?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study explores the impact of accumulated pension funds on the investment level and economic growth in South Africa using Bayesian Linear Regression (BLR) model. Time series data on Gross Domestic Product (GDP), total official pension funds and gross fixed capital formation (as a proxy for total investment level) from 1990(Q1) to 2019(Q3) were employed. The study makes use of MCMC (Markov Chain Monte Carlo) algorithm to obtain regression model parameters. The empirical findings from Bayesian Linear Regression estimation suggest that the mean effects of pension funds on economic growth and investment level in South Africa are approximately zero. The empirical conclusion is further corroborated by FMOLS results, which show that accumulated pension funds have no significant impact on the overall investment level and economic growth in South African economy. The study recommends that policy makers and the pension funds regulators have to come up with workable means by which pension funds can be invested to significantly benefit the economy; at the same time, ensuring the safety of the invested funds so as not to jeopardize the interest of pension funds owners.

PUBLIC INTEREST STATEMENT

Understanding the role of pension funds in promoting and accelerating economic fundamentals is critical and germane to attainment of economic targets and improved welfare. In the light of mounting pension funds in South African economy, the current study attempts to probe the possible impacts of pension funds on investment level and consequently economic growth. The findings from the study suggest that despite continuous increase in pension funds in South African economy, the impacts on the growth of the economy are approximately zero. Government must come up with sincere and transparent national policy that would allow the utilization of the huge pension funds in growing the real sector, as a means of diversifying the economy.

1. Introduction

Pension funds have increased rapidly over the past decades, perhaps because of population increase and the ever-expanding labour market. Thus, there has been a remarkable development in the pension industry. Quite a lot of countries have supported the investment of pension funds through several means such as tax exemptions because it is believed that this would enhance the capital mobilization function of the financial markets, increase the overall investment level in economy and consequently, economic growth. Pension fund assets are believed to be long-term in nature, hence higher pension funds should produce enduring economic and financial stimuli. Pension fund administrators invest pension funds in several financial instruments such as fixed deposits, commercial papers, corporate bonds, government infrastructural bonds, treasury bills among others. Such investments should make the accrued funds available to real sector investors, resulting in an increased overall investment level of the economy. However, there has been great concern, most especially among policy makers on the African continent that the growing nature of pension funds in the continent has not translated into an improved quality of life for the contributors of the funds and the populace in general. Fashola (Citation2016) argued that there is apparent deficit of infrastructure across Africa, in spite of the huge pool of pension funds available in most African countries. He is of the position that investment of pension funds remains one of the principal opportunities towards the diversification of the economy. On the other hand, in most of the countries, especially African countries, Pension Fund Administrators (PFAs) that are responsible for channeling the funds into economic-enhancing investments have argued that real sector investors are finding it difficult to access accumulated pension funds due to inability to meet criteria in the investment guidelines.

Empirical studies on pension funds have largely focused on stock market development, perhaps because it is traditionally believed that pension fund activities only influenced stock market. For instance, Alda & Marco (Citation2017) examined the nexus between stock market development and pension funds in 8 European countries both in short-term and long-term. Their empirical findings suggest that pension funds enhance stock market development. This position corroborated earlier empirical efforts (Alda, Citation2017; Davis, Citation1995; Davis & Steil, Citation2001; Meng & Pfau, Citation2010; Merton & Bodie, Citation1995). A more recent study on the impact of pension funds on stock market development was carried out by Babalos and Stavroyiannis (Citation2020). They explored the dynamic interaction between stock market development and pension fund investments in equities in 29 OECD countries. They submitted that pension fund investments in equities enhance stock market development. They also argued that there is significant bidirectional causality between stock market development and pension fund investments in equities. Another recent study by Ertuğrul and Gebeşoğlu (Citation2020) investigated the impact of pension funds on national savings in Turkey. The study concluded that pension funds enhanced national savings in Turkey.

