?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The Regional Governments’ Financial Statements in Indonesia that have obtained unqualified opinions had increased in recent years. However, the audit findings on the local government’s financial reports have also increased. Those conditions have motivated us to empirically analyze the factors that influence the increasing number of audit findings in district governments in Indonesia for the 2016 and 2017 fiscal years. The independent variables are the Size of the Regional Government, Local Income, Capital Expenditures, and Follow-Up of Audit Recommendations. We measure their influence on the Non-Compliance with Regulations using the Weaknesses of the Internal Control System as the moderating variable. Our results show that Size has a positive impact on the Internal Control System. Otherwise, the Completion of Audit Recommendation negatively affects both the Internal Control System and the Non-Compliance with Regulatory. The other independent variables of Local Income and Capital Expenditures did not show any influence on the number of audit findings. Simultaneously, Size, Local Income, Capital Expenditures, and Follow-Up of Audit Recommendation have an indirect relationship to Non-Compliance with Regulation findings through Internal Control System Weaknesses. Our research emphasizes the importance of developing a comprehensive internal control system for local governments, along with the improvement of asset governance. Moreover, we also encourage the completion of audit recommendations on local governments to avoid the reoccurrence of similar findings.

PUBLIC INTEREST STATEMENT

A fairly presented financial report, which is marked by an unqualified opinion, should contain fewer audit findings in its report. However, the number of audit findings in local governments in Indonesia tends to increase even though the overall acquisition of unqualified opinion in local governments also increases. This anomaly analyzed by testing the factors that are preassumed to affect the number of audit findings consisting of Size, Local Income, Capital Expenditure, and Completion of Audit Recommendation. The audit findings grouped into two categories namely The Weaknesses in The Internal Control System and Non-compliance with Regulations. Our research finds that the bigger the local governments’ asset size may cause greater audit findings. Contrary, the higher Completion of Audit Recommendations would result in fewer audit findings.

1. Introduction

Political and economic reforms in Indonesia were triggered by the 1998 global financial crisis, which manifested in the form of decentralization and government financial reform. Robust theories of economics and political science claim that decentralization would promote efficiency and accountability by forcing stronger pressures from both the demand and supply side (Yilmaz, Beris, & Serrano-Berthet, Citation2010). However, decentralization does not necessarily guarantee a better outcome, since the existence of some factors such as waste, corruption, and inefficiency, hence it depends on the presence of a regulatory framework that assures the operations of local governments are on the right track and the existence of accountability from regional officials (Baltaci & Yilmaz, Citation2006).

Decentralization in Indonesia embodied in the form of regional autonomy by devolving some central government authority to the regional government. Meanwhile, the accounting reform began with the enactment of the state financial package laws since 2003 through the implementation of the cash towards accrual accounting system, proceeded by the implementation of the full accrual accounting since the 2015 fiscal year. The implementation of the actual accounting system in government in Indonesia considered being successful due to a mandatory approach with detailed, rigid and inflexible applications of accounting regulations that foster government transparency and accountability (Pamungkas, Citation2018a).

Although the implementation of regional government accountability in Indonesia has shown progress with the number of unqualified audit opinion that continues to increase in recent years, however, the problems over the budget execution and financial activities of local governments seem not to improve along with the increasing number of audit findings. The above condition motivates us to investigate what factors influence the number of audit findings in the hope of contributing to local governments’ improvements and oversight of those factors.

2. Research background

In general, the public sector categorized into four layers, namely central government, local government, government-owned public entities, and public business entities joint funded with private capital (Sargiacomo & Gomes, Citation2010). In Indonesia, the local governments consist of two layers of provincial governments in the first tier and the district or municipal governments in the second tier (Pamungkas, Ibtida, Avrian, & Ntim, Citation2018). Since the adoption of accrual accounting for Indonesia local governments in 2015, the development of unqualified opinion for local governments has increased from 312 or 58% in the 2015 reporting year to 411 or 76% in the 2017 reporting year, as presented in Table .

Table 1. The development of audit opinion and audit findings on local governments in Indonesian during the 2015 to 2017 financial years

Although the percentages of unqualified opinions on the local governments’ financial statements have continually increased, the non-compliance findings, either in terms of the number of findings and the value of findings, instead continue to increase. The escalation number of compliance findings from 2015 with 6,150 cases valued at Rp2,522,796.00 million, increased to 6,558 cases with a total value of Rp2,544,963.84 million in 2017 (Table ). A similar condition also happened for the number of cases of weaknesses in the internal control system findings which, although declining from 2015 to 2016, have increased again in the 2017 fiscal year. Furthermore, analyses on The Indonesian’s Supreme Audit Board’s (BPK) semester reports for the last three years also shows that the number of regional losses cases also continued to increase in the last three reporting years, from 2,407 cases worth of Rp1,174,893.36 million in the 2015 fiscal year to 2,903 cases worth of Rp1,540,604.52 million in the 2017 fiscal year, as shown in Table .

Table 2. The number of cases of noncompliance finding on regional losses on financial audit of local governments in Indonesian during the 2015 to 2017 financial years

Furthermore, the results of monitoring of state/regional compensation settlement (BPK, Citation2018) shows that state/regional losses cases that have been legally verdict up to mid-2018 are Rp2.68 trillion, which dominated by the losses at the regional government level by 70.1% compared to losses at the central government of 24.7%. The problem of fraud or violations of the regulation that results in financial losses to local governments generally caused by the shortage of received services or goods by 36%, inappropriate spending by 22%, and miscellaneous wealth losses problems by 25%. Furthermore, the BPK audit results stated that those problems generally caused by the lack of responsibilities within government officials related to projects expenditure and treasury due to inadequate control of budget execution and disobedience to regulations (Supreme Audit Board of the Republic of Indonesia [Badan Pemeriksa Keuangan (BPK) Republik Indonesia], Citation2018).

This phenomenon of the increasing number of findings has interest us to do further research, considering the previous research by Pamungkas, Ibtida, Avrian, & Ntim (Citation2018) revealed that the awarding of audit opinions on local governments’ financial statements in Indonesia were determined by non-conformance with the Government Accounting Standard (GAS) and non-compliance with the regulations which result in regional losses. Therefore, this study attempts to identify empirically on factors that influence the findings of non-compliance with regulations moderated by the findings of internal control systems weakness.

Several studies have investigated factors influencing the audit findings, whether it is internal control system or the compliance to regulations using local governments characteristics such as size, complexity, economic growth rates, local incomes, capital expenditures, and the local population (Kristanto, Citation2009; Astriani, Citation2014; Mahmud, Hartono & Utaminingsih, Citation2014; Nuraeni, Citation2014; Putri & Makhmud, Citation2015; Iqbal, Tanjung, & Supriono, Citation2017; Gamayuni, Citation2016; Pratiwi & Aryani, Citation2016; Purniasari, Citation2016;; Adha, Afiah, & Pratama, Citation2019), however their results are vary.

