?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to obtain empirical evidence whether the criteria of forming an audit opinion have been significantly effecting audit opinion of municipal government financial statements in Indonesia. The considerations for expressing audit opinion are the deficiency in the internal control system (ICS), the non-compliance with regulations and laws, and the non-conformance with the Government Accounting Standards (GAS). The deficiency in internal control is analyzed by the number of findings on three categories, namely the number of weaknesses in the internal control structure, deficiency in the controlling system of revenue and expenditure budget realization, and the weakness in the accounting and reporting controlling system. The non-compliance with legislation is measured by the number of administrative findings and the ratio between the value of findings to the total value of expenditures of either the findings of regional losses, the potential regional losses, and the revenue shortfall. The non-conformances with the government accounting standard is represented by the number of accounts that were not presented in accordance with the GAS. The study is conducted on 182 municipal government financial statements for 2016 and 2015 financial years with the result of both the non-compliance with the regulations that result in regional losses and the non-conformance with the GAS have a negative effect on audit opinion, whereas the other criteria of forming audit opinion show no effect on audit opinions.

PUBLIC INTEREST STATEMENT

The audited government financial report is the embodiment of accountability and transparency of the public finance implementations. Governments’ financial reports in Indonesia are audited by the BPK annually to obtain independent opinions with the intention of providing reasonable assurance for the community that the financial statements are relevant, accurate, complete, and presented fairly. The opinions expressed from the audit of financial statements consist of disclaimer, adverse, qualified, and unqualified opinion. The criteria for forming an audit opinion for Indonesian’s government institutions are the compliance with the government accounting standard, adequate disclosures, compliance with laws and regulations, and the effectiveness of internal control systems. Using the samples of the municipal governments, our research finds that the non-compliance with the government accounting standard and the non-compliance with the statutory in the form of regional financial losses has a significant influence on the audit opinions obtained by the municipal governments.

1. Introduction

Under the Indonesian’s State Financial Act (Citation2003), the Regional Governments in Indonesia are required to present financial statement and submit it to the Regional House of Representatives subjected to audit by the Indonesian’s Supreme Audit Board (BPK). The audit report of the government financial statement generally results in three parts comprising an audit report on the financial statement and two optional reports namely the compliance with statutory and the evaluation of internal control systems. Within two years (2015–2016), BPK has conducted an audit of 1079 local government financial statements.

Table shows an accretion in the number of Local Governments’ Financial Statements obtained an unqualified opinion from 2015 to 2016. The Audit of State Financial Governance Act (Citation2004a) in the elucidation of Article 16 Paragraph 1 explaining the criteria for formulating an opinion are compliance with the government accounting standard, adequate disclosures, compliance with laws and regulations, and effectiveness of internal control systems. The development of the BPK’s opinions on government financial statements has been widely studied by several researchers. However, the results of research related to the criteria of giving opinion to audit opinion were inconsistent.

Table 1. The development of audit opinion and audit findings on local governments in Indonesian during the 2015 and 2016 financial years

Several studies have been conducted to determine the relationship between internal control weakness findings and audit opinions. For example, Safitri and Darsono (Citation2015) research of local governments on Java Island to identify the effect of the internal control system on audit opinion on financial statements. The results of the study stated that the weaknesses of the internal control system did not significantly influence the opinions given. Her result is contrary to the results of Setiawan’s (Citation2017) research which states that the weakness of internal control system influences audit opinion with the direction of a negative relationship.

Other researches also performed to identify the influence of the non-compliance to the regulation on audit opinion. Setiawan (Citation2017) conducted a study to determine the effect of compliance with laws and regulations on audit opinions on Indonesian’s local governments. The results of the study indicate that compliance with statutory has no effect on audit opinion. This finding is contradictory with the results of Prasetyaningsih, Yuhalifiyah, and Susanto (Citation2014) who state that non-compliance with laws and regulations has a significant effect on audit opinion.

BPK (Citation2016) has elaborated the internal control system (ICS) findings into three types namely deficiency in accounting and reporting control system (ARCS), weakness of control system of the revenue and expenditure budget realization (CSREBR), and weakness of internal control structure (Structure of IC). The findings of non-compliance are divided into four types namely, regional losses (RL), the potency of regional losses (PRL), revenue shortfall (RS), and administration finding (ADM). The effect of each item on the findings of ICS deficiencies and non-compliance above has not been broadly studied in the academic research field. Though, it is critical to be analyzed as the local governments need to be aware of the details of the findings that potentially have the most significant impact on decreasing their audit opinions.

Although several researchers have conducted research on the influence of internal control and non-compliance findings on opinion with the proxies of the value of the findings such as Maabuat et al. (Citation2016) or both the value and the number of findings by Atmajaya and Probohudono (Citation2015) and Fatimah, Ria, and Rasuli (Citation2014), they had not considered the materiality of the findings compared to the value of the expenditure accounts. The results of those three studies are also disparate depending on the consideration of which type of internal control and non-compliance findings are influential to the opinion. Therefore, our study will try to provide more detailed empirical evidence related to ICS and compliance findings which has a significant influence on audit opinion.

An unqualified opinion is provided if the financial statements present fairly in all material respects according to the GAS (BPK, Citation2014). From the definition, it is seen that the critical factor in giving an audit opinion is the conformity with GAS. Research related to the relationship between the reliability of the internal control system in improving the quality of financial statements, as conducted by Trisnani, Dimyati, and Paramu (Citation2018) and Sari and Witono (Citation2014), find that the reliability of ICS has a significant effect on the quality of financial statements as measured by the degree of conformity with GAS. Suparwan, Sujana, and Yuniarta (Citation2018) performed a study to determine the effect of the fair presentation of financial statements on the quality of financial accountability. The result shows that the conformity of the financial report with the GAP has a positive and significant effect on the quality of financial accountability.

Local governments in Indonesia consist of two levels, namely the provincial government at the first tier and the district or municipal government in the second tier. This study uses the municipal governments as the samples which are intended to meet the similarities of local government characteristics. Municipal governments have more in common in their economic activities where in general their regional income is derived from the service and industrial activities of their communities, compared to districts where their economic activities are influenced by the specialization of their natural resources. In addition, the municipal governments have obtained more unqualified opinions in the 2016 financial statements of 77%, compared to 66% of district governments. Although in general, the Indonesian’s local governments that have obtained unqualified opinions have been increased in recent years, nevertheless there are still some deteriorations of audit opinion in several regions which cannot be neglected. Through this research, the municipal governments are expected to develop appropriate strategies to improve or maintain the audit opinions they have obtained. The local government can focus on the improvements in one of the criteria or sub-criteria that are significant in obtaining an unqualified opinion.

Based on the above explanations, this study aims to provide an appropriate model on the relationship between criteria for forming an audit opinion against the issued audit opinion itself. The research questions would like to be answered on this research are whether (i) the internal control system, (ii) the non-compliance with regulations, and (iii) the non-conformity with GAS have an effect on the audit opinion of Indonesian’s Municipal Governments Financial Statements.

