Abstract

M&A prediction is a growing interest in the field of business studies. However, prevailing M&A prediction techniques are still widely based from the analyses of financial variables through quantitative approaches. This has led M&A scholars’ attention to call for the contribution of non-financial studies coupled with the opportunity for qualitative approaches to supplement new methodological insights. Accordingly, this study delved to explore the potential of qualitative data to describe M&A target firms and develop an M&A completion prediction model that is based on categorical patterns found among American and European owned firms’ letters to shareholders ranked in fortune/global/fast 500. This study postulates that analyzing M&A targets’ letters to shareholders could provide relevant categories to describe the attractiveness of firms as M&A targets that are also indicative to the prediction of the completion of the offered deals. This study employed a mixed methodology using content analysis and decision tree analysis. The results of the study had led to provide four interesting category observations that described M&A target firms’ letters to shareholders, which showed less sensitivity to ownership and border-related offers. Further, the study developed an M&A completion prediction model with 67% predictive accuracy. This study provides implications for firms’ management on the posturing contents featured in firm’s letters to shareholders could expose to signal their firms as M&A targets and to readers as such as stock traders and corporate investors to look into the posturing contents of firms’ letters to shareholders, so as to identify potential M&A targets.

1. Introduction

Predicting merger and acquisition (M&A) has been subject to increased interest and has received considerable attention from academic scholars of various management disciplines in pursuit to identify factors that describe firms as targets of M&A. Knowledge known at present generally points to the financial variables relative to firms’ managerial efficiency, financial leverage, liquidity, growth, capital expenditure, stock trading volume, valuation, payout, and firm size (Brar et al., Citation2009; Dietrich & Sorensen, Citation1984; Erdogan, Citation2012; Kim & Arbel, Citation1998; Polemis & Gounopoulos, Citation2012; Zanakis & Zopounidis, Citation1997) as bases for M&A target firms determination.

Several studies already demonstrated that share prices of firms involved in an M&A announcement substantially increase at a certain period, where most of these gains were enjoyed by the shareholders of the target firms (Asquith & Kim, Citation1982; Campa & Hernando, Citation2004; Dodd & Ruback, Citation1977; Goergen & Renneboog, Citation2004). These findings have increased the significance on the ability to generate information to locate M&A deals at an earlier stage. The information could provide abnormal returns for investors by trading in advance on potential target firms stocks prior to an M&A announcement.

Further, this study also found interest upon learning that M&A attempts based on empirical evidences suggest that 25% of the undertaking fails to precede deal completion (Holl & Kyriaziz, Citation1996) and only 68.7% of the announced cross-border M&A deals have reached consummation (Zhang et al., Citation2011). This is despite the costly associated losses brought by various fees related to the lock-up provisions of the undone deal that can go as high or over 6% of the transaction value (Rosenkranz & Weitzel, Citation2005), termination fees ranging from 5% to 35% that varies on industries and context (Doan et al., Citation2018; Rosenkranz & Weitzel, Citation2005), operational cost to facilitate the M&A processes, and the value at stake for acquiring firms disclosures of trade secret information regarding post-M&A synergy plans to the target’s resources (Officer, Citation2003). All these odds made M&A completion relatively valuable for acquiring firms (Dikova et al., Citation2010). Hence, their potential interest on the inclination of an eyed target firm to precede or forgo with an M&A offer.

The effort of the academic community on this matter is visible on international M&A deals, centered on empirical studies identifying outcome determinants of M&A offers that have led to suggest certain factors, such as target management resistance to acquisition bids, target company size, deal structure, managerial ownership, toehold shareholding levels of bidder companies, termination fees, the level of bid premiums offered in takeovers, presence of competing bidder, and ownership structure, were investigated in the intention of determining the likelihood result of an M&A offer (Zhang et al., Citation2011).

Similarly, predicting M&A targets and M&A completion both shared the centrality in the use of financial or quantitative data. It has been recommended that the inclusion of nonfinancial variables on prediction models could improve accuracy and could potentially explain incidence where financial-based prediction models have failed to provide reliable insights (Pasiouras & Tanna, Citation2010; Polemis & Gounopoulos, Citation2012). This had laden the opportunity for this study to depart from popular methodology and to offer an exploratory approach that utilizes qualitative data sets extracted from the target firms’ letters to shareholders to both serve the study’s intention in describing M&A target firms considering sensitivity for ownership (Bettinazzi et al., Citation2020) and border offers (Ahammad & Glaister, Citation2008), and in the development of an M&A completion prediction model.

Driven from the idea that letters to shareholders contains information that could reflect firms’ conditions and the record that analyzing letters to shareholders have already made remarkable contributions in the aspect of assessing firms’ performance (Smith & Taffler, Citation2000), corporate reputation (Geppert & Lawrence, Citation2008), corporate auditing (Clatworthy & Jones, Citation2006), investors’ perception (Baird & Zelin, Citation2000; Hodge, Citation2001), and assessment of firms’ current and future condition (Abrahamson & Amir, Citation1996), hence the possibility that analyzing letters to shareholders of firms that received an M&A offer, could provide information to the descriptive condition of the firms to explicate its attractiveness as M&A targets. This study could also be the first to have explored the potential of analyzing letters to shareholders in describing M&A target firms and in predicting the completion of an M&A offer.

The suggestion made by Hyland (Citation1998) regarding areas of opportunities in investigating letters to shareholders in other genres and business domains by identifying relative concept frequencies of its content to identify distinguishing features found within specific contexts, has led the study to employ mixed methods using content analysis and decision tree. This study analyzed the categories found within the letters to shareholders to describe firms as likely targets and modeled the completion outcome of the offer.

Ensuring the study’s conformance to qualitative research trustworthiness, a rigorous coding process observing Lincoln and Guba (Citation1986) coding consistency checks procedure was adopted, with the assistance of second coders who are scholars in the field of business and language. An M&A dictionary was then built to analyze the categories of the 135 target firms’ letters to shareholders.

The results of the study led to the identification of 8 major categories that was used to describe the portrait of the target firms’ letters to shareholders, which showed less sensitivity to ownership (American/European owned) and border-related offers. The results found connection to underpinning M&A prediction notions and correlation studies in explicating the target firms’ attractiveness for M&A offers.

Further, this study provides implications for firms’ management, that the posturing contents featured in firm’s letters to shareholders could signal their firms as M&A targets. This study also provides implication to the firms’ practice of publishing these letters as an avenue to signal the firm’s consideration to engage for a possible M&A offer by posturing the letters to shareholders contents on the vested categories of interest of M&A acquirers. Moreover, this study extends its implication to readers such as stock traders and corporate investors to look into the posturing contents of firms’ letters to shareholders to identify potential M&A targets.

Last, this study highlights its contribution to fill the observation by Pasiouras and Tanna (Citation2010), Polemis and Gounopoulos (Citation2012), and Zanakis and Zopounidis (Citation1997) with regards to the importance of nonfinancial variables for any future studies to improve financial-based M&A targets predictive models. This study offers to fill the methodological gap by presenting a method and a predictive model with the potential to work alongside financial-based M&A target prediction models, and bridges to incorporate both considerations on future M&A target prediction studies.

2. Literature review

2.1. Understanding M&A prediction and its value

Predicting M&A studies were largely anchored on six notions popularized by Palepu (Citation1986) as follows; (1) the inefficient management hypothesis; was based from finance theory that indicate M&A as a mechanism that facilitates managerial change in a firm govern by managers that have failed to maximize the firm’s market value, making the firm a likable target for an M&A offer. (2) The growth-resource mismatch hypothesis; was taken from finance literature that analyzed the financing and investment decisions of firms under asymmetric information, which specified two types of firms as likable targets of M&A: the high growth, low resource firms and the low growth, high resource firms. (3) The industry disturbance hypothesis; was based from economic disturbance theory which states that M&A were caused by market valuation differentials on firms as an effect caused by economic shocks such as regulations, technology and industry structure. Firms experiencing economic disturbances were viewed as likable targets for M&A offers. (4) The size hypothesis; was based on the associated costs for acquiring a firm, these costs were observed to likely increase along with the target’s firm size, which likely decreases the number of potential acquirers, suggesting that M&A likelihood decreases with firm size. (5) The market to book hypothesis; assumes firms with lower market value over its book value as likely targets of M&A, for it being considered as an economical acquisition opportunity. (6) The price-earnings hypothesis: states that high P/E acquirers search for low P/E firms as target for M&A in the acquirers’ intention to enjoy instantaneous capital gain, expressing low P/E ratio firms as likely target for M&A offers.

