Abstract

The controversial findings by Reinhart and Rogoff have continuously generated debates on the threshold of debt towards GDP. Hence, the aim of this study is to examine whether there exists mutual consensus on the effects of public debt on the economic growth of a country or group of economies. A systematic review on related articles from SCOPUS database was conducted by adopting a standard procedure in the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA), namely identification, screening and eligibility. Thirty-three articles were chosen as the main articles to be reviewed. It was found that there is no mutual consensus on the relationship between public debt and economic growth. The relationship can be positive, negative or even non-linear. Besides, the 90% threshold as argued in the Reinhart-Rogoff hypothesis is also not applied across all countries. The findings may help governments and policymakers to design their fiscal policy by investigating how existing debts affect the growth level. Future studies should investigate the effects of public debt on the economic growth in the upper-middle-income economies. These economies were least studied in this context.

PUBLIC INTEREST STATEMENT

This paper examines how public debt affects the economic growth of the selected countries. The investigations were conducted by analyzing past literature that focus on the same subject matter, but with different countries, income size, debt level and methods of analyses. This study is important because we want to prove that a 90% debt threshold as discussed previously by Reinhart and Rogoff are not the same for all countries in the world. In this regard, Reinhart and Rogoff argued that the public debt can give positive effects of the economic growth if the debt level is not exceeding 90% of the GDP. However, our findings suggest that the threshold is not identical for all countries. Instead, it varies depending on the countries’ income, macroeconomic stability, institutional quality and so on.

1. Introduction

The sustainable development goals (SDGs) by the United Nations outlined 17 goals that need to be achieved by 193 countries before 2030. One of the goals (goal no. 8) is to achieve higher economic growth (United Nations, Citation2018). Since the world economic structure is changing towards the fourth industrial revolution, the countries have been obliged to invest in critical areas such as artificial intelligence, machine learning, technological development and human capital. Without these important investments, the economic growth will be stagnant and the countries will become less competitive with investments being channeled into traditional production methods (World Economic Forum, Citation2017).

Investing in the critical areas specified above requires a massive amount of funds. Therefore, countries that are receiving fewer investments through domestic or international trades might require public borrowings to support their economic development. Moreover, some countries like Indonesia and Japan which are regularly affected with a series of natural catastrophes necessitates them to put aside a relevant amount of fund for emergencies. Even though funds can be collected from domestic and foreign aids, it might not be sufficient if the impacts are disastrous. Hence, in this case, taxation is regarded as one of the potential source of funds to finance emergencies (Ono & Uchida, Citation2018). However, since taxation creates distortionary effects on economic growth, it is less popular among the policymakers (Barro, Citation1979). Therefore, public debt is the only feasible option to finance government expenditures and other development projects if the country lacks funds. This argument is following the Ricardian invariance theorem, in which taxation gives excess burden to the public by increasing the cost of living and reducing the purchasing power of people (Barro, Citation1979).

Based on previous literature, public debt can either positively or negatively affect the whole economy. The effect depends on the amount of debt and its purposes. Usually, the amount of debt to be borrowed is measured using the debt-to-GDP ratio. To the contrary, Reinhart, Reinhart and Rogoff (Citation2015) claimed that the ratio should be at most 90%. The economy would still be able to grow with the debt threshold of less than 90%. Beyond the threshold, public debt will cause an adverse effect on the economy. It is proven empirically by looking at the case of developing countries, in which the debt threshold was found at 88.2% (Karadam Citation2018). The economy is able to grow positively when the debt level is below the threshold. However, when public debt to GDP exceeds the threshold, the growth start to decline.

Therefore, the main objective of this paper is to prove whether there is a mutual consensus on the effects of public debt on the economic growth of a country or group of economies. Is 90% debt threshold is applicable to all countries? If not, what is the right threshold for each country or group of economies? Besides, the other objective is to simplify the previous findings by assessing the major consensus on how public debt affects economic growth. In deriving the answers, a systematic review was conducted on selected articles that discussed the relationship between public debt and economic growth. The findings from these articles were grouped into two main themes in order to answer the objective.

