?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study investigates the association between institutional investors’ ownership and sell-side analysts’ stock recommendations in the context of the heterogeneous nature of institutional investors. Based on a sample of 281 Malaysian public listed companies over the period 2008–2013 (732 company-year observations), we find a significant positive relationship between institutional ownership, in particular ownership held by privately managed institutional investors and sell-side analysts’ stock recommendations, but no significant relationship between state owned institutional investors and sell-side analysts’ stock recommendations. This suggests that the relationship between institutional investors and analysts’ stock recommendations are different among different types of institutional investor. Our results are robust to tests for potential endogeneity between institutional ownership and analysts’ stock recommendations.

PUBLIC INTEREST STATEMENT

While the role of institutional investors in ensuring effective corporate governance is well established in the literature, it is unclear how this role translates into analyst stock recommendation. This study examines such relationship in an emerging market, Malaysia. The results suggest that relationship between institutional investor and analyst recommendation varies according to the types of institutional investor. Analysts seem to favour privately managed institutional investors, as reflected in them giving more favourable stock recommendations for firms with higher equity ownership by privately managed institutional investors. However, no significant relationship is found between state owned institutional investors and analyst recommendation. These findings imply that institutional investors are not homogeneous, and analysts perceive privately managed institutional investors are more engaged in value-enhancing activities through active monitoring.

1. Introduction

Institutional investors control a considerable percentage of capital markets worldwide, which gives them significant influence over these markets (Bena et al., Citation2017). Recent statistics by the Organisation for Economic Cooperation and Development (OECD) show that institutional investors hold around 41% of global market capitalisation (De La Cruz et al., Citation2019). As such, they play a significant role through constructive engagement and shareholder activism to improve the corporate governance of their investees or portfolio firms (Paek et al., Citation2020; Tan, Citation2019). Previous studies show that ownership by institutional investors has led to an improvement in the quality of reported earnings and corporate disclosure (Bird & Karolyi, Citation2016; Velury & Jenkins, Citation2006), stock returns (Jiambalvo et al., Citation2002), firm performance (Muniandy et al., Citation2016; Yang & Shyu, Citation2019), real social impact (Chen et al., Citation2020), and return volatility (Lin et al., Citation2018). In short, institutional investors represent an effective governance mechanism that alleviates agency conflict, resulting in better company outcomes. However, recent studies recommend researchers to consider the heterogeneity of institutional investors rather than seeing them as a homogeneous group (Chichernea et al., Citation2015; Dasgupta et al., Citation2020; De-la-hoz & Pombo, Citation2016; Garel, Citation2017; Muniandy et al., Citation2016; Oikonomou et al., Citation2020).

Institutional investors may have different investment horizons and engage in different forms of governance, with differential effects on company outcomes (Dasgupta et al., Citation2020; Edmans, Citation2014). For example, short-term (transient) institutional investors monitor companies’ activities via “exit”, that is through informed selling, without actually trying to intervene (Edmans, Citation2014). On the other hand, long-term (dedicated) institutional investors monitor companies by direct intervention,Footnote1 or “voice”, and are likely to press for greater transparency (Edmans, Citation2009; Switzer & Wang, Citation2017). However, while the role of institutional investors in ensuring effective corporate governance and increasing firm transparency is well established in the literature, it is unclear how this role translates into analysts’ stock recommendations, given the heterogeneity of institutional investors.

Financial analysts, who are mostly industry professionals, are key players in the financial markets, acting as sophisticated information intermediaries between companies and investors. They follow public listed companies (PLCs) and disseminate information such as earnings forecasts, stock recommendations and target price via research reports (García-Sánchez et al., Citation2020, Citation2019; Healy & Palepu, Citation2001; Imam & Spence, Citation2016; Pan & Xu, Citation2020; Su et al., Citation2020). Their stock recommendations and earnings forecasts are considered by executives as one of the most influential factors impacting their firms’ stock prices (Graham et al., Citation2005). Despite the key role played by financial analysts in accumulating and synthesising information from management and other sources on behalf of capital market participants (Newton, Citation2019), little is known about the association between institutional investor ownership and analyst stock recommendation, especially in emerging markets.

Malaysia provides a fertile ground to examine institutional investor ownership and analyst stock recommendation, for several reasons. First, in emerging economies the capital markets have experienced a dramatic increase in institutional investor ownership (Tee et al., Citation2017), encouraging regulators to demand greater monitoring of institutional investors on their stewardship, especially after the sub-prime mortgage crisis of 2008 and 2009 (OECD, Citation2009). In Malaysia, institutional investors with share ownership of more than 5% comprise 94% of the Top 100 Malaysian PLCs (Asian Development Bank, Citation2014). Compared to other countries in the East Asian region, Malaysia has one of the highest ownership concentrations (Fan & Wong, Citation2005), and a high level of institutional investors’ shareholdings (Abdul Wahab et al., Citation2007). Second, institutional investors in Malaysia are subject to government roles and interference; the Malaysian government has an active and dominant ownership in the financial market through government-linked investment companies (GLIC) (Abdul Wahab et al., Citation2008; Gomez et al., Citation2018; Tee, Citation2017). As a result, the effect of government ownership on capital markets and firm governance cannot be ignored. Third, the heterogeneity of institutional investor shareholding in Malaysia (Abdul Wahab et al., Citation2007) provides a good opportunity to examine the heterogeneous nature of institutional investors’ activism. Fourth, the analyst reports are publicly available on the Bursa Malaysia website for Malaysian companies that participated in the exchange-sponsored research scheme (see section 3.1 for details), which provides an excellent opportunity for scholars to study analysts’ stock recommendations.

This study uses a set of 281 Malaysian PLCs for the period 2008 to 2013 (732 company-year observations). The results show a positive and significant relationship between institutional investor ownership and analyst stock recommendation. Further, we extend our analysis to reflect the heterogeneity in institutional investor ownership in Malaysia, and the results show that privately owned institutional investors have a positive and significant relationship with analysts’ stock recommendations. Specifically, companies with a higher level of ownership by institutional investors comprising privately managed unit trusts, banks and insurance companies with limited links to the government i.e. non government linked investment companies (non-GLIC) gain more favourable stock recommendations from financial analysts. This suggests that from the analysts’ perspective, privately managed institutional investors engage in value-enhancing activities through active monitoring, consistent with agency theory. However, we find no significant relationship between ownership by GLIC and sell-side analysts’ stock recommendations. Our results are robust to tests for potential endogeneity between institutional investor ownership and analyst stock recommendations. The result showing that institutional investor types matter to analysts and may affect their behaviour is in broad agreement with the stream of literature that illustrates institutional investor preference for governance mechanisms and corporate policies differ according to their types (Alvarez et al., Citation2018; De-la-hoz & Pombo, Citation2016; Sherman et al., Citation1998).

The study makes the following contributions. First, most studies that examine the determinants of analysts’ stock recommendations have considered various firm-specific factors such as corporate governance strength (Papangkorn et al., Citation2020; Yu, Citation2011), corporate social responsibility initiatives (Alazzani et al., Citation2021; García-Sánchez et al., Citation2020; Ioannou & Serafeim, Citation2015; Wan-Hussin et al., Citation2021), earnings growth and risk (Peasnell et al., Citation2018), shareholder rights (Autore et al., Citation2009), equity incentive plans (Liu, Citation2017), financial restatements (Qasem et al., Citation2020) and degree of internationalisation (Luo & Zheng, Citation2018). Our study extends the literature by examining the relationship between institutional investor heterogeneity and sell-side analyst stock recommendation, an area that has so far received little attention. Second, most prior studies partition institutional investors into pressure-sensitive versus pressure-resistance (Brickley et al., Citation1988), transient versus dedicated (Bushee, Citation1998), foreign versus local (Tee, Foo et al., Citation2018) or independent versus grey (Alvarez et al., Citation2018; De-la-hoz & Pombo, Citation2016). We are among a few studies that classify institutional investors into state owned versus non-government-linked, inspired by Annuar (Citation2015) and Tan (Citation2019). Third, we add to the sparse literature of analyst behaviour in emerging markets. A few Malaysian studies have examined the relationship between corporate governance, culture, political patronage and analysts’ forecast errors (Abdul Wahab et al., Citation2018, Citation2015), association between institutional ownership, political connections and analyst following (How et al., Citation2014), and the influence of financial restatements on the sell-side analysts’ stock recommendations (Qasem et al., Citation2020). None has examined the relationship between types of institutional investor ownership and analyst stock recommendation, which makes our study unique. Our results should be useful to capital market regulators in recognising the differential effects of institutional investors in monitoring investee companies, based on analyst behaviour. The study offers some insights for policymakers and investors into how analysts’ stock recommendations might be influenced by the nature of institutional investor ownership (state versus privately managed).

The structure of the paper is as follows: Section 2 discusses the institutional background; Section 3 presents the literature review and hypothesis development; Section 4 discusses the research design; and Section 5 provides the empirical results and discussion. Section 6 offers further analysis; and Section 7 concludes the paper.

