Abstract

rfManagement accounting system (MAS) helps managers to make decisions and control activities to achieve short-term and long-term goals. Based on Upper Echelons Theory (UET), this study examines the impact of dynamic environment on CEO’s psychology characteristic (risk-taking propensity) that influences the choice of product innovativeness strategy and the level of using MASinformation. At the same time, this study also considers the moderator role of internal locus of control in some relationships. The research samples are CEOs in large manufacturing companies in Viet Nam. The PLS-SEM is used to test the hypotheses. The results showed that all the effects are significant. This study contributes to the existing literature of the UET in accounting field as it recognizes the important role of MASs, CEO’s risk-taking propensity and helps managers to design a MASs to operate firms effectively.

PUBLIC INTEREST STATEMENT

Psychological characteristics of upper managers have an important role impact on use management accounting system (MAS) information and choices of strategy. This study will explore and discuss about the causal role of environmental dynamic impact on risk-taking propensity of CEO and use management accounting system information to implement strategy choiced by upper managers, besides considering the role of CEO’s internal locus of control (a psychological characteristics of CEO) in that process. The results of our study suggest that the using of an effective MAS information suitable with CEO’s psychological characteristics can enhance organizationals’ performance (i.e. enterprises operating in a transitional economy such as that of Viet Nam), that wish to establish a business in a transitional economy in the Asian block (e.g. like Viet Nam) by companies in the Anglo-American block (e.g. Australia, United Kingdom, United States).

1. Introduction

The management accounting system (MAS) plays an important role in transforming the organization’s strategy into desired behaviors and results (Hoque, Citation2011). MAS is used by many business managers to improve and systematize the quality of information gained from the external and internal business environment (Naranjo-Gil & Frank, Citation2007).

Previous studies have examined how MAS design affects the behaviors of organizational members (e.g. Hall, Citation2011) and the organization’s results (for example, Guenther & Heinicke, Citation2019). However, there are still very few studies examining the antecedence variables that affect the MAS, especially characteristics from the outside environment and of the managers (e.g. CEO).

A dynamic environment is characterized by the uncertainty of the environment that limits the ability of managers to make decisions (Soin & Paul, Citation2013), so that managers try to balance the uncertainty in decision-making process. To do this, managers need a support system to make decisions. With that in mind, Galbraith (Citation1977, p. 4) argued that: “the greater the uncertainty of the task, the greater the amount of information that has to be processed between decision makers during its execution” and Scapens and Jazayeri (Citation2003) implied the key role of management accounting in the twenty-first century to integrate various sources of information, explain the link between implementation measures and results of each measures. Therefore, it is necessary to consider the impact of a dynamic environment on CEO’s managerial risk-taking propensity, product innovation strategies and MAS information usage levels.

Although the propensity of CEO’s risk-taking in decision-making process has been studied in strategic management field (Wangrow, Schepker, & Barker, Citation2015), this psychological characteristic of CEO is still limited in the accounting field. Besides, some studies focus only on the important roles, which are the effects on the success of implementation strategies (Jespersen & Bysted, Citation2016), and the choices of strategy (Hambrick & Mason, Citation1984; Zor, Linder, & Endenich, Citation2019), of the demographic characteristics of executives. In particular, the ILOC (Internal Locus of control) identified by Hambrick and Finkelstein (Citation1987) has a moderating role in the relationship between the upper managers’ characteristics and the organization’s outcomes/choices strategy, but it is not considered in studies of financial accounting and management accounting (Plöckinger, Aschauer, Hiebl, & Rohatschek, Citation2016; Wangrow et al., Citation2015). The characteristic of upper managers will determine the behavior of them (Hambrick & Mason, Citation1984) and then will affect the entire organization. This study will show the using level of MAS information of CEO to present the importance of this system. As a result, MAS adjustments are performed to fit the organization’s outside environment, managerial risk-taking propensity personality and product innovation strategy.

Upper Echelons Theory (UET) was first introduced by Hambrick and Mason (Citation1984), then extended and supplemented by Hambrick and Finkelstein (Citation1987), Hambrick (Citation2007). Recently, this theory has been gradually been used in the field of management accounting but still very limited (Zor et al., Citation2019). Based on UET, this research will explore the impact of a dynamic environment on CEO‘s characteristics (managerial risk-taking propensity) in decision-making processes, choices of product innovation strategies and using MAS information. The moderator role of ILOC in the research model will also be considered.

Current research contributes to the theory in the field of management accounting in several ways. This is the first study in which the author examines the relationship between the dynamic environment, the managerial risk-taking propensity, the use of MAS information and the choices of organization’s product innovation strategy in the same research model for analysis. At the same time, the ILOC’s moderator role is also considered in some relationships. Besides, Viet Nam is a transitional economics which from a planned economy to a market-based one “changes fundamental managerial assumptions, criteria and decision making, and represents a genuine transformation of the business” (Justin Tan & Litsschert, Citation1994, p. 3), which requires a fundamental shift of paradigm and mentality that thrives on chaos. Information, specially is regulatory information was difficult to obtain, and even when such information was available, it appeared to be too general and vague to help managers plan business activities because demands often came from various government agencies and were in many instances contradictory to each other, it is completely opposite with western. When implementation strategy, management accounting will help upper managers have suitable information (broad scope predict future, which aggregated and integrated in timely). So, choices of Viet Nam firms to investigate the extent to use MAS information are so important. In addition, in transitional economies like Viet Nam, the relationship between the characteristics of upper managers—the choice of strategy—use of MAS information in Viet Nam firms is still not be concerned by the researcher. Therefore, it is necessary to consider the above relationship in Viet Nam firms. The results of our study suggest that the using of an effective MAS information can enhance organizational s’ performance across national boundaries (i.e. enterprises operating in a transitional economy such as that of Viet Nam), that wish to establish a business in a transitional economy in the Asian block (e.g. like Viet Nam) by companies in the Anglo-American block (e.g. Australia, United Kingdom, United States).

The paper is structured as follows. The next two sections define the founded theory and develop the theoretical model ending with testable hypotheses. This is followed by the results and discussion. The final section identifies the limitation of this study and provides some directions for further study.

2. Literature review and hypothesis development

2.1. Upper Echelons Theory (UET)

UET was first introduced by Hambrick and Mason (Citation1984) and gained a lot of attention because it was a theory that explored aspects of human nature, such as demographic and psychology influencing the decisions of senior managers (Upper echelons) (Wangrow et al., Citation2015). More specifically, the characteristics of upper managers can be of two types: observable traits and psychological traits. Observable characteristics include demographics and job-related aspects such as age, job term, educational and functional background, socio-economic origin and financial status (Hambrick & Mason, Citation1984). Psychological features include a set of executive values, perceptions and personality characteristics (Carpenter, Geletkanycz, & Sanders, Citation2004).

In the model of UET (Figure ), we can see that the personality of upper managers will impact on Product innovation and Administrative complexity (MAS can be seen as Administrative complexity (Hambrick & Mason, Citation1984)). Besides that, the personality of upper managers will be affected by the external environment and dynamic environment is a characteristic of the external environment.

Figure 1. Conceptual model of upper echelons theory. Adjusted from Hambrick and Mason (Citation1984, p. 198)

CEO’s risk-taking personality traits have been overlooked in some studies (Wangrow et al., Citation2015). However, they are extremely limited in the field of accounting. In addition, UET pointed out that the characteristics of upper managers were influenced by the internal and external environment of the organization. Nevertheless, the combination of an external environment, that is a dynamic environment with personality characteristics tending to accept risks, and the use of MAS information has not been considered. On the other hand, UET was updated by Hambrick (Citation2007) to moderate the relationship between senior management characteristics and the way of the organization’s strategy/results. Therefore, based on UET, this study examines the impact of a dynamic environment on CEO risk-taking, using MAS information behavior and choice of product innovation strategy.