The adoptions of these six M&A predictions notions were popular among empirical studies, building around this paradigm to create and test prediction models (Ambrose & Megginson, Citation1992; Barnes, Citation1999; Cudd & Duggal, Citation2000; Meador et al., Citation1996; Powell, Citation1997; Walter, Citation1994), Some researchers have also offered some specifications, expanded Palepu (Citation1986), and popularized notions in the likes of Kim and Arbel (Citation1998) with their additions taken from finance literatures as follows: (1) financial leverage hypothesis state that M&A likelihood is reversely related to target’s financial leverage, indicating firms with high unused debt capacity as likely targets of M&A. (2) The liquidity hypothesis indicates that firms’ M&A likelihood increases along with its increase in liquidity. This is based on the premise that overly high liquidity shows firms’ inefficiency to allocate assets that may lead to suboptimal investments that compromises firms’ profitability for safety. These high cash reserves over short-term debt are seen by acquirers as an immediate cash cow that attracts the firm to receive M&A offers. (3) The relative capital expenditure hypothesis was based on the notion that firms with high level of capital expenditure over its total assets reflect firm’s adequacy to allocate its resources and its commitment to pursue growth through actual appropriations for capital investments, indicating firms with high ratio of capital expenditure to total assets as likely targets for M&A, under the assumption that acquirers’ preference favors firms with high growth potentials. (4) The dividend payout hypothesis was based on the notion that high dividend payout compromise future investment opportunities that may affect firms’ future cash flow performances. Further, firms’ payment of high dividends could also be viewed as firms not having adequate investment options, which led to the notion that M&A probability decreases as dividend payout ratio increases, indicating firms possessing high dividend payout ratio as unlikely targets for M&A. (5) The stock market trading volume hypothesis was based on the notion that high stock volume firms relative to its size enjoys lower M&A transaction cost brought by marketability, with size being controlled, firms with high trading volume were hypothesized to be likely targets of M&A. Brar et al. (Citation2009) also expanded Palepu (Citation1986) acquisition likelihood model after noticing that M&A target firms exhibited strong short-term price momentum and its shares were actively trading prior to the M&A deal announcement. Based on these observations, Brar et al. (Citation2009) developed a prediction model that integrates the probability of M&A for firms exhibiting increase in price momentum, increase in trading activities, and positive market sentiment. It is noticeable that predicting M&A literature were largely based on the examination of firms financial characteristics (Ali-Yrkkö et al., Citation2005; Doumpos et al., Citation2004; Erdogan, Citation2012; Pasiouras & Tanna, Citation2010; Polemis & Gounopoulos, Citation2012; Słowiński et al., Citation1997; Zanakis & Zopounidis, Citation1997).

The interest of the academic community on M&A prediction studies could be traced on the value to which the information could provide profitable insights for stock investment decisions. It has been reported that positive abnormal returns were seen to have been enjoyed by the target firms’ shareholders, upon the announcement of its firm’s involvement on an M&A deal (Asquith & Kim, Citation1982; Campa & Hernando, Citation2004; Dodd & Ruback, Citation1977; Goergen & Renneboog, Citation2004; Jensen & Ruback, Citation1983). The target firms share prices were observed to increase by 30% on successful tender offers and 20% upon deal completion (Jensen & Ruback, Citation1983), a 9% increase around the announcement date (Campa & Hernando, Citation2004) and 12.6–30% on hostile takeovers (Goergen & Renneboog, Citation2004). Ouzounis et al. (Citation2009) illustrated that predicting M&A provided better gains for stock trades made farther away from the M&A announcement date on a 12- month time frame.

Several quantitative studies () have already made progress in its investigation of this knowledge by formulating prediction models that could help identify firms that are likely to be given an M&A offer through the examination of the target firms’ financial ratios (Akkus et al., Citation2016; Brar et al., Citation2009; De Jong and Fliers (Citation2020); (Doumpos et al., Citation2004; Erdogan, Citation2012; Kim & Arbel, Citation1998; Meador et al., Citation1996); Meghouar and Ibrahimi (Citation2020); (Ouzounis et al., Citation2009; Polemis & Gounopoulos, Citation2012; Słowiński et al., Citation1997; Zanakis & Zopounidis, Citation1997). In spite of the contributions made by various studies in predicting M&A, there still exist a fair amount of misclassifications in the prediction models (Pasiouras & Tanna, Citation2010) along with the continuous call made by various researchers for the importance of incorporating nonfinancial variables for the improvement of the prediction models accuracy (Barnes, Citation1990; BELKAOUI, Citation1978; Pasiouras & Tanna, Citation2010; Polemis & Gounopoulos, Citation2012; Stevens, Citation1973; Zanakis & Zopounidis, Citation1997). Accompanying these cited studies were recommendations to explore nonfinancial data in describing firms that are likely to become targets of M&A. It is suggested that a qualitative research design be done and provide an alternative technique to identify target firms, which could possibly work along with existing prediction models and supplement prediction accuracy. This has laden the opportunity to purposely design this study to explore and address these identified gaps.

Table 1. Summary of methods and measures in predicting M&A targets

2.2. The value of M&A completion

Mergers and acquisitions (M&A) were observed to demand firms an immense amount of preparations that the entire processes of completing an M&A deal could pose a great challenge to the involved firms (Dikova et al., Citation2006). An examination of Holl and Kyriaziz (Citation1996) revealed that 25% of M&A undertakings failed to precede completion and only 68.7% of the announced cross-border M&A attempts were reported to have reached consummation (Zhang et al., Citation2011).

The effort of the academic community to investigate on this matter is visible on international M&A deals, centered on empirical studies identifying outcome determinants of M&A offers that have led to suggest certain factors such as target management resistance to acquisition bids, target company size, deal structure, managerial ownership, toehold shareholding levels of bidder companies, termination fees, the level of bid premiums offered in takeovers, presence of competing bidder, and ownership structure (Zhang et al., Citation2011). The findings relating to these studies were mostly drawn from quantitative studies under the discipline of finance, management, and corporate governance.

The value of M&A completion could be appreciated by viewing the associated cost of M&A deal forfeiture. It has been reported that lock-up provisions of undone deals can go as high or over 6% of the transaction value (Rosenkranz & Weitzel, Citation2005) while the termination rates ranges from 5% to 35% that varies on industry and context (Doan et al., Citation2018; Rosenkranz & Weitzel, Citation2005). Plus, the considerable operational cost in facilitating the M&A processes and importantly, the value at stake for disclosing trade secrets information regarding post-M&A synergy plans of the target’s resources (Officer, Citation2003). Reaching this point in the M&A transaction makes M&A completion relatively valuable for the acquiring firms (Dikova et al., Citation2010). Making it reasonable for firms facing to such considerable losses to be interested to the inclination of an eyed target firm to precede or forgo with an M&A offer. This information had led to the consideration of this study to explore the development of an M&A completion prediction model that would provide insight to the odds that an M&A offer will reach completion.

2.3. The value of letters to shareholders

The value of using letters to shareholders in this study could be attributed to the notion pointed out by Abrahamson and Amir (Citation1996) regarding the relevance of soft information as equally important to the information provided by financial statements. Hyland (Citation1998) also recommended letters to shareholders to be analyzed in other genres and business domains by determining relative concept frequencies of its content, to identify distinguishing features found within specific contexts. This section highlights letters to shareholders utility on various studies and its potential to characterize firms as targets of M&A.

Analyzing the content of letters to shareholders provides information to the assessment of the quality of firms’ earning numbers, which was found to be consistent with the firms reported financial statements (Abrahamson & Amir, Citation1996). Letters to shareholders were also used to evaluate firms’ future financial condition (Smith & Taffler, Citation2000), based on the letters content could classify ailing firms from those financially healthy (Poole, Citation2016; Smith & Taffler, Citation2000), at a very high degree of accuracy comparable to the meticulously developed financial ratio-based z-score models (e.g.,Altman et al., Citation1977; Taffler, Citation1983). Further, letters to shareholders were contributory to the determination of firms’ reputation (Geppert & Lawrence, Citation2008), future direction (Amernic et al., Citation2010), CEO personal traits (Brennan & Conroy, Citation2013), and performances (Olsen et al., Citation2013).