2. Background

2.1. Malaysian capital market

The stock market in Malaysia is one of the region’s leading emerging markets (Yusof & Majid, Citation2008). Bursa Malaysia is considered as one of the largest ASEAN stock exchanges with more than 900 listed companies. It comprises three main markets. The Main Market is the primary market for big companies with a strong track record of operations and profitability. The ACE Market is a sponsor-driven market for small companies with a shorter track record but high growth prospects. Lastly, the LEAP Market, launched in 2017, is an advisor-driven market that provides emerging small and medium-sized enterprises (SMEs) with greater access and visibility to funding through public markets. Corporate ownership in the Malaysian stock market can be divided by ethnicity: Malay, Chinese, Indian and other small minority groups (Abdul Wahab et al., Citation2015). According to Ball et al. (Citation2003), almost 69% of the market capitalisation is dominated by the Chinese group, while Bumiputera shareholdings stood at 21.9% in 2008 even after the implementation of the New Economic Policy (NEP) in 1970, which aimed to increase BumiputeraFootnote2 shareholdings in the capital market by various means (Benjamin et al., Citation2016; How et al., Citation2014). Various institutional funds were set up by the Malaysian government to increase the Bumiputera shareholdings from nearly zero in 1970 to at least 30% (Tee, Foo et al., Citation2018).

2.2. Institutional investors in Malaysia

Institutional investors are one of the major players in the Malaysian stock market, holding around 13% and 16.8% of the shareholdings in 2003 and 2009 respectively (How et al., Citation2014). In 2016, the market capitalisation of Bursa Malaysia was recorded at RM1.7 trillion, with local institutional investors owning 53% and foreign institutional investors 27% (Tee, Foo et al., Citation2018). In general, institutional investors in Malaysia, whether local or foreign, can be classified into four main groups: government-backed funds, unit trusts, insurance companies, and banks. Among the local institutional investors, government-backed funds are the dominant group, a unique feature in the Malaysian capital markets (Tee, Foo et al., Citation2018). Since the formation of the NEP in 1970, local institutional investors have provided government with the vehicle to support and protect the economic interests of Bumiputera investors (How et al., Citation2014). The five largest public institutional investors are Employees Provident Fund (EPF), Lembaga Tabung Angkatan Tentera (LTAT), Lembaga Tabung Haji (LTH), Permodalan Nasional Berhad (PNB) and Social Security Organisation (SOCSO) (Benjamin et al., Citation2016). These institutions are run by Bumiputera who typically hold the position of chair of the board of directors (How et al., Citation2014). The Board and Investment Panels of these institutions are appointed by and report directly to the Ministry of Finance (Benjamin et al., Citation2016; Norhashim & Abdul Aziz, Citation2005).

On the other hand, trust unit or mutual fund companies in Malaysia have grown by 310.5%, from RM87.3 billion in 2004 to RM358.4 billion in 2016 (Tee, Foo et al., Citation2018). Malaysian unit trusts or mutual funds have a unique position as they may be separated into privately managed and government-managed funds. The latter are funds under Amanah Saham Nasional Berhad (ASNB) management, which is completely owned by PNB, one of the government-managed funds established on 17 March 1987 to act as an essential tool in the NEP, with the main objective of encouraging the Bumiputeras’ share ownership in the corporate sectors. The other two main institutional investors, i.e., banks and insurance companies, are regulated by the Bank Negara Malaysia (Central Bank of Malaysia).

The Malaysian Finance Committee on Corporate Governance (FCCG), in particular after the Asian financial crisis, recognises the importance of institutional investors’ involvement with corporate governance. Besides this, FCCG made important recommendations leading to the creation of the Minority Shareholder Watchdog Group (MSWG, Citation2014) in 2000 with funding from four government-controlled institutional funds, LTH, LTAT, SOCSO and PNB, whose primary objective is “to monitor and combat abuses by insiders against the minority” (FCCG, Chapter 6 paragraph 9.1). In 2011, the Malaysian Securities Commission (SC) issued a recommendation on the corporate governance role of institutional investors (Tee et al., Citation2017). In 2014 MSWG and SC jointly issued the new Malaysian Code for Institutional Investors, the main principles of this code being to guide institutional investors in monitoring the investee companies and making investment decisions by incorporating sustainability and corporate governance considerations in the process of investment decision making.

3. Literature review and hypothesis development

Stock recommendations issued by sell-side analysts reflect their judgements on whether companies’ equities are overpriced or underpriced (Francis & Soffer, Citation1997). To set their stock recommendations, analysts develop explicit or implicit valuation models by evaluating and processing a wide variety of companies’ characteristics and specific information (Bradshaw, Citation2004, Citation2011; Conrad et al., Citation2006; Hamrouni et al., Citation2017; Papangkorn et al., Citation2020). Previous studies show that analysts are more likely to issue favourable stock recommendations for the companies which have better bond ratings (Harit, Citation2016), have higher past sales growth, trading volume, and earnings per share (Abarbanell & Bushee, Citation1997; Jegadeesh et al., Citation2004; Stickel, Citation2007). On the other hand, analysts revise their stock recommendations downward as bankruptcy approaches (Clarke et al., Citation2006).

Based on agency theory, analysts are expected to take into consideration corporate governance mechanisms when set their recommendations, as well-governed companies are associated with less agency conflicts and better firm decisions (Papangkorn et al., Citation2020). Prior studies show that analysts incorporate corporate governance strength into their stock recommendations to general investors. For instance, Yu (Citation2011) find that financial analysts have a tendency to issue more favourable stock recommendations for companies with better corporate governance mechanisms. Autore et al. (Citation2009) find that companies with stronger shareholder rights are associated with more favourable stock recommendations. More recently, Papangkorn et al. (Citation2020) conclude that companies with fewer co-opted directors tend to receive more favourable stock recommendations, which suggests that analysts prefer companies with strong corporate governance. Bednar et al. (Citation2015) support this view and argue that analysts negatively assess companies that adopt “poison pills”.

3.1. Sell-side analysts stock recommendations and institutional investors’ ownership

Efficient monitoring hypothesis suggests that institutional investor ownership has been recognised as an important corporate governance mechanism that plays a significant role in alleviating agency problems between managers and shareholders (Agrawal & Mandelker, Citation1990; Bataineh, Citation2021; Liu, Citation2017; Roberts & Yuan, Citation2010; Shleifer & Vishny, Citation1986). Institutional investors can pressure company management to adopt better corporate governance either directly through active monitoring or indirectly through the power of their trading shares (Aggarwal et al., Citation2011; Alnabsha et al., Citation2018; Gillan & Starks, Citation2003). Institutional investors have more incentive to monitor because they have invested large amounts in the companies that form part of their portfolio, and also enjoy the benefits of economies of scale and expertise (Chowdhury & Wang, Citation2009; Hartzell et al., Citation2014; Shin & Seo, Citation2011).

The argument of this study is based on the efficient monitoring hypothesis whereby analysts will consider the existence of institutional investors in the companies’ ownership as an indicator of effective corporate governance mechanisms when they evaluate the companies and form their opinion. In Malaysia, the effectiveness of institutional investors as monitoring bodies has been recognised in previous studies. For example, the existence of institutional investor leads to improved earnings quality (Abdul Jalil & Abdul Rahman, Citation2010; Tee & Rasiah, Citation2020), improved stock price informativeness (Tee, Citation2017), lower risk of stock price crashes (Tee, Citation2019; Tee, Yee et al., Citation2018), attenuated cost of debt (Tee, Citation2018), demand for higher audit quality (Tee et al., Citation2017), and is associated with higher dividend payouts (Benjamin et al., Citation2016) which indicate effective monitoring. Therefore, sell-side analysts as information intermediaries should issue more favourable stock recommendations for the companies with higher institutional investor ownership. Thus, the first hypothesis is stated as follows:

H1: There is a positive relationship between institutional investors’ ownership and sell-side analysts’ stock recommendations.

3.2. Sell-side analysts stock recommendations and types of institutional investors

Looking more closely at the influence of institutional investors’ ownership on sell-side analysts’ stock recommendations, this study examines how the heterogeneity of institutional investors may affect the analysts. Institutional investors’ heterogeneity suggests that they will arrive at different terms and conditions in their agency contracts with the companies’ managers (Ryan & Schneider, Citation2003). The results of previous studies suggest that institutional investors differ dramatically in their investment styles and forms of governance, are affected by company characteristics in different ways, and have different effects on company outcomes (Borochin & Yang, Citation2017; Edmans, Citation2014; Garel, Citation2017). Chang et al. (Citation2012) indicate that institutional investors’ heterogeneity, as short-term or long-term investors, means that these groups are more likely to have different objectives and influence the companies in very different ways.

