Abstract

Physical distancing policy that is encouraged by the World Health Organization (WHO) has inspired consumers to do contactless activities, including payment transaction. Government authorities in a growing number of countries are taking actions to encourage contactless payments as the COVID-19 pandemic escalates. People are worried that novel coronavirus (SARS-Cov2) can be transmitted through physical money. It drives them to shift to e-wallet. Due to a lack of study on this topic, the present study contributes to the literature by examining the effect of perceived risk, government support, and perceived usefulness on customers’ intention to use e-wallet during COVID-19 outbreak. To give more fruitful insight, another major contribution of this study is investigating the group difference between Indonesia and Malaysia in the overall model. Questionnaires are distributed to the respondents by using a proportional sampling technique. As a result, 259 total respondents from Indonesia and 207 from Malaysia are collected. Both countries are selected because Indonesia and Malaysia can be considered as the two-worst countries in ASEAN affected by COVID-19. The model is tested using PLS-Structural Equation Modeling (SEM) approach. The results show that the effects of government support on the intention to use e-wallets differ between countries. Besides, perceived usefulness fully mediated government support-intention to use e-wallets relationship, and partially mediated the effect of perceived risk on intention to use e-wallets.

PUBLIC INTEREST STATEMENT

This study raises special attention to the issue of COVID-19 pandemic and its relation with payment behavior. Physical distancing policy in many countries has also affected the way the consumer makes a payment. Some people fear the risk of using physical money since it can carry the droplets containing the COVID-19 virus. The current study provides some insights on some factors that might influence consumers to use e-wallet during the pandemic, such as COVID-19 risk perception, government support, and perceived usefulness. In addition, this study provides the comparative results between Indonesia and Malaysia.

1. Introduction

Recent papers show that physical distancing policy due to Corona Virus Disease 2019 (COVID-19) has significantly affected socio-economics (Fernandes, Citation2020; Nicola et al., Citation2020), finance (Goodell, Citation2020), and supply-chain (Ivanov, Citation2020; Turner & Akinremi, Citation2020). Previous research has also already shown the pandemic effect on business in general (Swift, Citation2009). However, studies examining the COVID-19 pandemic effect on the way consumers make a payment remain scarce. As known, novel coronavirus or SARS-Cov2 can be easily transmitted if the droplets land on inanimate objects nearby an infected individual and are subsequently touched by other individuals (Ather et al., Citation2020). Physical money can be the medium for the virus when it is touched by an infected person. Therefore, the WHO suggested using digital money when possible (Brown, Citation2020).

Before this outbreak, cashless payment through smartphones already gained popularity (Andrieu, Citation2001) in several developing countries (Capgemini, Citation2019) such as Thailand, Vietnam, and Indonesia PWC (Citation2019). Based on the Global Consumer Insight Survey 2019, there is a 67% customer or 19% growth in Thailand who already engaged in a mobile payment transaction, after Vietnam and Middle East countries by 24% and 20% growth, respectively. One form of mobile payment alternative is e-wallets payment. E-wallet is a type of e-money (Aji et al., Citation2020) where the money is stored in a server, not in a chip card. In Indonesia, there are several of server-based e-money (e-wallet) providers such as Go-Pay, OVO, LinkAja, DANA. On the other hand, BoostPay, Touch N’ Go Wallet, and Grab Pay are more popular in Malaysia. However, if compared to Indonesia, e-wallet adoption in Malaysia is still in its infancy (PWC, Citation2018).

Previous research on the usage of e-wallets in specific and mobile payment, in general, resulted in various findings. Aji et al. (Citation2020) found that consumers’ intention to use e-wallet is strongly affected by knowledge about riba (interest or usury) in a Muslim case. Mobile payment transaction also holds risk and uncertain possibility (Bagla & Sancheti, Citation2018; Leong et al., Citation2020) as it might be associated with certain criminal activities including theft, account take over, fraudulent transactions, and data breaches (Marria, Citation2018). Similarly, in banking and online payment through an application, consumers also perceived certain possible risks that might hold them to act (Lu et al., Citation2005; Marafon et al., Citation2018).

Earlier studies showed that there are numerous types of risks related with internet or online transaction including product performance risks, financial risks, time/convenience risks, and psychological risks (Forsythe & Shi, Citation2003). In general, mostly all studies found that the effect of perceived risk on behavior is negative (Marafon et al., Citation2018). However, the finding would probably be different if the risk is associated with the deadly pandemic outbreak, such as COVID-19. As mentioned, there is a high-risk possibility of SARS-Cov2 transmission in physical money. Perceived risk associated with virus transmission will be positively affected customers’ intention to use non-physical money. Unfortunately, empirical findings on this matter remain understudied.

Government support on e-wallets innovation during this deadly outbreak might also influence intention to use e-wallets. Following WHO’s advice (Brown, Citation2020; Huang, Citation2020), the government should encourage its people to engage in e-wallets payment. It is helpful to “flatten the curve” (Kaur, Citation2020). Interestingly, Indonesia and Malaysia government responded almost similarly in which the Malaysian government regulates the Movement Control Order (MCO) (MHTC, Citation2020), and the Indonesian government decided to implement the Large-Scale Social Restriction (PSBB) policy. Both imply a partial lockdown policy. However, MCO and PSBB do not explicitly encourage people to make a cashless payment transaction. Independent movement is also possible to exist. Especially in Indonesia, there is a call for using the digital payment to prevent COVID-19 transmission, echoed by the Bank of Indonesia governor (Bank Indonesia, Citation2020; IDN Financials, Citation2020). In Malaysia, on the other hand, the government has supported the use of e-wallet by introducing several initiatives, including ePENJANA e-wallet stimulus, Shop Malaysia Online initiative, and the Micro, Small and Medium Enterprises (MSME) e-commerce Campaign (The Star, Citation2020). Falls under the “Short-term National Economic Recovery Plan,” these initiatives also plays an important role to contribute towards the nation’s digital economy aspirations and develop its ecosystem. Nevertheless, consumers in both countries might build different perceptions toward the importance of e-wallet during COVID-19 pandemic. To illustrate, despite cashless payment transaction is encouraged by both countries, there is a possibily that the citizen still prefer traditional means of payment.