2.2. Management accounting system

The MAS can be considered as an outcome of an organization or an aspect of the organizational structure (Chenhall, Citation2003; Strauß & Zecher, Citation2013) and is also considered as a complex administrative system (Agbejule, Citation2005; Bouwens & Abernethy, Citation2000; Chenhall & Morris, Citation1986). MAS is often defined as systems that create management accounting information for internal users. According to Chenhall and Morris (Citation1986), MAS has four aspects: broad scope, timeliness, aggregation, and integration. In particular, broad scope information includes a wide range of information relating to the organization, that provides the nature of financial and historical information, as well as providing external, non-financial and future orientation including probabilistic data (which may or may not occur because of prediction only). Timeliness refers to the provision of required information and the frequency of reporting information, which are collected from the system and characterized by the high-frequency existence of reports and the rapid response to the environment. Aggregation refers to the aggregation of information corresponding to different functional parts of the organization over time. Finally, integration information relates to interactions between interdependent departments, and integrated information getting from sharing information within departments.

2.3. Dynamic environment

Currently, there are many definitions of a dynamic environment. Dess and Beard (Citation1984) defined that dynamic environment is characterized by a rapid and unpredictable change, which increases the uncertainty or an uncertainty for individuals and organizations operating in that environment, while Li and Liu (Citation2014) presented that dynamic environment is a volatility (i.e. the speed of change and innovation) as well as an uncertainty or an unpredictability of competitor actions and a demand of customers. Besides that uncertainty is a key contextual factor that affects the decision-making (Sniazhko, Citation2019). As a result, individuals in this environment are likely to suffer extreme stress and anxiety (Waldman, Ramirez, House, & Puranam, Citation2001). Therefore, they need help from highly predictable and timely information, as well as aggregation and integration information from various sources.

2.4. Managerial risk-taking propensity

According to Sitkin and Weingart (Citation1995), risk propensity can be defined as an individual’s current propensity toward risk-taking or risk-avoiding. Lopes (Citation1987) pointed out that risk-taking propensity has an important influence on an individual’s decision-making situations and behaviors of them. Risk-taking is not a gamble that individuals, when making risky decisions, can still control risks (March & Shapira, Citation1987). In other words, decision makers are risking but have to win more than lose (Shapira, Citation1986). Risk is a fundamental part of the business because an executive cannot know for sure whether the new product they deliver to the market can meet consumer needs, or profit can be determined before introducing new products or services (Tang & Tang, Citation2007). However, business owners or upper managers, who are more adventurous, have more appropriate actions and are better in governance (Brockhaus, Citation1980). In this study, the propensity of risk-taking is a willingness of CEO to commit resources significantly, force towards exploiting opportunities or lead to uncertain outcomes (Keh, Der Foo, & Lim, Citation2002). In addition, Prospect Theory is a theory of individual behavior predicts individuals’ choices in decisions that involve risk, it descriptives model of decision-making under risk and it was built by Kahneman and Tversky (Citation1980). In developing the theory, Kahneman and Tversky (Citation1980) relied on controlled experiments that offered individuals choices between alternatives, each of which contained possible outcomes and their respective probabilities of occurrence. Risk describes a situation in which an individual making a choice knows both the potential outcomes of each available option and the probabilities that those outcomes will occur. It is stated that individuals sometimes evidence risk-seeking, rather than risk-averse and suggested that individuals are often risk seeking and risk averse for gambles involving outcomes below (Kahneman & Tversky, Citation1979). After 30 years, Prospect Theory is used a lot in economics behavioral researches of decision-making under risk. From the content of this theory, we have enough evidence to say that individuals who risk-seeking in decision-making will impact on the outcomes of the decision.

2.5. Product innovativeness

Innovation can enhance economic success for companies and countries alike (Nathai-Balkissoon, Maharaj, Guerrero, Mahabir, & Dialsingh, Citation2017). Among many conditions to achieve the performance of management and organization, product innovation is considered as a decisive factor, because introducing new products has become a vital competitive weapon of every business organization (Katila & Chen, Citation2008). On the other hand, product innovation is an important mechanism for the organizations to adapt the environment (Tushman, Smith, Wood, Westerman, & O’Reilly, Citation2007). Product innovation is considered as an application of a new technology or a combination of commercially introduced technologies to meet user or market needs (Utterback & Abernathy, Citation1975). “Innovation is truly new to both the company and the market and is described as a new product in the world” (Olson, Walker, & Ruekert, Citation1995). In a dynamic environment, organizations need to constantly refresh themselves and adapt to environmental changes by introducing new products. In this research, product innovativeness is seen as innovativeness at the industrial and domestic level.

2.6. Internal locus of control

Managerial discretion, which is the level of influence of administrators, can be defined as the latitude of managerial action being available to a decision maker (e.g. a top manager) in a given situation (Hambrick & Finkelstein, Citation1987). Higher discretion enables leaders with a wider range of options (Campbell, Campbell, Sirmon, Bierman, & Tuggle, Citation2012), and a greater latitude of action (Hambrick & Eric, Citation1995). UET indicated that managerial discretion has a moderator role in the relationship between demographic characteristic of upper managers and choice of strategy and outcomes. Managerial discretion includes three factors: (1) individual factors, (2) organizational factors and (3) environmental factors (Hambrick & Finkelstein, Citation1987). Individual factors, that affect managerial discretion, are particularly less noticeable (Wangrow et al., Citation2015). Focusing on strategic behavior (Powell, Lovallo, & Fox, Citation2011), this study focuses on the individual level representing for managerial discretion. Related to the individual level, locus of control is one psychological manager's characteristic that may influence managerial discretion (Hambrick & Finkelstein, Citation1987; Wangrow et al., Citation2015). LOC includes two components: externals and internals of LOC, in which, CEO intended ILOC who believes that the events occurring in their lives are largely dependent on their own actions and efforts. Boone, De Brabander, and Van Witteloostuijn (Citation1996) indicated that ILOC represents the action of “persistent attempt[s] to control the environment”. CEO’s ILOC is essential to explain strategic leadership and “CEO’s role of formulator and implementer”. There are many reasons why this study chose ILOC is moderator in proposed mode: (1) ILOC scale is one moderate variable indicated in UET (Finkelstein & Hambrick, Citation1990) but still not concerned in researches based on UET in accounting field; (2) it is not only explain upper managers more efficient processors of information (Lefcourt, Citation1982), but also moderator behavior of upper managers when choosing a strategy. So ILOC will be better equipped to see the relationship between CEO ‘s risk-taking propensity characteristic and outcomes/choice strategy (MAS, Product innovativeness). Based on all of the above reasons, this study selects ILOC as a variable that moderates the relationship between the risk-taking propensity and the use of the CEO’s MAS, and the choices of strategic product innovation.

