Abstract

Based on Upper Echelon Theory (UET), this study established and examined the impact of upper managers ‘s characteristic (CEO) on choosing a cost leader strategy (CL), using cost management system (CMS) information in the process CEO ‘s strategic decisions. As well as considering the moderator role of advanced manufacturing technology (AMT) in some relationships. This study used SmartPLS3 software to evaluate measurement model and structure model. The results indicated that: (1) the positive effects of all direct relationships are accepted and; (2) the moderator role of AMT in the relationships between education background—choice of CL; Education background—CMS are both positive and statistically significant. This results reinforced for the important role of using CMS information, CEO ‘s demographic characteristic (eduction background), AMT ‘s moderator role. Then, this result will help managers to design a CMS effectively suitable to CEO and strategy of firm, enhancing financial performance of manufacturer.

PUBLIC INTEREST STATEMENT

Demographic characteristics of upper managers have an important role impact on use cost management system (CMS) information and choices of strategy. This study will explore and discuss about the impact of CEO ‘s education background on use cost management system information to implement strategy choiced by upper managers, besides considering the moderator role of advanced manufacturing technology in that process. The results of our study suggest that the using of an effective CMS information suitable with strategy and CEO’s demographic characteristics can enhance organizational s’ performance (i.e. enterprises operating in a transitional economy such as that of Viet Nam), that wish to establish a business in a transitional economy in the Asian block (e.g., like Viet Nam) by companies in the Anglo American block (e.g., Australia, United Kingdom, United States).

1. Introduction

In Viet Nam, the growth resulted from implementing the market reform policy, from lifting of the American embargo in February 1994, and from new membership in several groups including the Association of Southeast Asian Nations (ASEAN) in 1995, the Asia-Pacific Economic Cooperation (APEC) in 1998, the ASEAN Free Trade Agreement (AFTA) in 2003, and the World Trade Organization (WTO) in 2007. Vietnam has been under pressure to improve its social, economic and legal systems. In competitive environment, the rapid technological change impact on their cost structures, processes and controls and due to recent economic crisis affecting businesses worldwide lead to a decline in performance of organisational so manufacturer need to revise their strategy, manufacuting process and accounting techniques to be able to compete with their rivals (Aji & Husin, Citation2020; Ismail & Isa, Citation2011; Le et al., Citation2020; Nguyen et al., Citation2020).

Organizational performance will be improved if the management accounting and control system and the context variables (like strategy) is suitable fit (Chenhall, Citation2003). CL strategy can obtain the advantage by reducing the economic costs among its competitors (Barney, Citation2002) and CL may help a firm to gain “a low cost position” (Porter, Citation1985). However, the obsolescence and ineffectiveness of the traditional management accounting in advanced manufacturing environment has attracted many academia attentions (Davila & Wouters, Citation2007; Johnson & Kaplan, Citation1987; Nguyen et al., Citation2017; Pavlatos, Citation2012). In a competitive environment, managers may require information to make decisions in order to fulfill their functions (Liem & Hien, Citation2020a). Accounting information is critical among the different types of information that are made available to managers for their decision making (Demski, Citation2008). Vietnamese organisations face competition from both within and outside the economy (Zhu, Citation2002). For example, many of the companies have to compete with both local and FDI competitors for market share. In order to cope with the competitive and rapidly changing business environment, managers in Vietnamese enterprises require accounting information that is diverse and useful for making appropriate and timely decisions. Bruggeman and Slagmulder (Citation1995) defined CMS is a part of management accounting and focus on providing cost information. Then the relevant CMS information has identified and the derived level of accuracy provided to support decision making and control activities. A fit between strategy and control system (e.g CMS) will contribute to improving financial performance (Gerdin & Greve, Citation2004). Therefore, to pursue CL strategy, managers need a suitable management accouting tools (Chenhall, Citation2003).

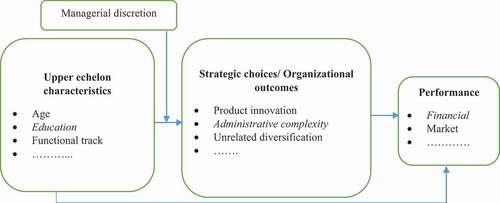

“Little attention has been given to identifying the factors that explain the content of cost management systems” (Chenhall, Citation2003) and Naranjo-Gil et al. (Citation2009) confirmed that “although the general management literature widely acknowledges that top manager characteristics are predictive of organizational outcomes, little is known about how individual managerial differences affect CMS design and use”. CMS is seen as a system administrative complexity (Chenhall & Morris, Citation1986) and be a modern management accounting tool. UET indicated characteristics of upper managers will impact on choosing an organizational strategy and using a system administrative complexity or management accounting techniques (Hambrick & Mason, Citation1984).

Hambrick & Mason first introduced UET in 1984. UET is considered as an important fundamental theory of the uppers managers ‘s behavior (Carpenter et al., Citation2004; Finkelstein et al., Citation2009). UET recognized uppers managers ‘s characteristics influence an organization ‘s outcomes and strategy by the choices they have made (Hambrick & Mason, Citation1984). UET is used in management accounting is quite limited ((Hiebl, Citation2014; Zor et al., Citation2018).

Based on UET, a few studies have examined the CEO ‘s education background impact on choosing CL strategy and the using of CMS information in the same research model (Le et al., Citation2020; Pavlatos, Citation2012; Zor et al., Citation2018). Beside that, the lack of the combination with financial performance is a dependence variable in model of research (Hiebl, Citation2014). Based on UET, AMT had identified to be a characteristic of managerial discretion (Hambrick and Finkelstein (Citation1987). However, AMT has not been considered in the field of management accounting as well as the moderator role of AMT on behavior of choosing CL strategy and using CMS information (Pavlatos, Citation2012). Therefore, in this study, I considered the AMT as a moderator variable in the research model

Consequently, the current paper seeks to make the following contributions to the existing literature. Firstly, this is the first study in which the author examines the relationship between the education background, choice of CL strategy, using CMS information and financial performance in the same research model. Secondly, the AMT’s moderator role is also considered in some relationships: (1) between CEO ‘s education background and choice of CL strategy and (2) between CEO ‘s education background and use of CMS information. Finally, in relation with Vietnnamese transitional economics, this study focuses on CEO ‘s education background to explain the behavior of them in choosing CL strategy, using CMS information for decision making, controlling and performance evaluating in strategy implementation process, which have not yet been studied in a manufacturing context before.

This study also contributes to managerial perspective in several ways. Firstly, choices of Viet Nam manufacturer to investigate the behaviour of using CMS information are so important. Viet Nam is a transitional economics which changed from a planned economy to a market-based one “changes fundamental managerial assumptions, criteria and decision making, and represents a genuine transformation of the business” (Justin Tan & Litsschert, Citation1994), which requires a fundamental shift of paradigm and mentality that thrives on chaos. While the strategy is implemented, CMS information will help upper managers have exactly cost information. Secondly, this study support for Vietnamese manufacturer understand: (1) CEO’ use of the CMS information in making decisions; (2) the influence of education background and choice strategy of CEO on use of CMS information and financial performance; and (3) the impact of AMT on these influences. Such understanding may help the organisations to develop appropriate strategy as well as to adapt the investment on AMT in order to encourage CEO to use the CMS information when making decisions. Finally, understanding the impact of related factors on CEO’ use of the CMS information in Vietnamese enterprises may help managers to use this information more effectively in making decisions, which may in turn improve financial performance of organization.

The proposed model is analyzed experimentally, I used PLS-SEM to test the hypotheses (Wold, Citation1980). Analysis procedure is performed in two steps: (1) assess measurement model and assess structural model.

