Abstract

Orthodox tea is one of the high-value agriculture commodities having enormous potential of export to international market. Nepal offers suitable climate, soil, and topography for profitable production of the orthodox tea having exceptional flavor, aroma, and taste. The study was designed to analyze the production trend, annual growth rate, export and import, and prospects of the Nepali orthodox tea. Findings showed that production of tea is in increasing trend with an average annual growth rate of 9.55%. Despite possessing ample opportunity in domestic and international markets, yet country only produces little amount of orthodox tea. Further, 90% of the total produced orthodox tea was imported primarily to India which has been one of the factors for not being able to receive optimum premium as compared to other tea exporting countries like China and India. Thus to revitalize tea subsector, it is recommended to focus on improving tea productivity with proper mechanization, establishing tea processing industries, easy and reliable certification, price intervention, market recognition, and enhancing diplomatic relations for easy market accessibility and duty-free trade.

PUBLIC INTEREST STATEMENT

Tea is second most widely consumed drink in the world. In general, there are two kinds of the tea: (1) orthodox tea and (2) CTC (crush, tear, and curl) tea. Orthodox tea is also known as hand-processed tea. CTC tea is the machine processed. Compared to the CTC, orthodox tea has higher antioxidant quality. Orthodox tea is produced using the traditional methods of tea production which includes plucking, withering, rolling, oxidation, and drying. That’s why demand of orthodox tea is very impressive nowadays.

Competing Interests

The authors declares no competing interests.

1. Introduction

Tea is considered as an oldest beverage and is also recognized as the most widely consumed drink (beverage) in the world after water (GIZ, Citation2012). Human being have been brewing beverage made from tea leaves for nearly 5,000 years. Tea has a unique flavor, taste, and aroma. It was invented in 2737 BC by Chinese Emperor Shen Nung who was also known as divine healer (NTCDB, Citation2019). Recognizing the benefits of tea, it has been spread all over the world and now in more than 35 countries with tropical and subtropical climate tea is grown. It is primarily produced in Asia and Africa, with China, India, Kenya, Sri Lanka, and Turkey accounting for 76% of global production (FAOSTAT, Citation2013). In Nepal, tea is planted in 28,241 hectares of land producing 24,409,326 kg of tea, with an engagement of 15,103 farmers from over three dozens of districts (NTCDB, Citation2017). Tea subsector contributes about 0.0105% to the national gross domestic products (GDPs) and 0.0347% to the agricultural gross domestic product (AGDP) (CBS, Citation2014). Agriculture Development Strategy (2015–2035): a long-term vision that guides agriculture sector of Nepal has also prioritized tea subsector for value chain development (ADS, Citation2014). Tea possess high export potential which is helpful for earning foreign currency, eradicating the existing poverty, and thus for uplifting the living standard of the Nepalese farmers (Adhikari et al., Citation2017; CED, Citation2008).

In Nepal, mainly three species of tea are cultivated: (1) Camellia sinensis var. sinensis, (2) Camellia sinensis var. assamica, and (3) Camellia sinensis var. lasiocalyx. Among these three species first two species are cultivated in the larger area (Shrestha, Citation2015). Mostly Camelia sinensis var. sinensis is planted for orthodox tea, whereas Camelia sinesis var. assamica and Camellia sinensis var. lasiocalyx for CTC (crush, tear, and curl). Due to similar geographical and topographical conditions, Nepali tea and Darjeeling tea resemble each other in its appearance, aroma, and fruity taste (ITC, Citation2017). However, Nepali tea has some unique features as compared to Darjeeling tea. The abundance of fine hairy growth (pubescence) on the underside of the leaf, on the bud and sometimes even on the stalk gives Nepali orthodox tea its fine “tippy” quality and precious flavors. Nepali orthodox tea is mostly produced in country’s hilly region and is especially known for its aroma, bright color, and fruity flavor. Similarly, CTC tea of Nepal is mostly grown in lower region (terai) and is famous for its strong, bright, and full-bodied taste. Further, it should be noted that Nepal tea is the symbol of quality from the Himalayas (NTCDB, Citation2019).

