?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Covid-19 pandemic is affecting the health of the public, and it is also impacting business and economy. The main objective of this paper is to investigate the impact of Covid-19 pandemic on listed firms’ performance and the abnormal stock returns in Vietnam. To study the impact of Covid-19 on firms’ performance, we collected data about announced earnings on Q1/2020 and Q4/2019 of 714 enterprises and made comparison. The results revealed the enormous impacts of Covid-19 pandemic on the business performance. However, the level of influence varies among sectors. To study the impact of Covid-19 on the abnormal stock returns, the study employed the event research method with 3 events related to Covid-19 pandemic in Vietnam. A sample of 364 companies listed on Ho Chi Minh Stock Exchange (HOSE) was utilized. The findings revealed that the Covid-19 event affects the abnormal returns of stocks and the level of influence varied from each stage of Covid-19 prevention measure in Vietnam. The degrees of influence of the Covid-19 event on each stock were also different. The paper concluded that Covid-19 pandemic information can be used to predict stocks’ prices.

PUBLIC INTEREST STATEMENT

The Covid-19 pandemic is not just a global health crisis, it has changed the world economy. The pandemic is posing challenges to the empirical analysis of its effects on the economy activities. This study, therefore, aims to assess the impact of Covid-19 on the stock markets. Particularly, the study found out investors’ reactions to events that related to the pandemic. These events can be the announcement of the first Covid-19 positive cases or the announcement of social distancing measurement. Indicator used to evaluate the market reaction is the abnormal stock returns. The study explored data in Vietnam, a frontier market. Vietnam is also one of the countries that have succeeded in controlling the pandemic. We highlighted the differences in market reactions which are reflected by the changes in abnormal returns of listed firms’ stocks to different phases of Covid-19 pandemic preventive measure in Vietnam.

1. Introduction

The Covid-19 pandemic has had a huge impact on the financial systems of countries around the world, including both developed and developing economies (Baker et al., Citation2020). Starting as a medical pandemic, Covid-19 has shown lasting consequences for markets, including the stock market. From a risk perspective, this could be considered as a macroeconomic shock that could cause systemic risk—the risk that would lead to the collapse of the financial system if it cannot be controlled and prevented. The 2008 economic crisis can be considered as a typical of systemic risk (Smaga, Citation2014).

Over the past few months, a number of research has begun to assess the impact of Covid-19 pandemic on the economy in general and the stock market in particular. However, in-depth studies analyzing different aspects of the market are still limited.

The Vietnamese stock market is no exception in the Covid-19 pandemic. While the Government of Vietnam has had successful solutions to prevent Covid-19, the impacts of the epidemic from the onset have affected the market development. This paper focused on analyzing the impact of Covid-19 on the abnormal return of listed companies in Vietnam using event study methodology. Abnormal returns fluctuations are one of the issues that investors and managers should consider and refer to in order to perform a preliminary screening or preliminary assessment of market movements when an event that could trigger contagious risk occurs.

2. Literature review

2.1. Theoretical background

2.1.1. Efficient market theory

In an efficient market, the stock prices are unpredictable and therefore the stock returns will also be random and mostly follow the normal distribution. The market is divided into three levels of efficiency: (i) Weak form efficiency, (ii) Semi-strong form efficiency and (iii) Strong form efficiency. Weak form efficiency states that current stock prices reflect fully information about past prices. At semi-strong form level of efficiency, the current stock prices fully reflect by the published information as well as information about the company, such as profits, dividends and management notices. Strong form efficiency states that all information in a market is reflected in stocks’ price; therefore, transactions cannot be conducted based on insider information (Fama, Citation1970).

2.1.2. Signalling theory

Signalling theory shows that asymmetric information problem occurring between companies and investors leads to the risk of adverse selection for investors. To avoid this situation, companies can give positive signals to the market by voluntarily publishing their information (Watts & Zimmerman, Citation1986). According to this theory, the larger the enterprises are, the greater the asymmetric information problem is. Moreover, businesses with higher profitability will tend to publish more information about their growth prospects in order to provide positive signals to investors, thereby having a positive impact on their stock prices (Inchausti, Citation1997).

