?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

In current volatile business environment, the owners of the corporations are worried about how diverse board composition influences the strategic performance of the corporations. Therefore, this study considered the agency theory, upper echelon and resource-based view of board heterogeneity as limited literature account for such integrated phenomenon of theories. Accordingly, the key aim of the study is to scrutinize the impacts of occupational heterogeneity (educational) and social heterogeneity (gender and national) on firm performance. At first, Blau’s heterogeneity index was applied to measure the occupational heterogeneity and social heterogeneity, then ordinary least square method was applied for analysis. The data set was obtained from the non-financial sector of Pakistan Stock Exchange for the years 2010–2016 with final sample of 375 firms. The findings of current research concluded that all measures of occupational heterogeneity significantly and positively contribute to firm value expect finance education and other education (defense, arts, political science etc.). However, in social heterogeneity, gender diversity has a negative effect on firm performance while nationally heterogeneous board demonstrate a positive effect on firm performance. Moreover, this study has beneficial implications for the corporate sector as firms can boost their profitability by extracting benefits from their diverse workforce.

PUBLIC INTEREST STATEMENT

Diversity at the workplace is prevalent nowadays, even top management of any organization is also consisting of heterogeneous members. Organizations are bearing the consequences of diversity; these consequences can be either beneficial or sometimes detrimental. Top management members with an educational background in Business & Economics, Engineering & Computer and MBA have a positive contribution to the business. While members specialized in finance are busier with other financial matters of the company and likewise, members with other educational backgrounds are also not contributing much. Female to male and international to national directors ratio also has a significant contribution to business. This study is helpful for organizations while selecting candidates for a top management position and beneficial for students to choose their specialization if they want to be among top management in the future.

1. Introduction

In current volatile business environment, the owners of the corporations are worried about how board composition influences the strategic performance of the corporations. Thus, a number of scholars intend to find out the board compositional factors that affect the board’s role in strategic decision making (Haynes & Hillman, Citation2010; Tuggle et al., Citation2010; Veltrop & Molleman, Citation2019). As the board has a central position in any organization and in strategic decision making, therefore, the influence of board heterogeneity on board’s decisions that affect the firm performance is an interesting point of research. Heterogeneity of the board becomes a priority of many corporations either to build their good social image or to attain a more diverse workforce (Kim, Citation2014). Moreover, heterogeneity among board members significantly influences the performance of the board (Burke et al., Citation2019). Likewise, existing studies (Burke et al., Citation2019; Hutzschenreuter & Horstkotte, Citation2013; Talavera et al., Citation2018) provide support for this notion and reported that heterogeneous board in terms of gender, age, experience and qualification has a positive influence over the firm performance and social performance.

Additionally, more heterogeneous board can bring more diverse resources to the firm (Midavaine et al., Citation2016), therefore, previous studies considered corporate board as a source of information and resources (Athmen & Samia, Citation2017). Such diverse information on board can help directors to critically evaluate an existing opportunity and problem of external environment (Hutzschenreuter & Horstkotte, Citation2013; Midavaine et al., Citation2016). Similarly, differences among the cognitive abilities of the directors enhance the effective strategic decisions and their monitoring ability (Anderson et al., Citation2011). Moreover, Variety of cognitive abilities on the board can enhance the human capital within the firm (Haynes & Hillman, Citation2010).

Additionally, large multinational firms like Pepsi Co. indicated that more heterogeneous board is beneficial for development of new products (Torchia et al., Citation2011). However, board diversity is not solely based on social image of organizations but the decision is made on cost and benefit analysis (Khan & Abdul Subhan, Citation2019). Though more diverse board brings more information, experience and professional background to the board and such a variety of talent and skills on board causes effective monitoring (Kim, Citation2014). Researchers (Adusei et al., Citation2017) stated that a diverse board can better predict the market in terms of customers’ needs, product demand and competition severity which result in a good performance. On the other hand, heterogeneity among board members causes severe coordination and communication problems (Midavaine et al., Citation2016). For instance, directors with disparate background bring a variety of deliberations to the board and this can increase controversies among board members that cause the prolonged decision-making process (Torchia et al., Citation2011). Moreover, differences in opinion of disparate directors lead to weak social capital (Hassan et al., Citation2020). Hence, due to the ambiguous pieces of evidence, this study is primarily centered on determining the role of board diversity for firm performance.

Furthermore, board heterogeneity is possible in different ways such as gender, age, experience, tenure and nationality. Except gender diversity, previous scholars focus less on how various forms of board heterogeneity can influence the board effectiveness and firm performance (Anderson et al., Citation2011). Apart from that, existing studies of corporate governance and firm performance are heavily rooted in one aspect (i.e. agency problems) of firms (Khan & Abdul Subhan, Citation2019). The other aspect such as human capital which works as the backbone of corporate of governance is widely ignored, specifically, how diverse human capital can reduce the firm’s uncertainties to achieve high performance is still an open question. Therefore, this study vetted the influence of board heterogeneity on firm performance using an integrated approach based on three theories agency theory, resource-based view and upper echelon theory to fill the gap in existing literature.

