?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The massive influx of global warming, pollution, natural resource depletion, waste, wastewater, climate change, and loss of biodiversity are the primary sources of motivating firms to innovate within their businesses. This has caused great concern for academicians, policymakers and practitioners to find solutions in dealing with the environmental issues. To provide the answer to the exiting challenges this study propounds the conceptual framework that explores the intervention of the new amendment in environment management system (14001–2015) towards innovation, comprehensive green innovation, and firm performance. Therefore, the main objective of this study is to find out the role and effect of ISO14001-(2015) on general innovation and comprehensive green innovation. This study combined the institutional theory, (environmental management system) resource-based theory (general innovation, comprehensive green innovation) and stakeholder theory (firm performance) to maximise the resources utilisation though newly amended EMS14001-2015 to meet the stakeholders demands without compromising the ecological standards. The proposed conceptual framework will provide a holistic view of the firm in formulating strategies and implementing a comprehensive green innovation to the industry. Implementation of a comprehensive green innovation will enable businesses to reduce the cost of production and end life cycle impact of the product, process, service and organisational innovation on the environment. By considering the end life cycle of innovation, including minimisation of the resource consumption, waste, waste to water and emission which will create a sustainable competitive advantage for the firm. All in all, this study propounds the conceptual framework of a comparative study between nomal innovation, comprehensive green innovation and organisation performance with the moderation of environmental management system (14001–2015).

PUBLIC INTEREST STATEMENT

In industrial revolution 4.0, environmental and economic challenges are the motivation for every firms to innovate within their businesses. Every innovation aims to save the resources of organisation and minimize the environmental pollution. However, current business practices of innovating product and process has increased the influx of global warming, pollution, natural resource depletion, waste, and wastewater

The environmental challenges have created pressuring needs to change the current practices of innovation. Therefore, there is need to think green at every level of the organisation. A comprehensive green innovation of firm refers to the procurement of raw materials until the end life cycle of the product, process, service and organisation. This study aims to provide holistic view of the business performance to the investors for investment decisions and for the government to implement and monitor the environment saver policy for the future generation.

1. Introduction

The global concern of environment and sustainable innovation has attracted the attention of industrialists, academia, local governments, and other institution. In light of current business practices, green innovation has emerged as a new way of solving current environmental challenges (Hernandez-Vivanco, Bernardo, & Cruz-Cázares, Citation2018). Researchers believe that the inclusion of green innovation in companies strategies will boost firms to overcome barriers (environment challenges) and create more sustainable innovation. However, still, there is a serious concern of an increasing rate of emission, waste, contaminated water, climate change, biodiversity loss, overuse of limited resources which are directly affecting the environment and society (World Bank, Citation2018).

Ho, Wang, & Shieh, (Citation2016) point out the sustainable thinking is essential to leverage both sides of the strategic integration for enterprises correctly to achieve green innovation. In the same way, the above-mentioned challenges need to develop comprehensive green innovation paradigm to uproots the environment problems, which is also lacking in most of the existing innovation paradigm. This study defines comprehensive green innovation as a combination of green product, green process, green service innovation (Operational) and green organisation innovation (Non-operational) which provide the strategic vision of a comprehensive green innovation in research and development activity. This study suggests that comprehensive green innovation may accelerate resource-saving, creating more sustainable process, competitive advantage and generate higher revenue for the business.

To address the environmental challenges, many improvements and implementations were made for the betterment of the environmental management system (EMS 14,001) from the year 1973 to 2004 The recent amendment, in the year of 2015 of EMS (1SO-14,001) is leadership and their commitment to addressing environmental challenges. Additional modifications were taken in the area to protect the environment, taking initiatives to address risk and opportunity of environment, considering lifecycle perspective of the product and operational control, and lastly establishing communication mechanisms for the organisation to improve the environmental management system.

