Abstract

This study employed a concurrent embedded design to compare the accounting curricula of selected universities in Africa, America, Asia, and Europe, guided by International Education Standards (IES) 2, 3, 4, and 5. Fourteen universities from different continents were conveniently selected, and a descriptive content analysis was conducted to analyse the undergraduate accounting program contents. The findings reveal that the accounting education in selected African universities aligns with IES 2, 3, 4 and other universities, countering claims of inferiority. However, the universities’ curricula in Africa lack practical job-related competencies (IES 5) due to limited opportunities for experiential learning. Disparities exist in the emphasis on IES competencies, potentially leading to imbalanced development among graduates. African universities prioritise employment-oriented education, while those in America, Asia, and Europe emphasise professional progression. Recommendations include enhancing ethics and professional values, allocating more curriculum space for ethical behaviour promotion, and creating room for practical skills acquisition to facilitate students’ application of learned concepts and facilitate potential remediation.

1. Introduction

Accounting plays a crucial role in any economy (Hakim, Citation2016). Accountants have been critical participants in achieving sustainable development goals through their contribution to quality reporting, as highlighted by Stanescu (2018). This claim was initially made by the Association of Chartered Certified Accountants (ACCA, 2012) when they emphasised that effective financial reporting and auditing can positively impact a country’s economy. Given the significance and relevance of the accounting profession to nations, it is imperative to place special attention on the education and curriculum used to develop accounting graduates, enabling them to excel as accountants and contribute to the developmental goals of a nation.

Historically, universities have been significant contributors to the development of prospective accountants through their accounting programs. Hence, universities need a curriculum focusing on holistic development and cultivating the competencies necessary for accounting trainees to perform well in their jobs (Hidayat & Budiatma, Citation2018). In the context of accounting education, these competencies also referred to as employability skills, have been outlined by the International Accounting Education Standards Board (International Accounting Education Standard Board [IAESB], Citation2017). The IAESB prescribes three main categories of competencies: technical competence, professional skills (generic skills), and professional values, ethics, and attitudes. These competencies serve as a curriculum guide for accounting education and are documented in the International Education Standards (IES). To ensure the comprehensive development of accounting graduates, the International Federation of Accountants (IFAC) has collaborated with universities, through local members, by signing Memorandums of Understanding (MoUs) to ensure universities’ commitment to developing these competencies in their accounting graduates (Institute of Chartered Accountants Ghana [ICAG], Citation2019).

While the IES guide the content of the accounting curriculum, universities have the autonomy to determine which aspects of the standards to prioritise (Busuioc et al., Citation2019). The emphasis placed on certain elements and the neglect of others within the IES and curriculum will affect the competencies that accounting graduates develop upon completing their education. Baah-Boateng (Citation2015) initially asserted that the failure of schools to build students adequately has led to a current issue of graduate unemployment in Ghana. It has also been strongly claimed that the quality of education in African universities, including accounting programs, has been a concern. Monga (Citation2019) highlights the frequently poor quality and outdated curricula in African universities, resulting in incompetent graduates, including accounting graduates. Consequently, a significant gap exists between academia and the job market, and employers may find that accounting graduates from African universities are not equipped to meet their desired standards, as discussed by Khan (Citation2018) and Abas & Imam (Citation2016). Although Monga’s (Citation2019) contention generalises the poor-quality curricula in African universities, adopting the IES in the accounting curricula of IFAC member countries aims to create globally comparable accounting programs, given the global regulation of accounting education among IFAC member countries.

This study, therefore, seeks to investigate the applicability of Monga’s (Citation2019) claim regarding the poor and obsolete curricula in selected African universities to accounting education programs. It introduces a novel perspective to the accounting education literature by comparing selected African universities with those on other continents in light of the IES. The remainder of this paper is structured as follows: First, the conceptual framework, which identifies the relevant IES (IES 2, 3, 4 and 5) to guide the arguments presented, is given after the introduction. This is followed by a review of empirical literature supporting previous studies’ positions. Subsequently, the research methods employed to derive the study results are presented. Finally, the results are presented with discussions and conclusions. Recommendations are consequently suggested.

