?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the role of domestic governance quality on the relationship between Chinese foreign direct investment (FDI), domestic investment, and African countries’ economic growth. The study utilized a larger dataset of Chinese FDI to 44 African countries applying the two-step system GMM estimation method for 2003–2017. This study’s findings reveal that Chinese FDI’s impact on economic growth is conditional to improving African countries’ aggregate and each component of individual governance indicators used to represent the countries’ institutional quality. The impact of Chinese FDI on African countries’ domestic investment is robustly positive. Besides, improvement in the governance environment stimulates the effect of Chinese FDI on domestic investment. More specifically, control of corruption, government effectiveness, and voice and accountability have mediating roles in the nexus of Chinese FDI and African countries’ domestic investment. Thus, African countries aiming to attract Chinese FDI and promote their economic growth and domestic investment need to improve governance quality.

PUBLIC INTEREST STATEMENT

Foreign direct investment (FDI) impacts the economic performance of countries. It affects the host countries’ domestic investment and economic growth negatively or positively. Thus, FDI receiving countries will have hardly any or many benefits from multinational firms, or their economic performance will be adversely affected by FDI. The role of FDI to enhance domestic investment and economic growth depends on specific characteristics to host countries’ business environment and absorptive capability. In this regard, good governance can play a significant role in determining the domestic investment and growth impacts of FDI. It can mediate the relationship between FDI and domestic investment and economic growth and FDI. Thus, we examined the effects of Chinese FDI on domestic investment and African countries’ economic growth, taking into account the moderating role of good governance indicators.

1. Introduction

Growing China-Africa economic relations received much attention among scholars and policymakers. This economic relation between Africa and China can be revealed in terms of FDI flow, foreign trade, and the development of financial aid from China to African countries. The literature on Africa-China’s relationship often falls under two broad categories: those who argue that the relationship is a positive for both China and African countries and those who view the relationship as a new form of imperialism. One particular focal point is African countries’ resource exploitation (Foster et al., Citation2008; Kolstad & Wiig, Citation2011).

More specifically, the impact of Chinese FDI on the economic growth of African countries is controversial. Some scholars argue that Chinese FDI to African countries has a negative or insignificant effect on African countries’ economic growth. For example, in a study by Busse et al. (Citation2016), FDI in Africa does not have an effect on the economic performance of African countries. They argue that FDI flows from China to African countries seem to play no major role in African countries’ economic development. Furthermore, China’s investment in Africa is generally perceived to follow the state-driven strategy of giving infrastructure and taking natural resources. More specifically, Foster et al. (Citation2008) listed some Chinese-financed infrastructure projects in Africa paid for by natural resources and raw materials, bringing a negative impact on African countries. Therefore, access to natural resources played a significant role in the Chinese FDI flow to African countries. Sanfilippo (Citation2010) empirically investigates the determinants of Chinese FDI in African countries and concludes that natural resources endowments and market potential drive Chinese FDI to Africa. The findings of the aforementioned literature are consistent because a host country’s natural resources have a significant effect on China’s decision on the actual amount to invest in the country; it does not affect rather than on whether to invest in the country or not (Kolstad & Wiig, Citation2011).

On the other hand, the strong interrelationship between Chinese FDI and economic cooperation indicates China’s significant role in African countries’ economic arena. A study by Pigato and Tang (Citation2015) concludes that many African countries have benefited from an increasingly favorable external environment, especially China’s strong demand for natural resources. However, a significant amount of Chinese investment is focused on a few resource-rich countries slow expansion to resource-poor countries. Furthermore, Doku et al. (Citation2017) indicate that an increase in China’s FDI in African countries promotes African countries’ economic growth. Moreover, Whalley and Weisbrod (Citation2012) suggest that a significant portion of some African countries’ accelerated growth is attributed to Chinese FDI inflows. However, Zhang et al. (Citation2014) find that Chinese FDI (total net FDI inflows and inflows from China) has no significant impact on African growth. Hence, this literature provides mixed evidence on the impacts of Chinese FDI on African countries’ economic growth. There is also concern that Chinese FDI in Africa has little skills transfer to Africans.

However, the mixed results on the impact of Chinese FDI on economic growth to African countries can be partly because of failure to control the institutional environment of African countries in their analysis as the institutional quality (good governance) can play a significant role in determining the growth impact of foreign direct investment (Ali et al., Citation2010; Jude & Levieuge, Citation2017; Khordagui & Saleh, Citation2013). Additionally, a study by Benáček et al. (Citation2014) finds that domestic institutions of FDI receiving countries are key factors in determining FDI flows, although results differ depending on the groups of countries considered. Thus, institutional quality modulates the two main channels of FDI-led growth, namely knowledge spillovers, and capital accumulation. In light of these arguments, we indicate that sound institutional quality is expected to favor economic growth to domestic economies.

Furthermore, some studies argue that FDI flow significantly affects domestic investment subject a targeted approach to FDI by increasing countries’ absorption capacity (Adams, Citation2009) FDI, mostly, Greenfield FDI has stronger long‐run complementarities with domestic investment. However, mergers and acquisitions do not significantly affect domestic investment (Juda, Citation2018). More specifically, the results of Megbowon et al. (Citation2019) indicate that China’s FDI in African countries has an insignificant effect on industrialization. Likewise, Busse et al. (Citation2016) reveal the displacement effect of African firms due to competition from China.

Therefore, this study’s main objective is to examine the effects of China’s FDI on the economic growth and domestic investment of African countries controlling the mediating role of domestic governance (institutional) quality of African countries.

2. Literature review

2.1. Chinese FDI and economic growth

The relationship between economic growth and FDI has been explained in different theoretical frameworks. The dependency theorists promoted early theories on FDI and its effect on FDI host economies’ economic growth. From a theoretical point of view, the dependency intellectuals claim that FDI flow from the advanced economies have a negative effect on the long-term economic growth of developing nations because the target FDI receiving countries will have very few benefits as the results of price distortions due to protectionism; market monopolization; and, natural resources depletion (Bos et al., Citation1974).

On the other hand, some other theoretical literature reveals that FDI flow to developing countries is particularly essential for developing economies as it provides access to resources that would otherwise be unavailable to developing countries. The positive relationship between FDI and economic growth is deeply discussed in the neo-classical school of thought. For example, according to the neo-classical exogenous growth model of Solow (Citation1956) and Solow (Citation1957), economic growth is a function of the capital, labor force, keeping technology exogenous. The theory assumes that economic growth is generated through the accumulation of exogenous factors of production, such as the stock of capital and labor. Empirical studies on economic growth using the exogenous model normally employ the aggregate production function. It has been shown that through this framework, capital accumulation contributes directly to economic growth in proportion to capital’s share of the national output.

