Abstract

The purpose of this paper is to investigate the factors affecting individuals’ intentions to adopt Islamic banking. Most of the previous studies have used theory of reasoned action and theory of planned behaviour; however, decomposed theory of planned behaviour, which is proven robust and superior, has been used in very few studies. The present study gauges this gap and proposes a comprehensive model for adoption of Islamic banking. The study also incorporated antecedents of attitude, subjective norms and perceived behavioural control to enhance understanding of factors relevant to the adoption of Islamic banking. A sample of 186 bank customers has been selected for data collection. Variance-based partial least-squares structural equation modelling was employed for data analysis. Results show that attitude and subjective norms have significant positive relationship with intention to adopt Islamic banking. The result depicts that attitude is determined by awareness, uncertainty, relative advantage and compatibility. Subjective norm is determined by normative beliefs. Perceived behavioural control is determined by self-efficacy and resource facilitation condition. The findings of the study are important for Islamic banks to revamp their marketing strategies. Marketing managers should try to develop positive attitude through creating awareness and benefits of Islamic banking services. Positive word of mouth is also an important aspect which can be created through enhancing the service delivery to the existing customers.

PUBLIC INTEREST STATEMENT

Choosing products and services which are according to one’s religious values is an important consideration before actual purchase. Interest is prohibited according to Islamic teaching, hence the conventional banking is questioned on religious grounds. Islamic banking services are available from decades and still lack acceptability among masses. The present study provides an insight into Islamic banks to improve their marketing strategies which can help to market their products in an effective and efficient manner.

1. Introduction

Conventional banking has been questioned by Islamic scholars as it contradicts Islamic business principles. Conventional banks deal with interest-based transactions for the generation of assets and liabilities. On the contrary, Islamic banks are not allowed to deal with interest-based activities (riba), indulging in speculative business activities (gharar), or specific unlawful investments and financing (haram) (Masood, Abdullah, Shahimi, & Ismail, Citation2011; Nawaz & Haniffa, Citation2017; Wulandari, Putri, Kassim, & Sulung, Citation2016). Islam clearly prohibits the use of the tradition of interest, and it is clearly specified in the Holy Quran as well in Surah Nisa and Surah Rehman (Ezeh & Nkamnebe, Citation2018). For that purpose, Islamic banking in return provides banking services which are based on Islamic principles. It is primarily based on non-interest and trade-based modes (Rashid, Hassan, Umar, & Ahmad, Citation2009).

Islamic banks have developed Murabaha, Mudarbaha Ijarah and Musharakah agreements (Butt, Ahmed, Naveed & Ahmed, Citation2018). Islamic banking is based on Islamic principles and is chosen by many due to their faith and religious commitments. However, there are other factors which are also considered by the individuals while choosing Islamic banking. These can be categorized into individual, social, cultural and religious factors (Asdullah and Yazdifar, Citation2016) as well as institutional factors such as facilities (Amin, Citation2013). Also, the extant literature shows factors such as a bank’s reputation, convenience, staff quality, availability of ATM, service quality and speed, fees, family and friends influence, service variety, and so on (Almossawi, Citation2001; Echchabi & Olaniyi, Citation2012; Md. Saleh, Mohamad, & Nani, Citation2013; Siddique, Citation2012; Yavas, Babakus, & Ashill, Citation2006).

Since its inception more than four decades ago, Islamic banking has been growing in different parts of the world. Assets of Global Islamic Banking reached US$1.00 trillion in 2015 (Young, Citation2016). It provides an option for millions of individuals to avail financial services according to their faith. Islamic banking accounts for major portion of Islamic finance industry with 79% share in overall Islamic finance industry in the world (IFSB, Citation2017). This depicts the importance of Islamic banking in overall Islamic finance architecture.

There are different levels at which Islamic banking is currently operating. Firstly, there are full-fledge Islamic banks which are providing only Islamic banking services. Secondly, there are conventional banks which only provide conventional banking services. Apart from that, there is a dual banking system which is also operating where some banks are providing both Islamic and conventional banking services. Therefore, Islamic banks are not only competing with full-fledged conventional banks but also with a dual banking system. Islamic banks are offering products and services, such as saving accounts, current accounts, credit cards, home financing and other products and services within the same segment (Amin et al., Citation2017). Increasing competition is pushing Islamic banks to develop unique marketing strategies to develop and maintain relationships with their customers for long-term corporate sustainability and success.

Islamic banking in Pakistan started operating more than three decades ago; however, State Bank of Pakistan constituted a commission for the transformation of financial system to promote Shariah-based financing. State Bank of Pakistan also developed a department of Islamic Banking on 15 December 2003. Since then, measures have been taken to increase the development and growth of Islamic banking in Pakistan. There has been a considerable shift in the Pakistani financial landscape that enables fresh avenues and prospects in the Islamic banking sector and hence shows that a huge untapped market still exists. Also, the Pakistani market has a huge market potential for Islamic banking (Khan, Ahmed, Rehman & Haleem, Citation2018). Masses in the rural areas are more than 50% of the Islamic banking’s customers of Pakistan (Akhtar, Citation2007a). Apart from that, different income-level groups are being exposed to Islamic banking products and services to make informed purchase decisions according to their needs (Thambiah, Eze, Santhapparaj, & Arumugam, Citation2010). In this regard, Islamic banks exhibit similarity to the conventional banks. However, Islamic banking in Pakistan currently has a 6.7% market share (Butt et al, 2018) in spite of having 98% Muslim population.

