?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The impact of innovation on every economy cannot be overemphasized. Hence, this study investigates empirically the impact of inward FDI on host firms’ innovation in Nigeria and South Africa using the World Bank Enterprise Survey dataset (WBES). In examining this relationship between FDI and firm innovation, two robust instrumental variable estimation techniques (two-stage least squares and limited information maximum likelihood) were employed so as to account for any endogeneity problems. The study establishes that while FDI positively influences firm innovation in Nigeria, it does not have any impact on firm innovation in South Africa. This study thus presents evidence that context is very crucial in the investigation of the link between FDI and innovation in Sub-Saharan Africa. It is thus recommended that FDI attraction into Africa should be selectively done with more focus on inflows from more advanced and innovative economies.

PUBLIC INTEREST STATEMENT

This paper investigates empirically the impact of foreign direct investment on firm innovation in South Africa and Nigeria. In recent times, foreign direct investment (FDI) has been a topical issue for discussion both in the boardroom and in the academic arena, especially in the developing world. This is simply because the concept is argued to have affected significantly on economic activities of firms in both developed countries and developing world. This link has been tested empirically in a number of studies but with a narrow focus on areas like economic growth, firm performance, firm value and firm efficiency. Not much is known on the link between FDI and firm innovation in Africa. This paper has, therefore, shed light on the link between FDI and firm innovation in the two economic giants in Africa; South African and Nigeria. The work is thus very useful to both academic and policymakers in general.

1. Introduction

Foreign Direct Investment (FDI) enhances productivity and economic growth via the infusion of innovation into host firms. Besides, innovation is said to be an engine that drives successful firms at the micro-level (Pai, Citation2016). Innovation occurs when firms are able to create new processes in producing existing products more efficiently or differentiating existing products or introducing entirely new products so as to increase sales and market performance (Girma et al., Citation2005). The inflow of FDI into host economies sparks up innovative activities via two main conduits.

Firstly, the injection of foreign capital by way of FDI causes parent companies to transfer some of their superior knowledge accumulated over the periods by way of employee transfer or technology transfer to the subsidiary firm. This enables the subsidiaries to be able to innovate and compete favourably as multi-national enterprises are noted to have better technologies and organizational skills than local firms (Smarzynska, Citation2003). Thus, firms that belong to larger corporation groups arguably have more innovative activities (Terk et al., Citation2007).

Secondly, one of the modes through which FDI infuses innovation into host firms is the reduction of financial constraint to the firms, enabling such firms with available finances to spend more resources on research and development (R&D), leading to more innovation in their operations. This is particularly very crucial as R&D does not only serve as a stimulant for innovation but it also enables the firm to be able to identify, assimilate and exploit outside knowledge (Kinoshita, Citation2000). Moreover, due to the availability of funds, FDI firms are likely to attract and retain more qualified personnel through higher wages (Aitken & Harrison, Citation1997; Glass & Saggi, Citation2002). Thus, access to finance drives innovation in firms (Fombang & Adjasi, Citation2018).

FDI is arguably one of the most important and cheapest means of technology transfer to developing countries (Mansfield $ Romeo, Citation1980). It is said to be the cheapest means of technology transfer since the host firms do not always have to finance the acquisition of the new technology. Besides, the transfer of newer technology is quicker to host firms through FDI than licensing and international trade (Mansfield & Romeo., Citation1980). Despite the link established between FDI and innovation theoretically (for instance, Bertschek, Citation1995; Blind & Jungmittag, Citation2004; Cheung & Lin, Citation2003; Iacovone et al., Citation2009; Liu & Zou, Citation2008; Saggi, Citation1999), it is still not entirely certain that FDI enhances innovation in host firms. It is argued that due to the profit motive of most foreign investors, foreign investors may concentrate more on short to medium term profits to the neglect of activities like innovation, which are cost intensive and long term geared. In that regard, FDI may stall or even retard innovation in host firms (see Stiebale & Reize, Citation2010; Maaso et al., Citation2013 and Garcia et al., Citation2013). Some authors also argue that FDI and innovation are endogenously determined. FDI may therefore not only drive innovation but innovative firms may end up attracting more FDI (Dunning, Citation1993). Again, the product life cycle theory believes that multi-national enterprises (MNEs) spend more on innovation during the early stage of the firm’s life cycle and move into host firms at later stages where less is spent on research and development (Vernon, Citation1966). Thus, FDI-based firms have the chance of hammering innovation than non-FDI firms. Apart from that, the pull factor theory also posits that some MNEs move into host firms so as to enable the home firms learn and adopt some innovations available at the host firms but are lacking in the home firms (Dunning, 1995).

On the empirical front too, there are varied results. In their study, Dachs and Ebersberger (Citation2009) established that membership of multinational enterprise group significantly improves firm’s innovative ability by way of assisting the firm to overcome innovation obstacles such as lack of financial resources, lack of technological and market information or organizational problems. In supporting these studies, Ghazel and Zulkhibri (Citation2015) and Khachoo and Sharma (Citation2016) in their separate studies noted that FDI is a good catalyst in the innovative abilities of host firms. On the contrary, some studies have also established a negative relationship between FDI and firm innovation (Barasa et al., Citation2018; Garcia et al., Citation2013; Stiebale & Reize, Citation2010).

Based on the above varied theoretical arguments and empirical findings, it is clear that there is a gap in the literature which is worth investigating. In addition, regional or country contexts may influence the FDI-innovation link and thus calls for further research with a contextual focus. There exists a great difference in countries/regions especially between industrialized western countries and developing countries (Latin America, Asia Africa etc.) when it comes to observing factors such as FDI, firm activity, structure, CSR, innovation and the factors which drive them and hence the impact on theory predictions. The situation is more stark from an African perspective.

For instance, all the studies carried out on the subject matter are based in advanced countries with only Barasa et al. (Citation2018) that has been carried out on SSA. However, Barasa et al. (Citation2018) focused only on technological innovation whereas our study is looking at innovation in general where technical innovation is just a sub-set. Again, while their study combined a lot of countries thus examining the impact on an aggregate level, our study is looking at two countries in SSA using firm level data so as to see how the link is in each country. As a result of the theoretical and empirical inconclusiveness established and the contextual gap, our study investigates the effect of FDI flow on host firm innovation in South Africa and Nigeria.

Our study also further departs from previous studies. Unlike previous studies, we create an innovation index using a multiple correspondent analysis (MCA) approach which captures innovation holistically. We use process and product innovation as proxies for innovation sourced from recently classified unique World Bank Enterprise Survey (WBES). With the exception of Bertschek (Citation1995), Liu and Zou (Citation2008), Stiebale and Reize (Citation2010), and Maaso et al. (Citation2013) who used product and process innovation and sale of new product as proxies for innovation, most of the previous studies on the subject matter have used R&D and patent protection as proxies for innovation.

As noted already the link between FDI and firm innovation could be a bi-directional one thus the problem of endogeneity emanating from simultaneity is eminent in such a study. Most previous studies have failed to control for endogeneity and this could account for some of the inconsistencies in their findings. We use an instrumental variable limited information maximum likelihood (IVLIML) estimation technique which has the ability to control for endogeneity problem in our models.

