?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The study investigates the key factors affecting the professional skepticism of independent auditors in Vietnam. The factors that are studied in this research include knowledge and experience, workload, time pressure, and incentives that affect professional skepticism of independent auditors. The authors have utilized quantitative and qualitative analyses in combination with a logistic regression model and other available analytical tools for conducting the research in SPSS software. All the statistics processed in the paper were based on 90 independent Vietnamese auditors in 2021. The results reveal that factors including knowledge, experience, and incentives positively affect professional skepticism, while workload and time pressure negatively impact professional skepticism. The findings suggest Vietnamese lawmakers and auditing firms should regulate annual training courses for auditors to enhance their professional ability and reasonably encourage the auditor’s motivation, while it is necessary to minimize workload and time pressure for auditors in order to maintain and improve the audit quality. This implication could be applied for Vietnamese auditing firms and international auditing firms.

PUBLIC INTEREST STATEMENT

We have been dealing with the factors affecting professional skepticism of independent auditors to improve the quality audit of independent auditing firms. Professional skepticism of independent auditors is the important skill and fundamental requirement of the auditing profession to help the independent auditors collect audit evidence to draw appropriate audit conclusions.

This study investigates the influence of key factors on the professional skepticism of independent auditors in Vietnam. The paper points out that the factors including knowledge and experience, incentives positively affect professional skepticism, while workload and time pressure negatively impact professional skepticism. From the results, the findings suggest that Vietnamese law-makers and auditing firms should regulate annual training courses for auditors to enhance their professional ability and reasonably encourage the auditor’s motivation while it is necessary to minimize workload and time pressure for auditors in order to maintain and improve the audit quality for Vietnamese auditing firms.

1. Introduction

Professional skepticism of independent auditors is not only one of the fundamental requirements of the auditing profession but also an important element for improving high-quality audit in the audit process. The term “professional skepticism” has been mentioned in a number of researches and recent audit standards. The AICPA has emphasized that professional skepticism is a critical skill and that research should be undertaken to assess how professional skepticism is implemented. The number of previous public studies related to the topic of professional skepticism is divided into two major research directions.

Firstly, the studies focused on the goal of clarifying the definitions of the professional skepticism of auditors, analyzing the composition of professional skepticism, and comparing these components under different perspectives to develop a scale to measure the professional skepticism Quadackers et al. (Citation2014); Hurtt (Citation2010).

Secondly, the studies focused on identifying factors affecting professional skepticisms such as the studies by Nelson (Citation2009), Hurtt et al. (Citation2013), and Nelson (Citation2009), which presented detailed models on professional skepticism in auditing and stressed the importance of implementing an acceptable degree of professional skepticism while carrying out the auditing process, is one of the notable studies. Hurtt et al. (Citation2013) was based on Nelson (Citation2009) and extended a lot more with four groups of factors that were auditors, evidence, customer characteristics, and external factors. Auditors with a higher level of occupational skepticism find more contradictory data than those with lower levels of occupational skepticism. Besides, Hurtt conducted a research in order to measure characters of professional skepticism with their own scale from previous ones. According to Brazel et al. (Citation2016), the auditing firms’ policy on incentive and punishment for auditors during the audit process motivates them to increase professional skepticism, thus minimizing audit risk and enhancing the quality of production audit performance. The study concluded that rewards for skepticism may not work as intended in the current environment due to the risks that auditors confront when exercising professional skepticism. A myriad of studies have not reached the unification in the definition of professional skepticism and the efficient quality of the audit probably be the lack of professional skepticism of auditors in audit firms because they may not carry out their research in a multidimensional perspective on factors affecting professional skepticism and scale to measure professional skepticism.

Up to date, most of the research related to professional skepticism is conducted in developed countries where they have a closely established audit system and they only concentrate on the analysis of different factors influencing the nature of professional skepticism of auditors. There are no studies that focus on factors affecting the professional skepticism of independent auditors, especially in the developing economic environment as Vietnam. Therefore, in this study, the paper will analyze not only factors affecting the professional skepticism of auditors, but also factors influencing three main characteristics of professional skepticism. The previous studies only show general theories to improve the professional skepticism of auditors, which has not introduced the specific policies to maintain, develop, and apply professional skepticism for various objects in the case of Vietnam. Therefore, through this research, it is highly practical to identify factors and assess their impact on professional skepticism of independent auditors. The paper finds that these factors, including knowledge, experience, and incentives, positively affect professional skepticism, while workload and time pressure negatively impact professional skepticism. Additionally, the study would give suggestions and policies to help relevant agencies and auditing firms to find solutions to enhance the professional skepticism of independent auditors with a view to obtaining reasonable assurance and providing high audit quality. These factors affecting professional skepticism help to improve professional skepticism of Vietnamese auditing firms.