In several empirical findings, government support has a significant effect on firm performance (Appiah et al., Citation2019), and also concerning its innovation (Wei & Liu, Citation2015). On an individual level, government support was found to significantly affect customers’ intention to adopt mobile payment in the context of internet banking (Rambocas & Arjoon, Citation2012; Tan & Teo, Citation1998), Islamic banking and finance (Ali et al., Citation2015; Reni & Ahmad, Citation2016), mobile commerce, and government service (Dawi, Citation2019; Mandari et al., Citation2017). Since COVID-19 can be considered as a national or even global threat, this study proposes that government support on e-wallets facilities and innovation would drive customers’ adoption and usage of e-wallet.

Due to a lack of study on this topic, the present study contributes to the literature by examining the effect of perceived risk, government support and perceived usefulness on customers intention to use e-wallet during COVID-19 outbreak. To give more fruitful insight, another major contribution of this study is investigating the group difference between Indonesia and Malaysia in the overal model.

2. Review of literature and hypotheses development

2.1. COVID-19 Impact on Business and Consumer Behavior

SARS-Cov2 has a deadly effect not only on humans but also on business (Turner and Akinremi, Citation2020; Ivanov, Citation2020), economics and finance (Goodell, Citation2020) activities within primary, secondary and tertiary sectors (Nicola, Alsafi, Sohrabi, et al., Citation2020). The world is anticipating a big global loss due to epidemic and pandemic situations (Fan, Jamison, and Summers, Citation2018). The novel coronavirus also changes consumer behavior in Asia, including Indonesian and Malaysian consumers (Nielsen, Citation2020). We also have seen in newspapers and television that consumers all over the globe committed in panic buying activities. Some of them are taking advantage of the situation to hoard the supply, the other consumers purchase all the supplies just because they do not want hoarders to take advantage. It is connected with Global Web Index&s (Citation2020) finding that there is a dramatic increase in consumer spending in many parts of the world. Based on that finding, 80% of consumers in the US and the UK consume more content at home since the outbreak.

Physical distancing and self-quarantine policy hold people at their homes. Consumers tried to do anything contactless. They avoid purchasing at groceries and malls. Online food deliveries and game demand are escalated in Indonesia (The Jakarta Post, Citation2020). In Malaysia, it was reported that some delivery companies had recorded more than a 30 percent increase in orders since a Movement Control Order (MCO) was enacted on 18 March(The ASEAN Post, Citation2020).Many retailers, transportation providers, and food merchants encourage consumers to make a payment by using digital wallets or e-wallets. In Indonesia, The central bank called more for digital payment transaction (Bank Indonesia, Citation2020; IDN Financials, Citation2020). Many people started to build a perceived risk that might be faced when using cash.

2.2. Perceived risk and government support

Perceived risk is defined as the perceived uncertainty in a purchase situation (Im et al., Citation2008). It is a sense of loss (Bauer, Citation1960), involving potentially positive or negative outcomes, but in consumer behavior literature, it is more focused on the negative outcomes (Stone & Gronhaug, Citation1993; Tanadi et al., Citation2015). According to the literature, perceived risk is a multi-dimensional construct. It has several dimensions that may vary according to the product (or service) class (Kassim & Ramayah, Citation2015). When associated with online transactions, perceived risk has several dimensions such as performance risks, financial risks, time/convenience risks, and psychological risks (Forsythe & Shi, Citation2003). Maser and Weiermair (Citation1998) also added another dimension which is disease risk, which is more relevant to this study context.

In a psychometric theory, the riskiness of something is judged based on the combination of risk characteristics including dread, knowledge, and controllability, which is then categorized into cognitive and emotional risks (Oh et al., Citation2015). In this study, perceived risk is defined as the situation where the customers are uncertain of novel coronavirus droplets on the physical money or cash. Therefore, following Oh et al. (Citation2015) and Maser and Weiermair (Citation1998), the risk dimension associated with this study is more connected to cognitive and disease risk, where customers are worried about getting infected by SARS-Cov2 through exchange of physical money.

Perceived risk and government support are correlated to some extent. In the theory of public policy and risk management, the government has a vital role. When risk is faced, the government can act as the manager (Baker & Moss, Citation2009). The government as the regulator has a primary obligation to prevent any potential negative outcomes addressed at its people. According to Sheikh et al. (Citation2020), government, as represented by Ministry of Health, has a “de jure” role which is responsible for people’s health. In this study, government support for e-wallets is influenced by potential COVID-19 risk associated with physical money. Therefore, the authors formulate that,

H1: Perceived risk positively affects government support for e-wallets

2.3. Perceived risk, government support, and perceived usefulness

Consumers are already familiar with cash; however, mobile payment as a new alternative can be adopted when consumers perceived certain advantages (Riquelme & Rios, Citation2010). In general, perceived trust and risk might be the key factors determining mobile payment adoption (Hampshire, Citation2017; Lu et al., Citation2005). Perceived risk has been added to TAM in several studies (Koenig-Lewis et al., Citation2010; Lee & Park, Citation2016), and it has a significant effect on perceived usefulness (Hampshire, Citation2017; Lee, Citation2009). For example, Lee and Park (Citation2016) applies the TAM to investigate the factors that affect the intention to use the mobile payment services. They found a significant role of perceived usefulness.

In general, perceived usefulness of technology can be affected by external factors such as government support (Haderi, Citation2014; Hai & Kazmi, Citation2015). In this study context, the government’s role in supporting e-wallets usage during COVID-19 outbreak can positively affect consumers’ perceived usefulness of e-wallets. Therefore, the authors hypothesize that,

H2: Perceived risk positively affects perceived usefulness of e-wallets

H3: Government support for e-wallets positively affects perceived usefulness of e-wallets

2.4. Perceived risk and intention to use e-wallet

According to Hasan et al. (Citation2017), disease risk is the possibility of individuals affected by epidemic diseases such as MARS, SARS, Anthrax, AIDS, etc. Therefore, the use of e-wallet is the best solution to prevent the risk of transmitting COVID-19. Most studies found that the effect of perceived risk on intention is negative (Marafon et al., Citation2018), such as in the context of tourism (Rittichainuwat & Chakraborty, Citation2009), internet banking (Kassim & Ramayah, Citation2015; Marafon et al., Citation2018), and online application (Lu et al., Citation2005). However, the results might be different for this study context. In this study, the higher the COVID-19 risk on physical cash perceived by the individuals, the stronger the intention to use e-wallets for the payment transaction. It is also important to consider that individual decisions in adopting an application system determined by the perceived usefulness (Davis et al., Citation1989; Venkatesh & Davis, Citation2000). In other words, perceived usefulness of e-wallets will encourage the consumer to utilize e-wallets as the anticipation for COVID-19. Therefore, the authors hypothesize that,

