Abstract

This study examined how job satisfaction affected the link between internal audit effectiveness and human capital dimensions in the context of Jordanian commercial banks. In this paper, from the distributed questionnaire copies distributed to internal auditors working in the commercial banks of Jordan, 102 copies were deemed useable. Data obtained was exposed to Partial Least Squares-Structural Equation Modeling (PLS-SEM). Based on the results, education, expertise, and training had a direct, positive, and significant influence on the effectiveness of internal audit, while job satisfaction had an incomplete role as a moderator, as underpinned by the Social Exchange theory. The study enumerates the implications for practice and academics, with the study contributions serving as guidelines for bank managers and literature research. On this basis, the study implications are categorized into two major types, theoretical and practical implications. Accordingly, the first contribution to theory is that social exchange theory adoption to examine the human capital dimensions (education, expertise, and training) and their relationship with internal audit effectiveness. Also, practically, the study findings indicate the strategic importance of internal audit, reminding executives and banks directors to enhance internal audit staff expertise and meet their satisfaction to promote the effectiveness of the internal audit.

PUBLIC INTEREST STATEMENT

This research serves as guidelines for bank managers and literature research. Internal audit effectiveness and its characteristics have become increasingly important to banks. On this basis, the study implications are categorized into two major types: theoretical and practical implications. Accordingly, the first contribution to theory is that social exchange theory adoption to examine the human capital dimensions (education, expertise, and training) and their relationship with internal audit effectiveness. Also, practically, the study findings indicate the strategic importance of internal audit, reminding executives, and banks directors to enhance internal audit staff expertise and meet their satisfaction to promote the effectiveness of the internal audit.

1. Introduction

In the field of auditing, internal audit has become a value-adding service to all organizations, as evidenced in the literature (Al-Twaijri et al., Citation2003, Arena & Azzone, Citation2009; Carcello et al., Citation2020; Mihret et al., Citation2010); and companies have been increasingly focusing on it (Jiang et al., Citation2020), as major corporate governance, risk management, and internal control systems component (Eulerich & Eulerich, Citation2020). According to Carcello et al. (Citation2020), internal auditing contributes to organizational value through the mitigation of risks, owing to its importance in recent years in light of a more extensive role in the risk management function of firms (Alzeban & Gwilliam, Citation2014). The proposed definition established by the Institute of Internal Auditors (IIA) provides a summary of the I.A. activities as assurance and audit services aiming to develop value and enhance the operations of the organization (IIA, 2020). The premise behind the added value of I.A. to organizations stems from the assumption of effective internal audit (Mihret et al., Citation2010), with effectiveness being a major issue for internal audit stakeholders, including internal auditors, customers, board and audit committee, senior management, and external auditors (Endaya & Hanefah, Citation2016). Therefore, the internal audit added value to the organizations and has garnered attention from public organizations in the past several years (Chang et al., Citation2019). As a subsequence, academic works have been focused on the factors affecting internal audit effectiveness (e.g., Drogalas et al., Citation2020; Rudhani et al., Citation2017).

The current business market environment that is characterized by globalization has experienced human capital development that has become a major source of effectiveness achievement. In other words, organizations invest in human capital management and recruitment from a pool of human capital having suitable skill sets and competencies to tackle the ever-changing management paradigms. Human capital evaluation involving knowledge, experience, skills, and suitable knowledge management capabilities are a must for long-lasting value generation (Lahiri & Kedia, Citation2009). In relation to this, Serenko et al. (Citation2007) contended that human capital encapsulates competence of knowledge, capabilities, skills, and experiential knowledge of people, the attitude of people reflected in their behaviour, motivation, and ethical conduct, and their intellectual agility, being encapsulated in their imitation, innovation, and adaptation. Other human capital elements include changeability, creativity, education/training, employee demographics, emotional intelligence, employee loyalty, flexibility, entrepreneurial spirit, individuals’ identity, formal relationships, informal relationships, influencing behaviour, workforce training, vocational qualification, and other aspects that are related to work (Cricelli et al., Citation2014).

In the Jordanian context, an UN-sponsored study showed that the country is a nation having high human capital levels (Bontis, Citation2004), and as such, the government of Jordan needs to leverage its workforce’s full potential by investing in suitable technological infrastructure in order for such human capital to be transformed into a high level of wealth and living standards. This is possible for organizations of all sizes (Serenko et al., Citation2007). Human capital can play a major role in effectiveness when investments in education and training are made and the external labour market is leveraged (Youndt et al., Citation2004). In this regard, the better exploitation of other capitals can be facilitated through a well-developed human capital and thus would lead to an effective internal audit, optimal decision-making, processes, and administrative procedures.

The present paper’s main objective is to examine the relationship between human capital (H.C.) components and internal audit (I.A.) effectiveness in the Jordanian banking sector. The paper also attempts to contribute to empirical evidence on the HC-IA effectiveness-positive relationship, as studies of this caliber are still required (Alawamleh et al., Citation2019; Al-Hawary et al., Citation2020; Alomari, Citation2020; Alqudah et al., Citation2019; Obeidat et al., Citation2018). Lastly, the paper analyses the moderating role of job satisfaction on the relationship between human capital and internal audit, which would provide insight into the variables’ behaviour, strength, and direction.