The next section presents the theoretical background and hypothesis development, followed by the presentation of the research methodology (the measurement variable and data collection). The last parts are to present results and implications, direction for the next researchs.

2. Background

Vietnam is a transitional economy changing from a centrally planned economy to a market-oriented one (Le et al., Citation2020). After the Vietnam War 1954–1975, the country was reunited; the centrally planned economy was established throughout the whole country (Chaponnière et al., Citation2007). Economic reform began in 1986 after a decade of isolation from western countries. The economy has shifted from a centrally planned economy to a “market-oriented socialist economy under state guidance” (Beresford, Citation2008).

The reform process was very successful. Rapid economic growth (in terms of increase in GDP) driven by first-generation renovation accelerated continuously from 8.1% in 1993 to 9.9% in 1997 and remained at the average rate of 6.9% per annum in the first decade of the 21st century (Phan, Citation2008). This growth resulted from implementing the market reform policy, from lifting of the American embargo in February 1994, and from new membership in several groups on over the world.These events have encouraged the economy’s development through expanding trade and investment, maintaining high growth rates (CIEM, Citation2010; Vo & Duong, Citation2009), and through Vietnam being one of the most attractive among emerging countries for foreign direct investment (FDI) from western countries (West, Citation2010).

FDI inflows increased massively each year, from 1.4 billion USD in 2000 to 11 billion USD in 2010 (Vietnam, Citation2012). In order to create an environment for the development of a multi- sector economy that complied with WTO rules, Vietnam has been under pressure to improve its social, economic and legal systems. From 2006, all enterprises have established, organised and operated under one law, the Law on Enterprises, promulgated by the Vietnamese National Assembly in November, 2005.

In the White Book of Enterprises published in 2020, the number and contribution to GDP of manufacturing enterprises is significant (accounting for 22% of GDP) and is considered to have an important role and lead the economy (Ministry of Planning and Investment, 2020, page 19). Therefore, researching this type of enterprise will help develop the overall economy of the country. Besides, the application of cost accounting in manufacturing enterprises in Vietnam is still limited. The cost accounting system is still mixed between financial accounting and management accounting, causing difficulties in the scientific and reasonable application of cost information for businesses, as well as upper managers is not yet aware of the importance of cost information in the decision-making process. However, in a manufacturing enterprises, the involvement of upper managers in the design, construction and use of information from CMS is crucial to the success of each enterprise (Nguyen, Citation2018).

Vietnam manufacturing enterprises require the CMS information to improve performance while operating in times of rapid change. Manager “s use of the cost information is important when enterprises operate in a dynamic and competitive business environment (Mia & Clarke, Citation1999). Therefore, Vietnam manufacturing enterprises may use more of CMS information for decision making. The extent to which CMS information is used in Vietnamese manufacturing enterprises may depend on CEO ‘s demographics (education background) and others factors (e,g CL strategy). To date, there has been no research on CEO’ use of the CMS information and related factors conducted in Vietnam. Such studies may provide a better understanding of managers” use of the CMS information in a transitional economy.

3. Theoretical framework

UET was first introduced by Hambrick and Mason (Citation1984). The characteristics of upper managers can be of two types: observable traits and psychological traits. Hambrick & Mason implicated that characteristics of upper managers influence their behavior in decision making related to choice strategy or outcome of organization and administration complicated system ().

Figure 1. Conceptual model of UET

The UET literature typically investigates the direct relationship between top manager composition and strategic decisions (Finkelstein & Hambrick, Citation1996). Porter (Citation1985) introduced CL strategy, and this kind strategy was adopted by many firms all over the world gain lots of success. CMS are an important component of MCS and MAS (Chenhall, Citation2003). CMS and MAS can be seen as an organizational outcome or as an aspect of organizational structure (Chenhall, Citation2003; Strauß et al., Citation2013). Based on UET, CL strategy and using CMS information can be expected to be influenced by CEO ‘s education background.

Financial performance is considered to be a dependent variable in the research model, it is influenced by CEO ‘s characteristics, strategies and complexity administration systems (Hambrick & Mason, Citation1984). Therefore, in this study, financial performance is also considered as the dependent variable that influenced by CEO ‘s education background, CL strategy and using CMS information.

Beside, managerial discretion is a moderator variable in UET (Hambrick, Citation2007). Hambrick and Finkelstein (Citation1987) showed the characteristics of managerial discretion are environmental characteristics, organizational characteristics and uppers manager individuals characteristics. Advanced Manufacturing Technology (AMT) investment is a characteristics of organization and it is necessary to apply advanced technology in today ‘s production processes and may also have an impact on choose strategy and the useful of cost information. As part of the strategic responses to escalating market competition and trade liberalization, manufacturing firms have been making significant changes to their manufacturing process through by invest on AMT. AMT has influence management accounting system use and imply that AMT investment requires a suitable strategy and changes in the operations of the organisations about the cost structures and managers ‘s information needs (Isa & Foong, Citation2005). AMT can be seen as a moderator variable on the relationship between CEO ‘s education background and behavior of choosing CL strategy; between CEO ‘s education background and using CMS information. Therefore, in this study, I considered the AMT as a moderator variable in the research model

4. Empirical literature review and hypotheses development

4.1. Cost leadership strategy

Based on Porter ‘s framework (Citation1980, Porter, Citation1985), strategy can be measured along two dimensions: product differentiation and cost leadership strategy. CL or low cost provider startegy is among the generic strategies that a firm can pursue to attain the status of a firm with the lowermost cost production in the business (Porter, Citation1985). Porter (Citation1980, p. 35) describes the core philosophy of this strategy as follows: “Cost leadership requires aggressive construction of efficient-scale facilities, vigorous pursuit of cost from experience, tight cost and overhead control, avoidance of marginal customer accounts, and cost minimization in areas like R&D, service, sales force, advertising, and so on. A great deal of managerial attention to cost control is necessary to achieve these aims. Low cost relative to competitors becomes the theme running through the entire strategy, though quality, service and other areas cannot be ignored”. The highlight features about CL strategy are: (1) level of differentiation must be near to the competitors and (2) in order to maintain its cost advantage, replicating the sources of competitive advantage should be hard for the competitors (Kay, Citation1993). CL strategies have provided manufacturing industry the competitive edge over its rival in winning the market in the competitive business environments (Mohammadzadeh et al., Citation2010). Probability of performing above the average industry performance becomes high when a firm attains CL and charges less than its competitor.

4.2. Cost management system

MCS provide information regard to a firm’s strategic domain. An CMS provides a means of gathering and processing cost information to assist managers in planning, control, and performance evaluation throughout the organization. Chenhall (Citation2003) asserts that “Considerations of interest to designers and researchers of CMS include the extent to which the systems provide information, and; the degree of use; the usefulness of the information or the beneficial nature of the cost systems; the importance in making operational decisions and whether they are helpful to the organization, and satisfaction with the systems”. Since CMS is a component of MCS and can be used to assist in implementing firm’s strategy. Managerial behavior is affected by information-based control systems. CMS is a narrower concept than MCS, MAS and CMS information used in strategic implementation as well as in operating decisions through process improvement, product design, performance measurement and evaluation decisions. The benefits of CMS information are quite significant. Level of detail: a cost system allow costs to be analyzed for different purpose (Karmarkar et al., Citation1990; Shank & Govindarajan, Citation1993). Classify costs according to behavior supports the ability to provide useful detailed cost information. Distinction between controllable and noncontrollable costs support in performance evaluation (Feltham & Xie, Citation1994; Tran & Nguyen, Citation2020). Frequency of cost reports identify problems and opportunities for improvement.

