?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Disruptive technology has been prominent as a spotlight with countless innovations that improve human’s life efficiently. In Vietnam, COVID-19ʹs outbreak has reinforced citizens to adopt other types of payment without using cash, which easily diffuses virus. Till now, the number of studies related to continuance usage of mobile wallets in Vietnam has been rare. Hence, our purpose in this research is to study continuance usage in COVID-19 through determinants. This paper concentrates on Millennials and Zillennials living Ho Chi Minh City. PLS-SEM with data collected from questionnaires assesses the conceptual model that indicates the correlation between UTAUT2ʹs constructs, trust, price saving orientation, behavioral intention and continuance usage. As predicted, the findings show that there are positive relationships among all determinants. In the event of effort expectancy and social influence, despite unsatisfactory of statistical significance, they reflect current context. Besides, direct positive influences from two variables to behavioral intention lead to further research studies after the pandemic to conclude properly about their significance. From the study’s result, business strategies together with security’s policies have to be modified by providers as well as the government to motivate mobile wallet adoption in Vietnam, amplifying cashless society and financial inclusion targets.

PUBLIC INTEREST STATEMENT

Vietnam is an emerging country experiencing disruptive technology where cashless channels such as mobile wallet have risen over the past decade. COVID-19 pandemic is fostering this noncash method since residents have to comply with large-scale social distancing without allowance for using traditional payment in cash. There have been several papers conducted on mobile wallet adoption; however, further investigation related to its continuance usage within an emerging country as Vietnam is still absent. Therefore, we are the first to explore which determinants affect mobile wallet continuous usage during COVID-19 outbreak in Vietnam based on our survey’s responses from the modified UTAUT2 model together with Smart-PLS. As expected, adopters are strongly impacted by all proposed determinants except effort expectancy and social influence. Instead of being rejected, both indicators must be further considered due to their positive relationship with the dependent variable. Our findings also contribute to managerial implications, which improve as well as accelerate not only mobile wallet adoption but also continuance usage.

1. Introduction

The digital revolution witnessed the growth in information and technology communication, which has been changing and reshaping human habits in various aspects of social life including payment. In the past, all financial transactions are conducted mostly by cash or cards. However, this method maintain limits since payment is required to be made directly at which merchandise is sold. It is a time-consuming, inconvenient and inflexible method. Recently, thanks to the advanced technology, the number of payment methods been improved as internet banking, mobile money and mobile wallet. In line with such new forms of payment, the business model has been promoted, which widens the existence ecosystem with different players, for instance, E-commerce platforms and suppliers, financial services, online shopping, etc. Thus, the cashless society has been matured around the world and mobile wallet has become a must-have payment method. In 0.04 seconds, there are more than 29,000 results appearing through Google Scholar. To investigate behavioral intention in the linkage to disruptive innovation, scholars have employed different models, for instance, Theory of Acceptance Model (TAM; Davis, Citation1989) Theory of Reasoned Action (TRA; Azjen, Citation1980; Fishbein & Ajzen, Citation1977); Theory of Planned Behavior (TPB; Ajzen, Citation1985); Model of PC Utilization (MPCU; Thompson et al., Citation1991); Theory of Acceptance Model in the coordination with Theory of Planned Behavior (C-TAM-TPB; Taylor & Todd, Citation1995); Innovation Diffusion Theory (IDT; Rogers, Citation1976) and Social Cognitive Theory (SCT; Venkatesh et al., Citation2003). Inherited feasibilities of antecedents, in 2012, Venkatesh, Thong, & Xu developed a model called Unified Theory of Acceptance and Use Technology (UTAUT) in order to cover and deepen the relationship between mobile wallet adoption and behavioral intention from previous models. The constructs of UTAUT2 combined, such as performance expectancy, effort expectancy, social influences and facilitating conditions – four constructs issued by the original UTAUT together with added variables such as hedonic motivation, price value and habit in the UTAUT2.

Over the past few years, Vietnam has been developing remarkably with the transformation from the bottom to the middle country in regard to income. Accordingly, the World Bank classified Vietnam as “one of the most dynamic emerging countries in East Asia Region”.Footnote1 To boost that ranking, disruptive innovation is a fundamental core. Vietnam has been experiencing and adapting to disruptive innovation including mobile wallet. To make any payment, users are required the most important infrastructure such as internet or 3 G/4 G in order to connect. In Vietnam, the percentage of individuals using internet is increasing sharply within ten years from 37.37% in 2007 to 58.14% in 2017.Footnote2 Besides, as Vietnam Ministry of Information and Communications reported, there are more than 51 million accounts over the population including about 95 people. This number expresses one 3 G/4 G account out of 2 civilians in Vietnam. Thus, that growth is a premise and positive instrument to create the linkage between users and mobile wallet. According to the statistics published by Global Financial Development in October 2019, the electronic payments of those who are above 15 years old have an upward trend when rising up 13.56% within 7 years (from 2.537% in 2011 to 16.097% in 2017).Footnote3 From data released, users are approaching noncash payment and this trend continues growing. However, their market share is not speedily scalable in comparison to traditional payment. Since COVID-19 outbreak, strict policies have been imposed by Vietnamese government; moreover, citizens hesitate using cash. Therefore, noncash payment including mobile wallets is the best choice to obey the regulations while preventing from being infected.

Although mobile wallet in Vietnam is an attractive topic, the number of empirical studies investigating this field is rare. “A study of factors affecting the intention to use mobile payment services in Vietnam. Economics” predicted variables influencing mobile payment’s intention through the TAM model (Liu & Tai, Citation2016); “An investigation of Generation Z’s Intention to use Electronic Wallet in Vietnam” employed TAM and UTAUT in together to examine factors that impact the mobile wallet adoption (DO & DO, Citation2020). These research studies put an end to behavioral intention only instead of considering continuance usage of mobile wallet. However, intention is just an early stage and retaining existing customers is essential for companies to reach growth or even maturity stage in mobile wallets’ life cycle. Furthermore, limited previous papers only employed TAM or UTAUT models instead of others. Nonetheless, UTAUT2 is considered as an extension of UTAUT2, which is specialized in adapting “consumer technology use context” (Venkatesh et al., Citation2012). In addition, our research supplements advanced variables as price saving orientation (substitute for price value), trust and continuance usage associated with UTAUT2’s model. Notably, trust’s construct includes trust from governmental policies besides centralizing only trust from providers’ policies. The reason is that customers will have hesitancy toward mobile wallet adoption if they are cognitive about the shortage of protection from the government.

Hence, this research is significant and unavoidable because it figures out dimensions influencing not only behavioral intention but also continuance usage by applying UTAUT2 in line with new additional variables and fulfills the gaps in mobile wallet adoption of customers in Vietnam. Millennials and Zillennials are the research’s target since they are sensitive, flexible and acceptable to experience innovative technology. Our study centralizes Ho Chi Minh City as a representative because this location is a key economic region and financial center where disruptive technology is always welcome as well as highly appreciated; this location has also been experiencing COVID-19 waves. Contributions resulted from this study allow both companies and the government to figure out solutions not only increasing continuance usage but also accelerating the cashless society of an emerging country as Vietnam.

Besides the introduction, this study is structured with five sections that are Theoretical, Model and Hypotheses; Data; Method; Result and Conclusion and Implication. Discussion on the current circumstance of mobile wallet is the initial stage in this paper. Then, to elucidate factors influencing behavioral intention as well as continuance usage of customers when adopting mobile wallet, the rest of this research including four sections is structured. Section 2 covers the theoretical framework together with proposed hypothesis development. Methodology is briefly presented in section 3. Subsequently, section 4 discusses results and in the last part, section 5, conclusions or implications are recommended relying on findings from section 4.

2. Theoretical framework and hypotheses development

This study concentrates on identifying determinants that motivate behavioral intention and continuance usage to adopt mobile wallet.

