Abstract

Mobile wallet (M-wallet), as an innovative alternative payment, is trendy in developed economies because it provides users with the ease, safety, and fast completion of daily financial activities. However, M-wallets have still been seen in the infancy stage in Vietnam. Therefore, the study aims to discover the main factors shaping behavioral intention to use mobile wallets in Vietnam. The extended version of the Technology Acceptance Model (TAM) with perceived enjoyment and trust was considered as a theoretical foundation for this study. The primary empirical data from 332 respondents were analyzed using structural equation modeling (SEM). Perceived ease of use, perceived usefulness, and enjoyment have positive and significant impacts on behavioral intention to use M-wallets, whereas trust showing no direct effect.

Keywords:

PUBLIC INTEREST STATEMENT

Although the habit of using cash for daily purchases remains popular in Southeast Asia, mobile wallet applications have attracted significant attention from both consumers and payment service providers in recent years. In Vietnam, the government also announced a document to reduce cash transactions and enhance electronic payment activities by 2020. Vietnamese consumers tend to be very supportive of this government plan towards building a cashless nation. Thus, this study aims to provide an insight into Vietnamese customers’ behavioral intention to use mobile payment applications. Perceived usefulness and perceived ease of use are the critical predictors for mobile payment adoption in Vietnam. Besides, enjoyment and trust may directly or indirectly motivate Vietnamese customers to use mobile payment applications. This paper recommends providers to upgrade or develop mobile payment applications with high usability, value-adding functions, and especially more pleasure to satisfy and attract Vietnamese young people.

1. Introduction

With the growth in demand for cashless transactions, digital payments have grown at light speed. Notably, mobile wallets have gradually replaced traditional leather wallets and plastic cards (Leong et al., Citation2013). By installing mobile wallet applications in the smartphone, a user can add or store money in his wallet by directly linking his bank account. Similarly, a user can do online transactions and make payments to merchants by entering the phone number, email, or scanning QR code (Singh et al., Citation2017).

Compared to developed countries, the period of transitioning from cash to mobile payments is shorter in emerging markets because many customers in these countries do not own a debit or credit card before using mobile wallets. The appearance of mobile wallets is also in line with the Vietnam government’s plan to develop a cashless society. According to Nikkei, “Vietnam has been promoting electronic payments since 2008. Only about 40% of Vietnam’s 95 million people have bank accounts, mostly in urban areas, while there are around 120 million mobile phone subscriptions, and the telecoms network covers the entire country” (Justina Lee, Citation2019). Until January 2017, the Vietnamese Government announced a document to reduce cash transactions and enhance electronic payment activities by 2020. “Under the plan, by 2020, total cash transactions would take up less than 10% of total market transactions; all supermarkets, shopping malls, and distributors would accept credit cards; 70% of water, electronics, and telecommunication service providers would accept cash-free payments from households and individuals, and 50% of total urban households would use electronic payment methods for daily transactions” (British Business Group Vietnam, Citation2019). It tends to move citizens away from cash use by encouraging money transfers and purchases through mobile phone accounts for small transactions. Consequently, the number of people making mobile payments in Vietnam growing faster than in the other Southeast Asian nations, and the proportion of consumers in Vietnam using mobile wallets increased from 37% in 2018 to 61% in 2019 (PWC Thailand, Citation2019).

The main objective of our study is to help the organizations providing mobile wallets in Vietnam to understand the intention of customers and determine their strategy to promote the use of mobile wallets. We use the Technology Acceptance Model (TAM) (Davis, Citation1989), in which Perceived Ease of Use (PEOU) and Perceived Usefulness (PU) are the main factors that affect behavioral intention to use. Besides, we develop a new research model by adding two constructs of trust and enjoyment after evaluating several past studies of TAM.

To register and get mobile wallets, customers asked to provide their personal and financial information to service providers. However, some customers are unwilling to place the trust of their information in the service providers. They are worried that their transactions can be tracked, or they can receive a lot of advertisements (Dahlberg et al., Citation2003). According to Shin (Citation2009), previous studies on mobile payments have not yet paid much attention to security and privacy concerns, and they only focus on the sheer technical aspects of security other than users’ perceived security or trust. Along with usefulness and ease of use, Schierz et al. (Citation2010) confirmed the positive impact of trust on behavioral intention. Especially, the new Circular 23/2019/TT-NHNN of State Bank of Vietnam dated 22 November 2019, which amendments and supplements to the existing Circular 39/2014/TT-NHNN is requiring e-wallet owners must verify their identity before July 7th, 2020. Therefore, this study will incorporate trust into TAM to predict users’ behavioral intention to use mobile wallets in Vietnam.

Besides, enjoyment may be considered to be a form of intrinsic motivation, while perceived usefulness is a form of extrinsic motivation (Davis et al., Citation1992). Because extrinsic motivation should be a stronger predictor of intention to use than intrinsic motivators (Davis et al., Citation1989), such intrinsic motivators were not considered in the TAM model. However, several studies support that individuals, who experience pleasure and fun from using technologies, are likely to use them more extensively (Lee et al., Citation2005; Li et al., Citation2005; Nysveen et al., Citation2005; Sun & Zhang, Citation2006). This argument encourages us to include enjoyment into the original TAM model and re-examine it in the context of Vietnam.

This article is organized as follows: The next section provides a literature review and develops the hypotheses. Section 3 describes the research methodology. Section 4 provides the results of empirical tests. Section 5 presents conclusions and some implications.