2.7. Hypothesis development

2.7.1. Impact of dynamic environment on CEO’s risk-taking propensity

Companies must maintain close observation with various volatile factors such as technological innovation, threats from new entrants and risks inherent from suppliers (Oktemgil & Greenley, Citation1997). If managers wait for stability and completeness, it will be difficult for businesses to earn profits or even affect the development of a new business area or new business opportunity (Vahlne, Hamberg, & Schweizer, Citation2017). Therefore, the CEO’s risk-taking personality as an action to balance the environmental dynamics or instability (Vahlne & Johanson, Citation2013). A few recent papers shed some light on the instability and impact of upper managers’ behavior such as strategic choices and resource allocation (Kim & Aguilera, Citation2016). Although some studies indicated that managers would not willing to take risk investment or decrease investment under dynamic environment (Leahy & Whited, Citation1995; Pindyck, Citation1993). However, this view is the investment side, this study concern managerial risk-taking propensity in strategy side. In this perspective, Gupta and Govindarajan (Citation1984) suggested that different strategies result in facing task environments that vary in their level of uncertainty and that implementing a particular strategy will require different levels of managers' risk-taking depending on the associated with uncertainty.

Thus, it can be seen that the more dynamic of the environment or the more uncertainty, the more likely the CEO will be to take risks in order to balance the uncertainty and create benefits and gain opportunities for businesses. Thus, it can be hypothesized that:

H1: High dynamic environment has positive impact on risk-taking propensity of CEO.

2.7.2. Impact of dynamic environment on CEO’s using MAS information

An organization operating in a highly dynamic environment can be caused changes of suppliers, buyers, the overall competitive environment and the competitive nature, which can be a challenge for the organization (Petrus, Citation2019). Therefore, in a dynamic environment, managers should also seek more information to allocate appropriate resources, perform more sophisticated and in-depth analyzes, make timely decisions and based on that information and develop organizational flexibility based on that information (Oktemgil & Greenley, Citation1997). Broad scope information related to financial, non-financial, records of past activities and forecasts of the future both inside and outside the organization is very important for management decision-making (Mia & Chenhall, Citation1994), especially for organizations that are facing a highly dynamic environment. This type of information is very important (Abernethy & Guthrie, Citation1994). In addition, environmental uncertainty has a positive impact on the usefulness of broad-scope information and timely information, which affect the managerial decision (Chenhall & Morris, Citation1986; Mia & Patiar, Citation2001). As such, organizations need accounting information to consider the cost structure to support managers within the organizations. Consequently, they can establish an effective way to deal with relevant businesses in the market and also manage the changing needs of customers for their products and services (Huefner & Largay, Citation2008). To do this, MAS information needs to be integrated and aggregated from different parts to have the most comprehensive information to deal with the dynamic of the environment, reduce the risk that the environment can cause for the organization.

H2: High dynamic environmental have positive impact on the use of MAS information.

2.7.3. Impact of dynamic environment on choices of product innovation strategy

Individuals, who tend to accept high risks, feel comfortable when making decisions in uncertain situations (Chan, Yee, Dai, & Lim, Citation2016). Competition in the form of rapid changes in production technology has the largest overall impact on innovation, and is positively correlated with most innovation (Moen, Tvedten, & Wold, Citation2018). In a dynamic environment with frequent and rapid changes, the consideration of customer demand, products, processes and technologies is obsolete and it is known that these changes have different effects on the organization’s product development function (Chong & Chong, Citation1997). Therefore, businesses must increase awareness of change, for example, if customer’s needs change, companies should make some necessary adjustments to suit that circumstance (Li & Liu, Citation2014), changing products for an instant highly dynamic environment impacts technology innovation and product innovation (Papadakis & Bourantas, Citation1998). Therefore, the more dynamic environment provides an incentive to further improve existing processes or develop new products (Chan et al., Citation2016).

H3: Dynamic environment has positive impact on product innovativeness

2.7.4. Impact of risk-taking propensity on CEO’s use of MAS information

To cope with risks, upper managers (including the CEO) need an assisting tool in the decision-making process. The literature shows that upper managers have different perceptions of the range of information, that they deem useful in making strategic decisions (Finkelstein & Hambrick, Citation1990); and is especially valued for those who have the propensity to make high-risk strategic decisions (Jensen & Zajac, Citation2004). In this case, MAS not only plays an important role in measuring risk (including risk aggregation, risk reporting and risk monitoring) but also reduces uncertainty in management decision-making (Winter, Citation2007) and supports risk management activities (Collier, Berry, & Burke, Risk and control: drivers, practices and consequence, Citation2004). In this same line of study, Zaleha Abdul Rasid, Ruhana, and Khairuzzaman Wan Ismail (Citation2014) showed that risk management activities have a positive relationship to the four dimensions of MAS because the MAS information includes broad scope, integrated, aggregated and very timely information (Agbejule, Citation2005; Chenhall & Morris, Citation1986).

Risk management activities are needed a holistic view of risk while broad scope information with forward-looking helps CEO to deal with uncertain future events caused by the environment. Timely information is also needed to respond to risks. In addition, integrated information assists the CEO to identify the impact of the decisions. They have made and aggregated information also accelerates the decision-making process. Therefore, when CEOs tend to accept risks, they will perform more risk management, consequently resulting in increasing the use of MAS information in four dimensions.

H4: CEO’s Risk-taking propensity will have positive impact on the use of MAS information.

2.7.5. The impact of CEO ‘s risk-taking propensity on product innovativeness

An enterprise need to assess risk at the early stages of new product development (Goswami, Citation2018). Based on UET, strategic choices are influenced by demographic and psychological characteristics (Hambrick & Mason, Citation1984). In psychological characteristics, the personality of upper managers with propensity of risk-taking is special in accordance with a risky-strategic choice. Personality of risk-taking encourages the conduct of risky behaviors that should have a positive relationship to innovation activities (Arrow, Citation1962), as well as encouraging the implementation of innovative ideas aimed at high variation in organizational output (March, Citation2010). Therefore, the risk-taking propensity promotes the ability to create new products. Catmull (Citation2008, p 66) showed that “Governance is not risk prevention but rather to building resilience when failure occurs”. Accordingly, creating innovative products requires managers to take risks and accept failures (Jaworski & Kohli, Citation1993). On the other hand, new product development requires new ideas (Park, Chang, & Park, Citation2015) and new product development propensity must succeed, so it requires organizations to allocate resources to the project with uncertain amounts (Miller & Friesen, Citation1983).

CEO’s risk-taking propensity refers to the CEO’s willingness to commit important resources to exploit opportunities or engage in behaviors with uncertain results (Keh et al., Citation2002). This personality can be identified as a driving force for innovation, so the CEO’s risk-taking propensity personality is an important factor in strategic decision-making (March & Shapira, Citation1987). Besides, in the financial sector, the CEO’s risk-taking propensity is related to the innovation of a new product portfolio (Talke, Salomo, & Kock, Citation2011). In a nutshell, the decision to choose product innovativeness is a risky action. Therefore, this choice fits the CEO’s propensity to take risks.

H5: CEO ‘s risk-taking propensity has positive impact on product innovativeness.

2.7.6. The impact of product innovativeness on the use of MAS information

Customize strategy is a strategy that allows the properties of the product/service produced by the business unit can be changed and selected according to customer needs. Focusing on the extent to which an organization is willing or able to make changes products or services according to “customer requirements” (Abernethy & Lillis, Citation1995). Customization mentioned in the study of Abernethy and Lillis (Citation1995) is a continuous product change in which customization is highest when the product/service is completely customized to suit customer requirements. Therefore, the customization strategy, which is similar to the product innovativeness strategy of product characteristics, is changed. In addition, Bouwens and Abernethy (Citation2000)’s results showed that customization strategies have a positive impact on the use of MAS information on four aspects. On the other hand, organizations wishing to pursue a product innovativeness strategy need to make daily decisions on a wide range of issues and therefore need timely, integrated, aggregated and broader information (Bouwens & Abernethy, Citation2000; Chenhall & Morris, Citation1986). For the risks of dealing with future events, a wide range of MAS such as future-oriented, timely information are needed to respond to risks. The impact of a number of decisions can be identified. Data integration is a key challenge for risk management and information aggregation accelerates the decision-making process (Zaleha Abdul Rasid et al., Citation2014). In addition, to face the possibility of product innovativeness, MAS supports risk management activities (Soin & Paul, Citation2013). MAS also plays an important role in measuring risk (including risk aggregation, risk reporting and risk monitoring) and communication. Information provided by MAS reduces uncertainty in management decision- making (Winter, Citation2007). So it will helpful in the implementation product innovativeness process.