This system has not been diffused among the Pakistani masses due to the maturity of the conventional banking system (Israr, Qureshi, & Butt, Citation2018; Salman, Nawaz, Bukhari, & Baker, Citation2018). To fill this gap and to determine what drives the Pakistani consumers to opt for Islamic banking services and taking lead from the decomposed theory of planned behaviour (DTPB), the present study is an attempt to find out the factors that motivate people to adopt Islamic banking. DTPB has been proven superior compared to other theories as it is based on decomposition of belief structures. Therefore, the present study uses DTPB to find out the factors driving adoption of Islamic banking in Pakistan. The findings of the present study can help Islamic banking to devise effective marketing strategies to enhance market share of Islamic banking in Pakistan.

2. Literature review

In the literature there are several theories which are used to study intention behaviour relationship. These theories comprise theory of reasoned action (TRA), theory of planned behaviour (TPB) and DTPB. These theories are discussed in the following section.

2.1. Theory of reasoned action

Ajzen and Fishbein (Citation1980) have presented TRA, and there are three constructs that constitute this theory, i.e. behavioural intention (BI), attitude and subjective norms (SN). TRA is concerned with an individual’s behaviour and motivation to do a certain action. According to Ajzen and Fishbein (Citation1980, p. 10), TRA helps to explain and predict human behaviour. This theory is based on two assumptions (Ajzen & Fishbein, Citation1980, p. 5); first, the human actions are under volitional control, and second, that human actions are determined by intentions.

Venkatesh, Morris, Davis, and Davis (Citation2003) state that TRA is the basic theory to elucidate human behaviour. This theory states that it is the intention which leads to a certain behaviour and this intention is called BI. According to TRA, these BIs are shaped by attitudes and SNs. Attitude is the opinion about behaviour either positive or negative, whereas SN is the social pressure to perform a certain behaviour or not. This theory has largely been applied in psychology in order to explain human behaviours.

2.2. Theory of planned behaviour

TPB is an extension of TRA. (Ajzen and Fishbein, Citation1975; Ajzen & Fishbein, Citation1980). TPB provides one of the most dominant conceptual frameworks in order to study human behaviour (Ajzen, Citation2001). TRA deals with behaviours which are under volitional control (Ajzen & Fishbein, Citation1980, p. 5). TPB extends and incorporates behaviours affected by non-voluntary variables (Ajzen, Citation1985, p. 30, 36). According to Ajzen (Citation1991), TPB incorporates attitudes, SNs and perceived behavioural control (PBC) to predict intentions with higher accuracy.

TPB comprises three components which determine BIs: attitude (Att), SN and PBC. Attitude is determined by behavioural beliefs, SNs are explained by normative beliefs and control belief determines PBC. Attitude refers to the measurement of evaluation of a performance of certain behaviour. SNs are the external factor referring to others thought about action or behaviour. PBC is to what extent an individual believes about his ability to perform behaviour.

PBC was additionally included in the model of TPB. Behaviour of the people is dependent upon the level of control they possess. The chances of a certain behaviour will be low if the control element is low in spite of favourable attitude and SNs. The notion was proved by Bundara, Adam, Hardly and Howells that behaviour is determined by confidence an individual possess regarding having control of performing a behaviour.

Other studies conducted by many researchers such as Bhattacherjee (Citation2000), Armitage and Conner (Citation2001), Fukukawa (Citation2002), Yap and Noor (Citation2008), Chun and Chun (Citation2010), Syed and Nazura (Citation2011), Goh Say Leng, Lada, Muhammad, Ibrahim, and Amboala (Citation2011) and Al- Jabari, Othman, & Nik Mat (Citation2012) also confirm that PBC is a significant determinant of intention to engage in a certain behaviour.

2.3. Decomposed theory of planned behaviour

Taylor and Todd (Citation1995) presented DTPB which describes three dimensions of human behaviour, i.e. attitude, SNs and PBC. This theory is a combination of TPB and technology acceptance model. In the original theory, attitude, SNs and PBC are further supported by multidimensional constructs to study behavioural intentions towards information technology. Research has confirmed that DTPB incorporates innovation literature along with normative and control beliefs and measures intention to adoption more accurately than TPB (Jaruwachirathanakul & Fink, Citation2005, p. 298).

In DTPB (Taylor & Todd, Citation1995), attitude is determined by relative advantage, complexity and compatibility which is mainly influenced by diffusion theory of Rogers (Citation1995). Depending upon the context, determinants of PBC can be included. According to DTPB, behavioural control is determined by self-efficacy, resource and technology facilitation. The concept of self-efficacy was derived from Bandura (Citation1986) which is self-belief to be able to perform a certain behaviour. Whereas resource facilitation condition is derived from Triandis (Citation1980).

DTPB has shown better explanatory power in explaining the BIs in comparison to the TPB and is a proven robust model in explaining behaviour regarding information systems (Beiginia, Besheli, Soluklu, & Ahmadi, Citation2011; Bhattacherjee, Citation2000; Pedersen, Citation2005; Shih & Fang, Citation2004). DTPB has been used in the study of financial services because theory can be modified to incorporate the relevant variables (Taylor & Todd, Citation1995). On the basis of this theory, attitude is decomposed further into awareness, uncertainty, compatibility and relative advantage. SNs is decomposed into normative belief. PBC is decomposed into self-efficacy and resource facilitation condition.