Furthermore, the growth of the economy depends on the augmentation of the labor force and technological progress. According to this theory, FDI increases the capital stock in the country receiving FDI; and this would, in turn, influence economic growth. This model provides evidence that capital accumulation promotes the economic growth of countries. In this framework, thus, FDI can affect economic growth directly via capital accumulation and the inclusion of new factors of production in the production function of the FDI host country (Mahembe & Odhiambo, Citation2014). This shows that FDI directly causes an increase in production by contributing tangible assets to the economy.

The Solow–Swan exogenous growth model was challenged by the endogenous growth model (Romer, Citation1990). The endogenous growth model emphasizes the role of technology; FDI remained assumed to transfer technology, improving domestic productivity (Johnson, Citation2006). Besides, Nair-Reichert and Weinhold (Citation2001) argue that the endogenous growth model takes into account long-run growth as a function of technological progress and is affected by improvement in technology. Thus, they propose a framework in which FDI can improve the host country’s economic growth through technology transfer and spillover effects.

The two growth theories and the relationship between FDI and economic growth reveal that FDI can improve the economic growth of countries through direct and indirect impacts. Therefore, FDI can boost the host country’s economy by adding to capital accumulation, promoting domestic investment, and resulting in productivity spillover. Therefore, theoretically, FDI can play a significant role in economic growth by raising capital accumulation and technological spillovers (Herzer et al., Citation2008).

Additionally, the theoretical framework of the relationship between FDI flow and economic growth has been evaluated by a number of empirical studies. For example, including some African countries, Khordagui and Saleh (Citation2013) examined the relationship between foreign direct investment and economic growth, considering domestic absorptive capacity in emerging economies. The findings of their study imply that the effect of FDI conditional to human capital, trade openness, and institutional quality of FDI receiving countries.

Likewise, Jude and Levieuge (Citation2017) investigate the effect of FDI on economic growth conditional on host countries’ institutional quality. To show the relationship between economic growth and FDI, the stimulating role of institutional quality, they developed several theoretical arguments and showed that institutional heterogeneity could be one of the explanations for the mixed results of previous empirical studies. Additionally, their results show that some reforms appear to promote faster marginal contributions of FDI, while governance improvement may result in an incremental impact on economic growth and development. Hence the impacts of FDI to enhance economic growth will depend on the domestic absorptive capacity of FDI receiving countries.

As this study aims to examine the impact of Chinese FDI on African countries, the empirical study, we further emphasis on the discussion of literature regarding the relationship between Chinese FDI and economic growth of African countries. Based on the previous studies on the nexus of Chinese FDI and economic performance, its impact on African countries’ economic performance is mixed.

Some scholars argue that Chinese FDI to African countries has a negative or insignificant effect on African countries’ economic growth. For example, studies by Foster et al. (Citation2008), Zhang et al. (Citation2014), and Busse et al. (Citation2016) imply that Chinese foreign investment in Africa does not have an impact on the economic growth of African countries. They argue that FDI flows from China to African countries seem to play no major role in African countries’ economic development. On the other hand, Whalley and Weisbrod (Citation2012), Pigato and Tang (Citation2015), and Doku et al. (Citation2017) find that the accelerated growth in some African countries can be attributed to Chinese FDI inflows.

However, the mixed results on the impact of Chinese FDI on economic growth to African countries can be partly because of failure to control the institutional environment of African countries in their analysis as the institutional quality can play a significant role in determining the growth impact of foreign direct investment (Ali et al., Citation2010; Jude & Levieuge, Citation2017; Khordagui & Saleh, Citation2013). Additionally, a study by Benáček et al. (Citation2014) finds that domestic institutions of FDI receiving countries are key factors in determining FDI flows, although results differ depending on the groups of countries considered. Thus, institutional quality modulates the two main channels of FDI-led growth, namely knowledge spillovers, and capital accumulation. In light of these arguments, we indicate that sound institutional quality is expected to favor productivity spillovers to domestic economies. A similar dynamic panel data model was used by (Acemoglu & Johnson, Citation2005) to estimate the role of democracy in economic growth. This paper adopts a similar dynamic panel data model to evaluate the impact of institutional quality on economic growth and the FDI-growth relationship.

In regard to mixed empirical results on the relationship between FDI and economic growth, other studies suggest that the effect of FDI on economic growth depends on characteristics that are specific to host countries and that the country has a minimum level of absorption capacity in terms of human capital, institutional infrastructure, and market liberalization which allows for the exploitation of the benefits of FDI (Adams, Citation2009). Thus, the mixed results on the FDI-growth relationship have led to our study’s focus on the host country’s absorptive capacity in the nexus of FDI-economic growth.

Therefore, based on the literature above, the following hypothesis is articulated.

Hypothesis (H1): The impact of Chinese FDI on African countries’ economic growth is positive conditional to African countries’ institutional environment.

2.2. FDI and domestic investment

FDI affects domestic investment by affecting the domestic capital formation, as foreign firms’ entry can change the spurs to invest by domestic firms. There are a number of channels that the FDI significantly affects domestic investment. First, FDI can act as a catalyst for domestic investment because multinationals usually have greater access to information and financial resources than most private investors do in developing countries. A study by Herzer et al. (Citation2008) has found that FDI promotes economic growth by augmenting domestic investment. Besides, the neoclassical growth model shows that FDI positively contributes to economic growth by increasing the amount and investment efficiency in the host country (Mahembe & Odhiambo, Citation2014). Additionally, the theoretical standpoint on the impact of institutional quality in the relationship between FDI and domestic investment is found on spillovers of FDI. In other words, the large spillovers from FDI flow to host countries domestic producers propose higher domestic investment because they increase the rate of return to domestic investment. Therefore, if spillovers are high, we may expect that FDI promotes domestic investment (Farla et al., Citation2016). According to the study by Adams (Citation2009), FDI flow significantly affects domestic investment conditional to a targeted approach to FDI by increasing countries’ absorption capacity. Some literature indicates that China’s FDI in African countries has an insignificant effect on industrialization, and there is also a displacement effect on African countries’ local private investment due to competition from China (Busse et al., Citation2016; Megbowon et al., Citation2019). Additionally, a study by Al-Sadig (Citation2013) examining the effects of FDI inflows on private investment in developing host countries. The results show that FDI stimulates domestic investment. Hence, based on this literature, the following hypotheses have been developed.

