?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The paper investigates the long run dynamics of money supply, budget deficit and inflation in Ghana. It also tests the validity of the classical, monetary and fiscal theories of price level within the vector error correction framework. Using quarterly data from 1999Q1 to 2019Q4, the paper employs Granger causality test and the vector error correction model (VECM) for the analysis. The results from the VECM show that budget deficit has a significant positive effect on inflation while money supply negatively affect it. By contrast, inflation exerts a positive and negative effect on budget deficit and money supply, respectively. The results from the impulse response function also indicate that inflation responds more positively to budget deficit shocks. However, it tends to respond negatively to money supply (M2) shocks. Also, budget deficit responds positively (negatively) to inflation (money supply [M2]) shocks. Furthermore, money supply responds positively (negatively) to budget deficit (inflation) shocks. Based on the weak exogeneity test, the result favours the fiscal theory of the price level in explaining the nexus between money supply, budget deficit and inflation in Ghana. A corollary of our results is that a reduction in government expenditure coupled with restrictive bureaucratic nature of government officials have the tendency of ensuring favourable and stable inflation in Ghana.

PUBLIC INTEREST STATEMENT

The dynamics of money supply, budget deficit and inflation continue to receive attention from both theoretical and empirical perspectives considering the negative repercussions inflation is likely to have on economies as well as the livelihood and welfare of the citizenry. Several studies have investigated the phenomenon in the Ghanaian context but fail to incorporate the key assumption regarding the exogenous property of money supply and budget deficit in explaining inflation. Therefore, the present study contributes to knowledge by incorporating the exogeneity test into the analysis to establish the exogenous property of money supply and budget deficit. This helps to completely ascertain the dynamics of money supply, budget deficit and inflation. The results show that budget deficit has a significant positive effect on inflation while money supply negatively affect it. Based on the weak exogeneity test, the result favours the fiscal theory of the price level in explaining the nexus between money supply, budget deficit and inflation in Ghana.

1. Introduction

The dynamics of money supply, budget (fiscal) deficit and inflation continue to receive attention from both theoretical and empirical perspectives considering the negative repercussions inflation is likely to have on economies (Adom et al., Citation2018), as well as the livelihood and welfare of citizens. Inflation is perceived to be a key macroeconomic indicator as it influences major decisions such as investment, consumption and savings among others. Inflation also renders the execution of some major policies or projects unsuccessful as it affects the budget allocation, and this ultimately retards the progress of an economy. In the Ghanaian context, successive governments have attempted to maintain a single digit as well as stable inflation rate with the aim of improving the wellbeing of citizenry and enhancing savings and investment decisions. However, these efforts have proven futile as inflation rate in the economy continues to fluctuate and remains double digit. For instance, inflation rate in Ghana averaged 22.40, 13.18, 11.50 and 12.91 percent for the periods 1999–2003, 2004–2008, 2009–2013 and 2014–2019, respectively (World Bank, Citation2019). Furthermore, the average inflation rate from 1999 to 2019 was 15.02%. This clearly indicates that inflation has not been stable and therefore could adversely affect major economic decisions. Given this, it is therefore prudent to ascertain the determinants of inflation in the Ghanaian economy for effective policy purposes; hence, the need for the present study.

From theoretical standpoint, the Classicalists and Monetarists have based their arguments regarding the nexus between money supply, budget deficit and inflation on what is known as the quantity theory of money, whereas that of the fiscal theory of the price level (FTPL) has been based on the quantity theory of government debt. These notwithstanding, the Keynesians and the Structuralists have argued differently about the nexus and dynamics among these macroeconomic variables. The Keynesians believe that inflation is caused by excessive demand oppressions in an economy, whereas the Structuralists argue that inflation in underdeveloped and developing countries is due to structural (economic and social) characteristics of an economy.

The diverse views among these school of thoughts have drawn the attention of researchers and policymakers in various economies to empirically test the dynamics proposed by these theories to ensure that appropriate measures or policies are put in place to curb inflation. In view of that, many scholars have extensively explored the relationship between money supply, budget deficit and inflation in both developing and developed countries with mixed results (Adom et al., Citation2015; Adu & Marbuah, Citation2011; Ahiabor, Citation2013; Anantha Ramu, Citation2014; Boamah, Citation2019; Chiaraah & Nkegbe, Citation2014; Gyebi & Boafo, Citation2013; Kovanen, Citation2011; Lin & Chu, Citation2013; Nasir et al., Citation2020a, Citation2020b; Nguyen, Citation2015).

This paper contributes to knowledge and extant literature by way of validating existing studies on the nexus between money supply, budget deficit and inflation in the Ghanaian context. This study also fills the lacuna that has been created regarding the links between these variables by considering the long run relationship between money supply, budget deficit and inflation. The reason for focusing primarily on the long run relationship is because the short run relationship may not be sufficient (though necessary) for effective policy discourse and therefore could render policies unsuccessful in an economy. Furthermore, the present study tests the validity of classical theory, monetarist theory and the fiscal theory of the price level within the context of Ghana.

Specifically on Ghana, studies (see: Sowa, Citation1994; Ghartey, Citation2001; Bawumia and Abradu-Otoo, Citation2003; Adu & Marbuah, Citation2011; Kovanen, Citation2011; Ahiabor, Citation2013; Gyebi & Boafo, Citation2013; Chiaraah & Nkegbe, Citation2014; Adom et al., Citation2015; Ibn Boamah, Citation2019) have examined the causal links between money supply, budget deficit and inflation. Results from these studies are mixed and have mostly considered the nexus using annual data, thereby ignoring how budget deficit and money supply influence inflation, and vice versa using quarterly data. Considering high-frequency data (quarterly data) is very important because it is likely to change the dynamics that exist among budget deficit, money supply and inflation and therefore could have a significant impact on policy implementation and hence, the present study becomes very essential. Another key contribution of the present study is the exogeneity test it incorporates in the analysis, which has been ignored in all previous studies (Sowa, Citation1994; Ghartey, Citation2001; Bawumia and Abradu-Otoo, Citation2003; Adu & Marbuah, Citation2011; Kovanen, Citation2011; Ahiabor, Citation2013; Gyebi & Boafo, Citation2013; Chiaraah & Nkegbe, Citation2014; Adom et al., Citation2015; Ibn Boamah, Citation2019). In understanding the relationship between money supply, budget deficit and inflation, an exogeneity analysis is very key in explaining the theoretical links. The neglect of the exogeneity property of money supply and budget (fiscal) deficit contradicts theoretical views on money supply and budget (fiscal) deficit. For instance, according to the classical and monetarist theories, money supply is exogenously determined by the monetary authorities, and hence inflation is everywhere a monetary phenomenon. By contrast, fiscal deficit, which is perceived to cause inflation in the long run, is assumed to be exogenous by the fiscal theory of the price level and the monetarist hypothesis. Thus, a test of exogeneity of these two variables in explaining inflation dynamics is crucial to understanding precisely the theoretical arguments espoused in the literature. More tersely, the paper seeks to test (using the weak exogeneity test) which of the theories is more relevant in explaining inflation dynamics in Ghana.

We find that budget deficit has a significant positive effect on inflation while money supply negatively affects it. By contrast, inflation exerts a positive and negative effect on budget deficit and money supply, respectively. Based on the weak exogeneity test, the result favours the fiscal theory of the price level in explaining the nexus between money supply, budget deficit and inflation in Ghana.

The rest of the paper is structured as follows: Section 2 reviews the theoretical and empirical literature, whiles Section 3 presents the data and empirical strategy used in the study. Section 4 presents the empirical results and the discussion thereof. Section 5 concludes the paper with some policy implications.

