Abstract

The impact of intellectual capital on firm performance is one of the key aspects of strategic management. This is particularly crucial for firms in the high-tech or service sectors. Intellectual capital dimensions, including human, organisational and social capital, are key to developing outstanding performance. From a strategic management perspective, there are still debates on the interrelationships between these dimensions, and on the moderating role of environmental uncertainty on their impacts on performance. In the context of an unstable environment like Vietnam, this study involved a survey of 350 information communication technology (ICT) firm’s directors and managers, which was used to analyse the impacts of intellectual capital dimensions on firm performance, the indirect effects of organisational capital on performance via human and social capital, and the moderating role of environmental uncertainty. Findings indicate that all dimensions of intellectual capital had direct impacts on firm performance. In addition, we found that the human and social capital mediated significantly the relationship between firm performance and organisational capital, and the environmental uncertainty moderated significantly the relationship between intellectual capital dimensions and firm performance.

PUBLIC INTEREST STATEMENT

Intellectual capital is currently a topical issue, especially in developing countries where firms are seeking for ways to improve efficiency in business operation. However, this has not been achieved given the fact that most of the managers in those countries do not understand the impact of the environmental uncertainty on the relationship between intellectual capital dimensions on firm performance. Due to its complexity and the higher costs involved in the development of the intellectual capital. This study, therefore, suggests that in improvement in intellectual capital development will lead positive impact on firm performance, especially in ICT sector.

1. Introduction

Information communication technology (ICT) has an increasingly large impact on economic and social lives (VietNamNet, Citation2020). The development of ICT enables “information societies” of over 3 billion people to access the Internet, of which 8 of 10 Internet users own a smartphone (VietNamNet, Citation2020). The demand for ICT services is increasing by leaps and bounds (VietNamNet, Citation2020). This rapid growth has led ICT to become one of the main drivers of economic growth, as well as a keystone of daily life in many countries; Vietnam is included in this movement. Vietnam’s ICT sector grew substantially during 2010–2016, and total 2016 revenue reached 59.9 USD billion USD, as Vietnam emerges as a production centre for ICT hardware and software products and services (VietNamNet, Citation2020). The government of Vietnam has increasingly recognized the important impacts of ICT industry on social and economic activities, and has recently devised a master plan for ICT which is called the “Taking-off strategy”, which specifies targets for 2020 and aims to continue the transformation of Vietnam into an advanced ICT country (VietNamNet, Citation2020). However, unlike other manufacturing industries in term of inputs, firm size, management knowledge, ICT involves short product life cycles, high customer demand, and very unpredictable technological changes. Thus, acquiring and managing “valuable, rare, inimitable, and non-substitutable” (VRIN) sources like intellectual capital are very important to achieve outstanding performance (Cao & Wang, Citation2015). To follow the worldwide ICT trend, ICT firms that survive and grow in a highly competitive and uncertain institutional environment must increase their efforts in intellectual capital development. Intellectual capital is often referred to as the value created by three types of intangible resources: that is, human capital such as individuals’ knowledge, skill and education; organisational capital including all non-human knowledge containers (e.g., information and communication systems, databases, process manuals, strategies, routines); and social capital, which refers to the social relationships of an organisation, as well as individual relationships with customers, investors, competitors, or suppliers (Dadfar et al., Citation2013). Western empirical research on intellectual capital are popular but have built on the assumption that intellectual capital is the key source of superior performance. There are very few studies conducted in developing countries that validate or operationalize this assumption where the business environment is very unstable, such as Vietnam. Therefore, in the context of Vietnam’s ICT industry, it is beneficial to examine environmental uncertainty as a moderator in the relationship between intellectual capital dimensions and firm performance.

This research can make several contributions to the strategic management literature, as follows. First, this study extends the existing literature by offering insights into the relevance of human, organisational, and social capital in achieving ICT firms’ outstanding performance in unstable environment like Vietnam. Second, it advances existing studies in this field by explicitly discussing how organisational capital effects the development of human and social capital, which lead in turn to outstanding performance. Lastly, it measures and evaluates the moderating effects of environmental uncertainty on the indirect relationship between organizational capital and firm performance (through human and social capital). In sum, this research builds and validates a conceptual model of the interrelationships among intellectual capital dimensions, environmental uncertainty, and firm performance, and then suggests how to use effectively the outcome of model tests.

2. Literature review

2.1. Firm performance

Firm performance has been examined by academia for a considerable time as a way to measure the health of a firm. The reliability and validity of measurements of performance are critical for empirical studies. From an initial reliance on purely financial perspectives, firm performance measurement has gradually extended to consider multiple dimensions. Venkatraman and Ramanujam (Citation1986) proposed that firm performance should be measured in terms of financial and operational aspects. Financial performance is measured by indicators such as sales growth, earnings per share, profitability, efficiencies and effectiveness which is reflected by return on investment, return on sales and return on equity (Taouab & Issor, Citation2019). However, operational (or non-financial) performance emphasizes indicating factors such as product quality and productivity, market share and marketing effectiveness (Demirbag et al., Citation2006). To ensure that firm performance is measured accurately, Dess and Robinson (Citation1984) recommended that firms should employ both financial and operational performance measurement indicators: utilizing multiple indicators enables firms to measure performance via more complex and informative measures, and to assess the contribution of each indicator to the latent variable.