2.3. H2A: Chinese FDI has a positive effect on domestic investment of African countries

H2B: The domestic absorptive capacity (institutional quality) has a mediating role on the impact of Chinese FDI on domestic investment.

3. Methodology and data

3.1. Method of analysis

This part primarily emphasizes the methods to analyze the effects of China’s FDI on the domestic investment and economic growth of African countries. A dynamic panel data model is applied to examine the impacts of Chinese FDI on the African countries’ economic growth, using the neoclassical augmented growth model developed by Mankiw et al. (Citation1992) that associates economic growth with various explanatory determinants and on domestic investment of African countries.

The two-step system GMM estimator of Arellano and Bover (Citation1995) is applied to examine the impacts of FDI on African countries’ growth and domestic investment based on a number of reasons. First, the analysis of the effect of Chinese FDI on the growth and investment is based on time-series and cross-country data using a sample of 44 African countries for the years 2003–2017. Second, the dynamic phenomenon of economic growth can be captured by suitable dynamic panel models. THEREFORE, to de this dynamic phenomenon, the system GMM model is suitable. Third, it can address the endogeneity problem and gives consistent estimates, even in the presence of measurement error. FDI contributes positively to the economic growth of FDI receiving countries, and positive economic growth stimulates FDI inflows positively. Therefore, FDI may not only contribute to higher economic growth, but growing markets might attract multinational corporations. The size of a particular market is likely to be an indication of its level of attractiveness to the FDI, in the case that the multinational corporation aims to produce for the local market, thereby promoting economic growth of the host country (Busse, Citation2004). That means, on theoretical bases, there is a bi-directional relationship between FDI and economic growth (Türkcan & Yetkiner, Citation2008). The lagged value of the dependent variable is widely used as an instrument for the level variable to deal with the issue (Alfaro et al., Citation2004). That is, the dynamic nature of the model allows us to control this issue; therefore, the lagged value of the dependent variable is used to deal with the endogeneity issue (Arshad, Citation2017). The two-step system GMM model is suitable because it extended the original model by adding equations in levels to the regressions run in first differences. The second equation allows for introducing additional instruments. For endogenous variables in levels, their own lagged differences serve as instruments (Arrelan and Bond, 1991). Fourth, this method gives efficient inference, supposing a minimal set of statistical assumptions (Arellano & Bover, Citation1995).

Overall, the two-step system GMM is a method aimed at situations with a large number of panels (N) and small-time (T). It is a systematic method with numerous individual units and a few time with a linear functional relationship among dependent variable that is dynamic, affected by its past and explanatory variables that are associated with past and possibly current realizations of the error fixed individual effects and not strictly exogenous, indicating autocorrelation within individual units’ errors and unobserved heterogeneity. In the model specification, Chinese FDI is included as endogenous because there will be a reverse causality between China’s FDI and the economic growth of African countries.

Based on the above information, an equation that relates the dependent variable (real GDP per capita growth) to Chinese FDI to Africa and other control variables is specified in the following equation.

Where gr represents the growth rate of African countries (dependent variable), grit-1 is the lag of the dependent variable. FDIchina is Chinese FDI to Africa, k represents the capital of African countries, gexp is government final consumption expenditure, inf is the inflation rate, trade is trade openness of African countries, aid is aid allocation to African countries, resour is resources availability and utilization of African countries, L is labor force participation rate, FDIchina*ins is the interaction term of institutional quality and Chinese FDI to African countries and εit is the stochastic term.

We treat lagged GDP per capita growth and Chinese FDI variables as endogenous, on the ground of potential reverse causality, and we instrument them using their lagged levels and differences. The dynamic nature of the equation with the lagged value of the dependent variable (growth) is included as one of the explanatory variables enables us to capture any relevant variable excluded from the model (Arshad, Citation2017). The coefficient of the lagged value of the dependent variable (growth) can take any sign. It can be positive, implying conditional convergence and negative if there are conditional divergence (Siyakiya, Citation2017; Slesman et al., Citation2015).

Government final consumption expenditure is used as a proxy of the government fiscal policy. General government final consumption expenditure as a percentage of GDP is used in this study. An increase in government spending is assumed to be associated with low economic growth (Siyakiya, Citation2017; Jude & Levieuge, Citation2017).

Foreign aid received by African countries is included in the specification to examine its impact on the economic growth of African countries in line with a study by Driffield and Jones (Citation2013). Trade openness is represented by the percent of trade per GDP of African countries. It shows the degree of openness of a country to the rest of the world. Highly opened economies are usually associated with high levels of economic growth (Siyakiya, Citation2017; Jude & Levieuge, Citation2017).

Good governance indicators of African countries are included to represent the institutional quality of African countries. The aggregate institutional quality index is developed using a ranking of six dimensions of good governance: control of corruption, government effectiveness, political stability and absence of violence or terrorism, regulatory quality, the rule of law and voice and accountability (Siyakiya, Citation2017).

The inflation rate represents macroeconomic stability captured by annual consumer price inflation. The higher inflation rate negatively affects economic growth (Siyakiya, Citation2017; Tamilina & Tamilina, Citation2014; Jude & Levieuge, Citation2017). Resources consumption, mainly energy (oil, fuel, and gas) usage, is controlled following the works of James and Aadland (Citation2011) that provides evidence of the positive growth effects of natural resource extraction.

Besides, the econometric equation estimated for the effect of Chinese FDI on domestic investment is specified in the following equation.

Where gfcf represents the domestic investment, gfcfit-1 is the lagged value of the dependent variable, g is the growth rate of per capita GDP, FDIchina is Chinese FDI to African countries, inf is the inflation rate of the countries, cre is the credit to the private sector, trade is the trade openness of the countries, aid is foreign aid to African countries, infra is the level of infrastructure of African countries, efree represents economic freedom of African countries, FDIchina*ins is the interaction of Chinese FDI and institutional quality and η is the stochastic term.

The dependent variable (domestic investment) is proxied by gross fixed capital formation. It represents the country’s investment share in the economy (Farla et al., Citation2016; Nawaz et al., Citation2014; Siyakiya, Citation2017). The lagged value of the dependent variable is included to control as one of the explanatory variables to capture the dynamic nature (Hecht et al., Citation2004). Chinese FDI and domestic credit are supposed to have a positive effect on domestic investment (Luca & Spatafora, Citation2012). FDI can positively affect domestic investment (Hecht et al., Citation2004).

