?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The present paper examines the impact of financial and social performance of microfinance institutions (MFIs) on lending interest rate. The paper has covered five-star-rated MFIs in all the six regions of the world individually and collectively for the period of 2006–2012. Data for 382 MFIs belonging to 70 countries around the world have been taken from the Microfinance Information Exchange (Mix Market). Financial performance is captured through return on assets, return on equity, and operational self-sufficiency, whereas social performance is measured through average loan size and number of credit clients. The lending interest rate is a weighted average of the interest rates actually received by the MFIs from their clients. The paper incorporated some control variables to capture variations in size, age, location, and infrastructure of MFIs. Panel data estimation techniques have been applied to find out the empirical association between the selected variables. Most of the results have shown that cost of funding, return on assets (ROA), and the number of credit clients have a significant positive impact on lending interest rate around the world. However, depth outreach as depicted by average loan size has significant inverse relation with lending interest rates. Moreover, results also highlight different factors that affect the productivity of MFIs around the world.

Public Interest Statement

The basic purpose of the microfinance institutions is to fulfill the demand of poor segment of the society by providing them credit facilities on affordable interest rates. This industry has a dual mission, that is to expand its social outreach and at the same time maintain its financial sustainability. The way microfinance institutions pursue their social and financial objectives has consequences on their interest rate determination. Thus, this paper helps MFIs, borrowers, and policymakers to understand this interest rate mechanism. The high interest rate signals more emphasis in attaining financial objectives on the cost of sacrificing the social outreach. The results suggest that MFIs required a tradeoff between social and financial objectives.

1. Introduction

As a result of incapacity of development and traditional banks to effectively finance the low-income population of the world, microfinance seems like a continuum between pure capitalism and socialism economies (World Bank, Citation2008).

In the literature, microfinance institutions (MFIs) seem to be understood as financial organizations engaged primarily in the business of giving small-scale loans and financial amenities to poor and financially “unbankable” customers, while also devising the key element of a “double bottom line”—concentrating on one side on social features including poverty reduction, promoting education, and outreach and on the other side financial yield and sustainability.

In developing countries, the problems triggered by informational lopsidedness that are distinctive to credit markets are intensified since low-income people lack collateral that can be provided against loans and because of the weak legal system enforcement cannot be possible, in case a client back out on his loan. Generally, the poor are unable to get money from formal money providers. These are the main cause of lack of access to credit that leads to persistent poverty traps and inequality in incomes (Beck, Demirguc-Kunt, & Levine, Citation2007; World Bank, Citation2008).

In the beginning era, most MFIs were not-for-profit organizations, usually known as non-governmental organizations (NGOs). The main aim of an NGO is not profit-seeking. If an NGO is profitable, the profit is used in funding additional financial services so in this way the profit remains in the organization and used for the welfare of clients. But many NGOs have ultimately started deposit-taking to their undertakings since they realize savings facilities allow them to increase their microlending operations and cliental. When NGOs seek permission from a government authority for taking up deposits, they are generally required to alter their businesses into for-profit shareholder-owned organizations. When this materializes, profits can wind up in the pockets of private stockholders, inexorably raising the approach of such owners making extreme returns on their investment by charging obnoxious interest rates to poor customers who have little-negotiating control since their other credit choices are limited (CGAP, Citation2009).

The issue of high interest rate and its influence on low-income clients has frequently faced by MFIs. One of the reasons is the inevitably higher operating costs for small-size loans as compared to typical bank loans. For example, the administrative cost in the form of staff salaries is generally higher for advancing $200,000 divided among 1,000 borrowers getting $200 each as compared to a single loan of $200,000. Therefore, MFIs have to charge higher interest rates as to the rates charged on normal bank loans.

As a result, MFIs claiming to have a social mission of helping poor nonetheless accuse them with high interest rates. These rates are considerably higher than the rates, paid on commercial bank loans by wealthier clients. No wonder this gives a negative impression to viewers those generally do not recognize and approve the philosophy that MFIs can benefit their clients effectively, if they function profitably, instead of making losses that need a persistent injection of subsidies.

As the beginning of the modern microfinance movement in the late 1970s, high microloan interest rates have been condemned largely. But in the past few years, this criticism has strengthened. Various countries of the world, therefore, considered interest rate ceiling. One of the purposes behind this augmented anxiety about interest rates is mere that microfinance industry is getting increased public attention on each passing day, and this increases the scope of this industry and giving it an opportunity to levied high rates on clientele.

Another element is that some of the MFIs at the moment are transformed into private commercial corporations. Since the financial and social objectives have a direct impact on the interest rate charged by MFIs, it is important to examine this relation empirically.

Therefore, this study tries to examine the relationship between the cost of funding and lending interest rate. The study also considers various indicators of financial and social performance of MFIs and their impact on the lending interest rate. Moreover, the study investigates the factors affecting the productivity of MFIs.