1.1. Conceptual review

The International Education Standards (IES) developed by the International Accounting Education Standards Board (IAESB) serve as a set of learning outcomes for accounting education. The IAESB, an independent subsidiary of the International Federation of Accountants (IFAC), is responsible for formulating these standards to guide the curriculum of accounting education (IAESB, Citation2017). These standards apply to all IFAC member countries and are intended to be used by universities, educational providers, employers, regulators, government authorities, accountants, and prospective accountants. While primarily developed for professional accountancy education, institutions of higher learning offering accounting education can also utilise these standards to shape their curricula. This enables graduates of these institutions to be granted exemptions from specific courses required for professional membership (International Accounting Education Standard Board [IAESB], Citation2017).

The current edition of the IAESB framework, effective from July 2015, encompasses eight primary standards: Entry Requirements to Professional Accounting Education Programs (IES 1), Technical Competence (IES 2), Professional Skills (IES 3), Professional Values, Ethics, and Attitudes (IES 4), Practical Experience (IES 5), Assessment of Professional Competence (IES 6), Continuing Professional Development (IES 7), and Professional Competence for Engagement Partners Responsible for Audits of Financial Statements (IES 8). Of these standards, IES 2, 3, 4 and 5 are particularly relevant to this study as they define the specific competencies accounting education should provide (IAESB, Citation2017).

1.1.1. IES 2, Technical Competence: this competence emphasises applying accounting knowledge at a required level (Busuioc et al., Citation2019; International Accounting Education Standard Board [IAESB], Citation2017). This competence encompasses 11 main subjects or courses, such as financial accounting and reporting, management accounting, financial management, taxation, audit and assurance, governance, risk management and internal control, business laws and regulations, information technology, business/organisational environment, economics, and business strategy/management. While the specific descriptions of these subjects may vary among universities and jurisdictions, the content remains consistent (International Accounting Education Standard Board [IAESB], Citation2017). Technical competence is to be developed at three levels: foundation, intermediate, and advanced, with each level corresponding to varying levels of ambiguity, complexity, and uncertainty in work environments (International Accounting Education Standard Board [IAESB], Citation2017).

1.1.2. IES 3, Professional Skills: this focuses on developing intellectual, interpersonal/communication, personal, and organisational skills in accounting graduates (International Accounting Education Standard Board [IAESB], Citation2017). These skills contribute to the credibility of the accountancy profession, enhance the quality of professional accountants’ work, and safeguard the public interest. The curriculum should include teaching and learning approaches that foster the acquisition of these skills, such as group study to promote teamwork and interpersonal relationships (Asare, Citation2016). The development of professional skills should extend beyond specific courses and be evident throughout the curriculum, with the academic environment supporting their cultivation (International Accounting Education Standard Board [IAESB], Citation2017).

1.1.3. IES 4, Professional Values, Ethics, and Attitudes: this encompasses the characteristics that distinguish individuals as members of the accounting profession (IAESB, Citation2017). These characteristics include ethical principles and other principles of conduct essential for professional behaviour. Graduates should be able to identify ethical issues and apply appropriate values, attitudes, and ethics in different situations (Busuioc et al., Citation2019). Professional values, ethics, and attitudes are underpinned by integrity, objectivity, confidentiality, professional competence/due care, and professional behaviour. Cultural and national values should be taken into account in developing this competency, and a mixed learning and development approach, including role-playing, case studies, seminars, and online forums, should be employed (International Accounting Education Standard Board [IAESB], Citation2017).

1.1.4. IES 5, Practical Experience: this is an essential component of the initial professional development (IPD) requirement for aspiring professional accountants. Practical experience refers to the workplace and other relevant activities that contribute to developing professional competence (IAESB, Citation2017). It complements classroom learning by providing opportunities to apply knowledge and skills in real-world settings. Accounting education providers are responsible for incorporating practical experience into their curriculum, with options like internships, cooperative education work periods, and secondments offering practical application opportunities. Practical experience is crucial for aspiring professional accountants to demonstrate the technical competence, professional skills, professional values, ethics, and attitudes necessary for their roles (Baah-Boateng, Citation2015; International Accounting Education Standard Board [IAESB], Citation2017).