H4a: Perceived risk positively affects intention to use e-wallets

H4b: Perceived usefulness mediates the effect of perceived risk on intention to use e-wallets

2.5. Government support and intention to use e-wallet

Consumer acceptance of technological systems is not only influenced by perceived risk (internal factor) but also by government support (external factor) (Haderi, Citation2014; Hai & Kazmi, Citation2015). In the context of internet banking, government support has a prominent role in determining individual intentions to use Internet Banking (Rambocas & Arjoon, Citation2012; Tan & Teo, Citation1998). Similarly, in the context of Islamic banking and financing (Ali et al., Citation2015; Reni & Ahmad, Citation2016), mobile commerce and government services (Dawi, Citation2019; Mandari et al., Citation2017). In the context of e-wallets, government support can be translated into the network infrastructure, policy packages, speed of access, and security guarantees in digital transactions. As the anticipation to “flatten the curve”, the WHO urged the public to use cashless transactions to minimize physical interaction (Brown, Citation2020; Huang, Citation2020). The governments’ support for ensuring e-wallet payment transactions is helpful to combat SARS-Cov2 transmission. Thus, when consumers feel the support from the government, they will have a stronger intention to use e-wallet. Besides, perceived usefulness is also considered as a fundamental factor to use technology systems or applications (Budi et al., Citation2011). In essence, the effect of government support on intention to use e-wallet can be more explained by perceived usefulness. Therefore, the authors hypothesize that,

H5a: Government support positively affects intention to use e-wallets

H5b: Perceived usefulness mediates the effect of government support on intention to use e-wallets

2.6. Perceived usefulness and intention to use e-wallet

Perceived usefulness can be understood as the degree of confidence that emphasizes the extent to which consumers believe that using a particular system can improve his or her performance (Davis et al., Citation1989). Technically, e-wallet platform is a very effective method in various types of payment during physical distancing or self-quarantine periods. Moreover, e-wallets can be an alternative payment system to support the government reducing the spreading risk of COVID-19. Several earlier studies consistently found that perceived usefulness is a strong predictor of intention to use e-money (Aji & Dharmmesta, Citation2019), and in explaining why consumers accept a technology or application (Venkatesh & Bala, Citation2008;; Rauniar et al., Citation2014; Beldad & Hegner, Citation2017). Thus, the authors hypothesize that,

H6: Perceived usefulness positively affects intention to use e-wallets

2.7. Multigroup moderation: Indonesia and Malaysia

Indonesia and Malaysia are two countries which possess a lot of similarities due to similar historical roots and cultural heritage (Chong, Citation2012). Nevertheless, both also differ in political systems and values (Sani & Hara, Citation2007), demographic characteristics, and lifestyle (Andik et al., Citation2018). All together formed consumer culture that affects consumer perception, attitude, and behavior (Kotler & Keller, Citation2012). In terms of political system, Malaysia embraces more elite deliberation which practically limits freedom of speech and press (Sani & Hara, Citation2007). Therefore, high loyalty given by Malaysian people to the King and the government is customary (Victoria & Amir, Citation2018). On the contrary, Indonesia embraces more deliberative democracy which gives more freedom of speech and press to its people (Sani & Hara, Citation2007). As a result, critics against the government are normal. Besides, in terms of demographic characteristics, Indonesia has more than 50 ethnic groups in comparison with Malaysia which is consisted of three major ethnic groups. This makes Indonesian consumers are more heterogenous (Andik et al., Citation2018).

Consequently, those have a significant impact on overall consumer perception and behavior in both countries, especially during this COVID-19 outbreak. In an essence, government support and perceived risk do not directly affect Indonesia consumers to use e-wallet, as it is more deliberative in politics (Sani & Hara, Citation2007), and heterogenous in demographics (Andik et al., Citation2018). It is different from Malaysian consumer which are generally more loyal to the government and the King as aforementioned (Victoria & Amir, Citation2018). Therefore, the comparison of nationality between Malaysians and Indonesians is much needed. Taken together, these differences may moderate the effect of perceived risk, government support, and perceived usefulness on intention to use e-wallet during COVID-19 pandemic. Therefore, the authors hypothesize that,

H7a: The effect of perceived risk positively affects intention to use e-wallets differs across countries

H7b: The effects of government support positively affect intention to use e-wallets differs across countries

H7 c: The effects of perceived usefulness positively affect intention to use e-wallets differs across countries

3. Research methods

3.1. Data collection and sampling technique

A quantitative approach is used by distributing online questionnaires to sample respondents in Indonesia and Malaysia. Both countries are selected purposively based on the total COVID-19 active cases. E-wallets in this study are all server-based non-bank e-wallets. There are several server-based non-bank e-wallet providers in Indonesia, such as Go-Pay, OVO, DANA, LinkAja, etc. In Malaysia, most well-known e-wallet providers are BoostPay, Touch N’ Go Wallet, Grab Pay.

3.2. Items measurement

All items intended to measure the constructs in this study were adopted from the previously validated instruments. Section A contained questions pertaining to demographic details such as gender, age, occupation and race. On the other hand, Section B consisted of 5-point Likert scale measurement questions ranging from strongly disagree (1) to strongly agree (5) to measure the intention to use e-wallets. Perceived risk is operationally defined as the situation where the customers are uncertain of novel coronavirus droplets on the physical money or cash measured. It is measured by four items adapted from Olya and Al-Ansi (Citation2018). TAM’s model from Davis et al. (Citation1989) is adopted to measure perceived usefulness. It is operationally defined in this paper as the degree of confidence that emphasizes the extent to which consumers believe that using e-wallets as a mode of payment during COVID-19 can be more useful to prevent transmission. Intention to use e-wallet is defined as users’ intention to use e-money during COVID-19 pandemic, measured by three items adapted from Aji et al. (Citation2020). Lastly, government support is operationally defined as the perceived support from the government in relation with promoting and improving e-wallets use and infrastructure during COVID-19 pandemic. It is measured by four self-administered questionnaires. Detailed items measurement can be seen in Table , and the research model can be seen in Figure .