In order to meet the above mentioned objectives, this research empirically analyzes the following: (1) What is the impact of the cost of funding on interest rate determination? (2) How the financial performance of MFIs affects their interest rate determination? (3) What is the impact of microfinance breadth and depth of outreach on the determination of lending interest rate around the world? (4) How the productivity of MFIs is affected by different factors?

The paper contributes to the existing literature by investigating that the high rate of lending is because of low outreach, low productivity, and high operating and administrative costs in MFIs. It also highlights that high interest rates reflect the intention of MFIs to become financially sustainable and self-sufficient. The paper also signifies that age, size of MFIs, and their geographic location affect the formation of lending interest rates. Furthermore, the paper proves that the productivity of MFIs has an important impact on the formation of lending interest rate.

The rest of the paper is organized as follows: Section 2 includes a literature review. Section 3 covers data and econometric specifications. In Section 4, results and discussions are given, whereas Section 5 concludes the paper along with policy implications.

2. Literature review

Historically, societies had commended on the use of usury interest rates. The ancient societies, mainly based on religious doctrine, consider the sole use of interest for a forbidden activity. According to Ashta (Citation2010), in economics of microfinance, ancient Greeks and Romans including Plato and Aristotle inveighed against moneylenders and the very act of charging interest on loans (Vermeersch, Citation1912).

In literature, there are two schools of thoughts to evaluate MFI mission. Researchers have discussed both a welfarist approach to microfinance and an institutionalist approach. The welfarist evaluates MFI’s success by values like poverty reduction and credit penetration (Gutiérrez-Nieto, Serrano-Cinca, & Mar Molinero, Citation2009; Hartarska & Denis, Citation2008), while the institutionalists measure on the basis of sustainability and profitability (Cull, Demirguc-Kunt, & Morduch, Citation2008; Nawaz, Citation2010). Most recent studies have tried to address both schools of thought and present outcomes in light of both financial and social (welfare) findings.

In microfinance framework generally, two levels of financial sustainability are mentioned (Ledgerwood, Citation1997). One of them is operational self-sufficiency (OSS) and the other is financial self-sufficiency (FSS). OSS normally shows the financial performance of the MFIs, where FSS depicts the actual financial health of MFIs. OSS only incorporates operating income and operating expenses along with a provision of loan loss. But it does not include the cost of capital, which is essential to portray the true picture of the financial sustainability of the MFIs. Thus, FSS includes the cost of capital (adjusted) apart from the factors covered by OSS.

These two levels of sustainability were mostly discussed by researchers. Pollinger, Outhwaite, and Guzmán (Citation2007) state that self-sufficiency is the stage when MFI can operate fully on the basis of the income generated through its lending operations and services. However, Vinelli (Citation2002) defines FSS as a ratio of operating income divided by the operating expenses incurred, therefore eliminating revenue from subsidies. A subsidy is a crucial matter in the case of sustainability of microfinance, and it is also observed as a constraint in achieving sustainability of microfinance program.

Moreover, past studies also disclose varied results in different locations of the world. For example, Adongo and Stork (Citation2005) conducted a paper in Namibia. They found that no MFI autonomously financially sustainable, whereas Robinson (Citation2001) in Indonesia found that MFIs are profitable, sustainable, stable, and widespread, letting millions of the world’s poor to construct enterprises, increase incomes, and attain self-confidence.

In defining the sustainability of MFIs, the impact of interest rates cannot be undervalued. Resultantly, nowadays, what motivates an MFI to formulate its interest rate strategy turn out to be a debate of immense importance. The high rate of interest, which is charged by many MFIs in the world, has drawn a widespread attention of policymakers throughout the world. It is mentioned that currently about 40 developing countries have interest rate ceilings of some kind (Helmes & Reille, Citation2004).

The financial and social performance of MFIs directly affects their interest rate planning; Hudon and Traca (Citation2008) state in their paper that MFIs should do a tradeoff between financial and social efficiency, preferably financial efficiency, so they can better perform their social work. Thus, the formation of interest rate policy is primarily influenced by the social intentions and financial performance of an MFI.

In emerging countries, borrowers are frequently surprised by the superficially high interest rates for small loans charged by MFIs. Typical rates of interest charged by MFIs range between 2% and 4% on monthly basis and 20% and 80% per annum, depending upon the package.

Lewis (Citation2008) points out that there are some institutes in the industry which charge from their customer’s extremely high rate of interest. He pointed those MFIs as “Microloan Sharks” indulged not in microlending but microloan‐sharking. With a different view, Cull, Demirguç‐Kunt, & Morduch. (Citation2007) stated that for individual-based lending, raising interest rates resulted in increased profitability for MFIs, and the reverse is true in the case of solidarity group lending.

Another paper written by Gonzalez (Citation2010) shows that the transaction cost in microfinance industry is the main cause of high interest rates. Lending in small amounts of money to poor people in remote areas absorbs high operational and administrative cost that pushes MFIs to charge high rates from clients to cover up their cost.