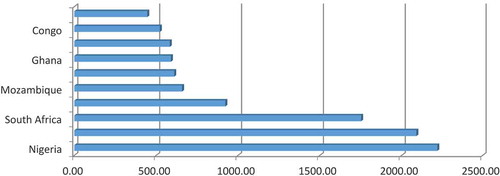

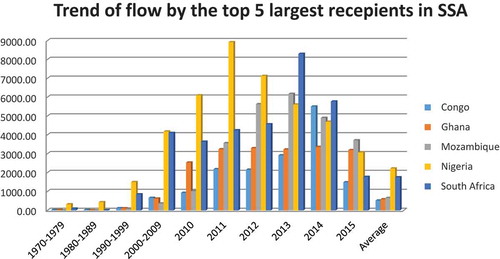

Finally, most studies are based on advanced countries with very few studies on developing countries, especially in Africa, where the attractiveness of FDI is increasing but where most firms also lag far behind in innovation as compared to their counterparts in other continents (African Development Bank, Citation2008). We focus our study on Nigeria and South Africa in SSA for a number of reasons. First, these countries are the leading economies in SSA and they are the top recipients of FDI inflows. While West African’s inflows of FDI heavily dominated by Nigeria and Ghana, with Nigeria being the largest recipient, southern African’s inflows are led by South Africa due to its economic power. South Africa is noted as the most attractive destination of all investors coming to the continent. As illustrated in Figures and , Nigeria and South African have consistently been the leading recipients of FDI in SSA for a long period of time. Second, although Nigeria and South Africa are in the common set of developing countries and also African countries, these two countries have different contexts and conditioning factors and structures which emerge in the interplay of any economic activity.

The rest of the paper is structured as follows: Section 2 reviews the related literature while data and methodological issues are presented in Section 3. The findings of the study are presented in Section 4 while conclusion and policy recommendations are in Section 5.

Figure 1. Top 10 largest recipients of FDI in Africa measured in million US dollars (Average annual flows from 1970–2015-US)

Figure 2. Trend of FDI flow to the top five largest recipients in SSA

2. Review of related literature

2.1. Theoretical literature

There is a theoretical debate on the link between FDI and firm innovation. While others are of the view that FDI leads to high innovation, some argue that FDI retards innovation. Yet there is another school of thought that believes that FDI-innovation link is a mixed one. They believe, it can be positive, negative or neutral depending on other underlying factors. We have grouped these debates into three main stances as discussed below.

2.1.1. Positive relationship between FDI and firm innovation

Caves (Citation1974) believes that FDI is positive for domestic firms as it transfers advanced technology and enhances innovation through knowledge transfers. The positive impacts of FDI on local firms’ innovation are twofold. Firstly, FDI impacts positively on the firms that host it and secondly, it affects other local firms positively in the same economy or sector. Summarising from previous literature (see Aghion et al., Citation2009; Bertschek, Citation1995; Findlay, Citation1978): we have explained here, starting with the host firms themselves, the channels through which FDI impacts positively on their (host firm) innovative activities. One of the possible channels through which host firms are impacted is the transfer of staff with superior knowledge from home firms to host firms or subsidiary firms (Caves, Citation1974; Blomström & Kokko, Citation1998). This normally happens because of the home firm’s financial interest in the host firm. This superior knowledge is transferred consciously to the local staff in the host firm by in-house training or transmitted to the local staff within the firm through continual observation by the host firm local staff.

Besides, superior knowledge can also be transferred by way of the home firm accepting host firm staff for skill training in the home firm; training which might not be available locally. During these training sessions, home firms train and reveal all their innovative skills to the host firms due to their (home firms) financial interest in the host firm. Besides, the presence of foreign owners on the management board of host firm through FDI infuse innovativeness into host firm activities as foreign owners bring on board their superior skills and knowledge for the effective and efficient operation of the host firm. Supporting this view, Garcia et al. (Citation2013) noted that knowledge transfer is one of the ways through which local firms get innovation and high firm performance from foreign direct investment. Other supporters of this superior knowledge transfer proposition believe strongly that foreign investors are diffusers of innovative practices to host firms (Bellak, Citation2004).

Apart from the superior knowledge transfer, host firms also benefit immensely from FDI by way of capital base enhancement. As local firms have access to foreign capital, their capital base is boosted, which can be translated into positive innovation for host firms. This is possible through a number of channels. The host firm is in a financial position to hire a qualified workforce and has the ability to adopt the best approaches and techniques needed in its operations (Glass & Saggi, Citation2002). Through enhanced capital, the host firm is in the position to hire and retain the best brains either locally or from the international job market, which is needed for the conception or expansion of every innovation. In addition to the qualified workforce, some material resources in the form of machinery, patent, license and other best operation mechanisms are needed for some kinds of innovation to take place. With the enhanced capital base, FDI-based firms are in a better position to acquire these resources than non-FDI-based firms.

The channels through which FDI impacts positively on other local firms besides firms hosting it is discussed as follows: the entrance of foreign investors leads to high competition thereby producing efficiency and engendering economies of scale for local firms, enabling them to increase productivity. As productivity goes up the firm has resources that it can spare for innovation through research and development. Competition has long been noted for engendering innovation (Schumpeter, Citation1942; Aghion et al., Citation2001). According to Blomström and Kokko (Citation1998), competition due to the foreign entrance also enhances the allocative and technical efficiency of firms and induces innovation, thus it is expected that FDI will lead to firms innovating better. Chung et al. (Citation2003) found evidence in the USA to support this argument when they established that through the entrance of Japanese automobile firms into the USA, competition became fierce and through that a lot of innovations were employed by the USA automobile industry in order for them to be competitive in business.

One of the channels through which FDI can impact positively on a domestic firm’s road to innovation is through the increase in demand for intermediate products (Rodrigue-Clare, Citation1996). Once there is a high demand for products from local firms, local firms are forced into adopting innovative and efficient ways of producing in large quantity to satisfy the demand in order not to lose their market share. Transfer of knowledge is also one of the means through which FDI impacts positively on local firms. This occurs through imitation by local firms by observations or learning from foreign firms during interactions or reverse engineering of the foreign products (Salomon, Citation2006). Knowledge again is transferred from FDI-based firms to other local firms through the transfer of employees.

2.1.2. Negative relationship between FDI and firm innovation

In contrast to the positive link between FDI and firm innovation, Vernon (Citation1966) using his “Product Life Cycle theory” believes that a negative relationship can exist between FDI and firm innovation. He argues that multi-national enterprises (MNEs) spend more on innovation in their activities at the introductory stage of the firm’s life cycle and move into host countries at the mature stage where less is spent here on research and development. During the introductory stage of a product, much is spent in researching into how to enhance the product and by so doing, the firm does not only develop its processes but it is able to train its staff on how to carry out these processes effectively and efficiently. By way of searching for a bigger market, cheap raw materials and other local advantages, MNEs migrate into host firms where everything is either done in the home country and sent to the host firm for distribution or for final processing where less innovation is needed (Yang et al., Citation2013). By so doing the FDI led firm stops completely to research at this time because it is being fed by its mother firm in the ways of carrying out its activities. Thus, less technical issues are left in the hands of the host firm employees who are not able to develop their skills and talents because their mother firm and its officers are doing everything for them. In this case, FDI is obviously retarding innovation in the host firm as no serious research and development activities are done at this level.