Furthermore, current research follows the lines of earlier researchers (Anderson et al., Citation2011; Midavaine et al., Citation2016) and categories board heterogeneity into two groups namely, occupational heterogeneity and social heterogeneity. Accordingly, this research includes precise measures of board heterogeneity rather emphasize on a single dimension of board heterogeneity as found in most of the previous studies (Adams & Ferreira, Citation2009; Carter et al., Citation2010; Midavaine et al., Citation2016). Yet, the heterogeneity of board has not gained much attention of scholars from emerging and developing countries. Therefore, using a sample of non-financial firms in Pakistan, this study specifically designs to answer how board occupational and social heterogeneity influence firms’ performance in Pakistan.

2. Theory and hypotheses

Heterogeneity of board has become the top-notch issue among academic researchers and business regulators (Ameer et al., Citation2010; Anderson et al., Citation2011; Burke et al., Citation2019; Hassan et al., Citation2020; Talavera et al., Citation2018). Recent business reports and official statements of companies show that greater heterogeneous board arises not due to moral or ethical pressure (Burke et al., Citation2019), but due to the fact that highly heterogeneous board has a competitive edge and has greater ability to overcome environmental uncertainties. Hence, organizational success and survival depend on the efficiency of firms to manage these uncertainties to create competitive advantage (Midavaine et al., Citation2016). According to resource-based theory, firms should have unique human and social capital to overcome external environment’s uncertainties (Taljaard et al., Citation2015). Moreover, uniqueness and heterogeneity of human and social capital owned by the organizations are critical for creative ideas (Nielsen & Nielsen, Citation2013).

Additionally, existing literature categorized the heterogeneity into two categories, occupational heterogeneity, also known as non-observable attributes of directors including education, tenure (experience), professional background (Anderson et al., Citation2011; Mahadeo et al., Citation2012). The second category is known as social heterogeneity or readily observable heterogeneity including age, gender and nationality (Anderson et al., Citation2011; Mahadeo et al., Citation2012). Most of the existing researches emphasized on observable heterogeneity (Carter et al., Citation2010; Hassan et al., Citation2020; Talavera et al., Citation2018) and more specifically focus on gender diversity (Bøhren & Staubo, Citation2014). However, the recent stream of studies also accounts for the other social attributes of heterogeneity like nationality, age and ethnic background (Kim, Citation2014). Meanwhile, few scholars provide empirical support for the occupational heterogeneity of board like education and experience (Haynes & Hillman, Citation2010; Taljaard et al., Citation2015).

2.1. Occupational heterogeneity

Specifically, upper echelon theory stated that occupational heterogeneity should affect the cognitive ability of the individuals and their decision-making ability (Athmen & Samia, Citation2017; Tuggle et al., Citation2010). When such individuals work in a group, their knowledge and ability to process information and previous experience influence the whole group decision (Kim, Citation2014). Moreover, occupational heterogeneity is taken as a proxy of human capital or intellectual capital in the previous investigations (Anderson et al., Citation2011; Midavaine et al., Citation2016). In this context, upper echelon’s educational background has gained considerable attention of academicians.

Some researchers found that educational level of directors has significant influence over the strategic change within organization (Haynes & Hillman, Citation2010). Scholars justify this statement by arguing that higher education brings openness, more capacity to organize information, effective information processing and less fear to adopt change (Bøhren & Staubo, Citation2014; Midavaine et al., Citation2016). Similarly, significant positive association between higher educational level of board members and research and development is reported by Haynes and Hillman (Citation2010). In addition, a higher level of education leads to international diversification (Herrmann & Datta, Citation2005). Therefore, the effect of educational diversity on firm performance is an important factor to question for firm profitability.

Additionally, heterogeneity of the board enhances the board independence and reduces agency conflicts. As independent directors with diverse education and experience can question the performance of management that probably cannot be expected from homogeneous board (Taljaard et al., Citation2015). According to the resource-based view, directors are responsible for resource allocation of organizations (Haynes & Hillman, Citation2010), thus, prior higher education has significant impact over their ability to efficiently allocate resources to profitable projects.

Contrary to that, scholars found that high occupational heterogeneity of board causes some problems of communication and collaboration (Hassan et al., Citation2020). For instance, more heterogeneous board remains unable to completely utilize the variety of available knowledge and information due to communication and social interaction problems (Midavaine et al., Citation2016). Directors with incongruent educational and functional background have different opinions and cognitive skills that cause communication and weak group integration. Similarly, directors with different educational backgrounds become unable to effectively communicate the information within the board, thus, face poor performance as compared to a homogeneous board (Nielsen & Nielsen, Citation2013).

