?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Traditional assets, like stocks and bonds, are mostly found to be highly influenced by uncertainties, and cause distress for investors most of the time, consequently investors look for safe investment options that can provide diversification benefits to cope with uncertainties. So, current research unveils the diversification characteristics of real estate by investigating its relationship with a set of selected financial assets like KSE-100 index, gold, sub-asset classes; growth stocks, value stocks, large stocks, small stock, and sector’s stock. Autoregressive distributive lag (ARDL) approach is employed on monthly time series data for a time span of 2011 to 2019. Findings indicate that real estate behaves quite differently than all of these assets and holds good diversification potential for Pakistani investors because it exhibits no relationship with any of the assets under study. Findings suggest that Pakistani investors must incorporate real estate in their asset allocation strategy for diversifying their portfolios. Current research contributes to literature by unveiling the diversification potential of real estate in comparison to a set of financial variables that are rarely investigated in previous literature. Moreover, it contributes well to the knowledge of Pakistani investors and asset/investment managers to make healthy investment decisions.

PUBLIC INTEREST STATEMENT

Dynamic business environments and highly volatile markets lead to mounting uncertainties surrounding the investment environments. Literature documents evidence for influence of such uncertainties on financial markets and economies, but it lacks documenting the mitigating measures, that if investments are hit by uncertainties then what should investors do to cope with the surprises and still enjoying benefits of their investments. The answer is diversification. But then the significant question arises here that which assets provide diversification benefits to investors. Hence, there is a need to explore the diversification characteristics of different assets. In this regard, current research explored the diversification characteristics of real estate in comparison with stocks, gold and some sub-asset classes and it is found that real estate is a good diversifier and investors should consider it in their asset allocation strategy.

1. Introduction

Uncertainties have become the fact of investors’ life. So amplified market volatilities along with subpar financial instruments’ performance have led investors to search for alternative assets (Oztek & Ocal, Citation2017); that do not belong to the traditional asset class of stocks and bonds, have differing features and lower or no correlations with traditional assets, so that they can generate more diversification benefits for a portfolio (Jacobs et al., Citation2014).

Real assets are the tangible assets that provide possession of the store of value (Brookfield, Citation2017), like precious metals, real estate, substantial resources, infrastructure etc. initially attracted institutional investors, but fluctuations in financial markets, economic conditions and political uncertainties have compelled individual investors as well to consider these as an alternative investment option (Davidow & Peterson, Citation2014; Davis et al., Citation2014; Phillips et al., Citation2017). Since last decade, institutional investors have enjoyed greater returns from real assets than traditional investments, due to significantly lesser volatilities (Low et al., Citation2016), low or negative correlations with traditional assets (Chan et al., Citation2011), and potential benefits to portfolios like inflation protection, portfolio level diversification, differentiated source of income and returns etc. (Mercer, Citation2014). Moreover, real assets are found to behave differently than traditional assets in varying economic and market conditions (Manganelli, Citation2015), thus individual investors could also cope with surprises through incorporation of some real assets in their portfolio (Brookfield, Citation2017; Chan et al., Citation2011).

Despite increasing popularity of alternative investments among investors of developed nations like UK and US (Brookfield, Citation2017; Deutsche Asset Management, Citation2016; Mercer, Citation2014), investors in emerging economies, like Pakistan who face uncertainties more frequently, are still unaware of the diversification benefits of such assets.

1.1. Uncertainties in Pakistan

Uncertainties surround all economies, and same is the case with Pakistan. Its long history provides evidence of various uncertainties hitting it severely (Rasheed & Tahir, Citation2012), including economic and political uncertainties among the dominating ones that significantly influence the investment behaviors in Pakistan (Abbas et al., Citation2019), and contribute significantly in stock market movements (Sarwar et al., Citation2013). Pakistan stock exchange (PSX) is found to be highly influential by such uncertainties (Ghufran et al., Citation2016; Murtaza et al., Citation2015; Nazir et al., Citation2014) so investors in such economies require some safe alternative investment options more critically, that can protect them during uncertain conditions.

In this regard, gold is widely investigated to act as a hedge or a safe haven during certain market, economical and political conditions, and is found to provide protection to investors due to its diversification characteristics (Baur & McDermott, Citation2016; Iqbal, Citation2017; Rasheed et al., Citation2021a) but rare evidence is found in literature which highlights the diversification benefits of real estate as alternative investment option, especially in Pakistan. Therefore, current research investigates the relationship of real estate not only with different kinds of stocks and PSX sectors, rather it also incorporates gold in its investigation to highlight the fact that whether investors considering stocks and gold in their diversified portfolios, must also consider real estate for diversification purpose? Current study contributes academically and practically as to the best of authors’ knowledge; no such investigation has been made by researchers or practitioners in Pakistan. Being a part of highly unstable economy, researchers as well as investment managers must understand the need for searching some safe alternatives that may protect investors against turmoil. Thus, by investigating the relationship of real estate with gold, KSE-100 index, PSX sectors, and sub-asset classes like growth stocks, value stocks, large stocks and small stocks, current study is a great contribution to investment and asset allocation literature and towards Pakistani investors’ knowledge by highlighting the fact that whether real estate possess diversification characteristics by having lower or no correlations with other assets or it co-moves with these? Following it, they can make healthy investment decisions that whether they should incorporate real estate in their portfolios for diversifying their traditional portfolio and getting generous returns from their investments.