Institutional quality indicators are controlled to following the works of Farla et al. (Citation2016) that used good governance to proxy the institutional quality of countries. Besides, economic freedom indicator is included in the model to proxy economic institutions following the study by Kalu, Gwatidzo and Kaniki (Citation2010) revealed that property right is the key channel through which better legal system influences investment.

The interaction between Chinese FDI and governance indicators of African countries is included to investigate the mediating role of good governance in the relationship between Chinese FDI and domestic investment (Farla et al., Citation2016).

The growth rate of per capita GDP is controlled to account for the fact that current investment decisions depend on the expected flow of future returns, increasing per capita income (Farla et al., Citation2016; Hecht et al., Citation2004). The inflation rate is included to proxy the macroeconomic stability of African countries. A price increase is expected to affect domestic investment negatively (Luca & Spatafora, Citation2012). The total trade per GDP of African countries is used to represent the trade openness of African countries. Trade openness can affect domestic investment substantially (Luca & Spatafora, Citation2012).

Financial aid to African countries is included in the specification, supposing that it can affect domestic investment. Financial aid to developing countries appeared to negatively affect domestic investment unless it is properly utilized (Salahuddin & Islam, Citation2008).

3.2. The data

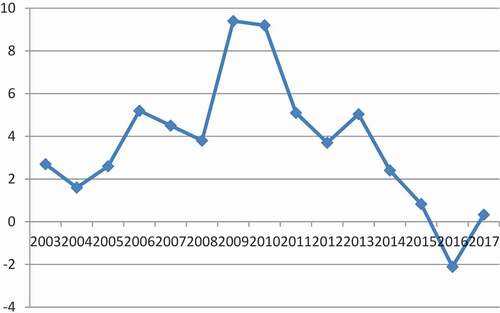

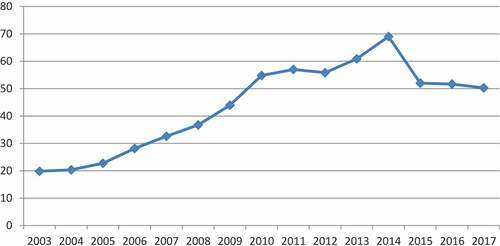

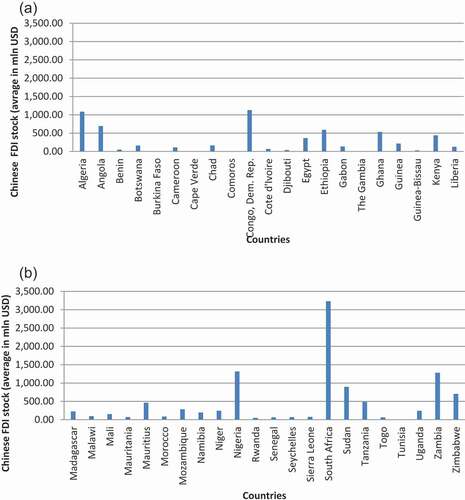

This study utilized data for the time periods 2003–2017 based on the data availability for 44 African countries. The list of countries is reported in Appendix B. The data used for this research are drawn from various sources. Chinese FDI to Africa is compiled from China Statistical Yearbook by Johns Hopkins China-Africa Research Institute. in the appendix show the flow and stock of Chinese FDI to African countries for the given period of time. Among African countries, South Africa, Zambia and Nigeria were the top host countries of Chinese FDI (see and in Appendix C). The definition and source of data are presented in .

Figure 1. China’s FDI flow to Africa (in billion US dollars)

Figure 2. China’s FDI stock to Africa (in billion US dollars)

Figure 3. (a). China’s FDI stock in the sample African countries. (b). China’s FDI stock in the sample African countries

Table 1. Definition of variables and source of data

The institutional quality index is developed using institutional quality indicators such as control of corruption, absence of violence and security, the rule of law, government effectiveness, voice and accountability, and regulatory quality of African countries ().

Table 2. Principal component analysis for the institutional quality index

4. Results and findings

4.1. The impacts of Chinese FDI on economic growth

This segment focuses on findings of the impacts of Chinese FDI to African countries on economic growth for African countries. The correlation among variables and statistical summary are reported in and in Appendix A, respectively. presents the two-step system GMM estimates of the effects of the Chinese FDI on the economic growth of African countries. STATA 13 is utilized to run the regression. The regression command (xtabond2) developed by Roodman (Citation2009) for a dynamic panel data model has been utilized.

Table 3. The effects of Chinese FDI on growth

The diagnostic tests of the model have been conducted to evaluate the robustness of the model. The serial correlation test (AB2) is used to test serial correlation. The result supports the null that there is no second-order serial correlation problem. The Hansen test is used to examine the overall effectiveness of the instrumental variables in the two-step system GMM. The results indicate that there are no over-identification issues. Besides, the Wald test for the joint significance of the variables is used and does not reject the model specification. Column (I) reports the two-step system GMM results controlling for aggregate governance index. Column (II) shows results, including the labor force participation rate to the model. Column (III) presents the mediating role of governance index in the relationship between the economic growth of African countries and Chinese FDI. The labor force participation rate is separately treated in Column (II) because there is a high correlation between foreign aid and labor force participation rate (see in Appendix A).

The coefficient of lagged economic growth is positive and statistically significant in all specifications in line with expectations, which implies the existence of the dynamic adjustment process and positive resistance in economic growth.

Among traditional determinants of growth, capital and labor are significant determinants of growth in African countries. In the economic process, thus, physical capital accumulation and labor can be a primary engine for economic growth. Besides, resource abundance has a robust effect on economic growth as it is indicated by a positive and statistically significant coefficient. The effect of trade openness on growth is also positive and statistically significant. Therefore, trade openness facilities a faster movement of capital and contributes to the economic growth of African countries. It is in line with the view that argues international integration can be beneficial for economic growth. However, the impact of financial aid is negative and statistically significant.

Furthermore, the coefficient of governance quality index is positive and statistically significant, implying that improving the governance level in African countries promotes economic growth. Therefore, improving the institutional environment can play an essential role in promoting economic growth in African countries. This finding is consistent with the findings of Acemoglu and Johnson (Citation2005), Robinson and Acemoglu (Citation2012), Tamilina and Tamilina (Citation2014), and Siyakiya (Citation2017) that provide evidence that good institutions provide a conducive environment that stimulates rapid economic growth.