H6: Product innovativeness has positive impact on the use of MAS information.

2.7.7. The moderating role of Internal Locus of Control (ILOC)

UET believes that the impact of the CEO’s personality on choices of strategy is stronger when the managerial discretion is higher (Finkelstein & Hambrick, Citation1990). CEOs with high ILOC are better in coping with complex and unstable environments (Miller & Friesen, Citation1982) and minimize performance degradation because CEOs with higher ILOCs, who are better in managing emotional conditions, can moderate and minimize personalization, increase professionalism (Sirén, Patel, Örtqvist, & Vincent, Citation2018) and differentiate leadership skills, that enable the CEO to persuade more frequently the behaviors of others in organizations to implement product innovation strategy together, and believe in their ability in order to impact the environment (Boone et al., Citation1996). On the other hand, the power of the CEO is positively related to the level of risk-taking (Lewellyn & Muller‐Kahle, Citation2012). Risk takers believe in their ability to control the appearance of risks or the bad outcomes more than those who avoid risk (Meertens & Lion, Citation2008). In addition, a review of Wangrow et al. (Citation2015) indicated that companies that choose and pursue an innovative strategy must have the highest discretion because the risk of this strategy type. In the same direction, this study suggests that product innovation decisions are also risky. Therefore, we have sufficient grounds to say that as the CEO’s confidence within himself increases, the CEO’s choice of product innovativeness becomes stronger. Combined with the hypothesis H5 above, when the risk-taking trend is higher, the CEO will increase the choice of product innovation strategy. Therefore, the positive relationship between the CEO’s risk-taking propensity and product innovation options will increase as the CEO’s ILOC increases.

H7a: A CEO’s ILOC will influence the positive association between the higher risk-taking propensity of CEO and the choice of product innovativeness such that this positive association will be stronger when the CEO has higher ILOC.The hypothetical relationships between each of the variables examined in this study are next depicted in Figure .

Figure 2. Proposed model

UET has pointed out that impact between upper managers characteristics and the organization’s outcomes that is governed by ILOC (Hambrick & Finkelstein, Citation1987). When implementing the chosen product innovativeness strategy, the CEO needs a system to control whether the work is carried out and acted timely as planned if the job is not as they expected. At the same time, this system must match their personality. ILOC-oriented CEOs are more likely to know when information is relevant and when it is not (Lefcourt, Citation1982). MAS is considered as a preeminent technology to integrate diverse activities from the creation of strategies, implement those integrated activities and provide clear accountability (Otley, Broadbent, & Berry, Citation1995). MAS can also be a possible ability to aggregate and integrate information among different parts of an organization (Collier, Citation2015). In addition, ILOC’s moderating role has a positive impact on the relationship between environmental uncertainty and the usefulness of MAS information (Fisher, Citation1996). Therefore, we can say that the more MAS information is useful and consistent with the CEO’s risk-taking propensity, the more ILOC’s moderating role-plays. Combined with hypothesis H4, the higher the CEO’s risk-taking propensity, the greater the CEO uses MAS information, and the relationship increases as the CEO’s ILOC increases.

H7b: A CEO ‘s ILOC will influence the positive association between the higher risk-taking propensity of CEO and the use of MAS information such that this positive association will be stronger when the CEO has higher ILOC.

3. Research method

3.1. Sample and data collection

This study, conducted in Viet Nam, an emerging economy, features a data set of 139 large manufacturing firms in Viet Nam. The sample was restricted to those firms because they possess sufficient financial resources to operate and implement the innovativeness strategy and functions of MAS. To include such specific manufacturers in the studied sample, a convenience-sampling approach has been used to identify potential participants. The CEOs were considered capable of providing information about their use of the MAS information in managerial decision-making (Chenhall & Morris, Citation1986), and about their perception and choice of strategic. Small companies were excluded because the MAS in these enterprises was not likely to be comprehensive. According to Degree 56/2009/NĐ-CP (Vietnamese Government, 2009), medium and large companies must have total assets of more than 20 billion Dong (Vietnamese currency) or more than 200 employees (for industry and construction sectors).

E-mail surveys were, then, distributed to CEOs. Interviews were conducted by telephone or face-to-face with CEOs from different large manufacturing Vietnamese business organizations. The survey questionnaires targeted 2,000 managers, whose email addresses and phone numbers had been collected from websites of enterprises, the Department of Planning and Investment, and the Businessperson Association. An invitation letter with a link to the web-based survey was sent to CEO s’ email addresses. The content of survey include two parts: (1) The first part will represent information of CEO (Age, Education, Tenure, Experience, Position of response in firm, type of business of the company), the study will eliminate the feedback was not as CEO and not the manufacturing sector and (2) The CEO will respond to the scales (presented in the appendix) regarding the research model.

Managers, who received the invitation letter, agreed to participate by clicking on the link to the web-based questionnaires to choose responding by email or face to face interview. Every 2 weeks in 3 months after the initial invitation letter, reminder letters were sent to encourage responses. If CEO chooses face to face interview, we will take an appointment. Out of 462 managers, who accepted to participate, there were only 216 answered the questions (92 CEOs answered questionnaire by E-mail, 95 CEOs had face to face interview and 29 CEOs had phone interview). One hundred and seventy-four out of these 216 participants completed the questionnaires (in which 71 CEOs completed questionnaires by E-mail, 82 CEOs used questionnaires by face-to-face method, 21 CEOs completed by telephone). Next, 27 responses from managers in small enterprises were excluded. Eight outlier cases were removed from the data. Finally, 139 cases were used for data analysis providing a response rate of 35.5%.

3.2. Variables measurement

The scales of environmental dynamism are quite mature from two perspectives. One measures environmental elements, and the other indicates the characteristics of key environmental factors. Based on research of Li and Liu (Citation2014), this study used four items as key environmental factors considering the effects of industrial environment, competitor behaviors, technological progresses and customer demands. CEO risk-taking propensity was measured by the four-item anchored scale adapted by Kraiczy, Hack, and Kellermanns (Citation2015) from Covin and Slevin (Citation1989) entrepreneurial strategic posture scale. The original construct contained nine items focusing on innovation, proactiveness, and risk-taking. To exclusively measure CEO risk-taking propensity, five of these items were excluded. The use of parts of wider multidimensional constructs was shown to yield valid and reliable results (Kraiczy et al., Citation2015). MAS information use was measured following Agbejule (Citation2005), Chenhall and Morris (Citation1986) using CEO’s “extent of use” of Likert 5-points in terms of broad scope (four items), integration (four items), timeliness (four items), and aggregation (three items) in their respective organizations. Product innovativeness was measured by the multi-item 7-point Likert scale with the degree to which the products, that a company introduced in the past few years, were new to the firm, the industry, and the market (Song & Chen, Citation2014). This research based on Mueller and Thomas (Citation2001)’s measurement of LOC (See Appendix ).

4. Results

SPSS24 is used for basic statistical analysis. Partial least squares structural equation modelling (PLS-SEM) is used primarily for path analysis (Wold, Citation1980). The analysis process consists of 2 steps, assessing the measurement model and assessing the structural model (Hair, Hult, Ringle, & Sarstedt, Citation2017).

