Abstract

The purpose of this study is to examine the moderating effect of corporate governance on the relationship between capital structure and firm performance. This study uses secondary data in the form of financial reports at the end of 2019 from micro-financial institutions (rural banks) with a total of 506 units. Data were analyzed using the Moderated Regression Analysis. Results indicate that capital structure financing decisions have a positive contribution to financial performance. However, this only applies to short-term debt. Otherwise, long-term debt has a negative and insignificant effect on both return on assets and return on equity. These results support the view of the pecking order theory, as empirical evidence that the opposite effect between firm profits and capital structure. The results of the moderation analysis show that only the size of the board of commissioners can strengthen the relationship between capital structure and company performance, while board size and ownership concentration are not able to moderate the relationship between capital structure and company performance.

PUBLIC STATEMENT OF INTEREST

This study contributes to the discourse of corporate governance as a variable that moderates the relationship between capital structure and firm performance, which is analyzed using modifying regression analysis (MRA). This is done to determine whether the strong relationship between capital structure and company performance is influenced by governance practiced by the firm. This study uses cross-sectional data from rural banks in West Java, East Java and Central Java, Indonesia. This research reveals that only the board of commissioners strengthens the relationship between capital structure and firm performance.

1. Introduction

The number of rural banks in Indonesia in 2019 reached 1,597 units, this number is decreasing when compared to 2015 which totaled 1,637 units (down 2.44%). the Financial Services Authority (FSA) has issued several directors for at least 2 people in each rural bank to carry out company operations in addition to requiring a minimum number of commissioners of 2 people to supervise. the running of the rural bank. However, in practice, not all rural banks meet the requirements of corporate governance, so some companies have up to 4 directors, while there are companies that have only one director. Likewise, the condition of the board of commissioners which has the same characteristics as the board of directors. where there are rural banks that do not have a board of commissioners, while others are rural banks that have a board of commissioners of 4 people. Furthermore, in rural governance, it is regulated that each bank outlet has a minimum number of shareholders of one person and a maximum of 10 shareholders.

Most of the previous studies examining the effects of leverage and corporate governance on performance were conducted separately. And the results also vary. One side of the effect of leverage on performance is positive (Gill et al., Citation2011), on the other hand it shows negative results (Arbor, Citation2007; Chinaemerem & Anthony, Citation2012). Therefore, to address this gap, a study examines the moderating effect of the corporate governance mechanism on the relationship between leverage and firm performance. This moderating effect assessment is based on the fact that corporate governance does not only effect on performance but also financial leverage. Corporate governance can have positive (Isik & Ince, Citation2016; Mollah et al., Citation2012; Sheikh & Wang, Citation2012; Tulung & Ramdani, Citation2018) and negative impact (Berger et al., Citation1997; Heng et al., Citation2012) on capital structure. Besides, corporate governance can have a positive impact (Ganiyu & Abiodun, Citation2012; Hermalin & Weisbach, Citation1988; Nandi & Ghosh, Citation2012). Thus, it is expected that this study can expand that the relationship between leverage and firm performance is influenced by corporate governance. This study aims to examine the moderating effect of corporate governance on the relationship between leverage and company performance. So that it can be seen whether corporate governance strengthens this relationship or vice versa.

2. Background

Principally, corporate governance is aimed at maintaining a balance of interests between corporate investors and stakeholders in a firm. This is a method for managing the firm in order to reduce agency conflicts, increase investor confidence, firm goodwill, shareholder wealth and investment opportunities. It also provides the correct direction to the firm how the firm should work and be supervised. The agency problem in using free cash flow (FCF) occurs when the market is inefficient and information asymmetry, so that managers act on their interests and the interests of shareholders by ignoring the interests of debtholders. The choice of a capital structure that is oriented to corporate value, often conflicts with the interests of the parties involved, shareholders are oriented towards equity value, and debtholder is oriented towards debt value. Managers can act on their interests by ignoring the interests of shareholders, such as empire building (Jensen and Meckling Citation1976). In addition, managers can act in the interests of shareholders, thereby hurting the interests of debtors by making suboptimal investments. With the existence of CG, the managerial opportunistic behaviour can be reduced so as to make optimal investment and increase firm value.

To date, most studies have explored the effect of capital structure and corporate governance on firm performance separately. Studies of Jahanzeb et al. (Citation2015) shows that the capital structure has a significant positive effect on profitability and dividend payments. However, the Mardones and Cuneo (Citation2020) study show that there is no significant relationship between capital structure and firm performance (Return on Equity and Return on Assets). Furthermore, Chinaemerem and Anthony (Citation2012) stated that the firm’s capital structure has a negative impact on firm performance. They prove that high leverage has a negative impact on company performance. They prove that high leverage has a negative impact on company performance. From several studies, it can be underlined that the relationship between capital structure and firm performance shows inconsistent results. Therefore, the authors place CG as a moderating factor, so that it can further clarify the relationship.

The relationship between CG and other fields, the results show that financial performance is a major concern in previous studies (Almaqtari, Al-Hattami, Al-Nuzaili, & Al-Bukhrani, Citation2020). Ishii and Metrick (Citation2003) state that CG in developing countries serves as a major objective in organizational success and can reduce the possibility of financial crises and management conflicts. CG serves as a gateway to facilitate the relationship between firm staff, owners, and other stakeholders. It can also be thought of as a system of guidelines, rules, and factors, which control the methods used to perform various operations in an organization (Shleifer & Vishny, Citation1997). Besides, CG is a method employed to reduce principal conflicts with agents and increase investor confidence, corporate goodwill, shareholder wealth, and investment opportunities. On the other hand, studies examining the moderating effect of corporate governance have received little attention in general, and particularly at small microfinance institutions in Indonesia.

This study was to determine the relationship between capital structure and firm performance by investigating the moderating impact of CG practices on rural banks in Indonesia. The previous literature generally shows a positive relationship between the characteristics of CG and capital structure. Abor (Citation2007) stated a significant and positive relationship between CG and financial decisions. Besides, companies that practice better governance have a greater chance of obtaining debt financing. On the contrary, Hassan and Butt (Citation2009) found a negative relationship between indicators of CG, namely the size of the board of commissioners and managerial share ownership and capital structure.

The findings of this study have practical importance for regulatory authorities and policymakers in terms of improving markets. Apart from research on the relationship of these variables, the role of the CG mechanism as a moderator is recognized by the relationship between capital structure and rural bank financial performance. In general, this study fills the gap in the literature series by capturing the moderating impact of a CG mechanism on the relation between capital structure and bank financial performance. Although several scholars (such as Ferrero-Ferrero et al., Citation2012; Ibrahim, Citation2016; Munisi & Randøy, Citation2013; Nodeh et al., Citation2016) have examined the relationship between CG to firm performance, the moderating effect of CG on the relationship between capital structure and firm performance has not been discussed. This study provides useful guidelines for the corporate sector, financial institutions, shareholders, depositors, and investors as these can help companies to react effectively and efficiently to different economic conditions. Besides, this serves as a good recipe for managers to consider a suitable set of CG models related to the specific rural bank system in their decision-making process.

3. Theory

3.1. Capital structure

The concept of capital structure can be defined as a proportional composition or combination of debt capital and equity capital. Scholars around the world have conceptualized the structure of capital in different contexts and different ways. Van Horne and Wachowicz (Citation2008) stated that capital structure as a long-term financing method is a combination of the firm’s preferred share capital, equity capital, and debt capital. Besley and Brigham (Citation2008), on the contrary, conceptualized capital structure as a combination of long-term debt capital, preferred share capital, and net worth, which is used as a method of permanent financing by companies. Therefore, it can be argued that the capital structure has been traditionally conceptualized as a combination of long-term debt capital and equity capital, and thus neglects short-term debt capital. The capital structure is usually used to fund the development of a firm’s business, with its use considered a crucial decision to make because of its direct influence on the risk and return of the firm.