2. Theory development and hypotheses

The concept of human capital is extensive and covers several components, although its primary concern is to shed light on workforce quality (Tran & Vo, Citation2020). Employees’ identification is human capital, with employees being business investors, remunerated for their human capital and expected returns on what they have invested (Davenport, Citation1999). The human capital concept is underlined by three basic views (Tran & Vo, Citation2020), with the first one being that human capital stems from investment, so its value is invested in improving physical strength, know-how and knowledge and skills-gaining (Schultz, Citation1961), in what is referred to as an investment perspective. In the second view, human capital is perceived as the exclusive knowledge, skills, experience, and working capacity of managers and technical innovators (Weijie & Zhao, Citation2001), and the total value of personal physical strength, knowledge, skills, and intelligence directed towards products creation (Wang et al., Citation2005). The final view considers human capital to be not limited to managers or technical innovators but is human resources, as talents, energy, skills, and knowledge that can be used for goods production or services provision (Micah et al., Citation2012).

Contrastingly, among researchers in the field of accounting and management, the focus is stressed on the employees’ intrinsic values when it comes to human capital definition. For instance, staff competencies were described as top human capital elements by Abeysekera and Guthrie (Citation2004), while training and employee satisfaction was revealed by Bontis and Fitz‐enz (Citation2002) as significantly and positively affecting human capital. Added to this, Tasheva and Hillman (Citation2019) described human capital through a broader term that covers skills, knowledge, abilities, and the awareness of differences throughout different domains. Also, Ulrich (Citation1998) and Bontis et al. (Citation2004) mentioned employees’ commitment, motivation, and attitude as top human capital elements. Similarly, the human capital design included elements like know-how, education, and vocational qualifications of employees and their knowledge and competencies about work, occupational, and psychometric assessments, cultural diversity, models, and frameworks (Lynn, Citation1998). Luthans et al. (Citation2004) mentioned creativity as a significant human capital element, along with personal experience, education, knowledge, and professional skills. Therefore, these elements of training, experience, and education, once thought of as personal skills, characteristics, and attitudes (Hatch & Dyer, Citation2004), have been more linked with the human capital concept, highlighting the need for several indicators for representing the concept.

In the same line of study, Becker (Citation1964) related that knowledge and experience are two major characteristics of the human capital concept. Despite the fact that prior literature, including Owhoso and Weickgenannt (Citation2009), investigated the way human factors like auditors’ self-perceived abilities and Obeid et al. (Citation2017) focused on personality traits and their influence on audit outcomes, knowledge about their relating to human capital role in auditing is still limited. One of the major models of human capital, namely the theory of human capital, developed and proposed by Becker (Citation1964), was an extension of microeconomics to extensive human behaviour, and the author promoted the notion of investing in education and training, akin to purchasing new equipment for the company. Generally speaking, the theory posits that individuals having higher quality human capital will have the ability to achieve more positive results. Hence, in this study, increased human capital is assumed to enhance the effectiveness of the internal audit. Internal auditors with higher human capital are assumed to have higher opportunities for enhanced effectiveness than their counterparts with low human capital.

As a result, internal auditors having higher general human capital should be viewed as valuable in light of their intelligence, skills, and generation of abstract principles from distinct circumstances (Dalziel et al., Citation2011). The learning and knowledge structure types reflected through higher general human capital levels will be more valuable as auditors need to process huge amounts of complex information in a short time, and thus, their effectiveness on the job is brought about by their possession of knowledge structures (Carpenter & Westphal, Citation2001). Also, auditors who participate in activities for their general human capital development are expected to be more capable of interpreting and categorizing information they come across.

In other words, human capital strengthens the effectiveness of auditing and auditors’ education (Dellai & Omri, Citation2016) and their experience (Badara & Saidin, Citation2013, Citation2014; Shamki & Alhajri, Citation2017) can have profound effects on the internal auditors’ effectiveness. In this regard, Pickett and Pickett (Citation2010) revealed the need for internal auditors to have sufficient education and experience for carrying out their duties and fulfilling their responsibilities, while Drogalas et al. (Citation2017) stated that internal audit effectiveness is significantly related to the level of their received suitable training. Also, auditor’s can up their technical competence by regularly providing short-term training with appropriate assessment of needs (Mihret & Yismaw, Citation2007). Of the different human capital dimensions mentioned, education, experience, and training stood out for the effectiveness of internal audit and thus, each dimension’s effect is examined on internal audit effectiveness by testing the following corresponding hypotheses,

H1a: Education has a direct effect on internal audit effectiveness.

H1b: Experience has a direct effect on internal audit effectiveness.

H1c: Training has a direct effect on internal audit effectiveness.

3. Moderating role of job satisfaction

Spector (Citation1997) defined job satisfaction as the level of employees’ liking/disliking his/her job, and according to Isik (2020), it is a top determinant of effectiveness. Job satisfaction constitutes an affective component and a non-affective (cognitive) component (Organ & Konovsky, Citation1989), with the former being the employees’ emotional state and the latter being the satisfaction that the employee associates with the effectiveness. Job satisfaction has become an increasingly researched topic in behavioural accounting, industrial/organizational psychology, social psychology, and organizational behaviour (Obeid et al., Citation2017; Al Shbail et al., Citation2018, Jin et al., Citation2018).

Nevertheless, job satisfaction as a mechanism that facilitates human capital’s influence over audit effectiveness has been largely untouched in the literature, although researchers have indicated that it might have a moderating role in the relationship between the two variables (e.g., Niu, Citation2014; Woo et al., Citation2017). More specifically, a moderating variable refers to an independent variable that influences the direction/strength or both of the relationship between an independent and outcome variable (Bennett, Citation2000). On this basis, it is proposed that improving the satisfaction of internal auditors with human capital can, in turn, enhance their audit work effectiveness, and thus, such examination of job satisfaction’s moderating role can explain the strength and direction of the human capital (independent variable)—internal audit effectiveness (outcome variable) relationship. Accordingly, the following sub-hypotheses were formulated to examine the moderating role of job satisfaction on the relationship between human capital dimensions and internal audit effectiveness,

H2a: Job satisfaction has a moderating effect on the relationship between education and internal audit effectiveness.