This study aims to obtain an empirical description of what factors affect the level of the internal control system and the compliance with authorities on the auditing results of financial statements at local governments in Indonesia. The phenomenon that occurs is the escalation of the number and value of compliance finding cases in regional governments of Indonesia, although simultaneously the overall quality of financial statements of local governments has increased by the number of unqualified audit opinions on regional governments from year to year. This study tries to reexamine several variables that have been tested by several previous studies for their effect on the quality of financial statements represented by the findings of the internal control system and non-compliance.

3. Theories

3.1. Underlying theories

The theories underlying this research is the agency theory that discusses the relationship between agents and principals and the internal control framework in which one of the objectives is the compliance to laws and regulations (Committee of Sponsoring Organizations of the Treadway Commission [COSO], Citation2013).

Agency theory discusses agency problems and the agency costs that incurred in a principal-agent relationship. Agency problems arise mainly due to differences in interests and motivation between the two parties and the asymmetric of information (Eisenhardt, Citation1989). When agency relationships occur, management tends to prioritize their interests in utilizing assets and carrying out the operations of the entity, possibly even ignoring their duties as agents, so that agency costs incurred to monitor the agents (Eisenhardt, Citation1989; Hay & Cordery, Citation2018).

Agency relationships not only present between capital owners and the management of a private company but also occur in the public sector (Hay & Cordery, Citation2018). Agency theory in the public sector may appear at various levels of the organization, both between the public and politicians (de Oliveira & Dan Filho, Citation2017) as well as within the internal of the executive itself, such as the higher government and lower government, or between government and partners (Dixit, Citation2002).

Dixit (Citation2002) revealed that agents have an advantage of the company’s information in presenting the achievement of their activities for their benefit in the accountability reports; therefore principals can choose to order an audit as a verification. Hay and Cordery (Citation2018) argue that audits in the public sector have functions related to agency theory and management control theory because the benefits of auditing can reduce agency costs. Furthermore, Jahera and Colbert (Citation1988) explain that one of the agency costs can be represented by the loss of wealth, which led by the management’s acts or decisions.

The weaknesses of the internal control system can trigger moral hazard behavior, which is one of the agency problems (Dixit, Citation2002), due to an opportunity for agents to prioritize benefits on their behalf above the principal’s interests. The moral hazard act it can be discovered in the non-compliance findings in the audit report. Compliance, which is one of the objectives of the internal control framework, is related to the obedience with laws and regulations that are subject to the entity (COSO, Citation2013). Huefner (Citation2011) states that inadequate monitoring would weaken the internal controls function, which results in a violation of regulations by providing an opportunity for fraud, abuse, and waste, and might proceed in losses or inefficiency in the use of the municipal resources.

Pamungkas (Citation2008) explains that the financial statements serve to present relevant information on the financial position at a particular date and an overall picture of an organization’s transactions during a particular period. Financial reporting, especially in the public sector, serves as a manifestation of accountability on the management of resources entrusted to public sector officials and to provide information for decision making (Wynne, Citation2003). An independent auditor is required to provide an adequate assurance through an opinion of the financial statement’s presentation (Pamungkas, Citation2018b).

Public sector auditing is a process of testing carried out in an objective and systematic manner by obtaining and examining audit evidence to ensure that the information presented or the conditions that occur are per governing criteria (Intosai, Citation2013a, 100). Auditing in the public sector is more related to agency theory and management control whereas the principal (citizens) demanding accountability of the public assets utilization to the official in charge on public sector entities (Hay & Cordery, Citation2018). Furthermore, public sector financial reports audits have broader objectives in general than in the private sector with the obligation to report the compliance with statutory on budgeting and accountability, and also examination on the internal controls’ effectiveness (Ånerud, Citation2007). Nevertheless, the primary purpose of public sector audits is to sustain accountability functions from those who responsible for the entity operations to the stakeholders (McCandless, Citation1993).

Public sector audits generally classified into three major types which are financial statements audits, compliance with regulations, and performance audits (Intosai, Citation2013a, 100). Similar within the private sector, the purpose of financial audit on public-sector in Indonesia is to provide opinions concerning the fairness of financial information presented in the financial reports with four classifications of audit opinions namely unqualified, qualified, adverse, and disclaimer opinion (Pamungkas, Ibtida, Avrian, & Ntim, Citation2018). In a financial audit, BPK also produced two reports which are internal control system evaluation of internal control systems and compliance with statutory which elaborating findings in both of those classifications aside from the audit opinion report (Nuraeni, Citation2014; Pamungkas,Ibtida, Avrian, & Ntim, Citation2018).

Before submitting to the legislative, BPK has the authority to audit the financial reports of both the central and local governments and produce the audit reports of the financial report (Government of Indonesia, Citation2003). Audits in the public sector have a critical function in monitoring, assuring, and assessing public sector accountability (Pamungkas,Ibtida, Avrian, & Ntim, Citation2018). In Indonesia, the audit standard refers to the State Financial Audit Standards issued by the BPK. The State Financial Auditing Standard (BPK, Citation2017a) explains that the audit opinion of government financial audit formulated by the criteria of confirmation with accounting standards, adequacy of disclosure, compliance with statutory regulations, and effectiveness of internal control system.

The audit findings are essential factors to measure the quality of financial statements; therefore, a better financial statement should contain fewer problems either in the number of findings or the value. The types of audit findings on the government financial statement audit in Indonesia grouped into two categories, namely the internal control system findings and the findings of compliance with authorities.

3.2. Internal control system

Internal control is a process involving the executive and the employees within an entity made to deliver reasonable assurance of the effectiveness and efficiency of the operations, reliability of financial reporting, and compliance with laws and regulations (COSO, Citation2013). Pathak (Citation2005) describes Internal controls as the instrumentation in forms of standards, policies, procedures, and rules utilized by the organization’s management to carry the vision, mission, strategy, and purpose throughout the organization. In relation with the financial reporting process, the internal control is systematically implemented to provide reasonable assurance for the stakeholders on the reliability of financial statements and the financial reporting presentment in conformation with the accounting standards (D’Aquila, Citation1998; Arens, Randal, & Beasley, Citation2008,; Mahaputra & Putra, Citation2014). Thus, the internal control system is meant to implement throughout the company operations, not only for temporary policy (Aziz, Rahman, Alam, & Said, Citation2015).