2.1. Mobile wallet

According to eGHL, a Malaysian payment company cooperating with more than 100 payment channels around ASEAN-5, China, Middle East, New Zealand and Australia, online wallet is recognized based on the payment method and the openness level. There are three groups of online wallet: digital wallet, e-wallet and mobile wallet. Personal information in a credit/debit card is stored, and payment deduction is conducted automatically from the bank/credit account if customers use digital wallet. e-wallet is different from the former, and credit/debit card is not requisite since users are enabled to use e-wallet by top-up money in e-wallet. Then, the amount of credit value is reloaded and deducted from the wallet account. However, in line with digital wallet, e-wallet does not also permit users depositing money from physical points as shops or counters. Therefore, without bank accounts, customers are unable to use digital wallet and e-wallet, which build the constraint on spreading online wallet usage. As a result, mobile wallet is created to remove this boundery since payment transfers are accepted via physical agencies such as stores, shops or counters by simple tapping or scanning. From the openness level point of view, online wallet is divided into three groups (1) closed wallet, (2) semi-closed wallet and (3) open wallet. The first type is considered as the most restrictive as it only accepts payments issued by the company in which customers purchase its goods or services. That company builds its own platform together with online wallet, providing coupons and differently attractive promotions for their customers. They can keep their rewards as well as top-up money; however, they are not allowed to withdraw money from the platform. Semi-closed wallet is an intermediation of payment since vendors and vendees are enabled to match, purchase and conduct transactions. Vendees take advantage either using promotions and rewards offered by both vendors and wallet providers or withdrawing money (it depends on online wallet’s policy since few wallets offer this function, but others do not). At the highest level of openness, open wallet allows users to add their cards (credit/debit) when making payment. In addition, users can even withdraw cash from the ATM machine and be served banking services. In Juniper’s research published in 2012, there are two sets of m-payment: proximity and remote m-payment, which leads to two subsets of mobile wallets. For proximity payment, mobile wallet uses near field communication (NFC) technology, and for remote m-payment, mobile wallet is dependable on wireless networks or phone number. As reported by Cimigo for the fourth quarter of the year 2019, Momo, Moca and Zalo pay are the key drivers that dominate mobile wallet’s payment sector as their market share accounts for 90% in Ho Chi Minh City together with Ha Noi Capital, the largest metropolitan areas in Vietnam. In line with classification from eGHL and Juniper, the most common types of mobile wallet in Vietnam are e-wallet/ semi-closed wallet (Moca and Zalo Pay) and mobile wallet/open wallet (Momo). It can be seen clearly that three online wallets are proximity m-payment as they offer NFC technology in their applications. Specifically, Momo does not belong only to proximity m-payment but also to remote m-payment when providing cash-in and cash-out services via personal mobile number.

2.2. Unified theory of acceptance and use technology 2 (UTAUT2)

To shed the light of behavioral intention and continuance usage toward mobile wallet adoption, the authors decide to apply Unified Theory of Acceptance and Use Technology 2 (UTAUT2) designed by Venkatesh et al. (Citation2012) in combination with Trust and Price Saving Orientation constructs. Moreover, continuance usage is another highlight notice for managerial positions to consider and develop long-term strategies. However, few constructs are modified to adapt to the context of this research.

Before reviewing on Unified Theory of Acceptance and Use Technology 2 (UTAUT2), it is essential to review UTAUT since UTAUT2 results from the development of UTAUT’s theoretical background. UTAUT is preferable to explore unfamiliar contexts (technologies and cultural patterns) and additional constructs to broaden intrinsic theoretical framework in UTAUT and extrinsic predictive factors resulting from UTAUT variables (Limayem et al., Citation2007), (Chan et al., Citation2008; Gupta et al., Citation2008; Neufeld et al., Citation2007; Sun et al., Citation2009). The model raises its utility by unifying Theory of Acceptance Model (TAM), Theory of Reasoned Action (TRA), Theory of Planned Behavior (TPB), Model of PC Utilization (MPCU), Theory of Acceptance Model in the coordination with Theory of Planned Behavior (C-TAM-TPB), Innovation Diffusion Theory (IDT) and Social Cognitive Theory (SCT; Venkatesh et al., Citation2003). The eight models are the most influential instruments in order to study behavioral intention of individuals. Therefore, it is reasonable when investigating key elements that influence intentional usage technology adoption’s field; UTAUT is one of the most prevailing model proposed by Venkatesh et al. (Citation2003). (Qasim & Abu-Shanab, Citation2016). The origin of UTAUT includes four fundamental constructs: performance expectancy, effort expectancy, social influences and facilitating conditions. Although the initial UTAUT is favorably applied toward innovations in different context, “consumer technology use context” requires further variables so as to clarify and specialize for this situation. As a result, in 2012, Venkatesh et al. upgraded the UTAUT model through including three constructs, hedonic motivation, price value and habit, which leads to UTAUT2.

In the original UTAUT, performance expectancy (PE) has been highlighted as the most forceful determinant toward users’ decision when adopting a technology (Venkatesh et al., Citation2003). Performance Expectancy’s definition has extended not only users’ beliefs but also perceptions that a technology is able to improve their performance (Venkatesh et al., Citation2003, Citation2012). Moreover, in previous research studies, performance expectancy was concluded that it interacts positively to an individual’s Behavioral Intention (BI) in association with adopting an IT system (Putri, Citation2018; Venkatesh et al., Citation2003, Citation2012). Consistently, recent studies conducted in Malaysia and India, emerging countries in Asia, have proved the significance of performance expectancy toward mobile wallet’s behavioral intention and even continuous usage (Revathy & Balaji, Citation2020; Saraswati et al., Citation2021). Thus, the first hypothesis is proposed:

H1: performance expectancy (PE) has a positive impact on behavioral intention (BI) of customers toward mobile wallet adoption

Effort expectancy (EE) is how easy the users are aware of when approaching technology (Venkatesh et al., Citation2003). This factor is inspired by Ease of Use in TAM, complexity in MPCU and Perceived Ease of Use in IDT (Cimperman et al., Citation2016; Venkatesh et al., Citation2003). In the context of innovation, easiness is a requisite for early adopters, especially, elderly people. Once the perceived ease of use experiences an upward trend, users recognize that new technology is beneficial and helpful. Users normally expect to sacrifice less effort in order to save intangible values; however, their demand toward a new product is unchanging. Thus, easiness is considered as an effective instrument so that users reduce their effort to get used to usage. (Cimperman et al., Citation2016; Or et al., Citation2011). According to previous studies, the influential degree of EE on BI is increasing powerfully on a positive side (Arning & Ziefle, Citation2009; Cimperman et al., Citation2016; Kijsanayotin et al., Citation2009; J. Kim & Park, Citation2012). Thus, we suggest next hypothesis:

H2: effort expectancy (EE) has a positive impact on behavioral intention (BI) of customers toward mobile wallet adoption

Social influence (SI) refers to the degree to which users are impacted to respond to the technology by their important acquaintances and relatives (Venkatesh et al., Citation2003). However, there have been several deliberations against the significance of SI in the linkage to Behavioral Intention. Cimperman et al. (Citation2016), Khalilzadeh et al. (Citation2017), Qasim and Abu-Shanab (Citation2016), and Venkatesh et al. (Citation2003) and Venkatesh et al. (Citation2012) supported that between BI in technology, adoption and SI exist a positive impact. In contrast, Alalwan et al. (Citation2017), Baptista and Oliveira (Citation2015) and Tamilmani et al. (Citation2020) argued that the role of SI affecting BI is minimal and even nonsignificant for utilitarian technologies, for example, mobile banking. Therefore, this study expects to test, in the context of Vietnam market, whether SI is classified as an important determinant for BI in technology adoption as mobile wallet. Based on the discussion mentioned above, we recommend the following hypothesis:

H3: social influence (SI) has a positive impact on behavioral intention (BI) of customers toward mobile wallet adoption

Facilitating conditions (FCs) are defined as how the technology supports users to experience the system by utilizing existing resources (Venkatesh et al., Citation2003). This definition is derived from perceived behavioral control in TPB/DTPB (Ajzen, Citation1985) and CTAMTPB (Taylor & Todd, Citation1995) and facilitating conditions in MPCU (Thompson et al., Citation1991) and compatibility in IDT (Rogers, Citation1976). Similar to SI, from empirical results, FC has received both supporters (Ajzen, Citation1985; Cimperman et al., Citation2016; Hongxia et al., Citation2011; Thakur, Citation2013; Venkatesh et al., Citation2000) and antagonists (Rogers, Citation1976; Thompson et al., Citation1991). Furthermore, Tamilmani et al. (Citation2020) noticed that scholars must be cautious in order to input FC in research models because this variable is the least impact factor when users decide to adopt innovative technology. However, Venkatesh et al. (Citation2003) claimed that EE stimulates FC together with the belief that EE is able to be a predictors and there is a need to conduct deeper investigation about EE. Therefore, we decided to add FC in our model to figure EE’s role. Thus, we underpin the next hypothesis:

H4: facilitating conditions (FCs) have a positive impact on behavioral intention (BI) of customers toward mobile wallet adoption

Hedonic motivation (HM) is one out of three additional factors to the extant UTAUT so as to formulate an advanced model: UTAUT2. HM is observed as users perceive using the technology that is attractive and delightful, which emphasizes the level of entertainment (Venkatesh et al., Citation2012). Before Venkatesh defined the definition of HM in 2012, plenty of scholars stated that HM is a critical determinant that predicts BI of consumers, specifically, in the consumer context (Brown & Venkatesh, Citation2005; Childers et al., Citation2001; Heijden, Citation2004; Hong et al., Citation2006; Putri, Citation2018). Furthermore, in a recent study, Tamilmani et al. (Citation2020) concluded that beside PE, HM is the most powerful predictor influencing consumers in technology usage, especially, early adopters. Hence, this study proposes the following hypothesis with regard to entertainment:

H5: hedonic motivation (HM) has a positive impact on behavioral intention (BI) of customers toward mobile wallet adoption

Habit (HB) is defined as the degree to which users’ behavior is unintentionally performed due to the learning process (Limayem et al., Citation2007; Venkatesh et al., Citation2012). In previous studies, HB was significantly related to not only usage but also continuance intention (H.-W. Kim & Kwahk, Citation2007; Putri, Citation2018; Tamilmani et al., Citation2020; Zhanyou et al., Citation2020). Therefore, we propose next hypothesis:

H6: Habit (H) has a positive impact on behavioral intention (BI) of customers toward mobile wallet adoption

2.3. Trust

Trust is the first modification besides six existing variables derived from the UTAUT model. This independent variable is observed under different perspectives as “the belief that vendors will perform some activities in accordance with customers’ expectation” (Shin, Citation2009); “important determinants with direct and indirect impacts, of other critical constructs (i.e., effort expectancy, hedonic and utilitarian performance expectancy, attitude and intention)” (Khalilzadeh et al., Citation2017) and “a significant role in determining consumer transaction intentions” (Lee, Citation2005). This means that when conducting research related to financial payment, trust is considered at a high level of importance (Gefen & Straub, Citation1997; Qasim & Abu-Shanab, Citation2016; Slade et al., Citation2015). Moreover, in the wireless environment, as payments are performed through online services in which uncertainty is surrounded, trust positions itself urgently and critically. When making cashless transactions in order to exchange for products or services, customers have undesirable information disclosure. They prefer and expect privacy accounts. In the event that information is required to be shared, consumers are afraid that hackers can access and steal not only personal details but also monetary values for illegitimate purposes. Trust is not only significant pre-COVID-19 but also critical as an influencer in the period of the outbreak. In the context of emerging countries, this feature is nominated for future research studies involved in behavioral intention toward mobile wallet adoption during the pandemic (Jesuthasan & Umakanth, Citation2021).

However, it will be a shortage if the research observes trust only covered with service providers and technology innovation since customers’ trust is also encouraged and evoked by the government (Shilpi Saraswat, Citation2017). As a result, in this research, along with concerning trust as a majority of previous studies did, trust is extended to government support. According to previous research, there are 38 over 40 respondents who stated that their decision is derived from trust (Putri, Citation2018). In line with Putri’s contribution, other scholars claimed that trust is a primary factor that impacts and boosts technology acceptance, predicting usage intention and even continuity of using (Qasim & Abu-Shanab, Citation2016; Slade et al., Citation2015). Additionally, latest scholars through empirical studies have examined that during the COVID-19 pandemic in emerging countries, trust arisen by policymakers is especially highlighted. Researchers tried to emphasize how efficient new noncash payment’s regulation is and recommendations are suggested for mobile wallet acceleration (Gelb & Mukherjee, Citation2020; Saraswati et al., Citation2021; Wong & Mohamed, Citation2021). Eventually, it is logical to include trust as one of the determinants in the model as researching about mobile wallet adoption. Thus,

H7: trust (T) has a positive impact on behavioral intention (BI) of customers toward mobile wallet adoption.

2.4. Price-saving orientation

Price-saving orientation is the second modification that is normally included in price value without being separated as an independent variable. According to Venkatesh et al. (Citation2012), price value is net remaining from the gap between monetary cost and actual values. Nevertheless, in the online environment, activities performed do not always incur monetary cost. For instance, when people book a ticket from a website, monetary cost does not exist. Escobar-Rodríguez and Carvajal-Trujillo (Citation2014) stated that nonmonetary technology still enable lower price. In fact, practical research about Go-Pay, an Indonesian mobile wallet, expressed that there is not any monetary cost for Go-Pay, but customers still enjoy its lower price (Putri, Citation2018). Currently, the ecosystem of payment method has changed dramatically, especially, mobile wallet. It does not only provide payment function but also diversify in various areas such as reservation (airline tickets, restaurants, hotels, etc.), entertainment (cinema tickets, spa service, etc.), food and beverage and even shopping online; therefore, customers have a wide range of selection. In a comparison price among providers, they prefer price saving. Previous studies indicated that consumers are motivated to reserve their products or services through online platforms since they believe that they can save both tangible (money) and intangible (time) values (Wu & Chang, Citation2005). To shed the light of reducing the amount of money in each transaction, promotions are the key. With a price-saving orientation variable, promotion is also combined to clarify how much customers perceive that they are able to save while finalizing transactions. In practical studies, scholars concluded that price-saving orientation should be added as a new construct in the UTAUT2 model since it enables to predict intentional and actual usage (Escobar-Rodríguez & Carvajal-Trujillo, Citation2014). Hence, price-saving orientation is proposed to incorporate in the research’s model, so the assumption is proposed:

H8: Price-saving orientation (PSO) has a positive impact on behavioral intention (BI) of customers toward mobile wallet adoption.

2.5. Behavioral intention

Following the definition issued by Davis (Citation1989), behavioral intention is the degree at which customers construct a plan for their behavior to respond or not respond in the future. Among a pool of massive research studies investigating about mobile wallet adoption in Vietnam, the number of studies discussing continuance usage is rare, while its vital role cannot be ignored. Practically, when innovative technology is launched in a market, immediately, the public responds inquisitively and desires being an owner. Therefore, consumers may intend to adopt mobile wallet at first; however, their willingness for continuance usage does not ensure. Thus, the correlation between behavioral intention and continuance usage is explored in this study.

H9: Behavioral Intention (BI) has a positive impact on Continuance Usage (CU) of customers toward mobile wallet adoption.

proposes the research model with the modified UTAUT2 Model to be tested.