Choosing between internal or external financing presents a serious problem in companies. Capital structure and its impact on firm value and performance remain a puzzle in corporate finance theory and financial literature. Capital structure theory based heavily on large firms fails to explain the optimal debt-to-equity mix. Therefore, the choice of capital structure is an important issue for large and small companies.

Three theories are related to the choice of capital structure in companies, namely Modigliani and Miller (MM) theory, trade-off theory, and Pecking order theory. MM theory is the most fundamental theory for capital structure. Assuming that there is no income rate, then the capital structure is irrelevant to the value of the company or the company has no way of increasing its value by changing the capital structure. Furthermore, by including corporate income tax, the value of companies that have more debt in their capital structure is the same as the market value of companies that have no debt. In short, this theory shows that the capital structure affects the market value of the firm. This trade-off theory concludes that the market value of a company with debt is equal to the value of the company without debt plus the value of the tax shield minus the present value of bankruptcy costs. This theory suggests that there is an optimal capital structure, in which the tax shield benefits the most to compensate for losses from debt due to financial difficulties and agency costs. Next is the pecking order theory that explains business managers’ funding decisions. In meeting their capital requirements, businesses place an order of priority for their funds: first using internal sources, followed by loans, then equity. In short, the pecking order theory states that internal capital will always take precedence over loans and the use of internal funds will reduce the company’s dependence on external parties, increase financial autonomy and reduce internal information leakage.

An optimal capital structure should be used according to financial theory and literature; however, there is no consensus on how to achieve an optimal debt-to-equity ratio. Finance theory is further unsupported in understanding the impact of the chosen capital structure on firm value. An optimal capital structure minimizes the cost of capital and ensures that firm profitability is maximized. Proper management of the capital structure is crucial at it affects the profitability and the value of the firm in the long run; inefficient management will cause financial difficulties that will ultimately lead to bankruptcy. Gill et al. (Citation2011) emphasized that although numerous theories attempted to explain the optimal capital structure, there is still no appropriate model to determine the optimal capital structure.

3.2. Corporate governance mechanism

There is no universal definition of CG agreed upon by all countries because of differences in economic, legal, political, and cultural systems. Consequently, different definitions can indicate CG depending on the related strengths of stakeholders such as owners, managers, shareholders, and suppliers (Craig, Citation2005). Cadbury (Citation2000) defined CG as a balance between economic and social goals and between individual and communal goals to encourage the efficient use of resources and equally require accountability for the management of these resources. Bodaghi and Ahmadpour (Citation2010) defined CG as a philosophy and mechanism that requires a process and structure for creating shareholder value and protecting the interests of all stakeholders. According to Cornelius (Citation2005), CG is a set of goals and strategies issued by firm directors and their implementation. Meanwhile, Shleifer and Vishny (Citation1997) defined it as the way in which financial suppliers to companies ensure themselves in getting a return on their investment. From some of these definitions, CG broadly refers to the mechanisms, processes, and relationships in which the firm is controlled and directed. Thus, CG can be described as a set of market and institutional tools and mechanisms that persuade managers (controllers) to maximize corporate value in the best interests of shareholders (owners), and their goals are to align the interests of individuals, corporations, and society. The relationship between owners and managers is a core topic of CG. Shareholders finance new investments in a business, and management is responsible for achieving the highest returns for them.

The theory that underlies the practice of corporate governance is agency theory. The main principle of this theory states that there is a working relationship between the party giving the authority (the principal), namely the investor, and the party receiving the authority (agency), namely the manager, in the form of a cooperation contract. This difference in economic interests can either be caused or cause the emergence of information asymmetry between the shareholders of the organization. The manager or board of directors is the agent of the shareholders. This agency theory assumes that all individuals act in their interests. Shareholders as principal are assumed to be only interested in increasing financial results or their investment in the company. While the agents are assumed to receive satisfaction in the form of financial compensation and the conditions that accompany the relationship. The principal wants the maximum possible return on investment, one of which is reflected in the increase in the dividend portion of each share owned. The principal assesses the agent’s performance based on his ability to increase profits to be allocated to dividends. The higher the profit, the share price and the bigger the dividend, the agent is considered successful/has good performance so that it deserves a high incentive. On the other hand, the agent also fulfills the principal’s demands for high compensation. So that if there is no adequate supervision, the board of directors can play several of company conditions so that the target is achieved. Therefore we need directors who can carry out the mandate of the shareholders.

CG mechanisms are part of CG. According to Hart (Citation1995), CG mechanisms can result from monitoring and controlling the voting of shareholders or the board of directors on management tools and financial structures represented by debt leverage. This tool regulates the firm’s ownership structure, relationships with stakeholders, financial transparency, and information disclosure as well as the figure of the board of directors. Shareholders elect the board of directors to oversee top management and ratify important decisions. Besides, this elected group has the power to replace the members of the management.

The board consists of executives (members of the management team) and non-executive directors (commissioners). Firms in Indonesia follow this dual board structure, namely, a supervisory board (i.e., a board of commissioners) and management (i.e. a board of directors). However, the structure of the board of directors had some critical problems. On the one hand, it is impossible for the executive director to monitor himself. On the other hand, nonexecutive directors (commissioners) may perform inefficient monitoring. First, they may not have a financial interest in the firm. Second, non-executive directors may serve on the board of directors of many companies; hence, they might not focus in detail on a firm’s exciting business. Finally, non-executive directors (commissioners) may owe their position to management; they may wish to remain on the board to benefit from rewards and fees and, therefore, may choose not to challenge management. These reasons may prompt shareholders to replace or change the composition of the board of directors. Shareholders can replace the board of directors once the elected group fails to properly monitor the management. Therefore, large shareholders play an important role in CG. Also, these shareholders can use their voting rights to obtain several interests by conspiring with management. Therefore, the concentration of ownership and the supervisory board are more important mechanisms (Kabir et al., Citation1997).

3.3. Firm performance

The Financial performance reveals how well an organization uses its financial resources and shows its financial health and fitness, as well as the results of the firm’s work, operations, and policies. These results are presented in the form return on equity (ROE), return on investment (ROA), dividends per share, and earnings per share.

The firm’s performance has been a topic of discussion for many researchers, with studies investigating the relationship between corporate performance and CG. For example, studies of Coleman and Biekpe. (Citation2006) in Ghana, Noor and Ayoib (Citation2009) in Malaysia, and Belkhir (Citation2009) in the US were undertaken to investigate the relationship between robust performance and board structure. Most of the studies on CG have ignored the problem of bank CG in developing countries (Caprio et al., Citation2007).

4. Empirical literature review and hypotheses

4.1. Capital structure and firm performance

The study of capital structure and firm performance is mainly based on the theory of information asymmetry, signalling, and agency costs. Ross (Citation1977) came up with a model that depicts the choice of the debt-to-equity ratio signifying firm quality. This study explains that low-quality firms face high costs for abusing the market and signals their high quality by including more debt capital. Companies with low debt capital tend to spend their free cash flow freely and ultimately result in lower returns. Conversely, companies with higher debt capital work very effectively because they are committed to meeting the interest payments of debt holders and managing the remaining cash flow more efficiently. Harris and Raviv (Citation1988) described the higher leverage of firms as an antitakeover instrument. A firm with higher leverage bears a higher risk, which in turn prevents or deters unwanted takeovers from other companies. For this reason, firm managers tend to manage higher amounts of debt, which is inconsistent with agency theory.

