Abstract

The present study aims to review systematically the state of the art of corporate governance in India. The study uses a sample of 161 published research papers extracted from 101 journals and 17 publishers’ databases. The results indicated that 151 studies investigated the board of directors’ issues, 90 studies analyzed ownership structure, 64 studies discussed audit committee attributes, and 11 articles studied audit quality. The results provided that among corporate governance issues, board and audit committee independence, foreign and institutional ownership have the highest and majority focus of research in India. In terms of the relationship of corporate governance with other areas, the results exhibited that financial performance has a major concern in prior research. The results also indicated that there is a lack of studies that have samples after 2015. Further, the results observed that there are numerous conceptual repetitive studies and the majority of the studies followed either descriptive statistics or basic regression analysis. The current study provides an insight for academicians, policymakers (e.g., Securities and Exchange Board of India and Ministry of Corporate Affairs—Government of India) research organizations and funding agencies of what has been done and what is left to be done. The study makes a novel contribution to the strand literature of corporate governance in India. It highlights the substantial knowledge gaps in this field and provides a potential agenda for academicians, research organizations, and funding agencies for future research.

PUBLIC INTEREST STATEMENT

Corporate governance has been gaining momentum and considerable attention from regulators, policy makers and academicians in India especially, in the past two decades due to economic growth and business failure. During this period, different studies have been conducted to assess different areas of corporate governance in India however, there are a large number of repetitive and conceptual studies. The present study has significant implications for government and private research funding agencies, stock markets, policy-makers, and academicians in India. The present study provides a clear picture of the status of corporate governance in India that will enable funding research agencies and academicians to direct their future research towards unhighlighted areas ignored by prior studies. This study brings reflective insights related to corporate governance mechanisms. It warns regulators and policy makers to revise the existing regulations of corporate governance and increase the disclosure and compliance levels in these regulations.

1. Introduction

Different studies have explored corporate governance reforms in India (e.g., Guha et al., Citation2019; Gupta & Shallu, Citation2014; Khanna & Palepu, Citation2004; Shikha, Citation2017; Srivastava et al., Citation2018). Shikha (Citation2017) states that there is a growing dialogue on how corporate governance should evolve to cope with the increasingly dynamic and global nature of the capital market. Khanna and Palepu (Citation2004) indicate that the globalization of product and talent markets has affected corporate governance of firms in the Indian software industry. Further, Gupta and Shallu (Citation2014) report that the major challenge to the corporate governance in India is the power of the dominant shareholders that can exercise influence over the political system of the country. India has a weak monitoring system with a multiplicity of regulators. Recent corporate frauds are sufficient to justify this phenomenon.

Different studies have been conducted in the field of corporate governance either used a systematic review (e.g., Ahmad & Omar, Citation2016; Azila-gbettor et al., Citation2018; Cucari, Citation2019; Daiser et al., Citation2017; Dinh & Calabrò, Citation2018; E-Vahdati et al., Citation2019; Nomran & Haron, Citation2020; Schiehll & Martins, Citation2016) or meta-analysis (e.g., García-meca & Sánchez-ballesta, Citation2009; Lagasio & Cucari, Citation2019; Mutlu et al., Citation2018). Snyder (Citation2019) differentiated among systematic review, Semi-systematic, and Integrative approaches of literature reviews. He indicates that systematic review aims to Synthesize and compare evidence, has specific research questions and systematic strategy, samples and evaluates quantitative articles, and contributes by informing policy and practice. The purpose of a “systematic review is to identify all empirical evidence that fits the pre-specified inclusion criteria to answer a particular research question or hypothesis” (Snyder, Citation2019, p. 334). Ahmad and Omar (Citation2016) indicate that there is a difference between meta-analysis and systematic review where meta-analysis may utilize different econometric and statistical procedures for analyzing and synthesizing the data and findings; systematic review does not use such tools. In this regard, (García-meca & Sánchez-ballesta, Citation2009; Lagasio & Cucari, Citation2019; Lin & Hwang, Citation2010) conducted a meta-analysis for corporate governance mechanisms using different statistical analysis such as effect size and subgroups analysis. Further, Mutlu et al. (Citation2018) used meta-analytical regression analysis (MARA) and Hedges (Citation1985) meta-analysis (HOMA) to estimate the meta-analytic mean association between firm performance and corporate governance mechanisms. From the other hand, some other studies used systematic review in corporate governance based on frequencies for published studies, studies by journals and publishers, applied statistical tools, methods, time frame, topic and area wise studies, primary and secondary research studies, and summary of the main findings (Ahmad & Omar, Citation2016; Azila-gbettor et al., Citation2018; Cucari, Citation2019; Daiser et al., Citation2017; Nomran & Haron, Citation2020; Schiehll & Martins, Citation2016). Following prior studies that used systematic review for corporate governance, we conducted a systematic review for corporate governance research in India that published between the years 2000 and 2020 subject to quality assessment which will be described later in this manuscript.

The current study aims to provide an overview of the state of the art and the existing research on corporate governance in India. We highlight how corporate governance studies in India are fragmented across a range of disciplinary fields. To the best of our knowledge, the current study is the first comprehensive review of corporate governance research in India that offers a navigation window into the existing research and methods related to corporate governance studies in India. We follow the methodology of Tranfield et al. (Citation2003) in conducting a systematic review. We also follow Ahmad and Omar (Citation2016) and Li et al. (Citation2018) who conducted a systematic review for corporate governance research. Our review offers multiple opportunities and benefits to researchers and practitioners by highlighting the importance of corporate governance research in India making a novel contribution to the strand literature of corporate governance in India. Building from this foundation, this review then discusses future research possibilities.

The present study is organized as follows: Section 2 introduces the literature review, section 3 provides the methodology of the study. Section 4 discusses the process of selection and quality assessment for inclusion the research studies in the current study, section 5 presents a discussion and data synthesis, and section 6 concludes.

2. Literature review

There are a wide variation and fragmentation among corporate governance studies in India across disciplinary fields including finance, corporate governance practices, earning management, firm performance, firm value, and some other issues. Different areas have been investigated with corporate governance such as corporate illegality (Kaur, Citation2017), financial disclosure (Haldar & Raithatha, Citation2017), equity (Fruin & Dossani, Citation2012; Srivastava et al., Citation2019), internal control disclosure (Ashfaq & Rui, Citation2019), international competitiveness (Haldar et al., Citation2016), ownership (Gollakota & Gupta, Citation2006), quality of financial information (Hundal, Citation2016), regulatory and market model (Sehgal & Mulraj, Citation2008), risk reporting (Saggar & Singh, Citation2017), Satyam failure (Narayanaswamy et al., Citation2015), stock market volatility and efficiency (Prasanna, Citation2013), sustainability (Kansil & Singh, Citation2018) and talent management (Chahal & Kumari, Citation2013).

Majority of corporate governance studies in India are linked with financial performance (e.g., Arora & Sharma, Citation2016; Bansal & Sharma, Citation2016; Bhatt & Bhattacharya, Citation2015; Kandukuri et al., Citation2015; Mishra & Mohanty, Citation2014; Palaniappan, Citation2017; Rani et al., Citation2014; Sanan, Citation2016; Singla & Singh, Citation2019; Yameen et al., Citation2019). The results of these studies are inconsistent and the findings are conflicted in some cases. Some studies reported that there is an association between corporate governance indicators and financial performance (Arora & Sharma, Citation2016; Kandukuri et al., Citation2015; Rani et al., Citation2014). Some other studies revealed that some corporate governance attributes only have a positive influence on firms’ performance; larger board size and attendance of the board members (Bhatt & Bhattacharya, Citation2015), promoters’ ownership (Mishra & Kapil, Citation2017), board age diversity (Kagzi & Guha, Citation2018), board size and CEO Chairman dual role (Bansal & Sharma, Citation2016), independent women directors (Sanan, Citation2016), board independence, board size and busyness (Mishra & Kapil, Citation2018). Contradictory, different studies reported that corporate governance attributes have no association with firms’ performance. For example, Mishra and Mohanty (Citation2014), Kagzi and Guha (Citation2018), Bansal and Sharma (Citation2016), Bhatt and Bhattacharya (Citation2015), and Mishra and Kapil (Citation2017) respectively declared that gender and tenure diversity of the board, audit committee independence and its meetings frequency, independent directors in the board, and board independence have insignificantly impact on firm performance. However, Bhatt and Bhattacharya (Citation2017) showed a negative impact of board structure on firm performance in family firms compared to nonfamily firms. Further, Palaniappan (Citation2017) found a statistically significant negative relationship between board size and firm performance. Kagzi and Guha (Citation2018) indicated that education diversity negatively affects firm performance.

Firm value also has been a subject of investigation by different corporate governance studies in India (e.g., Chauhan & Kumar, Citation2017; Khosa, Citation2017; Kumar & Singh, Citation2013; Mishra & Kapil, Citation2017, Citation2018, Citation2018). Kumar and Singh (Citation2013) reported a negative relationship between board size and firm value and a positive association of promoter ownership level and corporate performance. Khosa (Citation2017) revealed that there is a reverse relationship between board independence and firm value of group-affiliated firms in India which shows that foreign monitoring directors are largely influenced by the institutional setting and ownership structure. Singla and Singh (Citation2019) declared that board independence bears a significantly negative relationship with firm value however, audit committee independence was positively and significantly related to the firm value.