While classroom study is valuable for acquiring and demonstrating professional accountancy knowledge, it alone does not explain the attainment of professional competence as a professional accountant. Work experience equips aspiring professionals with the practical skills to become competent accountants (International Accounting Education Standard Board [IAESB], Citation2017).

2. Empirical review

In a study by Mah’d & Mardini (Citation2020) focusing on higher education institutions in the Middle East and North Africa (MENA) region, perceptions of academics and practitioners regarding the quality of accounting education and the integration of IES in accounting programs were examined. The results indicated a lack of IES utilisation in the universities. Similarly, Kadhim Al-Anbagi et al. (Citation2018) investigated Iraq’s compliance with International Accounting Standards, particularly IES 2. The study found that Iraq exhibited approximately 55% compliance with the second standard of accounting education, indicating a moderate level of adoption or implementation. Examining accounting programs in Saudi Arabian colleges, Al-Dhubaibi (Citation2022) discovered partial compliance with the guidelines of IESs. Furthermore, accounting academics in these universities exhibited significant variations in their level of knowledge.

Various empirical studies conducted in other contexts, including Jordan, Italy, Vietnam, and others, have identified issues such as the inadequate implementation of IES provisions, an overemphasis on technical competencies over generic skills, and insufficient inclusion of topics necessary for required competencies as prescribed in IES (Busuioc et al., Citation2019; Frijat & Mohammad, Citation2016; Jackling & De Lange, Citation2009; Veneziani et al., Citation2015). Busuioc et al. (Citation2019) observed that universities placed minimal emphasis on ethics development due to institutional discretion. Similar findings were identified by Ramaj (Citation2023) when he analysed to evaluate the level of adoption and implementation of International Education Standards (IES) in Albanian universities. The study findings revealed that IES 3 and 4 had been moderately adopted but poorly implemented by the universities. Conversely, IES 2 demonstrated high adoption and moderate implementation in the country.

Mustafa and Jaleel Kehinde Shittu (Citation2012) found that universities and polytechnics prioritised technical skills over other competencies in the Nigerian context. Conversely, Low et al. (Citation2013) noted adequate focus on developing soft skills among accounting graduates in New Zealand universities, evident through teaching/learning approaches and course structures (Low et al., Citation2013). Adaboh (Citation2014) evaluated an accounting bachelor’s degree program in a Ghanaian private university, revealing alignment between the program’s focus and IES requirements. However, the evaluation did not encompass a detailed curriculum analysis (Adaboh, Citation2014).

However, a notable gap in the literature is the lack of comprehensive empirical evidence benchmarking university curricula against IES requirements, particularly in terms of the three core competencies and their comparison with practices in other institutions. Thus, this study aims to contribute to this literature gap by employing the three dimensions of IPD (Initial professional development) to assess the aspects mentioned earlier.

3. Methods

3.1. Research design

The present study utilised a mixed-methods approach, explicitly employing the concurrent embedded mixed-method design. This approach integrates qualitative and quantitative data collection and analysis methods within a single study, with one method embedded within the other (Creswell & Creswell, Citation2017). The concurrent embedded design allows for simultaneous data collection and provides a comprehensive understanding of the research topic by capturing both breadth and depth of information. Both qualitative and quantitative data were gathered to describe and compare the adaption of IES by the selected universities. The quantitative process and analysis were nested within a predominantly qualitative process and analysis, creating a concurrent embedded mixed-method design. By combining these two approaches, the study yielded results and interpretations encompassing both qualitative and quantitative aspects, reflecting the comprehensive nature of the concurrent embedded design.

3.2. Sample selection procedure

A sample of 14 universities offering undergraduate accounting programs was selected for the content analysis of accounting curricula. The selection process involved convenience sampling of four universities from Africa (one from each of the East, West, North, and Southern regions) and universities from Europe, Asia, and America (three each). The four major African universities offering accounting programs were chosen based on their status as leading universities within their respective regional blocks, as indicated by the 2022 higher education rankings (Times Higher Education, 2021). An additional ten internationally recognised universities offering accounting education were selected as benchmark institutions based on their global recognition and rankings by Times Higher Education. The selection of universities was also influenced by the availability of relevant documents on their websites. The universities included in the study are presented in Table . Through selective reduction, the curricula or course outlines of the selected universities were coded into manageable content categories, including IES 2, IES 3, IES 4, practical experience (IES 5), and program goals. Reducing course outline content into specific categories enabled a focused analysis of the critical skills and knowledge areas relevant to the research question.