Privately managed institutional investors with a short-term investment horizon can enforce corporate governance and discipline the company management via share trading, otherwise known as “exit,” or “voting with their feet” (Edmans, Citation2014; Switzer & Wang, Citation2017). If the company’s manager destroys value, these institutions can sell their shares, pushing down the stock price and thus punishing the manager (Edmans, Citation2014). Such monitoring creates a more transparent information environment and also lowers the companies’ cost of equity (Chang et al., Citation2012). Edmans (Citation2009) shows that privately managed institutional investors can improve firm value. In this regard, Mintchik et al. (Citation2014) find a negative relationship between sell-side analysts’ earnings forecast error and a higher percentage of privately managed institutions’ ownership. Further, Firth et al. (Citation2013) find that the optimism of sell-side analysts’ stock recommendations increases if the companies’ stocks are held by mutual fund clients. The argument is therefore in the same direction as the efficient monitoring hypothesis of institutional investors, where we expect that analysts will issue more favourable stock recommendations for companies with a higher level of equity ownership held by privately managed institutional investors. In the Malaysian context, we argue that institutional investors such as privately-managed unit trust, banks and insurance companies are generally regarded as privately managed institutional investors.

On the other hand, the state involvement in business in Malaysia can be seen in the significant role played by the GLIC in the economy, with its unique consequences (Tan, Citation2019). The Malaysian Ministry of Finance has classified seven entities as GLIC, namely Minister of Finance Incorporated (a company under the jurisdiction of the Malaysian Ministry of Finance), Khazanah Nasional Berhad (the sovereign wealth fund), PNB, EPF, public sector pension funds (KWAP), LTH and LTAT. In 2013, 35 of the Top 100 listed companies in Malaysia were identified as government-linked companies (GLC) and represented 42% of the total market capitalisation (Gomez et al., Citation2018). The GLIC have a role in national development and the promotion of Bumiputera participation in the economy. As such, the state exerts control over GLIC through a variety of mechanisms, including board appointments of GLIC. These institutions are run by Bumiputera who typically hold the position of chair of the board of directors. Appointments to the Investment Advisory Board for these institutions are politically motivated (Norhashim & Abdul Aziz, Citation2005) as the Board reports directly to the Ministry of Finance (Benjamin et al., Citation2016). The investments of these institutional investors are heavily biased towards Bumiputera-run corporations (Norhashim & Abdul Aziz, Citation2005).

How et al. (Citation2014) argue that these GLIC are more likely to skew their investment to politically connected companies rather than companies with better corporate governance. In this regard, Lim et al. (Citation2016) find that these institutions do not contribute to the efficient processing of market-wide news in the Malaysian stock market; they assume the reason is that the majority of these institutions are government-controlled. Similarly, Chen et al. (Citation2010) conclude that analysts around the world experience greater difficulty in predicting the earnings of firms with political connections than their non-government-linked counterparts. In light of the above discussion, we expect the effect of state owned institutional investors on analyst recommendation is more muted as compared to the relationship between privately managed institutional investors and analyst recommendation . Thus, it is hypothesised that:

H2: Privately managed institutional investor has a stronger, positive relationship with analyst recommendation than does state owned institutional investor.

4. Research design

4.1. Sample data

Our sample comprises Malaysian PLCs listed on the Bursa Malaysia that participated in the Capital Market Development Fund (CMDF)—Bursa Research Scheme (CBRS) for the period 2008 to 2013. Bursa Malaysia launched the CBRS scheme in 2005, with the main aim of generating research coverage for Malaysian PLCs and providing investors with more information to help them in making investment decisions (Qasem et al., Citation2015). For the purpose of this study, selected companies must have participated in the CBRS scheme during the study period and have had at least one stock recommendation from one to six months after the issuance of the company’s annual report. Consequently, a total of 281 companies (732 company-year observations) are included in the sample. A summary of the sample selection criteria and distribution by sector is presented in , Panels A and B.

Table 1. Sample of study

The data related to stock recommendations, institutional investor and managerial ownerships, and board composition are collected manually from CBRS analysts’ reports and annual reports, which can be downloaded from the Bursa Malaysia website. Other data such as market capitalisation, leverage, book to market ratio, return on asset, share price return, earnings to price ratio and firm age are collected from Thomson Reuters DataStream.

4.2. Measurement of variables

4.2.1. Stock recommendation

We use the mean of CBRS analysts’ recommendations for each company from one to six months after the issuance of the company’s annual reports as the dependent variable for our empirical specifications (REC). CBRS research analysts issue three types of stock recommendation: buy, hold or sell. For the purpose of this study, REC is coded 1 if the recommendation is unfavourable “sell”, 2 if it is neutral “hold” and 3 if it is favourable “buy” (Arand & Kerl, Citation2015; Barber et al., Citation2006). Therefore, for a given company in the focal year, we first collect all CBRS analysts’ recommendations from one to six months after the issuance of the company’s annual reports, and then calculate the mean of these recommendations.

4.2.2. Institutional investors’ ownership

Institutional investors’ ownership is measured as the proportion of institutional investors’ shareholding (the total shares owned by institutional investors divided by the total shares outstanding) (Ghafoor et al., Citation2019; Tee, Citation2020; Zheng, Citation2010); the shareholding data is extracted from the list of the 30 largest shareholders reported in the company’s annual reports. We classify institutional investors according to privately managed institutions or state owned institutions. Privately managed institutions (IO_PRIV) include banks, privately managed unit trusts and mutual funds, and insurance companies. State owned institutions (IO_GOVT) include government-managed unit trust funds, government-managed pension funds (EPF, KWAP and LTAT), government-managed pilgrimage funds (LTH), and other GLIC such as Minister of Finance Incorporated, SOCSO, PNB, ValueCAP Sdn Bhd (Vlauecap), Federal Land Development Authority (FELDA), Petroliam National Berhad (PETRONAS) and the government-managed sovereign wealth fund Khazanah Nasional Berhad.

4.2.3. Control variables

Following previous studies on analysts’ outputs (Autore et al., Citation2009; Han et al., Citation2014; Ioannou & Serafeim, Citation2015; Jegadeesh et al., Citation2004; Liu, Citation2016, Citation2017; Qasem et al., Citation2020), this study includes several control variables, namely managerial ownership (MOWN), board size (BSIZE), board independence (BINDP), company size (LNSIZE), leverage (LEVGE), book to market ratio (BTM), company profitability (ROA), company return (RETURN), earning to price ratio (EP), and company age (AGE). The rationales for their inclusion are provided below.

Han et al. (Citation2014) and Liu (Citation2016) find a positive relationship between the precision of sell-side analysts’ earnings forecasts and managerial ownership, consistent with the alignment view of managerial ownership. This study therefore predicts the positive effect of managerial ownership on sell-side analysts’ stock recommendations. Some studies argued that small board size is more effective as the members can make sound decisions in less time than the bigger boards (Jensen, Citation1993; Yermack, Citation1996). In contrast, Haniffa and Hudaib (Citation2006) argue that large board size seems to provide companies with the diversity of contacts, experience and expertise needed to improve performance. Accordingly, this study predicts the non-directional effect of board size on sell-side analysts’ stock recommendations. Since board independence is often associated with strong corporate governance, this study expects a positive relationship between board independence and analysts’ stock recommendations.

Ioannou and Serafeim (Citation2015) claim that financial analysts may issue optimistic recommendations for larger companies because trading in them generates more commission and investment banking business. This study follows Gu et al. (Citation2013) and Young and Peng (Citation2013), who control for leverage in modelling analyst stock recommendations. Previous studies show that companies with a higher book to market ratio perform better, have higher earnings, higher returns and a larger analyst following (Da & Schaumburg, Citation2011; Ertimur et al., Citation2011). This study predicts that sell-side analysts will issue more favourable stock recommendations for companies with higher BTM, higher ROA, better-performing stocks, and higher earnings to price ratio (Ioannou & Serafeim, Citation2015; Jegadeesh et al., Citation2004). Finally, this study controls for company age, the number of years a company has been in operation until the year of stock recommendations. It is argued that more mature companies disclose greater amounts of information (Subramaniam et al., Citation2016). Thus, this study expects that the older companies will earn more favourable stock recommendations from sell-side analysts.

4.3. Model specification

Given that the dependent variable is a continuous variable representing the mean score of analysts’ stock recommendations, a pooled ordinary least square (OLS) regression model is used to test the study’s hypotheses. According to Reuveny and Li (Citation2003), some models with pooled time-series cross-sectional data may display heteroscedasticity and serial correlation. To control for these potential problems, the model was estimated using OLS regression with Huber-White robust standard errors. We include industry and year fixed effects to control for systematic variation.

The following models are used to test the hypotheses.

Where is the key to the variable names.