The EMS (14,001) is a set of rules, regulations, and guidance for the business to abide during the operations. EMS has been adopted by almost all companies around the globe. The primary purpose of EMS-14,001 is to improve the environmental performance of the firm by effective and efficient utilisation of resources, reduction of wastage, developing competitive advantage, and trust of related stakeholders.

Several studies (Ololade & Rametse, Citation2018; Salim et al., Citation2018) were conducted on sustainability and environmental management system but a clear understanding of the nexus and effect of environment management system EMS-14,001-2015 on comprehensive green innovation not investigated after the amendment in ISO14,001-2015.

2. Literature review and framework development

A framework model is a graphical and analytical tool that rationally combines the different variation and context of the notion to develop a method which will provide the immeasurable probable elucidation of the subject at stake. Currently, literature has coined various forms of innovation namely; user innovation, disruptive innovation, green innovation, open innovation, design-driven innovation, social innovation, common innovation, responsible innovation, convergence innovation, indigenous innovation, total innovation, secondary innovation and embracing innovation (Chen, Yin and Mei, Citation2018). This study integrates green innovation and holistic innovation to define comprehensive green innovation. Comprehensive green innovation can also be described as a combination of holistic innovation and sustainable innovation to enhance innovation and operation activity of the business. Comprehensive green innovation consists of two main elements, namely general innovation and green innovation. There are seven sub-elements, namely general product, process, service, green product innovation, green process innovation, green service innovation, and green organization innovation.

2.1. Innovation and firm performance

Companies that pursue innovation may reflect through the improvement and creation of a new product, process, and service, which will bring revenue for the business. Innovation can be highly achieved by spending a high amount on the adoption of new technology and research & development. These expenditures may increase the market value and the number of a patent of the business.

Several studies (González-Fernández & González-Velasco, Citation2018) (Atalay, Anafarta and Sarvan Citation2013) were conducted in different contexts, and countries that found business performance is positively associated with innovation. On another hand, Santos, Basso, Kimura, and Kayo (Citation2014) found there is no direct relationship or short term effect on a firm’s financial performance.

Also, prior literature showed conflict and mixed results of innovation and business performance relationship. In a recent study conducted by de Oliveira, Basso, Kimura, and Sobreiro (Citation2018) showed that innovation efforts had a positive effect in lieu of product, but this impact of innovation does not necessarily convert into financial business performance. On the contrary, research conducted by González-Fernández and González-Velasco (Citation2018) found that the level of innovation effort had positive economic performance, especially in generating sales revenue. The researcher also pointed out that innovation efforts and generating sales revenues depends and differs according to the size of the business Bamfo and Kraa (Citation2019). Also, González-Fernández and González-Velasco (Citation2018) founds that the relationship of innovativeness is more favourable among SMEs financial performance.

Atalay, Anafarta, and Sarvan (Citation2013) found that out of four types of innovation, (product, process, organisation, and marketing innovation) product and process innovation indicated a significantly positive relationship with financial performance and creating a sustainable competitive advantage for the firm. In longitudinal research conducted by Artz, Norman, Hatfield, and Cardinal (Citation2010), it was found that product innovation and firm performance in different industry in the US and Canada found product innovation had substantial significant nexus of business performance. This result seems to be consistent with the current literature of innovation and firm performance (Ramadani et al., Citation2019) (Wadho & Chaudhry, Citation2018) (Burrus, Graham, & Jones, Citation2018; Darroch, Citation2005). Whereas prior literature of service innovation, significant relationship with firm performance and measurement are under-researched.

