiness indicates that educators are ready to incorporate IFRS into plans and curricula, create theoretical and practical IFRS materials, allocate sufficient resources to adopt IFRS, prepare teachers to effectively communicate IFRS, schedule students to begin IFRS education, and help teachers accept necessary changes. This result agrees with that of Santos and Clayton Quilliam (Citation2013). Moreover, this study reveals that IFRS integration into accounting courses in Yemeni universities is still modest and incomplete. This reasoning was congruent with that of Al-Mujtaba and Al-Mawry (Citation2018). Al-Mujtaba and Al-Mawry (Citation2018) discovered that educational institutions in Yemen have failed to implement worldwide accounting education standards, which has hindered the quality of accounting education in Yemen and caused it to be devalued compared to the global business environment.

In addition, the findings demonstrate that academics’ understanding of IFRS has a considerable and beneficial influence on their intentions to incorporate IFRS into the accounting curriculum. This study demonstrated that academics considered their preparation positively, which validates the results of Rezaee et al. (Citation2010). In accordance with our results, a thorough transition strategy should be considered when implementing the IFRS. According to the majority of academics (Rezaee et al., Citation2010), strategies for IFRS integration in the accounting curriculum are essential for IFRS convergence. However, this research reveals that academics’ IFRS plans have little effect on the integration of IFRS into accounting curricula, showing that academics’ intentions must be turned into action.

Lastly, the findings demonstrate that the support of stakeholders had little effect on the incorporation of IFRS into the accounting curriculum, showing a lack of coordination and cooperation between institutions and stakeholders. These results indicate that stakeholder support has a substantial effect on academic awareness. This study implies that stakeholder assistance plays an important role in enhancing academic awareness. The Yemeni Association of Certified Public Accountants (YACPA) supports IFRS inclusion in the accounting curriculum the most, which is a favorable sign for the integration process (Sugahara, Citation2013), whereas the Ministry of Higher Education and Scientific Research has modest support. However, stakeholder support has little effect on academic intentions for IFRS integration into accounting courses, indicating that the IFRS integration process requires more work and support. This result supports the conclusion of Nwaiwu and Macgregor (Citation2018). He concludes that all levels of government, financial regulatory authorities, professional accountancy organizations, private and public enterprises and institutions, and accounting firms must expedite IFRS education to increase local acquisition of IFRS competencies. These findings contribute to the research gap by providing fresh insight into the context of Yemen and highlighting the need for strategies for IFRS integration in developing countries, as well as the need for stakeholder support and coordination to expedite IFRS education and increase the local acquisition of IFRS competencies.

5. Conclusion

In conclusion, IFRS integration into the accounting curriculum is at a modest level, which does not meet the criteria of the labor market and may hinder graduates’ market preparedness. Academic awareness has a favorable influence on IFRS implementation in the accounting curriculum. Despite the excellent level of academic preparation and academic activity, this research also revealed that academicians’ intentions about IFRS have little effect on the incorporation of IFRS into the accounting curriculum at Yemeni institutions. This suggests that the plans must be executed. Additionally, the influence of stakeholder support on IFRS inclusion and academic goals on IFRS integration is negligible. This finding indicates that stakeholder assistance does not change the need for IFRS integration or academics’ expectations. On the other hand, this study reveals that stakeholder support has a considerable influence on academic awareness, which at least offers a silver lining for the responsibilities of stakeholders in the IFRS integration process inside the accounting curriculum. In terms of demographic factors, the survey revealed that 53 percent of the respondents lacked professional certification, indicating an absence of professional credentials among academics. In addition, this study presents a detailed evaluation of IFRS integration into the accounting curriculum in the context of Yemen, concluding that IFRS integration requires more work. This study had a problem in that its sample was nationally representative of universities, but it may have omitted crucial participants.

