Abstract

There are many researches on different aspects of responsibility accounting system, but none of those researches has focused on the impact of responsibility accounting system on the performance of textile enterprises. The aim of this paper is to identify factors affecting the implementation of responsibility accounting and its effect on the performance of Vietnamese listed textile companies. Using the qualitative and quantitative methodology, qualitative method was used to prepare the questionnaire, while quantitative method was used to measure the scale and analyze the level of impact of each factor. Further, the study employs the Structural equation modeling (SEM) with AMOS—SPSS, results show that factors in the research model aside from measurement technology and level of competition had certain impacts, including the ability of accounting staffs (TDKT), the awareness of managers at different level (NTQL), the decentralization (PQQL), the reward systems (HTKT), and the forecast for responsibility centers (DTTT). In addition, the structural management (CCTC), the competitive strategy (CLCT), the competitive advantages (YTCT) and the responsibility centers’ reports (BCTT) that have greatly affected performance of listed firms. In addition, the implementation of responsibility accounting has the greatest effect on the performance of listed companies. In fact, the implementation of responsibility accounting changes by 1 point (level), it will increase/decrease the performance of listed companies by 0.409 points without considering the other factors

PUBLIC INTEREST STATEMENT

The aim of this paper is to identify factors affecting the implementation of responsibility accounting and its effect on the performance of Vietnamese-listed textile companies. Using the qualitative and quantitative methodology, and employing the Structural equation modeling (SEM) with AMOS—SPSS, results show that factors in the research model aside from measurement technology and level of competition had certain impacts, including the ability of accounting staffs, the awareness of managers at different level, the decentralization, the reward systems, and the forecast for responsibility centers. In addition, the structural management, the competitive strategy, the competitive advantages and the responsibility centers’ reports that have greatly affected performance of listed firms. In addition, the implementation of responsibility accounting has the greatest effect on the performance of listed companies. In fact, the implementation of responsibility accounting changes by 1 point (level), it will increase/decrease the performance of listed companies by 0.409 points without considering the other factors

1. Introduction

Economists stated that when Vietnam joined the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), textile industry is one of those industries that have many benefits along with downsides due to harsh competitions (MOIT, Citation2018). Therefore, the implementation of responsibility accounting plays a significant role in doing business, because responsibility accounting can provide managers with information that can help them make better business decisions. Additionally, responsibility accounting can also act as a tool to measure the efficiency and performance of departments in organizations. In order to grow and develop sustainably, managers need detailed information about costs and revenues from various departments, from which managers can construct and evaluate business plans, analyze errors and discrepancies to make long-term and short-term decisions.

Effective responsibility accounting systems should be able to clearly assign responsibilities to departments (Rugby, Citation2004). Delegation is the assignment of authority to managers based on their positions and responsibilities, which would allow managers to make decision within their departments, (Garrison et al., Citation2006) as well as measure actual results against plans (Horngren et al., Citation2005). Moreover, responsibility accounting is also an effective method to evaluate the performance of departments within an organization (Fowzia, Citation2011).

The target of responsibility accounting is to evaluate the relationship between managers’ activities and their effects. In order to achieve this target, two main tasks need to be executed: Firstly, responsibility accounting system needs to be designed to reflect the performance of a single department, product, and service, so that responsibility centers can be established within an organization. Secondly, all costs and revenues must be allocated to those responsibility centers for management purposes.

There are few researches on different aspects of responsibility accounting system as suggested in of Al- Htaybat & Alberti-Alhtaybat’s research (Citation2013) emphasized the significant impact of education and skill ability of accounting staffs and managers on the accounting process. In addition, Han (Citation2018) indicated that a firm should require its accounting to compete the transformation from the accounting to the management, therefore, the responsibility accounting is bound to boost the progress of the firm reform work. Another possibility, LE and BUI (Citation2020) responsibility accounting was not comprehensive in the institutions that are not financially anonymous, especially in the public universities. Totally, none of those researches has focused on the impact of responsibility accounting system on the performance of textile enterprises and to analyze the implementation of responsibility accounting system on the performance in an emerging economy. This is the existing gap that will be discussed in this study. In addition, in order for those textile enterprises to develop in a stable and sustainable way, managers require detailed and accurate information regarding costs and revenues generated by departments within the organization. Based on such information, managers can design plans and measure actual results against those plans to identify discrepancies, which could help managers make better short-term and long-term plans. Therefore, the topic of “Factor affecting the implementation of responsibility accounting on firm performance—empirical analysis of listed textile firms” is necessary as it can help textile companies identify factors affecting the implementation of responsibility accounting systems.

The remainder of this study is organized as follows: Section 2 depicts theoretical framework while data collection and methodology in Section 3. We have Section 4, and Section 5 for empirical results, and discussions. The conclusions and recommendation will be shown in Section 6.

2. Theoretical framework and literature review

As a basis for building research models, this study used the following theories: Management accounting theory, Contingency theory, Agency theory, and Sociological theory.

2.1. Management accounting theory

Management accounting theory is affected by the environment, society, ethics, and authority, which affects three important aspects of management accounting: planning, monitoring, and decision making. Al-Htaybat and Alberti-Alhtaybat (Citation2013) stated that management accounting theory was based on various other foundation theories regarding economic and social factors. According to this theory, the success of the implementation of management accounting system would depend on various factors, such as environment, technology, organizational size and structure, strategy, and national culture (Chenhall, Citation2003). Another important foundation theory is institutional theory, which reflects the interaction and changes in management accounting system under the influence of institutions and organizations. Such influence is compulsory, and necessary for organizations to reach their goals in many situations (Ma & Tayles, Citation2009). The foundation theory was also applied by Giddesn’s structuration theory. This theory examines the structure, rules, and resources of the society, as well as the relationship between those factors (Coad & Herbert, Citation2009). In order for management accounting to work properly, organizations need to rely on three main factors, which are Capacity, Target, and Social standards (Coad & Herbert). Simultaneously, Bourdieu’s theory of practice analyzes the interaction between organizations and individuals based on rules and standards of organizational goals and individual characteristics. Education and training have a significant impact on the skill level and awareness of individuals. Besides, some other theories were also applied to construct Management Accounting Theory, including Actor-Network theory—which reflects the relationship between factors in the accounting system, Theory of Communicative Action—which reflects the relationship between the economy, legality, and motivation to implement management accounting system (Haldma & Laats, Citation2002).

Management Accounting Theory was able to present a complete model of management accounting system using results of some previous important researches related to management accounting. This model could examine and evaluate important aspects of management accounting, including Budget, Performance Assessment, Authority, Strategy, Culture, Education, and Technology. The model could be demonstrated using the below :

Figure 1. Management accounting theory. Source: Al-Htaybat & Alberti-Alhtaybat (Citation2013)

indicates that management accounting has three main stages, including planning, monitoring, and decision making. Previous researches mainly focused on the technological aspect of management accounting while Al-Htaybat & Alberti-Alhtaybat (Citation2013) focused on management aspect with interaction based on external factors (environment, regulation system, etc.) and internal factors (organizational characteristics, organizational size, skill ability of accounting staffs, managers’ awareness, etc.). Further, planning is affected significantly by regulations and society factor. When managers of all level design budgeting plan, they need to consider all factors from internal factors, such as organizational targets, strategy, characteristics to external factors such as culture, society, environment, ethics, and economic conditions. Additionally, managers also need to pay attention to Risks, Technology, and Information system. These factors not only affect the Planning stage, but also Monitoring and Decision making. Adversely, the core value of Al-Htaybat & Alberti-Alhtaybat’s research (Citation2013) has been proposed, in which management accounting is examnined based on technological, managerial, and social perspectives. Al-Htaybat & Alberti- Alhtaybat (Citation2013) also emphasized a significant impact of education and skill ability of accounting staffs and managers on the accounting process.