Hence, board’s occupational heterogeneity may stimulate the emotional, interpersonal and behavioral issues. Most probably, when a board has directors with more diverse backgrounds, they may be unwilling to exchange and share their ideas with others due to communication problems and superiority complex (Torchia et al., Citation2011). Thus, ineffective and inefficient information processing, conflicts among board members and CEOs, delaying in strategic decision making and impasse at board level causes poor firm performance (Kim, Citation2014). Generally, weak firm performance is the result of late response towards available opportunities and poor shielding strategies against potential threats.

In summary, few existing studies favor the high occupational heterogeneity and the others oppose these propositions. It is difficult to draw a conclusion; therefore, this study further investigates the occupational heterogeneity of board with respect to firm performance. Hence, the following hypotheses are developed.

H1: Heterogeneity among board members’ educational level has a significant effect on firm performance.

H1a: Directors’ educational background in business and economics has a significant influence on firm performance.

H1b: Directors’ educational background in engineering and computer significantly influences firm performance.

H1 c: Director’s specialization in finance subject has a significant influence on firm performance.

H1d: Directors with a Master of Business Administration (MBA) degree significantly influence firm performance.

H1e: Directors holding a degree of other (defense, arts, political science etc.) disciplines have a significant influence on firm performance.

2.2. Social heterogeneity

In social and organizational psychology, a term “faultlines” is used to observe the difference among groups, specifically “faultlines” refers to the personal heterogeneity (Adams et al., Citation2015). These scholars claimed age, gender, nationality and ethnicity as a crucial point of faultlines. Specifically, gender heterogeneity has gained much attention from both academic scholars and human right workers (Adusei et al., Citation2017). However, few researchers shed light on gender heterogeneity in developing nations (Hutzschenreuter & Horstkotte, Citation2013). Likewise, some scholars focus on the idea of national heterogeneity (Adams et al., Citation2015). Therefore, the current research has aimed to investigate the gender and nationality heterogeneity impact on firm performance.

Besides, existing literature on gender diversity postulate that women on boards enhance board effectiveness, increase understanding of market place and produce a most creative solution to board agendas (Julizaerma & Sori, Citation2012; Zaid et al., Citation2020). Similarly, when women on board are only a few, they monitor the board activities more independently and effectively. Researchers argued that women have great potential to work and compete with their counterparts (Joecks et al., Citation2013). Mahadeo et al. (Citation2012) stated that women on corporate board have a positive effect on firm performance. Consequently, another study conducted by Campbell and Mínguez-Vera (Citation2008) using a sample of Spain firms, provides positive empirical support for gender diversity and firm performance. Moreover, according to (Dobbin & Jung, Citation2011), in terms of financial performance and corporate governance, companies can perform better where the female directors are more than three.

Contrary to that, Khan and Abdul Subhan (Citation2019) asserted that number of female directors on board did not have any significant effect on firm performance. On the same vein, other scholars (Adams & Ferreira, Citation2009; Ahern & Dittmar, Citation2012; Bøhren & Staubo, Citation2014) have found negative or no significant relationship between gender diversity and firm performance (Carter et al., Citation2010). Likewise, Ahern and Dittmar (Citation2012) argued that stock value goes down leaving a negative effect on firm performance by increasing female ratio as directors. In their opinion, male directors are senior and more expert than female directors. It is observed that corporate board’s gender diversity has an effect on stock performance and concluded that the organization with gender diversity shows negative or neutral results with different performance measures such as return on asset (ROA), Tobin’s Q and cumulative stock returns (Robb & Watson, Citation2012).

In addition, due to rapid and advanced globalization of labor market, scholars are more concerned about the foreign directors on board or directors nationality (Masulis et al., Citation2012; Zaid et al., Citation2020). Though, the nationality of board members is largely ignored by the academic scholars, Yet, only countable studies shed light on this phenomenon. The most prominent study is conducted in 2003, by Oxelheim and Randøy on director’s nationality using American data set. Heterogeneity in terms of directors’ nationality is subject to both cost and benefits. As board members having disparate nationality bring more information and ideas to expand business globally (Tuggle et al., Citation2010) and are better able to communicate information than other members, hence, they ultimately bring superior and positive firm performance (Zaid et al., Citation2020).

Similarly, according to upper echelon theory and resource-based perspective, foreign directors with different nationality, bring a variety of cognitive skills and capabilities to board and decision-making process which contributes to creative strategic decisions (Hambrick & Mason, Citation1984). A study on Swiss multinational companies conducted by the (Nielsen & Nielsen, Citation2013) reported a positive relationship between firm performance and nationally heterogeneous board. Heterogeneous board with dissimilar nationalities can work more creatively (Zaid et al., Citation2020) and, therefore, effectively contribute to strategic planning which in turn causes positive performance of organizations (Peck-Ling et al., Citation2016).