2. Theoretical background

External audits are part of a corporate governance structure that serves as monitoring tools by providing independent checks on financial statements prepared by company management, with the intention of enhancing the company’s reputation (Habib, Citation2013). Generally, the objective of the financial audit is to enable the auditor to express an opinion on the conformity of the financial statements, in all material aspects, with prevailing accounting standards (Ånerud, Citation2007).

Audits of public sector’s financial reports generally have broader objectives than in the private sector, such as the obligation to report compliance with regulations, including budget and accountability, and examination on the effectiveness of internal controls (Ånerud, Citation2007). Although the audit objectives in the public sector broadly vary, nevertheless the general purpose is to facilitate accountability functions both explicitly and implicitly between those who hold operational responsibility for those in a supervisory role (McCandless, Citation1993).

The role of the audit in government tends to follow changes in demands on the public sector which are determined by regulatory changes that allow the audit role adjusted to adapt to changes in public management (Pearson, Citation2014). As public attention increases on the credibility of auditors in the private sector, whom also occasionally provide advisory services to their audit clients, the concern has also been raised to government auditors regarding their independence in maintaining credibility and legitimacy (Gendron, Cooper, & Townley, Citation2001). Although Supreme Audit Institution activities are traditionally limited to legal and financial examinations, in the development, they are required to monitor all aspects of state services and report it to the government and to the public objectively by providing information highlighting both good governance and inefficiency of administrative structures if exist (Gonzales et al., Citation2011).

Hay and Cordery (Citation2018) argue that public sector audits function more as agency theory and management control rather than signaling, insurance, governance, and confirmation explanations theories. Citizens, as the principal, demand accountability to the management they placed on public sector entities, as the agents. Hence, the audit serves as monitoring techniques that evaluate and report the management’s financial assertions of the entity and examine the accounting instrument underlying the assertions (Sinason, Citation2000). Furthermore, audits by the supreme audit institution have also being promoted as a tool for combating corruptions and frauds on governmental institutions and public sectors. Dye (Citation2007) explains that corruptions and frauds emerge due to the absence of accountability and transparency; thus, an audit provides the required assurance on the financial economic condition of the audited entities.

2.1. Local government financial statements

Indonesian’s State Financial Act Number (Citation2003) requires local governments to present financial statements as an accountability for the realization of the Regional Budgetary of Revenue and Expenditure. The presentation of the financial statement is the manifestation of accountability and transparency of the local financial governance, including the report on the achievement of the budget realization. In order to comply with the statutory, the central government issued Government Regulation (Citation2005) regarding GAS. The GAS established the Cash Towards Accrual (CTA) accounting basis as a reference during the transition from the cash basis to the full accruals basis. Within the CTA, revenues, expenditures, and financing were recorded on a cash-basis while assets, debt, and equity were recorded on an accrual basis.

Initially, the accrual accounting basis was planned to be fully implemented no less than five years after the issuance of the State Financial Act (Citation2003). However, in 2010, the government has not been ready for the implementation. Hence, the Government Regulation Number 71 (Citation2010) regarding GAS was issued to supersede the prior GAS. The new GAS stated the overall governments of Indonesia shall commit the implementation of the full accrual basis by the 2015 financial year. During those transition periods, the governments remained to use the CTA basis. Eventually, by 2015, the overall Indonesian’s governments, both the central and local, officially adopted the full accrual accounting basis. The accrual-base government financial statement legitimately consists of the Budget Realization Report, Statement of Changes in Budget Balance, Balance Sheet, Operational Statement, Cash Flow Statement, Statement of Changes in Net Asset/Equity, and Financial Statements Notes.

2.2. Audit opinion

An auditor’s opinion prefaced on the financial statement is an auditor’s attestation, through examinations and verification of financial documents, management discretions, internal control system, and other audit procedures, over the fairness and fairly presented financial statement produced by the management (Brook, Citation2001). Hence, the detection of company’s frauds and errors are not the primary goal of an audit (Wisdom & Oyebisi, Citation2017).

An Audit opinion influence investors’ confidence as it provides affirmation of the validity of the financial statements (Tahinakis & Samarinas, Citation2016) and also plays a role to influence financial governance by purifying management assertion of company’s financial condition (Skaerbaek, Citation2009). In general, there are two alternative forms of audit opinion, namely the standard unqualified audit opinion and the modified audit reports, which are the format of other opinions than the unqualified opinion, including the unqualified reports with explanatory paragraphs (Habib, Citation2013). The auditor’s opinion in the financial report should include an introductory paragraph stating management’s responsibility of the financial statements and an appropriate audit opinion of the entire financial statement based on the circumstances of the situation (Siegel & Akel, Citation1989).

The Indonesian’s governments’ financial statements are subject to audit by the BPK annually prior to the submission to the legislature no later than six months after the end of the financial year (GoI, Citation2003). The BPK has authorities to execute three types of audits namely the financial audit, performance audit, and special purpose audit (GoI, Citation2004b and BPK, Citation2014). Audit of the local government financial statements were administered in term of the financial audit with the intention to express an opinion regarding the fairness of the information presented in the financial statements. BPK is authorized to express four types of audit opinions namely, (i) unqualified opinion, (ii) qualified opinion, (iii) adverse opinion, and (iv) disclaimer of opinion. Based on BPK’s State Financial Auditing Standard (Citation2017a), the formulation of opinion is based on criteria of compliance with accounting standards, adequacy of disclosure, compliance with statutory regulations, and effectiveness of internal control system.

2.3. Internal control system

Internal control is a process run by boards of directors, management, and staff to provide reasonable assurance regarding operational effectiveness and efficiency, financial reporting reliability, and compliance with laws and regulations (COSO, Citation2013). The internal control system of financial reporting is a designated process to provide reasonable assurance regarding the reliability of financial statements and the presentation of financial reporting for external parties in accordance with generally accepted accounting principles (D’Aquila & Jill, Citation1998; Arens, Randal, & Beasley, Citation2008; and Mahaputra & Putra, Citation2014). Furthermore, COSO (Citation2013) explains that internal control consists of five interrelated components such as the control environment, risk assessment, control activities, information and communication, and monitoring.

Ge and McVay (Citation2005) argue that a weak internal control environment will encourage earnings management and opportunistic behavior, thus reducing the reliability of financial reporting. The State Treasury Act (Citation2004b) determines the head of regional apparatus unit as the authority of the local government budget and assets to provide an assertion that the realization of the budget and the utilization of inventories/assets have been managed based on adequate internal control and financial accounting has been conducted in accordance with the GAS. In undertaking an audit, the external auditor should obtain an understanding of the ICS by testing and evaluating the effectiveness of the design of internal control and by identifying company-level controls thus is able to provide opinions on the effectiveness of the financial reporting internal control system and report the material deficiencies of the internal control if any (Griggs, Citation2004; Dye, Citation2007).