Letters to shareholders were also investigated to determine the reliability of its content under tough macroeconomic condition given that it influences investors’ and other readers’ perception on their assessment of the firms’ current condition (Baird & Zelin, Citation2000). The results revealed that firms’ incentives to distort public information during this time were strategically low (Patelli & Pedrini, Citation2014) that indicated its trustworthiness to reflect firm’s reality.

Several studies have already extended the use of letters to shareholders on various business domains () but none to the best knowledge of the researchers that it had been used to characterize M&A targets. Congruently, this study found that opportunity to explore the possibility that by analyzing M&A targets’ letters to shareholders content could reveal essential categories to describe the attractiveness of firms as targets and predict the completion of the offer.

Table 2. Summary of methods and measures for letter to shareholders studies

3. Methodology

3.1. The empirical setting and research approach

Letters to shareholders are published letters written by firms’ top officials and are included at the first part of the firm’s annual report or at the investor relations section of a firm’s website. These letters were intended to provide an overview report of firms’ operational whereabouts. The content of the letters basically provides information of the firm’s financial results, market position, future plans, and important events.

3.2. The data

This study observed a 5-year longitudinal investigation of M&A target firms’ letters to shareholders, taking in the year of M&A announcement and 4 years back, from large western firms (American/European owned) of technology, pharmaceuticals/chemicals, finance, energy, and consumer goods industries from the year 2005 to 2019 ( –5), whose stocks are publicly traded with market capitalization not less than a billion of dollars. The decision to favor large firms from the west for observation and analysis was deeply influenced by the practice of these firms to publish letters to shareholders on annual basis and of the availability and completeness of these letters for collection. The study was confronted with the difficulty of data collection brought by target firms webpage annual report record capacity and the unavoidable fact that completed mergers deceased the target pervious identity and most of its webpages are no longer made available. For these reasons the researchers have availed the services by other webpages that offers a historical keeping of annual reports of those target firms. But has still remained to be a bottleneck for the researchers especially for those M&A announcements made in the year 2010 and earlier.

By analyzing the M&A targets’ letters to shareholders at this length would reveal distinctive categories reflecting target firms’ past operational actuality, believed to be of importance to describe and explicate the firms attractiveness to M&A offers and to the prediction of the completion of the said deal.

This study analyzed 135 letters to shareholders published in the year 2001 to 2020, belonging to 27 M&A target firms of 5 various industries and geography with 30% cross-border M&A offer observation and 70% within border. This warrants that the study’s data were taken from various representations and encompass varying economic conditions providing the study’s empirical investigation with meritable observation of the content of M&A target firms’ letters to shareholders.

3.3. The research approach overview and considerations

A mixed method was employed in this study utilizing qualitative content analysis (Hsieh & Shannon, Citation2005) to build the study’s M&A dictionary through inductive coding, categorization, and identification of linguistic markers. A semi-automated quantitative content analysis was then performed for the quantification of the category frequency—these shall serve as data sets for the development of the M&A completion prediction model.

In this study, the prediction of completion and non-completion of M&A offers were performed via decision tree (recursive partitioning), a nonparametric technique for classification and prediction that is based on pattern recognition through machine learning algorithm that can automatically search for important relations and detect hidden structures in highly complex business data as stated in Espahbodi and Esphabodi (Citation2003). Tsagkanos et al. (Citation2007) enumerated some of the advantages of using decision trees as follows; (1) the technique doesn’t require assumption for statistical distributions of variables; (2) avoids transformations of variables; (3) similar variable can be utilized for more than one part of the tree which enables detection of interaction effects in certain variables. The considerations for its use were that, first, majority of the previous M&A prediction studies have adopted logit regression or multiple discriminant analysis (Tsagkanos et al., Citation2007). Second, the use of logit regression has been seen to become unrobust over time in predicting M&A (Powell, Citation1997) and last, both discriminant and logit regression were seen to be outperformed by the contemporary technique decision tree models through the use of machine learning algorithm (Espahbodi & Esphabodi, Citation2003). With these in consideration and in the hope that the study could provide a model essential to the prediction of forthcoming M&A deals completion and non-completion, this study was convinced for its adoption.

3.4. The data collection criteria and research process

Similar to most qualitative studies, this study employed a purposive sampling procedure which considered the following criteria for the inclusion of firms’ letters to shareholders in the study’s sample: (1) the M&A offer made to the target firms are verifiable through new articles; (2) the M&A offer was made within the year of 2005–2019; (3) the published letters to shareholders of the target firms during the year of M&A announcement and four years prior are complete and are available in the web for extraction.

3.5. The inductive coding and categorization

A pilot group of letters to shareholders was established and subjected for inductive coding (Glaser, Citation1978) as part of the processes needed for the creation of the study’s M&A dictionary. The pilot group consist 10 letters to shareholders that were taken equally from all industries, at varying years of publication. This is to provide sensitivity in coding concepts, specific to a particular industry or at a particular time.

The coding process was contextualized under the lens of M&A to explicate target firms’ attractiveness for M&A offers. A total of 605 coded quotations were produced in the process, which was a little bit more than the suggested 100–500 concepts deemed enough to code knowledge for a specific topic (Carley, Citation1993). Category saturation (Saunders et al., Citation2018) was declared on the tenth letter to shareholders after the observation that the last three letters to shareholders that were inductively coded have only contributed 1 category and the initial categories identified have already reached twenty-one, with these many categories identified in the pilot group. It is necessary to reduce these categories to at most 8 major categories by either merging related categories or removing categories deemed to be of less importance (Thomas, Citation2006).

A condition was then imposed that categories which were identified to be present only in a single letter to shareholders, were automatically removed as it fails to provide similarity and would be unlikely to provide relevant insight for pattern analysis. Based on this condition, 3 categories were then removed from the initial list of categories.

A review of all remaining categories and its codes was then conducted, aimed to further reduce the remaining categories. This review had provided the opportunity to remove 2 more categories after being noticed that only 2 codes were found within the category and no other relative category was found feasible for its merging. The other category was removed based on the heterogeneity of its codes, being it the category that holds the uncategorized codes. Subsequently, 8 categories were then merged to other related and broader categories that led the study to identify its major categories ().

Table 3. The identified major categories

Table 4. Distribution of sample according to industry

3.6. Conformance to qualitative research trustworthiness

The identified major categories along with its codes and quotations were then subjected to adhere to Lincoln and Guba (Citation1986) qualitative research trustworthiness by following Thomas (Citation2006) coding consistency checks procedure: (1) the independent parallel coding and (2) check on the clarity of categories. In the independent parallel coding the output of the initial coder which performed the inductive coding that led to the development of the 8 major categories were subjected for peer review for the appropriateness of the labels on the coded quotations and the relativeness of the assigned codes to its category.

A certified public accountant with 13 years’ experience in banking and 6 years as state auditor served as the second coder for this study. No orientation or coder training was given to the second coder in order to avoid any information that may cloud the coding consistency check assessment. The second coder was given the evaluation objective, along with some of the raw text from which the identified major categories were developed. The second coder was tasked to develop her own set of categories out of the given 128 quotations without any information about the categories developed by the initial coder.

The second coder was able to successfully develop 8 major categories with 6 categories identically labeled to that of the initial coder’s identified major categories. The other 2 categories were labeled slightly different from the initial coder, as the second coder labeled these categories with some specificity deemed to be in the subcategory of the initial coder’s category. The supposed growth and research categories were labeled by the second coder respectively as profitability and innovation categories. To reconcile this slight difference, the initial coder requested a review on some pointed quotations in these categories that led the second coder to realize and identify the correct labeling of these categories matching the initial coder’s category.

A check on the clarity of categories was then subsequently carried out, where the second coder was given the evaluation objective, and the categories developed by the initial coder with its descriptions. The second coder was then given a new set of quotations (114 quotations) where the identified major categories were developed. The second coder was then tasked to assign these quotations and codes to the developed major categories. A check was then performed and the second coder had similarly assigned the quotations and codes to the major categories of that to the work done by the first coder.

