?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The current study aims to examine the impact of the pandemic (Covid-19) on the financial performance of some of the selected Indian sectors. The study targets all Indian firms listed on the Bombay stock exchange, which belong to the following sectors (Constructing, tourism and hospitality, food and consumer sectors). The study extracted data of 444 firms from the Prowess database for four sectors. Due to some missing values, the study dropped 73 firms. Therefore, the final sample of this study consists of 371 firms. Results revealed a significant difference in total income, net sales, net profit, earnings per share, and diluted earnings per share before and after the pandemic in tourism, hospitality, and consumer sectors. The result of the study states that there is a significant difference in total income net sales before and after the pandemic in construction. There is a difference in the decline in both sectors’ net sales and total income during the pandemic. Conversely, there is no significant difference between net profit, earnings per share, diluted earnings per share before and after the pandemic in constructing and food sectors. Results of the study state that the food sector was not affected by the pandemic, whereas the construction sector reduced its expenses to their minimum. The study also found that the tourism, hospitality and customer sectors were the most effected by the Covid-19 pandemic, followed by the construction sector and food sector, which was a minor sector affected by the pandemic. Most of the prior research on Covid-19 is theoretical, and only a few have conducted an empirical investigation. The study is unique as it evaluates the financial performance of Indian firms before and after the Covid-19 pandemic, which has not been studied yet in the Indian context. Further, this study provides valuable insights to regulators and policymakers about the most affected sectors due to the pandemic by analysing Indian sectors.

Keywords:

PUBLIC INTEREST STATEMENT

Financial performance is the primary criterion used by investors worldwide. But the performance of any company gets affected on several predicted and unpredicted factors. Unpredicted factors are those which are out of management control such as Covid-19 pandemic which caused a major change in firms’ operations. Nationwide lockdown affected all businesses. Hospitality and tourism industry, transportation and airways were among the worst affected business. Hence, the current study aims to examine the impact of the pandemic (Covid-19) on the financial performance of most affected sectors in India. It was found that pandemic (Covid-19) has affect firms’ performance. Further, the COVID-19 pandemic in India has forced corporate leaders and owners to mobilize quickly and make quick decisions. A decision like reducing industrial output or even temporarily shutting down operations could have long-term consequences that were not anticipated. As a result of the government’s lockdown policy or order, this would influence firms’ financial performance. Furthermore, businesses should always have a scalable and effective emergency plan and be ready for the unexpected. Further, the business must learn many things from this pandemic to tackle such things if they happen in the future.

1. Introductions

On 31 December 2019, China Health Authority alerted the World Health Organization (WHO) about many cases of pneumonia of unknown etiology in Wuhan City, China (Harapan et al., Citation2020; Mohan & Nambiar, Citation2020). On 7 January 2020, the news was virus isolated and named as a temporary 2019 novel coronavirus (2019-nCoV) by the WHO (Lin et al., Citation2021; Spiteri et al., Citation2020) and identified from the throat swab sample of a patient with viral pneumonia in Wuhan, China (Harapan et al., Citation2020; Lin et al., Citation2021; Sofi et al., Citation2020). On 11 January 2020, China announced the first death from 2019-nCoV (Lin et al., Citation2021) and on the same day, the WHO declared 2019-nCoV to be a Public Health Emergency of International Concern, highly contagious, caused infections in large scale and proved difficult to contain (Shen et al., Citation2020).

The outbreak was a significant public health risk since it spread rapidly, resulting in widespread illness that overwhelmed health systems and proved difficult to contain (Wu et al., Citation2021). On 30 January 2020, the WHO declared the SARS-COV-2 outbreak a Public Health Emergency of International Concern (Harapan et al., Citation2020). Efficiently halt the spread of the virus and safeguard public health, most countries implemented strict lockdown measures. According to Jahangir et al. (Citation2020) and Liu et al. (Citation2020), two coronaviruses transmitted from animals in the past two decades, namely, severe acute respiratory syndrome SARS-COV and Middle East respiratory syndrome MERS-COV. These viruses caused severe pneumonia and high fatality rates. Thus, Jahangir et al. (Citation2020) suggests that pasts lessons learned in dealing with such diseases in stemming and eradicating infections should come in handy. The outbreak is still ongoing, posing an immense threat to global public health and economies. Thus, this study is motivated to investigate the impact of Covid-19 pandemic and how it affected the performance of Indian firms which has not been investigated yet due to non-availability of data. The authors have extracted the financial data from ProwessIQ database to examine the impact of the imposed lockdown on the performance of Indian companies.

Financial performance is the primary criterion used by investors worldwide, as the world has become smaller in the sense that enterprises may be conducted everywhere (Al-ahdal & Hashim, Citation2021; Al-Matari et al., Citation2014; Yahya et al., Citation2017). The performance management process is how a company runs its actions with the help of its corporate objectives and functional strategies (Bititci et al., Citation1997). The improvement procedure is required to identify at all the levels to which using organizational resources could impact business performance (Sharma & Gadenne, Citation2002). Performance measurement offers critical input that enables management to monitor performance, progress, motivation, communication, and issue diagnosis.

