Abstract

This study aimed to know the impact of management accounting systems on firm financial efficiency while considering the CEOs risk-taking propensity. The Data was collected with the help of a self-administered questionnaire-based survey from the manufacturing sector of India. Used purposive sampling technique to collect data from 338 respondents. Results have shown that the broad scope management accounting system and integrator’s impact is insignificant on firm financial efficiency. In contrast, the effects of timeline and aggregation are significant on firm financial efficiency. Simultaneously, the mediation of risk-taking propensity is significant in all the cases except for integrator and firm financial efficiency. The researcher has adopted the latest and useful tools and techniques for exploring the problem. This study is a valuable addition. It is practically inducing the higher management and CEOs to follow the high-risk and high return concept while implementing the organizations’ management accounting system. This study is also helpful for organisations that are willing to enhance financial efficiency by employing novel methods.

PUBLIC INTEREST STATEMENT

This study is conducted to understand what actually affects the financial effectiveness of the firm. There could be many factors as the previous study discussed. But this study provide new insights to reveal the relationship between Management accounting system and CEO; s Risk taking propensity with the financial soundness and effectiveness of the business or firm. It reveals very useful results which directly and indirectly affects not only firm performance but also internal structure of the business. It is conducted on the manufacturing sector of India. There is no doubt that management accounting systems play an essential role in converting the organisations’ strategies into their desired objectives. Therefore, the study is targeting the manufacturing sector of India for the purpose of finding out the impact of broad scope MAS, timeline, aggregation, and integrator on financial efficiency of the firms because, the financial efficiency has been targeted and the sector of India that is growing rapidly and significantly is the manufacturing sector.

1. Introduction

There is no doubt that management accounting systems (MAS) have played an essential role in converting the organisations’ strategies and goals into their desired objectives. This research has the aims to find out the impact of Broad scope MAS on Firm’s financial efficiency, to find out the impact of Timeline on Firm’s financial efficiency, to check out the impact of Aggregation on Firm’s financial efficiency, to assess the impact of Integrator on Firm’s financial efficiency and to find out the mediation of risk-taking propensity between Broad scope MAS, Timeline, Integrator, Aggregation and Firm’s financial efficiency.

2. Background

MAS is used by the organisations with the purpose to enhance the performance of the organisation and also to improve the quality of the system with all of the resources present inside and outside the business environment (Abernethy et al., Citation2015; Odar et al., Citation2015). Previous studies have explored how MAS impacts the performance and the outcomes in the organisations; however, not most of the studies have given importance to the variables involved in MAS that hold the unique characteristics that helped the organisation perform well and maintain the internal and external organisational environment.

A practical business environment is always considered a dynamic environment. Akbar et al. (Citation2017). The top management’s risk-taking ability depends entirely on the nature and the personal understating of returns because of risky decisions. A strong relationship between financial efficiency and risk-taking propensity as returns and risk-taking ability highly correlate positively. Studies established that high risks mostly result in high returns but require valuable individual decisions that are usually not easy to take. Managers feel helpless regarding tackling that uncertainties and risks. The managers’ efforts can minimise these risks but cannot eliminate them (Otley, Citation2016).

The study is targeting the manufacturing sector of India for the purpose of finding out the impact of broad scope MAS, timeline, aggregation, and integrator on financial efficiency of the firms because, the financial efficiency has been targeted and the sector of India that is growing rapidly and significantly is the manufacturing sector. Significant inflows of the foreign direct investment have also been seen in this sector, that is why it is appropriate to select this sector for measuring the financial efficiency, in terms of timeline, aggregation, integrator and broad scope MAS.

Moreover, quantitative method of research has been adopted for this research because the researcher was interested in conducting the research based on primary data and to focus on current situations of the manufacturing sector of India in terms of financial efficiency. Moreover, another aim of the researcher was to find out the impacts that broad scope MAS can have won the financial efficiency of the organizations in the manufacturing sector of India, so the researcher preferred to find out current situations of the sector, in order to recommend new forms and strategies that should be implemented for the purpose of enhancing the financial efficiency of the organizations positively and significantly.

Another important reason of selecting quantitative methodology of study conducting the study on the manufacturing sector of India was that the researcher wanted to get an insight of the policies and procedures of the manufacturing organizations of India currently. So that it can be made sure that the recommendations that the study is providing, or the context of the research completely resonate with the needs and limitations of the manufacturing sector of India, in terms of financial efficiency of the organizations.

2.1. Problem statement

Most of the time, managers intend to minimise or avoid the risk at their level best to make the decisions while balancing the uncertainty in the decision-making process. With the presence of uncertainty and risk in decision-making, especially when it comes to practical business scenarios, researchers agreed that the factor of risk is high (Andersén & Samuelsson, Citation2016). there is also a need for a more elevated amount of information. Information processing systems help managers to make the decision-making process fast, reliable, and profitable. To correctly manage the bulk of information and process, MAS becomes compulsory and different measures are required to integrate processing, implementation, and results. Therefore, it is crucial to know the impact of different MAS on the managers’ and CEOs’ risk-taking propensity (RTP). Hence, It is essential to understand the impacts of the firm’s financial efficiency (FE) and its factors responsible for affecting it (Arena et al., Citation2018).

2.2. Justifications and rationale

Although most of the studies have gone through the factor of how the higher authorities’ RTP can impact the FE of a firm, still, this topic studied under the influence of the strategic management field only; however, it is a psychological characteristic which is found in the CEOs, managers, and the higher authorities. This factor has not been given equal importance as other factors and is also undermined when it comes to accounting (Shahzadi et al., Citation2018; Shields & Shelleman, Citation2016). The higher authorities’ RTP lacks research and proper consideration for accounting, which excludes the MAS. Studies focused that if accounting and MAS are considering while researching the higher authorities’ RTP, it might result in tremendous success. However, studies have not focused on MAS dimensions. The survey (Buckley et al., Citation2018) focused on studying CEOs’ RTP’s impact on the firm FE. Still, the study also skipped the MAS and the accounting field’s role between these (Taylor & Scapens, Citation2016).

2.3. Research objectives

Following are the objectives of this research:

To find out the impact of Broad scope MAS on Firm’s financial efficiency.

To find out the impact of Timeline on Firm’s financial efficiency.

To find out the impact of Aggregation on Firm’s financial efficiency.

To find out the impact of Integrator on Firm’s financial efficiency.

To check the mediation of risk-taking propensity between Broad scope MAS, Timeline, Integrator, Aggregation and Firm’s financial efficiency.