2.4. Attitude and intention

TRA has presented a very important determinant of TRA called attitude that is used to explain the consumer’s intention (Amin et al, Citation2011). According to Fishbein and Ajzen (1975), previous literature is loaded with the evidence that positive attitude leads to positive consumer behavioural intentions in different domains such as Hsu, Chang and Yansritakul’s (Citation2017) green skin care products, Khasawne and Irshaidat’s (Citation2017) mobile banking, and Alavion, Allahyari, Al-Rimawi, and Surujlal’s (Citation2017) agricultural e-marketing. Similarly, in the context of Islamic banking, Abd Rahman, Asrarhaghighi, and Ab Rahman (Citation2015). Mansour, Eljelly, and Abdullah (Citation2016) and Souiden and Rani (Citation2015) found out that positive attitudes lead towards positive purchase intentions. However, attitude has been decomposed into awareness, compatibility, uncertainty and relative advantage. This study aims to further investigate the individual effect of the antecedents of attitude on the consumer intention to adopt Islamic banking services in Pakistan. For that purpose, we hypothesize as follows.

H1: Attitude has a positive influence on the intention to adopt Islamic banking services in Pakistan.

H2: Awareness has a positive influence on the attitude towards Islamic banking services.

H3: Uncertainty has a negative influence on the attitude towards Islamic banking services.

H4: Compatibility has a positive influence on the attitude towards Islamic banking services.

H5: Relative advantage has a positive influence on the attitude towards Islamic banking services.

2.5. Subjective norms and intention

SNs are a belief that a person’s immediate social circle with support or disapprove a certain behaviour. As human beings are social animals, therefore, they remain under a social pressure to behave in a definite manner. Previous literature shows mixed views about the relation of SNs with intentions. Armitage and Conner (Citation2001) showed a weak conceptualization of the SNs to predict intentions. The influence of SNs on forming intention proved to be generally weaker in previous studies than the influence of attitude. However other studies have found a significant relation of SNs with the positive intentions (Chang, Citation1998; Tarkiainen & Sundqvist, Citation2005). In the context of Islamic banking Lujja Mohammad, and Hassan (Citation2016) found that SNs have an indirect influence on the purchase intention through the mediated mechanism of attitude. Amin, Isa, and Fontaine (Citation2011) incorporated TRA in Islamic personal financing and found subject norms to positively predict purchase intention in the consumer. The conflicting role of SNs to predict purchase intention has encouraged to further investigate the role of normative beliefs to predict the behavioural intention of the prospective consumers. Hence, it could be hypothesized as follows.

H6: Subjective norm has a positive influence on the intention to adopt Islamic banking services.

H7: Normative belief has a positive influence on subjective norm.

2.6. PBC and intention

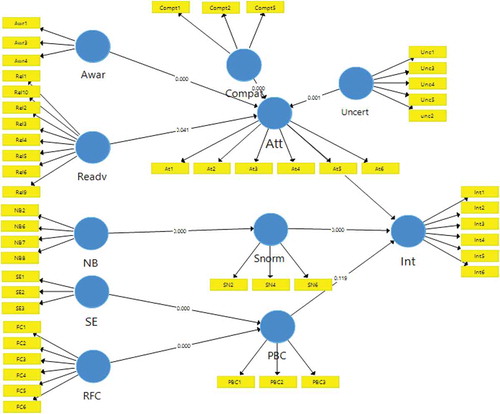

PBC refers to the perception whether a certain behaviour is controllable. It also ascertains the concept of the difficulty level of the initiation of that behaviour (Rauch & Hulsink, Citation2015). It reflects a certain behaviour with respect to a person’s capability and conditions (Cestac, Paran, & Delhomme, Citation2011). Thus, people having a higher personal control have strong intentions to behave in a certain manner (Ajzen, Citation1991). Shih and Fang (Citation2004) added that PBC has been decomposed into facilitation and efficacy. The importance of PBC has been highlighted in different contexts such as the use of different technologies like online systems (Khalifa & Ning Shen, Citation2008; Lin & Chang, Citation2011). Apart from that, PBC significantly and positively influences the intention to undertake Islamic home financing (Alam, Janor, Zanariah &Ahsan, Citation2012). Same result was found true for Islamic banking products in Nigeria (Ringim, Citation2014). Likewise, the literature is full of research that presents a unanimous consensus that if a person has adequate financial resources and is capable of investing for Islamic banking services, then it is very likely that he will develop a positive intention to Islamic banking services. Since the current research aims to examine the individual effect of the antecedents of PBC, therefore, it is hypothesized as follows (Figure ).

H8: Perceived behavioural control has a positive influence on the intention to adopt Islamic

banking services in Pakistan.

H9: Self -efficacy has a positive influence on the perceived behavioural control.

H10: Facilitating conditions have a positive influence on the perceived behavioural control.

3. Research method

The people who were considered for getting the survey questionnaires filled were the individuals that were availing the facilities of both the conventional and Islamic banks. The objective of the study was to find out to what extent behavioural beliefs, normative beliefs and control beliefs shaped an individual’s intention to adopt Islamic banking. Two cities in Pakistan, i.e. Rawalpindi and Islamabad, were selected for data collection predominantly due to three reasons. Firstly, Islamabad is the federal capital and Rawalpindi is the adjacent city and both are often termed as twin cities and people from almost all ethnic backgrounds and provinces are residing here. Secondly, being urban areas, the literacy rate is high in these cities. Thirdly, most of the banking facilities are available in urban areas.