1.1. The need for a systematic review

A systematic review is aimed to recognize, combine and evaluate all accessible quantitative data obtained from previous literature. This systematic review is focused on reliable articles that are related to this subject matter. Public debt is crucial for economic growth and development especially for countries with a lack of savings and investments. However, if not managed properly, public debt could also harm the economy. Therefore, this paper is aimed to address the gap whether there is a specific threshold for the public debt which can be applied to all economies. Besides, the other objective is to simplify the previous findings by assessing the major consensus on how public debt affects economic growth. The reason is to help the government and policymakers to carefully design their fiscal policy initiatives by considering the impact on high public debt to the economic growth of their countries.

2. Materials and methods

In ensuring the quality of the review, the Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) was used as publication standard due to its ability to classify previous literature in a specific database based on certain requirements. The information which is gathered from the review is then coded in order to help in the interpretation of the findings and to address the potential gaps that exist in the current literature.

2.1. Resources

The gathering of information from selected journal articles should commence from a credible source of database. Hence, the Scopus database was employed since the journal articles published in this database are of high quality and reliable. Besides, Scopus contains a large number of journal articles related to public debt successfully published from 2017 to 2019. These 3 years were chosen because we want to investigate the latest trends on how public debt affect the economic growth.

2.2. Identification, screening and eligibility

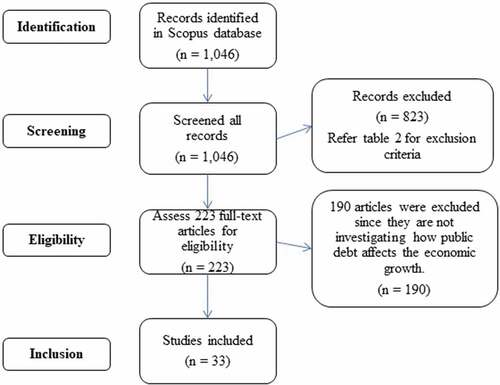

The first step of the review is to identify and select articles suitable for the scope of this study from the Scopus database. To do so, a search string was developed in April 2019 based on certain keywords related to public debt and economic growth. Table lists the search string used in this study. Based on the search string and the keywords, Scopus database managed to gather 1,046 articles.

Table 1. The search string

Once the identification stage is successfully completed, the populated articles were subjected to screening based on the inclusion and exclusion criteria. Non-relevant articles are to be excluded from the study to ensure the reliability of the outcome. Only articles suitable for the inclusion criteria were retained. The five inclusion criteria include the year, document type, publication stage, source type and language. For this study, only journal articles published in English (in the final stage) from 2017 to 2019 were included. Other articles that were published in other types of documents in other languages prior to 2017 were excluded from this study. The final count upon completing screening was 223 articles from 1,046 selected articles. The five criteria are tabulated in Table .

Table 2. The inclusion and exclusion criteria

However, screening alone is not sufficient without the eligibility assessment. Each of the 223 articles was assessed based on the titles, abstracts and the main contents. Hence, the articles explaining the relationship between public debt and economic growth were selected. As a result, 33 articles were selected for the systematic review since they suited to the objective of this study. The whole process of the selection of 33 articles is illustrated in Figure . This diagram is adopted from Moher et al. (Citation2009).

Figure 1. The process of selecting articles.

2.3. Data abstraction and analysis

The quantitative review was conducted by analyzing all 33 articles that have been selected. The analysis was conducted by tabulating the findings into main themes and sub-themes. The two main themes were employed are linear and non-linear. These two themes represent the main findings in all 33 articles, in which the relationship between public debt and economic growth can be either be linearlyFootnote1 or non-linearlyFootnote2 related. Within the linear theme, three sub-themes were developed. They represent the linear relationship in the forms of a positive, negative or insignificant linear relationship. Meanwhile, the non-linear relationship was further divided into six sub-themes based on a debt-to-GDP threshold. The sub-themes were coded with (0) indicating no non-linear relationship, (1) debt-to-GDP threshold less than 20%, (2) threshold of 21% to 50%, (3) threshold 51% to 70%, (4) threshold 71% to 90% and (5) debt-to-GDP threshold exceeding 90%. The findings were discussed in the next section of this paper.