4.3. Advanced manufacturing technology (AMT)

AMT is one of the integrated manufacturing practices invested by firms to reduce costs, improve quality, and faster manufacturing processes, in order to ensure continuous improvements (DEAN Jr. & Snell, Citation1996). Research has identified three broad categories of AMTs: design, manufacturing and administrative (Boyer et al., Citation1997). Design-based AMTs are technologies reduce design cycle times and hence time to market. Administrative-based AMTs are technologies such as electronic data interchange that enable faster and cheaper communication both within an organization and across a supply chain. Manufacturing-based AMTs are actual production technologies such as JIT, TQM, flexible manufacturing systems (FMS), computer numerical control (CNC) and group technology (GT) or activities based cost (ABC). Both three categories technologies improve the competitiveness of a manufacturing organization by improving many of the processes that support production. However, manufacturing-based AMT become the new contextual factors of technology that related in accounting field (Chenhall, Citation2003). Therefore, in this study, it is expected that the investment and implementation of manufacturing-based AMT would change the way managers in choosing cost leadership strategy and using CMS information.

4.4. Hypotheses development

4.4.1. Education background impact on choice of cost leadership strategy

Based on UET, education background impact on choice of a strategy (Hambrick & Mason, Citation1984). Managers with education in business were inclined toward the detailed control of outcomes of activities and processes (Armstrong, Citation1987) because their confident with, more inclined to rely on, distant and financial controls when managing the organization (Finkelstein & Hambrick, Citation1996; Song, Citation1982). Managers who focused cost control and efficiency which lead to following a CL (Porter, Citation1985). In the contrary, manager with non-business oriented education background will have propensity product innovation (Wijesinghe & Samudrage, Citation2016), so this characteristic is suitable with a strategy like product differentiation stratey. Due to the changing competitive forces a transitional economy (such as Vietnam), a company is required to reconsider its competitive strategies. CL strategy focus on cost monitoring; thus managers with education in business may be required to use more financial information such as actual costs and budgeted costs in order to persue and implement CL strategy.

H1: CEOs with the more business education background should have positive impact on choice of CL strategy.

4.4.2. Education background impact on use CMS information

Based on UET, education background impact on designing and using a complexity administration system (Hambrick & Mason, Citation1984). CMS can be seen as a complexity administration system in an organization (Chenhall & Morris, Citation1986). Business administrators and accounting professionals have developed several new accounting practices to deal with them (Bhimani & Bromwich, Citation1992; Hoque & James, Citation2000). Managers with an business orientated will be more confident with, and inclined to, the use of financial information, since this type of information aligns with their general, administrative view of organizations (Finkelstein & Hambrick, Citation1996; song, Citation1982). In additional, CFOs with a more business-oriented background are found to be more familiar with using CMS information. Moreover, Emsley et al. (Citation2006) found that business managers’ professional development are associated with the degree to which they initiate accounting innovations. Naranjo-Gil et al. (Citation2009) state that “CFOs with a business-oriented background are more receptive to institutional pressures to use CMS as their knowledge of these systems makes the apparent solutions that they offer more salient”. In the reform process of a transitional economy such as Vietnam, several new activities and operations have emerged: economic liberalisation, booming private consumption, and leadership styles (Farber et al., Citation2006). To make managing decisions in this context, managers have to update information related cost more exactly, aggregated, integrated and more timely. This kind of financial information is suitable with CEO ‘s education in business.

H2: CEO ‘s business oriented education background will have positive impact on using CMS information.

4.4.3. Education background and financial performance

UET indicated that CEO ‘s characteristic influence on financial performance (Hambrick & Mason, Citation1984). The researches in medical, medical education of managers toward emphasizing patient care and health improvement, rather than toward the improvement of overall organizational or financial performance (Kurunmäki, Citation2004). Besides that, top managers with a technical orientated are more familiar with the technical and operational process of the organization and are keen on improving the content of processes (Finkelstein & Hambrick, Citation1996) and less oriented towards improving the efficiencies of finance (Song, Citation1982). In the contrary, manager with business oriented education background focused on achieving controls and efficiencies (Liem & Hien, Citation2020b). Moreover, in a competitive business environment and operating in a rapidly changing, Vietname manufacturing enterprises need to encourage their managers to be more flexible, self- confident in their work, in order to adapt to several uncertain events to improve financial performance (Nguyen et al., Citation2017). So, CEOs ‘s business oriented education background have more ability to improve financial performance faster.

H3: CEO’s business oriented education background will have positive impact on financial performance.

4.4.4. Choice of cost leadership strategy impact on using CMS information

Althought, UET didn’t confirm a relationship between choice a strategy and design, use a complexity administration. But in contingency theory, many research indicated a fit between strategy and control system design and use (Bouwens & Abernethy, Citation2000; Chenhall, Citation2003). Research in industries generally contends that strategy influences control system design and use (Chenhall, Citation2003; Langfield-Smith, Citation1997). Any associated benefits or draw-backs are a function of the degree of alignment between strategy circumstances the firm pursing and the using of a firm ‘s cost system (Hill, Citation2001; Hill & Johns, Citation1994). When CL strategy is chose, managers will force to reduce cost in order to gain advantages (Porter, Citation1985). Using CMS information defines the degree to which a CMS supports strategic and operational decisions. In addition, organizations emphasizing cost control will have more functional cost systems because managers will require more cost information as well as require more extensive and detailed cost information for monitoring costs, performance evaluation (Hill, Citation2001; Lawrence, Citation1990). However, the extent to which CMS information is used to improve performance depends on the context (Chenhall, Citation2007). CL strategy focus on cost monitoring and reduce cost to gain competition advantage. So CEOs will use more financial information such as actual costs and budgeted costs in order to persue and implement CL strategy

H4: Choice of cost leadership strategy will have positive impact on using CMS information.

4.4.5. Choice of cost leadership strategy impact on financial performance

UET confirmed the impact of choice strategy has impacted on financial performance (Hambrick & Mason, Citation1984). The reason for applying the strategy of CL is to obtain the advantage by reducing the economic costs among its competitors (Barney, Citation2002). Porter (Citation1985) said that, by applying the business strategy of CL may help a firm to gain “a low cost position” which offers a firm a defence against competitors. If an organization is following CL strategy, firms performance can be enhanced by improving financial leverage and dividend payments (Valipour et al., Citation2012). Emphasizing on a cost-leadership strategy is kindly to create higher financial performance for firms competing in the emerging economies such as Viet Nam (Aulakh et al., Citation2000; Le et al., Citation2020). In the reform process, Vietnam manufacturing enterprises have been forced to improve their competitiveness, flexibility, and efficiency (Zhu, Citation2002). CL strategy gain a competitive advantage through cost reduction with constant product quality, which is the basis for increased profitability and high financial performance (Porter, Citation1985)

H5: The choice of cost leadership strategy will have positive impact on financial performance.

4.4.6. Using CMS information impact on financial performance

UET reflect that financial performance will be influenced by designing, using a complexity administration (Hambrick & Mason, Citation1984). Firm ‘s performance is directly correlated to a cost—system functions, which is posited by previous researches (Chenhall, Citation2003). CMS produce “better” data and information (i.e., more relevant and useful) that enhance managerial decision making, and thereby lead to improved economic performance (Cooper & Kaplan, Citation1991; Johnson, Citation1992). Chenhall and Morris (Citation1986) measured the frequency of cost reports and contended that more frequent reporting provides managers with feed-back on decisions and information on recent events that they can use to guide future courses of action. In other hand, benefits of cost system information elements identified (level of detail, classify costs according to behavior, cost categorization, frequency of cost reports) will help performance evaluation and improvement (Feltham & Xie, Citation1994). Vietnam is a developing and transitional economy, so several contemporary management practices have been implemented. Based on CMS information, managers may require necessary information related to these cost measures in managing decisions and performance measurements (Nguyen et al., Citation2017). The literature indicates that under high uncertainty conditions, managers use more information related to price and cost to facilitate their decision making in order to improve their performance (Chenhall & Morris, Citation1986).