On the other hand, few scholars negate the propositions of upper echelon theory and argued that board heterogeneity instigates group conflicts (Williams & O’Reilly, Citation1998) and national heterogeneity creates communication issues, increase the agency costs and in return decrease the organizational commitment (Tsui et al., Citation1992). Consequently, Masulis et al. (Citation2012) stated that nationally heterogeneous board triggers weak monitoring by foreign directors and increase the agency cost. These arguments lead towards the following hypotheses.

H2: Board gender heterogeneity has a significant influence on firm performance.

H3: Nationally heterogeneous board has a significant influence on firm performance.

3. Research methodology

This study used a quantitative research method to analyze the proposed model; secondary data from the annual reports and other data sources are used in this research. By going along the applications of quantitative research, the following section describes the various techniques applied in this study.

3.1. Research framework

Hypothesized framework of the current study is grounded on the underpinning theories and literature of board heterogeneity and firm performance. The framework is drawn in Figure .

Figure 1. Research Framework.

3.2. Econometrics model

3.3. Data and variables

The target population of the study is non-financial firms listed on Pakistan Stock Exchange (PSX). The total number of firms listed on PSX in November 2016 was 436 firms. This study considers a total of 436 firms as the final sample over the period of 2010–2016. Researchers of the study used secondary sources like annual reports, Bloomberg, 4traders and World-Scope database for data collection. Data collected from the database and other sources is rechecked and compare with the data reported in the corresponding firms’ annual reports.

Furthermore, the nature of data is unbalanced panel data because the number of firm years across the observations is not same due to numerous reasons. For instance, in case the required data of any variable is missing in a specific year then that particular firm year is excluded. Besides, a firm is excluded from sample if the required data is missing for more than three years, newly registered firms and firms delisted during the selected time span are also excluded from the final sample. In this way, total 61 firms were excluded from the sample. Moreover, the researchers applied the Cook’s distance test to detect the potential outliers or influential observations and found out that 33 firm years indicated outliers. Thus, the final sample of the study is 2592 firm years out of 2625 firm year observations from 375 firms.

Table illustrated the characteristics of the sample which show that from 2010 to 2016, sample firms have 70.33% of male and 29.67% of female members on board. Similarly, during the period of 2010 to 2016, sample firms have 27.16% of foreign directors on board and 72.84% of national directors on board. Both the representation of female directors and foreign directors on board is very low during the period under consideration.

Table 1. Firm year distribution

3.4. Measurement of variables

The dependent variable of the study is market-to-book ratio, which is measured by following Ahmed Sheikh and Wang (Citation2012) as this measurement is more appropriate to avoid outliers and dispersion in the data. Thus, market-to-book ratio in this study measured as the ratio of average of high and low market price per share for the year to book value per share.

The explanatory variables namely, educational, gender and national heterogeneity are measured using the Blau’s heterogeneity index following Heyden et al. (Citation2015). Blau’s heterogeneity index is generally used to measure diversity among groups. According to Blaus’ index, as the value of index approaches 1, there is high heterogeneity and low heterogeneity when its value is near to 0. When the value of the index is 0.5, it means that members in each category are equal. The following equation is used to compute the Blau’s heterogeneity index.

In the current research, gender is categorized into two groups namely, male and female. National heterogeneity includes the national and international directors on board while education grouped into five groups (Business & Economics, Engineering & Computer, Finance Specialist, MBA and others), and the level of education of board members are also considered (i.e. PhD, Masters, Bachelors).

3.5. Control variables

The study included two potential predictors of the firm performance namely, firm size and firm age. As some studies stated that the firm size directly influences the firm performance because larger firms have greater sources of diversification and able to outperform than smaller firms (Lehn et al., Citation2009). Since firm size is measured by the log of book value of assets. Firm age also matters for the firm performance as the older firms have more knowledge and experience in the market and hold an image in the customers’ mind (Ayuba et al., Citation2019). On the other side, newer firms have the ability to compete with older firms through their flexibility to adopt new ideas and they attract most energetic young customers. Firm age is measured as the log of number of years since incorporation of firm.

4. Data analysis

4.1. Univariate analysis

Descriptive statistics of the data are elaborated in Table ; results indicate some of the interesting facts about the sample firms. Descriptive statistics indicate that the maximum number of female directors on board is 3 with standard deviation (0.940) greater than the mean value 0.524 which means that there is a greater deviation in data, as well as the representation of female directors on board during the sample period, is 29.67%. According to univariate analysis, the maximum number of foreign directors are 7 with a minimum value of 0 which means no representation of foreign directors on board. Moreover, the percentage of foreign directors on board throughout the sample period is 27.14% which is quite low.