For India, the first and second waves occur around five months apart. The first wave peaked in September 2020; daily cases totalling roughly 0.1 million. Daily instances declined until mid-February when they began to climb rapidly. On 15 April 2021, the number of new cases was around 0.2 million, more than quadrupling the previous peak amount. COVID-19 cases and fatalities have seen a dramatic increase in India. On 15 April 2021, the number of new cases was around 0.2 million, more than quadrupling the previous peak amount. COVID-19 has dealt a severe blow to India’s economy in general and macroeconomic impact on every sector (Kar et al., Citation2021). The economy was already in a precarious state before the breakout of covid-19; with the suspension of economic activity and state-wide lockdown, the economy expected to experience a lengthy period of slowing. According to a recent Hindustan Times report, covid 19 affects 70% of the banking sector’s debt. It has impacted 19 industries with a combined debt of 15.5 lakh crore that was not stressed prior to the outbreak (Kumar & Kumar, Citation2021).

There is an immediate need to determine the impact of the pandemic (Covid-19) on the financial performance of some Indian sectors. Due to the data scarcity, the authors were confined to four sectors which are Construction, Tourism and hospitality, Food and Consumer sectors. The study aims to get an in-depth insight into measuring the present effect of the COVID-19 pandemic and identifying crucial short- and long-term response options. As such, this study aims to assist manufacturing and service organizations in managing similar disruptions (i.e. COVID-19) by addressing the following research question: What is the impact of pandemic (Covid-19) on the financial performance of some Indian sectors?

In answering this research question, we collated the data for the fourth quarter of 2019 and the first quarter of 2020 for the selected firms. Results revealed a significant difference in total income, net sales, earnings per share, net profit, and diluted earnings per share before and after the pandemic in tourism, hospitality, and consumer sectors. There is a significant difference in total income net sales before and after the pandemic in constructing and food sectors.

The paper contributes to the existing literature in the following ways. Firstly, to the best of researchers’ knowledge, this might be the first study that examines the impact of COVID-19 on firms’ performance in Indian Context. Secondly, this research is making a comparative study between more likely affected sectors, e.g., tourism and hospitality sector and less likely affected sectors, e.g., Food sector. Thirdly, this paper enriches the literature measuring the impact of major public health emergencies on Indian economy. Fourthly, this paper also proposes an empirical method to evaluate the impact of the pandemic on firm performance of Indian Constructing, tourism, hospitality, food and consumer sectors. Finally, the results presented in the paper have important policy implications as the central governments try to fight the pandemic and to support the economy recover from the downturn. The paper is divided into five parts introduction, literature review, research methodology, findings and discussions, and conclusion.

2. Theoretical analysis and research hypotheses

The pandemic’s rapid spread profoundly affected economies and financial markets worldwide (Chen & Chia-Wei, Citation2021). The entire world was forced to confront the COVID-19 pandemic, which inevitably resulted in significant upheavals in all spheres, from economics to social (Chen & Chia-Wei, Citation2021; Piccarozzi et al., Citation2021). Across the globe, businesses have been impacted by the COVID-19 epidemic, affecting practically every business sector and industry (Islam et al., Citation2020; Xu et al., Citation2021). Lockdown and social distancing restrictions are used as part of policies and efforts to control the ongoing COVID-19 pandemic (Cheval et al., Citation2020; Zhao & Feng, Citation2020).

According to Trueman’s theory, investors decide a firm’s worth based on their assessment of adaptability of managements to the economic environment in which it works (Trueman, Citation1986). Additionally, investors want substantial announcement of Covid-19-related information and how Covid-19 has impacted enterprises from a stakeholder viewpoint (Elmarzouky et al., Citation2021). Khatib and Nour (Citation2021) found that the COVID-19 pandemic has significantly impacted business characteristics, such as performance, governance structure, liquidity, and leverage level. Nevertheless, the difference between previous and post-pandemic times is insignificant. Another study by Ahmed (Citation2020) analysed the influence of COVID-19 on Pakistani stock market performance. The study used data on positive cases, fatalities, and recoveries associated with COVID-19.

Additionally, data of the first-half 2020 closing values of the PSX 100 index prices was utilized. The study’s findings indicated that only COVID-19 recoveries affect the index’s performance, while daily positive cases and fatalities have a negligible effect. Additional research can be conducted at the cross-country level by including additional variables such as economic growth, interest rates, and inflation rates in addition to the COVID-19-related factors.