For choosing appropriate sample size, statistical power criterion was used. “G*Power” table was being used for calculation of minimum sample size as recommended by Hair, Sarstedt, Hopkins, and Kuppelwieser (Citation2014). The model four predictors, the effect size was chosen as 0.15 and power 0.95. The minimum sample size obtained as per this criterion was 129. However, the sample size selected for the present study was above the minimum sample size, i.e. 186. The choice of sample size according to the method was proven advantageous and adopted in previous literature (Hair et al., Citation2014). The population base is very wide, and the data of such individuals does not exist hence there was no sampling frame available for the population. Therefore, the present study used non-probability sampling technique, i.e. judgemental sampling. Judgemental sampling is often employed when a limited figure of people are eligible for the data collection according to the objectives of the study. In such circumstances, a very specific group of people can be considered as a subject of interest. This method is appropriate as the required sample should have some characteristics, and presently availing banking facilities. For the present study the sample selected are working individuals who are potential customers of conventional banking services. The data was collected through a questionnaire which comprises two parts. The first part was related to the items which were adopted from the existing literature with Likert scale 1–7. The second part of the questionnaire included the demographic profiles of the respondents. In total, 250 questionnaires were distributed and 200 were received back. Due to suspicious responses, 14 questionnaires were discarded. Suspicious responses are found due to straight lining and inconsistent responses. Straight lining, middle or extreme response styles need to be removed from the data. Therefore, few of the responses with identical and inconsistent responses were removed from the final data as such responses could adversely affect the reliability of the dat. The final 186 useable questionnaires were selected.

3.1. Respondent profile

The data was analysed considering 186 respondents. There were around 120 male respondents and 66 female respondents who filled the questionnaires. Analysis showed that around 74 respondents were single and 112 respondents were married. Apart from that, majority of the respondents held a master’s degree, i.e. 104 respondents. The employment status of most of the respondents was private sector, 54.8%. In terms of age, almost 85.5% respondents were below the age of 40 years. In terms of availing banking, 38.7% were in Islamic banking and 34.9% used conventional banking (Table ).

Figure 1. Research model.

4. Structural equation modelling

The analysis was carried out by using partial least-squares structural equation modelling (PLS-SEM) technique by using SmartPLS software version 3.2.7 (Ringle, Wende, & Becker, Citation2015). The advantage of using this technique is that it can handle non-normal data and is used when the objective of the study is to explain the variance among the target construct. PLS-SEM is a two-step process where first measurement model is analysed to check the reliability and validity of the data. Secondly, structural model assessment is carried out for path analysis and hypothesis testing. Once the data is built into SmartPLS, a path model is constructed as shown below.

4.1. Measurement model

The first step in PLS-SEM is the measurement model assessment. Measurement model shows the relationship between construct and items. For measurement model assessment, three criteria need to be followed: indicator reliability (factor loadings), internal consistency reliability (composite reliability [CR]), construct validity (average variance extracted [AVE]) and discriminant validity (Fornell and Lacker (F & L) hetrotrait monotrait ratio [HTMT]). The measurement results were obtained after running algorithm is SmartPLS and are shown in Table .

Table 1. Demographic profile of the respondents

Table 2. Validity and reliability for constructs

The result of the measurement model is shown in Table : all factor loadings were above a cut of point of 0.7, CR is above 0.7 and AVE values are above 0.5, hence establishing an indicator reliability, internal consistency and CR.

Further, to assess the discriminant validity, Fornell and Larcker (Citation1981) criterion was used (Hair et al., Citation2014). According to this criterion, the square root of AVE of each construct was paralleled with its correlation of other construct. As exhibited in Table , square root of AVE of every construct had a greater value than its correlations with other constructs. HTMT is improved criteria to establish discriminant validity and cut-off shall be less than 0.90. F&L and HTMT criteria both have been fulfilled, hence establishing discriminant validity. Therefore, the measurement model had acceptable discriminant validity. Moreover, since the measurement model of this research showed a satisfactory level of reliability and validity, the analysis could be furthered to assess the structural model followed by hypotheses testing.

Table 3. The HTMT

4.2. Structural model

After the measurement model was assessed, the structural model was assessed. The structural model includes the model predictive competencies as well as the relationships among the reflective constructs. For that purpose, R2 values and Q2 predictive relevance were calculated. As shown in Table , R2 for adoption is 78%, suggesting that the model has a substantial explanatory power. Furthermore, to assess the predictive relevance of the model, blindfolding technique was used. Hair et al. (Citation2014) suggested that blindfolding should only be used for endogenous variable that has a reflective measurement. If Q2 > 0, then the model has a predictive relevance. As seen in Table , Q2 value for adoption is 0.637.

Table 4. Goodness of fit and predictive relevance

To test the hypothesized relationships among the constructs, the estimates were attained for the path coefficients. For that purpose, PLS-SEM algorithm was performed. Bootstrapping was exercised for 5,000 samples. Table presents a summary of the hypothesized relationships among the constructs. H1 represented the relation between attitude and adoption of Islamic banking, which is supported by having a B = 0.650, P < 0.01 and T statistics 10.910, H2 presented the relation between awareness and attitude which is supported with B = 0.274, P < 0.01 and T statistics 5.098, H3 revealed the relation between perceived uncertainty and attitude which showed an inverse relation with B = −0.196, P < 0.01 and T statistics 3.154. H4 showed the relationship between compatibility and attitude. The results showed a significant relationship with B = 0.483, P < 0.01 and T statistics 5.436. H5 showed a positive relationship between relative advantage and attitude, i.e. B = 0.149 and T statistics 1.771.

Table 5. Hypothesis testing

Table 6. Model fit value

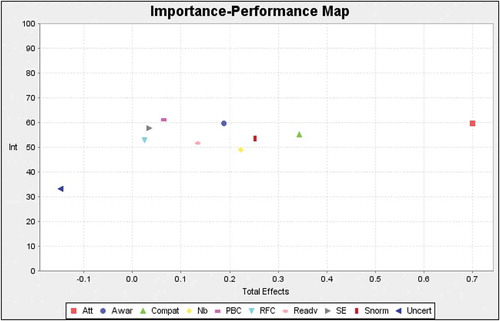

Table 7. IMPA results

H6 showed the relationship between SNs and intention with B = 0.246 and T statistics 3.969. H7 showed the relation between normative beliefs and SNs with B = 0.826 and T statistics 31.941.