2. Literature review

When uncertainties rise in the economy, investors usually move towards searching for alternative investments that can perform better amid such circumstances. Traditional investment strategies suggest investing in stocks, bonds etc. and allocating different weights to these traditional assets to diversify the risk of portfolio. But contemporary asset allocation strategies suggest allocating different non-traditional assets to the portfolios for enjoying better diversification benefits (Rasheed et al., Citation2021a).

2.1. Investment strategies and diversification

Initially, the concept of diversification was introduced by H. Markowitz (Citation1952). Markowitz’s work as a foundation of Modern Portfolio Theory (H. M. Markowitz, Citation1991), determines that the overall risk of the portfolio could be reduced by incorporating investments having lower correlations with one another. Since then greater contributions are made in Modern Portfolio Theory by many researchers like the introduction of CAPM by Sharpe (Citation1964) to describe the association of risk and return. Contributing further, Brinson et al. (Citation1986) and Ibbotson and Kaplan (Citation2000) studied the impact of asset allocation decisions on investment returns and found significant impact of asset allocation policy on individual investors’ level of return. But all these merits of Modern Portfolio Theory were criticized severely after 2008 financial crisis, as higher correlations were indicated between asset classes amid market turmoil, hence undermining diversification benefits when they were highly required by investors (Theron et al., Citation2018).

Despite all these facts, asset allocation is still found to be effective in investor portfolios even during market stress and diversification also still makes sense unless assets do not move in perfect lockstep (Benlagha & Hemrit, Citation2021; Feng et al., Citation2021; Jacobs et al., Citation2014). But a significant change in asset allocation strategies is to focus on the selection of asset classes to incorporate in a portfolio (Davidow & Peterson, Citation2014) as well as making strategic adjustments to the weights of assets according to the long- or short-term changes in economic or market environment (Wu et al., Citation2017).

2.2. Modern asset allocation

New market realities like increased assets’ correlations, increased external shocks, dominating equity risks, lowering bond yields and stock returns require Modern Portfolio Theory to evolve further (Davis et al., Citation2014). Such market realities and changing economic conditions caused asset allocation to evolve from traditional combinations of stocks, bonds and cash to non-traditional asset classes (Chan et al., Citation2011). Contemporary asset allocation now comprehends non-traditional asset classes like commodities, other real assets etc. (Ampomah et al., Citation2014), but allocation to these asset classes requires critical analysis of diversification potential of different assets for implementing an effective asset allocation strategy (Bredin et al., Citation2015).

According to Davidow and Peterson (Citation2014), contemporary asset allocation is based on three different perspectives: the weights of asset classes should be chosen in a manner that could enhance expected return at a certain level of risk, the aim of asset class weights should be to diversify the risk across numerous asset classes, and asset allocation should have a specific goal like income generation, inflation hedge, absolute return etc., which means contemporary asset allocation still relies on Modern Portfolio Theory assuming that investors are more concerned about avoiding losses than for acquiring gains (Manganelli, Citation2015).

Moving towards alternative investment options, investors face a critical question that which asset classes should be included in the portfolio to diversify portfolio risk? An important aspect of diversification is the lower or negative correlations of assets so that maximum diversification benefits could be availed by investors (Benlagha & El Omari, Citation2021; Chan et al., Citation2011). Due to negative or lower correlations with traditional assets like stocks (Mercer, Citation2014), the real assets, like precious metals (gold, silver etc.), real estate, infrastructure, energy etc., are becoming the priority of investors in their asset allocation strategy (Holmes et al., Citation2018; Vicente et al., Citation2015).

2.3. Real estate: from asset class to asset

Real estate, as a source of income as well as its appreciation potential, has made it to be considered as a value-added investment (Manganelli, Citation2015). Making more tangible asset investments, like real estate, is an emerging trend among institutional as well individual investors now a day (Candelon et al., Citation2021; He, Citation2002). Due to increased market turmoil and a need for alternative investment options, initially institutional investors draw their attention towards investing in real assets like real estate (Guo, Citation2010). But the diversification benefits enjoyed by institutional investors have also attracted individual investors and their asset managers to consider real estate as a part of their diversified portfolio (Holmes et al., Citation2011, Citation2017; Phillips et al., Citation2017), so real estate as an alternative investment has become an attractive and widely spoken topic among asset managers and investors (Damardji, Citation2017; Seiler et al., Citation2008).

Real estate generates returns for investors either by reselling at a higher price or through a continuous series of rent as a source of income (Damardji, Citation2017). The increasing demand of rental dwellings leading to increasing rental rates as well as potential of capital appreciation has made real estate as an attractive investment option (Seiler et al., Citation2008). The longer investment period provides a significant level of safety against uncertain depreciations in markets. Moreover, the longer duration makes it capable of recovering well from downturns (Rasheed et al., Citation2021b).