2.1.3. Behavioral finance theory

Behavioral financial theory which combines psychology with finance was formed and developed quite late compared to standard financial theory. In 1980, a French psychologist, Gabriel Tarde, began to study about the application of psychology to economic science. Later studies of Tversky and Kahneman (Citation1981) and especially Shiller (Citation2015) with the famous book “Irrational Exuberance” which accurately predicted the collapse of the global stock market shortly afterwards, created a great turning point for behavioral finance research. Behavioral finance can explain the phenomena related to market confidence, one of the factors causing stock price volatility or even contagious risk, which then leads to financial crises.

2.2. Literature review

Excess returns are the spread between a stock’s return and the benchmarking rate of return. The benchmarking rate of return can be the stock’s expected return calculated using Capital Asset Pricing Model (CAPM), the market portfolio rate of return or the return of a comparable enterprise. It can be said that returns, especially the abnormal returns, are the main factor that attracts the most attention of investors in the market because it has a direct effect on the magnitude and volatility of investors’ income. Therefore, there have been many studies on stock’s returns, the factors affecting the rate of return of a stock as well as the relationship between returns and some financial indicators of the company.

Among the factors that affect stock return, risk is considered one of the basic factors. All stocks in the market are affected by the market fluctuations, which is the core concept of a one-factor model, notably the Capital Asset Pricing Model (CAPM). CAPM was developed simultaneously and independently by Sharpe, (Citation1964) and Lintner (Citation1965). According to CAPM, a stock’s rate of return is affected by the systematic risk (beta) of the stock and market factors (market risk premium). Fama et al. (Citation1993) developed the CAPM model by adding variables representing the firm’s size and firm’s book value on market price of the firm. Meanwhile, bankruptcy risk is also proved to have a positive impact on the stock rate of return in the period before and after the time when the financial statements of enterprises are published, according to Griffin & Lemmon (Citation2002). The Covid-19 pandemic has been considered as an event that triggered the contagious risk. Market reactions to Covid-19 have shed light on the importance of international trade and financial policies to firms’ value. As the virus spreads to Europe and the US, the markets have shifted violently, even when Fed conducted interventions in the bond market. Overall, the results show that the health crisis has turned into an economic crisis which is amplified through financial channels.

Researches have begun to assess Covid-19’s influence on the financial sector. Globally, the Covid-19 shock is severe even compared to the great financial crisis of 2008. A thorough search of the relevant literature yielded few articles about the impact of Covid-19 on financial markets. Sansa (Citation2020) investigated the impact of Covid-19 on financial markets from 1 March 2020 to 25 March 2020 in China and in the United States. The study used a simple regression model to assess the impact of Covid-19 on financial markets. Statistics collected in Shanghai Stock Exchange were used as sample for China’s financial markets and data collected in the New York Dow Jones were used as sample for the United States’s financial markets. In order to investigate the impact of Covid-19 on financial markets, the study assumed that Covid-19 cases which are confirmed are the independent variable, while the Shanghai Stock Exchange and New York Dow Jones are dependent variables. The research results show that there is a positive relationship between Covid-19 confirmed cases and all studied financial markets from 1 March 2020 to 25 March 2020. It means that Covid-19 has a significant impact on China and the United States’ financial markets from 1 March 2020 to 25 March 2020.

In addition, Baker et al. (Citation2020) stated that there has not been any previous infectious disease, including the Spanish flu, that had affected the stock market as strongly as the Covid-19 pandemic. Policy responses to the Covid-19 pandemic provide the most convincing explanation for the impact of a pandemic on the market.

Onali (Citation2020) considered the impact of Covid-19 cases and Covid-19 related deaths on the US stock market. The study accounted for all changes in trading volume and volatility expectations, as well as day-of-the-week effects. Using GARCH(1,1) model and collecting data from 8 April 2019 to 9 April 2020, the research results suggest that changes in the number of cases and deaths in US and six other countries do not have impact on the US stock market returns, apart from the number of reported cases in China. However, there is evidence of a positive impact of Covid-19 pandemic on the conditional heteroscedasticity of the Dow Jones and S&P500 returns. The VAR models show that there was a negative relationship between the number of deaths reported in Italy and France and stock market returns and a positive relationship between the number of deaths reported in Italy and France and VIX’s returns. Finally, Markov-Switching models show that by the end of February 2020, VIX’s negative impact on stock market returns tripled.