Importantly, this study has substantial implications, including the necessity for universities, professionals, stakeholders, and decision-makers participating in the global convergence of accounting standards to pay more attention to how IFRS is integrated into accounting curricula because refraining from doing so could lead to a catastrophic shortage of qualified graduates. As a result, the implications of this study can potentially be applied not only to Yemen as a developing country, but also to other countries in the Middle East. Thus, this research provides incremental contributions to the state of IFRS adoption into the accounting curriculum in Yemen, a poor nation, notwithstanding its limitations. This study offers a good foundation for developing a plan to adopt IFRS in the accounting curriculum. One limitation of this study is the relatively small sample size and reliance on surveys and questionnaires as the primary data collection method. Future research could benefit from expanding the sample size and utilizing additional methods such as interviews and involving practitioners to gain a more comprehensive understanding of IFRS integration into the accounting curriculum, including a more nuanced understanding of the professional perspective. Based on the findings of this study, it is recommended that colleges allocate more resources toward the integration of IFRS into the accounting curriculum to ensure that graduates are equipped with the necessary skills for the real-world job market. Additionally, this study recommends that stakeholders actively support the execution of academic plans related to IFRS integration to facilitate more effective and comprehensive implementation of IFRS in the accounting curriculum.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1. (Law no. (26) of 1999 concerning the audit profession 2021).

2. (Cabinet Resolution No. 51 of 2019 was issued regarding the adoption and application of IFRSs, 2021).

References

- Abou-El-Sood, H., & Ghoniem, W. (2021). Exploring the effectiveness of total quality management in accounting education: The case of Egypt. Accounting Education, 31(2), 134–24. https://doi.org/10.1080/09639284.2021.1942937

- Al-Absy, M. S. M. (2015). Accountants’ perception on the factors affecting the adoption of international financial reporting standards in Yemen. Dissertation University Utara Malaysia, 6(12), 3–24.

- Al-Hattami, H. M. (2021, April). University accounting curriculum, IT, and Job Market Demands: Evidence from Yemen. Sage Open, 11(2), 215824402110071. https://doi.org/10.1177/21582440211007111

- Al-Mujtaba, M. A. I., & Al-Mawry, Y. A. M. (2018). The role of accounting education in Yemeni universities in enhancing the globalization of the Yemeni accountant field study on the scientific and professional institutions in the republic of Yemen. GCNU Journal ISSN, 289–304. http://repository.neelain.edu.sd:8080/xmlui/bitstream/handle/123456789/13778/16-47-1-12.pdf?sequence=1&isAllowed=y

- Alzeban, A. (2016). Factors Influencing Adoption of the International Financial Reporting Standards (IFRS) in accounting education. Journal of International Education in Business, 9(1), 2–16. https://doi.org/10.1108/JIEB-10-2015-0023

- Arnseth, H. C. (2008). Activity theory and situated learning theory: Contrasting views of educational practice. Pedagogy, Culture & Society, 16(3), 289–302. https://doi.org/10.1080/14681360802346663

- Atabey, N. A., Akmese, H., & Alev Akmese, K. (2014). Awareness level and educational efforts of academicians relating to the international financial reporting standards: A research on accounting academicians in Konya. Procedia Economics and Finance, 15(14), 1655–1662. https://doi.org/10.1016/s2212-5671(14)00637-6

- Bagozzi, R. P., Youjae, Y., & Phillips, L. W. (1991). Assessing construct validity in organizational research. Administrative Science Quarterly, 36(3), 421. https://doi.org/10.2307/2393203

- Becker, J. M., Klein, K., & Wetzels, M. (2012). Hierarchical latent variable models in PLS-SEM: Guidelines for using reflective-formative type models. Long Range Planning, 45(5–6), 359–394. https://doi.org/10.1016/J.LRP.2012.10.001

- Binh, B., Hoang, H., Phan, D. P. T., & Yapa, P. W. S. (2017). Governance and compliance in accounting education in Vietnam–case of a public university. Accounting Education, 26(3), 265–290. https://doi.org/10.1080/09639284.2017.1286603

- Black, W. H. (2012). The activities of the pathways commission and the historical context for changes in accounting education. Issues in Accounting Education, 27(3), 601–625. https://doi.org/10.2308/iace-50091

- Carmona, S., & Trombetta, M. (2010). The IASB and FASB convergence process and the need for ‘concept-based’ accounting teaching. Advances in Accounting, 26(1), 1–5. https://doi.org/10.1016/j.adiac.2010.03.003

- Carvalho, L. N., & Bruno, M. S. (2013). Adoption of IFRS in Brazil and the consequences to accounting education. Issues in Accounting Education, 28(2), 235–242. https://doi.org/10.2308/IACE-50373

- Cheah, J. H., Sarstedt, M., Ringle, C. M., Ramayah, T., & Ting, H. (2018). Convergent validity assessment of formatively measured constructs in PLS-SEM: On using single-item versus multi-item measures in redundancy analyses. International Journal of Contemporary Hospitality Management, 30(11), 3192–3210. https://doi.org/10.1108/IJCHM-10-2017-0649