To measure the financial and non-financial performance, researchers and industrialists have used different measurement techniques; such as registration of patents and trademarks, R&D investment and sales outcomes, ROI and gross margin from the sale of new products. Also, McKinsey & Company (Citation2018) recently published an article on “How to take the measure of innovation,” in which McKinsey provided the easiest way to measure innovation and R&D output that is considered reliable and watermark. McKinsey (2018) claimed that to measure innovation; one must first find out the return from every dollar spent on R&D to invent new products from their sales. Secondly, one must compare gross margin performance against fellow peers in the industry. Therefore, this study proposes the following hypotheses:

H1: Innovation has a positive nexus with firm performance

H1a: Product innovation has a positive nexus with firm performance

H1b: Process innovation have positive nexus with firm performance

H1c: Service innovation has a definite link with firm performance

2.2. Green innovation (GI) and firm performance (FP)

The concept of green innovation proposes modification or introduction of a new product, process, service, and system, which can minimise the emission and burden from the environment and contribute towards a green environment (Calza, Parmentola, & Tutore, Citation2017). Green innovation has proved to be a popular problem-solving concept in recent decades of global warming and environmental challenges. The term green innovation is a synonym for environmental innovation, eco-innovation, and ecological innovation has used by a different author, context and counties stated by Tariq, Badir, Tariq, and Bhutta (Citation2017) which aim to blend environmental and economic performance, thus creating value for all stakeholders in strengthening the firms.

Green innovation literature has evolved over the past two decades with mounting environmental threats (Tariq et al., Citation2017). Scholar Albort-Morant, Leal-Millán, and Cepeda- Carrión (Citation2016) claimed that firms are given an avenue to increase competitive advantage when they apply green innovation and green management (Ho, et al., Citation2016), while also enjoying numerous benefits such as goodwill, stakeholder trust, and high price. This is especially true if the firm is the first mover. Chen, Yin, and Mei (Citation2018) stated that effective and efficient performance and profitability of the firm could be achieved by implementing green innovation.

Green innovation may consider the chance for firms to include environmental issues into their strategies, along with consolidating another strategy, including implementation. Many companies fail to take up the aforementioned opportunities to create competitive advantage and make an effort to solve environmental problems (Yin, Gong, & Wang, Citation2018). Green innovation contributes in two ways, ecological and financial performance of the business. Many researchers have introduced forms of green innovation- green product innovation (Calza et al., Citation2017; Tariq et al., Citation2017; Xie, Huo, & Zou, Citation2019), green process innovation (Xie et al., Citation2019) and green service innovation (Calabrese, Castaldi, Forte, & Levialdi, Citation2018). This study includes the utmost aspect of green innovation found in the current literature, which is all operational outlook of business but non-operational is missing that is green organisational innovation. Therefore, the following hypothesis is:

H2: Green innovation has a positive relations//hip with firm performance

2.2.1. Green product innovation (GPI)

Green product innovation has shown more benefits among stakeholders throughout their lifespans. However, the development of the green product is sluggish in meeting future expectations, as stated by Ilg (Citation2019). Green product innovation emboldens the efficient and effective use of limited resources, and it minimises waste to generate additional revenue and cash flows (Ar, Citation2012).

Green product innovation also generates corporate goodwill, build a unique market position, obtain a competitive advantage, and build green leadership reputation. It is becoming a huge profit source for businesses and will be able to create goodwill in the minds of the customers. Furthermore, Ar (Citation2012) explains that if the organisation focuses on product innovation and environmental repercussions, it can gain a competitive advantage over its competitors.

Reinhardt (Citation1999) and Chen, Lai, and Wen (Citation2006) found that GPI is wholly linked with the competitive advantage of the organisation. GPI is more effective in attracting external stakeholders than internal stakeholders. GPI depicts the vision and mission of the firm along with green mindfulness of employees at every level of management.

H2a: GPI (Product) has positive nexus with firm performance

2.2.2. Green process innovation (GPI)

Green process innovation is initiated by adopting clean technology and eco-saving equipment to enhance energy efficiency and maximise resource utilisation along with eliminating the emission of greenhouse gases (Dai & Zhang, Citation2017). GPI is the second imperative element of green innovation, which mitigates the negative environmental impact through waste management, water management, and green raw material (Xie et al., Citation2019). It also enhances the operational efficiency and financial performances of the organisation and creates trust among internal stakeholders. This is because GPI provides a safe work environment for the employees by eliminating environmental effect within the firm’s premises. By minimising water wastage and recycling waste, it can also attract external stakeholders for future investment.