Table 1. Universities Included in the Study

3.3. Data collection procedure

The conceptual content analysis was conducted manually, involving a series of decisions and activities. Firstly, the analysis was based on the three overarching categories as previously mentioned. Data was collected from course outlines, program brochures, and program documents retrieved from the accounting department websites of each university. The International Education Standards (IES) framework was utilised as a guide to extract relevant information from the documents, thereby providing qualitative evidence about the universities’ focal points in the development of accounting graduates. Secondly, a decision was made to allow flexibility in the coding process, acknowledging the potential introduction and analysis of new and significant material that could substantially impact the research. This flexibility ensured that crucial information was not overlooked and enabled comprehensive analysis. Thirdly, the coding process focused on the presence of specific categories rather than their frequency; however, credit loadings were tallied to determine the overall emphasis. This approach facilitated the identification of skill and knowledge areas of concentration within the programs by pooling course titles under relevant categories. It was imperative to thoroughly examine each course outline to accurately identify its focus rather than relying solely on the course title. This systematic approach maintained consistency and organisation throughout the coding process, thus enhancing its eventual validity.

3.4. Data analysis procedure

Descriptive content analysis was performed to recognise systematic and objective techniques for identifying distinct attributes within a document to draw logical inferences (Holsti, Citation1968). The utilisation of the descriptive content analysis in this study was motivated by the desire to examine the written accounting curricula (including course outlines, program brochures, and program details) of selected universities across different continents. The descriptive content analysis design enables the description of existing practices and provides empirical evidence about the specific areas of interest (Bowen, Citation2009; Donald et al., Citation2010). By employing this analysis, the study aimed to identify the critical skills and knowledge areas emphasised in the accounting curricula of universities and to identify any discernible patterns in the course content of accounting programs for comparison. Specifically, a quantitative content analysis technique was employed to examine the alignment of the curricula with the competencies outlined in IES 2, 3, and 4 and to determine the corresponding credit loadings associated with each area. The primary objective was to assess the degree of emphasis on the identified skills and knowledge areas in the course outlines, as explicitly captured concerning IES 2, 3, and 4. Qualitative content analysis was also used to determine the focus of the accounting programmes. Furthermore, IES 5 guided the qualitative content analysis used to examine how practical experience was incorporated within the accounting programs offered by the universities, thereby providing evidence of the universities’ commitment to practical experience as a relevant component of students’ initial professional development (IPD).

Quantitative analysis involves computing the percentage of credits allocated to courses or subjects addressing specific competencies. In cases where students were given the option to choose among courses to study, a range encompassing the maximum and minimum percentages was presented in Supplemenatry Appendix Table A1. Additionally, the graph displayed the average percentage derived from the minimum and maximum values, providing an overall representation of credit allocation

Qualitative analysis entailed highlighting the observations made during the analysis process, organising them into themes, and supporting them with relevant quotations from the documents. This approach strengthened the analysis by providing evidential support for the identified themes.

4. Results

Contents of undergraduate accounting programme documents such as aims, objectives, structure/components, course outlines, and student handbooks were analysed. These provided rich and valuable insights to identify the focus of the selected African universities compared to those chosen in America, Asia and Europe and IES requirements when training accounting students. Results have been presented in a graph and themes.

4.1. Universities’ adaptation of IES

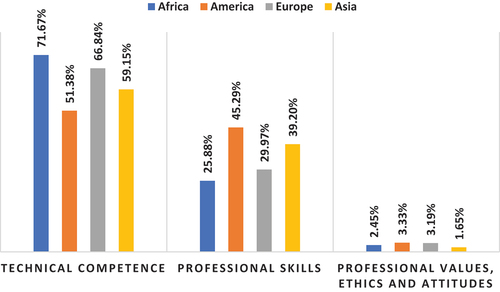

A comprehensive overview of how universities in Africa and other regions worldwide have structured their accounting education courses to align with the requirements of the International Education Standards (IES) is presented in Figure . The bar graph visually depicts the distribution of credit loadings allocated by these universities to develop students’ technical competencies. It is evident from Figure that universities in America, Asia, and Europe, similar to their counterparts in Africa, assign a significant portion (over 50%) of their credit loadings to technical competence. Among the selected universities from Europe, Asia, and America, the average credit loadings allocated to technical competence were 66.84%, 59.15%, and 51.18%, respectively. Similarly, among the selected African universities, the average credit loadings devoted to technical competence were 71.67%.