In this paper, Management Accounting Theory reinforces views on the implementation of responsibility accounting system and the impact of planning and evaluation. Based on this foundation theory, several hypotheses were identified: (1) allocation of revenue and costs; (2) Forecasts for responsibility centers; (3) Responsibility centers’ reports; (4) Assess forecasts and reality; (5) Managers’ awareness; (6) Measurement technology; (7) Skill levels of accounting staffs that impact the implementation of responsibility accounting system. By utilizing this theory, the research can ensure both technological perspective and managerial perspective, from which managers can make decisions to establish and provide information on the organization’s performance by evaluating the organization’s results.

2.2. Contingency theory

Contingency theory was developed based on Organizational theory to define the best organizational structure for a certain situation (D.T. Otley, Citation1980; D. Otley, Citation2016). According to Elsayed and Hoque (Citation2010), effective management should be adjusted in accordance with the situations. Initially, Contingency theory was solely applied in researches on behaviors and managements with Fiedler’s model (Fiedler, Citation1964), which stated that managers’ styles are permanent habits and it would be really difficult for managers to attempt to change their styles. Fiedler’s model (Fiedler, Citation1964) was able to explain why managers may succeed in one particular situation but not in other situations. Managers may be successful when the situations suited their styles of management, or when the situations changed and fitted with their styles of management coincidentally.

Research conducted by Pennings (Citation1975) has opened up ways to apply contingency theory to researches on accounting, in which many researches on accounting, especially management accounting, has been published since 1970 (D.T. Otley, Citation1980). In addition, Pennings (Citation1975) suggested that authors could use contingency theory to identify factors affecting the efficiency of internal control systems depended on changes in the environment (both internal and external). According to D.T. Otley (Citation1980), accounting systems should be designed in accordance with the organization’s characteristics, since there was no accounting system that could be implemented by all types of organizations under every situation.

One of the first researches on contingency theory based on organizational behavior, Hopwood (Citation1976) evaluated the performance of low-level managers to top-level managers. However, results of those researches varied due to difference in sample size and geographical location. Another research that had gathered attentions of many researchers in management accounting field is environmental uncertainty because of several reasons: (1) organizational structures need to be flexible so that they can adapt to sudden changes in the environment due to the high level of uncertainty; (2) because of economic union, competition is becoming harsh, which leads to high level of uncertainty. This also suggests that small and medium enterprises are affected by the level of uncertainty. The next factor that needs to be considered is culture, including national culture and organizational culture. This factor would affect the behaviors of organizations, as well as employees within an organization. However, behaviors of top-level managers in an organization could be modified by training. Organizational culture is an indirect variable that shows certain degree of impact on organizational behaviors, and it could also control behaviors of employees in an organization (D. Otley, Citation2016). According to Rook and Fisher (Citation1995), organizational culture includes social norms, ethics, values, beliefs, and it could affect the behaviors of employees. An organization with strong organizational culture would have less demand for internal control, which would in turn impact the design of the accounting system.

Based on several researches that had applied contingency theory from 1980 to 2014, D. Otley (Citation2016) was able to identify factors affecting the implementation of accounting system: (1) independent variables include external and internal factors. Internal factors include organizational size, organizational structure, strategy, information system, rewards system, staffs, organizational culture, managers of all levels. Meanwhile, external factors include Technology, competition, national culture, level of uncertainty. (2) dependent variables include Accounting systems that ensure financial efficiency, Budget, Internal control, Effectiveness, Job satisfaction, Changes in operations, Organizational efficiency. Efficiency is the dependent variable of the implementation of accounting system in organization (D. Otley, Citation2016) and is the most widely used variable. Currently, the trend of many researchers is to study the relationship and interaction between factors to evaluate the effectiveness of the implementation of accounting systems instead of focusing on the relationship between a single independent variable and a dependent variable (D. Otley, Citation2016). According to D. Otley (Citation2016), the understanding of the coherence between several independent variables would explain the dependent variables better in analysis.

Contingency theory helps identify external and internal factors affecting different aspects of the implementation of accounting system. Based on this foundation, several internal factors were identified, which are (1) Awareness; (2) organizational size; (3) Rewards system; (4) organizational structure. Meanwhile, external factors were also pointed out: (1) Competitiveness; (2) level of competition; (3) Strategy. Those factors affect the implementation of accounting system as well as the performance of organizations. By applying contingency theory, it is possible to investigate several independent and dependent variables in a research model, which would result in a better overview of the impact.

2.3. Agency theory

Agency Theory suggests that there would be conflicts between shareholders and managers when the amount of provided information is insufficient, and asymmetrical. Agency relationship (or authorized relationship) is when shareholders (owners) appoint managers (agents) to manage the organization with the authority to make business-related decisions that would affect owners’ assets and properties (Jensen & Meckling, Citation1976). Agency theory is important as it contributed to the development of organizational theory; agency theory focuses on the relationship between owners and agents (Eisenhardt, Citation1989).

Agency theory states that when managers want to maximize their benefits in the relationship between shareholders and managers, they would not act on shareholders’ interests. In order to satisfy both sides, good reward systems could be employed to decrease the conflicts between shareholders and managers; internal control systems should also be established to limit unethical behaviors and decisions made by managers. Agency relationship is also shown in the relationship between top-level managers and low-level managers in the hierarchy, as well as between managers and individuals who employ the organizations’ resources. According to Healy and Palepu (Citation2001), in order to reduce the amount of conflicts between managers and shareholders, it would be wise to engage in contracts regarding remunerations and bonus for managers. Agency theory also explains the reasons to implement responsibility accounting in enterprises, and the type of information that listed companies should provide to ensure the benefits of shareholders and investors. Agency theory also acts as a foundation theory to construct internal reports and responsibility reports in accordance with the organizational hierarchy. Agency theory affects the establish and provision of information on organizational structure and hierarchy, which are important for the establishment of responsibility accounting system. From this, researchers can conduct in-depth study on several factors, such as organizational size and structure, level of management.

2.4. Sociological theory

Sociological Theory focuses on how organizations are established through the interaction between people, organizations, and society. According to Covaleski et al. (Citation1996) behaviors that are in accordance with social norms would result in the optimum productivity. Sociological theorists examined management accounting system from a social perspective instead of technological perspective to make internal decision to improve organization’s performance. Wildavsky and Caiden (Citation2004) argued that the budget system could also be used to establish and maintain political relationship in the complexity of the society. Further, Hopper and Armstrong (Citation1991), Oakes and Covaleski (Citation1994) all argued that management accounting and cost information could be employed to maximized productivity.

Sociological theory suggested that management accounting systems were affected not only by internal factors but also by external factors, such as policies and labor regulations. Therefore, organizational goals should be in line with social benefits. For example, remuneration policies and reward systems should follow government policies. Sociological Theory also explains behaviors of the working class in the relationship between them and managers. This theory provides information related to factors affecting the behaviors of the working class in the organization’s responsibility accounting system. Based on this, researchers who study the implementation of responsibility accounting system can focus on the Reward System factor.

2.5. Responsibility accounting

Responsibility accounting is a system that involves collecting results from individuals and departments to analyze and evaluate the efficiency of those individuals and departments. Responsibility accounting is a system that specializes in collecting, analyzing, and transferring information under the responsibility of managers. According to Higgins (Citation1952), responsibility accounting is an accounting system designed to control costs associated to individuals who are in charge of management within an organization. Atkinson et al. (Citation2001) stated that responsibility accounting is an accounting system that can collect, summarize, and report all accounting information related to associated tasks of each manager in one organization. The system can provide information regarding costs and revenues generated by each responsibility center to evaluate the responsibility and performance of managers.