In another context, several studies explored corporate governance practices (e.g., Abraham et al., Citation2015; Al‐Mudhaki & Joshi, Citation2004; Bose, Citation2009; Chatterjee, Citation2011; Haldar et al., Citation2018; Islam, Citation2016; Katarachia et al., Citation2018; Kiranmai & Mishra, Citation2019; Kota & Tomar, Citation2010; Mayur & Saravanan, Citation2017; Prasad et al., Citation2019; Sarkar et al., Citation2012; Srivastava et al., Citation2018; Subramanian, Citation2017; Subramanian & Reddy, Citation2012). Abraham et al. (Citation2015) stated that Indian companies have a high level of compliance with corporate governance disclosure requirements especially, after amendments to Clause 49 as the penalties for noncompliance increase in severity. Importantly, they reported that government-controlled firms have a low level of compliance than privately owned firms. However, Katarachia et al. (Citation2018) declared that there is a need for improvement in corporate governance disclosure by Indian companies, as they fail to comply with the majority of the proposed disclosure items. Subramanian and Reddy (Citation2012) showed that firms gain competitiveness in international markets when they voluntarily disclose more about their board practices, but ownership-related disclosures reduce market share. Al‐Mudhaki and Joshi (Citation2004) concluded there is a lack of audit committee independence in their representation and composition. Prasad et al. (Citation2019) found that CEOs directors who belong to controlling shareholders got higher pay as compared to professional CEOs. Chauhan and Kumar (Citation2017) pointed out that female directors face more attendance problems compared to male directors, and are less likely to be employed in monitoring-related committees.

In another quest, corporate governance studies in India can be divided into three streams according to the research approach and data used by these studies. These three streams are: (1) studies based on primary data and indices, (2) research studies based on secondary data, and 3) conceptual or review research studies.

2.1. Studies based on primary data and indices

Different studies have been conducted and linked with corporate governance. Some of these studies utilized a qualitative approach using primary data in the form of interviews or content analysis and some other studies used a quantitative approach in the form of surveys. There are 10 studies that used questionnaires and 22 other studies that employed corporate governance score or index to investigate corporate governance issues. Table illustrates corporate governance studies in India that utilized surveys, interviews, and indices.

Table 1. Corporate governance studies based on primary data and indices

2.2. Research studies based on secondary data

The majority of corporate governance studies in India used secondary data in the form of financial information derived from annual reports of firms or from some other data sources. There are 92 research studies that used a firm-specific/bank-specific quantitative data or quantitative score to investigate corporate governance issues. These studies linked corporate governance attributes with different areas of research such as firm performance, stock market performance, earning management, cash flow, and some other areas of research. The following is Table which demonstrates corporate governance studies in India that utilized secondary data.

Table 2. Corporate governance studies based on secondary data

2.3. Conceptual and review studies

There are a large number of corporate governance research studies that have a conceptual or review approach in India. Thirty-three research studies discuss various issues of corporate governance such as governance regulations, governance reforms or compare Indian with some other countries. Following is Table which shows conceptual or review corporate governance studies in India.

Table 3. Conceptual and review corporate governance studies in India

3. Methodology

The present study uses a systematic review of prior studies related to corporate governance in India. The systematic review approach is widely used by researchers (e.g., Petticrew & Roberts, Citation2006; Tranfield et al., Citation2003; Walker, Citation2010). Tranfield et al. (Citation2003) advocate that systematic review is a genuine piece of investigation science and enhances the quality of the review. Similarly, Petticrew and Roberts (Citation2006) state that systematic review is an appropriate and effective approach in identifying the areas where little or no evidence exists. Further, Tranfield et al. (Citation2003) argue that “traditional or narrative reviews frequently thoroughness, and in many cases are not undertaken as a genuine piece of investigation”. Accordingly, the present study follows a systematic review of the pertinent literature of corporate governance in India. Tranfield et al. (Citation2003) described three stages with nine phases to conduct a systematic review in management research. However, Ahmad and Omar (Citation2016) in their systematic review of corporate governance customized these phases into five-step process which are presented in Figure ) as follows:

Figure 1. Steps of Systematic Review [Source: Ahmad and Omar (Citation2016), extracted from Tranfield et al. (Citation2003), adopted from NHS Centre for Reviews and Dissemination (2001)].

![Figure 1. Steps of Systematic Review [Source: Ahmad and Omar (Citation2016), extracted from Tranfield et al. (Citation2003), adopted from NHS Centre for Reviews and Dissemination (2001)].](/cms/asset/3da2efe0-5ae5-4482-847b-5cfae32cad8e/oabm_a_1803579_f0001_oc.jpg)

3.1. Defining research questions

Three research questions are formulated for the present study in order to address the state of the art related to corporate governance in India which are as follows:

RQ1: What are the research outlets that have been used to publish corporate governance studies in India?

RQ2: How corporate governance attributes have been addressed by prior studies in India?

RQ3: What are the different types of sampling units, data, statistical tools, and time frame that have been used by prior corporate governance research in India?

RQ4: What are the different areas of research that have been linked with corporate governance research in India?

3.2. Boolean search and keywords

3.2.1. Identification of keywords

Different keywords used to extract the research studies required for the present study. At the outset, a general term of corporate governance was used regardless of the area or aspect of the research. This yielded a huge number of studies and reports about corporate governance. Some of these sources were not useful for the present study. Consequently, different terminologies were used to limit the search such as corporate governance mechanisms, corporate governance attributes, board of directors, audit committee, and ownership.

3.2.2. Databases

At the time of search, we identified different databases that contain such studies, these databases include Emerald, Since Direct, Springer, Taylor and Francis, Wiley online Library, Sage Journals, Inderscience, and Google Scholar. Besides to the identified databases, we identified different websites and databases that have some research related to corporate governance in India. Some of these research databases and publishers are either predatory or commercial journals that publish manuscripts without peer-review. However, some studies published by these publishers have some citations which make us to consider them among our review because they are cited by different studies and leading some other publications. The criteria for selection of research studies are discussed in the next section.

3.2.3. Boolean search

The present study analyses the governance literature from 2000 to 2020. The reason behind starting the time period from 2000 is that India introduced its Desirable Corporate Governance Code by CII in 1998. Further, the formal enactment of corporate governance code in India represented by Clause 49 of listing agreement which is issued by Securities Board Exchange of India (SEBI) was started in the years between 2000 and 2004.

Different Boolean search operators were used to extract the required studies from the databases and search engines. At the outset, AND was used to connect different concepts and limit our search. Further, OR Boolean search operator was used to find different ways to phrase a concept and expand the search. At the same time, Truncation was used to search any ending on a root word. For better results, different advanced Boolean search operators are used such as: Wildcards, Quotation marks, “adj,” publication date, material type, language, and country of origin. Finally, snowballing as an effective way of identifying further keywords and synonyms for our search was used. Table shows the different Boolean search operators used by the study.

Table 4. Boolean search

4. Selection of studies and quality assessment

Based on the preceding step, different criteria for inclusion and exclusion of a research study are applied in order to avoid duplications and select the relevant and high-quality papers; the following criteria are followed:

a-Including articles that only related to India or have empirical evidence from India.

b-Studies that explicitly related to audit committee, board of directors, ownership structure, and some other related issues of corporate governance such as board committees, remuneration, audit quality, and some other issues.

c-Studies that are published based on peer-reviewed journals.

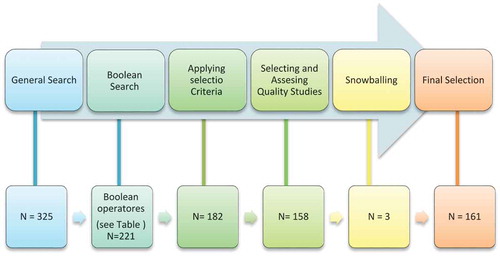

As noted in Figure , a general search opted which yielded about 325 studies related to corporate governance in India. Consequently, to reduce the search limit, Boolean operators were used which produced 221 studies. Further, after applying the selection criteria, a number of 182 studies were selected for screening and final check. Then, a final selection and quality assessment of studies were conducted which exclude 19 studies and left with 158 research papers. Finally, to make sure that at least the majority of the quality studies are included, we conducted a snowballing analysis in which the bibliographies of the selected research papers were checked. This step produced 3 studies that were added to the final selection and to produce 161 studies as a final sample for the current study.

Figure 2. The process of selecting the search studies.