Turning to the variable of our interest, the impact of Chinese FDI is robustly negative, indicating a negative association between Chinese FDI and growth when we consider it individually. The negative effect of Chinese FDI on the economic growth of African countries can be explained because the impacts of FDI on economic growth should be mediated by the domestic adaptive capability to utilize the benefit of Chinese FDI to stimulate economic growth. This finding on the impacts of China’s FDI economic growth of African countries is not astonishing because many empirical studies on the growth-FDI relationship found inconclusive results. For instance, Bruno and Campos (Citation2013) show that 50% of empirical studies find robustly positive impacts of FDI on economic growth, 11% of empirical studies show that FDI has a negative effect on growth, 39% find economic growth is not affected by FDI.

This finding is not in line with the findings of some previous studies such as Whalley and Weisbrod (Citation2012) and Doku et al. (Citation2017) analyzed the impacts of Chinese FDI on the economic growth of African countries and provided evidence that China’s FDI to African countries promotes economic growth. Besides, this study’s results do not support the results of Zhang et al. (Citation2014) and Busse et al. (Citation2016) find that China’s FDI inflow to African countries has no significant impact on African growth.

We further investigated the mediating role of the institutional quality of African countries because the role of FDI to enhance economic growth may depend on the domestic absorptive capacity of FDI receiving countries. The study’s finding implies that the conditional effect of Chinese FDI flow to African countries to domestic institutional quality is strongly positive. This result shows that institutional quality improvements can promote FDI’s marginal effects as institutional accompaniment could result in an incremental impact on growth. To enhance the positive effect of FDI on economic growth, therefore, institutional reforms should precede FDI attraction policies. Therefore, the positive effect of FDI on economic growth will be stronger in countries with relatively high institutional quality. This result is in line with some literature such as Khordagui and Saleh (Citation2013), Acemoglu and Johnson (Citation2005), and Jude and Levieuge (Citation2017) that reveal FDI spillovers exist in different economies yet are more evident when controlling for domestic absorptive capacities of countries.

Furthermore, we repeated the exercise changing the study sample, excluding South, Nigeria and Zambia, to conduct sensitivity analysis and partly control reverse causality concerns. South Africa, Nigeria and Zambia are excluded because they are the largest hubs for Chinese FDI. South Africa is the top host African country for Chinese FDI. Likewise, Nigeria and Zambia are the major destinations of Chinese FDI (see Appendix C1b). The results are reported in in Appendix A. The coefficients and significance of almost all control variables are hardly affected ( in Appendix A).

Additionally, having analyzed the effect of the composite index of institutional quality on economic progress, the focus is now to quantify the impacts of disaggregated institutional variables. It is argued that individual governance indicators exert different impacts on economic performance for countries at various levels of development (Zhuang et al., Citation2010).

A disaggregated analysis of individual governance indicators shows that government effectiveness has a positive and significant impact on economic growth. The disaggregated governance indicators have various effects on the economic growth of African countries. The result implies that government effectiveness in the formulation and implementation of quality of policy and the credibility of its commitment to policies are worthwhile to promote economic growth in African countries. Similarly, the absence of political instability and lack of violence has a robust positive effect on African countries’ economic growth. Thus, political instability and violence, especially when it is of a violent nature, negatively affects the productive as well as the transactional capacities of the countries. This has adverse consequences for economic growth. Therefore, political instability or violence results in poor performance of economic growth. The finding is consistent with the findings of Adams (Citation2009) and Aisen and Veiga (Citation2013), which give evidence that political stability and absence of violence robustly affect the economic performance of countries.

The coefficients of the rule of law and corruption control are negative and significant at a 10% level of significance. The negative effect of corruption control may imply the degree of impotency of anti-corruption policies and strategies in African countries (Hammed, Citation2018). Likewise, regulatory quality has a negative effect on economic growth. The negative effects of these indicators may advocate that economic growth requires a long-term stable institutional environment (Siyakiya, Citation2017; Zouhaier, Citation2012). In general, the variations in the coefficients of disaggregated governance quality indicators entail those institutions in their various forms that influence economic growth differently (Siyakiya, Citation2017).

The result in indicates that political stability and lack of violence affects economic growth indirectly through its mediating role on Chinese FDI to African countries. Besides, government effectiveness significantly influences the growth-enhancing effect of Chinese FDI to African countries.

Table 4. The impacts of individual governance indicators on economic growth

Even though control of corruption, regulatory quality, voice and accountability, and the rule of law do not have independent positive effects, their interactions with Chinese FDI have a significant positive impact on the economic growth of African countries. This implies that the growth effect of FDI is stimulated in the presence of effective regulatory quality, control of corruption, the rule of law, and voice and accountability ().

Table 5. The impacts of individual governance indicators on the relationship between Chinese FDI and economic growth

Thus, the positive impacts of Chinese FDI on African countries’ economic growth depend on institutional factors such as political stability and absence of violence, the rule of law, regulatory quality, the effectiveness of government and control of corruption (Asheghian, Citation2004; Hansen & Rand, Citation2006). Besides, this study’s finding is in line with the results of Adams and Opoku (Citation2015) that the impact of FDI on economic growth is positive and significant conditional to the level of regulations in the FDI host countries. This implies that the growth effect of FDI is stimulated in the presence of efficient and quality governance. Thus, these findings imply significant possible means via which FDI impacts economic growth and are consistent with previous results on domestic institutional requirements.

From the theoretical arguments, it is hypothesized that FDI can impact the host economies through capital accumulation. For instance, among the neo-classical economic growth models, the Solow (Citation1956) and Solow (Citation1957) exogenous growth model indicates that economic growth is a function of the capital and labor force, keeping technology exogenous. This model states that capital accumulation promotes countries’ economic growth. FDI can positively affect economic growth directly through capital accumulation (Mahembe & Odhiambo, Citation2014). In this regard, this study extended this theory to control the mediating role of governance quality of African countries in the economic growth of African countries’ and Chinese FDI relationship. Therefore, the results in supported the hypothesis of this study ().

Table 6. Hypothesis test

The results of the study sum up that the economic growth-enhancing effect of Chinese FDI on African countries is subject to the African countries’ governance environment. Therefore, improving all components of governance indicators is valuable in terms of absorptive capacity to enhance the growth impact of China’s FDI flow to Africa.