Furthermore, Arbor (Citation2007) examined the relationship between capital structure and performance of SMEs in Ghana and South Africa over the 6-years (1998–2003). Empirical results show a significant negative relationship between short-term debt and the gross profit margin of the two countries and a significant positive relationship between long-term debt and the gross profit margin of the two countries. More profitable companies should have a lower leverage ratio compared with the less profitable companies because they can finance their investment opportunities with theoretical retained earnings. Besides, the theory says that leverage has a negative effect on a firm’s profitability. Arbor (Citation2005) and Arbor (Citation2007) reinforced this idea by stating that more profitable companies tend to use their income to pay off debt and are therefore will have lower leverage compared with less profitable companies. Likewise, Omondi and Muturi (Citation2013) presented that leverage has a significant negative effect on corporate financial performance, and there is a negative correlation between capital structure and firm profitability. Gill et al. (Citation2011), on the contrary, showed a positive effect of short-term debt, long-term debt, and total debt on profitability. Furthermore, they classified the sample as the service and manufacturing sector and found a positive impact of short-term debt and total debt on return on assets (ROA) in the service and manufacturing industries.

In short, some studies show a positive relationship between capital structure and firm performance, whereas other studies express the opposite. This is in accordance with the results of the meta-analysis research by Thi et al. (Citation2020), which exhibited that 63 studies showed positive effects, 117 studies showed negative effects, and 65 studies showed insignificant effects. However, because rural banks in their operations depend more on short term debt, and this short term debt is used to lend back to customers, the relationship between total debt to total assets (TDTA) and short term debt to total assets (SDTA) is related to firm performance is expected to be positive. Therefore we propose the following hypothesis:

H1: There is a positive relationship between leverage to performance.

4.2. CG mechanism, leverage and performance

Maximizing firm value is the ultimate goal of shareholders. CG is a set of mechanisms to ensure that companies safeguard the interests of shareholders. However, according to agency theory, there are often conflicts of interest between firm managers and shareholders (M. C. Jensen and Meckling, Citation1976). Other conflicts of interest also arise between top controlling shareholders and minority shareholders, arguing that large shareholders can directly or indirectly exploit minority shareholders as well as employee rights, causing enormous agency problems (Shleifer & Vishny, Citation1997).

Corporate debt policy is generally observed as a significant CG tool in reducing agency conflicts between shareholders and managers (Milton Harris & Raviv, Citation1991). Debt financing can solve agency problems by reducing free cash flow and increasing the likelihood of bankruptcy risk (Morellec et al., Citation2012); in other words, commitment to fulfil the principle of debt and reduce free cash flow for activities that are not optimal. Debt financing can increase the likelihood of costly bankruptcy and job loss, consequently encouraging managers to perform optimally and make better investment decisions (Grossman & Hart, Citation1982). In addition, agency problems can also be reduced through the top shareholders, because of their interest in gathering information and monitoring management (Jensen & Meckling, Citation1976; Shleifer & Vishny, Citation1997). Another assumption of agency theory is that advanced CG and strong shareholder rights will minimize agency costs and increase investor confidence in the firm’s cash flow, thereby reducing the cost of equity capital and increasing the potential for equity financing, as well as reducing dependence on corporate debt (Drobetz et al., Citation2004; Gompers et al., Citation2003). Better CG and stronger shareholder rights can improve a firm’s ability to gain access to external finance (Shleifer & Vishny, Citation1997). On the contrary, large shareholders in poorly managed companies may prefer debt financial obligations while retaining primary ownership rights and control over the firm (Haque et al., Citation2011).

Several capital structure studies focus on examining the relationship between the main characteristics of CG and capital structure, such as board size, board composition, board independence, ownership structure, chief executive officer (CEO) tenure, CEO duality, management compensation, disclosure, auditing, and other mechanisms (Wen et al., Citation2002). This study investigates the relationship between board size, commissioner size, and ownership concentration as three tools of CG and their effects on capital structure and firm performance. Tsifora and Eleftheriadou (Citation2007) studied the mechanisms of CG and the financial performance of the manufacturing sector. Findings revealed better performance for companies included in an expanded group of shareholders compared with those included in a small group of shareholders or are family-owned. In general, companies that have a CG system are characterized by high profitability. Therefore, this study is expected to clarify the relationship between CG and firm performance. Large boards of directors are more likely to provide better access to multiple resources than small boards. On the other hand, a board with a variety of experience and knowledge is more likely to produce better processes and efficient decisions resulting in better performance.

4.2.1. Board size, leverage and performance

The relationship between board size and leverage yielded mixed results. Adams and Mehran (Citation2002) argued that some companies need large boards for effective oversight. Heng et al. (Citation2012) showed an inverse relationship between the total number of board members and the ratio of debt to assets. In contrast, several other studies (e.g., Isik & Ince, Citation2016; Mollah et al., Citation2012; Tulung & Ramdani, Citation2018) found that companies with larger board sizes have higher financial leverage than firms with smaller board sizes; moreover, companies with large board sizes are more likely to use debt financing than companies with smaller board sizes. These results can be explained in accordance with the assumption that companies with larger boards have mixed experience and large networks that facilitate better access to external finance. In line with this opinion, Sheikh and Wang (Citation2012) in Pakistan found that board size has a positive relationship with the firm’s debt ratio. Hussainey and Aljifri (Citation2012) in UAE found similar findings, stating that the number of boards of directors has a positive relationship with the debt-to-equity ratio. Meanwhile, the relationship between BS and firm performance is estimated to have positive results. This is in accordance with the results of research from Ganiyu and Abiodun (Citation2012) which found a positive relationship, indicating that large boards tend to practice effective monitoring because large numbers of directors apply high levels of debt to increase firm value. Nandi and Ghosh (Citation2012) findings revealed a positive relationship between board size and profitability. With a larger director, the company has wider opportunities to get investment funding. With a variety of experiences that exist in each director, it can produce better processes and decisions to result in better firm performance. Therefore we propose the following hypothesis:

H2: The relationship between leverage and performance will be stronger when the number of BS is larger.

4.2.2. Commissioner size, leverage and performance

In general, empirical studies that have investigated the effect of board size on firm performance use the number of executive and non-executive directors as board size (eg (O’Connell & Cramer, Citation2010). Under a dual board structure, executives cannot sit on the board of commissioners, and this allows the board of commissioners to carry out its supervisory role more independently than as directors. Commissioners are very important in influencing company performance, because independent commissioners can think objectively without having interests with various parties. This board of commissioners can provide strategic direction to the company and help make decisions in achieving firm performance. Therefore, in the case of SMES, the greater the number of CS, the better the decisions and strategies will be carried out. This is in accordance with the agency theory that the board of commissioners has the responsibility to supervise the company director. This is also in accordance with the stewardship theory that the board of commissioners can provide valuable advice to the company.

A larger board is expected to improve the monitoring and advisory functions of underperforming companies and thus improve firm results. This is shown from several previous studies. Sheikh and Wang (Citation2012) show that the size of the board of commissioners has a positive effect on the capital structure. Outsiders are expected to increase the independence of the management and improve firm performance. This argument is supported by research results which show that there is a positive effect of the board of commissioners on firm performance (Mburu & Kagiri, Citation2013). In line with these findings, the size of the board of commissioners in companies is expected to have a positive influence on the relationship between capital structure and firm performance. The task of the board of commissioners is to oversee the operational duties of the director in making decisions, especially in investment funding. Therefore, the more commissioners, the more effective the supervision will be compared to the supervision which is only carried out by one commissioner. Therefore we propose the following hypothesis:

H3: The relationship between leverage and performance will be stronger when the number of CS is larger.