4.1. Respondents profile

Table shows the demographics of the participating respondents. The final sample reflects 76 % of male CEOs and 24% of female CEOs, which is only 1/3 compared to the number of male in the survey sample. Average tenure of the respondents in 13 years indicates that they have adequate experience to represent their firms to answer the survey. The sample comprises 6% less than undergraduates, 58% undergraduates, and 37% post-graduates. It shows that most of CEO’s education background are undergraduates. Average age of the respondents is 53 years old.

Table 1. Sample demographic characteristics

4.2. Measurement model

To evaluate the problem of common method bias, the Harman’s single factor test was employed. A un-rotated factor analysis accompanied on all measurement constructs (except for age and education) to extract 7 factors. Total cumulative variance of 7 factors is 75.6%. The first factor is only accounted for 35.76%. Therefore, the errors of total cumulative variance of the whole model (<50%) is not a serious problem in this study (Podsakoff, MacKenzie, Lee, & Podsakoff, Citation2003).

Scale reliability is assessed through internal reliability, which is expressed through Cronbach’s alpha, composite reliability (Hair et al., Citation2017; Nunnally & Bernstein, Citation1994) and rhoA (Dijkstra & Henseler, Citation2015). Convergent validity is evaluated through the outer loading of observed variables and average variance extracted (AVE). Outer loading greater than 0.7 and AVE greater than 0.5 are acceptable (Hair et al., Citation2017). Data are run bootstrap 5.000 times to evaluate the statistical significance of the data (Hair et al., Citation2017).

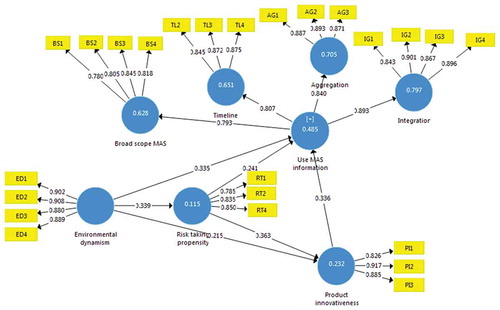

The results in Table show that the scales have factors, which are Cronbach’s alpha, composite reliability and rhoA greater 0.5. Thus, the scales reach the required reliability (Hair et al., Citation2017; Nunnally & Bernstein, Citation1994). The result of convergent validity presents that TL1 variable has an outer loading of 0.64 and RT3 has outer loading of 0.66 (<0.7), which should be excluded from the model. After excluding TL1 and RT3 variables, the AVE value range of scales is greater than 0.5 and the outer loading of the observed variables is greater than 0.7, so the scale reaches convergence value (Figure ).

Table 2. Scale Accuracy Analyses

Discriminant validity of the scale is evaluated through the factor including cross-loading, Fornell-Larker criterion and HTMT ratio (Heterotrait-monotrait ratio) (Hair et al., Citation2017; Henseler, Ringle, & Sarstedt, Citation2015). As can be seen from the results, cross-loading coefficient in its structure is much larger than in other structures. Fornell-Larcker criterion results (Table ) show that the square root of AVE of each structure is greater than the correlation coefficient between the structures. In addition, the value of HTMT (Table ) is less than 0.9 ensuring the discriminant value of the scale.

Table 3. Fornell-Larcker criterion

Table 4. Heterotrait-Monotrait Ratio (HTMT)

4.3. Structural model

Variance-inflating factor (VIF) is used to evaluate multi-collinearity between independent variables (Hair et al., Citation2017). Because there are many dependent variables, the research model is classified into 3 models with 1 dependent variable. The remaining scales have VIF < 2, so they do not appear to be multi-collinearity.

Coefficient of determination (R2) is a common measure to assess the predictive capability of the independent variables. Results in Table show that R2 values of risk-taking propensity and product innovativeness are weak (R2 Risk-taking propensity = 0.115; R2 Product innovativeness = 0.232), MAS variables can be considered to have enough level of prediction (R2 of Use MAS information = 0.485) (Hair et al., Citation2017).

Table 5. Hypotheses testing results

Besides, predictive relevance (Q2) is also used to evaluate the out-of-sample predictive power. The results of Table also show that the Q2 coefficients of the dependent variables are greater than zero. Thus, they support the model’s predictive capacity (Hair et al., Citation2017).

To test the statistical significance of the regression coefficients, this study performed the bootstrap procedure 5,000 times as suggested by Hair et al. (Citation2017). Table presents that the relationships in the theoretical model (from H1 to H6) are statistically significant with more than 95% confidence.

Figure 3. PLS-SEM analysis results of the theoretical model

Testing the moderating roles of the internal locus of control on the impact of risk-taking propensity and product innovativeness on the use of MAS information is considered as the main objective of this study. Evaluation of measurement model with the presence of moderating variables indicates that internal locus of control measurement concepts is reliable (Cronbach’s alpha = 0.877, composite reliability = 0.907 and value AVE = 0.787, square root 2 of AVE of ILOC is greater than the correlation coefficient between the structures, HTMT < 0.9 and the confidence interval of the ILOC’s HTMT value does not contain 1).

Next, to assess the impact of the ILOC moderating variable, the two-stage approach of Chin, Marcolin, and Newsted (Citation2003) was used. Phase 1 estimated the main impact model while stage 2 multiples the moderating and exogenous variables to measure the interaction rank (Risk-taking propensity x internal locus of control).

Table shows that the internal locus of control plays a moderating role in the relationship between product innovativeness and the use of MAS information and ILOC also plays a moderating role between risk-taking propensity and the use of MAS information. Thus, when the internal locus of control increases, the impact of risk-taking propensity to product innovativeness and risk-taking propensity to the use of MAS information also increases. As such, H7a and H7b are supported.

Table 6. Tests for moderating effects

5. Discussion

All hypotheses are supported. In particular, the impact of risk-taking on product innovation is highest (0.363). As a moderator, ILOC moderator the relationship between risk-taking and product innovativeness (0.138) is higher than the relationship between risk-taking and MAS. With the results of the study, it can be seen that under the impact of dynamic environmental, the higher dynamics the higher psychology risk-taking of CEO, and from this, risk-taking will impact the same way with the product innovativeness strategy and Use MAS of firms. In addition, MAS and product innovativeness will be effected directly by dynamic environment and this direct impact is quite large.

This study has the following theoretical implications. First, it is contributed as a follow-up of previous studies of the direct impact between dynamic environment and risk-taking propensity of CEO (Hambrick & Mason, Citation1984; Kim & Aguilera, Citation2016), MAS (Chenhall & Morris, Citation1986; Fisher, Citation1996; Huefner & Largay, Citation2008; Mia & Patiar, Citation2001) and product innovativeness (Hambrick & Mason, Citation1984). The results confirm again the positive impact of risk-taking propensity of CEO on product innovativeness and reinforcement for a previous study (March & Shapira, Citation1987). This study agrees with results of Zaleha Abdul Rasid et al. (Citation2014), which implies that the use of MAS information can reduce the risk of product innovativeness strategy so firms producing highly customized products are more likely to adopt broad scope MASs (Bouwens & Abernethy, Citation2000). Moreover, in uncertain environment, managers perceive the usefulness of traditional MAS in four perspectives (Chenhall & Morris, Citation1986). This result is suitable with UET proposed by Hambrick and Mason (Citation1984).