2. Literature review

2.1. Technology acceptance models

The best-known model for defining and testing individual intentions to adopt new technology is the technology acceptance model (TAM), which was presented by Davis (Citation1989). He attempted to prove that behavioral intention is influenced by a user’s attitude towards using a new technology, and perceived usefulness and perceived ease of use are the two major impact factors on an individual’s adoption.

Besides, the unified theory of acceptance and use of technology (UTAUT), suggested by Venkatesh et al. (Citation2003), has been proposed as an extended version of TAM because TAM lacks a diversity of variables for explaining a user’s intention. UTAUT has four constructs, such as effort expectancy, performance expectancy, social influence, and facilitating conditions, which are proved to be direct antecedents of behavioral intention and behavior. The control variables, i.e., gender, age, experience, and voluntariness of use, are used to moderate the influence of the four key constructs on usage intention and behavior.

Although both TAM and UTAUT may provide a reasonable theoretical foundation for studying behavioral intention to use e-payment (Shin, Citation2009), the simplicity and ease of implementation enhance the wider application of TAM (Chuttur, Citation2009). Most previous studies focus on the determinants of mobile payment adoption and TAM is often considered as the theoretical foundation (Oliveira et al., Citation2016; Zhou, Citation2011). Moreover, Shin (Citation2009) confirmed that there is no direct relationship between social influence and behavioral intention in their study of mobile payment usage based on the UTAUT model. Similarly, Wang and Yi (Citation2012) also found no significant relationship between social influence and intention. However, TAM may not contain enough significant factors to explain intention to use M-wallets because it is initially introduced to explain computer usage behavior. Hence, many studies often add other variables into the TAM such as perceived trust and perceived security for mobile payment service (Yang et al., Citation2015; Slade et al., Citation2015; Singh et al., Citation2020; Schierz et al., Citation2010); perceived enjoyment (G. C. & Kumar, Citation2005; Childers et al., Citation2001). Thus, this study incorporates trust and enjoyment into the TAM to better explain variances.

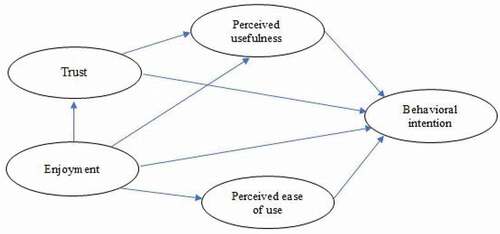

2.2. Conceptual model and research hypothesis

2.2.1. Perceived usefulness (PU)

Perceived usefulness (PU), which is one of the fundamental precedents in the TAM model, is defined as the degree to which a person believes that using a particular system would enhance his/her performance and effectiveness (Davis, Citation1993; Redzuan et al., Citation2016). It means that consumers’ usage intention of a system is significantly affected by their perception of its usefulness. Similarly, Khayati and Zouaoui (Citation2013) also identified that perceived usefulness is the same as the performance expectancy of the UTAUT model and represents the gain in performance that a person can achieve when using new technology.

The impact of perceived usefulness on usage intention has been demonstrated in empirical research on e-payment acceptance (Francisco et al., Citation2015; Cheng & Huang, 201; Wang et al., Citation2006). Francisco et al. (Citation2015) found that perceived usefulness directly affects the users’ attitude towards the payment tool. Cheng and Huang (Citation2013) also agreed that the perceived usefulness associated with mobile ticketing services has a positive and direct influence on mobile usage behavior. Similarly, Wang et al. (Citation2006) show that higher perceived usefulness will lead to higher behavioral intention to use mobile services. In brief, customers will use mobile services more when they find mobile services useful for their transactions.

H1: Perceived usefulness positively influences a customer’s behavioral intention

2.2.2. Perceived ease of use (PEU)

Perceived ease of use refers to an individual’s feeling about the amount of physical and mental efforts to use a particular system (Davis, Citation1993). In other words, a person will use a mobile wallet application more if he/she find it easy or not too much effort to use. Some limitations of mobile wallets, such as complications and difficult manipulations, can cause dissatisfaction and disapproval of using M-wallets, especially for old and inexperienced consumers. Therefore, ease of learning and use is crucial for M-wallet services regardless of whether consumers are technically proficient or not (Dai & Palvi, Citation2009). Previous works have shown that perceived ease of use was positively associated with behavioral intention to use (Pousttchi & Wiedemann, Citation2007; Rigopoulos & Askounis, Citation2007; Jayasingh & Eze, Citation2015). Accordingly, the following hypothesis is then evaluated:

H2: Perceived ease of use positively influences a customer’s behavioral intention

2.2.3. Trust (TRU)

To develop a successful mobile payment application, providers also need to pay much attention to building and maintaining customers’ trust because these applications usually require customers to provide personal or financial information. Thus, customers usually concern about the level of security and privacy when preparing commerce via the internet (Kim et al., Citation2009; Toufaily et al., Citation2013) or conducting mobile payments (Zhou, Citation2011). Consumers will see trust as worry-free and secure. They want to make sure that the transaction will be completed as expected and that their information will not be shared with inappropriate parties or will not be hacked (Chellappa et al., Citation2002). Jarvenpaa et al. (Citation1999) agreed that trust has an important influence on consumer behavior, especially in uncertain environments like electronic payment. According to T. Lee (Citation2005), it is very likely to be an important factor in mobile wallet adoption. Past research has also shown that trust is positively related to behavioral intention (Gao and Waechter, Citation2017; Khalilzadeh et al., Citation2017; Shin, Citation2009; Luo et al., Citation2010; Zhang et al., Citation2010). Additionally, the studies by Francisco et al. (Citation2015), Gefen et al. (Citation2003), and Pavlou (Citation2003) also showed a positive impact of trust on perceived usefulness. Hence, the following hypotheses are postulated:

H3: Trust positively influences a customer’s behavioral intention

H4: Trust positively influences perceived usefulness

2.2.4. Enjoyment (ENJ)

Researchers have suggested that consumers do not only use new technologies for enhancing performance but also experiencing enjoyment. Venkatesh et al. (Citation2012) considered perceived enjoyment as “the fun, pleasure, entertainment, or playfulness derived from using a technology” and found its significant impact on consumers’ technology acceptance. In this study, we consider perceived enjoyment as the degree to which a person feels enjoyable when using e-wallets. The higher the level of perceived enjoyment is, the lower the anxiety or concern is. Previous studies regarding mobile commerce or online shopping have empirically incorporated perceived enjoyment to the TAM to explain user acceptance; and approved that this construct has a positive impact on behavioral intention (G. C. & Kumar, Citation2005; Childers et al., Citation2001). Besides, according to Agarwal and Karahanna (Citation2000), enjoyable technology helps customers feel easier to use and more useful, thus perceived enjoyment can positively influence perceived ease of use and perceived usefulness. Besides, a higher level of perceived enjoyment in using new technology may also lead to a decrease in worry, in turn enhancing trust (Koenig-Lewis et al., Citation2015) Accordingly, this study proposes the four hypotheses:

H5: Perceived enjoyment positively influences a customer’s behavioral intention

H6: Perceived enjoyment positively influences perceived usefulness

H7: Perceived enjoyment positively influences perceived ease of use

H8: Perceived enjoyment positively influences trust

Figure 1. Conception model

3. Research methodology

The research had five main constructs: perceived ease of use, usefulness, trust, enjoyment, behavioral intention. To measure the above constructs, we used 17 scale items adapted from previous related studies shown in the Appendix. Then, we developed a questionnaire and invited five experts to review the content validity and appropriateness of questions. The items were measured by 7-point Likert scales, ranging from “strongly disagree” to “strongly agree”. Moreover, the questionnaire also contained some questions about demographic characteristics of Vietnamese users such as gender, age, occupation status, income, etc. The survey process was conducted in two phases. First of all, a pilot test was implemented by interviewing 45 users directly to check the suitability of the questionnaire and adjust the wording of questions. Then the online questionnaire was distributed online through email and Facebook. The questionnaire was originally in English but was translated into Vietnamese by a professional native translator.

Data was collected through an online survey in Vietnam, a total of 345 questionnaires were submitted, but only 332 acceptable responses were used for data analysis after carefully screening to eliminate low-quality surveys. We used an online a priori sample size calculator for structural equation models (Soper, Citation2019) to determine an efficient and adequate sample size. Through examining the statistical power levels (0.95), desired probability (0.05), anticipated effect size (0.3), the number of latent constructs (5), and the number of observed (17 items), the results show that 223 responses are needed as the lowest sample size to detect the effect, 148 responses are needed as the lowest sample size for model structure. Therefore, our sample of 332 is considered adequate for structural equation models and statistically strong to detect any significant effects.

Following Anderson and Gerbing (Citation1988), we present a two-step modeling approach: First, we examined the measurement model to test reliability and validity. Second, we examined the structural model to investigate relationships among the theoretical constructs and model fitness.

4. Results and discussion

represents the demographic details of the sample. Of 332 usable surveys, 220 (66.3%) of them were female, and 112 (33.7%) were male. Most of those participants (49.4%) were within the age group of under 25. Regarding education, the number of respondents having a college/university level accounted for a significant proportion of the sample (77.4%). The majority of respondents were observed to have a monthly income of under 5 million VND (35.5%) and to be students (37.3%). In brief, the sample is rather unbalanced in terms of age, education, and income because the majority of mobile users are young.

Table 1. Descriptive statistics of respondents

The measurement model was evaluated for indicator reliability, construct reliability, convergent validity, and discriminant validity. Firstly, the indicator reliability was evaluated by using principal axis factoring analysis with Promax rotation on 17 items. As shown in , all the items with factor loading more than 0.6 were considered to be significant (Zainudin, Citation2010). Moreover, the Kaiser-Meyer-Oklin value was 0.870, which is higher than the threshold value of 0.7. Secondly, we tested construct reliability through the calculation of Cronbach’s alpha and composite reliability (CR) for each construct. All the constructs have composite reliability and Cronbach’s alpha values above 0.8, which suggests that the constructs are reliable. Thirdly, we also used the average variance extracted (AVE) to assess convergent validity. From , AVE is higher than the minimum required level of 0.50 (Hair et al., Citation2010). Besides, presents discriminant validity. The square root of each construct’s AVE values is higher than the correlations with other latent constructs, supporting that there is discriminant validity between all the constructs. In brief, the measurement model results show that the reliability and validity of the constructs are satisfactory, and we continue to test the structural model as proposed above.