Table 2. Descriptive Statistics

Likewise, descriptive statistics of educational information of directors describe that at least 2 members of the board earned Business and Economics degree with maximum 5 and average 2 members. Maximum directors specialized in Engineering and Computer are 5 with a minimum of 0 members specialized in this field while the average value of this group is 1.783. Moreover, maximum 3 Finance Specialist has been setting on the board and in some cases, there are no directors on board with Finance specialization. A similar case is with the MBA educational group as the maximum number of MBA degree holders are 4 and mean value illustrate that average of MBA degree holders on board are 1.65 while standard deviation value shows a moderate dispersion in data. Since majority of the board members earned degrees of other disciplines (defense, law, art, political sciences etc.) as the maximum members with other educational degree are 9. The average age of sample firms is 41.599 and the oldest firm is 156-year-old.

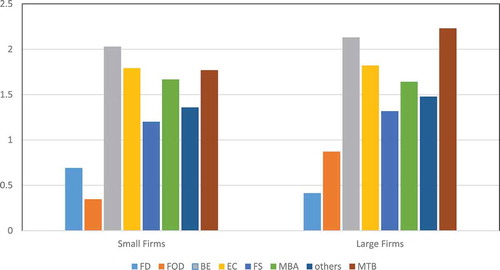

This research also summarizes the small and large firm’s characteristics graphically. Researchers differentiate between large and small firms using the median value of firm size. A firm has been categorized as small if the value of firm size (log of total assets) is less than the median value in at least 5 recent past years during the sample period. On the contrary, a firm has been fallen in the large category if its firm size value is greater than the median value in the last 5 years. Then the authors took an average of each group to portray them graphically.

Figure is evident that representation of female directors on board is higher in small firms. However, foreign directors on board are more in large firms as compared to small firms. While the educational background of directors remained almost the same in both large and small firms and can be seen in Figure . Moreover, large firms outperformed than small firms as there is a clear difference in their performance.

Figure 2. Small Vs Large Firms.

4.2. Regression analysis

Before applying any data analysis technique, data is critically examined and cross-checked in order to avoid any ambiguity. In addition, the availability of data is not viable through a sole source of annual reports. Hence, in order to have maximum data related to education, many different sources are used that resulted in a unique data set.

Additionally, Cook’s distance test is applied to examine the existence of an outlier and the findings illustrate that there are no outliers in the data as the data is entered and handled carefully. The Cook’s distance test is a commonly used test to find out any influential data points before applying ordinary least square analysis (OLS).

Driscoll and Kraay’s regression analysis is applied to evaluate the proposed relationships; this technique accounts for the issues of cross-sectional dependencies, heteroskedastic and auto-correlation (Hoechle, Citation2007). Moreover, the Hausman test is applied to choose between fixed and random effects model as it is required in panel data to choose the most appropriate model. In Hausman test, the H0 or null hypothesis is that the random effect model is more appropriate and H1 or alternative hypothesis is that the fixed effect model is much suitable for the data. After analyzing the data for the choice between random and fixed effect, the statistics illustrate that fixed effect model is more appropriate for the current study’s data set as the value of Hausman test is 0.427 which is greater than 0.05, if the is less than 0.05 then the case would have been reversed. Results of the Driscoll and Kraay’s regression analysis are illustrated in Table using the Blau’s Heterogeneity index of education, gender and nationality as explanatory variables.

Table 3. Multiple regression analysis

Here, results of the multiple regression analysis describe that educational heterogeneity positively influence the firm value since the more diverse board in terms of educational background brings more cognitive abilities and skills to firms (Darmadi, Citation2013). As per H1, the relationship between educational level heterogeneity and firm performance is accepted. Additionally, the Business and Economics education background of directors positively influence the market-to-book ratio at 1% level of significance which provides support for the acceptance of H1a. Likewise, the Engineering and Computer education of directors has positive and significant (at 10%) relationship with firm value, thus, the proposed relationship in H1b is proved. While in this research, the financial education of board members failed to prove a connection with firm performance, hence, H1 c is not proved and accepted in this study. However, MBA degree holders have a significant positive contribution to the firm value which leads to the acceptance of hypothesized relationship in H1d, this study has no evidence for the relationship of directors’ other education with performance, therefore, H1e is rejected.

Moreover, gender diversity in this study negatively and significantly influence the firm value. Ahern and Dittmar (Citation2012) research claimed that the presence of female directors on board leads to lower firm value. There are many reasons behind this negative relationship such as most of the female directors on board of the sample firms have close ties with the owners which restrict their ability to perform independently. Another possible reason for the negative relationship is that the number of female directors on board is very limited and voice of minority members in most of the firms is ignored (Carter et al., Citation2010).

Moreover, the national heterogeneity significantly enhances the firm value, as the results of OLS regression analysis indicate that coefficient (0.4220) of national heterogeneity is positive and significant at 5% level of significance. These findings illustrate that a nationally diverse board is rich in knowledge of various markets as well as foreign directors onboard bring an abundance of resources required in firms (Zaid et al., Citation2020). It is in favor of resource dependence theory of the firm which asserted that humans are a source of unique resources that help organizations to compete successfully (Haynes & Hillman, Citation2010). Additionally, two control variables added in regression describe that firm size and firm age both have a significant connection with firm performance as already discussed in the univariate analysis that board diversity varied in small and large firms. Moreover, the relationship between firm size and performance is confirmed in the existing literature of firm performance (Arena et al., Citation2015). The following section concludes the whole study.