Figure 1. Research model.

3. Methodology

3.1. Respondent

Millennials or Generation Y who were born in the period from 1981 to 1996 and those whose nationality is Vietnamese are particularly targeted. Samples are mainly collected in Ho Chi Minh City as this is one of the metropolises in Vietnam with accelerating growth of mobile wallet usage. This research employs convenience sampling throughout online survey distribution; furthermore, in-depth interview is arranged to collect managers’ perspectives.

3.2. Instrument development

All questionnaires are translated from English to Vietnamese in order for Vietnamese respondents to comprehensively apprehend. Before officially distributing the survey, we conducted a pilot test with 30 people to ensure that respondents understand visibly questionnaires’ content. Google Form is employed as a tool for designing questionnaires, and then the link was created to send to respondents. After that, data are gathered by online survey. All question items adapted by the theoretical framework are measured by the Likert scale where the range is from “strongly disagree” to “strongly agree” (Likert, Citation1932). The survey was completed within a month from the beginning of December 2020 to the beginning of January 2021.

3.3. Measurement scales

This study inherited previous studies’ scale to measure the key variables and their items. Performance Expectancy was measured by Venkatesh et al. in 2003 and 2012. Putri (Citation2018) modified this measurement scale to be accordant with mobile wallet context. Therefore, in this research, Performance Expectancy was adapted from Putri (Citation2018). The adjustment of Effort Expectancy (Putri, Citation2018) was proposed by Venkatesh (Citation2012) with the additional item “It does not take long time to learn to use Go-Pay”, which concerns with time-saving orientation. Hence, we used the scale of Effort Expectancy based on Putri (Citation2018). Social Influence, Facilitating Conditions, Hedonic Motivation, Habit and Behavioral Intention were adapted from the study by Venkatesh (2012); Continuance Usage adapted from Trust was adapted by Venkatesh (2012). The scale of Trust was developed by Gefen (Citation2000) for E-commerce. After that, in 2004, Zmijewska, Lawrence, & Steele revised to be appropriate for mobile payment’s context. These modifications paid attention to another perspective of Trust as security. Accordingly, security plays a critical role in mobile wallet’s research since users are always afraid that privacy information will be stolen without constructing a stringent security framework. Thus, this study measured Trust under the selective combination of Trust’s items issued by both Gefen (Citation2000) and Zmijewska et al. (Citation2004). In Putri’s research (Putri, Citation2018), together with suppliers, governments are responsible for mobile wallets’ security by controlling and imposing relevant policies and laws. Therefore, in the case of trust factor, items are adapted by Gefen (Citation2000), Zmijewska et al. (Citation2004) and Putri (Citation2018). Price-saving orientation is an essential key determinant in recent studies involved in adopting technological payment. Our study relied on Putri (Citation2018) to build price-saving orientation’s questionnaires.

4. Results and discussion

In this research, Smart-PLS 3.2.8 software is used to assess the Partial Least Squares (PLS)-SEM model (Hair et al., Citation2017). The analytical procedures are performed by the measurement model and structural model, respectively. The measurement model is assessed, in which the reliability and validity of the constructs are analyzed. Then, the structural model is used to identify the significance of the hypotheses.

shows research’s demographics collected from 181 respondents (n = 181) who are above 18 years old. Furthermore, recipients are using mobile wallet or at least have used to experience it in the past when contributing to the survey. In gender, female takes advantage over male with 65.7% and 34.3%, respectively. The range between 18 and 24 years old dominates others with 97.8%.

Table 1. Demographic characteristics of respondents

4.1. Assessment of the measurement model

First of all, to ensure that the research model constructed is valid and reliable, convergent validity, discriminant validity and reliability included in the measurement model must be evaluated (Hair et al., Citation2014). Next, due to higher-order constructs together with the Refective-Reflective model, we employ the hierarchical component modeling technique. Then, with reference to Becker et al. (Citation2012), in this paper, model assessment is conducted by using the method as repetitive indicators.

After the first phase, items that do not meet the standards of Cronbach’s Alpha, Composite Reliability and Average Variance Extracted are eliminated from the measurement model. As a result, HM3, HM4, HM6, HA1, HA5, EE2, EE3, PSO4, T2, T6 and T7 are discarded. Then, the second assessment of the measurement model has to be performed so that the latest results are presented as .

Table 2. Reliability and validity

In terms of reliability, we pay attention to Cronbach’s Alpha and composite reliability; convergent validity and discriminant validity are in charge of construct validation. According to Nunnally (Citation1978), Composite–reliability (CR) values must exceed the 0.7 threshold. shows that Cronbach’s Alpha’s values are greater than the 0.6 boundary when they fall into the range between 0.621 and 0.787 (Churchill, Citation1979). The AVE values, which must be beyond 50% (Fornell & Larcker, Citation1981), are also satisfactory with the outcomes starting from 0.506. To examine the discriminant validity in the measurement model, the Fornell-Larcker criterion is employed. Definitely, all the constructs are well-satisfied convergent validity’s criteria.

As shown in , the square root value of AVE (diagonal) of each indicator is greater than the highest value of the correlation coefficient for all reflective constructs (off-diagonal). Hence, there is an establishment of discriminant validity between the constructs based on Fornell and Larcker (Citation1981).

Table 3. Fornell-Larcker criterion

Multicollinearity is defined as a condition in which more than two predictors are highly correlated (Williams et al., Citation2013). The application of multiple linear regression analysis assumes that there is no multicollinearity among the predictors (Shou & Smithson, Citation2015). According to the multicollinearity’s assumption, when a strong linear relationship exists among predictors, the coefficient of related variance (VIF) is large (>5), which is an evidence of multicollinearity. In the case of a complex research model including independent variables, intermediate variables and dependent variables, Hair et al. (Citation2014) proposes to assign subgroups into models including only independent variables and a dependent variable. In this research, we use the VIF index generated by the results of PLS_SEM analysis on Smart PLS 3.2.8 so as to examine the multicollinearity. VIF values are below 2 so there is no multicollinearity among the constructs.

To strengthen an evidence that all discriminant values are fully valid, this paper takes into consideration the Heterotrait-Monotrait ratio (HTMT), an up-to-date criterion in PLS_SEM’s report (Hair et al., Citation2017). HTMT is proposed by Henseler et al. (Citation2016) to measure the ratio “between-trait correlations” to the “within-trait correlations” (Hair et al., Citation2017). presents all HTMT values that are below 0.9; therefore, a respective couple of values does not correlate with each other greater than 0.9; then, discriminant validity of the measurement model is certified.

Table 4. Discriminant Validity (HTMT criterion)

4.2. Assessment of the structural model

After completing phase one—assessment of the measurement model, phase two, assessment of the structural model, must be carried out by examination hypothesis testing, effect size and coefficient of determination. We set 5% for the level of significance and run boot-strapping for the sample whose size varies from 100 to 500 with Smart PLS. Then, T-statistics and P-value play a role in whether the hypothesis is accepted or rejected.

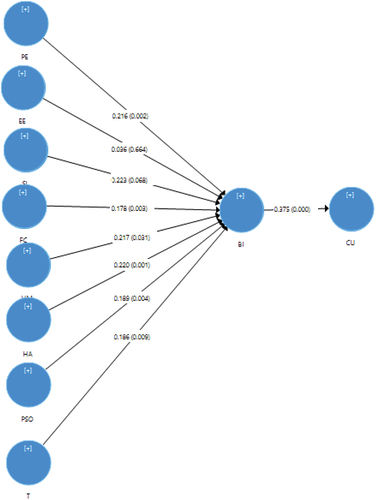

shows that independent variables such as EE, FC, HA, HM, PE, PSO, SI and T have a medium effect on BI. Besides, in relationship with CU, BI affects CU moderately. The number 0.262 of R square adjusted from indicates that independent variables impact BI at 26,2%. Similarly, BI is able to explain 13.6% for CU.