Second, the role of ILOC in decision-making of choosing product innovativeness strategy is an important personality’s characteristic of CEO. In this regard, different levels of MAS usage and choices of product innovativeness strategy across a psychology of CEO (risk-taking propensity) can be explained via the degree of CEO‘s ILOC in process of strategic decision-making, which has not been examined in previous studies. This study provides further empirical evidence of the important role of CEO’s internal Locus of control in decision-making choices of product innovativeness strategy and the use of MAS information proposed by Finkelstein and Hambrick (Citation1990) and Hambrick and Mason (Citation1984) of firms in an emerging economy like Viet Nam.

Finally, this study contributes to limited research on the psychology of CEO/marketing/accounting interface (Plöckinger et al., Citation2016) with the combination between environmental dynamism, risk-taking propensity of CEO, ILOC (a personality characteristics variable), choices of product innovativeness strategy (a marketing variable) and the use of MAS (an accounting variable) in the theoretical model. It would be necessary for MAS designers to comprehend the relevant moderating variables, that may occur in a particular MAS design in an organization. To do so, this study is based on UET to add to the extant literature on the management accounting field (Plöckinger et al., Citation2016).

6. Managerial implication

The findings of the study are in line with the findings of Hambrick and Mason (Citation1984) Upper Echelon Theory (UET). Therefore, the current study confirms the applicability of UET in the Viet Nam manufacturing sector. The study further emphasized the importance of management accounting in providing information to match organizational strategy implementation. Organizations adopting the product innovativeness emphasize competitor position and information, and product market moves and information. Besides, CEO in firms should consider the moderating role of ILOC in the relationships between the risk-taking propensity and MAS in order to determine the need of management accounting information and design MAS and between risk-taking propensity and choices of product innovativeness strategy to have suitable strategy to cope with dynamic environment such as change of customer needs, technological advances, competitors’ actions, which are unpredictable. Although environmental dynamism is a necessary condition for the use of MAS information and the choice of product innovativeness strategy, it can be integrated with the psychology of CEO. The study also has a practical significance because it provides CEO with implications on how to develop competitive advantages via designing MAS, suitable strategy in actual psychology characteristic of each CEO. This study provides guidance to CEO of firms not only to design and use MAS, but also to choose product innovativeness strategy toward enhanced performance suiting with their characteristics (CEO’s risk-taking propensity) and provided insights into the links between uses of MASs and product innovativeness strategy, accordingly, it was revealed that the implementation of product innovativeness will incentives CEO to use of MASs (in four perspective). The results of the study help the CEO of an organization to gain a better understanding of the potential uses of MASs for improving organizational performance, mainly relating to different types information of MAS. Thus, they can better adjust the use of MASs to suit the specific style of strategy implementation.

7. Directions for future research

This study is subjected to several limitations. Firstly, this cross-sectional study does not take into consideration of the possibility of causing and affecting the relationships between the research variables, which may involve certain time lags. Secondly, further research should take into account other components (such as labour markets, etc.), or moderating variables listed by (Hambrick & Finkelstein, Citation1987; Hambrick & Mason, Citation1984). Finally, this research just concentrated on risk-taking propensity of, but nowadays, lots of other psychology characteristics need to be concerned in the future. Future research should consider the above-listed limitations.

Acknowledgements

Researches would like to express our gratitude to all those who gave us the possibility to complete this study especially to University of Economics Ho Chi Minh City, Industrial University of Ho Chi Minh City, Viet Nam for providing a research grant for this study.

Additional information

Funding

Notes on contributors

Vo Tan Liem

Vo Tan Liem is a lecturer in Department of Accounting, Van Hien University, Viet Nam. At the moment, he is still in the final stage as a PhD Student at University of Economics Ho Chi Minh City, Viet Nam. His research interests are Management Accounting, Accounting Information Systems.

Nguyen Ngoc Hien

Dr. Nguyen Ngoc Hien received Doctor of Philosophy in Management from University of Economics Ho Chi Minh City, Vietnam. Working as a lecture at Faculty of Business Administration, Industrial University of Ho Chi Minh City, Vietnam. His research interests include organization behaviour, corporate social responsibility and organizational psychology.

Related Research Data

References

- Abernethy, M. A., & Guthrie, C. H. (1994). An empirical assessment of the “fit” between strategy and management information system design. Accounting & Finance, 34(2), 49–20. doi:10.1111/acfi.1994.34.issue-2

- Abernethy, M. A., & Lillis, A. M. (1995). The impact of manufacturing flexibility on management control system design. Accounting, Organizations and Society, 20(4), 241–258. doi:10.1016/0361-3682(94)E0014-L

- Agbejule, A. (2005). The relationship between management accounting systems and perceived environmental uncertainty on managerial performance: A research note. Accounting and Business Research, 35(4), 295–305. doi:10.1080/00014788.2005.9729996

- Arrow, K. J. (1962). Economic welfare and the allocation of resources for invention. In R. R. Nelson (Ed.), The rate and direction of inventive activity (pp.609). Princeton: Princeton University Press.

- Boone, C., De Brabander, B., & Van Witteloostuijn, A. (1996). CEO locus of control and small firm performance: An integrative framework and empirical test. Journal of Management Studies, 33(5), 667–700. doi:10.1111/joms.1996.33.issue-5

- Bouwens, J., & Abernethy, M. A. (2000). The consequences of customization on management accounting system design. Accounting, Organizations and Society, 25(3), 221–241. doi:10.1016/S0361-3682(99)00043-4

- Brockhaus, R. H. (1980). Psychological and environmental factors which distinguish the successful from the unsuccessful entrepreneur: A longitudinal study. In Academy of Management Proceedings, 1980(1), 368–372. doi:10.5465/ambpp.1980.4977943

- Campbell, J. T., Campbell, T. C., Sirmon, D. G., Bierman, L., & Tuggle, C. S. (2012). Shareholder influence over director nomination via proxy access: Implications for agency conflict and stakeholder value. Strategic Management Journal, 33(12), 1431–1451. doi:10.1002/smj.2012.33.issue-12

- Carpenter, M. A., Geletkanycz, M. A., & Sanders, W. G. (2004). Upper echelons research revisited: Antecedents, elements, and consequences of top management team composition. Journal of Management, 30(6), 749–778. doi:10.1016/j.jm.2004.06.001

- Catmull, E. (2008). How Pixar fosters collective creativity. Boston, MA: Harvard Business School Publishing.

- Chan, H. K., Yee, R. W., Dai, J., & Lim, M. K. (2016). The moderating effect of environmental dynamism on green product innovation and performance. International Journal of Production Economics, 181, 384–391. doi:10.1016/j.ijpe.2015.12.006

- Chenhall, R. H. (2003). Management control systems design within its organizational context: Findings from contingency-based research and directions for the future. Accounting, Organizations and Society, 28(2–3), 127–168. doi:10.1016/S0361-3682(01)00027-7

- Chenhall, R. H., & Morris, D. (1986). The impact of structure, environment, and interdependence on the perceived usefulness of management accounting systems. Accounting Review, 61(1),16–35.

- Chin, W. W., Marcolin, B. L., & Newsted, P. R. (2003). A partial least squares latent variable modeling approach for measuring interaction effects: Results from a Monte Carlo simulation study and an electronic-mail emotion/adoption study. Information Systems Research, 14(2), 189–217. doi:10.1287/isre.14.2.189.16018

- Chong, V. K., & Chong, K. M. (1997). Strategic choices, environmental uncertainty and SBU performance: A note on the intervening role of management accounting systems. Accounting and Business Research, 27(4), 268–276. doi:10.1080/00014788.1997.9729553

- Collier, P. M. (2015). Accounting for managers: Interpreting accounting information for decision making. Chichester: John Wiley & Sons.