Shen et al. (Citation2020) studied the impact of COVID-19 on the corporate performance of listed Chinese companies. Results depicted that COVID-19 distorts effect on firm performance. D’Orazio and Dirks (Citation2020) proved that introducing COVID-19-related policies from 1 January 2020 to 17 May 2020 in the Euro Area had a considerable negative influence on stock markets. Movements in Google trends, bond yields, EU volatility index and infection rates indicate a detrimental influence. Fiscal policy announcements had a negligible effect, whereas health initiatives had a large one. Fu and Shen (Citation2020) investigated the influence on the energy industry that COVID-19 had on corporate performance and found that COVID-19 has had a considerable detrimental influence on the performance of energy businesses. Goodwill impairment was introduced as a moderating variable, the pandemic affected companies experiencing goodwill impairment more substantially. So, decision-makers at all levels should pay closer attention to the impact of COVID-19 on energy firms and implement counter measures to limit the consequences on the energy industry. Islam et al. (Citation2020) discovered a sizeable association between entrepreneurial self-efficacy, financial performance, and entrepreneurial resilience of small and medium-sized businesses. Moreover, the study discovered a substantial moderating effect of innovative work behaviour on the connection between financial performance and entrepreneurial efficacy.

Moreover, Rababah et al. (Citation2020) discovered that small and medium-sized businesses were the most brutal hit or affected by this pandemic. Furthermore, their results demonstrated that serious-impact locations and industries hardest affected by COVID-19 experienced a more severe loss in financial performance than other industries. The study’s conclusion presented significant policy implications, as banks, regulatory agencies central banks and governments must work cooperatively to address the financial and economic consequences of COVID-19 problems. Shen et al. (Citation2020) examined the effects of COVID-19 on company performance using financial data from publicly traded Chinese enterprises. It demonstrates that COVID-19 had a detrimental effect on company performance. COVID-19 posed a more substantial detrimental effect on firm performance when a firm’s investment scale or sales income is less.

Zou & li (Citation2020) discovered that the COVID-19 pandemic had impacted virtually every aspect of the global economy and society. The study examined enterprises in Guangdong Province to ascertain the pandemic’s impact on them and to suggest public strategies to mitigate the negative impacts. Businesses in Guangdong Province have encountered significant hurdles due to the outbreak. Their manufacturing and operations are curtailed, and they face substantial dangers. It is vital to enact regulations that significantly reduce enterprises’ production costs, allowing them to weather this difficult phase and gradually resume normal operations. Xu et al. (Citation2021) found that the epidemic’s severity has a significant negative effect on import and export cargo throughputs; further, the impact of the pandemic on import is more significant than export.

In Indian context, Dash et al. (Citation2021) found that fatalities from communicable diseases have negatively impacted the Indian aviation market. Inline, Kumar Das and Patnaik (Citation2020) found that various industries such as telecom, tourism and aviation, auto sector and transportation are the most impacted sectors facing negative backlash of the present disaster. Existing studies analysed the connection between COVID-19 and economic performances (Debata et al., Citation2020; Goswami et al., Citation2021). In contrast, no studies analysed the impact of COVID-19 on the performance of public companies of various sectors in India. Based on this above discussion, we proposed the following research hypothesis:

: COVID-19 has a negative impact on the performance of Indian listed companies.

: COVID-19 has a negative impact on the total income of Indian listed companies.

: COVID-19 has a negative impact on the net sales of Indian listed companies.

: COVID-19 has a negative impact on the net profit of Indian listed companies.

: COVID-19 has a negative impact on the earnings per share of Indian listed companies.

: COVID-19 has a negative impact on the diluted earnings per share of Indian listed companies.

Based on the above discussion, it is found that this is the first study on COVID-19 and its impact on firm performance in different industries sectors using secondary data. Further, this article contributes to the body of knowledge about the economic effect of significant public health emergencies in India. It also proposes an empirical method to evaluate the impact of the pandemic on firm performance of Indian Constructing, tourism, hospitality, food and consumer sectors. The findings in this article have significant policy implications as the central government’s attempt to contain the epidemic and aid the economy’s recovery from the slump.

3. Research methodology

The study targets all Indian firms listed on the Bombay stock exchange, which belong to the following sectors (Constructing, tourism and hospitality, food and consumer sectors). The study incorporates secondary data, which collate data in the following manner (fourth quarter of 2019, i.e., 01/01/2020–31/03/2020; first quarter of the year 2020, i.e., 01/04/2020–30/06/2020. The timeline is divided as the Fourth quarter of 2019 is considered for the pre-COVID-19 period. India started implementing the lockdown form on 15/03/2020. The first quarter of 2020 is considered for the post-COVID-19 period. The data for the study is extracted for 444 firms from the Prowess database. Many researchers have used this database for extracting financial data for Indian companies (e.g., Al-Ahdal et al., Citation2018; Al-Homaidi et al., Citation2018; Almaqtari et al., Citation2020; Farhan et al., Citation2019). Due to some missing values, the study dropped 73 firms. Therefore, the final sample of this study consists of 371 firms; shows the sample size of each sector. Financial performance is measured by total income, net sales, net profit, earnings per share and diluted earnings per share. Wilcoxon Signed Ranks Test, which corresponds to the one-way ANOVA test, is used to analyse the non-normal distribution data.