5. Data synthesis and discussion

The retrieved literature is analyzed and categorized to meet the research questions framed above. Following is a discussion of the analyzed studies:

5.1. Publishers and journals outlets

This classification summarizes the retrieved studies based on the journals that the studies published in. Further, it provides a classification of these studies based on different periods that the studies have been published with their number of citations. This subsection provides an answer for the first question framed for this study which asks about the different research outlets used by prior corporate governance research in India. The highest number of research articles were published in the International Journal of Corporate Governance, Inderscience publishers which have 9 papers. With regards to the publisher’s outlet, the results provide an idea about the forums that the studies have been published in. The studies are mostly published in Emerald and Elsevier which have 46 studies each followed by Inderscience which has 29 papers, Springer which has 19 studies, 4 studies for SAGE, 2 articles for Wiley and the remaining studies are distributed among the other publishers (Please see Table below). Further, the results show that Elsevier journals have the highest number of citations; 4336 followed by Wiley (1051), Springer (852), and Emerald (658) which indicates that these journals are leading corporate governance studies in India.

Table 5. Publishers’ Outlets and Top 10 Journals by No. of published papers

Table below shows the publishers’ and journals’ outlets with a detailed description of the number of citations for each manuscript and the period of publishing each article. The rationale behind providing the number of citations for each article is to show the manuscript that has high numbers of citations. Logically, some research articles published in early years may have higher numbers of citations compared to recent years’ articles. However, when an early published issued article is cited by recent years’ manuscripts, it indicates that the early issued articles are the main source of recent years’ articles and they are leading all recent research articles. Accordingly, the number of citations is presented to indicate the leading articles in corporate governance in India.

Table 6. Journals’ Outlets and Frequency of Studies by Years

The sampled studies are published in different numbers of journals; 101 journals. 17 journals have 2 publications each, 2 journals have 3 research studies each, 4 other journals have 5 papers each, 3 journals published 6 manuscripts each, 1 journal has 9 publications. Moreover, there is an increasing number of studies over time which are distributed as 1 study in the period up to 2000, 8 studies in the period from 2001 to 2005, 16 research papers were published during the period from 2006 to 2009, 35 articles were found in the years from 2010 up to 2014 and 101 research papers were published in the period from 2015 up to 2020 (January).

5.2. Corporate governance attributes studied by prior research

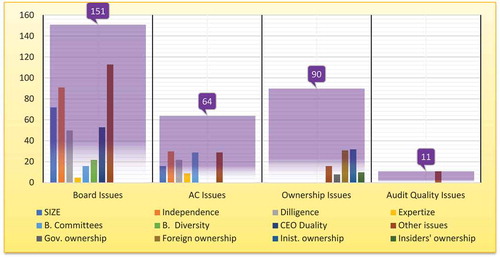

This section provides an answer to the second question outlined for this study which asks about how corporate governance attributes have been addressed by prior studies in India? The results show that there are 151 studies that investigated board of directors’ issues which is the highest frequency among corporate governance attributes, 90 studies that analyzed ownership structure, 64 studies are discussed audit committee attributes and 11 articles studied audit quality by Big-Four audit companies see (Figure ). More specifically, Figure ) proposes that among board of directors’ issues, board independence has the majority focus by prior research in India (91), followed by board size (72), CEO duality (53), board diligence (50), board diversity and gender (22), board committees (16) and board expertise (5). Further, 113 studies investigated different issues of board such as board interlocks, multiple directorships, board profile, remuneration, and some other issues. Similarly, audit committee attributes investigated by prior research in India were distributed in different areas such as Audit committee size, independence, diligence, expertise, and some other issues with a frequency distribution of 16, 30, 22, 9, and 29 respectively. This means that audit committee independence and diligence have the majority concentration by the majority of prior research in India. Finally, ownership structure has been a matter of research by several studies in India. However, both foreign and institutional ownership have the highest frequency of research articles (32 and 31 respectively) as compared to other ownership variables like; government ownership, insider ownership, and ownership concentration (8, 10 and 16 respectively).

Figure 3. Corporate Governance Issues Investigated.

5.3. Sampling, data, statistical tools and time frame

5.3.1. Sampling units

With regards to the sampling units investigated by prior studies of corporate governance in India, Table panel (A) presents industry-wise research studies. The results show that 64 studies have been conducted using data from different industries. These studies are distributed as 35 qualitative studies, 15 qualitative studies based on index and score, 3 quantitative scores, 9 studies which are based on a questionnaire, and 2 conceptual and review studies. Likewise, studies are distributed among different industries including non-financial industries, service industries except financial, financial industry and manufacturing which have 24, 13, 13, and 10 respectively. However, there are 27 review and conceptual studies and 21 papers that we could not identify their research field.

Table 7. Sampling data and statistical tools (Frequencies)

Concerning sectors wise studies, Table panel B also shows that 87 studies have mixed data from both private and public sectors. However, corporate governance studies focused on the public sector have a frequency of 6 studies as compared to the private sector which has 18 studies.

5.3.2. Data types

With regards to the type of data, panel (C) of Table shows that the majority of corporate governance studies used secondary data 56% of 154 articles sourced from annual reports of listed firms, stock markets databases, Prowess Q data base or/and some other sources. However, only 7% of the researches conducted have primary data using questionnaire surveys. Further, the results report that 84 studies have been found to have quantitative aspects with secondary data from annual reports. These studies were focused on absolute financial and non-financial data. However, there are 22 studies that were based on Qualitative Index and 15 other studies that were based on quantitative `scores. These studies either frame a compliance index of 0 and 1 or a quantitative score based on a list of items of corporate governance issues.

5.3.3. Modeling and analyzing tools

As far as the statistical tools are concerned, the majority of prior studies of corporate governance in India have applied multiple regression models. Table in its panel (D) demonstrates that 73 studies used regression analysis 21 studies adopted panel analysis with fixed or random effect models, 14 articles analyzed their results using descriptive statistics and frequency distributions, 3 articles utilized non-parametric tests, 3 research papers used GMM, and 18 other articles used different statistical tools such as event analysis, GARCH analysis, and some other tools.

5.3.4. Time frame and sampling period

Table provides a description of sample size, time frame and sampling periods considered by prior studies of corporate governance in India. Panel (A) of Table indicates that there are 8 studies that have a sample of below 10 firms. Similarly, 8 studies have a sample ranging between 11 and 30 firms, 14 articles sampled 31 and 70 firms, 17 research papers have a sample of 71 up to 100 sample units, 33 research have samples between 101 and 200, 31 studies have samples of 201 up to 400 firms, and 11, 7 and 3 papers used samples of 401 up to 1000, 1001 up to 2000 and more than 2000 firms respectively. This means that the majority of prior studies in India have samples ranging between 100 up to 400 firms.

Table 8. Description of sampling size and time frame of prior research of corporate governance in India

The results in panel (B) demonstrate that there are some studies that made a comparison of India with some other countries. These studies were distributed as 20 studies that compared India with 2 up to 10 other countries, 8 research papers that compared India with more than 20 other countries, and 7 articles made a comparison between India and 11 to 20 other countries.

Panel (C) provides frequencies of studies that have samples that start at a certain point of time. The time frame was divided into five categories. The first category includes studies that start their sampling from the period before 2000. This category has 14 studies which indicate that 14 studies have a sampling period starting before 2000. The second category contains the studies that start their sampling in the years between 2000 and 2005. In this category, 42 studies have samples with a time frame starting in the years between 2000 and 2005. Similarly, the other three categories include studies that have sampling periods starting in the years between 2006 and 2010, 2011 and 2015, and 2016 onwards. 46 studies have sampling periods starting in the years between 2006 and 2010. Further, 22 studies have sampling periods starting in the years between 2011 and 2015 against 4 studies only that have samples with a time frame that starts from 2016 onwards.

Panel (D) presents frequencies of studies that have samples that end at a certain point of time. the results show that there is one study that has a sample with a time frame ended in the period before 2000. Further, the results show that 15 articles have sampling periods that ended in the years between 2000 and 2005. Similarly, 20 researches have a sampling time frame that ended in the years between 2006 and 2010 against 74 papers that have a sampling time frame ended in the years between 2011 and 2015. However, there are 9 studies only that have samples with the time frame ended in 2016. This indicates that the majority of corporate governance studies have samples in the years between 2006 and 2015.

5.4. Research areas linked with corporate governance attributes

Table demonstrates that among the areas linked with corporate governance attributes, firm performance has the highest frequency among other studies which have been a subject of an investigation by 51 studies. The other areas that statistically functioned by corporate governance mechanisms are corporate governance disclosures which have 7 articles, stock performance which has 8 studies, earning management with 3 manuscripts, remuneration with 6 studies, CSR with 3 papers, cash flow and dividends with 2 articles each and some other issues that have 33 research.