Table 2. Reliability and validity of constructs

Table 3. Discriminant validity

To test structural relationships, the conceptualized causal paths were estimated. The results are shown in . Seven hypotheses were supported, and one was rejected. The results support the proposed model. The specified relationship between perceived usefulness and behavioral intention was supported (β = 0.244, P-value <0.01). This finding is in line with the previous technology adoption studies in the UK, India, Hong Kong, Brazil, and so forth (Apanasevic et al., Citation2016; Madan & Yadav, Citation2016; Amoroso & Watanabe, Citation2012; Oliveira et al., Citation2016). They emphasize that perceived usefulness is a critical motivator for user’s intention.

Table 4. Summary of hypothesis tests

Perceived ease of use of mobile wallets also reached a high level of positive behavioral intention (β = 0.131, P-value <0.01). The result is consistent with other studies of TAM (Dwivedi et al., Citation2019; Liébana-Cabanillas et al., Citation2018; Shaw, Citation2014; Turner et al., Citation2010). It indicates that less efforts to use M-wallets by customers will significantly impact its adoption. Some previous studies explained that consumer is usually concerned about the extent of easiness in using M-wallets (Thakur & Srivastava, Citation2014; Alalwan et al., Citation2018). Therefore, mobile wallet providers should conduct market research on the demands and habits of their target customers, especially the youth, to upgrade the functions, provide value-adding characteristics of the current applications, or develop new potential applications. Dahlberg et al. (Citation2008) also advised the providers to offer more value to customers to enhance the success of mobile payment services.

Regarding trust, its direct effect (β = 0.053, P-value = 0.392) on behavioral intention was not supported, which is in contrast to the findings of Duane et al. (Citation2014) and Shaw (Citation2014). Despite that, trust had a positive impact on perceived usefulness (β = 0.529, P-value <0.01). It provided strong evidence about the role of trust to perceived usefulness because trust might lessen the necessity to govern and supervise the activity, enabling customers to employ the services easily and efficiently (Setyadinsa et al., Citation2018). In other words, consumers need to be assured that payment by mobile wallets is trustworthy. Indeed, the role of trust has been largely validated and confirmed by many studies (Luo et al., Citation2010; Zhou, Citation2011; Kim et al., Citation2009). Along with the significant impact of perceived usefulness on behavioral intention as mentioned above, perceived usefulness might also mediate the influence of trust on a customer’s behavioral intention, which supporting an indirect relationship between trust and M-wallet usage behavior. If mobile wallets have not been tested and secured appropriately, customers will feel them less useful and therefore have less intention to use them (Shaw, Citation2014). Therefore, Iman (Citation2018) recommended that mobile payment service providers should invest more to minimize fraud and theft, as well as pay more attention to customers’ privacy protection.

Besides, also showed that perceived enjoyment had significant impacts on behavioral intention (β = 0.252, P-value <0.01), perceived usefulness (β = 0.247, P-value <0.01), perceived ease of use (β = 0.221, P-value <0.01). These findings are in line with the studies by Agarwal and Karahanna (Citation2000), Van Der Heijden (Citation2004), and Venkatesh et al. (Citation2012), suggesting that higher perceived enjoyment will lead to higher acceptance, perceived ease of use, and perceived usefulness. It implies that the role of fun and pleasure should be taken into more consideration because Vietnam’s population is heavily skewed towards younger age groups, with an average age of 30.9 years (J.P. Morgan, Citation2019), who are the target users of mobile payment applications. Another contribution in this study is the enhancing effect of enjoyment on trust (β = 0.534, P-value <0.01), which is consistent with Rouibah et al. (Citation2016). They also concluded that perceived enjoyment is the most important antecedent to consumer behavior and trust.

To test the model goodness of fit, we analyzed fit indices such as goodness of fit index (GFI), adjusted goodness of fit index (AGFI), comparative fit index (CFI), normal chi-square to degree-of-freedom (CMIN/DF), root mean square error of approximation (RMSEA), standardized root mean squared residual (SRMR), and normal-fit index (NFI). The main results supported that the overall fit of the model is satisfactory as all the fit indices mentioned in are within the recommended level.

Table 5. Goodness-of fit indicators

5. Conclusion

5.1. Summary findings and implications

The main purpose of this study is to analyze Vietnamese customers’ behavioral intention to use M-wallet and identify its determinants, we reviewed related variables in the Technology Acceptance Model (TAM) and defined an extended model of TAM with trust and enjoyment which may directly or indirectly motivate Vietnamese customers to use mobile payment applications. By applying SEM for a sample data of 332 people, two primary constructs in TAM, perceived usefulness, and perceived ease of use are the critical predictors for M-wallet usage behavior in Vietnam. This result is consistent with the traditional TAM (Davis et al., Citation1989) and with many recent empirical studies on the adoption of mobile technologies. This research, therefore, confirms that TAM is a robust model for studying the intention to use new mobile payment applications. Similarly, enjoyment favors technology acceptance through the pleasure of an interaction with the applications. This result is also in line with Shaw (Citation2014) and Alalwan et al. (Citation2018). In contrast, trust has no direct impact on the intention to use, which is different from previous studies (Gao and Waechter, Citation2017; Khalilzadeh et al., Citation2017; Shin, Citation2009; Luo et al., Citation2010; Zampou et al., 2012; Zhang et al., Citation2010). These studies stated that trust increases the intention to use due to less fear of negative consequences in their transactions. Despite that, trust can indirectly influence behavioral intention to use through perceived usefulness because consumers who feel safe in their transactions with mobile wallets may perceive mobile wallets more useful and hence, tend to use the M-wallet apps. Therefore, this paper contributes to this research field by adding the impact of these two factors to the adoption of M-wallets in Vietnam.