2.2. Resource-based view (RBV)

Knowledge on how to manage effectively intellectual capital is vital, especially in sectors that are innovation oriented and non-manufacturing, and thus possess more intangible than tangible resources (Zeglat & Zigan, Citation2013). ICT sector is part of the service sector, and thus possesses intangible, intellectual capital resulting from the knowledge, experience, and skills of employees, as well as processes, information systems, and customer relationships. One may argue that, with strong intangible resources, ICT can achieve sustainable advantages, and differentiate themselves from competitors (Mathews, Citation2019). For this reason, the current study uses a resource-based view (RBV) as its theoretical framework. RBV is an economic tool used to determine the strategic resources available to a firm: looking closely at a company’s resources enables a firm to strategically improve its efficiency and effectiveness, especially by identifying rare resources that crucial to superior performance are, but which are rare, irreplaceable, imperfectly imitable, difficult to implement, and not available to competitors (Wernerfelt, Citation1984). Therefore, it is argued here that the management and development of intellectual capital are vital to ICT firm’s strategic management and performance.

2.3. Intellectual capital

The first definition of intellectual capital was suggested by an economist, John Kenneth Galbraith, in 1969. Galbraith believed that intellectual capital is not only an intangible asset but also an ideological process (Edvinsson & Sullivan, Citation1996; Huang & Wu, Citation2010). Other scholars suggest that intellectual capital is the accumulation of all knowledge, information, intellectual property, experiences, social networks, capabilities and competencies that enhance organisational performance—not only as held by individuals, but also as embedded in business processes (Subramaniam & Youndt, Citation2005). Rastogi (Citation2003) offered a comprehensive definition describing intellectual capital “as the holistic or meta-level capability of a company to coordinate, orchestrate and deploy its knowledge resources toward creating value in pursuit of its future vision”. Over the past years, the concept of intellectual capital has been defined in multiple ways, often resulting in a lack of consensus regarding its components (Choo Huang et al., Citation2010). A synthesises of extant academic discussions argues that a widely applicable definition of intellectual capital should have three dimensions: human, organisational and social capital (Aramburu & Saenz, Citation2011; Hsu & Fang, Citation2009; Phusavat et al., Citation2011; Sharabati et al., Citation2010).

2.4. Environmental uncertainty

The concept of uncertainty has been a central variable in many studies focusing on the features of the relationship between firm performance and its internal and external effects (Yu et al., Citation2016). Environmental uncertainty is a situation that cannot be predicted (Latan et al., Citation2018). With a rising frequency of environmental dynamism and complexity in business operations, firms are operating in environments that are becoming increasingly unpredictable. Therefore, the management (i.e., reduction or avoidance) of uncertainty is one of the main tasks of a successful business. Uncertainty includes macro-environmental, competitive, customer demand and technological dimensions. “Macro-environmental” uncertainty includes political, regulatory, and economic conditions, and may weaken an organisation’s capacity to map and pursue strategic choices (Miller & Friesen, Citation1984). “Competitive” uncertainty reflects the intensity of competition and the relative powers of competitors, as well as competitors’ strategies and future courses of action (Tushman & Anderson, Citation1986). “Customer demand” uncertainty is caused by the lack of clarity in market information, and by supply-and-demand imbalances in the industry (Tushman & Anderson, Citation1986). “Technological” uncertainty links to unpredictable and continuous trends in the technology (Tushman & Anderson, Citation1986).

3. Hypothesis development

3.1. The impact of human, organizational and social capital on firm performance

Embedded in employees, “human” capital may be defined as the summation of abilities, skills, attitudes, commitments, experience and educational background of employees, which enables them to act in ways which are economically valuable to both individuals and to their firm (Shih et al., Citation2010). Human capital brings value to the company as a criterion of competency and creativity possessed by employees, which allows them to identify business opportunities, to create new knowledge, and to solve problems (Boon et al., Citation2018). Firms do not possess human capital directly, but rather lease the acquired knowledge, skills and experiences of employees. The quality of human capital available to a firm is influenced by hiring practices and training activities (Gilbert et al., Citation2017). The economic value of human capital is dependent on how effectively the employer is able to use and develop it. Therefore, scholars have confirmed that it is deemed to be the most important intangible resource for the development of the firm itself, especially in innovative sectors such as ICT. Hence, the first hypothesis proposed here is:

H1: Human capital has positive and significant influences on firm performance

Organisational capital is defined as the institutionalized knowledge and codified experiences preserved in organisational images, culture, routines, procedures, information systems and patents (Gilbert et al., Citation2017), and as such is a strategic intangible asset. The purpose of organisational capital is to coordinate communication and action between individuals in an organisation (Gilbert et al., Citation2017). From a review of the literature, scholars suggest three distinct dimensions of organisational capital: (a) structural, (b) cultural and (c) knowledge dimensions (Gilbert et al., Citation2017). The first “structural” dimension includes the formal procedures and processes of the organisation providing decision-making guidelines. This also includes human resource policies and guidelines for labour management practices such as hiring, tasking, staffing and disciplinary actions (Gilbert et al., Citation2017; Nahapiet & Ghoshal, Citation1998; Nonaka & Von Krogh, Citation2009). The “cultural” dimension accounts for processes serving the long-term strategies of a firm. This includes formal objectives, strategic plans, missions, values, and vision (Djuric & Filipovic, Citation2015), organisational culture and traditions (Asiaei & Jusoh, Citation2015; Baughn et al., Citation2011; Dess & Shaw, Citation2001) and conceptions of corporate social responsibility (Ferreira-Lopes et al., Citation2012). The “knowledge” dimension of organisational capital accounts for processes through which knowledge and information is created, utilized, exchanged and preserved, including investment in research and development (Youndt et al., Citation2004), as well as copyrights and patents (Ellinger et al., Citation2011).