However, many firms are lagging in the adoption of green process innovation. Dai and Zhang (Citation2017) found that this is due to the lack of complete customer awareness, risk of huge investment promotion, and enforcement of green innovation by the government. If the firm adopts green process innovation, GPI can benefit firms in terms of revenue and directing the external stakeholders’ attention towards their firm performance.

H2b: GPI (process) has positive nexus with firm performance

2.2.3. Green service innovation (GSI)

Green service innovation is the third element of green innovation. It has attracted section of the academia and industrialists on the demand of competitiveness, which is under-researched (Chang, Citation2018). It is after sales operational activity that is highly considered as a deciding factor in purchasing behaviour. Green service innovation after sales is less scrutinised by the environmental regulators. Further, that can also minimise the cost of capital of the business.

In addition, companies must not only look for minimising costs from the green service innovation aspect but also the environmental perspective, that can make the firm stand out among its competitors. Due to increasing awareness of customers and investors, companies must not only focus on other green innovation elements but also, pay attention to green process innovation which advocates the elimination of environmental effects along with winning the confidence of investors and customers (Chang, Citation2018). Green service innovation can equally contribute to achieving economic, social, and sustainable development, just like every element of green innovation. This study thus hypothesises that green service innovation positively affects the performance of the business.

H2c: GSI (Service) has positive nexus with firm performance

2.2.4. Green organization innovation (GOI)

Green organisation innovation is a non-operational innovation element of green innovation. It may indirectly save the capital cost and enhance the revenue of the business if the non-operational activities are sustainable. Sustainable non-operational activities of the business refer to minimising the electricity consumption, indirect and direct emission, waste management, and water management in non-production/manufacturing innovation.

Also, green organisational innovation can be another practical element in generating revenue of the business and attracting the responsible investment, boost confident of related stakeholders to create competitive advantage. Therefore, this research thus hypothesises;

H2d: GOI (organisational) has positive nexus with firm performance

3. Firm performance

Firm performance is almost objective of every related shareholder of the firm. Measuring firm performance is significantly imperative as it provides entropy on the goal and objective of the business that how well they have been achieved in the financial year. Well, performing business attracts investors, as prospect investor monitors business in making an investment decision on whether to initiate, to wait or not to invest.

Business performance measured though financial outcome is not the only one way to asses in this industrial revolution, but by incorporating the environmental social and governance (ESG) factors in business reporting has become another compelling way to assess the firm performance.

The incorporation of ESG and introduction of sustainable development goals has attracted investors to consider the investment decision on ESG and SDG parameters, but due to limited resources this study will adopt the financial measure to assess the effect of ISO 14,001 on innovation, green innovation and firm performance

In this study, business performance can be measured through mainly three metrics namely return on capital employed (ROCE), net profit after tax (NOPTA), and total shareholder return (TSR).

Return on capital employed is financial ratio which measures company efficiency and profitability on capital invested. ROCE will clarify the ability of profit generation and sustainability of the firm.

Whereas net profit after tax (NOPT) measures the core operating efficiency without any influence of debtors, merger and acquisition. This ratio will refine the finding of the ISO14,001 effect on innovation and firm performance. On the other hand, total shareholder return will provide this study more refine performance of the firm in terms of capital gain and dividend to the investor.

Therefore, using these three accounting ratios will provide a more precise performance of the business.

4. Moderating effect of environment management system (EMS)

The environment management system is a set of rule, regulation, and guidance for the business to be followed during the operational and non-operational activity (Ferrón-Vílchez, Citation2016).

Since the introduction of EMS, it has been adopted by business around the world and but due to a recent amendment in the year, 2015 EMS (1SO-14,001) added risk & opportunity, including environmental aspects in the product, product life cycle, environmental requirements for purchasing, leadership and commitment toward the environment brings into the discussion of investors.