In addition, Pavlyshenko (Citation2020) employed various regression methods to determine the Covid-19 spread and its impact on the stock market. Logistic curve regression was used with Bayes regression for predictive analysis about coronavirus spread. The results showed that different crises with different causes have different effects on the same stock.

Yan et al. (Citation2020) analyzed the potential impacts that Covid-19 might have on the stock market and suggested some possible ways that an individual can gain profits from the market which is affected by the global virus outbreak. The authors examined past outbreaks and came to the conclusion that markets often react negatively to such incidents in the short term but in the long run, the market will eventually correct itself. Based on the findings, the authors proposed to buy and sell stocks of industries that will be affected immediately by the virus in a short time. Specifically, the authors viewed the tourism industry, the technology industry, the entertainment industry and gold as potential areas where huge profits can be made.

It can be said that the research on the impacts of Covid-19 on the financial market and the stock market focused much on identifying the spread and the impact of the disease on the financial aspect. To the best of our knowledge, there has not been any study focusing on analyzing the fluctuations in the abnormal returns of stocks—factors that reflect directly investors’ behavior towards changes in the economy. In the context of Vietnam, few studies attempt to examine the impact of Covid-19 pandemic on the economy as well as on the stock market. Moreover, Vietnam stock market is a frontier market and one of the countries that has succeeded in controlling the pandemic due to effective government pandemic responses. On that basis, this research aims to explore data about returns in order to find the relationship between the Covid-19 pandemic and abnormal returns on Vietnam’s stock market. In addition, the performances of firms were also analyzed.

3. Method

The event study method is a method used to examine the impact of an event on a specific dependent variable. In common, the specific dependent variable is the stock price of a company. In other words, the event study method determines the association between the abnormal return of the company’s stock price and an event during a specified window of time (event window). This study employed the traditional event study methodology which was used in the workings of Pettit (Citation1972), Al-Malkawi et al. (Citation2010).

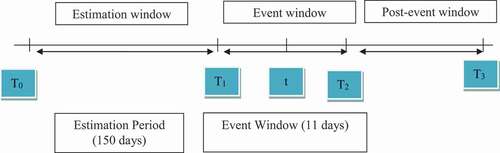

3.1. Event study timeline

The timeline for a typical event study consists of two concepts: Event Window and Estimation Period. In particular, the event window is used to assess the level of market reaction before and after the event x days; and t = 0 is the event date. Event date can be the day that the first Covid-19 cases were detected in Vietnam. Event date can also be the first day of social distancing in Vietnam. Estimation period is used to estimate the coefficient of the Market Model in calculating the abnormal rate of return of a stock.

The date of review of the effect of Covid-19 was determined by the authors as the first day of the phase (There are three phases) to implement the prevention of the Covid-19 pandemic in Vietnam, selected as the event date (“t” = 0). The length of the event window is 11 days, starting 5 days before the event date (“t” = −5) and lasting for up to 5 days after the event date (“t” = + 5). Based on the event window, this study was divided into three event windows: [−5; +5], [−5; −1], [0; +5]. The event window [−5; +5] was used to evaluate the accumulative effects on the stock prices during the period of 5-day before and 5—day after the event date ().

Figure 1. Event study timeline

The estimation period is 150 days before the event date (calculated from the “t” = −161 to “t” = −11). The estimation period should be long enough to be able to estimate the stock’s expected return more accurately, limiting the effects of short-term fluctuations. In addition, such estimation period may limit the impact of certain corporate disclosure activities on stock prices during the observation period.

3.2. Research method

Step 1:

- Calculating abnormal returns for each stock in each day of event study timeline:

where ARi,t is the abnormal return of stock i on date t; Ri,t is the real return of stock i on date t; E(Ri,t) is the expected return of stock i on date t.

- The real return of stock is calculated based on the spread between the stock price on date t and date t—1:

where Pi,t, Pi,t-1 are the prices of stock i on date t and t-1, respectively

- The expected return of a stock can be calculated using a variety of methods. Two of the common methods are Market Model and asset valuation model (CAPM—Capital Asset Pricing Model). This study chooses the first method—Market Model. According to this model, the only factor affecting the return of stock i on date t is market return on day t. This model is quite similar to the CAPM with the exception of a selected fixed coefficient rather than a risk-free rate. Given the available information in Vietnam, it is also difficult to fully determine factors of CAPM model: (i) firms’ beta coefficients are not available, (ii) information on risk-free rates often do not have complete statistics for time estimates. Therefore, the expected return of a stock will be calculated based on the market model:

where E(Ri,t) is the expected return of stock i on date t; Rm,t is daily return of market portfolio on date t (calculated by EquationEquation 1(1)

(1) );

are market model coefficients;

is error term.