The roles of internal control in the public sector are to sustain the established organizational system while simultaneously maintain the accountability of the decision-makers (Bianchi, Citation2010). A systematic and adequate internal control in government is needed not only to provide reasonable assurance to the stakeholders, yet also useful for the government officials to protect accusations of fraud and collusion within the public sector (Aziz et al., Citation2015) also as an effective mechanism in handling threats (Pathak, Citation2005). Furthermore, Huefner (Citation2011) explains that decent internal control would promote the efficiency of the municipality’s financial resources utilization by allowing better service delivery to the society and minimalized the use of local taxes. Baltaci and Yilmaz (Citation2006) argue that internal control and audit are primary factors of the implementation of public financial management (PFM) systems for enhancing efficiency and effectiveness, particularly in local government operations through accounting controls, administrative controls, and management controls.

The development of an internal control system in the public sector and non-profit organization is crucial to maintaining and enhancing accountability (Aziz et al., Citation2015). The implementation of proper internal control ensured through monitoring and supervision, especially by the internal auditors. Moreover, Jones and Beattie (Citation2015) explain that the internal auditing is a monitoring tool meant to improve the effectiveness of internal controls within the organizations with primary concerns are to identify areas in risk and to establish a mechanism in controlling and minimalizing those risks. Furthermore, Badara and Saidin (Citation2013) argue that an effective internal control system at a local level would promote the internal auditor’s effectiveness.

Conversely, inadequate monitoring would weaken the internal controls function, which results in providing an opportunity for fraud, abuse, and waste, and might proceed in losses or inefficiency in the use of the municipal resources, hence increases costs to the taxpayers (Huefner, Citation2011). Furthermore, Ge and McVay (Citation2005) argue that earnings management and opportunistic behavior will emerge in a weak internal control environment, which eventually reduces financial reporting reliability. Thus, failing to build a reliable and sound internal control system could threaten the public sector organization, thus jeopardizing the effort of maintaining accountability (Aziz et al., Citation2015). However, Baltaci and Yilmaz (Citation2006) argue that internal control and audit at the local level are still scarce, especially in developing countries, since the reformation process is still focusing on increasing capacity and controlling mechanisms at the central government level.

Griggs (Citation2004) and Dye (Citation2007) emphasize the importance of the understanding the ICS for an external auditor through examining and evaluating the effectivity of the internal control design and identifying organization-level controls to be able to give proper opinion on the effectiveness of internal control in the financial reporting system and also required to report any material deficiencies of the internal control. In Indonesia, BPK must evaluate the internal control system to provide adequate assurance of the fairness of the financial statements in performing financial audits (Pamungkas, Ibtida, Avrian, & Ntim, Citation2018). BPK (Citation2017b) classified the material findings of the ICS deficiencies as weaknesses of the accounting and reporting control system, weakness of control system of revenue and expenditure budget realization, and weakness of internal control structure.

3.3. Compliance with authorities

Compliance auditing is an independent examination on a particular matter performed by assessing whether material operations, financial transactions and information satisfy with the statutory and procedures, identified as the criteria, which rule the entity (Intosai, Citation2013b, 400). Unlike audits in the public sector, compliance audits in the public sector have a crucial function in ensuring that the organization’s operations have been carried out under related regulations due to legal liability. BPK (Citation2017b) explains that any fraud or violation of the law, particularly the audit findings of the state/regional losses, the potency of state/regional losses, or revenue shortfall, most likely to be reported to the law enforcement.

The objective of public-sector compliance auditing is to assess whether the operations of public-sector entities are following the procedures and statutory which regulate those entities (Intosai, Citation2013b, 400). Aside from the internal control evaluation in acquiring adequate assurance of the fairness of the financial statements, BPK must also examine whether governments’ activities have been complying with statutory related to government financial reporting in Indonesia (Pamungkas, Ibtida, Avrian, & Ntim, Citation2018). Not only attached to financial audits, but compliance audits can also be a separate independent audit on a regular or ad hoc basis related to a particular subject matter (Intosai, Citation2013b, 400).

BPK (Citation2014) classifies the findings of non-compliance with regulations in six categories namely non-compliance which causing regional/state losses, the potency of regional/state losses, revenue shortfall, administration findings, inefficiency, and ineffectiveness. In the financial statement audit, a compliance audit report is an optional report, which must be published only if any of the non-compliance findings appeared within the financial audit process (Pamungkas, Ibtida, Avrian, & Ntim, Citation2018).

4. Empirical literature review and hypotheses development

4.1. Prior studies

Numerous studies were conducted to analyze the factors influencing the audit findings on public sectors or government agencies using various variables. Nuraeni (Citation2014) conducted a study of the influence of regional government characteristics in Indonesia on audit quality, by using size, dependency levels, welfare levels, local government type, and the Finance and Development Supervisory Agency’s (BPKP) assistance as regional characteristics variables, with audit findings classification and audit opinions as the audit quality variables. The result is that the population number shows a positive impact on audit quality in the form of non-compliance findings, yet finding no correlation between local government characteristics with weaknesses of internal control. Doyle, Ge, and McVay (Citation2007) explain that deficiencies in internal control over financial reporting frequently more appear in smaller, younger and less financially firms, otherwise similar weaknesses were less existing in financially healthier firms with complicated, diverse, and rapid changing operations.

Rich and Zhang (Citation2014) show that fewer internal control issues appear in municipalities with audit committees, which indicate that those municipals would have less risk in financial reporting failures. Icerman and Hillison (Citation1990) examine the relationship of the internal controls with the accounting errors and irregularities, they found that larger companies generally have stronger internal control systems; thus less number of errors appeared in firms with stronger internal control systems than the weaker firms. Furthermore, Petrovits, Shakespeare, & Shih (Citation2010, January) study on nonprofit organizations shows that the possibility of internal control problems rises in low financial health, growing, more complex, or smaller organizations.

Adha et al. (Citation2019) examined the effect of entity’s size (asset and budget) and complexity on the weaknesses of the internal control system at the Ministry of Public Works and Public Housing of Indonesia. Their results indicate that assets have a negative impact on the internal control system’s weaknesses, while budget and complexity show a positive effect on the internal control system’s weaknesses. Afiah and Azwari (Citation2015) research on the Governments of South Sumatra shows that the implementation of an internal control system affects the quality of local governments’ financial reporting, then through quality financial reporting, the internal control system has a better, significant and positive impact on good governance.