2. Literature review and hypotheses

In recent years, the increasing inappropriate audit opinions of independent auditing firms has led to controversy that the auditors have not maintained enough professional skepticism to collect audit evidence to draw appropriate audit conclusions. Trompeter et al. (Citation2013) demonstrated that auditors must exercise professional skepticism during risk assessments so they can assess the risk for material misstatements in financial statements. After numerous discussions and meetings, a model of the antecedents of professional skepticism and the dependent variable predicted skeptical activities such as questioning the client or doing additional test work were created by M. K. Shaub and Lawrence (1996 cited in Nelson, Citation2009). Following this, Quadackers et al. (Citation2014) performed an experimental study with 96 auditors from one of the Big 4 auditing firms in the Netherlands, ranging in experience from senior to associate. The findings indicate that professional skepticism’s presumptive doubt perspective is more predictive of auditor skeptical judgments and decisions than neutrality, especially in higher-risk settings. Similarly, Nelson (Citation2009) offers an outline of a basic model that includes variables that have a significant impact on auditors’ professional skepticism. Nelson addresses the lack of specificity in the word “technical skepticism” and distinguishes professional expectations and empirical study into three categories: neutral, probable uncertainty, and skepticism or a position of Bayesian unbiasedness when discussing professional skepticism. The research suggests particular elements of the model: knowledge, traits, incentives, judgment, and actions. Based on Nelson (Citation2009), Hurtt (Citation2010) developed and extended a lot more with four groups of factors that were auditors, evidence, customer characteristics, and external factors. He approaches professional skepticism from a neutral perspective, describing it as a multi-dimensional construct that characterizes an individual’s proclivity to withhold conclusions until the proof offers ample justification for one alternative/explanation over others. Recent research result of Brazel et al. (Citation2016), the auditing firms’ policy on incentive and punishment for auditors during the audit process motivates them to increase professional skepticism, thus minimizing audit risk and enhancing the quality of audit performance. He mainly focused on analyzing the effect of incentives on professional skepticism with 3 models and based on the participation of 110 people from audit firms.

2.1. Professional skepticism (PS)

Professional skepticism is essential when the auditor raises questions throughout the implementation, especially when collecting evidence to supply mistakes or the risk of errors (McMillan & White, Citation1993). This is because of sufficient requirement’s audit, appropriate evidence to provide a basis for the audit opinion. The attitude that poses essential questions constantly reflects the level of skepticism of the auditor and the skepticism of any evidence gathered. Questions are posed during the process to help the auditor improve cognitive thinking (Anderson & Maletta, Citation1999). Hurtt (Citation2010) described six PS characteristics in the audit community, including (1) questioning attitude; (2) pause in judgment; (3) desire to learn; (4) the ability to read others; (5) self-determination; and (6) self-confidence.

2.2. Knowledge & experience of independent auditors (KT)

Experience allows the auditor to develop background knowledge and specialized knowledge, allowing the auditor to determine when additional evidence needs to be collected. According to Nelson (Citation2009), Professional Skepticism is maintained if the auditor’s experience provides knowledge about error frequency and zero error, and the consequences indicate a higher risk of bias. Experience is recognized through years of experience in auditing, industry-relevant experience, experience in a specific position (reviewer), and other types of experience (fraud detection). M.K. Shaub and Lawrence (1999 cited in Nelson, Citation2009), Payne and Ramsay (Citation2005) found that the experienced auditors were less skeptical than the less experienced auditors. Griffith et al. (Citation2012) suggested that knowledge is directly related to Professional Skepticism, mainly by assessing knowledge related to gathering additional evidence. The publication claims that with lower levels of knowledge and other aspects such as training or personal motivation lead to low Professional Skepticism levels, without gathering additional evidence. Not all results show that experience affects Professional Skepticism. Furthermore, these findings are based on the risk assessment context during the incomplete audit planning phase, suggesting that perennial auditors often rely on low-risk assessments despite the contrary evidence. Through the above results, it implies that experience influences Professional Skepticism. Recent articles about the auditor’s ability to influence Professional Skepticism: Castro (Citation2013) claim that experience has no effect on Professional Skepticism; Phan et al. (Citation2020) found that knowledge and experience have not yet reached the level of confidence in the significance level, Grenier (Citation2017) thinks that technicians with in-depth knowledge of the customer’s business will have a high Professional Skepticism; Kim et al. (Citation2015) conclude that the auditor responsible for the results will have a high degree of skepticism and the less experienced auditor has a higher Professional Skepticism than the more experienced auditor. Therefore, in general, long-term experience tends to be subjective in the audit. However, with deep knowledge about the business lines of customers, technicians have a higher level of skepticism. Conclusion of Peecher et al. (Citation2010) that if auditors are trained to change cognitive thinking processes or biases affect the Professional Skepticism level of auditors. Ciołek and Emerling (Citation2019) claim that PS has increased with university training. Tong (Citation2018) investigated the impact of various factors on independent auditors’ professional skepticism during the audit of financial statements in Ho Chi Minh City in Vietnam. The study concluded that the knowledge has a positive impact on professional skepticism of auditors.

Based on literature review and current situation of Vietnam, the following hypothesis is proposed:

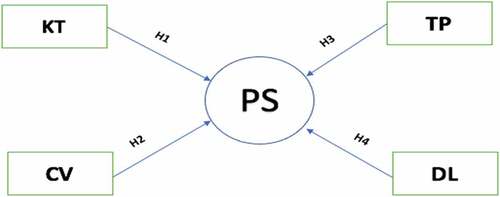

H1: Knowledge & Experience of Independent Auditors positively affects Professional Skepticism.

2.3. Workload of independent auditors (CV)

Prior study has backed up questions about the potential implications of excessive workloads. Sweeney and Summers (Citation2002) studied the number of hours worked, job stressors, and career burnout of 142 auditors, tax accountants, and consultants from a national firm before and after the busy season in a public accounting environment, their analysis reveals burnout is caused by working long hours during the busy season. Fogarty et al. (Citation2000) studied the relationship between work and task characteristics, burnout, and job outcomes in a cross-sectional sample of 188 AICPA participants. Almer and Kaplan (Citation2002) build on the work of Fogarty et al. (Citation2000) by looking at how fluid work conditions affect task tension and burnout. In a study examining accounting professionals’ work–life balance, Buchheit et al. (Citation2016), they polled 1,063 CPAs to see how they felt about work–life balance in different situations, such as (1) Big 4 versus smaller public accounting firms, (2) audit versus tax functions, and (3) public accounting versus industry work settings. Work-family conflict and job burnout perceptions (their proxy for work–life balance) were highest in the Big 4, which was consistent with predictions based on institutional logics theory. They were the first to assess both support for and sustainability of traditional alternative work arrangements (AWAs), and they found a significant difference between the two constructs. As previously stated, the Big 4 companies provide workload in their audit quality reports on a regular basis for the simple reason that, for example, delivering audit quality allows our audit team leaders to have adequate time to complete their tasks. Persellin et al. (Citation2019) indicated that high workloads result in decreased audit quality via compromised audit procedures (including taking shortcuts), impaired audit judgment (including reduced professional skepticism), and difficulty retaining staff with appropriate knowledge and skills. However, Phan et al. (Citation2020) indicated wokload has a positive effect on PS. Based on this, the paper proposes the second hypothesis as follows:

H2: Workload of Independent Auditors negatively affects Professional Skepticism.

2.4. Time pressure of independent auditors (TP)

Time pressure requires technicians to accomplish fairly complex tasks promptly. Time pressure reduces efficiency and puts the auditor under constant stress (McDaniel, Citation1990). Many auditors accept that in times of pressure to accomplish the audit and the number of working hours requested during the busy period creates an openness to embrace customer-modified financial data to accomplish the goal (Glover, Citation1997). Without time to review the manager’s explanations, auditors cannot carefully evaluate the accounting records (Weick, 1983 cited in Holstrom, Citation2015). Disclosure of Coram et al. (Citation2004) evidenced that auditors’ tendency to perform behaviors that degrade quality, as well as to accept suspicious evidence or perform less audit procedures under time pressure. It is found that under high time pressure, auditors are more likely to consider suspicious data, regardless of the possibility of error. Low and Tan (Citation2011) argue that there is a difference between time constraints and random time pressure. When facing with a sudden enlarge in time pressure, the auditor is more prone to depend on the audit procedures of the previous year, meaning that the auditor is less likely to show Professional Skepticism. Under time constraints, auditors are more likely to approve less audit procedures, but only if the probability of error is limited. However, Nelson (Citation2009) and Phan et al. (Citation2020) presented time has positive influence on PS. Based on this, the paper proposes the following hypothesis:

H3: Time pressure of Independent Auditors negatively affects Professional Skepticism.

2.5. Incentives of independent auditors (DL)

A discussion clearance can enhance motivation to improve performance by providing more specific information about audit tasks, reducing task uncertainty, and increasing task performance (Earley, Citation1988). In addition, incentives are considered as motivation that is psychological processes creating initiation, direction, intensity, and persistence of behavior (Klein, Citation1989), motivation improves when employees work with clear goals (Locke, Citation1997), motivational language theory assists assertions (Sullivan, Citation1988). The auditor’s incentive to enhance efficiency is expected to extend as they gain a better sense of the function and value of audit procedures (Sullivan (Citation1988). Finally, by better knowing the mission, the auditor will be able to see if his efforts will produce the desired outcome. Nelson (Citation2009) presented incentives that can affect judgment in at least two ways: the first way is to the extent that PS is reduced by judgmental mistakes and the second way is that incentives can affect judgment via motivated-reasoning processes that drive evidential search, evaluation, and weighting to outcomes. Phan et al. (Citation2020) found that incentives have slightly affected on PS, but they have not yet reached a reliable level of significance. Nguyen (Citation2020) has mentioned factors affecting positively professional skepticism of independent auditors in Ho Chi Minh City that includes incentives of auditing firms and auditors. Based on this, the paper proposes the fourth hypothesis as following:

H4: Incentives of Independent Auditors positively affect Professional Skepticism.

The relationship between these above factors and Professional Skepticism can be illustrated in Figure as follows:

Figure 1. The proposed study.

The detailed description and expected tendency direction of independent variables and dependent variables are shown in Table .

Table 1. Variable and description

3. Research methodology

Based on a literature review on professional skepticism of auditors during the audit, the authors identify factors significantly influencing professional skepticism and measure them according to appropriate methods, from which choosing suitable independent variables and regression models. Then, the authors collected relevant studies to build up an appropriate model. First, secondary information collected from previous studies on factors that influence independent auditors’ professional skepticism. Second, primary data was collected through semi-structured in-depth interviews and online surveys of independent auditors, including those working in the audit department of auditing firms in Vietnam. Third, the collected data are cleansed by removing duplicate and inhomogeneous elements and raw statistics are processed using appropriate calculations and formulas of financial ratios to achieve values of variables. Finally, SPSS Statistics 20 software is exploited for regression analysis and descriptive statistics.

In this research, the sample is chosen according to the convenient sampling method by selecting non-probability samples. Independent auditors selected to survey are individuals who are working for audit firms in Vietnam. The formula for determining the minimum sample size for research to achieve reliability. The size of the sample applied in the study is based on the requirements of Exploratory Factor Analysis (EFA) and multivariate regression. Formula 1: For exploratory factor analysis EFA: the minimum sample size is 5 times the total number of observed variables, the minimum sample size is 31 × 5 = 155 samples. The sample size (157) should be larger than the standard to avoid losses during the survey. Formula 2: For multivariate regression analysis: the minimum sample size needed is calculated by the formula is 50 + 8 * 4 = 82 (4 independent variables). Therefore, 157 respondents satisfy both above formulas and 90 valid respondents used in regression analysis are sufficient.

The author used regression with the dependent variable Professional Skepticism as professional skepticism to assess the effect of variables on independent auditors’ professional skepticism. The factors described in the exploratory analysis (EFA) above are the independent variables affecting. The following is an example of a regression model:

The values βi are regression coefficients, which represent the impact of each independent factor on the dependent variable’s fluctuation. When the regression coefficients are significant (as determined by measuring the significance of the regression coefficient) and the m is large, the regression model is considered suitable.