Another theory that explains the inverse relationship between FDI and firm innovation is the pull factor theory developed by (Dunning, 1995). This theory argues that foreign investors are sometimes pulled into a host firm due to the higher innovation that the host firm has so as to learn and adopt it into the mother firm. Normally firms that move into host firm with such intension do not spend anything on research and innovation as they do not intend to innovate in the host firms but rather try to replicate same in their home firms. By doing that more research and development is rather concentrated on their home country so as to adopt the superior innovation from the host firms into the home firm. One of the channels such MNEs adopt that aids the destruction of value in the host firms is by way of sending most of the high skills and talented staff from the host firms to the home firm so as to replicate the superior technology and because MNEs are able to pay better remunerations they end up weakening the host firms’ ability to innovate by not only taking away their superior innovation but also taking away most of their best brains. This, therefore, destroys the host firms’ ability to innovate and hence the inverse relationship between FDI and firm innovation.

2.1.3. Mixed relationship between FDI and firm innovation

One of the theories that explains the possible mixed theoretical link between FDI and firm innovation is the reconciled FSA/CSA framework with Dunning’s four motives of FDI illustrated by Yang et al. (Citation2013). The framework is shown in Figure . In this framework, FSA stands for firm-specific advantages referring to the MNEs valuable, non-substitutable and difficult to imitate resources and capabilities (Barney, Citation1991). These advantages could include upward-technological knowledge, administrative knowledge, reputational resources and institutional routines (Yang et al., Citation2013). The FSAs are categorized into internationally transferable and non-transferable (Rugman & Verbeke, Citation2001). While the former is noted to transfer innovation across borders, the latter does not (Verbeke, Citation2009). On the other hand, CSA stands for country-specific advantages and this refers to the whole set of strengths of a host country or firm (Barney, Citation1991). These could be in the form of land, labour, capital, entrepreneurship, demand conditions, knowledge base or conducive social and institutional advantages.

The x-axis of the reconciled FSA/CSA framework focuses on whether MNEs’ FSAs are weak or strong compared with competitors whereas the y-axis looks at whether or not CSAs of the host country/firm are weak or strong compared with other hosts.

Figure 3. Reconciled FSA/CSA framework

From the Figure 3, cell 1 is where the FSAs are low while the CSAs are high. Thus, FDI is attracted by the CSAs and it does not matter at all whether or not the MNEs have some firm-specific advantages or not. In this cell, the MNEs’ motives of FDI are the resource seeking, market seeking and efficiency seeking. Cell 3 is the strategic asset seeking FDI motivated MNEs activities. This is where the parent company has FSAs but seeks to explore the CSAs that exist in the host firm so as to augment its strengths. In this cell, the MNEs expand into the host firm with the view to searching for advanced resources including upward-technological knowledge, downward marketing knowledge, administrative knowledge or reputational resources. For instance, Almeida (Citation1996) established that in the semiconductor industry, the objective of MNEs from Europe and Korea to the USA was to offset a technological deficient in their home countries. Apart from that small Taiwanese MNEs treat FDI as a conduit to link with resources that MNEs need but do not have them at home markets.

Cells 2 and 4 would not attract FDI as CSAs are low. In that case, no MNEs will be interested in expanding into such locations/firms. Hence, our concentration is on cells 1 and 3 alone. Whereas high CSAs are needed for each of Dunning’s four FDI motives to take place, FSAs are not a necessity for the natural resource seeking FDI, market seeking FDI and Efficiency seeking FDI (Rugman, Citation2010). Thus, there is a low probability of host firms benefiting in innovation from FDI inflows which fall into cell 1 category as the MNEs may not have any FSAs to transfer to the host firms with the exception of boosting the capital base of the host firm. Cell 3 category is where more gains and losses exist for the host firms in the FDI inflows. Gains in this cell are enormous if the FSAs are internationally transferable into the host firms. In this case, the host firms are able to benefit from the FSAs of the MNEs and hence their innovative capacity will enhance as compared to the non-FDI firms who have no affiliation with any MNEs.

On the contrary, where the MNEs FSAs are non-transferable, the parent country is likely going to gain from the host firms by exploiting the host firms’ advantages without transferring any of their advantages to the local firms to boost their innovation. In this instance, FDI inflows will have no significant impact on host firms or at worst destroys firm innovative capabilities by taking away their strategic assets without leaving behind any benefits to the firm. Blind and Jungmittag (Citation2004) also state that the relationship between FDI and innovation will depend on the type of FDI flow. Where the FDI flow is in the form of “greenfield investment” i.e. new business, the impact on the host firm will be positive as they will have access to more capital. Where it is a takeover deal, it will depend on which firm has superior innovations (the acquired firm or the buyer). If the foreign firm has superior innovations, it will lead to a positive impact on the host firm while the reverse is also true. Another theory that illustrates the mixed relationship is the distance to the technology frontier. The theory believes that the larger the technological gap between the host FDI and home FDI, the more likely a positive innovation impact of FDI will be realised. From other perspectives, the impact of FDI on innovation depends mainly on the absorptive capacity of host firms. With a higher absorptive capacity innovation is positively impacted by FDI. However, if absorptive capacity is low then domestic firms struggle to adopt new and superior technologies and this could negatively affect innovation.

2.2. Overview of empirical literature

The empirical research on the relationship between FDI and innovation has varied findings. Some studies here established that FDI inflows have a positive impact on innovations of host country firms, whilst others have established different findings. For instance, Bertschek (Citation1995), studied the impact of FDI on local innovation among 1,270 firms in the West German manufacturing industry. With a probit model, it was realized that FDI has a positive effect on product and process innovation as local firms have to increase their efficiency in order to stay in the market. Using more comprehensive data of 2,019 firms in the same economy, Blind and Jungmittag (Citation2004) confirmed this earlier finding. They realised that the inflows of FDI into target firms have a high positive significance on both product and process innovation. Lin and Lin (Citation2009) using the technological survey carried out in Taiwan from 2001 to 2002, concluded that FDI leads to technological development. With GMM estimators, Liu and Zou (Citation2008) studied the impact of FDI on domestic firms. They realized that importing foreign technology through FDI leads to domestic innovation.

In their study, Dachs and Ebersberger (Citation2009) established that membership of multi-national enterprise group significantly improves firm’s innovative ability by way of assisting the firm to overcome innovation obstacles such as lack of financial resources, lack of technological and market information or organizational problems. In supporting these studies, Ghazel and Zulkhibri (Citation2015) and Khachoo and Sharma (Citation2016) in their separate studies noted that FDI is a good catalyst in the innovative abilities of host firms. Khachoo and Sharma (Citation2016) studies however pointed out that the positive FDI-innovation link is seen more in firms residing in identical industries. Again Antonietti et al. (Citation2014) established a positive relationship between FDI and firm innovation only in the service sector of the economy among firms in Italy.