From a practical viewpoint, the study provides knowledge about the influential factors that can help M-wallets providers in Vietnam to attract more customers. As stated above, it clearly shows that perceived usefulness and perceived ease of use are key antecedents of behavioral intention to use. In this sense, the findings suggest that M-wallets providers should upgrade or develop mobile payment applications with high usability, more benefits to satisfy Vietnamese young people. Accordingly, marketing efforts should be directed towards communicating these two attributes of M-wallets. Furthermore, to increase the consumer’s feelings of excitement, the user interactivities should be kept simple and pleasant. Consumer groups’ behavior and habits should be deeply investigated to offer personalized service. Finally, trust had a positive impact on perceived usefulness, thus enhancing the intention to use. It is recommended that M-wallets providers should link trust with the perceived benefits of M-wallets. For example, they should provide precise information, fulfill their promises, apply adequate security measures, guarantee to return any financial losses caused by technology defects.

5.2. Limitation and future research

The current study has several limitations that call for future research. First, the sample size includes mostly the people pursuing a university/college degree and predominately female. Second, future research should compare mobile wallets with competing methods such as credit cards, VISA, and MasterCard, to better explain the behavioral intention to use mobile wallets. Third, the absence of the direct effect of trust on behavioral intention should be taken into more consideration because past studies have identified trust as an important factor for the intention to use mobile wallets. One potential explanation is that our respondents were young people under 25 years old, and they mainly use mobile payments for small transactions. Therefore, perceived risk for mobile payments was less important to them. Finally, it is possible to generalize the research model to new technological mobile applications, different emerging countries, and various consumer groups.

Additional information

Funding

Notes on contributors

Anh Tho To

Anh Tho To is a lecturer at the University of Finance - Marketing, Ho Chi Minh City, Vietnam. He earned his Ph.D. in Economics at Hiroshima University, Japan. His research papers were successfully published in many international journals indexed by Scopus. His research interests include financial behavior, financial technology, consumer behavior.

Thi Hong Minh Trinh

Thi Hong Minh Trinh is a lecturer at the University of Finance - Marketing. She earned a master’s degree at the University of Economics in Ho Chi Minh City, Vietnam. She has a strong research interest in the topics of marketing and commerce.

References

- Agarwal, R., & Karahanna, R. (2000). Time flies when you’re having fun: Cognitive absorption and beliefs about information technology usage. MIS Quarterly, 24(4), 665–14. https://doi.org/https://doi.org/10.2307/3250951

- Alalwan, A. A., Baabdullah, A. M., Rana, N. P., Tamilmani, K., & Dwivedi, Y. K. (2018). Examining adoption of mobile internet in Saudi Arabia: Extending TAM with perceived enjoyment, innovativeness and trust. Technology in Society, 55, 100–110. https://doi.org/https://doi.org/10.1016/j.techsoc.2018.06.007

- Amoroso, D. L., & Watanabe, R. M. (2012). Building a research model for mobile wallet consumer adoption: The case of mobile Suica in Japan. Journal of Theoretical and Applied Electronic Commerce Research, 7(1), 94–110. https://doi.org/https://doi.org/10.4067/S0718-18762012000100008

- Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modeling in practice: A review and recommended two-step approach. Psychological Bulletin, 103(3), 411. https://doi.org/https://doi.org/10.1037/0033-2909.103.3.411

- Apanasevic, T., Markendahl, J., & Arvidsson, N. (2016). Stakeholders’ expectations of mobile payment in retail: Lessons from Sweden. International Journal of Bank Marketing, 34(1), 37–61. https://doi.org/https://doi.org/10.1108/IJBM-06-2014-0064

- Bentler, P. M., & Dudgeon, P. (1996). Covariance structure analysis: Statistical practice, theory, and directions. Annual Review of Psychology, 47(1), 563–592. https://doi.org/https://doi.org/10.1146/annurev.psych.47.1.563

- British Business Group Vietnam. (2019). Vietnam 2019 – Fintech. https://bbgv.org/business-center/knowledge/sector-reports-knowledge/vietnam-2019-fintech/

- Chellappa, R., Pavlou, K., & Paul, A. (2002). Perceived information security, financial liability and coonsumer trust in electronic commerce transactions. Logistics Information Management, 15(5/6), 358–368. https://doi.org/https://doi.org/10.1108/09576050210447046

- Cheng, Y. H., & Huang, T. Y. (2013). High speed rail passengers’ mobile ticketing adoption. Transportation Research Part C: Emerging Technologies, 30, 143–160. https://doi.org/https://doi.org/10.1016/j.trc.2013.02.001

- Childers, T. L., Carr, C. L., Peck, J., & Carson, S. (2001). Hedonic and utilitarian motivations for online retail shopping behavior. Journal of Retailing, 77(4), 511–535. https://doi.org/https://doi.org/10.1016/S0022-4359(01)00056-2

- Chuttur, M. Y. (2009). Overview of the technology acceptance model: Origins, developments and future directions. Working Papers on Information Systems, 9(37), 9–37. http://adam.co/lab/pdf/test/pdfs/TAMReview.pdf