H8 showed the relationship between PBC and intention with B = 0.059 and T statistics 1.185. H9 showed the relation between resource facilitation and PBC with B = 0.336 and T statistics 0.802. H10 showed the relationship between financial self-efficacy and PBC with B = 0.490 and T statistics 5.379. Hence, the data for the current research supported all the hypotheses except for H8 having important research implications for Islamic banks.

5. PLS-SEM results

5.1. Model fit

For model fit, SmartPLS provided values of standardized mean square values (SRMR), and the cut-off for acceptable level of model fit is less than 0.080. For the present study, the value of SRMR was 0.041 which showed acceptable value for model fit (Table ).

5.2. Importance performance map analysis

The importance performance map analysis showed that attitude was the most important factor in determining the adoption of Islamic banking which was followed by SNs (Table ).

6. Conclusion

6.1. Discussion

Drawing from the TPB, the current research had set out to determine whether the attitude, SNs and PBC have any influence in determining the consumers’ intention to adopt financial banking services in Pakistan. These three factors were decomposed into their antecedents for an in-depth analysis to ensure the robustness of the research. All the hypotheses were supported by the data except for H8 that represented the relationship of PBC with the adoption intention. The results exposed that the influence of consumer attitude on the adoption intention is the strongest compared to SNs and PBC. For that purpose, it was hypothesized that the consumers’ attitude has a positive influence on Islamic banking services adoption.

The findings harness and support the previous findings (Jaffar & Musa, Citation2016; Lajuni, Wong, Yacob, Ting & Jausin, Citation2017) showing that the role of attitude in shaping a positive adoption intentions for Islamic banking and financing products in the emerging and developing markets is very vital. So, if the consumer will develop a positive attitude towards adopting Islamic banking services, he will very likely intend to adopt them. Thus the results can be generalized in the Pakistani context as well. Furthermore, interestingly, of the four antecedents of attitude, uncertainty had an inverse relation attitude, depicting that if a consumer is uncertain about the Islamic banking products, he will develop a negative attitude regarding the adoption of Islamic banking services. These findings are supported by previous literature where it has been empirically tested that consumers who consider adopting lay emphasis on uncertainties related to the drawbacks of the adoption. Especially if the adoption decision is to be made in the near future (Castano, Sujan, Kacker & Sujan, Citation2008). Also, the compatibility of the IB services with the consumer’s financial needs was found out to be the most important of all the factors. The results are consistent with the previous literature where the consumer evaluations of a product are based on the compatibility of consumers’ goals that enable them to explore the choice alternatives (Chernev, Citation2004). Thus, presenting important implications for IB managers.

The current research also sought to investigate the role a consumer’s SNs play in developing a positive intent in him to adopt Islamic banking services. The results of the analysis posited that SNs also significantly affect the consumers’ intention in the context of Islamic banking services (Amin et al., Citation2011). When the SNs were decomposed into normative beliefs, the results confirmed that the normative beliefs strongly affect the SNs as supported by the previous literature (Ajzen, Citation2002).

Furthermore, this research set out to find whether a consumer’s PBC has any effect on the adoption of Islamic banking services. The PBC was decomposed into self-efficacy and resource facilitation. It was found out that in the context of Islamic banking both the above-mentioned antecedents had a significant role in forming the PBC. The findings revealed that PBC does not affect the intention of the consumer’s PBC signalling the importance of attitude in determining the consumer intention to adopt Islamic banking system. These research findings are consistent with the previous findings (Taylor & Todd, Citation1995; Beiginia et al., Citation2011). Hence as a result, the findings of the current research can be easily generalized and provide important implications to the Islamic banking management in a Pakistani context.

6.2. Theoretical implications

It is evident that Islamic banking services are gaining popularity among not only Muslim consumers, but also non-Muslim consumers. The increase in Islamic banking services use will significantly increase its growth. But before that the marketers need to develop a profound understanding and an in-depth insight of the dynamics that enable the consumer to have a positive intention to purchase and adopt the Islamic banking services. For that purpose, the application of the TPB potentially predicts a consumer’s intention to adopt Islamic banking services in a Pakistani context, thus signifying the generalizability of the results with respect to Islamic banking domain. This research embarks on three potential individual predictors to predict the intention stemming and taking guidance from the TPB as well as previous literature. The three important predicts are attitude, SNs and PBC. Furthermore, these predictors are further decomposed and their antecedents have also been taken into account.

6.3. Practical implications

The results of the current research offer valuable insights for the management of Islamic banking services. The current research is loaded with valuable information for the marketing managers to enable them to attract and retain the potential consumers. Attitude towards adopting Islamic banking significantly predicts the consumer’s intention. So, the marketing managers can target the consumer attitude and ensure positive intention. Drawing from the results of the study, the uncertainty of the consumers could be targeted to develop a positive attitude in the consumers. Managers could first identify the favourable attitudes that will lead to positive purchase intentions and devise their promotional tools accordingly.

Secondly, they could take suitable measures to improve these consumer attitudes. One way of doing this could be to create awareness in the consumers about the benefits of the Islamic banking services. Alternatively, apart from the positive attitudes, negative attitudes could be explored which hinder the development of a positive attitude. Consequently, the managers can gauge on eliminating those factors. Another way could be that marketers develop a comprehensive marketing campaign that not only creates awareness but also aids in developing a positive attitude in the potential consumers so that they may be inclined to adopt Islamic banking services. These campaigns could include advertising and sales attractive sales promotions to the prospective consumers. Television talk shows could create awareness of the economic and social well-being of the consumers by inviting religious scholars and Islamic banking experts. Apart from that, social media campaigns on Facebook, Twitter and Instagram would be very beneficial in spreading the word out to the masses about the advantages of Islamic banking.