2.6. Performance

The performance is one important aspect of management accounting in general, and, more specifically, responsibility accounting. According to Santos and Brito (Citation2012), performance is measured using 3 main factors: profitability, growth rate, and market value of the enterprise. Barney (Citation2011) stated that even though the performance of a company, which is shown through financial reports and figures, is really important to stakeholders, the available information is often insufficient, and untransparent to emphasize the role and needs of stakeholders. Therefore, it is necessary to measure and report the performance of companies using detailed financial ratios and information. Santos and Brito (Citation2012) suggested some benchmarks to measure the performance of enterprises. Firstly, profitability, reflected by several ratios of financial performance as return on assets (ROA), return on equity (ROE), return on scale (ROS). Secondly, growth rate, reflected by several ratios: Asset growth, Equity growth, Gross Profit growth.

3. Data and methodology

3.1. Data

Data collection and analysis are important stages in qualitative researches (Marshall & Rossman, Citation1989; Merriam, Citation1988). According to Dao et al. (Citation2021), sample is not selected using statistical approach; instead, it is selected to construct theory or theoretical approach. Candidates for the sample are experts in the field of management accounting or responsibility accounting, such as Professors, Associated Professors, Doctor of Philosophy, and managers such as Chief Accountants, General Accountants, Heads of departments, and accounting staffs. Opinions and perspectives of those experts can be used to explore factors affecting the implementation of responsibility accounting system in listed textile enterprises in Vietnam. In addition, candidates for In-depth Interviews are top-level managers, such as Chairman of the Board of Management, Members of the Board of Management, Presidents, Directors, Chief Accountants, General Accountants, Heads of departments, and staffs who have deep understanding about management accounting and responsibility accounting

According to Tabachnick and Fidell (Citation2007), Tran and Foroudi (Citation2020), and Tran (Citation2020), sample size can be determined using the formula n ≥ 50 + 8k, with k being the independent variables in the research model. In this research, the total of independent variables is between 15 and 59 observable variables. Therefore, minimum acceptable sample size would be n = 50 + 8*15 = 170. From Feb 2019 to June 2019, the authors had distributed 500 questionnaire forms; among those, 385 were valid and 13 forms were invalid; therefore, the sample size was 385, which was larger than 170, and was deemed to be appropriate.

3.2. Methodology

For this research, the authors employed mixed methods, which combine both qualitative and quantitative methodology, to study and identify factors affecting the implementation of responsibility accounting system and its effect on the performance of listed textile enterprises in Vietnam. Mixed methods have been approved and widely applied in several researches on society and business.

Qualitative methodology is used to analyze and process qualitative data to explore and explain scientific subjects. Therefore, the authors employed qualitative methodology to explore new factors affecting the implementation of responsibility accounting system and its effect on listed textile enterprises in Vietnam, and identify new factors that cannot be tested using quantitative methodology.

Quantitative research, which is conducted based on available information and data set, is favored by researchers. This approach mainly relies on experiments, logical reasoning, and measuring. According to Dao et al. (Citation2021) deductive approach is conducted by carrying out large-scale measuring and logical, realistic reasoning. In this study, we use Likert with 5 scales, including (1) Strongly Disagree, (2) Disagree, (3) Neither Disagree nor Agree, (4) Agree, and (5) Strongly Agree (Tran & Vu, Citation2019).

3.3. Research model

The authors have identified 15 factors with 59 observable variables that have certain impacts on the implementation of responsibility accounting to improve the performance of listed textile companies in Vietnam; those factors could be seen in the research model in , in which independent variables are summarized in , and depedent variable is summarized in .

Figure 2. Research model.

Table 1. Independent variables

Table 2. Dependent variables

4. Empirical results

4.1. Descriptive statistics

The descriptive statistics will discuss the general information regarding survey, including gender, education level, age, working position, and working experience in the sample data. The results will be shown in Table as follows:

As suggested in , approximately 59% of respondents were male and the remaining 41% were female. Respondents who hold Master degrees accounted for 44.4% of the survey audience, and 48.6% of the target audience were people with Bachelor degrees; 45.5% of them had experience of 5 to 10 working years and 44.9% of them had experience of 10 to 20 years of working. Besides, 47.8% of respondents were in the age range of 30 to 40, while 33.5% of them were in the age range of 40 to 50. This suggested that the result of the preliminary quantitative research was reliable because most of the respondents were above 30 years old with at least 5 years of working in the field, and all had bachelor’s degrees.

Table 3. General information regarding survey targets

Descriptive statistics is a method to analyze data, with the total of valid respondents of 385, which satisfied the minimum amount of 125. In order to have an overall view of collected data, the authors constructed the below table to present a statistical summary of respondents based on sample size, mean, standard deviation, minimum value, and maximum value.

indicates that measured value of variables was mainly (1, 5) and (2, 5). Mean varied from 1.85 to 3.98. Standard deviation showed that all variables scattered evenly. For dependent variable, the measure of performance is shown by operating efficiency and responsibility accounting system in textile firms. Mean varied from 3.11 to 3.45 and quite stable among sub-variables.

Table 4. Statistical description of the measurement of variables

4.2. Cronbach’s alpha test results

By using Cronbach’s Alpha to test reliability shown in , it can be stated that all observable variables are qualified, and all pass the test of reliability, since minimum item-total correlation of each factor is greater than 0.3 (Dao et al., Citation2021; Islam et al., Citation2015), and Cronbach’s Alpha > 0.6. Therefore, all variables are used in the following EFA.

Table 5. Summary of Cronbach’s Alpha test results

4.3. Exploratory factor analysis (EFA) analysis

shows that KMO = 0.840, which satisfied the condition of 0.5< KMO = 0.840 < 1, so EFA was deemed appropriate. Meanwhile, Bartlett’s test with Sig. <0.01 proves that all variables have linear correlation with the represented factors. In addition, with the total variance explained, indicates that At Eigenvalue = 1.384 > 1 extracted from 8 factors from 59 observed variables with a total variance extracted is 78.440% (>50%) and no new factors have been formed compared to the proposed research model. Thus, after EFA analysis, these 59 observed variables ensure the EFA analysis standard (satisfactory). No variables were excluded at this stage

Table 6. KMO analysis and Bartlett’s Test

Table 7. Total variance explained

After extracting Principal components and executing Varimax rotation, the authors constructed the below to show new factors.

Table 8. Summary of new factors

4.4. Confirmatory factor analysis (CFA) analysis

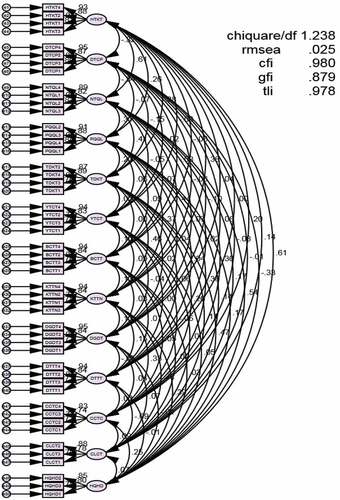

By applying CFA, it could be stated that the Measurement Model is valid since Chi-square/df = 1.238 ≤ 3 p value = 0.000, which means that the value is statistically valid. Besides, with TLI = 0.978 and CFI = 0.980 > 0.9 (the closer this figure is close to 1, the more valid the model is present), RMSEA = 0.025 < 0.08, the model satisfied every condition and was deemed appropriate with practical data, and there was no correlation between measurement, so the unidimensionality of the model was confirmed (see Appendix A and ).