Table 1. Study sample

4. Findings and discussions

4.1. Descriptive statistics

reports the descriptive statistics of financial performance variables of all sectors. Regarding the financial performance of the construction sector, the results in show that the mean value of total income of firms in the construction sector before the pandemic is 5494.42 million, while the mean value after the pandemic is 3855.07. The results imply that the total income of construction firms decreased after the pandemic due to the lockdown that the Indian government implemented. In the same vein, net sales of construction companies declined from 5324.68 before the pandemic to 3721.93 after the pandemic. Similarly, the results in reveal that the mean values of net profit of constructing companies before and after the pandemic are 559.95 and 324.82, respectively. These results imply that constructing companies’ net profit decreased after the pandemic. demonstrates that the mean earnings per share before the pandemic are 3.32 and 3.9. Similarly, the mean values of diluted earnings per share before and after are 3.31 and 3.9, respectively. The increase in the earnings per share and diluted earnings per share after the pandemic could be attributed to the extraordinary items and the profits from discontinuing operations.

Table 2. Descriptive statistics

Discussing the results of the tourism and hospitality sector results, the results in reveal that the mean value of total income of tourism and hospitality firms before the pandemic is 659.21million, while the mean value after the pandemic is 139.99. The results imply that the total income of tourism and hospitality firms shrunk after the pandemic due to the lockdown that was implemented by the Indian government in which all tourism and hospitality sectors were closed tourism activities were suspended. In the same vein, net sales of tourism and hospitality companies significantly declined from 597.69 before the pandemic to 109.72 after the pandemic, which means that net sales of tourism and hospitality companies were significantly affected by the lockdown of Covid-19. Similarly, results in reveal that the mean values of net profit of tourism and hospitality companies before and after the pandemic are −29.27 and −133.81, respectively. These results imply that the net profit of tourism and hospitality firms also decreased significantly after the pandemic. demonstrates that the mean earnings per share before the pandemic are 0.11 and −3.39. Similarly, the mean values of diluted earnings per share before and after are 0.11 and −3.39, respectively. The significant decline in the earnings per share and diluted earnings per share after the pandemic attributed to the total closure of tourism activities to stop the spread of covid-19.

Regarding the results of the food sector, results in show that the mean value of total income of food firms before the pandemic is 3788.9 million, while the mean value after the pandemic is 3332.64. The results imply that the total income of food firms declined slightly after the pandemic. In the same vein, net sales of food companies significantly declined from 3582.34 before the pandemic to 3210.27 after the pandemic, which stated net sales of food companies were relatively affected by the lockdown of Covid-19. Similarly, the results in reveal that the mean values of net profit of food companies before and after the pandemic are 402.57 and 325.39, respectively. These results imply that the net profit of food firms also decreased after the pandemic. Results could indicate that, however, with the lockdown implemented by the Indian government, there were some relaxations for food providing companies. demonstrates that the mean values of earnings per share before the pandemic are 1.16 and 2.21. Similarly, the mean values of diluted earnings per share before and after are 1.16 and 2.21, respectively. The increase in the earnings per share and diluted earnings per share after the pandemic attributed to the extraordinary items and the profits from discontinuing operations. The decline in the performance of food sector after the pandemic could be attributed to the fact that dues to the lockdown most people were unable to go to the markets to get what they want which affected the sales of the sector for the lockdown period. Further, in terms of the essential food materials, most people bought them in large quantities and stored them fearing a future crisis which affected the sales of the sector during the lockdown.

Illustrating the financial performance results in the Consumer sector, the results in show that the mean value of total income of firms in the Consumer sector before the pandemic is 6311.7 million, while the mean value after the pandemic is 3569.62. The results imply that the total income of consumer firms decreased after the pandemic due to the lockdown that the Indian government implemented. In the same vein, net sales of construction companies declined from 6171.34 before the pandemic to 3486.37 after the pandemic.

Similarly, the results in reveal that consumer companies’ mean values of net profit before and after the pandemic are 464.07 and 330.38, respectively. These results imply that constructing companies’ net profit decreased after the pandemic. demonstrates that the mean earnings per share before the pandemic are 2.32 and 0.13. Similarly, the mean values of diluted earnings per share before and after are 2.31 and 0.13, respectively.