As compared to human and social capital, organisational capital is the least flexible (Gilbert et al., Citation2017). Even major ICT firms are of small and medium size, and thus are able to develop organisational capital that is less hierarchical in nature, and that allows for the autonomy and independence in decision making necessary to increase innovation and absorb new knowledge. Based on these arguments, hypothesis is proposed as the following:

H2: Organisational capital positively relates to firm performance

The relevant literature acknowledges that the influence of social capital on firm performance has been increasing (Kianto et al., Citation2013). However, the concept of social capital has been much debated in terms of definition, measurement, and operationalisation (Hsu et al., Citation2011). So far, scholars have proposed three distinct theoretical perspectives of social capital: functional, network and multidimensional perspectives (Gilbert et al., Citation2017). The “functional” perspective developed, as by Coleman (Citation1988) and Putnam (Citation1993) defines social capital as a functional resource that enhances collaboration among individuals in an organisation. The “network” perspective of social capital theory, as suggested by Bourdieu (Citation2011), defines social capital as resources embedded in social networks in which individuals or organisations are members: when member’s network is expanded and trust is established, members are more willing to share intellectual resources within the network and, in turn, more motivated to participate in knowledge-exchange activities. The third perspective, the “multidimensional” perspective, was developed by synthesizing the functional and network perspectives (Gilbert et al., Citation2017), and conceptualizes social capital as a resource both inherent in a network and as a resource facilitating action among network members that it is available for productive purposes (Grootaert, Citation2004). In general, social capital encompasses the context, stock of relationships, interpersonal trust, and shared norms that allow certain behaviours and sustainable relationships between individuals and ensure favourable conditions for organisational development and knowledge exchanges (Donate et al., Citation2019). Hence, how social capital enables the access, processing, synthesis, and exchange of knowledge within and across organisations will significantly impact performance, especially in knowledge-based organisations like ICT firms. From this, we hypothesize the following:

H3: Social capital positively relates to firm performance

3.2. The impact of organisational capital on human and social capital development, and the mediating role of organisational capital

Investment in research and development (R&D) (i.e., a type of investment in organisational capital) is fundamental for the creation of new knowledges, products and services. R&D investment activities increase the opportunities and avenues for organisational members to identify and apply technology in products and services (Zack et al., Citation2009). This also improves members’ own understanding and learning about new knowledge and technologies (Youndt et al., Citation2004). Accordingly, the more an organization invests in R&D, the more it supports member individuals as they enhance their expertise, knowledge. Thus, this form of investment in organisational capital builds human capital.

The other major type of investment in organisational capital is the provision for regular employee training. It is broadly accepted that firms can increase their human capital by providing comprehensive training activities to current employees. Training activities that focus on developing personal knowledge and skills may not only increase employees’ human capital, but also help employees to maximize social capital by building relationships and sharing knowledge with their colleagues (Tseng et al., Citation2014). Likewise, as individuals learn and increase their human capital, they may create knowledge that potentially forms the foundation for organisational learning and knowledge accumulation (Youndt et al., Citation2004).

Investment in information systems (IS) is also important for human and social capital. There is a general consensus that IS represents the infrastructure of many organisations (Youndt et al., Citation2004). At a primary level, IS creates repositories where knowledge can be codified and institutionalized; IS investments also enable the creation and diffusion of knowledge from and across dispersed and globalized sources (Youndt et al., Citation2004). Today, computer networks (a type of IS) remove physical and temporal limitations to communication and connect people to create online social networks (Youndt et al., Citation2004). These online connections enhance cooperation, and the sharing of knowledge not only among employees within a firm, but also across multiple firms (Youndt et al., Citation2004).

The fourth and last major type of investment in organisational capital is investment in organisational culture. A significant body of literature regards organisational culture as having an important impact on the development of the components of intellectual capital, especially on human and social capital (Ellinger et al., Citation2002; Kostopoulos et al., Citation2015). Mouritsen et al. (Citation2001) argued that organisational culture is pivotal to realising the value of intellectual capital. Guthrie et al. (Citation2004) advocate that corporate culture is crucial toward a firm’s success and is capable of increasing intellectual capital within that firm. Different kinds of organisational culture would have different impacts on intellectual capital—developing the type of organisational culture that allows flexibility, openness, quick adaptability, and responsiveness is appropriate for knowledge-based organisations like ICT firms, and is an important driver for supporting the development of the components of intellectual capital, especially human and social capital (Gilbert et al., Citation2017). From the above arguments, the following hypotheses are proposed:

H4: Investment on organisational capital positively affects human capital

H5: Investment on organisational capital positively affects social capital

H6: Organisational capital mediates the relationship between social capital and firm performance

H7: Organisational capital mediates the relationship between human capital and firm performance

3.3. The moderation effect of the environmental uncertainty

The nature, source, and extent of environmental uncertainty will have clear impacts on firms’ strategic management and development. The current study proposes a measurement technique for a given uncertainty construct. It begins by establishing different levels of the extent of environmental uncertainty as (a) low uncertainty or (b) high uncertainty (Jabnoun et al., Citation2003). In “low uncertainty” environments, changes are relatively small and causes are fairly predictable (Jabnoun et al., Citation2003). When environmental changes are insignificant, firms are little motivated to improve firm performance; in such environments, physical resources suffice to achieve business processes efficiently, with minimal reconfiguration, customization and updates; intellectual capital has few opportunities to demonstrate its importance in term of acquiring and sustaining competitive advantages (Jabnoun et al., Citation2003). In contrast, environments with high degrees of uncertainty are characterized by unpredictable changes, and unclear relationships between environmental components and the organisation; in such contexts, intellectual capital and intangible resources demonstrate more flexibility than physical resources, and should be dynamically managed to achieve superior performance (Jabnoun et al., Citation2003). In such environments, firms in traditional industries may quickly become incompatible with new business requirements, and their tangible resources may become obsolete; consequently, such firms are no longer able to sustain good performance—whereas high-tech firms are managed dynamically, and are agile enough to reconfigure their existing intellectual capital and acquire new capital to cope with external changes (Jabnoun et al., Citation2003). Therefore, these additional hypotheses are proposed:

H9: Environmental uncertainty significantly moderate the effects of human capital on firm performance

H10: Environmental uncertainty significantly moderates the effects of organisational capital on firm performance.