The primary purpose of EMS-14,001 to improvise the ecological performance by effective and efficient utilisation of resources and reduction of wastage. Numerous research has found similar sets of findings that environment standard 14,001 enables the business to reduce the impact of their operational and non-operational activity on the environment (Castillo-Rojas et al., Citation2012; Link & Naveh, Citation2006; Sartor, Orzes, Touboulic, Culot, & Nassimbeni, Citation2019),

The growth of the number of certified organisations worldwide increases at an increasing rate of 10% annually which is the evidence of popularity amongst investors and organisations. Researcher. Several scholarly studies have described the positive impact of the standard on various aspects such as corporate image (Sambasivan & Fei, Citation2008) regulatory compliance and waste minimisation (Psomas, Fotopoulos, & Kafetzopoulos, Citation2011). Other studies have questioned the positive impact of the standard on environmental performance (Boiral and Henri Citation2012), claiming that the adoption of ISO 14,001 does not lead to significant improvements. Generally speaking, various studies have shown that the growth of management practices and standards such as ISO 14,001 can be driven by various institutional pressures and is not indicative of their real effectiveness (Castka & Prajogo, Citation2013)

In the same way implementation of the environmental management system will affect the firm innovation and green innovation activity.

The adoption and outcome of ISO 14,001 are inconclusive be it in operating activities or organisational activities.

Therefore this study intends to analyze the effect of ISO 14,001 in organisational innovation and green innovation activity with the assumption of a positive effect. Below hypothesis is developed on the assumption of ISO claims of positive effect over firm performance.

H3: Does the environment management system moderate the positive nexus between innovation and firm performance

H4: Does the environment management system moderate the positive nexus between GI and firm performance

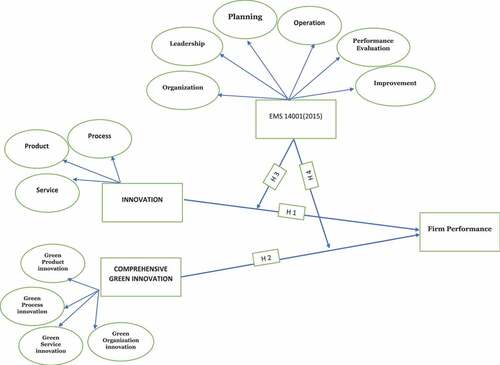

5. Conceptual framework

A proposed conceptual framework is an analytical tool or study design which is designed to guide the entire research; theories are constructed to explain the relationship between variables. A conceptual framework is backed by two main philosophies: Stakeholder theory, pertinent with the innovation and comprehensive green innovation and institutional theory with an emphasis on the pressure or hindrance of environment management system on emphasising of selecting investment at the effective and efficient frontier line to enhance the overall performance.

The proposed framework model is composed of three variables: independent as innovation and comprehensive innovation, moderator as EMS-14,001-2015 and dependent variable as firm performance as shown in Figure .

Figure 1. Firm Performance.

It has been theorized that certification and implementation of EMS 14,001–2004 have a positive effect on business performance. So does the updated EMS 14,001 2015 have accelerated the innovation and comprehensive innovation activity which will have a positive impact on the firm performance? This moderating variable namely EMS 14,001–2015 will help efficient use of resources, adoption of clean energy, technologies, as well as EMS 14,001–2015 will be able to guide top-level managers to respond the expectation of stakeholder without affecting the future generation needs and wants.

Also, to measure each variable, there is the main critical element namely; waste, water consumption, emission management, electricity consumption, responsible investment, and certification, which will be considered in collecting primary and secondary source.

6. Future research

Future researches may empirically examine and validate the propounded conceptual framework. The authors anticipate future research to explore the theoretical framework of various industries and nations. For instance, the propounded research model can be examined in different domains and with larger sample size. This study will encourage to generalised the framework of EMS-14,001-2015 innovation and comprehensive green innovation in future business activity to sustainable competitive advantage.