H6: Using CMS information will have positive impact on financial performance.

4.4.7. Moderator role of advanced manufacturing technology

In application of UET, this study considers manufacturing based AMT as moderator role in the relationship between: (1) business oriented background education and choice of cost leadership strategy; (2) between business oriented background education and using CMS information.

Ministry of industry and trade of the socialist republic of Viet Nam insisted that the application of scientific and technological (S&T) advances in production and business activities is a key driving force for the sustainable development of production sectors. The S&T Development Strategy for the period 2011–2020 affirms that Vietnam is determined to consider S&T as the foundation for the country’s sustainable development; regulates the increase in investment in S&T at 1.5% of GDP in 2015 and over 2% in 2020. The fund has a charter capital of VND 1,000 billion from the state budget, focusing on concessional loans, loan interest support, guarantee for loans, capital support for organizations, individuals and businesses to conduct research, technology transfer, renewal and improvement.

In market competition, manufacturing firms are constantly reviewing and revising their manufacturing strategies, and they typically achieve this through adoption of AMT (Khandwalla, Citation1977). Organizations that implement cost leadership strategy employs several activities like accurate demand forecasting, technology advancement (Bordean et al., Citation2010; Porter, Citation1985). Frohwein and Hansjurgens (Citation2005) suggested that to gain cost leadership advantage the organization should emphasize on cost minimization and involve with process innovation activities. Low-cost factory layout in the production systems is necessary for enhancing competitiveness (Kreng & Tsai, Citation2002). For example, FMS scheduling must be organized not only to reduce costs but also to maximize throughput (=revenue—material cost). In addition, AMT implementation leads to changes in manufacturing operations or a strategy pursued. When a company changes to flexible automation, the overhead allocation base has to be changed to maintain the desired level of accuracy of product cost. It will support for CL strategy gain advantages.

H7a: The more invest on AMT based manufacturing, the more CEOs with business oriented business education background choose cost leadership strategy.

Choice of the management accounting techniques use can be affected leaders (Abdel-Kader & Luther, Citation2008; Hoque & James, Citation2000). To remain competitive, the adoption and investment in AMT in some firms have changed not only their management accounting, control systems but also information needs (Johnson & Kaplan, Citation1987). Firms have made investments in AMT, advanced management accounting practices will be more useful (Abdel-Maksoud et al., Citation2005). At that time, using CMS information can improve and keep the organization running smoothly in implementation strategy like CL. On the other hand, Isa and Foong (Citation2005) argued that AMT leads to use new costing techniques. Their findings were strengthened by Al-Omiri and Drury (Citation2007), lean production techniques and the degree of JIT implementation, which high positively related to sophisticated cost systems (e.g CMS).

H7b: The more invest on AMT based manufacturing, the more CEOs with business oriented business education background using CMS information ().

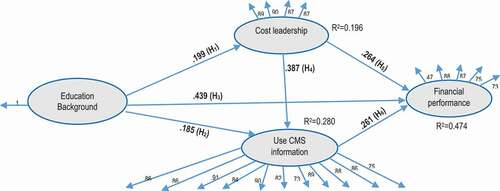

Figure 2. Research model

Research model includes eight hypotheses. In which, there are six hypotheses showing direct effects between variables (H1 to H6) and two hypotheses considers manufacturing based AMT as moderator role in the relationship between: (1) business oriented background education and choice of cost leadership strategy; (2) between business oriented background education and using CMS information.

5. Research design

5.1. Variables measurement

The measurement of Naranjo-Gil et al. (Citation2009) is used to measure CEO’s educational background. Each CEO was asked to state their educational background in years of studies (college, bachelors, master degrees and courses attended) in two streams: (1) business orientated and (2) non-business orientated. Following, the variable “educational background” is measured by dividing the years studied in business programs with the total years of studies. According to Naranjo-Gil et al. (Citation2006, Citation2007a), if the index showing the educational orientation of CEO is 1, it shows the orientation of the business education background of the CEO at the highest level. On the contrary, if this index is 0, this represents the highest level of non-business education orientation of senior CEO.

Based on the research of (Zott & Amit, Citation2008), we measure cost leadership strategy compared with a firm’s main competitors using four items, which include evaluating the firm’s agility in responding to the environment, the rate of equipment utilization, the operational costs and the efficiency of production and organization. The behavior of using cost data (USE) was measured using an instrument developed (Pavlatos & Paggios, Citation2009). Respondents were asked to indicate the extent of the use of cost data on the aforementioned scale. Financial performance is measured based on (Jaworski & Kohli, Citation1993) and (Calantone et al., Citation2002), this measurement includes five indicators: Return on sales (ROS), Return on investments (ROI), Sales growth, Return on assets (ROA) and Overall profitability. Based on Jonsson (Citation2000) research, AMT is measured by indicate the eight items about amount of investment manufacturing plant has in the activities.

5.2. Sample collection

According to the White Book 2020 was published by Ministry of Planning and Investment in 2020, of the 610,637 enterprises with business results as of 31 December 2018, the South region (account for 52% of the sample of this study) and there are a large number of enterprises (nearly 46% of the total number of enterprises in the country). Enterprise southern region, typically in HCM city has 239,623 businesses, Binh Duong province has 31,599 businesses, Long An province (top of the Mekong Delta) has 8,883 businesses, the central region has 95,558 enterprises (13.4%), in the North there are all 252,694 enterprises (accounting for 35%). In addition, according to the 2020 white book, the investment capital scale in the southern provinces mentioned above accounts for over 60% of the national investment. To increase representation of sample in population, this study selected the norm sample according to the proportion of enterprises between the economic regions of Vietnam.

Population of this study includes the CEOs, General Directors and Directors in enterprises manufacturing in Vietnam with three forms of ownership (State, private and foreign), operating under the Enterprise Law 2014 in Vietnam. Respondents have the most important and powerful role in choosing the strategy and using accounting information from a complex administrative system such as CMS (Hambrick & Mason, Citation1984; Hiebl, Citation2014). Small-scale manufacturing firms are rejected because CMS is not suitable to be designed in firms of this size (Nguyen et al., Citation2017). I used two method of sample collection: (1) Survey by Google form: The questionnaire targeted more than 1,916 CEOs, General Directors and Directors of manufacturing enterprises with personal email addresses (websites of businesses, Entrepreneurs Clubs and Entrepreneur Association) . And (2) by direct survey: base on the author’s convenient relationship, 800 questionnaires were sent directly to the respondents in manufacturing enterprises.

This study conducted an online and direct survey. By online survey, the missing values can be controlled by setting mandatory questions. This force-answer approach allows respondents to move to the next question only when they finish the current one (Smyth et al., Citation2010). Consequently, in this kind of survey there are no missing values in all responses submitted. By direct survey, the question will be excluded. The total number of questionnaires received was 353. Missing value is 9. After excluding small firm through two ways of data collection, 167 questionnaires were used to analyze because the amount of sample is suitable with the proportion of enterprises between the economic regions of Vietnam and can representative for population (See below).

Table 1. Scale items of variables

6. Empirical results and discussion

Partial least squares structural equation modelling (PLS-SEM) is used primarily for path analysis (Wold, Citation1980). The procedure of analysis consists 2 steps: (1) assessing the measurement model and (2) assessing the structural model (Hair et al., Citation2017).

6.1. Measurement model

The measurement model estimates the relationship between the variable and its observed variables. It is evaluated by many different indicators that help express the complete concepts, thereby improving scale accuracy and results.