H11: Environmental uncertainties significantly moderates the effects of social capital on firm performance

In addition, it is assumed here that the environmental uncertainty may have conditional impacts on the strength of indirect relationships between the organisational capital and firm performance. In other words, the mediating effects of organisational capital on firm performance may be moderated by environmental uncertainty, thereby demonstrating a moderated mediation effect. The paper proposes that a strong indirect influence of the organisational capital on firm performance when the moderating degree of environmental uncertainty are high. Therefore, the following hypotheses are presented:

H12: Human capital positively mediates the indirect relationship between organisational capital when the moderating effect of environmental uncertainty is high.

H13: Social capital positively mediates the indirect relationship between organisational capital when the moderating effect of environmental uncertainty is high.

4. Model formulation

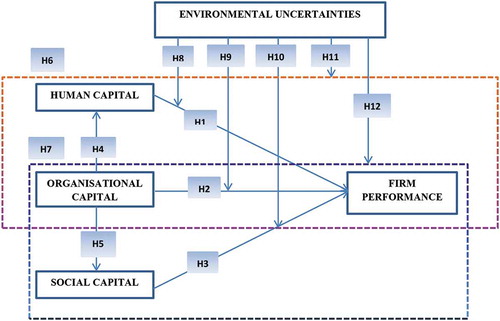

Based on the above theoretical backgrounds and hypotheses, the paper proposes the following integrated model (Figure )

Figure 1. Research model.

5. Methodologies

5.1. Data collection and respondent characteristics

A survey of ICT firms in Ho Chi Minh City and Ha Noi was conducted. The majority of firms are 5 years old or younger. The targeted respondents were directors, project managers and senior managers who represented the best source of information for our study. Eventually, 370 responses were directly collected from 450 distributed questionnaires. After excluding missing data and outliers based on boxplot analyses, 350 responses were retained for analysis. Table presents the demographic information of respondents in the research sample.

Table 1. The demographic information of respondents in the research sample

5.2. Measurement scales

The questionnaire was developed from validated scales to ensure content validity; however, due to the predominantly Vietnamese setting, the survey was translated into Vietnamese, with the help of two academic domain experts fluent in Vietnamese and proficient in English. The questionnaire was pre-tested in meetings with 10 academic domain experts and 10 senior managers from Vietnamese ICT firms. The purpose of the pre-test was to evaluate the content validity of the translated measures, and whether the respondent understood the instructions, items and scales.

To measure the intellectual capital dimensions, firm performance and environmental uncertainty, 5-point Likert-scale items ranging from ‘1ʹ (strongly disagree or strong dissatisfaction) to ‘5ʹ (strongly agree or strong satisfaction) were created. (All items are reported in detail in Appendix A.) This is the simple sum or average of questionnaire responses over the set of individual items (questions). In so doing, Likert scaling assumes distances between each choice (answer option) are equal. The measurement of the three dimensions of intellectual capital (human, organisational and social capital) was mainly derived from measurement scales developed by Subramaniam and Youndt (Citation2005). Firm performance measurements were adapted from scales used, developed and validated by Wiklund and Shepherd (Citation2003). Environmental uncertainty measurement scales were developed based on the basis of studies by Atuahene-Gima and Murray (Citation2004).

6. Results

6.1. The result of the construct reliability and validity evaluation

We began tests with Cronbach alpha (α) for reliability analysis in order to measure the internal consistency of the measurement scales (Hair et al., Citation1998). Acceptable values of α are above 0.6 (Hair et al., Citation1998): the α of human, social and organisational capital were 0.89, 0.90 and 0.60, representing reasonable scale reliability. For firm performance and environmental uncertainty, α was 0.61 and 0.70, also represent good scale reliability. Next, we used an exploratory factor analysis (EFA) technique to conduct dimensionality analyses as indicated by factor loading score. The general purpose of factor analysis techniques is to condense the information contained in an original construct into smaller set of new composite dimensions or factors (Hair et al., Citation1998). All factor loading scores meeting a suggested level of 0.5 satisfy the condition of unidimensionality (Hair et al., Citation1998). In this study, with an original set of 35 measurement items, there were only 23 items which qualified with a factor loading score of 0.5, with a minimum score of 0.677.

6.2. The result of convergent and discriminant validity evaluation

Confirmatory factor analysis (CFA) is a statistical technique used to verify the factor structure of a set of observed variables. CFA allows the researcher to test the hypothesis that a relationship between observed variables and their underlying latent constructs exists. To test the hypothesis that a relationship between observed variables and their underlying latent constructs exists, confirmatory factor analyses (CFA) were conducted to assess how the conceptual model fit data with the help of AMOS software version 23. Regarding overall model fitness, to make sure data fit well to model, the root means square error of approximation (RMSEA) should be smaller than or equal to 0.08 (Hair et al., Citation1998). Goodness-of-fit index (GFI), and Comparative fit index (CFI) should satisfy thresholds of 0.9 (Hair et al., Citation1998). Our test results show an acceptable fit for data set (GFI = 0.9, CFI = 0.91 and RMSEA = 0.08). Further, we used a CFA technique to test convergent and discriminant validity. We checked all average variances extracted (AVEs) and composite reliabilities (CRs). All AVEs were higher the suggested level of 0.5, and CRs were also above the proposed level of 0.7 (Hair et al., Citation1998). Therefore, convergent validity was satisfied. For the test of the discriminant validity, Cheung et al. (Citation2010) suggested that if the AVE of each construct is larger than the squared correlation coefficient of that construct compared with any other construct in the model, constructs indeed are different from one another. The test result in Table demonstrates that all constructs carry sufficient discriminant validity.