Despite these facts, real estate investments require certain aspects to be considered very carefully like recent market condition, the reputation and key features of location, rental level and price, and a need for renovation (Panagiotidis & Printzis, Citation2016; Phillips et al., Citation2017). Although its long investment horizon and requirement of huge starting capital than stocks, makes it less attractive for some investors, but on the other hand certain inherent features make it as an attractive investment for others (Chan et al., Citation2011). The imperfection of real estate market due to the heterogeneity of properties in terms of age, location, size, quality etc. creates difficulty for accurate price formation hence leaving a room for individuals to influence prices (Pellatt, Citation1972). In such situation, it provides opportunity for investors to make comparatively better deals to enhance profits (Manganelli, Citation2015). Moreover, the diversification benefits provided by real estate investment in a portfolio also makes it an attractive investment option (Brookfield, Citation2017).

2.4. Real estate in a real asset portfolio

Real asset portfolio construction is a complete process requiring numerous considerations in terms of strategy selection, planning, monitoring, implementation, and capitalization of opportunities (Mercer, Citation2014). It incorporates considering investors’ objectives for defensive or a growth strategy as well as his/her inflation sensitivity (Deutsche Asset Management, Citation2016). Providing a diversified strategy is imperative for a real asset portfolio so that along with corresponding to investors’ objectives, overall risk or volatility of the portfolio should also be mitigated (Kaplan, Citation2015). A significant aspect of building a real asset portfolio is balancing between complexity tolerance and liquidity requirement. Real assets play multiple roles in a portfolio like diversification and return generation (Chan et al., Citation2011). Although diversification, returns, inflation linkage and store of value feature of real assets make them as an attractive option for portfolio construction but the risks and benefits of real assets should be considered in the overall context of the portfolio (He et al., Citation2017).

Contradictory views prevail regarding the behaviors of real assets during uncertainties, some finding these as a safe investment option during uncertainties while others finding these as weak performers (Phillips et al., Citation2017). Similarly, real estate is also found to exhibit varying behaviors under varying conditions like Pellatt (Citation1972) argue that despite being safe as a long-term investment, real estate investments have greater exposure to risks as compare to equities due to the ignorance of investors. Investors are found to be less knowledgeable for real estate investments and its market conditions as compare to stock markets. Guo (Citation2010) indicates that the heterogeneity of real estate assets due to age, design, location, functional utility etc. and its long horizon for investment causes inherent uncertainties in property prices, while the lack of precise knowledge about property market makes such investments more exposed to external uncertainties.

Seiler et al. (Citation2008) suggest that real estate attributes appraisal requires great deal of judgment to appraise its price appropriately, because according to Squirrell () real estate investment is a one-shot decision requiring huge investment capital along with the risk of loss due to inappropriate knowledge and judgment about property and real estate market. Phillips et al. (Citation2017) state that declining returns, lowering yields, sluggish economic growth and eroded political certainty may cause other assets no longer holding the status of safe haven, hence attracting investors towards real estate investments. Although investors’ appetite for real estate is increasing but the outlook is clouded by uncertainty. Geopolitical challenges are the dominating ones surrounding real estate industry in recent era, and the outperformers may turn into underperformer following uncertain political events. Damardji (Citation2017) states that the emerging concern for real estate is becoming more significant due to increased social disputes and global political instability. Although political instabilities and social issues are clouding the outlook of economies, but still real estate investors are found to be more confident than others.

Based on the above discussion, current study proposes the main research question as; could real estate provide diversification benefits to Pakistani investors by indicating no relationship with the other assets under study or it fails to provide diversification by co-moving with these assets?

3. Research methodology

Appropriate methodologies play a significant role in fulfilling the purpose of study. Selected methodology should be suitable for finding reliable answers for the proposed research questions so that inferences can be made accordingly and accurately.

3.1. Data description and sample

The study uses share prices of firms listed on Pakistan Stock Exchange, prices of KSE 100 index, prices of gold bullion and real estate prices in Pakistan. The financial information of listed firms as well as KSE 100 index is collected from official website of Pakistan Stock Exchange (PSX), data for daily gold prices (gold bullion Pkr. per Tola) is obtained from goldrates.pk (https://goldrates.pk) and data for property prices (price per sq. ft.) is collected from Zameen.com (The leading property portal in Pakistan). The time span of current study is from January 2011 to December 2019. As of December 2019, there were 35 sectors listed on Pakistan stock exchange, but current study incorporates 33 sectors due to the limitation of data availability of 2 sectors. Among the selected 33 sectors, 471 listed companies are included in study out of a total of 543 listed companies on Pakistan stock exchange, hence representing more than 85% of the population.

4. Asset returns

Initially log returns of all assets under study are calculated using their current and previous day prices through following formula:

where Rit is the normal return for asset i at time t, Pit is the current price of asset i at time t, and Pit-1 is the previous day price of asset i. These calculated asset returns are used for further empirical analysis.

4.1. Time series analysis

Selection of an appropriate methodology for time series analysis depends on the stationary of data because methodologies suitable for stationary data could not be implemented for non-stationary data. Unit root test indicates the stationary or non-stationary of variables (Shabbir et al., Citation2019) hence; ADF (Augmented Dickey-Fuller) test is implemented to test the stationary of series under study.