This present study differs from previous studies, as extant studies on pension funds have largely focused on the capital market sector, by examining the impact of pension funds on the overall economy. The study makes use of Bayesian linear regression model to explore the impacts of pension funds on the overall investment level in the economy and the growth of the economy. The rest of the study is organized as follows: section 2 probes the existing literature while section 3 presents the empirical method; section 4 presents empirical findings while section 5 concludes the study.

2. Empirical review

Empirical studies on pension funds have not received significant attempt as existing empirical findings are still largely inconclusive and debatable. The role of pension funds on the growth of stock market developments was examined by Holzmann (Citation1997) and Catalan et al. (Citation2000). They argued that pension funding significantly enhances stock market growth and development. This position was corroborated by subsequent studies such as Impavido et al. (Citation2003), Hu (Citation2006), Davis and Hu (Citation2008), Hu (Citation2006) argued that pension asset growth has positive impact on the performances of equity prices in OECD and emerging economies.

Similarly, Impavido et al. (Citation2003) observed that the savings’ institutionalization deepens the length of stock and bond markets and also improve the liquidity of stock market. Meng and Pfau (Citation2010) investigated the impacts of pension assets on the stock market development in 32 countries. Their empirical findings show that pension assets exert positive effect on the size of the market and liquidity in the observed 32 stock markets. This is consistent with findings by Ertuğrul and Gebeşoğlu (Citation2020). They investigated the impact of pension funds on national savings in Turkish economy. The study concluded that pension funds enhanced and promoted national savings in Turkey.

In another study, Hu (Citation2012) queried the impacts of pension funds on the stock market development in Asian economies, Hu’s findings showed that pension funds have positive impact on market capitalization and value stocks traded. Similarly, the impact of pension funds on stock market development was recently investigated by Babalos and Stavroyiannis (Citation2020). They made use of the dynamic interaction between stock market development and pension fund investments in equities in 29 OECD countries. They concluded that pension fund investments in equities enhanced and strengthened the stock market development in selected economies. Significant bidirectional causality between stock market development and pension fund investments in equities was also documented.

The relationship between pension funds and other market aspects such as turnover ratio and dividend yield among other, has been hardly examined. For instance, Walker and Lefort (Citation2002) investigated the relationship between pension fund and dividend yield in 33 emerging economies. They argued that growth of pension funds positively negatively impacts dividend yield.

In the same vein, Hu (Citation2012) queried the relationship between pension fund and turnover ratios in both developed and developing economies. He found that the growth of pension assets does not significantly improve the turnover ratios in developing economies but however improves turnover ratios in more developed economies.

On the other hand, Zandberg and Spierdijk (Citation2013) investigated the impact of market return on the growth of pension fund. He observed two-way relationship as high market return enhances the pension assets growth and vice versa. They also showed that there is no relationship between pensions funds and economic growth using a sample of OECD and non-OECD countries during the period 2001–2008. On the contrary, Bijlsma, Bonekamp, Bijlsma et al. (Citation2018) investigated the effects of the pension funds on the growth of firms using the differential impact on firms that rely on external finance. They made use of data on 69 manufacturing industry sectors in 34 OECD countries from 2001 to 2010 and concluded that increased pension savings are associated with higher growth of firms that rely more on external finance.

Meanwhile, Walker and Lefort (Citation2002) found that the growth of pension funds reduces market volatility. This was corroborated by Faugere and Shawky (Citation2003). Bohl et al. (Citation2009) observed that the presence and the growth of pension funds significantly lower Polish stock market. In the same vein, Thomas et al. (Citation2014) argued that share of pension funds invested in stocks is negatively related to stock market performance and volatility in 34 OECD countries. This empirical position is in sharp contrast with Davis (Citation2004) and Davis and Hu (Citation2004). They queried the impact of pension and life insurance assets on equity price volatility in G-7 countries. They observed a positive relationship between equity price volatility and the equity share held by pension funds and life insurance. By implication, hey meant that higher equity share held by pension funds and life insurance increases the volatility of equity prices. This position is also confirmed by Hu (Citation2006). Hu (Citation2006) established that the growth of pension funds increases and worsens market volatility in 16 OECD countries and eight emerging countries. The survey of the literature on pension funds shows that empirical studies on pension funds in general is quite limited, and have been mainly and largely carried in respect of capital market. The present study contributes to limited empirical documentations on pension funds in general, but differs from the limited existing one by providing insight on the impacts of pension funds on the overall investment level as well as growth of the economy.