2. Theoretical and empirical literature review

Several theories related to the dynamics of money supply, budget deficit and inflation have emerged in monetary economics. This section provides a brief review of theories as well as earlier studies on money supply, budget deficit and inflation nexus. With respect to the theoretical underpinning, the classical theory, the monetarist hypothesis (MH) and the fiscal theory of the price level (FTPL), the Keynesian approach and the Structuralist theory of inflation are reviewed.

The classical theory, based on the quantity theory of money, argues that the quantity of nominal money supply, which is exogenously determined is sorely responsible for changes in the general price level (inflation) in an economy. Thus, changes (increase and decrease) in the nominal money supply directly leads to a change in the general price level at an equal proportion. The theory further argues that the real sector operates independently from the monetary sector, and for that matter, real wages are determined in the real sector whiles changes in nominal money supply determine the nominal wages. Therefore, real output in an economy is not influenced by an increase in nominal money supply but general price level (inflation) rises when nominal money supply increases. The classical theory therefore views inflation as a monetary phenomenon.

The monetarist hypothesis (theory), just like the classical theory, is based on the quantity theory of money, which requires that the price level is determined (controlled) by the nominal money supply. The proponents argue that the general price level is exclusively determined as the price that ensures that the desired level of real balances equals the purchasing power of the nominal money supply at any given level of nominal money supply, which is determined (exogenously) by the monetary authority. The implication is that deviation of nominal money supply from the desired real balances (given any price level) will channel into changes in the price level. Notwithstanding, the monetarists further posit that budget deficit is the cause of inflation through money supply. The reason is that a budget deficit financed by monetary authority (Central Bank) through seigniorage (printing of money by the central bank) or financing government expenditure through the open market operation (purchase of government interest-bearing securities) changes the nominal money supply in an economy and hence changes in the general price level. Given this, Friedman (Citation1963) argues that inflation is always and everywhere a monetary phenomenon.

The fiscal theory of the price level (FTPL) also known as the quantity theory of government debt analyzes how fiscal (budget) deficit feeds through general price level in different mechanism other than that of the monetarist approach. The FTPL considers the government’s intertemporal budget constraint (GBC) as an instrument that links both fiscal and monetary policies. According to the FTPL, the GBC is at equilibrium when the discounted value of the government’s future primary surplus (which includes seigniorage as a revenue source) is greater than (equal to) the current nominal value of the government (public) debt, which considers the monetary base. The proponents opine that the discount rate is measured by the ratio of real interest rate to the growth rate of the economy. The FTPL assumes that the future path of revenues and primary expenditures is determined exogenously by fiscal authority. The theory further argues that, at a given discount rate, the price level will rise to equilibrate the GBC condition anytime the discounted value of primary surplus is lower than the value of nominal public debt. Therefore, price is the only adjustment variable to maintain equilibrium condition in the GBC.

To understand how the price level is affected by fiscal policy, Woodford (Citation1995) suggests that a positive and exogenous price shock reduces the value of government debt (liabilities) owed to private individuals who have purchased or invested in government securities which in turn lowers their wealth as well as demand for goods. The FTPL theory postulates that, when this happens, the individual’s expectations with respect to the sustainability of fiscal policy will generate similar wealth-effect. If the market recognizes a negative perception about the sustainability of public finances (when discounted value of government primary surplus deviate from the nominal value of government liabilities), such negative perception will trigger an increase in the level of price to a higher level required to equalize the GBC. This higher price lowers the value of private assets, which generates the abovementioned wealth-effect. Therefore, higher government debt (liabilities) generates higher distortion, and hence, higher prices are required to restore the GBC. The implication is that budget deficit causing long run inflation with money supply playing no role may establish a strong backing for the FTPL as indicated by Lozano-Espitia and Lozano-Espitia (Citation2008).

On the contrary, the Keynesian approach to determination of inflation is subjected to excessive demand dominations, which assumes that the economy is at full employment. Keynes argues that firms generate more profit at a fixed nominal wages when there exists excess demand at full employment level. As result, firms demand for labour increases with the aim of meeting the growing demand in the economy, which in turn leads to higher wages paid by firms. As documented by Kotwal (Citation1987) and Frisch (Citation1989)), the higher wages increase the general price level as cost of production increases and hence inflation arise. The structuralist theory of inflation on the other hand attributes inflation in underdeveloped and developing countries to the structural characteristics (economic and social structure) in the process of economic growth but not monetary factors as argued by the classical and the monetarist economists. Given the idea of structuralism, early contributors like Noyola (Citation1956), Sunkel (1Citation958), Olivera (Citation1964) and Chenery (Citation1975) argued that aggregate demand in an economy increases in periods of rapid economic growth and development but the increase in the aggregate supply does not match the increase in aggregate demand. These contributors therefore posit that the gap is because of structural bottlenecks. Arndt (Citation1985) indicates that the gap between aggregate demand and supply caused by the structural bottlenecks results in inflationary pressure in the economy. Thus, the overall price level in the economy increases due to shortage of goods as the economy grows and develops.

The conflicting propositions by the aforementioned theories have therefore inspired many researchers to empirically analyze the causal effect of money supply, budget deficit and inflation in both developing and developed world.

Specifically, on Ghana, studies have been conducted to analyze the dynamics among money supply, budget deficit and inflation. For instance, Sowa (Citation1994) examined the relationship between fiscal deficits, output growth and inflation targets for the period 1965 to 1991 using the error correction model (ECM) as estimation technique. The results revealed that nominal money (M0) and real income have a significant positive impact on inflation, whereas exchange rate tend to have a positive significant impact on inflation. The study further indicated that, for periods with consistent fiscal deficit or policy (inconsistent fiscal deficit), inflation tends to be within target (above target).

Also, Ghartey (Citation2001) investigated macroeconomic instability and inflationary financing nexus using quarterly time series data covering the period 1970 to 1992. Employing the pair-wise Granger causality test and vector error correction model (VECM) for the analysis, the study showed that monetary base and currency ratio cause inflation and real output growth and inflation also cause exchange rate growth. Real output growth is revealed to have a bi-directional causal relationship with money supply growth, monetary base, currency ratio, budget deficit as a percentage of GDP, and inflation. Similarly, using annual time series data spanning 1983 to 1999, Bawumia and Abradu-Otoo (Citation2003) explored the relationship between monetary growth, exchange rates and inflation. The results from the error correction model showed that money supply (M2+) and exchange rate have a significant positive relationship with inflation, whereas the effect of real income on inflation is revealed to be negative and significant.

Using the ordinary least squares and generalized method of moments estimation techniques, Kovanen (Citation2011) investigated whether money matter for inflation using quarterly time series data spanning 1990 to 2009. The study revealed that inflation gap and real output gap have a positive and significant effect on inflation. Real money gap and nominal money gap are also found to have insignificant negative effect on inflation in both estimation techniques. Currency depreciation is also found to have significant negative (significant positive) effect on inflation in four quarters (eight quarters) in both the OLS and GMM estimators. Also, Adu and Marbuah (Citation2011) employed the autoregressive distributed lag (ARDL) model to examine the determinants of inflation using annual time series data over the period 1960 to 2009. The study showed that money supply (M1, M2 and M3) has a significant positive influence on inflation in both the long and short run. The relationship between fiscal deficit and inflation is revealed to be insignificant in the long run but positive and significant in the short run. Exchange rate is found to exert significant negative (insignificant positive) effect in the long run (short run). The study further showed that, while interest rate impacted positively on inflation, real output is found to have a significant negative effect on inflation in both the long- and short-run.