Cull et al. (Citation2007) state another dimension by analyzing interest rates and lending methodologies of MFIs. They found that individual lenders—those lenders who do not lend money using a group-collateral scheme—are more profitable by charging increasing interest rates. The evidence indicated that profits will increase for individual lenders up to an interest rate of around 60%, providing some insight into problems with MFI incentives. On the other hand, the opposite is true for solidarity lenders, like Grameen Bank. MFIs lending to groups normally show a reduction in profits when interest rates increased. Other studies have also established that group lending is preferred for social objectives since it leads to better outreach (Roy & Strom, Citation2010).

Another important aspect regarding interest rate is its regulation as pointed by Brand (Citation2003) that it is necessary to regulate the interest rate to safeguard the poor borrowers against the high rate charged by MFIs. Another view is that the ceiling of the interest rates could motivate the MFIs to let the poor and to serve the rich as documented by Ashta (Citation2009).

According to Yunus (Citation2007), the use of consumer protection law and disclosure practices as those generally used by banking sector assists the lender to disclose loan information that permits comparison and the effectiveness of interest rate. This is a manner to aware the clients about the agreement and avoid exploitation. Moreover, truth-in-lending and disclosure practices in a competitive environment are considered to be more efficient in dropping interest rates than the interest rate ceilings. So before going to regulate interest rates, government should necessarily ensure that it really has the means to guarantee the respect of this disposition to all related parties. An interest rate regulation should be considered the facets guaranteeing the transparency (Cotler, Citation2010).

Hartarska (Citation2005) finds that in Eastern Europe and Central Asia, the regulated MFIs have a lower return on assets (ROA) compared to other regions, and there is an insignificant evidence that the breadth of outreach is affected by regulations. In another study, Hartarska and Denis (Citation2007), after controlling the endogeneity problem, find out that the regulations have no impact on the financial performance of MFIs, and there is a small proof that MFIs who are regulated normally serve less poor borrowers.

When investigating interest rates, the important aspect is to see how much competition is faced by MFIs in the region or country in which they operate. According to the structure–conduct–performance theory, competition and interest rates are inversely related, which means that the more the competition among lending institutions, the less the interest rates are. There are different views about this argument (Kai, Citation2009).

Petersen and Rajan (Citation1995) find that lending institutions that have greater market power are those with sufficient funds to invest in relationship lending. Consequently, as market power increases, the possibility that small firms will be granted loans is greater and therefore interest rates should decline. With a different argument, Marquez (Citation2002) and McIntosh and Wydick (Citation2005) arrive at the conclusion that, as competition among financial institutions increases, default risks may follow a similar path and so does interest rates.

Other authors, including Boot and Thakor (Citation2000), claim that a relationship bearing helps to somewhat safeguard the financial institution from the competition. Thereby, greater competition may reassure financial firms to transfer resources to more relationship lending, and consequently, smaller firms may face a decline in the lending interest rates. Thus, in the theoretical literature, there are two contradictory suppositions regarding the impact of an increased competition on interest rates.

One of the studies by Hartarska, Gropper, and Caudill (Citation2009) describes the size of MFIs. By taking data from the Mix market for MFIs in Eastern Europe and Central Asia, they found that MFIs with a large number of total assets have experience decrease in their costs, thus indicating the benefits to scaling.

Roy and Strom (Citation2010) have the most recent paper on MFI mission drift. They found no substantial signal of mission drift and found that although MFIs attain higher profits with higher loan sizes, this permitted them to continue to target poor customers. Therefore, the cost–benefit comparison allowed MFIs to stay on track, serving typically poor customers rather than targeting wealthier clients.

After reviewing the literature, it is clear that higher interest rates in the microfinance industry are the combination of different factors. The determination of interest rate in the microfinance industry mainly depends upon the motive of MFI. In the case of sustainability motive, there is an upward trend in interest rates, whereas opposite happens in the case of social objectives (Copestake, Citation2007).

3. Data and methodology

3.1. Data

For the current study, the data have been collected for financial performance indicators: ROA, ROE, and OSS. Social performance is captured by average loan size (AVGLS) and number of credit clients (CC). Other variables are the cost of funds, lending interest rates, operating costs, productivity, for 382 MFIs, those are located in 70 countries throughout six regions of the world namely Africa, Eastern Europe, East Asia, Latin America, Middle East, and South Asia (Appendix 1). All the variables are described in Section 3.2. The annual information for the five-star MFIs is taken from Microfinance Information Exchange (Mix Market) which is an authentic source, providing uniform data for all registered MFIs around the world. This enables me to work with high-rated MFIs, having a third-party rating and audited financial statements. Given the time span from 2006 to 2012, the paper has an unbalanced panel data with 2,631 observations.

3.2. Variables used in the study

Following are the details of dependent, independent, and control variables used in the study along with their description.

3.3. Econometric specification

In order to analyze the relationship among variables, panel data estimation technique is used and Hausman test suggests to apply random effect model as the p-value turned out to be insignificant. I also applied the generalized method of moments (GMM), but for brevity, only the results of random-effects estimations are presented.