Table 2. Definitions of variables

5. Empirical results and discussion

5.1. Descriptive statistics

reports the descriptive statistics for all the variables in this study. The statistical results show that the mean of stock recommendations (REC) is 2.352. The mean of institutional investors’ ownership (IO_TOTAL) is 16.750% and ranges from 0.000 to 91.280%. This result is consistent with How et al. (Citation2014) who report the mean percentage of institutional investors in Malaysia as 16.884%. The average shareholdings by privately managed institutional investors (IO_PRIV) and state owned institutional investors (IO_GOVT) are 7.321% and 9.429% respectively. This result is consistent with the findings of previous Malaysian studies which report mean scores for GLICs between 8% and 9.70% (Abdul Wahab et al., Citation2007; Tee et al., Citation2017).

Table 3. Descriptive statistics for all variables (n = 732)

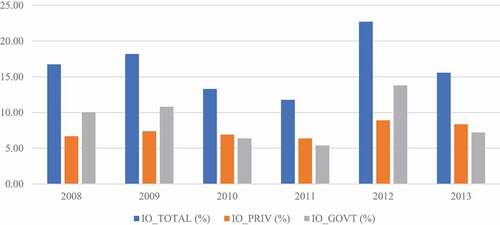

and illustrate the yearly mean of IO_TOTAL, IO_PRIV and IO_ GOVT over the study period. The table shows fluctuations in institutional investors ownership over the years with highest ownership in 2012 (22.71%, 8.91%, 13.80%) and lowest in 2011 (11.78%, 6.38%, 5.40%) for IO_TOTAL, IO_PRIV and IO_ GOVT respectively. The highest ownership institutional investors in 2012, may be due to the growing importance placed upon them to participate in the ownership and monitoring of Malaysian PLCs, as advocated in the CG Blueprint (2011, p. 13) “institutional investors are in a unique position to exercise influence over companies and to hold them accountable for good governance. Given the typically significant stake they hold, they have the ability to demand meetings with the senior management of companies, challenge them on issues of concern, discuss strategies for achieving the companies’ goals and objectives and be the leading voice of shareholders in demanding corrective action when wrongdoing occurs”.

Figure 1. Distribution of average institutional investor ownership (%) by year

Table 4. Institutional investors’ types and shareholdings (n = 732)

With regards to the control variables, indicates that the average direct managerial ownership (MOWN) is 9.525% with a maximum of 71.150% and minimum 0. The average board size is almost 8, and mean board independence (BINDP) is 44%, similar to previous Malaysian studies showing it to be around 45–50% (Ghaleb et al., Citation2020; Katmon et al., Citation2019). Regarding company size, which is proxied by market capitalisation (SIZE), there is considerable variation, ranging from RM8.6 million to RM77.6 billion with a mean of RM2.2 billion. In addition, the average debt to assets ratio is 19%, consistent with AlQadasi and Abidin (Citation2018) who report a mean for LEVGE of 19%. The book to market ratio (BTM) mean is 1.233, ranging from 0.006 to 7.373. The results also show that the sample companies are profitable with an average ROA of 7.103%. The mean of company return is 0.074, ranging from −0.937 to 4.900, and the earnings to price ratio (EP) mean is 0.102, ranging from −2.829 to 1.212. Finally, the mean company age is 20.4 years.

In , we divide the companies into those with “high” and “low” institutional investors’ ownership using the sample median as the cut-off. The results in show a significant mean difference in analysts’ stock recommendations (REC) between the companies with high and low institutional investors’ ownership. This suggests that analysts tend to issue more favourable stock recommendations for companies with higher institutional investors’ ownership. The univariate tests also show significant mean differences for most of the control variables except company return (RETURN) and earnings to price ratio (EP) between the companies with high and low institutional investors’ ownership.

Table 5. Tests of differences in mean between firms with high and low institutional investors

5.2. Correlation analysis

This study uses Pearson correlation to test for significant relationships between variables. Consistent with study expectations, the results in show a positive and significant correlation between institutional investors (IO_TOTAL) and stock recommendations (REC). Further, the results show a positive and significant correlation between privately managed institutional investors (IO_PRIV) and stock recommendations (REC). Hence, the initial results support the study hypotheses that analysts issue more favourable stock recommendations for companies with a higher level of institutional investors’ ownership. Regarding the control variables, the results show a positive and significant correlation between REC and most of the control variables, namely, company size (LNSIZE), return on assets (ROA), earnings to price ratio (EP), and share return (RETURN). In contrast, the results show negative and significant correlation between REC and company leverage (LEVGE). The variance inflation factor is less than 10 (unreported), indicating no multicollinearity problem.

Table 6. Correlation matrix (n = 732)

5.3. Regression results

reports the results of the influence of institutional investors’ ownership on sell-side analysts’ stock recommendations. In model (1) we include institutional investors and in model (2) the heterogeneity of institutional investors. Overall, as shown in , regression models in all columns are significant. The highly significant results indicate that most explanatory variables have a significant effect on sell-side analysts’ stock recommendations.

Table 7. Ordinary Least Square (OLS) regression results

Consistent with expectations, the results in model (1) indicate that institutional investors are positively and significantly associated with sell-side analysts’ stock recommendations (Coef. = 0.003, p-value = 0.024). This implies that sell-side analysts issue more favourable stock recommendations for companies with a higher level of ownership by institutional investors. This result supports the arguments that the presence of institutional investors represents an effective governance mechanism that alleviates agency conflict, resulting in good company outcomes, reflected in the analysts’ stock recommendations.

In model (2) we include the heterogeneity of institutional investors in Malaysia (privately managed and state owned). The results show a positive and significant relationship between IO_PRIV and sell-side analysts’ stock recommendations (Coef. = 0.006, p-value = 0.001). This implies that the analysts issue more favourable stock recommendations for companies with a higher level of IO_PRIV ownership. These findings are consistent with previous studies, that through their trading activities and monitoring via exit, IO_PRIV can improve a company’s value, reflected in optimistic stock recommendations. Furthermore, our result is consistent with those of Gu et al. (Citation2013) and Firth et al. (Citation2013), who find that sell-side analysts issue more optimistic stock recommendations for companies which emphasise mutual funds.

Furthermore, the results show no significant association between IO_GOVT and analysts’ stock recommendations. This insignificant result could be attributed to the fact that the mechanisms of corporate governance and many business dealings in emerging markets are based on political considerations (Haniffa & Hudaib, Citation2006; Mohammed et al., Citation2017). According to Faccio (Citation2006), nearly one-third of the Malaysian listed companies are known to be politically connected. In Malaysia, most of IO_GOVT are domestic institutional investors such as EPF, PNB, LTH, LTAT and SOCSO. These institutions are run by Bumiputra who are naturally the Chair of the board of directors. Appointment to the Investment Advisory Board for these institutions is politically motivated (Norhashim & Abdul Aziz, Citation2005). In addition, previous studies indicate that preferential treatment for politically connected companies, as proxied by Bumiputra directors, will lead these companies to be inefficient and riskier (Gul, Citation2006; Johl et al., Citation2012). In particular, these companies are more likely to report a loss (Benjamin et al., Citation2016), be charged higher interest rates by lenders (Bliss & Gul, Citation2012), and be charged higher audit fees (Abdul Wahab et al., Citation2009).

With regards to the control variables, the results in show that managerial ownership (MOWN) has a positive and significant association with sell-side analysts’ stock recommendations (REC) with a significance level of 5% (Coef. = 0.003, p = 0.050) and (Coef. = 0.003, p = 0.047) in models 1 and 2 respectively. These results are consistent with other studies which support the shareholder alignment view of managerial ownership (Han et al., Citation2014; Liu, Citation2016, Citation2017). Further, book to market ratio (BTM) has a positive and significant relationship with REC with a significance level of 5% (Coef. = 0.073, p = 0.019) and (Coef. = 0.047, p = 0.018) in models 1 and 2 respectively, indicating that analysts tend to issue more favourable recommendations for companies with higher BTM. In terms of company profitability, ROA has a positive and significant relationship with REC with a significance level of 1% (Coef. = 0.013, p = <0.001) and (Coef. = 0.013, p = <0.001) in models 1 and 2 respectively. These results show that analysts issue more optimistic recommendations for highly profitable companies, which is consistent with previous empirical studies (Gu et al., Citation2013; Ioannou & Serafeim, Citation2015).

There is a positive and significant relationship between RETURN and REC with a significance level of 1% (Coef. = 0.117, p = <0.001) and (Coef. = 0.115, p = <0.001), indicating that analysts have a tendency to issue optimistic stock recommendations for companies with higher RETURN, consistent with the results from previous studies (Ioannou & Serafeim, Citation2015). Earnings to price ratio (EP) is positively and significantly associated with the sell-side REC with a significance level of 5% (Coef. = 0.289, p = <0.001) and (Coef. = 0.283, p = <0.001). This indicates that companies with higher EP gain more favourable stock recommendations, consistent with the findings of previous studies (Gu et al., Citation2013; Ioannou & Serafeim, Citation2015; Jegadeesh et al., Citation2004). For other control variables, BSIZE, BINDP, LNSIZE, LEVGE, and LNAGE, the results show no significant relationship with sell-side analysts’ stock recommendations.