4.2. The impacts of Chinese FDI on the domestic investment of African Countries

This section provides the results of the impact of Chinese FDI on domestic investment. Correlation and statistical summary of variables are reported in and Appendix A, respectively. We treat lagged GFCF and all the FDI-related variables as endogenous, on the ground of potential reverse causality, and we instrument them using their lagged levels and differences.

The results in indicate that the lagged dependent variable has a robust positive effect on domestic investment. Similarly, improvement in economic growth positively affects domestic investment. Besides, the domestic investment is positively affected by a credit to the private sector. Thus, access to credit to the private sector promotes domestic investment. The coefficient of economic freedom is positive and statistically significant, implying that promoting economic freedom in African countries stimulates investment. In a similar fashion, the institutional quality index has a significantly positive effect on African countries’ domestic investment. However, against the expectation, the coefficient of inflation is negative and statistically significant. It might be loosely justified if the inflation rate remains below the threshold level that can negatively affect investment; increasing prices can increase investment level (Amin et al., Citation2010).

Table 7. The impacts of Chinese FDI on domestic investment

The coefficient of Chinese FDI is positive and statistically significant, indicating a positive association between Chinese FDI and African countries’ domestic investment (). FDI complements to domestic investment by relaxing the liquidity constraint, therefore, escalating economic growth. Furthermore, the interaction term between Chinese FDI with domestic institutional quality is positive, implying that the domestic investment effect of Chinese FDI should be backed by good domestic governance indicators to use the benefit of Chinese FDI to excel domestic investment. Besides, positive interaction between good governance and FDI can be interpreted as a sign that, especially in countries with weak institutions, rent-seeking interests deter foreign investors from entering markets. This result is consistent with the findings of Farla et al. (Citation2016) that reveal the good governance positively influences the effect of FDI.

Additionally, we have repeated the exercise using each component of governance indicators and their mediating role in the nexuses of domestic investment and Chinese FDI to Africa. The results are reported in .

Table 8. The impacts of individual governance indicators on domestic investment

Table 9. The role of individual governance indicators on the relationship between Chinese FDI and domestic investment

The coefficient of government effectiveness is positive and statistically significant revealing that government effectiveness robustly stimulates domestic investment. However, the effect of political stability and absence of violence has negative effect on domestic investment ().

The interaction between the control of corruption and Chinese FDI to African countries has a robust and positive effect on domestic investment for African countries. Similarly, the coefficient of the interaction between Chinese FDI and government effectiveness is positive and statistically significant. Besides, voice and accountability positively affect the impact of Chinese FDI on domestic investment of African countries.

Therefore, the findings are in line with our hypothesis. Based on the results in , the hypothesis on the relationship between Chinese FDI and domestic investment is presented in below.

Table 10. Hypothesis test

5. Conclusions and policy implications

This study has examined the impacts of Chinese FDI on the economic growth and domestic investment of African countries. It conducts the dynamic panel data model (the two-step system GMM) to examine the effects of Chinese FDI on domestic investment and economic growth of African countries controlling the mediating role of good governance for a panel of 44 African countries for the periods 2003–2017.

The conditional effect of Chinese FDI on domestic investment and economic growth subject to domestic institutional quality has been considered. Thus, the novel part of this study, in this regard, is considering the conditional effect of Chinese FDI on the domestic investment and economic growth of African countries extending economic relationship theories to include the mediating role of the governance environment of African countries.

The study results reveal that the interaction of Chinese FDI with the good governance indicator to proxy the institutional quality of the countries has a significant positive effect on the growth of African countries, indicating the conditional effect of China’s FDI on the economic growth of African countries. This study’s findings further reveal that each component of the good governance indicator has a significant effect on the association between Chinese FDI and the economic growth of African countries.

However, Chinese FDI has a robustly positive effect on domestic investment, implying a positive association between Chinese FDI and African countries’ domestic investment. Furthermore, good governance has a mediating role in the nexuses of Chinese FDI and African countries’ domestic investment. Among the governance quality indicators, control of corruption, government effectiveness, and voice and accountability positively affect the relationship between Chinese FDI and African countries’ domestic investment.

Our main conclusion is that improvement in governance quality indicators clearly complements the impact of Chinese FDI on domestic investment and economic growth in African countries. Thus, the results show that Chinese FDI alone has no significant positive effect on African countries’ economic growth, while a better governance environment encourages a growth and domestic investment enhancing effect of Chinese FDI to Africa. Thus, the host countries’ governments have a key role in creating the conditions by improving the level of domestic governance environment that consent for the leverage of the helpful effects or reducing the adverse effects of FDI on the FDI flow to the host country’s economic growth. Therefore, to reap full benefits from Chinese FDI to economic growth and domestic investment, it will require considerable improvements in African economies’ governance quality.

Additional information

Funding

Notes on contributors

Miao Miao

Miao Miao is a Professor at the School of Economics and Management, Southwest Jiaotong University, PR China. Her research focuses on business innovation management and international trade.

Dinkneh Gebre Borojo

Dinkneh Gebre Borojo is a Post-doctoral Researcher at the School of Economics and Management, Southwest Jiaotong University, PR China. His research interest includes international economics, quantitative finance, and institutional economics. He has published extensively in the high ranked international journals and served as a reviewer for some economics and business journals.

Jiang Yushi

Professor Jiang Yushi is a Professor at the School of Economics and Management, Southwest Jiaotong University, PR China. His research interest includes international trade, finance, and business administration.

Tigist Abebe Desalegn

Tigist Abebe Desalegn is a PhD Scholar and Researcher at the school of Economics and Management, Southwest Jiaotong University, PR China.