Similarly, Cheung and Lin (Citation2003) found in their study that FDI is positive in driving innovation to domestic firms in China. Iacovone et al. (Citation2009) arrived at the same conclusion when they investigated the impact of the entry of Walmart into Mexico. Closely related to these studies is Vahter (Citation2010), whose study established that there was no evidence of increases in productivity as a result of FDI inflows. It equally found that there was a positive spillover of innovation as a result of the FDI while Saggi (Citation1999) noted in his study that foreign firms transfer the best technology to local firms through the channel of FDI.

On the other hand, Maaso et al. (Citation2013) found that FDI does not lead to innovation. Their study was carried out in Central and Eastern Europe between the period of 1998 and 2006 with the use of the Tobit model. Using the same Tobit model on German firms, Stiebale and Reize (Citation2010) did not only find that FDI does not lead to innovation transfer but also that it leads to a negative effect on local firms’ innovations. Similarly, using a comprehensive dataset of 1799 Spanish manufacturing firms, Garcia et al. (Citation2013) established that FDI has a negative relationship with the innovative performance of local firms. Using 418 firms from the World Bank Enterprise Survey dataset on SSA, Barasa et al. (Citation2018) realized that foreign technology has a negative effect on technical efficiency of firms in SSA.

A host of studies also confirms the endogeneity between FDI and innovation. For instance, De la Potterie and Lichtenberg (Citation2001) using 13 industrialised countries found that FDI inflow transfers technology to local firms but the effect is felt in countries where research and development are intensive. Another study by Kinoshita (Citation2000) in Czechoslovakia also established that there was an increase in innovation by FDI but this was limited to sectors that had invested in innovative research and development. Thus, Rosell-Martinez and Sanchez-Sellero (Citation2012), using GMM on Spanish manufacturing industry firms found that FDI flows to sectors which are research and development intensive sectors. Using a Tobit model on 30,000 state-owned firms in China, Girma et al. (Citation2005) found similar results. They realized that FDI has a negative effect on state-owned firms that do not export, invest in research and development or had earlier innovation experience. They concluded that research and development are principal components to innovation in firms; thus, FDI could be endogenous to innovation.

Sivalogathasan and Wu (Citation2014) carried out a study on FDI and innovation in South Asian countries covering a period of 12 years (from 2000–2011). They discovered that R&D is a very significant determinant of innovation capability. Besides, they noted that though FDI impacts positively on firms’ innovation, the strength of this positive link depends heavily on the availability of the absorptive capacity and the presence of innovative complementary assets in the host firms. Similarly, Loukil (Citation2016) realized that below certain threshold value of technological development, FDI has a negative impact on innovation of host firms but above this threshold, FDI impacts positively on the innovative ability of host firms in developing countries. This implies that though FDI could be a key channel through which innovation moves from advanced economies to developing economies, there must be some complementary assets to realize this effectively.

From the discussion, there is clearly a high degree of uncertainty surrounding the link between FDI and firm innovation. Nonetheless, a part of the literature which has not been fully investigated. This is the endogeneity between FDI and innovation as demonstrated by the “pull factor theory” developed by Dunning (1995). Dunning (1995) argues that foreign investors in recent times are not just pushed into host countries because foreign companies have more economic advantages than the host firms but they are also pulled by the innovations located in the recipient countries so that they can also learn and adopt such innovations into the mother firm at home. This, therefore, shows that FDI and innovation are endogenous and thus there is a need to control for this endogeneity. Failure to control for endogeneity can result in conflicting results.

3. Data and methodology

3.1. Data and sample

The study employed cross-sectional data of the standardised version of the World Bank Enterprise Survey for our investigation. We used the latest survey on Nigeria 2014 and South Africa 2007. The survey provides firm-level data on a sample of service and manufacturing firms across developing countries in the world. The survey uses a face-to-face interview preceded by a random sampling technique and consistent methodology of implementation across all surveyed countries. In the survey, both qualitative and quantitative information are sought from business owners and managers. The composition of the firms of the two countries is indicated in Table .

Table 1. Composition of the sample

3.2. Construction of innovation index

According to OECD/OCDE (Citation2005, p. 46), product innovation is the introduction of goods or a service that is new or significantly improved with respect to its characteristics or intended uses while a process innovation is the implementation of a new or significantly improved production or delivery method. We adopt the World Bank Enterprise Survey database definitions with modifications where product innovation is made up of the combination of two variables: international quality certificate and foreign technology license; while process innovation is made up of three variables: usage of email, possession of website and having audited financial statements. Unlike previous studies, we created innovation indexes using multiple correspondent analysis (MCA). MCA is chosen as it is very appropriate for our data. It does not only assign weight according to the significance of the variables in the index but it is well suited for the creation of indexes with categorical components. It is therefore viewed as a generalisation of principal component analysis when the variables are binary or categorical in nature (Abdi & Valentin, Citation2007; Asselin & Anh, Citation2002). The MCA indexes are created using a standard correspondence analysis on an indicator matrix whose entries are coded categorically. The MCA extracts the first factorial axis which retains the maximum information contained in the matrix. In this instance, the index, innovation, is a function of some underlying variables Kij, such that Kij represents firm i’s possession or usage of a particular innovation element or the lack or non-usage of it j (Akotey & Adjasi, Citation2015; Booysen et al., Citation2008; Johnston & Breu, Citation2013).

Following previous studies (See Akotey & Adjasi, Citation2015; Benze´cri, Citation1973; Booysen et al., Citation2008) we adopt the MCA innovation index as stated below in computing the weight of the individual innovation elements:

where ith firm innovation index is αi, dki is the kth value of the categorical variables (with k = 1 … K) indicating the firms’ innovation variables included in the index construction. F1k is the MCA weights generated for the analysis. The weights computed are presented below in Table . At the creation of the innovation index, there should not be any reverse variable. In the construction of the index, the alpha command was used to detect any reverse variables. If any reverse variable was detected it was dropped. This is because reverse variables have a negative impact on the index (Booysen et al., Citation2008). All the indices met the a priori expectation.

Table 2. Weight generated from the MCA

Summary statistics of the indexes created are shown below in Table . It is realized from the minimum scale of reliability that there is sufficient credibility on the indexes created and can, therefore, be relied on for any analysis.

Table 3. Summary statistics of the innovation indexes

3.3. Analytical procedure

From the literature (see Bertschek, Citation1995; Blundell et al., Citation1999; Crepon et al., Citation1998; Girma et al., Citation2005; Maaso et al., Citation2013; Stiebale & Reize, Citation2010), we adopt the model below.

The expanded forms of the model will take the forms as follows:

where

From EquationEquation (3)(3)

(3) , FDI refers to foreign direct investment while the control variables are export, size, age, sales and training. Our a priori expectation is that FDI will have a positive impact on product innovation and process innovation. This is premised on the background that FDI leads to the transfer of superior knowledge from parent companies to host firms (Smarzynska, Citation2003). FDI furthermore reduces the financial constraints on firms, making them capable of carrying out research and development and also have the ability to hire highly qualified workers which together serve as stimulants to innovation in firms (Kinoshita, Citation2000). The context of Nigeria and South Africa, as already discussed, is different from that of other developing countries and likely to provide us with interesting results and addition to the literature. A full description of all the variables is shown in Table .