Table 5. Effect size

From , it is obvious to imply that H1, H4, H5, H6, H7, H8 and H9 are supported since their hypotheses impact in the same direction and p-values are smaller than 0.05. H2 and H3 are not rejected in the structural model although they are not statistically significant with p-values of 0.664 and 0.068, respectively. The reason for accepting both hypotheses mainly originates from Vietnam market’s characteristic within the COVID-19 pandemic,which is discussed further in the next section. In line with , the direct hypothesis testing is presented in , a logical evidence whether the hypothesis is accepted. BI () positively influences CU, which supports H1 PE that determines BI (Putri, Citation2018; Venkatesh et al., Citation2003, Citation2012). However, H2 is not supported because of EE (p-value >0.05), which contradicts previous studies (Arning & Ziefle, Citation2009; Cimperman et al., Citation2016; Kijsanayotin et al., Citation2009; J. Kim & Park, Citation2012). Likewise, H3 is not supported as SI (t-value<1.96), which is similar to the research of Alalwan et al. (Citation2017), Baptista and Oliveira (Citation2015), and Tamilmani et al. (Citation2020). The result for H4 shows that FC positively influences BI (

), and accordingly, H4 is accepted (Ajzen, Citation1985; Cimperman et al., Citation2016; Hongxia et al., Citation2011; Thakur, Citation2013; Venkatesh et al., Citation2000, Citation2003). As predicted in Tamilmani’s findings (Tamilmani et al., Citation2020), the positive coefficient value between HM and BI and statistically significant values lead to an acceptance of H5 (

). HA raises a positive correlation with BI along with H6 (

, which should be maintained (H.-W. Kim & Kwahk, Citation2007; Putri, Citation2018; Tamilmani et al., Citation2020; Zhanyou et al., Citation2020). The result from H7 indicates that trust positively interact with behavioral intention; besides, all statistical values are satisfied (

) so H7 is accepted, which consolidates trust position as previous scholars concluded (Gefen & Straub, Citation1997; Putri, Citation2018; Qasim & Abu-Shanab, Citation2016; Shilpi Saraswat, Citation2017; Slade et al., Citation2015). Subsequently, price-saving orientation plays an important role since it is statistically significant and positive correlation with behavioral intention (

and then H8 is supported (Escobar-Rodríguez & Carvajal-Trujillo, Citation2014; Putri, Citation2018). As for H8, behavioral intention positively influences continuance usage (

and accordingly, H9 is accepted. Based on H9, top managers are able to find out solutions in which mobile wallet not only hooks consumers but also retains their loyalty.

Figure 2. Bootstrap results.

Table 6. Direct hypothesis testing

This research emphasizes and clarifies how behavioral intention is impacted by several factors. Furthermore, different from previous studies, especially for the Vietnam market, continuance usage is taken into consideration instead of putting a stop at behavioral intention only.

Overall, UTAUT2ʹs constructs were expected to define behavioral intention that later describes continuance usage of consumers once adopting mobile wallet. As one of the related factors, performance expectancy influences behavioral intention. Possible implication is that respondents believe and are aware of innovative technology from mobile wallet, which enhances their performance. This finding is consistent with a majority of previous studies on new technology adoption (Venkatesh et al., Citation2003, Citation2012). Furthermore, our contribution also consolidates recent conclusion that performance expectancy is significant in emerging countries and during the COVID-19 pandemic, its roles still remained as an indispensable determinant (Revathy & Balaji, Citation2020; Saraswati et al., Citation2021). Facilitating conditions used to be undervalued due to its trivial benefits toward technology adoption. When asked, respondents have a tendency to experience new technology if it is compatible with existing resources that they are owning in order to avoid time-consuming and risky activities in learning unfamiliar systems, which results in the decisive role of facilitating conditions. Following previous research studies, hedonic motivation receives optimistic perception (Brown & Venkatesh, Citation2005; Childers et al., Citation2001; Heijden, Citation2004; Hong et al., Citation2006; Putri, Citation2018; Tamilmani et al., Citation2020). This could be inferred that participants in the survey have a tendency to experience mobile wallet adoption whenever it was found to be delightful and entertaining. During COVID-19, citizens are required to obey social distancing together with quarantine strictly, which accelerates digital payment as a primary channel. Moreover, this is the third time that the pandemic has broken out in Vietnam; therefore, users have to perform cashless payment. As a result, respondents utilize mobile wallet as a habit at least within the difficult time. Hence, habit is another significant factor that affects behavioral intention (H.-W. Kim & Kwahk, Citation2007; Limayem et al., Citation2007; Putri, Citation2018; Tamilmani et al., Citation2020; Venkatesh et al., Citation2012; Zhanyou et al., Citation2020). Surprisingly, effort expectancy is not decisive toward user’s intention, which contradicts the UTAUT2 theory as well as previous empirical examinations (Arning & Ziefle, Citation2009; Cimperman et al., Citation2016; Kijsanayotin et al., Citation2009; J. Kim & Park, Citation2012). However, it is consistent with recent findings (Saraswati et al., Citation2021; Verkijika, Citation2018). Remarkably, among arguments about social influence’s position, our study participates in one out of rare scholarly journals, supporting that this factor is insignificant in association with decision on adopting mobile wallet, which is in line with present papers (Alalwan et al., Citation2017; Baptista & Oliveira, Citation2015; Saraswati et al., Citation2021; Tamilmani et al., Citation2020). This unfamiliarity might be explained as the special characteristics of the Vietnam mobile wallet market. In normal conditions, early adopters desire for adopting new technology if it can lessen their efforts or be easy to use. However, in the context of Vietnam, especially the lockdown period, regardless of difficulties, people have to use noncash transactions to protect themselves. Therefore, they have fell into mandatory rather than optional situation without basic information about mobile wallet. To conclude whether effort expectancy affects mobile wallet adoption, providers must wait and observe how adopters response after the pandemic is under controlled because at that time, consumers are in active and free-stressful status so that they are able to fully experience all features and send feedbacks properly. Social influence emphasizes relationships that boost her/him to imitate (Venkatesh et al., Citation2003). However, in step with effort expectancy, there are few constraints behind that vague or misunderstanding of this factor. Although in the case that customers are eager to follow their acquaintances in order to use mobile wallet adoption, they are unable to adopt, which results in lacking of own bank account or personal identification documents. On account of working from home, respondents had to deal with multitask pressure and lacks time for detailed questionnaires, which lessens our sample size. Hence, our research will have bias when confirming that social influence plays a minimal role in behavioral intention.

By the data from our survey, trust rises as a key driver determining behavioral intention of participants. Respondents have faith in security systems offered; accordingly, mobile wallets’ providers must maintain frequently to keep its performance sustainable and low-risk. Exceptionally, in comparison with traditional trust constructs, this study added the role of governments so as to promote the trust level in users’ mindset. As expected, respondents propose that governments involved consolidate their belief in usage. This is an evidence to specify that trust is not constructed by not only mobile wallets’ providers but also governmental protection; particularly, during the COVID-19 pandemic with innumerable frauds and scams existing, humans become reserved and have avoidable money-related activities.

Price-saving orientation is the last independent variable engaged in the research model to evaluate whether consumers’ intention is affected. As predicted, responses show enthusiasm toward price-saving orientation through hot deals, flash sales, etc.; moreover, they evaluate promotions provided that are trendy and suitable for their interests or preference. Additionally, participants whose age is between 18 and 24 dominate the sample. This means that among alternatives, young generation still prioritizes for technology products, which lessen cost or spending both tangible and intangible values while satisfying their diversification.

