?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study, which analysed the profitability of 42 reinsurers in Sub-Saharan Africa from 1991 to 2020, revealed that various factors such as gross domestic product, competition (HHI), premium growth, investment performance, underwriting risk, and operational efficiency affect the profitability in these companies. This study is quantitative and dynamic using system-generalised method of moments to analyse the data. The study discovered that reinsurers should broaden their services to remain highly competitive and boost their premium growth such that their profitability is sustained. Also, there should be a separate department of qualified professionals overseeing the adequate management of risk before sealing ceding agreement with insurers.

1. Introduction

Financial institutions are critical for economic growth of any country (Bertucci, Citation2019; McKillop et al., Citation2020) and insurance sector is a major financial institution that spurs economic growth and advancement. Insurance sector does not only focus on improving individual living by hedging their risk but also perpetrate inflow of fund into the economy. Thus, their profitability is of most important concern to researchers. A profitable financial institution enhances the stability of an economy because such economy can be deemed to be healthy. Insurance and reinsurance are a major financial institution that play a critical role in economic development of both developed and developing countries (Tsvetkova et al., Citation2021). Due to recent climate changes, there is an upsurge in occurrence of risk in the world. From Swiss report, over 70% of the insured losses globally are from natural disaster caused by weather, destroying businesses, homes, and properties and this has led to increased claims by the insured.Footnote1 This led the insurers to require coverage from reinsurers in other not to be a victim of the insureds’ hedged risks (Tegegn et al., Citation2020). As the burden is much on insurance companies, there is a huge rush for further covering by the reinsurance companies. In recent times, African reinsurance markets profitability has been a strength. Yet, over 60% of reinsurance executives report reinsurers’ profitability as low, propelled by declining rates, rising claims, and increasing costs. Hence, the importance of investigating the profitability of reinsurance companies cannot be overemphasised.

According to Eling and Jia (Citation2019), a profitable insurance sector is efficient enough to cater for the catastrophes that would have befallen individuals and an economy. Insurance drives economic growth by expediting the recovery of claimants and beneficiaries; and reinsurers act as an important risk management tool available to insurers which leads to reduction in insurance risks (Weisbart, Citation2018). Furthermore, reinsurance is a vital tool insurer use to manage risks (Park et al., Citation2019) and the amount of capital they must hold to support those risks. This in turn ensure that the volatility of financial results is reduced, solvency is stabilized, capital is more efficiently used, and underwriting capacity is increased (Carter, Citation2013).

According to the AtlasMagazine (A.M) report 2021, sub-Saharan Africa (henceforth SSA), over the past decade experienced a surge in infrastructure investment that has significantly impacted the growth of the reinsurance market. Surprisingly, the trend is projected to continue due to the significant natural resources, strongly growing economic indicators, strong insurance growth potential, young and dynamic population and evolving insurance legislation that has characterised the region. During the period 2011–2020, SSA reinsurers achieved an average yearly growth of 9.15% in gross written premiums. This performance comes at a time when most local currencies are undergoing significant depreciation against the dollar. For instance, the South African Rand and the Nigerian Naira have depreciated by 54.8% and 63.5%, respectively, over the past decade. However, the Covid-19 crisis plunged the insurance market back into stagnation with reinsurance premiums still growing by 0.82% in 2020.Footnote2

It is a clear fact that insurance sector is faced with globalisation, market liberalisation, and increased competition, having the interest in unveiling the significant factors affecting the profitability of reinsurance which is like a mother of the success of the sector becomes relevant and crucial. Based on the average stable growth detected in SSA reinsurance despite the myriad of adverse situations affecting insurance sector in the region, investigating what factors significantly determine their profitability is vital to keep up with the projected growth and continue to be a huge support for the economic growth of the region. Aside the fact that profitability is one of the major determinants of a company’s success and performance, it has been further confirmed by Öner Kaya (Citation2015), Kripa and Ajasllari (Citation2016b), that a profitable insurance sector will keep growing.

Hence, if significant determinants of profitability are known and properly monitored, the projected growth will not be jeopardized as those factors will be given full concentration (O.M. Olarewaju & Msomi, Citation2021a). A profitable reinsurance fosters image that attracts dealings with many insurers such that there will be more fund to carry out investment that will yield higher return on investment (ROI). In fact, profitability is a tangible factor to convince an individual to get a cover for their businesses, properties, or lives with insurers that are reinsured with a profitable reinsurer. A profitable reinsurance is a force that propels gross written premium that can help keep up with the growth that has been forecasted to persist in the region, it is paramount to investigate what factors affects their profitability.

Undoubtedly, a substantial amount of research has explored different factors that impact firm profitability. In fact, the issue of profitability continues to be a factual, important, and continual phenomenon that attracts the attention of many researchers globally. In the context of insurance sector, the determinants of profitability or factors that affects financial performance in insurance companies; and the effect of reinsurance on the profitability or financial performance of both life and non-life have been widely examined, for instance, Hasan et al. (Citation2018), Akotey et al. (Citation2013), Boadi et al. (Citation2013), and Camino-Mogro and Bermúdez-Barrezueta (Citation2019) etc.

Nonetheless, there is a dearth of research on the factors that affect profitability of reinsurance companies globally. To the best knowledge of the researcher, the known studies in this context are the studies of Mukherjee et al. (Citation2020) and Sidhu and Verma (Citation2017). These two studies have been limited to only firm-specific variables and both studies have been carried out on a single public India reinsurance company. Surprisingly, there has been no known study on the determinants of profitability or factors affecting the profitability of reinsurance companies in any economy in SSA not to talk of a study that has examined the factors affecting profitability of reinsurance companies using SSA as a region.

Basically, SSA is considered relevant for this study because of the unique reinsurance landscape and the huge reinsurance growth potential.Footnote3 Although there are barriers to entry in reinsurance markets due to the tightened local regulations and there are some other odd operating conditions such as volatile oil prices, high inflation rates in most economies, elevated competition, local currency depreciation among many other internal challenges, there is still significant potential growth. The fact that one of the goals of financial management is to maximise owners’ wealth, profitability remains an important objective of financial management (Kripa and Ajasllari, 2016). Profitability being a major determinant of a company’s performance, efficiency, and growth has made investigating the factors affecting the profitability of reinsurance companies in SSA paramount.