3.3.1. Impact of financial and social performance on lending interest rate

This study used three financial performance indicators ROE, ROA, and OSS, which are estimated through three separate models 1(a), 1(b), and 1(c), respectively. Social performance that represents the outreach of MFIs includes both breadth and depth dimensions. The breadth of outreach is shown by the number of CC. However, the depth of outreach is shown by the average loan size (AVGLS). This indicator has been used by different studies including, Cull et al. (Citation2007), and Olivares-Polanco (Citation2005). All of them have agreed that the smaller is the average loan size, the deeper is the outreach of MFIs. The model 1 also includes regional dummies to examine the cross-regional differences in the lending interest rate. There are six geographical regions in which the MFIs perform their functions: East Asia and the Pacific (EAP); Eastern Europe and Central Asia (EECA); Middle East and North Africa (MENA); Africa (AF); Latin America and the Caribbean (LAC); and South Asia (SA).

Other dummy variables include lending methodology, regulation, and legal status. The lending methodology is classified into two categories: Individual (I); and Group/Solidarity (S). On the basis of legal status, MFIs are classified into four classes: non-governmental organizations (NGO); banks (B); non-banking financial institute (NBFI); and cooperatives or credit unions (Coop). Among control variables are competition (COMP), age, size, depth of information index (DINI), biodiversity index (BDI), and population density index (PDPSM).

The omitted variables (reference categories) are individual for lending methodology, Africa for region, for legal status, Banks; and for regulation, not-regulated.

3.3.2. Region-wise impact of financial and social performance on interest rate including the interaction of size and age

My sample consists of different sizes (small, medium, and large) and age (number of years of operation) of MFIs that may create heterogeneous impact, so I tried to capture these differences in all regions by including size and age interaction terms with the cost of lending and productivity and ROA in the model 2.

3.3.3. Evidence on productivity

To see the impact of different factors on the productivity of MFIs, I regress productivity against the set of control variables including age, size, competition, biodiversity index, Human Development Index (HDI), population density per square mile, depth of information index, and strength of legal rights index, along with the joint effect of biodiversity with population density and HDI with population density.

4. Results and discussion

This section reports MFIs distribution on the basis of regions, legal status, and regulations. Later in this section, descriptive statistics of all variables are presented. Finally, the main results of all the models are presented along with discussions.

4.1. Distribution of MFIs

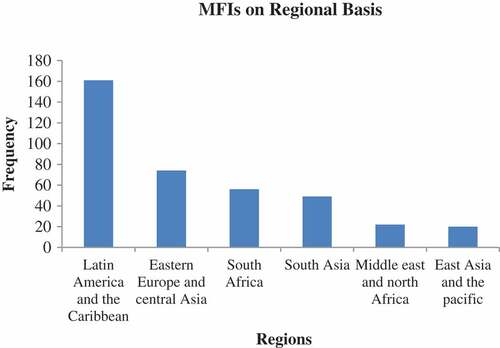

4.1.1. MFIs on regional basis

Table depicts the geographical distributions of my data set. Out of total, 42% MFIs are located in Latin America, 19% in Eastern Europe, 15% in South Africa, 13% in South Asia, 6% in Middle East, and the lowest sample constitutes only about 5% of East Asian MFIs.

Table 1. MFIs on regional basis

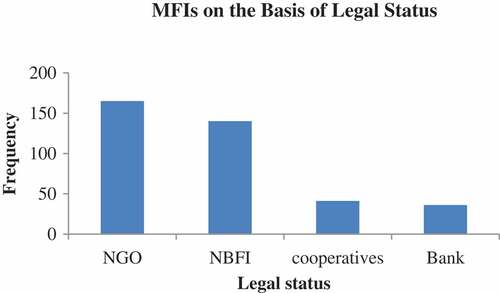

Table 2. MFIs on the basis of legal status

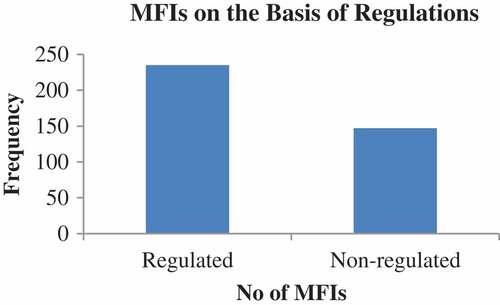

Table 3. MFIs on the basis of regulations

4.1.2. MFIs on the basis of legal status

Table shows the comparison of data set on the basis of the legal status of MFIs. Out of total, 43% of total MFIs are registered as NGOs, 36% as NBFIs, and 11% as cooperatives/credit union. Bank constitute only 10% of total MFIs of data set.

4.1.3. MFIs on the basis of regulations

Table shows, more than half (62%) of the MFIs in data set are regulated. However, 38% of MFIs are non-regulated.

4.2. Summary statistics

In this section, the descriptive statistics of the dependent and independent variables are presented.