Table 2. The test result demonstrates that all constructs carry sufficient discriminant validity

6.3. Hypotheses verification

In the hypothesis verification step, we tested all hypotheses using process software. Collectively, H1, H2, H3, H4 and H5 represent direct individual effects, H6 and H7 represent indirect effects whereby the association between organisational capital and firm performance is mediated by human and social capital, respectively. Such mediated effects were tested using a bootstrapping analysis: a powerful method for determining the statistical significance of mediation to confirm a significant indirect effect as proposed by Preacher and Hayes (Citation2013). In H9, H10 and H11, we assumed the moderating effect of environmental uncertainty on the relationship between human, social and organisational capital and firm performance. In H12 and H13, we assumed as the moderating effect of environmental uncertainty on indirect effect of organisational capital on firm performance via human and social capital. Such moderated and moderated mediation effects were tested by hierarchical regression analysis.

6.3.1. The tests of the direct and indirect effects

The study adopted Hayes’s suggestion to test direct and indirect effects (H1, H2, H3, H4, H5, H6 and H7). At first, organisational, human and social capital should be regressed on firm performance. The results in Table showed that organisational (β = 0.308, p < 0.001) and human capital (β = 0.28, p < 0.001) were positively related to firm performance, while social capital were less positively related to firm performance than two other dimensions (β = 0.0983, p < 0.05). Thus, H1, H2 and H3 are statistically supported. Organisational capital is positively related to human and to social capital ((β = 0.2630, p < 0.01) and (β = 0.404, p < 0.001), respectively), so H4 and H5 are supported. Based on the test outcomes above, the study confirms that there are no full mediation effects in this model: full mediation effects will occur if organisational capital has no direct influence on firm performance (Hayes, Citation2009). Therefore, there may be only partial mediation effects of human and social capital on the relationship between organisational capital and firm performance. The test outcomes showed that the partial mediation effects of human and social capital are confirmed ((β = 0.0755, p < 0.001) and (β = 0.0680, p < 0.001)), so H6 and H7 are supported.

Table 3. Regression analysis of moderating effects

6.3.2. Moderation and moderated mediation effect of environmental uncertainty

H8, H9 and H10 postulated that the influence of human, social and organisational capital would be positive for firm performance in conditions of high degrees of environmental uncertainty. To test H8, H9 and H10, the interactions of (human capital x environmental uncertainty), (organisational capital x environmental uncertainty) and (social capital x environmental uncertainty) were included in regression analysis. The results in Table indicate that environmental uncertainty only moderate the influence of social capital on firm performance. That is, H8 and H9 are not supported. For H10, in contrast with what was assumed for H10, the outcome of a slope test indicated that social capital has strong impact on firm performance analysis when the degree of environmental uncertainty is low, not high. Therefore, H10 is not fully supported.

Table 4. Regression analysis of moderating effects

After confirming that H10 was partially significant, moderated mediation impacts (H11 and H12) were analysed. Process software was used to measure moderated mediation impacts. The output of analyses provided detailed results of the indirect effects by presenting statistical significance relating to the degree of environmental uncertainty. This allowed us to verify the values of environmental uncertainty for which conditional indirect effects of the organisational capital on firm performance via human and social capital were significant at α = 0.05. The results in Table demonstrate that both moderated mediation effects were significant when the level of environmental uncertainty is low but not when high. Therefore, H11 and H12 are not fully supported.

Table 5. Index of moderated mediation of the environmental uncertainty

7. Discussion

The main contributions of this study are to interpret the mediating effect of human and social capital between organisational capital and Vietnamese ICT firm performance, and the moderating effects of environmental uncertainty. First, this article reveals that intellectual capital dimensions have significant impacts on firm performance, in which findings confirm that human capital makes the most important contributions to forming these influences. Therefore, any innovative or creative activity must focus on human resource development.

Second, this article has drawn a conceptual framework based on RBV and intellectual capital theory to complement the limitations of both. Prior studies relied on RBV and intellectual capital for explaining better business performance in well-developed countries and in traditional industries (Radjenović & Krstić, Citation2017). By developing intellectual capital dimensions’ deployment as an aspect of RBV, the current study provides an answer to why, with similar amounts of intellectual capital, Western ICT firms use intellectual capital more successfully than Vietnamese ICT companies. The key point here is the moderating role of environmental uncertainty in Vietnam on the relationship between intellectual capital and firm performance. Therefore, the moderating role of environmental uncertainty was confirmed. Major local ICT firms are micro-, small, or medium firms; they work in a business environment in which they face a number of challenges in terms of regulatory frameworks and intellectual property protection, plus quality and availability of skilful persons and financial supporters, all of which are barriers to the development of the Vietnamese ICT sector. Therefore, they can expect long-term development and improved performance only if such environmental factors are improved. Otherwise, Vietnamese ICT firms are not strong enough to survive in a business environment with highly dynamic markets and uncertain conditions.