Furthermore, quantitative methodologies could be tested and validate the nexus of innovation, comprehensive innovation, and organisational performance with the moderating effect EMS 14,001–2015. Additionally, this research could be useful for academia to conduct research and analysis to find out EMS 14,001–2015 on environment and society.

7. Conclusion

This study is at the initial stage, presenting a research model that investigates the moderating effect of the environmental management system (14,001–2015) onto the nexus between comprehensive green innovation, general innovation and business performance measured through financial ratios. The objective of the proposed study is to investigate the positive/negative pressure of EMS (14001–2015) on eco-friendly innovation which could save the firm resources (cost of operation, product and process) natural resources (energy, water, waste and emission minimisation) that ultimately leads to increase in firm revenue generation and performance.

The study can be conducted on the public listed firms as there is a requirement to adopt and follow the ecological standards proposed by ISO14001. The expected finding of this research framework model is expected to be different as this study is intended to see the effect of newly amended EMS14001-2015 on green innovation and general innovation.

On the other hand, this research framework will be helpful to senior-level management to apprehend the impact of comprehensive green innovation framework for public listed companies of Malaysia. Apart from this proposed model may also provide a reference to public listed companies Bursa Malaysia to apprehend and identify the decisive factors and serve as an imperative channel to improve their financial value. Secondly, the integration of comprehensive green innovation and EMS (14001–2015) certification will assist the business in the improvement of return on capital employed (ROCE), net profit after tax (NOPTA) and total shareholder return (TSR).

Cover Image

Source: Author.

Correction

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Acknowledgements

The authors like to thanks to the Management and Humanities Department of Universiti Teknologi Petronas, Malaysia, for providing all facilities throughout the research.

Additional information

Funding

Notes on contributors

Parvez Alam Khan

Parvez Alam Khan is currently in second year PhD student under the supervision of Dr. Johl at University Technology PETRONAS Malaysia. His research intrest is in the area of Corporate Governance and Sustaibility.

Satirenjit Kaur Johl

Associate Professor Dr. Satirenjit Kaur Johl has been in the academic, research & consultancy field since 1992. She is currently attached with University Teknologi Petronas (UTP). Prior to that she was with the Universiti Utara Malaysia (UUM). She obtained her PhD (Business) from The University of Nottingham, U.K and Master’s in Management majoring in HRM from UUM. Dr. Johl is also a certified trainer from the Institute of Personnel and Development, U.K. She supervises Master and PhD students in the areas of Entrepreneurship, Corporate Governance and Strategic Management. Dr. Johl has received awards from International bodies for Best Dissertation awarded by British Aerospace and Loughborough University, U.K. She has also received the Hariram Jayaran Special Award and Gold Award in the 23rd International Invention Innovation & Technology Exhibition.

Related Research Data

References

- Albort-Morant, G., Leal-Millán, A., & Cepeda-Carrión, G. (2016). The antecedents of green innovation performance: A model of learning and capabilities. Journal of Business Research, 69(11), 4912-4917.

- Ar, I. M. (2012). The impact of green product innovation on firm performance and competitive capability: The moderating role of managerial environmental concern. Procedia - Social and Behavioral Sciences, 62, 854–12. doi:10.1016/j.sbspro.2012.09.144

- Artz, K. W., Norman, P. M., Hatfield, D. E., & Cardinal, L. B. (2010). A longitudinal study of the impact of R&D, patents, and product innovation on firm performance. Journal of Product Innovation Management, 27(5), 725–740. doi:10.1111/j.1540-5885.2010.00747.x

- Atalay, M., Anafarta, N., & Sarvan, F. (2013). The relationship between innovation and firm performance: An empirical evidence from Turkish automotive supplier industry. Procedia - Social and Behavioral Sciences, 75, 226–235. doi:10.1016/j.sbspro.2013.04.026

- Bamfo, B. A., & Kraa, J. J. (2019). Market orientation and performance of small and medium enterprises in Ghana: The mediating role of innovation. Cogent Business & Management, 6(1), 1605703. doi:10.1080/23311975.2019.1605703

- Boiral, O, & Henri, J. F. (2012). Modelling the impact of iso 14001 on environmental performance: a comparative approach. Journal of Environmental Management, 99, 84–97.