4.2. Trend analysis

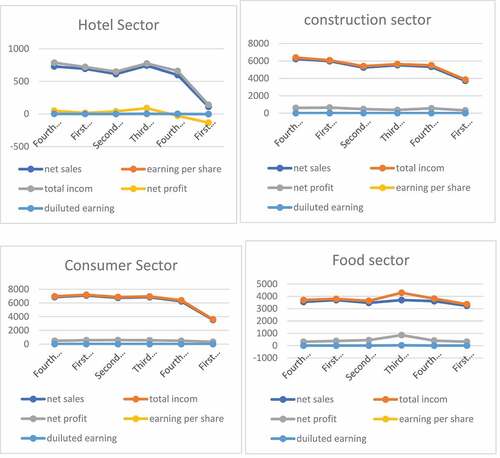

The trend plots drawn below in show the performance of Indian firms affected by the pandemic. The figure below shows the trend analysis for the quarterly financial performance for the selected sectors. The figures reveal that the tourism, hospitality and customer sectors were the majorly affected by the Covid-19 pandemic, followed by the construction sector, and the food sector was the least affected by the pandemic. Figures demonstrate the performance of all sectors started deteriorating from the fourth quarter of 2019, i.e., 01/01/2020-31/03/2020. Net sales and total income figures show that sales of tourism, hospitality and consumer sectors were markedly affected by the Covid-19 pandemic. Whereas it is observed that sales and income of tourism and hospitality sector were at pick in the third quarter 2019, i.e., 01/09/2019–13/12/2019 During pandemic sales and income of tourism and hospitality sector decreased significantly due to the spread and travel restrictions imposed in the course of lockdown. These two reasons were behind the significant decline in tourism and hospitality sector sales and income. Slowdown in sales and income of tourism and hospitality sector. The net profit also was declined but not as severe as the sales and income, which could indicate that most tourism and hospitality companies laid off their employees and reduced their disbursement to nominal. The figure shows that the pandemic affected net sales and income, and net profit and earnings per share were stable, which means that the consumer sector reduced expenses to their minimum during the lockdown. Figures communicate those sales and income were fluctuating since the second quarter of 2019, but after the pandemic, there was a significant decline in net sales and total income, which means that the construction sector was affected by the Covid-19 pandemic. Regarding food sector, figure downstate that the food sector was not affected by the Covid-19 pandemic as we see the lines are stable over the period from fourth-quarter 2018 to first quarter 2020. This result is illustrated by the fact that food is something that humans cannot dispense with food.

Figure 1. Results of trend analysis.

4.3. Wilcoxon signed ranks test

In order to perform the analysis, normality tests (Kolmogorov-Smirnov and Shapiro-Wilk) were run for examining the normal distribution of the data. Testing the normality suggests which test to be performed, whether parametric (paired sample t-test) or non-parametric (Wilcoxon Signed Ranks Test). The normality tests in show that data is normally distributed as the PVs of all variables in all sectors were less than 0.05. Therefore, the appropriate test is the non-parametric test Wilcoxon Signed Ranks Test, the alternative to the parametric test (paired sample test).

Table 3. Test of normality

** implies that significant at the 0.01 level The Wilcoxon Signed Ranks Test results in show a significant difference between total income before and after pandemic (Covid-19) in all sectors, constructing, tourism and hospitality, food, and consumer sector at 0.01 significance level. These results mean that Covid-19 have affected all sectors. In other words, the lockdown that the Indian government imposed on 13 March 2020. Thus, H01a, which states that COVID-19 has a negative impact on the total income of Indian companies sector that are listed, is accepted. Similarly, results of the Wilcoxon Signed Ranks Test in reveals that there was a significant difference between net sales before the pandemic and after the pandemic) in all sectors; constructing, tourism and hospitality, food, and consumer sector at 0.01 significance level. These results imply that the pandemic affected the net sales of Indian firms in respective of their nature. This result indicates that H0b, which states that COVID-19 has a negative impact on the net sales of Indian listed companies, is accepted.

Table 4. Wilcoxon signed ranks test

a.Total income2 < total income1, b. total income2 > total income1, c. total income2 = total income1, d. net sales2 < net sales1, e. net sales2 > net sales1, f. net sales2 = net sales1, g. net profit2 < net profit1, h. net profit2 > net profit1, i. net profit2 = net profit1, j. earnigs per share2 < earnigs per share1, k. earnigs per share2 > earnigs per share1, l. earnigs per share2 = earnigs per share1, m. diluted earnigs per share2 < diluted earnigs per share1, n. diluted earnigs pershare2 > diluted earnigs pershare1, o. diluted earnigs per share2 = diluted earnigs per share1.

For Z, b. Based on positive ranks, c. Based on negative ranks.

Concerning net profit, results of the Wilcoxon Signed Ranks Test in demonstrate a significant difference in net profit before and after the turmoil in the tourism and hospitality sector and consumer sector at 0.01 level, which means that the lockdown imposed by Indian authorities had affected the net profit of consumers, tourism, and hospitality companies. On the contrary, results showed no significant difference in net profit before and after the construction and food sector pandemic. These results imply that food items were necessary and excluded from the lockdown even though lockdown was imposed in the country. For example, manufacturing companies were continuously working, stores and groceries were allowed to work during some hours, and that is a way there was no difference in the net profit before and after the pandemic. In comparison, tourism, hospitality and consumer firms’ net profit was affected because there was a complete shut down for all activities in these sectors. Therefore, H0c, which states COVID-19 has a negative impact on the net profit of Indian listed companies, is accepted in the tourism and hospitality sectors and consumer sectors and rejected in the case of food and construction sectors.

In line with the net profit results, the Wilcoxon Signed Ranks Test results in show a significant difference in earnings per share diluted earnings per share before and after the pandemic in the tourism, hospitality, and consumer sectors at a 0.01% level. The lockdown imposed by Indian authorities had affected earnings per share and Diluted earnings per share of consumer, tourism, and hospitality companies.