- Chin, W. W. (1998). The partial least squares approach to structural equation modeling. In G. A. Marcoulides (Ed.), Modern methods for business research (pp. 295–336). NJ Lawrence Erlbaum associates. - References - scientific research Publishing. https://www.scirp.org/S351jmbntvnsjt1aadkposzje/reference/ReferencesPapers.aspx?ReferenceID=534264

- Claes, F., & Larcker, D. F. (2018). Structural equation models with unobservable variables and measurement error: Algebra and statistics. Journal of Marketing Research, 18(3), 382–388. https://doi.org/10.1177/002224378101800313

- Cohen, J. (1992). A power primer. Psychological Bulletin, 112(1), 155–159. https://doi.org/10.1037/0033-2909.112.1.155

- Danks, N. P., & Ray, S. (2018, December). Predictions from partial least squares models. Applying Partial Least Squares in Tourism and Hospitality Research, 35–52. https://doi.org/10.1108/978-1-78756-699-620181003/FULL/XML

- Diamantopoulos, A., Sarstedt, M., Fuchs, C., Wilczynski, P., & Kaiser, S. (2012). Guidelines for choosing between multi-item and single-item scales for construct measurement: A predictive validity perspective. Journal of the Academy of Marketing Science, 40, 434–449.

- Dong, N., Bai, M., Zhang, H., & Zhang, J. (2019). Approaches to learning IFRS by Chinese accounting students. Journal of Accounting Education, 48, 1–11. https://doi.org/10.1016/j.jaccedu.2019.04.002

- Drolet, A. L., & Morrison, D. G. (2001). Do we really need multiple-item measures in service research?. Journal of Service Research, 3(3), 196–204.

- Folashade, O., Osiregbemhe, I. S., Felix, E. D., Adewale, A. J., & Ibanga, B. I. (2016). International financial reporting standards education and its inclusion in the Nigerian curriculum. Vision 2020: Innovation Management, Development Sustainability, and Competitive Economic Growth, I - Vii, 4509–4516.

- Galit, S., & Koppius, O. R. (2011). Predictive analytics in information systems research. MIS Quarterly: Management Information Systems, 35(3), 553–572. https://doi.org/10.2307/23042796

- Geisser, S. (1974). A predictive approach to the random effect model. Biometrika, 61(1), 101–107. https://doi.org/10.1093/BIOMET/61.1.101

- Hair, J. F., Hult, G. T. M., Marko Sarstedt, C. R., Danks, N., & Ray, S. (2021). Partial Least Squares Structural Equation Modeling (PLS-SEM) using R: A workbook. Springer.

- Hair, J., Joe, F., Lucy, M. M., Ryan, L. M., & Marko, S. (2017). PLS-SEM or CB-SEM: Updated Guidelines on which method to use. International Journal of Multivariate Data Analysis, 1(2), 107. https://doi.org/10.1504/IJMDA.2017.087624

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

- Hair, J. F., Risher, J. J., Sarstedt, M., & Ringle, C. M. (2019). When to use and how to report the results of PLS-SEM. European Business Review, 31(1), 2–24.

- Hair, J. F., Sarstedt, M., Ringle, C. M., & Mena, J. A. (2011). An assessment of the use of partial least squares structural equation modeling in marketing research. Journal of the Academy of Marketing Science, 40(3), 414–433. https://doi.org/10.1007/S11747-011-0261-6

- Hayek, A. F. A., Hadi, A., & Al Khasawneh, M. (2013). The suitability of the accounting education in private universities for the requirements of the Jordanian labor market: A field study from the perspective of accounting graduate students. Academy of Contemporary Research Journal, 2(2), 79–85.

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Henseler, J., Ringle, C. M., & Sinkovics, R. R. (2009). The use of partial least squares path modeling in international marketing. Advances in International Marketing, 20, 277–319. https://doi.org/10.1108/S1474-797920090000020014

- IFAC. 2021. Yemeni association of certified public accountants | IFAC.”|“Yemeni association of certified public accountants | IFAC. https://www.ifac.org/about-ifac/membership/members/yemeni-association-certified-public-accountants.

- James, M. L., Blaszczynski, C., & Hulme, R. (2003). Students’ facility with U.S. AND international accounting standards. US and International Accounting Standards, 1. https://scholarworks.calstate.edu/downloads/ng451k67s

- Jöreskog, K. G. (1971). Statistical analysis of sets of congeneric tests. Psychometrika, 36(2), 109–133.