3.7. The dictionary building process

A total of 135 letters to shareholders of firms that were targets of M&A were gathered and prepared for analysis. This voluminous body of text compels the study to create an efficient way to process these letters and that is through the creation of an M&A dictionary to facilitate a semi-automated content analysis. In this part of the study, it generally followed the semiautomatic dictionary building process (S-DBP) introduced by Deng et al. (Citation2017).

The creation of the M&A dictionary required the identification and extraction of linguistic markers found within the quotations of the major categories that was carried out in the inductive coding phase. The initial identification of the linguistic markers was carried out by the first coder. These initially identified linguistic markers were then subjected for review and verification of the second coder, specially, that some of the quotations required specialization for accurate understanding of the concepts and of the identification and usage of the linguistic markers in the quotations. The review was followed by a discussion between the researcher and the second coder pertaining to suggested inclusion and removal of some linguistic markers that resulted to the creation of the initial dictionary, composed of 365 linguistic markers (words).

A dictionary expansion work was then subsequently carried out by the researcher to increase the span of capture of the linguistic markers by adding some morphology of the linguistic markers. Two language studies scholars were then asked to review the identified linguistic markers, the quotations where they were extracted and the morphologies that were added, which resulted to the creation of the final dictionary of 716 linguistic markers. At this point, the M&A dictionary was completed and was embedded in the content analysis software.

The 135 letters to shareholders were then individually extracted from the firms’ annual reports and were transferred to word office software for spelling checks; it was at this point that the researchers have noticed that letters to shareholders were written in American English and others in British English. Because of this, variations in word spelling needed to be addressed.

The researchers decided to adopt the American English on two reasons (1) the M&A dictionary was taken from American English written letters to shareholders; (2) the word office software was running an American English based spelling checker and auto correction feature. The words detected as misspelled for this reason were then corrected in favor of the American English spelling. It was also noticed that the use and non-use of hyphens posed a problem since the content analysis software is précised on spellings and this might impact the results. This prompted the researcher to update the M&A dictionary for linguistic markers that were written with hyphens and without. It also came to a surprise that letters to shareholders in spite being well prepared would still have its own share of spelling errors mostly brought by non-spacing. The researcher was considering that these could have been influenced in the transfer of the text in one file format into another, making this pre-process screening vital in running any semi-automated content analysis.

After all letters to shareholders passed the pre-processing it was then saved under .txt format, which were then individually embedded in the content analysis software. The 135 letters to shareholders were then processed individually, where the content analysis software generated the results in terms of concept counts (linguistic marker counts) for every major category. With due consideration to the heterogeneity of the letters to shareholders length and the possibility of any biases it may lead, it was then decided that the count results should be in percentages.

3.8. The M&A prediction model development process

The development of the model to predict the likelihood of M&A completion and non-completion was then carried and facilitated through machine learning. A spreadsheet was prepared which classified firms with M&A completion as 1 and non-completion as 0. The data file contained the results of the major categories percentages provided from the conduct of this study’s content analysis of the target firms’ letters to shareholders, which presented a total of 40 factorials of the major categories with each category indicating 5 years of observation that includes the year of M&A announcement and 4 years prior. Each observation was then classified and designated to a terminal node where it belongs after analyzing the specified yes/no questions on the percentage values of the major categories serving as independent variables in this study with data partition of 80% as training set and 20% for the test set. This study was then able to develop two decision tree models with the same prediction accuracy with one having 3 features with a max depth = 3 and the other with 6 features with a max depth = 5. This study adheres to Occam’s razor principle in the selection between the two generated models which let the study embraced the former. The study’s entire research process is shown in .

Figure 1. The research process diagram.

4. Results & discussions

4.1. Descriptive results

The study’s approach led to provide a descriptive portrait of target firms’ letters to shareholders through the utilization of key concepts and of the 8 identified major categories: (1) challenges; (2) growth; (3) investment; (4) mergers and acquisitions (M&A); (5) performance; (6) research and development (R&D); (7) strategy; and (8) sustainability that explicate target firms’ attractiveness on M&A offers. Based on the descriptive evidences of these categories, 4 out of the 8 categories showed observable patterns: (1) the mean scores revealed that target firms’ letters to shareholders were largely and consistently featuring growth concepts of around 45% of the entire identified major categories across all years of observation. (2) The R&D category mean scores revealed an upward trend towards the year of M&A announcement. (3) Mean scores of the investment category revealed a declining trend approaching the year of M&A announcement. (4) The maximum values of the challenges category revealed a declining trend as it approaches the year of M&A announcement.

Further analysis was also carried out to investigate the sensitivity of the observed patterns to ownership (American/European owned) and border-related offers. Results revealed that the descriptive portrait provided earlier in this study is less sensitive to ownership and border-related offers, as the results provided close similarity in the provided descriptive portrait. This goes to show the strength of the presented method to describe potential M&A targets that is less sensitive to the influence by such factors.

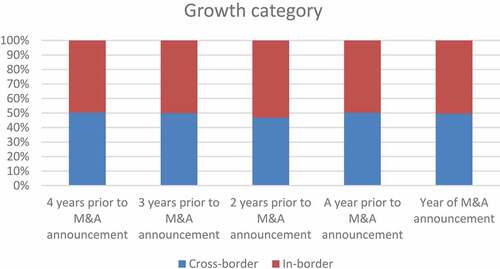

4.1.1. The growth category

The growth category features various progressive concepts of the target firms’ holistic organic growth condition and potentials; it being the dominant category goes to describe that these M&A target firms were largely experiencing momentum of advancement in various areas.

This also described how attractive these firms were as M&A targets, which may have exposed these firms to growth-seeking acquirers. Under the lens of M&A targets, the firms through its letters to shareholders pose to be an enticing prospect for inorganic growth-seeking acquirers. These are acquirers who seeks growth through M&A deals (Baghai et al., Citation2007) and take advantage of targets’ growth potentials as a viable strategic move, since M&A drives 35% of large firms growth performance which is vital in outperforming other firms in terms of its pace in increasing revenues (Baghai et al., Citation2007), employee growth, sales growth, financial performance, and market performance (Rodney et al., Citation2009). It appears that growth via M&A is a strategic hopping option for growth-seeking acquirers particularly on firms facing substantial growth barriers, and these firms as described in its letters to shareholders turns out to be fit for this intention.

Growth as a variable has always been a consideration for M&A likelihood models which showed to be a significant predictor for M&A targets (Brar et al., Citation2009; Kim & Arbel, Citation1998; Meador et al., Citation1996; Palepu, Citation1986). Under the premise of growth imbalance that states the two types of M&A likely targets: the low-growth, high-resource firms and the high-growth, low-resource firms. The notion is that low-growth, high-resource firms are natural acquisition targets as frequently indicated in finance textbooks (Palepu, Citation1986). Whereas for high-growth, low-resource firms could be attractive targets as seen in finance literature that analyzes the investing decisions of firms under asymmetric information (Myers & Majluf, Citation1984).

High-growth companies with low-resources are logically attractive for acquiring firms with the contrary low-growth high resources position, this may be the case where acquirers see that the target firm’s growth opportunities can be more profitably finance at the acquirers’ lower cost of capital or that the target has insufficient financial support. On the other hand, low-growth high-resource firm could also be attractive for M&A offers coming from firms having high-growth low-resource position, as both firms may enjoy the advantages of the excess resources of one firm that is better invested to finance the other firms’ projects. It is expected that through M&A both firms with opposing growth-resource imbalances when combined would have a larger value over two firms in separation (Powell, Citation1997).

Growth also plays a vital consideration for diversification, a known motive of acquirers which seeks flexibility and risk reduction over global and domestic shocks. By targeting firms who exhibits higher growth potentials to absorb some of the foreseen affected portfolios in the event (DePamphilis, Citation2019).

In fact, growth was instrumental to the third M&A wave in the conglomerate era wherein firms with high price to earnings ratios was able to increase its earnings per share through M&A by capitalizing on its advantage over firms with lower P/E but with high growth for earnings (DePamphilis, Citation2019). Klasa and Stegemoller (Citation2007) in their study of time-varying investment opportunities posit that M&A sequences were corporate attempts at inorganic growth that have a definitive start and end, emphasizing that these sequences occur during periods of considerable economic growth in the industry. These goes to suggest that growth is an important factor that could describe an M&A target. This study revealed that letters to shareholders of firms offered with M&A deals features growth concepts at an average of 45% on all major categories of the target firms’ letters to shareholders. Suggesting that firms’ growth attracts acquirers in offering M&A deals.