Table 9. Summary of CFA results with standardized regression weights (Standardized Regression Weights)

4.5. Testing theoretical models with structural equation modeling (SEM)

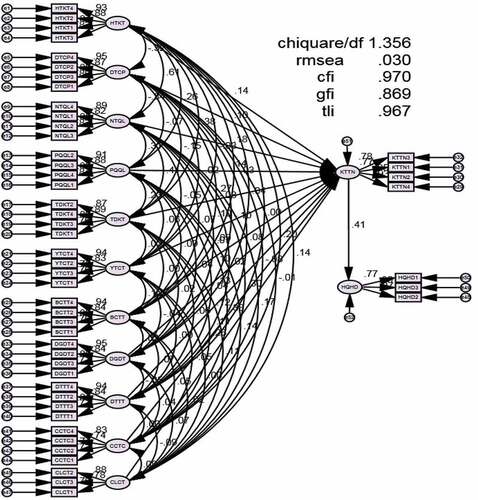

Results of SEM confirmed the validity of the research model, with Chi-square/df = 1.356 ≤ 3 with p value = 0.000, which means that the value is statistically valid. Besides, with TLI = 0.967 and CFI = 0.970 > 0.9 (the vale is to close 1, the more valid the model is present), RMSEA = 0.030 < 0.08, the model satisfied every condition and was deemed appropriate with practical data (see Appendix B).

shows the degree of impact, from the strongest to the weakest: Ability of accounting staffs (TDKT), Awareness of managers at different level (NTQL), Decentralization (PQQL), Reward systems (HTKT), Forecast for responsibility centers (DTTT), Structural management (CCTC), Competitive strategy (CLCT), Allocate revenue—costs (DTCP), Assess forecasts and reality (DGDT), Competitive advantages (YTCT), Responsibility centers’ reports (BCTT).

Table 10. The causal relationship between concepts in the theoretical model

Multigroup Analysis was executed to identify discrepancies between relationship of hypotheses and relationship of variables in the model: organizational size, Measurement techniques, Level of Awareness, Level of Competition. Maximum Likelihood method was used in the Multigroup Analysis, while chi-square test of independence was used to compare the two models. If there is no difference between the constrained estimation and unconstrained estimation (p-value > 0.05), it could be stated that there would be no statistical meaning at reliability of 95%, or the model is not affected by the hypotheses. On the other hand, if p-value ≤ 0.05, there would be statistical meaning and the theoretical model is affected by the hypotheses (see Appendix C).

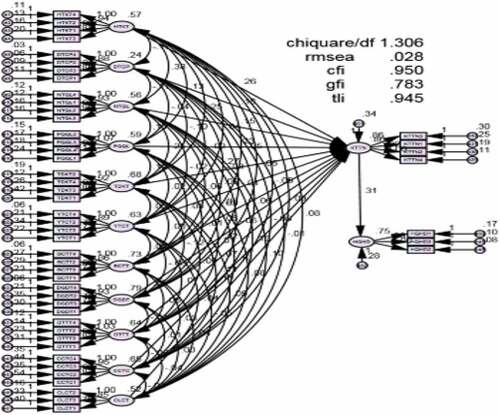

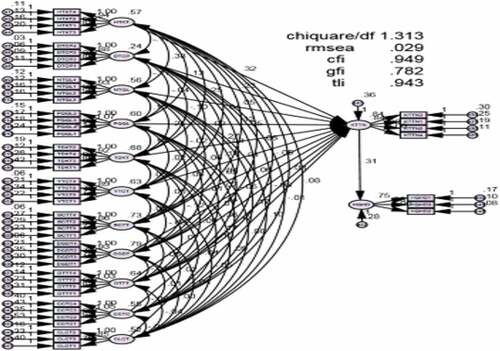

4.5.1. Hypothesis testing—organizational size

Result of SEM for the Unconstrained estimation was appropriate with practical data since Chi-square/df = 1.306 ≤ 3 with p value = 0.000, which means there is statistical meaning. Besides, TLI = 0.943 and CFI = 0.949 > 0.9 (the closer those figures are to 1, the more valid and appropriate they are); RMSEA = 0.028 < 0.08 (this figure is best kept as small as possible), which satisfy all requirements. So the theoretical model is appropriate and suitable with practical data. Result of SEM for the Constrained estimation was appropriate with practical data since Chi-square/df = 1.313 ≤ 3 with p value = 0.000 which means there is statistical meaning. Besides, TLI = 0.945 and CFI = 0.950 > 0.9 (the closer those figures are to 1, the more valid and appropriate they are); RMSEA = 0.029 < 0.08 (this figure is best kept as small as possible), which satisfy all requirements. So the theoretical model is appropriate and suitable with practical data (see Appendix D)

In order to test the impact of the hypothesis on the theoretical model, the authors carried out chi-square test of independence for Constrained and Unconstrained Estimation.

As shown in , there are discrepancies between Chi Square and Degrees of Freedom of the two models, and statistical meaning also exists (p-value ≤ 0.05). Therefore, the theoretical model is affected by Organizational size.

Table 11. Chi-square test of Independence—Organizational size

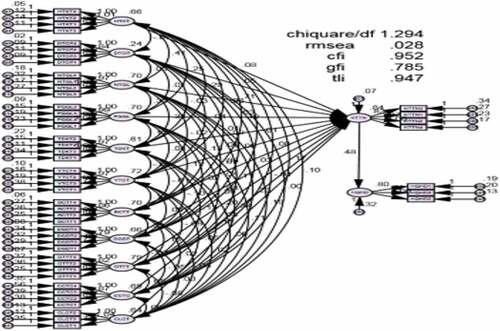

4.5.2. Hypothesis testing—Measurement techniques

Result of SEM for Unconstrained and Constrained Estimations was appropriate with practical data since Chi-square/df = 1.294 ≤ 3 with p value = 0.000, which means there is statistical meaning. Besides, TLI = 0.947 and CFI = 0.952 > 0.9 (the closer those figures are to 1, the more valid and appropriate they are); RMSEA = 0.028 < 0.08 (this figure is best kept as small as possible), which satisfy all requirements. So the theoretical models are appropriate and suitable with practical data (see Appendix E and F). In order to test the impact of the hypothesis on the theoretical model, the authors carried out Chi square test of independence for Constrained and Unconstrained Estimation.

As shown in , there are discrepancies between Chi Square and Degrees of Freedom of the two models, and statistical meaning does not exist at reliability level of 95% (p-value = 0.25 > 0.05). Therefore, the theoretical model is not affected by Measurement Techniques.

Table 12. Chi square test of Independence—Measurement Techniques

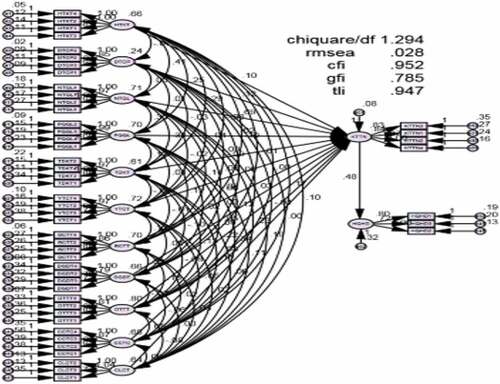

4.5.3. Hypothesis testing—Level of Awareness

Result of SEM for Unconstrained and Constrained Estimations was appropriate with practical data since Unconstrained estimation showed Chi-square/df = 1.294 ≤ 3 with p value = 0.000, and Constrained estimation also showed Chi-square/df = 1.294 ≤ 3 with p value = 0.000, which means there is statistical meaning. Besides, for both Estimations, TLI = 0.937 and CFI = 0.943 > 0.9 (the closer those figures are to 1, the more valid and appropriate they are); RMSEA = 0.030 < 0.08 (this figure is best kept as small as possible), which satisfy all requirements. So the theoretical models are appropriate and suitable with practical data (see Appendix G, and H).

shows that, there are discrepancies between Chi Square and Degrees of Freedom of the two models, and statistical meaning also exists (p-value = 0.25 > 0.05). Therefore, the theoretical models are affected by Level of Awareness.