In a related study, Adom et al. (Citation2015) analyzed inflation dynamics using annual time series data covering the period 1960 to 2012. The study employed the fully modified ordinary least squares (FMOLS) estimation technique for the analysis. The study concluded that money supply exerts a positive significant impact on inflation, whereas fiscal deficit has insignificant effect on inflation. Crude oil price and interest rate are found to have positive and significant effect on inflation. Food production index is revealed to impact negatively on inflation. The results further indicated that output growth and exchange rate have insignificant effect on inflation. Similarly, Adjei (Citation2018) explored the monetarists’ theory on inflation determinants using annual time series data spanning 1965 to 2012. Applying the autoregressive distributed lag (ARDL) model as the estimation technique, the study found that broad money (M2) growth and broad money as a percentage of GDP have a significant positive relationship with inflation in the long run. In the short-run, only broad money growth is revealed to have significant positive effect on inflation and broad money as a percentage of GDP impacts negatively on inflation. The results further showed that import of goods and services have insignificant negative (significant positive) effect on inflation in the long run (short run), whereas GDP per capital growth exert a negative and significant (positive and significant) impact on inflation in the long run (short run). Domestic credit to the private sector is found to have insignificant effect on inflation in both the long and short run.

Furthermore, Boamah (Citation2019) investigated inflation dynamics using annual time series data from 1972 to 2016, and the ordinary least squares (OLS) and error correction model (ECM) are applied to the dataset. The results from the OLS revealed that money supply (M2), real effective exchange rate, foreign price and nominal interest rate exert a significant positive impact on inflation. The results from the ECM also showed that real effective exchange rate, foreign price and nominal interest rate have a significant positive effect on inflation, whereas money supply (real income per capita) is found to exert insignificant positive (significant negative) effect on inflation.

In Colombia, Lozano-Espitia and Lozano-Espitia (Citation2008) examined the relationship between budget deficit, money growth and inflation in Colombia. The study employs quarterly (annual) time series data from the period 1982Q1 to 2007Q4 (1955 to 2007) and applies the vector error correction model to the dataset. The results from the quarterly data showed that money growth (M0, M1 and M3) has a positive and significant impact on inflation, and inflation also affects money growth positively. The results further indicate that budget deficit has a significant positive effect on money growth (M1). The result from the annual data is, however, not different from the quarterly data except for budget deficit having insignificant effect on both inflation and money growth (M0, M1 and M3).

Employing time series data from the period 1967 to 2010, Ndanshau (Citation2012) investigated the nexus between budget deficits, money supply and inflation in Tanzania. The pair-wise Granger causality test and vector error correction model (VECM) are used for the analysis. The study showed that inflation Granger causes budget deficit, budget deficit Granger causes money supply (M0), money supply (M1) Granger causes inflation, inflation Granger causes money supply (M0) and inflation Granger causes budget deficit when deflated with monetary base (M0). The VECM results revealed that budget deficit has insignificant positive effect on inflation, but inflation exerts significant negative effect on budget deficit. Policy regime is also revealed to exert a positive and significant effect on both inflation and budget deficit.

Similarly, Lin and Chu (Citation2013) employed the dynamic panel quantile regression (DPQR) model under the autoregressive distributional lag (ARDL) specification to examine deficit–inflation relationship in 91 countries (OCED and non OCED) for the period 1960 to 2006. The results showed that current and lagged deficit have positive and significant impact on inflation. DPQR results with additional explanatory variables revealed that deficit and oil price inflation have a positive and significant effect on inflation, whereas trade openness has significant negative relationship with inflation. The effect of real GDP growth is insignificant. With regard to separate OCED and non-OCED country analysis, the results showed that deficit, real GDP growth and oil price exert a significant positive impact on inflation, whereas the effect of trade openness is negative in OCED countries. For the non-OCED countries, the study shows that deficit and oil price have significant positive effect on inflation, but the effect of real GDP growth and trade openness is negative and significant. In a related study, Anantha Ramu (Citation2014) investigated the relationship between fiscal deficit and inflation in India using time series data from the period 1980–81 to 2011–12. The results from the autoregressive distributed lag (ARDL) model indicated that gross fiscal deficit, interest rate and oil import price have a significant positive effect on inflation, whereas the effect of exchange rate and GDP growth rate are negative and significant. Money supply growth rate is found to have insignificant positive impact on inflation.

Also, Nguyen (Citation2015) examined the effect of fiscal deficit and money supply (M2) on inflation in selected economies (Bangladesh, Cambodia, Indonesia, Malaysia, Pakistan, Philippines, Sri Lanka, Thailand and Vietnam) of Asia. Using time series data from the period 1985 to 2012, the study applies the pooled mean group (PMG) estimation-based error correction model and the panel differenced GMM estimation techniques. The results from the PMG indicated that fiscal deficit and money supply (M2) have a significant positive effect on inflation in long run, but in the short run, only money supply has significant negative effect on inflation, and the effect of fiscal deficit is insignificant. The outcome from the GMM also showed that fiscal deficit has significant positive effect on inflation, whereas the effect of money supply is revealed to be insignificant. Also, whereas government expenditure and interest rate exert significant positive effect on inflation, the effect of real GDP per capita, exchange rate and trade openness are insignificant in both PMG and GMM estimators.

More recently, Nasir et al. (Citation2020a) examined inflation expectations in the face of oil shocks for New Zealand and United Kingdom from the period January 1984 to June 2018. The results from the non-linear autoregressive distributed lag (NARDL) model indicated that real effective exchange rate has a significant negative relationship with inflation expectations in both the short- and long-run for both countries. The results further revealed that inflation, real effective exchange rate, money supply, output growth, unemployment and fiscal deficit/surplus have significant implications for inflation expectations for the two countries. Further, Nasir et al. (Citation2020b) investigated the exchange rate pass-through and management of inflation expectations for Czech Republic using the NARDL. The outcome of the study showed that real effective exchange rate has a significant negative relationship with inflation expectations in both the short- and long-run. However, the relationship between inflation expectations and oil price shocks is positive but insignificant in both periods. Fiscal stance and money supply are also revealed to have insignificant negative relationship with inflation expectations in both periods.

Indisputably, evidence from past studies on Ghana and other parts of the world have revealed mixed (inconclusive) results regarding budget deficit, money supply and inflation dynamics; hence, further research on the subject matter becomes imperative as far as validity of previous outcomes is concerned. Again, it is evident that studies on Ghana that use quarterly data for the analysis rarely exist. Mention can only be made to studies by Ghartey (Citation2001) and Kovanen (Citation2011). Given the fact that high frequency data (quarterly) has the tendency of changing the dynamics that exist among budget deficit, money supply and inflation, as well as having significant impact on policy implementation, it is therefore worthwhile for studies to focus on high frequency data in such analysis, and the present study seeks to contribute to literature in that direction. It is also revealed from the empirical review that none of the studies, especially those on Ghana, incorporates the exogeneity test in the analysis, and this renders these studies incomplete to a greater extent. This is so because, the major issue about the exogenous nature of the determinants of inflation such as money supply and budget deficit, which theories postulate, is ignored. The present study therefore incorporates this major test in the analysis to fully ascertain the validity of the theories that seek to explain the nexus between budget deficit, money supply and inflation, and this is a key contribution of this study to existing literature.

3. Methodology and data

This section presents the theoretical and methodological framework, as well as data and estimation technique the study employs. The section is divided into three parts. The first part presents the theoretical framework and model specification. The second part focuses on the estimation strategy, whereas the third part presents the data and variable description.

3.1. Theoretical framework and model specification

The study adopts a theoretical model of inflation with the aim of identifying the important factors that influence inflation in a small open economy like Ghana. Inflation, measured as the percentage change in the overall (general) price level of goods and services, is defined as the persistent (sustained) increase in the overall price level of goods and services in an economy. The model assumes a small open economy, where the general price level is given as the weighted average of the price of tradable goods () and the price of non-tradable goods (

), which is expressed in Equationequation (1)

(1)

(1) .

where γ is the weight of tradable goods and lies within zero and one (0 < γ < 1).