5. Conclusion and recommendation

Regression results in the current research favored the upper echelon and resource dependence preposition that occupational heterogeneity influences the cognitive capabilities of directors and their decision-making ability. Hence, in this research, educational heterogeneity as a proxy of occupational heterogeneity remains positive and significant as reported in previous studies. Moreover, the direction of the relationship between directors’ educational backgrounds and firm performance is positive but only few chosen educational backgrounds significantly load on firm performance. As the relationship between finance specialization and directors’ other education is not proved to have a significant effect on firm performance in this study, directors with finance education are only few in numbers and their prime focus is to ensure the audit quality and financial disclosure. Likewise, in most of the sample firms, a board comprised the majority of high ranked retired army staff with an education degree in defense and other disciplines; such degrees are not much beneficial in civil manufacturing organizations. Therefore, other education (defense, arts, political science etc.) has no significant effect on firm performance.

This research also points out some of the sever issues of gender heterogeneity as gender diversity has been negatively influenced firm performance in this study. Characteristics of sample firms show that only family control firms have women directors on board and such females have strong family relations with the owners. Since such nepotism negatively affects the independence of the board and the quality of its decisions. On the contrary, national diversity has a positive and significant association with firm because foreign directors bring finance and own large shareholdings, such complex association of foreign directors encourages them to critically observe board activities. It is also evident that large firms tend to have more foreign directors. This study also concluded that considering only agency perspectives for organization’s performance is not reliable in a current business environment, for this, scholars must consider other aspects of humans capital (i.e. resource-based view and upper echelon).

This study has numerous practical implications for sample firms to improve their performance and to have access to copious resources. This research suggests that foreign directors not only bring unique resources to firms, they also increase the independence of the board and its decision-making credibility. Moreover, the firms should appoint the independent women directors on board rather have female directors from the owner’s family; as such favoritism is injurious to the firm.

Despite the significance of the research, this study has several points which are out of its scope. These points can be covered in future research. For instance, due to the unavailability of data on age, tenure and experience, this research does not include this type of heterogeneity in this study. However, in future this limitation can be considered by using primary data, and which can be an interesting expansion of the study. Moreover, this study only graphically compared the small and large firms; future scholars can make an in-depth analysis using compare means or other relevant methodological analysis of small and large firms.

Additional information

Funding

Notes on contributors

Farheen Akram

Dr. Farheen Akram has completed her PhD (Banking & Finance) from Universiti Utara Malaysia. She served as an assistant professor in several universities in Pakistan and Kingdom of Bahrain. Her research interest lies in corporate governance, business innovation, green finance and firm performance.

Muhammad Abrar ul Haq

Dr. Muhammad Abrar ul Haq working as an assistant professor at College of Administrative & Financial Sciences, AMA International University-Bahrain. He has done his PhD (Economics) from Universiti Utara Malaysia. His research interest includes, but not limited to: development economics, welfare economics, empowerment and poverty.

Vinodh K Natarajan

Dr. Vinodh K Natarajan currently working as an Associate Dean in AMA International University-Bahrain. He has done his PhD in Economics and graduated with a master’s degree in international economics and Finance from Cardiff Business School, UK.

R. Stephen Chellakan

Dr. R Stephen Chellakan serves as an Assistant Professor in the College of Administrative and Financial Sciences, AMA International University-Bahrain. He has done his PhD in Economics from Manonmaniam Sundaranar University, India.

References

- Adams, R. B., & Ferreira, D. (2009). Women in the boardroom and their impact on governance and performance. Journal of Financial Economics, 94(2), 291–14. https://doi.org/10.1016/j.jfineco.2008.10.007

- Adams, R. B., Haan, J., Terjesen, S., & Ees, H. (2015). Board diversity: Moving the field forward. Corporate Governance: An International Review, 23(2), 77–82. https://doi.org/10.1111/corg.12106

- Adusei, M., Akomea, S. Y., & Poku, K. (2017). Board and management gender diversity and financial performance of microfinance institutions. Cogent Business & Management, 4(1), 1360030. https://doi.org/10.1080/23311975.2017.1360030

- Ahern, K. R., & Dittmar, A. K. (2012). The changing of the boards: The impact on firm valuation of mandated female board representation. Quarterly Journal of Economics, 127(1), 137–197. https://doi.org/10.1093/qje/qjr049

- Ahmed Sheikh, N., & Wang, Z. (2012). Effects of corporate governance on capital structure: Empirical evidence from Pakistan. Corporate Governance: The International Journal of Business in Society, 12(5), 629–641. https://doi.org/10.1108/14720701211275569