Table 13. Chi square test of Independence—Level of Awareness

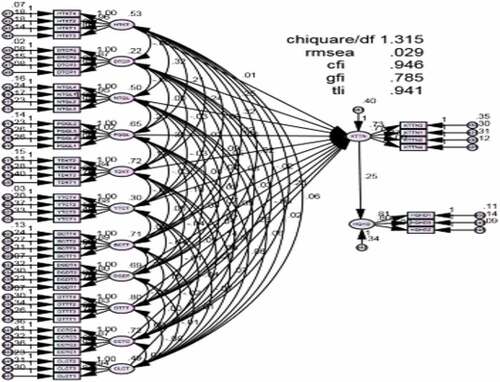

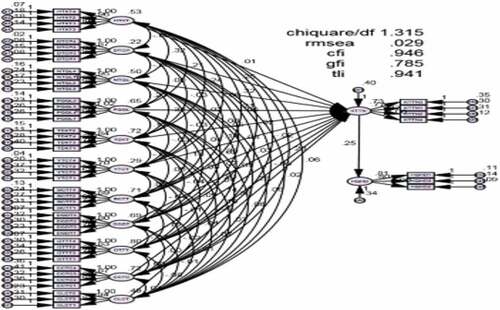

4.5.4. Hypothesis testing—Level of competition

Result of SEM for Unconstrained and Constrained Estimations was appropriate with practical data since Chi-square/df = 1.315 ≤ 3 with p value = 0.000, which means there is statistical meaning. Besides, TLI = 0.941 and CFI = 0.946 > 0.9 (the closer those figures are to 1, the more valid and appropriate they are); RMSEA = 0.029 < 0.08 (this figure is best kept as small as possible), which satisfy all requirements. So the theoretical models are appropriate and suitable with practical data (see Appendix I, and J).

depicts that, there are discrepancies between Chi Square and Degrees of Freedom of the two models, and statistical meaning does not exist at reliability level of 95% (p-value = 0.56 > 0.05). Therefore, the theoretical models are not affected by Level of Competition.

Table 14. Chi square test of Independence—Level of Competition

4.5.5. Testing and estimating theoretical models with Bootstrap

The Bootstrap test is used to re-estimate the parameters in the theoretical model that are estimated by the optimal estimation method (Maximum Likelihood). The result is shown in below:

Table 15. Estimated results by Bootstrap with N = 500

In this study, we performed Bootstrap by repeated sampling with a sample size of N = 500. The value of CR is less than 2, so we can confirm the bias is very small and not statistically significant in reliability 95%. This proves that the estimates in the model are reliable.

4.6. Result of the evaluation of theoretical model

After EFA, CFA, and SEM analysis, Bootstrap test, and Multigroup Structural analysis, the authors were able to identify 11 independent variables and 4 moderating variables (2 of which were eliminated) affecting the implementation of responsibility accounting system and its impact on the performance of listed textile companies in Vietnam. Apparently, 11 independent variables were identified after SEM analysis, while the 4 moderating variables were identified after Multigroup structural analysis. Results were presented in as follows:

Table 16. Overview of factors

5. Discussions

5.1. Management—related factors

5.1.1. Organizational size

Research result suggests that there is a relationship between organizational size and the implementation of responsibility accounting system, in which the bigger (in term of revenue, total departments, staffs, and years of operating) the organizational size is, the easier it would be to implement responsibility accounting system. This finding agrees with previous studies conducted by Hatibat (Citation2005); Tram-Nguyen et al. (Citation2021). This confirms the fact that listed textile companies with big organizational size, strong financial power, and complex management would find it easier to implement responsibility accounting system.

During the survey process, the authors were also able to realize the high demands for responsibility accounting systems in listed textile companies in Vietnam, because by implementing responsibility accounting systems, organizations with big organizational size, good amount of clearly defined departments, strong financial power, stable and loyal workforce would be able to boost their performance. Besides, assessment and evaluation of departments could also be done accurately, which also helps motivate employees.

5.1.2. Organizational structure

Without a well-defined organizational structure, it would be impossible for any organization to implement responsibility accounting system. This is because one of the requirements to establish responsibility centers in a responsibility accounting system is the division of departments and branches with well-assigned tasks and responsibilities. Research result suggests that organizations with clearly defined hierarchies, good task assignments, detailed targets, and strong cooperation between departments would be more likely to succeed in establishing responsibility accounting systems. Previous researches conducted by Al Hanini (Citation2013), Ramadan (Citation2016), N.T. Nguyen et al. (Citation2019), and Le et al. (Citation2018), have confirmed that organizational structure is one of the factors that have impact on the implementation of responsibility accounting system. In other words, organizational structure could determine the success of the implementation.

5.1.3. Degree of delegation

Research result suggests that delegation is one of the factors affecting the implementation of responsibility accounting system in listed textile companies in Vietnam. Delegation happens when managers are assigned with tasks and specific targets; in their responsibility centers, managers are given authority to make all decisions. This result is similar with results of previous studies conducted by Al Hanini (Citation2013), Ramadan (Citation2016), N.T. Nguyen et al. (Citation2019), and Le et al. (Citation2018). In prior to making any decisions, managers should seek advice from higher-management and take into account external factors, such as competitors. However, in each responsibility center, staffs should have appropriate expertise and experience, and they should be responsible for making detailed reports. In order to evaluate managers’ performance in responsibility centers, managers should be given enough time to carry out their tasks and duties.

5.2. Technique—related factors

5.2.1. Measurement technique

Research result suggests that measurement technique does not affect the implementation of responsibility accounting system in listed textile companies in Vietnam, which contradicts with results of previous researches conducted by Fowzia (Citation2011); Islam et al. (Citation2015). This difference could be due to the data set. This result is appropriate with practical situations and conditions in Vietnam, since responsibility centers do not employ any measure technique to measure their performance; instead, many tools would be employed to measure the performance of each responsibility center.

5.2.2. Allocation of revenue—cost

Research result suggests that Allocation of revenue—costs is one of the factors affecting the implementation of responsibility accounting system in listed textile companies in Vietnam. In order to establish responsibility accounting system, each department would become a responsibility center with well-defined tasks and responsibilities. Each responsibility center would then be allocated revenue and costs based on its roles and duties. The records of those costs would require a good cost accounting system to define and assign direct as well as indirect costs to each responsibility center. Besides, revenue generated by each responsibility center needs to be recorded accurately. This would help top-level managers to compare, evaluate, and control the relationship between revenue and costs when they decide to implement responsibility accounting systems. This result is similar with results of previous studies conducted by Al Hanini (Citation2013), Ramadan (Citation2016), N.T. Nguyen et al. (Citation2019), and Le et al. (Citation2018).

5.2.3. Forecasts for responsibility centers

Research result is similar with results of previous researches, which all confirmed that Forecasts for responsibility centers has an impact on the implementation of responsibility accounting system in listed textile companies in Vietnam, conducted by Al Hanini (Citation2013), Ramadan (Citation2016), N.T. Nguyen et al. (Citation2019), and Le et al. (Citation2018). Apparently, responsibility centers are clearly assigned tasks and duties. Budgets and forecasts would be prepared by managers and staffs in the responsibility centers based on their tasks and duties. Staffs are encouraged to participate in the planning process, since they should know their responsibilities and targets well. Besides, staffs in each responsibility center would receive training and motivation to strive to achieve their targets in accordance with forecasts. Since forecasts are detailed plans for future activities, it’d be necessary for managers to make adjustments to them based on the targets and goals of the whole organizations as well as of each responsibility center.