The results also showed that compatibility of the consumers is a very good predictor of the development of a positive attitude. The Islamic banking products and services will ensure more customer base if it will be according to their needs and wants and will add more financial value to their lives. For that purpose, Islamic banks need to first identify their target market very clearly and focusing of the concept of niche marketing strategies, the products and services could be offered which will increase the customer base, thus enabling consumer loyalty in the longer run.

6.4. Future research direction

Islamic banking services have remained under a very sceptical eye of the masses. For that reason, further research could value the role of consumer trust and consumer scepticism to predict the consumer’s intention. Furthermore, future research could take into account the role of social media and e WOM to find out their significance in developing a positive attitude towards adoption of Islamic Banking Services. Additionally, the role of PBC could be replaced by self-efficacy as suggested by Armitage and Corner (Citation2001) in the future research studies.

Author statement

The main author is working in Islamic banking industry and also conducts research in this area. The present study is an attempt to address the issue low Islamic banking penetration. Pakistan is a Muslim state with a significant Muslim population. However, in comparison to other Muslim countries, the Islamic banking product market penetration remains very low. The current research takes guidance from the theory of planned behaviour and tries to find out the factors that drive the consumers to develop a positive intention to adopt Islamic banking. Keeping in view those factors, the marketing managers and regulators can effectively penetrate the Pakistani market to increase its customer base. This study will enable the Islamic banking managers to devise effective marketing strategies to not only retain the existing customers, but also to increase its customer base to increase the overall market share of Islamic banking products.

Additional information

Funding

References

- Abd Rahman, A., Asrarhaghighi, E., & Ab Rahman, S. (2015). Consumers and Halal cosmetic products: Knowledge, religiosity, attitude and intention. Journal of Islamic Marketing, 6(1), 148–163. doi:10.1108/JIMA-09-2013-0068

- Ajzen, I. (1985). From intentions to actions: A theory of planned behavior. In Action control (pp. 11–39). Berlin, Heidelberg: Springer.

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179-211.

- Ajzen, I. (2001). Nature and operation of attitudes. Annual Review of Psychology, 52(1), 27–58. doi:10.1146/annurev.psych.52.1.27

- Ajzen, I. (2002). Perceived behavioral control, self‐efficacy, locus of control, and the theory of planned behavior 1. Journal of Applied Social Psychology, 32(4), 665-683.

- Fishbein, M., & Ajzen, I. (1975). Belief, attitude, intention and behavior: An introduction to theory and research.

- Ajzen, I., & Fishbein, M. (1980). Understanding attitudes and predicting social behaviour. Ajzen Englewood Cliffs, NJ: Prentice-Hall

- Akhtar, S. (2007a). Building an effective Islamic financial system. BIS Review, 38, 1–7.

- Alam, S. S., Janor, H., Zanariah, C. A. C. W., & Ahsan, M. N. (2012). Is religiosity an important factor in influencing the intention to undertake Islamic home financing in Klang Valley? World Applied Sciences Journal, 19(7), 1030–1041.

- Alam, S. S., & Sayuti, N. M. (2011). Applying the Theory of Planned Behavior (TPB) in halal food purchasing. International Journal of Commerce and Management, 21(1), 8–20. doi:10.1108/10569211111111676

- Alavion, S. J., Allahyari, M. S., Al-Rimawi, A. S., & Surujlal, J. (2017). Adoption of agricultural E-marketing: Application of the theory of planned behavior. Journal of International Food & Agribusiness Marketing, 29(1), 1–15. doi:10.1080/08974438.2016.1229242

- Almossawi, M. (2001). Bank selection criteria employed by college students in Bahrain: An empirical analysis. International Journal of Bank Marketing, 19(3), 115–125. doi:10.1108/02652320110388540

- Amin, H. (2013). Factors influencing malaysian bank customers to choose islamic credit cards: Empirical evidence from the tra model. Journal of Islamic Marketing, 4(3), 245-263.

- Amin, M., Isa, Z., & Fontaine, R. (2011). The role of customer satisfaction in enhancing customer loyalty in Malaysian Islamic banks. The Service Industries Journal, 31(9), 1519–1532. doi:10.1080/02642060903576076

- Amin, H., Rahim Abdul Rahman, A., Laison Sondoh Jr, S., & Magdalene Chooi Hwa, A. (2011). Determinants of customers’ intention to use Islamic personal financing: The case of Malaysian Islamic banks. Journal of Islamic Accounting and Business Research, 2(1), 22–4.

- Amin, H., Rahman, A. R. A., Razak, D. A., Rizal, H. (2017). Consumer attitude and preference in the Islamic mortgage sector: A study of Malaysian consumers. Management Research Review, 40(1), 95–115.

- Armitage, C. J., & Conner, M. (2001). Efficacy of the theory of planned behaviour: A meta‐analytic review. British Journal of Social Psychology, 40(4), 471–499.

- Asdullah, M. A, & Yazdifar, H. (2016). Evaluation of factors influencing youth towards islamic banking in pakistan. ICTACT Journal on Management Studies, 2(1).