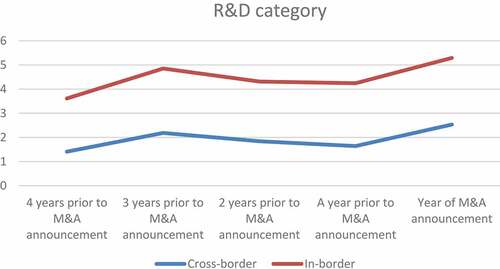

4.1.2. R&D category

R&D facilitate advancement of firms’ valuable technology resources (Grabowski & Vernon, Citation1990) built through firms’ sustained capitalization (Winter, Citation2003). The ownership of these R&D resources often increases its firm’s attractiveness as potential M&A target (Heeley et al., Citation2006; Ranft & Lord, Citation2000), which was observed to have exposed these firms from the acquirers brought by its patenting activities (Ali-Yrkkö et al., Citation2005). It is also believed that firms’ recent history of R&D expenditures plays a key factor for M&A prediction (Heeley et al., Citation2006) of which the R&D and M&A activities were initially seen to be positively related (Jensen, Citation2005), later, R&D alone became a modest predictor of acquisition likelihood (Heeley et al., Citation2006) relatively technological indicators are further explored to serve as predictors of M&A targets citing the work done by (Yang et al., Citation2014) which proposed that M&A prediction modeled from technology related variables could provide better prediction effectiveness than those offered through financial variables.

The firm’s need for innovativeness often drives M&A offers on technology-based targets to take advantage of targets’ innovation-enabling technological resources (Hitt et al., Citation2001; King et al., Citation2003), especially when the acquiring firms undergoes R&D maturity blocks, and would like to get pass from it through M&A with firms showing promising R&D advancements.

M&A and R&D ventures may substitute for one another as drivers of innovation (Blonigen & Taylor, Citation2000) given the conceivable benefits of M&A as a technology-sourcing strategy (Ahuja & Katila, Citation2001) that could provide a new competitive landscape for the involved firms (Bettis & Hitt, Citation1995).

Recalling the M&A wave in the 1990s where firms struggled to keep up with the technological advancement and environmental changes triggered series of M&A activities (Heeley et al., Citation2006) of which 20% of the quantity and 40% of the value involved were technology-based firms (Inkpen et al., Citation2000), which suggested that high-technology-related M&A signifies responses to the need of innovation (Bower, Citation2001; (Ranft & Lord, Citation2002). Particularly that firms seen to be performing beyond industry averages may develop and commercialize disruptive technologies that changes the landscape and may threaten industry players that triggers rivals to target firms that performed significant R&D engagements in attempt to either further advance its technology resources or prevent those deemed disruptive technologies from advancing and commercializing (Heeley et al., Citation2006).

These goes to suggest that firm’s R&D ventures is an important factor that may characterize M&A targets and the upward trend in the R&D category describes to indicate that the activities relating to firms R&D engagement blossomed over the years nearing to the year of M&A announcement, a description seen to be an attractive characteristic of firms being offered with M&A deals, which could have exposed the firms from technology-seeking acquirers. Citing that firms showing sustained upscale in R&D could be the most attractive acquisition targets, under ceteris paribus (Heeley et al., Citation2006). Last, the upscale result of the R&D category describes to coincide with the correlation seen by (Del Monte & Papagni, Citation2003) between research intensity and growth rate, with our study’s results showing R&D category in upward trend and growth as the dominant category. Suggesting that firms research developments attract acquirers in offering M&A deals.

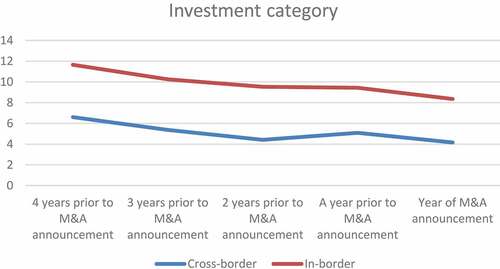

4.1.3. Investment category

It has been viewed in M&A prediction studies that investment seen through firms’ capital expenditures determines the likelihood of a firm being an M&A target. Firms that do exhibit high level of capital expenditures were likely to become targets of M&A (Kim & Arbel, Citation1998).

The continued reduction of the investment concepts in the target firms’ letters to shareholders as it approaches M&A announcement draws several considerations; (1) firms resource constraints that may have limit the firms investments execution (Calomiris & Hubbard, Citation1993), following Kaplan and Zingales (Citation1997), which showed the effect of cash flow on investment for financially least-constrained firms was higher than those financially more constrained firms. On the other hand, the study could not roll out the possibility that the firms were self-sufficient in its resources given that highly creditworthy firms’ investment depends heavily on internal funds (Cleary, Citation1999) and large firms such as in this study are less likely to experience financing obstacles as compared to small firms (Mulier et al., Citation2016) also following (Kallapur & Trombley, Citation1999) which state that capital expenditures to assets is positively correlated with realized growth, ensuing that with growth as the dominant category of this study also mirrors out the supposed picture of capital expenditures that tainted the resource constraint consideration. (2) The lack of investment prospects that meet the firms’ investment criteria may have restricted the firms to pour in its resources on new ventures causing the downward trend in the investment category. The study finds this consideration to be less persuasive given that the growth category was largely visible throughout the observation that could indicate various investment opportunities to pour in firms’ resources. That is why the researchers is inclined to believe on the third consideration, based on the evidence that the reduction of the investment concepts counts nearing the M&A announcement were brought by (3) the firms’ coring strategy that were evident in the quotations. Ensuing that firms have voluntarily reduced its portfolio to emphasize focus on few but more gainful investments, which resulted to lesser necessity of featuring the concepts in the letters to update its shareholders. Suggesting that firms’ portfolio coring investment strategies attract acquirers in offering M&A deals.

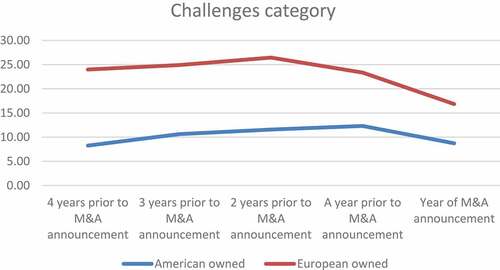

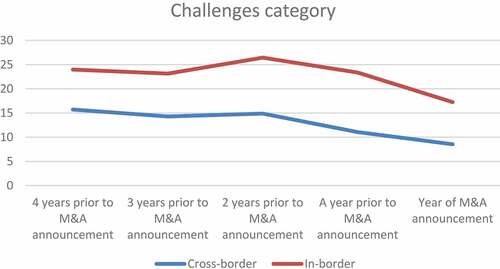

4.1.4. Challenges category

This downward trend in the challenges category is taken by this study as a mirroring image of the capacity of the firms’ management to address business issues. It has been viewed in in the literature, that M&A is a mechanism that facilitate the replacement of management who failed to maximize the shareholders’ wealth (Palepu, Citation1986) given that firms with inefficient managers are likely to suffer from poor performance (Powell, Citation2004) and as a result becomes natural and preferred targets for M&A (Kaul & Wu, Citation2016; Kim & Arbel, Citation1998). It is also good to note that underperforming firms are attractive for M&A offers (Erdogan, Citation2012) and has always been part of the lens in explicating M&A offers (Kim & Arbel, Citation1998; Meador et al., Citation1996) especially that the potential for wealth creation is greater involving inefficient targets (Kohers et al., Citation2000).

The rationale behind the notion of inefficient management as predictor for M&A targets revolves around the idea that acquirers taking over the management of the target firm believe that it could deliver better results than the incumbent (Weston et al., Citation1998); this is known as the relative efficiency hypothesis. Also, inefficiency seen on either or both the target and the acquirer over other firms in the industry prior to the M&A as described in the low efficiency hypothesis (Berger et al., Citation1999) asserts that, the deeper the inefficiency the greater there is for value enhancement opportunities, as provided by M&A that facilitates restructuring improvements of the consolidated firms (Kohers et al., Citation2000). Further, the inefficiency management notion is seen to be relative to the exercise of the disciplinary motive of shareholders on firm’s management who failed to maximize their wealth (Ravenscraft, Citation1987). However, this notion of inefficient management has its fair share of disagreements and sparse of evidence in its favor (Agrawal & Jaffe, Citation2016; Alcalde & Espitia, Citation2003), after being observed that firms’ underperformance generally occurs five to seven years back before the M&A takes place (Agrawal & Jaffe, Citation2016) a time lag too long and evidence too thin that makes the notion of inefficient management inconclusive (Agrawal & Jaffe, Citation2016).