4.2.3. Ownership concentration, leverage and firm performance

Several previous studies have shown that the relationship between ownership concentration and capital structure has a negative character. Fayez et al. (Citation2019) presented an opposite result, where ownership concentration has a negative relationship with long-term debt and debt-to-equity ratio. Some of the results of these studies confirm that the effect of ownership concentration on capital structure is far from clear. We argue that the top shareholders being on the board of directors reduce the level of agency costs between managers and shareholders and facilitate issuance of equity. In addition, shareholders will not be diversified, increasing their reluctance to get into debt. On the contrary, if some of these shareholders are banks, they may force the firm to borrow from them. Thus increasing long-term debt and resulting in poor performance.

Although the traditional perspective supports the positive effect of ownership concentration on firm performance, some researchers have also observed a negative effect. With a large number of owners, they can get more control to control the company which can provide greater personal benefits. The relationship between ownership concentration and firm performance, from several previous studies shows negative results. Rashid and Nadeem (Citation2014) showed a negative relationship between family-concentrated ownership and performance. When the performance of family members is concentrated, it loses. While Nowak and Kubíček (Citation2012) did not find a relationship between concentration and performance in Czech firms. Tran et al. (Citation2020), find no relation between ownership concentration and firm profitability. The more relevant study (Lukas & Ondrej, Citation2016), by taking a sample of more than 5000 companies in Czech with data in the period 2010 to 2012, where the results found a negative effect of ownership concentration on ROA. Building on this argument based on empirical research, SS is expected to weaken the relationship between capital structure and firm performance. By following the agency problem, between the larger number of shareholders and the smaller number of shareholders, where if the number of shareholders is small, there will be little consideration or input in decision making by the board of directors, so the result is less effective. Conversely, if the number of shareholders is large, there will be a lot of input to the director in making decisions, so that the decisions are better. Therefore we propose the following hypothesis:

H4: The relationship between leverage and performance will be stronger when the number of SS is smaller.

5. Methods

5.1. Collecting data

A sample of all conventional rural banks owned by individuals (not institutions, be it government, companies, or cooperatives) in Central Java, East Java, and West Java, Indonesia was taken using secondary data in the form of financial reports (balance sheet reports and profit and loss reports) at the end of the year (December 2019). A total of 506 rural banks were collected. Data were analyzed using multiple linear regression analysis and moderation analysis with SPSS 23 software.

5.2. Measurement

This study consists of three main variables: capital structure, performance, and CG. Proxies represent these three variables, as shown in . The purpose of this study was to determine the effect of capital structure decisions on rural banks performance. To facilitate the overall effect, this study uses the ratio of total debt to total assets (TDTA), the ratio of long-term debt (in the form of loans) to total assets (LDTA), and the ratio of short-term debt (in the form of savings and deposits) to total assets (SDTA). Two measures of firm performance are used: how firm management uses total assets to generate profit (ROA) and how well management uses debt and equity capital to increase firm profitability (ROE). Two measures of CG are moderating variables in this study. The quality of CG is measured by board size (number of directors, number of commissioners, and concentration of shareholders). The number of directors and commissioners are measured by the number of individuals elected as directors and commissioners, respectively. The concentration of share ownership is measured by the number of shareholders.

Table 1. Variables, notation, and proxies of the research

5.3. Data analysis

Multiple regression analysis is used to examine the effect of capital structure on RB performance. This method explores the relationship between one dependent variable and several independent variables. Furthermore, Moderated Regression Analysis is used to analyze the moderating effect. The regression analysis was conducted to identify the relationship between capital structure, performance, and moderating effects of the organizational environment. Here the capital structure is the independent variable, firm performance is the dependent variable, and the organizational environment is the moderating variable. The following relationships are formulated from these variables. To test these two relationships, the authors have used multiple regression models with the term interaction (Jaccard et al., Citation1990). This regression equation for analyzing the moderation effect can be formulated as follows:

ROA = a + β1TDTA + β2BS + β3CS + β4SS + β5TDTA*BS + β6TDTA*CS + β7TDTA*SS + e

ROE = a + β1TDTA + β2BS + β3CS + β4SS + β5TDTA*BS + β6TDTA*CS + β7TDTA*SS + e

ROA = a + β1LDTA + β2BS + β3CS + β4SS + β5LDTA*BS + β6LDTA*CS + β7LDTA*SS + e

ROE = a + β1LDTA + β2BS + β3CS + β4SS + β5LDTA*BS + β6LDTA*CS + β7LDTA*SS + e

ROA = a + β1SDTA + β2BS + β3CS + β4SS + β5SDTA*BS + β6SDTA*CS + β7SDTA*SS + e

ROE = a + β1SDTA + β2BS + β3CS + β4SS + β5SDTA*BS + β6SDTA*CS + β7SDTA*SS + e

In this equation, if the coefficient of the interaction between the independent variables (TDTA, LDTA and SDTA) and the moderator variables (BS, CS, SS) is statistically significant then it can be said to be moderator, and vice versa.

6. Empirical result and discussion

6.1. Descriptive statistics

shows the descriptive statistics related to the dependent, independent, and moderating variables. It can be seen that 71.64% of People’s Credit Bank assets are financed from debt (TDTA), of which 58.73% are in the form of savings (SDTA) and 10.88% in the form of loans (LDTA). This finding proves a point that the rural bank sector in Indonesia highly depends on savings in the form of regular savings and time deposits, while the remaining 28.36% is financed from the firm’s equity. Judging by the total assets (TA) owned by each rural bank, the average asset ownership is IDR 60,149,162,337.9. Meanwhile, the average equity is IDR 10,956,717,533.60. The provisions of the OJK require the rural bank to fulfil equity of at least 6 billion rupiahs. If reviewed in accordance with these provisions, the average rural bank fulfils the stipulated provisions (44.57%), and only 55.43% have complied with the provisions. The average total rural bank debt is IDR 49,192,444,804.30. The average rural bank income is IDR 1,500,523,041.50 with a minimum profit of IDR −43,392,611.00 and a maximum profit of IDR 79,652,785.00. Thus, not all rural banks gain profits. As many as 93 rural banks (18.23%) suffered losses, and the rest (81.77%) were able to yield profits.

Table 2. Descriptive statistics

Regulations from the Financial Fervices Authority concerning the Implementation of rural bank governance state that (1) rural banks that have core capital of at least IDR 50,000,000,000.00 (50 billion rupiahs) are required to have at least 3 members of the board of directors and (2) at least 2 members for those with less than IDR 50,000,000,000.00 (50 billion rupiah) capital. shows a minimum number of 1 person and a maximum of 4 people on the board of directors, with an average of 2.14 people, in rural banks. If examined more deeply, 259 rural banks (51.18%) failed to meet the required number of directors in accordance with the provisions, and only 157 rural banks (48.82%) have met the stipulated requirements.

Similar provisions are made for the number of board of commissioners: (1) a rural bank that has a core capital of at least IDR 50,000,000,000.00 (50 billion rupiahs) is required to have at least 3 members of the board of commissioners and a maximum of members of the Board of Directors, and (2) at least 2 members of the board of commissioners and a maximum number of members of the board of directors for those with a core capital of less than IDR 50,000,000,000.00 (50 billion rupiahs). shows the minimum number of commissioners (CS) at 0 and a maximum of 4 people, with an average of 1.57 people. If examined more deeply, 391 rural banks (77.27%) have not met the required number of commissioners, whereas only 110 rural banks (21.73%) have met the requirements.