Third, the mediating roles of human and social capital should be considered key sensors in explaining how organisational capital positively improves firm performance. ICT staffs are highly educated and creative experts who prefer working as non-managerial staff—and as employees work under significant time management pressure, firms’ organisational culture, environment, and structure will influence their performance as well as the performance of their firms as a whole. Because of this special feature of ICT jobs, staffs must actively build their own social networks to support their work independently. In addition, their major communication and information exchanges are online and carried out in multi-culture environments, when mutual trust in social network is established, people are willing to share intellectual resources, which in turn motivate innovation activities and consequently build a positive corporate culture, as well as improving firm performance. In addition, ICT advances applied to organisational changes and operations are considered to play a central role in enhancing working environments as well as fostering staff productivity. The discussion of the impact of ICT advancements on growth and productivity was inspired here by the famous sentence by Robert Solow: “You can see the computer age everywhere but in the productivity statistics” (Solow, Citation1987). We argue, therefore, that the effective accumulation of organisational capital is necessary to help employees create and acquire knowledge derived from the range of intangible assets that comprise a firm’s competitive advantages. Concretely, organisational capital should not be seen as the sole factor influencing on firm performance: the integration of interrelationships among social, organisational, and social capital explain firm performance in specific contexts, and will provide a clear picture of how crucial intellectual capital is to the successful development of ICT firms.

8. Implications

The findings in this paper provide meaningful theoretical and practical contributions to the intellectual capital literature by extending prior findings. The first theoretical contribution pertains to dimensions of intellectual capital as they apply to Vietnam-like emerging economies. Because of inadequate markets and legal support, dysfunctional behaviours of competitor firms are widespread; the evaluation of intellectual capital should not be the same as in Western countries.

Second, despite extensive discussions of the influence of organisational capital on firm performance, there are very few studies on its impacts on firm performance via other intellectual capital dimensions within the context of the ICT sector. These findings show that values of corporate cultures form the foundation of the “valuable, rare, inimitable, and non-substitutable” (VRIN) assets, and that there are needs for building mutual trust in social-network extensions.

In addition, these findings also provide practical implications for ICT management. Facing global trends and an unpredictable environment, ICT managers must develop their own human, organisational, and social capital to meet customers’ challenging demands, and must also maintain and build strong network ties with employees, customers, suppliers, and competitors, to observe rapidly changing environments—and in response, to adjust their own business direction quickly, flexibly, and effectively.

9. Conclusion

Vietnam is on the road to a knowledge-based economy in which ICT will be a key sector. This study gives brief insights into factors shaping the Vietnamese ICT sector in terms of the interrelationships among social, human, and organisational capital on one hand, and firm performance on the other. By refining objectives in business operations, ICT firms must understand their own capabilities—especially their internal strengths—in order to face unpredictable changes in the environment. Social, organisational, and human capital, as dimensions of intellectual capital, are recognized as key intangible resources for firms’ long-term performance.

Accordingly, this study investigating the central role of organisational capital as the key factor for the sustainable development of the ICT firms, especially in a future in which firms become larger and better structured. However, the initiative of Vietnamese ICT firms to motivate innovation activities and to develop intellectual capital is still in its infancy. Hence, we hope that the findings presented here will be helpful to top managers and policy makers in Vietnam, and in developing countries, as they work to find a good path to enhance the long-term performance of ICT firms.

10. Limitations and further research

This research also reflects some limitations. First, this study explores primarily definitions of the dimensions of intellectual capital, and its impact on firm performance. This study employs static data at one point in time, which has inevitable drawbacks in describing the long-term patterns in ICT’s development and performance. The use of panel data may be advisable for follow-up studies. Second, other dimensions of intellectual capital (such as customer capital) could be included in future research. Lastly, other stakeholders such as employees and managers are involved in the relationship between intangible capital and firm performance; further studies should also take into account their perspectives.

Additional information

Funding

Notes on contributors

Hoang Thanh Nhon

Hoang Thanh Nhon is a PhD Candidate of Business Administration in International University, Vietnam National University and a Lecturer in The Faculty of Commerce, Van Lang University in Ho Chi Minh City, Vietnam. He holds Master of Business Administration of Latrobe University, Australia. His research interests are in the areas of Intellectual capitals and Corporate Performance.

References

- Aramburu, N., & Saenz, J. (2011). Structural capital, innovation capability, and size effect: An empirical study. Journal of Management & Organisation, 17(3), 307–18. https://doi.org/10.5172/jmo.2011.17.3.307

- Asiaei, K., & Jusoh, R. (2015). A multidimensional view of intellectual capital: The impact on organisational performance. Management Decision, 53(3), 668–697. https://doi.org/10.1108/MD-05-2014-0300

- Atuahene-Gima, K., & Murray, J. Y. (2004). Antecedents and outcomes of marketing strategy comprehensiveness. Journal of Marketing, 68(4), 33–46. https://doi.org/10.1509/jmkg.68.4.33.42732

- Baughn, C. C., Neupert, K. E., Anh, P. T. T., & Hang, N. T. M. (2011). Social capital and human resource management in international joint ventures in Vietnam: A perspective from a transitional economy. The International Journal of Human Resource Management, 22(5), 1017–1035. https://doi.org/10.1080/09585192.2011.556776

- Boon, C., Eckardt, R., Lepak, D. P., & Boselie, P. (2018). Integrating strategic human capital and strategic human resource management. The International Journal of Human Resource Management, 29(1), 34–67. https://doi.org/10.1080/09585192.2017.1380063

- Bourdieu, P. (2011). The forms of capital. (1986). Cultural Theory: An Anthology, 1, 81–93.

- Cao, J., & Wang, Z. (2015). Impact of intellectual capital on firm performance: The influence of innovation capability and environmental dynamism [paper Presentation]. The AMCIS Conference, Fajardo, Puerto Rico.