The result portrayed by the challenges category in this study goes to describe quite the opposite of what the popular inefficient management notion inoculates, as the declining portrait of the challenges category goes to described that these target firms management were capable to reduce its business issues and complexities, visible in the decreasing trend of the category serving as a descriptor for inefficient management nearing the M&A announcement year. Suggesting that M&A acquirers are looking into the target firms operational capabilities to resolve business issues.

4.1.5. The descriptive portrait sensitivity to ownership and border-based offers

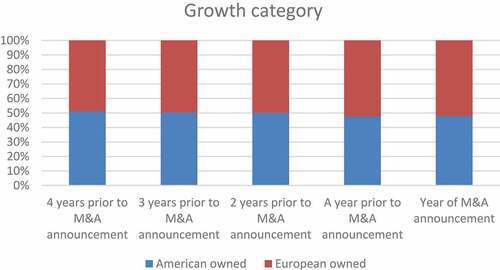

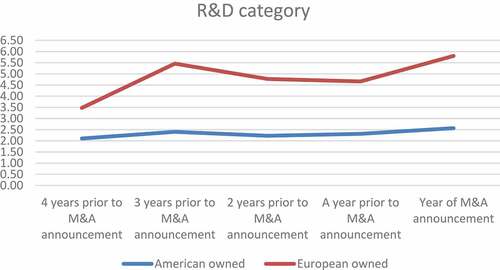

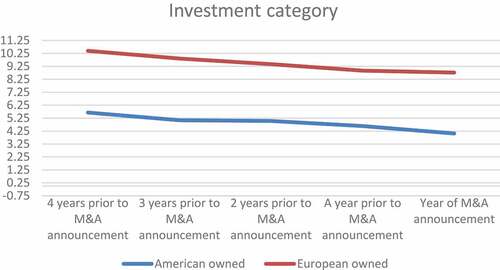

The conduct of the semi-automated content analysis generated the category counts of the identified major categories that allowed the study to describe the target firms’ letters to shareholders, where four interesting descriptions were drawn. In this part, the study expanded these observations as to investigate its sensitivity to ownership (American/European). The results revealed as shown below in that the descriptive portrait provided earlier in this study is less sensitive to ownership, as the figures provided similarity in the provided descriptive portrait. Thus, providing reassuring application of the method over geographical border concern as shown in so long as the M&A target firm letters to shareholders is published with an American or European ownership

Figure 2. The mean score percentage of the growth category in the analyzed letters to shareholders of American and European owned M&A target firms over 5 years observation.

Figure 3. The mean score percentage of the R&D category in the analyzed letters to shareholders of American and European owned M&A target firms over 5 years observation.

Figure 4. The mean score percentage of the investment category in the analyzed letters to shareholders of American and European owned M&A target firms over 5 years.

Figure 5. The maximum values of the challenges category in the analyzed letters to shareholders of American and European owned M&A target firms over 5 years observation.

Figure 6. The mean score percentage of the growth category in the analyzed letters to shareholders of in and cross-border offers to the M&A target firms over 5 years observation.

Figure 7. The mean score percentage of the R&D category in the analyzed letters to shareholders of in and cross-border offers to the M&A target firms over 5 years observation.

Figure 8. The mean score percentage of the investment category in the analyzed letters to shareholders of in and cross-border offers to the M&A target firms over 5 years observation.

Figure 9. The maximum values of the challenges category in the analyzed letters to shareholders of in and cross-border offers to the M&A target firms over 5 years observation.

4.2. The M&A completion prediction model

The M&A completion prediction model developed through supervised machine learning with 67% predictive accuracy.

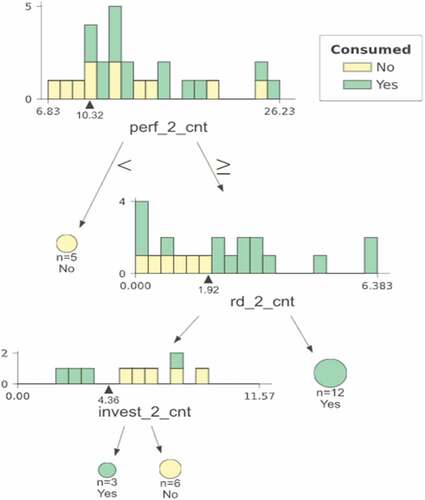

The M&A completion likelihood model (, ) tree resulted to a max depth = 3. The decision tree model has 3 features coming from the categories performance, R&D, and investment of the target firms’ letters to shareholders year 2.

Figure 10. M&A completion prediction model.

Figure 11. Actual distribution of M&A announcements from year 2005–2019.

Starting from the root node of the decision tree, the software has set the criteria value of 10.32. Which classify to predict the target firms’ letters to shareholders with performance category percentage below 10.32 as non-completed, directing all observation meeting the decision criteria to the first-level unconsumed terminal node (NO) while those with percentages greater or equal to 10.32 were directed to a second-level decision node.

The subjected observations from the first-level decision were then further examined to a newly imposed decision criteria R&D category percentage value of 1.92 which classify to predict the target firms’ letters to shareholders with R&D category percentage equal or above 1.92 as completed or consumed deal, directing all observation meeting the decision criteria to the consumed terminal node (YES) while those with percentages lower than 1.92 were directed to the third-level decision node. It is important to note that the decision tree model presented in this study classified completion or consumption of M&A deal after 2 levels of decision criteria were met.

Remaining observations which have met the first decision criteria but have failed on the second were all subjected to a last decision criteria which is the investment category percentage value of 4.36 that classify to predict the target firms’ letters to shareholders with investment category percentage equal or above 4.36 as non-completed, directing all observation meeting the decision criteria to the unconsumed terminal node (NO) while those with percentages lower than 1.92 were directed to the consumed terminal node (YES).

The extracted quotations from the performance category showed to describe the firms’ fulfillment of its promised performance and to some extent even over delivered. This goes to show that letters to shareholders of target firms which featured performance concepts beyond the set decision criteria 10.32 in year 2 of its published letters to shareholders are more likely to complete the M&A deal with 37% of the explanatory power of the model.

This first-level criterion of the decision tree model could be described as a strategic consideration of the acquirers in identifying beneficial targets. Given that acquirer firms’ returns are significantly lower when the target firms poorly performed preceding the M&A announcement (MORCK et al., Citation1990). This makes performing firms such as in this study beneficially attractive that could have added to the acquirers commitment to pursue completion of the offered M&A deal, described in this study as firms with performance category percentage equal or above 10.32.

The second-level criterion of the decision tree model points the study to describe that R&D is a major consideration in the interest of acquirers, which factor out in the completion likelihood of the offered M&A deal. This second-level decision criteria in this study suggests to favor completion likelihood for target firms’ letters to shareholders with R&D category percentage equal or above 1.92.

The presence of this much R&D concepts in the target firms’ letters to shareholders suggest that there is a considerable amount of relevant R&D undertakings that the target firms are working on, which this study highlights as an interesting factor in the M&A completion likelihood with 27% of the explanatory power of the prediction model.

There are considerable areas pointed by literatures that could rationalize the importance of firms’ R&D undertakings described in this study’s R&D category, which could have influenced the acquirers’ commitment to pursue completion. First, R&D related resources increase firm’s attractiveness as a target and is a modest predictor for M&A offers (Heeley et al., Citation2006; Ranft & Lord, Citation2000); second, target firms’ R&D resources provides possible solution to acquiring firms R&D maturity blocks (Ahuja & Katila, Citation2001), which could push acquirers to be more committed in pursuing the completion of its offer to break free from the current R&D stagnation and take advantage of the targets innovation-enabling technological resources (Hitt et al., Citation2001; (King et al., Citation2003) that could now provide a new competitive landscape for the acquiring firms (Bettis & Hitt, Citation1995); third, targets R&D engagement could produce disruptive technologies that may change the industry landscape and may threaten industry players. This gives more motivation for acquirers to push through M&A completion, either for advancement or prevention from the changes that these R&Ds may bring to the industry (Heeley et al., Citation2006). It is important to note at this point that the model predicts M&A offer completion after observations meet both decision criteria set in the first and second level.