4.2.1. Descriptive statistics of main variables

Table shows the descriptive statistics of all the main variables along with their mean, median, maximum, minimum, and standard deviation. Tables and show the descriptive statistics of all the control and dummy variables, respectively.

Table 4. Descriptive statistics of main variables

Table 5. Descriptive statistics of control variables

Table 6. Descriptive statistics of dummy variables

4.3. Correlation

The correlation matrix examines the degree and direction of relationship among the variables.

Table shows that the correlation among variables is not high and this reflects the non-existence of multicollinearity among variables.

4.4. Results of panel data estimation

4.4.1. Results of model 1

The results of model 1 are presented in Table . The empirical results show that all indicators of financial performance (ROE, ROA, and OSS) have a significant positive relation with the lending interest rate as shown by model 1a, 1b, and 1c respectively. The results of financial performance indicators and funding cost are according to my expectations and in accordance with the findings of Cotler (Citation2010) and Rosemberg, Gonzalez, and Narain (Citation2009)

Table 7. Correlation matrix

Table 8. The Impact of Financial and Social Performance of MFIs on lending Interest Rate

As to depth outreach, AVGLS has a significant negative impact on lending interest rate. The results show the fact that the smaller is the size of loan, the higher is the interest charged on these loans. Cull et al. (Citation2007) state that the small size of loans symbolizes that MFI is targeting poor customers as the well-off customers are not attracted to small loans. Significant inverse relation between IL and AVGLS is line with the results of Cotler (Citation2010) and Rosenberg et al. (Citation2009).

The variable breadth outreach (CC) has also shown a significant positive impact on the lending interest rate and in line with the findings of Hermes, Lensink, and Meesters (Citation2009). As expected, there is a significant inverse relationship between the lending interest rates and productivity. As MFI becomes more productive, it tends to manage its operating expenses and thus able to charge lower interest rates.

With regard to dummy variables, lending methodology shows that those MFIs who mostly lend to individuals generally charge significantly high rates of interest. The result is in line with the findings of Cull et al. (Citation2008), showing that individual-based lenders are more profitable as compared to group lenders since they charge higher interest rates.

As to legal status, MFIs with bank’s status charge high rates of interest from their customers in comparison to NGOs, NBFIs, and cooperatives, who on average charge lower interest rates. As to regions, MFIs who are operating in East Asia, Eastern Europe, Middle East, South Asia, and Latin America are charging relatively low interest rates as to African MFIs, who normally charge significantly high rates of interest. Furthermore, the results point out that the coefficient of competition is significantly negative at 5% level.

In terms of control variables, MFI size, age, depth of information index (DINI), biodiversity index (BDI), and population density (PDPSM), results show that MFI size, DINI, and BDI are positive and significant at 5% and 10% levels. However, age has a significant inverse effect which shows that as MFIs become older, they tend to charge a low rate of interest from their clients, and this result is in line with the findings of Campion, Ekka, and Wenner (Citation2010). Over time, MFIs tend to learn more from their clients and able to cut costs while providing even more better services.

4.4.2. Results of model 2

The results of model 2 are presented in Table . In order to show a heterogeneous impact, the variables size and age are included as interaction terms with the lending interest rate (IL) productivity (PROD) and return on assets (ROA) in the model 2. The results show that funding cost (IF) has a positive and depth of outreach that is average loan size (AVGLS) has a negative impact on lending rate.

Table 9. Region-wise impact of financial and social performance on lending interest rate with the interaction of size and age

However, breadth of outreach as measured by the number of credit clients (CC) has a positive impact on lending interest rate. While, except Middle East, age shows an insignificant impact on lending rate. Overall, the results indicate that size has positive impact and age has an insignificant impact on the lending rate.

However, the result of the interaction terms show that as productivity and size increases, it negatively influence interest rate, but when productivity and age together increase, it has no significant influence on lending rate.

Likewise, productivity, size, and age as an interaction term have no impact on the interest rate. After incorporating size interaction with funding cost (IF), the results show significant impact in the case of overall world and all regions except Eastern Europe.

4.4.3. Results of model 3

The results of model 3 are presented in Table . The results show different factors having an impact on the productivity of MFIs. The results reveal a negative relation between the lending interest rate and productivity. Therefore, by increasing productivity, the lending interest rate can be reduced.

Table 10. Determinants of Productivity in MFIs

The results regarding age and size of the MFIs matter in most of the regions and the overall world and are consistent with the findings of Gonzalez (Citation2008) who state that MFI is more productive in first six years of its age in which efficiency of MFI increases from 2% to 8% annually. This supports my finding that in early years of operations, MFIs build a strong cliental base which in the future results in greater productivity. The variable competition also shows a significant positive result in all cases except for Eastern Europe and Latin America. This supports my finding that as competition increases, it puts more pressure on MFIs and tend to increase their productivity.