In the model of small open economy, the world market determines the price of tradable goods (), which depends on foreign price (

) assumed as given and exchange rate (ER). By incorporating the purchasing power parity, price of tradable good can then be express as follows:

Taking logarithm of Equationequation (2)(2)

(2) then gives Equationequation (3)

(3)

(3) .

Since a small open economy’s influence in the world market is completely insignificant, foreign price is treated as given, which without loss of generality is normalized to one, and hence exchange rate becomes the only determinant of the price of tradable goods, which is specified in Equationequation (4)(4)

(4) .

The implication of Equationequation (4)(4)

(4) is that changes in exchange rate may cause the price of tradable goods to change by the same proportion, especially if the economy is import dependent. EquationEquation (4)

(4)

(4) also indicates that exchange rate plays very crucial role in determining domestic inflation (as depreciation leads to domestic inflation), hence a partial exchange rate pass-through effect on domestic prices (see: Amoah & Aziakpono, Citation2018).

The model further assumes that the domestic money market on the other hand determines the price of non-tradable goods, where the demand for non-tradable goods is assumed, for simplicity, to move together with the overall demand of the economy. The implication is that the money market equilibrium (which requires equalization between real money supply and real money balances) determines the price of non-tradable goods. This is expressed in Equationequation (5)(5)

(5) .

where δ is a scale factor denoting the relationship between demand for non-tradable goods and aggregate demand of the economy. The demand for real money balances is assumed to depend on real income and inflationary expectations. Interest rate, also being the opportunity cost of money, determines the demand for money. Therefore, the demand function for real money balances can be represented as follows.

where Y, and I denote real income, expected inflation rate and nominal interest rate, respectively. Demand for money theory assumes that there exists a positive relationship between real income, expected inflation and demand for real money, whereas on the other hand, the relationship between real money demand and interest rate is assumed to be negative. Based on Ubide (Citation1997), Laryea and Sumaila (Citation2001), Adu and Marbuah (Citation2011), and Adom et al. (Citation2015), the study specifies the following inflationary expectation equation.

where L() denotes a distributed lag learning process for economic agents (consumer and producer). Without loss of generality, the expectations of these agents are assumed to be fully backward looking, which means that the coefficient (τ) of the distributed lag learning process equals zero. Following this, Equationequation (7)

(7)

(7) can be reduced to Equationequation (8)

(8)

(8) .

Substituting Equationequation (8)(8)

(8) into Equationequation (6)

(6)

(6) generates Equationequation (9)

(9)

(9) .

By further substituting Equationequation (9)(9)

(9) into Equationequation (5)

(5)

(5) also gives Equationequation (10)

(10)

(10) .

Substituting both Equationequations (10)(10)

(10) and (Equation4

(4)

(4) ) into Equationequation (1)

(1)

(1) and rearranging then gives the final inflation equation as:

From Equationequation (11)(11)

(11) , the general price level of goods and services in a small open economy can, therefore, be generally expressed in Equationequation (12)

(12)

(12) .

It is observed from Equationequation (12)(12)

(12) that, inflation in a small open economy is influence by real income, exchange rate, money supply, nominal interest rate and previous year’s price level (inflation).

The general specification of the overall price level of goods and services [Equationequation (12)(12)

(12) ] is then modified to capture other variables such as budget deficit, which has the potential of influencing inflation. For instance, financing budget deficit through seigniorage (printing money) or purchases of government securities leads to temporal disequilibrium in the money market and could therefore leads to inflation.

The modified Equationequation (12)(12)

(12) for estimation is therefore specified in Equationequation (13)

(13)

(13) .

where ,

,

,

,

and

represent the overall price level (Inflation), real income, money supply [measured by narrow (M1) and broad (M2) money], nominal interest rate and budget (fiscal) deficit, respectively, and t denotes the time trend.

The estimable form of Equationequation (13)(13)

(13) is given by Equationequation (14)

(14)

(14) .

where the variables in Equationequation (14)(14)

(14) are as explained earlier.

is measured by M1 and M2, which represent narrow and broad money supply, respectively,

and

are the constant and the stochastic error terms, respectively, such that the error term is normally distributed with a mean of zero and a constant variance [

~ N (0,

]. Again, the β’s (1, 2, 3, …, 5) are the respective coefficients of the variables to be estimated, and ln denotes the natural logarithm. It must be emphasized that Equationequation (14)

(14)

(14) is estimated twice. In the first and second cases, the equation is estimated using narrow money supply (M1) and broad money supply (M2), respectively. In each estimation, inflation is normalized first, and this is followed by money supply normalization and finally budget deficit normalization. The motivation for this normalization is to see how each variable (budget deficit, money supply and inflation) influences the other. The choice of the variables for the present study is influenced by existing works (Ghartey, Citation2001; Bawumia and Abradu-Otoo, Citation2003; Lozano-Espitia & Lozano-Espitia, Citation2008; Adu & Marbuah, Citation2011; Kovanen, Citation2011; Ahiabor, Citation2013; Gyebi & Boafo, Citation2013; Lin & Chu, Citation2013; Anantha Ramu, Citation2014; Chiaraah & Nkegbe, Citation2014; Adom et al., Citation2015; Nguyen, Citation2015; Ibn Boamah, Citation2019; Nasir et al., Citation2020a, Citation2020b).

3.2. Estimation strategy

The study adopts the vector error correction model (VECM) propounded by Johansen (Citation1988) and Granger causality test (Granger, Citation1969) to test the hypothesis regarding the relationship between money supply, budget deficit and inflation. As a prerequisite of the VECM model, stationarity properties of the sampled variables in the study are checked to avoid inconsistent and unreliable results. The VECM is applicable when the series are integrated of order one [I (1)] (or at the first difference), and there exists a long run relationship (cointegration) among the variables. In establishing the stationarity properties of the series, the parametric Augmented Dickey-Fuller (ADF) test (Dickey & Fuller, Citation1979, Citation1981) and the non-parametric Phillips and Perron (Citation1988) are employed. In these tests, the null hypothesis of unit root (non-stationarity) is tested against the alternative hypothesis of stationarity (no unit root). The rejection (non-rejection) of the null hypothesis implies that the series are stationary (non-stationary) within the sampled period. After establishing the stationarity properties of the series, the cointegration test of the variables is tested using the Johansen cointegration test introduced by Johansen and Juselius (Citation1990), which provides two test statistics—the trace and maximum eigenvalue test statistics—to decide whether there exists a long run relationship among the variables. The null hypothesis of no cointegration is rejected when either the trace or maximum eigenvalues statistic exceeds the 5% significance level. In this study, the optimal lag selection is chosen using the Schwartz Bayesian Criterion (SBC). According to Pesaran and Pesaran (Citation2010), SBC provides more parsimonious specification of the model and more suitable for relatively smaller sample.

After confirmation of a valid long run relationship among the variables, the study first estimates the direction of causality among the variables using the pair-wise Granger causality test. The vector error correction model (VECM), which can produce the long run relationship among the variables, is then estimated after the causality test for a valid confirmation of the relationship as well as the exact impact of the explanatory variables on the dependent variable. EquationEquations (15)(15)

(15) and (Equation16

(16)

(16) ) are the general and individual variable specification of the vector error correction model, respectively.

where is an m x 1 vector of first difference variables (inflation, money supply, budget deficit, exchange rate, real income and nominal interest rate), Г’s (1, 2, …, ρ-1) and ∏ denote the short-run and long-run parameters of the respective variables.

is the error term such that

~ N (0,

. The notation, ∏ = α

, α and β are 6 x r matrices that denote the short-run to long-run adjustments coefficients and the cointegration vectors among the variables.