Internal reliability is used to assesse scale reliability, which is presented by Cronbach’s alpha, composite reliability (Hair et al., Citation2017; Nunnally & Bernstein, Citation1994) and rhoA (Dijkstra & Henseler, Citation2015). Outer loading of observed variables (greater than 0.7) and average variance extracted (AVE greater than 0.5) is used to assess convergent validity(Hair et al., Citation2017). Significance of relationships is identified by run bootstrap 2.000 times from data collected(Hair et al., Citation2017). Results of indicators is showed in . All scales reached the required reliability.

Table 2. Demographics of the participating firms and respondents

All the scale reached convergence value, shows value range of scales is greater than 0.5, observed variables have outer loading greater than 0.7.

Figure 3. PLS-SEM analysis results of the theoretical

Cross-loading coefficient in its structure is much larger than in other structures. Besides the results of Fornell-Larcker criterion () and factor HTMT () present that the scale ensures discriminating value(Hair et al., Citation2017; Henseler et al., Citation2015).

Table 3. Scale accuracy analyses

Table 4. Fornell-Larcker criterion

Table 5. Heterotrait-monotrait ratio (HTMT)

6.2. Structural model

After confirming that structural measurements are reliable and valid. The next step is to evaluate the structural model results, to test the predictive capability of the model and the relationships between research variables.

To ensure multicollinearity between independence variables isn’t exist, this study used variance-inflating factor (VIF). VIF of all scales is less than 2.0, so multicollinearity is ensured (Hair et al., Citation2017).

Predictive capability of the independent variables is assessed through coefficient of determination (R2). In show, R2 value of CL is 0.196, CMS is 0.280 and Financial performance is 0.474, presented level of prediction is enough (Wijesinghe & Samudrage, Citation2016). The factor Q2 of dependence variables is greater than 0. Consequently, it ensured the predictive power of the model. With bootstrap 2,000 times, theoretical model tested and relationships were statistically significant (p-value < 0.5) ().

Table 6. Hypotheses testing results

Testing the moderator of AMT is a major objective in this research. The results of AMT ‘s measurement model indicated that the reliable and valuable is ensured. Next, the two-stage approach (Chin et al., Citation2003) was applied to assess moderator variable of AMT. The first stage estimate the main impact model, and second stage multiplied the moderator variables and exogenous variables to measure interaction terms (Education background x advanced manufacturing technological; Education background x advanced manufacturing technological).

Results in shows that the advanced manufacturing technological play a moderator role in the relationship between education background and Cost leadership, and between education background . The hypotheses are statistically significant (p-value < 0.05).

Table 7. Tests for moderating effects

6.3. Discussion

The results indicated that the relationship between CEO ‘s business oriented education background and their behaviour of choosing CL strategy, using of the CMS information, financial performance was significant and positive, providing support for hypothesis 1,2 and 3. CEO “s behaviour of choosing CL strategy increased when their education background oriented business. This result reinforced for research of (Wijesinghe & Samudrage, Citation2016). It can be interpreted that CEO” using of CMS information may increase when their education background is oriented business, this result supported for research of (Pavlatos, Citation2012). CEOs will use CMS information in process improvement, product design, and performance measurement and evaluation decisions. The more CEO with business orientation, the more financial performance of firm is improved. This result support for UET is proposed by (Hambrick & Mason, Citation1984).

This study found a positive association between choice of CL strategy and use of the CMS information in Vietnam manufacturing enterprises. Under pressure of the reform process and the increase of competition, many companies have developed comprehensive CMS linked to CL strategy to gain competitive advantage. And when CL strategy is chose, CEO will force to reduce cost in order to gain advantages. A fit between strategy and control system will improve financial performance. This result reinforced for the research of (Porter, Citation1985), (Gerdin & Greve, Citation2004) and (Chenhall, Citation2003). These findings support hypothesis 4,5,6.

Vietnam with a transition economy, rapid growth of the economy and innovation and investment in technology are being focused. Beside, AMT has influence management accounting system use and imply that AMT investment requires a suitable strategy and changes in the operations of the organisations about the cost structures and managers ‘s information needs. When the investment on AMT increase, the ability of choosing CL strategy and using CMS information will increase. These findings support hypothesis 7a, 7b. Therefore, the moderator role of AMT investment in research model is supported. This result reinforced for research of Hambrick and Finkelstein (Citation1987).

7. Summary and conclusion

7.1. Summary

This research investigated the influence of factors, namely education background, CL strategy and CEO’ using CMS information and their financial performance in the context of Vietnam. In addition, the moderator role of AMT was also investigated in some relationships. The results of this study reveal that all direct relationships were positive and significant. AMT had a moderating effect on the relationships: (i) between education background and CEO’ use of the CMS information (ii) between education background and CEO’ choice of CL strategy.

Several software packages, such as Amos, LISREL, PLS-Graph, and Mplus, are available for estimating SEM models. The SmartPLS3 Beta software package (Ringle et al., Citation2005) was used to test the hypotheses of the PLS model of the research. SmartPLS is appropriate for this study for several reasons.

As with other component-based SEM techniques, PLS allows the simultaneous examination of both the measurement model (outer model: the relationship between the latent variable and its indicators) and the structural model (inner model: the relationship between the constructs). According to (Ringle et al., Citation2005), in the SmartPLS, the assessment of the measurement model is similar to the principal components analysis (using the PLS algorithm with 300 maximum iteration, standardised values and centroid weighting scheme), while the structural model with path coefficients is comparable with ordinary least squares regression (using bootstrapping of 2,000 resamples). PLS is a technique of latent variable modeling that requires a relatively small sample size and requires ten cases for the most complex regression (Chin, Citation1998). In my study, the most complex regression was that of managerial performance as the dependent variable with five independent variables, suggesting a minimum sample size of 50 cases. Besides that, given that all the responses of this study came from the same CEO to a set of survey items, the potential problem of common method biases may exist. To evaluate the problem about common method bias, The Harman’s single factor test was employed. A un-rotated factor analysis accompanied on all measurement constructs (Except for education) extracted 4 factors. Total cumulative variance of 4 factors is 65.5%. Therefore, the errors of total cumulative variance didn’t appear.

7.2. Conclusion

7.2.1. Theoretical implications

In this study, some theoretical implications as follows: Firstly, I found that the behavior of choosing CL strategy is significantly positively associated with the CEOs ‘s education background. This result about the impact of education background on CL strategy supported for UET (Hambrick & Mason, Citation1984) and support for proposed of Porter (Citation1985). This result in line with their implication, in that managers who focused cost control and efficiency which lead to following a CL strategy. Secondly, the role of CEOs ‘s characteristic in using CMS information, supports for Pavlatos (Citation2012) ‘s result. Companies, CEOs with the more business oriented, not only the implementing and maintaining a more sophisticated costing system will increase (Al-Omiri & Drury, Citation2007) but also be more familiar with using CMS information. This is in line with prior literature, which suggests that the educational background of upper managers affects their behaviour (e.g., Finkelstein & Hambrick, Citation1996; Naranjo-Gil et al., Citation2009; Pavlatos, Citation2012). This study also reinforced for Naranjo-Gil et al. (Citation2009). Thirdly, manufacture firm increase invest in AMT, CEOs with propensity business education background will more intend to choose a CL strategy and using CMS information. So, in this perspective, the moderator role of AMT reinforced for the proposed of Hambrick (Citation2007). Finally, financial performance variable is less concerned in UET model, this study contribute to fill the gap and reply the appeal of Hiebl (Citation2014) and Pavlatos (Citation2012).