5.2.4. Responsibility centers’ reports

Research result suggests that Reports prepared by responsibility centers would have an impact on the implementation of responsibility accounting system in listed textile companies in Vietnam. This result agrees with results of previous researches conducted by Al Hanini (Citation2013), Ramadan (Citation2016), N.T. Nguyen et al. (Citation2019), and Le et al. (Citation2018). Successful implementation of responsibility accounting system would require each responsibility center to make detailed reports and plans. Reports should reflect actual results and plans for the future made by each responsibility center. Additionally, reports can also be used to evaluate the performance of responsibility centers. Besides, managers can use those reports to identify discrepancies between actual results and plans to make necessary adjustments. For the purpose of evaluation, managers and staffs should be able to make reports whenever the Board of Directors requests.

5.2.5. Assess forecasts and reality

Evaluation of forecasts and reality is one of the factors affecting the implementation of responsibility accounting system in listed textile companies in Vietnam. Responsibility centers would make reports to evaluate forecasts and actual results periodically. In order to make accurate reports, various evaluation tools must be employed. Among those tools and ratios, efficiency is the most widely used due to its accuracy and effectiveness. Besides, Standard costs is also an effective tool to measure efficiency. Comparison method is also employed to compare staffs’ achievements and performance based on actual results and forecasts. This method is used to help with control and monitoring, identifying discrepancies. Discrepancies which are discovered will be investigated to determine its importance and impact, from which adjustments can be made to prevent those from happening in the future. This result agrees with results of previous studies conducted by Al Hanini (Citation2013), Ramadan (Citation2016), N.T. Nguyen et al. (Citation2019), and Le et al. (Citation2018).

5.3. Awareness—related factors

5.3.1. Level of awareness

Awareness is one of the moderating factors affecting the implementation of responsibility accounting system in listed textile companies in Vietnam. Awareness includes managers’ awareness of the efficiency of responsibility accounting system, awareness of a reward system in which rewards, bonus, and punishments are clearly defined using quantitative tools. Awareness also includes accountants’ awareness of the implementation and effective use of responsibility accounting systems. Therefore, this factor could affect the reward systems, managers’ awareness, and skills of accounting staffs in the process of implementing responsibility accounting systems in listed textile companies in Vietnam. This result agrees with results of previous researches conducted by Le et al. (Citation2018).

5.3.2. Reward systems

Research result suggests that reward system is one of the factors affecting the implementation of responsibility accounting system in listed textile companies in Vietnam. Reward systems are designed by managers to encourage their employees to reach their targets. Incentives and bonus can actually boost the efficiency and performance of staffs since those staffs know that their efforts are recognized and contribute to the organizations’ successes. Reward systems need to be reviewed periodically for managers to make necessary adjustments based on actual situations. Managers should make sure that the reward systems are transparent and take into account staffs’ efforts. By doing this, staffs would feel satisfied and content with the reward systems in their organizations. This result agrees with results of previous researches conducted by Al Hanini (Citation2013); Ramadan (Citation2016).

5.3.3. Managers’ awareness

Research result suggests that Managers’ awareness is the factor with the second-biggest impact on the implementation of responsibility accounting system in listed textile companies in Vietnam. Managers should be aware of the decision to implement responsibility accounting system in the organization and in their departments, as well as the benefits this decision can bring to their departments and the whole organizations. Those benefits usually include: increase of managers’ authority, profit, productivity, employee satisfaction, customers satisfaction, and cost reduction. Among those, the most important benefit is the increase of customer satisfaction (regarding quality of products, attitude of staffs, etc.) since the current trend in the business world is to maximize customers satisfaction, which could lead to customer loyalty and sustainable development of the organizations. This result re-confirms the results of previous researches conducted by Mohammad et al. (Citation2014).

5.3.4. Skills of accounting staffs

Research result suggests that Skills of accounting staffs is the factor with the strongest impact on the implementation of responsibility accounting system in listed textile companies in Vietnam, because responsibility accounting systems would be established and operated mainly by accountants. Therefore, staffs who have good knowledge about the system and know how to utilize its tools would be able to generate accurate plans and reports. Besides, it is necessary for accountants to know their responsibilities and have a high level of ethics; without those characteristics, accountants can be a threat to the organization since they could leak confidential and strategical information. Additionally, accounting staffs should regularly enroll in training sessions to update their knowledge and skills to be able to operate responsibility accounting systems. This result actually agrees with results of previous researches conducted by Mohammad et al. (Citation2014); Tram-Nguyen et al. (Citation2021).

5.4. Competition—related factors

5.4.1. Competitive advantages

Research result suggest that Competitive advantages is one of the factors affecting the implementation of responsibility accounting system in listed textile companies in Vietnam. In this era of globalization, competition is becoming harsh; therefore, competitive advantages (in term of resources, workforce, price, quality of products, etc.) must be taken into consideration when staffs prepare plans and reports. With this piece of information, managers can make decisions to reduce costs or improve revenue, which affects responsibility centers directly. This result is similar with results of previous researches conducted by Doan (Citation2012); Hoque and James (Citation2000).

5.4.2. Level of competition

Research result suggests that the Level of competition does not have any impact on the implementation of responsibility accounting system in listed textile companies in Vietnam, which contradicts with results of previous researches conducted by Mia and Clarke (Citation1999); Tram-Nguyen et al. (Citation2021). This difference could be due to the data set. This result is deemed to be appropriate with the current practical conditions, since textile companies are constantly competing with both domestic enterprises and foreign enterprises.

5.4.3. Competitive strategy

Research result suggests that Competitive strategy is one of the factors affecting the implementation of responsibility accounting system in listed textile companies in Vietnam. Currently, textile companies are always in need of competitive strategies regarding costs, product differentiation, target market penetration, etc. Based on the characteristics of markets, textile companies can have different competitive strategies to allow them to enter the markets. Responsibility accounting systems can help by developing plans and budgets to ensure optimum efficiency. This result is deemed to be appropriate in the current practical conditions and it also agrees with results of previous researches conducted by Govindarajan and Fisher (Citation1990); Tram-Nguyen et al. (Citation2021).

5.5. Causal relationship

After the overall structure model is analyzed and tested, the next step is to look at the estimated values to examine causal relationships shown in . Through the results, for instance, we see that all factors have a positive impact on the implementation of responsibility accounting. The ability of accounting staffs (TDKT) is the strongest factor (standardized weight is 0.269). The second most powerful factor is the Awareness of managers at different level (NTQL) (standardized weight is 0.185). The third most powerful factor is the Decentralization (PQQL) (standardized weight is 0.143). The fourth is the Reward systems (HTKT) level factor with a standardized weight of 0.138, the fifth is the Forecast for responsibility centers (DTTT) factor (standardized weight is 0.126), the sixth is the Structural management (CCTC) factor (standardized weight is 0.125), the seventh is the Competitive strategy (CLCT) factor (standardized weight is 0.110), the eighth is the Allocate revenue—costs (DTCP) factor (standardized weight is 0.104), the ninth is the Assess forecasts and reality (DGDT) factor (standardized weight is 0.102), the tenth is the Competitive advantages (YTCT) factor (standardized weight is 0.096). Finally, the Responsibility centers’ reports (BCTT) (standardized weight is 0.091) have the lowest impact. There is a strong correlation between the implementation of responsibility accounting and the improvement of the performance of listed textile companies in Vietnam. Estimated results show that this hypothesis is accepted and achieved a standardized beta value of 0.409 with significance level P = 0.000 < 0.05. If the implementation of responsibility accounting changes by 1 point (level), it will increase the performance of listed textile companies in Vietnam (or decrease) by 0.409 points without considering the other factors.