H2b: Job satisfaction has a moderating effect on the relationship between experience and internal audit effectiveness.

H2c: Job satisfaction has a moderating effect on the relationship between training and internal audit effectiveness.

4. Method

4.1. Sample and data collection procedure

In the data collection procedure, the target population distinguishes between respondents and non-respondents, and in effect, the specific target population has to be determined during the process of sampling design. The target population essentially constitutes the sample elements that hold the required information, from which inferences can be obtained. A large sample is crucial for generalizing the results of obtained data. The sampling approach adopted was the simple random sample and generally, which assures fair and independent representation of data, as proposed by Hair et al. (Citation2007). the survey data collecting method is predicated on the survey interaction nature and questionnaire administration method.

A cover letter was attached to the survey instrument, within which the purpose and instruction of completing the survey were detailed—copies of the questionnaire were then distributed to 250 internal auditors from Jordanian commercial banks at all levels. In all, 119 internal auditors replied to our survey. Following content analysis, 15 replies were eliminated due to incomplete or missing information. For further statistical analysis, 102 questionnaires were employed, representing a response rate of 40.8%, and because the study intends to measure the effects and generalize information concerning a population, the authors made sure that the response rate was higher than the minimum threshold level for a face-to-face survey. Data collected through the survey was carried out in Amman, Jordan, between April 2021 and June 2021.

4.2. Research measurements

Under this section, the measurement of the three variables (human capital, job satisfaction, and internal audit effectiveness) is discussed using a 7-point Likert scale to rate the items. Internal audit effectiveness was measured by six items adapted from Dellai and Omri (Citation2016) and Pham and And Nguyen (Citation2021), job satisfaction was measured by eight items adopted from Vieira (Citation2005) and auditor’s education, expertise and training (human capital dimensions) were measured by nine items adopted from Skaggs and Youndt (Citation2004) and Sharabati et al. (Citation2010).

4.3. Profile of survey respondents

Most of the respondents (88.4%) were males, while the remaining (11.6%) were female. The majority of them (51.8%) fell between the age range of 36–40 years of age, and most (72.4%) had been working for over 5 years in their companies. Also, most respondents (86.5%) held bachelor’s degrees.

4.4. Common method bias (CMB)

This study ruled out common method bias (CMB) by using Harman’s One Factor Test proposed by Podsakoff and Organ (1986), and based on the results, the highest covariance explained by a single factor was 32.47%, which is lower than the cutoff (50%). Another CBM diagnostic method, known as the PLS Marker Variable technique, involves the inclusion of a variable unrelated to the survey as a marker variable. Based on the results, the correlation between the marker variable and the entire variables is positive and lower than 0.30, indicating a relative lack of correlation between the marker variable and the dependent variable. Next, the market was included as an endogenous variable in the research model for analyzing the new results and comparing them with the baseline findings—insignificant changes in the beta coefficient and coefficient variance were found. Following Alserhan and Shbail (Citation2020), Eldalabeeh et al. (Citation2021), and Shbail and Shbail (Citation2020), the study also tested for multicollinearity among constructs through VIF. Bias is said to exist when the VIF exceeds 3.3 (Kock, 2015). In this study, VIF remained lower than 3.3 among the constructs; thus, the model was deemed CMB-free (refer to ).

Table 1. Construct Reliability and Validity

4.5. Statistical method

Partial Least Squares-Path Modeling (PLS-PM) is a variance-based structural equation modeling technique (Henseler, Ringle, et al., Citation2015, Sarstedt et al., Citation2017), and the present study adopted it as a statistical method to analyze data. The inception of PLS-PM was followed by its extensive use for statistical analyses and promotion among academicians (Alshurafat et al., Citation2021; Rigdon, Citation2016) despite the critical assumptions about the analysis throughout the years (Rönkkö et al., Citation2016). The present study adopted PLS-PM for many reasons, the first being that PLS-PM is a suitable method for prediction-orientated research (Eldalabeeh et al., Citation2021; Shbail & Shbail, Citation2020). Another reason is its apt nature in testing and estimating complex structural construct relationships (direct and moderating relationships; Latan, Citation2018). The third reason is that PLS-PM is suitable to be used even with small-sized sample research lacking normal data distribution (W.W. Chin, Citation1998). Lastly, PLS-PM provides researchers with current data analysis tools like effect size to obtain the relative contribution of every predictor, graphs for moderation analysis and heterotrait-monotrait (HTMT) criteria for the construct discriminant validity assessment (Al Shbail et al., Citation2018, Henseler et al., Citation2015). For the PLS-PM, the study used SmartPLS 3 software recommended by Ringle et al. (Citation2017), which has available computational tools for descriptive statistics (SPSS). Smart PLS was used to analyze data using Hair et al.’s (Citation2019) two-step approach involving the measurement model and structural model in the right order.

4.6. Measurement model

The five measured constructs, namely education, experience and training (human capital dimensions), job satisfaction, and internal audit effectiveness, were assessed in the first stage of the measurement model. This is done by running a confirmatory factor analysis, entailing the estimation of a model containing the five constructs with the saturated structural model. The overall model fit test was accepted (RMS theta = 0.112), and the Standardized Root Mean Square Residual (SRMR) was 0.054, which is lower than 0.08 (cutoff threshold; Hu & Bentler, Citation1999), which means the model has an acceptable fit. The next step involved obtaining the empirical evidence for the operational constructs and establishing indicator and construct reliability, convergent validity and discriminant validity (Eldalabeeh et al., Citation2021).