2.4. Research questions

Following are the Questions of this research:

What is the impact of Broad scope MAS on Firm’s financial efficiency?

What is the impact of Timeline on Firm’s financial efficiency?

What is the impact of Aggregation on Firm’s financial efficiency?

What is the impact of Integrator on Firm’s financial efficiency?

What is the mediation of risk-taking propensity between Broad scope MAS, Timeline, Integrator, Aggregation and Firm’s financial efficiency?

2.5. Research significance

This study shows how vital MAS is to the organisation regarding RTP and increasing FE. This research aims to know the impact of broad scope MAS (BS-MAS), timeline (TI), aggregation (AG), and integrator (IN) on the financial efficiency (FE) of the firm. Moreover, to know about the mediating impact of RTP between these variables. The current study significantly contributes to the literature in management accounting. This study is the first study that considers the relationship between RTP and firm FE while considering BS-MAS’s dimensions. Previous studies were too vague regarding the topic under investigation. The current research will transparently exaggerate how RTP can be triggered with efficient BS-MAS and its dimensions. This study will also help firms consider and restructure their policies and regulations to consider MAS and measurements to enhance firm FE and enhance the RTP. The research has significant contributions to the literature for addressing the naive factor of broad scope MAS. Moreover, it has significantly also related the factor with financial efficiency of the firms. the research has considered factors like integrator, aggregation, and timeline in relationship with financial efficiency of the firms, which have not been considered in almost any previous studies. This study will also be contributing to the improvement in the policies and regulations of the manufacturing sector of India, by recommending sufficient and suitable strategies, for the improvement of the financial efficiency of the manufacturing sector of India.

2.6. Research structure

First section comprises of the introduction, background, problem statement, justifications and rationale, objectives, research questions, and research significance. The next section of the study is a literature review. The 3rd section is a research methodology. The 4th section consists of data analysis and interpretation, followed by the last section of the study, discussion, and conclusion.

3. Theoretical literature review and hypothesis development

3.1. Upper echelons theory (UET)

Hambrick and mason introduced the upper echelons theory. It was put forward to explain the aspects of a person’s nature, such as the factors involving demographic or psychological factors that can impact that person’s decisions. This was mainly used to observe the upper management and senior managers (Colombelli, Citation2015). In this theory, MAS was taken as administrative complexity. It was observed that these kinds of complexities could impact that scene, making power off the senior management. It was established that there is a need for proper information collecting and processing tools so that the dynamic internal and external environment will not impact the decision-making power of the senior management (Faccio et al., Citation2016). The theory also discussed certain internal aspects of an organisation and certain aspects from an organisation’s environment that impact senior managers’ decision-making and RTP. This theory ignored the field of accounting hugely. The study is being carried out based on this theory’s central idea (Gamache & McNamara, Citation2019).

3.2. Broad scope MAS and firm financial efficiency

Broad scope MAS consists of the internal, external, quantitative, qualitative, financial, non-financial, history and future-oriented data, which help firms’ management better cope with uncertain and risk-related situations. An organisation’s FE is crucial as it will keep the organisation running on for an extended period. Without FE, there will be no financial backup present to back up its operation anymore. While it is being studied, there is a study of (Gan, Citation2019) which imposes the fact that whenever there is a situation of uncertainty or risk regarding any financial decisions that can impact the FE, an abundant amount of information must be present with the senior managers and CEOs while the decisions to be made. The MAS helps the organisations, and the managers make decisions that can ensure long-term profitability and financial stability.

The MAS is accounting for several aspects of an organisation according to the study (García-Granero et al., Citation2015) even the functions of financial accounting are baseless and not worth making the decisions, as (García-Granero et al., Citation2015) elaborated that when the financial position is reported through financial accounting the MAS help to decide different budgets, decide about the coordination and control of further economic activities and also coordinate the decisions regarding other business plans based on the efficiently done financial forecasting. Moreover, when it comes to cost accounting operations and reporting, quality decisions are made after the analysis of cost accounting reports (Hanousek et al., Citation2019). Business problems are solved so that the business is run with an adequate amount of liquidity present, and there are no loopholes when it comes to the firm’s financial decisions and FE. The study of Abdusalomova (Citation2019) proposes that there is a significant impact of broad scope MAS on the financial efficiency of the organizations, the study has proposed a positive and a significant impact. Moreover, based on the manufacturing sector of India, and the extent to which technology and latest tools and techniques are significantly being implemented in India, broad scope MAS is proposed to have significant impacts in making the financial efficiency of the organizations sustainable and effective. So, it can be proposed that,

Hypothesis H1: The impact of BS-MAS is significant on firm FE.

3.3. Aggregation and firm financial efficiency

According to the study (Hoskisson et al., Citation2017), when it comes to aggregation in MAS, it is followed by data collection from all individuals of financial accounts and store in a single place (Josef et al., Citation2016). This process’s primary purpose is to list all the account holders’ financial information centralised, safe, and secure, helping maintain the financial information, thus helping the managers and the organisation take significant finance-related decisions. Moreover, this will not only help the organisation in collecting and placing the data from a single financial institution, but it also helps them in data aggregation from multiple institutions creating a bank of information that can significantly and profitably back up all the financial decisions enhancing the financial efficiency of a firm (Kraiczy et al., Citation2015). The study of Ahmad (Citation2017) has proposed positive and significant impact of aggregation on the financial efficiency of the organizations. Moreover, the study of Antoncic et al. (Citation2018) also has proposed significant impact of aggregation on the firm financial efficiency, but the direction of relationship has not been specified. So, the second hypothesis can be proposed as,

Hypothesis H2: The impact of AG on firm FE is significant.

3.4. Timeline and firm financial efficiency

The MAS uses internal systems and timelines that an organisation utilises to measure and evaluate its ongoing processes for making significant and long-lasting decisions for the organisation (Kraiczy et al., Citation2015). The management requires this information of the organisation to enhance the organisation’s overall efficiency. In the researcher’s study, systematic timelines are required by the higher authorities and management of the organisations to ensure that the general decisions and the finance-specific decisions are made to enhance the firm’s efficiency (Krause and Tse (Citation2016). According to the research done by Ahmad (Citation2017), timeline plays a very significant role in enhancing the financial efficiency of the organizations, the study has proposed a positive and significant impact of timeline on the financial efficiency of the organizations. Moreover, it can also be proposed to that in the case of manufacturing sector of India, time London play a very significant role in enhancing and sustaining the financial efficiency of the organizations. Moreover, to increase the firm’s profitability of operations effectively (Laufs et al., Citation2016). So, it can be proposed that,

Hypothesis (H3): The impact of TI on firm FE is significant.