This study is successful when verifying behavioral intention to positively impact continuance usage, which is a new finding as well as upper level for mobile wallet adoption’s research in Vietnam context. In line with a significant influence, tiny p-values (0.000) bolster that behavioral intention is reliable enough to explain for continuance usage. In other words, once owners of mobile wallets understand and take all intentions arisen by users into serious consideration, they will not only hook but also retain existing adopters simultaneously. Furthermore, the product life cycle is possible to shift entirely to a higher stage as growth or even maturity.

5. Conclusion & implications

Theoretically, our findings extent literature of mobile wallet adoption in Asian emerging countries. These areas are characterized by disruptive technology, which has been widely fostering dense population with technophile generation, while policies or regulatory framework for noncash payment have not been fully efficient. As an emerging economy, there are corresponding results between Vietnam and other countries—Malaysia, India and Cameroon, for instance. Besides, this study is more special since it is the pioneer in researching about the Vietnam market within the time of COVID-19 in order to understand behavioral intention or even investigation in continuous usage of adopters. Managerially, the regulatory framework and relevant providers still maintain limitations that raise constraints on IT adoption and need to improve better and sooner.

Keeping pace with the purpose at the beginning, this study would deepen further continuance usage of users toward the mobile wallet market in Vietnam by investigating behavioral intention of adopters and relevant determinants. Age ranging from 18 to 24 dominates the survey sample, and these respondents have to live in Ho Chi Minh City and experience mobile wallets. This centralization fits to adoption context of innovative technology where young generation is sensitive to quickly respond to new things, and Ho Chi Minh is the busiest city in Vietnam that always welcomes disruptive inventions. There have been several research studies discussing behaviors in mobile wallet in the Vietnam market; nevertheless, the number of papers that investigate further about continuance usage of adopters is rare. Besides, no studies have been conducted in order to observe and concern with this topic in COVID-19 while mobile wallets become a must-have payment method to prevent from being infected during the pandemic. As a result of the study, behavioral intention of adopters depends on performance expectancy, effort expectancy, social influence, facilitating conditions, hedonic motivation, habit, trust and price-saving orientation. Six out of eight independent variables indicate both positive correlation and statistical significance with behavioral intention. In line with findings from emerging nations in Asia such as Malaysia and India, effort expectancy is not a key to deciding mobile wallet adoption in the lockdown period (Revathy & Balaji, Citation2020; Saraswati et al., Citation2021). Similarly, social influences do not meet criteria of statistical significance in spite of their positive effect on behavioral intention. However, two variables are not rejected from the model since they reflect literally current characteristics of information technology market in Vietnam. Once COVID-19 outbreaks, the government promptly enacted large-scale social distancing or lockdown policies. Inevitably, the cashless society covers as well as takes priority for the majority of transactions, implying that people passively adopt mobile wallet as an official channel to pay for even essential necessities. Besides, it is too hard to succeed an online order for food or medicine, which pushes people under pressure, and then their mental health might be affected negatively. As a result, unfamiliar proceeding payment will intensify efforts regardless of its actual easiness. In fact, social influence also lacks evidence to confirm whether this factor is important. According to policies imposed, because everyone has to stay home at all the time, their relatives and acquaintances are unable to amplify preferences, or in other words, social influence on mobile wallet adoption is objectively restrained. As a result, it could be a shortage to eliminate hastily effort expectancy and social influence in relationship with behavioral intention since more considerations should be taken after COVID-19 in a well-controlled situation when effort expectancy and social influence will reveal comprehensively.

Moving forward with continuance usage, behavioral intention sets up a powerful impact on continuance usage. This will inspire customer service department and marketers in order to upgrade mobile wallets and retain existing users, and then social influence could perform its function to hook more adopters.

6. Managerial implications

The result of the study contributes valuable information to relevant parties within mobile wallet’s ecosystems, especially for the managerial level.

Providers’ perception factors strongly influence users’ intention and continuance; moreover, factors whose performance have been fully unknown because of limitations issued by the pandemic should be noticed and reevaluated as soon as COVID-19 is handled. Products must be modified based on customers’ preferences and expectations without wasting their available resources. In the comparison with rivals, developers need to figure out competitive advantages that are distinct them other mobile wallet companies and banks. Therefore, it is also an opportunity for marketers to develop creativities so that consumers feel attracted and enjoyable enough to adopt in willing status. Various promotions also need motivation relying on the connections to partnership such as Fintech companies or banks, telecommunications corporations, entertainment organizations and fast-food chains, leading to price-saving orientation which outsiders usually pay attention before making a decision on experiencing a specific mobile wallet among others. More importantly, service providers should conduct more in-depth interviews or research studies to figure out whether when people will not be stressful under COVID-19 and effort expectancy and social influence still affect or not. Managers are able to keep one step ahead by giving further solutions so as to simplify the systems combining eKYC (Know Your Customer), bank account requirement, etc. while maintaining security along with impressive campaigns broadcasted by social media such as Youtube, Facebook, Instagram, etc. to encourage new comers involving.

Traditional research studies assumed that trust in the innovative technology field is mostly built up by the suppliers. It is normally thought that suppliers mean service providers only; however, in a completed mechanism, especially in latest studies, policymakers must be included (Gelb & Mukherjee, Citation2020; Saraswati et al., Citation2021; Wong & Mohamed, Citation2021). After the empirical testing, our findings explore that government support significantly affects mobile wallet adoption. Interestingly, it is totally consistent with previous investigation from other emerging nations in Asia such as Malaysia and Sri Lanka (Aji et al., Citation2020; Jesuthasan & Umakanth, Citation2021; Saraswati et al., Citation2021). Accordingly, the result of this study also emphasizes the government’s responsibility for enhancing trust from public. In fact, with the aim of fostering using mobile wallet during tough time of COVID-19 pandemic, Vietnam government issued Directive No. 22/CT-TTg in which relevant authorities are assigned in order to accelerate cashless payments in different sectors, for instance, healthcare cost, tuition fee or even social security benefits. aLthough regulation for mobile wallet acceleration was positively modified, it needs further specification that particularly allocateS role, process, method, etc. rather than general boosting as current Directive. Therefore, our findings contributed by the survey help government to understand what residents expect from the Vietnam authority. After that, regulatory framework must be enacted, modified and updated in a timely manner so personal accounts are secured and patronized legally. Additionally, government should notice on awakening and educating mobile wallet literacy for public through social media or campaigns. Along with reinforcement trust, the government might reach the aim at massive scale-up of noncash society and financial inclusion.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Nguyen Vinh Khuong

Huynh Thi Ngoc Ly is an associate researcher at the University of Economics and Law, Vietnam National University, Ho Chi Minh City, Vietnam. The author's interest research mainly concentrates on Fintech, Sustainability as Corporate Social Responsibilities and Branding. Nguyen Vinh Khuong holds a PhD from the University of Economics Ho Chi Minh City, Vietnam, and is a Lecturer in the Faculty of Accounting and Auditing at the University of Economics and Law, Viet Nam National University, Ho Chi Minh City, Vietnam. Tran Hung Son holds a PhD degree in Finance from the University of Economics and Law, Vietnam. Collectively, the authors have published several papers in quality journals, including Sustainability, Business Strategy and Development, Journal of Sustainable Finance and Investment, Asia-Pacific Journal of Business Administration, International Journal of Accounting & Information Management, Cogent Business and Management, Social Responsibility Journal, Journal of Open Innovation: Technology, Market and Complexity, etc.