Iqbal, Tanjung, & Supriono (Citation2017) examines several factors related to their influences to weaknesses of internal control in local governments of Riau and West Sumatera Province, with the results that economic growth rates, local incomes, size, and the population do have relation to the internal control weaknesses, but not so for capital expenditure. Similar to that research, Purniasari (Citation2016) also uses the same variables with samples of local governments in Central Java Province, thus found that only economic growth rates have effects on internal control deficiencies. While Kristanto’s (Citation2009) study argues that Size, PAD, and capital expenditures are simultaneously influencing internal control weaknesses significantly; however, his partial test only shows a significant correlation of variable Size. Mahmud, Hartono, & Utaminingsih, (Citation2014) added local government complexity alongside Economic Growth, Size, and PAD with the results that only PAD which did not show a significant effect, while Size and Economic Growth show negative correlations. While using similar variables as Mahmud, Hartonoand, & Utaminingsih, (Citation2014) research, Putri and Makhmud (Citation2015) only found a negative correlation between Size and internal control weaknesses.

Several studies also have been conducted regarding the audit opinion of local governments’ financial reports and performances. Pratiwi and Aryani (Citation2016) argue that local government size, financial dependency, assets, capital expenditures, follow-up of audit findings, and local leader characteristics were likely to influence audit opinion. Gamayuni (Citation2016) examine the effect of local government characteristics (with the size of assets and expenditures as proxies) and the audit result (audit findings and opinions) on the economic growth of Regional Governments in Lampung, with Financial Performances (effectiveness, efficiency, and autonomy ratio) as Intervening Variable. Her research only found the effect of government characteristics on financial performance in the form of effectiveness ratio; however, the audit results have no effect on financial performance as well as no relationship between the financial performances and economic growth. Astriani (Citation2014) argues that the level of completion of audit findings with the quality of financial statements has a robust relationship.

Concerning Indonesian Subnational Governments’ capital expenditures, Lewis and Oosterman (Citation2011) explain that a significant portion of capital expenditures in local governments tended to invested in unproductive assets such as administrative office buildings; hence it must be focused more on the provision of assets that are more beneficial to communities. Moreover, they explain that local governments of Indonesia have not optimized the proportion of their funding resources from loans or cash reserves to fund capital acquisitions since their issue is not on the finance, but also regulatory stiffness of budgeting and weaknesses of planning and implementation.

4.2. Hypotheses development

Based on a review of the underlying theories, an audit of local government related to agency theory beneficial to provide reasonable assurance of the reliability and fairness of the government’s financial statements which embody the accountability of agents to the principal. Foregone wealth is considered to be one of the forms of agency cost (Jahera & Colbert, Citation1988). To minimizing a disadvantageous act of management, it is necessary to conduct an audit in which some of the objectives are to capture the company’s decisions or activities that were detrimental to the entity and also to identify weaknesses in internal control. A weak internal control system allows management to exploit this gap for their benefit above the principal’s interests; this would generate non-compliance, which can result in wealth losses or potential losses.

Previous studies have shown factors that influence the number of audit findings in the public sector, especially in regional government, but their results still vary. The larger the amounts of assets, revenues, and expenditures will require a better and more sophisticated internal control system to ensure that government officials work for the best interests of their stakeholders. Also, the number of completions to audit recommendations shows the level of management’s commitment to overcoming weaknesses or noncompliance that occur in the local government’s activities.

Based on the review on the theories and previous researches, we develop several hypotheses to determine whether Size of the District Governments (Size), Local Incomes (PAD), Capital Expenditures (BM) and Follow-Up of Audit Results (TLHP) have affected the occurrence of the non-compliance with the Laws and Regulations (KP) and the internal control system weaknesses (KSPI) findings. Those operational variables explained in Tableel . Thus, the development of the hypotheses as follows:

The first hypothesis (H1): The Size has a significant direct effect on KSPI.

The second hypothesis (H2): The PAD has a significant direct effect on KSPI.

The third hypothesis (H3): The BM has a significant direct effect on KSPI.

The fourth hypothesis (H4): The level of completion of the TLHP has a significant direct effect on KSPI.

The fifth hypothesis (H5): The level of completion of TLHP has a significant direct effect on KP.

The sixth hypothesis (H6): The KSPI has a significant direct effect on KP.

The seventh hypothesis (H7): The Size, PAD, BM, and TLHP have an indirect relationship to KP moderated through KSPI.

Table 3. Operational variabel

5. Research design

5.1. Population and sampling techniques

Our study focused on District Governments in Indonesia as the samples of local governments, due to the uniformity of district governments’ operational and organizational characteristics, with consideration to gain a better validity of results from this study. Using a quantitative research method, we use secondary data obtained from the Audit Results Summary of first Semester Year 2017 and 2018 (BPK, Citation2017b, Citation2018) and the Audit Report of each District Governments Financial Statements for 2016 and 2017 financial years.

The population of this study includes all districts in Indonesia consisting of 416 districts in the 2017 and 2016 financial years. This research only tests local governments at the district level due to the uniformity of their operational and organizational characteristics, with consideration to gain a better validity of results from this study. Furthermore, the district population used as a basis for determining the minimum number of samples using Slovin formula as follows:

n: Number of Samples

N: Number of Population

e: Margin of error

Based on the Slovin formula, with a margin of error of 5%, the minimum samples to represent the population are 135 districts at minimum or 270 samples for two financial years. Furthermore, seven districts excluded due to incomplete data since they were late in submitting financial reports to the BPK. Therefore, by excluding those districts, the samples of this study are years or 818 samples for two financial, which has met the minimum sample according to the Slovin formula.

5.2. Definition of operational variables

The independent variables used in this study include (a) Size of the Local Government (Size), (b) Local Income (PAD), (c) Capital Expenditure (BM) and (d) Follow-Up on Audit Results (TLHP). While the moderating variable is the weakness of the internal control system (KSPI) and the dependent variable is the Non-compliance with Laws and Regulations. This study uses secondary data obtained from the Audit Results Summary for Semester I Year 2017 and 2018 (Supreme Audit Board of the Republic of Indonesia [Badan Pemeriksa Keuangan (BPK) Republik Indonesia], Citation2017b, and Citation2018) and the Audit Report of each District Governments Financial Statements for 2016 and 2017 financial years.

Size is the value of district governments’ total assets as of 31 December 2016 and 2017, while PAD is the total realized districts’ genuine income and BM is the realization of districts’ total capital expenditures both during 2016 and 2017 financial years. Meanwhile, the TLHP is the percentage of completion of the corrective actions of the audit results by the District Governments compared to the number of recommendations. Furthermore, KSPI and KP, respectively are the numbers of cases from the findings of the internal control system weaknesses and the non-compliances to the laws and regulations, based on the Audit Reports on the District Government Financial Reports.