3. Results

Out of 33 articles, 15 of them were using time series analysis, while the remaining 18 articles were employing panel data analysis. In the time series analysis, the Autoregressive Distributed Lag Model (ARDL) is widely used by previous researchers (Burhanudin, Muda, Nathan, & Arshad, Citation2017; Maitra, Citation2019; Mhlab & Phiri, Citation2019). However, the use of the same method does not guarantee the same results. For instance, there is a negative relationship found between public debt and economic growth in Sri Lanka and South Africa (Maitra, Citation2019; Mhlab & Phiri, Citation2019). By employing the same ARDL method, the results were different in the case of Malaysia (Burhanudin et al., Citation2017). One of the reasons might be due to the level of debt a country possess, together with different stability in macroeconomic conditions. From the perspective of the panel data analysis, various methods have been used in previous empirical studies such as panel ordinary least square (Butkus & Seputiene, Citation2018), panel VAR (Liaqat, Citation2019), panel ARDL (Gómez-Puig and Sosvilla-Rivero Citation2018a), fixed effects (Arčabić et al. Citation2018; Ahlborn & Schweickert, Citation2016), GMM (Arčabić et al. Citation2018; Butkus & Seputiene, Citation2018), least square dummy variable (Butkus & Seputiene, Citation2018) and so on. Different studies employed different methods based on the number of cross sections and year for each analysis. For example, any studies that have cross sections and time less than 25 should employ GMM, while studies with more than 25 cross sections and time should use pooled ordinary least square (POLS), fixed effects (FE) or random effects (RE).

Besides, most of the articles were focusing on the mixed economies and high-income economies. Based on Table , very limited research on the relationship between public debt and economic growth have been conducted specifically on the low-income economies, lower-middle-income economies and upper-middle-income economies. Hence, there is room to investigate these economies since some of the countries within these economies are facing a problem of low capital accumulation. Given the lower level of investments, public debt is highly sought after to transform the economic condition and groom it to a higher level. Therefore, attention should be given to low, lower-middle-income and middle-income economies as they might be facing difficulties in uplifting the economic growth without the assistance from public debt.

Table 3. Types of countries under investigation

During the assessment of the relationship between public debt and economic growth, the findings from the 33 articles were tabulated based on two main themes and nine sub-themes. Table summarizes the findings. In both lower-middle-income-economies, public debt in Sri Lanka and Nigeria were found to give adverse effect to the economic growth of these countries.

Table 4. The main themes and sub-themes for the relationship between public debt and economic growth

3.1. Discussion

Generally, the findings were divided into two main themes, namely linear and non-linear relationship. From the main themes, nine sub-themes were developed.

3.1.1. Linear negative relationship

Overall, 24 of 33 articles which were investigated revealed a linear relationship between public debt and economic growth. The linear relationship can be further divided into a positive, negative or insignificant relationship. Linear positive relationship means that the economy is able to grow as the debt level increases. It is a preferred condition since the country is able to increase public debt to meet their national objectives such as enhancing their infrastructures, investing in human capital and so on. On the other hand, a linear negative relationship indicates that the economic growth is declining when the country increases its debt level. If it happens, many projects might need to be postponed, as additional debts will only lead to the slowdown of the economic growth. As a result, the country might not be able to remain competitive since investors would no longer interested to invest in the country.

Regardless of the type of public debt, the majority of the articles that discussed the relationship between public debt and economic growth from 2017 to 2019 demonstrated a significant negative relationship between the two series. This relationship is applicable to all types of economies, regardless whether they are lower-middle-income, upper-middle-income or high-income economies. By referring to Table , this relationship exists in highly indebted countries such as Sri Lanka and Nigeria (lower-middle-income economies), South Africa (upper-middle-income economies) as well as high-income economies such as Japan, United States, United Kingdom and European countries.