Specifically, this study builds on the empirical research in numerous ways. First, this study is on reinsurance companies in SSA which is a step ahead of the previous studies that have focused on insurance companies, life, and non-life. The welfare of reinsurance is so important because of their prevailing impact on the sustainability of insurance companies. Second, this study will concurrently comprise three different dimensions of factors (firm-specific, industry-level, and macroeconomic) that may affect firm’s profitability. Therefore, the model built in this study represents an upgrade to those two existing research in India (Mukherjee et al., Citation2020; and Sidhu and Verma, Citation2017) as they focused only on firm-specific factors. While firm-specific factors have been suggested by Kripa and Ajasllari (2016); Zainudin, Mahdzan and Leong (Citation2017), Derbali (Citation2014), etc. as important factors influencing profitability of insurance sector, macroeconomic, and industry-level factors have also been suggested by Camino-Mogro and Bermúdez-Barrezueta (Citation2019), Hasan et al. (Citation2018); as very important factors affecting insurance sector profitability. As a result, this model is unique enough to have incorporated the three dimensions of factors, hence it will present a more precise picture of SSA reinsurance companies’ profitability.

Third, since the evident research on the determinants of reinsurance companies’ profitability are from India, this research will contribute to literature by providing comparable data from SSA. This is an exploratory regional-based panel study using data from a region of mostly developing and emerging economies which can be used for the generalisation of the findings across economies at such stages of development across the globe. Fourth, the model is formulated in a way that encompasses the dynamic aspect of profitability. A wide number of economic relationships have dynamic features. For this study, the reinsurers’ profitability in the previous period is related to their current period profitability such that the lagged profitability is one of the regressors in the specified model. To the best of the researchers’ knowledge, the factors affecting profitability of reinsurance companies in SSA have not been analysed using three level factors dimension with a dynamic model.

Thus, this study seeks to fill the gaps identified using all the reinsurance companies with up-to-date data in SSA focusing on the firm-specific, industry-level, and macroeconomic factors. The rest of the paper is organised as follows. Literature review section reviews the variables employed in the determinants of profitability used in this research. In methodology section, the empirical model is formulated, and the data used for analysis is described. Analysis section provides the results, discussion of findings, and policy implications. Concluding remarks are presented in the final section.

2. Literature review and hypotheses formulation

Resource based value developed by Welnerfelt (Citation1984) underpins this study. The theory posits that organisations with strategic capabilities and resources can create a competitive advantage which leads to higher profitability over organisations that do not (Egbunike & Okerekeoti, Citation2018; O.M. Olarewaju & Msomi, Citation2021a). The theory postulates that profitable firms have competitive advantages over others. All variables in this research were chosen based on relevant theories, extant empirical review, and accessibility of data. The theoretical reasoning for each of the variable used in this study is presented in the successive paragraphs.

2.1. Gross domestic product (GDP)

GDP denotes the overall changes in economic activities that affects an individual company. It is expected that a change in economic activities can affect firms’ profitability, and hence the addition of GDP growth rate in the model of this study will control for both the economic boom and recession. It is expected that during the economic growth, there is a boom of activities that spurs the profitability of firms including reinsurers. On the other hand, a declining economic growth is expected to crumble economic activities and deteriorate profitability. Scholars such as Sinha and Sharma (Citation2016) observed positive profitability to GDP relationship in India, Trujillo‐Ponce (Citation2013) reported positive effect of GDP growth on Return on assets (ROA), the measure of profitability in Spain and Alshammari et al. (Citation2019) revealed a positive relationship between GDP growth and the efficiency of insurance sector in the Gulf Cooperation Council countries. However, Lee (Citation2009) found an insignificant relationship between GDP and profitability in US firms.

Hypothesis 1 (H01): GDP growth does not affect the profitability of reinsurers in SSA.

2.2. Interest rates (INT)

The term interest rate was defined by Ismail et al. (Citation2018) as the price which the borrower will pay for using borrowed funds from the lender or the fee paid on the loaned assets. It is the annual placement rate that reflects the actual price money has in the financial markets. Reinsurers are concerned with interest rate as the value of products sold depends on interest rate and long-term investment is directly related to interest rates (Berends et al., Citation2013). Also, lower interest rates will improve overall liquidity in the general sector and therefore lead to “increased investment and consumption” that can spur reinsurance sectors profitability (Msomi, Citation2022; Murungi, Citation2013).

Hypothesis 2 (H02): Interest rate does not affect the profitability of reinsurers in SSA.

2.3. Exchange rate (EXR)

The exchange rate is the price that a national currency is exchangeable for the other nations. Barnor (Citation2014) revealed that the exchange rate had a considerable beneficial influence on performance in Africa for listed businesses. The fact that most economies in SSA are witnessing currency depreciation makes it germane to investigate the effect of exchange rate on the profitability of reinsurers.

Hypothesis 3 (H03): Exchange rate does not affect the profitability of reinsurers in SSA.

2.4. Competition (HHI)

Structure-Conduct-Performance (SCP) hypothesis avers that market structure influences the firms’ structure and performance. Competition is used to evaluate how concentrated reinsurance market in SSA is and the Herfindahl-Hirschman index (HHI) is used to capture it as it compares the size of the individual companies to the entire sector. Following the studies conducted by Bastruk, Shim (Citation2017), Yanase and Limpaphayom (Citation2017), and Alshammari et al. (Citation2019), the HHI is used to capture the intensity of competition as it reflects the rivalry amongst industry actors. HHI weighs the sum of squares of net premium written of each reinsurance company against overall written premium of the company. HHI ranges from 0 to 1 such that a value greater than 0.5 denotes high concentration of activities or low competition and the value of less than 0.5 denotes low concentration and a highly competitive market. The closer the value is to 0, the higher the degree of diversification and competition. Based on the SCP hypothesis, a positive effect of HHI is expected on profitability. The formula is stated below:

all things being equal, .

P stands for total number of reinsurance companies examined, NPW is the reinsurance net premium written, and denotes the reinsurance companies.

Hypothesis 4 (H04): Competition does not affect the profitability of reinsurers in SSA.