5.3. Data analysis technique

The research model developed in this study is a path analysis with one mediator. Ghozali (Citation2005) explains that path analysis is the development of a regression model that is useful to test the congruence of the correlation matrix with two or more models compared in a study.

Amos version 24 is used to perform path analyses. The analytical method used is Generalized Least Square (GLS) by considering the number of tested samples. According to Waluyo (Citation2016), the estimation technique used for samples larger than 200 is GLS. Thus, the equation in this study is:

Based on the above equations, we applied data transformation in the form of Ln for the independent variables and the Sqrt form for both the moderating and the dependent variables. Transformation conducted so that the tested data can meet the assumption of normality.

6. Empirical results and discussion

6.1. Descriptive statistics

Table shows that the PAD variable has the highest standard deviation of 1.17162 with a mean of 25.345, while Size, BM and TLHP have standard deviations below 1.0 with a mean of 28.413, 27.760 and 0.6977, respectively. Dependent and Moderating Variables which are the KP and KSPI, both have statistical means less than 3.26 and standard deviations below 0.8.

6.2. Model fit assessment

The goodness of Fit measures the suitability of the observational or the actual inputs (matrices of covariances or correlations) with predictions from the proposed models. The result of the evaluation of the index of goodness of fit in this study considered to have been fit, thus the hypotheses testing can describe the actual situation as presented in Table .

Table 4. Descriptive statistics

6.3. Hypotheses test

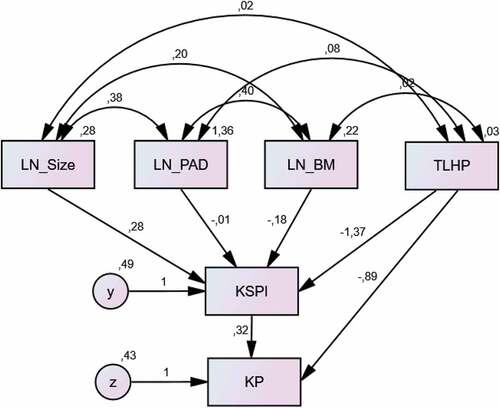

To understand the relationship pattern of the six variables which has specified in earlier chapters, we perform a statistical test on each hypothesis. The hypotheses are analyzed using path analysis to test the effect of each independent variable on the dependent variable simultaneously. From the results of data processing with path analysis as in Figure which shows the coefficient of each variable against other variables. The analyses of the hypotheses use a model evaluation in the form of squared multiple correlations for the dependent variable and the value of the Standardized Regression Weights Coefficient for the independent variables, which are then assessed by their significance value C.R (t count) for each path.

Figure 1. Results of data processing with path analysis.

Data of variables Size, PAD, and BM are transformed in the form of Ln to produce normal data distribution, whereas the TLHP variable not transformed to Ln since the data is already in the form of ratios. The results of The Goodness of Fit and The Research Hypothesis test are shown in Table and Tabel 6, respectively.

Table 5. The goodness of fit result

Table 6. Standardized regression weights, C.R dan P-value

The first hypothesis in this study is that the Size of the District Governments has a significant direct effect on the KSPI. Based on the test results it is known that the path between Size and KSPI has a beta coefficient of 0.200 and CR of 3.565 with a p-value of ≤ 0.05; thus it can be concluded that statistically, the Size has a significant effect with a positive correlation to KSPI.

The test results show that the path between PAD and KSPI has a negative beta coefficient of 0.021 and a CR of negative 0.422 with a p-value > 0.05, while the path between BM and KSPI has a negative beta coefficient of 0.117 and a CR of negative 1.814 with a p-value > 0.05. Hence, statistically, neither PAD and BM have a significant effect on KSPI. Consequently, both the second and third hypotheses are rejected.

The fourth and fifth hypotheses are that the level of TLHP completion directly has a significant effect on KSPI and KP, respectively. Based on the test results it is known that the path between TLHP and KSPI has a negative beta coefficient of 0.314 and a CR of negative 8.751 with a p-value ≤ 0.05, while the path between TLHP and KP has a negative beta coefficient of 0.209 and a CR of negative 6.270 with a p-value ≤ 0.05. Thus, those results statistically show that TLHP has a significant effect relationship with a negative direction toward either KSPI and KP.

The sixth hypothesis is that KSPI has a significant direct effect on KP. Based on the test results it is known that the path between KSPI and KP has a beta coefficient of 0.323 and a CR of 9.701 with a p-value ≤ 0.05, so statistically, TLHP has a significant effect with a positive correlation to KP.

The seventh hypothesis proposed in this study is the indirect relationship between overall Size, PAD, BM, and TLHP variables on KP moderated through KSPI. Based on the model shown in Figure and the results of the standardized indirect effect analysis, it shows that the indirect effect of Size on the KP, through KSPI, is 0.065 or 6.5%. The indirect effect of PAD on KP, through KSPI, is negative 0.07 or 7%, while the indirect effect of BM on KP is 0.038 or 3.8%. Furthermore, the indirect effect of the level of TLHP settlement with KP through KSPI was negative 0.102 or negative 10.2%. Therefore, those results support the seventh hypothesis.

6.4. Analysis and interpretation of results

Based on statistical testing, the results of the study include the size of the local government has a positive influence on KSPI. These results are not in line with researches conducted by Purniasari (Citation2016) who did not find a relationship between Size and KSPI or with Mahmud, Hartono, & Utaminingsih (Citation2014) and Putri and Makhmud (Citation2015) who discovered the relationship between the two variables but in the opposite direction. However, this result corresponded with Kristanto (Citation2009) dan Iqbal, Tanjung, and Supriono (Citation2017).

As explained in the earlier chapter, the Size in this study is the value of district governments’ assets, while KSPI is the number of cases of weaknesses in the internal control system found by BPK auditors. Considering the probability of audit findings occurrence, the larger the assets size of the regional government as objects of BPK’s audit, the higher the possibility of cases of weaknesses in the internal control system found by BPK auditors.

Meanwhile, both the PAD and BM do not have a significant influence on the weakness of the KSPI. These results support research conducted by Kristanto (Citation2009), Hartono, Mahmud, and Utaminingsih (2014), and Purniasari (Citation2016), but contrarily with Iqbal, Tanjung, & Supriono(2017) in the matter of PAD. Those results show that regional government that has high PAD and realized high capital expenditure does not necessarily have a better internal control system than LGs with low PAD and capital expenditure. Furthermore, the level of completion of the BPK’s previous audit results (TLHP) had a negative influence both on the KSPI and KP. These results support research conducted by Astriani (Citation2014) which states that the higher the completion of audit findings will have an impact on decreasing the number of findings. District governments that follow up on recommendations from the results of the previous year’s audit tend to have better internal control systems.