6.2. Correlation analysis

presents the correlation coefficients between variables. All observational data won at 5% on both sides of the distribution before the correlation matrix was implemented. Financial performance variables (ROA, ROE) have a significant and high positive correlation at the 1% significance level, which indicates the variable alternation. The correlation coefficient between ROE and ROA is.723. The independent variable of the capital structure represented by TDTA has a significant positive correlation with ROA of .090 at the 5% significance level and positive with an ROE of .08 with a significance level of 5%. The independent variable of the capital structure represented by SDTA has a significant and positive correlation with ROA of .096 at a significance level of 5% and a significant correlation with ROE of .093 with a significance level of 5%. Meanwhile, long-term debt (LDTA) has a negative and insignificant correlation with ROA and ROE. CG variables provide different correlations with firm performance variables. CG is represented by the size of the board of directors (BS), the committee size (CS), and concentration of ownership (SS). These three have no significant correlation with both ROA and ROE.

Table 3. Correlation analysis

Regarding the correlation between CG and financial leverage, results show that the size of the board of directors (BS) has a significant positive correlation with TDTA, SDTA, and LDTA. Meanwhile, CS is not significantly correlated with TDTA. On the contrary, CS has a significant positive correlation with SDTA and LDTA Furthermore, the concentration of share ownership does not correlate with TDTA, SDTA, or LDTA. Finally, the relationship between CG elements shows that the size of the board of directors (BS) has a negative and significant correlation with the size of the board of commissioners (CS) and, conversely, has a positive correlation with the concentration of share ownership (SS). There is no correlation between the SS and the CS.

6.3. Regression analysis

6.3.1. Effect of leverage on ROA and ROE

The main effect of the ratio of total debt to total assets (TDTA) on ROA is shown in Model 1 in . These results indicate that TDTA has a significant positive effect on ROA (β = .202; sig. <.05). TDTA has a significant positive effect on ROE as shown in Model 3, (β = .324; sig. <.05). The long-term debt element (LDTA) has a negative and insignificant effect on ROA as seen in Model 5 in , (β = −.043; sig. >.10). While the effect of LDTA on ROE as seen in model 7 in (β = −.002; sig. >.10). shows that SDTA has a positive significant effect on ROA as seen in model 7 (β = .204; sig. <.05) and ROE as seen in model 9 (β = .324; sig. <.05). Therefore H1 is parcial supported, where if the leverage is measured by total debt or short term debt has a positive impact on company performance. However, if leverage is measured from long-term debt, it has no effect on firm performance. These results are consistent with those from the previous study, showing a positive effect of debt capital on profitability (Waweru, Citation2016). This result provides evidence that rural banks in their operations emphasize the use of short-term debt in the form of savings, both ordinary savings and savings deposits from their customers. This result is in line with MM theory which concludes that increasing debt can improve firm performance. With increasing debt, especially short-term bank debt (savings or customer deposits), the profitability will be better.

Table 4. Regression of TDTA, board size, committee size, and ownership concentration on ROA and ROE

Table 5. Regression of LDTA, board size, committee size, and ownership concentration on ROA and ROE

Table 6. Regression of LDTA, board size, committee size, and ownership concentration on ROA and ROE

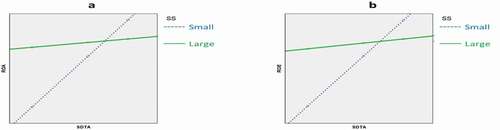

6.3.2. Moderating effect of BS on the relationship between leverage and performance

Based on the regression results of the interaction (TDTA*BS), it shows that the insignificant results as shown in model 2 in (β = .082; sig. >.10), while the regression results of the interaction between TDTA and BS (TDTA*BS) on ROE shown in model 4 in (β = −.018; sig. >.10).

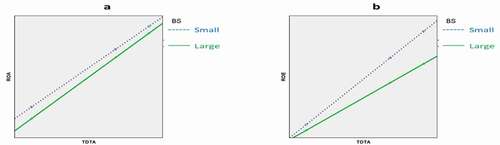

Figure 1. Moderating effect of BS on the relation between TDTA and ROA & ROE

) shows the moderating effect of BS on the relationship between TDTA and ROA, which illustrates the difference in line direction between small BS and large BS. Meanwhile, ) shows the moderating effect of BS on the relationship between TDTA and ROE, which illustrates the difference between the small BS and large BS lines. ) illustrates that between small BS and large BS there is no difference in line direction, this explains that the effect of TDTA on ROA does not depend on the number of BS. Likewise in ) illustrates that the effect of TDTA on ROE is slightly stronger at small BS.

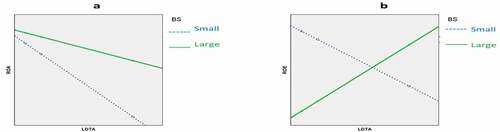

The moderating effect of BS on the relationship between LDTA and ROA and ROE is represented in the regression coefficient results of the interaction of LDTA and BS (LDTA*BS). The regression coefficient of LDTA*BS on ROA is positive but not significant as shown in model 6 (β = .043; sig. >.10). Likewise, the regression coefficient of LDTA*BS on ROE shows the same result as shown in model 8 in (β = .233; sig >.10). ) illustrates the moderating effect of BS on the relationship between LDTA and ROA, while ) illustrates the moderating effect of BS on the relationship between LDTA and ROE. ), it can be seen that the relationship between LDTA and ROA in small BS has a stronger negative effect than in large BS. This illustrates that more BS can reduce the negative impact of LDTA on ROA. Thus, it is better for firms to use large BS. Thus, in ) shows the same thing, where firms that use more BS have a better impact on ROE.

Figure 2. Moderating effect of BS on the relation between LDTA and ROA & ROE

The regression coefficient of SDTA*BS on ROA is positive but not significant as shown in model 10 (β = .143; sig. >.10). Likewise, the regression coefficient of SDTA*BS on ROE shows the same result as shown in model 12 in (β = −.115; sig. >.10). ) illustrates the moderating effect of BS on the relationship between SDTA and ROA, while ) illustrates the moderating effect of BS on the relationship between SDTA and ROE. Although the moderating effect of BS on the relationship between SDTA and ROA and ROE is not significant, and b) show the characteristics of the moderating effect of BS that the large number of BSs tends to have a slightly negative impact on the relationship between SDTA and both ROA and ROE. Therefore, if the company has a large BS, it will slightly reduce ROA and ROE.

Figure 3. Moderating effect of BS on the relation between SDTA and ROA & ROE

Therefore, H2 is not supported, the board size (BS) cannot strengthen the relationship between leverage and performance. This implies that BS is unable to moderate the effect of leverage on performance. Thus the strength of the effect of leverage on performance does not depend on the amount of BS. These results provide evidence to refute the view that a larger number of directors provide better access to resources than a smaller board. Moreover, the idea that larger boards may have more communication and experience and diversified knowledge and lead to efficient decisions in addition to more monitoring and control on management, resulting in better performance, is also rejected.