3. Empirical approach

The empirical approach employed in the study is Bayesian Linear Regression model (BLR). The general multiple linear regression model can be written as:

Where is a column matrix of the dependent variable,

is a vector of independent variables

is a vector of regression model parameters

is a column vector of error terms

Bayesian linear regression obtains parameter estimation by means of prior, likelihood distribution and posterior distribution. Estimation of parameters is done through posterior distribution, which is used to multiply both prior distribution and likelihood distribution. Linear regression model assumes error terms are normally distributed, and as such, variables are assumed to be normally distributed. In Bayesian approach, probability density function of the variables can be stated as follows:

The likelihood function of the variables can be stated as follows:

Bayesian approach to regression analysis makes use of several prior distributions. Parameters estimation using Bayesian approach can be executed through iteration of the marginal posterior. Posterior distribution is obtained by multiplying both prior distribution and likelihood function.

The study makes use of MCMC (Markov Chain Monte Carlo) algorithm to obtain regression model parameters. Gibbs Sampling method of algorithms in MCMC is adopted. Quarterly data on Gross Domestic Product, total official pension funds and gross fixed capital formation (as a proxy for total investment level) from 1990(1) to 2019(3) were obtained from South African Reserve Bank (SARB). The observed data are modelled using Bayesian techniques by employing MCMC pack available in R statistical package. Robustness check was done by adopting Fully Modified Least Square (FMOLS).

4. Empirical results

All the variables were expressed in their logarithmic form and stationary after first differencing. contains summary properties of the variables. The means and the standard deviations of all the variables are close to zero. This shows that the variables exhibit low volatility as suggested by low standard deviations. Another important inference that can be made from the descriptive statistics is that the null hypothesis of the Jacque Berra statistic is accepted by all the variables, suggesting that all the variables are normally distributed. However, the Bayesian approach to parameter estimation does not necessarily require the assumption of normality to hold. The tabular presentation of the empirical efforts so far is contained in .

Table 1. Summary of literature

Table 2. Descriptive statistics of the variables

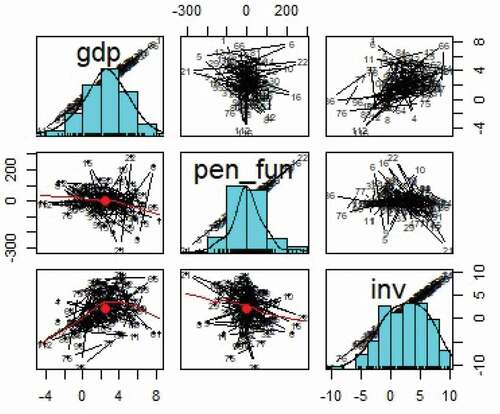

demonstrates the pairwise correlation coefficients amongst the variables being investigated. Unexpectedly, the correlation coefficient between pension funds and economic growth, as well as between investments and pension funds is quite low as it is very close to zero. The correlation chart among the variables is presented in . The correlation chart confirms near-zero correlation between pension fund and economic growth on the one hand, and pension funds and investment on the another hand.

Figure 1. Correlation chart among the variables

Table 3. Correlation matrix

The result of the Bayesian Linear Regression is presented in as well as posterior distributions plots in . In , Gross Domestic Product (GDP) is the dependent variable while overall investment level in the economy (measured by gross fixed capital formation) is the dependent variable in . The algorithm employed Gibbs Sampling by means of Markov Chain Monte Carlo (MCMC) method. Iteration used as many as 10,000 with Burn in at 500 and thin of 1. Empirical results from clearly shows that the mean effect of pension fund on economic grow is near zero. The simple implication from the finding is that pension funds have no significant impact on the growth of South African economy. Obviously, the impact of pension fund on the overall investment level in the South African economy is also insignificant as contained in . Despite the high level of pension funds in the South African economy, its impact on the overall investment level in the economy is not significant, and consequently has no impact on the growth of the economy.