2.5. Premium growth (PGR)

Premium from insurers serves as the bedrock of revenue generation for reinsurance companies. Moreover, reinsurance companies make revenue by investing the insurance premiums received from insurers. This variable specifically reveals the market penetration of the reinsurance companies and a positive effect of premium growth on profitability of SSA reinsurers is expected as it was found by Sidhu and Verma (Citation2017) in India.

Hypothesis 5 (H05): Premium Growth does not affect the profitability of reinsurers in SSA.

2.6. Risk retention ratio (RRR)

This reveals the efficiency of reinsurance in managing their risk. As one of the major roles of reinsurance is to transfer risk, it is expected that the more efficient they can manage their inherited risk, the more profitable they are. This variable is calculated as the ratio of net premium to the gross written premium in a particular reporting period. Reinsurers absorbs the transferred components of insurers risk portfolios by the ceding agreement such that the possibility of paying a huge obligation stemming from an insurance claim is minimised. Generally, the higher this ratio (RRR), the more profitable reinsurance companies will be (Mukherjee et al., Citation2020).

Hypothesis 6 (H06): Risk Retention ratio does not affect the profitability of reinsurers in SSA.

2.7. Investment performance (INP)

Investment plays a very crucial role in the profitability of a company. IP reveals the proficiency of investment decisions of the company. Organisations are investing their resources to make a return that will encourage them to improve their profit making. Njeru (Citation2018) avers that there is a positive relationship between investment and the level of profitability of a company. IP shows the earnings of the reinsurers via its investment which might be a little portion of their total portfolio, however, constitute a crucial source of profitability to them.

Hypothesis 7 (H07): Investment capability does not affect the profitability of reinsurers in SSA.

2.8. Underwriting risk (UNR)

This measures the performance of the reinsurance companies by highlighting their efficiency in managing the underwriting function. The underwriting risk shows the sufficiency of reinsurance companies’ inventive performance, hence, determines their profitability (AlAli et al., Citation2019). The reinsurance company’s financial success is dominated by robust underwriting from the insurers. Thus, the amount of claim covered by the net premium will affect their profitability. A lower underwriting risk is expected to better spur profitability of reinsurers.

Hypothesis 8 (H08): Investment capability does not affect the profitability of reinsurers in SSA.

3. Other control variables used

3.1. Inflation rate (INF)

Inflation captures the price variations of goods and services from year to year as monetary instability is expected to affect firms’ profitability. Inflation which is a prolonged increase in the overall price level of the economy over time is expected to have negative effect on reinsurance profitability (Alhassan et al., Citation2015; Demir, Citation2009; Pattitoni et al., Citation2014; Shiu, Citation2004). Suheyli (Citation2015) state that an unprecedented surge in prices increases reinsurers liability because it reduces real income of an economy and causes sales activities to be hampered. Suheyli (Citation2015) furthermore adds that inflation surely plays an imperative role in insurance and has a negative effect on various aspects of insurance operations such as claims, technical provisions, and expenses. In anticipation of inflation, the payment of claims increases as well as the reserves required in expectation of higher claims, thereby lessening the technical result and profitability.

3.2. Size (SIZ)

The reinsurer’s size is included to control for the economies of scale. The size of a company contributes in many ways to its financial success. Large reinsurers benefit from economies of scale compared to start-ups (Ahmed, Citation2010; Flamini et al., Citation2009). Size is measured as the natural logarithm of gross written premium. Previous studies have established a positive correlation between size and profitability. Nevertheless, there are arguments that if assets get to optimal ratio, it may have negative impact on profitability (Al-Shami, Citation2013; O. Olarewaju & Msomi, Citation2021b).

3.3. Operational efficiency (OPE)

This captures the expense ratio of reinsurance companies. There is a sure linkage between efficiency and profitability (Karadağ Erdemir, Citation2019). Operating efficiency is a company’s capacity to decrease adverse situations and optimise resources to offer excellent products and services to customers (Ndolo, Citation2015). Thus, ability of reinsurance to settle their claims and finance other operational expenses from the net premium earned will determine their profitability.

3.4. Liquidity (LIQ)

The uncertainty in predicting the timing, severity, and frequency of claims or benefits by insurers has made it very crucial for reinsurers to plan their liquidity painstakingly to achieve profitability. Reinsurance liquidity refers to the ability of the reinsurer to fulfil its immediate obligations to insurers (policyholders) without having to increase profits from underwriting and/or liquidate financial assets (Kariuki & Nguyo, Citation2020). It is a clear fact that reinsurance must be liquid enough to hedge the risk and loss of the insurers. Although there are ambiguous findings on the relationship of liquidity and profitability. While Boadi et al. (Citation2013), Charumathi (Citation2012) suggests a positive relationship between liquidity and profitability, studies such as Ahmed et al (Citation2010) found a negative relationship between liquidity and profitability such that high liquid assets lead to higher maintenance cost, discourage external funds that inadvertently reduces the value of the company instead of maximising the value.

4. Research method

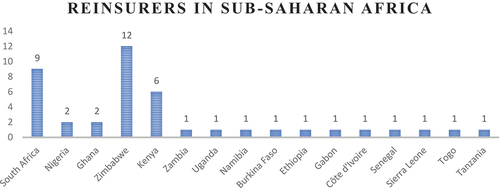

This is an exploratory regional-based dynamic panel longitudinal study that used secondary data from 1991 to 2020 on the existing 42 reinsurance companies in SSA. The firm-specific and the component of the HHI index data required for this study are drawn from S&P CapitallQ, ReportLinker, and annual reports of the respective companies while the macroeconomic data are drawn from the World Bank’s database and international financial statistics. This is a regional-based and unbalanced panel study with 1260 observations (42 reinsurers for 30 years) from 16 SSA countries. The distribution of the companies across the countries is shown in the graph below.

Source: Authors’ compilation from A.M. 2021 report.Footnote4 Note that these companies are the only existing reinsurers in SSA.

A longitudinal panel study is justified and preferred based on its ability to cater for behaviourial differences across a time period, cross-section or both, manage heterogeneity problems, and allow for more estimation of parameters (Hsiao, Citation2014; Kutu & Ngalawa, Citation2016). The reinsurance companies used were selected purposively due to data availability for the period of study.