6.3.3. Moderating effect of CS on the relationship between leverage and performance

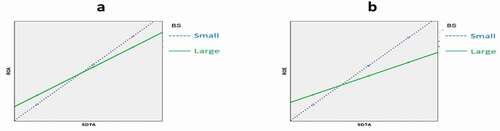

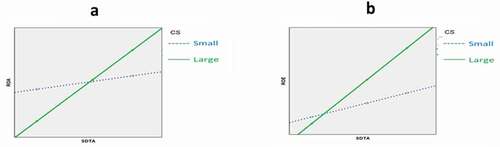

The moderating effect of the CS on the relationship between TDTA with ROA and ROE represented in interactions (TDTA*CS). The results showed that the moderating effect of CS on the relationship between TDTA and ROA was positive and significant as shown in model 4 (β = .403; sig. <.01). ) shows the moderating effect of CS on the relationship between TDTA and ROA, which illustrates the difference between the small CS and Large CS lines. The moderating effect of CS on the relationship between TDTA and ROE is shown in model 4 in (β = .485; sig. <.05). ) shows the moderating effect of CS on the relationship between TDTA and ROE, which illustrates the difference between the small CS and large CS lines. The two figures show that the effect of TDTA on ROA is positive if the firm has a large number of CS. This explains that the number of CS that meets the requirements can increase ROE and ROA. The large number of CS can increase the supervision of the director in making decisions related to debt.

Figure 4. Moderating effect of CS on the relation between TDTA and ROA & ROE

The regression results of the interaction between LDTA and CS (LDTA*CS) on ROA and ROE show insignificant results as shown in model 6 in (β = .010; sig. >.10) and model 8 in (β = −.181; sig. >.10). ) illustrates the moderating effect of CS on the relationship between LDTA and ROA, while ) illustrates the moderating effect of CS on the relationship between LDTA and ROE. These two figures illustrate that a large number of CS has a good impact on LDTA policies and on firm performance (ROA and ROE). This indicates that the addition of CS can increase the effectiveness of supervision, so that it can produce good performance.

Figure 5. Moderating effect of CS on the relation between LDTA and ROA & ROE

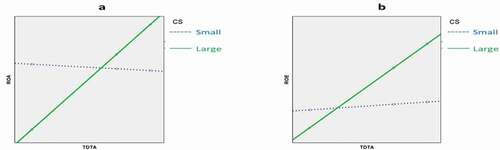

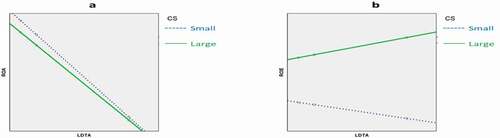

]The moderating effect of CS on the relationship between SDTA and ROA is positively significant as shown in model 10 in (β = .130; sig. <.05). On the other hand, the moderating effect of CS on the relationship between SDTA and ROE is not significant as seen in model 12 in (β = .307; sig. >.10). ) shows the difference in the relationship between SDTA and ROA if the number of CS is large and if the amount of CS is small. A large number of CS can have a good effect on the relationship between SDTA and ROA. Likewise, 6b shows that a large number of CS has a good impact on the relationship between SDTA and ROE.

Figure 6. Moderating effect of CS on the relation between SDTA and ROA & ROE

Based on this analysis, H3 is partially supported. Therefore CS is able to moderate the relationship between leverage (as measured by total debt or short-term debt) and firm performance. However, the opposite is not significant if the leverage is measured by long-term debt. This implies that the effect of leverage on performance will be stronger if the amount of CS is larger. The number of commissioners cannot increase the company’s performance. This suggests that a growing number of commissioners provide no evidence of improving supervisory performance.

6.3.4. Moderating effect of SS on the relationship between leverage and performance

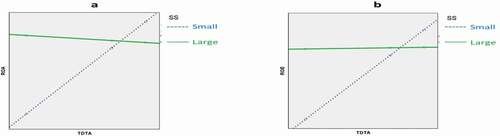

The moderating effect of SS on the relationship between TDTA and ROA is as shown in model 1 in (β = .027; sig. >.10), while the moderating effect of SS on the relationship between TDTA and ROE is shown in model 3 in (β = .015; sig. >.10). and ) show the difference between the small SS and large SS lines. Although the moderating effect of SS is not significant, and b) show the characteristics that a large number of SS has a negative impact on the relationship between TDTA and ROA and ROE. Therefore, in the case of rural banks, to strengthen the relationship between TDTA and ROA and ROE, a large number of shareholders is not required.

Figure 7. Moderating effect of SS on the relation between TDTA and ROA & ROE

The regression coefficient of the interaction between LDTA and SS (LDTA * SS) on the relationship between LDTA and ROA shows insignificant results (β = .005; sig. >.10) and the relationship between LDTA and ROE also shows insignificant results. Although the moderating effect of SS is not significant, ) shows that the relationship between LDTA and ROA, which does not show a difference in direction between large shareholders and small shareholders. ) has the same characteristics as ). Therefore, the size of SS does not affect the relationship between LDTA and ROA and ROE.

Figure 8. Moderating effect of SS on the relation between LDTA and ROA & ROE

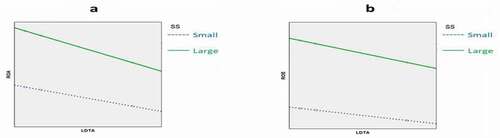

Furthermore, the moderating effect of SS on the relationship between SDTA and ROA shows a positive but insignificant result as seen in model 10 in (β = .009; sig. >.10). While the moderating effect of SS on the relationship between SDTA and ROE shows insignificant negative results, as in model 12 in (β = −.047; sig. >.10). This moderating effect is illustrated in and b). Although the moderating effect of SS on the relationship between SDTA and ROA and ROE is not significant, and b) illustrate the characteristics of the moderating effect of SS in that a large number of SS has a negative impact on the relationship between SDTA and ROA and ROE. Having a small number of SS has a positive impact on the relationship between SDTA and ROA and ROE.

Figure 9. Moderating effect of SS on the relation between SDTA and ROA & ROE

Therefore, SS is not able to moderate the relationship between leverage and firm performance. This result implies that SS is unable to moderate the relationship between leverage and performance. In other words, the strength of the relationship between leverage and the performance does not depend on the number of SS. This explains that a greater number of shareholders cannot provide effective control over the company’s activities.

7. Conclusion and Recomendations

The regression results provide moderate evidence of a significant positive relationship between capital structure as represented by total debt and firm performance as represented by ROA and ROE. Results indicate a positive contribution of capital structure financing decisions on financial performance. However, this is only true for short-term debt. Long-term debt has a negative and insignificant effect on both ROA and ROE. These results support the view of the pecking order theory, which consists of empirical evidence of the opposite effect between firm profits and capital structure.

A board size variable was added to the regression model to test for moderation effect (measured by interactions between leverage and corporate governance) on the relationship between capital structure (total debt, short-term debt, and long-term debt) and firm performance. Results showed that from several effects of these interactions, only interaction between leverage and commissioners had a significant effect. This means that the size of the board of commissioners affects on management funding decisions. On the contrary, board size and ownership concentration do not affect firm performance. Thus, companies with a larger board of commissioners can improve the control and monitoring functions of management decisions, thereby increasing firm performance. Conversely, board size has an insignificant influence on funding decisions related to the capital structure made by the firm management. Ownership concentration also has an insignificant effect on funding decisions related to the capital structure made by firm management. These results, however, are not sufficient to support the view that large shareholders can pressure managers to increase debt to reduce free cash flow in their best interest and increase their financial discipline to meet debt and interest repayments.

This result shows evidence of CG in Indonesia in the form of control and monitoring of capital structure decisions and can increase company value. With the presence of a commissioner, the opportunistic manager’s behaviour can be constrained, as evidence the commissioner can play an optimal role. Managers can make capital structure decisions, so that risky debt does not occur, resulting in an increase in firm value. In the case of Indonesia, what often happens is that managers act on their interests such as empire building, so that debt can reduce cash flow. If the company is in debt, the first is to pay interest and principal on the loan, thereby reducing managerial opportunistic behavior with additional monitoring from CG, thus increasing the value of the company.