- Cheung, M. K., Chiu, Y., & Lee, K. O. (2010). Online social networks: Why do students use Facebook? Computers in Human Behavior, 27(4), 1337–1343. https://doi.org/10.1016/j.chb.2010.07.028

- Choo Huang, C., Tayles, M., & Luther, R. (2010). Contingency factors influencing the availability of internal intellectual capital information. Journal of Financial Reporting and Accounting, 8(1), 4–21. https://doi.org/10.1108/19852511011055916

- Coleman, J. S. (1988). Social capital in the creation of human capital. American Journal of Sociology, 94, S95–S120. https://doi.org/10.1086/228943

- Cyert, R. M., & March, J. G. (1963). A behavioral theory of the firm. Englewood Cliffs, NJ, 2.

- Dadfar, H., Dahlgaard, J. J., Brege, S., & Alamirhoor, A. (2013). Linkage between organisational innovation capability, product platform development and performance: The case of pharmaceutical small and medium enterprises in Iran. Total Quality Management & Business Excellence, 24(7–8), 819–834. https://doi.org/10.1080/14783363.2013.791102

- Demirbag, M., Tatoglu, E., Tekinkus, M., & Zaim, S. (2006). An analysis of the relationship between TQM implementation and organisational performance: Evidence from Turkish SMEs. Journal of Manufacturing Technology Management, 17(6), 829–847. https://doi.org/10.1108/17410380610678828

- Dess, G. G., & Robinson, R. B. (1984). Measuring organisational performance in the absence of objective measures: The case of the privately held firm and conglomerate business unit. Strategic Management Journal, 5(3), 265–273. https://doi.org/10.1002/smj.4250050306

- Dess, G. G., & Shaw, J. D. (2001). Voluntary turnover, social capital, and organisational performance. Academy of Management Review, 26(3), 446–456. https://doi.org/10.5465/amr.2001.4845830

- Djuric, M., & Filipovic, J. (2015). Human and social capital management based on complexity paradigm: Implications for various stakeholders and sustainable development. Sustainable Development, 23(6), 343–354. https://doi.org/10.1002/sd.1595

- Donate, M. J., Ruiz-Monterrubio, E., de Pablo, J. D. S., & Peña, I. (2019). Total quality management and high-performance work systems for social capital development. Journal of Intellectual Capital, 21(1), 87–114. https://doi.org/10.1108/JIC-07-2018-0116

- Edvinsson, L., & Sullivan, P. (1996). Developing a model for managing intellectual capital. European Management Journal, 14(4), 356–364. https://doi.org/10.1016/0263-2373(96)00022-9

- Ellinger, A. D., Ellinger, A. E., Bachrach, D. G., Wang, Y. L., & Elmadağ Baş, A. B. (2011). Organisational investments in social capital, managerial coaching, and employee work-related performance. Management Learning, 42(1), 67–85. https://doi.org/10.1177/1350507610384329

- Ellinger, A. D., Ellinger, A. E., Yang, B., & Howton, S. W. (2002). The relationship between the learning organisation concept and firms’ financial performance: An empirical assessment. Human Resource Development Quarterly, 13(1), 5–22. https://doi.org/10.1002/hrdq.1010

- Ferreira-Lopes, A., Roseta-Palma, C., & Sequeira, T. N. (2012). When sociable workers payoff: Can firms internalize social capital externalities? Structural Change and Economic Dynamics, 23(2), 127–136. https://doi.org/10.1016/j.strueco.2012.01.004

- Gilbert, J. H., Von Ah, D., & Broome, M. E. (2017). Organisational intellectual capital and the role of the nurse manager. A proposed conceptual model. Nursing Outlook, 29.

- Grootaert, C. (Ed.). (2004). Measuring social capital: An integrated questionnaire (No. 18). World Bank Publications.

- Guthrie, J., Petty, R., Yongvanich, K., & Ricceri, F. (2004). Using content analysis as a research method to inquire into intellectual capital reporting. Journal of Intellectual Capital, 5(2), 282–293. https://doi.org/10.1108/14691930410533704

- Hair, J. F., Anderson, R. E., Tatham, R. L., & Black, W. C. (1998). Multivariate data analysis. Prentice Hall.

- Hayes, A. F. (2009). Beyond Baron and Kenny: Statistical mediation analysis in the new millennium. Communication Monographs, 76(4), 408–420. https://doi.org/10.1080/03637750903310360

- Hayes, A. F. (2013). Introduction to mediation, moderation, and conditional process analysis. A regression-based approach. Guilford.

- Hsu, C. P., Chang, C. W., Huang, H. C., & Chiang, C. Y. (2011). The relationships among social capital, organisational commitment and customer‐oriented prosocial behaviour of hospital nurses. Journal of Clinical Nursing, 20(9‐10), 1383–1392. https://doi.org/10.1111/j.1365-2702.2010.03672.x

- Hsu, Y. H., & Fang, W. C. (2009). Intellectual capital and new product development performance: The mediating role of organisational learning capability. Technological Forecasting and Social Change, 76(5), 664–677. https://doi.org/10.1016/j.techfore.2008.03.012

- Huang, Y. C., & Wu, J. (2010). Intellectual capital and knowledge productivity: The Taiwan biotech industry. Management Decision, 48(4), 580–599. https://doi.org/10.1108/00251741011041364

- Jabnoun, N., Khalifah, A., & Yusuf, A. (2003). Environmental uncertainty, strategic orientation, and quality management: A contingency model. Quality Management Journal, 10(4), 17. https://doi.org/10.1080/10686967.2003.11919081

- Kianto, A., Andreeva, T., & Pavlov, Y. (2013). The impact of intellectual capital management on company competitiveness and financial performance. Knowledge Management Research & Practice, 11(2), 112–122. https://doi.org/10.1057/kmrp.2013.9

- Kostopoulos, K. C., Bozionelos, N., & Syrigos, E. (2015). Ambidexterity and unit performance: Intellectual capital antecedents and cross‐level moderating effects of human resource practices. Human Resource Management, 54(S1), s111-s132. https://doi.org/10.1002/hrm.21705

- Latan, H., Jabbour, C. J. C., De Sousa Jabbour, A. B. L., Wamba, S. F., & Shahbaz, M. (2018). Effects of environmental strategy, environmental uncertainty and top management’s commitment on corporate environmental performance: The role of environmental management accounting. Journal of Cleaner Production, 180, 297–306. https://doi.org/10.1016/j.jclepro.2018.01.106

- Mathews, J. (2019). Human Resource-Based View of the Organisation. Available at SSRN 3403098.