4.1. Model specification

The factors affecting the profitability of SSA reinsurance companies is depicted using the below dynamic linear relationship between dependent and independent variables is shown as:

is the vector of macroeconomic factors,

denotes the industry-related factor and

is the vector of firm-specific factors.

is the composite error term (IID

. The

is composed of

is the observable time-specific effect which can be related to the global shocks,

is the time variant reinsurers’ characteristics and

is the idiosyncratic error.

To be explicit on EquationEq. (2)(2)

(2) and reflect the dynamism of the model, it leads to the following:

where is the dependent variable, ROA;

is the constant term,

is the speed of convergence in the direction of equilibrium.

is the one year lagged ROA which denotes the lagged profitability measure which signifies the dynamic dimension of the model and

denotes the research is a panel study. To incorporate the variables as explained in the hypotheses above, the empirical model of the factors affecting profitability of SSA reinsurance companies is

are the estimated coefficients for macroeconomic variables,

is the estimated coefficient for industry-level variable, and

are the estimated coefficient for firm-specific variables. The study used the ROA as the dependent variable to measure profitability. ROA is used to capture profitability as it is referred to as the most reliable indicator of profitability (Hardwick and Adams, Citation2002; Malik, Citation2011, Sidhu and Verma, Citation2017; Zainudin, Mahdzan and Leong, 2017). ROA reflects the proceeds from assets owned by the firm, and this truly represents the profitability. In addition, ROA has been used by scholars to measure profitability in previous studies on insurance sectors. For instance, Sambasivam and Ayele, (2013); Lee (2014), Zainudin et al. (2017), Sidhu and Verma (Citation2017).

The measurement of the variables used in this study are explicitly defined as shown below ()

Table 1. Variable definition, measurement and A priori expectation

4.2. Estimating technique

Specifically, two-step system generalised method of moments (SYS-GMM) is used to estimate the model of this study. This technique is appropriate of this study due to the following reasons:

It caters for cross-sectional dependency problems,

it controls for time-invariant company specific effects,

it deals with the endogeneity problem of lagged dependent variable,

it permits a certain degree of endogeneity in the other regressors,

it optimally combines information on cross-company variation in levels with that of within-company variation in changes (Fukase, Citation2010).

For robustness check, the validity and reliability of the model are verified using Arellano and Bond’s test (AR1 and AR2) for auto correlation and Hansen J test for over-identification of instrument are used. These two tests are conducted because, notably, GMM estimator’s validity is justified if the following two conditions are met. First, validity of over-identifying restrictions on all chosen instrument and second, exclusion of the presence of second-order serial correlation in residuals.

Particularly, AR1 and AR2 tests were conducted to test for the serially correlated errors in the idiosyncratic disturbance term incorporated in the GMM estimator. Remarkably, Anderson and Hsiao (Citation1981) noted that the first order autocorrelation in the differenced residuals does not signal an inconsistent estimation. Thus, the existence of first order autocorrelation does not hamper the consistency of the GMM estimator whilst there should not be any trace of the second order autocorrelation in the model. Furthermore, Hansen J test which is most preferred for SYS-GMM than Sargan test is used to test for over-identification of instrument in the model. With these tests being passed by the model, the validity and reliability of the estimation in this study is justified.

5. Empirical results and discussion

reports the descriptive statistics of the variables analysed while the pairwise correlation matrix is reported in .

Table 2. Descriptive statistics

Table 3. Correlational analysis

shows that the number of observations reveals that the panel is unbalanced as none of the variables have up to 1260 as expected. The mean denotes the average values of 0.0228178, 2.682895, 18.25703, 33.98836, 3.603197, 0.21063, 4.650519, 0.7012148, 1.333708, 0.5575952, 3.305809, 0.7405357, and 1.552689 for ROA, GDP, interest rate, exchange rate, inflation rates, HHI, premium growth rate, risk retention ratio, liquidity ratio, investment performance, reinsurer’s size, underwriting risk, and operational efficiency, respectively. The values of standard deviation for the variables show that most of the variables have minimal values which indicates that the data points are close to the mean of the data set. On the other hand, only exchange rate has a high standard deviation which implies that the data points are scattered out over a broader range of value. The minimum and the maximum values reveal the first order (smallest) and the last order (largest) observation in the dataset.

show that most of the correlation coefficient’s values are low. This is desirable as it reveals that the analysis is free from multicollinearity. The highest correlation coefficient values are between inflation risk retention ratio (0.542); exchange rate and risk retention ratio (0.549); size and underwriting risk (0.5622). None of these vales exceed 0.7 which is the value of correlation that signifies multicollinearity and considered harmful by Gujarati (Citation1995). Thus, there is no multicollinearity problem in the study’s model estimation or analysis.

6. Regression analysis

The result of GMM estimation is shown in . Following Roodman (Citation2009), a credible lagged dependent variable should obtain values less than 1.00 to suggest a stable dynamic with slower divergence from equilibrium values. The point estimate of 0.417 is lower than 1.00 which justifies the credibility of our dynamic model estimation.

Table 4. Two-step system-GMM

Accordingly, the 1003 number of observations reveals that the panel is unbalanced. Roodman (Citation2009), Heid et al. (Citation2012), and Oseni (Citation2016) noted that only the Hansen J test is relevant to determine the reliability of instrument specified in SYS-GMM; hence, the Sargan J test is not required. The insignificant probability value of 0.847 revealed by the Hansen J statistic test implies that the null hypothesis of no over-identifying restrictions is accepted shows the reliability of instruments specified and implies that there is no over identification of all chosen instrument or cross-sectional dependence in the model. Notably, where the number of instruments is greater than the number of groups leads to a weak Hansen test which inadvertently flaws the estimation. In the case of this study, the number of instruments (9) is far less than the number of groups (42) and this reveals that the test is not weakened and the system GMM estimation is reliable.

Also, the Wald test statistic which tests the joint significance of the independent variables under the null hypothesis of no relationship is rejected because of its significance. Furthermore, the probability values of the Arellano-Bond first and second order serial correlation are 0.000 and 0.535 respectively signifies that there is no existence of serial correlation in the model specified. The fact that all the statistical tests align with the GMM requirements, its is established that the model specification and instruments used are valid.