Several limitations that may impact results have been noted in this study. CG in this study only takes the element of the CG mechanism; therefore, future studies should include a wider variety of CG variables (board characteristics, ownership structure, takeover and antitakeover mechanisms) to test their moderating effect on the relationship between capital structure and firm performance. This is because CG influence varies according to different political, judicial, social, and economic systems.

Additional information

Funding

Notes on contributors

Ngatno

Ngatno is an Associate Professor at Diponegoro University, Business Administration Department, Indonesia. Research interests in finance and business policy. I have several articles published in Scopus indexed journals. Several books published include Analysis of Mediation and Moderation Variables, Management Strategy.

Endang P Apriatni is an Associate Professor at Diponegoro University Business Administration Department, Semarang, Indonesia.

Arief Yoelianto is an Associate Professor at Semarang State University, Management Department, Semarang, Indonesia.

References

- Abor, J. Y. (2007). Corporate governance and financing decisions of Ghanaian listed firms. International Journal of Business in Society, 7(1), 83–22. https://doi.org/http://doi.org/10.1108/14720700710723131.

- Adams, R., & Mehran, H. (2002). Is corporate governance different for bank holding companies. Journal of Economic Policy Review-Federal Reserve Bank of New York, 9(1), 123–142.

- Almaqtari, Faozi A., Hamood Mohd Al-Hattami, Khalid M.E. Al-Nuzaili, and Mohammed A. Al-Bukhrani. 2020. Corporate Governance in India: A Systematic Review and Synthesis for Future Research. Cogent Business and Management, 7(1). https://doi.org/https://doi.org/10.1080/23111975.2020

- Arbor, J. (2005). The effect of capital structure on profitability: An empirical analysis of listed firms in Ghana. The Journal of Risk and Finance, 6(5), 438–447. https://doi.org/https://doi.org/10.1108/15265940510633505

- Arbor, J. (2007). Debt policy and performance of SMEs: Evidence from Ghanaian and South African firms. The Journal of Risk and Finance, 8(4), 364–379. https://doi.org/https://doi.org/10.1108/15265940710777315

- Belkhir, M. (2009). Board of directors’ size and performance in the banking industry. Journal of Managerial Finance, 5(2), 201–221. https://doi.org/https://doi.org/10.1108/17439130910947903

- Berger, P. G., Ofek, E. L. I., Yermack, & Yermack, D. L. (1997). Managerial entrenchment and capital structure decisions. The Journal of Finance, 52(4), 1411–1438. https://doi.org/https://doi.org/10.1111/j.1540-6261.1997.tb01115.x

- Besley, S., & Brigham, E. F. (2008). Essentials of managerial finance. Thomson South- Western.

- Bodaghi, A., & Ahmadpour, A. (2010). The effect of corporate governance and ownership structure on capital structure of Iranian listed companies. In 7th International Conference on Enterprise Systems, Accounting and Logistics (pp. 28–29).

- Cadbury, S. A. (2000). The corporate governance agenda. Corporate Governance: An International Review, 8(1), 7–15. https://doi.org/https://doi.org/10.1111/1467-8683.00175

- Caprio, G., Laeven, L., & Levine, R. (2007). Governance and banks valuations. Journal of Financial Intermediation, 16(October), 584–617. https://doi.org/http://doi.org/10.1016/j.jfi.2006.10.003

- Chinaemerem, O., & Anthony, O. (2012). Impact of capital structure on the financial performance of Nigerian Firms. Oman Chapter of Arabian Journal of Business and Management Review, 1(12), 43–61. https://doi.org/http://doi.org/10.12816/0002231.

- Coleman, A., & Biekpe., N. (2006). The relationship between board composition CEO duality and firm performance. Corporate Ownership & Control, 4(2), 114–122. https://doi.org/https://doi.org/10.22495/cocv4i2p11

- Cornelius, P. (2005). Governance good corporate practices in poor corporate governance system. Corporate Governance, 5(3), 12–23. https://doi.org/https://doi.org/10.1108/14720700510604661

- Craig, V. V. (2005). The changing corporate governance environment: Implications for the banking industry. FDIC Banking Review, 16(4), 1–15.

- Drobetz, W., Schillhofer, A., & Zimmermann, H. (2004). Corporate governance and expected stock returns: Evidence from Germany. European Financial Management, 10(2), 267–293. https://doi.org/https://doi.org/10.1111/j.1354-7798.2004.00250.x

- Fayez, M., Ragab, A. A., & Moustafasoliman, M. (2019). The impact of ownership structure on capital structure : An empirical study on the most active firms in the Egyptian stock exchange. Open Access Library Journal, 6(e5266), 1–13.http://doi.org/10.4236/oalib.1105266.

- Ferrero-Ferrero, I., Fernández-Izquierdo, M. Á., & Muñoz-Torres, M. J. (2012). The impact of the board of directors characteristics on corporate performance and risk-taking before and during the global financial crisis. Review of Managerial Science, 6(3), 207–226. https://doi.org/https://doi.org/10.1007/s11846-012-0085-x

- Ganiyu, Y. O., & Abiodun, B. Y. (2012). The impact of corporate governance on capital structure decision of Nigerian firms. Research Journal in Organizational Psychology & Educational Studies, 1(2), 121–128.

- Gill, A., Biger, N., & Mathur, N. (2011). The effects of capital structure on profitability : Evidence from United States The effect of capital structure on profitability : Evidence from the United States. International Journal of Management, 28(4), 3–15.

- Gompers, P. A., Ishii, J., & Metrick, A. (2003). Corporate governance and equity prices. Quarterly Journal of Economics, 118(1), 107–156. https://doi.org/https://doi.org/10.1062/00335530360535162

- Grossman, S. J., & Hart, O. (1982). Corporate financial structure and managerial incentives (McCall, J.). University of Chicago Press.

- Haque, F., Arun, T., & Kirkpatrick, C. (2011). Corporate governance and capital structure in developing countries: A case study of Bangladesh. Applied Economics, 43(6), 673–681. https://doi.org/https://doi.org/10.1080/00036840802599909

- Harris, M., & Raviv, A. (1988). Corporate control contests and capital structure. Journal of Financial Economic, 20(1-2), 55–86. https://doi.org/https://doi.org/10.1016/0304-405X(88)90040-2

- Harris, M., & Raviv, A. (1991). The theory of capital structure. The Journal of Finance, 46(1), 297–355. https://doi.org/https://doi.org/10.1111/j.1540-6261.1991.tb03753.x

- Hart, O. (1995). Corporate governance: Some theory and implications. The Economic Journal, 105(430), 678–689. https://doi.org/https://doi.org/10.2307/2235027

- Hassan, A., & Butt, S. A. (2009). Impact of ownership structure and corporate governance on capital impact of ownership structure and corporate governance on capital structure of Pakistani listed companies. International Journal of Business and Management, 4(2), 50–57. https://doi.org/http://doi.org/10.5539/ijbm.v4n2p50.