While the decision tree model could already predict M&A completion after both the first and second-level criteria are satisfied, the model could still proceed to predict completion for observations that have not satisfied the second-level criterion, having investment category percentage value of 4.36 as the last measure, for investment category percentage lesser than 4.36 as predicted completed offers and those investment category percentages greater or equal to 4.36 predicted as uncompleted.

To recall investment category describes the target firms’ various investment related decisions and updates. This third criterion of the model suggests that target firms with investment category percentage lesser than 4.36 are more likely to give in to M&A offers. This may be so, since investment category with lesser percentage could be described as firms with lesser investment featured engagements in its letters to shareholders, that may have caused by the possibility of having either no new viable investment projects or resource constraints have struck these firms that could have limit the firms investments execution (Calomiris & Hubbard, Citation1993). These considerable circumstances may have exposed these firms to vulnerability to be persuaded with M&A offers as it could provide them with the possible solution to the firms’ current investment condition. While those target firms showing above or equal to the decision criterion could be described as firms with substantial investment undertakings that could provide considerable confidence for the firms to unlikely accept unluxurious M&A offers, which may have contributed to the likelihood of non-completion (Betton et al., Citation2000).

Further, it is interesting to note that the portrait given by the descriptive statistics for R&D and investment categories as characteristic descriptions of an M&A target are consistent with the decision criteria set by the decision tree model for target firms predicted for completion on both categories.

The study also notes that the determinant categories set as decision criteria in the prediction model were all observed in the target firms’ letters to shareholders, 2 years prior from the M&A announcement, serving as the indicative year for predicting the possible completion or non-completion of the announced M&A deals.

This study believes that 2 years prior to the made M&A announcement could be the year where acquirers have initially noticed the target firms as M&A prospects and the stature of the target firms on that specific year could have been the base consideration for the offered M&A deal that persuades to explain the decision criteria set by the model to predict completion likelihood, and the following year entails the series of activities in preparation for the acquirers’ private initiation plan and execution before the M&A announcement could be made public as described in Boone and Harold Mulherin (Citation2008) M&A process. Noting that publicly owned targets take longer to complete the M&A deal, for it being large and so being more complex (Dikova et al., Citation2010).

This study’s M&A prediction model and the decision criteria it had set suggests that the target firms’ performance, R&D, and investment categories could be taken as the description of the acquirers’ vested areas of interest over the target firms that explicate the made M&A offering. While the prediction results could be viewed as a description of the target firms’ openness to engage and complete M&A deals, this generated information of the model could provide acquirers with additional insights as to the probability of its identified target firms to accept or complete an M&A offer that could widen up the opportunity for acquirers to make considerable M&A offers, bearing in mind the undesirable cost, largely shouldered by acquirers on non-completed M&A offers.

Acquirers were observed to start incurring significant cost for conducting activities related to prospecting viable M&A targets (Bainbridge, Citation1990) and as such spend for activities in market intelligence gathering. Once viable target is identified, necessary preparations are required so as to initiate an offer, this usually requires the services of various external advisers in accounting, finance, and legal sectors (Dikova et al., Citation2010). On top of it, commitment and other financing charges are also expected for payments made other than cash reserves (Bainbridge, Citation1990). In the event of bid competitions the acquirers could further incur cost for payments on stock premiums that could even lead to a winner’s curse (Kagel & Levin, Citation2009). Knowing that target firms are more likely to resist low-premium offers (Betton et al., Citation2000) and renegotiation of initial contract are pushed when new information are made available (Dikova et al., Citation2010) that could change the original agreed cost related clauses. Further, the considerable operational cost associated to facilitate the M&A processes on the acquirers’ firm for its various planning on the implementation of announcement strategies, human resource and external communication plans and most of all the acquirers assume the associated cost for exposing trade secrets information regarding the post-M&A synergy plans for the target’s resources (Officer, Citation2003), reaching this point in the M&A deal makes M&A completion relatively valuable for the acquiring firms (Dikova et al., Citation2010). Making the assessment of the target firms’ probability to complete an M&A offer very valuable for acquirers as this information could provide them insights of the possible risk awaiting their offers.

5. Conclusions

This study showed the viability and strength of a qualitative based methodology and its methods to describe potential M&A targets with less sensitivity to influencing variables such as ownership (Bettinazzi et al., Citation2020) and borders (Ahammad & Glaister, Citation2008). This helps affirm its encompassing application to describe and explicate the attractiveness of an M&A target with lesser disconcertment whether the target described is American/European owned or whether it is a cross-border offer or within borders. Further, the study also showed the viability of the decision tree through a supervised machine learning in developing an M&A completion prediction model with 67% predictive accuracy.

This study provides implications (1) to firms’ management that the posturing contents featured in firm’s letters to shareholders could expose to signal their firms as M&A targets, (2) that this posturing contents in the firm’s letters to shareholders could also be used to signal the firm’s openness to engage in the possibility of an M&A offer or even entice acquirers, through the utilization of the categories deemed in this study as vested areas of interest of M&A acquirers and (3) to readers to look into the posturing contents of firms’ letters to shareholders, so as to identify potential M&A targets.

5.1. Theoretical implications

The study supplement existing knowledge and open the opportunity to increase available M&A predictive techniques. Especially for those incidents where financial-based prediction models have failed to provide reliable insights (Pasiouras & Tanna, Citation2010; Polemis & Gounopoulos, Citation2012). Further, this study expands the current M&A prediction literature by establishing linkage of the study’s results derived from the use of qualitative data to underpinning M&A prediction notions and correlation studies that were based on financial data, particularly on the relevance of the categories as variables for explicating targets attractiveness for M&A offers.

5.2. Practical implications

The study explored to contribute practice of utilizing qualitative data to describe and predict M&A completion by offering a methodology that could work alongside with financial-based prediction models to provide affirming and considerable insights for corporate acquirers, investors, and stock traders to firms’ susceptibility to M&A offers and deal completion. This study provides added information to parties interested in the likelihood of firms becoming an M&A target. Essentially, the study reinforces its value in the practice of stock investments particularly on generating profits through stock trading prior to an M&A announcement.

5.3. Limitations and future research

The implications stated in this study were limited to the data collected from large western firms (American/European owned) of technology, pharmaceuticals/chemicals, finance, energy, and consumer goods industries from the year 2005 to 2019, whose stocks are publicly traded with market capitalization not less than a billion of dollars.

The decision to favor large firms from the west for observation and analysis was deeply influenced by the practice of these firms to publish letters to shareholders on annual basis and of the availability and completeness of these letters for collection. Besides, the general interest of investors and stock traders are those that includes large publicly traded companies and M&A announcement in Asia were reported with contrary effects on target firms’ share prices (Wong & Cheung, Citation2009) with that of the western firms.

This study acknowledges the need for further studies to reaffirm the portrait description provided in this study, as basis for describing potential M&A targets on other industries and test the robustness of the developed M&A completion prediction model on forthcoming M&A announcements.

The researchers also put notice to a possible downside of machine learning generated models, as it could also suffer from adversarial perturbations of data inputs (Schmidt et al., Citation2018). This study recognizes several rooms for improvements particularly in the enhancement of our proposed technique’s predictive power. Given that machine learning increases its accuracy to provide decision with the increase in data inputs. Another direction might be to perform a random forest algorithm for the development of the M&A completion and non-completion prediction model. Further, to explore the potential for this study’s predictive model to be used alongside with other existing financial-based prediction model, so as to possibly enhance M&A predictive accuracy. Moreover, this study puts notification ahead on the possibility that the application of the proposed model and the provided description could be limited at a specific time range, given that M&A era are driven by one factor to the other as seen in historical M&A waves. Therefore, the need for recalibration of this study’s approach in the future may require redoing the process with recent sets of targets’ letters to shareholders to be sensitive on emerging changes in the indicative categories.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Manolito E. Parungao

Manolito Parungao is an assistant professor at Mindanao State University at Naawan, Misamis Oriental, Philippines. Under the College of Business Administration and Accountancy. He is in the academe for a decade which he holds a master’s degree in Business Management and is currently in his dissertation for his pursuit of a doctor degree in Business Administration at Mindanao State University Iligan Institute of Technology. His area of interest is in Business communications and mergers and acquisitions.