With regard to biodiversity index that internment the disparity of any country or region in terms of height and climate. The values of the index can range from 0 (no biodiversity) to 100 (highest level of biodiversity). A higher value of biodiversity shows more variability and thus increasing cost and lowering productivity of MFIs. For biodiversity, my results show a significant inverse relation in most of the regions except East Asia and South Africa. The results support the findings of Cotler (Citation2010) that an increase in biodiversity leads to low productivity and increases operating cost, which in return give rise to the lending interest rate.

The HDI is a measure that ranks countries on the basis of human development. It has four levels ranging from “very high, “high, “medium”, and “low human development countries. This Index relatively measures the level of education, literacy, standards of living, and life expectancy of habitants in countries worldwide. In my analysis, contrary to expectations, the results show a significant inverse relation between HDI and productivity.

For measuring the impact of economies of scale, another explanatory variable population density has been introduced. This index shows the relation between a population and the area in which it lives. According to Kai (Citation2009), the higher value of this index shows more population concentration. The value can range from 0 (the population would be equally scattered all over county or region) to 100 (all population would be concentrated in one area of the country or region).

Considering the effect of economies of scale, a higher value of index may lead to reducing the operational costs, thus increasing productivity. The results show a significant positive trend in the case of East Asia and Eastern Europe, but not in the case of all world, and thus supports the findings of Fernando (Citation2006) that poor physical infrastructure and transportation facilities in many areas in which microlenders operate are not up to the mark, thus increasing the operating costs and reducing the productivity of MFIs.

To see the joint impact of interactions between population density and HDI, the results mostly show a positive but insignificant impact on productivity. With regard to the joint impact of population density and BDI, results are highly significant and positive. Supporting the fact that high cost associated with the high value of BDI is offset with the higher value of population density. These findings are in line with the findings of Cotler (Citation2010).

The strength of legal right (SLRI) is an important explanatory variable. This index is about the rights of borrowers and lenders and measures the degree to which collateral and bankruptcy laws facilitate and safeguard lending. The value of index ranges from 0 to 10, with a higher value representing that laws are well intended to enhance credit access. My result shows that SLRI has a significant positive impact on productivity in Middle East Latin America and the overall world and consistent with the results of Gonzalez (Citation2007).

The last important control variable is depth of information index that measures rules regarding the quality, accessibility, and scope of credit information which are accessible from public or private credit agencies and bureaus. The index’s values move from 0 to 6. A greater value shows more availability of credit information. The results are positive and significant in the case of Eastern Europe and all world and consistent with the results of Gonzalez (Citation2007).

5. Conclusion

The present paper sheds light on the impact of financial and social performance of MFIs on lending interest rate across 70 countries belonging to six different regions of the world individually and collectively. The random-effects technique is applied on the basis of Hausman test.

The findings of the paper clearly illustrate that funding interest rate (IF) and proxies of financial performance (ROA, ROE, and OSS) have a significant positive impact on the lending interest rate. These findings verify that if MFIs get expensive funds, they will also charge high interest rates on their lending activities. When the motive is to increase financial performance, MFIs deliberately charge high interest rates to become more sustainable. These results are in line with the findings of Cotler (Citation2010) and Rosemberg et al. (Citation2009).

The social performance indicator breadth of outreach, measured by the number of credit clients (women and men borrowers) served, the results show a significant positive impact on the lending interest rate, supporting the fact as there are more customers, the interest rate charged by MFIs will be high to meet the demand of other borrowers. Contrary to breadth dimension, depth of outreach has a negative impact on the lending interest rate, indicating that as MFIs are catering less poor clients by giving the small amount of loans, they charge a high rate of interest to cover the service cost associated with the loan.

In control variables, age has an insignificant impact, whereas size has a strong positive impact on the lending rate, and these results are in line with the findings of Campion et al. (Citation2010). The results also indicate that the productivity of the MFI is influenced by its funding cost. The countries ranking in terms of strength of legal rights, depth of information, human development and population density matters in financial performance, and outreach of MFI in a particular region. These indexes also have a significant impact on the productivity of MFIs.

Overall, the finding suggests that MFIs should have a tradeoff between their financial performance and social objectives. By achieving operational sustainability, they can cut down their lending interest rate and fulfill their social mission of reducing poverty . There is no difference between MFIs and conventional banks, If they ignore their social mission and just focus on their financial performance.

5.1. Policy implications

Overall, the paper has identified various challenges that MFIs face in maintaining their financial and social performance, which subsequently affect their lending interest rate determination. So various policy implications are drawn from the outcomes of this paper.

5.1.1. For microfinance institutions

MFIs can increase their performance by lowering their operational and administrative cost, and this can be achieved by reducing the delinquency rates and transaction cost. Staff productivity should also be increased by giving them incentives. And there should be an optimal number of clients per staff member.

In order to fulfill their social mission of reducing poverty, MFIs should cater more rural areas; once they become operationally efficient, they have to design special arrangements for remote areas where previously they are not operating.

MFIs must aware their clients about the total cost associated with their loans such as the cost of loan, inflation, and other administrative costs so that they are able to understand the logic of high rates. Also, maintaining proper documentation of all loans can help MFIs in reducing default rates and enhancing operational efficiency.