- Ameer, R., Ramli, F., & Zakaria, H. (2010). A new perspective on board composition and firm performance in an emerging market. Corporate Governance: The International Journal of Business in Society, 10(5), 647–661. https://doi.org/10.1108/14720701011085607

- Anderson, R. C., Reeb, D. M., Upadhyay, A., & Zhao, W. (2011). The economics of director heterogeneity. Financial Management, 40(1), 5–38. https://doi.org/10.1111/j.1755-053X.2010.01133.x

- Arena, C., Cirillo, A., Mussolino, D., Pulcinelli, I., Saggese, S., & Sarto, F. (2015). Women on board: Evidence from a masculine industry. Corporate Governance: The International Journal of Business in Society, 15(3), 339–356. https://doi.org/10.1108/CG-02-2014-0015

- Athmen, B., & Samia, B. (2017). The importance of human resources in corporate governance. Mediterranean Journal of Social Sciences, 8(4–1), 161–164. https://doi.org/10.2478/mjss-2018-0086

- Ayuba, H., Bambale, A. J. A., Ibrahim, M. A., & Sulaiman, S. A. (2019). Effects of financial performance, capital structure and firm size on firms’ value of insurance companies in Nigeria. Journal of Finance, Accounting & Management, 10(1), 57-74. https://www.questia.com/read/1P4-2182400212/effects-of-financial-performance-capital-structure

- Bøhren, Ø., & Staubo, S. (2014). Does mandatory gender balance work? Changing organizational form to avoid board upheaval. Journal of Corporate Finance, 28(5), 152–168. https://doi.org/10.1016/j.jcorpfin.2013.12.005

- Burke, J. J., Hoitash, R., & Hoitash, U. (2019). The heterogeneity of board-level sustainability committees and corporate social performance. Journal of Business Ethics, 154(4), 1161–1186. https://doi.org/10.1007/s10551-017-3453-2

- Campbell, K., & Mínguez-Vera, A. (2008). Gender diversity in the boardroom and firm financial performance. Journal of Business Ethics, 83(3), 435–451. https://doi.org/10.1007/s10551-007-9630-y

- Carter, D. A., D’Souza, F., Simkins, B. J., & Simpson, W. G. (2010). The gender and ethnic diversity of US boards and board committees and firm financial performance. Corporate Governance: An International Review, 18(5), 396–414. https://doi.org/10.1111/j.1467-8683.2010.00809.x

- Darmadi, S. (2013). Do women in top management affect firm performance? Evidence from Indonesia. Corporate Governance: The International Journal of Business in Society, 13(3), 288–304. https://doi.org/10.1108/CG-12-2010-0096

- Dobbin, F., & Jung, J. (2011). Board diversity and corporate performance: Filling in the gaps: Corporate board gender diversity and stock performance: The competence gap or institutional investor bias. North Carolina Law Review, 89(3), 809–839

- Hambrick, D. C., & Mason, P. A. (1984). Upper echelons: The organization as a reflection of its top managers. Academy of Management Review, 9(2), 193–206. https://doi.org/10.5465/amr.1984.4277628

- Hassan, L. S., Saleh, N. M., & Ibrahim, I. (2020). Board diversity, company’s financial performance and corporate social responsibility information disclosure in Malaysia. International Business Education Journal, 13(1), 23–49. http://ejournal.upsi.edu.my/index.php/IBEJ/article/download/3153/2313

- Haynes, K. T., & Hillman, A. (2010). The effect of board capital and CEO power on strategic change. Strategic Management Journal, 31(11), 1145–1163. https://doi.org/10.1002/smj.859

- Herrmann, P., & Datta, D. K. (2005). Relationships between top management team characteristics and international diversification: An empirical investigation. British Journal of Management, 16(1), 69–78. https://doi.org/10.1111/j.1467-8551.2005.00429.x

- Heyden, M. L., Oehmichen, J., Nichting, S., & Volberda, H. W. (2015). Board background heterogeneity and exploration‐exploitation: The role of the institutionally adopted board model. Global Strategy Journal, 5(2), 154–176. https://doi.org/10.1002/gsj.1095

- Hoechle, D. (2007). Robust standard errors for panel regressions with cross-sectional dependence. The Stata Journal: Promoting Communications on Statistics and Stata, 7(3), 281–312. https://doi.org/10.1177/1536867X0700700301

- Hutzschenreuter, T., & Horstkotte, J. (2013). Performance effects of top management team demographic faultlines in the process of product diversification. Strategic Management Journal, 34(6), 704–726. https://doi.org/10.1002/smj.2035

- Joecks, J., Pull, K., & Vetter, K. (2013). Gender diversity in the boardroom and firm performance: What exactly constitutes a “critical mass?”. Journal of Business Ethics, 118(1), 61–72. https://doi.org/10.1007/s10551-012-1553-6