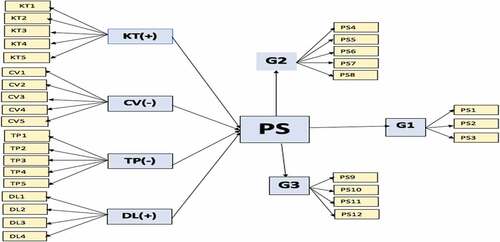

Professional skepticism includes three characteristics: Questioning mind (G1), Suspension of judgment (G2), Search for knowledge (G3). Therefore, in this study, we use three sub-regression models to reflect the influence of the independent variables on each characteristic of professional skepticism and they are presented in Figure as following:

Figure 2. The regression model.

Researchers designed a questionnaire with 31 observations including 1 dependent variable and 4 independent variables, using the 5-level Likert scale (Score 1: Absolutely disagree, Score 5: Absolutely agree). Dependent variable is Professional Skepticism. Model HEP measured professional skepticism by six characteristics. In this study, the research team decided to measure professional skepticism with 12 items according to three main characteristics of Professional Skepticism (a questioning mind, suspension of judgment, search for knowledge).

Independent variables are variables that affect the dependent variable, in other words, the dependent variable is determined by the independent variable. In this research, there are four (4) variables considered four factors that are knowledge & experience (H1) with five observations, workload (H2) with five observations, time pressure (H3) with five observations and incentives (H4) with four observations. The scales of variable are inherited from previous studies by Nelson (Citation2009), Hurtt (Citation2010), (Citation2013), and Zarefar et al. (Citation2016), Brazel et al. (Citation2019), HEP Model used in research of Fullerton and Durtschi (Citation2004) and Mai and Nguyen (Citation2018).

4. Analysis of results

4.1. Descriptive statistical analysis

The Table and Table illustratethe general information related to the demographic information of independent auditors such as working position, level of education, professional qualification, gender, and working experience.

Table 2. Demographic information of respondents related to working positon, education degree, and professional certificate

Table 3. Demographic information of respondents related to gender and working experience

4.1.1. Working positions

According to the Table , the respondents also shared some information about their current employment. Juniors/assistants made up about 12.22% of the participants, which was still higher than the director and partner figures of 10.0% and 8.89%, respectively. Seniors accounted for approximately 41.11% of the total, while managers accounted for 27.78% of the total.

4.1.2. Educational level

In terms of academic achievement, 82.22% of participants have received a bachelor’s degree, while 17.78% of participants have gained a master’s degree. The research concludes that the proportion of the respondents have a Bachelor’s degree and have a solid financial, accounting, and auditing background based on this figure.

4.1.3. Professional certification

This following result shows that 77.78% of the independent auditors in Vietnamese auditing firms held a professional certification such as CPA, ACCA, ICAEW. There are only 22.22% of Independent auditors currently completing international certificates and knowledge to perform independent audit functions.

4.1.3.1. Gender

According to the Table , 48 independent auditors (53.33% of respondents) were male, while 42 independent auditors (46.67% of respondents) were female. Female auditors account for about as many as male auditors.

4.1.3.2. Working experience years

The results also show that the majority of the respondents, 45 respondents (50%) and 27 respondents (30%), have under 5 years of work experience and from 5 to 7 years of work experience, respectively. Auditors working from 7 years to 10 years (11.11%) are slightly higher than auditors with 10 experience years (8.89%). As a result, the majority of respondents have extensive experience performing independent audit functions as presented in Table .

In summary, demographic information of respondents presents that the interviewees account for the majority of key positions to perform the audit requires a lot of professional skepticism to gather audit evidence and make audit conclusions.

4.2. Reliability analysis—Cronbach’s Alpha

The Cronbach’s Alpha coefficient for all items is higher than 0.6 (Table ). The Corrected Item-Total Correlation of each observed independent and dependent variable is greater than 0.3 except for KT1. As a result, the study’s scale only remained 30 observations for subsequent EFA review

Table 4. Cronbach’s alpha

4.3. Exploratory factors analysis

The KMO coefficient computed from the sample is 0.798 greater than 0.5, according to the table of KMO and Barlett’s test results. The Bartlett test has a p-value of 0.000 < 0.05% of variance >50%, the factor loading is greater than 0.5 and the coefficient Eigenvalue >1. Thus, the criteria for using the EFA discovery analysis show that the factors are consistent with the data set of the study. As a result, the survey sample size is sufficient for factor analysis. The correlation between observed factors is zero in the overall statistically significant since the P-value (Sig.) determined from the sample is 0.00 less than a significance level of 0.05, according to Barlett’s test with the hypothesis H0 (or 5%).

The analysis results show that with 12 items to evaluate professional skepticism of independent auditors and three main factors can be extracted (Table ). According to the calculation results from the sample, these 12 factors explain 64.346% of the variation of the data set.

Table 5. Rotated component matrix

4.4. Pearson correlations

The results of correlation analysis revealed that all independent variables influencing the dependent variable PS were statistically significant at the 5%. Many of the Sig. values have a high correlation with the independent variables (KT, DP, CV, and DL).

The author's team used the Pearson coefficient of correlation to analyze the correlation between quantitative variables. In the Table , the coefficients of correlation indicate the relationship between the variables, which is rational in both sign. and level. Specifically, the values of coefficient of correlation (KT, DL) are greater than 0. The coefficients of correlation are positive which show a positive relationship. The coefficients of correlation (CV, TP), on the other hand, are less than 0; the coefficients of correlation are negative, suggesting a negative relationship.