To obtain adequate assurance in the fairness of the financial statements, BPK also conducts an audit on internal control and compliance with laws and regulations. BPK’s report (Citation2017b) defines the findings of deficiencies in ICS as a finding that contains problems of weaknesses of accounting and reporting control system, weakness of control system of revenue and expenditure budget realization, and weakness of internal control structure.

2.4. Compliance with legislation

Audits in the government sector have a fundamental purpose of monitoring, ensuring, and assessing government accountability. Liu and Lin (Citation2012) argue that by overseeing their implementation, especially how resource use is used, government audit can strengthen accountability and reduce abuse of authority and resources. Furthermore, they state that the most important function of government audits is to determine whether the process of aggregation and utilization of public funds and other relevant transactions is in conformity with government regulations and legislation. Schelker and Eichenberger (Citation2010) and Blume and Voigt (Citation2011) also express that government audits can improve the transparency of public policy and reduce waste of government spending.

State Financial Auditing Standard (Citation2017a) express that BPK’s audit encourages good governance of the state finances to achieve national goals, one of which is through improving the compliance of state financial governance and accountability to legislation. As explained earlier, to obtain adequate confidence in the fairness of the financial statements, BPK also conducts examination on the internal control system and the compliance with statutory related to government financial reporting. BPK (Citation2014) indicates that the findings of non-compliance with statutory regulations include (i) a non-compliance causing regional/state losses, (ii) the potency of regional/state losses, (iii) revenue shortfall, (iv) administration findings, (v) inefficiency, and (vi) ineffectiveness.

BPK (Citation2017b) explains the audit findings of the state/regional losses, potency of state/regional losses, or revenue shortfall are matters with an impact on financial and most likely to be reported to the law enforcement if there is any fraud or violation of the law, while the administrative findings do not necessarily have an impact on government finance. The compliance audit report within the financial statements audit framework is an optional report which means that it is issued if a non-compliance occurred during the financial audit process.

2.5. Conformity with Government Accounting Standards

BPK (Citation2014) describes the criteria underlie the decision for each type of audit opinion as follow: (i) unqualified opinion is given if the financial statements present fairly in all material respects in accordance with the GAS; (ii) qualified opinion is granted if the financial statements present fairly in all material respects in accordance with GAS, with an exception on the impact of matters regarding the exclusions; (iii) adverse is expressed if the financial statements do not present fairly in all material respects in accordance with the GAS; (iv) disclaimer means the auditor does not express an opinion on the financial statements. By that description, it can be understood that the main criterion that determines the audit opinion by the BPK is the conformity with the GAS. Furthermore, the State Finance Act (Citation2003) requires the structure and content of the state/regional revenue and expenditure budget execution report arranged and presented in accordance with the GAS.

3. Development of hypotheses

3.1. Internal control system

Numerous Researchers have studied the relationship between the Internal Control System and Audit Opinion. However, the consistency on the results of their studies is still questionable. Safitri and Darsono (Citation2015) conducted research to identify the influence of the internal control system on audit opinion using samples of 354 local governments’ financial report on Java Island, from 2010 until 2012. The weakness of the internal control system is measured by the number of internal control system’s findings. Their result indicates that the weakness of internal control system does not significantly influence the BPK’s audit opinion on Local Governments’ Financial Statements. In contrast to the result, Setiawan (Citation2017) also conducted a similar study with samples of local government financial statements in South Sulawesi also using the number of internal control system findings as a proxy. He came up with the result that the weakness of internal control system influences audit opinion with a negative relationship, which indicates that the greater the internal control system findings, the smaller the probability of local governments to get an unqualified opinion. His results are in line with other research findings conducted by Munawar et al. (Citation2016), Fatimah et al. (Citation2014), Setyaningrum (Citation2015), Winanti (Citation2014), Atmajaya and Probohudono (Citation2015), Sari et al. (Citation2015) and Taufikurrahman (Citation2014). Based on the inconsistency of the results of previous studies, further profound research on internal control findings which influence the opinion of the financial statements is required.

Ge and McVay (Citation2005) conducted a study related to the disclosure of material weaknesses over internal controls following the publication of the Sarbanes-Oxley Act. The material deficiencies of these internal controls were included weaknesses in revenue recognition policies, lack of tasks and authority distribution, weaknesses in the accounting policies and reporting process at the end of the period, and inadequate account reconciliation. Their research identifies that the accounts that are most likely affected by those weaknesses are the current accrual accounts such as accounts receivable and inventory. Furthermore, Atmajaya and Probohudono (Citation2015) have also conducted a study of the effects of internal control system deficiencies in audit opinion by dividing it into three types of internal control system deficiencies. They came up with the results that the aspects which have a significant influence on opinion are the weaknesses of accounting and reporting control system and the weakness of controlling system on budget expenditure realization. Meanwhile, the deficiency in the internal control structure does not affect the audit opinion.

The Guidelines for Reviewing Local Government Financial Statements (MoHA, Citation2008) state that one of the objectives of the internal control system is to achieve the reliability of financial statements. Therefore, the Regional Government should design and implement an appropriate internal control to improve the reliability of financial information. By the basis of that description, this research develops hypotheses as follows:

H1: The deficiencies in the ICS negatively affect the opinion of municipal governments’ financial statements

H1a: The deficiency in the structure of internal control negatively affects the audit opinion of municipal governments’ financial statements

H1b: The deficiency in the control system on revenue and expenditure budget realization has a negative effect on the audit opinion of municipal governments’ financial statements

H1c: The deficiency in accounting and reporting control system negatively affects the audit opinion of municipal governments’ financial statements

3.2. Compliance with regulations

Similar to research on internal control systems, studies on the relationship between compliance with regulations and audit opinions have also been conducted by some researchers, yet there are still disputes regarding the results. Setiawan’s (Citation2017) study indicates that compliance with laws and regulations does not affect the opinion of the Indonesian regional government financial statements. On the contrary, an earlier research by Prasetyaningsih et al. (Citation2014) using 371 local governments in Indonesia in 2012 financial year shows that the findings of non-compliance with laws and regulations have a significant influence on audit opinion. The existence of such a relationship is also expressed by Carslaw, Mason, and Mills (Citation2007), Sipahutar and Khairani (Citation2013), Safitri and Darsono (Citation2015), Fatimah et al. (Citation2014), Ge and McVay (Citation2005), Munawar and Abdullah (Citation2016), and Atmajaya and Probohudono (Citation2015). Furthermore, Sipahutar and Dan Khairani (Citation2013) analyzed the changes of BPK’s opinion on the Empat Lawang Regency Financial Report. The result shows that both the level of non-compliance with the statutory and the conformity with GAS affects the auditor opinion. Nevertheless, all of those prior studies are arguably used variables of compliance to legislation solely by the number and/or value of the findings without considering the materiality of the findings.