6. Additional analyses

6.1. Random-effect Ordinary Least Square (OLS)

As a further robustness check, this study re-examined the main hypotheses using random-effects OLS regressions (employing the STATA procedure, xtreg). As shown in , the main findings remain unchanged.

Table 8. Random-effect Ordinary Least Square (OLS) regression results

6.2. Endogeneity test

The endogeneity problem occurs when the dependent variable is influenced by factors that simultaneously affect the independent variables (Brauer & Wiersema, Citation2018; Ghaleb et al., Citation2021). By offering advice in terms of stock recommendations, financial analysts highlight institutional investors’ awareness as the key audience for their research, which influences company values as well as the demand for stock (Brauer & Wiersema, Citation2018). Chen and Cheng (Citation2006) also find that analysts’ stock recommendations significantly influence institutional investors’ ownership, meaning that institutional investors increase their holdings in companies with more favourable stock recommendations.

However, to alleviate possible endogeneity in our models, we employed the two-stage least squares (2SLS) technique with instrumental variables (IVs). This technique has been widely used in previous studies to alleviate endogeneity bias such as omitted variables, measurement error and reverse causality (AL-Qadasi et al., Citation2019; Chichernea et al., Citation2015; Chung et al., Citation2015; How et al., Citation2014; Huang & Petkevich, Citation2016). To identify the suitable IVs, we seek to find instruments that may influence institutional investors but not analysts’ stock recommendations except indirectly through other independent variables.

Following previous studies, the selected instrument variables for (IO_TOTAL, IO_PRIV, and IO_GOVT) are dividends, systematic risk, and company size (Chichernea et al., Citation2015; Chung et al., Citation2015; How et al., Citation2014; Huang & Petkevich, Citation2016). Chichernea et al. (Citation2015) find that different institutional investors (short-term versus long-term) have different perferences towards dividends; we therefore use annual devidend per share (DVD) as proxy for company dividend. How et al. (Citation2014) assert that systematic risk is more likely to affect institutional ownership, so we use BETA as a proxy of systematic risk. Finally, institutional investors are more likely to be attracted to larger companies (Al-Jaifi et al., Citation2019); we use the natural logarithm of market capitalisation (LNSIZE) to proxy for company size.

Panel A of shows the results of the first-stage regressions that use IO_TOTAL, IO_PRIV, and IO_GOVT as the dependent variables. These are regressed on selected IVs, and other control variables. The first-stage regression results (columns 1, 2, and 3) indicate DVD is negatively associated with IO_PRIV. BETA is negatively associated with IO_TOTAL and IO_GOVT. Finally, LNSIZE is positively associated with IO_TOTAL, IO_PRIV, and IO_GOVT, respectively. The reported significant F-test results suggest that the instruments are strong, thus rejecting the hypothesis that these instruments can be excluded from the first-stage regressions.

Table 9. Two-stage least squares (2SLS) equations

Panel B of (columns 1, 2, and 3) present the results from the second-stage regressions, where the analysts’ stock recommendations are the dependent variable. Consistent with our main results (i.e. OLS results in ), the 2SLS approach finds a positive and significant relationship between IO_TOTAL and IO_PRIV and sell-side analysts’ stock recommendations. These results suggest that our main results are not driven by endogeneity.

6.3. Controlling for self-selection bias

The problem of self-selection bias is commonly highlighted in the literature on institutional investors (Elyasiani & Jia, Citation2010; Gaspar et al., Citation2005; Hutchinson et al., Citation2015). To control for this potential problem, we use Heckman’s (Citation1979) two-step procedure as a robustness test, because our sample may be biased. Following the Heckman procedure, we first calculate the Inverse Mills Ratio (IMR) (Heckman, Citation1979; Lennox et al., Citation2012) from the models that predict the factors related to institutional investors’ ownership. The dependent variables in each model are IO_TOTALDMY, IO_PRIVDMY, and IO_GOVTDMY, dummies equal to 1 if the company has a high level of institutional investors’ ownership (above the sample median) and 0 otherwise. columns (1), (3) and (5) show the first-stage probit regression results. In the second stage we include the IMR as a correction factor for potential sample selectivity bias. The results in columns (2), (4) and (6) strengthen the findings in the main analysis.

Table 10. Institutional investors’ ownership and stock recommendations (Heckman, Citation1979)

7. Summary and conclusion

The main objective of this study is to examine the association between institutional investors’ ownership and sell-side analysts’ stock recommendations in the context of the heterogeneous nature of institutional investors. The results suggest that such relationships are indeed different among different types of institutional investor. In particular, we find a significant and positive relationship between total institutional investors’ ownership, privately managed institutional investors and analysts’ stock recommendations. However, no significant relationship between state owned institutional investors and sell-side analysts’ stock recommendations is found.

Our study has some significant implications. First, the results emphasise the crucial role of the financial analyst as an information intermediary and an external monitor in the financial markets. Second, this study has important implications for companies, as the results demonstrate that institutional investors’ ownership is incorporated into analysts’ stock recommendations. Finally, our study offers some insight for policymakers and investors into how analysts’ stock recommendations might be influenced by ownership and control characteristics, such as institutional investors’ ownership. Overall, these findings should be useful to policymakers in emerging countries, in recognising the important role played by institutional investors in monitoring investee companies. As in any research, this study has limitations that should be mentioned to ensure that the findings are interpreted fairly. This study focuses on a limited number of Malaysian companies that participated in the exchange-sponsored CBRS research scheme, ignoring other non-exchange-sponsored analysts’ recommendations as contained in the Thomson I/B/E/S and Bloomberg databases. Future studies may capitalise on analyst reports from these comprehensive databases.

Additional information

Funding

Notes on contributors

Ameen Qasem

Ameen Qasem is an Assistant Professor of Accounting at University of Hail, Saudi Arabia & Taiz University, Yemen. He obtained his PhD in Accounting from Universiti Utara Malaysia (UUM). His research interests include financial restatements, analysts’ recommendations, institutional investors ownership, and CSR reporting.

Norhani Aripin

Norhani Aripin is an Associate Professor at Universiti Utara Malaysia (UUM), Malaysia. She obtained her PhD from Curtin University of Technology, Australia. Her research interest focuses on financial reporting, corporate governance, and CSR reporting.

Wan Nordin Wan-Hussin

Wan Nordin Wan Hussin is a Professor in Financial Reporting and Corporate Governance at Universiti Utara Malaysia (UUM). He obtained his PhD from Warwick Business School, UK. His research interest focuses on financial reporting, audit report lag, financial restatements, corporate governance, and CSR reporting.

Shaker Al-Duais

Shaker AL-Duais is an Assistant Professor of Accounting and Auditing at Faculty of Administrative Science, Ibb University, Yemen. His research interests include earnings management, financial accounting and reporting, corporate governance, and auditing.

Notes

1. Direct intervention would include “the exercise of voting powers, the dissemination of open letters to undermine the credibility of management or the board, the request for special disclosures from the board, holding public meetings, and engaging in private negotiations with management” (Switzer & Wang, Citation2017, p. 59).

2. Bumiputera or Bumiputra means “son of earth” in Malay; translated accurately it means “princes of the earth” and is a formal explanation commonly used in Malaysia, embracing ethnic Malays in addition to other indigenous ethnic groups (Amran & Devi, Citation2008).

References

- Abarbanell, J. S., & Bushee, B. J. (1997). Fundamental analysis, future earnings, and stock prices. Journal of Accounting Research, 35(1), 1–27. https://doi.org/https://doi.org/10.2307/2491464

- Abdul Jalil, A., & Abdul Rahman, R. (2010). Institutional investors and earnings management: Malaysian evidence. Journal of Financial Reporting and Accounting, 8(2), 110–127. https://doi.org/https://doi.org/10.1108/19852511011088370

- Abdul Wahab, E. A., How, J., & Verhoeven, P. (2008). Corporate governance and institutional investors: Evidence from Malaysia. Asian Academy of Management Journal of Accounting and Finance, 4(2), 67–90. http://web.usm.my/journal/aamjaf/vol%204-2-2008/4-2-4.pdf

- Abdul Wahab, E. A., How, J. C. Y., Park, J., & Verhoeven, P. (2018). Political patronage and analysts’ forecast precision. Journal of Contemporary Accounting & Economics, 14(3), 307–320. https://doi.org/https://doi.org/10.1016/j.jcae.2018.07.003

- Abdul Wahab, E. A., How, J. C. Y., & Verhoeven, P. (2007). The impact of the Malaysian code on corporate governance: Compliance, institutional investors and stock performance. Journal of Contemporary Accounting & Economics, 3(2), 106–129. https://doi.org/https://doi.org/10.1016/S1815-5669(10)70025-4

- Abdul Wahab, E. A., Mat Zain, M., James, K., & Haron, H. (2009). Institutional investors, political connection and audit quality in Malaysia. Accounting Research Journal, 22(2), 167–195. https://doi.org/https://doi.org/10.1108/10309610910987501