The negative relationship is consistent with the conventional view of debt (Elmendorf & Gregory Mankiw, Citation1998), in which there will be a crowding-out effect on the private investment when the economy is facing high debt problem (Bahal, Raissi, & Tulin, Citation2018; Chudik, Mohaddes, Hashem Pesaran, & Raissi, Citation2017; De Vita, Trachanas, & Luo, Citation2018; Kim, Ha, & Kim, Citation2017; Shahor, Citation2018). The effect is valid for the long-run. It happens when the interest rate starts to increase as the government borrow more funds in the loanable funds market. An increase in the interest rate will demotivate investors from investing in a country. If this condition persists, the economic growth will face an adverse effect in the long-run.

Lower economic growth that is caused by high public debt can also be explained through the overlapping generations model (Blanchard, Citation1985; Diamond, Citation1965; Modigliani, Citation1961), where the increase in the public debt will be partly used up national savings that were meant for the future generation. A reduction in the level of national savings will force the interest rate to increase, thus demotivate incoming investors. Lower investments will result in lower capital accumulation, leading to lower economic growth.

Apart from that, the linear negative relationship can also be explained theoretically using the debt overhang (Krugman, Citation1988). Debt overhang happens when the highly indebted countries have a lower present value of the national income relative to their total accumulated debt (Burhanudin et al., Citation2017; Ewaida, Citation2017; Snieska & Burksaitiene, Citation2018). One possible reason is the inefficiency of the country to manage the borrowed funds (Shkolnyk & Koilo, Citation2018). Instead of channeling the borrowed funds to productive purposes, the governments choose to use the funds to pay previous debts, or to finance operating expenditures which are normally non-productive in nature. Consequently, these funds which are not being used for productive purposes will not create significant value added to the economy, thus contributing to lower economic growth.

3.1.2. Linear positive relationship

On the other hand, public debt can also contribute to higher economic growth, for instance, Malaysia (Burhanudin et al., Citation2017) and European countries (Gómez-Puig & Sosvilla-Rivero, Citation2017a). Theoretically, it can be explained by using the conventional view of debt by Elmendorf and Gregory Mankiw (Citation1998). Even though this view has a negative perspective on public debt to economic growth, it also has a positive standpoint on the two series. An increase in public debt will help to stimulate aggregate demand and output, among others, via the employment generation and productive investment. However, this relationship is only applicable in the short-run. If it continues to increase in the long run, the effect can switch to becoming negative. Therefore, it is important for the government to be alert on the debt threshold that can switch the debt’s effect from positive to negative. The findings on the threshold are further discussed in the next section.

3.1.3. Non-linear relationship

In addition, when public debt can affect economic growth in both positive and negative directions, the non-linear relationship appears. The previous literature captured the threshold effect by including the square term of debt in the growth equation (Ahlborn & Schweickert, Citation2016; Butkus & Seputiene, Citation2018) or by conducting the panel smooth transition regression (Chen, Yao, Hu, & Lin, Citation2016; Karadam, Citation2018).

When testing the existence of the non-linear relationship, two main findings emerged. The non-linear relationship may or may not exists. The non-linear relationship exists in the European countries (Brida, Gómez, & Seijas, Citation2017; Gómez-Puig & Sosvilla-Rivero, Citation2017b; Pegkas, Citation2018, Citation2019) and emerging economies (Shkolnyk & Koilo, Citation2018). In contrary, it is also found that non-linear relationship is not exists in Spain (Esteve & Tamarit, Citation2018) and other countries (Arčabić et al. Citation2018; Kim et al., Citation2017). One possible reason for the contradict findings is the years under investigation. Two of the three studies which revealed the non-existence of non-linear relationship were conducted in the early years of 1851 in Spain (Esteve & Tamarit, Citation2018) and 1960 onwards in Organization for Economic Cooperation and Development (OECD) and non-OECD countries (Arčabić et al. Citation2018). The economic condition then is totally different from the scenario in the last thirty to fifty years.