5. ADF (Augmented Dickey-Fuller) test

ADF test proposes the null hypothesis of having unit root (non-stationary series) while if test statistics do not support null hypothesis then series is assumed to be stationary. Test results are compared with the critical values and null hypothesis is rejected if value of test statistics is lower or more negative than the critical values (Shrestha & Bhatta, Citation2018).

reports the results of ADF test (at level), indicating that the null hypothesis for all the variables under study is rejected except for real estate. Test statistics are compared with the test critical values at 1%, 5% and 10% significant levels. Results show that the test statistics are significantly lower than the critical values for all the variables indicating that the variable returns are stationary at level while real estate is tested at first difference as well and found to be stationary at 1st difference so based on these characteristics of series Autoregressive Distributed Lags (ARDL) model best suits for empirically investigating the relationship of variables under study.

Table 1. ADF test results for data series at level

5.1. Autoregressive distributive lags model (ARDL)

ARDL test allows stationary and non-stationary series to be investigated at same time. ARDL models are OLS-based models that not only allow investigating non-stationary time series but also series with mix order of integration (Shrestha & Bhatta, Citation2018). This approach helps identifying long-term relationships even for small data series. Moreover, it assumes the variables to be of I(0) and I(1) or a mixture of both but not of I (2). Simply, if data series are stationary at level, or stationary at 1st difference, or a mixture of both then ARDL approach is suitable for investigating their long-term relationships (Shabbir et al., Citation2019). Therefore, current study applies ARDL approach to find out the relationship of real estate I(1) with all other assets’ I(0) under study. The model can be specified as follows:

where

RER = Real estate returns

KR = KSE 100 index returns

GR = Gold returns

GrR = Growth stock returns

VR = Value stock returns

LR = Large stock returns

SR = Small stock returns

SecRi = Sectori’s stock returns

ARDL approach helps identifying the long-term relationships between real estate and all other non-traditional assets under study. If existence of long-term relationship is indicated, then it creates an ECM (error correction model) equation for all assets under study. The coefficients resulting from the ECM equation indicate about the speed of dependent variable to return to equilibrium after any shock. ARDL long-run bound test statistics is used to identify the long-run relationship of variables. Estimation equation for ARDL model is specified as follows:

where n = length, indicate the short-run elasticity of above model and

indicate long-term elasticity. Null hypothesis for ARDL long-run bound test proposes absence of long-run relationship, while F statistics resulting from bound test is considered to support or reject the null hypothesis by comparing it with the lower and upper bound CVs (critical values). Null hypothesis of absence of long-run relationship is supported if the resulting F statistics value is less than the lower bound CV indicating that the variables under study do not hold any long-run relationship. While null hypothesis is rejected if F statistics is higher than the upper bound CV hence indicating the presence of long-run relationship, while if the value of F statistics falls between upper and lower bounds than the result is inconclusive.

If long-run relationship is found to be present among variables then optimal lag length is selected for variables through different criteria like SBC (Schwarz Bayesian criterion) or AIC (Akaike Information criterion) and the resulting long-term and short-term coefficients are predicted. The long-run form of ARDL is indicated in equation (3):

Equation (4) indicates the ECT (error correction term) used in the short-run ARDL model depicting short-run dynamics:

where ECT indicates the error correction term.

Current study applies the above mentioned ARDL model to indicate the relationship of real estate with all other variables of study and helps finding the answer for the proposed research question. The absence of relationship between real estate and other assets under study would indicate its diversification potential, while the presence of relationship would indicate its failure as a diversifier.

6. Results and findings

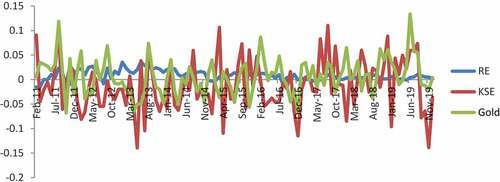

Graphical representation of the behavior of real estate returns in relation to gold and stock market is as follows:

Graph 1. Behavior of real estate, gold and KSE 100 index.

indicates the behavior of return series of real estate, gold and stocks in Pakistan for a time span of 2011 to 2019. It is indicated that real estate returns have quite different movements than gold and stocks.

indicates the graphical representation of the behavior of returns of real estate, gold and KSE 100 index for the time period under study. The graph indicates that although real estate returns also indicate fluctuations but gold and KSE 100 index exhibit more volatile behavior as compare to real estate. Moreover, it is also indicated that in contrast to two other assets, real estate rarely indicates negative returns. So the graphical representation indicates that real estate behaves differently than the two other assets so it could provide diversification benefits, so the diversifying behavior of real estate is further explored by investigating the relationship of real estate with stock market, gold, sub-asset classes and sectors’ stock using ARDL approach.

6.1. Descriptive stats of variables under study

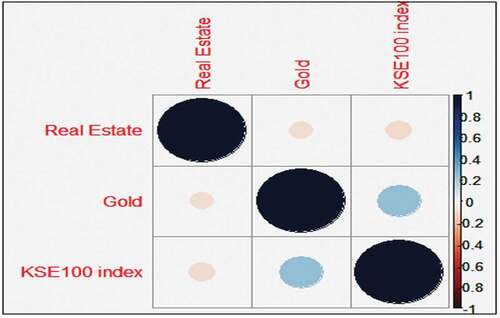

indicates that real estate exhibits less extreme minimum and maximum values as compare to gold and stock exchange, and also indicates comparatively lower standard deviation. Moreover, it is indicated that kurtosis coefficients of almost all variables are less than three and skewness coefficients are mostly positive, lie between −0.5 to 0.5, which means distribution of returns produces fewer and less extreme outliers than does the normal distribution as well as the distribution is fairly symmetrical. A correlation matrix for real estate, gold and KSE100 index is generated:

Figure 1. Correlation matrix of real estate, gold and KSE100 index.