Specifically, the coefficients can be estimated through a linear regression model between the company’s stock price and the market price index (VN-Index) during the estimation window, from

to

. The study conducted regression for each published event related to Covid-19 −19,

Step 2: Calculating average abnormal return and accumulated abnormal return using the following 2 formulas:

: The average abnormal return of N stocks, calculated for each day in the event window (

to

)

: the cumulative average abnormal returns calculated for 1 share in the event window

Step 3: Calculating t—stat for AAR and CAAR

Using statistical theory (t—test) to test the significance of abnormal return values. If the test’s results show that the abnormal return value is different from 0 and significant, the first announcement made at each stage of the Covid-19 pandemic prevention measure has an impact on stock prices. Consequently, it is also possible to evaluate the level of efficiency of the stock market by analyzing the stock price adjustment speed regarding to the availability of information about Covid-19 pandemic’s influence at each stage.

Assuming that the average returns AARi,t is independent and follow the normal distribution, the value (AARi,t) denotes the t-student distribution with (N—1) degrees of freedom under the Ho hypothesis. Although the value of abnormal daily returns is generally not normally distributed. However, according to the Central Limit Theorem theory, the value of the firms’ abnormal returns will gradually approach the normal distribution when the number of shares increase (Gurgul et al., Citation2003). The formula for calculating t—stat for AARt and CAARt in the event window is as follows:

t- statistic (4)

where is the Standard Error of AARt in the estimation window

t- statistic (5)

3.3. Data

The authors have collected data of enterprises listed in Vietnam’s stock market. To achieve the research objectives, the collected data include:

+ Data about profits in Quarter 1, 2020, Quarter 4, 2019 and Quarter 1, 2019 of 714 enterprises listed in Vietnam’s stock market.

+ Stock prices of 346 enterprises listed in HOSE and VN-Index during the period from 1 January 2019 to 30 April 2020.

+ Data for the happening of Covid-19 cases in Vietnam and Vietnam’s Covid-19 pandemic preventive measures. In this study, we identified three event dates: 3 February 2020, 9 March 2020, and 1 April 2020 which are corresponding to the first day of each stage of Covid-19 preventive measures in Vietnam.

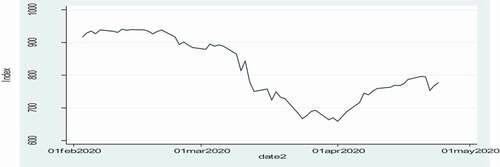

The evolution of the VN-index during the period from 1 January 2019 to 30 April 2020 and from 1 January 2020 to 30 April 2020 is presented in , .

Figure 2. VN-Index performance from 01/01/2019 to 30/04/2020

Figure 3. VN-Index performance from 03/02/2019 to 30/04/2020

VN-index performance from 01/01/2019 to 30/04/2020 and from 01/01/2020 to 30/04/2020 is presented in , .

4. Results

4.1. Listed firm performance

To study the impact of Covid-19 on firms’ performance, we collected data on Q1 2020 announced earnings of 714 enterprises as of 9 May 2020 (accounting for 93% of total listed firms) and data on Q4 2019 earnings.

The results from show that the average profit in Q1 2020 was 62.24 billion VND, while the average profit in Q4 2019 was 96.05 billion VND and Q1 2019 was 72.42 billion VND. The average percentage change in profits of total sectors is −35% and −14% compared to the previous quarter and to the same period in 2019, respectively. It can be seen that the impact of Covid-19 has an enormous influence on the listed enterprises’ performance. However, the level of influence varied among industries. Service sector enterprises were greatly affected with rate of profit decreased by 276% and 171.1% compared to the previous quarter and the same period of the previous year, respectively. In contrast, enterprises in material production sector maintained the growth rates of 58% and 26% compared to the previous quarter and the same period of the previous year, respectively. Technology sector also maintained the growth rates of 7% and 5.6%, respectively.