- Bandura, A. (1986). The explanatory and predictive scope of self-efficacy theory. Journal of Social and Clinical Psychology, 4(3), 359–373. doi:10.1521/jscp.1986.4.3.359

- Beiginia, A. R., Besheli, A. S., Soluklu, M. E., & Ahmadi, M. (2011). Assessing the mobile banking adoption based on the decomposed theory of planned behaviour. European Journal of Economics, Finance and Administrative Sciences, 28(1), 7–15.

- Bhattacherjee, A. (2000). Acceptance of e-commerce services: The case of electronic brokerages. IEEE Transactions on Systems, Man, and cybernetics-Part A: Systems and Humans, 30(4), 411–420. doi:10.1109/3468.852435

- Butt, I., Ahmad, N., Naveed, A., & Ahmed, Z. (2018). Determinants of low adoption of islamic banking in pakistan. Journal of Islamic Marketing, 9(3), 655-672.

- Castaño, R., Sujan, M., Kacker, M., & Sujan, H. (2008). Managing consumer uncertainty in the adoption of new products: Temporal distance and mental simulation. Journal of Marketing Research, 45(3), 320-336.

- Cestac, J., Paran, F., & Delhomme, P. (2011). Young drivers’ sensation seeking, subjective norms, and perceived behavioral control and their roles in predicting speeding intention: How risk-taking motivations evolve with gender and driving experience. Safety Science, 49(3), 424–432. doi:10.1016/j.ssci.2010.10.007

- Chang, M. K. (1998). Predicting unethical behavior: A comparison of the theory of reasoned action of the theory of planned behavior. Journal of Business Ethics, 17(16), 1825–1833. doi:10.1023/A:1005721401993

- Chernev, A. (2004). Goal-attribute compatibility in consumer choice.

- Chun, H. S. L., & Chun, F. C. (2010). Application of theory of planned behavior on the study of workplace dishonesty. International Conference on Economics, Business and Management, 2, 66–69.

- Echchabi, A., & Olaniyi, O. N. (2012). Malaysian consumers’ preferences for Islamic banking attributes. International Journal of Social Economics, 39(11), 859–874. doi:10.1108/03068291211263907

- Ezeh, P. C., & Nkamnebe, A. D. (2018). A conceptual framework for the adoption of Islamic banking in a pluralistic-secular nation. Journal of Islamic Marketing, 9, 951–964. doi:10.1108/jima-03-2017-0022

- Fornell, C., & Larcker, D. F. (1981). Structural equation models with unobservable variables and measurement error: Algebra and statistics. Journal of Marketing Research, 18, 382–388. doi:10.2307/3150980

- Fukukawa, K. (2002). Developing a framework for ethically questionable behavior in consumption. Journal of Business Ethics, 41(1), 99–119. doi:10.1023/A:1021354323586

- Hair, J. F., Jr, Sarstedt, M., Hopkins, L., & Kuppelwieser, V. G. (2014). Partial least squares structural equation modeling (PLS-SEM) An emerging tool in business research. European Business Review, 26(2), 106–121. doi:10.1108/EBR-10-2013-0128

- Hsu, C. L., Chang, C. Y., & Yansritakul, C. (2017). Exploring purchase intention of green skincare products using the theory of planned behavior: testing the moderating effects of country of origin and price sensitivity. Journal of Retailing and Consumer Services, 34, 145-152.

- IFSB. (2017). Islamic financial services board. Islamic Financial Services Industry Stability Report.

- Israr, A., Qureshi, F. A., & Butt, M. (2018). Selection criteria of public for account opening: A case study of Islamic banks in Pakistan. Al-Iqtishad Journal of Islamic Economics, 10(1), 153–170. doi:10.15408/aiq.v10i1.6011

- Jaffar, M. A., & Musa, R. (2016). Determinants of attitude and intention towards Islamic financing adoption among non-users. Procedia Economics and Finance, 37, 227–233. doi:10.1016/S2212-5671(16)30118-6

- Jaruwachirathanakul, B., & Fink, D. (2005). Internet banking adoption strategies for a developing country: The case of Thailand. Internet Research, 15(3), 295–311. doi:10.1108/10662240510602708

- Khalifa, M., & Ning Shen, K. (2008). Explaining the adoption of transactional B2C mobile commerce. Journal of Enterprise Information Management, 21(2), 110–124. doi:10.1108/17410390810851372

- Khan, T., Ahmad, W., Rahman, M. K. U., & Haleem, F. (2018). An investigation of the performance of Islamic and interest based banking evidence from Pakistan. HOLISTICA–Journal of Business and Public Administration, 9(1), 81–112. doi:10.1515/hjbpa-2018-0007

- Khasawneh, M. H. A., & Irshaidat, R. (2017). Empirical validation of the decomposed theory of planned behaviour model within the mobile banking adoption context. International Journal of Electronic Marketing and Retailing, 8(1), 58–76. doi:10.1504/IJEMR.2017.083553

- Lajuni, N., Wong, W. P. M., Yacob, Y., Ting, H., & Jausin, A. (2017). Intention to use Islamic banking products and its determinants. International Journal of Economics and Financial Issues, 7(1), 329–333.

- Leng, G. S., Lada, S., Muhammad, M. Z., Ibrahim, A. A. H. A., & Amboala, T. (2011). An exploration of social networking sites (SNS) adoption in Malaysia using Technology Acceptance Model (TAM), Theory of Planned Behavior (TPB) and intrinsic motivation. The Journal of Internet Banking and Commerce, 16(2), 1-27.

- Lin, J. S. C., & Chang, H. C. (2011). The role of technology readiness in self-service technology acceptance. Managing Service Quality: An International Journal, 21(4), 424–444. doi:10.1108/09604521111146289

- Lujja, S., Mohammad, M. O., Hassan, R. B., & Oseni, U. A. (2016). The feasibility of adopting islamic banking system under the existing laws in uganda. International Journal of Islamic and Middle Eastern Finance and Management, 9(3), 417-434.