Specifically, the reliability of individual items can be established by analyzing their standardized loadings (λ) following Sarstedt et al.’s (Citation2017) suggestion, with a loading of more than 0.70 deemed desirable. Regarding the measurement model quality, the constructs items loadings (λ) tabulated in are significant and higher than 0.70. Moving on to construct reliability, composite reliability (C.R.), Cronbach’s alpha (a) and Dijkstra-Henseler’s rhoA (ρA) are all generally employed. Based on current developments, the last analysis is the most consistent form of estimating reliability (Dijkstra & Henseler, Citation2015) and was thus used in this study. The constructs had ρA scores higher than the 0.70 thresholds. Added to this, the C.R., a and rhoA should exceed 0.70 but lower than 0.95, according to Dijkstra and Henseler (Citation2015). AVE values were obtained for convergent validity to calculate the variance amount a construct obtains from its indicators, indicating variance due to a measurement error. In this regard AVE value was higher than 0.50 (AVE>0.50), as evident from the values in , indicating that 50% and over of the construct variance is attributed to its indicators (Ali et al., Citation2018). Overall, sufficient evidence was obtained to support the reliability of constructs. The values obtained established the internal consistency of the measurement model (refer to ).

As for confirmation of discriminant validity, this study used cross-loadings, the Fornell-Larcker criterion (Fornell & Larcker, Citation1981) and the Heterotrait-Monotrait (HTMT) criteria following Henseler et al. (Citation2015). The first step involved the examination of the cross-loadings to assess the discriminant validity of constructs (refer to ). The hypothesized model constructs’ loadings should exceed the loadings on the other constructs for each item surveyed (Hair et al., Citation2019). No cross-loadings were found among the measurement items. In the second step, the AVE square root should be higher than the inter-construct correlations in the correlation matrix, which was the case in this study, indicating the presence of discriminant validity (Fornell & Larcker, Citation1981; refer to ). For a more conservative measure proposed by Henseler et al. (Citation2015), the study also examined discriminant validity using the Heterotrait-Monotrait (HTMT) criteria. HTMT is described as the mean value of the item correlations throughout the constructs in relation to the geometric mean of the average correlations of the items measuring a single construct (Hair et al., Citation2019). Discriminant validity becomes an issue when high HTMT values are obtained—in contrast, this study obtained HTMT values lower than 0.85 (refer to ), establishing the presence of the discriminant validity of variables (Al Shbail et al., Citation2018).

Table 2. Discriminant validity based on cross-loadings criterion

Table 3. Discriminant validity based on Fornell-Larcker criterion

Table 4. Discriminant validity based on HTMT ratio

4.7. Structural model

Following the measurement model’s validity assessment, the study tested the formulated hypotheses using the structural model. In this study, the explained variance (R2) value of the research model was found to be 0.472, which means the model could explain 47.2% of the internal audit effectiveness variance. Aside from R2 values assessment, the study also used effect size (f2) to examine if a certain independent variable substantively impacted a dependent variable. In this regard, Cohen’s (Citation1988) guideline was used to show whether f2 for the hypotheses was acceptable or otherwise (refer to ). Finally, the study used predictive relevance (Q2) value through a blindfolding procedure and cross-validated redundancy method. As per W. W. Chin’s (Citation2010) suggestion, (Q2) value higher than 0 supports the model’s predictive relevance, and based on this, predictive relevance (Q2) was 0.326, and thus, the model has satisfactory predictive relevance.

Table 5. Model predictive capabilities

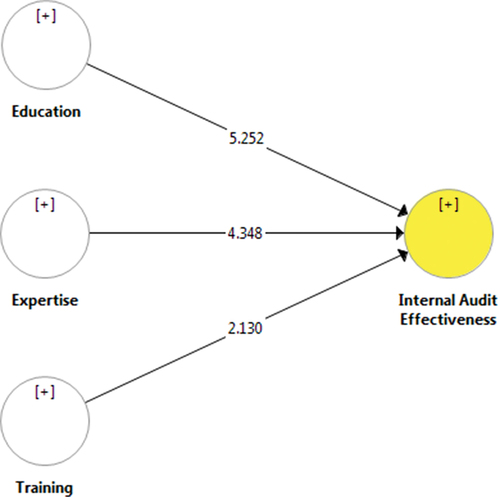

The study assessed the standardized path coefficients using a full bootstrapping procedure with 5000 replicate samples. The hypotheses results are tabulated in , where it is evident that education, expertise, and training all had positive and significant effects on audit effectiveness (β 0.364, t-value 5.252, p < 0.01, β 0.304, t-value 4.348, p < 0.01 and β 0.122, t-value 2.130, p < 0.05, respectively), which means, H1a, H1b, and H1c are all supported. The structural model analysis results are shown in and .

Figure 1. Coefficient significance test without moderator variable.

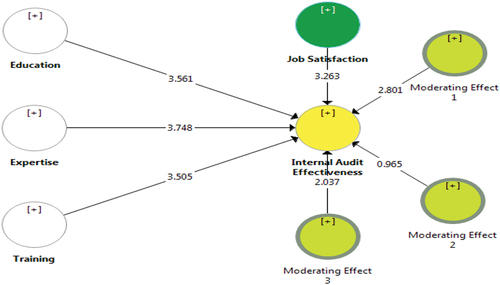

H2a: job satisfaction moderates the relationship between education and internal audit effectiveness (moderating effect 1: t-value = 2.801). The H2b: job satisfaction moderates the relationship between expertise and internal audit effectiveness (moderating effect 2: t-value = 0.965) it was not supported. H2c: training moderates the relationship between job satisfaction and internal audit effectiveness (moderating effect 3: t-value 2.037). It was also approved by statistical outcomes. The results of the T-tests are shown in . The given results indicate that hypotheses are acceptable at 95 and 99% significance levels. Hence, all hypotheses are supported except for H2b. As it is characterized in , the significance coefficient for the moderator variable of job satisfaction is greater than the designated value of 1.96. In other words, it can be confirmed at confidence levels of 95 and 99% that job satisfaction moderates the relationship between human capital and internal audit effectiveness. The results of the t-test and path coefficients are given in .