- Burrus, R. T., Graham, J. E., & Jones, A. T. (2018). Regional innovation and firm performance. Journal of Business Research, 88, 357–362. doi:10.1016/j.jbusres.2017.12.042

- Calabrese, A., Castaldi, C., Forte, G., & Levialdi, N. G. (2018). Sustainability-oriented service innovation: An emerging research field. Journal of Cleaner Production, 193, 533–548. doi:10.1016/j.jclepro.2018.05.073

- Calza, F., Parmentola, A., & Tutore, I. (2017). Types of green innovations: Ways of implementation in a non-green industry. Sustainability, 9(8), 1301.

- Castillo-Rojas, S. M., Casadesús, M., Karapetrovic, S., Coromina, L., Heras, I., & Martín, I. (2012). Is implementing multiple management system standards a hindrance to innovation? Total Quality Management & Business Excellence, 23(9–10), 1075–1088. doi:10.1080/14783363.2012.678587

- Castka, P., & Prajogo, D. (2013). The effect of pressure from secondary stakeholders on the internalization of ISO 14001. Journal of Cleaner Production, 47, 245–252. doi:10.1016/j.jclepro.2012.12.034

- Chang, C.-H. (2018). How to enhance green service and green product innovation performance? The roles of inward and outward capabilities. Corporate Social Responsibility and Environmental Management, 25(4), 411–425. doi:10.1002/csr.v25.4

- Chen, J., Yin, X., & Mei, L. (2018). Holistic innovation: An emerging innovation paradigm. International Journal of Innovation Studies, 2(1), 1–13. doi:10.1016/j.ijis.2018.02.001

- Chen, Y. S., Lai, S. B., & Wen, C. T. (2006). The influence of green innovation performance on corporate advantage in Taiwan. Journal of Business Ethics, 67(4), 331–339. doi:10.1007/s10551-006-9025-5

- Dai, R., & Zhang, J. (2017). Green process innovation and differentiated pricing strategies with environmental concerns of South-North markets. Transportation Research Part E: Logistics and Transportation Review, 98, 132–150. doi:10.1016/j.tre.2016.12.009

- Darroch, J. (2005). Knowledge management, innovation and firm performance. Journal of Knowledge Management, 9(3), 101–115. doi:10.1108/13673270510602809

- de Oliveira, J. A. S., Basso, L. F. C., Kimura, H., & Sobreiro, V. A. (2018). Innovation and financial performance of companies doing business in Brazil. International Journal of Innovation Studies, 2(4), 153–164. doi:10.1016/j.ijis.2019.03.001

- Ferrón-Vílchez, V. (2016). Does symbolism benefit environmental and business performance in the adoption of ISO 14001? Journal of Environmental Management, 183, 882–894. doi:10.1016/j.jenvman.2016.09.047

- González-Fernández, M., & González-Velasco, C. (2018). Innovation and corporate performance in the Spanish regions. Journal of Policy Modeling, 40(5), 998–1021. doi:10.1016/j.jpolmod.2018.05.005

- Hernandez-Vivanco, A., Bernardo, M., & Cruz-Cázares, C. (2018). Sustainable innovation through management systems integration. Journal of Cleaner Production, 196, 1176–1187. doi:10.1016/j.jclepro.2018.06.052

- Ho, Y. C., Wang, W. B., & Shieh, W. L. (2016). An empirical study of green management and performance in Taiwanese electronics firms. Cogent Business & Management, 3(1), 1266787. doi:10.1080/23311975.2016.1266787