Table 4. Variable description

3.4. Instrumental variable

To overcome the endogeneity problem between FDI and innovation in our estimation, we employed the instrumental variable two-stage least square (IV2SLS) and instrumental limited information maximum likelihood (IVLIML) estimation techniques. IV has the power to control for all unobservable factors and measurement errors in the model due to the introduction of the instruments (Baum, Citation2008). The general model of IV as presented by Stock and Watson (Citation2007), is as follows:

where

is the independent variable.

is the error term which represents measurement errors or omitted factors.

are k endogenous regressors which are potentially correlated with

are included exogenous regressors which are uncorrelated with the

are unknown regression coefficients.

The coefficients are over identified if there are more instruments than endogenous regressors (m > k); they are under identified if m < k and they are exactly identified if m = k.

The model in EquationEquation (4)(4)

(4) is computed in two stages. In the first-stage regression(s): the endogenous variable X1i is regressed on the instrumental variables (Z1i, … Zmi) together with the exogenous variables (W1i, … Wri) and we compute the predicted values from this regression.

In the second-stage regression, we regress the dependent variable Yi on the predicted values of the endogenous variables and the included exogenous variables.

To produce unbiased results under the IV model, an observed variable which is the instrumental variable is required which has a strong correlation with FDI, our main independent variable, but does not correlate with the error term. We selected labour cost and court fairness as instruments for South Africa and Nigeria, respectively. Court fairness, impartiality and incorruptibility means there is rule of law working effectively. Every foreign investor is interested in the safety of their investment and rights as an investor. Therefore, FDI is attracted to countries where the court system guarantees investor rights by way of fair judgment (Globerman & Shapiro, Citation2003; Lee & Mansfield, Citation1996).

Similarly, labour cost is a key determinant of FDI inflows. Theoretically, one of the reasons for foreign investors going abroad to invest is to leverage cheap labour so as to reduce the cost of production (Dunning, Citation1993). This is particularly apparent where foreign investment is in labour-intensive sectors like the extraction of raw materials and the manufacturing sectors. Hence, firms that have a lower cost of labour will tend to attract foreign investors than those with a high cost of labour. Cost of labour, on the other hand, will have no correlation with a firm’s ability to innovate.

Our first-stage regression is an OLS regression but has the selected instruments, zi, as additional independent variables. Following the approach ofAkotey and Adjasi (Citation2015), Janzen and Carter (Citation2013), and Khandker (Citation2005) the first-stage regression is:

where FDIi is equal to one (1) if firmi has at least 10% of its equity being foreign, otherwise zero (0), zi is the selected instruments xi is a vector of covariates which affect a firm’s innovation ability and μi is the error term. In the second stage, the predicted values of FDI () are substituted in Equation (5.6) to obtain the outcome equation (Khandker, Citation2005).

where is the predicted probability of getting FDI inflows. Under the IV the impact of FDI on innovation is

.

The validity of our instruments is very crucial in determining the robustness of our results. Every valid instrument must satisfy the condition of instrument relevance and instrument exogeneity. Where an instrument fails to pass the test of relevance the instrument is said to be weak and the results produced from such an instrument will be biased. According to Stock and Watson (Citation2007), the rule of thumb in checking for weak instrument is that in a situation where there is a single endogenous regressor, a first-stage F-statistic less than 10 indicates that the instrument is weak. Stock and Yogo (Citation2005) have, however, provided for a formal test for a weak instrument. In their test, the null hypothesis is that the instruments are weak and the alternative hypothesis is that the instruments are strong. The strong instruments are those for which the bias of 2SLS estimator is at most 10% of the bias of the OLS estimator.

This test entails the comparison of the F-statistic with a critical value that depends on the number of instruments. For a test with a 5% significance level, this critical value ranges between 9.08 and 11.52, so the rule of thumb of comparing F-statistic to 10 is a good approximation to the Stock and Yogo test. To test for the relevance of these instruments chosen, we employed the critical values of Stock and Yogo (Citation2005) and the minimum Eigenvalue of Cragg and Donald (Citation1993). To reject the null hypothesis and conclude that the instruments are valid, the Cragg and Donald (Citation1993) minimum Eigen value must be greater than the Stock and Yogo (Citation2005) critical value. As shown in Table in Appendix A for our post-estimation tests, our minimum Eigenvalues of Cragg and Donald (Citation1993) for South Africa are greater than the Stock and Yogo (Citation2005) critical values of Wald test at 15%,20% and 30%. For that of Nigeria, the minimum Eigenvalues of Cragg and Donald (Citation1993) are only greater than the Stock and Yogo (Citation2005) critical values of Wald test at only 20% and 30%. However, at 10% both instruments have their minimum Eigenvalues at less than the critical values. Thus, we conclude that both of the instruments are relevant for both the countries but are weak. Stock and Watson (Citation2007) established that IVLIML estimator is a better option with weak instruments in producing unbiased results than IV2SLS. The IVLIML tends to be more centered on the true β than IV2SLS. Where the instruments are strong the IV2SLS and IVLIML estimators coincide in a large sample. Following this, we relied on the IVLIML estimation results for our analysis. We could not test for our instruments’ exogeneity in our models since our models are just identified (our endogenous variables are equal to the instruments) and hence there is no formal way of testing for this (Stock & Watson, Citation2007).

4. Empirical findings

4.1. Descriptive statistics

Table shows the descriptive statistics of firms in the two countries. On average both countries have higher process innovation than product innovation at the firm level as seen in the table. Expectedly, South African firms perform better in both innovation indexes. It has about the highest average mean of the product innovation (1.14) and process innovation (1.96). Nigeria recorded the least average performance of 0.11 and 0.89 indexes for the product and process innovations, respectively.

Table 5. Summary statistics

There is a great gap between South Africa and Nigeria in terms of a firm’s age. While the average age in Nigeria is approximately 18 years and 10 months that of South Africa is approximately 26 years and 3 months. The size of firm measured by the number of employees is varied with South Africa having the highest average number of employees of 104 employees while Nigeria has the least with an average number of 43 employees. This means that while the majority of firms in South Africa are classified as large firms, most of the firms in Nigeria are medium size firms.

4.2. Regression results

For all our estimations, we made use of STATA 12 software in a generation of our results. Tables – show our regression results for both IV2SLS and IVLIML estimations on the linkages between FDI and innovation for our two selected countries, Nigeria and South Africa, respectively. We, however, rely on the IVLIML for our discussions and analysis as our post-estimation tests shown in Appendix A indicate that our instruments are weak and hence IVLIML is preferred to the IV2SLS. From our results, it is evident that there is a link between FDI and innovation. In Nigeria, there is a positive significant relationship between FDI and both product and process innovation. The positive link between FDI and innovation established in Nigeria could be attributed to two things.