The positively and significantly affects the ROA which confirms the dynamic nature of the model. This implies a direct and significant influence of past year profitability on the present year profitability of the SSA reinsurance companies at 1 per cent having a Z-statistic value of 3.13 > 2.58. Likewise, the results reveal a low profitability persistence in SSA reinsurance companies as presented by the lagged ROA variable. This low value signifies the relatively high intensity of competition among reinsurers in SSA and due to this intensity, the adjustment process speed towards the mean profit is relatively high. The findings conform to the findings of Marigu, Otambo (Citation2016) and Pervan et al (Citation2019).

From the results, economic growth measured by GDP growth rate has a positive and significant effects on the profitability of SSA reinsurers. GDP, which is used globally as the main measure of output and economic activity, exhibits a significant effect on profitability of SSA reinsurers. A promising economic condition spurs economic activities, increase people’s income and encourage greater insurance deals with insurers. This, in turn, increases the need for higher cover by reinsurance to reduce the risk of the insurers and hence reinsurers profitability is improved. This finding aligns with a study conducted in India by Sinha and Sharma (Citation2016) and a study conducted in Spain by Trujillo‐Ponce (Citation2013).

Interest rate and exchange rate have positive but insignificant effect on SSA reinsurers’ profitability. This indicates that these macroeconomic determinants contribute to a more profitable SSA reinsurance companies, but they are insignificant. Exchange rate aligns with the a priori expectation while interest is against the a priori expectation because a higher interest rate is expected to reduce liquidity that will limit investment and financial performance, hence hamper profitability (Murungi, Citation2013).

Inflation rate has negative and insignificant effect on SSA reinsurer’s profitability. The negative effect of inflation rate aligns with the a priori expectation and the results of a study conducted on the USA and UK insurance sector by Batool and Sahi (Citation2019). Certainly, that payment of claims and other operating costs are higher above revenue which during inflation which accidentally leads to reduced profitability.

The competition (HHI) coefficient which is the only industry-level factor considered in this study is positive and statistically significant. This validates the SCP hypothesis for SSA reinsurance companies and suggests that competition affects the profitability of SSA reinsurers. A competitive company diversifies to outrun their competitors which broadens their line of businesses and generate more profit.

Premium growth rate, liquidity, investment performance, size, and operational efficiency have direct effect on profitability of SSA reinsurers. Starting with premium growth, which is the annual increase in premium, signifies the market penetration of the reinsurers. The finding conforms with the previous study on insurance companies such as Sambasivam and Ayele (2013) but negates the findings of insurance sector studies by Ana-Maria and Ghiorghe (Citation2014) in Romania and Charumathi (Citation2012) in India. In 2020, despite the hit of COVID-19, reinsurance premiums in SSA attained approximately five billion U.S. dollars (Rudden, 2022).Footnote5 Clearly, premium is the main source of income for reinsurers, and this is used to expand businessand broadens their customer base such that expenses are managed critically to generate more profit.

Liquidity also has positive and insignificant effect on SSA reinsurers’ profitability. This finding negates the agency cost theory that posits managers take advantages of liquid assets, incur higher agency costs that reduces their profitability (Adams & Buckle, 2000) and the finding from the study by Malik (Citation2011) on insurance sector in Pakistan. In SSA reinsurance sector, liquidity is not a significant factor affecting their profitability. This finding is consistent with Mehari and Aemiro (2013), Derbali (Citation2014) and Zainudin et al., (2017) who have found insignificant effect of liquidity on profitability of insurance companies. The finding also implies that the more liquid SSA reinsurers are, the more profitable even though it is insignificant. This implication of a positive effect of liquidity on the profitability of the examined reinsurers is that cash is readily available to meet and settle the instant request for claims due for payment in SSA reinsurance companies.

For investment performance, the direct and significant effect on profitability conforms to the studies of Lee (2013), Njeru (Citation2018) and Rajapathirana and Hui (Citation2018). Investment which is the second major source of income for reinsurers next to premium. Insurers might have higher returns from underwriting but for reinsurers, investment income is very germane (Chen and Hamwi, Citation2000). The more investment reinsurance company can launch into, the better their chances to overcome underwriting losses and the more profitable they become. Shrewd investment acts as cushion to combat the challenges posed by dwindling interest rate, political instability, inflation rate, and currency depreciation among many others. That reflects the hence the positive effect of investment performance on profitability of SSA reinsurance sector indicates the huge maximisation of investment opportunities with the earned premium which significantly improves their profitability.

Size has a positive but insignificant effect on the profitability of SSA reinsurance companies. The insignificance of size negates the findings of Malik (Citation2011), Almajali et al. (Citation2012) and Mehari and Aemiro (2013) who had previously examined the effect of firm size on profitability of insurance sector. The size of the firm affects its profitability directly because first, large firms can exploit economies of scale which makes them grow faster than small firms; second, larger firms have the ability to hire talented employees that will improve business performance; third, larger firms are able to withstand the shocks from dwindling and uncertain market conditions; Fourth, larger firms are capable of hiring professional experts that deliver improved services that will cause a boom in the firm (Flamini et al., Citation2009). All these opportunities from size makes them more efficient, stable and open to more opportunities that leads to increased profitability (Ahmed, Citation2010). However, for the factors affecting SSA reinsurance companies, size is insignificant.

For operational efficiency, it was revealed that the net premium of SSA reinsurers covers their operating expenditure which indicates a sustainable, healthy, and consistent reinsurance sector in SSA. The more profitable reinsurers are, the higher their operational efficiency. This finding conforms to the study of Wongchai (Citation2017).

On the other hand, from the firm specific factors examined, it was found that risk retention ratio and underwriting risk have negative effect on profitability. While risk retention ratio is insignificant, underwriting risk significantly affect profitability of SSA reinsurance companies. The negative effect on underwriting risk aligns with Al-Shami, Mehari and Aemiro (2013), Lee (2014) and Hussain) but contrast the findings of Zainudin et al (2017) and Milidonis et al. (Citation2019). Underwriting risk reveals the efficiency of a company in making its underwriting decisions. It shows the claims incurred out of the premium earned by the company. The finding reveals the inadequacy of the underwriting capacity of SSA reinsurers as more claims paid with respect to the premium earned raised the subsequent expenses that reduces their profitability.