Table 6. Pearson correlations

4.5. Regression analysis

The value of determination coefficient Adjusted R2 is 0.585, which shows the regression model of the relationship between the four main factors to the Professional Skepticism, which can explain 58.5% of the variation of the PS. In the F-test in the ANOVA table, an observed F value of 32.305 with a P-value (Sig.) of 0.000 is less than the significance level of 0.05. The regression model is suitable to describe the relationship between factors to the Professional Skepticism of independent auditors.

Based on the P-value values corresponding to each independent variable in Table , it can be seen that all the independent factors have P-value values less than the significance level of 0.05. It can be said that, with the sample, there is enough evidence to reject the H0 hypothesis. The sign of the regression coefficients reflects the impact of independent factors on dependent factors. The values of βi of these two factors (KT, DL) have positive signs, indicating that these factors have a positive impact on the PS, according to the survey results. Otherwise, these two variables (CV, TP) have negative βi values, meaning that they have a negative effect on the PS. The standardized regression coefficient (Beta) is used to evaluate the impact of each independent factor on PS. The DL factor has a standardized regression coefficient of 0.398, which is higher than the KT factor’s standard regression coefficient, indicating that the DL factor has a greater effect on the independent auditors’ PS. The VIF of variables affecting less than 10 shows that there is no multi-collinear phenomenon. The regression equation of the PS:

Table 7. Coefficient

4.5.1. About sub-regression model

The values of βi of these knowledge and experience variables (KT) and the incentives (DL) have positive signs, indicating that they have a positive effect on the PS. However, the other independent variables (CV and TP) indicate that they influence negatively on the Professional Skepticism. B2 = −153 < 0 indicates that when CV increases by 1 unit, the professional skepticism—Professional Skepticism decreases by 0.153 units; standardized β of the CV variable affects 15.3% on the level of Professional Skepticism. B3 = −0.271 < 0 indicates that when TP increases by 1 unit, the professional skepticism—PS decreases by 0.271 units; standardized β of the TP variable affects 27.1% on the level of PS. The effect of each independent factor on Questioning mind is measured using the standardized regression coefficient (Beta). VIF of factors affecting less than 10 proves no multi-collinear phenomenon. The regression equation of three characteristic of the PS:

All independent variables both have an impact on the three features of the PS. The sign of the regression coefficients reflects the impact of independent factors on dependent factors. According to the survey results, the βi values of these two factors (KT, DL) have positive signs, suggesting that these factors have a positive effect on the PS. The standardized regression coefficient (Beta) is used to evaluate the impact of each independent factor on three characteristics. VIF of factors affecting less than 10 proves no multi-collinear phenomenon.

4.5.2. Research hypothesis testing results

All of the hypotheses that include knowledge and experience, workload, time pressures, and incentives are initially accepted. It turns out that H1 and H4 have a positive impact on professional skepticism, while H2 and H3 have a negative influence on professional skepticism.

4.5.3. Independent sample T-Test

Independent samples T-Test is used to compare mean values of male and female groups with professional skepticism. Because of the sig value = 0.816 > 0.05 (Table ), so we conclude that there is no significant difference in the mean of the two populations. In other words, between the two gender groups of auditors, there is no evidence to show a difference in professional skepticism. Specifically, in the mean column in the Group statistic table below, the average value of professional skepticism for men is 3.5749 and for women is 3.5545 (Table ). Moreover, the authors use independent Samples T-Test to compare the mean of two groups of certified and non-certified auditors affecting professional skepticism. The table indicates that there is no substantial difference in the mean of the two populations because the Sig. value = 0.379 and F = 0.782 in Levene’s Test for Equality of Variances >0.05. In other words, there is little distinction between the two groups of independent auditors who have gained and have not gained the qualification certificate in terms of professional skepticism

Table 8. Independent samples test

Table 9. Independent samples test

5. Discussion

Through linear regression results, two factors, the knowledge & experience and Incentives have positive impacts, while workload and time pressure have been negative influences on professional skepticism of independent auditors.

Previous research indicated that PS is affected by knowledge in both positive and negative ways in audit practice, specializing in fundamental Nelson (Citation2009) research. However, the result in this research are consistent with the results of Griffith et al. (Citation2012) and Grenier (Citation2017) where knowledge has a direct influence on the PS. In addition, experience has a positive impact on PS which has the same point with research of Griffith et al. (Citation2012), Peecher et al. (Citation2010), with conclusion: if auditors are trained to change cognitive thinking processes or biases affect the PS level of auditors. The research results also agree with Tong (Citation2018) that knowledge of auditors is the most influential factor on PS in the Vietnam. Otherwhile, a lot of previous research showed opposite sides of opinion, such as Castro (Citation2013) claim that experience has no effect on PS, and Kim et al. (Citation2015) conclude that the less experienced auditor has a higher PS than the more experienced auditor, Phan et al. (Citation2020) knowledge and experience have the influence on PS, but they have not yet reached a reliable level of significance. Applying to the Vietnam situation, many audits are usually being carried out in particular months of the year, in a peak season, auditors have to work for more than one job at the same time; therefore, experienced trained auditors have higher probability to discover misstatements and tend to have advantages when communicating with clients about their doubtful issues. On top of that, auditors may not only raise their abilities to acknowledge every detailed problem, detect misstatements and combined evidence, but also they are not easily being disturbed by inappropriate information in order to find out misstatements as soon as possible.