Table 1. Comparison of industries’ average profits

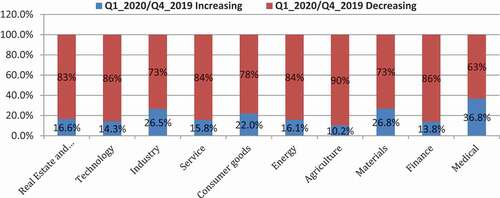

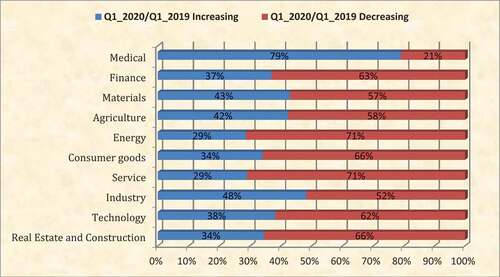

and show the increase/decrease in enterprises’ profits and income between Q1 2020 and Q4 2019. The results imply that the majority of enterprises witnessed a decline in the rate of profit, decreasing by 63% regarding to medical enterprises and 90% regarding to agricultural firms.

Figure 4. Proportion of enterprises increasing/decreasing profits in Q1 2020 compared to Q4 2019

Figure 5. Proportion of enterprises increasing/decreasing income in Q1 2020 compared to Q4 2019

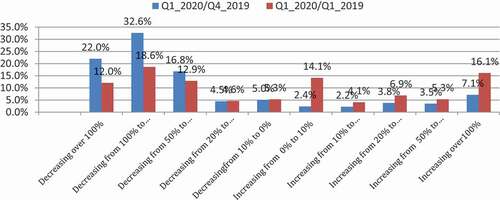

To assess the level of profit reduction (), we compared the profits of Q1 2020 with the previous quarter () and the same period of the previous year (). Based on the changes in profits, we divided studied companies into three groups. The first group includes the companies with highest level of profit reduction (profits decreased of 50%—100%). The second group includes firms whose profits decreased of over 100% and the last group of firms witnessed a decrease of 20–50%. These results show the serious impact of Covid-19 on the firms’ profits.

Figure 6. The level of increase/decrease in profits

Figure 7. The level of increase/decrease in profits in Q1 2020 compared to Q4 2019

Figure 8. The level of increase/decrease in profits in Q1 2020 compared to Q1 2019

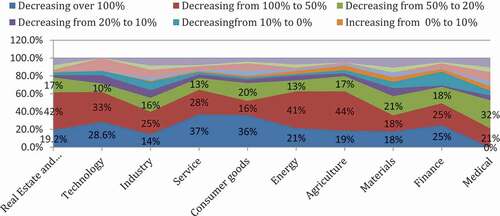

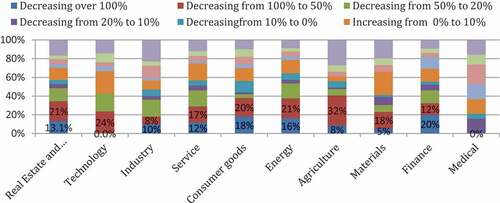

We continue to examine the impact of Covid-19 on each industry (, ). Sectors which had a high rate of reduction (from over 100%) were service sectors, consumer goods sector with 37% and 36%, respectively. Firms in medical sector witnessed the lowest influence.

4.2. Event study results

The results show that the Covid-19 event affects the abnormal returns of stocks and the level of influence varied from each stage of Covid-19 preventive measure in Vietnam. The degrees of influence of the Covid-19 event on each stock were also different, thereby creating spread on abnormal return. For a more complete assessment of the effect of the Covid-19 event on the abnormal return of a stock, we analyzed it according to the event windows. As shown in the table, the 11-day period was divided into three event windows: [−5; −5], [−5; −1], [+1; +5]. The calculation results of cumulative average abnormal return CAAR were presented in , , for firms in Service, Technology and Medical sector.