Table 1. Respondent characteristics

Table 2. Convergence validity and construct reliability results

Figure 1. Research model.

4. Results

4.1. Respondents demographics

A total of 466 respondents’ data were successfully collected from both Indonesia and Malaysia between March and April 2020. There are 259 respondents from Indonesia and 207 from Malaysia. As for Indonesian data, male respondents (159 or 61.4%) are more dominant as compared with the female (100 or 18.6%). Most respondents in Indonesia are born between 1996 and 2019 (163 or 62.9%), followed by those who are born between 1977 and 1995 (82 or 31.7%), and only 14 respondents (5.4%) who are born between 1965 and 1976. Perhaps, that is because most Indonesian respondents are dominated by students (140 or 54.1%), while the rest are non-students (119 or 45.9%). Different from Indonesia data, female respondents are more dominating (117 or 56.5%) in Malaysian data. Also, respondents born between 1977 and 1995 have more proportion (113 or 54.6). Malaysian respondents mostly are student (70 or 33.8%), non-state-owned company workers (67 or 32.4%), and civil servant (26 or 11.6%). More detailed respondent characteristics are shown in Table .

4.2. Measurement model test—validity and reliability

Structural Equation Modeling (SEM) approach is used to test the measurement and structural model. It is very effective since both direct and indirect effects can be verified (Cheung & Lee, Citation2008; Huh et al., Citation2009). The validity and reliability of the items are measured by Average Variance Extracted (AVE), square roots AVE, loading factors, and Composite Reliability (CR) scores. The AVE and factor loadings are used to measure covergent validity, whereas discriminant validity is measured by calculating the square roots AVE (Hair et al., Citation2014). Reliability is also an indicator for convergent validty (Hair et al., Citation2014). It is measured by computing the squared sum of factor loadings for each constructs and sum of the error variance terms for a construct. As shown in Table , all items have loadings greater than 0.70 with AVE score >0.50. These results indicated that the items are free from convergence validity issue. Also, CR score is >0.70, indicating that all the constructs are consistent or reliable (Hair et al., Citation2014; Nunnally, Citation1967).

Based on the information shown in Table , the square root AVE score for each construct in the diagonal section is greater than the correlation with the other constructs. This means that the discriminant validity is supported (Fornell & Larcker, Citation1981). Besides, the model’s goodness-of-fit is also examined to determine the fit between the data and the model. It is reported that the CMIN/DF = 2.581 (p-value < 0.01), CFI = 0.97, GFI = 0.94, NFI = 0.96, RMSEA = 0.06. Therefore, it can be concluded that the model is fit (Hair et al., Citation2014; Hooper et al., Citation2008).

Table 3. Means, standard deviation and discriminant validity results

4.3. Structural model test—hypotheses testing and multigroup analysis

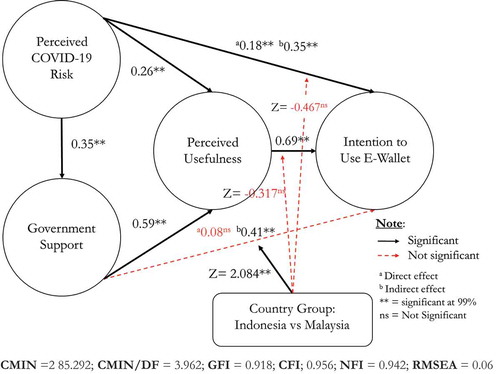

The results of the structural model in Tables and described that not all hypotheses are supported. The estimated effect of perceived risk on government support is supported since the β = 0.35, significant at p-value <0.01. This gives support on H1. The test also supported H2 (β = 0.26, p-value <0.01) and H3 (β = 0.59, p-value <0.01) stating the relationship between perceived risk and government support on perceived usefulness. The mediation hypotheses in H4a (β direct effect = 0.18, p-value < 0.01) and H4b (β indirect effect = 0.35, p-value < 0.01) are also supported. This implies a partial mediation between perceived risk-perceived usefulness-intention to use e-wallets. Moreover, H5a which states the effect of government support on intention to use e-wallets is not supported (β direct effect = 0.08, p-value > 0.05). Yet, H5b stating the mediating role of perceived usefulness on government support-intention to use e-wallets link is supported (β indirect effect = 0.41, p-value < 0.01). Therefore, it implies a full mediating role of perceived usefulness. In another word, the effect of government support on intention to use e-wallets can only be explained by the perceived usefulness of e-wallets, especially during COVID-19 pandemic. The effect of perceived usefulness on intention to use e-wallets also found significant (β = 0.69, p-value < 0.01). This gives support for H6.

Table 4. Direct and indirect testing results

Table 5. Multigroup testing results

The Multigroup Analysis (MGA) is assessed to determine whether the original structural model tests are different across countries (Indonesia and Malaysia). A parametric approach using a Z-test or Z-score is used to examine the difference between groups (Aji & Dharmmesta, Citation2019). The Z-test can be implemented when the data are large (Afthanorhan et al., Citation2015). As shown in Table , the difference between Indonesia and Malaysia only existed on government support and intention to use e-wallets link (Z-score = 2.084, p-value < 0.01). Thus, H7b is supported. The effects of perceived risk (Z-score = −0.467, p-value > 0.05) and perceived usefulness (Z-score = −0.317, p-value > 0.05) on intention to use e-wallets are not significantly different between Indonesia and Malaysia. Therefore, H7a and H7 c are not supported. Figure shows a complete model testing result.

Figure 2. Model testing results.