7.2.2. Managerial implications

There are some managerial implication by this study. Firstly, results indicated CEO in manufacturers Viet Nam used more the cost data not only for many difference decisions making but also support them for decision making daily and in process to implement CL strategy. Hence, it appears that there is a relation between using CMS information and CEO ‘s education background, intend to choose CL strategy in manufacturer. Secondly, the results provide empirical evidence of the relation between CEO ‘s education background, CL strategy and using CMS information in the manufacture industry. Thirdly, whether an organization has increased to invest in AMT (e.g: ABC, TQM, JIT.), not only the pursing a CL strategy will increased, but also multidimensional characterization of the functions a CMS can perform also increased. This leads to the need of using CMS information by CEO in manufacturer in Viet Nam. Fourthly, financial performance in manufacturer will be improved by combine factors: (1) CL strategy and using CMS information, this is in line with Chenhall (Citation2003); and (2) CEOs “s education background, CL strategy, using CMS information and invest in AMT, suitable with framework of Hambrick and Mason (Citation1984). Finally, in the manufacturing enterprises Vietnam, education background of CEOs, CL strategy and investment on AMT play important roles within organisations. This study contributes to existing knowledge by providing evidence of the effect of these factors on CEOs s” use of the CMS information in the context of the transitional economy of Vietnam. The results of our study suggest that the adoption of an effective CMS design can enhance financial performance across national boundaries (i.e. enterprises operating in a transitional economy such as that of Vietnam). Given the number of foreign investment firms operating in transitional economies in the Asian block (e.g., Vietnam), our results have important implications for companies in the Anglo-American block (e.g., Australia, United Kingdom, United States) that wish to establish a business in a transitional economy in the Asian block.

7.3. Directions for future research

This study also show some limits. Firstly, future research should consider other important variables from UET that influence choose CL strategy, the cost system scope to support for decision making and performance evaluation. Secondly, future study should also concern to other characteristics of upper manager and other moderator variables. Thirdly, prior studies (Thornton, Citation1968) argue that the use of self-rated scales (e.g., financial performance) is likely to generate higher mean values (higher leniency error) and a restricted range (lower variability error) in the observed scale. Future research may improve the validity of the construct by using 360° feedback (from other members in top management team: CFO, Chairman, Vice-Chairman …) to assess financial performance (Fletcher & Baldry, Citation2000). Fourthly, our path (structural) model implies causality. However, the survey method employed in our study allows for the examination of statistical associations at one point in time. The various statements about the direction of relationships proposed in this study can only be made in terms of the consistency of the results with the effects proposed in the theoretical discussions. The use of a different research method, such as a longitudinal field study, would be appropriate to investigate systematically the theoretical causal relationships proposed in our study. Finally, performance variable should be measured by other indicators (e.g makert share, non-financial indicators…)

Acknowledgements

Researcher would like to express my gratitude to all those who gave me the possibility to complete this study especially to University of Economics Ho Chi Minh City.

Additional information

Funding

Notes on contributors

Vo Tan Liem

Vo Tan Liem is a lecturer in Department of Accounting, Van Hien University, Viet Nam. At the moment, he is completing his PhD at University of Economics Ho Chi Minh City, Viet Nam. His research interests are Management Accounting, Accounting Information Systems.

References

- Abdel-Kader, M., & Luther, R. (2008). The impact of firm characteristics on management accounting practices: A UK-based empirical analyses. The British Accounting Review, 40(1), 2–20. https://doi.org/https://doi.org/10.1016/j.bar.2007.11.003

- Abdel-Maksoud, A., Dugdale, D., & Luther, R. (2005). Non– Financial performance measurement in manufacturing com-panies. The British Accounting Review, 37(3), 261–297. https://doi.org/https://doi.org/10.1016/j.bar.2005.03.003

- Aji, H. M., Berakon, I., & Husin, M. M. (2020). COVID-19 and e-wallet usage intention: A multigroup analysis between Indonesia and Malaysia. Cogent Business & Management, 7(1), 1804181. https://doi.org/https://doi.org/10.1080/23311975.2020.1804181

- Al-Omiri, M., & Drury, C. (2007). A survey of factors influ-encing the choice of product costing systems in UK organiza-tions. Management Accounting Research, 18(4), 399–424. https://doi.org/https://doi.org/10.1016/j.mar.2007.02.002

- Armstrong, P. (1987). Engineers, Management and Trust. Work, Employment & Society, 1(4), 421–440. https://doi.org/https://doi.org/10.1177/0950017087001004002

- Aulakh, P. S., Kotabe, M., & Teegen, H. (2000). Export strategies and performance of firms from emerging economies: Evidence from Brazil, Chile, and Mexico. Academy of Management Journal, 43(3), 342–361. https://doi.org/https://doi.org/10.5465/1556399

- Barney, J. B. (2002). Strategic management: From informed conversation to academic discipline. Academy of Management Perspectives, 16(2), 53–57. https://doi.org/https://doi.org/10.5465/ame.2002.7173521

- Beresford, M. (2008). Doi Moi in review: The challenges of building market socialism in Vietnam. Journal of Contemporary Asia, 38(2), 221. https://doi.org/https://doi.org/10.1080/00472330701822314

- Bhimani, A., & Bromwich, M. (1992). Advanced manu-facturing technology and accounting: A renewed alliance. Advanced Manufacturing Engineering. Advanced Manufacturing Engineering, 5(3), 199–207. https://doi.org/https://doi.org/10.1016/0951-5240(92)90031-7

- Bordean, O., Borza, A., Nistor, R., & Mitra, C. (2010). The use of Michael Porter’s generic strategies in the Romanian hotel industry. International Journal of Trade, Economics and Finance, 1(2), 173–178. https://doi.org/https://doi.org/10.7763/IJTEF.2010.V1.31

- Bouwens, J., & Abernethy, M. A. (2000). The consequences of customization on management accounting system design. Accounting, Organizations and Society, 25(3), 221–241. https://doi.org/https://doi.org/10.1016/S0361-3682(99)00043-4

- Boyer, K. K., Leong, G., Ward, P. T., & Krajewski, L. (1997). Unlocking the potential of advanced manufacturing technologies. Journal of Operations Management, 15(4), 331–347. https://doi.org/https://doi.org/10.1016/S0272-6963(97)00009-0

- Bruggeman, W., & Slagmulder, R. (1995). The impact of technological change on management accounting. Management Accounting Research, 6(3), 241–252. https://doi.org/https://doi.org/10.1006/mare.1995.1016

- Calantone, R. J., Cavusgil, S. T., & Zhao, Y. (2002). Learning orientation, firm innovation capability, and firm performance. Industrial Marketing Management, 31(6), 515–524. https://doi.org/https://doi.org/10.1016/S0019-8501(01)00203-6

- Carpenter, M. A., Geletkanycz, M. A., & Sanders, W. G. (2004). Upper echelons research revisited: Antecedents, elements, and consequences of top management team composition. Journal of Management, 30(6), 749–778. https://doi.org/https://doi.org/10.1016/j.jm.2004.06.001

- Chaponnière, J.-R., Cling, J.-P., & Bin, Z. (2007). Vietnam following in China’s footsteps: The third wave of emerging Asian economies. Paper presented at the WIDER Conference on Southern Engines of Global Growth. China, India, Brazil, and South Africa, Helsinki. http://www.adetef.org.vn/website/

- Chenhall, R. H. (2003). Management control systems design within its organizational context: Findings from contingency-based research and directions for the future. Accounting, Organizations and Society, 28(2–3), 127–168. https://doi.org/https://doi.org/10.1016/S0361-3682(01)00027-7

- Chenhall, R. H. (2007). Theorizing contingencies in management control systems research. In C. S. Chapman, A. G. Hopwood & M. Shields, D. (Eds.), Handbooks of Management Accounting Research (Vol. 1, pp. 163–205). Amsterdam, The Netherlands: Elsevier.