Notes

1. https://www.worldbank.org/en/country/vietnam/overview#1. Retrieved on Monday, December 07, 2020

2. https://data.worldbank.org/indicator/IT.NET.USER.ZS?locations = VN. Retrieved on Thursday, November 26, 2020

3. https://www.worldbank.org/en/publication/gfdr/data/global-financial-development-database. Retrieved on Thursday, November 26, 2020

References

- Aji, H. M., Berakon, I., Md Husin, M., & Tan, A. W. K. (2020). COVID-19 and e-wallet usage intention: A multigroup analysis between Indonesia and Malaysia. Cogent Business & Management, 7(1), 1804181. https://doi.org/10.1080/23311975.2020.1804181

- Ajzen, I. (1985). From intentions to actions: A theory of planned behavior Action control. Springer.

- Alalwan, A. A., Dwivedi, Y. K., & Rana, N. P. (2017). Factors influencing adoption of mobile banking by Jordanian bank customers: Extending UTAUT2 with trust. International Journal of Information Management, 37(3), 99–20. https://doi.org/10.1016/j.ijinfomgt.2017.01.002

- Arning, K., & Ziefle, M. (2009 November). Different perspectives on technology acceptance: The role of technology type and age. n Symposium of the Austrian HCI and usability engineering group (pp. 20-41). Springer, Berlin, Heidelberg.

- Azjen, I. (1980). Understanding attitudes and predicting social behavior. Englewood Cliffs.

- Baptista, G., & Oliveira, T. (2015). Understanding mobile banking: The unified theory of acceptance and use of technology combined with cultural moderators. Computers in Human Behavior, 50, 418–430. https://doi.org/10.1016/j.chb.2015.04.024

- Becker, J.-M., Klein, K., & Wetzels, M. (2012). Hierarchical latent variable models in PLS-SEM: Guidelines for using reflective-formative type models. Long Range Planning, 45(5–6), 359–394. https://doi.org/10.1016/j.lrp.2012.10.001

- Brown, S. A., & Venkatesh, V. (2005). A model of adoption of technology in the household: A baseline model test and extension incorporating household life cycle. Management Information Systems Quarterly, 29(3), 11. https://doi.org/10.2307/25148690

- Chan, K. Y., Gong, M., Xu, Y., & Thong, J. (2008). Examining user acceptance of SMS: An empirical study in China and Hong Kong. PACIS 2008 Proceedings, 294 https://citeseerx.ist.psu.edu/viewdoc/download?doi=10 .1.1.930.6274&rep=rep1&type=pdf.

- Childers, T. L., Carr, C. L., Peck, J., & Carson, S. (2001). Hedonic and utilitarian motivations for online retail shopping behavior. Journal of Retailing, 77(4), 511–535. https://doi.org/10.1016/S0022-4359(01)00056-2

- Churchill, G. A., Jr. (1979). A paradigm for developing better measures of marketing constructs. Journal of Marketing Research, 16(1), 64–73. https://doi.org/10.1177/002224377901600110

- Cimperman, M., Brenčič, M. M., & Trkman, P. (2016). Analyzing older users’ home telehealth services acceptance behavior—applying an Extended UTAUT model. International Journal of Medical Informatics, 90, 22–31 doi:10.1016/j.ijmedinf.2016.03.002. https://www.sciencedirect.com/science/article/abs/pii/S1386505616300338?via%3Dihub

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319–340 doi:10.2307/249008. https://www.koreascience.or.kr/article/JAKO202031064817089.view?orgId=kodisa

- DO, N. B., & DO, H. N. T. (2020). An investigation of generation Z’s intention to use electronic wallet in Vietnam. The Journal of Distribution Science, 18(10), 89–99.

- Escobar-Rodríguez, T., & Carvajal-Trujillo, E. (2014). Online purchasing tickets for low cost carriers: An application of the unified theory of acceptance and use of technology (UTAUT) model. Tourism Management, 43, 70–88 doi:10.1016/j.tourman.2014.01.017. https://www.sciencedirect.com/science/article/abs/pii/S0261517714000181?via%3Dihub

- Fishbein, M., & Ajzen, I. (1977). Belief, attitude, intention, and behavior: An introduction to theory and research. Philosophy and Rhetoric, 10(2 130–132).

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Gefen, D. (2000). E-commerce: the role of familiarity and trust. Omega, 28(6), 725–737

- Gefen, D. (2000). E-commerce: the role of familiarity and trust. Omega, 28(6), 725–737.

- Gefen, D., & Straub, D. W. (1997). Gender differences in the perception and use of e-mail: An extension to the technology acceptance model. MIS Quarterly, 21(4), 389–400. https://doi.org/10.2307/249720

- Gelb, A., & Mukherjee, A. (2020). Digital technology in social assistance transfers for COVID-19 relief: Lessons from selected cases. CGD Policy Paper, 181 https://www.ictworks.org/wp-content/uploads/2020/09/lessons-learned-digital-technology-social-assistance-programs.pdf.

- Gupta, B., Dasgupta, S., & Gupta, A. (2008). Adoption of ICT in a government organization in a developing country: An empirical study. The Journal of Strategic Information Systems, 17(2), 140–154. https://doi.org/10.1016/j.jsis.2007.12.004

- Hair, J. F., Jr, Sarstedt, M., Hopkins, L., & Kuppelwieser, V. G. (2014). Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. European Business Review 26(2) 106–121 doi:10.1108/EBR-10-2013-0128 .

- Hair, J. F., Jr, Sarstedt, M., Ringle, C. M., & Gudergan, S. P. (2017). Advanced issues in partial least squares structural equation modeling: SaGe publications https://us.sagepub.com/en-us/nam/advanced-issues-in-partial-least-squares-structural-equation-modeling/book243803#preview.

- Heijden, H. (2004). User acceptance of hedonic information systems. MIS Quarterly, 28(4), 695–704. https://doi.org/10.2307/25148660

- Henseler, J., Hubona, G., & Ray, P. A. (2016). Using PLS path modeling in new technology research: Updated guidelines. Industrial Management & Data Systems, 116(1), 2–20. https://doi.org/10.1108/IMDS-09-2015-0382

- Hong, S., Thong, J. Y., & Tam, K. Y. (2006). Understanding continued information technology usage behavior: A comparison of three models in the context of mobile internet. Decision Support Systems, 42(3), 1819–1834. https://doi.org/10.1016/j.dss.2006.03.009

- Hongxia, P., Xianhao, X., & Weidan, L. (2011). Drivers and barriers in the acceptance of mobile payment in China. Paper presented at the 2011 International Conference on E-business and E-government (ICEE) (Shanghai, China: ICEE).

- Jesuthasan, S., & Umakanth, N. (2021). Impact of behavioural intention on E-wallet usage during Covid-19 period: A study from Sri Lanka. Sri Lanka Journal of Marketing, 7(2), 24. https://doi.org/10.4038/sljmuok.v7i2.63

- Khalilzadeh, J., Ozturk, A. B., & Bilgihan, A. (2017). Security-related factors in extended UTAUT model for NFC based mobile payment in the restaurant industry. Computers in Human Behavior, 70, 460–474. https://doi.org/10.1016/j.chb.2017.01.001

- Kijsanayotin, B., Pannarunothai, S., & Speedie, S. M. (2009). Factors influencing health information technology adoption in Thailand’s community health centers: Applying the UTAUT model. International Journal of Medical Informatics, 78(6), 404–416. https://doi.org/10.1016/j.ijmedinf.2008.12.005

- Kim, H.-W., & Kwahk, K.-Y. (2007). Comparing the usage behavior and the continuance intention of mobile Internet services. Paper presented at the Eighth World Congress on the Management of eBusiness (WCMeB 2007) (Toronto, Canada).

- Kim, J., & Park, H.-A. (2012). Development of a health information technology acceptance model using consumers’ health behavior intention. Journal of Medical Internet Research, 14(5), e133. https://doi.org/10.2196/jmir.2143

- Lee, T. (2005). The impact of perceptions of interactivity on customer trust and transaction intentions in mobile commerce. Journal of Electronic Commerce Research, 6(3), 165 http://www.jecr.org/sites/default/files/06_3_p01.pdf.