- Heng, T. B., Azrbaijani, S., & San, O. T. (2012). Board of directors and capital structure: Evidence from leading Malaysian companies. Asian Social Science, 8(3), 123–136. https://doi.org/https://doi.org/10.5539/ass.v8n3p123

- Hermalin, B., & Weisbach, M. (1988). The determinants of board composition. Rand Journal of Economics, 19(4), 7–26. https://doi.org/https://doi.org/10.2307/2555459

- Hussainey, K., & Aljifri, K. (2012). Corporate governance mechanisms and capital structure in UAE. Journal of Applied Accounting, 13(2), 145–160. https://doi.org/https://doi.org/10.1108/09675421211254849

- Ibrahim, I. (2016). Ownership structure and dividend policy of listed deposit money banks in Nigeria: A Tobit regression analysis. International Journal of Accounting and Financial Reporting, 6(1), 1–18. https://doi.org/https://doi.org/10.5296/ijafr.v6i1.9277

- Ishii, J., & Metrick, A. (2003). Corporate governance and equity prices. The Quarterly Journal of Economics, 118(1), 107–156. https://doi.org/https://doi.org/10.1162/00335530360535162

- Isik, O., & Ince, A. R. (2016). Board size, board composition and performance : An investigation on Turkish Board size, board composition and performance : An investigation on Turkish Banks. International Business Research, 9(2), 74–84. https://doi.org/https://doi.org/10.5539/ibr.v9n2p74

- Jaccard, J., Turrisi, R., & Wan, C. K. (1990). Interaction effects in multiple regression. Sage.

- Jahanzeb, A., Bajuri, N. H., & Ghori, A. (2015). Market power versus capital structure determinants: Do they impact leverage? Cogent Economics and Finance, 3(1), 1017948. https://doi.org/https://doi.org/10.1080/23322039.2015.1017948

- Jensen, C., & Meckling, H. (1976). THEORY OF THE FIRM : MANAGERIAL BEHAVIOR, AGENCY COSTS AND OWNERSHIP STRUCTURE I. Introduction and Summary in This Paper WC Draw on Recent Progress in the Theory of (1) Property Rights, Firm . In Addition to Tying Together Elements of the Theory of E, 3, 305–360.

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs costs and ownership structure. Journal of Financial Economics, 3(4), 305–359. https://doi.org/https://doi.org/10.1016/0304-405X(76)90026-X

- Kabir, R., Cantrijn, D., & Jeunink, A. (1997). Takeover defenses, ownership structure and stock returns in the Nederlands : An empirical analysis. Strategic Management Journal, 18(March), 97–109. https://doi.org/https://doi.org/10.1002/(SICI)1097-0266(199702)18:2<97::AID-SMJ855>3.0.CO;2-2

- Lukas, K., & Ondrej, Č. (2016). The effect of ownership structure on corporate financial performance in the Czech Republic. Ekonomický Časopis, 64(č. 5, s), 477–498.

- Mardones, J. G., & Cuneo, G. R. (2020). Capital structure and performance in Latin American companies. Economic Research-Ekonomska Istrazivanja, 33(1), 2171–2188. https://doi.org/https://doi.org/10.1080/1331677X.2019.1697720

- Mburu, & Kagiri. (2013). Effects of board composition on financial performance of banking institutions listed at Nairobi securities exchange. International Journal of Science and Research, 6(14), 2319–7064.

- Mollah, S., Farooque, O. A., & Karim, W. (2012). Evidence from an African emerging market. Studies in Economics and Finance, 29(4), 301–319. https://doi.org/https://doi.org/10.1108/10867371211266937

- Morellec, E., Nikolov, B., & Schurhoff, N. (2012). Corporate governance and capital structure dynamics. The Journal of Finance, 67(3), 803–848. https://doi.org/https://doi.org/10.1111/j.1540-6261.2012.01735.x

- Munisi, G., & Randøy, T. (2013). Corporate governance and company performance across Sub-Saharan African countries. Journal of Economics and Business, 70(November-December), 92–110. https://doi.org/https://doi.org/10.1016/j.jeconbus.2013.08.003

- Nandi, S., & Ghosh, S. K. (2012). Corporate governance attributes, firm characteristics and the level of corporate disclosure : Evidence from the Indian listed firms.Decision Science Letters2(1): 45-58. https://doi.org/http://doi.org/10.4267/j.dsl.2012.10.004.

- Nodeh, F. M., Anuar, M. A., Ramakrishnan, S., & Raftnia, A. A. (2016). The effect of board structure on banks financial performance by moderating firm size. Mediterranean Journal of Social Sciences, 7(1), 258–263. https://doi.org/http://doi.org/10.5901/mjss.2016.v7n1p258.

- Noor, A. A., & Ayoib, C. A. (2009). Family business, board dynamics and firm value: Evidence from Malaysia. Journal of Financial Reporting and Accounting, 7(1), 53–74. https://doi.org/https://doi.org/10.1108/19852510980000641

- Nowak, O., & Kubíček, A. (2012). Corporate governance and company performance : Evidence from the Czech Republic. In Advances in Economics Risk Management, Political and Law Science, 235–240.

- O’Connell, V., & Cramer, N. (2010). The relationship between firm performance and board characteristics in Ireland. European Management Journal, 28(5), 387–399. https://doi.org/https://doi.org/10.1016/j.emj.2009.11.002

- Omondi, M., & Muturi, W. (2013). Factors affecting the financial performance of listed companies at the Nairobi securities exchange in Kenya. Research Journal of Finance and Accounting, 4(15), 99–104.

- Rashid, K., & Nadeem, S. (2014). The Role Of Ownership Concentration, Its Types And Firm Performance: A quantitative study of financial sector in Pakistan. Oeconomics of Knowledge, 6(2), 10–61. http://econpapers.repect.org,RePEC:eok:journl:v:6:y:2014:i:2:p:10-61.

- Ross, S. (1977). The determination of financial structure: The incentive signalling approach. Bell Journal of Economics, 8(1), 23–40. https://doi.org/https://doi.org/10.2307/3003485

- Sheikh, D. N., & Wang, Z. (2012). Effects of corporate governance on capital structure: Empirical evidence from Pakistan. Corporate Governance: The International Journal of Business in Society, 12(5), 629–641. https://doi.org/https://doi.org/10.1108/14720701211275569

- Shleifer, A., & Vishny, R. W. (1997). A survey of corporate governance. The Journal of Finance, 52(2), 737–783. https://doi.org/https://doi.org/10.1111/j.1540-6261.1997.tb04820.x

- Thi, B., Dao, T., Dieu, T., & Ta, N. (2020). A meta-analysis : Capital structure and firm performance. Journal of Economics and Development, 22(1), 111–129. https://doi.org/https://doi.org/10.1108/JED-12-2019-0072

- Tran, N. H., Le, C. D., & Mcmillan, D. (2020). Ownership concentration, corporate risk-taking and performance : Evidence from Vietnamese listed firms. Cogent Economics & Finance, 8(1), 1–41. https://doi.org/http://doi.org/10.1080/23322039.2020.1732640.

- Tsifora, E, and P. Eleftheriadou. (2007). Corporate Governance Mechanisms and Performance : Evidence from Greek Manufactoring Sector. Management of International Business and Economic Systems, 1(1), 181–2011.

- Tulung, J. E., & Ramdani, D. (2018). Independence, size and performance of the board : An emerging market research. Corporate Ownership & Control, 15(2), 201–208. https://doi.org/https://doi.org/10.22495/cocv15i2c1p6

- Van Horne, J. C., & Wachowicz, J. M. (2008). Fundamentals of financial management. Prentice Hall.

- Waweru, M. W. (2016). Effect of capital structure on profitability of microfinance institutions in Nakuru Town, Kenya. International Journal of Economics, Commerce and Management, 4(10), 1144–1167. https://doi.org/http://doi.org/10.9790/487x-1810044349

- Wen, Y., Rwegasira, K., & Bilderbeek, J. (2002). Corporate governance and capital structure decisions of the Chinese listed firms”. Corporate Governance. AnInternational Review, 10(2), 75–83.