Orthodox tea is produced by a special process in which only the top two leaves and bud from each branch are picked at the precise moment when they are budding. Rolling leaves with hand or by the use of such kinds of machine which provides similar rolling action to the tea leaves is common practice (Shrestha, Citation2015). For orthodox tea, leaves are partially dried and then allowed to ferment to produce black tea but for green tea process of fermentation is restricted or not allowed (NTCDB, Citation2019). Therefore, sometimes “orthodox’” also refers to “traditional” or “hand-processed” tea. In Nepal, orthodox tea is generally produced from 1,000 to 2,000 m above sea level (masl) in hilly areas (ITC, Citation2017; NTCDB, Citation2017). Orthodox tea also has its various forms according to its processing nature. Mainly orthodox green, orthodox black, white, and oolong are produced in Nepal. Orthodox tea produced in the hills for export and is available only in limited quantities, while the CTC tea produced in the terai is mostly for domestic consumption (Poudel, Citation2010). Due to higher returns from orthodox tea as compared to other crops, it is also regarded as strong engine for income generation and poverty reduction for farmers especially in rural areas (NEAT, Citation2011). Tea farming is centered in the eastern hills of Nepal. At present, among 77 districts of Nepal, tea is commercially grown in the 14 districts (NTCDB, Citation2017). Among these districts, Jhapa accounts for the highest number of estates/institutions (69) and 1,532 individual tea holdings with highest production of 82.72 million metric ton green tea. Whereas, the highest number (5,582) of the individual tea holdings are present in Illam with 16 estate/institution accounting the second highest production of 15.97 million MT green tea. Altogether there are 9,127 (98.8%) individual small tea holding and 108 (1.2%) estate/institution large tea holding in an area of 12,066.5 hectares with total production of 100.08 million MT green tea (NTCDB, Citation2017). Total income generated from green leaf production among these 14 districts is NRs. 1,766.38 million (USD 15.856 million).

Global tea production is ever increasing. The reason for the growth in world output is the considerable increase in production in the major tea-producing countries, China and India, and also in the two largest tea-exporting countries, Kenya and Sri Lanka. China continues to be the largest tea-producing country with an output of around 2.3 million tons, accounting for more than 43% of the world total. On the other hand, production in India increased to 1.2 million tons in that same year. Kenya and Sri Lanka also increased production output, with the former reaching 399,211 tons and the latter 328,964 tons. China, India, Kenya, Sri Lanka, and Turkey are the top five producer of the tea that occupies together 76% of the total tea production over the world (ITC, Citation2017). Further Sri Lanka is the world’s largest producer and exporter of black tea, accounting for 26.2% of world exports, followed by Kenya (16%), India (13.6%), China (6.6%), and the United Arab Emirates (6.4%). Orthodox tea is becoming famous because of its antioxidant and antibacterial properties. It has performed remarkably well over the past 5 years (2010–2015). World exports of green tea stood at 1.7 billion USD in 2015, growing at a compound annual growth rate (CAGR) of approximately 10% over the past 15 years. While green tea imports have recorded growth in almost every region, substantial growth has been observed in sub-Saharan Africa and to a lesser extent the Middle East and East Asia and the Pacific. Morocco is the leading green tea importer, accounting for 13% of world imports in 2015, followed by the United States (8.9%), France (5.5%), Germany (5%), and the Russian Federation (3.9%). China dominates production and exports of green tea accounting for 62.6% of world green tea exports in 2015, followed by Japan (4.9%) and Sri Lanka (2.7%). Germany and Poland are re-exporters of green tea, accounting, respectively, for 5.1% and 2.3% of world exports (ITC, Citation2017).

The favorable soil conditions, high altitude, and excellent climatic condition favors profitable production of tea in Nepal (Karki et al., Citation2011). Cultivation of the orthodox tea has enormous opportunity in the domestic as well as international market. Orthodox tea is generally exported to international markets and CTC tea is supplied for domestic consumption apart from some export to India and Pakistan. Mainly orthodox tea was produced in hill districts such as Ilam, Panchthar, Dhankuta, Terathum, Solokhumbhu, Udayapur, Sankhuwasava, and Bhojpur in the eastern part of the country; and Sindhupalchowk, Kavre, Makwanpur, Lalitpur, Ramechhap, and Kaski districts in the central part (ITC, Citation2017). The aim of the present research was to study the prospects of Nepali orthodox tea especially its production and marketing.