Moreover, since the government audit agency in China are tasked with detecting deficiencies that occur in government financial statements and are authorized to impose administrative sanctions and penalties to responsible institutions/individuals, Liu and Lin (Citation2012) conducted a study to determine the role of government audits on corruption control in China. The results revealed that the escalation of audit findings on regulatory violations by the local governments in China was positively associated with an increase in corruption, thus resulting in a lower quality of financial statements.

Based on the review on the inconsistency results of previous research above and the consideration to include the materiality of the findings, this study will try to add depth on this field of study by examining which types of non-compliance findings significantly affect the audit opinion of the municipal government’s financial statements in Indonesia. The variable of non-compliance on regulations in this study will consider materiality by using the ratio of the findings’ value to the total expenditure of the accounts as the proxies. Hence, the development of the research hypotheses for non-compliance with statutory as follows:

H2: Non-compliance with laws and regulations negatively affects the audit opinion of municipal governments’ financial statements

H2a: The findings of regional losses negatively affect the audit opinion of municipal governments’ financial statements

H2b: The findings of potential regional losses negatively affect the audit opinion of municipal governments’ financial statements

H2c: The findings of revenue shortfall have a negative effect on the audit opinion of municipal governments’ financial statements

H2d: Administrative findings have a negative effect on the audit opinion of municipal governments’ financial statements

3.3. Conformity with GAS

The relationship between conformity with GAS and financial statement opinion has been expressed by BPK (Citation2017b) which revealed that the 162 local governments’ financial statements that have not yet received unqualified opinion by 2017 generally because there were several accounts that do not present in accordance with the GAS, particularly on current assets, fixed assets, and operating expenditures accounts. Research conducted by Sipahutar and Dan Khairani (Citation2013) shows that the conformity of the entities financial statements with the GAS affects the auditor’s opinion on financial statements. Furthermore, Mahaputra and Putra (Citation2014) analyzed the factors affecting the quality of local government financial reporting information with a result that GAS implementation has a positive effect on the quality of financial information. Those results are also in line with research conducted by Nugraheni and Subaweh (Citation2008). Based on the descriptions, we will also include the conformity with GAS in this research. Thus the research hypothesis is developed as follows:

H3: Non-compliance with government accounting standards negatively affects the audit opinion of municipal governments’ financial statements

4. Research methodology

This research is a quantitative research using descriptive and inferential statistical analysis. The inferential analysis is performed using ordinal logistic regression in SPSS software. Logistic regression is a regression method used to find relationships between dependent variables that have a nominal scale with independent variables that with a mix of ratio and ordinal scale, while the ordinal logistic regression is used if the dependent variables are ordinal scale (Ghozali, Citation2011).

The object of the study is the municipal government’s financial statements audited by the BPK. The sampling technique uses purposive sampling, which means that the population that will be used as a sample of this study must meet the criteria based on the considerations in accordance with the research purpose. Sample selection criteria are:

1. The Municipal Governments present the financial statements audited by the BPK in both the 2015–2016 fiscal year; and

2. The Municipal Governments with audit opinion data and audit findings for the fiscal year 2015–2016 available.

This research uses secondary data obtained from BPK’s Summary of Audit Result Reports for First Semester of 2016 and 2017, and both the BPK’s Audit Reports and Municipal Governments’ Financial Statements of 2015 and 2016 financial years. The study conducted using the period 2015 and 2016 financial years by the consideration of the implementation of the full accrual basis of GAS in Indonesian Governments in 2015.

The dependent variable in this research is the audit opinion of the 2015 and 2016 municipal governments’ financial statements (Y) by classifying them into an ordinal scale. An ordinal scale is not only used to categorize data into groups but also by ranking the categories (Ghozali, Citation2011). The independent variables used in this study are developed from BPK’s State Financial Audit Standard (Citation2017a), namely the deficiency in the internal control system (X1); the non-compliance with laws and regulations (X2); and the non-conformance with the GAS (X3). Furthermore, those independent variables were generated based on the classification of BPK’s findings (2016), namely Deficiency in the Structure of Internal Control (IC), Deficiency in Control System of Revenue and Expenditure Budget Execution (CSREBE), Deficiency in Accounting and Reporting Control System (ARCS), Regional Losses (RL), Potency of Regional Losses (PRL), Revenue Shortfall (RS) Administration (ADM), and Non-conformity with the GAS.

The ICS weaknesses (X1) is translated into three variables with an indicator of the number of cases. Non-compliance with laws and regulations (X2) is represented by three variables, two with the indicators of the ratio between the value of findings and total expenditure and one variable with indicator number of cases. The conformity variable with the GAS (X3) is explained by the indicator of the number of accounts that do not congruent with the GAS. The audit opinion variable (Y) is constructed by establishing scores to the types of the audit opinion received by the municipal governments, namely: value 4 for entities receiving an unqualified opinion, 3 for qualified opinion, 2 for adverse opinions, and 1 for disclaimer of opinion.

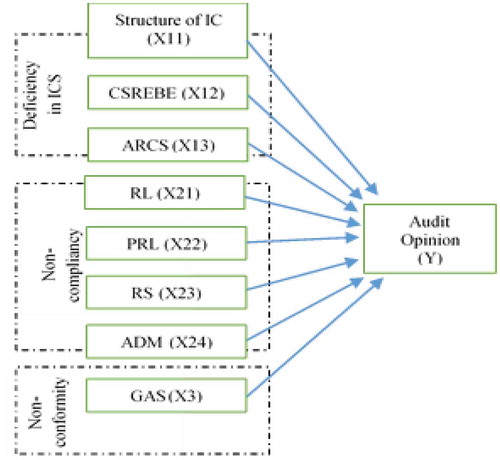

The quantitative test is developed with the following variables in the picture below (Figure ):

Figure 1. Conceptual research framework.

Description: Y = Audit Opinion, (X11) = Deficiency in the Structure of Internal Control (IC), CSREBE (X12) = Deficiency in Control System of Revenue and Expenditure Budget Execution, ARCS (X13) = Deficiency in Accounting and Reporting Control System, RL (X21) Regional Losses = PRL (X22) = Potential Regional Losses, RS (X23) = Revenue Shortfall, ADM (X24) = Administration, GAS (X3) = Non-conformance with Government Accounting Standards.The organization of research variables is on Table .

Table 2. Operational variables

5. Results and discussion

From 186 municipal governments financial statements 2015 and 2016, there were 4 samples excluded from the analyses due to the unavailability of the audit report data. Information obtained from BPK’s Report (2016) is that those municipalities were tardy in submitting financial statements in a timely manner in accordance with the statutory. Therefore, the total tested samples are 182. This study performs a descriptive statistical test and logistic regression to measure the relationship between the independent and the dependent variables.

The descriptive statistic in Table shows the number of 182 of the observed data with minimum, maximum, and average values of each variable to be tested. As for the dependent variable, the distribution of audit opinions of municipal government financial statements for the financial year 2015 and 2016 can be seen in the table.