5. Discussion

Statistical tests show that the intention to use e-wallets is directly determined by perceived risks and perceived usefulness. The MGA test also revealed that the results do not differ between Indonesia and Malaysia. The results show that COVID-19 outbreak has made customers in both countries worried about getting infected by SARS-Cov2 that can be possibly transmitted through physical money. As mentioned, SARS-Cov2’s droplets might easily land on inanimate objects (Ather et al., Citation2020). Based on this possibility, therefore, the WHO advised and encouraged the use of digital payment when possible (Brown, Citation2020). The results supported and also gave an alternative to previous findings. Earlier studies confirmed that there is a negative relationship between perceived risk and intention (Kassim & Ramayah, Citation2015; Lu et al., Citation2005; Marafon et al., Citation2018; Rittichainuwat & Chakraborty, Citation2009). In this study context, perceived risk of COVID-19 significantly affects customers’ intention to use e-wallet. On the other hand, it means that COVID-19 risk perception has a negative connection with the intention to use physical money.

Interestingly, the effect of government support on intention to use e-wallets is not similar between Indonesia and Malaysia. It is only significant in Malaysia. This result shows that even though Indonesia and Malaysia are relatively similar in history and culture (Chong, Citation2012), but both are different when it comes to consumers’ characteristics and lifestyle (Andik et al., Citation2018), more specifically in a form of perception, attitude, and behavior (Kotler & Keller, Citation2012). People’s trust and loyalty to the government, as influenced by the political system in both countries, might explain the result. As argued, people in Malaysia strongly respect the King and the government (Victoria & Amir, Citation2018). Either directly or indirectly, it made Malaysian people perceive that the government is really on their side to support them. Especially during COVID-19, the perception of government support is needed to alienate the fear and worry felt by the people. However, in Indonesia, the government exists to support people which can be easily criticized since it embraces more deliberative democracy (Sani & Hara, Citation2007).

Responding to COVID-19 outbreak, the Malaysian government decided to regulate the MCO to all Malaysian territory. During the MCO, the government shows its presence by providing some assistance. In the official website of Prime Minister Office (PMO) of Malaysia (PMO, Citation2020), the government issued a program called “Economic Stimulus Package Concerning the People” or Pakej Rangsangan Ekonomi Prihatin Rakyat (PRIHATIN). The program has a serious tagline that is “Goal 1: Protect The People”. There are 29 packages in “PRIHATIN” program, and one of them is free internet access during the MCO. Surely, it affects Malaysian consumers’ perception toward government support and eventually influences the intention to use e-wallets.

In almost a similar form, the Indonesian government regulated the Large-Scale Social Restriction (PSBB). It restricts the people from having a crowd. However, the PSBB is regulated partially, only in particular cities where the COVID-19 cases are many. As a consequence, the government’s assistance is given only to the people in the area where PSBB is implemented. Yet, those assistances are not equally felt by those who lived in the PSBB area. As a consequence, many of them are refused to stay at home and insisted to work outside as usual (Negara, Citation2020). Perhaps, this is the reason why the effect of government support on the intention to use e-wallets is not significant.

Another interesting finding revealed that the insignificant effect of government support on the intention to use e-wallets is fully explained or mediated by perceived usefulness. This means the Indonesian consumers are willing to use e-wallets when government supports are felt in the form of usefulness. The support from the government without the perception of benefit does not trigger them to use e-wallets. Thus, this finding provides the input for Indonesian and any other governments to strengthen support for the people as well as focusing on measurable benefits, so that the people may directly feel it. It is useful for encouraging them to use digital payment, such as e-wallets, and hopefully stopping the transmission of SARS-Cov2 or novel coronavirus.

6. Limitations and future research directions

There are several limitations to this study. First, the sample between Indonesia and Malaysia in this study is not exactly proportional in numbers. It is also very difficult to pursue an exact proportion of gender, year of birth, and other demographical cohorts, especially if countries are taken into consideration. Second, since it is difficult to ensure proportion in demographical cohorts, therefore, the findings of the results are more subjective to more dominant respondent characteristics. Third, this study only captured the intention to use e-wallets during COVID-19 pandemic. The insight could be better in the longitudinal study comparing before and after the pandemic. In addition, future studies are suggested to consider income and education background as moderating variables. It is believed that consumers from this group are more open to accept financial technology or innovation.

7. Conclusion

This study is aimed at examining customers’ intention to use e-wallets during COVID-19 pandemic comparing Indonesia and Malaysia using multigroup analysis. The direct and indirect effects of perceived risk, government support, and perceived usefulness are also tested on the intention to use e-wallets. This study concluded that perceived risk and perceived usefulness directly affected intention to use e-wallets during COVID-19 outbreak. This study also concluded that the effect of government support on the intention to use e-wallets is fully mediated by perceived usefulness. Lastly, this study revealed that there is a difference between Indonesia and Malaysia in government support and intention to use e-wallets relationship. In summary, this study highlighted that COVID-19 might drive customers’ intention to use e-wallets.

Additional information

Funding

Notes on contributors

Hendy Mustiko Aji

Hendy Mustiko Aji is an assistant professor at the Department of Management, Faculty of Busines and Economics (FBE), Universitas Islam Indonesia (UII). He has a strong research interest in the topics of digital wallet and Islamic marketing. Currently, he is the head of Islamic Business and Economics Development at the P3EI FBE UII.

Izra Berakon

Izra Berakon is a lecturer in the Department of Sharia Financial Management Faculty of Islamic Economics and Business, Universitas Islam Negeri Sunan Kalijaga (UINSUKA), Yogyakarta, Indonesia. He actively conducts research and discussion in the topic of Islamic social funds, financial technology, consumer behavior, and the halal industry.

Maizaitulaidawati Md Husin

Dr. Maizaitulaidawati Md Husin is a senior lecturer at Azman Hashim International Business School (AHIBS) Universiti Teknologi Malaysia. Her Ph.D. in Islamic Economy from Universiti Malaya was focusing on the adoption of family takaful among Muslims in Malaysia. She has also authored and co-authored more than 60 research papers, book chapters, universities, seminars, conferences and journal publications.

References

- Afthanorhan, A., Nazim, A., & Ahmad, S. (2015). A parametric approach using z-test for comparing 2 means to multi-group analysis in partial least square structural equation modeling (pls-sem). British Journal of Applied Science & Technology, 6(2), 194–16. https://doi.org/10.9734/BJAST/2015/14380

- Aji, H. M., Berakon, I., & Riza, A. F. (2020). The effects of subjective norm and knowledge about riba on intention to use e-money in Indonesia. Journal of Islamic Marketing, ahead-of-print(ahead–of–print). https://doi.org/10.1108/JIMA-10-2019-0203

- Aji, H. M., & Dharmmesta, B. S. (2019). Subjective norm vs dogmatism: Christian consumer attitude towards Islamic TV advertising. Journal of Islamic Marketing, 10(3), 961–980. https://doi.org/10.1108/JIMA-01-2017-0006

- Ali, M., Raza, S. A., & Puah, C. H. (2015). Factors affecting intention to use islamic personal financing in Pakistan: Evidence from the modified TRA model. In Munich Personal RePEc Archive (pp. 66023).