2. Methodology

The study was carried out to reveal the production and marketing status of tea especially orthodox tea in local and global context for Nepal. To understand the production and marketing function in tea industry primarily secondary data were collected from the publications of National Tea and Coffee Development Board (NTCDB), Trade and Export Promotion Center (TEPC), Ministry of Industry, and Commerce and Supply (MoICS) which include book, booklets, and other statistical records. Relevant policies, laws, and regulation existing in this sector were also taken into consideration to suggest the possible policy implication for improvement of this subsector of agriculture.

More than two dozens of literature including open access online peer reviewed national and international research and review papers form different journals, presentation report of different related departments, conference proceedings, and abstract, blogs, and websites were reviewed. The collected secondary data were assembled in Microsoft Excel and graphs were generated.

Linear trend line analysis was carried for estimating the average annual change in the tea production in the country.

Mathematical expression for linear trend line:

Y = a + bt.

Where “Y” is a production of the tea at time (t), “b” is an average annual growth (kg), “t” is a time factor in years, and “a” is an intercept.

Percentage change was estimated with following expression:

Percentage (%) change = X2 - X1/X1 * 100

3. Results and discussion

3.1. Tea production in Nepal

Government of Nepal and Nepal Trade Integration Strategy (NTIS) have recognized tea as high-value commodity with export potential (ITC, Citation2017; National Planning Comission Secretarait, Citation2004). Cultivation of tea had been expanding over central and western regions (Poudel, Citation2010). Agriculture sector profile prepared by Government of Nepal had projected a possibility of expansion of total tea cultivating area of 62,800 hectares within the next 15 years (Investment Board Nepal, Citation2017). Tea cultivation was marked as most fascinating subsector of agriculture with huge potential of promoting agrotourism. Land suitability for tea plantation was well renowned and recognized for Nepal. Most of the Nepal’s topography belongs to mountainous or hilly region where many barren land terrain and terraces are commonly seen. These virgin barren lands could be exploited for the tea plantation based on agroforestry model to reap much benefit and to alleviate existing poverty in mid-hills of Nepal (NEAT, Citation2011).

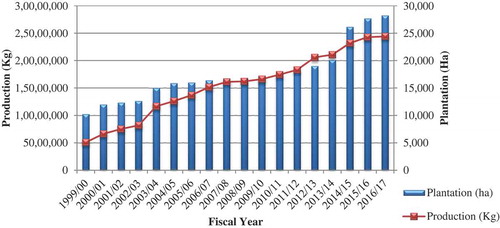

In the base year 1999/2000, the tea plantation was in 10,249 hectare accounting the production of 5,085,237 kg while it grew in recent fiscal year 2016/17 to 28,241 hectare with the tea production of 24,409,326 kg. Hence, Figure clearly showed that increasing trend of the tea producing area and tea production in the country.

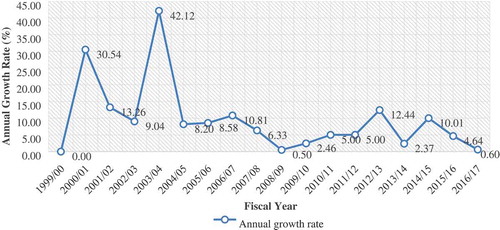

The average annual growth rate of tea production in Nepal was estimated around 9.55%. Further estimation of the percentage change in the tea production from base year (1999/2000) to recent year (2016/17) showed 380.004% increase. While similar estimation for the tea-cultivated area showed that there was increase of tea cultivating area by 175.54% from 1999/2000 to fiscal year 2016/17. Annual growth rate for individual fiscal year was shown in Figure . Over the course of the last decade, Nepal’s tea industry has witnessed a significant increase in the areas of cultivation and production. Thapa (Citation2004) also reported that growth of tea production in Nepal has been impressive; increasing at significant rate where most of the growth in the recent year has come from expansions in area.