6. Conclusions

The implementation of responsibility accounting plays a significant role in doing business, responsibility accounting can significantly provide managers with information that can help them make better business decisions. The aims of the study identify factors affecting the implementation of responsibility accounting on the performance of Vietnamese listed textile companies. Using the qualitative methodology by employing the questionnaire, while quantitative methodology was used to measure the analysis, and also employing the Structural equation modeling (SEM) with AMOS—SPSS, results indicate that factors aside from measurement technology and level of competition had certain impacts, including the ability of accounting staffs (TDKT), the awareness of managers at different level (NTQL), the decentralization (PQQL), the reward systems (HTKT), and the forecast for responsibility centers (DTTT). Additionally, factors such as the structural management (CCTC), the competitive strategy (CLCT), the competitive advantages (YTCT) and the responsibility centers’ reports (BCTT) that have significant effects on firm performance. In addition, the implementation of responsibility accounting is the most powerful effect on firm performance. In fact, a one-point increase of the implementation of responsibility accounting change will increase/decrease the performance of listed companies by 0.409 points without considering the other factors

Correction

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Van Chien Nguyen

Van Tung Tran is an associate professor at the Faculty of Finance and Commerce, HUTECH University - 475A Dien Bien Phu Street, Ward 25, Binh Thanh District, Ho Chi Minh City. He specializes in accounting, and business management. He has published some scientific papers on worldwide.

Phat Cuong Ly works for Ho Chi Minh City University of Foreign Languages – Information technology (Huflit), Vietnam. He specializes in accounting, and business management.

Ngoc Nguyen Thao Ngo is a lecturer at the Faculty of Finance and Commerce, HUTECH University. Her research interests are economics, and business management

Phuong Hai Tran is a lecturer at the Faculty of Finance and Commerce, HUTECH University.

Van Chien Nguyen is a graduate of doctoral study at the Department of Economics of University of Colombo, Sri Lanka. He works for Thu Dau Mot University and his research interests are financial economics, finance, and energy.

References

- Ahmad, K. (2012). The use of management accounting practices in Malaysia SMEs [ Phd thesis], University of Exeter. https://ore.exeter.ac.uk/repository/handle/10036/3758?show=full

- Al Hanini. (2013). The extent of implementing responsibility accounting features in the Jordanian Banks. European Journal of Business and Management, 5(1), 217–32. https://www.ccsenet.org/journal/index.php/ijbm/article/view/28969

- Al-Htaybat, K., & Alberti-Alhtaybat, L. (2013). Management accounting theory revisited: Seeking to increase research relevance. International Journal of Business and Management, 8(18), 12–24. https://doi.org/10.5539/ijbm.v8n18p12

- Atkinson, A. A., Banker, R. D., Kaplan, R. S., & Young, S. M. (2001). Management accounting- (3th ed.). Prentice Hall.

- Barney, J. (2011). Gaining and sustaining competitive advantage (4th ed.). Pearson Education, Inc.

- Chenhall, R. H. (2003). Management control systems design within its organizational context: Findings from contingency-based research and directions for the future. Accounting, Organizations and Society, 28(2–3), 127–168. https://doi.org/10.1016/S0361-3682(01)00027-7

- Coad, A.F., and Herbert, I. (2009). Back to the Future: New Potential for Structuration Theory in Management Accounting Research. Management Accounting Research, 20(3), 177–192. 10.1016/j.mar.2009.02.001

- Covaleski, M. A., Dirsmith, M. W., & Samuel, S. (1996). Managerial accounting research: The contributions of organizational and sociological theories. Journal of Management Accounting Research, 8(1), 1–35. https://www.researchgate.net/publication/284594334_'Managerial_Accounting_Research_The_Contributions_of_Organizational_and_Sociological_Theories'

- Dao, L. K. O., Loc, H. H., Nguyen, V. C., Hang, L. T. T., & Do, T. T. (2021). Factors affecting the choice of banks: Do bank’s interest rate, employee image and brand matter? Journal of Asian Finance, Economics and Business, 8(1), 457–470. doi:10.13106/JAFEB.2021.VOL8.NO1.457

- Doan, N. P. A. (2012). Factors affecting strategic management accounting in Vietnam’s medium and large sized enterprises. Journal of Economic Development, 214(10), 81–90. http://jabes.ueh.edu.vn/Content/ArticleFiles/oldbv_en/2012/Thang%2010/6doanngocphianh.pdf

- Eisenhardt, K. M. (1989). Agency theory: An assessment and review. The Academy of Management Review, 14(1), 57–74. https://doi.org/10.2307/258191

- Elsayed, M. O., & Hoque, Z. (2010). Perceived international environmental factors and corporate voluntary disclosure practices: An empirical study. The British Accounting Review, 42(1), 17–35. https://doi.org/10.1016/j.bar.2010.01.001

- Fiedler, F. E. (1964). A Contingency Model of Leadership Effectiveness. Advances in Experimental Social Psychology, 1, 149–190. https://doi.org/10.1016/S0065-2601(08)60051-9

- Fowzia, R. (2011). Use of responsibility accounting and measure the satisfaction levels of service organizations in Bangladesh. International Review of Business Research Papers, 7(5), 53–67. http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.698.8409&rep=rep1&type=pdf

- Garrison, R., Noreen, E., & Brewer, P. (2006). Managerial Accounting (Eleventh () ed.). McGraw-Hill Irwin.

- Govindarajan, V., & Fisher, J. (1990). Strategy, control systems, and resource sharing: Effects on business-unit performance. The Academy of Management Journal, 33(2), 259–285. https://www.jstor.org/stable/256325

- Haldma, T., & Laats, K. (2002). Contigencies influencing the managerment accounting practies of Etonian manufacturing companies. Management Accounting Research, 13(4), 379–400. https://doi.org/10.1006/mare.2002.0197

- Han, Y. (2018). Implementation of Responsibility Accounting in Electric Power Enterprises. International Conference on Information Technology and Management Engineering (ICITME 2018) Atlantis Press, 148, 152–154.

- Hatibat, K. A. (2005). Management accounting practices in Jordan: a contingency approach [ Thesis (Ph.D.)]. University of Bristol. https://ethos.bl.uk/OrderDetails.do?uin=uk.bl.ethos.419378

- Healy, P. M., & Palepu, K. G. (2001). Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics, 31(1 – 3), 405–440. https://doi.org/10.1016/S0165-4101(01)00018-0

- Higgins, J. A. (1952). Responsibility accounting (Vol. 12). The Arthur Andersen chronicle.

- Hopper, T., & Armstrong, P. (1991). Cost accounting, controlling labor and the rise of conglomerates. Accounting Organizations and Society, 16(5 – 6), 408–438. https://doi.org/10.1016/0361-3682(91)90037-F

- Hopwood, A. G. (1976). Accounting and human behavior, Eaglewood Cliffs. Prentice Hall.

- Hoque, Z., & James, W. (2000). Linking balanced scorecard measures to size and market factors: Impact on organizational performance. Journal of Management Accounting Research, 12(1), 1–17. https://doi.org/10.2308/jmar.2000.12.1.1

- Horngren, C. T., Bhimani, A., Datar, S., & Foster, G. (2005). Management and cost accounting. Financial Times Prentice Hall.