- Andik, S. D. S., Munandar, J. M., & Najib, M. (2018). A comparative study on Indonesian and Malaysian consumers’ perception and preference towards handphones from China, South Korea, America, and Europe, Indonesian. Journal of Business and Entrepreneurship, 4(2), 130–140. https://doi.org/10.17358/ijbe.4.2.130

- Andrieu, M. (2001). The future of e-money: An internatioal review of policy and regulatory issues. The Journal of Futures Studies, Strategic Thinking and Policy, 3(6), 502–522. https://doi.org/10.1108/14636680110420459

- Appiah, K., Osei, C., Selassie, H., & Osabutey, E. (2019). The role of government and the international competitiveness of SMEs: Evidence from Ghanaian non-traditional exports. Critical Perspectives On International Business, 15(4), 296–322. https://doi.org/10.1108/cpoib-06-2018-0049

- The ASEAN Post. (2020). Food delivery on the rise in ASEAN. https://theaseanpost.com/article/food-delivery-rise-asean

- Ather, A., Patel, B., Ruparel, N. B., Diogenes, A., & Hagreaves, K. M. (2020). Coronavirus disease 19 (COVID-19): Implications for clinical dental care. Journal of Endodontics, 46(5), 584–595. https://doi.org/10.1016/j.joen.2020.03.008

- Bagla, R. K., & Sancheti, V. (2018). Gaps in customer satisfaction with digital wallets: Challenge for sustainability. Journal of Management Development, 37(6), 442–451. https://doi.org/10.1108/JMD-04-2017-0144

- Baker, T., & Moss, A. (2009). New perspectives on regulation (1st ed.). The Tobin Project.

- Bank Indonesia. (2020). Latest economic developments and Bank Indonesia measures to control COVID-19. Bank Indonesia, Bank Sentral Republik Indonesia. Retrieved March 26, 2020, from https://www.bi.go.id/en/ruang-media/info-terbaru/Pages/Perkembangan-Terkini-Perekonomian-dan-Langkah-BI-dalam-Hadapi-COVID-19-26032020.aspx

- Bauer, R. A. (1960). Consumer behavior as risk-taking. In R. S. Hancock (Ed.), Dynamic marketing for a changing world (pp. 389–398). American Marketing Association.

- Beldad, A. D., & Hegner, S. M. (2017). Expanding the technology acceptance model with the inclusion of trust, social influence, and health valuation to determine the predictors of German users’ willingness to continue using a fitness app: A structural equation modeling approach. International Journal of Human-computer Interaction, 34(9), 882–893. https://doi.org/10.1080/10447318.2017.1403220

- Brown, D. (2020). Can cash carry coronavirus? World Health Organization says use digital payments when possible. USA Today. Retrieved April 1, 2020, from https://www.usatoday.com/story/money/2020/03/06/coronavirus-covid-19-concerns-over-using-cash/4973975002/

- Budi, A. S. L., Efendi, E., & Dahesihsari, R. (2011). Perceived usefulness as key stimulus to the behavioral intention to use 3G technology. ASEAN Marketing Journal, 3(2), 105–114. https://doi.org/10.21002/amj.v3i2.2025

- Capgemini. (2019). World payment report 2019. Capgemini Research Institute. Retrieved April 2, 2020, from. https://worldpaymentsreport.com/wp-content/uploads/sites/5/2019/09/World-Payments-Report-WPR-2019.pdf

- Cheung, C. M. K., & Lee, M. K. O. (2008). The structure of web-based information systems satisfaction: Testing of competing models. Journal of the American Society for Information Science and Technology, 59(10), 1617–1630. https://doi.org/10.1002/asi.20881

- Chong, J. M. (2012). Mine, yours or ours?: The Indonesia-Malaysia disputes over shared cultural heritage. Sojourn: Journal of Social Issues in Southeast Asia, 27(1), 1–53. https://doi.org/10.1353/soj.2012.0008

- Davis, F., Bagozzi, R., & Warshaw, P. (1989). User acceptance of computer technology: A comparison of two theoretical models. Management Science, 35(8), 982–1003. https://doi.org/10.1287/mnsc.35.8.982

- Dawi, N. M. (2019). Factors influencing consumers intention to use QR code mobile payment – A proposed framework. International Journal of Recent Technology and Engineering, 8(2S), 114–120. https://www.ijrte.org/wp-content/uploads/papers/v8i2S/B10170782S19.pdf

- Fan, V. Y., Jamison, D. T., & Summers, L. H. (2018). Pandemic risk: How large are the expected losses? Bulletin of the World Health Organization, 96(2), 129–134. https://doi.org/10.2471/BLT.17.199588

- Fernandes, N. (2020, April 13). Economic effects of coronavirus outbreak (COVID-19) on the world economy. SSRN. Retrieved April 2, 2020, from https://papers.ssrn.com/sol3/papers.cfm?Abstract_id=3557504

- Fornell, C., & Larcker, F. D. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Forsythe, S. M., & Shi, B. (2003). Consumer patronage and risk perceptions in internet shopping. Journal of Business Research, 56(11), 867–875. https://doi.org/10.1016/S0148-2963(01)00273-9

- Global Web Index. (2020). Coronavirus research series 4: Media consumption and sport. Global Web Index. Retrieved April 2, 2020, from https://www.globalwebindex.com/coronavirus

- Goodell, J. W. (2020). COVID-19 and finance: Agendas for future research. Finance Research Letters, 35, 101512. https://doi.org/10.1016/j.frl.2020.101512

- Haderi, S. M. (2014). The influences of government support in accepting the information technology in public organization culture. International Journal of Business and Social Science, 5(5), 118–124. http://www.ijbssnet.com/journals/Vol_5_No_5_April_2014/14.pdf

- Hai, L. C., & Kazmi, S. H. A. (2015). Dynamic support of government in online shopping. Asian Social Science, 11(22), 1–9. https://doi.org/10.5539/ass.v11n22p1

- Hair, J. F., Jr, Black, W. C., Babib, B. J., & Anderson, R. E. (2014). Multivariate data analysis (7th ed.). Edinburgh.