The Reinhart-Rogoff hypothesis argued that public debt can positively affect the economic growth if the debt to GDP level is lesser than 90% (Reinhart, Reinhart, & Rogoff, Citation2015). Once the debt-to-GDP is beyond the threshold, the effect changes to negative. Empirically, the evidence from previous literature demonstrated that the debt-to-GDP threshold for all countries is not necessarily 90%. The threshold can range from 15% (Butkus & Seputiene, Citation2018) up to 2000% (Pegkas, Citation2018).

The studies that found the threshold to be 90% and above were conducted in Lebanon (Taher, Citation2017), Israel (Shahor, Citation2018) and Greece (Pegkas, Citation2018, Citation2019). The debt level that is beyond 90% of the GDP indicates that the countries are among the highly indebted countries. In this case, these countries may not be able to pay back the debt within the stipulated time period. In order to limit the default risk, the risk premium is added in the interest rate on public debt, leading to the high cost of borrowings. Indirectly, it distorts the economic growth once the threshold is met through the crowd-out effects on private investments.

There were also studies that found the threshold to be lower than 50%. Among them were the European countries (Gómez-Puig & Sosvilla-Rivero, Citation2017b) and advanced economies such as Belgium, Canada, United Kingdom and United States (Lee, Park, Seo, & Shin, Citation2017). For these high-performing economies, the debt threshold is lower due to the lack of investments since the investors fear that the governments will impose higher taxes to finance the debt. As a result, the investors would prefer to channel their investments into other developing economies that costs lower to run a business.

Based on the above findings, it cannot be concluded that the debt-to-GDP threshold for the advanced economies is below 50% while for the highly indebted countries is 90% and above. Besides, the findings from Reinhart & Rogoff (2010) may not be true for all economies since the threshold reported by other researchers varied. Hence, no mutual consensus on the right threshold for each country or group of economies. The threshold for each country depends on their current economic situation, the period of studies, the method and the proxies used to test the relationship. Countries such as Lebanon and Greece that have a debt threshold more than 90% should start in reducing their public debt level in order to ensure greater economic prosperity in the future. Further increase in public debt will not only burden the current generation due to an increase in taxation and reduce in investments. It will also create a burden to the future generation who will have to bear higher costs. In their cases, the government should not impose higher taxes to generate more income since the countries are having a debt crisis. Instead, in order to stimulate higher economic growth, they should slowly reduce inappropriate expenditures and attract more investors to invest in the countries.

In addition, for high-income economies, even though the threshold is in between 21% and 50% (Lee et al., Citation2017), they should carefully design their fiscal policy by limiting the amount of debt as previous researches found linear negative relationship between public debt and economic growth (Amann & Middleditch, Citation2017; De Vita et al., Citation2018; Liaqat, Citation2019). In this regard, they might have to impose higher taxes to generate more revenues since public debt is not a good choice for their economic growth.

Thus, the policy recommendation to achieve higher economic growth for a country should not be applied to the other country or group of economies (Balaguer-Coll, Prior, & Tortosa-Ausina, Citation2016).

4. Conclusion

This paper intends to examine whether there exists a mutual consensus on the effects of public debt on the economic growth of a country or group of economies. In reference to the 33 selected articles, 20 were found to report a negative relationship between public debt and economic growth. However, the findings also indicated that the relationship could turn out to be positive if the borrowings were used for productive purposes. At the same time, both positive and negative relationship can also occur if a threshold for the debt-to-GDP exists. Therefore, there is no mutual consensus on the relationship between public debt and economic growth. The relationship can be positive, negative or even non-linear. Even if a country was found to have a positive relationship between public debt and economic growth, the government should still be cautious in designing their fiscal policy by investigating the best level of debt to be borrowed from time to time. The economic growth could turn out to be negative if the funds are not being managed properly. Due to the above findings, different countries should design their own fiscal initiatives to combat higher public debt and stimulate economic growth. Imposing higher taxes to replace debt might not be a good move for all countries especially for low and middle-income economies. The governments can embark with other fiscal initiatives such as providing tax incentives, with an aim to boost the private sector’s contribution as an engine of growth.