- Joshi, P. L., Wayne, G. B., & Al-Ajmi, J. (2008). Perceptions of accounting professionals in the adoption and implementation of a single set of global accounting standards: Evidence from Bahrain. Advances in Accounting, 24(1), 41–48. https://doi.org/10.1016/j.adiac.2008.05.007

- Julieth, O.-D., García-Benau, M. A., & Zorio-Grima, A. (2016). Massive open online courses for IFRS education: A point of view of Spanish accounting educators. Procedia - Social & Behavioral Sciences, 228(June), 356–361. https://doi.org/10.1016/j.sbspro.2016.07.053

- Leguina, A. (2015). A primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). International Journal of Research & Method in Education, 38(2), 220–221. https://doi.org/10.1080/1743727x.2015.1005806

- Li Tze, H., & Bentler, P. M. (2009). Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural equation modeling: A multidisciplinary journal, 6(1), 1–55. https://doi.org/10.1080/10705519909540118

- Lohmöller, J.-B. (1989). Latent Variable Path Modeling with Partial Least Squares. Latent Variable Path Modeling with Partial Least Squares. https://doi.org/10.1007/978-3-642-52512-4

- Mah’d, O. A., & Mardini, G. H. (2020). The quality of accounting education and the integration of the international education standards: Evidence from middle eastern and North African Countries. Accounting Education, 0(0), 1–21. https://doi.org/10.1080/09639284.2020.1790020

- Nassar, M., & Al-Khadash Osama, H. (2013). Accounting education and accountancy profession in Jordan : The current status and the processes of improvement. Research Journal, 4(11), 107–120. https://www.researchgate.net/profile/Osama-Mahd/publication/259785850_Acc_Education/data/0a85e52de68b612b6f000000/ACCOUNTING-EDUCATIION2013.doc

- Natoli, R., Wei, Z., & Jackling, B. (2020). Teaching IFRS: Evidence from course experience and approaches to learning in China. Accounting Research Journal, 33(1), 234–251. https://doi.org/10.1108/ARJ-09-2018-0142

- Nwaiwu, J. N., & Macgregor, T. C. (2018). THE rise and rise of IFRS: Practitioners and academics in Nigeria. International Journal of Advanced Academic Research | Social & Management Sciences |, 4(2), 2488–9849.

- O Cualain, G., & Tawiah, V. (20231). Review of IFRS consequences in Europe: An enforcement perspective. Cogent Business & Management, 10 (1). https://doi.org/10.1080/23311975.2022.2148869.

- Patro, A., & Gupta, V. K. (2012). Adoption of International Financial Reporting Standards (IFRS) in accounting curriculum in India-an empirical study. Procedia Economics and Finance, 2(January 2005), 227–236. https://doi.org/10.1016/S2212-5671(12)00083-4

- Pett, M. A., Pett, N. R., & Sullivan Lackey, J. J. 2003. Making Sense of Factor Analysis: The use of factor analysis for instrument. SAGE Publications. https://doi.org/10.4135/9781412984898.

- Puri, N., & Singh, H. (2021, July). Current trends in finance in the context of adoption of principle-based accounting standards in accounting education. Financial Intelligence in Human Resources Management, 151–171. https://doi.org/10.1201/9781003083870-8

- Raithel, S., Sarstedt, M., Scharf, S., & Schwaiger, M. (2012). On the value relevance of customer satisfaction. multiple drivers and multiple markets. Journal of the Academy of Marketing Science, 40(4), 509–525. https://doi.org/10.1007/s11747-011-0247-4

- Rezaee, Z., Murphy Smith, L., & Szendi, J. Z. (2010). Advances in accounting, incorporating advances in international accounting convergence in accounting standards : Insights from academicians and practitioners. International Journal of Cardiology, 26(1), 142–154. https://doi.org/10.1016/j.adiac.2010.01.001

- Rich, K. T., Cherubini, J. C., & Zhu, H. (2012). IFRS in introductory financial accounting using an integrated, comparison-based approach. Advances in Accounting Education: Teaching and Curriculum Innovations, 13. https://doi.org/10.1108/S1085-462220120000013019

- Rigdon, E. E. (2012). Rethinking partial least squares path modeling: In praise of simple methods. Long Range Planning, 45(5–6), 341–358. https://doi.org/10.1016/J.LRP.2012.09.010

- Rivera-Valentin, L. R., & North Central University. (2017, April). Exploring accounting educators ’ perceptions and intentions to teach international financial reporting standards: A multiple-case study dissertation manuscript submitted to Northcentral University graduate faculty of the school of business and technology.