On the contrary, results showed no significant difference in earnings per share diluted earnings per share before and after the construction and food sector pandemic. These results can be attributed to firms’ net profit working in these sectors. As the net profit of tourism hospitality and consumer companies were significantly affected by the pandemic, sequent earnings per share and Diluted earnings per share will be affected. In constructing and food firms’ net profit was not affected; therefore, earnings per share and Diluted earnings per share were not affected. The result means that H01d and H01d accepted in the tourism, hospitality and consumer sectors are rejected in the case of the food and construction sector.

5. Conclusion

The study aims to examine the impact of the pandemic (Covid-19) on the financial performance of some Indian sectors. The study has targeted all Indian firms listed on the Bombay stock exchange, which belong to the following sectors (constructing, tourism and hospitality, food and consumer sectors). Financial performance is measured by total income, net sales, net profit, and diluted earnings per share. The study is on secondary data; data collated for the fourth quarter of 2019, i.e., 01/01/2020–31/03/2020 and the first quarter of 2020, i.e., 01/04/2020-30/06/2020. 2019 Fourth quarter is considered the pre-COVID-19 period, lockdown implemented from 15/03/2020, and the first quarter of 2020 is considered the post-COVID-19 period. Results revealed a significant difference in Total income, net sales, net profit, earnings per share, and Diluted earnings per share before and after the pandemic in tourism, hospitality, and consumer sectors. It is constituted that there is a significant difference in total income net sales before and after the pandemic in constructing and food sectors. This difference results from declining both sectors’ net sales and total income during the pandemic.

On the contrary, there is no significant difference between net profit, earnings per share, diluted earnings per share before and after the pandemic in constructing and food sectors. These results could be explained because the food sector was not affected by the pandemic and the construction sector reduced its expenses to their minimum. The study also revealed that tourism, hospitality, and customer sectors were the most affected by the Covid-19 pandemic, followed by the construction sector and food sector, the last sector affected by the pandemic.

This work is of three-fold contributions:

It bridges an existing gap in the literature by empirically evaluating the effect of the Covid-19 pandemic on the performance of Indian firms (in light of different sectors), which has not yet been investigated as most of the literature on Covid-19 is theoretical.

This study provides valuable insights to regulators and policymakers about the most affected sectors due to the pandemic by analysing Indian sectors.

The study provides helpful directions for academicians and researchers to include in future research.

This study, like other studies, has several limitations that must be considered while reading the findings, which paves the way for future directions. For instance, the study is limited to profitability measures of firms’ performance. Therefore, future researchers could take leverage and turnover ratios. Further, due to data availability, this study is limited to firms that belong to the tourism and hospitality, food, consumer, and construction sectors. Thus, future research could take another sector like the telecommunication and aviation sector as an example. Finally, because of the non-availability of data, the study could not get the latest data. Hence, researchers are encouraged to provide findings on updated data for 2021. Despite these, our findings have an important theoretical and practical implication on the impact of COVID-19ʹs on Indian firms’ performance.

The COVID-19 pandemic in India has forced corporate leaders and owners to mobilize quickly and make quick decisions. A decision like reducing industrial output or even temporarily shutting down operations could have long-term consequences that were not anticipated. As a result of the government’s lockdown policy or order, this would influence firms’ financial performance. Furthermore, businesses should always have a scalable and effective emergency plan and be ready for the unexpected. Further, the business must learn many things from this pandemic to tackle such things if they happen in the future.

correction

This article has been republished with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Mohammed H. Alsamhi

Mohammed Alsamhi, Associate Professor at IBB University-Yemen. His area of interest is in the field of Accounting & Financial Management.

Fuad Al-Ofairi, Associate Professor at IBB University-Yemen. His areas of interest are in the fields of Cost Accounting, Managerial Accounting and Financial analyses.

Najib H.S. Farhan, Assistant Professor at Universal Business School, India. His areas of interest are in the fields of sustainability accounting, climate change accounting, environmental, social, governance (ESG), financial reporting quality, corporate governance, working capital and financial performance.

Waleed M. Al-Ahdal, Assistant Professor at Department of Accounting, Faculty of Business, Economics and Social Development, University Malaysia Terengganu, Malaysia. His areas of interest are in the fields of ESG; corporate governance; environmental disclosure; CSR; IFRS and financial performance.

Ayesha Siddiqui is a faculty member at Universal Business School, India. Her areas of interest include in the fields of International Finance, Structural Break, Stock Markets, Time Series and Volatility modelling.