- Dahlberg, T., Mallat, N., Ondrus, J., & Zmijewska, A. (2008). Past, present and future of mobile payments research: A literature review. Electronic Commerce Research and Applications, 7(2), 165–181. https://doi.org/https://doi.org/10.1016/j.elerap.2007.02.001

- Dahlberg, T., Mallat, N., & Öörni, A. (2003). Trust enhanced technology acceptance modelconsumer acceptance of mobile payment solutions: Tentative evidence. Stockholm Mobility Roundtable, 22(1), 145. http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.200.7189&rep=rep1&type=pdf

- Dai, H., & Palvi, P. C. (2009). Mobile commerce adoption in China and the United States: A cross-cultural study. ACM SIGMIS DATABASE: The DATABASE for Advances in Information Systems, 40(4), 43–61. https://doi.org/https://doi.org/10.1145/1644953.1644958

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Q, 13(3), 319–340. https://doi.org/https://doi.org/10.2307/249008

- Davis, F. D. (1993). User acceptance of information technology: System characteristics, user perceptions and behavioral impacts. International Journal of ManMachine Studies, 38(3), 475–487. https://doi.org/https://doi.org/10.1006/imms.1993.1022

- Davis, F. D., Bagozzi, R. P., & Warshaw, P. R. (1989). User acceptance of computer technology: A comparison of two theoretical models. Management Science, 35(8), 982–1003. https://doi.org/https://doi.org/10.1287/mnsc.35.8.982

- Davis, F. D., Bagozzi, R. P., & Warshaw, P. R. (1992). Extrinsic and intrinsic motivation to use computers in the workplace. Journal of Applied Social Psychology, 22(14), 1111–1132. https://doi.org/https://doi.org/10.1111/j.1559-1816.1992.tb00945.x

- Duane, A., O’Reilly, P., & Andreev, P. (2014). Realising M-Payments: Modelling consumers’ willingness to M-pay using Smart Phones. Behaviour & Information Technology, 33(4), 318–334. https://doi.org/http://dx.doi.org/10.1080/0144929X.2012.745608

- Dwivedi, Y. K., Rana, N. P., Jeyaraj, A., Clement, M., & Williams, M. D. (2019). Re-examining the unified theory of acceptance and use of technology (UTAUT): Towards a revised theoretical model. Information Systems Frontiers, 21(3), 719–734. https://doi.org/https://doi.org/10.1007/s10796-017-9774-y

- Francisco, L. C., Francisco, M. L., & Juan, S. F. (2015). Payment systems in new electronic environments: Consumer behavior in payment systems via SMS. International Journal of Information Technology & Decision Making, 14(2), 421–449. https://doi.org/https://doi.org/10.1142/S0219622015500078

- G. C., B., II, & Kumar, A. (2005). Explaining consumer acceptance of handheld Internet devices. Journal of Business Research, 58(5), 553–558. https://doi.org/https://doi.org/10.1016/j.jbusres.2003.08.002

- Gao, L., & Waechter, K. A. (2017). Examining the role of initial trust in user adoption of mobile payment services: An empirical investigation. Information Systems Frontiers, 19(3), 525–548. https://doi.org/https://doi.org/10.1007/s10796-015-9611-0

- Gefen, D., Karahanna, E., & Straub, D. W. (2003). Trust and TAM in online shopping: An integrated model. MIS Quarterly, 27(1), 51–90. https://doi.org/https://doi.org/10.2307/30036519

- Hair, J. F., Anderson, R. E., Tatham, R. L., & William, C. B. (2010). Multivariate data analysis (7th ed.). Pearson Prentice Hall.

- Hooper, D., Coughlan, J., & Mullen, M. R. (2008). Structural equation modelling: Guidelines for determining model fit. Electronic Journal of Business Research Methods, 6(1), 53–60. https://academic-publishing.org/index.php/ejbrm/article/view/1224/1187

- Hu, L. T., & Bentler, P. M. (1999). Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling: A Multidisciplinary Journal, 6(1), 1–55. https://doi.org/https://doi.org/10.1080/10705519909540118

- Iman, N. (2018). Is mobile payment still relevant in the fintech era? Electronic Commerce Research and Applications, 30, 72–82. https://doi.org/https://doi.org/10.1016/j.elerap.2018.05.009

- Jarvenpaa, S. L., Tractinsky, N., & Saarinen, L. (1999). Consumer trust in an Internet store: A cross-cultural validation. Journal of Computer-Mediated Communication, 5(2), JCMC526. https://doi.org/https://doi.org/10.1111/j.1083-6101.1999.tb00337.x

- Jayasingh, S., & Eze, U. C. (2015). An empirical analysis of consumer behavioural intention towards mobile coupons in Malaysia. International Journal of Business and Information, 4(2), 221-242. https://www.researchgate.net/publication/267206478_An_Empirical_Analysis_of_Consumer_Behavioral_Intention_Toward_Mobile_Coupons_in_Malaysia

- Khalilzadeh, J., Ozturk, A. B., & Bilgihan, A. (2017). Security-related factors in extended UTAUT model for NFC based mobile payment in the restaurant industry. Computers in Human Behavior, 70, 460–474. https://doi.org/https://doi.org/10.1016/j.chb.2017.01.001

- Khayati, S., & Zouaoui, S. K. (2013). Perceived usefulness and use of information technology: The moderating influences of the dependence of a subcontractor towards his contractor. Journal of Knowledge Management, Economics and Information Technology, 3(6), 68–77. https://citeseerx.ist.psu.edu/viewdoc/download?