As it clears from the finding of the paper that high rates of interest are mainly due to high operating cost, so there should be an implementation of new technology such as telecommunication networks, and branch less banking in order to reduce the cost.

5.1.2. For policymakers

The government must facilitate MFIs through the establishment of credit agencies and bureaus, which could help MFIs in assessing the level of indebtedness and credit risk. With such facilities, MFIs can better set interest rates and enhance their lending operations.

5.2. Limitations and recommendations for future research

The present paper has covered a sample size of 382 MFIs throughout the world during the period of 2006–2012. The future research can be carried out on a more comprehensive sample in terms of countries, MFIs, and time span.

The present paper has covered just five-star MFIs, although these represent MFIs, having audited financial statements and a rating from third party. For future research, by considering other classes of MFIs, more generalized results can be inferred.

Some factors like technological advancement as telecommunication networks, electricity, infrastructures, and ATMs are not incorporated in this paper. The future research can be conducted by incorporating such factors as well.

5.3. Robustness

All the models are re-estimated using GMM panel estimation technique. As therefore, most of the results remain the same under GMM estimation, these are not presented in the paper.Footnote1

Additional information

Funding

Notes on contributors

Afsheen Abrar

Afsheen Abrar obtained MBA degree from the Quaid-e-Azam University Islamabad and MS-Finance degree from Shaheed Zulfikar Ali Bhutto Institution of Science and Technology, Islamabad, Pakistan. At present, she is pursuing her PhD from the University of Twente, the Netherlands. Her broad research area is financial markets and institutions. Currently, she is on study leave from National University of Modern Languages, Islamabad, where she is working as an assistant professor. She has also attended various professional and research training sessions at domestic and international level.

Notes

1. The results of GMM estimations are not reported but available from the author upon request. As the model includes endogenous variables, it can be possible that causality run from these regressors (ROA, AVGLS, and IF) to lending interest rate and vice versa. In this case, our regressors may also correlate with the error term. Another issue can be that time-invariant country-fixed effects may also related to the error term. Therefore, in order to deal with endogeneity issue and to eliminate the unobservable country-fixed effects, this study also employed GMM method. This method uses the lag value of regressors as instruments to deal with endogeneity problem. Through transforming the regressors by first differencing, the country-specific unobservable effects are removed. Tests of Hansen/Sargan are estimated to test the model specification validity. This test examines the lack of correlation between the instruments and the error term. And the p-value turn out greater than 0.05; therefore, the null cannot be rejected that the instruments as a group are exogenous. And also the results are consistent with random-effects method.

References

- Adongo, J., & Stork, C. (2005). Factors Influencing the Financial Sustainability of Selected Microfinance Institutions in Namibia NEPRU Research Report No.39. The Namibian Economic Policy Research Unit, Olympia, Windhoek, Namibia.

- Ashta, A. (2009). Creating a world without poverty: Social business and the future of capitalism. Journal of Economic Issues, 43(2), 289–290.

- Ashta, A. (2010). Interest rates ethics: An aspect of social performance in microfinance. Retrieved from http://www.findevgateway.org/sites/default/files/mfg-en-paper-interest-rate-ethics-an-aspect-of-social-performance-in-microfinance-nov

- Beck, T., Demirguc-Kunt, A., & Levine, R. (2007). Finance inequality and the poor. Journal of Economic Growth, 12(1), 27–49. doi:10.1007/s10887-007-9010-6

- Boot, A. W. A, & Thakor, A. V. (2000). Can Relationship Banking Survive Competition? Journal Of Finance, 55(2), 679–713.

- Brand, M. (2003). Market intelligence: making market research work for microfinance. Accion’s inSight Series, No. 7.

- Campion, A., Ekka, R., & Wenner, M. (2010). Interest Rates and Implications for Microfinance in Latin America and the Caribbean” Inter-American Development Bank working paper series-177.

- CGAP. (2009). Are microcredit interest rates excessive? Consultative group to assist the poor brief.

- Copestake, J. (2007). Mainstreaming microfinance: Social performance management or mission drift? World Development, 35(10), 1721–1738. doi:10.1016/j.worlddev.2007.06.004

- Cotler, P. (2010). What drives lending interest rates in the microfinance sector? Microfinance Workshop University of Groningen, The Netherlands.

- Cull, R., Demirguc-Kunt, A., & Morduch, J. (2007). Financial performance and outreach: A global analysis of leading microbanks. The Economic Journal, 517(2), 107–133. doi:10.1111/j.1468-0297.2007.02017.x

- Cull, R., Demirguc-Kunt, A., & Morduch, J. (2008). Microfinance meets the market. Journal of Economic Perspectives, 23(1Winter), 167–192. doi:10.1257/jep.23.1.167

- Mix Market: The Microfinance Information Echange (MIX): Available at http://www.mixmarket.org/en.