Table 2. Abnormal returns of service-sector stocks over 11 days around the date of event announcement

Table 3. Abnormal returns of technology-sector stocks over 11 days around the date of event announcement

Table 4. Abnormal returns of medical-sector stocks over 11 days around the date of event announcement

Regarding to the Covid-19 event’s phase 1, there are a number of medical-sector firms’ stocks showing the influence and statistical significance (see ). The cumulative average abnormal return of total service-sector research sample during the event window from −5 to +5 decreased by 2.87%, including 2.21% over the period from −5 to −1 day and 0.66% from 0 to +5 days. However, these above results are not statistically significant. In the period before and after the announcement of Covid-19 event’s phase 2, CAAR decreased by 6.01% and have statistical significance at the 0.05 level. During the period after the announcement of the event from 0 to 5 days, CAAR decreased by 7.49% and had statistical significance at the 1% level. Therefore, in phase 2, Covid-19 had significant impact on the abnormal returns and stock prices of service-sector enterprises. Regarding to the effect of the Covid-19 event in phase 3, the impact of event after the start of social distancing made sectors’ average stock prices increased by 4.16% and had statistical significance at the 0.05 level.

5. Discussion

Regarding to the effect of Covid-19 on stock prices of enterprises in Technology and Medical sector, the results show that in phase 1, the influence of Covid-19 event, after the time of event announcement made CAAR of Technology sector decreased by 0.21% and the medical sector decreased by 4.1% but it was not statistically significant. However, before the event of phase 1, from 5 to −1 day CAAR of Technology sector enterprises decreased by 2.2%, while the medical sector increased by 5.87% with 1% significance level. In phase 2, the Covid-19 event greatly affected the shares of Technology and Medical firms. During the period from 0 to +5 days, CAAR of Technology sector decreased by 10.16% and CAAR of Health sector decreased by 11.28%, all had statistical significance. In phase 3, the effect of Covid-19 event had a strong impact on stock prices. CAAR of the two Technology and Medical sectors increased by 8.84% and 12.21%, respectively, and these results had statistical significance during the period from 0 to +5 days.

We also examined the effect of the Covid-19 event on the abnormal returns of other sectors, according to the tier 1 sector code which includes 10 sectors. The results from shows that, in phase 1, the Covid-19 event had an impact on the business but it was not significant. In phase 1, the CAAR of the two sectors of Agriculture and Consumer Goods decreased 4.58% and 2.05%, respectively, and these results are statistically significant. The other sectors witnessed a decrease in the values of CAAR, however, these results were not statistically significant. In phase 2, the Covid-19 event had the largest and most negative impact on the abnormal returns of stocks. Among the listed enterprises on HOSE, medical firms experienced the lowest decline in CAAR while technology firms suffered the deepest drop, decreasing by 7.43% and 17.27%, respectively. In contrast, in phase 3 of Covid-19 Preventive measure, cumulative average abnormal returns of all sectors’ enterprises increased and had statistical significance. Technology firms’ stocks recorded the highest increase in CAAR while CAAR of industrial sectors had lowest growth, increasing by 15.63% and 5.06%, respectively. The market had positive reaction to a “bad” event because the investors were psychologically prepared, and they believed that Covid-19 preventive measures could solve the issue. These results were in accordance with behavioral finance theory.

Table 5. Abnormal returns of sectors’ average stocks over 11 days around the date of event announcement

Overall, the results revealed that 03/02/2020 event (the first day of Phase 1 of Covid-19 preventive measures in Vietnam) has no impact on the stock market. This result can be explained as follows: At that time, investors in Vietnam had not realized the danger of Covid-19 pandemic. As of 3 February 2020, there were only 8 positive cases of Covid-19 in Vietnam. All of these cases were entries into Vietnam from abroad. There was no infection in the country. Consequently, the market did not react to the information about Covid-19 preventive measures given by the government. However, the results uncovered a difference in the cumulative average abnormal returns of stocks before and after the announcement of Phase 2 (09/03/2020 event) and Phase 3 (01/04/2020 event) of Covid-19 preventive measures in Vietnam. It confirmed that these two events gave a signal, and there was a reaction to the abnormal returns of stocks for the 5 days before and after the announcement dates. Technology and Medical Firms’ stocks were among the most affected stocks. It is because the investors believed that technology and medical sector could receive huge profits during Covid-19 pandemic period. These findings are in accordance with signaling theory and the efficient market hypothesis.