Table 2. Descriptive stats of assets under study

The negative correlation of real estate with gold and stock market indicates that real estate do not move with any of these assets rather moves in opposite direction.

6.2. Autoregressive distributive lags (ARDL) bounds test

Initially, the long-run bound test is implemented in order to identify the long-run relationship between variables. Test statistics of bound test facilitate identifying the presence of cointegration or long-run relationship in variables under study while inferences are made on the basis of resulting values of F-statistics compared with its upper and lower bounds. When bound test provides evidences of the existence of long-run relationship then error correction model is implemented to find out the extent of convergence of any short-term disequilibrium towards long-run relationship.

Moreover, if the existence of long-run relationship between variables is evident then the selection of appropriate lag length is important in such modeling while the optimal number of lags can be selected by using available lag length selection criteria. Some most popular criteria are Schwartz Bayesian Criterion (SBC), Akaike Information Criterion (AIC), and Hannan Quinn criterion (HQC), so that the short- and long-run coefficients could be predicted (Shrestha & Bhatta, Citation2018).

The test results are as follows:

indicates the test statistics of ARDL long-run bound test for real estate, gold, KSE, growth, value, large and small stocks, where real estate is the dependent variable. It is indicated that the calculated value of F-statistics falls below the lower bound at all significance levels. Hence, results indicate that real estate does not show any significant relationship with stock exchange, gold, growth, value, large and small stocks. Hence, there is no evidence for long-run relationship between these variables, so there is no need to further investigate the short form of this relationship.

Table 3. Test statistics of long-run relationship real estate, gold, KSE, sub-asset classes

indicates the test statistics of ARDL long-run bound test of real estate with seven sectors; Automobile Assembler (AMAS), Automobile parts and accessories (AMPA), Cable and electric goods (CAEG), Cement (CMNT), Chemical (CHEM), Close-end mutual funds (CEMF), and commercial banks (BANK). It is indicated that the calculated value of F-statistics falls below the lower bound at all significance levels. Hence, results indicate that real estate does not show any significant relationship with all the above sectors. As, there is no evidence for long-run relationship between these variables, so there is no need to further investigate the short form of this relationship.

Table 4. Test statistics of long-run relationship real estate and sectors (1–7)

indicates the test statistics of ARDL long-run bound test for Real estate, Engineering (ENGR), Fertilizer (FRTZ), Food and Personal Care Products (FPCP), Glass and Ceramics (GACR), Insurance(INSR), Inv. Banks/ Inv. Cos./Securities Cos. (INVBK) and Leasing Companies (LEAS), where real estate is the dependent variable. It is indicated that the calculated value of F-statistics falls below the lower bound at all significance levels. Hence, results indicate that real estate does not show any significant relationship with the above-mentioned stocks. As, there is no evidence for long-run relationship between these variables, so there is no need to further investigate the short form of this relationship.

Table 5. Test statistics of long-run relationship real estate and sectors (8–14)

indicates the test statistics of ARDL long-run bound test for Real estate, Leather and Tanneries (LEAT), Miscellaneous (MISC), MODARABA (MODR), Oil & Gas Exploration Companies (OGEC), Oil & Gas Marketing Companies (OGMC) and Paper & board (PABR), where real estate is the dependent variable. It is indicated that the calculated value of F-statistics falls below the lower bound at 1% significance levels. Hence, results indicate that real estate does not show any significant relationship with these sectors. As, there is no evidence for long-run relationship between these variables, so there is no need to further investigate the short form of this relationship.

Table 6. Test statistics of long-run relationship real estate and sectors (15–20)

indicates the test statistics of ARDL long-run bound test for Real estate, Pharmaceuticals (PHRM), Power Generation & Distribution (PWGD), Refinery (REFN), Sugar and Allied Industries (SUGR), Synthetic and Rayon (SYAR) and Technology & Communication (TECH), where real estate is the dependent variable.

Table 7. Test statistics of long-run relationship real estate and sectors (21–26)

indicates that the calculated value of F-statistics falls below the lower bound at 1% significance levels. Hence, results indicate that real estate does not show any significant relationship with Pharmaceuticals, Power Generation & Distribution, Refinery, Sugar and Allied Industries, Synthetic and Rayon and Technology & Communication sectors. As, there is no evidence for long-run relationship between these variables, so there is no need to further investigate the short form of this relationship.

indicates the test statistics of ARDL long-run bound test for Real estate, Textile Composite (TEXC), Textile Spinning (TEXS), Textile Weaving (TEXW), Tobacco (TOBC), Transport (TRNS), Vanaspati & Allied Industries (VAAI), and Woolen (WOOL), where real estate is the dependent variable. It is indicated that the calculated value of F-statistics falls below the lower bound at all significance levels. Hence, results indicate that real estate does not show any significant relationship with Textile Composite, Textile Spinning, Textile Weaving, Tobacco, Transport, Vanaspati & Allied Industries, and Woolen. As, there is no evidence for long-run relationship between these variables, so there is no need to further investigate the short form of this relationship.