- Abdul Wahab, E. A., Pitchay, A. A., & Ali, R. (2015). Culture, corporate governance and analysts forecast in Malaysia. Asian Review of Accounting, 23(3), 232–255. https://doi.org/https://doi.org/10.1108/ARA-03-2014-0033

- Aggarwal, R., Erel, I., Ferreira, M., & Matos, P. (2011). Does governance travel around the world? Evidence from institutional investors. Journal of Financial Economics, 100(1), 154–181. https://doi.org/https://doi.org/10.1016/j.jfineco.2010.10.018

- Agrawal, A., & Mandelker, G. N. (1990). Large shareholders and the monitoring of managers: The case of antitakeover charter amendments. The Journal of Financial and Quantitative Analysis, 25(2), 143–161. https://doi.org/https://doi.org/10.2307/2330821

- Alazzani, A., Wan-hussin, W. N., Jones, M., & Al-hadi, A. (2021). ESG reporting and analysts ’ recommendations in GCC: The Moderation role of royal family directors. Journal of Risk and Financial Management, 14(72), 1–21. https://doi.org/https://doi.org/10.3390/jrfm14020072

- Al-Jaifi, H. A., Al-Rassas, A. H., & Al-Qadasi, A. (2019). Institutional investor preferences: Do internal auditing function and audit committee effectiveness matter in Malaysia? Management Research Review, 42(5), 641–659. https://doi.org/https://doi.org/10.1108/MRR-11-2016-0258

- Alnabsha, A., Abdou, H. A., Ntim, C. G., & Elamer, A. A. (2018). Corporate boards, ownership structures and corporate disclosures: Evidence from a developing country. Journal of Applied Accounting Research, 19(1), 20–41. https://doi.org/https://doi.org/10.1108/JAAR-01-2016-0001

- AlQadasi, A., & Abidin, S. (2018). The effectiveness of internal corporate governance and audit quality: The role of ownership concentration – Malaysian evidence. Corporate Governance: The International Journal of Business in Society, 18(2), 233–253. https://doi.org/https://doi.org/10.1108/CG-02-2017-0043

- AL-Qadasi, A. A., Abidin, S., & Al-Jaifi, H. A. (2019). The puzzle of internal audit function budget toward specialist auditor choice and audit fees: Does family ownership matter? Malaysian evidence. Managerial Auditing Journal, 34(2), 208–243. https://doi.org/https://doi.org/10.1108/MAJ-09-2017-1655

- Alvarez, R., Jara, M., & Pombo, C. (2018). Do institutional blockholders influence corporate investment? Evidence from emerging markets. Journal of Corporate Finance, 53( September), 38–64. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2018.09.003

- Amran, A., & Devi, S. S. (2008). The impact of government and foreign affiliate influence on corporate social reporting: The case of Malaysia. Managerial Auditing Journal, 23(4), 386–404. https://doi.org/https://doi.org/10.1108/02686900810864327

- Annuar, H. A. (2015). Changes in ownership forms and role of institutional investors in governing public companies in Malaysia: A research note. Journal of Accounting & Organizational Change, 11(4), 455–475. https://doi.org/https://doi.org/10.1108/JAOC-08-2012-0068

- Arand, D., & Kerl, A. G. (2015). Sell-side analyst research and reported conflicts of interest. European Financial Management, 21(1), 20–51. https://doi.org/https://doi.org/10.1111/j.1468-036X.2012.00661.x

- Asian Development Bank. (2014). Asean corporate governance scorecard country reports and assessments. Asian Development Bank. Retrieved from http://www.adb.org/sites/default/files/publication/42600/asean-corporate-governance-scorecard.pdf

- Autore, D. M., Kovacs, T., & Sharma, V. (2009). Do analyst recommendations reflect shareholder rights? Journal of Banking and Finance, 33(2), 193–202. https://doi.org/https://doi.org/10.1016/j.jbankfin.2008.07.008

- Ball, R., Robin, A., & Wu, J. S. (2003). Incentives versus standards: Properties of accounting income in four East Asian countries. Journal of Accounting and Economics, 36(1–3), 235–270. https://doi.org/https://doi.org/10.1016/j.jacceco.2003.10.003

- Barber, B. M., Lehavy, R., McNichols, M., & Trueman, B. (2006). Buys, holds, and sells: The distribution of investment banks’ stock ratings and the implications for the profitability of analysts’ recommendations. Journal of Accounting and Economics, 41(1–2), 87–117. https://doi.org/https://doi.org/10.1016/j.jacceco.2005.10.001

- Bataineh, H. (2021). The impact of ownership structure on dividend policy of listed firms in Jordan. Cogent Business & Management, 8(1), 1863175. https://doi.org/https://doi.org/10.1080/23311975.2020.1863175

- Bednar, M. K., Geoffrey Love, E., & Kraatz, M. (2015). Paying the price? The impact of controversial governance practices on managerial reputation. Academy of Management Journal, 58(6), 1740–1760. https://doi.org/https://doi.org/10.5465/amj.2012.1091

- Bena, J., Ferreira, M. A., Matos, P., & Pires, P. (2017). Are foreign investors locusts? The long-term effects of foreign institutional ownership. Journal of Financial Economics, 126(1), 122–146. https://doi.org/https://doi.org/10.1016/j.jfineco.2017.07.005

- Benjamin, S. J., Mat Zain, M., & Abdul Wahab, E. A. (2016). Political connections, institutional investors and dividend payouts in Malaysia. Pacific Accounting Review, 28(2), 153–179. https://doi.org/https://doi.org/10.1108/PAR-06-2015-0023

- Bird, A., & Karolyi, S. A. (2016). Do institutional investors demand public disclosure? Review of Financial Studies, 29(12), 3245–3277. https://doi.org/https://doi.org/10.1093/rfs/hhw062

- Bliss, M. A., & Gul, F. A. (2012). Political connection and cost of debt: Some Malaysian evidence. Journal of Banking and Finance, 36(5), 1520–1527. https://doi.org/https://doi.org/10.1016/j.jbankfin.2011.12.011

- Borochin, P., & Yang, J. (2017). The effects of institutional investor objectives on firm valuation and governance. Journal of Financial Economics, 126(1), 171–199. https://doi.org/https://doi.org/10.1016/j.jfineco.2017.06.013

- Bradshaw, M. T. (2004). How do analysts use their earnings forecasts in generating stock recommendations? The Accounting Review, 79(1), 25–50. https://doi.org/https://doi.org/10.2308/accr.2004.79.1.25

- Bradshaw, M. T. (2011). Analysts’ forecasts: What do we know after decades of work? Working Paper. Available at SSRN 1880339.

- Brauer, M., & Wiersema, M. (2018). Analyzing analyst research: A review of past coverage and recommendations for future research. Journal of Management, 44(1), 218–248. https://doi.org/https://doi.org/10.1177/0149206317734900

- Brickley, J. A., Lease, R. C., & Smith, C. W. (1988). Ownership structure and voting on antitakeover amendments. Journal of Financial Economics, 20, 267–291. https://doi.org/https://doi.org/10.1016/0304-405X(88)90047-5

- Bushee, B. J. (1998). The influence of institutional investors on myopic R & D investment behavior. The Accounting Review, 73(3), 305–333. https://www.jstor.org/stable/248542

- Chang, X., Chen, Y., & Dasgupta, S. (2012). Institutional investor horizons, information environment, and firm financing decisions. Working paper. Available at SSRN: https://ssrn.com/abstract=2042476 or https://doi.org/http://dx.doi.org/10.2139/ssrn.2042476.

- Chen, C. J., Ding, Y., & Kim, C. (2010). High-level politically connected firms, corruption, and analyst forecast accuracy around the world. Journal of International Business Studies,41(9), 1505–1524. https://doi.org/10.1057/jibs.2010.27

- Chen, T., Dong, H., & Lin, C. (2020). Institutional shareholders and corporate social responsibility. Journal of Financial Economics, 135(2), 483–504. https://doi.org/https://doi.org/10.1016/j.jfineco.2019.06.007

- Chen, X., & Cheng, Q. (2006). Institutional holdings and analysts’ stock recommendations. Journal of Accounting, Auditing & Finance, 21(4), 399–440. https://doi.org/https://doi.org/10.1177/0148558X0602100405

- Chichernea, D. C., Petkevich, A., & Zykaj, B. B. (2015). Idiosyncratic volatility, institutional ownership, and investment horizon. European Financial Management, 21(4), 613–645. https://doi.org/https://doi.org/10.1111/j.1468-036X.2013.12033.x

- Chowdhury, S. D., & Wang, E. Z. (2009). Institutional activism types and CEO compensation: A time-series analysis of large Canadian corporations. Journal of Management, 35(1), 5–36. https://doi.org/https://doi.org/10.1177/0149206308326772

- Chung, C. Y., Liu, C., Wang, K., & Zykaj, B. B. (2015). Institutional monitoring: Evidence from the F-Score. Journal of Business Finance and Accounting, 42(7–8), 885–914. https://doi.org/https://doi.org/10.1111/jbfa.12123

- Clarke, J., Ferris, S. P., Jayaraman, N., & Lee, J. (2006). Are analyst recommendations biased? Evidence from corporate bankruptcies. Journal of Financial and Quantitative Analysis, 41(1), 169–196. https://doi.org/https://doi.org/10.1017/S0022109000002465

- Conrad, J., Cornell, B., & Landsman, W. R. (2006). How do analyst recommendations respond to major news? Journal of Financial and Quantitative Analysis, 41(1), 25–49. https://doi.org/https://doi.org/10.1017/S0022109000002416

- Da, Z., & Schaumburg, E. (2011). Relative valuation and analyst target price forecasts. Journal of Financial Markets, 14(1), 161–192. https://doi.org/https://doi.org/10.1016/j.finmar.2010.09.001

- Dasgupta, A., Fos, V., & Sautner, Z. (2020) Institutional investors and corporate governance. ECGI Working Paper Series in Finance 700/2020.