- Julizaerma, M., & Sori, Z. M. (2012). Gender diversity in the boardroom and firm performance of Malaysian public listed companies. Procedia-Social and Behavioral Sciences, 65, 1077–1085. https://doi.org/10.1016/j.sbspro.2012.11.374

- Khan, A. W., & Abdul Subhan, Q. (2019). Impact of board diversity and audit on firm performance. Cogent Business & Management, 6(1), 1611719. https://doi.org/10.1080/23311975.2019.1611719

- Kim, K.-H. (2014). Board heterogeneity: Double-edged sword? Focusing on the moderating effects of risk on heterogeneity-performance linkage. Academy of Strategic Management Journal, 13(1), 129. http://electronic-businessjournal.com/images/2014/2014-9/3.pdf

- Lehn, K. M., Patro, S., & Zhao, M. (2009). Determinants of the size and composition of US corporate boards: 1935‐2000. Financial Management, 38(4), 747–780. https://doi.org/10.1111/j.1755-053X.2009.01055.x

- Mahadeo, J. D., Soobaroyen, T., & Hanuman, V. O. (2012). Board composition and financial performance: Uncovering the effects of diversity in an emerging economy. Journal of Business Ethics, 105(3), 375–388. https://doi.org/10.1007/s10551-011-0973-z

- Masulis, R. W., Wang, C., & Xie, F. (2012). Globalizing the boardroom—The effects of foreign directors on corporate governance and firm performance. Journal of Accounting and Economics, 53(3), 527–554. https://doi.org/10.1016/j.jacceco.2011.12.003

- Midavaine, J., Dolfsma, W., & Aalbers, R. (2016). Board diversity and R & D investment. Management Decision, 54(3), 558–569. https://doi.org/10.1108/MD-09-2014-0574

- Nielsen, B. B., & Nielsen, S. (2013). Top management team nationality diversity and firm performance: A multilevel study. Strategic Management Journal, 34(3), 373–382. https://doi.org/10.1002/smj.2021

- Oxelheim, L., & Randøy, T. (2003). The impact of foreign board membership on firm value. Journal of Banking & Finance, 27(12), 2369–2392. https://doi.org/10.1016/S0378-4266(02)00395-3

- Peck-Ling, T., Nai-Chiek, A., & Chee-Seong, L. (2016). Foreign ownership, foreign directors and the profitability of Malaysian Listed Companies. Procedia-Social and Behavioral Sciences, 219(1), 580–588. https://doi.org/10.1016/j.sbspro.2016.05.037

- Robb, A. M., & Watson, J. (2012). Gender differences in firm performance: Evidence from new ventures in the United States. Journal of Business Venturing, 27(5), 544–558. https://doi.org/10.1016/j.jbusvent.2011.10.002

- Talavera, O., Yin, S., & Zhang, M. (2018). Age diversity, directors’ personal values, and bank performance. International Review of Financial Analysis, 55(1), 60–79. https://doi.org/10.1016/j.irfa.2017.10.007

- Taljaard, C. C., Ward, M. J., & Muller, C. J. (2015). Board diversity and financial performance: A graphical time-series approach. South African Journal of Economic and Management Sciences, 18(3), 425–447. https://doi.org/10.4102/sajems.v18i3.926

- Torchia, M., Calabrò, A., & Huse, M. (2011). Women directors on corporate boards: From tokenism to critical mass. Journal of Business Ethics, 102(2), 299–317. https://doi.org/10.1007/s10551-011-0815-z

- Tsui, A. S., Egan, T. D., & O’Reilly, C. A., III. (1992). Being different: Relational demography and organizational attachment. Administrative Science Quarterly, 37(4), 549–579. https://doi.org/10.2307/2393472

- Tuggle, C. S., Schnatterly, K., & Johnson, R. A. (2010). Attention patterns in the boardroom: How board composition and processes affect discussion of entrepreneurial issues. Academy of Management Journal, 53(3), 550–571. https://doi.org/10.5465/amj.2010.51468687

- Veltrop, D. B., & Molleman, E. (2019). Board informal hierarchy and board performance research Handbook on boards of directors. Edward Elgar Publishing.

- Williams, K. Y., & O’Reilly, C. A., III. (1998). Demography and diversity in organizations. A review of 40 years of research. Research in Organizational Behavior, 20(20), 77–140. https://www.researchgate.net/profile/Charles_OReilly/publication/234022034_Demography_and_Diversity_in_Organizations_A_Review_of_40_Years_of_Research/links/55b0f45d08aec0e5f430e49e/Demography-and-Diversity-in-Organizations-A-Review-of-40-Years-of-Research.pdf

- Zaid, M. A., Wang, M., Adib, M., Sahyouni, A., & Abuhijleh, S. T. (2020). Boardroom nationality and gender diversity: Implications for corporate sustainability performance. Journal of Cleaner Production, 251, 119652. https://doi.org/10.1016/j.jclepro.2019.119652