Regarding the previous research results, this study’s results corroborated with the research results carried out by Sansa (Citation2020), Baker et al. (Citation2020), and Onali (Citation2020), Pavlyshenko (Citation2020) and Yan et al. (Citation2020) which verified that Covid-19 has a significant impact on the financial markets.

6. Conclusion

The study has shown a severe impact of Covid-19 on the firms listed on the Vietnamese stock market. By comparing the profits of 714 firms in 3 periods: Q1/2019, Q4/2019 and Q1/2020, the research results showed a significant decrease in average profitability of these enterprises. Specifically, compared to Q4/2019 and Q1/2019, the average profits of businesses had decreased by 35% and 14.1%, respectively. The results of the research also showed that firm performance varies between different industries. The service sector was heavily influenced by Covid-19, while the medical sector was less affected by the pandemic. The study also examined the reaction of stock market to Covid-19, which can be reflected in the changes in abnormal stock returns. Therefore, the study used the event research method to examine the effect of Covid-19 on abnormal returns over three stages of Covid-19 Preventive Measure. The results showed that the market reacted to the Covid-19 event and the impact of the event on the abnormal returns of stock in each phase of Covid-19 Preventive measure is different. In phase 1, the effect of Covid on abnormal returns of stocks is not great, but in phase 2, Covid-19 had negatively affected the abnormal returns of businesses. In phase 3, the implementation of social distancing and the psychological preparation helped the Covid-19 event to have positive effect on abnormal returns of firms’ shares. However, these returns were still lower than these before the Covid-19 event.

According to the research results, the authors proposed some recommendations for firms, investors and government regulatory agencies, as follows: (i) For investors, Covid-19 pandemic information can be used to predict stocks’ prices. In particular, investors can receive abnormal returns based on the effectiveness of Covid-19 pandemic preventive measures in each country. Therefore, investors should actively capture the information to make trading decisions at the right time during the event timeline. (ii) For firms, the Covid-19 pandemic has seriously affected production and business activities. In order to recover soon, enterprises should consider the following aspects: Prioritizing the “human” factor. Enterprises should pay attention to the physical and mental health of workers and develop appropriate plans for resuming work. Timelines and goals in short and medium term should be rearranged. Executive leaders should accept changing their focus from strategy to tactics; (iii) For the Government and government regulatory agencies, it is important to effectively and quickly implement measures to support enterprises which are greatly affected by the Covid-19 pandemic, helping enterprises to cope with difficulties and restore production and operations.

Vietnam’s stock market is a frontier market Vietnam and the Covid-19 pandemic situation in Vietnam has been different from other countries. However, this study did not consider any country-specific factor. It is the limitation of the study. Future research can be done by adding country-specific factor or examining other market indicators such as Trading Volume Activity, Trading Frequency Activity to evaluate the market reaction to Covid-19 related events.

Acknowledgements

This research was supported by National Economics University, Hanoi, Vietnam

Additional information

Funding

Notes on contributors

Hung Dang Ngoc

Dr. Dang Ngoc Hung is working and teaching at the Faculty of Accounting & Auditing, Hanoi University of Industry, Vietnam. His research interest includes accounting and finance. He has published in the high ranked international journals.

Dr. Vu Thi Thuy Van is a lecturer at the School of Banking and Finance, National Economics University, Vietnam. Her works focus on corporate finance and stock market.

Le Van Chi is currently a lecture and Post-doctoral Researcher at the School of Banking and Finance, National Economics University, Vietnam. Her research interest includes monetary policy, finance and banking.

References

- Al-Malkawi, H.-A. N., Rafferty, M., & Pillai, R. (2010). Dividend policy: A review of theories and empirical evidence. International Bulletin of Business Administration, 9 (1), 171–18. https://d1wqtxts1xzle7.cloudfront.net/32143154/DividendMalkawi_Rafferty___Pillai__IBBA_9_2010.pdf?1382525099=&response-content-disposition=inline%3B+filename%3DDividend_Policy_A_Review_of_Theories_and.pdf&Expires=1598636616&Signature=gjncl-S0YJzOPZMubJaG6Sl7HrVVM8xQ85izV6ESMSZjLzwizSUtJSNGp3ULy-EQ5em5-vLQ1tG8vTCdwzkmNN7ZFqNfNrvUFDNTYbAUKfrTGpUzjjzVoJdaKOS4zalTi-gMJT-sKXqL~HvPWKM0ltLNsFepf9iuOEd4tlmLr0y~ZLzj5ocLu~yRx3JLJhuzVqzRsQuY3PvsC2VWUujLHJg~iWmOeYgHH5nr5NVkGQbPJm9i0xLch3slRFv5YlZQY9W78FUbFQnGRTmJrRXMI3Fq14Z1bbsSy9XNaI9t9vihi~P1VOYbDCM0vlG5MEzB9Mp7Jq2ZkIzNXVd8G0d43Q__&Key-Pair-Id=APKAJLOHF5GGSLRBV4ZA