Figure 1. Adaptation of IES by universities across four continents.

The second-highest allocation of credit loadings was dedicated to professional skills, which ranged from 25.88% to 45.29% across the universities from the four continents. Conversely, professional values, ethics, and attitudes, one of the competencies outlined in the IES, received the lowest credit loadings, ranging from 1.65% to 3.33% in accounting programs offered by universities across all four continents. On initial examination, there appears to be a convergence in adapting the three main competencies (IES 2, IES 3, and IES 4) across accounting education programs in universities, regardless of geographical location.

Further analysis of the universities’ curricula revealed the presence of courses such as project work and research methods focused on developing research skills. Notably, courses such as “Logic and Reasoning” and “Critical Thinking” indicated the universities’ efforts to cultivate logical reasoning skills among accounting graduates, as required by the IES (see Table A1 in Supplemenatry Appendix). A noteworthy observation was that universities in America, Asia, and Europe frequently provided accounting students with the option to choose alternative courses. Conversely, universities in Africa offered limited to no opportunities for course selection. Optional courses accounted for 0% to 4.5% of the total credit loadings in African universities, while in universities from America, Asia, and Europe, this range expanded from 2.44% to 22.5% (see Supplemenatry Appendix Table A1). Additionally, none of the compulsory courses in the African context constituted less than 95% of the total credit loadings. In contrast, among selected universities in America, Asia, and Europe, this range was between 77% and 97%.

Similar to the observations made among the selected universities in Africa, leading international universities in America, Asia, and Europe also offered courses related to accountancy, such as Marketing, Supply Operation, and studying other languages in business. However, the notable difference was that these international universities gave students the autonomy to choose the type of course and the semester in which they wished to pursue them. In contrast, universities in Africa typically offer such courses within the first two years of their undergraduate accounting programs.

Analysing universities’ accounting curricula showcased their varying approaches to addressing the IES requirements. While similarities were observed in allocating credit loadings to the three main competencies, there were notable differences in course selection options, credit loading distribution, and the timing of specific specialised courses across different regions. These findings shed light on the diverse strategies universities employ to adapt their accounting education programs to meet the demands of the IES.

4.2. Further areas of departure of accounting education in Africa from those in America, Asia and Europe

Additional findings from the qualitative content analysis revealed significant differences between the accounting education provided by selected African universities and those in America, Asia, and Europe. These disparities can be categorised into two overarching themes: the objectives of accounting education delivery and the emphasis on theory versus practice.

In the context of aims and objectives, universities in Africa primarily focus on preparing students for employment in accounting. For instance, one accounting program in an African university states its objective as follows:

“The program aims to provide accounting and business education that develops accounting personnel with the requisite technical knowledge, skills, character, and abilities fit for the prudent steward of resources for private and public sectors of the economy”. (University in Africa)

Another objective highlighted by a university in Africa emphasises that ”Graduates of the programme will be able to prepare and present financial reports by International Financial Reporting Standards and the institutional, legal, and regulatory framework of … ’ (a University in Africa) These findings seem to affirm that the accounting program offered by universities in Africa place significant emphasis on developing students’ technical competence in accounting.

In contrast, accounting education programs in America, Asia, and Europe focus on facilitating professional progression. For example, a competitive program outside Africa articulates its accounting program’s goal as follows:

…prepares students for a professional qualification in accounting and provides the broad-based education necessary for progressing towards a leadership role in the financial sector… Graduates of the degree are eligible to obtain maximum exemptions from professional examinations organised by the Association of Chartered Certified Accountants (ACCA) and need to take only five papers. (University in Asia)

Regarding the emphasis on theory and practice, a notable observation from the document analysis is the limited integration of practical experience into the selected universities’ accounting education programs in Africa. Evidence shows that only one out of the four universities chosen in Africa emphasised the completion of a three-credit-hour practicum in the industry for accounting students. Moreover, not all students in the program had access to practical experience opportunities. In contrast, universities in America, Asia, and Europe demonstrate a deliberate effort to collaborate with industries, providing accounting trainees with the necessary competencies for the job market.