Table 8. Test statistics of long-run relationship real estate and sectors (27–33)

6.3. Discussion

Empirical analysis indicates that real estate in Pakistan does not exhibit any kind of relationship with stock market, gold or the sub-asset classes under study. As indicated by Baur and McDermott (Citation2016) an asset having lower or no correlation with other assets could provide better diversification in portfolios so through indicating the absence of relationship with all the other assets under study, real estate qualifies the criteria for being a good diversifier for investment portfolios of Pakistani investors. As Pakistan has a long history of its financial markets and economy being hit by uncertainties most of the time (Rasheed et al., Citation2021a) so Pakistani investors must focus on incorporating such assets, like real estate, in their portfolios that can provide them diversification benefits by indicating no relationship with other assets. Because non-existence of any relationship of real estate with the assets under study indicates that if these assets are hit by any kind of uncertainty and investors of these assets have to face losses, then real estate can save them by having different behavior than all of these assets because the time other assets are being hit by any uncertainity, real estate would be safe from such risk. Hence, the findings suggest that Pakistani investors must consider real estate as an alternative investment for diversification purpose and must incorporate it in their portfolios because having such good diversification potential it would generate benefits for Pakistani investors during acute circumstances. So having no relationship with other assets under study, it should be the part of asset allocation strategy of individual investors in Pakistan. Current study has practical implications for investment/asset managers in Pakistan because following the findings of current research they could create optimal portfolios for their risk adverse clients by incorporating real estate in their portfolios.

7. Conclusion and recommendations

Amplified uncertainties surrounding investments have ignited the need to search for safe investment options that could provide diversification benefits to investors and help them coping with the risk of uncertainties. During recent dynamic business environment, financial markets are found to be highly influential by uncertainties, either economic, market or political. As Pakistan is among unstable economies across globe, so Pakistani investors face uncertainties and acute market conditions more frequently which cause distress for them for their future returns. Such scenario emphasized the need for searching for some safe alternative investment options like assets that do not co-move with each other during uncertain situations.

Current research makes a contribution in searching for such alternative investment option by investigating the behavior of real estate against KSE-100 index, gold, PSX sectors, and sub-asset classes; growth stocks, value stocks, large stocks and small stocks. Employing Autoregressive distributive lags (ARDL), the long-run relationship of real estate is investigated against all assets and it is found that real estate does not exhibit any relation with PSX, its sectors, sub-assets classes and even gold, which means that real estate does not co-move with any of these assets, rater has quite different behavior and reacts differently than these in varying circumstances. So the uncertainties hitting other assets would not influence real estate in same manner, which means real estate has the potential to provide diversification to traditional investment portfolios in Pakistan. Moreover, the behavior of real estate, KSE-100 index and gold returns is compared during the period under study through their graphical representation and it is found that real estate returns have comparatively smooth patterns as compared to the high volatilities of gold and stocks, and it rarely indicated negative returns during the whole time span under study as compare to gold and KSE100 index, which means that real estate provides better protection even than gold, so investors already considering diversification through gold in traditional portfolios should also incorporate real estate in their portfolios for having highly diversified portfolio.

Hence, results imply that real estate can be considered among the best diversifiers for asset allocation strategies, because having no relation with traditional assets, the sub-asset classes and even gold makes it a safe asset that can protect investors during uncertain situations. Pakistan stock exchange is highly influential for economic and political uncertainties, so Pakistani investors must incorporate real estate in their portfolios to make it an optimal portfolio that can provide protection to cope with the risk of such uncertainties.

8. Future recommendations

Still a huge gap exists in the area of real estate research, especially in the context of Pakistan, so researchers and asset managers should search for some other safe alternatives for investors so that investors in Pakistan and from other emerging economies may have a variety of safe options from where they can choose according to their risk and return appetite.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Hafsa Rasheed

Hafsa Rasheed is a PhD Scholar at Air University School of Management (AUSOM), Islamabad, Pakistan. Her research interests are Portfolio Management and Asset Allocation.

Habib Ahmad

Habib Ahmad is an Associate Professor at Air University School of Management (AUSOM), Islamabad. His research interests are Portfolio Management, Financial Vulnerability of Households, Microfinance and Capital Markets.

Attiya Yasmin Javid

Attiya Yasmin Javid is a Professor of Economics at Pakistan Institute of Development Economics (PIDE), Islamabad. Her research interests are Financial Economics, Financial Markets and Asset Management.

Idrees Khawaja

Idrees Kawaja is an Associate Professor and Senior Economist at Pakistan Institute of Development Economics (PIDE), Islamabad. His research interests are Economic Policy Implications, Financial Assets and Financial Economics.