Table 9. Panel E: Studies by Areas Linked and Studied with Corporate Governance Attributes (Frequencies)

6. Conclusion

The present study highlights a review of corporate governance research in India. More importantly, this study discusses the different types of studies, publishing outlets, sampling units, data types, statistical tools, and the most researched areas that have been linked with corporate governance in India. The results found that the sampled studies are published in different numbers of journals spreading in 101 journals and are mostly published in Emerald which has 46 studies followed by Elsevier which has 46 articles, Inderscience which has 29 papers, Springer which has 16 studies and 4 studies for SAGE and 2 for Wiley each and 18 other studies were published by different publishers. Concerning corporate governance attributes studied, the results indicated that 151 studies investigate board of directors’ issues which is the highest frequency among corporate governance attributes, 90 studies that analyzed ownership structure, 64 studies are discussed audit committee attributes and 11 articles studied audit quality by Big-Four audit companies. More specifically, board independence has the majority focus by prior research in India 91 research, followed by board size 72 studies. Further, the results showed that there is a lack of studies that have samples after 2015. The results also observed that there are numerous conceptual repetitive studies and the majority of the studies followed either descriptive statistics or basic regression analysis. With regards to the research areas linked and studied with corporate governance attributes, the results found that firm performance has the highest frequency amongst other studies which have been a subject of investigation.

The present study has significant implications for government and private research funding agencies, stock markets, policy-makers, and academicians in India. Generally, research funding agencies and academicians conduct research in corporate governance; however, there is no clear picture of the current status of corporate governance research in India. The present study provides a clear picture of the status of corporate governance in India that will enable funding research agencies and academicians to direct their future research towards unhighlighted areas ignored by prior studies. Different research areas can be investigated by future studies such as IT governance, the impact of corporate governance on environmental disclosure, the impact of corporate governance on financial reporting quality post-Ind. AS convergence, corporate governance and compliance with accounting standards, corporate governance practices during COVID-19, the role and impact of board and audit committee expertise in India. Further, some other research areas which need to be addressed in India are also narrative reporting and corporate governance, green governance, and sustainability reporting.

Regulators and policymakers should revise the existing regulations of corporate governance and increase the disclosure and compliance levels with these regulations. This study brings reflective insights related to corporate governance mechanisms. The pertinent literature points to the existence of a gap in practice, not only in the issues of transparency and disclosure of corporate governance mechanisms but also the methods, sampling periods and the statistical tools that have been used by prior research. Further, corporate governance practices after the revised corporate governance code in India have not been covered adequately by research studies. Therefore, the present study adds to the existing stock of knowledge and the body of literature by providing an opportunity to understand the status of corporate governance research in India.

Additional information

Funding

Notes on contributors

Faozi A. Almaqtari

Faozi A. Al Maqatari is an assistant professor, department of Accounting, Hodeidah University,Yemen. Dr. Faozi has participated in several international, national conferences, and workshops. He has authored, coauthored, and reviewed various international and national papers in different esteemed journals from different publishers including: Wiley, Taylor & Francis, Emerald, and Inderscience.

Hamood Mohd. Al-Hattami is a senior lecturer at department of Accounting, Hodeidah University, Yemen. He attended different international and national conferences. He has published several papers indexed in Scopus and SCI journals in different countries.

Khaled M. E. Al-Nuzaili is a senior lecturer, department of Accounting, Ibb University, Yemen. He attended different international and national conferences. He has published papers in International conferences.

Mohammed A. Al-Bukhrani is a senior lecturer, department of Accounting, Al baydha University, Yemen. He attended different international and national conferences. He has published papers in International conferences.

References

- Abraham, S., Marston, C., & Jones, E. (2015). Disclosure by Indian companies following corporate governance reform. Journal of Applied Accounting Research, 16(1), 114–56. https://doi.org/10.1108/JAAR-05-2012-0042

- Adnan, S. M., Hay, D., & Van Staden, C. J. (2018). The influence of culture and corporate governance on corporate social responsibility disclosure: A cross country analysis. Journal of Cleaner Production, 198, 820–832. https://doi.org/10.1016/j.jclepro.2018.07.057

- Aggarwal, R., & Ghosh, A. (2015). Director’s remuneration and correlation on firm’s performance. International Journal of Law and Management, 57(5), 373–399. https://doi.org/10.1108/IJLMA-08-2011-0006

- Aggarwal, R., Jindal, V., & Seth, R. (2019). Board diversity and fi rm performance: The role of business group a ffi liation. International Business Review, 28(6), 1–17. https://doi.org/org/10.1016/j.ibusrev.2019.101600

- Ahmad, S., & Omar, R. (2016). Basic corporate governance models: A systematic review. International Journal of Law and Management, 58(1), 73–107. https://doi.org/10.1108/IJLMA-10-2014-0057

- Akbar, M., & Khan, A. (2008). Corporate governance and the role of institutional investors in India corporate governance and the role of institutional investors in India. Journal of Asia-Pacific Business, 7(2), 37–41. https://doi.org/org/10.1300/J098v07n02

- Al-ahdal, W. M., Alsamhi, M. H., Tabash, M. I., & Farhan, N. H. S. (2020). Research in international business and finance the impact of corporate governance on fi nancial performance of Indian and GCC listed fi rms : An empirical investigation. Research in International Business and Finance, 51(August2019), 101083. https://doi.org/10.1016/j.ribaf.2019.101083

- Almaskati, N., Bird, R., & Lu, Y. (2020). Corporate governance, institutions, markets, and social factors. Research in International Business and Finance, 51(2020101089), 1–20. https://doi.org/org/10.1016/j.ribaf.2019.101089

- Al‐Mudhaki, J., & Joshi, P. L. (2004). The role and functions of audit committees in the Indian corporate governance: Empirical findings. International Journal of Auditing, 8(1), 33–47. https://doi.org/10.1111/j.1099-1123.2004.00215.x

- Amaladoss, M. X., Manohar, H. L., & Jacob, F. (2011). Communicating corporate governance through websites : A case study from India. International Journal of Business Governance and Ethics, 6(4), 311–339. https://doi.org/10.1504/IJBGE.2011.044734

- Annamalai, B., & Ranjan, P. (2018). Corporate governance data of 6 Asian economies (2010 – 2017). Data in Brief, 20, 53–56. https://doi.org/org/http://dx.doi.10.1016/j.dib.2018.07.048

- Aparna, M., & Mehta, M. (2014). Empirical study of board and corporate governance practices in indian corporate sector : Analysis of CG practices of ITC and ONGC. Procedia Economics and Finance, 11(14), 42–48. https://doi.org/org/http://dx.doi.10.1016/S2212-5671(14)00174-9

- Arora, A., & Bhandari, V. (2017). Do firm-level variables affect corporate governance quality and performance? Evidence from India. International Journal of Corporate Governance, 8(1), 1–24. https://doi.org/10.1504/IJCG.2017.085230

- Arora, A., & Sharma, C. (2016). Corporate governance and firm performance in developing countries : Evidence from India. Corporate Governance, 16(2), 420–436. https://doi.org/10.1108/CG-01-2016-0018

- Ashfaq, K., & Rui, Z. (2019). The effect of board & audit committee effectiveness on internal control disclosure under different regulatory environments in South Asia. Journal of Financial Reporting and Accounting, 17(2), 170–200. https://doi.org/10.1108/JFRA-09-2017-0086

- Azila-gbettor, E. M., Honyenuga, B. Q., Berent-braun, M. M., & Kil, A. (2018). Structural aspects of corporate governance and family firm performance : A systematic review governance. Journal of Family Business Management, 8(3), 306–330. https://doi.org/10.1108/JFBM-12-2017-0045

- Bachmann, S., & Pereira, V. (2014). Corporate human rights responsibility and multinationality in emerging markets – A legal perspective for corporate governance and responsibility. International Journal of Business Governance and Ethics, 9(1), 52–67. https://doi.org/10.1504/IJBGE.2014.062770

- Bajpai, A., & Mehta, M. (2014). Empirical study of board and corporate governance practices in Indian corporate sector: Analysis of CG practices of ITC and ONGC. Procedia Economics and Finance, 11(2014), 42–48. https://doi.org/10.1016/S2212-5671(14)00174-9

- Balasubramanian, N., Black, B. S., & Khanna, V. (2010). The relation between firm-level corporate governance and market value : A case study of India. Emerging Markets Review, 11(4), 319–340. https://doi.org/10.1016/j.ememar.2010.05.001

- Balasubramanian, N., & George, R. (2012). Corporate governance and the Indian institutional context : Emerging mechanisms and challenges In conversation with K. V. Kamath, Chairman, Infosys and ICICI Bank. IIMB Management Review, 24(4), 215–233. https://doi.org/10.1016/j.iimb.2012.10.001

- Bansal, N., & Sharma, A. K. (2016). Audit committee, corporate governance and firm performance : Empirical evidence from India. International Journal of Economics and Finance, 8(3), 103–116. https://doi.org/org/10.5539/ijef.v8n3p103

- Bell, R. G., Moore, C. B., & Filatotchev, I. (2012). Strategic and institutional effects on foreign IPO performance : Examining the impact of country of origin, corporate governance, and host country effects. Journal of Business Venturing, 27(2), 197–216. https://doi.org/10.1016/j.jbusvent.2010.11.001

- Bepari, M. K. (2015). Relative and incremental value relevance of book value and earnings during the global financial crisis. International Journal of Commerce and Management, 25(4), 531–556. https://doi.org/10.1108/IJCoMA-11-2012-0072