Figure 2. Coefficient significance test with moderator variable.

Table 6. PLS-SEM analysis of research model

Aligned with the study’s prediction, the study hypotheses were generally supported. The study results show that five of the six formulated hypotheses were supported. Also, the chapter provided evidence that supported the proposed model’s goodness of fit.

5. Conclusions

This study examined the moderating role of job satisfaction on the human capital dimensions-internal audit effectiveness, and the findings supported the hypothesized relationships. The study also theoretically validated the relationship of human capital and internal audit effectiveness with construct dimensions and constructs. Using structural equation modelling, this validation was obtained with 102 internal auditors’ inputs. The model revealed that these internal auditors focus on specific items of human capital and internal audit effectiveness to strategically enable a strong relationship between them. Based on the results, education, expertise, and training positively and directly influenced audit effectiveness, and that job satisfaction had no moderating effect on the relationship between expertise and internal audit effectiveness despite its direct effect on the latter. Similar to studies of its caliber, it has managerial implications, academic implications, limitations and recommendations for future research.

6. Contributions, limitations, and suggestions for future studies

Under this section, the study enumerates the implications for practice and academics, with the study contributions serving as guidelines for bank managers and literature research. In Jordan, internal audit effectiveness and its characteristics have become increasingly important to banks. On this basis, the study implications are categorized into two major types, theoretical and practical implications. Accordingly, the first contribution to theory is that social exchange theory adoption to examine the human capital dimensions (education, expertise, and training) and their relationship with internal audit effectiveness. The study used a questionnaire with contents based on the review of the literature. Owing to the limitation in studies concerning factors that drive the effectiveness of internal audits, there is a need for further empirical studies to explore the relationship deeper (Turetken et al., Citation2019). Aside from the factors examined in this study, the literature also mentions investigating other factors, including bank size and bank type (Islamic or commercial). It is also suggested that future studies examine potential influencing factors in theory. Also, practically, the study findings indicate the strategic importance of internal audit, reminding executives and banks directors to enhance internal audit staff expertise and meet their satisfaction to promote the effectiveness of the internal audit.

References

- Abeysekera, I., & Guthrie, J. (2004). Human capital reporting in a developing nation. The British Accounting Review, 36(3), 251–15. https://doi.org/10.1016/j.bar.2004.03.004

- Al Shbail, M. O., Salleh, Z., & Nor, M. N. M. (2018). The effect of ethical tension and time pressure on job burnout and premature sign-off. Journal of Business and Retail Management Research, 12(4), 43–53. https://doi.org/10.24052/JBRMR/V12IS04/ART-05

- Al-Hawary, S. I. S., Mohammad, A. S., Al-Syasneh, M. S., Qandah, M. S. F., & Alhajri, T. M. S. (2020). Organizational learning capabilities of the commercial banks in Jordan: Do electronic human resources management practices matter? International Journal of Learning and Intellectual Capital, 17(3), 242–266. https://doi.org/10.1504/IJLIC.2020.109927

- Al-Twaijry, A. A., Brierley, J. A., & Gwilliam, D. R. (2003). The development of internal audit in Saudi Arabia: An institutional theory perspective. Critical Perspectives on Accounting, 14(5), 507–531. https://doi.org/10.1016/S1045-2354(02)00158-2

- Alawamleh, M., Ismail, L. B., Aqeel, D., & Alawamleh, K. J. (2019). The bilateral relationship between human capital investment and innovation in Jordan. Journal of Innovation and Entrepreneurship, 8(1), 1–17. https://doi.org/10.1186/s13731-019-0101-3

- Ali, F., Rasoolimanesh, S. M., Sarstedt, M., Ringle, C. M., & Ryu, K. (2018). An assessment of the use of partial least squares structural equation modeling (PLS-SEM) in hospitality research. International Journal of Contemporary Hospitality Management, 301. https://doi.org/10.1108/IJCHM-10-2016-0568

- Alomari, Z. (2020). Does human capital moderate the relationship between strategic thinking and strategic human resource management? Management Science Letters, 10(3), 565–574. https://doi.org/10.5267/j.msl.2019.9.024

- Alqudah, H. M., Amran, N. A., & Hassan, H. (2019). Factors affecting the internal auditors’ effectiveness in the Jordanian public sector. EuroMed Journal of Business, 14(3), 251–273. https://doi.org/10.1108/EMJB-03-2019-0049

- Alserhan, H., & Shbail, M. (2020). The role of organizational commitment in the relationship between human resource management practices and competitive advantage in Jordanian private universities. Management Science Letters, 10(16), 3757–3766. https://doi.org/10.5267/j.msl.2020.7.036

- Alshurafat, H., Al Shbail, M. O., Masadeh, W. M., Dahmash, F., & Al-Msiedeen, J. M. (2021). Factors affecting online accounting education during the COVID-19 pandemic: An integrated perspective of social capital theory, the theory of reasoned action and the technology acceptance model. Education and Information Technologies, 1–19. https://doi.org/10.1007/s10639-021-10550-y