- Hampshire, C. (2017). A mixed methods empirical exploration of UK consumer perceptions of trust, risk and usefulness of mobile payments. International Journal of Bank Marketing, 35(3), 354–369. https://doi.org/10.1108/IJBM-08-2016-0105

- Hasan, M. K., Ismail, A. R., & Islam, M. F. (2017). Tourist risk perceptions and revisit intention: A critical review of literature. Cogent Business and Management, 4(1), 1–21. https://doi.org/10.1080/23311975.2017.1412874

- Hooper, D., Coughlan, J., & Mullen, M. R. (2008). Structural equation modelling: Guidelines for determining model fit. Electronic Journal of Business Research Methods, 6(1), 53–60. http://www.ejbrm.com/volume6/issue1

- Huang, R. (2020). WHO encourages use of contactless payments due to COVID-19. Forbes. Retrieved March 15, 2020, from https://www.forbes.com/sites/rogerhuang/2020/03/09/who-encourages-use-of-digital-payments-due-to-covid-19

- Huh, H. J., Kim, T. T., & Law, R. (2009). A comparison of competing theoretical models for understanding acceptance behavior of information systems in upscale hotels. International Journal of Hospitality Management, 28(1), 121–134. https://doi.org/10.1016/j.ijhm.2008.06.004

- IDN Financials. (2020.) BI encourages public to use non-cash transaction method. IDN Financials. Retrieved March 28, 2020, from https://www.idnfinancials.com/news/32945/encourages-public-non-cash-transaction-method

- Im, I., Kim, Y., & Han, H.-J. (2008). The effects of perceived risk and technology type on users’ acceptance of technologies. Information & Management, 45(1), 1–9. https://doi.org/10.1016/j.im.2007.03.005

- Ivanov, D. (2020). Predicting the impacts of epidemic outbreaks on global supply chains: A simulation-based analysis on the coronavirus outbreak (COVID-19/SARS-CoV-2) case. Transportation Research Part E: Logistics and Transportation Review, 136, 1–14. https://doi.org/10.1016/j.tre.2020.101922

- The Jakarta Post. (2020). Food deliveries, online game purchases up as people stay at home during COVID-19 pandemic. Retrieved March 25, 2020, from https://www.thejakartapost.com/news/2020/03/20/food-deliveries-online-game-purchases-up-as-people-stay-at-home-during-covid-19-pandemic.html

- Kassim, N. M., & Ramayah, T. (2015). Perceived risk factors influence on intention to continue using internet banking among Malaysians. Global Business Review, 16(3), 393–414. https://doi.org/10.1177/0972150915569928

- Kaur, H. (2020). Forget ‘social distancing.’ The WHO prefers we call it ‘physical distancing’ because social connections are more important than ever. CNN. Retrieved April 20, 2020, from https://edition.cnn.com/2020/04/15/world/social-distancing-language-change-trnd/index.html

- Koenig-Lewis, N., Palmer, A., & Moll, A. (2010). Predicting young consumers’ take up of mobile banking services. International Journal of Bank Marketing, 28(5), 410–432. https://doi.org/10.1108/02652321011064917

- Kotler, P., & Keller, K. L. (2012). Marketing management (14th ed.). Prentice Hall.

- Lee, M.-C. (2009). Factors influencing the adoption of internet banking: An integration of TAM and TPB with perceived risk and perceived benefit. Electronic Commerce Research and Applications, 8(3), 130–141. https://doi.org/10.1016/j.elerap.2008.11.006

- Lee, S. Y., & Park, J. (2016). A study on the intention of the use of mobile payment services: Application of the technology acceptance model. Korean Management Science Review, 33(2), 65–74. https://doi.org/10.7737/KMSR.2016.33.2.065

- Leong, L.-Y., Hew, T.-S., Ooi, K.-B., & Jun, J. W. (2020). Predicting mobile wallet resistance: A two-staged structural equation modeling-artificial neural network approach. International Journal of Information Management, 51, 1–24. https://doi.org/10.1016/j.ijinfomgt.2019.102047

- Lu, H., Hsu, C., & Hsu, H. (2005). An empirical study of the effect of perceived risk upon intention to use online applications. Information Management and Computer Security, 13(2), 106–120. https://doi.org/10.1108/09685220510589299

- Mandari, H. E., Chong, Y.-L., & Wye, C.-K. (2017). The influence of government support and awareness on rural farmers’ intention to adopt mobile government services in Tanzania. Journal of Systems and Information Technology, 19(1/2), 42–64. https://doi.org/10.1108/JSIT-01-2017-0005

- Marafon, D. L., Basso, K., Espartel, L. B., de Barcellos, M. D., & Rech, E. (2018). Perceived risk and intention to use internet banking: The effects of self-confidence and risk acceptance. International Journal of Bank Marketing, 36(2), 277–289. https://doi.org/10.1108/IJBM-11-2016-0166

- Marria, V. (2018). What a cashless society could mean for the future. Forbes. Retrieved April 5, 2020, from https://www.forbes.com/sites/vishalmarria/2018/12/21/what-a-cashless-society-could-mean-for-the-future/#77c7528a3263

- Maser, B., & Weiermair, K. (1998). Travel decision-making: From the vantage point of perceived risk and information preferences. Journal of Travel & Tourism Marketing, 7(4), 107–121. https://doi.org/10.1300/J073v07n04_06

- MHTC. (2020). PM statement to Covid-19 social distancing measures. Malaysia Healhcare. Retrieved March 18, 2020, from https://www.mhtc.org.my/mhtc/2020/03/16/pm-statement-to-covid-19-social-distancing-measures/

- Negara, S. D. (2020). Commentary: Indonesia’s COVID-19 fight has deeper challenges. CNA: Channel News Asia. Retrieved April 15, 2020, from https://www.channelnewsasia.com/news/commentary/is-indonesia-doing-enough-to-fight-covid-19-12614440

- Nicola, M., Alsafi, Z., Sohrabi, C., Kerwan, A., Al-Jabir, A., Losifidis, C., Agha, M., & Agha, R. (2020). The socio-economic implications of the coronavirus and covid-19 pandemic: A review. International Journal of Surgery, 78, 185–193. https://doi.org/10.1016/j.ijsu.2020.04.018

- Nielsen. (2020). Asian consumers are rethinking how they eat post Covid-19. Nielsen. Retrieved March 28, 2020, from https://www.nielsen.com/id/en/insights/article/2020/asian-consumers-are-rethinking-how-they-eat-post-covid-19/

- Nunnally, J. C. (1967). Psychometric theory. McGraw-Hill.