Table 6. Instrumental variables two-stage least square regression for Nigeria

Table 7. Instrumental variable LIML regression for Nigeria

Table 8. Instrumental variables two-stage least square regression for South Africa

Table 9. Instrumental variable LIML regression for South Africa

Firstly, with the inflows of FDI into host firms, capital level of the firms is enhanced relieving such firms from financial constraints which is a key challenge to most firms in Africa. With the availability of finance, these firms are able to devote some funds to research and development activities which stimulate innovation in the long run. Having enough funds through FDI inflows also means that these firms are able to acquire high technology tools and equipment together with hiring the best human resources who can propel innovation in such firms. Secondly, the inflow of FDI does not only boost the financial strength of the host firms but it comes with it the transfer of superior knowledge from source firms. This is possible as MNEs are said to have better technology than non-MNEs firms (Markusen, Citation2002). This relationship between FDI and innovation in Nigeria is a confirmation of previous studies which realized that through improved efficiency and more capital availability brought by FDI inflow, FDI firms perform better in innovation than non-FDI firms both in process and product innovations (Bertschek, Citation1995; Blind & Jungmittag, Citation2004; Lin & Lin, Citation2009; Liu & Zou, Citation2008; Saggi, Citation1999). This is contrary to other earlier studies which found FDI to have a negative impact on the innovation ability of firms (Stiebale & Reize, Citation2010 and Garcia et al., Citation2013).

The results can also be explained by the position of Nigeria in the Global Innovation Index. Nigeria has been ranked 123rd position globally on the ability to innovate and placed 20th in the SSA region. Given that most of the inflows to Africa are not from Africa but other advanced world, it is thus plausible to believe that most of the FDI are flowing into Nigeria from countries which have better innovative capacity than Nigeria hence the positive impact realized from the inflow of FDI on the Nigerian firms. Again, according to the Global Innovative Index (2015), Nigeria is poorly ranked as far as access to domestic credit by the private sector (116th position), adoption of R&D activities in firms (80th position) and access to ICT (127th position) are concerned. This, therefore, means the inflows of FDI into Nigeria firms strongly boost access to capital by the host firms. Thus, the enhanced capital base of the host firms together with superior knowledge from FDI inflows, the host firms are able to increase their spending on both R&D and ICT access which are serious catalyst in provoking innovation in firms.

FDI has no significant impact on both product and process innovation in South Africa. It is in support of Maaso et al. (Citation2013) which established that FDI has no impact on innovation in Central and Eastern Europe. It is also in tandem with the findings of Kinoshita (Citation2000), De la Potterie and Lichtenberg (Citation2001), and Garcia et al. (2005) who established that the positive impact of FDI on innovation is only possible in firms where research and development are intensive. In our case, South Africa is advanced, especially in the area of process innovation and this could explain the insignificant effect. It is in line with both “the distance to technology frontier (DTF)” and “pull factor (PF)” theories. The DTF believes that the greater the difference in technology development between the home and host country of FDI, the greater the pressure to adopt the new technology and the reverse is true (Findlay, Citation1978).

Similarly, PF argues that foreign investors are sometimes pulled into a host firm due to the higher innovation that the host firm has so as to learn and adopt it into the mother firm (Dunning, 1995). In the case of South Africa, there may be no technology gap at all with the home firm of the FDI. In some cases, where FDI is coming from other developing world countries, South Africa could be ahead of such foreign investors’ home countries in terms of innovation and this could be accounting for such insignificant relationships. For instance, on domestic credit to private sector, South Africa is ranked 16th globally (Global Innovation Index, 2015). This implies that South Africa is doing better than most countries in the world; thus, the inflow of FDI may not be seen significantly as far as the private firm capital base is concerned, unlike most African countries where access to credit is the main challenge to private firms’ performance (Global Innovation Index, 2015). Again South Africa has demonstrated its dominancy when it comes to R&D (36th position) and access to ICT (86th position) globally. This shows that South African firms are doing very well in research and development already and thus MNEs moving into South Africa may not concentrate again on these areas but also channel their resources into other areas that may need to be boosted for better performance in the firm thus the non-significant of the inflows on the host firms’ innovation.

5. Conclusion and policy recommendations

Innovation in firms has been a huge catalyst in productivity and hence, a booster for economic growth (Blomstrom & Sjoholm, Citation1999). This study set out to investigate empirically the impact that FDI has on firm innovation in Nigeria and South Africa. The study made use of the latest surveys of the World Bank Enterprise Survey dataset available for Nigeria and South Africa. Using IVLIML estimation techniques, the study established the following:

For Nigeria, it is noticeable that FDI has contributed positively to the innovative ability of their firms both through product and process innovation. This positive impact is realized through the transfer of superior knowledge, technology transfer and the injection of capital into host firms. It is thus appropriate for policymakers in these countries to create a congenial atmosphere for foreign investment to be attracted. This could be done by way of tax holidays, protection of investor interest by way of enforcement of the rule of law in businesses, construction of the needed infrastructure such as roads, electricity, telecommunication facilities and a stable economy devoid of conflicts and wars.

At the firm level too, good corporate governance principles could be institutionalized so as to attract inward FDI. It is obvious from the discussion that the guarantee of investor interest is a key determinant of inward FDI. The protection of investor interest could be guaranteed in two ways. One is the effective functioning of rule of law in the country while the other way is the establishment of effective internal control mechanisms by the firm which is championed by the adoption of good corporate governance principles. Furthermore, the availability of cheap labour attracts the flow of FDI into a firm.

We noted that FDI has no significant impact on product and process innovation in South Africa. This we believe could be partly attributable to the kind of foreign firms that acquire ownership in firms in South Africa. As indicated by Dunning (1995), some firms of less innovation can acquire ownership in other firms in order to learn their technology but not to transfer any new technology to the host firms. It is, therefore, possible that FDI flows to South Africa are not necessarily coming from higher technology-based countries than South Africa.

In situations where inward FDI is flowing from countries of comparable innovation or less innovation than South Africa, it will be possible to realize no impact of the FDI on host firm innovation or in the worst scenario, where the foreign investors only have an aim of investing in the host firm in order to learn and sometimes poach some of their best brains back to the home firm, a negative impact can be seen. For policy purpose, it is thus recommended that FDI attraction activities in South Africa should be geared towards countries that are more advanced in terms of innovation abilities than South Africa so as to enable the host firm benefit holistically in terms of transfer of innovation and superior managerial skills in addition to capital accumulation. Besides, nations in the continent of Africa should woe in FDI selectively by focusing more on inflows from countries that are more innovative than the host nations.

Notwithstanding the novelty of this paper, it has a number of limitations. Firstly, this study could not explore the time dynamics of the phenomenon as the available data is a one data point. For future research, we recommend that the time dynamics on this link should be investigated as and when data availability has made it possible. This would make it possible for the use of panel data estimators like generalized method of moments (GMM), fixed effect and random effect. Secondly, we could not do pure comparison of the link between Nigeria and South Africa. This is because the survey for Nigeria was collected in 2014 while that of South Africa was collected as far back 2007. This does not give a good platform for the result to be compared purely. As a result, only we only explained our results separately and that is why we did not also combine our data to run a single regression. Again we suggest a pure comparative study as and when data are available.

Additional information

Funding

Notes on contributors

Joseph Dery Nyeadi

Dr. Joseph Dery Nyeadi is a senior lecturer and a chartered accountant with the University of Mines and Technology in Ghana. His area of interest ranges from Corporate Finance to Corporate governance in African context. He has widely published in a number of renowned journals including Cogent Finance and Economics, Journal of Accounting and Management, Journal of Global Responsibility etc.