The test result between the moderating and dependent variables shows that the KSPI has a significant positive relationship with KP. This result supports the notion that governments that have inadequate internal control systems tend to not comply with statutory provisions. Furthermore, the internal control system is designed to prevent abuse or misappropriation. Thus, a sound internal control system expected to minimize fraud. Meanwhile, simultaneously, Size, PAD, BM, and TLHP variables have an indirect relationship with non-compliance with legislation variable through the weaknesses in the Internal Control System.

Based on the partial hypotheses test results, in relation to regional characteristics, only the size of the regional government (size) has a positive influence on the weakness of the internal control system (KSPI) while PAD and Capital Expenditures (BM) do not have an influence on the weakness of the internal control system (KSPI). Previous studies argued that internal control weaknesses tend to occur in smaller private sector firms (Doyle et al., Citation2007) or nonprofit organizations (Petrovits, Shakespeare, & Shih, Citation2010, January). However, this does not to be the case in Indonesian District Governments. This can be caused to the higher the value of government assets, the greater complexity of supervision and security needed on the assets utilization, thus it may also be related to the low capacity of district government apparatus, both in terms of quality and quantity, that affect the occurrence of the internal control and noncompliance cases. Furthermore, related to the absence of influence of Local Incomes and Capital Expenditures to Internal Control Deficiency, possibly because of the small composition of PAD compared to district governments funds from the central government as well as the small proportion of capital expenditures in district governments compared to their total expenditures.

The level of completion of the BPK’s audit results in the previous period (TLHP) shows a negative effect on the weakness of the internal control system (KSPI) and non-compliance with the statutory regulations (KP) findings. These results explain the necessity for district governments to settle any prior audit recommendations to prevent the reoccurrence of similar findings. Rich and Zhang (Citation2014) assert the importance of audit committees, which argue that fewer internal control issues appear in municipalities with audit committees since one of the functions of such a committee is to scrutinize the government regarding corrective actions that have been taken following the audit recommendations.

Regarding the internal control system and the non-compliance with laws and regulations problems, the existence of a positive relationship between those two variables is very much understandable because one of the internal control functions is to support the fulfillment of the compliance with laws and regulations (Committee of Sponsoring Organizations of the Treadway Commission, Citation2013). On the contrary, a weak internal control function will provide an opportunity for the occurrence of fraud, abuse, and waste (Huefner, Citation2011) as well as earnings management and opportunistic behavior (Ge & McVay, Citation2005). Furthermore, the simultaneous indirect relationship of Size, PAD, BM, and TLHP variables on KP through KSPI shows the importance of those factors to be managed and appropriately resolved to avoid audit findings.

7. Summary and conclusion

This study intended to obtain empirical evidence of factors affecting the level of the Internal Control System Weaknesses and the Non-Compliance with Authority audit findings of local governments’ financial statements in Indonesia. The phenomenon that occurs is the continual increase either in the number or value of findings of local governments’ financial audit report, albeit the improvement of the overall local governments’ financial statements shown by the increasing number of regional governments obtained unqualified opinions.

The underlying theories are weaknesses of the internal controls function that would result in the opportunity of noncompliance to regulations (Huefner, Citation2011) and the agency theories that state that one of the agency costs are indicated by the wealth losses (Jahera & Colbert, Citation1988). Moreover, compliance with laws and regulations is one of the objectives of internal control implementation (Committee of Sponsoring Organizations of the Treadway Commission, Citation2013). This study explores previous researches and works of literature to try to identify the factors that influence the number of non-compliance and weaknesses in the internal control findings. This study examines the effect of Size, PAD, BM, and TLHP variables on the findings of non-compliance with a moderating variable in the form of weaknesses in the internal control system, using a sample of district governments in Indonesia for the 2016 and 2017 fiscal years.

Our study finds that only the size of the regional government has a positive influence on the weakness of the internal control system. Otherwise, the level of completion of the BPK’s audit results in the previous period has a negative effect both on the weakness of the internal control system and non-compliance with the statutory regulations. Our findings are expected to encourage local governments to improve control and security over their assets and intensify the completion of audit recommendations to minimize the risk of reoccurrence of audit findings.

BPK’s Audit Results Summary for Semester I Year 2018 (Supreme Audit Board of the Republic of Indonesia [Badan Pemeriksa Keuangan (BPK) Republik Indonesia], Citation2018) revealed that up to mid-2018, from 119,670 recommendations worth Rp30.14 trillion on 542 local governments, only 54.9% of the follow-up had been completed in accordance to audit recommendations. Also, from 13 government organizations in Indonesia with incomplete recommendation status above 70%, 10 of them are district governments. Those conditions suggest that the local government has not been optimal in trying to resolve the audit problems that have occurred. That condition could lead to the recurrence of similar problems in the future and the less usefulness of audit results in encouraging improvements of the regional government.

This study recommends local governments to manage assets and utilize assets properly and make the best effort to resolve audit recommendations, both the weaknesses in the internal control system and the non-compliance with legislation to minimize the occurrence of findings. Also, local governments need to improve the quality of financial reports by developing and implementing adequate and comprehensive internal control systems. The limitation of this study is that we only analyze the characteristics of local government using secondary data in the form of the size, income, and expenditures, without examining managerial behavior factors of local government. Future in-depth studies are strongly recommended to be performed using government official character variables to test whether these variables affect internal control and compliance issues.

Additional information

Funding

Notes on contributors

Bambang Pamungkas

Bambang Pamungkas currently serves as a permanent lecturer at the Institute of Economic Science (STIE) Kesatuan, Bogor, Indonesia, and as an extraordinary lecturer at the University of Indonesia, University of Pakuan, and several universities in Jakarta. Graduated from the State Accounting Institute (STAN) and obtained M.B.A (accounting) from The Hull University, England. He then awarded Doctorate of Economic (Accounting) from Pajajaran University and recently promoted as Professor in Accounting in August 2019. Experiences in both the public and private sector accounting and auditing practices started from the Ministry of Finance, Finance and Development Supervisory Agency (BPKP), the Ministry of Home Affairs, apprenticeship in several accountant offices, roles in Tax Auditing of the Joint Team of BPKP and Directorate General of Taxation, member of the Audit Committee at Krakatau Steel. He is currently actively serving at the Supreme Audit Board (BPK) and board member of the Institute of Indonesia Chartered Accountants (IAI).

References

- Adha, A. F., Afiah, N. N., & Pratama, A. (2019). Pengaruh Ukuran Entitas dan Kompleksitas Terhadap Kelemahan Pengendalian Intern pada Kementerian PUPR [Effect of entity size and complexity on weaknesses in internal control at the ministry of public works and housing]. SIKAP, 3(2), 122–18.