- Oh, S.-H., Paek, H.-J., & Hove, T. (2015). Cognitive and emotional dimensions of perceived risk characteristics, genre-specific media effects, and risk perceptions: The case of H1N1 influenza in South Korea. Asian Journal of Communication, 25(1), 14–32. https://doi.org/10.1080/01292986.2014.989240

- Olya, H. G. T., & Al-Ansi, A. (2018). Risk assessment of halal products and services: Implication for tourism industry. Tourism Management, 65, 279–291. https://doi.org/10.1016/j.tourman.2017.10.015

- PMO. (2020). [PRIHATIN] Matlamat 1: Lindungi Rakyat. PMO: Prime Minister Office. Retrieved March 20, 2020, from https://www.pmo.gov.my/2020/03/pre-prihatin-matlamat-1-lindungi-rakyat/

- PWC. (2018). Banking on the e-wallet in Malaysia. PWC: PricewaterhouseCoopers. Retrieved March 29, 2020, from https://www.pwc.com/my/en/assets/blog/pwc-my-deals-strategy-banking-on-the-ewallet-in-malaysia.pdf

- PWC. (2019). It’s time for a consumer-centred metric: Introducing ‘return on experience’ – Global consumer insights survey. PWC: PricewaterhouseCoopers. Retrieved March 29, 2020, from https://www.pwc.com/gx/en/consumer-markets/consumer-insights-survey/2019/report.pdf

- Rambocas, M. M., & Arjoon, S. (2012). Using diffusion of innovation theory to model customer loyalty for internet banking: A TT millennial perspective. International Journal of Business and Commerce, 1(8), 1–14. https://pdfs.semanticscholar.org/91dc/0b67507e55cfb30a73251c74533bd83e6eea.pdf

- Rauniar, R., Rawski, G., Yang, J., & Johnson, B. (2014). Technology acceptance model (TAM) and social media usage: An empirical study on Facebook. Journal of Enterprise Information Management, 27(1), 6–30. https://doi.org/10.1108/JEIM-04-2012-0011

- Reni, A., & Ahmad, N. H. (2016). Application of theory reasoned action in intention to use Islamic banking in Indonesia. Al-Iqtishad: Journal of Islamic Economics, 8(1), 137–148. https://doi.org/10.15408/aiq.v8i1.2513

- Riquelme, H. E., & Rios, R. E. (2010). The moderating effect of gender in the adoption of mobile banking. International Journal of Bank Marketing, 28(5), 328–341. https://doi.org/10.1108/02652321011064872

- Rittichainuwat, B. N., & Chakraborty, G. (2009). Perceived travel risks regarding terrorism and disease: The case of Thailand. Tourism Management, 30(3), 410–418. https://doi.org/10.1016/j.tourman.2008.08.001

- Sani, M. A. M., & Hara, A. B. E. (2007). Deliberative democracy in Malaysia and Indonesia: A comparison. Retrieved April 19, 2020, from https://www.researchgate.net/publication/237620648_Deliberative_Democracy_in_Malaysia_and_Indonesia_A_Comparison

- Sheikh, K., Sriram, V., Rouffy, B., Lane, B., Soucat, A., & Bigdeli, M. (2020). Governance roles and capacities of ministries of health: A multidimensional framework. International Journal of Health Policy Management, 1–7. https://doi.org/10.34172/ijhpm.2020.39

- The Star. (2020). Boost supports government’s e-wallet initiatives. Retrieved July 11, 2020, from https://www.thestar.com.my/business/business-news/2020/06/12/boost-supports-governments-e-wallet-initiatives

- Stone, R. N., & Gronhaug, K. (1993). Perceived risk: Further considerations for the marketing discipline. European Journal of Marketing, 27(3), 39–50. https://doi.org/10.1108/03090569310026637

- Swift, K. T. (2009). Economic effects of a flu pandemic. Chemical Engineering Progress, 105(9), 22.

- Tan, M., & Teo, T. S. H. (1998). Factors influencing the adoption of the Internet. International Journal of Electronic Commerce, 2(3), 5–18. https://doi.org/10.1080/10864415.1998.11518312

- Tanadi, T., Samadi, B., & Gharleghi, B. (2015). The impact of perceived risks and perceived benefits to improve an online intention among generation-y in Malaysia. Asian Social Science, 11(26), 226. https://doi.org/10.5539/ass.v11n26p226

- Turner, J., & Akinremi, T. (2020). The business effects of pandemics – A rapid literature review. ERC Insight Paper. Retrieved April 10, 2020, from https://www.enterpriseresearch.ac.uk/wp-content/uploads/2020/04/ERC-Insight-The-business-effects-of-pandemics-%E2%80%93-a-rapid-literature-review-Final.pdf

- Venkatesh, V., & Bala, H. (2008). Technology acceptance model 3 and a research agenda on interventions. Decision Sciences, 39(2), 273–315. https://doi.org/10.1111/j.1540-5915.2008.00192.x

- Venkatesh, V., & Davis, F. D. (2000). A theoretical extension of the technology acceptance model: Four longitudinal field studies. Management Science, 46(2), 186–204. https://doi.org/10.1287/mnsc.46.2.186.11926

- Victoria, O. O., & Amir, F. (2018). Systems and political development in malaysia. International Journal of Law Reconstruction, 2(2), 122–137. https://doi.org/10.26532/ijlr.v2i2.3306

- Wei, J., & Liu, J. (2015). Government support and firm innovation performance: Empirical analysis of 343 innovative enterprises in China. Chinese Management Studies:, 9(1), 38–55. https://doi.org/10.1108/CMS-01-2015-0018