- Russell, K. A., “Bud” Kulesza, C. S., Albrecht, W. S., & Sack, R. J. (2000). Accounting education: Charting the course through a perilous future. Management Accounting Quarterly, 2(1), 4–11.

- Santos, N. E., & Clayton Quilliam, W. (2013). An interview-based study of individual and institutional preparedness for teaching IFRS. International Journal of Accounting and Financial Reporting, 3(2), 1. https://doi.org/10.5296/ijafr.v3i2.4122

- Sarstedt, M., Hair, J. F., Hwa Cheah, J., Michael Becker, J., & Ringle, C. M. (2019). How to specify, estimate, and validate higher-order constructs in PLS-SEM. Australasian Marketing Journal, 27(3), 197–211. https://doi.org/10.1016/j.ausmj.2019.05.003

- Sarstedt, M., Hair, J. F., Pick, M., Liengaard, B. D., Radomir, L., & Ringle, C. M. (2022). Progress in partial least squares structural equation modeling use in marketing research in the last decade. Psychology & Marketing, 39(5), 1035–1064. https://doi.org/10.1002/MAR.21640

- Sarstedt, M., Hair, J. F., Ringle, C. M., Thiele, K. O., & Gudergan, S. P. (2016). Estimation issues with PLS and CBSEM: Where the bias lies! Journal of Business Research, 69(10), 3998–4010. https://doi.org/10.1016/J.JBUSRES.2016.06.007

- Sayed Ahmad, A., & Zalzali, Y. (2022). Competencies and skills in higher education in accounting in lebanon. 1, 4. https://doi.org/10.17613/k2km-0x09

- Shmueli, G. (2010). To explain or to predict? Statistical Science, 25(3), 289–310. https://doi.org/10.1214/10-STS330

- Shmueli, G., Sarstedt, M., Hair, J. F., Hwa Cheah, J., Ting, H., Vaithilingam, S., & Ringle, C. M. (2019). Predictive model assessment in PLS-SEM: Guidelines for using PLSpredict. European Journal of Marketing, 53(11), 2322–2347. https://doi.org/10.1108/EJM-02-2019-0189

- Stone, M. (1974). Cross-validatory choice and assessment of statistical predictions. Journal of the Royal Statistical Society: Series B (Methodological), 36(2), 111–133. https://doi.org/10.1111/J.2517-6161.1974.TB00994.X

- Sugahara, S. (2013). Japanese accounting academics’ perceptions on the global convergence of accounting education in Japan. Asian Review of Accounting, 21(3), 180–204. https://doi.org/10.1108/ARA-09-2012-0050

- Szmanda, T. (2018). Examining the adequacy of international accounting coursework from the perspectives of students and faculty. ProQuest LLC.

- Tawiah, V. (2019). The state of IFRS in Africa. Journal of Financial Reporting and Accounting, 17(4), 635–649. https://doi.org/10.1108/JFRA-08-2018-0067

- Tawiah, V., & Boolaky, P. (2020). A review of literature on IFRS in Africa. Journal of Accounting & organizational change, 16(1), 47–70. https://doi.org/10.1108/JAOC-09-2018-0090

- Tenenhaus, M., Esposito Vinzi, V., Marie Chatelin, Y., & Lauro, C. (2005). PLS path modeling. Computational Statistics and Data Analysis, 48(1), 159–205. https://doi.org/10.1016/J.CSDA.2004.03.005

- Wong, H., & Wong, R. (2013). An empirical study - adoption of International Financial Reporting Standards (IFRS) in Hong Kong education. Journal of Management Research, 5(4), 98. https://doi.org/10.5296/jmr.v5i4.4256

- The World Bank. 2010. Education status report: Challenges and opportunities. T. https://documents1.worldbank.org/curated/en/182051468154759836/pdf/571800WP0Yemen10Box353746B01PUBLIC1.pdf.

- Zhu, H., Rich, K. T., Michenzi, A. R., & Cherubini, J. (2011). User-Oriented IFRS education in introductory accounting at U.S. academic institutions: Current status and influencing factors. Issues in Accounting Education, 26(4), 725–750. https://doi.org/10.2308/iace-50058