- De La Cruz, A., Medina, A., & Tang, Y. (2019). Owners of the World’s listed companies. OECD Capital Market Series. https://www.oecd.org/corporate/Owners-of-the-Worlds-Listed-Companies.pdf

- De-la-hoz, M. C., & Pombo, C. (2016). Institutional investor heterogeneity and firm valuation: Evidence from Latin America. Emerging Markets Review, 26( March 2016), 197–221. https://doi.org/https://doi.org/10.1016/j.ememar.2015.12.001.

- Edmans, A. (2009). Blockholder trading, market efficiency, and managerial myopia. The Journal of Finance, 64(6), 2481–2513. https://doi.org/https://doi.org/10.1111/j.1540-6261.2009.01508.x

- Edmans, A. (2014). Blockholders and corporate governance. Annual Review of Financial Economics, 6(1), 23–50. https://doi.org/https://doi.org/10.1146/annurev-financial-110613-034455

- Elyasiani, E., & Jia, J. (2010). Distribution of institutional ownership and corporate firm performance. Journal of Banking and Finance, 34(3), 606–620. https://doi.org/https://doi.org/10.1016/j.jbankfin.2009.08.018

- Ertimur, Y., Muslu, V., & Zhang, F. (2011). Why are recommendations optimistic? Evidence from analysts’ coverage initiations. Review of Accounting Studies, 16(4), 679–718. https://doi.org/https://doi.org/10.1007/s11142-011-9163-6

- Faccio, M. (2006). Politically connected firms. The American Economic Review, 96(1999), 369–386. https://doi.org/https://doi.org/10.1257/000282806776157704

- Fan, J. P. H., & Wong, T. J. (2005). Do external auditors perform a corporate governance role in emerging markets? Evidence from East Asia. Journal of Accounting Research, 43(1), 35–72. https://doi.org/https://doi.org/10.1111/j.1475-679x.2004.00162.x

- Firth, M., Lin, C., Liu, P., & Xuan, Y. (2013). The client is king: Do mutual fund relationships bias analyst recommendations? Journal of Accounting Research, 51(1), 165–200. https://doi.org/https://doi.org/10.1111/j.1475-679X.2012.00469.x

- Francis, J., & Soffer, L. (1997). The relative informativeness of analysts’ stock recommendations and earnings forecast revisions. Journal of Accounting Research, 35(2), 193–211. https://doi.org/https://doi.org/10.2307/2491360

- García-Sánchez, I. M., Aibar-Guzmán, B., Aibar-Guzmán, C., & Rodríguez-Ariza, L. (2020). “Sell” recommendations by analysts in response to business communication strategies concerning the sustainable development goals and the SDG compass. Journal of Cleaner Production, 255(May), 120194. https://doi.org/https://doi.org/10.1016/j.jclepro.2020.120194

- García-Sánchez, I. M., Gómez-Miranda, M. E., David, F., & Rodríguez-Ariza, L. (2019). Analyst coverage and forecast accuracy when CSR reports improve stakeholder engagement: The global reporting initiative-international finance corporation disclosure strategy. Corporate Social Responsibility and Environmental Management, 26(6), csr.1755. https://doi.org/https://doi.org/10.1002/csr.1755

- Garel, A. (2017). When ownership structure matters: A review of the effects of investor horizon on corporate policies. Journal of Economic Surveys, 31(4), 1062–1094. https://doi.org/https://doi.org/10.1111/joes.12180

- Gaspar, J. M., Massa, M., & Matos, P. (2005). Shareholder investment horizons and the market for corporate control. Journal of Financial Economics, 76(1), 135–165. https://doi.org/https://doi.org/10.1016/j.jfineco.2004.10.002

- Ghafoor, A., Zainudin, R., & Mahdzan, N. S. (2019). Factors eliciting corporate fraud in emerging markets: Case of firms subject to enforcement actions in Malaysia. Journal of Business Ethics, 160(2), 587–608. https://doi.org/https://doi.org/10.1007/s10551-018-3877-3

- Ghaleb, B. A. A., Kamardin, H., & Tabash, M. I. (2020). Family ownership concentration and real earnings management: Empirical evidence from an emerging market. Cogent Economics & Finance, 8(1), 1–17. https://doi.org/https://doi.org/10.1080/23322039.2020.1751488

- Ghaleb, B. A. A., Qaderi, S. A., Almashaqbeh, A., & Qasem, A. (2021). Corporate social responsibility, board gender diversity and real earnings management: The case of Jordan. Cogent Business and Management, 8(1), 0–19. https://doi.org/https://doi.org/10.1080/23311975.2021.1883222

- Gillan, S. L., & Starks, L. T. (2003). Corporate governance, corporate ownership, and the role of institutional investors: A global perspective. Journal of Applied Finance, 13(2), 4–22. https://doi.org/https://doi.org/10.2139/ssrn.439500

- Gomez, E. T., Padmanabhan, T., Kamaruddin, N., Bhalla, S., & Fisal, F. (2018). Minister of finance incorporated: Ownership and control of corporate Malaysia (1st ed.). Palgrave Macmillan.

- Graham, J. R., Harvey, C. R., & Rajgopal, S. (2005). The economic implications of corporate financial reporting. Journal of Accounting and Economics, 40(1–3), 3–73. https://doi.org/https://doi.org/10.1016/j.jacceco.2005.01.002

- Gu, Z., Li, Z., & Yang, Y. G. (2013). Monitors or predators: The influence of institutional investors on sell-side analysts. The Accounting Review, 88(1), 137–169. https://doi.org/https://doi.org/10.2308/accr-50263

- Gul, F. A. (2006). Auditors’ response to political connections and cronyism in Malaysia. Journal of Accounting Research, 44(5), 931–963. https://doi.org/https://doi.org/10.1111/j.1475-679X.2006.00220.x

- Hamrouni, A., Benkraiem, R., & Karmani, M. (2017). Voluntary information disclosure and sell-side analyst coverage intensity. Review of Accounting and Finance, 16(2), 260–280. https://doi.org/https://doi.org/10.1108/RAF-02-2015-0024

- Han, S., Jin, J. Y., Kang, T., & Lobo, G. (2014). Managerial ownership and financial analysts’ information environment. Journal of Business Finance and Accounting, 41(3–4), 328–362. https://doi.org/https://doi.org/10.1111/jbfa.12070

- Haniffa, R., & Hudaib, M. (2006). Corporate governance structure and performance of Malaysian listed companies. Journal of Business Finance & Accounting, 33(7–8), 1034–1062. https://doi.org/https://doi.org/10.1111/j.1468-5957.2006.00594.x

- Harit, D. S. (2016). The impact of analysts’ recommendations on the cost of debt: International evidence. European JournalofEconomics, LawandPolitics, 3(1), 60–76. https://doi.org/https://doi.org/10.15640/rcbr.v4n2a2

- Hartzell, J. C., Sun, L., & Titman, S. (2014). Institutional investors as monitors of corporate diversification decisions: Evidence from real estate investment trusts. Journal of Corporate Finance, 25(6), 61–72. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2013.10.006

- Healy, P. M., & Palepu, K. G. (2001). Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics, 31(1), 405–440. https://doi.org/https://doi.org/10.1016/S0165-4101(01)00018-0

- Heckman, J. J. (1979). Sample selection bias as a specification error. Econometrica, 47(1), 153–161. https://doi.org/https://doi.org/10.2307/1912352

- How, J., Verhoeven, P., & Abdul Wahab, E. A. (2014). Institutional investors, political connections and analyst following in Malaysia. Economic Modelling, 43(December), 158–167. https://doi.org/https://doi.org/10.1016/j.econmod.2014.07.043

- Huang, K., & Petkevich, A. (2016). Investment horizons and information. Journal of Business Finance and Accounting, 43(7–8), 1017–1056. https://doi.org/https://doi.org/10.1111/jbfa.12205