Table 3. Case processing summary

5.1. Logistic regression analysis

Before running the hypothetical test, a classical assumption test is performed which includes the test of Model Fitting Information, Goodness of Fit, Pseudo R2, and Parallel Lines. A feasibility model test such as Model Fitting Information and Goodness of Fit test according to Ghozali (Citation2011) is used to determine the probability of whether the hypothesized model describes the input data.

Based on the model fitting information test on Table , it can be seen that when solely inputting the intercept model, the result of 2 Log Likelihood is 195.744. Then by incorporating the independent variable, 2 Log likelihood decreased to 111,738 and significant at p = 0.00. Thus, it can be concluded that this model provides better accuracy to predict BPK’s audit opinion.

Table 4. Model fitting information

The Goodness of Fit in Table shows the significance value of 1.00, which is greater than α = 5%. Therefore, it can be concluded that this model is sufficient to be used in research.

Table 5. Goodness of fit

5.2. Test of Parallel Lines

The purpose of this test is to assess whether the assumptions of all categories have the same parameters (Ghozali, Citation2011). The model is said to be appropriate if the p-value is greater than 0.05.

Based on Test of Parallel Lines result in Table , it can be seen that the p-value is 0.999, which greater than 0.05. Therefore, it can be concluded that the test model is appropriate.

Table 6. Test of Parallel Lines

5.3. Pseudo R2

Descriprive statistics in Table shows the minimum/maximum and mean values for each variable. Pseudo R2 test is used to determine the robustness of the regression equation in explaining the dependent variables.The Pseudo R2 test result in Table shows aresult of 0.561 of the highest Negelkerke value. This indicates the level of the independent variables ability in explaining the variance of BPK’s audit opinion is 56.1%, while the rest of 43.9% is explained by various indicators outside the model.

Table 8. Pseudo R2

Table 7. Descriptive statistic

5.4. Hypotheses testing

This study employed a parameter estimation method to analyze the hypotheses with the results in Table .

Table 9. Parameter estimates result

5.4.1. The effect of the internal control system weakness over audit opinions of municipal governments’ financial reports

As explained earlier, the weakness of the internal control system in this study is represented by three indicators: H1a, the weakness of internal control structure, H1b, the weakness of controlling system of budget expenditure execution, and H1c, the weakness of accounting and reporting system.

H1a test shows the value of β1 is −0.102 with a significance level of 0.469 (sig > 0.05). This indicates that the weaknesses of the internal control system represented by the internal control structure do not affect the opinions obtained by the municipal governments. This output is parallel to the research findings conducted by Maabuat et al. (Citation2016), Atmajaya and Probohudono (Citation2015), and Fatimah et al. (Citation2014).

H1b test generates β3 = −0.96 with 0.388 (sig > 0.05) of level of significance. This means that the weakness of the internal control system in the form of CSREBE does not affect the audit opinion obtained by the municipal governments. The results of this study are in line with research conducted by Fatimah et al. (Citation2014), but contrary to the studies of Maabuat et al. (Citation2016) and Atmajaya and Probohudono (Citation2015) where they indicate that the weaknesses of CSREBE and ARCS have a negative effect on audit opinion.

H1c test shows that the β3 is −0.005 with significance level of 0.968 (sig > 0.05). This indicates that the weakness of ARCS does not affect the audit opinion of the municipal government’s financial statements. The results of this study contradict the research of Maabuat et al. (Citation2016), Atmajaya and Probohudono (Citation2015), and Fatimah et al. (Citation2014) which argued that the weakness of ARCS negatively affected the audit opinion.

Based on the overall test results of the three forms of internal control system weaknesses above, it can be concluded that in general, the weakness of internal control system represented by the number of internal control system findings in the audit reports over municipal governments financial statements have no effect on the audit opinion. The results of this study are contrary to prior researchers such as Setiawan (Citation2017), Munawar and Abdullah (Citation2016), Agusti (Citation2014), Setyaningrum (Citation2015), Winanti (Citation2014), and Taufikurrahman (Citation2014) who stated that the weakness of the internal control system has negative effects on audit opinion. Nevertheless, the results of this study are in line with Safitri and Darsono (Citation2015) who argues that the internal control system has no effect on opinion and has a positive relationship toward audit opinion.

5.4.2. The effect of non-compliance with regulatory on the audit opinion of municipal government financial statements

As previously described, the non-compliance with the laws and regulations in this study is divided into four variables namely: H2a Regional Losses (RL), H2b Potency of Regional Losses (PRL), H2c Revenue Shortfall (RS), and H2d Administration (ADM).

H2a test shows the β4 = −5.217 with significance level 0.000 (sig < 0.05). This means that non-compliance with laws and regulations in the form of regional losses negatively affects the opinion obtained by the municipal governments. This result is parallel with researches conducted by Maabuat et al. (Citation2016), Atmajaya and Probohudono (Citation2015), and Fatimah et al. (Citation2014).

Test on H2b obtains the β5 value of 1.755 with a significance level of 0.493 (sig > 0.05). This indicates that the non-compliance with legislation represented by potential regional losses variable does not affect the audit opinion obtained by the municipal governments. This result corresponds with research of Maabuat et al. (Citation2016) and Fatimah et al. (Citation2014). Nevertheless, it is contradicting the research conducted by Atmajaya and Probohudono (Citation2015) which states that the findings of potential regional losses negatively affect an audit opinion.

H2c test result generates β6 = 1.883 with 0.472 of significance level (sig > 0.05). This means that non-compliance with regulations represented by revenue shortfall variable does not affect the municipal governments’ audit opinion. This result is in line with research conducted by Maabuat et al. (Citation2016), Atmajaya and Probohudono (Citation2015), and Fatimah et al. (Citation2014).

H2d test produces β7 = −0.070 with level of significance of 0.539 (sig > 0.05). This shows that the non-compliance with regulations in the form of administration findings does not affect the audit opinion of municipal financial statements. This result is similar to Maabuat et al.’s (Citation2016) findings. However, it is contradictory to Atmajaya and Probohudono (Citation2015) and Fatimah et al.’s (Citation2014) studies which indicate that the findings of non-compliance with the administration have a negative effect on audit opinion.

Based on the analyses of those four variables of the non-compliance with legislation, it can be deduced that the type of findings of non-compliance which affect the audit opinion is the finding related to regional losses, while the other three variables of non-compliance findings do not impact the audit opinion of the municipal government financial statements. However, the results of previous studies are still diverse, especially in determining the types of findings of non-compliance which affecting the audit opinion.

5.4.3. The effect of non-conformity with government accounting standards on the audit opinion of municipal government financial statements

H3 test result shows β8 is −1.450 with significance level of 0.000 (sig < 0.05). This means that the findings of non-conformity with GAS affect negatively to the audit opinion obtained by the municipal governments. This finding is parallel with research conducted by Nugraheni and Subaweh (Citation2008) and Mahaputra and Putra (Citation2014). The GAS sets out the accounting principles that should be applied in the preparation and presentation of the government financial statements; thus, the GAS serves as a requirement as well as a guideline enforced by regulations by means of improving the quality of government financial information in Indonesia (Mahaputra & Putra, Citation2014). Therefore, the discrepancy with the GAP shall have a significant influence on the audit opinion of a government financial statement.