- Afiah, N. N., & Azwari, P. C. (2015). The effect of the implementation of Government Internal Control System (GICS) on the quality of financial reporting of the local government and its impact on the principles of good governance. Procedia Social and Behavioral Sciences, 211, 811–818. doi:10.1016/j.sbspro.2015.11.172

- Ånerud, K. (2007). Harmonization of financial auditing standards in the public and private sectors – What are the differences? Accounting, Tax & Banking Collection, 34(4), 17.

- Arens, A. A., Randal, J. E., & Beasley, M. S. (2008). Auditing and assurance services (12th ed.). New Jerssey, NJ: Pearson International Edition.

- Astriani, D. (2014). Pengaruh Penyelesaian Temuan Audit Terhadap Kualitas Laporan Keuangan Pemerintah Daerah (Survei pada Badan Pengawasan Keuangan dan Pembangunan (BPKP) Perwakilan Provinsi Jawa Barat) [The effect of completion of audit findings on the quality of regional government financial statements (survey of the west java provincial representative of the financial and development supervisory agency (BPKP))]. Retrieved from https://repository.widyatama.ac.id/xmlui/handle/123456789/3069?show=full

- Aziz, M. A. A., Rahman, H. A., Alam, M. M., & Said, J. (2015). Enhancement of the accountability of public sectors through integrity system, internal control system and leadership practices: A review study. Procedia Economics and Finance, 28, 163–169. doi:10.1016/S2212-5671(15)01096-5

- Badara, M. S., & Saidin, S. Z. (2013). Impact of the effective internal control system on the internal audit effectiveness at local government level. Journal of Social and Development Sciences, 4(1), 16–23.

- Baltaci, M., & Yilmaz, S. (2006). Keeping an eye on subnational governments: Internal control and audit at local levels. Stock No. 37257. The International Bank for Reconstruction and Development/The World Bank.

- Bianchi, C. (2010). Improving performance and fostering accountability in the public sector through system dynamics modelling: From an “external” to an “internal” perspective. Systems Research and Behavioral Science, 27, 361–384. doi:10.1002/sres.v27:4

- Committee of Sponsoring Organizations of the Treadway Commission. (2013). Internal control-integrated framework. New York, NY: American Institute of Certified Public Accountants.

- D’Aquila, J. M. (1998). Is the control environment related to financial reporting decisions? Managerial Auditing Journal, 13(8), 472–478. doi:10.1108/02686909810236334

- de Oliveira, C. B., & Dan Filho, J. R. F. (2017). Agency problems in the public sector: The role of mediators between central administration of city hall and executive bodies. Brazilian Journal of Public Administration, 51(4), 596–615.

- Dixit, A. (2002). Incentives and organizations in the public sector: An interpretative review. Journal of Human Resources, 37, 696–727. doi: 10.2307/3069614

- Doyle, J., Ge, W., & McVay, S. (2007). Determinants of weaknesses in internal control over financial reporting. Journal of Accounting and Economics, 44, 193–223. doi:10.1016/j.jacceco.2006.10.003

- Dye, K. M. (2007, November–December). Corruption and fraud detection by public sector auditors. The EDP Audit, Control and Security. 36(5–6). 6. Accounting, Tax & Banking Collection.

- Eisenhardt, K. M. (1989). Agency theory: An assessment and review. The Academy of Management Review, 14(1), 57–74. doi:10.5465/amr.1989.4279003

- Gamayuni, R. R. (2016). The effect of local government characteristics and the examination result of Indonesian supreme audit institution on economic growth, with financial performance as intervening variable in district and city government of lampung province. Research Journal of Finance and Accounting, 7(18), 75–81.

- Ge, W., & McVay, S. (2005). The disclosure of material weaknesses in internal control after the Sarbanes–Oxley act. Accounting Horizons, 19(3), 137–158. doi:10.2308/acch.2005.19.3.137

- Ghozali, I. (2005). Model Persamaan Struktural - konsep dan aplikasi dengan program AMOS Ver 16.0. Badan Penerbit Universitas Diponegoro, Semarang.

- Government of Indonesia. (2003). Undang-Undang Keuangan Negara Nomor 17 Tahun 2003 [The state finance act no. 17/2003]. Jakarta: Author.

- Griggs, L. L. (2004, April). Audits of internal control over financial reporting: What do they mean? Insights, The Corporate & Securities Law Advisor, 18(4), 2. Research Library.

- Hay, D., & Cordery, C. (2018). The value of public sector audit: Literature and history. Journal of Accounting Literature, 40, 1–15. doi:10.1016/j.acclit.2017.11.001

- Huefner, R. (2011). The state of internal controls in local government: Evidence from town and village audits. The CPA Journal, LXXXI, 20–27.

- Icerman, R. C., & Hillison, W. A. (1990). Distributions of audit-detecfted errors partitioned by internal control. Journal of Accounting, Auditing & Finance, 5, 527–543. doi:10.1177/0148558X9000500405

- Intosai. (2013a). ISSAI 100 - Fundamental principles of public-sector auditing. Retrieved from http://www.issai.org/issai-framework/3-fundamental-auditing-priciples.htm

- Intosai. (2013b). ISSAI 400 - Fundamental principles of compliance auditing. Retrieved from http://www.issai.org/issai-framework/3-fundamental-auditing-priciples.htm

- Iqbal, M., Tanjung, A. R., & Supriono, S. (2017). Pengaruh Tingkat Pertumbuhan Ekonomi, Pendapatan Asli Daerah, Ukuran Pemerintah Daerah, Belanja Modal, dan Jumlah Penduduk terhadap Kelemahan Pengendalian Intern pada Pemerintah Daerah (Studi Empiris pada Kabupaten dan Kota Provinsi Riau dan Sumatera Barat [The influence of economic growth rate, local own revenue, size of local government, capital expenditures, and number of population on weaknesses of internal control in local government (Empirical study in the regencies and cities of Riau and West Sumatra provinces]. Jurnal Online Mahasiswa Fakultas Ekonomi Universitas Riau, 4(1), 881–895.

- Jahera, J. J., & Colbert, J. (1988). The role of the audit and agency theory. Journal of Applied Business Research, 4(2): 17–65. doi:10.19030/jabr.v4i2.6427

- Jones, G., & Beattie, C. (2015). Local government internal audit compliance. Australasian Accounting, Business and Finance Journal, 9(3), 59–71. doi:10.14453/aabfj

- Kristanto, S. B. (2009, Januari). Pengaruh Ukuran Pemerintahan, Pendapatan Asli Daerah (PAD), Dan Belanja Modal Sebagai Prediktor Kelemahan Pengendalian Internal [Effects of government size, local own revenue (PAD), and capital expenditures as predictors of weaknesses in internal control]. Jurnal Akuntansi UKRIDA, 9(1), 41–62.