References

- Abbas, A., Ahmed, E., & Husain, F. (2019). Political and economic uncertainty and investment behavior in Pakistan. The Pakistan Development Review, 58(3), 307–17. https://doi.org/10.30541/v58i3pp.307-331

- Ampomah, S. A., Gounopoulos, D., & Mazouz, K. (2014). Does gold offer a better protection against losses in sovereign debt bonds than other metals? Journal of Banking and Finance, 40(C), 507–521. https://doi.org/10.1016/j.jbankfin.2013.11.014

- Baur, D. G., & McDermott, T. K. J. (2016). Why is gold a safe heaven? Journal of Behavioral and Experimental Finance, 10(8), 63–71. https://doi.org/10.1016/j.jbef.2016.03.002

- Benlagha, N., & El Omari, S. (2021). Connectedness of stock markets with gold and oil: New evidence from COVID-19 pandemic. Finance Research Letters, 46(B), 1–8. https://doi.org/10.1016/j.frl.2021.102373

- Benlagha, N., & Hemrit, W. (2021). Does investment in insurance stocks reap diversification benefits? Static and time varying copula modeling. Communications in Statistics-Simulation and Computation, 1–19. https://doi.org/10.1080/03610918.2021.1884713

- Bredin, D., Conlon, T., & Poti, V. (2015). Does gold glitter in the long-run? Gold as a hedge and safe heaven across time and investment horizon. International Review of Financial Analysis, 41(C), 320–328. https://doi.org/10.1016/j.irfa.2015.01.010

- Brinson, G., Hood, R., & Beebower, G. (1986). Determinants of portfolio performance. Financial Analysts Journal, 51(1), 133–138. https://doi.org/10.2469/faj.v51.n1.1869

- Brookfield. (2017). Real assets real diversification.

- Candelon, B., Fuerst, F., & Hasse, J. B. (2021). Diversification potential in real estate portfolios. International Economics, 166, 126–139. https://doi.org/10.1016/j.inteco.2021.04.001

- Chan, K. F., Treepongkaruna, S., Brooks, R., & Gray, S. (2011). Asset market linkages: Evidence from financial, commodity and real estate assets. Journal of Banking and Finance, 35(6), 1415–1426. https://doi.org/10.1016/j.jbankfin.2010.10.022

- Damardji, Y. (2017). Real estate: Uncertainty is the new market reality. Luxembourg Press Release. https://www.pwc.lu/en/press-releases/(2017)/real-estate-uncertainty-new-market-reality.html

- Davidow, A. B., & Peterson, J. D. (2014). A modern approach to asset allocation and portfolio construction. Schwab Center for Financial Research. Charles Schwab and Co. Inc.

- Davis, H., Minaya, J., & Hopper, T. (2014). Private real assets: Improving portfolio diversification with uncorrelated market exposure. TIAA-CREF Asset Management. TIAA-CREF Financial Services. Teachers Insurance and Annuity Association-College Retirement Equities Fund.

- Deutsche Asset Management. (2016). Utilizing real assets in strategic asset allocation. Deutsche AM Distributors, Inc.

- Feng, Y., Yao, S., Wang, C., Liao, J., & Cheng, F. (2021). Diversification and financialization of non-financial corporations: Evidence from China. Emerging Markets Review, 50(March), 100834. https://doi.org/10.1016/j.ememar.2021.100834

- Ghufran, B., Awan, H. M., Khakwani, A. K., & Qureshi, M. A. (2016). What causes stock market volatility in Pakistan? Evidence from the field. Economics Research International, 2016, 1–9. https://doi.org/10.1155/2016/3698297

- Guo, P. (2010). Private real estate investment analysis within a one-shot decision framework. International Real Estate Review, 13(3), 238–260. https://doi.org/10.53383/100127

- He, L. T. (2002). Excess returns of industrial stocks and the real estate factor. Southern Economic Journal, 68(3), 632–645. https://doi.org/10.1002/j.2325-8012.2002.tb00442.x

- He, Z., Kelly, B., & Manela, A. (2017). Intermediary asset pricing: New evidence from many asset classes. Journal of Financial Economics, 126(1), 1–35. https://doi.org/10.1016/j.jfineco.2017.08.002

- Holmes, M., Otero, J., & Panagiotidis, T. (2011). Investigating regional house price convergence in the United States: Evidence from a pair-wise approach. Economic Modeling, 28(6), 2369–2376. https://doi.org/10.1016/j.econmod.2011.06.015

- Holmes, M., Otero, J., & Panagiotidis, T. (2017). A pair-wise analysis of intra-city price convergence within the Paris housing market. The Journal of Real Estate Finance and Economics, 54(1), 1–16. https://doi.org/10.1007/s11146-015-9542-z

- Holmes, M., Otero, J., & Panagiotidis, T. (2018). Climbing the property ladder: An analysis of market integration in London property prices. Urban Studies, 55(12), 2660–2681. https://doi.org/10.1177/0042098017692303

- Ibbotson, R. G., & Kaplan, P. D. (2000, January/February). Does asset allocation policy explain 40%, 90% or 100% of performance? Financial Analyst Journal, 56(1), 26–33. https://doi.org/10.2469/faj.v56.n1.2327

- Iqbal, J. (2017). Does gold hedge stock market, inflation, and exchange rate risk? An econometric investigation. International Review of Economics and Finance, 48(C), 1–17. https://doi.org/10.1016/j.iref.2016.11.005

- Jacobs, H., Muller, S., & Weber, M. (2014). How should individual investors diversify? An empirical evaluation of alternative asset allocation policies. Journal of Financial Markets, 19(C), 62–85. https://doi.org/10.1016/j.finmar.2013.07.004

- Kaplan, P. D. (2015). Fixed income, real estate and alternatives. Chapter II. In P. D. Kaplan (Ed.), Frontier of modern asset allocation (pp. 131). Morningstar Inc.