References

- Ahmed, S. Y. (2020) Impact of COVID-19 on performance of Pakistan stock exchange. MPRA Paper No. 101540. https://mpra.ub.uni-muenchen.de/101540

- Al-Ahdal, W. M., Farhan, N. H., Tabash, M. I., & Prusty, T. (2018). The impact of demonetization on Indian firms’ performance: Does company’s age make a difference? Investment Management and Financial Innovations, 15(3), 71–16. https://doi.org/10.21511/imfi.15(3).2018.06

- Al-ahdal, W. M., & Hashim, H. A. (2021). Impact of audit committee characteristics and external audit quality on firm performance: Evidence from India. Corporate Governance, ahead-of-print No. ahead-of-print. https://doi.org/10.1108/CG-09-2020-0420

- Al-Homaidi, E. A., Tabash, M. I., Farhan, N. H., Almaqtari, F. A., & McMillan, D. (2018). Bank-specific and macro-economic determinants of profitability of Indian commercial banks: A panel data approach. Cogent Economics & Finance, 6(1), 1548072. https://doi.org/10.1080/23322039.2018.1548072

- Al-Matari, E. M., Al-Swidi, A. K., & Fadzil, F. H. B. (2014). The measurements of firm performance’s dimensions. Asian Journal of Finance & Accounting, 6(1), 24–49. https://doi.org/10.5296/ajfa.v6i1.4761

- Almaqtari, F. A., Hashid, A., Farhan, N. H., Tabash, M. I., & Al‐ahdal, W. M. (2020). An empirical examination of the impact of country‐level corporate governance on profitability of Indian banks. International Journal of Finance & Economics, 1–21. https://doi.org/10.1002/ijfe.2250

- Bititci, U. S., Carrie, A. S., & McDevitt, L. (1997). Integrated performance measurement systems: A development guide. International Journal of Operations & Production Management, 17(5), 522–534. http://dx.doi.org/10.1108/01443579710167230

- Chen, H.-C., & Chia-Wei, Y. (2021). Global financial crisis and COVID-19: Industrial reactions. Finance Research Letters, 42, 101940. https://doi.org/10.1016/j.frl.2021.101944

- Cheval, S., Mihai, C., Georgiadis, T., Herrnegger, M., Piticar, A., & Legates, D. (2020). Observed and Potential Impacts of the COVID-19 Pandemic on the Environment. International Journal of Environmental Research and Public Health, 17(11), 4140. https://doi.org/10.3390/ijerph17114140

- D’Orazio, P., & Dirks, M. (2020). COVID-19 and financial markets: Assessing the impact of the coronavirus on the eurozone, Ruhr Economic Papers, No. 859, RWI-Leibniz-Institut für Wirtschaftsforschung, Essen, https://doi.org/10.4419/86788995.

- Dash, D. P., Dash, A. K., & Sethi, N. (2021). Understanding the pandenomics: Indian aviation industry and its uncertainty absorption. The Indian Economic Journal, 69(4), 729–749. https://doi.org/10.1177/00194662211013211

- Debata, B., Patnaik, P., & Mishra, A. (2020). COVID‐19 pandemic! It’s impact on people, economy, and environment. Journal of Public Affairs, 20(4), 1–5. https://doi.org/10.1002/pa.2372

- Elmarzouky, M., Albitar, K., & Hussainey, K. (2021). Covid-19 and performance disclosure: Does governance matter? International Journal of Accounting & Information Management, 29(5), 776–792. https://doi.org/10.1108/IJAIM-04-2021-0086

- Farhan, N. H., Alhomidi, E., Almaqtari, F. A., & Tabash, M. I. (2019). Does corporate governance moderate the relationship between liquidity ratios and financial performance? Evidence from Indian pharmaceutical companies. Academic Journal of Interdisciplinary Studies, 8(3), 144–144. https://doi.org/10.36941/ajis-2019-0013

- Fu, M., & Shen, H. (2020). COVID-19 and corporate performance in the energy industry - Moderating effect of goodwill impairment. Energy Research Letters, 1(1), 2967. https://doi.org/10.46557/001c.12967

- Goswami, B., Mandal, R., & Nath, H. K. (2021). Covid-19 pandemic and economic performances of the states in India. Economic Analysis and Policy, 69, 461–479. https://doi.org/10.1016/j.eap.2021.01.001

- Harapan, H., Itoh, N., Yufika, A., Winardi, W., Keam, S., Te, H., Megawati, D., Hayati, Z., Wagner, A. L., & Mudatsir, M. (2020). Coronavirus disease 2019 (COVID-19): A literature review. Journal of Infection and Public Health, 13(5), 667–673. https://doi.org/10.1016/j.jiph.2020.03.019

- Islam, D., Khalid, N., Rayeva, E., & Ahmed, U. (2020). COVID-19 and financial performance of SMEs: Examining the nexus of entrepreneurial self-efficacy, entrepreneurial resilience and innovative work behavior. Revista Argentina de Clínica Psicológica, XXIX(3), 587–593. https://doi.org/10.24205/03276716.2020.761

- Jahangir, M. A., Muheem, A., and Rizvi, M. F. et al. (2020). Coronavirus (COVID-19). History, current knowledge and pipeline medications. Journal of Pharmacy and Pharmacology, 4(1), 1–9. https://doi.org/10.31531/2581-3080.1000140

- Kar, S. K., Ransing, R., Arafat, S. Y., & Menon, V. (2021). Second wave of COVID-19 pandemic in India: Barriers to effective governmental response. EClinical Medicine, 36 100915 . https://doi.org/10.1016/j.eclinm.2021.100915

- Khatib, S. F. A., & Nour, A. (2021). The impact of corporate governance on firm performance during the COVID- 19 pandemic: Evidence from Malaysia. Journal of Asian Finance, Economics and Business, 8(2), 0943–0952. https://ssrn.com/abstract=3762393

- Kumar, & Kumar, S. (2021). Impact of Covid-19 on Indian economy with special reference to banking sector: An Indian perspective. International Journal of Law Management & Humanities, 4(1), 12–20.