The general form can be expressed in individual variables form as follows:

where all the variables are as explained earlier, Δ represents first difference operator, ECT is the error correction term and γ’s (1, 2, 3, …, 6) are the short-run coefficients of the error correction term, which lie within 0 and 1 and must be negative and significant. The , ϕ, τ, ω, θ and δ represent the coefficients of the respective variables.

Furthermore, as indicated earlier in the introduction section regarding the major contribution of the paper, the weak exogeneity test within the VECM framework is employed to assess whether money supply and budget deficit variables used in the study are exogenous to ascertain which of the theories discussed earlier (especially the classical, the monetarist and FTPL theories) hold in the Ghanaian context. The non-rejection of the null hypothesis of the weak exogeneity test implies that the tested variable satisfies weak exogeneity, and therefore the variable is said to be exogenous; otherwise, the variable is endogenous. Also, the study performs series of diagnostic tests to confirm that the estimations are free from any econometric problem. To this end, the normality and autocorrelation issues are checked using the Jarque-Bera and the Lagrange Multiplier test, respectively, while the White heteroscedasticity test is employed to check the issue of heteroscedasticity. In these tests, the null hypothesis of absence of these problems is tested against the alternative hypothesis of the presence of these problems. The non-rejection (rejection) of the null hypothesis indicates the absence (presence) of these problems in the study.

3.3. Data and variable description

The study employs quarterly time series data spanning 1999Q1 to 2019Q4. The sources of data for the study are Bank of Ghana Research Department Database, International Financial Statistics and World Bank’s World Development Indicators. Specifically, data on money supply (M1 and M2) and budget deficit is obtained from Bank of Ghana Research Department Database, whereas those on exchange rate and inflation are obtained from International Financial Statistics of the International Monetary Fund (IMF; Citation2019). Real income and interest rate data is sourced from World Bank’s World Development Indicators (World Bank, Citation2019). shows a brief description of the variables used in the study.

Table 1. Description of variables

4. Results and discussion

This section discusses the empirical results of the study. The section starts with the summary of descriptive statistics of variables, trends of inflation, budget deficit and money supply (the key variables of the study), and this is followed by the analysis of the stationarity properties of the series. Afterwards, the cointegration test, pair-wise Granger causality test, normalized long run results, weak exogeneity test, impulse response functions and the diagnostic tests are discussed accordingly.

4.1. Descriptive and trend analysis

The summary of the descriptive statistics in terms of mean, standard deviation, skewness, kurtosis, Jarque-Bera and linear correlation are reported in , respectively.

Table 2. Summary of descriptive statistics

Table 3. Linear correlation results

From , it is observed that money supply (M2), budget deficit (BD) and inflation (INF) have mean (standard deviation) values of 8.90 (1.62), 7.99 (1.59) and 2.63 (0.40) respectively. The maximum (minimum) values for money supply (M2), budget deficit (BD) and inflation (INF) are 11.05 (5.77), 10.18 (5.09) and 3.71 (1.58), respectively. In all, it is observed that the sample variables do not deviate much from their respective mean values as indicated by the standard deviation values. Furthermore, the values for the Skewness, Kurtosis and the Jarque-Bera show that the data is normally distributed. Turning to the linear correlation results (), it is observed that money supply (M1 and M2) and budget deficit (BD) have a weak significant negative correlation with inflation. However, budget deficit (BD) has a strong significant positive correlation with money supply (M1 and M2).

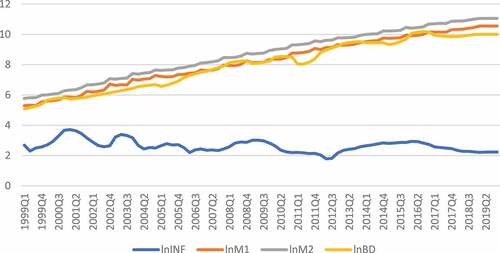

The trends of money supply (M1 and M2), budget deficit (BD) and inflation (INF) over the study period (1999Q1 to 2019Q4) are shown in .

Figure 1. Trends of money supply (M1 and M2), budget deficit (BD) and inflation (INF).Source: Authors’ construction

It is observed that money supply (M1 and M2) has a steady upward trend over the study period. However, budget deficit and inflation have been fluctuating over the years, but the former shows an upward trend. It is further observed that, in periods of election (2000, 2004, 2008, 2012 and 2016), both budget deficit and inflation tend to rise, indicating that budget deficit could explain inflation dynamics in Ghana.

4.2. Unit root test

The results from the ADF and P-P unit root tests are reported in . From the results, both tests confirm that narrow money (M1), budget deficit, real income and interest rate are all stationary at the first difference [I (1)]. However, exchange rate and inflation are stationary at the first difference [I (1)] in the P-P test, whereas the ADF test confirms that broad money (M2) is stationary at the first difference [I (1)]. Following the confirmation of stationarity properties of the variables, the study proceeds with the Johansen cointegration test.

Table 4. Unit root test

4.3. Johansen cointegration test

The Johansen cointegration (trace and maximum-eigenvalue statistics) results are reported in and .

Table 5A. Johansen cointegration test results (Model 1)

Table 5B. Johansen cointegration test results (Model 2)

The results from the Johansen cointegration test in both estimations (Models 1 and 2) reveal that there exists a long run relationship among the variables. Specifically, the trace and maximum-eigenvalue tests for Models 1 and 2 show that there exists at least two cointegrations among the variables at 5% significance level. Given the valid long run relationship among the variables, the study then continues with the direction of causality analysis using the pair-wise Granger causality test, after which the VECM technique is also employed for the long run dynamics.

4.4. Pair-wise granger causality test

The results from the pair-wise Granger causality among the variables is reported in . The results show the money supply (M1 and M2), budget deficit and real income Granger-cause inflation; however, the null hypothesis of the opposite is not rejected. The result regarding money supply (M1 and M2) causing inflation supports both the classical theory and monetarist hypothesis, which claim that inflation is always and everywhere a monetary phenomenon. Further, the FTPL, which argues that fiscal (budget) deficit causes inflation, also holds. However, to completely ascertain these claims, these theories propose that money supply and budget deficit should be exogenously determined.

Table 6. Pair-wise Granger causality test results (F-statistics)

Given that, this proposition is not obtained from the Granger causality analysis, it is therefore important to conduct the weak exogeneity test, especially for the validation of the classical, the monetarist and the FTPL theories that explain the relationship among budget (fiscal) deficit, money supply and inflation. Furthermore, the fact that real income (output) and interest rate Granger-cause inflation also supports the structuralist and Keynesian theories regarding inflation determination. It is also revealed that money supply Granger-causes budget deficit but budget deficit does not Granger-causes money supply. This result is, however, contrary to the hypothesis by Sargent and Wallace (Citation1981) that budget-deficit Granger-causes money supply and afterwards, money supply Granger-causes inflation. The latter is observed in this study, but the former does not hold in this context. About interest rate and inflation, the results reveal a bi-directional causal relationship, which reiterate the significance of interest rate in determining inflation.

4.5. Johansen normalized long run results

The results of the normalized long run estimates are reported in . Narrow money (M1) and broad money (M2) are estimated separately, and the results are reported under Models 1 and 2, respectively. It must be emphasized that in interpreting VECM results, the signs of the coefficients are interpreted in the reverse form—a positive (negative) coefficient means a negative (positive) relationship. The study also uses Model 2 as the benchmark model for the interpretation of the elasticities (coefficient), because, in measuring money supply, M2 captures M1.