- Likert, R. (1932). A technique for the measurement of attitudes. Archives of Psychology.

- Limayem, M., Hirt, S. G., & Cheung, C. M. (2007). How habit limits the predictive power of intention: The case of information systems continuance. MIS Quarterly, 31(4), 705–737. https://doi.org/10.2307/25148817

- Liu, G.-S., & Tai, P. T. (2016). A study of factors affecting the intention to use mobile payment services in Vietnam. Economics World, 4(6), 249–273 http://www.davidpublisher.com/Public/uploads/Contribute/5795c20c3bdc3.pdf.

- Neufeld, D. J., Dong, L., & Higgins, C. (2007). Charismatic leadership and user acceptance of information technology. European Journal of Information Systems, 16(4), 494–510. https://doi.org/10.1057/palgrave.ejis.3000682

- Nunnally, J. C. (1978). Psychometric Theory (2nd ed.). Mcgraw hill book company.

- Or, C. K., Karsh, B.-T., Severtson, D. J., Burke, L. J., Brown, R. L., & Brennan, P. F. (2011). Factors affecting home care patients’ acceptance of a web-based interactive self-management technology. Journal of the American Medical Informatics Association, 18(1), 51–59. https://doi.org/10.1136/jamia.2010.007336

- Putri, D. A. (2018). Analyzing factors influencing continuance intention of e-payment adoption using modified UTAUT 2 model. Paper presented at the 2018 6th International Conference on Information and Communication Technology (ICoICT) (Bandung, Indonesia https://www.icoict.org/wp-content/uploads/sites/5/2017/10/Call-For-Papers-ICoICT-2018.pdf).

- Qasim, H., & Abu-Shanab, E. (2016). Drivers of mobile payment acceptance: The impact of network externalities. Information Systems Frontiers, 18(5), 1021–1034. https://doi.org/10.1007/s10796-015-9598-6

- Revathy, C., & Balaji, P. (2020). Determinants of behavioural intention on E-Wallet usage: An empirical examination in amid of Covid-19 lockdown period. International Journal of Management (IJM), 11(6), 92–104 10.34218/IJM.11.6.2020.008.

- Rogers, E. M. (1976). New product adoption and diffusion. Journal of Consumer Research, 2(4), 290–301. https://doi.org/10.1086/208642

- Saraswati, D. A., Desvi, P. S., Putra, N. S., & Hendriana, E. (2021). Examination of the extended UTAUT model in mobile wallet continuous usage intention during the COVID-19 outbreak Turkish Online Journal of Qualitative Inquiry (TOJQI) 12(6) https://www.researchgate.net/profile/Praditta-Desvi/publication/354754021_Examination_of_the_Extended_UTAUT_Model_in_Mobile_Wallet_Continuous_Usage_Intention_during_the_COVID-19_Outbreak/links/614b2035a595d06017e18523/Examination-of-the-Extended-UTAUT-Model-in-Mobile-Wallet-Continuous-Usage-Intention-during-the-COVID-19-Outbreak.pdf .

- Shilpi Saraswat, M. M. (2017). Cashless transaction: Challenges faced by the consumers. International Journal of Research Culture Society, 10(1) 228–236 http://ijrcs.org/wp-content/uploads/201712042.pdf .

- Shin, D.-H. (2009). Towards an understanding of the consumer acceptance of mobile wallet. Computers in Human Behavior, 25(6), 1343–1354. https://doi.org/10.1016/j.chb.2009.06.001

- Shou, Y., & Smithson, M. (2015). Evaluating predictors of dispersion: A comparison of dominance analysis and Bayesian model averaging. Psychometrika, 80(1), 236–256. https://doi.org/10.1007/s11336-013-9375-8

- Slade, E., Williams, M., Dwivedi, Y., & Piercy, N. (2015). Exploring consumer adoption of proximity mobile payments. Journal of Strategic Marketing, 23(3), 209–223. https://doi.org/10.1080/0965254X.2014.914075

- Sun, Y., Bhattacherjee, A., & Ma, Q. (2009). Extending technology usage to work settings: The role of perceived work compatibility in ERP implementation. Information & Management, 46(6), 351–356. https://doi.org/10.1016/j.im.2009.06.003

- Tamilmani, K., Rana, N. P., & Dwivedi, Y. K. (2020). Consumer acceptance and use of information technology: A meta-analytic evaluation of UTAUT2. Information Systems Frontiers 23(4) , 1–19 doi:10.1007/s10796-020-10007-6.

- Taylor, S., & Todd, P. (1995). Decomposition and crossover effects in the theory of planned behavior: A study of consumer adoption intentions. International Journal of Research in Marketing, 12(2), 137–155. https://doi.org/10.1016/0167-8116(94)00019-K

- Thakur, R. (2013). Customer adoption of mobile payment services by professionals across two cities in India: An empirical study using modified technology acceptance model. Business Perspectives and Research, 1(2), 17–30. https://doi.org/10.1177/2278533720130203

- Thompson, R. L., Higgins, C. A., & Howell, J. M. (1991). Personal computing: Toward a conceptual model of utilization. MIS Quarterly, 15(1), 125–143. https://doi.org/10.2307/249443

- Venkatesh, V., Morris, M. G., & Ackerman, P. L. (2000). A longitudinal field investigation of gender differences in individual technology adoption decision-making processes. Organizational Behavior and Human Decision Processes, 83(1), 33–60. https://doi.org/10.1006/obhd.2000.2896

- Venkatesh, V., Morris, M. G., Davis, G. B., & Davis, F. D. (2003). User acceptance of information technology: Toward a unified view. MIS Quarterly, 27(3), 425–478. https://doi.org/10.2307/30036540

- Venkatesh, V., Thong, J. Y., & Xu, X. (2012). Consumer acceptance and use of information technology: extending the unified theory of acceptance and use of technology. MIS quarterly, 157–178 MIS quarterly.

- Venkatesh, V., Thong, J. Y., & Xu, X. (2012). Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology. MIS Quarterly, 36(1), 157–178. https://doi.org/10.2307/41410412

- Verkijika, S. F. (2018). Factors influencing the adoption of mobile commerce applications in Cameroon. Telematics and Informatics, 35(6), 1665–1674. https://doi.org/10.1016/j.tele.2018.04.012

- Williams, M. N., Grajales, C. A. G., & Kurkiewicz, D. (2013). Assumptions of multiple regression: Correcting two misconceptions. Practical Assessment, Research, and Evaluation, 18(1), 11 doi:10.7275/55hn-wk47.

- Wong, C. Y., & Mohamed, M. I. P. (2021). Understanding the factors that influence consumer continuous intention to use E-wallet In Malaysia. Research in Management of Technology and Business, 2(1), 561–576 doi:10.30880/rmtb.2021.02.01.042.

- Wu, J. J., & Chang, Y. S. (2005). Towards understanding members’ interactivity, trust, and flow in online travel community. Industrial Management & Data Systems, 105(7), 937–954. https://doi.org/10.1108/02635570510616120

- Zhanyou, W., Dongmei, H., & Yaopei, Z. (2020). How to improve users’ intentions to continued usage of shared bicycles: A mixed method approach. PLoS one, 15(2), e0229458.

- Zhanyou, W., Dongmei, H., Yaopei, Z., & Kato, H. (2020). How to improve users’ intentions to continued usage of shared bicycles: A mixed method approach. PLoS One, 15(2), e0229458. https://doi.org/10.1371/journal.pone.0229458

- Zmijewska, A., Lawrence, E., & Steele, R. (2004). Towards understanding of factors influencing user acceptance of mobile payment systems. Icwi, 2004, 270–277 https://www.researchgate.net/publication/220969444_Towards_Understanding_of_Factors_Influencing_User_Acceptance_of_Mobile_Payment_Systems.