- Hussain, S., Nguyen, V. C., Nguyen, Q. M., Nguyen, H. T., & Nguyen, T. T. (2021). Macroeconomic factors, working capital management, and firm performance—A static and dynamic panel analysis. Humanities Social Sciences Communications, 8(1), 123. https://doi.org/10.1057/s41599-021-00778-x

- Islam, M. S., Miah, M. S., & Fakir, A. N. M. A. (2015). Environmental accounting and reporting practices in the corporate sector of Bangladesh. https://www.researchgate.net/publication/308646803

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- LE, O. T. T., & BUI, N. T. (2020). Responsibility accounting in public universities: A case in Vietnam. The Journal of Asian Finance, Economics and Business, 7(7), 169–178. https://doi.org/10.13106/jafeb.2020.vol7.no7.169

- Le, P. H., Huynh, N. L. A., & Luu, T. T. (2018). Influence of responsible accounting on the performance of enterprises in the Mekong Delta. Can Tho University Journal of Science, 54(4), 168–177. https://doi.org/10.22144/ctu.jvn.2018.082

- Ma, Y., & Tayles, M. (2009). On the emergence of strategic management accounting: An institutional perspective. Accounting and Business Research, 39(5), 473–495. https://doi.org/10.1080/00014788.2009.9663379

- Marshall, C., & Rossman, G. B. (1989). Designing qualitative research. Sage Publications.

- Merriam, S. B. (1988). Case study research in education: A qualitative approach. Jossey-Bass.

- Mia, L., & Clarke, B. (1999). Market competition, management accounting systems and business unit performance. Management Accounting Research, 10(2), 137–158. https://doi.org/10.1006/mare.1998.0097

- Mohammad, E. N., Abdul-rahman, Z., Mahmoud, F., & Atala, Q. (2014). An empirical assessment of measuring the extent of implementing responsibility accounting rudiments in Jordanian industrial companies listed at amman stock exchange. Advances in Management & Applied Economics, 4(3), 123–138. https://ideas.repec.org/a/spt/admaec/v4y2014i3f4_3_9.html

- MOIT. (2018). Issues for the development of processing and manufacturing industry in the case of participating in CPTPP. http://cptpp.moit.gov.vn/data

- Nguyen, V. C. (2020). Human capital, capital structure choice and firm profitability in developing countries: An empirical study in Vietnam. Accounting, 6(2), 127–136. https://doi.org/10.5267/j.ac.2019.11.003

- Nguyen, N. T., Nguyen, T. L. H., & Pham, D. C. (2019). Factors affecting the responsibility accounting in Vietnamese firms: A case study for livestock food processing enterprises. Management Science Letters, 9(9), 1349–1360. https://doi.org/10.5267/j.msl.2019.5.015

- Nguyen, T. T., Nguyen, V. C., Tran, T. N., & McMillan, D. (2020). Oil price shocks against stock return of oil and gas-related firms in the economic depression: A new evidence from a copula approach. Cogent Economics & Finance, 8(1), 1799908. https://doi.org/10.1080/23322039.2020.1799908

- Oakes, L. S., & Covaleski, M. A. (1994). A historical examination of the use of accounting based incentive plans in the structuring of labor-management relations. Accounting Organizations and Society, 19(7), 579–599. https://doi.org/10.1016/0361-3682(94)90025-6

- Otley, D. T. (1980). The contingency theory of management accounting: Achievement and prognosis. Accounting, Organizations and Society, 5(4), 413–428. https://doi.org/10.1016/0361-3682(80)90040-9

- Otley, D. (2016). The contingency theory of management accounting and control. Management Accounting Research, 31, 45–62. https://doi.org/10.1016/j.mar.2016.02.001

- Pennings, J. M. (1975). The relevance of the structural-contingency model for organizational effectiveness. Administrative Science Quarterly, 20(3), 393–410. https://doi.org/10.2307/2391999

- Ramadan, I. Z. (2016). Implementing responsibility accounting in Jordanian industrial companies. International Business Management, 10(23), 5501–5506. https://medwelljournals.com/abstract/?doi=ibm.2016.5501.5506

- Rook, D. W., & Fisher, R. J. (1995). Normative influences on impulsive buying behavior. Journal of Consumer Research, 22(3), 305–313. https://doi.org/10.1086/209452

- Rugby, A. H. (2004). Management accounting (3rd ed.). Dar-Wael for Publication.

- Santos, J. B., & Brito, L. A. L. (2012). Toward a subjective measurement model for firm performance. Brazilian Administration Review, 9(6), 95–117. https://doi.org/10.1590/S1807-76922012000500007

- Tabachnick, B. G., & Fidell, L. S. (2007). Using multivariate statistics (5th ed.). Allyn and Bacon.

- Tram-Nguyen, T. H., Tuan-Le, A., & Nhi-Vo, V. (2021). Factors affecting the implementation of management accounting techniques in medium-sized enterprises of Vietnam. Problems and Perspectives in Management, 19(3), 440–452. https://doi.org/10.21511/ppm.19(3).2021.36

- Tran, V. D. (2021). Using mobile food delivery applications during the COVID-19 pandemic: Applying the theory of planned behavior to examine continuance behavior. Sustainability, 13(21), 12066. https://doi.org/10.3390/su132112066

- Tran, V. D., & Foroudi, P. (2020). Assessing the relationship between perceived crowding, excitement, stress, satisfaction, and impulse purchase at the retails in Vietnam. Cogent Business & Management, 7(1), 1858525. https://doi.org/10.1080/23311975.2020.1858525

- Tran, V. D., & Vu, Q. H. (2019). Inspecting the relationship among E-service quality, E-trust, E-customer satisfaction and behavioral intentions of online shopping customers. Global Business & Finance Review (GBFR), 24(3), 29–42. https://doi.org/10.17549/gbfr.2019.24.3.29

- Wildavsky, A., & Caiden, N. (2004). The new politics of the budgetary process (5rd () ed.). Longman Classics Series.

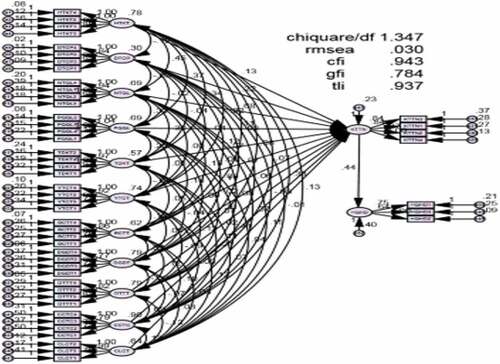

Appendix A.

Standardized model.

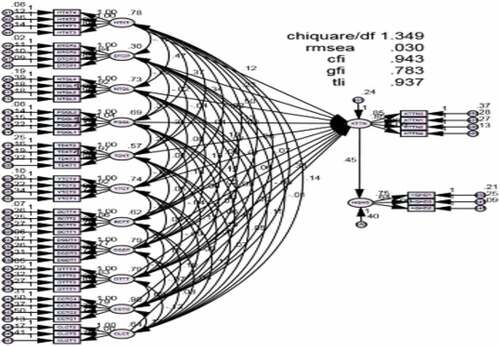

Appendix B.

Standardized theoretical model.

Appendix C.

Unconstrained estimation of organizational size.

Appendix D.

Constrained estimation of organizational size.

Appendix E.

Unconstrained estimation of measurement techniques.

Appendix F.

Constrained estimation of measurement techniques.

Appendix G.

Unconstrained estimation of level of awareness.

Appendix H.

Constrained estimation of level of awareness.

Appendix I.

Unconstrained estimation of level of competition.

Appendix J.

Constrained estimation of level of competition.