3.5. Integrator and firm financial efficiency

Studies show that integration is the most crucial factor in the integrity and overall connexion of the data and results (Li et al., Citation2015). The integrators help the MAS to connect all kinds of accounting applications and functions. This helps the firm enhance its operations’ efficiency and help the organisations enhance their FE. All of the information is connected and related to each other, making the analysis much more effective and accurate (Liem et al., Citation2020). These integrators help organisations take all kinds of accounting and financial decisions with a high accuracy level and undoubtedly result in profitable real-time results (Mata et al., Citation2016). According to the study of Ahmad (Citation2017), there is a significant impact of integrator on the financial efficiency of the organizations, however yet there are some conflicts according to the study of Azudin and Mansor (Citation2018), which do not propose a significant and direct impact of integrator on the financial efficiency of the organizations. Such type of systems is free of any potential human errors, so it can be hypothesised that,

Hypothesis (H4): The impact of IN on firm FE is significant.

3.6. Risk-taking Propensity and Financial Efficiency

The managerial and entrepreneurial literature mostly considers risk-taking a vital step to distinguish a person from being a manager to being a leader or owner. According to (Naseem et al., Citation2019) RTP measures a person’s orientation towards taking the risk and measures his willingness and ability to deal with risk-related situations. Moreover, several studies have been done on the RTP of the CEOs and the entrepreneurs, all of which have significantly and collectively concluded that the efficiency and the success of an organisation lie in the ability of its owners and CEOs to get their selves into highly risky situations that will bring out high returns (Ndofor et al., Citation2015). Risk taking propensity has a significant impact on the financial efficiency of the organizations, according to Dong et al. (Citation2017) higher risks lead to higher returns and financial efficiency but at the same time the risk of loss is high as well. Moreover, according to the study of Baixauli-Soler et al. (Citation2015) risk taking propensity also does not have significant level of sustainability, but the impacts on financial efficiency are significant. It has been proven by past studies again and again that higher RTP results in higher firm FE, and it has also been found that such firms take their leaps towards success far before the others (Opper et al., Citation2017). So, it can be hypothesised that.

Hypothesis (H5): The impact of RTP on a firm’s FE is significant.

3.7. MAS, TI, AG, IN, RTP and FE

Previous studies show the significant relationship between broad scope MAS and firm FE. However, the study conducted by Indriani and Nadirsyah (Citation2015) implies that the mediation RTP enhances the chances of higher returns. The significant and positive impact of broad scope MAS can be obtained firm financial efficiency. The integrator factor acts as an essential element for the incorporation of operations of the organisation. The study of Indriani and Nadirsyah (Citation2015) suggested that an integrator, when associated with an organisation’s RTP managers, results in a higher efficiency level. Moreover, when it comes to the financial and accounting aspect of the organisations, TI of the operations and AG are two significant factors, according to Ghasemi et al. (Citation2016), RTP positively aligned with the result in positive enhancement of the firm’s financial efficiency. The study of Ismail et al. (Citation2018) has also suggested a significant RTP enhances the firm’s financial efficiency by implementing broad scope MAS. The mediation of risk-taking propensity has been found to be significant for the enhancement of financial efficiency of the organizations, Gaganis et al. (Citation2019) also proposes that there is a significant and positive role of risk-taking propensity in enhancing the financial efficiency of the organizations. Moreover, the study of Faccio et al. (Citation2016) proposes that the impact of risk-taking propensity on firm financial efficiency is significant. With the review of previous literature, the following hypotheses are formulated:

H6: The mediating role of risk-taking propensity between broad scope mas and firm financial efficiency is significant.

H7: The mediating role of risk-taking propensity between timeline and firm financial efficiency is significant.

H8: The mediating role of risk-taking propensity between aggregation and firm financial efficiency is significant.

H9: The mediating role of risk-taking propensity between an integrator and firm financial efficiency is significant.

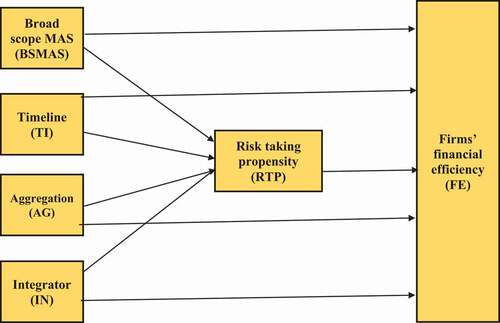

represents the developed theoretical framework of this study. There are four independent variables: Broad scope MAS, TI, AG, and IN. RTP is taken as a mediating variable, and the Firm’s FE is taken as a dependent variable. The impact of independent variables is checked on the dependent variable directly. Moreover, the impact of independent variables on the dependent variable is also checked through the mediator. The study of García-Granero et al. (Citation2015) significantly points out that developed technology and usage of latest tools and techniques enhance the financial efficiency of the organizations, it has also been proposed by the study that there is a very significant role of integrator in building up sustainable and efficient financial position of an organization. According to the study of Jamil et al. (Citation2015), there is a significant and positive impact of broad scope MAS on the financial efficiency of the organizations. Moreover, the study has also presented risk taking propensity as a major factor in contributing to the enhancement of financial efficiency of the organizations. The study of several other researchers as well, resonate with the fact that there is a positive and significant impact of broad scope MAS on the financial efficiency of the organizations (Joshi & Li, Citation2016). It has been observed by several researchers that there exists significant relationship between this taking propensity and financial efficiency of the organizations, and for most of the times, it has been observed that higher risks result in higher level of returns, thus enhancing the financial efficiency of the organizations.

Figure 1. The theoretical framework of the study

4. Empirical literature review

The study of Appelbaum et al. (Citation2017) has focused on the relationship between broad scope MAS and from financial efficiency, it has been found out that there is a significant impact of broad scope MAS on the financial efficiency of the organization. Moreover, the mediation of risk-taking propensity has been studied in relationship with organization’s financial efficiency and broad scope MAS, it has been concluded in the research that risk taking propensity enhances the level of returns for the organizations, it has also been observed that risk taking propensity also enhances the risk of loss, but Ghasemi et al. (Citation2016) has proposed the results in relationship with high-risk, high return principle.