- Hutchinson, M., Seamer, M., & Chapple, L., (Ellie). (2015). Institutional investors, risk/performance and corporate governance. The International Journal of Accounting, 50(1), 31–52. https://doi.org/https://doi.org/10.1016/j.intacc.2014.12.004

- Imam, S., & Spence, C. (2016). Context, not predictions: A field study of financial analysts. Accounting, Auditing & Accountability Journal, 29(2), 226–247. https://doi.org/https://doi.org/10.1108/AAAJ-02-2014-1606

- Ioannou, I., & Serafeim, G. (2015). The impact of corporate social responsibility on investment recommendations: Analysts’ perceptions and shifting institutional logics. Strategic Management Journal, 36(7), 1053–1081. https://doi.org/https://doi.org/10.1002/smj.2268

- Jegadeesh, N., Kim, J., Krische, S. D., & Lee, C. M. C. (2004). Analyzing the analysts: When do recommendations add value? The Journal of Finance, 59(3), 1083–1124. https://doi.org/https://doi.org/10.1111/j.1540-6261.2004.00657.x

- Jensen, M. C. (1993). The modern industrial revolution, exit, and the failure of internal control systems. Journal of Finance, 48(3), 831–880. https://doi.org/https://doi.org/10.1111/j.1540-6261.1993.tb04022.x

- Jiambalvo, J., Rajgopal, S., & Venkatachalam, M. (2002). Institutional ownership and the extent to which stock prices reflect future earnings. Contemporary Accounting Research, 19(1), 117–145. https://doi.org/https://doi.org/10.1506/EQUA-NVJ9-E712-UKBJ

- Johl, S., Subramaniam, N., & Mat Zain, M. (2012). Audit committee and CEO ethnicity and audit fees: Some Malaysian evidence. International Journal of Accounting, 47(3), 302–332. https://doi.org/https://doi.org/10.1016/j.intacc.2012.07.002

- Katmon, N., Mohamad, Z. Z., Mat Norwani, N., & Al Farooque, O. (2019). Comprehensive board diversity and quality of corporate social responsibility disclosure: Evidence from an emerging market. Journal of Business Ethics, 157(2), 447–481. https://doi.org/https://doi.org/10.1007/s10551-017-3672-6

- Lennox, C. S., Francis, J. R., & Wang, Z. (2012). Selection models in accounting research. Accounting Review, 87(2), 589–616. https://doi.org/https://doi.org/10.2308/accr-10195

- Lim, K. P., Hooy, C. W., Chang, K. B., & Brooks, R. (2016). Foreign investors and stock price efficiency: Thresholds, underlying channels and investor heterogeneity. North American Journal of Economics and Finance, 36( April 2016), 1–28. https://doi.org/https://doi.org/10.1016/j.najef.2015.11.003.

- Lin, Y., Fu, X., Gu, X., & Song, H. (2018). Institutional ownership and return volatility in the casino industry. International Journal of Tourism Research, 20(2), 204–214. https://doi.org/https://doi.org/10.1002/jtr.2173

- Liu, S. (2016). Ownership structure and analysts’ forecast properties: A study of Chinese listed firms. Corporate Governance: The International Journal of Business in Society, 16(1), 54–78. https://doi.org/https://doi.org/10.1108/CG-02-2015-0018

- Liu, S. (2017). The impact of equity incentive plans on analysts’ earnings forecasts and stock recommendations for Chinese listed firms: An empirical study. Journal of International Accounting, Auditing and Taxation, 29, 1–13. https://doi.org/https://doi.org/10.1016/j.intaccaudtax.2017.03.002

- Luo, X., & Zheng, Q. (2018). How firm internationalization is recognized by outsiders: The response of financial analysts. Journal of Business Research, 90(September), 87–106. https://doi.org/https://doi.org/10.1016/j.jbusres.2018.04.030

- Mintchik, N., Wang, A., & Zhang, G. (2014). Institutional investor preferences for analyst forecast accuracy: Which institutions care? International Review of Accounting, Banking and Finance, 6(1), 1–31. http://search.ebscohost.com/login.aspx?direct=true&db=bsu&AN=113339033&site=ehost-live

- Mohammed, N. F., Ahmed, K., & Ji, X.-D. (2017). Accounting conservatism, corporate governance and political connections. Asian Review of Accounting, 25(2), 288–318. https://doi.org/https://doi.org/10.1108/ARA-04-2016-0041

- MSWG. (2014). Malaysian code for institutional investors. Minority Shareholder Watchdog Group & Securities Commission Malaysia. http://www.sc.com.my/wp-content/uploads/eng/html/cg/mcii_140627.pdf.

- Muniandy, P., Tanewski, G., & Johl, S. K. (2016). Institutional investors in Australia: Do they play a homogenous monitoring role? Pacific Basin Finance Journal, 40(Part B), 266–288. https://doi.org/https://doi.org/10.1016/j.pacfin.2016.01.001

- Newton, N. J. (2019). When analysts speak, do auditors listen? Auditing: A Journal of Practice & Theory, 38(1), 221–245. https://doi.org/https://doi.org/10.2308/ajpt-52059

- Norhashim, M., & Abdul Aziz, K. (2005). Smart partnership or cronyism? A Malaysian perspective. International Journal of Sociology and Social Policy, 25(8), 31–48. https://doi.org/https://doi.org/10.1108/01443330510629081

- Oikonomou, I., Yin, C., & Zhao, L. (2020). Investment horizon and corporate social performance: The virtuous circle of long-term institutional ownership and responsible firm conduct. European Journal of Finance, 26(1), 14–40. https://doi.org/https://doi.org/10.1080/1351847X.2019.1660197

- Organization for Economic Co-operation and Development (OECD). (2009). Corporate governance and the financial crisis: Key findings and main messages. Paris: Organization for Economic Co-operation and Development (OECD).

- Paek, S., Kim, J. Y., Mun, S. G., & Jun, C. (2020). In hotel REITs, are institutional investors beneficial for firm value? Tourism Economics, In press. 135481662090870. https://doi.org/https://doi.org/10.1177/1354816620908702

- Pan, S., & Xu, Z. R. (2020). The association of analysts’ cash flow forecasts with stock recommendation profitability. International Journal of Accounting and Information Management, 28(2), 343–361. https://doi.org/https://doi.org/10.1108/IJAIM-05-2019-0055

- Papangkorn, S., Chatjuthamard, P., Jiraporn, P., & Phiromswad, P. (2020). Do analysts’ recommendations reflect co-opted boards? Corporate Governance (Bingley), 20(6), 1091–1103. https://doi.org/https://doi.org/10.1108/CG-10-2019-0310

- Peasnell, K., Yin, Y., & Lubberink, M. (2018). Analysts’ stock recommendations, earnings growth and risk. Accounting and Finance, 58(1), 217–254. https://doi.org/https://doi.org/10.1111/acfi.12202

- Qasem, A., Aripin, N., & Wan-Hussin, W. N. (2015). An overview of capital market development fund-bursa research scheme (CBRS). Advanced Science Letters, 21(5), 1477–1480. https://doi.org/https://doi.org/10.1166/asl.2015.6075

- Qasem, A., Aripin, N., & Wan-Hussin, W. N. (2020). Financial restatements and sell-side analysts’ stock recommendations: Evidence from Malaysia. International Journal of Managerial Finance, 16(4), 501–524. https://doi.org/https://doi.org/10.1108/IJMF-05-2019-0183

- Reuveny, R., & Li, Q. (2003). Economic openness, democracy, and income inequality. Comparative Political Studies, 36(5), 575–601. https://doi.org/https://doi.org/10.1177/0010414003036005004

- Roberts, G., & Yuan, L. E. (2010). Does institutional ownership affect the cost of bank borrowing? Journal of Economics and Business, 62(6), 604–626. https://doi.org/https://doi.org/10.1016/j.jeconbus.2009.05.002

- Ryan, L. V., & Schneider, M. (2003). Institutional investor power and heterogeneity: Implications for agency and stakeholder theories. Business & Society, 42(4), 398–429. https://doi.org/https://doi.org/10.1177/0007650303260450

- Sherman, H., Beldona, S., & Joshi, M. P. (1998). Institutional investor heterogeneity: Implications for strategic decisions. Corporate Governance: An International Review, 6(3), 166–173. https://doi.org/https://doi.org/10.1111/1467-8683.00101

- Shin, J. Y., & Seo, J. (2011). Less pay and more sensitivity? Institutional investor heterogeneity and CEO pay. Journal of Management, 37(6), 1719–1746. https://doi.org/https://doi.org/10.1177/0149206310372412

- Shleifer, A., & Vishny, R. W. (1986). Large shareholders and corporate control. Journal of Political Economy, 94(3), 461–488. https://doi.org/https://doi.org/10.1086/261385

- Stickel, S. E. (2007). Analyst incentives and the financial characteristics of Wall Street darlings and dogs. The Journal of Investing, 16(3), 23–32. https://doi.org/https://doi.org/10.3905/joi.2007.694759