- Ilg, P. (2019). How to foster green product innovation in an inert sector. Journal of Innovation & Knowledge, 4(2), 129–138. doi:10.1016/j.jik.2017.12.009

- Link, S., & Naveh, E. (2006). Standardization and discretion: Does the environmental standard ISO 14001 lead to performance benefits? IEEE Transactions on Engineering Management, 53(4), 508–519. doi:10.1109/TEM.2006.88370

- McKinsey & Company. 2018. How to take the measure of innovation. Accessed from: https://www.mckinsey.com/business-functions/strategy-and-corporate-finance/our-insights/how-to-take-the-measure-of-innovation

- Ololade, O. O., & Rametse, P. P. (2018). Determining factors that enable managers to implement an environmental management system for sustainable construction: A case study in Johannesburg. Business Strategy and the Environment, 27(8), 1720–1732. doi:10.1002/bse.v27.8

- Psomas, E. L., Fotopoulos, C. V., & Kafetzopoulos, D. P. (2011). Motives, difficulties and benefits in implementing the ISO 14001 environmental management system. Management of Environmental Quality: an International Journal, 22(4), 502–521. doi:10.1108/14777831111136090

- Ramadani, V., Hisrich, R. D., Abazi-Alili, H., Dana, L. P., Panthi, L., & Abazi-Bexheti, L. (2019). Product innovation and firm performance in transition economies: A multi-stage estimation approach. Technological Forecasting and Social Change, 140, 271–280. doi:10.1016/j.techfore.2018.12.010

- Reinhardt, F. (1999). Market failure and the environmental policies of firms: Economic rationales for “beyond compliance” behaviour. Journal of Industrial Ecology, 3(1), 9–21. doi:10.1162/108819899569368

- Salim, H. K., Padfield, R., Hansen, S. B., Mohamad, S. E., Yuzir, A., Syayuti, K., … Papargyropoulou, E. (2018). Global trends in environmental management system and ISO14001 research. Journal of Cleaner Production, 170, 645–653. doi:10.1016/j.jclepro.2017.09.017

- Sambasivan, M., & Fei, N. Y. (2008). Evaluation of critical success factors of implementation of ISO 14001 using analytic hierarchy process (AHP): A case study from Malaysia. Journal of Cleaner Production, 16(13), 1424–1433. doi:10.1016/j.jclepro.2007.08.003

- Santos, D. F. L., Basso, L. F. C., Kimura, H., & Kayo, E. K. (2014). Innovation efforts and performances of Brazilian firms. Journal of Business Research, 67(4), 527–535. doi:10.1016/j.jbusres.2013.11.009

- Sartor, M., Orzes, G., Touboulic, A., Culot, G., & Nassimbeni, G. (2019). ISO 14001 standard: Literature review and theory-based research agenda. Quality Management Journal, 26(1), 32–64. doi:10.1080/10686967.2018.1542288

- Tariq, A., Badir, Y. F., Tariq, W., & Bhutta, U. S. (2017). Drivers and consequences of green product and process innovation: A systematic review, conceptual framework, and future outlook. Technology in Society, 51, 8–23. doi:10.1016/j.techsoc.2017.06.002

- Wadho, W., & Chaudhry, A. (2018). Innovation and firm performance in developing countries: The case of Pakistani textile and apparel manufacturers. Research Policy, 47(7), 1283–1294. doi:10.1016/j.respol.2018.04.007

- World Bank. 2018. Environment. Accessed from: https://www.worldbank.org/en/topic/environment/overview

- Xie, X., Huo, J., & Zou, H. (2019). Green process innovation, green product innovation, and corporate financial performance: A content analysis method. Journal of Business Research, 101, 697–706. doi:10.1016/j.jbusres.2019.01.010

- Yin, J., Gong, L., & Wang, S. (2018). Large-scale assessment of global green innovation research trends from 1981 to 2016: A bibliometric study. Journal of Cleaner Production, 197, 827–884. doi:10.1016/j.jclepro.2018.06.169