- Mahmoud, L., Mohamed, O., & Abduh, M. (2014). The role of awareness in Islamic bank patronizing behavior of mauritanian: An application of TRA. Journal of Islamic Finance, 3(2), 030–038. doi:10.12816/0025103

- Mansour, I. H. F., Eljelly, A. M., & Abdullah, A. M. (2016). Consumers’ attitude towards e-banking services in Islamic banks: The case of Sudan. Review of International Business and Strategy, 26(2), 244–260. doi:10.1108/RIBS-02-2014-0024

- Masood, O., Abdullah, M., Shahimi, S., & Ismail, A. G. (2011). Operational risk in Islamic banks: Examination of issues. Qualitative Research in Financial Markets, 3(2), 131–151. doi:10.1108/17554171111155366

- Nawaz, T., & Haniffa, R. (2017). Determinants of financial performance of Islamic banks: AnIntellectual capital perspective. Journal of Islamic Accounting and Business Research, 8(2), 130–142. doi:10.1108/JIABR-06-2016-0071

- Al- Jabari, M. A., Othman, S. N., & Nik Mat, N. K. (2012, June). Actual online shopping behavior among Jordanian customers. American Journal of Economics, (125–129).

- Pedersen, P. E. (2005). Adoption of mobile internet services: An exploratory study of mobile commerce early adopters. Journal of Organizational Computing and Electronic Commerce, 15(3), 203–222. doi:10.1207/s15327744joce1503_2

- Rashid, M., Hassan, M. K., Umar, A., & Ahmad, F. (2009). Quality perception of the customers towards domestic Islamic banks in Bangladesh. Journal of Islamic Economics, Banking and Finance, 5(1), 109–131.

- Rauch, A., & Hulsink, W. (2015). Putting entrepreneurship education where the intention to act lies: An investigation into the impact of entrepreneurship education on entrepreneurial behavior. Academy of Management Learning & Education, 14(2), 187–204. doi:10.5465/amle.2012.0293

- Ringim, K. J. (2014). Perception of Nigerian Muslim account holders in conventional banks toward Islamic banking products. International Journal of Islamic and Middle Eastern Finance and Management, 7(3), 288–305. doi:10.1108/IMEFM-04-2013-0045

- Ringle, C. M., Wende, S., & Becker, J.-M. (2015). Smartpls 3. Boenningstedt: SmartPLS GmbH. Retrieved from http://www.smartpls.com.

- Rogers, E. M. (1995). Lessons for guidelines from the diffusion of innovations. Joint Commission Journal on Quality And Patient Safety, 21(7), 324-328.

- Saleh, M. S., Md, Mohamad, R. M. R., & Nani, N. K. (2013). Bank selection criterion in a customers’ perspective. Journal of Business and Management, 7(6), 15–20.

- Salman, A., Nawaz, H., Bukhari, S. M. H., & Baker, A. (2018). Growth analysis of Islamic banking in Pakistan: A qualitative approach. Academy of Accounting and Financial Studies Journal, 22, 1–8.

- Shih, Y. Y., & Fang, K. (2004). The use of a decomposed theory of planned behavior to study Internet banking in Taiwan. Internet Research, 14(3), 213–223. doi:10.1108/10662240410542643

- Siddique, M. N. (2012). Bank selection influencing factors: A study on customer preferences with reference to Rajshahi city. Asian Business Review, 1(1), 80–87. doi:10.18034/abr.v1i1.147

- Souiden, N., & Rani, M. (2015). Consumer attitudes and purchase intentions toward Islamic banks: The influence of religiosity. International Journal of Bank Marketing, 33(2), 143–161. doi:10.1108/IJBM-10-2013-0115

- Tarkiainen, A., & Sundqvist, S. (2005). Subjective norms, attitudes and intentions of Finnish consumers in buying organic food. British Food Journal, 107(11), 808–822. doi:10.1108/00070700510629760

- Taylor, S., & Todd, P. A. (1995). Understanding information technology usage: A test of competing models. Information Systems Research, 6(2), 144–176. doi:10.1287/isre.6.2.144

- Thambiah, S., Eze, U. C., Santhapparaj, A. J., & Arumugam, K. (2010). Customers’ perception on Islamic retail banking: A comparative analysis between the urban and rural regions of Malaysia. International Journal of Business and Management, 6(1), 187. doi:10.5539/ijbm.v6n1p187

- Triandis, H. C. (1980). Reflections on trends in cross-cultural research. Journal of Cross-Cultural Psychology, 11(1), 35–58. doi:10.1177/0022022180111003

- Venkatesh, V., Morris, M. G., Davis, G. B., & Davis, F. D. (2003). User acceptance of information technology: Toward a unified view. MIS Quarterly, 27, 425–478. doi:10.2307/30036540

- Wulandari, P., Putri, N. I. S., Kassim, S., & Sulung, L. A. (2016). Contract agreement model for murabahah financing in Indonesia Islamic banking. International Journal of Islamic and Middle Eastern Finance and Management, 9(2), 190–204. doi:10.1108/IMEFM-01-2015-0001

- Yap, S. F., & Noor, A. (2008). An extended model of theory of planned behaviour in predicting exercise intention. International Business Research, 1(4), 108–122.

- Yavas, U., Babakus, E., & Ashill, N. J. (2006). What do consumers look for in a bank? An empirical study. Journal of Retail Banking Services, 216-222.

- Young, E. (2016). World Islamic banking competitiveness report 2016. New Realities New Opportunities.