Table 7. Johansen normalized long run results

Regarding the estimations based on the normalization of inflation and money supply (M1 and M2), the results reveal a significant negative relationship between inflation and money supply (M1 and M2) in both inflation and money supply (M1 and M2) equations. The coefficients (Model 2) indicate that all other things been equal, a 1% increase (decrease) in broad money supply decreases (increases) inflation by approximately 0.41% at 1% significance level, whereas the coefficient of inflation in the money supply equation (Model 2) suggests that a 1% rise (fall) in inflation causes broad money (M2) supply to decrease (increase) by about 2.43% at 1% significance level. The results further show that the negative effect of inflation on money supply is relatively higher than that of money supply on inflation. The negative impact of money supply (M2) on inflation implies that inflation in the context of Ghana is not caused by money supply but could be attributed to other factors (as argued by the Keynesian and Structuralist theories) in the economy as revealed by the study. Thus, this result does not support the classical and monetarist theories that money supply is the cause of inflation. This result contradicts findings of studies on Ghana by Bawumia and Abradu-Otoo (Citation2003), Adu and Marbuah (Citation2011), Adom et al. (Citation2015), Adjei (Citation2018), and Boamah (Citation2019); however, it is consistent (in terms of the negative relationship but not significance) with the study by Kovanen (Citation2011).

The results also indicate that budget deficit (inflation) is revealed to exert a significant positive effect on inflation (budget deficit) in both inflation and budget deficit equations in Models 1 and 2 when inflation and budget deficit are normalized. The coefficient of budget deficit from Model 2 shows that all other factors held constant, a 1% increase (decrease) in budget deficit induces a rise (fall) in inflation by about 0.29% at 1% significance level. Also, a 1% rise (fall) in inflation causes a rise (reduction) in budget deficit by about 3.45% at 1% level of significance.

These results seem realistic, as budget deficit financed by printing of money or borrowing (through issuing of government securities) causes disequilibrium in the money market, which in turn raises the prices of non-tradable goods, and hence a rise in general price level of goods and services (inflation). On the other hand, inflation in an economy implies higher government expenditure because rising prices of goods and services cause the cost of government projects to rise and, therefore, exceeding its revenue, which results in budget deficit. The significant positive impact of the budget deficit validates the FTPL. Our result regarding the effect of budget deficit on inflation contradicts the insignificant findings by Adom et al. (Citation2015) and Adu and Marbuah (Citation2011). However, this finding is consistent with studies on countries in other parts of the world (Anantha Ramu, Citation2014; Lin & Chu, Citation2013; Ndanshau, Citation2012; Nguyen, Citation2015). The significant positive impact of budget deficit on inflation implies that budget deficit is very crucial in determining inflation in the Ghanaian economy, and hence, policymakers should not overlook its potency.

Furthermore, normalizing money supply (M1 and M2) and budget deficit in both models, the results reveal that money supply (M1 and M2) exerts a significant positive impact on budget deficit, and budget deficit also has a significant positive effect on money supply (see money supply and budget deficit equations) in both Models 1 and 2. From Model 2, the coefficient of budget deficit indicates that money supply will increase (decrease) by about 0.70% if budget deficit increases (decreases) by 1%, whereas the coefficient of money supply shows that a 1% increase (decrease) in money supply increases (reduces) budget deficit by about 1.42%, and these are significant at 1% level. The positive impact of budget deficit on money supply also seems factual, as budget deficit financed by printing of money (seigniorage) or borrowing increases money supply in an economy. Exchange rate is found to exert a negative impact on inflation and money supply, but the effect on budget deficit is positive in both models. However, the impacts in Model 2 are insignificant. The coefficients from Model 1 reveal that a rise in exchange rate (measured by real effective exchange rate) by 1% induces inflation to fall by about 0.49% at 1% significance level. This result is plausible in the sense that when there is a rise in real effective exchange rate, domestic goods become more expensive and less competitive relative to their trading partners. As a result, exports are expected to fall, while imports are expected to increase, all other things being equal. The fall in exports implies that there will be more goods in the domestic market (higher supply), which is likely to exceed the quantity demanded by consumers, and hence a fall in the general price level. This outcome is consistent with the results obtained by Adu and Marbuah (Citation2011) and Anantha Ramu (Citation2014).

Regarding real income (output), the results from both models show that its effect on inflation and money supply (M1 and M2) is significantly negative. However, the effect on budget deficit is positive in both models. This means that expansion in output growth in an economy is considered as a potential way of reducing inflation. The coefficient in Model 2 indicates that a 1% rise (fall) in real income lowers (increases) inflation by about 0.22%, ceteris paribus. Studies by Bawumia and Abradu-Otoo (Citation2003), Adu and Marbuah (Citation2011), Adjei (Citation2018), and Boamah (Citation2019) on Ghana and Anantha Ramu (Citation2014) on India have also reported a significant negative relationship between real income and inflation. The results further show that interest rate exerts a significant positive effect on inflation and money supply, but the effect is negative for budget deficit in both models. This significant positive outcome of the interest rate on inflation is consistent with previous studies on Ghana (see: Adom et al., Citation2015; Adu & Marbuah, Citation2011; Boamah, Citation2019).

From , the adjustment coefficients (’s) confirm a valid cointegration among the variables. Specifically, disequilibrium in inflation in the short run will be restored to its long run equilibrium at a speed of approximately 51%. In addition, the significant negative coefficients indicate the stability of the models.

4.6. The weak exogeneity test

The results from the weak exogeneity test (specifically for money supply and budget deficit) are reported in .

Table 8. Weak exogeneity test results

It is observed that both money supply and budget (fiscal) deficit satisfy the weak exogeneity test. This is because the study fails to reject the null hypothesis of weak exogeneity (exogenous) since the probability values of both money supply (M1 and M2) and budget deficit (BD) are all greater than the 5% significance level. This implies that money supply and budget deficit are exogenous or are exogenously determined statistically.

4.7. Analysis of the impulse response function

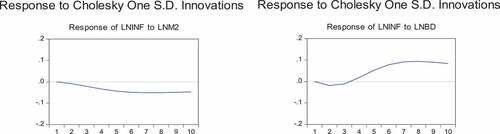

To further examine the dynamics of money supply, budget deficit and inflation, we go a step further to analyze how inflation responds to budget deficit and money supply shocks. We also analyze how money supply (budget deficit) responds to budget deficit and inflation (money supply [M2] and inflation) shocks. The impulse response functions are presented in .

Figure 2a. Response of inflation to money supply and budget deficit shocks.Source: Authors’ construction

Starting with (response of inflation to money supply [M2] and budget deficit shocks), it is observed that inflation responds negatively to money supply (M2) shocks over the period (see left panel). Specifically, the response declines with marginal fluctuations from period 1 to period 6 and remains stable from periods 6 to 10 with a marginal increase in period 9. The implication is that shocks to money supply reduces inflation. Again, the response of inflation to budget deficit shocks (see right panel) indicates that inflation responds more positively to budget deficit shocks (especially from period 4 to period 10). However, the response is negative from the 1st period to 3rd period. Therefore, the implication is that shocks to the budget deficit increase inflation, given the more positive response to budget-deficit shocks.

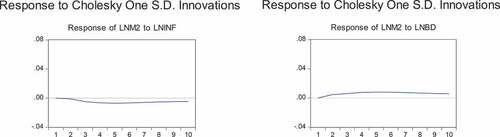

Regarding the response of money supply (M2) to inflation and budget deficit shocks (), the results show that money supply (M2) responds negatively to inflation over the period (see left panel). Precisely, the response declines from period 1 to period 5 and then with a little rise from period 6 to period 8. It remains relatively stable for the rest of the periods. This implies that a shock to inflation does not increase money supply (M2) in the Ghanaian economy. In addition, it is indicated that money supply (M2) responds positively to budget deficit shocks (from period 1 to period 10) (see the right panel). Given the positive response, a shock to the budget deficit has a higher likelihood of increasing the money supply (M2) in the Ghanaian economy.