- Chenhall, R. H., & Morris, D. (1986). The impact of structure, environment, and interdependence on the perceived usefulness of management accounting systems. Accounting Review, 61(1), 16–35. https://www.jstor.org/stable/247520

- Chin, W. W. (1998). Issues and opinion on structural equation modeling. MIS Quarterly, March, pp vii–xvi. Lawrence Erlbaum Associates.

- Chin, W. W., Marcolin, B. L., & Newsted, P. R. (2003). A partial least squares latent variable modeling approach for measuring interaction effects: Results from a Monte Carlo simulation study and an electronic-mail emotion/adoption study. Information Systems Research, 14(2), 189–217. https://doi.org/https://doi.org/10.1287/isre.14.2.189.16018

- CIEM. (2010). Vietnam after three years of WTO membership. http://www.ciem.org.vn/home/en/home/InfoDetail.jsp?area=1&cat=389&ID=15 82

- Cooper, R., & Kaplan, R. (1991). The design of cost manage-ment systems: Text, cases, and readings. Englewood Cliffs.

- Davila, T., & Wouters, M. (2007). Management Accounting in the Manufacturing sector: Managing costs at the Design and Production stage”. In C. Chapman, A. Hopwood, & M. Shields (Eds.), Handbook of management accounting research (pp. 831-858). Elsevier.

- DEAN Jr., J. W., & Snell, S. A. (1996). The strategic use of integrated manufacturing: An empirical examination. Strategic Management Journal, 17(6), 459–480. https://doi.org/https://doi.org/10.1002/(SICI)1097-0266(199606)17:6<459::AID-SMJ823>3.0.CO;2-8

- Demski, J. S. (2008). Managerial uses of accounting information (Vol. 4). Springer Science Business Media: LLC.

- Dijkstra, T. K., & Henseler, J. (2015). Consistent partial least squares path modeling. MIS Quarterly, 39(2), 297–316. https://doi.org/https://doi.org/10.25300/MISQ/2015/39.2.02

- Emsley, D., Nevicky, B., & Harrison, G. (2006). Effect of cognitive style and professional development on the initiation of radical and non‐radical management accounting innovations. Accounting & Finance, 46(2), 243–264. https://doi.org/https://doi.org/10.1111/j.1467-629X.2006.00165.x

- Farber, A., Nguyen, V. N., & Vuong, Q. H. (2006). Policy impacts on Vietnam stock markets: A case of anomalies and disequilibria 2000–2006. http://dipot.ulb.ac.be:8080/dspace/bitstream/2013/14581/1/rou-0199.pdf.

- Feltham, G. A., & Xie, J. (1994). Performance measure congruity and diversity in multi-task principal/agent rela-tions. The Accounting Review, 69(3), 429–453. https://www.jstor.org/stable/248233

- Finkelstein, S., & Hambrick, D. (1996). Strategic leadership: Top executives and their effects on organizations. West Publishing Company.

- Finkelstein, S., Hambrick, D., & Cannella, A. (2009). Strategic leadership. Oxford University Press.

- Fletcher, C., & Baldry, C. (2000). A study of individual differences and self-awareness in the context of multi-source feedback. Journal of Occupational and Organizational Psychology, 73(3), 303–319. https://doi.org/https://doi.org/10.1348/096317900167047

- Frohwein, T., & Hansjurgens, B. (2005). Chemicals regulation and the Porter hypothesis: A critical review of the new European chemical regulation. Journal of Business Chemistry, 2(1), 19–36.

- Gerdin, J., & Greve, J. (2004). Forms of contingency fit in management accounting research—a critical review. Accounting, Organizations and Society, 29(3–4), 303–326. https://doi.org/https://doi.org/10.1016/S0361-3682(02)00096-X

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2017). A primer on partial least squares structural equation modeling. Sage.

- Hambrick, D. C. (2007). Upper echelons theory: An update. Academy of Management Review, 32(2), 334–343. https://doi.org/https://doi.org/10.5465/amr.2007.24345254

- Hambrick, D. C., & Finkelstein, S. (1987). Managerial discretion: A bridge between polar views of orga-nizational outcomes. Research in Organizational Behavior, 9(4), 369–406.

- Hambrick, D. C., & Mason, P. A. (1984). Upper echelons: The organization as a reflection of its top managers. Academy of Management Review, 9(2), 193–206. https://doi.org/https://doi.org/10.5465/amr.1984.4277628

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/https://doi.org/10.1007/s11747-014-0403-8

- Hiebl, M. R. (2014). Upper echelons theory in management accounting and control research. Journal of Management Control, 24(3), 223–240. https://doi.org/https://doi.org/10.1007/s00187-013-0183-1

- Hill, N. T. (2001). Adoption of costing systems in U.S. hospitals: An event history analysis 1980-1990. Journal of Accounting and Public Policy, 19(3), 41–71. https://doi.org/https://doi.org/10.1016/S0278-4254(99)00013-7

- Hill, N. T., & Johns, E. (1994). Adoption of costing systems by U.S. hospitals. Hospital & Health Services Administration, 39(2), 521–537.

- Hoque, Z., & James, W. (2000). Linking balanced scorecard measures to size and market factors: Impact on organiza-tional performance. Journal of Management Accounting Research, 12(1), 1–17. https://doi.org/https://doi.org/10.2308/jmar.2000.12.1.1

- Isa, C. R., & Foong, S. Y. (2005). Adoption of advanced manufacturing technology (AMT) and management accounting practices: The case of manufacturing firms in Malaysia. World Review of Science, Technology and Sustainable Development, 2(1), 35–48. https://doi.org/https://doi.org/10.1504/WRSTSD.2005.006726

- Ismail, K., & Isa, C. R. (2011). The role of management accounting systems in advanced manufacturing environment. Australian Journal of Basic and Applied Sciences, 5(9), 2196–2209.

- Jaworski, B. J., & Kohli, A. K. (1993). Market orientation: Antecedents and consequences. Journal of Marketing, 57(3), 53–70. https://doi.org/https://doi.org/10.1177/002224299305700304

- Johnson, H. T. (1992). It s time to stop overselling activity-based concepts. Management Accounting Research, 74(2), 26–35.

- Johnson, H. T., & Kaplan, R. S. (1987). Relevance lost: The rise and fall of management accounting. Harvard Business School Press.

- Jonsson, P. (2000). An empirical taxonomy of advanced manufacturing technology. International Journal of Operations & Production Management, 20(12), 26-35. https://doi.org/https://doi.org/10.1108/01443570010353103

- Justin Tan, J., & Litsschert, R. J. (1994). Environment‐strategy relationship and its performance implications: An empirical study of the Chinese electronics industry. Strategic Management Journal, 15(1), 1–20. https://doi.org/https://doi.org/10.1002/smj.4250150102

- Karmarkar, U. S., Lederer, P. J., & Zimmerman, J. L. (1990). Choosing manufacturing production control and cost accounting systems. Harvard Business School Press.

- Kay, J. (1993). Foundations of corporate success. Oxford University Press.

- Khandwalla, P. N. (1977). The chemistry of effective management. Vikalpa: The Journal for Decision Makers, 2(2), 151–164. https://doi.org/https://doi.org/10.1177/0256090919770205

- Kreng, V. B., & Tsai, C. M. (2002). Use of a robustness index for flexible facility layout design in a changing environment. Asia Pacific Management Review, 7(4), 427–448.