3.2. Production of orthodox and CTC tea

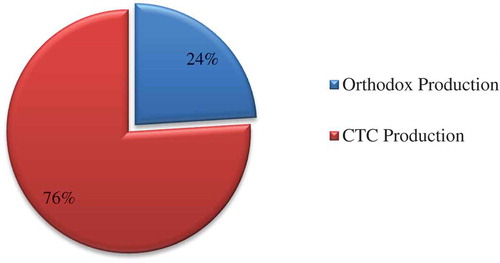

In fiscal year 2016/17, orthodox tea was cultivated in 16,798 hectares of land with a production of 5,861,894 kg (NTCDB, Citation2017). Figure showed the share of orthodox tea was less compared to CTC tea in the total tea production in the country in 2016/17. It was found that productivity of the orthodox tea was far lower than CTC tea, while the price of former is higher than later (Sapkota, Citation2012). ITC (Citation2017) reported orthodox tea had a yield of 334 kg per ha, while CTC produced 1,598 kg per hectare. However, NTCDB forecasted the total tea production of 54.7 million kg by 2020, of which CTC will account for 22.5 million kg and orthodox tea, 32.2 million kg (ITC, Citation2017). Higher returns and greater health benefits, increasing public interest in domestic markets may be the contributing factors for increased production and blooming market opportunity for orthodox tea in near future.

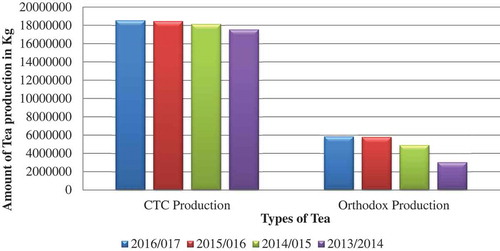

Moreover, it was found that most of the plantation area in CTC is owned by estates, whereas the plantation area in orthodox tea is dominated by small farmers. Figure showed production of CTC over orthodox tea for last four fiscal years. ITC (Citation2017) also reported similar findings, where 75.6% of the total land occupied by small land holding tea farmers was under orthodox tea cultivation. This clearly marked the greater engagement and contrbution of small farmers for the orthodox tea production.

3.3. Tea market

The world demand for tea was surprisingly high as compared to its current production (Thapa, Citation2004). Unlike coffee and cocoa, majority of the tea production is consumed locally in the domestic markets. In the total tea production, black tea production was found higher as compared to orthodox tea. However, with increasing public interest and eminent health benefits the demand of orthodox tea is also blooming.

3.4. Export and import of tea in Nepal

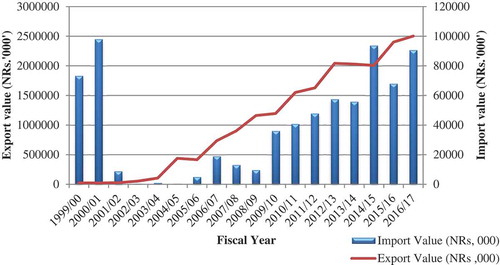

The overall trend is positive and increasing for export of tea in Nepal. Import of the tea in the country is relatively low as compared to export as shown in Figure .

The Ninth Five-Year Plan recognized orthodox tea as a major export potential product (Kattel, Citation2011; SAWTEE and AAN, Citation2006). At present, more than 90% of the orthodox tea produced in the country was currently exported (Sapkota, Citation2012; Investment Board Nepal, Citation2017). Further, about 88.5% of the orthodox tea of Nepal is exported to India only. Rest of the market for the Nepalese orthodox tea includes Germany, the Czech Republic, the Russian Federation, China, France, the United States, Japan, Canada, and Ukraine (ITC, Citation2017). For Nepal, India (Darjeeling), Sri Lanka, China, Bangladesh, and Chinese Taipei are the major competitor in orthodox leaf grade. Compared with Nepal, these countries have better quality management (QM) and certification practice (NEAT, Citation2011).

Nowadays, traders who were focusing on exports a few years ago are now expanding their business in the domestic sector too. However, one of the biggest challenges that remain is the lack of direct access to the international market. ITC (Citation2017) reported that the price of orthodox green leaves was mostly determined by the price received by made tea in the Siliguri and Kolkata markets. Farmers had to accept the price levels offered by the factories. So there was need of proper intervention from concerned authority to fix scientific price for tea farmers.