The study of Krahel and Titera (Citation2015) has applied the dimensions of timeline, and aggregation for finding out the impact of these dimensions on organization’s financial efficiency, it has been found out that there is a significant impact of these factors and their dimensions on the financial efficiency of an organization. The study of Nguyen et al. (Citation2017) has proposed significant and positive impacts of broad scope MAS on the financial efficiency of the organizations, moreover it has also proposed that risk taking propensity enhances the financial efficiency of the organizations in most of the cases. the study of Tuan et al. (Citation2016) also alliance with the previous study and proposes that there is a significant and positive impact of broad scope MAS on the financial efficiency of the organizations.

5. Research design

As suggested by the previous studies, The researcher has used the quantitative research methodology to determine the impacts of MAS dimensions on its FE. This method has helped the researcher to quantify the results and analyze them in a better way (Albashabsheh et al., Citation2018; Husain & Javed, Citation2019; Javed et al., Citation2019; Javed, Husain et al., Citation2020; Javed, Khan et al., Citation2020; Javed, Malik et al., Citation2020; Khan et al., Citation2017; Khan & Javed, Citation2016; Malik et al., Citation2020). The researcher has used the deductive approach two develop the hypothesis; the researcher has concluded results that will generally be applied to the entire population (Javed, Citation2017) . The researcher has worked on this research with the help of positivist philosophy through which the results have been concluded with the help of factual knowledge and observations made. This study was a cross-sectional study, as the data was collected only one time (Alhroob et al., Citation2017; Farrukh et al., Citation2021; Javed & Husain, Citation2021; Javed & Khan, Citation2017; Javed; Javed, Malik et al., Citation2020; Khan et al., Citation2017)

5.1. Research population and sample

The population for this research was the manufacturing sector of India. The Indian manufacturing sector is growing fast, and several manufacturing companies get initiated through local investment and foreign direct investment in the manufacturing sector. Indian market is overgrowing. Competition within each industry is increasing very rapidly. The organizations need to survive in this competitive environment, but it has become almost impossible to operate in this environment without efficiently attaining it.

Moreover, almost no study in the past has considered RTP in the context of India. For the study, these variables on such a large-scale economy are preferred by the researcher. The researcher used the purposive sampling technique Otley (Citation2016) to take out an adequate sample from the population. The sampling frame was different manufacturing companies in India. Specifically, the manufacturing sector was targeted because the competition within this sector is increasing. The reason to select the Manufacturing sector of India is that no study was available that took the CEO risk variable related to the firm financial efficiency. In India, the manufacturing industry is growing too rapidly. Due to the increased competition, the firms can only survive by enhancing financial efficiency, so it has become essential to consider this aspect. The manufacturers are only focusing on enhancing the level of manufacturing by ignoring financial efficiency. Furthermore, the sampling unit was the CEOs of those manufacturing companies. The total participants verse 400 out of which 338 participants adequately responded to this research (See ).

Table 1. Population and sampling

5.2. Data collection method

The study was collected with the help of a self-administered questionnaire-based survey. The researcher got the questionnaires filled by the CEOs of the manufacturing firms on his own. All the ethical considerations were considered before the collection of data.

5.3. Data analysis method

The researcher uses the latest tools and techniques, contributing to this study’s novelty and authenticity. SPSS and AMOS have been used for data analysis, and later, the Structural Equation Modeling elaborates the direct and indirect impacts of the variables employed.

5.4. Description of variables

Broad scope MAS: The broad scope management accounting systems are the internal systems that are utilized for the purpose of providing critical information to the management, that can be utilized for the operational business decision making processes.

Firm financial efficiency: The firm financial efficiency refers to getting significant financial output from the same resources of the firm, these are measured with the help of efficiency ratios.

Timeline: Timeline represents a written period of time, which is usually a line, representing order in which different events will happen, that are related together.

Integrator: Integrator represents control applications and devices that perform mathematical integration functions.

Aggregation: Aggregation represents cluster of different things that have been put together, or the collection of related items or contents that are being utilized together.

Risk taking propensity: Risk taking propensity is defined as the orientation of a person to take risks, this is often judged by the personality of an individual.

5.5. Measures

For broad scope MAS, four items were taken and were taken from (Liem et al., Citation2020), which has been cited and adopted by previous researchers. For the timeline, four items were taken from (Ismail et al., Citation2018). For aggregation, four items were taken and were taken from (Liem et al., Citation2020); for the integrator, four items were taken and were taken from (Ghasemi et al., Citation2016). Four items were taken for risk-taking propensity and were taken from (Liem et al., Citation2020). Furthermore, four items were taken for firm financial efficiency and were taken (Liem et al., Citation2020).

6. Empirical results and discussion

6.1. Demographical details

The researcher aimed to see the relationship between broad scope MAS, TI, AG, IN, FE and RTP as a mediator between these variables. The collected Data was exposed to different analysis techniques to conclude the results. The sample selected demographics will be discussed in this section. It involved 338 participants in total, out of which 186 were males and 152 were females. 32.5% of the participants were of less than 25 years of age, 39.6% were of age between 25 to 35 years, 23.4% were of age between 35 to 45 years, and 15 individuals were of more than 45 years of age. 47 participants had fewer than two years, 147 individuals had an experience of 2 to 5 years, 113 individuals had 5 to 8 years, and 31 individuals had more than 8 years.

shows the validity and reliability of data to ensure that the Data is suitable for further testing. There is no outlier present in the data, and the data values are present between the valid minimum and maximum values of the five-point Likert’s’ scale. Moreover, the standard error value is low, showing that the difference between the sample and population mean is low. Low values of standard deviation show that the Data is valid enough to go on for further testing.

Table 2. Descriptive statistics

shows that KMO and Bartlett’s test shows the Data’s suitability. This test also shows the proportion of variance present among the variables because of some underlying factors. The value of 93.9% is showing that the factor analysis will be useful with the data. Moreover, the significant value of Bartlett’s test of sphericity shows the significance of factor analysis.

Table 3. KMO and bartlett’s test

shows the estimates of the correlations between all the variables. As the value of correlation for all variables is more than 70%, all variables have maximum loading in all variables. Hence, the model is adequate and reliable for further testing.

Table 4. Rotated component matrix

BSMAS = broad scope MAS, TI = Timeline, AG = Aggregation, IN = Integrator, FE = Financial Efficiency, RTP = Risk-Taking propensity.

is showing the results for convergent and discriminant validity; all the resultant values are more than 80%, which is a significant value, where convergent validity shows that how two measures are related, oppositely discriminant validity shows that how two measures that are not supposed to be related or unrelated. So, the results are showing this validity as all the values are above 80%.