- Kim, G., Shin, B., & Lee, H. G. (2009). Understanding dynamics between initial trust and usage intentions of mobile banking. Information Systems Journal, 19(3), 283–311. https://doi.org/https://doi.org/10.1111/j.1365-2575.2007.00269.x

- Koenig-Lewis, N., Marquet, M., Palmer, A., & Zhao, A. L. (2015). Enjoyment and social influence: Predicting mobile payment adoption. The Service Industries Journal, 35(10), 537–554. https://doi.org/https://doi.org/10.1080/02642069.2015.1043278

- Lee, J. (2019). Vietnam and Thailand lead drive to make Southeast Asia cashless. https://asia.nikkei.com/Business/Business-trends/Vietnam-and-Thailand-lead-drive-to-make-Southeast-Asia-cashless

- Lee, M., Cheung, K. O., Christy, M. K., & Chen, Z. (2005). Acceptance of internet-based learning medium: The role of extrinsic and intrinsic motivation. Information & Management, 42, 1094–1104. https://doi.org/https://doi.org/10.1016/j.im.2003.10.007

- Lee, T. (2005). The impact of perceptions of interactivity on customer trust and transaction intentions in mobile commerce. Journal of Electronic Commerce Research, 6(3), 165. http://www.jecr.org/sites/default/files/06_3_p01.pdf

- Leong, L. Y., Hew, T. S., Tan, G. W. H., & Ooi, K. B. (2013). Predicting the determinants of the NFC-enabled mobile credit card acceptance: A neural networks approach. Expert Systems with Applications, 40(14), 5604–5620. https://doi.org/https://doi.org/10.1016/j.eswa.2013.04.018

- Li, D., Chau, P. Y. K., & Lou, H. (2005). Understanding individual adoption of instant messaging: An empirical investigation. Journal of the Association for Information Systems, 6(4), 102–126. https://doi.org/https://doi.org/10.17705/1jais.00066

- Liébana-Cabanillas, F. L., Marinkovic, V., Luna, I. R., & Kalinic, Z. (2018). Predicting the determinants of mobile payment acceptance: A hybrid SEM-neural network approach. Technological Forecasting and Social Change, 129, 117–130. https://doi.org/https://doi.org/10.1016/j.techfore.2017.12.015

- Luo, X., Li, H., Zhang, J., & Shim, J. P. (2010). Examining multi-dimensional trust and multi-faceted risk in initial acceptance of emerging technologies: An empirical study of mobile banking services. Decision Support Systems, 49(2), 222–234. https://doi.org/https://doi.org/10.1016/j.dss.2010.02.008

- Madan, K., & Yadav, R. (2016). Behavioral intention to adopt mobile wallet: A developing country perspective. Journal of Indian Business Research, 8(3), 227–244. https://doi.org/https://doi.org/10.1108/JIBR-10-2015-0112

- Matemba, E. D., & Li, G. (2018). Consumers’ willingness to adopt and use WeChat wallet: An empirical study in South Africa. Technology in Society, 53, 55–68. https://doi.org/https://doi.org/10.1016/j.techsoc.2017.12.001

- Morgan, J. P. (2019). E-commerce payments trends: Vietnam. J.P. Morgan. https://www.jpmorgan.com/merchant-services/insights/reports/vietnam

- Nysveen, H., Pedersen, P. E., & Thorbornsen, H. (2005). Intention to use mobile services: Antecedents and cross-service comparison. Journal of the Academy of Marketing Science, 33(3), 330–346. https://doi.org/https://doi.org/10.1177/0092070305276149

- Oliveira, T., Thomas, M., Baptista, G., & Campos, F. (2016). Mobile payment: Understanding the determinants of customer adoption and intention to recommend the technology. Computers in Human Behavior, 61, 404–414. https://doi.org/https://doi.org/10.1016/j.chb.2016.03.030

- Pavlou, P. A. (2003). Consumer acceptance of electronic commerce: Integrating trust and risk with the technology acceptance model. International Journal of Electronic Commerce, 7(3), 101–134. https://edisciplinas.usp.br/pluginfile.php/941339/mod_resource/content/1/ConsumEcomPavlou.pdf

- Pousttchi, K., & Wiedemann, D. G. (2007). What influences consumers’ intention to use mobile payments. LA Global Mobility Round table, 1–16. https://www.researchgate.net/profile/Key_Pousttchi/publication/228453033_What_influences_consumers'_intention_to_use_mobile_payments/links/0fcfd50f93b6775b68000000.pdf

- Redzuan, N., Razali, A., Muslim, A., & Hanafi, W. (2016). Studying perceived usefulness and perceived ease of use of electronic human resource management (e-HRM) with behavior intention. International Journal of Business Management (IJBM), 1(2), 118–131. https://dokumen.tips/documents/studying-perceived-usefulness-and-perceived-ease-of-volume-1-issue-2-20166intention.html

- Rigopoulos, G., Askounis. (2007). D. A TAM framework to evaluate users’ perception towards online electronic payments. Journal of Internet Banking and Commerce, 12(3), 1–6. https://www.researchgate.net/publication/237406649_A_TAM_Framework_to_Evaluate_Users'_Perception_towards_Online_Electronic_Payments