The Ministry of Agricultural Development (MoAD) has recently endorsed the Nepal Orthodox Tea Certification Trademark Implementation Directive, which has envisioned such collective trademark for domestically produced orthodox tea for the first time in history. The collective trademark “Nepal Tea, Quality from the Himalayas” is believed to increase the credibility of Nepali tea in the global market and assure competitive quality of the product (ITC, Citation2017). Basically, the use of collective trademark in tea that is being exported to different countries will guarantee proper production, processing, and packaging of Nepali tea in the international market. Therefore, Nepal has immense opportunities in enhancing the tea industry with favorable market access condition in most of the export destination, especially in duty-free access in destination. However, feeble supply side capacity was major problem for establishing reliable and long-term trade relationship with international market agents.

3.5. Top exporters and importers of tea around the world

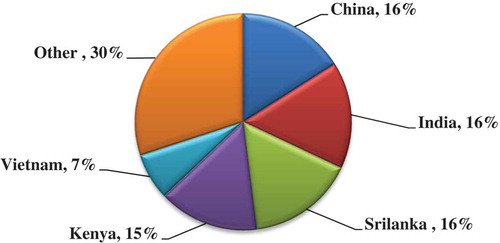

China, India, Sri Lanka, Kenya, and Vietnam are the top five exporters of tea in the world which together occupies about 70% of total tea exports as shown in Figure .

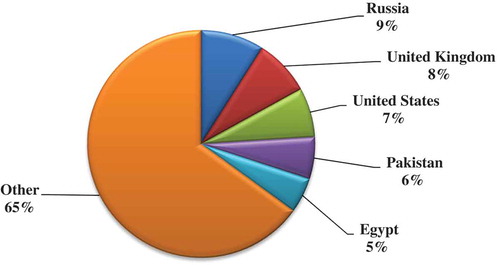

Amount of the tea imported by individual country was found to differ with the types of tea. For instance, Morocco is the major importer of green tea. In overall Russia, the United Kingdom, the United States, Pakistan, and Egypt are the top five importers of tea, which together occupy 35% of the total imports as shown in Figure .

3.6. SWOT analysis

Strength, weakness, opportunity, and threat associated with production and marketing of orthodox tTea are presented in Table .

Table 1. Strength, weakness, opportunity, and threats

4. Conclusions

Land occupied by tea and tea production in the country is in increasing trend with expansion of tea-cultivating lands from eastern to central and western part of country. Among different types of tea processed in the country, CTC dominates other types of tea like orthodox, green tea, etc. Export of the Nepalese tea is positive and is in increasing trend. Major destination of tea produced in Nepal is India. Endorsement by the Nepal Orthodox Tea Certification Trademark Implementation Directive is believed to increase the credibility of Nepali tea in the global market and assure competitive quality of the product. However, feeble supply side capacity of country is becoming immersing challenge in establishing long-term partnership with international markets agents. So for the improvement of this subsector, government should first focus on improving the status of the domestic tea estate to enhance their production per unit of land. There is need of adequate, efficient, and effective extension services to the tea growers for improving their cultivation and management practices. Subsidy on the tea seedling is vital for encouraging farmers to grow tea. Tea subsector should be mechanized by introducing innovative and advance modern technology, tools, and equipment which will help to boost the tea production and attract more farmers in this sector. Government intervention through price fixation of the orthodox tea and green leaves is urgent need. With the increasing competitiveness in the international market, Nepal has to make easy and cheap procedure of the certifying domestic tea in farm level. International competitor like China, Kenya, and India are reaping the benefits of premium (1–20%) with standard complaint of Organic Certification, or Fairtrade International Certification, or UTZ Certification, or Rainforest Alliance Certification, etc. In international market, Fairtrade-International-certified tea receive high premium whereas UTZ-certified receive least one. Thus there is a strong need to make tea growers aware of competitive advantage by adopting good agricultural practice and recognizing their products as GAP certified to enhance the competitiveness of the Nepali tea.