- Lewis, B., & Oosterman, A. (2011). Sub-national government capital spending in indonesia: Level, structure, and financing. Public Administration and Development, 31(3), 149–158. doi:10.1002/pad.v31.3

- Mahaputra, I. P. U. R., & Putra, I. W. (2014). Analisis Faktor- Faktor Yang Memengaruhi Kualitas Informasi Pelaporan Keuangan Pemerintah Daerah [The analysis of factors affecting quality of information on local government financial reporting]. e-Journal Accountancy Udayana University, 8(2), 230–244.

- Mahmud, Hartono, R, & Utaminingsih, N. S. (2014). Faktor-faktor yang mempengaruhi kelemahan pengendalian intern pemerintah daerah [factors influencing the weaknesses of internal control of local governments]. Call of Paper in Simposium Nasional Akuntansi 17, Mataram.

- McCandless, H. E. (1993, April). Auditing to serve public accountability. International Journal of Government Auditing, 20(2), 14. Accounting, Tax & Banking Collection.

- Nuraeni. (2014). The impact of local governments characteristics to audit quality Indonesia perspectives. Finance and Banking Journal, 16(1), 87–103.

- Pamungkas, B. (2008). Akuntabilitas Instansi Pemerintah, Survei Pada Pemerintah Dati II DI Yogyakarta [Accountability of government agencies, survey on government region II of Yogyakarta]. Bogor: Kesatuan Press.

- Pamungkas, B. (2018a). Accrual-based accounting implementation in Indonesian’s local governments compared to other countries’ experiences. Man in India, 98(1), 1–23.

- Pamungkas, B. (2018b, Januari). Determinan penerapan basis akrual secara penuh pada pemerintah daerah [Determinants of the full implementation of accrual basis to local governments. Accounting journal]. Jurnal Akuntansi, XXII(01), 68–85.

- Pamungkas, B., Ibtida, R., Avrian, C., & Ntim, C. G. (2018). Factors influencing audit opinion of the Indonesian municipal governments’ financial statements. Cogent Business & Management, 5(1), 1540256. doi:10.1080/23311975.2018.1540256

- Pathak, J. (2005). Risk management, internal controls and organizational vulnerabilities. Managerial Auditing Journal, 20(6), 569–577. doi:10.1108/02686900510606065

- Petrovits, C, Shakespeare, C, & Shih, A. (2010, January). The causes and consequences of internal control problems in nonprofit organizations. The Accounting Review, 86(1), 325–357. doi: 10.2308/accr.00000012

- Pratiwi, R., & Aryani, Y. A. (2016). Pengaruh Karakteristik Pemerintah Daerah, Kepala Daerah, Tindak Lanjut Temuan Audit Terhadap Opini [Effect of regional governments characteristics, regional heads, follow-up audit findings on opinion]. Jurnal Akuntansi, 20(2), 167–189. doi:10.24912/ja.v20i2.52

- Purniasari, C. (2016). Analisis Faktor-Faktor Yang Mempengaruhi Kelemahan Pengendalian Internal Pemerintah Daerah (Studi Kasus pada Kabupaten dan Kota di Provinsi Jawa Tengah Tahun 2013–2014) [Analysis of Factors Affecting the Weaknesses of Local Government Internal Control (Case Studies in Regencies and Cities in Central Java Province 2013–2014)] (Doctoral dissertation). Universitas Muhammadiyah Surakarta.

- Putri, N. K., & Makhmud, A. (2015). Pengaruh Pertumbuhan Ekonomi, Pad, Ukuran Dan Kompleksitas Terhadap Kelemahan Pengendalian Intern Pemda [Effects of economic growth, pad, size and complexity on weaknesses of local government internal control]. Accounting Analysis Journal, 4, 2.

- Rich, K. T., & Zhang, J. X. (2014, December). Does audit committee monitoring matter in the government sector? Evidence from municipal internal control quality. Journal of Governmental & Nonprofit Accounting, 3(1), 58–80. doi:10.2308/ogna-50832

- Sargiacomo, M., & Gomes, D. (2010). Accounting and accountability in local government: Contributions from accounting history research. The sixth accounting history international conference “accounting and the state”, Wellington.

- Supreme Audit Board of the Republic of Indonesia [Badan Pemeriksa Keuangan (BPK) Republik Indonesia]. (2014). Petunjuk Pelaksanaan Pemeriksaan Keuangan BPK RI Nomor 4/K/I-XIII.2/7/2014 [Auditing guideline nomor 4/K/I-XIII.2/7/2014]. Jakarta: Republic of Indonesia.

- Supreme Audit Board of the Republic of Indonesia [Badan Pemeriksa Keuangan (BPK) Republik Indonesia]. (2016). Ikhtisar Hasil Pemeriksaan Semester I Tahun 2016 [Summary of audit result semester I year 2016]. Jakarta: Republic of Indonesia.

- Supreme Audit Board of the Republic of Indonesia [Badan Pemeriksa Keuangan (BPK) Republik Indonesia]. (2017a). Standar Pemeriksaan Keuangan Negara [State audit standard]. Jakarta: Republic of Indonesia.

- Supreme Audit Board of the Republic of Indonesia [Badan Pemeriksa Keuangan (BPK) Republik Indonesia]. (2017b). Ikhtisar Hasil Pemeriksaan Semester I Tahun 2017 [Summary of audit result semester I year 2017]. Jakarta: Republic of Indonesia.

- Supreme Audit Board of the Republic of Indonesia [Badan Pemeriksa Keuangan (BPK) Republik Indonesia]. (2018). Ikhtisar Hasil Pemeriksaan Semester I Tahun 2018 [Summary of audit result semester I year 2018]. Jakarta: Republic of Indonesia.

- Waluyo, M. (2016). Mudah cepat tepat penggunaan tools amos dalam aplikasi (sem). Surabaya: UPN Veteran Jawa Timur.

- Wynne, A. (2003). Do private sector financial statements provide a suitable model for public sector accounts?. Paper for a Conference on Public Law and the Modernizing State in Oeiras, Portugal, 3–6 Sept. 2003.

- Yilmaz, S., Beris, Y., & Serrano-Berthet, R. (2010). Linking local government discretion and accountability in decentralisation. Development Policy Review, 28(3), 259–293. doi:10.1111/j.1467-7679.2010.00484.x