5. Policy suggestions

The findings from the current systematic review have led to several suggestions for policymakers. Firstly, policymakers should not set the debt-to-GDP threshold at 90% as proposed by Reinhart and Rogoff without prior investigation. The government should carefully analyze the economic condition of the country by considering the purposes of the borrowings, the sources of the borrowings along with the ability of the country to pay back. Since each country has its own uniqueness and capabilities, a standard threshold cannot be applied to all.

A country with high debt but with low income should consider to reduce their debt level up to a condition in which the national income is sufficient to pay back the debt. However, in case if the country needs an additional source of financing, increase in tax rate to replace the debt level is not a good move. Instead, the government should create an investment friendly environment to attract more investments in supporting the national income.

On the other hand, a high-income country with a high debt level might consider to increase taxes to replace the debt if the debt level is unmanageable. Nevertheless, the government should implement progressive tax system, in which the imposition of tax is only for individuals and firms who earned higher income. Or else, it will cause disruption to the entire economy due to lower purchasing power and lower private consumptions.

6. Recommendation for future research

It is proposed that the future research should be conducted on how the public debt affects the economic growth of the low, lower-middle-income and upper-middle-income economies. This proposal was made because these economies are suffering from low capital accumulation. Due to the lack of information on these economies, more attention needs to be channeled towards them since they require a massive amount of fund to groom their economies and uplift their economic status to a higher level.

Cover Image

Source: Author.

Additional information

Funding

Notes on contributors

Nur Hayati Abd Rahman

Nur Hayati Abd Rahman is a lecturer in the Universiti Teknologi MARA Melaka, Malaysia. She is highly interested in the areas of public finance, monetary economics and econometric analysis.

Shafinar Ismail

Shafinar Ismail is an Associate Professor in the Universiti Teknologi MARA Melaka, Malaysia. She completed her PhD at Brunel University, West London, United Kingdom. Her areas of expertise include personal finance and Islamic finance.

Abdul Rahim Ridzuan

Abdul Rahim Ridzuan is a senior lecturer in the Universiti Teknologi MARA Melaka, Malaysia. He obtained his PhD in environmental economics from Universiti Sains Malaysia. His areas of interest include environmental economics, international economics, development economics and monetary economics.

Notes

1. Linear relationship means public debt affects economic growth in a positive or negative way.

2. Non-linear relationship indicates the existence of inverted U-curve, in which public debt helps the economy to grow at the first place. Once the debt threshold is reached, further increase in the debt level will slow down the economic growth.

Related Research Data

References

- Ahlborn, M., & Schweickert, R. (2016). Public debt and economic growth – Economic systems matter. International Economics and Economic Policy, 15(2), 373–16. doi:10.1007/s10368-017-0396-0

- Amann, J., & Middleditch, P. (2017). Growth in a time of austerity: Evidence from the UK. Scottish Journal of Political Economy, 64(4), 349–375. doi:10.1111/sjpe.12132

- Arčabić, V., Tica, J., Lee, J., & Sonora, R. J. (2018). Public debt and economic growth Conundrum: Nonlinearity and inter-temporal relationship. Studies in Nonlinear Dynamics and Econometrics, 22(1), 1–20. doi:10.1515/snde-2016-0086

- Awdeh, A, & Hamadi, H. (2017). Factors hindering economic development: evidence from the mena countries. International Journal Of Emerging Markets, 14(2), 281–299.

- Bahal, G., Raissi, M., & Tulin, V. (2018). Crowding-out or crowding-in? Public and private investment in India. World Development, 109(September), 323–333. doi:10.1016/j.worlddev.2018.05.004

- Balaguer-Coll, M. T., Prior, D., & Tortosa-Ausina, E. (2016). On the determinants of local government debt: Does one size fit all? International Public Management Journal, 19(4), 513–542. doi:10.1080/10967494.2015.1104403

- Barro, R. J. (1979). On the determination of the public debt. Journal of Political Economy, 87(5, Part 1), 940–971. doi:10.1086/260807

- Blanchard, O. (1985). Debt, deficits, and finite horizons. Journal Of Political Economy, 93(2), 223–247. doi: 10.1086/261297