- Bhatt, R. R., & Bhattacharya, S. (2015). Board structure and firm performance in Indian IT firms. Journal of Advances in Management Research, 12(3), 232–248. https://doi.org/10.1108/JAMR-07-2014-0042

- Bhatt, R. R., & Bhattacharya, S. (2017). Family fi rms, board structure and fi rm performance : Evidence from top Indian fi rms. International Journal of Law and Management, 59(5), 699–717. https://doi.org/http://dx.doi.10.1108/IJLMA-02-2016-0013

- Bhaumik, S., Dri, N., Gaur, A., Mickiewicz, T., & Vaaler, P. (2019). Corporate governance and MNE strategies in emerging economies. Journal of World Business, 54(4), 234–243. https://doi.org/10.1016/j.jwb.2019.03.004

- Black, B. S., & Khanna, V. S. (2007). Can corporate governance reforms increase firm market values? Event study evidence from India. Journal of Empirical Legal Studies, 4(4), 749–796. https://doi.org/10.1111/j.1740-1461.2007.00106.x

- Bose, I. (2009). Corporate governance and law-role of independent directors : Theory and practice in India. Social Responsibility Journal, 5(1), 94–111. https://doi.org/10.1108/17471110910940032

- Braga-alves, M. V., & Morey, M. (2012). Predicting corporate governance in emerging markets. Journal of International Money and Finance, 31(6), 1414–1439. https://doi.org/10.1016/j.jimonfin.2012.02.009

- Buvanendra, S., Sridharan, P., & Thiyagarajan, S. (2017). Firm characteristics, corporate governance and capital structure adjustments : A comparative study of listed firms in Sri Lanka and India. IIMB Management Review, 29(4), 245–258. https://doi.org/10.1016/j.iimb.2017.10.002

- Chahal, H., & Kumari, A. (2013). Examining talent management using CG as proxy measure : A case study of State Bank of India. Corporate Governance: The International Journal of Business in Society, 13(2), 198–207. https://doi.org/10.1108/14720701311316670

- Chakrabarti, R., Megginson, W., & Yadav, P. K. (2008). Corporate governance in India. Journal of Applied Corporate Finance, 20(1), 59–72. https://doi.org/10.1111/j.1745-6622.2008.00169.x

- Chatterjee, D. (2011). A content analysis study on corporate governance reporting by Indian Companies. Corporate Reputation Review, 14(3), 234–246. https://doi.org/org/10.1057/crr.2011.13

- Chauhan, Y., & Kumar, D. (2017). Do female directors really add value in Indian firms? Journal of Multinational Financial Management, 42–43(2017), 24–36. https://doi.org/10.1016/j.mulfin.2017.10.005

- Chauhan, Y., Lakshmi, K. R., & Dey, D. K. (2016). Journal of contemporary accounting & economics corporate governance practices, self-dealings, and firm performance : Evidence from India. Journal of Contemporary Accounting & Economics, 12(3), 274–289. https://doi.org/10.1016/j.jcae.2016.10.002

- Chen, K. C. W., Chen, Z., & Wei, K. C. J. (2009). Legal protection of investors, corporate governance, and the cost of equity capital. Journal of Corporate Finance, 15(3), 273–289. https://doi.org/10.1016/j.jcorpfin.2009.01.001

- Claessens, S., & Yurtoglu, B. B. (2013). Corporate governance in emerging markets : A survey. Emerging Markets Review, 15, 1–33. https://doi.org/10.1016/j.ememar.2012.03.002

- Col, B., & Sen, K. (2017). The role ofcorporate governance for acquisitions by the emerging market multinationals: Evidence from India. Journal of Corporate Finance, 59, 239–254. https://doi.org/10.1016/j.jcorpfin.2017.09.014

- Connor, T. O., Kinsella, S., & Sullivan, V. O. (2013). Legal protection of investors, corporate governance, and investable premia in emerging markets. International Review of Economics and Finance, 29, 426–439. https://doi.org/10.1016/j.iref.2013.07.003

- Cucari, N. (2019). Qualitative comparative analysis in corporate governance research: A systematic literature review of applications. Corporate Governance: The International Journal of Business in Society, 19(4), 717–734. https://doi.org/10.1108/CG-04-2018-0161

- Daiser, P., Ysa, T., & Schmitt, D. (2017). Corporate governance of state-owned enterprises : A systematic analysis of empirical literature. International Journal of Public Sector Management, 30(5), 447–466. https://doi.org/10.1108/IJPSM-10-2016-0163

- Das, A., & Dey, S. (2016). Role of corporate governance on firm performance : A study on large Indian corporations after implementation of Companies ’ Act 2013. Asian Journal of Business Ethics, 5(1–2), 149–164. https://doi.org/10.1007/s13520-016-0061-7

- Das, N., & Pattanayak, J. K. (2016). Corporate governance mechanism for academic institutions imparting higher education in India. International Journal of Management Education, 10(2), 204–217. https://doi.org/10.1504/IJMIE.2016.075561

- Dash, A. K. (2012). Media impact on corporate governance in India : A research agenda. Corporate Governance: The International Journal of Business in Society, 12(1), 89–100. https://doi.org/10.1108/14720701211191355

- De Jonge, A. (2014). The glass ceiling that refuses to break : Women directors on the boards of listed firms in China and India. Women’s Studies International Forum, 47(Part B), 326–338. https://doi.org/10.1016/j.wsif.2014.01.008

- Diallo, B. (2017). Corporate governance, bank concentration and economic growth. Emerging Markets Review, 32, 28–37. https://doi.org/10.1016/j.ememar.2017.05.003

- Dinh, T. Q., & Calabrò, A. (2018). Asian family firms through corporate governance and institutions: A systematic review of the literature and agenda for future research. International Journal of Management Reviews, 21(1), 50–75. https://doi.org/10.1111/ijmr.12176

- Dwivedi, N., & Jain, A. K. (2005). Corporate governance and performance of Indian firms : The effect of board size and ownership. Employee Responsibilities and Rights Journal, 17(3), 161–172. https://doi.org/10.1007/s10672-005-6939-5

- Esqueda, O. A., & Connor, T. O. (2020). Research in international business and finance corporate governance and life cycles in emerging markets. Research in International Business and Finance, 51(January–101077), 1–24. https://doi.org/10.1016/j.ribaf.2019.101077

- Estrin, S., & Prevezer, M. (2011). The role of informal institutions in corporate governance: Brazil, Russia, India, and China compared. Asia Pacific Journal of Management, 28(1), 41–67. https://doi.org/10.1007/s10490-010-9229-1

- E-Vahdati, S., Zulkifli, N., & Zakaria, Z. (2019). Corporate governance integration with sustainability: A systematic literature review. Corporate Governance (Bingley), 19(2), 255–269. https://doi.org/10.1108/CG-03-2018-0111

- Francis, B., Hasan, I., Song, L., & Waisman, M. (2013). Corporate governance and investment-cash fl ow sensitivity : Evidence from emerging markets. Emerging Markets Review, 15(June 2013), 57–71. https://doi.org/10.1016/j.ememar.2012.08.002

- Fruin, M., & Dossani, R. (2012). Private equity and corporate governance in India. Journal of Asia Business Studies, 6(2), 223–238. https://doi.org/10.1108/15587891211254416

- García-meca, E., & Sánchez-ballesta, J. P. (2009). Corporate governance and earnings management : A meta-analysis. Corporate Governance: An International Review, 17(5), 594–610. https://doi.org/10.1111/j.1467-8683.2009.00753.x

- Gill, S. (2013). Rethinking the primacy of board efficacy for governance : Evidence from India. The International Journal of Business in Society, 13(1), 99–129. https://doi.org/10.1108/14720701311302440

- Goel, K., & Mciver, R. (2015). India’s corporate governance reforms and listed corporations’ capital structures. Delhi Business Review, 16(2), 7–19. https://www.indianjournals.com/ijor.aspx?target=ijor:dbr&volume=16&issue=2&article=002

- Goel, P. (2018). Implications of corporate governance on financial performance : An analytical review of governance and social reporting reforms in India. Goel Asian Journal of Sustainability and Social Responsibility, 3(4), 1–21. https://doi.org/10.1186/s41180-018-0020-4

- Gollakota, K., & Gupta, V. (2006). History, ownership forms and corporate governance in India. Journal of Management History, 12(2), 185–198. https://doi.org/10.1108/13552520610654078

- Gopinath, S. (2008). Corporate governance in the Indian banking industry. International Journal of Disclosure and Governance, 5(3), 186–204. https://doi.org/10.1057/jdg.2008.8

- Guha, S. K., Samanta, N., Majumdar, A., Singh, M., & Bharadwaj, A. (2019). Evolution of corporate governance in India and its impact on the growth of the financial market : An empirical analysis. Corporate Governance: The International Journal of Business in Society, 19(5), 945–984. https://doi.org/10.1108/CG-07-2018-0255