Dr. Adrian Galido is currently a full professor of the Information Systems Programme in the College of Computer Studies, MSU-Iligan Institute of Technology, Philippines. He has an M Technology Management (2005) from the University of the Philippines, Diliman and MS Data Science (2019) from the Asian Institute of Management. He obtained his PhD in Management from the University of San Carlos, Cebu, Philippines in 2012. His areas of interests are in Information Systems Adoption and Data Analytics.

Lovely Parungao is an associate professor of the College of Education and Social Sciences in Mindanao State University at Naawan. She is a copy editor of the Journal of Environment and Aquatic Resources of the university and a co-author of Workbook-Textbook for English in Hospitality Industry. She has led and participated researches in applied linguistics in the lenses of peace, environment, and business. She is currently in pursuit of her PhD in English language studies at Mindanao State University Iligan Institute of Technology.

Maria Leah Suazo is a Certified Public Accountant and currently an Assistant Professor at the College of Business Administration and Accountancy, Mindanao State University at Naawan, Misamis Oriental, Philippines. She holds two master’s degrees: Master in Business Management and Master of Arts in English. She is currently pursuing her doctor’s degree in business administration at Mindanao State University Iligan Institute of Technology. Her dissertation is in progress and is focused on micro enterprises amidst the Covid-19 pandemic. Before joining the academe, she worked for several banks for about 13 years and was a state auditor for six years.

References

- Abrahamson, E., & Amir, E. (1996). The information content of the president’s letter to shareholders. Journal of Business Finance and Accounting, 23(8), 1157–33. https://doi.org/10.1111/j.1468-5957.1996.tb01163.x

- Agrawal, A., & Jaffe, J. F. (2016). Do takeover targets underperform ? Evidence from operating and stock returns author (s): Anup Agrawal and Jeffrey F. Jaffe Published By?: Cambridge University Press on Behalf of the University of Washington School of Business Administration Stable URL, 38(4), 721–746. https://doi.org/10.2307/4126741

- Ahammad, M. F., & Glaister, K. W. (2008). Recent trends in UK cross‐border mergers and acquisitions. Management Research News, 31(2), 86–98. https://doi.org/10.1108/01409170810846812

- Ahuja, G., & Katila, R. (2001). Technological acquisitions and the innovation performance. Strategic Management Journal, 22(3), 197–220. https://doi.org/10.1002/smj.157

- Akkus, O., Cookson, J. A., & Hortacsu, A. (2016). The determinants of bank mergers: A revealed preference analysis. Management Science, 62(8), 2241–2258. https://doi.org/10.1287/mnsc.2015.2245

- Alcalde, N., & Espitia, M. (2003). The characteristics of takeover targets: The Spanish experience 1991-1997. Journal of Management and Governance, 7(1), 1–26. https://doi.org/10.1023/A:1022416521512

- Ali-Yrkkö, J., Hyytinen, A., & Pajarinen, M. (2005). Does patenting increase the probability of being acquired? Evidence from cross-border and domestic acquisitions. Applied Financial Economics, 15(14), 1007–1017. https://doi.org/10.1080/09603100500186978

- Altman, E. I., Haldeman, R. G., & Narayanan, P. (1977). ZETATM analysis A new model to identify bankruptcy risk of corporations. Journal of Banking and Finance, 1(1), 29–54. https://doi.org/10.1016/0378-4266(77)90017-6

- Ambrose, B. W., & Megginson, W. L. (1992). The role of asset structure, ownership structure, and takeover defenses in determining acquisition likelihood. Journal of Financial and Quantitative Analysis, 27(4), 575–589. https://doi.org/10.2307/2331141

- Amernic, J., Craig, R., & Tourish, D. (2010). Measuring and assessing tone at the top using annual report CEO letters. The Institute of Chartered Accountants of Scotland.

- Asquith, P., & Kim, E. H. A. N. (1982, December). American finance association the impact of merger bids on the participating firms ’ security holders author (s): Paul Asquith and E . Han Kim Source : The Journal of Finance, 37(5), 1209–1228. Published by : Wiley for th. Journal of Finance. https://doi.org/10.1111/j.1540-6261.1982.tb03613.x

- Baghai, M., Smit, S., & Viguerie, S. P. (2007). The granularity of growth. McKinsey Quarterly, 21, 41–51. https://doi.org/10.1002/9781119197409

- Bainbridge, S. M. (1990). Exclusive merger agreements and lock-ups in negotiated corporate acquisitions. Minnesota Law Review, 75, 239. https://scholarship.law.umn.edu/mlr/2359

- Baird, J., & Zelin, R. (2000). the effects of information ordering on investor perceptions: An experiment utilizing presidents’letters. Journal of Financial and Strategic Decisions, 13(3), 71–80. http://www.financialdecisionsonline.org/archive/pdffiles/v13n3/baird.pdf

- Barnes, P. (1990). the prediction of takeover targets in the U.K. by means of multiple discriminant analysis. Journal of Business Finance & Accounting, 17(1), 73–84. https://doi.org/10.1111/j.1468-5957.1990.tb00550.x

- Barnes, P. (1999). Predicting UK takeover targets: Some methodological issues and an empirical study. Review of Quantitative Finance and Accounting, 12(3), 283–302. https://doi.org/10.1023/A:1008378900054

- BELKAOUI, A. (1978). Financial ratios as predictors of Canadian takeovers. Journal of Business Finance & Accounting, 5(1), 93–107. https://doi.org/10.1111/j.1468-5957.1978.tb00177.x

- Berger, A. N., Demsetz, R. S., & Strahan, P. E. (1999). The consolidation of the financial services industry: Causes, consequences, and implications for the future. Journal of Banking and Finance, 23(2), 135–194. https://doi.org/10.1016/S0378-4266(98)00125-3

- Bettinazzi, E. L., Miller, D., Amore, M. D., & Corbetta, G. (2020). Ownership similarity in mergers and acquisitions target selection. Strategic Organization, 18(2), 330–361. https://doi.org/10.1177/1476127018801294

- Bettis, R. A., & Hitt, M. A. (1995). The new competitive landscape. Strategic Management Journal, 16(1 S), 7–19. https://doi.org/10.1002/smj.4250160915

- Betton, S., Berk, J., Dann, L., Ferson, W., Hansen, R., Harris, R., Holderness, C., Hollifield, B., Jennings, R., Kahn, C., Malatesta, P., Perotti, E., Ritter, J., Smith, D., Spencer, B., Spiegel, M., Stulz, R., & Titman, S. (2000). Toeholds, bid jumps, and expected. Society, 13(4), 841–882. https://doi.org/10.1093/rfs/13.4.841

- Blonigen, B. A., & Taylor, C. T. (2000). R&D intensity and acquisitions in high-technology industries: Evidence from the US electronic and electrical equipment industries. Journal of Industrial Economics, 48(1), 47–70. https://doi.org/10.1111/1467-6451.00112

- Boone, A. L., & Harold Mulherin, J. (2008). Do auctions induce a winner’s curse? New evidence from the corporate takeover market. Journal of Financial Economics, 89(1), 1–19. https://doi.org/10.1016/j.jfineco.2007.08.003

- Bower, J. L. (2001). Not all M&As are alike: And that matters. Harvard Business Review. March 2001. https://hbr.org/2001/03/not-all-mas-are-alike-and-that-matters

- Brar, G., Giamouridis, D., & Liodakis, M. (2009). Predicting European takeover targets. European Financial Management, 15(2), 430–450. https://doi.org/10.1111/j.1468-036X.2007.00423.x

- Brennan, N. M., & Conroy, J. P. (2013). Executive hubris: The case of a bank CEO. Accounting, Auditing & Accountability Journal, 26(2), 172–195. https://doi.org/10.1108/09513571311303701

- Calomiris, C. W., & Hubbard, R. G. (1993). Internal finance and investment: Evidence from the undistributed profits tax of 1936-1937. https://doi.org/10.3386/w4288