- Baker, S. R., Bloom, N., Davis, S. J., Kost, K., Sammon, M., & Viratyosin, T. (2020). The unprecedented stock market reaction to COVID-19. The Review of Asset Pricing Studies, 10(4), 742-758. https://doi.org/https://doi.org/10.1093/rapstu/raaa008

- Fama, E. F. (1970). Efficient capital markets: A review of theory and empirical work. The Journal of Finance, 25(2), 383–417. https://doi.org/https://doi.org/10.2307/2325486

- Fama, E. F., French, K. R., Booth, D. G., & Sinquefield, R. J. F. A. J. (1993). Differences in the risks and returns of NYSE and NASD stocks. Financial Analysts Journal, 49(1), 37–41. https://doi.org/https://doi.org/10.2469/faj.v49.n1.37

- Griffin, J. M., & Lemmon, M. L. (2002). Book‐to‐market equity, distress risk, and stock returns. The Journal of Finance, 57(5), 2317–2336. https://doi.org/https://doi.org/10.1111/1540-6261.00497

- Gurgul, H., Mestel, R., & Schleicher, C. (2003). Stock market reactions to dividend announcements: Empirical evidence from the Austrian stock market. Financial Markets and Portfolio Management, 17(3), 332. https://doi.org/https://doi.org/10.1007/s11408-003-0304-1

- Inchausti, B. G. (1997). The influence of company characteristics and accounting regulation on information disclosed by Spanish firms. European Accounting Review, 6(1), 45–68. https://doi.org/https://doi.org/10.1080/096381897336863

- Lintner, J. (1965). Security prices, risk, and maximal gains from diversification. The Journal of Finance, 20(4), 587–615. https://doi.org/https://doi.org/10.2307/2977249

- Onali, E. (2020). Covid-19 and stock market volatility. Available at SSRN 3571453. https://doi.org/http://dx.doi.org/10.2139/ssrn.3571453

- Pavlyshenko, B. M. (2020). Regression approach for modeling COVID-19 spread and its impact on stock market. arXiv Preprint arXiv, 2004, 01489. https://arxiv.org/abs/2004.01489v1

- Pettit, R. R. (1972). Dividend announcements, security performance, and capital market efficiency. The Journal of Finance, 27(5), 993–1007. https://doi.org/https://doi.org/10.1111/j.1540-6261.1972.tb03018.x

- Sansa, N. A. (2020). The impact of the COVID-19 on the financial markets: Evidence from China and USA. Electronic Research Journal of Social Sciences and Humanities, 2(2), 29 - 39. https://doi.org/http://dx.doi.org/10.2139/ssrn.3562530

- Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance, 19(3), 425–442. https://doi.org/https://doi.org/10.2307/2977928

- Shiller, R. J. (2015). Irrational exuberance: Revised and expanded third edition. Princeton University press. https://doi.org/https://doi.org/10.2307/j.ctt1287kz5

- Smaga, P. (2014). The concept of systemic risk. SRC Special Paper, 5 (1), 134–142. https://ssrn.com/abstract=2477928

- Tversky, A., & Kahneman, D. (1981). The framing of decisions and the psychology of choice

- Watts, R. L., & Zimmerman, J. L. (1986). Positive accounting theory. Prentice-Hall, NJ. https://ssrn.com/abstract=928677

- Yan, B., Stuart, L., Tu, A., & Zhang, T. (2020). Analysis of the effect of COVID-19 on the stock market and potential investing strategies. Available at SSRN 3563380. https://doi.org/http://dx.doi.org/10.2139/ssrn.3563380