- Miller, D., & Friesen, P. H. (1984). A longitudinal study of the corporate life cycle. Management Science, 30(10), 1161–1183. https://doi.org/10.1287/mnsc.30.10.1161

- Mouritsen, J., Larsen, H. T., & Bukh, P. N. (2001). Intellectual capital and the ‘capable firm’: Narrating, visualising and numbering for managing knowledge. Accounting, Organisations and Society, 26(7), 735–762. https://doi.org/10.1016/S0361-3682(01)00022-8

- Nahapiet, J., & Ghoshal, S. (1998). Social capital, intellectual capital, and the organisational advantage. Academy of Management Review, 23(2), 242–266. Management, 22(05), 1017-1035. https://doi.org/10.5465/amr.1998.533225

- Nonaka, I., & Von Krogh, G. (2009). Perspective-tacit knowledge and knowledge conversion: Controversy and advancement in organisational knowledge creation theory. Organisation Science, 20(3), 635–652. https://doi.org/10.1287/orsc.1080.0412

- Phusavat, K., Comepa, N., Sitko-Lutek, A., & Ooi, K. B. (2011). Interrelationships between intellectual capital and performance: Empirical examination. Industrial Management & Data Systems, 111(6), 810–829. https://doi.org/10.1108/02635571111144928

- Putnam, R. D. (1993). The prosperous community. The American Prospect, 4(13), 35–42.

- Radjenović, T., & Krstić, B. (2017). Intellectual capital as the source of competitive advantage: The resource-based view. Facta Universitatis, Series: Economics and Organization.

- Rastogi, P. N. (2003). The nature and role of IC: Rethinking the process of value creation and sustained enterprise growth. Journal of Intellectual Capital, 4(2), 227–248. https://doi.org/10.1108/14691930310472848

- Sharabati, A. A. A., Jawad, S. N., & Bontis, N. (2010). Intellectual capital and business performance in the pharmaceutical sector of Jordan. Management Decision, 48(1), 105–131. https://doi.org/10.1108/00251741011014481

- Shih, K., Chang, C., & Lin, B. (2010). Assessing knowledge creation and intellectual capital in banking industry. Journal of Intellectual Capital, 11(1), 74–89. https://doi.org/10.1108/14691931011013343

- Solow, R. M. (1987). We’d better watch out. New York Times Book Review, 12.

- Subramaniam, M., & Youndt, M. A. (2005). The influence of intellectual capital on the types of innovative capabilities. Academy of Management Journal, 48(3), 450–463. https://doi.org/10.5465/amj.2005.17407911

- Taouab, O., & Issor, Z. (2019). Firm performance: Definition and measurement models. European Scientific Journal, 15(1), 93–106.

- Tseng, J. F., Wang, H. K., & Yen, Y. F. (2014). Organisational immovability: Exploring the impact of human and social capital in the banking industry. Total Quality Management & Business Excellence, 25(9–10), 1088–1104. https://doi.org/10.1080/14783363.2013.781294

- Tushman, M. L., & Anderson, P. (1986). Technological discontinuities and organisational environments. Administrative Science Quarterly, 31(3), 439–465. https://doi.org/10.2307/2392832

- Venkatraman, N., & Ramanujam, V. (1986). Measurement of business performance in strategy research: A comparison of approaches. Academy of Management Review, 11(4), 801–814. https://doi.org/10.5465/amr.1986.4283976

- VietNamNet. (2020, March 17). ICT Industry Earns $59.9 Billion. [online]. https://english.vietnamnet.vn/fms/science-it/170268/ict-industry-earns–59-9-billion.html

- Wernerfelt, B. (1984). A resource‐based view of the firm. Strategic Management Journal, 5(2), 171–180. https://doi.org/10.1002/smj.4250050207

- Wiklund, J., & Shepherd, D. (2003). Knowledge‐based resources, entrepreneurial orientation, and the performance of small and medium‐sized businesses. Strategic Management Journal, 24(13), 1307–1314. https://doi.org/10.1002/smj.360

- Youndt, M. A., Subramaniam, M., & Snell, S. A. (2004). Intellectual capital profiles: An examination of investments and returns. Journal of Management Studies, 41(2), 335–361. https://doi.org/10.1111/j.1467-6486.2004.00435.x

- Yu, C. L., Wang, F., & Brouthers, K. D. (2016). Competitor identification perceived environmental uncertainty, and firm performance. Canadian Journal of Administrative Sciences/Revue Canadienne Des Sciences De l’Administration, 33(1), 21–35. https://doi.org/10.1002/cjas.1332

- Zack, M., McKeen, J., & Singh, S. (2009). Knowledge management and organisational performance: An exploratory analysis. Journal of Knowledge Management, 13(6), 392–409. https://doi.org/10.1108/13673270910997088

- Zeglat, D., & Zigan, K. (2013). Intellectual capital and its impact on business performance: Evidences from the Jordanian hotel industry. Tourism and Hospitality Research, 13(2), 83–100. https://doi.org/10.1177/1467358413519468