References

- Acemoglu, D., & Johnson, S. (2005). Unbundling Institutions. Journal of Political Economy, 113(5), 949–28. https://doi.org/https://doi.org/10.1086/432166

- Adams, S. (2009). Foreign Direct Investment, domestic investment, and economic growth in Sub-Saharan Africa. Journal of Policy Modeling, 31(6), 939–949. https://doi.org/https://doi.org/10.1016/j.jpolmod.2009.03.003

- Adams, S., & Opoku, E. (2015). Foreign Direct Investment, Regulations and Growth in Sub-Saharan Africa. Economic Analysis and Policy, 47, 48–56. https://doi.org/https://doi.org/10.1016/j.eap.2015.07.001

- Aisen, A., & Veiga, J. (2013). How does political instability affect economic growth? European Journal of Political Economy, 29(March 2013), 151‒167. https://doi.org/https://doi.org/10.1016/j.ejpoleco.2012.11.001

- Alfaro, L., Chanda, A., Kalemli-Ozcan, S., & Sayek, S. (2004). FDI and Economic Growth: The Role of Local Financial Markets. Journal of International Economics, 64(1), 89–112. https://doi.org/https://doi.org/10.1016/S0022-1996(03)00081-3

- Ali, F. A., Fiess, N., & MacDonald, R. (2010). Do Institutions Matter for Foreign Direct Investment? Open Economies Review, 21(2), 201–219. https://doi.org/https://doi.org/10.1007/s11079-010-9170-4

- Al-Sadig, A. (2013). The effects of foreign direct investment on private domestic investment: Evidence from developing countries. Empirical Economics, 44(3), 1267–1275. https://doi.org/https://doi.org/10.1007/s00181-012-0569-1

- Amin, K. R., Mosayeb, P., & Abbas, V. (2010). Modelling the Asymmetric Effects of Inflation on Real Investment in Iran, 1959-2008. Applied Econometrics and International Development, 10(1), 162–172. https://www.usc.gal/economet/reviews/aeid10111.pdf

- Arellano, M., & Bover, O. (1995). Another Look at the Instrumental Variable Estimation of Error-Components Models. Journal of Econometrics, 68(1), 29–51. https://doi.org/https://doi.org/10.1016/0304-4076(94)01642-D

- Arshad, H. (2017). Foreign Direct Investments, Institutional Framework and Economic Growth (IES Working Paper, No. 09/2017). Prague: Charles University in Prague, Institute of Economic Studies (IES)

- Asheghian, P. (2004). Determinants of economic growth in the United States: The Role of Foreign Direct Investment. The International Trade Journal, 18(1), 63–83. https://doi.org/https://doi.org/10.1080/08853900490277350

- Benáček, V., Lenihan, H., Andreosso-O’Callaghan, B., Michalíková, E., & Kan, D. (2014). Political Risk, Institutions and Foreign Direct Investment: How Do They Relate in Various European Countries? The World Economy, 37(5), 625–653. https://doi.org/https://doi.org/10.1111/twec.12112

- Bos, H., Sanders, M., & Secchi, C. (1974). Private Foreign Investment in Developing Countries: A Quantitative Study on Macro-Economic Effects. D. Riedel Publishing.

- Bruno, R., & Campos, N. (2013). Reexamining the Conditional Effect of Foreign Direct Investment (IZA Discussion Paper No. 7458).

- Busse, M. (2004). ‘Transnational Corporations and Repression of Political Rights and Civil Liberties: An Empirical Analysis. Kyklos, 57(1), 45–66. https://doi.org/https://doi.org/10.1111/j.0023-5962.2004.00242.x

- Busse, M., Erdogan, C., & Mühlen, H. (2016). China’s Impact on Africa - The Role of Trade, FDI and Aid. KYKLOS, 69(2), 228–262. https://doi.org/https://doi.org/10.1111/kykl.12110

- Doku, I., Akuma, J., & Owusu-Afriyie, J. (2017). Effect of Chinese Foreign Direct Investment on Economic Growth in Africa. Journal of Chinese Economic and Foreign Trade Studies, 10(2), 1–11. https://doi.org/https://doi.org/10.1108/JCEFTS-06-2017-0014

- Driffield, N., & Jones, C. (2013). Impact of FDI, ODA and migrant remittances on economic growth in developing countries: A systems approach. The European Journal of Development Research, 25(2), 173‒196. https://doi.org/https://doi.org/10.1057/ejdr.2013.1

- Farla, K., de Crombrugghe, D., & Verspagen, B. (2016). Institutions, Foreign Direct Investment, and Domestic Investment: Crowding Out or Crowding In? World Development, 88(December 2016), 1–9. https://doi.org/https://doi.org/10.1016/j.worlddev.2014.04.008

- Foster, V., Butterfield, W., Chuan, C., & Pushak, N. (2008). Building Bridges: China’s Growing Role as Infrastructure Financier for sub-Saharan Africa. World Bank/PPIAF.

- Hammed, A. (2018). Corruption, Political Instability and Development Nexus in Africa: A Call for Sequential Policies Reforms (MPRA Paper No. 85277). The Munich University Library, Germany

- Hansen, H., & Rand, J. (2006). On the Causal Links Between FDI and Growth in Developing Countries. The World Economy, 29(1), 21–41. https://doi.org/https://doi.org/10.1111/j.1467-9701.2006.00756.x

- Hecht, Y., Razin, A., & Shinar, A. (2004). Interactions Between Capital Inflows and Domestic Investment: Israel and Developing Economies. Israel Economic Review, 2(2), 1–14. https://ideas.repec.org/a/boi/isrerv/v2y2004i2p1-14.html

- Herzer, D., Klasen, S., & Nowak-Lehmann, F. (2008). In search of FDI-led growth in developing countries: The way forward. Economic Modelling, 25(5), 793–810. https://doi.org/https://doi.org/10.1016/j.econmod.2007.11.005

- James, A., & Aadland, D. (2011). The curse of natural resources: An empirical investigation of U.S. counties. Resource and Energy Economics, 33(2), 440–453. https://doi.org/https://doi.org/10.1016/j.reseneeco.2010.05.006

- Johnson, A. (2006). The effects of FDI on host country economic growth (CESIS Electronic Working Paper Series No. 58). Stockholm, Sweden.

- Jude, C. (2018). Does FDI crowd out domestic investment in transition countries? Economics of Transition and Institutional Change, 27(1), 163–200. https://doi.org/https://doi.org/10.1111/ecot.12184

- Jude, C. (2018). Does FDI crowd out domestic investment in transition countries? Economics of Transition and Institutional Change, 27(1), 163–200. https://doi.org/https://doi.org/10.1111/ecot.12184

- Jude, C., & Levieuge, G. (2017). Growth Effect of Foreign Direct Investment in Developing Economies: The Role of Institutional Quality. The World Economy, 40(4), 715–742. https://doi.org/https://doi.org/10.1111/twec.12402

- Kalu, O., Gwatidzo, T., & Kaniki, S. (2010). Legal Environment, Finance Channels and Investment: The East African Example. The Journal of Development Studies, 46(4), 724–744. https://doi.org/https://doi.org/10.1080/00220380903012722

- Khordagui, N. H., & Saleh, G. (2013). FDI and Absorptive Capacity in Emerging Economies. Topics in Middle Eastern and African Economies, 15(1), 141–172. https://meea.sites.luc.edu/volume15/meea15.html

- Kolstad, I., & Wiig, A. (2011). Better the Devil You Know? Chinese Foreign Direct Investment in Africa. Journal of African Business, 12(1), 31–50. https://doi.org/https://doi.org/10.1080/1536710X.2011.555259

- Luca, O., & Spatafora, N. (2012). Capital Inflows, Financial Development, and Domestic Investment: Determinants and Inter-Relationships (IMF Working Paper No. 12/120). International Monetary Fund.