- Low, R. K. W., Faff, Y. Y. R., & Faff, R. (2016). Diamond vs. precious metals: What shines brightest in your investment portfolio? International Review of Financial Analysis, 43(C), 1–14. https://doi.org/10.1016/j.irfa.2015.11.002

- Manganelli, B. (2015). Real estate investing, market analysis, valuation techniques, and risk management. Springer International Publishing.

- Markowitz, H. (1952). Portfolio selection. The Journal of Finance, 7(1), 77–91. https://doi.org/10.2307/2975974

- Markowitz, H. M. (1991). Foundations of portfolio theory. The Journal of Finance, 46(2), 469–477. https://doi.org/10.1111/j.1540-6261.1991.tb02669.x

- Mercer. (2014). Building a real asset portfolio. Marsh and McLennan Companies.

- Murtaza, H., Abrar, M., & Ali, R. (2015). Impact of major political events on stock market returns of Pakistan. Public Policy and Administrative Research, 5(4), 69–83. ttps://www.researchgate.net/publication/304096843_Impact_of_Major_Political_Events_on_Stock_Market_Returns_of_Pakistan

- Nazir, M. S., Anwar, Z., Kaleem, A., & Anwar, Z. (2014). Impact of political events on stock market returns: Empirical evidence from Pakistan. Journal of Economic and Administrative Sciences, 30(1), 60–78. https://doi.org/10.1108/JEAS-03-2013-0011

- Oztek, M. F., & Ocal, N. (2017). Financial crises and the nature of correlation between commodity and stock markets. International Review of Economics and Finance, 48(March), 58–68. https://doi.org/10.1016/j.iref.2016.11.008

- Panagiotidis, T., & Printzis, P. (2016). On the macroeconomic determinants of the housing market in Greece: A VECM approach. International Economics and Economic Policy, 13(3), 387–409. https://doi.org/10.1007/s10368-016-0345-3

- Pellatt, P. G. K. (1972). The analysis of real estate investments under uncertainty. The Journal of Finance, 27(2), 459–471. https://doi.org/10.2307/2978488

- Phillips, M., Roberts, J., & Watson, S. (2017). Emerging trends in real estate: New market realities. PWC: Urban Land Institute. https://www.pwc.com/gx/en/asset-management/emerging-trends-real-estate/europe/emerging-trends-in-real-estate-(2017).pdf

- Rasheed, H., & Tahir, M. (2012). FDI and terrorism: Co-integration & granger causality. International Affairs and Global Strategy, 4, 1–5. https://www.iiste.org/Journals/index.php/IAGS/article/view/1453

- Rasheed, H., Ahmad, H., & Javid, A. Y. (2021a). Is gold a hedge and safe haven during political uncertainties? Business & Economic Review, 13(2), 1–28. https://doi.org/10.22547/BER/13.2.1

- Rasheed, H., Ahmad, H., & Javid, A. Y. (2021b). Gold vs.Psx sectors during political uncertainties: An event study analysis. Business Review, 16(2), 1–20. https://doi.org/10.54784/1990-6587.1382

- Sarwar, S., Hussain, W., & Malhi, S. N. (2013). Empirical relation among fundamentals, uncertainty and investor sentiments: Evidence of Karachi stock exchange. International Review of Management and Business Research, 2(3), 674–681. https://www.researchgate.net/publication/309417650_Empirical_Relation_Among_Fundamentals_Uncertainty_and_Investor_Sentiments_Evidence_of_Karachi_Stock_Exchange

- Seiler, M. J., Seiler, V. L., Traub, S., & Harrison, D. M. (2008). Regret aversion and false reference points in residential real estate. Journal of Real Estate Research, 30(4), 461–474. https://doi.org/10.1080/10835547.2008.12091229

- Shabbir, A., Kousar, S., & Batool, S. A. (2019). Impact of old and oil prices on the stock market in Pakistan. Journal of Economics, Finance and Administrative Science, 25(50), 279–294. https://doi.org/10.1108/JEFAS-04-2019-0053

- Sharpe, W. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance, 19(3), 425–442. https://doi.org/10.1111/j.1540-6261.1964.tb02865.x

- Shrestha, M. B., & Bhatta, G. R. (2018). Selecting appropriate methodological framework for time series data analysis. The Journal of Finance and Data Science, 4(2), 71–89. https://doi.org/10.1016/j.jfds.2017.11.001

- Theron, L., Vuuren, G., & McMillan, D. (2018). The maximum diversification investment strategy: A portfolio performance comparison. Cogent Economics and Finance, 6(1), 1–16. https://doi.org/10.1080/23322039.2018.1427533

- Vicente, L. A. B. G., Cerezetti, F. V., Faria, S. R. D., Iwashita, T., & Pereira, O. R. (2015). Managing risk in multi-asset class, multi market central counterparties: The core approach. Journal of Banking and Finance, 51(C), 119–130. https://doi.org/10.1016/j.jbankfin.2014.08.016

- Wu, H., Ma, C., & Yue, S. (2017). Momentum in strategic asset allocation. International Review of Economics and Finance, 47(c), 115–127.