- Collier, P. M., Berry, A. J., & Burke, G. (2004). Risk and control: Drivers, practices and consequence. Chartered Institute of Management Accountant. Oxford.

- Covin, J. G., & Slevin, D. P. (1989). Strategic management of small firms in hostile and benign environments. Strategic Management Journal, 10(1), 75–87. doi:10.1002/(ISSN)1097-0266

- Dess, G. G., & Beard, D. W. (1984). Dimensions of organizational task environments. Administrative Science Quarterly, 29, 52–73. doi:10.2307/2393080

- Dijkstra, T. K., & Henseler, J. (2015). Consistent partial least squares path modeling. MIS Quarterly, 39(2), 297–316. doi:10.25300/MISQ

- Finkelstein, S., & Hambrick, D. C. (1990). Top-management-team tenure and organizational outcomes: The moderating role of managerial discretion. Administrative Science Quarterly, 35, 484–503. doi:10.2307/2393314

- Fisher, C. (1996). The impact of perceived environmental uncertainty and individual differences on management information requirements: A research note. Accounting, Organizations and Society, 21(4), 361–369. doi:10.1016/0361-3682(95)00029-1

- Galbraith, J. R. (1977). Organization design. Boston: Addison Wesley Publishing Company.

- Goswami, M. (2018). An enterprise centric analytical risk assessment framework for new product development. Cogent Business & Management, 5(1), 1540255. doi:10.1080/23311975.2018.1540255

- Guenther, T. W., & Heinicke, A. (2019). Relationships among types of use, levels of sophistication, and organizational outcomes of performance measurement systems: The crucial role of design choices. Management Accounting Research, 42, 1–25. doi:10.1016/j.mar.2018.07.002

- Gupta, A. K., & Govindarajan, V. (1984). Business unit strategy, managerial characteristics, and business unit effectiveness at strategy implementation. Academy of Management Journal, 27(1), 25–41.

- Hair, J. F., Hult, G. T., Ringle, C. M., & Sarstedt, M. (2017). A primer on partial least squares structural equation modeling. Thousand Oaks: Sage.

- Hall, J. A., (ed.). (2011). Accounting Information Systems (7th ed.). Mason: SouthWestern Cengage Learning.

- Hambrick, D. C. (2007). Upper echelons theory: An update. Academy of Management Review, 32(2), 334–343. doi:10.5465/amr.2007.24345254

- Hambrick, D. C., & Eric, A. (1995). Assessing managerial discretion across industries: A multimethod approach. Academy of Management Journal, 38(5), 1427–1441.

- Hambrick, D. C., & Finkelstein, S. (1987). Managerial discretion: A bridge between polar views of organizational outcomes. Research in Organizational Behavior, 9(4):369–406.

- Hambrick, D. C., & Mason, P. A. (1984). Upper echelons: The organization as a reflection of its top managers. Academy of Management Review, 9(2), 193–206. doi:10.5465/amr.1984.4277628

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. doi:10.1007/s11747-014-0403-8

- Hoque, Z. (2011). The relations among competition, delegation, management accounting systems change and performance: A path model. Advances in Accounting, 27(2), 266–277. doi:10.1016/j.adiac.2011.05.006

- Huefner, R. J., & Largay, J. A., III. (2008). The role of accounting information in revenue management. Business Horizons, 51(3), 245–255. doi:10.1016/j.bushor.2008.01.013

- Jaworski, B. J., & Kohli, A. K. (1993). Market orientation: Antecedents and consequences. Journal of Marketing, 57(3), 53–70. doi:10.1177/002224299305700304

- Jensen, M., & Zajac, E. J. (2004). Corporate elites and corporate strategy: How demographic preferences and structural position shape the scope of the firm. Strategic Management Journal, 25(6), 507–524. doi:10.1002/(ISSN)1097-0266

- Jespersen, K., & Bysted, R. (2016). Implementing new product development: A study of personal characteristics among managers. International Journal of Innovation Management, 20(3), 1650043. doi:10.1142/S1363919616500432

- Justin Tan, J., & Litsschert, R. J. (1994). Environment‐strategy relationship and its performance implications: An empirical study of the Chinese electronics industry. Strategic Management Journal, 15(1), 1–20. doi:10.1002/(ISSN)1097-0266

- Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision under Risk. Econometrica, 47(2),363–391.

- Kahneman, D., & Tversky, A. (1980). Prospect theory. Econometrica, 12.

- Katila, R., & Chen, E. L. (2008). Effects of search timing on innovation: The value of not being in sync with rivals. Administrative Science Quarterly, 53(4), 593–625. doi:10.2189/asqu.53.4.593

- Keh, H. T., Der Foo, M., & Lim, B. C. (2002). Opportunity evaluation under risky conditions: The cognitive processes of entrepreneurs. Entrepreneurship Theory and Practice, 27(2), 125–148. doi:10.1111/1540-8520.00003

- Kim, J. U., & Aguilera, R. V. (2016). Foreign location choice: Review and extensions. International Journal of Management Reviews, 18(2), 133–159. doi:10.1111/ijmr.2016.18.issue-2

- Kraiczy, N. D, Hack, A, & Kellermanns, F. W. (2014). New product portfolio performance in family firms. Journal Of Business Research, 67(6), 1065–1073.

- Kraiczy, N. D., Hack, A., & Kellermanns, F. W. (2015). What makes a family firm innovative? CEO risk‐taking propensity and the organizational context of family firms. Journal of Product Innovation Management, 32(3), 334–348. doi:10.1111/jpim.12203

- Leahy, J. V., & Whited, T. M. (1995). The effect of uncertainty on investment: Some stylized facts (No. w4986). National Bureau of Economic Research.

- Lefcourt, H. M. (1982). Locus of control: Current trends in theory & research. Hillsdale, NJ: Lawrence Erlbaum.

- Lewellyn, K. B., & Muller‐Kahle, M. I. (2012). CEO power and risk taking: Evidence from the subprime lending industry. Corporate Governance: An International Review, 20(3), 289–307. doi:10.1111/j.1467-8683.2011.00903.x

- Li, D. Y., & Liu, J. (2014). Dynamic capabilities, environmental dynamism, and competitive advantage: Evidence from China. Journal of Business Research, 67(1), 2793–2799. doi:10.1016/j.jbusres.2012.08.007

- Lopes, L. L. (1987). Between hope and fear: The psychology of risk. In Advances in Experimental Social Psychology, 20, 255–295.

- March, J. G. (2010). The ambiguities of experience. New York, NY: Cornell University Press.