6. Conclusion and recommendation

6.1. Conclusion

This research is expected to obtain an empirical evidence of the relationship between the criteria for forming audit opinion against the issued audit opinion itself by employing parameter estimation method on182 municipals’ financial statements of 2015 and 2016 financial years. Based on the partial hypotheses test results, we find diverse results of each hypotheses tests.

The first hypothesis shows that the weakness in the internal control system, neither in form of deficiencies of the IC structure, the weakness of CSREBE, nor the weakness of ARCS, does not affect the audit opinion of a financial report obtained by the municipal governments. The results of this study are contrary to prior researchers such as Setiawan (Citation2017), Munawar and Abdullah (Citation2016), Agusti (Citation2014), Setyaningrum (Citation2015), Winanti (Citation2014), and Taufikurrahman (Citation2014) who stated that the weakness of the internal control system has negative effects on audit opinion. Nevertheless, the findings are in line with Safitri and Darsono (Citation2015) and Budiawan and Budi (Citation2014) who argue that the internal control system has no effect on audit opinion and has a positive relationship toward audit opinion. Although the effectiveness of ICS is one of the criteria in forming an audit opinion according to Audit of State Financial Governance Act (GoI, Citation2004b), our results on Indonesian local governments’ financial statements show otherwise. The possible explanation of this result is that the numbers of findings do not necessarily materially affect the value of an account and also may not automatically result in misstatements of an account in the financial statement. Thus, it can be concluded that the number of internal control system findings regardless of the materiality value of the findings does not affect the audit opinion on the Indonesian municipal governments’ financial statements.

The second hypothesis of the non-compliance with laws and regulations represented by regional financial loss findings show the negative effect on the audit opinion of municipalities financial statements, whereas the other variables of the potency of regional loss, revenue shortfall, and administration findings do not affect the audit opinion of financial statements obtained by municipalities. However, the results of previous studies by Maabuat et al. (Citation2016), Atmajaya and Probohudono (Citation2015), and Fatimah et al. (Citation2014) are varied, especially in determining the types of findings of non-compliance which affect the audit opinion. Another researcher such as Setiawan (Citation2017) came up with a finding of non-compliance with laws and regulations has no effect on audit opinion. As explained previously, the variable of non-compliance with the laws and regulations in this study is represented by the ratio of the number of non-compliance findings with the value of the expenditure account. Prior studies in most case analyze the non-compliance variables using either the figures or the value of non-compliance findings as the proxy, thus neglecting the discrepancy in the size of expenditures among the local governments. This, of course, can lead to diversity in results.

The third hypothesis test result shows that the non-conformity with the GAS has a significant effect on the audit opinion of the municipal governments’ financial statements. This finding is parallel with research conducted by Nugraheni and Subaweh (Citation2008) and Mahaputra and Putra (Citation2014). The GAS sets out the accounting principles that should be applied in the preparation and presentation of the government financial statements; thus, the GAS serves as a requirement as well as a guideline enforced by regulations by means of improving the quality of government financial information in Indonesia (Mahaputra & Putra, Citation2014).

Based on the overall results, only two variables have the negative effect on audit opinions, which are the non-compliance with the regulations resulted in regional financial losses and the non-conformance with the GAS. Whereas the other criteria of forming audit opinion show no effect against audit opinion. State/region financial loss according to BPK (Citation2017a) is the diminishing of state/regional assets in the form of money, securities, or goods, which is tangible and in an exact number as a result of an act against the law, intentionally or negligently. Based on this definition, it can be understood that the regional financial losses on a considerable amount are likely to have a substantive impact on the value of the related account in the financial statements. Whereas the GAS is the main requirement for presenting government financial statement, therefore, the discrepancy with the GAP shall significantly influence the auditor’s opinion.

6.2. Recommendation

BPK (Citation2017b) expresses that by 2017 financial reporting year, 20.8% (38) of the Indonesian Municipal Governments have not yet received an unqualified audit opinion for their financial statements. Therefore, this study recommends that the local government should focus to design adequate strategies to minimize the number of cases of financial losses in the budget execution process and to ensure that their financial statements are presented in accordance with the GAS.

Additional information

Funding

Notes on contributors

Bambang Pamungkas

Bambang Pamungkas currently serves as a permanent lecturer at the Institute of Economic Science (STIE) Kesatuan, Bogor, Indonesia, and is also active as an extraordinary lecturer at the University of Indonesia, University of Pakuan, and several universities in Jakarta. Graduated from the State Accounting Institute (STAN) and obtained MBA (accounting) from the Hull University, England, he then was awarded Doctorate of Economic (Accounting) from Pajajaran University. Experiences in both the public and private sector accounting and auditing practices started from the Ministry of Finance, Finance and Development Supervisory Agency (BPKP), the Ministry of Home Affairs, apprenticeship in several accountant offices, roles in Tax Auditing of the Joint Team of BPKP and Directorate General of Taxation, member of the Audit Committee at Krakatau Steel, and currently is active at the Supreme Audit Board (BPK). He has also been involved in professional organizations as a member of the working group and Government Accounting Standards Committee.

References

- Agusti, A. F. (2014). Determinants factors of accountability and transparency of ministries/institutions [Faktor Determinan Akuntabilitas dan Transparansi Kementerian/Lembaga] ( Thesis). Economic Faculty, University of Indonesia.

- Ånerud, K. (2007, October). Harmonization of financial auditing standards in the public and private sectors – what are the differences? Accounting, Tax & Banking Collection, 34(4), 17.

- Arens, A. A., Randal, J. E., & Beasley, M. S. (2008). Auditing and assurance services (12th ed.). New Jerssey, NJ: Pearson International Edition.

- Arifin, I., & Fitriasari, D. (2014). Disclosure of ministry/institution financial statements, organizational characteristics and results of BPK’s audit. Proceeding SNA 17, Mataram, 24–27 September.

- Atmajaya, R. M. S. A., & Probohudono, A. N. (2015). Analisis Audit BPK RI Terkait Kelemahan SPI, Temuan Ketidakpatuhan dan Kerugian Negara [Audit analysis of BPK RI regarding weaknesses of ICS, findings of non-compliance and state losses]. Jurnal Integritas, 2(11), 81-110.

- Blume, L., & Voigt, S. (2011). Does organizational design of supreme audit institutions matter? A cross-country assessment. European Journal of Political Economy, 27(2), 215–229. doi:10.1016/j.ejpoleco.2010.07.001

- Brook, D. A. (2001). Business-style financial statements under the CFO Act: An examination of audit opinions ( Dissertation). Graduate Faculty of George Mason University.