- Alzeban, A., & Gwilliam, D. (2014). Factors affecting the internal audit effectiveness: A survey of the Saudi public sector. Journal of International Accounting, Auditing and Taxation, 23(2), 74–86. https://doi.org/10.1016/j.intaccaudtax.2014.06.001

- Arena, M., & Azzone, G. (2009). Identifying organizational drivers of internal audit effectiveness. International Journal of Auditing, 13(1), 43–60. https://doi.org/10.1111/j.1099-1123.2008.00392.x

- Badara, M. A. S., & Saidin, S. Z. (2013). The relationship between audit experience and internal audit effectiveness in the public sector organizations. International Journal of Academic Research in Accounting, Finance and Management Sciences, 3(3), 329–339. https://doi.org/10.6007/IJARAFMS/v3-i3/224

- Badara, M. A. S., & Saidin, S. Z. (2014). Internal audit effectiveness: Data screening and preliminary analysis. Asian Social Science, 10(10), 76–85.

- Becker, G. S. (1964). Human capital theory. Columbia, New York.

- Bennett, J. A. (2000). Mediator and moderator variables in nursing research: Conceptual and statistical differences. Research in Nursing & Health, 23(5), 415–420. https://doi.org/10.1002/1098-240X(200010)23:5<415::AID-NUR8>3.0.CO;2-H

- Bontis, N. (2004). National intellectual capital index: The benchmarking of Arab countries. Journal of Intellectual Capital, 5(1), 13–39. https://doi.org/10.1108/14691930410512905

- Bontis, N. (2012). National intellectual capital index: The benchmarking of Arab countries. In Intellectual capital for communities (pp. 124–149). Routledge.

- Bontis, N., & Fitz‐enz, J. (2002). Intellectual capital ROI: A causal map of human capital antecedents and consequents. Journal of Intellectual Capital, 3(3), 223–247. https://doi.org/10.1108/14691930210435589

- Carcello, J. V., Eulerich, M., Masli, A., & Wood, D. A. (2020). Are internal audits associated with reductions in perceived risk? Auditing: A Journal of Practice & Theory, 39(3), 55–73. https://doi.org/10.2308/ajpt-19-036

- Carpenter, M. A., & Westphal, J. D. (2001). The strategic context of external network ties: Examining the impact of director appointments on board involvement in strategic decision making. Academy of Management Journal, 44(4), 639–660. https://doi.org/10.5465/3069408

- Chang, Y. T., Chen, H., Cheng, R. K., & Chi, W. (2019). The impact of internal audit attributes on the effectiveness of internal control over operations and compliance. Journal of Contemporary Accounting & Economics, 15(1), 1–19. https://doi.org/10.1016/j.jcae.2018.11.002

- Chin, W. W. (1998). The partial least squares approach to structural equation modeling. Modern Methods for Business Research, 295(2), 295–336. https://books.google.jo/books?hl=en&lr=&id=EDZ5AgAAQBAJ&oi=fnd&pg=PA295&dq=The+partial+least+squares+approach+to+structural+equation+modeling.+Modern+Methods+for+Business+Research&ots=49vB3pv-go&sig=WK_apYiFpF47j0mTS7bCpfxM8R4&redir_esc=y#v=onepage&q=The%20partial%20least%20squares%20approach%20to%20structural%20equation%20modeling.%20Modern%20Methods%20for%20Business%20Research&f=false

- Chin, W. W. (2010). How to write up and report PLS analyses. In V. E, W. W. Chin, J. Henseler, & H. Wang (Eds.), Handbook of partial least squares (pp. 655–690). Springer.

- Cohen, J. (1988). Statistical power analysis for the social sciences.

- Cricelli, L., Greco, M., & Grimaldi, M. (2014). An overall index of intellectual capital. Management Research Review, 37 (10), 880–901. Management Research Review. https://doi.org/10.1108/MRR-04-2013-0088

- Dalziel, T., Gentry, R. J., & Bowerman, M. (2011). An integrated agency–resource dependence view of the influence of directors’ human and relational capital on firms’ R&D spending. Journal of Management Studies, 48(6), 1217–1242. https://doi.org/10.1111/j.1467-6486.2010.01003.x

- Davenport, T. O. (1999). Human capital. Management Review, 88(11), 37.

- Dellai, H., & Omri, M. A. B. (2016). Factors affecting the internal audit effectiveness in Tunisian organizations. Research Journal of Finance and Accounting, 7(16), 208–211.

- Dijkstra, T. K., & Henseler, J. (2015). Consistent partial least squares path modeling. MIS Quarterly, 39(2), 297–316. https://doi.org/10.25300/MISQ/2015/39.2.02

- Drogalas, G., Pazarskis, M., Anagnostopoulou, E., & Papachristou, A. (2017). The effect of internal audit effectiveness, auditor responsibility and training in fraud detection. Accounting and Management Information Systems, 16(4), 434–454. https://doi.org/10.24818/jamis.2017.04001

- Drogalas, G., Petridis, K., Petridis, N. E., & Zografidou, E. (2020). Valuation of the internal audit mechanisms in the decision support department of the local government organizations using mathematical programming. Annals of Operations Research, 294(1–2), 267–280. https://doi.org/10.1007/s10479-020-03537-4

- Eldalabeeh, A. R., Obeid Al-Shbail, M., Almuiet, M. Z., Baker, M. B., & E’leimat, D. (2021). Cloud-based accounting adoption in jordanian financial sector. The Journal of Asian Finance, Economics, and Business, 8(2), 833–849.