- March, J. G., & Shapira, Z. (1987). Managerial perspectives on risk and risk taking. Management Science, 33(11), 1404–1418. doi:10.1287/mnsc.33.11.1404

- Meertens, R. M., & Lion, R. (2008). Measuring an Individual’s Tendency to Take Risks: The Risk Propensity Scale 1. Journal of Applied Social Psychology, 38(6), 1506–1520. doi:10.1111/j.1559-1816.2008.00357.x

- Mia, L., & Chenhall, R. H. (1994). The usefulness of management accounting systems, functional differentiation and managerial effectiveness. Accounting, Organizations and Society, 19(1), 1–13. doi:10.1016/0361-3682(94)90010-8

- Mia, L., & Patiar, A. (2001). The use of management accounting systems in hotels: An exploratory study. International Journal of Hospitality Management, 20(2), 111–128. doi:10.1016/S0278-4319(00)00033-5

- Miller, D., & Friesen, P. H. (1982). Innovation in conservative and entrepreneurial firms: Two models of strategic momentum. Strategic Management Journal, 3(1), 1–25. doi:10.1002/(ISSN)1097-0266

- Miller, D., & Friesen, P. H. (1983). Strategy‐making and environment: The third link. Strategic Management Journal, 4(3), 221–235. doi:10.1002/(ISSN)1097-0266

- Moen, Ø., Tvedten, T., & Wold, A. (2018). Exploring the relationship between competition and innovation in Norwegian SMEs. Cogent Business & Management, 5(1), 1564167. doi:10.1080/23311975.2018.1564167

- Mueller, S. L., & Thomas, A. S. (2001). Culture and entrepreneurial potential: A nine country study of locus of control and innovativeness. Journal of Business Venturing, 16(1), 51–75. doi:10.1016/S0883-9026(99)00039-7

- Naranjo-Gil, D., & Frank, H. (2007). How CEOs use management information systems for strategy implementation in hospitals. Health Policy (Amsterdam, Netherlands), 81(1), 29–41. doi:10.1016/j.healthpol.2006.05.009

- Nathai-Balkissoon, M., Maharaj, C., Guerrero, R., Mahabir, R., & Dialsingh, I. (2017). Pilot development of innovation scales for beverage manufacturing companies in a developing country. Cogent Business & Management, 4(1), 1379214. doi:10.1080/23311975.2017.1379214

- Nunnally, J. C., & Bernstein, I. H. (1994). Psychological theory. New York, NY: MacGraw-Hill.

- Oktemgil, M., & Greenley, G. (1997). Consequences of high and low adaptive capability in UK companies. European Journal of Marketing, 31(7), 445–466. doi:10.1108/03090569710176619

- Olson, E. M., Walker, J. O., & Ruekert, R. W. (1995). Organizing for effective new product development: The moderating role of product innovativeness. Journal of Marketing, 59(1), 48–62. doi:10.1177/002224299505900105

- Otley, D., Broadbent, J., & Berry, A. (1995). Research in management control: An overview of its development. British Journal of Management, 6, S31–S44. doi:10.1111/bjom.1995.6.issue-s1

- Papadakis, V., & Bourantas, D. (1998). The chief executive officer as corporate champion of technological innovation: Aii empirical investigation. Technology Analysis & Strategic Management, 10(1), 89–110. doi:10.1080/09537329808524306

- Park, H. Y., Chang, H., & Park, Y. S. (2015). Firm’s knowledge creation structure for new product development. Cogent Business & Management, 2(1), 1–19. doi:10.1080/23311975.2015.1023507

- Petrus, B. (2019). Environmental dynamism: The implications for operational and dynamic capabilities effects. Management Sciences, 24(1), 28–36. doi:10.15611/ms

- Pindyck, R. S. (1993). A note on competitive investment under uncertainty. The American Economic Review, 83(1), 273–277.

- Plöckinger, M., Aschauer, E., Hiebl, M. R., & Rohatschek, R. (2016). The influence of individual executives on corporate financial reporting: A review and outlook from the perspective of upper echelons theory. Journal of Accounting Literature, 37, 55–75. doi:10.1016/j.acclit.2016.09.002

- Podsakoff, P. M., MacKenzie, S. B., Lee, J. Y., & Podsakoff, N. P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology, 88(5), 879. doi:10.1037/0021-9010.88.5.879

- Powell, T. C., Lovallo, D., & Fox, C. R. (2011). Behavioral strategy. Strategic Management Journal, 32(13), 1369–1386. doi:10.1002/smj.968

- Scapens, R. W., & Jazayeri, M. (2003). ERP systems and management accounting change: Opportunities or impacts? A research note. European Accounting Review, 12(1), 201–233. doi:10.1080/0963818031000087907

- Shapira, Z. (1986). Risk in managerial decision making. Unpublished manuscript, Hebrew University, 1404–1418.

- Sirén, C., Patel, P. C., Örtqvist, D., & Vincent, J. (2018). CEO burnout, managerial discretion, and firm performance. Long Range Planning. doi:10.1016/j.lrp.2018.05.002

- Sitkin, S. B., & Weingart, L. R. (1995). Determinants of risky decision-making behavior: A test of the mediating role of risk perceptions and propensity. Academy of Management Journal, 38(6), 1573–1592.

- Sniazhko, S. (2019). Uncertainty in decision-making: A review of the international business literature. Cogent Business & Management, 6(1), 1650692. doi:10.1080/23311975.2019.1650692

- Soin, K., & Paul, C. (2013). Risk and risk management in management accounting and control. 82–87. doi:10.1177/1753193412453424

- Song, M., & Chen, Y. (2014). Organizational attributes, market growth, and product innovation. Journal of Product Innovation Management, 31(6), 1312–1329. doi:10.1111/jpim.12185

- Strauß, E., & Zecher, C. (2013). Management control systems: A review. Journal of Management Control, 23(4), 233–268. doi:10.1007/s00187-012-0158-7

- Talke, K., Salomo, S., & Kock, A. (2011). Top management team diversity and strategic innovation orientation: The relationship and consequences for innovativeness and performance. Journal of Product Innovation Management, 28(6), 819–832. doi:10.1111/jpim.2011.28.issue-6

- Tang, J., & Tang, Z. (2007). The relationship of achievement motivation and risk-taking propensity to new venture performance: A test of the moderating effect of entrepreneurial munificence. International Journal of Entrepreneurship and Small Business, 4(4), 450–472. doi:10.1504/IJESB.2007.013691

- Tushman, M., Smith, W. K., Wood, R. C., Westerman, G., & O’Reilly, C. A. (2007). Organizational designs and innovation streams. Boston, MA: Division of Research, Harvard Business School.

- Utterback, J. M., & Abernathy, W. J. (1975). A dynamic model of process and product innovation. Omega, 3(6), 639–656. doi:10.1016/0305-0483(75)90068-7

- Vahlne, J. E., Hamberg, M., & Schweizer, R. (2017). Management under uncertainty–The unavoidable risk-taking. Multinational Business Review, 25(2), 91–109. doi:10.1108/MBR-03-2017-0015

- Vahlne, J. E., & Johanson, J. (2013). The Uppsala model on evolution of the multinational business enterprise–From internalization to coordination of networks. International Marketing Review, 30(3), 189–210. doi:10.1108/02651331311321963

- Waldman, D. A., Ramirez, G. G., House, R. J., & Puranam, P. (2001). Does leadership matter? CEO leadership attributes and profitability under conditions of perceived environmental uncertainty. Academy of Management Journal, 44(1), 134–143.

- Wangrow, D. B., Schepker, D. J., & Barker, V. L., III. (2015). Managerial discretion: An empirical review and focus on future research directions. Journal of Management, 41(1), 99–135. doi:10.1177/0149206314554214

- Winter, P. (2007). managerial risk accounting and control-A German perspective. Available at SSRN 1117205. doi:10.2139/ssrn.1117205

- Wold, H. (1980). Model construction and evaluation when theoretical knowledge is scarce: Theory and application of partial least squares. In Evaluation of econometric models (pp. 47–74). Boston, MA: Harvard Business School.

- Zaleha Abdul Rasid, S., Ruhana, I. C., & Khairuzzaman Wan Ismail, W. (2014). Management accounting systems, enterprise risk management and organizational performance in financial institutions. Asian Review of Accounting, 22(2), 128–144. doi:10.1108/ARA-03-2013-0022

- Zor, U., Linder, S., & Endenich, C. (2019). CEO characteristics and budgeting practices in emerging market SMEs. Journal of Small Business Management, 57(2), 658–678. doi:10.1111/jsbm.v57.2