Figure 2b. Response of money supply to inflation and budget deficit shocks.Source: Authors’ construction

Figure 2c. Response of budget deficit to money supply and inflation shocks.Source: Authors’ construction

Furthermore, indicates that the response of the budget deficit to the shocks of the money supply (M2) is negative and declines from period 1 to period 3 and remains relatively stable throughout the remaining periods (see left panel). The negative response implies that a shock to money supply (M2) in the economy reduces budget deficit. On the other hand, the response of budget deficit to inflation shocks is positive over the period. The response from period 1 to period 10 is stable with a marginal rise in periods 3 and 5. The positive response suggests that any shock to inflation will increase budget deficit in Ghana.

4.8. Diagnostic test

In ensuring the outcome from the estimation is robust, reliable and good for effective policy purposes, various diagnostic tests (normality, serial correlation, and heteroscedasticity) are performed, and the results are reported in . It is observed that both models are free from the aforementioned econometric problems. This is because the probability values of the serial correlation, heteroscedasticity and normality tests exceed 5% significance level, implying non-rejection of the null hypothesis of serial correlation, heteroscedasticity and normality tests.

Table 9. Diagnostic test results of the VECM model

5. Concluding remarks and policy implications

Using quarterly data over the period 1999Q1 to 2019Q4, this paper has explored the relationship (dynamics) between budget (fiscal) deficit, money supply and inflation in Ghana. Also, using the weak exogeneity test, the study tests which of the theories (especially the classical, the monetarist and FTPL theories) explain the relationship between inflation, money supply and budget deficit in the Ghanaian context. The pair-wise Granger-causality test as well as the vector error correction model (VECM) are also employed for the analysis. The results from the pair-wise Granger causality test show that there is a unidirectional causal relationship that runs from money supply, budget deficit, and real income to inflation. There is also a unidirectional causal relationship that moves from money supply to budget deficit. The results further indicate that there is a bi-directional causal relationship between interest rate and inflation. Regarding the VECM analysis, the benchmark results (Model 2) reveal that money supply has significant negative relationship with inflation, whereas budget deficit is found to exert a significant positive effect on inflation. It is further revealed that money supply and inflation have significant positive relationship with budget deficit. The budget deficit also exerts a significant positive effect on the money supply. The effect of exchange rate on inflation is also negative albeit insignificant. Furthermore, the effects of real income and interest rate on inflation, money supply and budget deficit are revealed to be significant. The results from the impulse response function also indicate that inflation responds more positively to budget deficit. However, it (inflation) tends to respond negatively to money supply (M2) shocks. Also, budget deficit responds positively (negatively) to inflation (money supply [M2]) shocks. Further, money supply responds more positively (negatively) to budget deficit (inflation) shocks. Based on the VECM, the weak exogeneity test and impulse response function, it is concluded that the fiscal theory of the price level (FTPL) holds in the Ghanaian context as it is able to explain the nexus between money supply, budget deficit and inflation. The classical and monetarist theories, however, do not hold in the Ghanaian context.

The findings of the study have some policy implications for government of Ghana and other African countries that share similar characteristics with Ghana. Based on the positive effect of the budget deficit on inflation, the study suggests that a reduction in government spending is one sure way to curb inflation, as this minimizes government expenditure. The study therefore recommends reduction in government spending. Specifically, this can be achieved by reducing spending on unproductive sectors of the economy, reducing the size of the government, and putting stringent measures in place to control the bureaucratic nature of government officials. Further, there should also be conscientious effort by the government to ensure spending within the allocated budget. This will ensure that expenditure of the government is within its budget to avoid or reduce budget deficit. Another implication of the findings is that, in curbing inflation, policymakers should pay more attention to budget deficit rather than money supply. In all, ensuring reduction in government expenditure, government size and avoiding budget deficit is likely to result in stable and favorable inflation in the Ghanaian economy, which is also likely to enhance economic growth and development.

However, there is a caveat in generalizing the findings of the present study to other African countries as the data used relate to Ghana, and this becomes a limitation of the study. Given this, future studies should consider using a panel of African countries to improve the generalization of the results and validate the present findings.

correction

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Emmanuel Duodu

Emmanuel Duodu is currently a Master of Science student at Department of Fundamentals of Economic Analysis, University of Alicante, Alicante-Spain. His research interests include macroeconomics, international economics, monetary economics and public economics.

Samuel Tawiah Baidoo is a PhD candidate at the Department of Economics, Kwame Nkrumah University of Science and Technology (KNUST), Kumasi-Ghana, and a lecturer at the Department of Accounting and Finance, School of Business, Christian Service University College, Kumasi-Ghana. His research interests include microeconomics, monetary economics, international economics and economic policy analysis.

Hadrat Yusif is a Professor at the Department of Economics, Kwame Nkrumah University of Science and Technology (KNUST), Kumasi-Ghana. He holds PhD in Economics from the National University of Malaysia. He is specialised in economics of education and monetary economics.

Prince Boakye Frimpong holds a PhD in Economics from the University of Milan, Italy. He is currently a senior lecturer at the Department of Economics, KNUST. His areas of specialisation are Applied Econometrics and general Applied Microeconomics.

References

- Adjei, S. K. (2018). Inflation determinants - Milton Friedman’s theory and the evidence from Ghana, 1965-2012 (Using ARDL Framework). International Journal of Applied Economics, Finance and Accounting, 3(1), 21–23. https://doi.org/10.33094/8.2017.2018.31.21.36

- Adom, P. K., Agradi, M. P., & Quaidoo, C. (2018). The transition probabilities for inflation episodes in Ghana. International Journal of Emerging Markets, 13(6), 2028–2046. https://doi.org/10.1108/IJoEM-08-2017-0313

- Adom, P. K., Zumah, F., Mubarik, A. W., Ntodi, A. B., & Darko, C. N. (2015). Analysing inflation dynamics in Ghana. African Development Review, 27(1), 1–13. https://doi.org/10.1111/1467-8268.12118

- Adu, G., & Marbuah, G. (2011). Determinants of inflation in Ghana: An empirical investigation. South African Journal of Economics, 79(3), 251–269. https://doi.org/10.1111/j.1813-6982.2011.01273.x

- Ahiabor, G. (2013). The effects of monetary policy on inflation in Ghana. Developing Country Studies, 3(12), 82–89.

- Amoah, L., & Aziakpono, M. J. (2018). Exchange rate pass-through to consumer prices in Ghana: Is there asymmetry? International Journal of Emerging Markets, 13(1), 162–184. https://doi.org/10.1108/IJoEM-07-2016-0179

- Anantha Ramu, M. R. (2014). Relationship between fiscal deficit and inflation in India: A long-term empirical analysis. The Indian Economic Journal, 62(3), 1099–1120. https://doi.org/10.1177/0019466220140303

- Arndt, H. W. (1985). The origins of structuralism. World Development, 13(2), 151–159. https://doi.org/10.1016/0305-750X(85)90001-4

- Bawumia, M., & Abradu-Otoo, P. (2003). Monetary growth, exchange rates and inflation in Ghana: An error correction analysis. Bank of Ghana (Working Paper). Bank of Ghana, Accra.