Table 5. Convergent and discriminant validity

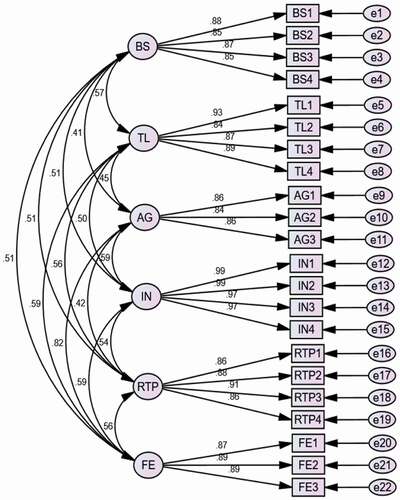

shows the model’s fitness level. CMIN’s value lies in the valid range because of being <3 (lesser than 3). GFI is also more than 0.80, a valid value IFI and CFI also have the value according to the threshold value. RMSEA is less than 0.08 lying in a valid range. A path analysis of CFA is given below as .

Figure 2. Confirmatory factor analysis

Table 6. Model fit indices

represents the confirmatory factor analysis, a graphical representation of cause and effect relationships between the variables, based on the theoretical background.

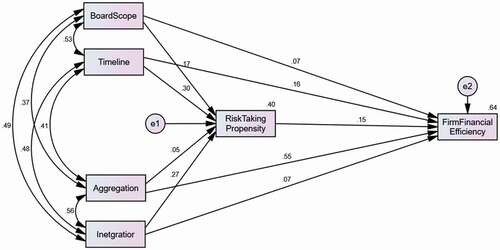

shows the exact impacts of the independent variables on the dependent variable. It can be seen from the table that the impact of BS-MAS is insignificant on firm FE as the p-value is more than 0.05. The p-value for TI’s impact on firm FE is less than .05, so the impact is significant. If the TI increases by 1%, firm FE will increase by 16%. Then aggregation will increase by 1%; firm FE will increase by 55.2%, whereas the impact of IN on firm FE is insignificant. RTP mediation between BS-MAS and firm FE is significant as it will increase the independent variable’s impact by 2.5%. RTP mediation between BS-MAS firm FE is significant, and the same is the case with AG and firm FE. At the same time, the mediation of RTP between IN and farm FE is insignificant. The loading of SEM is given below in .

Figure 3. Structure equational model

Table 7. Structural equation modeling

represents the path diagram extracted by performing structural equation modeling; the SEM diagram shows the assumed causal relations.

6.2. Discussion

This study aimed to know about MAS’s impact on firm FE with the mediation of RTP. The first hypothesis was rejected, and the same results have been backed up by the other survey (Park et al., Citation2016). The study has presented the idea that a broad-spectrum system of accounting and BS-MAS can enhance an organization’s financial section’s efficiency, positively impacting the whole organization. The second hypothesis that was proposed by the researcher was accepted as well. As aggregation helps in the decision-making process and enhances the operational and FE of a firm. The same results are backed up by the research work (Sekścińska et al., Citation2018). The third hypothesis was proposed, the results of this study have accepted this hypothesis, and the same idea has been backed up by a survey (Wang et al., Citation2016). This study’s fourth hypothesis has been rejected and provides the same findings (Chenhall & Moers, Citation2015). The results of this study also accepted the fifth hypothesis proposed by the researcher as RTP was seen to be a strong mediator and impact enhancer between BS-MAS and FE (Liem et al., Citation2020). This study’s results accepted the sixth hypothesis proposed by this research, and the same results are backed by a survey of (Chiarini & Vagnoni, Citation2015). This study’s results have accepted the seventh hypothesis proposed by the study, and the same results have been concluded by (Ghasemi et al., Citation2016). The researcher’s eighth hypothesis was rejected by this study’s results. There are several researchers that have proposed that there is a significant impact of this taking propensity on the financial efficiency of the organizations. Moreover the researchers have also supported the proposition that there is a significant impact of technological advancements and utilization of latest tools and techniques in enhancing the performance and financial efficiency of the organizations (Latan et al., Citation2018; Otley, Citation2016). The study of Tan and Anchor (Citation2017) proposes that there is a very significant impact of this taking propensity on the financial efficiency of the organizations, and the researcher proposes significant and positive impact of the variable on firm financial efficiency.

7. Summary and conclusion

7.1. Conclusion

In the study, the impact of Broad scope MAS, TI, AG, and IN is checked on the firm’s FE and RTP as a mediator. RTP mediation between IN and FE is observed to be insignificant, whereas BS and IN’s impact on FE is analyzed to be insignificant. However, it has been observed through the analysis that the impact of TI and AG on FE is significant. The mediation of RTP in BS, TI and AG is also observed to be significant. In conclusion, it can be established with this empirical and research-based evidence that Broad scope MAS cannot significantly impact firm FE. The impact of the IN is also insignificant on the firm FE. The mediating impact of RTP is also insignificant between the IN and firm FE. However, the evidence from different studies has shown that TI and AG’s impacts are significant on firm FE and positively influence RTP between BS-MAS, TI, AG, and firm FE.

7.1.1. Implications of the research

The research holds great significance in the theoretical-practical and policy-making sector; the researcher has addressed all the least-discussed variables in this research. There is a valuable addition of this study concerning adding research-based evidence regarding the impact of BS-MAS, IN, AG, and TI on firm FE. The study has also shed light on the impactful role of RTP as a mediator between these variables. Practically, going through this study, organizations can better focus on BS-MAS essential elements to improve their FE. This study will assist firms consider and restructure their policies and regulations to consider MAS and measurements to enhance firm FE and enhance the RTP. The research has significant contributions to the literature for addressing the naive factor of broad scope MAS. Moreover, it has significantly also related the factor with financial efficiency of the firms. the research has considered factors like integrator, aggregation, and timeline in relationship with financial efficiency of the firms, which have not been considered in almost any previous studies. This study will also be contributing to the improvement in the policies and regulations of the manufacturing sector of India, by recommending sufficient and suitable strategies, for the improvement of the financial efficiency of the manufacturing sector of India. Moreover, firms can also divide wise policies and industry-wise rules and regulations to help them upgrade and efficiently use their MAS for efficient and profitable accounting and financial systems.