- Budiawan, D. A., & Budi, S. P. (2014). Pengaruh Sistem Pengendalian Internal Dan Kekuatan Koersif Terhadap Kualitas Laporan Keuangan Pemerintah Daerah [The influence of internal control systems and coercive strengths on the quality of local government financial reports]. Jurnal Riset Akuntansi Dan Keuangan, University of Education Indonesia, 2(1), 276-288.

- Carslaw, C., Mason, R., & Mills, J. R. (2007). Audit timeliness of school district audits. Journal of Public Budgeting, Accounting & Financial Management, 19(3), 290–316.

- Committee of Sponsoring Organizations of the Treadway Commission. (2013). Internal control-integrated framework. New York, NY: American Institute of Certified Public Accountants.

- D’Aquila, J. M. (1998). Is the control environment related to financial reporting decisions? Managerial Auditing Journal, 13(8), 472–478. doi:10.1108/02686909810236334

- Dye, K. M. (2007, November/December). Corruption and fraud detection by public sector auditors. The EDP Audit, Control and Security, 36(5–6), 6. Accounting, Tax & Banking Collection.

- Fatimah, D., Ria, N. S., & Rasuli, M. (2014). Pengaruh Sistem Pengendalian Intern, Kepatuhan Terhadap Peraturan Perundang-Undangan, Opini Audit Tahun Sebelumnya dan Umur Pemerintah Daerah Terhadap Penerimaan Opini Wajar Tanpa Pengecualian pada Laporan Keuangan Pemerintah Daerah Di Seluruh Indonesia [Effect of internal control systems, compliance with legislation, previous year audit opinions, and lifespan of local governments against unqualified opinion acceptance on local government financial reports throughout Indonesia]. Jurnal Akuntansi, 3(1), 1–15.

- Ge, W., & McVay, S. (2005). The disclosure of material weaknesses in internal control after the Sarbanes–Oxley Act. Accounting Horizons, 19(3), 137–158. doi:10.2308/acch.2005.19.3.137

- Gendron, Y., Cooper, D. J., & Townley, B. (2001). In the name of accountability: State auditing, independence and new public management. Accounting, Auditing & Accountability Journal 14(3): 278. Accounting, Tax & Banking Collection. doi:10.1108/EUM0000000005518

- Ghozali, I. (2011). Aplikasi Analisis Multivariate dengan Program IBM SPSS 19 [Multivariate analysis application with IBM SPSS 19 program]. Semarang: Badan Penerbit Universitas Diponegoro.

- Gonzalez, B., Lopez, A., & Garcia, R. (2011). How do supreme audit institutions measures the impact of their work? Public Sector Accounting, 3, 503–517. Sage Library in Accounting and Finance. Corn wall.

- Government of Indonesia. (2003). Undang-Undang Keuangan Negara Nomor 17 Tahun 2003 [The State Finance Act No. 17/2003]. Jakarta: Government of Indonesia.

- Government of Indonesia. (2004a). Undang-Undang Pemeriksaan Pengelolaan dan Tanggung Jawab Keuangan Negara Nomor 15 Tahun 2004 [The audit of the management and responsibility of the State Finance Act No. 15/2004]. Jakarta: Government of Indonesia.

- Government of Indonesia. (2004b). Undang-Undang Perbendaharaan Negara Nomor 1 Tahun 2004 [The State Treasury Act No. 1/2004]. Jakarta: Government of Indonesia.

- Government of Indonesia. (2005). Peraturan Pemerintah tentang Standar Akuntansi Pemerintahan - Berbasis Kas Nomor 24 Tahun 2015 [The government regulation of governmental accounting standard – cash-based no. 24/2005]. Jakarta: Government of Indonesia.

- Government of Indonesia. (2006). Undang-Undang Badan Pemeriksa Keuangan Nomor 15 Tahun 2016 [The Supreme Audit Board Act No. 15/2006]. Jakarta: Government of Indonesia.

- Government of Indonesia. (2010). Peraturan Pemerintah tentang Standar Akuntansi Pemerintahan Berbasis Akrual [The government regulation of governmental accounting standard – accrual-based no. 71/2010]. Jakarta: Government of Indonesia.

- Griggs, L. L. (2004, Apr). Audits of internal control over financial reporting: What do they mean? Insights, The Corporate & Securities Law Advisor, 18(4). 2. Research Library.

- Habib, A. (2013). A meta-analysis of the determinants of modified audit opinion decisions. Managerial Auditing Journal, 28(3), 184–216. doi:10.1108/02686901311304349

- Hay, D., & Cordery, C. (2018). The value of public sector audit: Literature and history. Journal of Accounting Literature, 40, 1–15. doi:10.1016/j.acclit.2017.11.001

- Liu, J., & Lin, B. (2012). Government auditing and corruption control: Evidence from China’s provincial panel data. China Journal of Accounting Research, 5, 163–186. doi:10.1016/j.cjar.2012.01.002

- Maabuat, J. S., Morasa, J., & Saerang, D. P. E. (2016). Pengaruh Kelemahan Sistem Pengendalian Internal, Ketidakpatuhan pada Peraturan Perundang-Undangan dan Penyelesaian Kerugian Negara terhadap Opini BPK RI atas Laporan Keuangan Pemerintah Daerah di Indonesia [The influence of weaknesses in the internal control system, non-compliance with legislation and settlement of state losses against BPK’s opinion on local government financial statements in Indonesia]. e-Journal Accountability. Sam Ratulangi University, 5(2), 52–62.

- Mahaputra, I. P. U. R., & Putra, I. W. (2014). Analisis Faktor- Faktor Yang Memengaruhi Kualitas Informasi Pelaporan Keuangan Pemerintah Daerah [The analysis of factors affecting quality of information on local government financial reporting]. e-Journal Accountancy Udayana University, 8(2), 230–244.

- McCandless, H. E. (1993, April). Auditing to serve public accountability. International Journal of Government Auditing, 20(2), 14. Accounting, Tax & Banking Collection.

- Ministry of Home Affair of the Republic of Indonesia. (2008). Peraturan Menteri Dalam Negeri Nomor 4 Tahun 2008 tentang Pedoman Pelaksanaan Reviu atas Laporan Keuangan Pemerintah Daerah [Ministry of home affair regulation no 4 of 2008 regarding guidance of implementation review on local government financial statement]. Jakarta: Government of Indonesia.

- Munawar, N., & Abdullah, S. (2016). Pengaruh Jumlah Temuan Audit Atas SPI Dan Jumlah Temuan Audit Atas Kepatuhan Terhadap Opini Atas Laporan Keuangan Pemerintah Kabupaten/Kota Di Aceh [The influence of number of audit findings on ICS and number of compliance audit findings on the opinion of financial statements of district/municipal governments in Aceh]. Jurnal Magister Akuntansi Pascasarjana Universitas Syiah Kuala, 5(2), 57-67.