- Mahembe, E., & Odhiambo, N. M. (2014). Foreign Direct Investment and Economic Growth: A Theoretical Framework. Journal of Governance and Regulation, 3(2), 63–70. https://doi.org/https://doi.org/10.22495/jgr_v3_i2_p6

- Mankiw, N. G., Romer, D., & Weil, D. N. (1992). A Contribution to the Empirics of Economic Growth. Quarterly Journal of Economics, 107(2), 407–437. https://doi.org/https://doi.org/10.2307/2118477

- Megbowon, E., Mlambo, C., Adekunle, B., & Nsiah, C. (2019). Impact of China’s outward FDI on sub-Saharan Africa’s industrialization: Evidence from 26 countries. Cogent Economics & Finance, 7(1), 1681054. https://doi.org/https://doi.org/10.1080/23322039.2019.1681054

- Nair-Reichert, U., & Weinhold, D. (2001). Causality Tests for Cross-Country Panels: A New Look at FDI and Economic Growth in Developing Countries. Oxford Bulletin of Economics and Statistics, 63(2), 153–171. https://doi.org/https://doi.org/10.1111/1468-0084.00214

- Nawaz, S., Iqbal, N., & Khan, M. A. (2014). The Impact of Institutional Quality on Economic Growth: Panel Evidence. The Pakistan Development Review, 53(1), 15–31. https://doi.org/https://doi.org/10.30541/v53i1pp.15-31

- Pigato, M., & Tang, W. (2015). China and Africa: Expanding Economic Ties in an Evolving Global Context. Invest in Africa Forum.

- Robinson, J. A., & Acemoglu, D. (2012). Why nations fail: The origins of power, prosperity and poverty. Crown.

- Romer, P. M. (1990). Endogenous technological change. Journal of Political Economy, 98(5, Part 2), 71–102. https://doi.org/https://doi.org/10.1086/261725

- Roodman, D. (2009). How to do xtabond2: an introduction to difference and system GMM in Stata. The Stata Journal, 9(1), 86–136. https://doi.org/https://doi.org/10.1177/1536867X0900900106

- Salahuddin, M., & Islam, M. (2008). Factors affecting investment in developing countries: a panel data study. The Journal of Developing Areas, 42(1), 21–37. https://doi.org/https://doi.org/10.1353/jda.0.0011

- Sanfilippo, M. (2010). Chinese FDI to Africa: what is the nexus with foreign economic cooperation? African Development Review, 22(S1), 599–614. https://doi.org/https://doi.org/10.1111/j.1467-8268.2010.00261.x

- Siyakiya, P. (2017). The impact of institutional quality on economic performance: an empirical study of Turkey and 28 Countries in the European Union. World Journal of Applied Economics, 3(2), 3–24. https://doi.org/https://doi.org/10.22440/wjae.3.2.1

- Slesman, L., Baharumshah, A. Z., & Ra’ees, W. (2015). Institutional infrastructure and economic growth in member countries of the organization of Islamic Cooperation (OIC). Economic Modelling, 51(C), 214–226. https://doi.org/https://doi.org/10.1016/j.econmod.2015.08.008

- Solow, R. (1956). A contribution to the Theory of Economic Growth. Quarterly Journal of Economics, 70(1), 65–94. https://doi.org/https://doi.org/10.2307/1884513

- Solow, R. (1957). Technical Change and the Aggregate Production Function. The Review of Economics and Statistics, 39(3), 312–320. https://doi.org/https://doi.org/10.2307/1926047

- Tamilina, L., & Tamilina, N. (2014). Heterogeneity in institutional effects on economic growth: Theory and empirical evidence. The European Journal of Comparative Economics, 11(2), 205–249. http://ejce.liuc.it/Default.asp?tipo=fascicoli&vol=11&fasc=2

- Türkcan, B., & Yetkiner, I. H. (2008). Endogenous Determination of FDI Growth and Economic Growth: The OECD Case (Working Paper No. 08/07). Izmir University of Economics, Turkey.

- Whalley, J., & Weisbrod, A. (2012). The contribution of Chinese FDI to Africa’s Pre Crisis Growth Surge. Global Economy Journal, 12(4), 1–28. https://doi.org/https://doi.org/10.1515/1524-5861.1873

- Zhang, J., Alon, I., & Chen, Y. (2014). Does Chinese investment affect Sub-Saharan African Growth? International Journal of Emerging Markets, 9(2), 257–275. https://doi.org/https://doi.org/10.1108/IJoEM-10-2013-0171

- Zhuang, J., de Dios, E., & Martin, A. L. (2010). Governance and institutional quality and the links with economic growth and income inequality: With special reference to developing Asia (Asian Development Bank Working Paper No. 193).

- Zouhaier, H. (2012). Institutions, investment and economic growth. International Journal of Economics and Finance, 4(2), 152–162. https://doi.org/https://doi.org/10.5539/ijef.v4n2p152

Appendix

Table A1. Correlations among capital formation and explanatory variables

Table A2. Correlation among variables used for growth estimation

Table A3. Statistical summary variables used for growth estimation

Table A4. The impacts of Chinese FDI on growth

Appendix B:

The list of countries

Angola, Benin, Burkina Faso, Botswana, Ivory Coast, Cameroon, Congo Republic, Comoros, Cabo Verde, Djibouti, Algeria, Egypt, Ethiopia, Gabon, Ghana, Guinea, Gambia, Guinea-Bissau, Kenya, Liberia, Libya, Morocco, Madagascar, Mali, Mozambique, Mauritania, Mauritius, Malawi, Namibia, Niger, Nigeria, Rwanda, Sudan, Senegal, Sierra Leone, Seychelles, Chad, Togo, Tunisia, Tanzania, Uganda, South Africa, Zambia and Zimbabwe.