7.1.2. Limitations and future research recommendations

Despite all the implications and useful contributions that this study has made, it has some drawbacks as well, which the researcher is mentioning so that future researchers can get over those drawbacks. According to the researcher, the first drawback is the small sample size and coverage of smaller area commander researchers who have only considered India’s manufacturing sector to have been done while considering several sectors, such as construction and mining sectors. The researcher also believes that because of time limitations, personal one-on-one interviews were not conducted. Still, the researcher proposes that future researchers consider researching with both the survey and the interviews.

Additional information

Funding

Notes on contributors

Sarfaraz Javed

Sarfaraz Javed has completed his education at Aligarh Muslim University, Aligarh, India. He is honoured with a laurel award winner from AMU. published 27+ research papers and articles, edited book, attended seminars and conferences, 20+ workshops, and motivational lectures for higher education international students. Presently, he is chief and Managing Editor of the International Journal of Economics Business and Human Behaviour (USA), His research focuses on corporate finance, intellectual capital, CSR, environmental, financial and Management accounting.

Mustafa Malik

Mustafa Malik is presently Assistant Professor of Management, Assistant Dean for Undergraduate Studies and Quality Management Officer in the College of Economics, Management and Information Systems, University of Nizwa, Oman. He has over 15 years of experience in teaching, research and academic administration. His research interests include tourism and community development, sustainability, organizational leadership, and quality management in higher education. He has published in several international journals and completed two funded research projects. Presently he is working on a funded research project on sustainability of heritage sites in Oman.

References

- Abdusalomova, N. (2019). Principles of ties of internal control and management accounting systems at the enterprises of black metallurgy. Архив Научных Исследований, (2). https://doi.org/https://dx.doi.org/10.15863/TA.

- Abernethy, M. A., Kuang, Y. F., & Qin, B. (2015). The influence of CEO power on compensation contract design. The Accounting Review, 90(4), 1265–17. https://doi.org/https://doi.org/10.2308/accr-50971

- Ahmad, K. (2017). The implementation of management accounting practice and its relationship with performance in small and medium enterprises sector. International Review of Management and Marketing, 7(1), 342-353. https://econjournals.com/index.php/irmm/article/view/3394

- Akbar, S., Kharabsheh, B., Poletti-Hughes, J., & Shah, S. Z. A. (2017). Board structure and corporate risk taking in the UK financial sector. International Review of Financial Analysis, 50, 101–110. https://doi.org/https://doi.org/10.1016/j.irfa.2017.02.001

- Albashabsheh, A., Alhroob, M., Irbihat, B., & Javed, S. (2018). Impact of accounting information system in reducing costing in Jordanian banks. International Journal of Research Granthaalayah, 6(7), 210–215. https://doi.org/https://doi.org/10.5281/zenodo.1336672

- Alhroob, M., Irbihat, B., Albashabsheh, A., & Javed, S. (2017). Does corporate governance create volatility in performance? International Journal of Informative & Futuristic Research, 4 (7), 6859–6866. http://www.ijifr.com/pdfsave/01-04-2017495IJIFR-V4-E7-075.pdf

- Andersén, J., & Samuelsson, J. (2016). Resource organization and firm performance: How entrepreneurial orientation and management accounting influence the profitability of growing and non-growing SMEs. International Journal of Entrepreneurial Behaviour & Research, 22(4), 466–484. https://doi.org/https://doi.org/10.1108/IJEBR-11-2015-0250

- Antoncic, J. A., Antoncic, B., Gantar, M., Hisrich, R. D., Marks, L. J., Bachkirov, A. A., Coelho, A., Polzin, P., Borges, J. L., Coelho, A., & Kakkonen, M.-L. (2018). Risk-taking propensity and entrepreneurship: The role of power distance. Journal of Enterprising Culture, 26(1), 1–26. https://doi.org/https://doi.org/10.1142/S0218495818500012

- Appelbaum, D., Kogan, A., Vasarhelyi, M., & Yan, Z. (2017). Impact of business analytics and enterprise systems on managerial accounting. International Journal of Accounting Information Systems, 25, 29–44. https://doi.org/https://doi.org/10.1016/j.accinf.2017.03.003

- Arena, C., Michelon, G., & Trojanowski, G. (2018). Big egos can be green: A study of CEO hubris and environmental innovation. British Journal of Management, 29(2), 316–336. https://doi.org/https://doi.org/10.1111/1467-8551.12250

- Azudin, A., & Mansor, N. (2018). Management accounting practices of SMEs: The impact of organizational DNA, business potential and operational technology. Asia Pacific Management Review, 23(3), 222–226. https://doi.org/https://doi.org/10.1016/j.apmrv.2017.07.014

- Baixauli-Soler, J. S., Belda-Ruiz, M., & Sanchez-Marin, G. (2015). Executive stock options, gender diversity in the top management team, and firm risk taking. Journal of Business Research, 68(2), 451–463. https://doi.org/https://doi.org/10.1016/j.jbusres.2014.06.003

- Buckley, P. J., Chen, L., Clegg, L. J., & Voss, H. (2018). Risk propensity in the foreign direct investment location decision of emerging multinationals. Journal of International Business Studies, 49(2), 153–171. https://doi.org/https://doi.org/10.1057/s41267-017-0126-4

- Chenhall, R. H., & Moers, F. (2015). The role of innovation in the evolution of management accounting and its Integration into management control. Accounting, Organizations and Society, 47, 1–13. https://doi.org/https://doi.org/10.1016/j.aos.2015.10.002

- Chiarini, A., & Vagnoni, E. (2015). World-class manufacturing by fiat. comparison with Toyota production system from a strategic management, management accounting, operations management and performance measurement dimension. International Journal of Production Research, 53(2), 590–606. https://doi.org/https://doi.org/10.1080/00207543.2014.958596

- Colombelli, A. (2015). Top management team characteristics and firm growth. International Journal of Entrepreneurial Behavior & Research, 21(1), 107–127. https://doi.org/https://doi.org/10.1108/IJEBR-10-2013-0181

- Dong, Y., Girardone, C., & Kuo, J.-M. (2017). Governance, efficiency and risk taking in Chinese banking. The British Accounting Review, 49(2), 211–229. https://doi.org/https://doi.org/10.1016/j.bar.2016.08.001

- Faccio, M., Marchica, M.-T., & Mura, R. (2016). CEO gender, corporate risk-taking, and the efficiency of capital allocation. Journal of Corporate Finance, 39, 193–209. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2016.02.008

- Farrukh, M., Javed, S., Javed, S., & Lee, J. W. C. (2021). Twenty years of green innovation research: Trends and way forward. World Journal of Entrepreneurship, Management and Sustainable Development, Ahead-of-p(ahead-of-print), ahead-of-print(ahead–of–print). https://doi.org/https://doi.org/10.1108/WJEMSD-06-2020-0068