- Boamah, M. I. (2019). Inflation Dynamics in a Small Developing Economy: An Empirical Analysis for Ghana. The Journal of Developing Areas, 53(3), 229–237. https://doi.org/10.1353/jda.2019.0049

- Chenery, H. B. (1975). The structuralist approach to development policy. The American Economic Review, 65(2), 310–316 Accessed 13 January 2021 https://www.jstor.org/stable/1818870.

- Chiaraah, A., & Nkegbe, P. K. (2014). GDP growth, money growth, exchange rate and inflation in Ghana. Journal of Contemporary Issues in Business Research, 3(2), 75–87 Accessed 13 January 2021 http://citeseerx.ist.psu.edu/viewdoc/download?doi=10 .1.1.680.6400&rep=rep1&type=pdf.

- Dickey, D. A., & Fuller, W. A. (1979). Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association, 74(366a), 427–431 https://doi.org/10.1080/01621459.1979.10482531.

- Dickey, D. A., & Fuller, W. A. (1981). Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica: Journal of the Econometric Society, 49(4), 1057–1072. https://doi.org/10.2307/1912517

- Friedman, M. (1963). Inflation: Causes and consequences. Asia Publishing House.

- Frisch, H. (1989) Inflation Theories). Elif Printing Limited, Istanbul, Turkey: .

- Ghartey, E. E. (2001). Macroeconomic instability and inflationary financing in Ghana. Economic Modelling, 18(3), 415–433. https://doi.org/10.1016/S0264-9993(00)00047-X

- Granger, C. W. (1969). Investigating causal relations by econometric models and cross-spectral methods. Econometrica: Journal of the Econometric Society, 37(3), 424–438. https://doi.org/10.2307/1912791

- Gyebi, F., & Boafo, G. K. (2013). Macroeconomic determinants of inflation in Ghana from 1990-2009. International Journal of Business and Social Research (IJBSR), 3(6), 81–93 Accessed 13 January 2021 https://citeseerx.ist.psu.edu/viewdoc/download?doi=10 .1.1.683.3210&rep=rep1&type=pdf.

- International Monetary Fund (IMF). (2019). International Financial Statistics (IFS).

- Johansen, S. (1988). Statistical analysis of cointegration vectors. Journal of Economic Dynamics & Control, 12(2), 231–254. https://doi.org/10.1016/0165-1889(88)90041-3

- Johansen, S., & Juselius, K. (1990). Maximum likelihood estimation and inference on cointegration-with applications to the demand for money. Oxford Bulletin of Economics and Statistics, 52(2), 169–210. https://doi.org/10.1111/j.1468-0084.1990.mp52002003.x

- Kotwal, O. P. (1987). Theories of Inflation: A Critical Survey. The McGraw-Hill Publishing Companies.

- Kovanen, A. (2011). IMF Working Papers (London, United Kingdom: Palgrave Macmillan), 1–23.

- Laryea, S. A., & Sumaila, U. R. (2001). Determinants of inflation in Tanzania. Chr. Michelsen Institute.

- Lin, H. Y., & Chu, H. P. (2013). Are fiscal deficits inflationary? Journal of International Money and Finance, 32(1), 214–233. https://doi.org/10.1016/j.jimonfin.2012.04.006

- Lozano-Espitia, L. I., & Lozano-Espitia, I. (2008). Budget deficit, money growth and inflation: Evidence from the Colombian case. Borradores de Economía, Central Bank of Colombia, Colombia, No. 537 1–25 Accessed 13 January 2021 https://repositorio.banrep.gov.co/bitstream/handle/20.500.12134/5554/BORRADOR%20537.pdf?sequence=1 .

- Nasir, M. A., Balsalobre-Lorente, D., & Huynh, T. L. D. (2020a). Anchoring inflation expectations in the face of oil shocks & in the proximity of ZLB: A tale of two targeters. Energy Economics, 86, 104662. https://doi.org/10.1016/j.eneco.2020.104662

- Nasir, M. A., Huynh, T. L. D., & Vo, X. V. (2020b). Exchange rate pass-through & management of inflation expectations in a small open inflation targeting economy. International Review of Economics & Finance, 69, 178–188. https://doi.org/10.1016/j.iref.2020.04.010

- Ndanshau, M. O. (2012). Budget deficits, money supply and inflation in Tanzania: A multivariate granger causality test, 1967–2010. University of Dar Es Salaam Working Paper, 04(12), 1–36 doi:http://dx.doi.org/10.2139/ssrn.2142328).

- Nguyen, B. (2015). Effects of fiscal deficit and money M2 supply on inflation: Evidence from selected economies of Asia. Journal of Economics, Finance and Administrative Science, 20(1), 49–53. https://doi.org/10.1016/j.jefas.2015.01.002

- Noyola, V. J. (1956). El desarollo economico y la inflacion en Mexico y otros paises latino-americanos. Investagacion Economica, 16(4), 603–649.

- Olivera, J. H. (1964). On Structural Inflation and Latin-American’Structuralism’. Oxford Economic Papers, 16(3), 321–332. https://doi.org/10.1093/oxfordjournals.oep.a040958

- Pesaran, B., & Pesaran, M. H. (2010). Time series econometrics using Microfit 5.0: A user’s manual. Oxford University Press, Inc. https://pdfs.semanticscholar.org/8773/45b2c11ce28d55a1a15d6de3078fbfa75f1f.pdf

- Phillips, P. C., & Perron, P. (1988). Testing for a unit root in time series regression. Biometrika, 75(2), 335–346. https://doi.org/10.1093/biomet/75.2.335

- Sargent, T. J., & Wallace, N. (1981). Some unpleasant monetarist arithmetic. Federal Reserve Bank of Minneapolis Quarterly Review, 5(3), 1–17 https://d1wqtxts1xzle7.cloudfront.net/35204863/QR531-with-cover-page-v2.pdf?Expires=1646000868&Signature=SIShuw5JuJ-u~Uefo4gXP~SauhYjLL4gUquOtBAN2KKvtItsVGBG8sB0GemK52R8DyWnT7szbelU47hn~0PCvxGRrGJPC9bQMH8CeOu0miknk-FnnmuIkROT8DtgRms8qihd06WmBxpGWEsiZwZj-Hbxt5Y266f1eKe7m3bW9C6Leu6bIhm~CoTHUxIm2cYulO8k~9YWDMVSsa7Q9vJehlSiDS-2DHTwz-4BYkeIM5ICIP8t9pQq7hi6RjPg5qcAFnca2xVMdzfpW1~ee8ecX9sqLtUfg-WLq4Nw~-iNoMt9iW1scgcz4dIkS4XDnnYppWpaRAeszIhcERqllIsVYQ__&Key-Pair-Id=APKAJLOHF5GGSLRBV4ZA.

- Sowa, N. K. (1994). Fiscal deficits, output growth and inflation targets in Ghana. World Development, 22(8), 1105–1117. https://doi.org/10.1016/0305-750X(94)90079-5

- Sunkel, O. (1958). La inflación chilena: Un enfoque heterodoxo. El Trimestre Económico, 25(4), 570–599 https://www.jstor.org/stable/pdf/20855451.pdf?casa_token=UDthiri0JTUAAAAA:WVfGtFfaBrN0rEyJPJ3xYyCbE0zdQlXmiDS_QxS3iQ4cboeMlHUvfgmMot-XpWvYSncJqXK4vsH_FXxBNREbU3DsM76Pdpi2bF2okbYS4Ngfjklxtxbi.

- Ubide, M. A. J. (1997). Determinants of inflation in Mozambique. Working Paper, No. 97-145. International Monetary Fund.

- Woodford, M. (1995). Price-level determinacy without control of a monetary aggregate. In Carnegie-Rochester conference series on public policy, Vol.43, pp.1–46, North Holland.

- World Bank. (2019). World Banks’ World Development Indicators.