- Endaya, K. A., & Hanefah, M. M. (2016). Internal auditor characteristics, internal audit effectiveness, and moderating effect of senior management. Journal of Economic and Administrative Sciences, 32(2), 160–176. https://doi.org/10.1108/JEAS-07-2015-0023

- Eulerich, A. K., & Eulerich, M. (2020). What is the value of internal auditing?–A literature review on qualitative and quantitative perspectives A literature review on qualitative and quantitative Perspectives. Maandblad Voor Accountancy En Bedrijfseconomie, 94(3/4), 83–92. (April 22, 2020). https://doi.org/10.5117/mab.94.50375

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Hair, J., Money, A. H., Samouel, P., & Page, M. (2007). Research methods for business. Education & Training, 49(4), 336–337. https://doi.org/10.1108/et.2007.49.4.336.2

- Hair, J., Risher, J. J., Sarstedt, M., & Ringle, C. M., 2019. When to use and how to report the results of PLS-SEM. European business review, 31(1), 2–24. https://doi.org/10.1108/EBR-11-2018-0203

- Hatch, N. W., & Dyer, J. H. (2004). Human capital and learning as a source of sustainable competitive advantage. Strategic Management Journal, 25(12), 1155–1178. https://doi.org/10.1002/smj.421

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135.

- Hu, L. T., & Bentler, P. M. (1999). Cut-off criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling: a Multidisciplinary Journal, 6(1), 1–55. https://doi.org/10.1080/10705519909540118

- Jiang, L., Messier, W. F.,sJr, & Wood, D. A. (2020). The association between internal audit operations-related services and firm operating performance. Auditing: A Journal of Practice & Theory, 39(1), 101–124. https://doi.org/10.2308/ajpt-52565

- Jin, M. H., McDonald, B., & Park, J. (2018). Person–organization fit and turnover intention: Exploring the mediating role of employee followership and job satisfaction through conservation of resources theory. Review of Public Personnel Administration, 38(2), 167–192. https://doi.org/10.1177/0734371X16658334

- Lahiri, S., & Kedia, B. L. (2009). The effects of internal resources and partnership quality on firm performance: An examination of Indian BPO providers. Journal of International Management, 15(2), 209–224. https://doi.org/10.1016/j.intman.2008.09.002

- Latan, H. (2018). PLS path modeling in hospitality and tourism research: The golden age and days of future past. In F. Ali, S. M. Rasoolimanesh, and C. Cobanoglu (Eds.), Applying Partial Least Squares in Tourism and Hospitality Research. https://doi.org/10.1108/978-1-78756-699-620181004

- Luthans, F., Luthans, K. W., & Luthans, B. C. (2004). Positive psychological capital: Beyond human and social capital. Business Horizons, 47(1), 45–50. https://doi.org/10.1016/j.bushor.2003.11.007

- Lynn, B. E. (1998). The management of intellectual capital: The issues and the practice. Society of Management Accountants.

- Micah, L. C., Ofurum, C. O., & Ihendinihu, J. U. (2012). Firms financial performance and human resource accounting disclosure in Nigeria. International Journal of Business and Management, 7(14), 67. https://doi.org/10.5539/ijbm.v7n14p67

- Mihret, D. G., James, K., & Mula, J. M. (2010). Antecedents and organizational performance implications of internal audit effectiveness: Some propositions and research agenda. Pacific Accounting Review, 22(3), 224–252. https://doi.org/10.1108/01140581011091684

- Mihret, D. G., & Yismaw, A. W. (2007). Internal audit effectiveness: An Ethiopian public sector case study. Managerial auditing journal, 22(5), 470–484. https://doi.org/10.1108/02686900710750757

- Niu, H. J. (2014). Is innovation behavior congenital? Enhancing job satisfaction as a moderator. Personnel Review, 43 (2), 288–302. Personnel Review. https://doi.org/10.1108/PR-12-2012-0200

- Obeid, M., Salleh, Z., & Nor, M. N. M. (2017). The mediating effect of job satisfaction on the relationship between personality traits and premature sign-off. Academy of Accounting and Financial Studies Journal, 21(2), 1–17.

- Obeidat, A. M., Abualoush, S. H., Irtaimeh, H. J., Khaddam, A. A., & Bataineh, K. A. (2018). The role of organizational culture in enhancing the human capital applied study on the social security corporation. International Journal of Learning and Intellectual Capital, 15(3), 258–276. https://doi.org/10.1504/IJLIC.2018.094718

- Organ, D. W., & Konovsky, M. (1989). Cognitive versus affective determinants of organizational citizenship behavior. Journal of Applied Psychology, 74(1), 157. https://doi.org/10.1037/0021-9010.74.1.157

- Owhoso, V., & Weickgenannt, A. (2009). Auditors’ self-perceived abilities in conducting domain audits. Critical Perspectives on Accounting, 20(1), 3–21. https://doi.org/10.1016/j.cpa.2007.04.005

- Pham, D. C., & And Nguyen, T. T. (2021). Factors affecting the internal audit effectiveness of steel enterprises in Vietnam. The Journal of Asian Finance, Economics, and Business, 8(1), 271–283.

- Pickett, K. S., & Pickett, J. M. (2010). The internal auditing handbook. Wiley Online Library.