Charles Adjasi

Prof. Charles Adjasi is a renowned professor of development Finance at University of Stellenbosch Business School in South Africa. He has published in diverse fields ranging from Economics, Finance to Business Management focusing more on African Economies.

References

- Abdi, H., & Valentin, D. (2007). Multiple correspondence analysis. In Neil, S. (Ed.), Encyclopaedia of measurement and statistics(pp. 651–23) Sage.

- African Development Bank. (2008). Eminent speakers’ series: Sharing the visions of Africa’s development. African Development Bank Series, 1, 25–61.

- Aghion, P., Blundell, R., Griffith, R., Howitt, P., & Prantl, S. (2009). The effects of entry on incumbent innovation and productivity. The Review of Economics and Statistics, 91(1), 20–32. https://doi.org/10.1162/rest.91.1.20

- Aghion, P., Harris, C., Howitt, P., & Vickers, J. (2001). Competition, imitation and growth with step-by-step innovation. Review of Economic Studies, 68(3), 467–492. https://doi.org/10.1111/1467-937X.00177

- Aitken, B. J., & Harrison, A. E. (1997). Do Domestic firms benefit from direct foreign investments? Evidence from Venezuela. American Economic Review, 89(3), 605–618. https://doi.org/10.1257/aer.89.3.605

- Akotey, J. O., & Adjasi, C. K. D. (2015). Does microcredit increase household welfare in the absence of micro insurance? World Development, 77, 380–394. https://doi.org/10.1016/j.worlddev.2015.09.005

- Almeida, P. (1996). Knowledge sourcing by foreign multinationals: Patent citation analysis in the US semi-conductor industry. Strategic Management Journal, 17(S2), 155–165. https://doi.org/10.1002/smj.4250171113

- Antonietti, R., Bronzini, R., & Cainelli, G. (2014). Inward greenfield FDI and innovation. Economic Political Industry, 41, 93–116.

- Asselin, L.-M., & Anh, V. T. (2002). Multidimensional poverty and multiple correspondence analysis. Retrieved 2015, April 4, from http://www.aed.auf.org/IMG/pdf/Louis-Marie_Asselin.pdf

- Ayyagari, M., Demirguc-kunt, A., & Maksimovic, V. (2011). Firm innovation in emerging markets: The role of finance, governance, and competition. Journal of Financial and Quantitative Analysis, 46(6), 1545–1580. https://doi.org/10.1017/S0022109011000378

- Barasa, L., Vermeulen, P., Knoben, J., Kinyanjuni, B., & Kimuyu, P. (2018). Innovation inputs and efficiency: Manufacturing firms in Sub-Saharan Africa. European Journal of Innovation Management. https://doi.org/10.1108/EJIM-11-2017-0176

- Barney, J. B. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120. https://doi.org/10.1177/014920639101700108

- Baum, C. F. (2008, June). IV techniques in economics and finance. Boston College, DIW, DESUG.

- Bellak, C. (2004). How domestic and foreign firms differ and why does it matter. Journal of Economic Surveys, 18(4), 483–514. https://doi.org/10.1111/j.0950-0804.2004.00228.x

- Benze´cri, J. P. (1973). Data analysis: The correspondence analysis. Dunod.

- Bertschek, I. (1995). Product and process innovation as a response to increasing imports and FDI. Journal of Industrial Economics, XLIII(4).

- Blind, K., & Jungmittag, A. (2004). Foreign direct investment, imports and innovations in service industry. Review of Industrial Organisation, 25(2), 205–227. https://doi.org/10.1007/s11151-004-3537-x

- Blomström, M., & Kokko, A. (1998). Multinational corporations and spillovers. Journal of Economic Surveys, 12(3), 247–277. https://doi.org/10.1111/1467-6419.00056

- Blomstrom, M., & Sjoholm, F. (1999). Technology transfer and spillovers: Does local participation with multinationals matter. European Economic Review, 43(4–6), 915–923. https://doi.org/10.1016/S0014-2921(98)00104-4

- Blundell, R., Griffith, R., & van Reenen, J. (1999). Market share, market value and innovation in a panel of British manufacturing firms. Review of Economic Studies, 66(3), 529–554. https://doi.org/10.1111/1467-937X.00097

- Booysen, F., Servaas, V. D. B., Ronelle, B., Micheal, V. M., & Gideon, D. R. (2008). Using an index to assess trends in poverty in seven Sub-Saharan African countries. World Development, 36(6), 1113–1130. https://doi.org/10.1016/j.worlddev.2007.10.008

- Caves, R. E. (1974). Multinational firms, competition and productivity in host country markets. Economica, 41(162), 176–193. https://doi.org/10.2307/2553765

- Cheung, K., & Lin, P. (2003). Spillover effects of FDI on innovation in China: Evidence from the provincial data. China Economic Review, 15(1), 25–44. https://doi.org/10.1016/S1043-951X(03)00027-0

- Chung, W., Mitchell, W., & Yeung, B. (2003). Foreign direct investment and host country productivity: The American automotive component industry in the 1980s. Journal of International Business Studies, 34(2), 199–218. https://doi.org/10.1057/palgrave.jibs.8400017

- Cragg, J. G., & Donald, S. G. (1993). Testing identifiability and specification in instrumental variable models. Econometric Theory, 9(2), 222–240. https://doi.org/10.1017/S0266466600007519

- Crepon, B., Duguet, E., & Mairesse, J. (1998). Research, innovation, and productivity: An econometric analysis at the firm level (NBER Working Paper 6696).

- Dachs, B., & Ebersberger, B. (2009). Does foreign ownership matter for the innovative activities of enterprises? International Economic Policy, 6(1), 41–59. https://doi.org/10.1007/s10368-009-0126-3

- De la Potterie, P. B., & Lichtenberg, F. (2001). Does foreign direct investment transfer technology across borders? The Review of Economics and Statistic, 83(3), 490–497. https://doi.org/10.1162/00346530152480135

- Dunning, J. (1993). Multinational enterprises and the global economy. Addition-Wesley.

- Findlay, R. (1978). Relative backwardness, direct foreign investment, and the transfer of technology: A simple dynamic model. Quarterly Journal of Economics, 92(1), 1–15. https://doi.org/10.2307/1885996

- Fombang, M. S., & Adjasi, C. K. (2018). Access to finance and firm innovation. Journal of Financial Economic Policy, 10(1), 73–94.

- Garcia, F., Jin, B. and Salomon, R. (2013). Does inward foreign direct investment improve the innovative performance of local firms? Research Policy, 42, 231–244.

- Ghazel, R., & Zulkhibri, M. (2015). Determinants of innovation outputs in developing countries: Evidence from panel data negative binomial approach. Journal of Economic Studies, 42(2), 237–260. https://doi.org/10.1108/JES-01-2013-0016

- Girma, S., Gong, Y., & Gorg, H. (2005). Can you teach old dragon new tricks? FDI and innovation activity in Chinese state-owned enterprises. China and the World Research Papers, 2005/34.