Universities in America, Asia, and Europe have implemented internship programs that allow students to apply classroom knowledge in real-world settings, enhancing their understanding of the subject matter. For instance, an accounting program in Europe ” … provide … [students] with a fast track to an accountancy qualification and the four-year degree offers … [students] the opportunity of a full-year paid work placement in your [their] third year of study‘. Additionally, it ’provide … [students] with the opportunity to meet companies who offer internships through the UPP, such as Ernst and Young, Goldman Sachs, Grant Thornton, Mazars and PwC. The course integrates the study of the theory and practice of accounting … ”.

In addition to the above evidence, another university, in its programme document, described the focus of a particular course (Work-Integrated Education, WIE) as a mandatory component of the curriculum. “It is work-based learning experiences which take place in an organisational context relevant to a student’s future profession, or the development of generic skills that will be valuable in that profession”. An essential and compulsory component in the Faculty’s BBA education, WIE facilitates the integration of knowledge, skills, and competencies between the classroom and the real world, thus equipping students with valuable work experience and practical readiness for full-time (a university in America). Similarly, a university in Asia stated, “The learning outcomes and objectives set out represent a balance between the continuing need for practicality in programmes and the pressing need for whole-person development of students”.

These findings suggest that accounting education provided by selected African universities places a greater emphasis on theory than their counterparts in America, Asia, and Europe. Consequently, students in African universities may have limited opportunities for practical experiences within their accounting education programs.

5. Discussion

The analysis of program structures from various universities provides evidence that all the 11 courses/subjects recommended by the International Education Standards (IES) to develop technical competence are incorporated by the selected universities across the four continents. These courses are designed to span the entire four-year study period, with fundamental proficiencies covered in the first and second years, intermediate proficiencies in the second and third years, and advanced proficiencies in the third and final years. While the general aims of accounting programs subtly suggest consideration for the development of professional skills among accounting graduates, the allocated credit loadings for courses on professional skills in all the selected universities from the four continents do not fully support these intended program aims. The credit loadings for professional skills courses are consistently lower than those for technical competence.

The objectives of accounting programs seldom address the development of professional values, ethics, and attitudes. The credit hours and the number of courses allocated to this aspect further demonstrate the limited attention given to developing these competencies. None of the universities allocates more than six-hour credit loadings to courses focused on professional values, ethics, and attitudes. While ethics, values, and attitudes are addressed to some extent in other technical competency courses, such as Advanced Financial Reporting and Auditing, methods like role-playing and seminars specifically targeting ethics, values, and attitudes are not commonly used in course delivery across the universities. Although the universities incorporate most learning outcomes related to professional values, ethics, and attitudes as required by the IES, the allocated credit hours for achieving these outcomes are limited. Overall, it can be concluded that universities do not prioritise the development of professional values, ethics, and attitudes in their accounting curricula, aligning with the findings of Veneziani et al. (Citation2015), Busuioc et al. (Citation2019) and Ramaj (Citation2023) that highlighted the lack of emphasis on these aspects among accounting graduates.

Regarding developing students’ professional skills, there are more similarities than differences between selected African universities and leading international universities across Africa, America, Asia, and Europe. Commonalities can be observed in credit loadings, course contents, and program goals. The selected universities outside Africa also demonstrate a focus on developing professional skills in accounting students, indicating that the quest for fostering these skills is not undermined. However, the attention and priority given to professional skills development in selected African universities are relatively less pronounced than in technical competence. This difference may influence the significance students attribute to such skills and how they develop and apply them in their professional endeavours. This finding partially supports the study conducted by Low et al. (Citation2013) in New Zealand, which revealed a strong emphasis on developing professional skills. Nonetheless, the focus on professional skills in selected African universities falls short, overshadowed by the emphasis on technical competence. This finding resonates with the observations of Ramaj (Citation2023), Kadhim Al-Anbagi et al. (Citation2018), Al-Dhubaibi (Citation2022), Jackling & De Lange (Citation2009), Mustafa & Jaleel Kehinde Shittu (Citation2012), and Busuioc et al. (Citation2019) who noted that universities tend to prioritise the development of technical skills while neglecting other essential competencies.