- Gulati, R., Kattumuri, R., & Kumar, S. (2019). A non-parametric index of corporate governance in the banking industry: An application to Indian data. Socio-economic Planning Sciences, 70(June 2020), 100702, 1–13. https://doi.org/10.1016/j.seps.2019.03.008

- Gupta, P., & Sharma, A. M. (2014). A study of the impact of corporate governance practices on firm performance in Indian and South Korean companies. Procedia - Social and Behavioral Sciences, 133(2014), 4–11. https://doi.org/10.1016/j.sbspro.2014.04.163

- Gupta, P. K., & Shallu, S. (2014). Evolving legal framework of corporate governance in India – Issues and challenges. Juridical Tribune/Tribuna Juridica, 4(2), 240–253. http://www.tribunajuridica.eu/arhiva/An4v2/20%20Gupta.pdf

- Gupta, P. K., & Singh, S. (2018). Corporate governance structures in transition economies–issues and concerns for India. Acta Universitatis Agriculturae et Silviculturae Mendelianae Brunensis, 66(6), 1459–1467. https://doi.org/10.11118/actaun201866061459

- Haldar, A., & Raithatha, M. (2017). Do compositions of board and audit committee improve financial disclosures? International Journal of Organizational Analysis, 25(2), 1–31. https://doi.org/10.1108/IJOA-05-2016-1030

- Haldar, A., Rao, S. N., & Momaya, K. S. (2016). Can flexibility in corporate governance enhance international competitiveness? Evidence from knowledge-based industries in India. Global Journal of Flexible Systems Management, 17(4), 389–402. https://doi.org/10.1007/s40171-016-0135-3

- Haldar, A., Shah, R., Rao, N., Stokes, P., Demirbas, D., & Dardour, A. (2018). Corporate performance: Does board independence matter? - Indian evidence. International Journal of Organizational Analysis, 26(1), 185–200. https://doi.org/10.1108/IJOA-12-2017-1296

- Hedges, A. (1985). Group interviewing. In R. Walker (Ed.), Applied qualitative research (pp. 71–91). Gower.

- Heinberg, M., Ozkaya, H. E., & Taube, M. (2018). Do corporate image and reputation drive brand equity in India and China? - Similarities and differences. Journal of Business Research, 86(September 2016), 259–268. https://doi.org/http://dx.doi.10.1016/j.jbusres.2017.09.018

- Helmers, C., Patnam, M., & Rau, P. R. (2017). Do board interlocks increase innovation? Evidence from a corporate governance reform in India. Journal of Banking and Finance, 80(July2017), 51–70. https://doi.org/10.1016/j.jbankfin.2017.04.001

- Hundal, S. (2016). Busyness of audit committee directors and quality of financial information in India. International Journal of Business Governance and Ethics, 11(4), 335–363. https://doi.org/10.1504/IJBGE.2016.082606

- Iqbal, S., Nawaz, A., & Ehsan, S. (2019). Financial performance and corporate governance in micro fi nance : Evidence from Asia $. Journal of Asian Economics, 60(February 2019), 1–13. https://doi.org/10.1016/j.asieco.2018.10.002

- Islam, A. U. (2016). Corporate governance performance of publicly listed companies in India : A cross-sectional industry analysis of BSE 200. International Journal of Corporate Governance, 7(4), 306–324. https://doi.org/10.1504/IJCG.2016.082348

- Jackling, B., & Johl, S. (2009). Board structure and firm performance: Evidence from India ’ s Top companies. Corporate Governance: An International Review, 17(4), 492–509. https://doi.org/10.1111/j.1467-8683.2009.00760.x

- Jacoby, G., Liu, M., Wang, Y., Wu, Z., & Zhang, Y. (2019). Corporate governance, external control, and environmental information transparency: Evidence from emerging markets. Journal of International Financial Markets, Institutions & Money, 58(2019), 269–283. https://doi.org/10.1016/j.intfin.2018.11.015

- Jaiswall, M., & Firth, M. (2009). CEO pay, firm performance, and corporate governance in India’s listed firms. International Journal of Corporate Governance, 1(3), 227–240. https://doi.org/10.1504/IJCG.2009.029367

- Jaiswall, S. S. K., & Bhattacharyya, A. K. (2016). Corporate governance and CEO compensation in Indian firms. Journal of Contemporary Accounting & Economics, 12(2), 159–175. https://doi.org/10.1016/j.jcae.2016.06.001

- Jameson, M., Prevost, A., & Puthenpurackal, J. (2014). Controlling shareholders, board structure, and fi rm performance : Evidence from India ☆. Journal of Corporate Finance, 27(2014), 1–20. https://doi.org/10.1016/j.jcorpfin.2014.04.003

- Kagzi, M., & Guha, M. (2018). Does board demographic diversity influence firm performance? Evidence from Indian Knowledge-Intensive Firms. Benchmarking: An International Journal, 25(3), 1028–1058. https://doi.org/10.1108/BIJ-07-2017-0203

- Kamath, B. (2019). Impact of corporate governance characteristics on intellectual capital performance of firms in India. International Journal of Disclosure and Governance, 16(1), 20–36. https://doi.org/10.1057/s41310-019-00054-0

- Kandukuri, R. L., Memdani, L., & Babu, P. R. (2015). Effect of corporate governance on firm performance? A study of selected Indian listed companies. In Kensinger, J. W. (Ed.), Overlaps of private sector with public sector around the globe (Research in Finance, Vol. 31) (pp. 47–64). Emerald Group Publishing Limited. https://doi.org/10.1108/S0196-382120150000031010

- Kang, L. S., & Nanda, P. (2015). What determines the disclosure of managerial remuneration in India? Journal of Financial Reporting and Accounting, 16(1), 2–23. https://doi.org/10.1108/JFRA-04-2015-0050

- Kang, L. S., & Nanda, P. (2017). Journal of accounting in emerging economies how is managerial remuneration determined in India? Journal of Accounting in Emerging Economies, 7(2), 154–172. https://doi.org/10.1108/JAEE-03-2015-0017

- Kansil, R., & Singh, A. (2018). Sustainability enhancement of corporate governance regime in India. World Journal of Science, Technology and Sustainable Development, 15(2), 186–199. https://doi.org/10.1108/WJSTSD-08-2017-0026

- Kapoor, N., & Goel, S. (2019). Do diligent independent directors restrain earnings management practices? Indian lessons for the global world. Asian Journal of Accounting Research, 4(1), 52–69. https://doi.org/10.1108/AJAR-10-2018-0039

- Katarachia, A., Pitoska, E., Giannarakis, G., & Poutoglidou, E. (2018). The drivers of corporate governance disclosure: The case of Nifty 500 Index. International Journal of Law and Management, 60(2), 681–700. https://doi.org/10.1108/IJLMA-02-2017-0020

- Kaur, A., & Singh, B. (2018). Corporate reputation: Do board characteristics matter? Indian evidence. Indian Journal of Corporate Governance, 11(2), 122–134. https://doi.org/10.1177/0974686218797758

- Kaur, G. (2017). The influence of board characteristics on corporate illegality. Journal of Financial Regulation and Compliance, 25(2), 133–148. https://doi.org/10.1108/JFRC-05-2016-0045

- Kavitha, D., & Nandagopal, R. (2013). Changing perspectives of corporate governance in India. International Journal of Indian Culture and Business Management, 7(1), 72–89. https://doi.org/10.1504/IJICBM.2013.054818

- Kavitha, D., Nandagopal, R., & Maheswari, B. U. (2018). Impact of the busyness and board independence on the discretionary disclosures of Indian firms. International Journal of Law and Management, 61(1), 250–265. https://doi.org/10.1108/IJLMA-04-2018-0062

- Kayalvizhi, P. N., & Thenmozhi, M. (2018). Does quality of innovation, culture and governance drive FDI? : Evidence from emerging markets. Emerging Markets Review, 34(March2018), 175–191. https://doi.org/10.1016/j.ememar.2017.11.007

- Khanna, T., & Palepu, K. G. (2004). Globalization and convergence in corporate governance: Evidence from Infosys and the Indian software industry. Journal of International Business Studies, 35(6), 484–507. https://doi.org/10.1057/palgrave.jibs.8400103

- Khosa, A. (2017). Independent directors and firm value of group-affiliated firms. International Journal of Accounting & Information Management, 25(2), 217–236. https://doi.org/10.1108/IJAIM-08-2016-0076

- Kimber, D., Lipton, P., & O’Neill, G. (2005). Corporate governance in the Asia Pacific region: A selective review of developments in Australia, China, India and Singapore. Asia Pacific Journal of Human Resources, 43(2), 180–197. https://doi.org/10.1177/1038411105055057

- Kiranmai, J., & Mishra, R. K. (2019). Corporate governance practices in listed enterprises in India : An empirical research. Indian Journal of Corporate Governance, 12(1), 91–121. https://doi.org/10.1177/0974686219849760

- Klapper, L. F., & Love, I. (2004). Corporate governance, investor protection, and performance in emerging markets. Journal of Corporate Finance, 10(5), 703–728. https://doi.org/10.1016/S0929-1199(03)00046-4