Related to incentives, the result pointed out that this factor has a positive influence on professional skepticism of independent auditors which is in agreement with previous studies such Nelson (Citation2009), Nguyen (Citation2020). On the other hand, Phan et al. (Citation2020) which have the same research subject in Vietnam, which showed incentive of auditing firms, have not yet reached the level of confidence in the significance level, despite their influence. The findings of this study are in line with the majority of previous studies around the world. The company’s performance evaluation and incentive system is an important component of the internal quality control that rewards actions based on the auditor’s skepticism towards the firm’s interests, namely contributing to effective audit.

However, workload and time pressure have been negative influences on the professional skepticism of independent auditors. In previous research, there are many controversial results on the impact of time pressure on professional skepticism, whether positive or negative. Typically, Nelson (Citation2009) indicated that time has a positive effect on PS as well as Phan et al. (Citation2020) indicates that time and both workloads have a positive impact on professional skepticism. Nevetheless, the results of this research confirm that time pressure has a negative impact on PS. Time pressure is a common problem in the working environment (Glover, Citation1997) and arises from the conflict between completing an effective but timely audit. Audits and the number of working hours required in the busy season creates a willingness to accept financial information modified by customers’ target achievement (Glover, Citation1997). Time pressures cause performance degradation and cause joint stress practice for the auditor (McDaniel, Citation1990). Low and Tan (Citation2011) argued that the difference between time restriction be informed and random time pressure. When confronted with a sudden increase in time pressure, the auditor is more likely to rely on previous year’s audit procedures, which means the auditor is less likely to show PS as Coram et al. (Citation2004). Similarly, workload factor, according to Nasution and Fitriany (2012 cited in Rahmawati and Indrijawati, Citation2012), the auditor’s workload can be reflected in the vast number of customers that must be managed by auditors, and the pressure of employment that results in excess jobs will decrease job satisfaction and performance of auditors.

6. Conclusion and recommendations

6.1. Firstly, for the independent auditors and independent auditing firms

Recruitment policies may affect professional skepticism by evaluating knowledge and personal traits. Auditing firms need to emphasize the significance of assessing professional skepticism in the employment process in order to select the auditors whose professional skepticism is suitable with the policy of the corporate. It is essential for the company to apply an appropriate payroll regime so that auditors are willing to have long-term attachment with the firms. In addition, the auditing firm must create a working environment as well as a sense of solidarity among auditors and leaders to foster professional skepticism.

Competence of auditors must be maintained and updated regularly through internal training courses of the firms. Consequently, the training policies play a key role in determining PS in knowledge, skills, and personal incentives of auditors. It is also important to schedule training sessions for workers by rank; each class would have its own training program that is specifically connected to each job for each position. It is possible to collaborate with other organizations, such as the Vietnam Association of Certified Public Accountant or professional institutions, to hold workshops on auditor professional ethics.

The audit workload and time pressure are more demanding for auditors due to the burden on time to complete the work progress while conducting the audit, decreasing professional skepticism. Reduce the amount of time it takes to complete tasks and reduce the amount of time it takes to record progress. Until conducting the end-of-fiscal-year audit, auditing companies should conduct interim audits during the year.

A public and transparent incentive and liability scheme for auditors who adhere to ethical skepticism guidelines. Auditors prefer to function well because they have strong entitlements, so auditors can develop policies and processes for evaluating auditors’ results, with a particular emphasis on the opportunity to apply professional skepticism to award, fine, and determine the salaries.

6.2. Secondly, for governmental agencies, especially the ministry of finance and association of chartered auditors

Propagating and strictly enforcing the administrative penalties clauses of the Government’s Decree No 41/2018/ND-CP dated 12 March 2018 on the sanctioning of administrative irregularities in accounting and inspection. independent audit, thus raising awareness about auditing laws; at the same time, deterring auditors from breaking the rules. Arrange daily workshops, instruction, or knowledge sharing sessions relating to professional skepticism so that auditors can exchange and gain realistic experiences.

6.3. Finally, for universities and training institutions

Universities should understand the professional requirements and skills necessary for independent auditors and basing on them to expand their training courses of professional skepticism in combination with professional Independent Audit certification to facilitate the improvement of professional qualifications and skills for independent audit professions.

Vietnam is a developing country, the market economy is incomplete, the independent legal framework has not been established in a comprehensive manner, and corporate governance is still limited, so it has not voluntarily applied. Using advanced management practices to be able to deeply participate in the international market in the integration process. Therefore, the Government agencies, entities and universities should coordinate based on the roadmap, plan, and apply international practices in accordance with the conditions of Vietnam for the development of Vietnam’s Independent Audit.

Despite the accomplishment of the findings and remarks, this study still has a variety of limitations. First, since the study is taking place during Vietnam’s peak season, the number of samples collected is not large enough, so that the statistics might not be completely correct. Second, the restriction is due to a lack of conceptual calculation, two viewpoints on PS, and an acceptable degree of skepticism. As a result, other methods may be used to compare the PS-level evaluation and to compare these measures. Third, in this research, it is pointed out that the effects of independent variables affecting three characteristics of professional skepticism include (questioning mind, suspension of judgment and search for knowledge), not mentioning the rest (interpersonal understanding, self-esteem, and autonomy). Fourth, the concepts can have relationships with each other, with the exception of the relationships between the variables in the model. Fifth, the statistics came from a method that was relying on respondents’ perceptions of the response, which can trigger issues if the respondent is not truthful, as the answer would vary from fact. Following that, direct questioning methods with the auditor should be used in future studies. Sixth, the surveys were created using a URL connection and sent to all of the participants via Facebook messenger and email so that it was hard to assist responders in completing the survey and describing unclear questions in order to increase the number of responders and avoid receiving unreliable answers from the participants. Seventh, the final limitation of the scope of the study is collected information related to the individual auditors working at independent auditing firms. Therefore, the research has not collected information related to auditee such as organizational and management characteristics, characteristics of auditee’s environment, internal control of auditee affecting professional skepticism of independent auditors. From limitation of the research, future research will study more research variables related to characteristics of auditee affecting PS and and increase the number of samples, especially the number of independent auditors interviewed.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Thanh Nga Doan

Nga Doan is a senior lecturer of accounting and auditing at School of Accounting and Auditing- The National Economics University, Vietnam. Her research interests include financial accounting and reporting, management accounting, sustainability, and auditing.