The overall analysis suggests a general convergence between the undergraduate accounting curricula of selected universities across Africa, America, Asia, and Europe and the requirements outlined in the IES. This finding supports Adaboh’s (Citation2014) conclusion that the general aims of accounting programs align with the standards set by the International Federation of Accountants (IFAC). However, a closer examination reveals variations in the emphasis placed on each competency. The courses and objectives of the programs align with the guidelines provided by the International Accounting Education Standards Board (IAESB). This contrasts with the situation in Jordan, where Frijat & Mohammad (Citation2016) found inadequate coverage of the IES requirements in the university courses.

6. Conclusions and recommendations

The accounting education provided by selected universities in Africa demonstrates a mutual adaptation and alignment with the International Education Standards (IES) 2, 3, and 4, indicating its competitive nature and dismissing claims of inferiority. However, the curriculum falls short of providing students with sufficient time and opportunities to acquire practical job-related competencies and experiences typically gained through internship programs. Consequently, graduates of accounting programs from these African universities may face challenges in adapting to the work environment when they secure employment after graduation. This delayed learning curve and associated productivity can be a contrast to graduates from selected universities across America, Asia, and Europe. It is crucial to note that practical job-related competencies represent only a fraction of the overall competencies students are expected to develop. Therefore, making sweeping statements about the inadequacy of African undergraduate accounting curricula would be unjustified. Consequently, Monga’s (Citation2019) findings do not apply to the accounting education the selected universities in Africa offer. Nonetheless, there is a need for deliberate efforts to allocate curriculum space for practical on-the-job training and establish partnerships with relevant industry stakeholders to accommodate students and provide supervision and assessment, which can offer feedback to faculty for necessary remediation and potential curricular modifications.

The universities’ commendable overall commitment to incorporating all the competencies prescribed by the IES is a positive step in the right direction. However, the emphasis placed on specific competencies over others raises concerns. While it is reasonable that not all competencies can receive equal attention, the significant disparities observed in this study can result in imbalanced development among accounting graduates. This finding is not surprising, as institutions often prioritise teaching factual knowledge at the expense of attitudes and generic skills. Universities must strive to strike a balance in their focus when developing the competencies of accounting graduates. Specifically, efforts to cultivate professional values, ethics, and attitudes should be reviewed and enhanced. This becomes particularly important when corruption has been identified as a hindrance to a nation’s development. It is, therefore, essential to allocate more curriculum space to interventions promoting ethics, contributing to the moral development of students.

7. Limitations and suggestions for future studies

The assumption that the universities’ documents would ultimately reflect universities’ focus when training accounting graduates might not entirely be the case. For instance, a department may decide to prepare a comprehensive curriculum but implement something different. However, given the rigorous procedure, the study’s validity is assured. It is therefore recommended that future studies observe how the IES are being implemented in addition to the document analysis.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Supplemental Material

Download MS Word (33.8 KB)Disclosure statement

No potential conflict of interest was reported by the author(s).

Supplemental data

Supplemental data for this article can be accessed online at https://doi.org/10.1080/2331186X.2023.2239632.

Additional information

Funding

References

- Abas, M. C., & Imam, O. A. (2016). Graduates’ competence on employability skills and job performance. International Journal of Evaluation & Research in Education (IJERE), 5(2), 119–12. https://doi.org/10.11591/ijere.v5i2.4530

- Adaboh, S. (2014). An evaluation of the bachelor degree in accounting program in a Ghanaian private university. Andrews University.

- Al-Dhubaibi, A. A. S. (2022). Conformance of Accounting Education in Saudi Arabia Universities to the International Accounting Education Standards: An Exploratory Study. The Journal of Asian Finance, Economics & Business, 9(6), 313–324.

- Asare, P. Y. 2016. “Assessment of business students’ preference for cooperative learning: A survey study at the University of Cape Coast.” PhD diss., University of Cape Coast.