- Brida, J. G., Gómez, D. M., & Seijas, M. N. (2017). Debt and growth: A non-parametric approach. Physica A: Statistical Mechanics and Its Applications, 486, 883–894. doi:10.1016/j.physa.2017.05.060

- Burhanudin, M. D. A., Muda, R., Nathan, S. B. S., & Arshad, R. (2017). Real effects of government debt on sustainable economic growth in Malaysia. Journal of International Studies, 10(3), 161–172. doi:10.14254/2071-8330.2017/10-3/12

- Butkus, M., & Seputiene, J. (2018). Growth effect of public debt: The role of government effectiveness and trade balance. Economies, 6(4), 62. doi:10.3390/economies6040062

- Chen, C., Yao, S., Hu, P., & Lin, Y. (2016). Optimal government investment and public debt in an economic growth. China Economic Review, 45, 257–278. doi:10.1016/j.chieco.2016.08.005

- Chiu, Y, & Lee, C.-C. (2017). On The Impact Of Public Debt on Economic Growth: Does Country Risk Matter? Contemporary Economic Policy, 35(4), 751–766. doi: 10.1111/coep.12228

- Chudik, A., Mohaddes, K., Hashem Pesaran, M., & Raissi, M. (2017). Is there a debt-Threshold effect on output growth? Review of Economics and Statistics, 99(1), 135–150. doi:10.1162/REST

- De Vita, G., Trachanas, E., & Luo, Y. (2018). Revisiting the Bi-directional causality between debt and growth: Evidence from linear and nonlinear tests. Journal of International Money and Finance, 83, 55–74. doi:10.1016/j.jimonfin.2018.02.004

- Diamond, P. A. (1965). National debt in a neoclassical growth model. The American Economic Review, 55(5), 1126–1150.

- Elmendorf, D. W., & Gregory Mankiw, N. (1998). Government debt (pp. 6470). Cambridge: National Bureau of Economic Research.

- Esteve, V., & Tamarit, C. (2018). Public debt and economic growth in Spain, 1851–2013. Cliometrica, 12(2), 219–249. doi:10.1007/s11698-017-0159-8

- Ewaida, H. Y. M. (2017). The impact of Sovereign debt on growth: An empirical study on GIIPS versus JUUSD countries. European Research Studies Journal, 20(2), 607–633.

- Gómez-Puig, M., & Sosvilla-Rivero, S. (2017a). Public debt and economic growth: Further evidence for the Euro Area Working Papers Del Instituto Complutense de Estudios Internacionales 1709. Madrid. doi:10.2139/ssrn.3041117

- Gómez-Puig, M., & Sosvilla-Rivero, S. (2017b). Heterogeneity in the debt-growth nexus: Evidence from EMU countries. International Review of Economics and Finance, 51, 470–486. doi:10.1016/j.iref.2017.07.008

- Gómez-Puig, M., & Sosvilla-Rivero, S. (2018a). On the Time-varying nature of the debt-growth nexus: Evidence from the Euro Area. Applied Economics Letters, 25(9), 597–600. doi:10.1080/13504851.2017.1349284

- Gómez-Puig, M., & Sosvilla-Rivero, S. (2018b). An investigation of nonlinear effects of debt on growth. Journal of Economic Asymmetries, 18, 1–13. doi:10.1016/j.jeca.2018.e00097

- Intartaglia, M, Antoniades, A, & Bhattacharyya, S. (2018). Unbundled debt and economic growth in developed and developing economies: an empirical analysis. World Economy, 41(12), 3345–3358. doi:10.1111/twec.12626

- Karadam, D. Y. (2018). An investigation of nonlinear effects of debt on growth. Journal Of Economic Asymmetries, 18, 1–13. doi: 10.1016/j.jeca.2018.e00097

- Kempa, B, & Khan, N. S. (2017). Spillover effects of debt and growth in the euro area: evidence from a gvar model. International Review Of Economics And Finance, 49, 102–111. doi: 10.1016/j.iref.2017.01.024