- Rigdon, E. E. (2016). Choosing PLS path modeling as analytical method in European management research: A realist perspective. European Management Journal, 34(6), 598–605. https://doi.org/10.1016/j.emj.2016.05.006

- Ringle, C. M., Wende, S., & Becker, J. M. (2017). Handbook of Market Research. https://doi.org/10.1007/978-3-319-05542-8

- Rönkkö, M., McIntosh, C. N., Antonakis, J., & Edwards, J. R. (2016). Partial least squares path modeling: Time for some serious second thoughts. Journal of Operations Management, 47-48(1), 9–27. https://doi.org/10.1016/j.jom.2016.05.002

- Rudhani, L. H., Vokshi, N. B., & Hashani, S. (2017). Factors contributing to the effectiveness of internal audit: Case study of internal audit in the public sector in Kosovo. https://www.um.edu.mt/library/oar//handle/123456789/27336

- Sarstedt, M., Ringle, C. M., & Hair, J. F. (2017). Partial least squares structural equation modeling. Handbook of Market Research, 26(1), 1–40.

- Schultz, T. W. (1961). Investment in human capital. The American Economic Review, 51(1), 1–17.

- Serenko, A., Bontis, N., & Hardie, T. (2007). Organizational size and knowledge flow: A proposed theoretical link. Journal of Intellectual Capital, 8(4), 610–627. https://doi.org/10.1108/14691930710830783

- Shamki, D., & Alhajri, T. A. (2017). Factors influence internal audit effectiveness. International Journal of Business and Management, 12(10), 143–154. https://doi.org/10.5539/ijbm.v12n10p143

- Sharabati, A. A. A., Jawad, S. N., & Bontis, N. (2010). Intellectual capital and business performance in the pharmaceutical sector of Jordan. Management Decision, 48 (1), 105–131. Management decision. https://doi.org/10.1108/00251741011014481

- Shbail, M., & Shbail, A. (2020). Organizational climate, organizational citizenship behaviour and turnover intention: Evidence from Jordan. Management Science Letters, 10(16), 3749–3756. https://doi.org/10.5267/j.msl.2020.7.037

- Skaggs, B. C., & Youndt, M. (2004). Strategic positioning, human capital, and performance in service organizations: A customer interaction approach. Strategic Management Journal, 25(1), 85–99. https://doi.org/10.1002/smj.365

- Sl Shbail, M., Salleh, Z., & Mohd Nor, N. N. (2018). Antecedents of burnout and its relationship to internal audit quality. Business and Economic Horizons (BEH), 14 (1232–2019–871), 789–817. http://dx.doi.org/10.22004/ag.econ.287230

- Spector, P. E. (1997). Job satisfaction: Application, assessment, causes, and consequences (Vol. 3). Sage.

- Tasheva, S., & Hillman, A. J. (2019). Integrating diversity at different levels: Multilevel human capital, social capital, and demographic diversity and their implications for team effectiveness. Academy of Management Review, 44(4), 746–765. https://doi.org/10.5465/amr.2015.0396

- Tovstiga, G., & Tulugurova, E. (2007). Intellectual capital practices and performance in Russian enterprises. Journal of Intellectual Capital, 8(4), 695–707. https://doi.org/10.1108/14691930710830846

- Tran, N. P., & Vo, D. H. (2020). Human capital efficiency and firm performance across sectors in an emerging market. Cogent Business & Management, 7(1), 1738832. https://doi.org/10.1080/23311975.2020.1738832

- Turetken, O., Jethefer, S., & Ozkan, B. (2019). Internal audit effectiveness: Operationalization and influencing factors. Managerial Auditing Journal, 35(2), 238–271. https://doi.org/10.1108/MAJ-08-2018-1980

- Ulrich, D. (1998). A new mandate for human resources. Harvard Business Review, 76(1), 124–135.

- Vieira, J. A. C. (2005). Skill mismatches and job satisfaction. Economics Letters, 89(1), 39–47. https://doi.org/10.1016/j.econlet.2005.05.009

- Wang, X., Xu, C., & Zhao, Z. (2005). Study on the human capital accounting based on the enterprise co-governance logic by human capital and physical capital. Accounting Research, 8(1), 72–76.

- Weijie, Z., & Zhao, J. (2001). Consider about the human capital as enterprise system factor. Theory Front, 10(1), 3–4.

- Woo, H., Park, S., & Kim, H. (2017). Job satisfaction as a moderator on the relationship between burnout and scholarly productivity among counseling faculty in the U.S. Asia Pacific Education Review, 18(4), 573–583. https://doi.org/10.1007/s12564-017-9506-5

- Wu, A. (2005). The integration between balanced scorecard and intellectual capital. Journal of Intellectual Capital, 6(2), 267–284. https://doi.org/10.1108/14691930510592843

- Youndt, M. A., Subramaniam, M., & Snell, S. A. (2004). Intellectual capital profiles: An examination of investments and returns. Journal of Management Studies, 41(2), 335–361. https://doi.org/10.1111/j.1467-6486.2004.00435.x

Disclosure statement

The authors report there are no competing interests to declare

Additional information

Funding

Notes on contributors

Mohannad Obeid Al Shbail

Mohannad Obeid Al Shbail is an assistant professor in the accounting department at Al al-Bayt University. His interests include behavioural accounting, auditing, AIS, and forensic accounting. He has research papers published in journals indexed under the data source Scopus.

Hashem Alshurafat

Hashem Alshurafat an assistant professor in the accounting department at Al al-Bayt University. His interests include behavioural accounting, auditing, AIS, and forensic accounting. He has research papers published in journals indexed under the data source Scopus.

Husam Ananzeh

Husam Ananzeh assistant professor in the accounting department at Al al-Bayt University. His interests include behavioural accounting, auditing, AIS, and forensic accounting. He has research papers published in journals indexed under the data source Scopus.

Tareq O Bani-Khalid

Tareq O Bani-Khalid Assistant professor in the accounting department at Al al-Bayt University. His interests include behavioural accounting, auditing, AIS, and forensic accounting. He has research papers published in journals indexed under the data source Scopus.