- Baah-Boateng, W. (2015). Unemployment in Ghana: A cross sectional analysis from demand and supply perspectives. African Journal of Economic and Management Studies, 6(4), 402–415. https://doi.org/10.1108/AJEMS-11-2014-0089

- Bowen, G. A. (2009). Document analysis as a qualitative research method. Qualitative Research Journal, 9(2), 27–40. https://doi.org/10.3316/QRJ0902027

- Busuioc, A., Jean-Marie Borgonovo, A., & Thi Phuong Mai, T. (2019). Vietnam Corporate Accounting Education in Universities. Washington DC: The World Bank.

- Creswell, J. W., & Creswell, J. D. (2017). Research design: Qualitative, quantitative, and mixed methods approach. Sage publications.

- Donald, A., LCr Jacobs, A. R., & Sorensen, C. (2010). Introduction to research in education (8th ed ed.). Wadsworth.

- Frijat, Y. S. A., & Mohammad, K. S. (2016). Jordanian Universities and their role in the trend towards the development of technical competence for accounting learning outcomes in line with IES# 2. Accounting and Finance Research, 5(2), 20–31. https://doi.org/10.5430/afr.v5n2p20

- Hakim, R. R. C. (2016). Are accounting graduates prepared for their careers? A comparison of employees’ and employers’ perceptions. Global Review of Accounting and Finance, 7(2), 1–17. https://doi.org/10.21102/graf.2016.09.72.11

- Hidayat, R., & Budiatma, J. (2018). Education and job training on employee performance. International Journal of Social Sciences and Humanities, 2(1), 171–181. https://doi.org/10.29332/ijssh.v2n1.140

- Holsti, O. R. (1968). Content analysis. In G. Lindzey & E. Aronson (Eds.), The handbook of social psychology (2nd ed.), (pp. 596–692). Addison-Wesley.

- Institute of Chartered Accountants Ghana [ICAG]. (2019). Attestation of ongoing SMO compliance. IFAC.

- International Accounting Education Standard Board [IAESB]. (2017) . Handbook for International Pronouncement. IFAC.

- Jackling, B., & De Lange, P. (2009). Do accounting graduates’ skills meet the expectations of employers? A matter of convergence or divergence. Accounting Education: An International Journal, 18(5), 369–385. https://doi.org/10.1080/09639280902719341

- Kadhim Al-Anbagi, A. T., Al-Azzawi, N. S., & Al-Obaidi, H. H. M. (2018). Compliance with International Education Standards (IES 2) in Iraq towards the adoption of International accounting standards. Opcion, 34(86), 2456–2469.

- Khan, S. (2018). Demystifying the impact of university graduate’s core competencies on work performance: A Saudi industrial perspective.”International. International Journal of Engineering Business Management, 10, 1847979018810043. https://doi.org/10.1177/1847979018810043

- Low, M., Samkin, G., & Liu, C. (2013). Accounting Education and the Provision of Soft Skills: Implications of the recent NZICA CA Academic requirement changes. E-Journal of Business Education and Scholarship of Teaching, 7(1), 1–33.

- Mah’d, O. A., & Mardini, G. H. (2020). The quality of accounting education and the integration of the international education standards: Evidence from Middle Eastern and North African countries. Accounting Education, 31(2), 113–133. https://doi.org/10.1080/09639284.2020.179002

- Monga, C. (2019). Jobs: An African manifesto. In C. Monga, A. Shimeles, & A. Woldemichael (Eds.), Creating decent jobs strategies, policies, and instruments (pp. 2–52). African Development Bank.

- Mustafa, M. O. A., & Jaleel Kehinde Shittu, A. (2012). Graduates’ perception of career success and skill emphasis in accounting programme in Nigerian institutions. Journal of Business Management and Accounting (JBMA), 2(2), 49–64. https://doi.org/10.32890/jbma2012.2.2.8667

- Ramaj, B. Z. (2023). Core model of accountancy education and initial professional development in University-Level Programs in Albania. European Journal of Multidisciplinary Studies, 8(1), 157–168. https://revistia.com/index.php/ejms/article/view/6916

- Veneziani, M., Teodori, C., & Bendotti, G. (2015). The role of the University in the education of accountants in Italy and the degree of the IES 2 application. Proceedings of the 38th EAA Annual Congress, University of Strathclyde, Glasgow.