In the same manner, the risk retention ratio indicates the risk bearing capacity of the SSA reinsurers. Generally, the higher this ratio, the more profitable reinsurers should be. However, the inverse effect reveals that there are inefficiencies in the SSA reinsurers’ ability to manage their risk such that their profitability is not hampered. This finding aligns with Sidhu and Verma (Citation2017) but negates the finding of Mukherjee et al. (Citation2020) from their studies on the largest India General insurance Re (GIC Re).

7. Recommendations and conclusion

This study unveils the factors affecting the profitability of SSA reinsurance companies using triple dimensional factors (macroeconomic, industry-level and firm-specific) which has surpassed the limitations of the only existing two studies (Sidhu and Verma, Citation2017; Mukherjee et al., Citation2020) on factors affecting profitability in reinsurance companies. The uniqueness of this study aside the fact that it is a regional-based dynamic panel study is that it considers reinsurance companies as its sample. Having used ROA as the measure of profitability, it is deduced from this study that the significant factors that affects profitability of SSA reinsurance companies are lagged profitability, gross domestic product, competition (HHI), premium growth, investment performance, underwriting risk, and operational efficiency.

Furthermore, inflation, risk retention ratio and underwriting risk have negative effect on SSA reinsurers’ profitability. While inflation is a systemic factor that is uncontrollable by the company, retention ratio and underwriting risk are internal factors which reflects excessive claim payments, huge managerial expenditures, and overtrading, etc. From the findings, it is recommended that SSA reinsurers should restructure to have separate department that monitors their ceding agreements and underwriting engagements with insurers. This will assist in building risk management structures and adopt a risk-based approach in the supervision of activities. As reinsurers are meant for hedging risk for insurers, adequate risk assessments must be conducted before any commitment is undertaken.

Also, the significance of competition, premium growth, investment performance, and operational efficiency on the profitability of SSA reinsurers informs that the companies should maintain mechanisms such as automated systems that reduces operational costs, increase its business to boost premium growth, come up with many more innovative products to remain highly competitive such that their profitability is sustained to make the forecasted growth in the region realistic.

In conclusion, this study is limited by inability to have a balanced panel. Not all the companies have all the data required for the whole years of study. However, this has not affected the validity and reliability of the findings in any way as adequate technique was used. By identifying the macroeconomic, industry level and firm-specific factors that affects profitability of SSA reinsurers, our findings should offer industry practitioners and regulators important connotations about the determinants of the firm’s profitability.

Further research can extend their study to global reinsurance companies using the same model that encompasses the three-dimensional factors.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

References

- Ahmed, A. (2010). Global financial crisis: an Islamic finance perspective. International Journal of Islamic and Middle Eastern Finance and Management. 3(4), 306–17. https://doi.org/10.1108/17538391011093252

- Akotey, J. O., Sackey, F. G., Amoah, L., & Manso, R. F. (2013). The financial performance of life insurance companies in Ghana. The Journal of Risk Finance, 14(3), 286–302. https://doi.org/10.1108/JRF-11-2012-0081

- Al-Shami, H. A. A., 2013. Determinants of insurance companies’ stock return in GCC countries. [Doctoral dissertation]. Universiti Utara Malaysia.

- AlAli, M. S., Al-Yatama, S. K., AlShamali, N. M., & AlAwadhi, K. M. (2019). The impact of dividend policy on Kuwaiti insurance companies share prices. World Journal of Finance and Investment Research, 4(1), 34–39.

- Alhassan, A. L., Addisson, G. K., & Asamoah, M. E. (2015). Market structure, efficiency and profitability of insurance companies in Ghana. International Journal of Emerging Markets, 10(4), 648–669. https://doi.org/10.1108/IJoEM-06-2014-0173

- Almajali, A. Y., Alamro, S. A., & Al-Soub, Y. Z. (2012). Factors affecting the financial performance of Jordanian insurance companies listed at Amman Stock Exchange. Journal of Management research, 4(2), 266. doi:10.5296/jmr.v4i2.1482.

- Alshammari, A. A., Alhabshi, S. M. B. S. J., & Saiti, B. (2019). The impact of competition on cost efficiency of insurance and takaful sectors: Evidence from GCC markets based on the stochastic frontier analysis. Research in International Business and Finance, 47, 410–427. https://doi.org/10.1016/j.ribaf.2018.09.003

- Anderson, T. W., & Hsiao, C. (1981). Estimation of dynamic models with error components. Journal of the American Statistical Association, 76(375), 598–606. https://doi.org/10.1080/01621459.1981.10477691

- Barnor, C., 2014. The effect of macroeconomic variables on stock market returns in Ghana (2000-2013). [Doctoral dissertation]. Walden University.

- Batool, A., & Sahi, A. (2019). Determinants of financial performance of insurance companies of USA and UK during global financial crisis (2007–2016). International Journal of Accounting Research, 7(1), 1–9. https://d1wqtxts1xzle7.cloudfront.net/80766099/determinants-of-financial-performance-of-insurance-companies-of-usa-and-uk-during-global-financial-crisis-20072016-with-cover-page-v2.pdf?Expires=1656541456&Signature=Ey3DjCFNtNLh9~qugvUsaJ6-KOPMSdQ8q11iIKP6SUjjVa15Cu-0SxIUgbOdNt0YHbXxkh-XfvOdtjfhI6MSs80X--HmQvF7D5ILj-lyk4KK4isWNONzYMR5F2nB1kIKW~CGReU9YRimLZlebRz6faS9DxCCGr7~VQKgNjQ~tEmDtiLhxu6upHV3lq1i-NOER060w2ft6I1EaBIgxMPH88aj6rsNVJ82FVJTjllXD4WSNSodmgPf6ouNBIUHGhdMym6SZFtS160~2MhkseyqCt4T0N-Qc1cV0Pgm~EvsAyPs0HGYP11fOOnbg4miKzf3QN6bKkUQ8DpNBu2yf-kdZg__&Key-Pair-Id=APKAJLOHF5GGSLRBV4ZA

- Berends, K., McMenamin, R., Plestis, T., & Rosen, R. J. (2013). The sensitivity of life insurance firms to interest rate changes. Economic Perspectives, 37(2), 47–78.