Figure 2. Posterior distribution plot

Figure 3. Posterior distribution plot

Table 4. BLR results

Table 5. BLR results

The robustness of the empirical findings is done by estimating the fully modified least square version of equation (1). Having earlier confirmed that the variables are stationary after first differencing, the Johannsen cointegration test is done to establish the cointegration relations among the variables. The result is contained in . The result suggests the presence of at least one cointegrating relationship among the variables. Hence, we estimate the fully modified least square version of equation (1) to verify the impact of pension funds on investment and economic growth.

Table 6. Cointegration test results

The empirical findings from shows that pension funds have no significant impact on investment level and economic growth in South African economy. This finding confirms the Bayesian Linear Regression results.

Table 7. FMOLS results

5. Conclusion

The study investigates the impact of accumulated pension funds on the investment level and economic growth in South Africa using the MCMC (Markov Chain Monte Carlo) algorithm to obtain regression model parameters. Quarterly data on Gross Domestic Product, total official pension funds and gross fixed capital formation (as a proxy for total investment level) from 1990(1) to 2019(3) were sourced from South African Reserve Bank (SARB). The empirical findings from Bayesian Linear Regression model show that mean effects of pension funds on economic growth and investment level in South African economy are near zero. The empirical conclusion is affirmed by FMOLS results which shows that accumulated pension funds have no significant impact on the overall investment level and economic growth in South African economy. This empirical submission substantiates growing concerns among the policy makers that growing accumulated pension funds in the African continent has not impacted the quality of life of people in the continent positively and favourably.

5.1. Recommendation

From the foregoing, this study recommends that both policy makers and pension regulators have to come up with workable means by which pension funds can be invested to significantly benefit the economy and at same time ensuring the safety of the invested funds so as not to jeopardize the interest of pension fund owners. Government must come up with sincere and transparent national policy that would allow the utilization of the huge pension fund in growing the real sector, as a means of diversifying the economy. Also, therae must be a collective national attitude that would ensure investment of pension funds into real sectors in order to diversify and strengthen the economy for the attainment as well as sustainment of inclusive growth. Consequently, this study recommends that both policy makers and pension regulators have to come up with workable means by which pension funds can be invested to significantly benefit the economy and at the same time ensuring the safety of the invested funds so as not to jeopardize the interest of pension fund owners.

Additional information

Funding

Notes on contributors

Kazeem Abimbola Sanusi

Kazeem Abimbola Sanusi holds a PhD in Economics and his research interests among others include financial economics, and fiscal and monetary policies.

Professor Forget M Kapingura holds a PhD in Economics and is a professor of Economics at University of Fort Hare, South Africa.

References

- Alda García, M., & Marco Sanjuan, I. (2017). The importance of domestic equity pension funds on stock market. Spanish Journal of Finance and Accounting/Revista Española De Financiación Y Contabilidad, 46(2), 227–11. https://doi.org/https://doi.org/10.1080/02102412.2016.1265709

- Alda, M. (2017). The relationship between pension funds and the stock market: Does the aging population of Europe affect it? International Review of Financial Analysis, 49, 83–97. https://doi.org/https://doi.org/10.1016/j.irfa.2016.12.008

- Babalos, V., & Stavroyiannis, S. (2020). Pension funds and stock market development in OECD countries: Novel evidence from a panel VAR. Finance Research Letters, 34, 101247. https://doi.org/https://doi.org/10.1016/j.frl.2019.07.020

- Bijlsma, M., Bonekamp, J., van Ewijk, C., & Haaijen, F. (2018). Funded pensions and economic growth. De Economist, 166(3), 337–362. https://doi.org/https://doi.org/10.1007/s10645-018-9325-z

- Bohl, M. T., Brzeszczynski, J., & Wilfling, B. (2009). Institutional investors and stock returns volatility: Empirical evidence from a natural experiment. Journal of Financial Stability, 5(2), 170–182. https://doi.org/https://doi.org/10.1016/j.jfs.2008.02.003

- Catalan, M., Impavido, G., & Musalem, A. R. (2000). Contractual savings or stock market development-which leads? World bank eLibrary, 2421. World Bank Group.