Trang Ta is a senior lecturer of accounting and auditing at School of Accounting and Auditing- The National Economics University, Vietnam. Her research interests include financial accounting and reporting, management accounting, sustainability, fraud audit, internal audit, and financial audit.

Cuong Pham is Associate Professor of Accounting at School of Accounting and Auditing- The National Economics University, Vietnam. His research interests include financial accounting, management accounting, financial statement analysis, earnings management, CSR, and accounting information system.

Nam Tran is statistical lecturer at Faculty of Statistics - National Economics University, Vietnam. His research interests include business administration, data science, sustainability, and statistics.

References

- Almer, E. D., & Kaplan, S. E. (2002). The effects of flexible work arrangements on stressors, burnout, and behavioral job outcomes in public accounting. Behavioral Research in Accounting, 14(1), 1–18. https://doi.org/10.2308/bria.2002.14.1.1

- Anderson, B. H., & Maletta, M. J. (1999). Primacy effects and the role of risk in auditor belief‐revision processes. Auditing: A Journal of Practice & Theory, 18(1), 75–89. https://doi.org/10.2308/aud.1999.18.1.75

- Brazel, J. F., Gimbar, C., Maksymov, E. M., & Schaefer, T. J. (2019). The outcome effect and professional skepticism: A replication and a failed attempt at mitigation. Behavioral Research in Accounting, 31(2), 135–143.

- Brazel, J. F., Jackson, S. B., Schaefer, T. J., & Stewart, B. W. (2016). The outcome effect and professional skepticism. The Accounting Review, 91(6), 1577–1599. https://doi.org/10.2308/accr-51448

- Buchheit, S., Dalton, D. W., Harp, N. L., & Hollingsworth, C. W. (2016). A contemporary analysis of accounting professionals’ work-life balance. Accounting Horizons, 30(1), 41–62. https://doi.org/10.2308/acch-51262

- Castro, G. S. (2013). Internal auditors skepticism in detecting fraud: A quantitative study [ Doctoral dissertation]. Capella University.

- Ciołek, M., & Emerling, I. (2019). Can we shape professional skepticism through university accounting programs? Evidence from Polish University. Sustainability, 11(1), 291. https://doi.org/10.3390/su11010291

- Coram, P., Ng, J., & Woodliff, D. R. (2004). The effect of risk of misstatement on the propensity to commit reduced audit quality acts under time budget pressure. Auditing: A Journal of Practice & Theory, 23(2), 159–167. https://doi.org/10.2308/aud.2004.23.2.159

- Earley, P. C. (1988). Computer-generated performance feedback in the magazine-subscription industry. Organizational Behavior and Human Decision Processes, 41(1), 50–64. https://doi.org/10.1016/0749-5978(88)90046-5

- Fogarty, T. J., Singh, J., Rhoads, G. K., & Moore, R. K. (2000). Antecedents and consequences of burnout in accounting: Beyond the role stress model. Behavioral Research in Accounting, 12(2000), 31–68. Accessed 25 November 2021. https://www.researchgate.net/profile/Jagdip-Singh/publication/228307795_Antecedents_and_Consequences_of_Burnout_in_Accounting_Beyond_the_Role_Stress_Model/links/00463529f17f943472000000/Antecedents-and-Consequences-of-Burnout-in-Accounting-Beyond-the-Role-Stress-Model.pdf

- Fullerton, R., & Durtschi, C. (2004). The effect of professional skepticism on the fraud detection skills of internal auditors. Utah State University. Available at SSRN:

- Glover, S. M. (1997). The influence of time pressure and accountability on auditors’ processing of nondiagnostic information. Journal of Accounting Research, 35(2), 213–222. https://doi.org/10.2307/2491361

- Grenier, J. H. (2017). Encouraging professional skepticism in the industry specialization era. Journal of Business Ethics, 142(2), 241–256. https://doi.org/10.1007/s10551-016-3155-1

- Griffith, E. E., Hammersley, J. S., & Kadous, K. (2012). Auditing complex estimates: Understanding the process used and problems encountered. Auditing: A Journal of Practice & Theory, 31(2), 73–111. https://doi.org/10.2139/ssrn.1857175

- Holstrom, T. (2015). The effect of time pressure on professional skepticism levels exhibited by student auditors. Texas Christian University. Retrieved 20 November 2021. https://repository.tcu.edu/bitstream/handle/116099117/10348/Professional_Skepticism_and_Time_Pressure_by_Taylor_Holstrom.pdf?sequence=1

- Hurtt, R. K. (2010). Development of a scale to measure professional skepticism. Auditing: A Journal of Practice & Theory, 29(1), 149–171. https://doi.org/10.2308/aud.2010.29.1.149

- Hurtt, R. K., Brown-Liburd, H., Earley, C. E., & Krishnamoorthy, G. (2013). Research on auditor professional skepticism: Literature synthesis and opportunities for future research. Auditing: A Journal of Practice, 32(1), 45–97. https://doi.org/10.2308/ajpt-50361

- Kim, S., Trotman, K. T., & Fargher, N. (2015). The comparative effect of process and outcome accountability in enhancing professional scepticism. Accounting & Finance, 55(4), 1015–1040. https://doi.org/10.1111/acfi.12084

- Klein, H. (1989). An integrated control theory model of work motivation. The Academy of Management Review, 14(2), 150–172. https://doi.org/10.2307/258414

- Locke, E. A. (1997). The motivation to work: What we know. In M. M. Maehr & P. R. Pintrich (Eds.), Advances in motivation and achievement, tenth edition (pp. 375–412). JAI Press.