- Kohli, N., & Saha, G. C. (2008). Corporate governance and valuations : Evidence from selected Indian companies. International Journal of Disclosure and Governance, 5(3), 236–251. https://doi.org/10.1057/jdg.2008.10

- Koirala, S., Marshall, A., & Neupane, S. (2018). Corporate governance reform and risk-taking: Evidence from a quasi-natural experiment in an emerging market. Journal of Corporate Finance, 1–75. https://doi.org/10.1016/j.jcorpfin.2018.08.007

- Kota, H. B., & Tomar, S. (2010). Corporate governance practices in Indian firms. Journal of Management & Organization, 16(2), 266–279. https://doi.org/10.1017/S1833367200002170

- Kumar, N., & Singh, J. P. (2013). Effect of board size and promoter ownership on firm value: Some empirical findings from India. Corporate Governance: The International Journal of Business in Society, 13(1), 88–98. https://doi.org/10.1108/14720701311302431

- Kumari, P., & Pattanayak, J. K. (2017). Linking earnings management practices and corporate governance systems with a firms ’ financial performance : A study of Indian Commercial Banks. Journal of Financial Crime, 4(2), 223–241. https://doi.org/10.1108/JFC-03-2016-0020

- Kutubi, S. S., Ahmed, K., & Khan, H. (2018). Bank performance and risk-taking—Does directors’ busyness matter? Pacific-Basin Finance Journal, 50(September2018), 184–199. https://doi.org/10.1016/j.pacfin.2017.02.002

- Lagasio, V., & Cucari, N. (2019). Corporate governance and environmental social governance disclosure: A meta‐analytical review. Corporate Social Responsibility and Environmental Management, 26(4), 701–711. https://doi.org/10.1002/csr.1716

- Lakhani, A. (2012). Cross-cultural implications on the legal requirements for corporate governance in China and India. International Journal of Private Law, 5(2), 136–156. https://doi.org/10.1504/IJPL.2012.046058

- Lakshman, C., & Akhter, M. (2013). Corporate governance scandals in the Indian Premier League (IPL): Implications for labour. Labour & Industry: A Journal of the Social and Economic Relations of Work, 23(1), 89–106. https://doi.org/10.1080/10301763.2013.769859

- Li, H., Terjesen, S., & Umans, T. (2018). Corporate governance in entrepreneurial firms: A systematic review and research agenda. Small Business Economics, 54, 43–74. https://doi.org/10.1007/s11187-018-0118-1

- Lin, J. W., & Hwang, M. I. (2010). Audit quality, corporate governance, and earnings management: A meta‐analysis. International Journal of Auditing, 14(1), 57–77. https://doi.org/10.1111/j.1099-1123.2009.00403.x

- Machold, S., & Vasudevan, A. K. (2004). Corporate governance models in emerging markets : The case of India. International Journal of Business Governance and Ethics, 1(1), 56–77. https://doi.org/10.1504/IJBGE.2004.004897

- Marques, T. A., De Sousa Ribeiro, K. C., & Barboza, F. (2018). Corporate governance and debt securities issued in Brazil and India: A multi-case study. Research in International Business and Finance, 45(October2018), 257–270. https://doi.org/10.1016/j.ribaf.2017.07.156

- Masud, A. K., Nurunnabi, M., & Bae, S. M. (2018). The effects of corporate governance on environmental sustainability reporting : Empirical evidence from South Asian countries. Asian Journal of Sustainability and Social Responsibility, 3(3), 1–26. https://doi.org/10.1186/s41180-018-0019-x

- Mayur, M., & Saravanan, P. (2017). Performance implications of board size, composition and activity: Empirical evidence from the Indian Banking Sector. Corporate Governance: The International Journal of Business in Society, 17(3), 466–489. https://doi.org/http://dx.doi.10.1108/CG-03-2016-0058

- Mishra, M. (2016). Audit committee characteristics and earnings management: Evidence from India. International Journal of Accounting and Financial Reporting, 6(2), 247–273. https://doi.org/10.5296/ijafr.v6i2.10008

- Mishra, R. K., & Kapil, S. (2017). Effect of board characteristics on firm value: Evidence from India. South Asian Journal of Business Studies, 7(1), 41–72. https://doi.org/10.1108/SAJBS-08-2016-0073

- Mishra, R. K., & Kapil, S. (2018). Board characteristics and fi rm value for Indian companies. Journal of Indian Business Research, 10(1), 2–32. https://doi.org/10.1108/JIBR-07-2016-0074

- Mishra, S., & Mohanty, P. (2014). Corporate governance as a value driver for firm performance : Evidence from India. Corporate Governance, 14(2), 256–280. https://doi.org/10.1108/CG-12-2012-0089

- Mishra, S., & Mohanty, P. (2018). Does good governance lead to better financial performance? International Journal of Corporate Governance, 9(4), 462–480. https://doi.org/10.1504/IJCG.2018.096276

- Mitton, T. (2004). Corporate governance and dividend policy in emerging markets. Emerging Markets Review, 5(2004), 409–426. https://doi.org/10.1016/j.ememar.2004.05.003

- Mohapatra, P. (2016). Board independence and firm performance in India. International Journal of Management Practice, 9(3), 317–332.

- Morey, M., Gottesman, A., Baker, E., & Godridge, B. (2009). Does better corporate governance result in higher valuations in emerging markets? Another examination using a new data set. Journal of Banking and Finance, 33(2), 254–262. https://doi.org/10.1016/j.jbankfin.2008.07.017

- Muniapan, B., & Shaikh, J. M. (2007). Lessons in corporate governance from Kautilya’s Arthashastra in ancient India. World Review of Entrepreneurship, Management and Sust. Development, 3(1), 50–61. https://doi.org/10.1504/WREMSD.2007.012130

- Mutlu, C. C., Essen, M., Van Peng, M. W., Saleh, S. F., & Duran, P. (2018). Corporate governance in China : A meta-analysis. Journal of Management Studies, 55(6), 943–979. https://doi.org/10.1111/joms.12331

- Muttakin, M. B., & Subramaniam, N. (2015). Firm ownership and board characteristics : Do they matter for corporate social responsibility disclosure of Indian companies? Sustainability Accounting, Management and Policy Journal, 6(2), 138–165. https://doi.org/10.1108/SAMPJ-10-2013-0042

- Nagar, N., & Raithatha, M. (2016). Does good corporate governance constrain cash flow manipulation? Evidence from India Evidence from India. Managerial Finance, 42(11), 1034–1053. https://doi.org/10.1108/MF-01–2016-0028

- Narayanaswamy, R., Raghunandan, K., & Rama, D. V. (2015). Satyam failure and changes in Indian audit committees. Journal of Accounting, Auditing & Finance, 30(4), 529–540. https://doi.org/10.1177/0148558X15584124

- Narwal, K. P., & Pathneja, S. (2016). Effect of Bank-specific and Governance- specific variables on the productivity and profitability of banks. International Journal of Productivity and Performance Management, 65(8), 1057–1074. https://doi.org/http://dx.doi.10.1108/IJPPM-09-2015-0130

- Nomran, N. M., & Haron, R. (2020). A systematic literature review on Sharı’ah governance mechanism and firm performance in Islamic banking. Islamic Economic Studies, 27(2), 91–123. https://doi.org/10.1108/IES-06-2019-0013

- Oehmichen, J. (2018). East meets west — Corporate governance in Asian emerging markets: A literature review and research agenda. International Business Review, 27(2), 465–480. https://doi.org/10.1016/j.ibusrev.2017.09.013

- Oliveira, M. C., Ceglia, D., & Filho, F. A. (2016). Analysis of corporate governance disclosure: A study through BRICS countries. The International Journal of Business in Society, 16(5), 923–940. https://doi.org/10.1108/CG-12-2015-0159

- Palaniappan, G. (2017). Determinants of corporate financial performance relating to board characteristics of corporate governance in Indian manufacturing industry: An empirical study. European Journal of Management and Business Economics, 26(1), 67–85. https://doi.org/10.1108/EJMBE-07-2017-005

- Patibandla, M. (2006). Equity pattern, corporate governance and performance: A study of India’s corporate sector. Journal of Economic Behavior & Organization, 59(1), 29–44. https://doi.org/10.1016/j.jebo.2004.04.004

- Patra, K. K. (2013). Opportunities and challenges of corporate governance reforms in India: A study on Infosys Technologies. International Journal of Indian Culture and Business Management, 7(3), 430–440. https://doi.org/10.1504/IJICBM.2013.056218

- Petticrew, M., & Roberts, H. (2006). Why do we need systematic reviews. In Petticrew, M., Roberts, H., (Eds.), Systematic reviews in the social sciences: A practical guide (pp. 1–26). Blackwell Oxford.