Author’s Statement

Dharmendra Kalauni, Binod Joshi, and Arati Joshi are an agriculture graduate from Agriculture and Forestry University, Ramupur, Chitwan, Nepal. Dharmendra Kalauni is a young researcher and youth activist. His area of interest includes Agricultural and Applied Economics and Statistics. He is currently working as an Agriculture Extension Officer in Ditketl Rupakot Majhuwagadhi Municipality. Binod Joshi is serving as the field officer at Sankalpa project. He has special interest in horticultural crops. Arati Joshi is currently working as an agriculture instructor of Agri-business management and Agri-extension. Her area of interest includes agricultural extension, agricultural economics, and gender.

Additional information

Funding

Notes on contributors

Dharmendra Kalauni

Dharmendra Kalauni, Binod Joshi and Arati Joshi are an agriculture graduate from Agriculture and Forestry University, Ramupur, Chitwan, Nepal. Mr. Kalauni is a young researcher and youth activist. His area of interest includes agricultural and applied economics and statistics. He is currently working as an Agriculture Extension Officer in Ditketl Rupakot Majhuwagadhi Municipality. Mr. Joshi is serving as the field officer at Sankalpa project. He has special interest in horticultural crops. Ms. Joshi is currently working as an agriculture instructor of Agri-business management and Agri-extension. Her area of interest includes agricultural extension, agricultural economics and, gender.

References

- Adhikari, K. B., Regmi, P., Gautam, D., Thapa, R., & Joshi, G. R. (2017). Value chain analysis of orthodox tea: Evidence from Ilam district of Nepal. Journal of Agriculture and Forestry University, 1(1), 61–10. http://afu.edu.np/sites/default/files/Value_chain_analysis_of_orthodox_tea_Evidence_from_Ilam_district_of_Nepal_6168_K._B._Adhikari_P.P._Regmi_D._M_Gautam_R.B._Thapa_and_G.R._Joshi.pdf

- ADS. (2014). Agriculture development strategy (2015-2035). Ministry of Agriculture Development.

- CBS. (2014). Statistical year book of Nepal. Central Bureau of Statistics, National Planning Commission of Secretariat, Government of Nepal.

- CED. (2008). Developing strategy to explore the feasibility of mainstreaming and linking (cooperative) processing units in the tea sector in the ongoing coc strategic (supply chain) activities in Ilam And Panchthar Districts. SNV East Portfolio.

- FAOSTAT. (2013). Faostat database. Rome, Italy: Food and Agriculture Organization of the United Nations.

- GIZ. (2012, May). Nepal Trade Issue 3.

- ITC. (2017). Nepal national sector export strategy tea (2017-2021). Government of Nepal.

- Karki, L., Schleenbecker, R., & Hamm, U. (2011). Factors influencing a conversion to organic farming. Journal of Agriculture and Rural Development in the Tropics and Subtropics, 112(2), 113–123. http://jarts.info/index.php/jarts/article/view/351

- Kattel, K. (2011). A swot analysis on tea cultivation in Nepal. Department of Agricultural Extension.

- National Planning Comission Secretarait. (2004). Enhancing the competitive strength of Nepalese agricultural produce. National Planning Commission Secretariat, Central Monitoring and Evaluation Division, Government of Nepal.

- NEAT. (2011). Value chain/market analysis of the orthodox tea sub-sector in Nepal. Nepal Economic Agriculture, and Trade Activity, USAID Nepal.

- Nepal, I. B. (2017). Agriculture sector profile. Ministry of Industry.

- NTCDB. (2017). Survey on commercial tea cultivation-2075. CBS.

- NTCDB. (2019). National tea and coffee development board: Government of Nepal. NTCDB. Retrieved May 9, 2019, from http://www.teacoffee.gov.np/

- Poudel, K. (2010). Orthodox tea production and its contribution in Nepal. The Third Pole, 34–42. https://www.nepjol.info/index.php/TTP/article/view/11510

- Sapkota, K. B. (2012). Implication of WTO on Nepalese agriculture: Competitiveness of Tea. Tribhuwan University.

- SAWTEE and AAN. (2006). Trade and industrail policy environment in Nepal. South Asia Watch on Trade, Economics & Environment (SAWTEE) and ActionAid Nepal (AAN).

- Shrestha, S. (2015). Tea Cultivation Manaul. NTCDB.

- Thapa, Y. (2004). Commodity case study - tea. In FAO, the implications of the WTO memberhsip on the Nepalese Agriculture (pp. 222–240). Food and Agriculture Organization.