- Davis, E. P. (1995). Pension funds-retirement income security and capital markets-An international perspective. Clarendon Press.

- Davis, E. P. (2004). Financial development, institutional investors and economic performance. In C. A. E. Goodhart (Ed.), Financial development and economic growth: Explaining the links London: (Palgrave–Macmillan).

- Davis, E. P., & Hu, Y. (2008). Does funding of pensions stimulate economic growth? Journal of Pensions Economics and Finance, 7(2), 221–249. https://doi.org/https://doi.org/10.1017/S1474747208003545

- Davis, E. P., & Hu, Y.-W. (2004). Is there a link between pension-fund assets and economic growth? A cross-country study. London. Brunel University and NIESR, mimeo.

- Davis, E. P., & Steil, B. (2001). Institutional investors. Cambridge. The MIT Press.

- Ertuğrul, H. M., & Gebeşoğlu, P. F. (2020). The effect of private pension scheme on savings: A case study for Turkey. Borsa Istanbul Review, 20(2), 172–177. https://doi.org/https://doi.org/10.1016/j.bir.2019.12.001

- Fashola, B. (2016). The Nigerian Pension Industry Strategy Implementation Roadmap Retreat Pulse.ng. https://www.legit.ng/714471-fashola-reveals-secrets-saving-nigerias-econmy.html

- Faugere, C., & Shawky, H. A. (2003). Volatility and institutional investor holdings in a declining market: A study of NASDAQ during the year 2000. Journal of Applied Finance 13 (2), 32–42.

- Holzmann, R. (1997). Pension reform, financial market and economic growth, preliminary evidence from Chile. Staff Papers (International Monetary Fund), 44(2), 149–178. https://doi.org/https://doi.org/10.2307/3867541

- Hu, Y. (2006). The impact of pension funds on financial markets. Financial Market Trends- OECD Journal, 2, 143–165.

- Hu, Y. (2012). Growth of Asian pension assets: Implications for financial and capital markets (ADBI Working Paper Series, 360). Asian Development Bank Institute.

- Impavido, G., Musalem, A. R., & Tressel, T. (2003). The impact of contractual savings institutions on securities markets (World Bank Policy Research Working Paper 2948). The World Bank.

- Meng, C., & Pfau, W. D. (2010). The role of pension funds in capital market development (National Graduate Institute for Policy Studies (GRIPS) Discussion Papers 10-17). GRIPS.

- Merton, R., & Bodie, Z. (1995). A conceptual framework for analysing the financial environment. In D. B. Crane, K. A. Froot, S. P. Mason, A. Perold, R. C. Merton, Z. Bodie, E. R. Sirri, & P. Tufano (Eds.), The global financial system: A functional perspective (pp. 3-31). HarvardBusiness School Press.

- Thomas, A., Spataro, L., & Mathew, N. (2014). Pension funds and stock market volatility: An empirical analysis of OECD countries. Journal of Financial Stability, 11, 92–103. https://doi.org/https://doi.org/10.1016/jjfs.2014.01.001

- Walker, E., & Lefort, F. (2002). Pension reform and capital markets: Are there any (hard) links? Revista ABANTE, 5(2), 77–149. https://www.academia.edu/download/34098339/Walker_Lefort.pdf

- Zandberg, E., & Spierdijk, L. (2013). Funding of pensions and economic growth: Are they really related? Journal of Pension Economics & Finance, 2(2), 151–167. https://doi.org/https://doi.org/10.1017/S1474747212000224