- Glass, A. J., & Saggi, K. (2002). Multinational firms and technology transfer. Scandinavian Journal of Economics, 104(4), 495–513. https://doi.org/10.1111/1467-9442.00298

- Globerman, S., & Shapiro, D. (2003). Governance infrastructure and US foreign direct investment. Journal of International Business Studies, 34(1), 19–39. https://doi.org/10.1057/palgrave.jibs.8400001

- Iacovone, L., Javorcik, B., Keller, W., & Tybout, J. (2009). Walmart in Mexico: The impact of FDI on innovation and industry productivity. World Bank Working Paper.

- International Monetary Fund, and Organisation for Economic Co-operation andDevelopment. (2003). Foreign direct investment statistics: How countries measure FDI. http://www.imf.org/external/pubs/ft/fdis/2003/index.htm

- Janzen, S. A., & Carter, M. R. (2013). The impact of micro-insurance on asset accumulation and human capital investment: Evidence from a draught in Kenya (ILO Micro-Insurance Innovation Facility Research Paper No. 31). International Labour Organisation.

- Johnston, D., & Breu, A. (2013, April 18–20). Asset indices as a proxy for poverty measurement in African countries: A reassessment. The conference of African economic development: Measuring success and failure, Vancouver, Canada: Simon Fraser University.

- Khachoo, Q., & Sharma, R. (2016). FDI and innovation: An investigation into intra-and inter-industry effects. Global Economic Review, 45(4), 311–330. https://doi.org/10.1080/1226508X.2016.1218294

- Khandker, S. R. (2005). Microfinance and poverty: Evidence using panel data from Bangladesh. The World Bank Economic Review, 19(2), 263–286. https://doi.org/10.1093/wber/lhi008

- Kinoshita, Y. (2000). R&D and technology spillovers via FDI: Innovation and absorptive capacity. William Davidson Institute Working Papers, No. 349.

- Lee, J., & Mansfield, E. (1996). Intellectual property protection and US foreign direct investment. Review of Economics and Statistics, 78(2), 181–186. https://doi.org/10.2307/2109919

- Lin, H., & Lin, S. E. (2009). FDI, trade and product innovation: Theory and evidence. Southern Economic Journal, 77(2), 434–464. https://doi.org/10.4284/sej.2010.77.2.434

- Liu, X., & Zou, H. (2008). The impact of greenfield FDI and mergers and acquisitions on innovation in Chineses high-tech industries. Journal of World Business, 43(3), 352–364. https://doi.org/10.1016/j.jwb.2007.11.004

- Loukil, K. (2016). Foreign direct investment and technological innovation in developing countries. Oradea Journal of Business and Economics, 1(2), 31–40.

- Maaso, J., Roolaht, T., & Varblane, U. (2013). Foreign direct investment and innovation in Estonia. Baltic Journal of Management, 8(2), 231–248. https://doi.org/10.1108/17465261311310036

- Mansfield, E., & Romeo., M. (1980). Technology transfer to overseas subsidiaries by U.S. based firms. Quarterly Journal of Economics, 95, 737–750.

- Markusen, J. R. (2002). Multinational firms and the theory of international trade. MIT Press.

- OECD/OCDE. (2005). Oslo manual: Guidelines for collecting and interpreting innovation data (3rd ed.). OECD.

- Pai, M. K. (2016). The technical progress and resilience in productivity growth of Korea’s growth-leading industries. Asian Economic Papers, 15(2), 167–191. https://doi.org/10.1162/ASEP_a_00441

- Qu, Y., & Wei, Y. (2017). The role of domestic institutions and FDI on innovation— Evidence from Chinese firms. Asian Economic Papers, 16(2), 55–76. https://doi.org/10.1162/ASEP_a_00519

- Rodrigue-Clare, A. (1996). The division of labour and economic development. Journal of Development Economics, 49(1), 3–32. https://doi.org/10.1016/0304-3878(95)00051-8

- Rosell-Martinez, J., & Sanchez-Sellero, P. (2012). Foreign direct investment and technical progress in Spanish manufacturing. Applied Economics, 44(19), 2473–2489. https://doi.org/10.1080/00036846.2011.564155

- Rugman, A. M. (2010). Reconciling internalization theory and the eclectic paradigm. Multinational Business Review, 18(2), 1–12. https://doi.org/10.1108/1525383X201000007

- Rugman, A. M., & Verbeke, A. (2001). Subsidiary-specific advantages in multinational enterprises. Strategic Management Journal, 22(3), 237–250. https://doi.org/10.1002/smj.153

- Saggi, K. (1999). Foreign direct investment, licensing and incentives for innovation. Review of International Economics, 7(4), 699–714. https://doi.org/10.1111/1467-9396.00194

- Salomon, R. M. (2006). Spillovers to foreign market participants: Assessing the impact of export strategies on innovative productivity. Strategic Organization, 4(2), 135–164. https://doi.org/10.1177/1476127006064066

- Schumpeter, J. A. (1934). Theory of economic development. Harvard University Press.

- Schumpeter, J. A. (1942). Capitalism socialism and democracy. Harper and Brothers.

- Sivalogathasan, W., & Wu, X. (2014). The effect of foreign direct investment on innovation in South Asian emerging markets. Global Business and Organizational Excellence, 33(3), 63–76. https://doi.org/10.1002/joe.21544

- Smarzynska, B. K. (2003). Does foreign direct investment increase the productivity of domestic firms? In search for spillovers through backward linkages (Williams Davidson, Working Paper No. 548). University of Michigan Business School, Ann Arbor.

- Stiebale, J., & Reize, F. (2010). The impact of FDI through mergers and acquisitions on innovation in target firms. International Journal of Industrial Organisation, 29(2), 155–167. https://doi.org/10.1016/j.ijindorg.2010.06.003

- Stock, J. H., & Watson, M. W. (2007). Introduction to econometrics (2nd ed.). Pearson International Edition.

- Stock, J. H., & Yogo, M. (2005). Testing for weak instruments in linear IV regression. In D. W. K. Andrews & J. H. Stock (Eds.), Identification and inference for econometric models: Essays in honor of Thomas Rothenberg (pp. 80–108). Cambridge University Press.

- Terk, E., Viia, A., Lumiste, R., & Heinlo, A. (2007). Innovation in Estonian enterprises, estonian results of the fourth community innovation survey (CIS4). Enterprise Estonia.

- Vahter, P. (2010). Does FDI spur innovation, productivity and knowledge sourcing by incumbent firms? Evidence from manufacturing industry in Estonia. William Davidson Institute Working Papers, No. 986.

- Verbeke, A. (2009). International business strategy: Rethinking the foundations of global corporate success. Cambridge University Press.

- Vernon, R. (1966). International investment and international trade in the product cycle. The Quarterly Journal of Economics, 106(2), 190–207. https://doi.org/10.2307/1880689

- World Bank Enterprise Survey Dataset. (2015). World bank database. The World Bank.

- Yang, Y., Yang, X., & Doyle, B. W. (2013). The location strategy and firm value creation of Chinese multinationals. Multinational Business Review, 21(3), 232–256. https://doi.org/10.1108/MBR-03-2013-0012

Appendix A.

Table A1. Post-estimation tests on the instrumental variable model