- Bertucci, L., 2019. The role of financial institutions: Limits and perspectives. [Doctoral dissertation]. Université Paris sciences et lettres.

- Boadi, E. K., Antwi, S., & Lartey, V. C. (2013). Determinants of profitability of insurance firms in Ghana. International Journal of Business and Social Research (IJBSR), 3(3), 43–50.

- Burca, A. M., & Batrinca, G. (2014). The determinants of financial performance in the Romanian insurance market. International Journal of Academic Research in Accounting, Finance and Management Sciences, 4(1), 299–308.

- Camino-Mogro, S., & Bermúdez-Barrezueta, N. (2019). Determinants of profitability of life and non-life insurance companies: Evidence from Ecuador. International Journal of Emerging Markets, 14(5), 831–872. https://doi.org/10.1108/IJOEM-07-2018-0371

- Carter, R. L., ed. (2013). Vol. Reinsurance Springer Science & Business Media. https://books.google.co.za/books?id=j0nqCAAAQBAJ&lpg=PP9&ots=9Ib4tutbrm&dq=capital%20is%20more%20efficiently%20used%20and%20underwriting%20capacity%20is%20increased%20(Carter%2C%202013).&lr&pg=PP9#v=onepage&q&f=false.

- Charumathi, B. (2012, July). On the determinants of profitability of Indian life insurers–an empirical study. Proceedings of the World Congress on Engineering, 1(2), 4–6. London.

- Chen, Y., & Hamwi, I. S. (2000). Performance analyses of US property-liability reinsurance companies. Journal of Insurance Issues, 140–152. https://www.jstor.org/stable/41946186.

- Demir, F. (2009). Financial liberalization, private investment and portfolio choice: Financialization of real sectors in emerging markets. Journal of Development Economics, 88(2), 314–324. https://doi.org/10.1016/j.jdeveco.2008.04.002

- Derbali, A. M. S. (2014). Determinants of performance of insurance companies in Tunisia: The case of life insurance. International Journal of Innovation and Applied Studies, 6(1), 90–96.

- Egbunike, C. F., & Okerekeoti, C. U. (2018). Macroeconomic factors, firm characteristics and financial performance: A study of selected quoted manufacturing firms in Nigeria. Asian Journal of Accounting Research, 3(2), 142–168. https://doi.org/10.1108/AJAR-09-2018-0029

- Eling, M., & Jia, R. (2019). Efficiency and profitability in the global insurance industry. Pacific-Basin Finance Journal, 57, 101–190. https://doi.org/10.1016/j.pacfin.2019.101190

- Flamini, V., McDonald, C. A., & Schumacher, B. L., 2009. The determinants of commercial bank profitability in Sub-Saharan Africa (January 2009), IMF Working Paper No. 09/15, Available at SSRN: or https://doi.org/10.2139/ssrn.1356442

- Fukase, E. (2010). Revisiting linkages between openness, education and economic growth: System GMM approach. Journal of Economic Integration, 193–222.

- Gujarati, D. N. (1995). Basic econometrics, New York: MacGraw-Hill. Inc. 838p.

- Hardwick, P., & Adams, M. (2002). Firm size and growth in the United Kingdom life insurance industry. Journal of Risk and Insurance. 69(4), 577–593. https://doi.org/10.1111/1539-6975.00038

- Hasan, M., Islam, S. N., & Wahid, A. N. (2018). The effect of macroeconomic variables on the performance of non-life insurance companies in Bangladesh. Indian Economic Review, 53(1–2), 369–383. https://doi.org/10.1007/s41775-019-00037-6

- Heid, B., Langer, J., & Larch, M. (2012). Income and democracy: Evidence from system GMM estimates. Economics Letters, 116(2), 166–169. https://doi.org/10.1016/j.econlet.2012.02.009

- Hsiao, C. (2014). Analysis of panel data (No. 54). Cambridge university press.

- Ismail, N., Ishak, I., Manaf, N. A., & Husin, M. M. (2018). Macroeconomic factors affecting performance of insurance companies in Malaysia. Academy of Accounting and Financial Studies Journal, 22, 1–5. Available: https://www.proquest.com/openview/1c1c6f1359e051bb384216bcaea9819e/1?pq-origsite=gscholar&cbl=29414

- Karadağ Erdemir, Ö. (2019). Selection of financial performance determinants for non-life insurance companies using panel data analysis. Journal of Accounting & Finance, 82, 251–264.

- Kariuki, P., & Nguyo, R. (2020). Firm level factors and organization performance: The moderating role of industry environment. Journal of International Business and Management, 3(3), 01–13.

- Kripa, D., & Ajasllari, D., 2016a. Brexit and its potential impact on the Albanian economy, 13th International Conference of ASECU, Social and Economic Challenges in Europe 2016-2020, 313–324.

- Kripa, D., & Ajasllari, D. (2016b). Factors affecting the profitability of Insurance Companies in Albania. European Journal of Multidisciplinary Studies, 1(1), 352–360. https://doi.org/10.26417/ejms.v1i1.p352-360

- Kutu, A. A., & Ngalawa, H. (2016). Dynamics of industrial production in BRICS countries. International Journal of Economics and Finance Studies, 8(1), 1–25.

- Lee, J. (2009). Does size matter in firm performance? Evidence from US public firms. International Journal of the Economics of Business, 16(2), 189–203. https://doi.org/10.1080/13571510902917400

- Malik, H. (2011). Determinants of insurance companies’ profitability: an analysis of insurance sector of Pakistan. Academic research international, 1(3), 315. http://www.savap.org.pk/journals/ARInt./Vol.1(3)/2011(1.3-32)stop.pdf.