- Rouibah, K., Lowry, P. B., & Hwang, Y. (2016). The effects of perceived enjoyment and perceived risks on trust formation and intentions to use online payment systems: New perspectives from an Arab country. Electronic Commerce Research and Applications, 19, 33–43. https://doi.org/https://doi.org/10.1016/j.elerap.2016.07.001

- Schierz, P. G., Schilke, O., & Wirtz, B. W. (2010). Understanding consumer acceptance of mobile payment services: An empirical analysis. Electronic Commerce Research and Applications, 9(3), 209–216. https://doi.org/https://doi.org/10.1016/j.elerap.2009.07.005

- Setyadinsa, R., Shihab, M. R., & Sucahyo, Y. (2018). Individual factors as antecedents of mobile payment usage. Proceeding of the Electrical Engineering Computer Science and Informatics, 5(5), 514–518. https://doi.org/https://doi.org/10.11591/eecsi.v5.1678

- Shaw, N. (2014). The mediating influence of trust in the adoption of the mobile wallet. Journal of Retailing and Consumer Services, 21(4), 449–459. https://doi.org/https://doi.org/10.1016/j.jretconser.2014.03.008

- Shin, D. H. (2009). Towards an understanding of the consumer acceptance of mobile wallet. Computers in Human Behavior, 25(6), 1343–1354. https://doi.org/https://doi.org/10.1016/j.chb.2009.06.001

- Singh, N., Sinha, N., & Liébana-Cabanillas, F. J. (2020). Determining factors in the adoption and recommendation of mobile wallet services in India: Analysis of the effect of innovativeness, stress to use and social influence. International Journal of Information Management, 50, 191-205. https://doi.org/https://doi.org/10.1016/jijinfomgt.

- Singh, N., Srivastava, S., & Sinha, N. (2017). Consumer preference and satisfaction of M-wallets: A study on North Indian consumers. International Journal of Bank Marketing.

- Slade, E., Williams, M., Dwivedi, Y., & Piercy, N. (2015). Exploring consumer adoption of proximity mobile payments. Journal of Strategic Marketing, 23(3), 209–223. https://doi.org/https://doi.org/10.1080/0965254X.2014.914075

- Soper, D. S. (2019). A-priori sample size calculator for structural equation models [software]. https://www.danielsoper.com/statcalc

- Sun, H., & Zhang, P. (2006). Causal relationships between perceived enjoyment and perceived ease of use: An alternative approach. Journal of the Association for Information Systems, 7(9), 618–645. https://aisel.aisnet.org/jais/vol7/iss9/24

- Tabachnick, B. G., & Dan Fidel, L. S. (2007). Using multivariate statistics. Person Education Inc.

- Thailand, P. W. C. (2019). Mobile payments in Vietnam fastest growing globally, Thailand emerges second in Southeast Asia. https://www.pwc.com/th/en/press-room/press-release/2019/press-release-30-04-19-en.html

- Thakur, R., & Srivastava, M. (2014). Adoption readiness, personal innovativeness, perceived risk and usage intention across customer groups for mobile payment services in India. Internet Research, 24(3), 369–392. https://doi.org/https://doi.org/10.1108/IntR-12-2012-0244

- Toufaily, E., Nizar, S., & Ladhari, R. (2013). Consumer trust toward retail websites: Comparison between pure click and click-and-brick retailers. Journal of Retailing and Consumer Services, 20(6), 538–548. https://doi.org/https://doi.org/10.1016/j.jretconser.2013.05.001

- Turner, M., Kitchenham, B., Brereton, P., Charters, S., & Budgen, D. (2010). Does the technology acceptance model predict actual use? A systematic literature review. Information and Software Technology, 52(5), 463–479. https://doi.org/https://doi.org/10.1016/j.infsof.2009.11.005

- Van Der Heijden, H. (2004). User acceptance of hedonic information systems. MIS Quarterly, 28(4), 695–704. https://doi.org/https://doi.org/10.2307/25148660

- Venkatesh, V., Morris, M. G., Davis, G. B., & Davis, F. D. (2003). User acceptance of information technology: Toward a unified view. MIS Quarterly, 27(3), 425–478. https://doi.org/https://doi.org/10.2307/30036540

- Venkatesh, V., Thong, J. Y., & Xu, X. (2012). Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Quarterly, 36(1), 157–178. https://doi.org/https://doi.org/10.2307/41410412

- Wang, L., & Yi, Y. (2012). The impact of use context on mobile payment acceptance: An empirical study in China. In Advances in computer science and education (pp. 293–299). Springer.

- Wang, Y. S., Lin, H. H., & Luarn, P. (2006). Predicting consumer intention to use mobile service. Information Systems Journal, 16(2), 157–179. https://doi.org/https://doi.org/10.1111/j.1365-2575.2006.00213.x

- Yang, Y., Liu, Y., Li, H., & Yu, B. (2015). Understanding perceived risks in mobile payment acceptance. Industrial Management & Data Systems.

- Zainudin, A. (2010). Research methodology for business and social science. Universiti Teknologi Mara Publication Centre (UPENA).

- Zhang, J., Huang, J., & Chen, J. (2010). Empirical research on user acceptance of mobile searches. Tsinghua Science and Technology, 15(2), 235–245. https://doi.org/https://doi.org/10.1016/S1007-0214(10)70056-0

- Zhou, T. (2011). An empirical examination of initial trust in mobile banking. Internet Research, 2(5), 1085–1091. https://doi.org/https://doi.org/10.1108/10662241111176353