- Gaganis, C., Hasan, I., Papadimitri, P., & Tasiou, M. (2019). National culture and risk-taking: Evidence from the insurance industry. Journal of Business Research, 97, 104–116. https://doi.org/https://doi.org/10.1016/j.jbusres.2018.12.037

- Gamache, D. L., & McNamara, G. (2019). Responding to bad press: How CEO temporal focus influences the sensitivity to negative media coverage of acquisitions. Academy of Management Journal, 62(3), 918–943. https://doi.org/https://doi.org/10.5465/amj.2017.0526

- Gan, H. (2019). Does CEO managerial ability matter? Evidence from corporate investment efficiency. Review of Quantitative Finance and Accounting, 52(4), 1085–1118. https://doi.org/https://doi.org/10.1007/s11156-018-0737-2

- García-Granero, A., Llopis, Ó., Fernández-Mesa, A., & Alegre, J. (2015). Unraveling the link between managerial risk-taking and innovation: The mediating role of a risk-taking climate. Journal of Business Research, 68(5), 1094–1104. https://doi.org/https://doi.org/10.1016/j.jbusres.2014.10.012

- Ghasemi, R., Mohamad, N. A., Karami, M., Bajuri, N. H., & Asgharizade, E. (2016). The mediating effect of management accounting system on the relationship between competition and managerial performance. International Journal of Accounting and Information Management, 24(3), 272–295. https://doi.org/https://doi.org/10.1108/IJAIM-05-2015-0030

- Hanousek, J., Shamshur, A., & Tresl, J. (2019). Firm efficiency, foreign ownership and CEO gender in corrupt environments. Journal of Corporate Finance, 59, 344–360. https://doi.org/https://doi.org/10.1016/j.jcorpfin.2017.06.008

- Hoskisson, R. E., Chirico, F., Zyung, J., & Gambeta, E. (2017). Managerial risk taking: A multitheoretical review and future research agenda. Journal of Management, 43(1), 137–169. https://doi.org/https://doi.org/10.1177/0149206316671583

- Husain, U., & Javed, S. (2019). Impact of climate change on agriculture and Indian economy : A quantitative research perspective from 1980 to 2016. Industrial Engineering & Management, 8 (2), 2–5. https://www.hilarispublisher.com/open-access/impact-of-climate-change-on-agriculture-and-indian-economy-a-quantitative-research-perspective-from-1980-to-2016.pdf

- Indriani, M., & Nadirsyah, N. (2015). Interaction effect of budgetary participation and management accounting system on managerial performance: Evidence from Indonesia. Global Journal of Business Research, 9(1), 1–13. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2654399

- Ismail, K., Isa, C. R., & Mia, L. (2018). Market competition, lean manufacturing practices and the role of management accounting systems (MAS) information. Jurnal Pengurusan (UKM Journal of Management), 52. https://doi.org/https://doi.org/10.17576/pengurusan-2018-52-04

- Jamil, C. Z. M., Mohamed, R., Muhammad, F., & Ali, A. (2015). Environmental management accounting practices in small medium manufacturing firms. Procedia-Social and Behavioral Sciences, 172, 619–626. https://doi.org/https://doi.org/10.1016/j.sbspro.2015.01.411

- Javed, S. (2017). Unified Theory Of Acceptance And Use Of Technology (UTAUT) model-mobile banking. Journal of Internet Banking and Commerce, 22 (3), 1–20. https://www.icommercecentral.com/open-access/unified-theory-of-acceptance-and-use-of-technology-utaut-modelmobile-banking.php?aid=86597

- Javed, S., Atallah, B., Aldalaien, E., & Husain, U. (2019). Performance of venture capital firms in UK : Quantitative research approach of 20 UK venture capitals. Middle-East Journal of Scientific Research, 27(5), 432–438. https://doi.org/https://doi.org/10.5829/idosi.mejsr.2019.432.438

- Javed, S., & Husain, U. (2021). Corporate CSR practices and corporate performance: Managerial implications for sustainable development. DECISION, 1-12. https://doi.org/https://doi.org/10.1007/s40622-021-00274-w

- Javed, S., Husain, U., & Ali, S. (2020). Relevancy of investment decisions and consumption with asset pricing : GMM and CCAPM model approach. International Journal of Management, 11(8), 10–17. https://doi.org/https://doi.org/10.34218/IJM.11.8.2020.002

- Javed, S., & Khan, A. A. (2017). Analysing parsimonious model of OL and OE using SEM technique. International Journal of Applied Business and Economic Research, 15 (22), 685–712. https://serialsjournals.com/abstract/53799_sarfarz_and_azeem.pdf

- Javed, S., Khan, M. S., & Farooqi, A. R. (2020). Impact of population, trade openess, education, life expectancy and gross capital formation on the economy of Indian sub-continent. International Journal of Psychosocial Rehabilitation, 24(6), 8034–8044. https://doi.org/https://doi.org/10.37200/IJPR/V24I6/PR260811

- Javed, S., Malik, A., & Alharbi, M. M. H. (2020). The relevance of leadership styles and Islamic work ethics in managerial effectiveness. PSU Research Review, 4(3), 189–207. https://doi.org/https://doi.org/10.1108/PRR-03-2019-0007

- Josef, A. K., Richter, D., Samanez-Larkin, G. R., Wagner, G. G., Hertwig, R., & Mata, R. (2016). Stability and change in risk-taking propensity across the adult life span. Journal of Personality and Social Psychology, 111(3), 430. https://doi.org/https://doi.org/10.1037/pspp0000090

- Joshi, S., & Li, Y. (2016). What is corporate sustainability and how do firms practice it? A management accounting research perspective. Journal of Management Accounting Research, 28(2), 1–11. https://doi.org/https://doi.org/10.2308/jmar-10496

- Khan, A., Baseer, S., & Javed, S. (2017). Perception of students on usage of mobile data by K-mean clustering algorithm. International Journal of Advanced and Applied Sciences, 4(2), 17–21. https://doi.org/https://doi.org/10.21833/ijaas.2017.02.003

- Khan, A., & Javed, S. (2016). Determining factors responsible in shifting consumption of mobile data (2G to 3G). International Journal of Computer Applications, 155(14), 30–33. https://doi.org/https://doi.org/10.5120/ijca2016912452