- Prasad, K., & Sankaran, K. (2017). Relationship between gray directors and executive compensation in Indian firms. European Journal of Management and Business Economics, 28(3), 239–265. https://doi.org/http://dx.doi.10.1108/EJMBE-11-2017-0038

- Prasad, P., Sivasankaran, N., Saravanan, P., & Kannadhasan, M. (2019). Does corporate governance influence the working capital management of firms: Evidence from India. International Journal of Corporate Governance, 10(1), 42–80. https://doi.org/10.1504/IJCG.2019.098039

- Prasanna, P. K. (2013). Impact of corporate governance regulations on Indian stock market volatility and efficiency. International Journal of Disclosure and Governance, 10(1), 1–12. https://doi.org/10.1057/jdg.2011.28

- Prasanna, P. K. (2014). Firm-level governance quality and dividend decisions: Evidence from India. International Journal of Corporate Governance, 5(3/4), 197–222. https://doi.org/10.1504/IJCG.2014.064726

- Prasanna, P. K., & Menon, A. S. (2012). Corporate governance and stock market liquidity in India. International Journal of Behavioural Accounting and Finance, 3(1/2), 24–45. https://doi.org/10.1504/IJBAF.2012.047358

- Puri, V., & Kumar, M. (2018). Factors influencing adoption and disclosure of voluntary corporate governance practices by the Indian listed firms. International Journal of Corporate Governance, 9(1), 91–126. https://doi.org/10.1504/IJCG.2018.090621

- Qurashi, M. H. (2018). Corporate governance code comparison for South Asian emerging economies Mubashir. International Journal of Law and Management, 60(2), 250–266. https://doi.org/10.1108/IJLMA-05-2017-0115

- Rajablu, M. (2016). Corporate governance: A conscious approach for Asia and emerging economies. International Journal of Law and Management, 58(3), 317–336. https://doi.org/10.1108/IJLMA-04-2015-0017

- Rajagopalan, N., & Zhang, Y. (2008). Corporate governance reforms in China and India: Challenges and opportunities. Business Horizons, 51(1), 55–64. https://doi.org/10.1016/j.bushor.2007.09.005

- Rani, N., Yadav, S. S., & Jain, P. K. (2014). Impact of corporate governance score on abnormal returns and financial performance of mergers and acquisitions. Decision, 41(December), 371–398. https://doi.org/10.1007/s40622-014-0067-8

- Ravi, S. P. (2012). Strategic change management: Corporate governance failures in India and USA – A tale of two countries. International Journal of Strategic Change Management, 4(3/4), 281–304. https://doi.org/10.1504/IJSCM.2012.051850

- Reed, A. M. (2002). Corporate governance reforms in India. Journal of Business Ethics, 37(3), 249–268. https://doi.org/10.1023/A:1015260208546

- Road, S. (2016). Board independence and firm performance in India Pranati Mohapatra. International Journal of Management Practice, 9(3), 317–332. https://doi.org/10.1504/IJMP.2016.077834

- Roy, A. (2018). Corporate Governance and Cash Holdings: An Empirical Investigation. Advances in Finance & Applied Economics, 255–280. https://doi.org/10.1007/978-981-13-1696-8

- Saggar, R., & Singh, B. (2017). Corporate governance and risk reporting : Indian evidence. Managerial Auditing Journal, 32(4/5), 378–405. https://doi.org/http://dx.doi.10.1108/MAJ-03-2016-1341

- Sanan, N. K. (2016). Board gender diversity and firm performance: Evidence from India. Asian Journal of Business Ethics, 5(1–2), 1–18. https://doi.org/10.1007/s13520-016-0050-x

- Saravanan, P., Sivasankaran, N., Srikanth, M., & Shaw, T. (2017). Enhancing shareholder value through efficient working capital management: An empirical evidence from India. Finance India, 31(3), 851–871. https://www.financeindia.org/data/2017/FI313/FI-313-Art05.pdf

- Saravanan, P., Srikanth, M., & Avabruth, S. M. (2016a). Compensation of top brass, corporate governance and performance of the Indian family firms – An empirical study. Social Responsibility Journal, 13(3), 529–551. https://doi.org/10.1108/SRJ-03-2016-0048

- Saravanan, P., Srikanth, M., & Avabruth, S. M. (2016b). Executive compensation, corporate governance and firm performance : Evidence from India. International Journal of Corporate Governance, 7(4), 377–403. https://doi.org/10.1504/IJCG.2016.082351

- Sarkar, J., & Sarkar, S. (2000). Large shareholder activism in corporate governance in developing countries: Evidence from India. International Review of Finance, 1(3), 161–194. https://doi.org/10.1111/1468-2443.00010

- Sarkar, J., & Sarkar, S. (2009). Multiple board appointments and firm performance in emerging economies : Evidence from India. Pacific-Basin Finance Journal, 17(2), 271–293. https://doi.org/10.1016/j.pacfin.2008.02.002

- Sarkar, J., Sarkar, S., & Marg, A. K. V. (2012). A corporate governance index for large listed companies in India. Pace University Accounting Research Paper No. 2012/08. https://ssrn.com/abstract=2055091

- Sayari, N., & Marcum, B. (2018). Does enhancing corporate governance work? Cuadernos de Economía y Dirección de La Empresa, 21(2), 124–139. https://doi.org/10.1016/j.brq.2018.01.002

- Sayed, S. A., & Chawla, D. (2017). The impact of country-level corporate governance on analyst boldness and performance with target price forecasts. International Journal of Indian Culture and Business Management, 14(2), 237–255. https://doi.org/10.1504/IJICBM.2017.081976

- Schiehll, E., & Martins, H. C. (2016). Cross-National governance research: A systematic review and assessment. Corporate Governance: An International Review, 24(3), 181–199. https://doi.org/10.1111/corg.12158

- Sehgal, A., & Mulraj, J. (2008). Corporate governance in India: Moving gradually from a regulatory model to a market-driven model — A survey. International Journal of Disclosure and Governance, 5(3), 205–235. https://doi.org/10.1057/jdg.2008.9

- Shahid, M. (2019). Does corporate governance play any role in investor confidence, corporate investment decisions relationship? Evidence from Pakistan and India. Journal of Economics and Business, 105(September–October 2019), 1–11. https://doi.org/10.1016/j.jeconbus.2019.03.003

- Shaw, T. S., Cordeiro, J. J., & Saravanan, P. (2016). Director network resources and firm performance: Evidence from Indian corporate governance reforms. Asian Business & Management, 15(3), 165–200. https://doi.org/10.1057/s41291-016-0003-1

- Shikha, N. (2017). Corporate governance in India - the paradigm shift. International Journal of Corporate Governance, 8(2), 81–105. https://doi.org/10.1504/IJCG.2017.087359

- Shikha, N., & Mishra, R. (2019). Corporate governance in India – Battle of stakes. International Journal of Corporate Governance, 10(1), 20–41. https://doi.org/10.1504/IJCG.2019.098041

- Sidhu, M. K., & Kaur, P. (2019). Effect of corporate governance on stock market liquidity: Empirical evidence from Indian companies. DECISION, 46(3), 197–218. https://doi.org/10.1007/s40622-019-00221-w

- Singareddy, R. R., Chandrasekaran, S., Annamalai, B., & Ranjan, P. (2018). Corporate governance data of 6 Asian economies (2010–2017). Data in Brief, 20(October 2018), 53–56. https://doi.org/10.1016/j.dib.2018.07.048

- Singh, A., & Kansil, R. (2017). Impact of foreign shareholdings on corporate governance score : Evidence from Bombay Stock Exchange, India. International Journal of Business and Globalisation, 19(1), 93–110. https://doi.org/10.1504/IJBG.2017.085116

- Singh, J. P., Kumar, N., & Uzma, S. H. (2011). The changing landscape of corporate governance framework in India. International Journal of Indian Culture and Business Management, 4(5), 506–522. https://doi.org/10.1504/IJICBM.2011.042322

- Singla, M., & Singh, S. (2018). Impact of institutional set-up on the responsiveness to change in a firm’s governance structure: A comparative study of public and private sector enterprises in India. Global Journal of Flexible Systems Management, 19(2), 159–172. https://doi.org/10.1007/s40171-018-0185-9

- Singla, M., & Singh, S. (2019). Board monitoring, product market competition and firm performance. International Journal of Organizational Analysis, 27(4), 1036–1052. https://doi.org/10.1108/IJOA-07-2018-1482

- Snyder, H. (2019). Literature review as a research methodology : An overview and guidelines. Journal of Business Research, 104(July), 333–339. https://doi.org/10.1016/j.jbusres.2019.07.039

- Srivastava, V., Das, N., & Pattanayak, J. K. (2016). Corporate governance: Mapping the change. International Journal of Law and Management, 60(1), 19–33. https://doi.org/10.1108/IJLMA-11–2016-0100

- Srivastava, V., Das, N., & Pattanayak, J. K. (2018). Women on boards in India : A need or tokenism? Management Decision, 56(8), 1769–1786. https://doi.org/10.1108/MD-07-2017-0690

- Srivastava, V., Das, N., & Pattanayak, J. K. (2019). Impact of corporate governance attributes on cost of equity Evidence from an emerging economy. Managerial Auditing Journal, 34(2), 142–161. https://doi.org/10.1108/MAJ-01-2018-1770