- Nugraheni, P., & Subaweh, I. (2008, April). Pengaruh Penerapan Standar Akuntansi Pemerintahan Terhadap Kualitas Laporan Keuangan [The implemention effect of government accounting standards on the quality of financial statements]. Jurnal Ekonomi Bisnis, 13(1), 48-58.

- Pearson, D. (2014). Significant reforms in public sector audit – Staying relevant in times of change and challenge. Journal of Accounting and Organizational Change, 10(1), 150–161. doi:10.1108/JAOC-06-2013-0054

- Prasetyaningsih, E., Yuhalifiyah, G., & Susanto, H. (2014). Internal control system weakness and non-compliance to the provision of legislation in practicing audit of local government in Indonesia. Open Journal of Political Science, 4(4), 257–264. doi:10.4236/ojps.2014.44028

- Safitri, N. L. K. S. A., & Darsono. (2015). Pengaruh Sistem Pengendalian Internal dan Temuan Kepatuhan Terhadap Opini Audit pada Pemerintah Daerah [The influence of the internal control system and findings of compliance on audit opinions local governments]. Diponegoro Journal of Accounting, 5(1), 1–12.

- Sari, A. P., Martani, D., & Setyaningrum, D. (2015). Pengaruh temuan audit, tindak lanjut hasil pemeriksaan dan kualitas sumber daya manusia terhadap opini audit melalui tingkat pengungkapan laporan keuangan kementerian/lembaga [Effect of audit findings, follow-up of audit results and quality of human resources on audit opinions through the level of disclosure of ministry/agency financial statements]. Simposium Nasional Akuntansi XVIII, Medan.

- Sari, S. P., & Witono, B. (2014). Keterandalan dan ketepatwaktuan pelaporan keuangan daerah ditinjau dari sumber daya manusia, pengendalian internal dan pemanfaatan Teknologi informasi [Reliability and timeliness of regional financial reporting viewed from human resources, internal control and information technology utilization]. In Seminar Nasional dan Call for Paper (Sancall 2014). Research Methods and Organizational Studies, 418-425.

- Schelker, M., & Eichenberger, R. (2010). Auditors and fiscal policy: Empirical evidence on a little big institution. Journal of Comparative Economics, 38(4), 357–380. doi:10.1016/j.jce.2010.09.002

- Setiawan, R. A. (2017). Pengaruh Sistem Pengendalian Intern dan Kepatuhan Pada Peraturan Perundangundangan Terhadap Opini Laporan Keuangan Pemerintah Daerah [The influence of internal control systems and compliance with laws and regulations on opinions of local government financial reports]. Essay. The University of Hasanuddin.

- Setyaningrum, D. (2015). Kualitas Auditor, Pengawasan Legislatif dan Pemanfaatan Hasil Audit dalam Akuntabilitas Pengelolaan Keuangan Daerah [Auditor quality, legislative supervision and utilization of audit results in regional financial management accountability] ( Dissertation). Economic Faculty, University of Indonesia.

- Siegel, J. G., & Akel, A. (1989, January). Identifying responsibility for the audit report. The National Public Accountant, 34(1), 38.

- Sinason, D. H. 2000. A study of the effects of accountability and engagement risk on auditor materiality decisions in public sector audits. Journal of Public Budgeting, Accounting & Financial Management, 12,1. Accounting, Spring, 12, 1. Tax & Banking Collection. doi:10.1108/JPBAFM-12-01-2000-B001

- Sipahutar, H., & Dan Khairani, S. (2013). Analisis Perubahan Opini LHP BPK RI Atas Laporan Keuangan Pemerintah Daerah Kabupaten Empat Lawang [Analysis of development in BPK’s opinion reports to the financial statements of the regional government of Empat Lawang district]. Journal STIE MDP, 1(1), 1-9.

- Skaerbaek, P. (2009). Public sector auditor identities in making efficiency auditable: The national audit office of denmark as independent auditor and modernizer. Accounting, Organizations and Society, 34(8), 971-987.

- Suparwan, D. K. T., Sujana, E., & Yuniarta, G. A. (2018). Pengaruh Kewajaran Penyajian Laporan Keuangan terhadap Kualitas Akuntabilitas Keuangan pada Dinas-Dinas Kabupaten Bangli [The effect of financial statement fairness presentation on the quality of financial accountability at Bangli district offices]. Jurnal Ilmiah Mahasiswa Akuntansi (JIMAT), Universitas Pendidikan Ganesha, 8(2), 1-12.

- Supreme Audit Board of the Republic of Indonesia [Badan Pemeriksa Keuangan (BPK) Republik Indonesia]. (2014). Petunjuk Pelaksanaan Pemeriksaan Keuangan BPK RI Nomor 4/K/I-XIII.2/7/2014 [Auditing guideline nomor 4/K/I-XIII.2/7/2014]. Jakarta: Republic of Indonesia.

- Supreme Audit Board of the Republic of Indonesia [Badan Pemeriksa Keuangan (BPK) Republik Indonesia]. (2017a). Standar Pemeriksaan Keuangan Negara [State audit standard]. Jakarta: Republic of Indonesia.

- Supreme Audit Board of the Republic of Indonesia [Badan Pemeriksa Keuangan (BPK) Republik Indonesia]. (2017b). Ikhtisar Hasil Pemeriksaan Semester I Tahun 2016 dan 2017 [Summary of audit result semester I year 2016 and 2017]. Jakarta: Republic of Indonesia.

- Tahinakis, P., & Samarinas, M. (2016). The incremental information content of audit opinion. Journal of Applied Accounting Research, 17(2), 139–169. doi:10.1108/JAAR-01-2013-0011

- Taufikurrahman. (2014). Analisis faktor – faktor yang mempengaruhi pemberian opini audit oleh BPK RI atas LKPD Provinsi, kabupaten dan kota di Sumatera Utara [Analysis of factors influencing the provision of audit opinion by the BPK for provincial, district and municipal financial statements in North Sumatra] ( Unpublished essay). University of North Sumatera.

- Trisnani, E. D., Dimyati, M., & Paramu, H. (2018). Pengaruh Sistem Pengendalian Intern Terhadap Keandalan Laporan Keuangan dengan Mediasi Penatausahaan Aset Tetap [The influence of the internal control system on the reliability of financial statements with fixed asset administration intermediation]. Jurnal Bisnis dan Manajemen, 11(3), 271–282.

- Winanti, B. A. (2014). Analisis Pengaruh Temuan dan Tindak Lanjut Pemeriksaan BPK, Legitimasi Kepala Daerah serta Pengawasan Pemerintahan terhadap Opini Audit LKPD 2010–2011 [Analysis of the influence of BPK findings and follow-up of audit results, legitimacy of regional leaders and government oversight of local governments’ financial statements audit opinions 2010–2011]. Accountancy Essay. Economic Faculty, University of Indonesia.

- Wisdom, O., & Oyebisi, O. M. (2017, December). Impact of public sector auditing in promoting accountability and transparency in Nigeria. Journal of Internet Banking and Commerce, 22(3), 22.