- Kim, E., Ha, Y., & Kim, S. (2017). Public debt, corruption and sustainable economic growth. Sustainability, 9(3), 433. doi:10.3390/su9030433

- Krugman, P. (1988). Financing vs forgiving a debt overhang. Journal of Development Economics, 29(3), 99–104. doi:10.1016/0304-3878(88)90044-2

- Lee, S., Park, H., Seo, M. H., & Shin, Y. (2017). Testing for a debt-threshold effect on output growth. Fiscal Studies, 38(4), 701–717. doi:10.1111/1475-5890.12134.This

- Liaqat, Z. (2019). Does government debt crowd out capital formation? A dynamic approach using panel VAR. Economics Letters, 178, 86–90. doi:10.1016/j.econlet.2019.03.002

- Lim, J. J. (2019). Growth in the shadow of debt. Journal Of Banking And Finance, 103, 98–112. doi:10.1016/j.jbankfin.2019.04.002

- Maitra, B. (2019). Macroeconomic impact of public debt and Foreign Aid in Sri Lanka. Journal of Policy Modeling, 41(2), 372–394. doi:10.1016/j.jpolmod.2019.03.002

- Mhlab, N., & Phiri, A. (2019). Is public debt harmful towards economic growth? New evidence from South Africa. Cogent Economics and Finance, 7(1). doi:10.1080/23322039.2019.1603653

- Modigliani, F. (1961). Long-run implications of alternative fiscal policies and the burden of the national debt. Economic Journal, 71(284), 730–755.

- Moher, D, Liberati, A, Tetzlaff, J, & Altman, D. G. (2009). Preferred reporting items for systematic reviews and meta-analyses: the prisma statement. Plos Med, 6, 7. doi: 10.1371/journal.pmed.1000097

- Onafowora, O, & Owoye, O. (2017). Impact of external debt shocks on economic growth in nigeria: a svar analysis. Economic Change and Restructuring, 52(2), 157–179. doi: 10.1007/s10644-017-9222-5

- Ono, T., & Uchida, Y. (2018). Human capital, public debt, and economic growth: A political economy analysis. Journal of Macroeconomics, 57(March), 1–14. doi:10.1016/j.jmacro.2018.03.003

- Pegkas, P. (2018). The effect of government debt and other determinants on economic growth: The Greek experience. Economies, 6(1), 10. doi:10.3390/economies6010010

- Pegkas, P. (2019). Government debt and economic growth: A threshold analysis for Greece. Peace Economics, Peace Science and Public Policy, 25(1), 1–7. doi:10.1515/peps-2018-0003

- Ramos-Herrera, M. C, & Sosvilla-Rivero, S. (2017). An empirical characterization of the effects of public debt on economic growth. Applied Economics, 49(35), 3495–3508. doi: 10.1080/00036846.2016.1262522

- Reinhart, C. M., Reinhart, V., & Rogoff, K. (2015). Dealing with debt. Journal of International Economics, 96(S1), S43–55. doi:10.1016/j.jinteco.2014.11.001

- Shahor, T. (2018). The impact of public debt on economic growth in the Israeli economy. Israel Affairs, 24(2), 254–264. doi:10.1080/13537121.2018.1429547.

- Shkolnyk, I., & Koilo, V. (2018). The relationship between external debt and economic growth: Empirical evidence from Ukraine and other emerging economies. Investment Management and Financial Innovations, 15(1), 387–400. doi:10.21511/imfi.15(1).2018.32

- Snieska, V., & Burksaitiene, D. (2018). Panel data analysis of public and private debt and house price influence on GDP in the European Union countries. Engineering Economics, 29(2), 197–204. doi:10.5755/j01.ee.29.2.20000

- Taher, H. (2017). The impact of government debt on economic growth: An empirical investigation of the Lebanese market. International Journal of Euro-Mediterranean Studies, 10(1), 23–41.

- United Nations. (2018). Sustainable development goals. Retrieved from https://www.un.org/sustainabledevelopment/

- World Economic Forum. (2017). The global competitiveness Report 2017–2018. Geneva: World Economic Forum.