- Low, K. Y., & Tan, H. T. (2011). Does time constraint lead to poorer audit performance? Effects of forewarning of impending time constraints and instructions. Auditing: A Journal of Practice & Theory, 30(4), 173–190. https://doi.org/10.2308/ajpt-10180

- Mai, T. H. M., Nguyen, V. K. (2018). Các nghiên cứu về mối quan hệ giữa thái độ hoài nghi nghề nghiệp và tính độc lập của kiểm toán viên. Ta.p chí khoa ho.c, 12(6), 101–109. ISSN: .

- McDaniel, L. S. (1990). The effects of time pressure and audit program structure on audit performance. Journal of Accounting Research, 28(2), 267–285. https://doi.org/10.2307/2491150

- McMillan, J. J., & White, R. A. (1993). Auditors’ belief revisions and evidence search: The effect of hypothesis frame, confirmation bias, and professional skepticism. Accounting Review, 68(3) , 443–465. Accessed 30 November 2021. https://www.proquest.com/docview/218531879/fulltextPDF/82E2DE3733474F9CPQ/1?accountid=47774

- Nelson, M. W. (2009). A model and literature review of professional skepticism in auditing. Auditing: A Journal of Practice & Theory, 28(2), 1–34. https://doi.org/10.2308/aud.2009.28.2.1

- Nguyen, V. K., (2020). Factors influencing career skepticism and audit quality: Research in Vietnam [ Doctoral dissertation]. University of Economics, Ho Chi Minh City.

- Payne, E. A., & Ramsay, R. J. (2005). Fraud risk assessments and auditors’ professional skepticism. Managerial Auditing Journal, 20(3), 321–330. https://doi.org/10.1108/02686900510585636

- Peecher, M. E., Piercey, M. D., Rich, J. S., & Tubbs, R. M. (2010). The effects of a supervisor’s active intervention in subordinates’ judgments, directional goals, and perceived technical knowledge advantage on audit team judgments. The Accounting Review, 85(5), 1763–1786. https://doi.org/10.2308/accr.2010.85.5.1763

- Persellin, J. S., Schmidt, J. J., Vandervelde, S. D., & Wilkins, M. S. (2019). Auditor perceptions of audit workloads, audit quality, and job satisfaction. Accounting Horizons, 33(4), 95–117. https://doi.org/10.2308/acch-52488

- Phan, T. H., Le, D. T., Le, N. D. Q., Nguyen, T. T. (2020). Research on factors affecting professional skepticism and audit quality: Experiment in Vietnam. International Journal of Innovation, Creativity and Change, 13(1) , 830–847. https://www.researchgate.net/profile/Hai-Phan-Thanh/publication/341755895_Research_Factors_Affecting_Professional_Skepticism_and_Audit_Quality_Evidence_in_Vietnam/links/5ed20de745851529451bdeae/Research-Factors-Affecting-Professional-Skepticism-and-Audit-Quality-Evidence-in-Vietnam.pdf

- Quadackers, L., Groot, T., & Wright, A. (2014). Auditors’ professional skepticism: Neutrality versus presumptive doubt. Contemporary Accounting Research, 31(3), 639–657. https://doi.org/10.1111/1911-3846.12052

- Rahmawati, H. S., & Indrijawati, A. (2012). Auditor Experience, Work Load, Personality Type, And Professional Auditor Skeptisism Against Auditors' Ability In Detecting Fraud. Talent Development & Excellence, 12(2), 1878–1890. Retrieved 25 November 2012. https://www.researchgate.net/profile/Arifuddin-Mannan-2/publication/348446272_Auditor_Experience_Work_Load_Personality_Type_And_Professional_Auditor_Skeptisism_Against_Auditors_'Ability_In_Detecting_Fraud/links/5fffddfa92851c13fe0d7ead/Auditor-Experience-Work-Load-Personality-Type-And-Professional-Auditor-Skeptisism-Against-Auditors-Ability-In-Detecting-Fraud.pdf

- Sullivan, J. J. (1988). Three roles of language in motivation theory. Academy of Management Review, 13(1), 104–115. https://doi.org/10.5465/amr.1988.4306798

- Sweeney, J. T., & Summers, S. L. (2002). The effect of the busy season workload on public accountants’ job burnout. Behavioral Research in Accounting, 14(1), 223–245. https://doi.org/10.2308/bria.2002.14.1.223

- Tong, T. T. (2018). Factors affecting professional skepticism of independent auditors in auditing financial statements - empirical research at auditing firms in Ho Chi Minh City [ Master thesis]. Ho Chi Minh City University of Economics.

- Trompeter, G. M., Carpenter, T. D., Desai, N., Jones, K. L., & Riley, R. A. (2013). A synthesis of fraud-related research. AUDITING: A Journal of Practice & Theory, 32(1), 287–321. https://doi.org/10.2308/ajpt-50360

- Zarefar, A., Zarefar, A., & Zarefar, A. (2016). The influence of ethics, experience and competency toward the quality of auditing with professional auditor scepticism as a moderating variable. Procedia-Social and Behavioral Sciences, 219(1), 828–832. https://doi.org/10.1016/j.sbspro.2016.05.074