- Fernando, N. A. (2006). Understanding and dealing with high interest rates on microcredit. East Asia Department, Asian Development Bank, Philippines.

- Gonzalez, A. (2007). Resilience of microfinance institutions to national macroeconomic events: An econometric analysis of MFI asset quality. MIX Discussion Paper No. 1.

- Gonzalez, A. (2008). Efficiency drivers of microfinance institutions (MFIs): The case of operating expenses. MIX Discussion Paper No. 2. Washington, D.C.

- Gonzalez, A. (2010). Analyzing microcredit interest rates. Mix data brief No.4. Retervied from www.themix.org.

- Gutiérrez-Nieto, B., Serrano-Cinca, C., & Mar Molinero, C. (2009). Social efficiency in microfinance institutions. The Journal of the Operational Research Society, 60(1), 104–119. doi:10.1057/palgrave.jors.2602527

- Hartarska, V. (2005). Governance and performance of microfinance institutions in Central and Eastern Europe and the newly independent states. World Development, 33(10), 1627–1643. doi:10.1016/j.worlddev.2005.06.001

- Hartarska, V., & Denis, N. (2007). Do regulated microfinance institutions achieve better sustainability and outreach? Crosscountry Evidence, 39(12), 1207–1222.

- Hartarska, V., & Denis, N. (2008). An impact analysis of microfinance in Bosnia and Herzegovina, World Development 36(12), 2605–2619.

- Hartarska, V., Gropper, D., & Caudill, S. (2009). Which microfinance institutions are becoming more cost-effective with time? Evidence from a mixture model. Journal of Money, Credit, and Banking, 41(4), 651–672. doi:10.1111/j.1538-4616.2009.00226.x

- Helmes, B., & Reille, X. (2004). Interest rate ceilings and microfinance: The story so far. CGAP Occasional Paper No.9.

- Hermes, N., Lensink, R., & Meesters, A. J. (2009). Outreach and efficiency of microfinance institutions. World Development, 39(6), 938–948. doi:10.1016/j.worlddev.2009.10.018

- Hudon, M., & Traca, D. (2008). On the efficiency effects of subsidies in microfinance: An empirical inquiry. Working Paper CEB 06020. Solvay Business School, Brussels, Belgium.

- Kai, H. (2009). Competition and wide outreach of microfinance institutions. Munich Personal RePEc Archive 17143.

- Ledgerwood, J. (1997). Sustainable banking with the poor microfinance handbook: An institutional and financial perspective. Washington, D.C: The World Bank.

- Lewis, J. (2008). Microloan Sharks. Stanford Social Innovation Review, Summer 2008.

- Marquez, R. (2002). Competition adverse selection, and information dispersion in the banking industry. The Review of Financial Studies, 15, 901–926. doi:10.1093/rfs/15.3.901

- McIntosh, C., & Wydick, B. (2005). Competition and microfinance. Journal of Development Economics, 78, 271–298. doi:10.1016/j.jdeveco.2004.11.008

- Nawaz, A. (2010). Performance of microfinance: The impact of subsidies. CEB Working paper series. Universite Libre de Bruxelles, Solvay Brussels School of Economics and Management, Centre Emile Bernheim.

- Olivares-Polanco, F. (2005). Commercializing microfinance and deepening outreach? Empirical evidence from Latin America. Journal of Microfinance, 7, 47–69.

- Petersen, M. A, & Rajan, R. G. (1995). The effect of credit market competition on lending relationships. The Quarterly Journal Of Economics, 110(2), 407–443.

- Pollinger, J. J., Outhwaite, J., & Guzmán, H. C. (2007). The question of sustainability for microfinance institutions. Journal of Small Business Management., 45(1), 23–41. doi:10.1111/jsbm.2007.45.issue-1

- Robinson, M. (2001). The microfinance revolution: Sustainable finance for the poor. Washington, DC: World Bank. Retervied from https://openknowledge.worldbank.org/handle/10986/28956

- Rosemberg, R., Gonzalez, A., & Narain, S. (2009). The new moneylenders: Are the poor being exploited by high microcredit interest rates? CGAP Occasional paper 15, Washington, D.C.

- Roy, M., & Strom, R. O. (2010). Microfinance mission drift. World Development, 38(1), 28–36. doi:10.1016/j.worlddev.2009.05.006

- Vermeersch, A. (1912). Usury catholic encyclopedia. Robert Appleton company. Retrieved from: http://www.newadvent.org/cathen/15235c.html.

- Vinelli, A. (2002). Financial sustainability in U.S. microfinance organizations: Lessons from developing countries. In J. H. Carr & Z. Y. Tong (Eds.), Replicating microfinance in the United States, Washington, D.C. Woodrow Wilson Center Press.

- World Bank. (2008). Finance for all? Policies and pitfalls in expanding access. A World Bank policy research report. Washington, D. C.

- Yunus, M. (2007). Creating a world without poverty: social business and the future of capitalism. Global Urban Development, 4(2), 1–19.

Appendix

Appendix 1. MFIs on the basis of countries