- Kumar Das, D., & Patnaik, S. (2020). The impact of COVID-19 in Indian economy–An Empirical Study. International Journal of Electrical Engineering and Technology, 11(3), 194–202. https://ssrn.com/abstract=3636058

- Lin, Q., Zhao, S., Gao, D., Lou, Y., Yang, S., Musa, S. S., Wang, M. H., Cai, Y., Wang, W., Yang, L., & He, D. (2021). A conceptual model for the coronavirus disease 2019 (COVID-19) outbreak in Wuhan, China with individual reaction and governmental action. International Journal of Infectious Diseases, 93, 211–216. https://doi.org/10.1016/j.ijid.2020.02.058

- Liu, Y.-C., Kuo, R.-L., & Shih, S.-R. (2020). COVID-19: The first documented coronavirus pandemic in history. Biomedical Journal, 4(3), 328–333. https://doi.org/10.1016/j.bj.2020.04.007

- Mohan, B. S., & Nambiar, N. (2020). COVID-19: An insight into SARS-CoV-2 pandemic originated at Wuhan City in China’s Hubei Province. Journal of Infectious Diseases and Epidemiology, 6(4), 1–8. https://doi.org/10.23937/2474-3658/1510146

- Piccarozzi, M., Silvestri, C., & Morganti, P. (2021). COVID-19 in management studies: A systematic literature review. Sustainability, 13(7), 3791. https://doi.org/10.3390/su13073791

- Rababah, A., Al-Haddad, L., Sial, M. S., Chunmei, Z., & Cherian, J. (2020). Analyzing the effects of COVID-19 pandemic on the financial performance of Chinese listed companies. Journal of Public Affairs, e2440. https://doi.org/10.1002/pa.2440

- Sharma, B., & Gadenne, D. (2002). An inter‐industry comparison of quality management practices and performance. Managing Service Quality: An International Journal, 12(6), 394–404. https://doi.org/10.1108/09604520210451876

- Shen, H., Fu, M., Pan, H., Yu, Z., & Chen, Y. (2020). The impact of the COVID-19 pandemic on firm performance. Emerging Markets Finance and Trade, 56(10), 2213–2230. https://doi.org/10.1080/1540496X.2020.1785863

- Sofi, M. S., Hamid, A., & Sami, B. (2020). SARS-CoV-2: A critical review of its history, pathogenesis, transmission. Biosafety and Health, 2(4), 217–225. http://dx.doi.org/10.1016/j.bsheal.2020.11.002

- Spiteri, G., Fielding, J., Diercke, M., Campese, C., Enouf, V., Gaymard, A., & Ciancio, B. C. (2020). First cases of coronavirus disease 2019 (COVID-19) in the WHO European region. Eurosurveillance, 25(9), 2000178. https://doi.org/10.2807/1560-7917.ES.2020.25.9.2000178

- Trueman, B. (1986). Why do managers voluntarily release earnings forecasts? Journal of Accounting and Economics, 8(1), 53–71. https://doi.org/10.1016/0165-4101(86)90010-8

- Wu, S., Zhou, W., Xiong, X., Burr, G. S., Cheng, P., Wang, P., Niu, Z., & Hou, Y. (2021). The impact of COVID-19 lockdown on atmospheric CO2 in Xi’an, China. Environmental Research, 197, 1–7. https://doi.org/10.1016/j.envres.2021.111208

- Xu, L., Yang, S., Chen, J., & Shi, J. (2021). The effect of COVID-19 pandemic on port performance: Evidence from China. Ocean & Coastal Management, 209(2021), 105660. https://doi.org/10.1016/j.ocecoaman.2021.105660

- Yahya, A. T., Akhtar, A., & Tabash, M. I. (2017). The impact of political instability, macroeconomic and bank-specific factors on the profitability of Islamic banks: An empirical evidence. Investment Management and Financial Innovations, 14(4), 30–39. http://dx.doi.org/10.21511/imfi.14(4).2017.04

- Zhao, H., & Feng, Z. (2020). Staggered release policies for COVID-19 control: Costs and benefits of relaxing restrictions by age and risk. Mathematical Biosciences, 326(2020), 108405. https://doi.org/10.1016/j.mbs.2020.108405

- Zou & li. (2020). The impact of the COVID-19 pandemic on firms: A survey in Guangdong Province, China. Global Health Research and Policy, 5(1), 1–10. https://doi.org/10.1186/s41256-020-00166-z