- Krahel, J. P., & Titera, W. R. (2015). Consequences of big data and formalization on accounting and auditing standards. Accounting Horizons, 29(2), 409–422. https://doi.org/https://doi.org/10.2308/acch-51065

- Kraiczy, N. D., Hack, A., & Kellermanns, F. W. (2015). What makes a family firm innovative? CEO risk‐taking propensity and the organizational context of family firms. Journal of Product Innovation Management, 32(3), 334–348. https://doi.org/https://doi.org/10.1111/jpim.12203

- Krause, T. A., & Tse, Y. (2016). Risk management and firm value: Recent theory and evidence. International Journal of Accounting and Information Management, 24(1), 56–81. https://doi.org/https://doi.org/10.1108/IJAIM-05-2015-0027

- Latan, H., Jabbour, C. J. C., De Sousa Jabbour, A. B. L., Wamba, S. F., & Shahbaz, M. (2018). Effects of environmental strategy, environmental uncertainty and top management’s commitment on corporate environmental performance: The role of environmental management accounting. Journal of Cleaner Production, 180(10), 297–306. https://doi.org/https://doi.org/10.1016/j.jclepro.2018.01.106

- Laufs, K., Bembom, M., & Schwens, C. (2016). CEO characteristics and SME foreign market entry mode choice. International Marketing Review, 33(2), 246–275. https://doi.org/https://doi.org/10.1108/IMR-08-2014-0288

- Li, C.-R., Lin, C.-J., & Tien, Y.-H. (2015). CEO transformational leadership and top manager ambidexterity. Leadership & Organization Development Journal, 36(8), 927–954. https://doi.org/https://doi.org/10.1108/LODJ-03-2014-0054

- Liem, V. T., Hien, N. N., & Ntim, C. G. (2020). Exploring the impact of dynamic environment and CEO’s psychology characteristics on using management accounting system. Cogent Business & Management, 7(1), 1712768. https://doi.org/https://doi.org/10.1080/23311975.2020.1712768

- Malik, A., Khan, N., Faisal, S., Javed, S., & Faridi, M. (2020). An Investigation On Leadership Styles For The Business Productivity And Sustainability Of Small Medium Enterprises (SME’S). International Journal of Entrepreneurship, 24 (5), 1–10. https://www.abacademies.org/articles/an-investigation-on-leadership-styles-for-the-business-productivity-and-sustainability-of-small-medium-enterprises-smes-9845.html

- Mata, R., Josef, A. K., & Hertwig, R. (2016). Propensity for risk taking across the life span and around the globe. Psychological Science, 27(2), 231–243. https://doi.org/https://doi.org/10.1177/0956797615617811

- Naseem, M. A., Lin, J., Ur Rehman, R., Ahmad, M. I., & Ali, R. (2019). Does capital structure mediate the link between CEO characteristics and firm performance? Management Decision, 58(1), 164-181. https://doi.org/https://doi.org/10.1108/MD-05-2018-0594

- Ndofor, H. A., Wesley, C., & Priem, R. L. (2015). Providing CEOs with opportunities to cheat: The effects of complexity-based information asymmetries on financial reporting fraud. Journal of Management, 41(6), 1774–1797. https://doi.org/https://doi.org/10.1177/0149206312471395

- Nguyen, T. T., Mia, L., Winata, L., & Chong, V. K. (2017). Effect of transformational-leadership style and management control system on managerial performance. Journal of Business Research, 70, 202–213. https://doi.org/https://doi.org/10.1016/j.jbusres.2016.08.018

- Odar, M., Kavčič, S., & Jerman, M. (2015). The role of a management accounting system in the decision-making process: Evidence from a post-transition economy. Engineering Economics, 26(1), 84–92. https://doi.org/https://doi.org/10.5755/j01.ee.26.1.4873

- Opper, S., Nee, V., & Holm, H. J. (2017). Risk aversion and guanxi activities: A behavioral analysis of CEOs in China. Academy of Management Journal, 60(4), 1504–1530. https://doi.org/https://doi.org/10.5465/amj.2015.0355

- Otley, D. (2016). The contingency theory of management accounting and control: 1980–2014. Management Accounting Research, 31, 45–62. https://doi.org/https://doi.org/10.1016/j.mar.2016.02.001

- Park, K., Min, H., & Min, S. (2016). Inter-relationship among risk taking propensity, supply chain security practices, and supply chain disruption occurrence. Journal of Purchasing and Supply Management, 22(2), 120–130. https://doi.org/https://doi.org/10.1016/j.pursup.2015.12.001

- Sekścińska, K., Rudzinska-Wojciechowska, J., & Maison, D. A. (2018). Future and present hedonistic time perspectives and the propensity to take investment risks: The interplay between induced and chronic time perspectives. Frontiers in Psychology, 9, 920. https://doi.org/https://doi.org/10.3389/fpsyg.2018.00920

- Shahzadi, S., Khan, R., Toor, M., & Ul Haq, A. (2018). Impact of external and internal factors on management accounting practices: A study of Pakistan. Asian Journal of Accounting Research, 3(2), 211–223. https://doi.org/https://doi.org/10.1108/AJAR-08-2018-0023

- Shields, J., & Shelleman, J. M. (2016). Management accounting systems in micro-SMEs. Journal of Applied Management and Entrepreneurship, 21(1), 19. https://doi.org/https://doi.org/10.9774/GLEAF.3709.2016.ja.00004

- Tan, Y., & Anchor, J. (2017). The impacts of risk-taking behaviour and competition on technical efficiency: Evidence from the Chinese banking industry. Research in International Business and Finance, 41, 90–104. https://doi.org/https://doi.org/10.1016/j.ribaf.2017.04.026

- Taylor, L. C., & Scapens, R. W. (2016). The role of identity and image in shaping management accounting change. Accounting, Auditing & Accountability Journal, 29(6), 1075–1099. https://doi.org/https://doi.org/10.1108/AAAJ-10-2014-1835

- Tuan, N., Nhan, N., Giang, P., & Ngoc, N. (2016). The effects of innovation on firm performance of supporting industries in Hanoi, Vietnam. Journal of Industrial Engineering and Management, 9(2), 413–431. https://doi.org/https://doi.org/10.3926/jiem.1564

- Wang, C. M., Xu, B. B., Zhang, S. J., & Chen, Y. Q. (2016). Influence of personality and risk propensity on risk perception of Chinese construction project managers. International Journal of Project Management, 34(7), 1294–1304. https://doi.org/https://doi.org/10.1016/j.ijproman.2016.07.004