- Kurunmäki, L. (2004). A hybrid profession—the acquisition of management accounting expertise by medical professionals. Accounting, Organizations and Society, 29(3–4), 327–347. https://doi.org/https://doi.org/10.1016/S0361-3682(02)00069-7

- Langfield-Smith, K. (1997). Management control systems and strategy: A critical review. Accounting, Organizations and Society, 22(2), 207–232. https://doi.org/https://doi.org/10.1016/S0361-3682(95)00040-2

- Lawrence, C. H. (1990). The effect of ownership structure and accounting system type on hospital costs. Research in Governmental and Nonprofit Accounting, 6(2), 35–60.

- Le, H. M., Nguyen, T. T., & Hoang, T. C. (2020). Organizational culture, management accounting information, innovation capability and firm performance. Cogent Business & Management, 7(1), 1857594. https://doi.org/https://doi.org/10.1080/23311975.2020.1857594

- Liem, V. T., & Hien, N. N. (2020a). Exploring the impact of dynamic environment and CEO’s psychology characteristics on using management accounting system. Cogent Business & Management, 7(1), 1–20. https://doi.org/https://doi.org/10.1080/23311975.2020.1712768

- Liem, V. T., & Hien, N. N. (2020b). The impact of manager’s demographic characteristics on prospector strategy, use of management accounting systems and financial performance. Journal of International Studies, 13(4), 54–69. https://doi.org/https://doi.org/10.14254/2071-8330.2020/13-4/4

- Mia, L., & Clarke, B. (1999). Market competition, management accounting systems and business unit performance. Management Accounting Research, 10(2), 137–158. https://doi.org/https://doi.org/10.1006/mare.1998.0097

- Mohammadzadeh, M., Bakhtiari, N., Safarey, R., & Ghari, T. (2010). Pharmaceutical industry in export marketing: A closer look at competitiveness. International Journal of Pharmaceutical and Healthcare Marketing, 13(3), 331–345. https://doi.org/https://doi.org/10.1108/IJPHM-02-2018-0011

- Naranjo-Gil, D., Maas, V. S., & Hartmann, F. G. H. (2009). How CFOs determine management accounting innovation: An examination of direct and indirect effects. European Accounting Review, 18(4), 667–695. https://doi.org/https://doi.org/10.1080/09638180802627795

- Naranjo-Gil, D., & Hartmann, F. (2006). How top management teams use management accounting systems to implement strategy. Journal of Management Accounting Research, 18, 21–53.

- Naranjo-Gil, D., & Hartmann, F. (2007a). How CEOs use management information systems for strategy implementation in hospitals. Health Policy, 81(1), 29–41.

- Nguyen, N. P. (2018). Performance implication of market orientation and use of management accounting systems. Journal of Asian Business and Economic Studies, 25(1), 33–49. https://doi.org/https://doi.org/10.1108/JABES-04-2018-0005

- Nguyen, T. T., Mia, L., Winata, L., & Chong, V. K. (2017). Effect of transformational-leadership style and management control system on managerial performance. Journal of Business Research, 70, 202–213. https://doi.org/https://doi.org/10.1016/j.jbusres.2016.08.018

- Nguyen, T. T., Nguyen, V. C., & Tran, T. N. (2020). Oil price shocks against stock return of oil and gas-related firms in the economic depression: A new evidence from a copula approach. Cogent Economics & Finance, 8(1), 1799908. https://doi.org/https://doi.org/10.1080/23322039.2020.1799908

- Nunnally, J. C., & Bernstein, I. H. (1994). Psychological theory. MacGraw-Hill.

- Pavlatos, O. (2012). The impact of CFOs’ characteristics and information technology on cost management systems. Journal of Applied Accounting Research, 13(3), 242–254. https://doi.org/https://doi.org/10.1108/09675421211281317

- Pavlatos, O., & Paggios, I. (2009). A survey of factors influencing the cost system design in hotels. International Journal of Hospitality Management, 28(2), 263–271. https://doi.org/https://doi.org/10.1016/j.ijhm.2008.09.002

- Phan, M. N. (2008). Sources of Vietnam’s economic growth. Progress in Development Studies, 8(3), 209–229. https://doi.org/https://doi.org/10.1177/146499340800800301

- Porter, M. (1980). Competitive strategy: techniques for analyzing industries and competitors. New York, NY: The Free Press.

- Porter, M. E. (1985). Competitive advantage. The Free Press.

- Ringle, C. M., Wende, S., & Will, S. (2005). SmartPLS 2.0 (beta). Hamburg: University of Hamburg. http://www.smartpls.de

- Shank, J., & Govindarajan, V. (1993). Strategic cost manage-ment: The new tool for competitive advantage. The Free Press.

- Smyth, J. D., Dillman, D. A., Christian, L. M., & O’Neill, A. C. (2010). Using the internet to survey small towns and communities: Limitations and possibilities in the early 21st century. American Behavioral Scientist, 53(9), 1423 - 1448. doi: https://doi.org/10.1177/0002764210361695

- Song, J. (1982). Diversification strategies and the experience of top executives of large firms. Strategic Management Journal, 3(4), 377–380. https://doi.org/https://doi.org/10.1002/smj.4250030411

- Strauß, E., Zecher,, & Zecher, C.. (2013). Management control systems: A review. Journal of Management Control, 23(4), 233–268. https://doi.org/https://doi.org/10.1007/s00187-012-0158-7

- Thornton, G. C. (1968). The relationship between supervisory and self appraisals of executive performance. Personnel Psychology, 21(4), 441–455. https://doi.org/https://doi.org/10.1111/j.1744-6570.1968.tb02044.x

- Tran, Y. T., & Nguyen, N. P. (2020). The impact of the performance measurement system on the organizational performance of the public sector in a transition economy: Is public accountability a missing link? Cogent Business & Management, 7(1), 1792669. https://doi.org/https://doi.org/10.1080/23311975.2020.1792669

- Valipour, H., Birjandi, H., & Honarbakhsh, S. (2012). The effects of cost leadership strategy and product differentiation strategy on the performance of firms. Journal of Asian Business Strategy, 2(1), 14–23.

- Vietnam, F. d. i. i. (2012). Statistical publisher. http://fia.mpi.gov.vn/News.aspx?ctl=newsdetail&p=2.43&aID=1153

- Vo, T. T., & Duong, N. A. (2009). Vietnam after two years of WTO accession: What lessons can be learnt? ASEAN Economic Bulletin, 26(1), 115–135. https://doi.org/https://doi.org/10.1355/AE26-1H

- West, C. (2010). Global investors have great expectations for emerging markets. Schroder Investment Management. http://www.freshbusinessthinking.com/news.php?NID=6146#.U_DWu0iE4Xw

- Wijesinghe, D., & Samudrage, D. (2016). Top manager orientation, management accounting systems and strategy implementation: Evidence from the Sri Lankan manufacturing sector. NSBM Journal of Management, 1(1), 73. https://doi.org/https://doi.org/10.4038/nsbmjm.v1i1.5

- Wold, H. (1980). Model construction and evaluation when theoretical knowledge is scarce: Theory and application of partial least squares. In Evaluation of Econometric Models, 47–74.

- Zhu, Y. (2002). Economic reform and human resource management in Vietnam. Asia Pacific Business Review, 8(3), 115–135. https://doi.org/https://doi.org/10.1080/713999155

- Zor, U., Linder, S., & Endenich, C. (2018). CEO characteristics and budgeting practices in emerging market SMEs. Journal of Small Business Management, 57(2), 658–678. https://doi.org/https://doi.org/10.1111/jsbm.12438

- Zott, C., & Amit, R. (2008). The fit between product market strategy and business model: Implications for firm performance. Strategic Management Journal, 29(1), 1–26. https://doi.org/https://doi.org/10.1002/smj.642