- McKillop, D. D., French, B. Q., Sobiech, A., Wilson, J. O., & Wilson, J. O. S. (2020). Cooperative financial institutions: A review of the literature. International Review of Financial Analysis, 71, 101520. https://doi.org/10.1016/j.irfa.2020.101520

- Milidonis, A., Nishikawa, T., & Shim, J. (2019). CEO inside debt and risk taking: Evidence from property–liability insurance firms. Journal of Risk and Insurance, 86(2), 451–477. https://doi.org/10.1111/jori.12220

- Msomi, T. S. (2022). Factors affecting non-performing loans in commercial banks of selected West African countries. Banks and Bank Systems, 17(1), 1. https://doi.org/10.21511/bbs.17(1).2022.01

- Mukherjee, T., Gorai, P., & Sen, S. S. (2020). Financial performance analysis of GIC Re. Vilakshan-XIMB Journal of Management, 17(½), 181–195. https://doi.org/10.1108/XJM-08-2020-0071

- Murungi, J. (2013). An introduction to African legal philosophy. Lexington Books.

- Ndolo, P. S., 2015. The relationship between operational efficiency and financial performance of firms listed at the Nairobi Securities Exchange. [Doctoral dissertation]. University of Nairobi.

- Njeru, P. W., 2018. Redefining the substantive and procedural protections of most favoured nation clauses in bilateral investment treaties (bits) [Doctoral dissertation]. Strathmore University.

- Olarewaju, O. M., & Msomi, T. S. (2021a). Intellectual capital and financial performance of South African development community’s general insurance companies. Heliyon, 7(4), e06712. https://doi.org/10.1016/j.heliyon.2021.e06712

- Olarewaju, O., & Msomi, T. (2021b). Determinants of insurance penetration in West African countries: A panel auto regressive distributed lag approach. Journal of Risk and Financial Management, 14(8), 350. https://doi.org/10.3390/jrfm14080350

- Öner Kaya, E. (2015). The effects of firm-specific factors on the profitability of non-life insurance companies in Turkey. International Journal of Financial Studies, 3(4), 510–529. https://doi.org/10.3390/ijfs3040510

- Oseni, I. O. (2016). Exchange rate volatility and private consumption in Sub-Saharan African countries: A system-GMM dynamic panel analysis. Future Business Journal, 2(2), 103–115. https://doi.org/10.1016/j.fbj.2016.05.004

- Otambo, T. D., 2016. The effect of macro-economic variables on financial performance of commercial banking sector in Kenya. [Doctoral dissertation]. University of Nairobi.

- Park, S. C., Xie, X., & Rui, P. (2019). The sensitivity of reinsurance demand to counterparty risk: Evidence from the US property–liability insurance industry. Journal of Risk and Insurance, 86(4), 915–946. https://doi.org/10.1111/jori.12244

- Pattitoni, P., Petracci, B., & Spisni, M. (2014). Determinants of profitability in the EU-15 area. Applied Financial Economics, 24(11), 763–775. https://doi.org/10.1080/09603107.2014.904488

- Pervan, M., Pervan, I., & urak, M. (2019). Determinants of firm profitability in the Croatian manufacturing industry: evidence from dynamic panel analysis. Economic research-Ekonomska istraživanja, 32(1), 968–981. https://doi.org/10.1080/1331677X.2019.1583587

- Rajapathirana, R. J., & Hui, Y. (2018). Relationship between innovation capability, innovation type, and firm performance. Journal of Innovation & Knowledge. 3(1), 45–55. https://doi.org/10.1016/j.jik.2017.06.002.

- Roodman, D. (2009). How to do xtabond2: An introduction to difference and system GMM in Stata. The Stata Journal, 9(1), 86–136. https://doi.org/10.1177/1536867X0900900106

- Shim, J. (2017). An investigation of market concentration and financial stability in property–liability insurance industry. Journal of Risk and Insurance, 84(2), 567–597. https://doi.org/10.1111/jori.12091

- Shiu, Y. (2004). Determinants of United Kingdom general insurance company performance. British Actuarial Journal, 10(5), 1079–1110. https://doi.org/10.1017/S1357321700002968

- Sidhu, A. S., & Verma, N. (2017). Unveiling the factors affecting the profitability of reinsurance companies. Management and Labour Studies, 42(3), 190–204. https://doi.org/10.1177/0258042X17720062

- Sinha, P., & Sharma, S. (2016). Determinants of bank profits and its persistence in Indian Banks: A study in a dynamic panel data framework. International Journal of System Assurance Engineering and Management, 7(1), 35–46.

- Suheyli, R., 2015. Determinants of profitability on insurance companies in Ethiopia, Unpublished Master’s Thesis, Addis Ababa University.

- Tegegn, M., Sera, L., & Merra, T. M. (2020). Factors affecting profitability of insurance companies in Ethiopia: Panel evidence. International Journal of Commerce and Finance, 6(1), 1–14.

- Trujillo‐Ponce, A. (2013). What determines the profitability of banks? Evidence from Spain. Accounting & Finance, 53(2), 561–586. https://doi.org/10.1111/j.1467-629X.2011.00466.x

- Tsvetkova, L., Bugaev, Y., Belousova, T., & Zhukova, O. (2021). Factors affecting the performance of insurance companies in Russian Federation. Montenegrin Journal of Economics, 17(1), 209–218. https://doi.org/10.14254/1800-5845/2021.17-1.16

- Weisbart, S. (2018). How insurance drives economic growth. Insurance Information Institute.

- Welnerfelt, B. (1984). A Resource-based View of the Firma. Strategic Management Journal, 5(2), 171–182. https://doi.org/10.1002/smj.4250050207

- Woldegebriel, M. M., 2010. Assessment of the reinsurance business in developing countries: Case of Ethiopia ( Doctoral dissertation).

- Wongchai, A. (2017). The operational efficiency analysis of insurance companies in Thailand. Advanced Science Letters, 23(11), 10632–10635. https://doi.org/10.1166/asl.2017.10118

- Yanase, N., & Limpaphayom, P. (2017). Organization structure and corporate demand for reinsurance: The case of the Japanese Keiretsu. Journal of Risk and Insurance, 84(2), 599–629. https://doi.org/10.1111/jori.12092

- Zainudin, R., Mahdzan, N.S.A, and Leong, E.S. 2018. Firm-specific internal determinants of profitability performance: An exploratory study of selected life insurance firms in Asia. Journal of Asia Business Studies. 12(4): 533–550.