?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The study evaluates the influence of cash flow on the financial distress of private listed enterprises on the Vietnamese stock market from 2010 to 2020. We use the data collected from the financial statements of 263 private non-financial enterprises listed on the Ho Chi Minh and Hanoi stock exchanges from 2010 to 2020 in the FinPro database. The quantile regression method was employed to analyze the effect of cash flow on the financial distress of listed non-financial private enterprises. The results show that the cash flow from operating activities and the cash flow from financial activities have negative relationships with financial distress. However, the cash flow from investing activities has a positive relationship. Based on experimental results, the study proposes some recommendations on cash flow forecasting, building an optimal budget model to help business managers have appropriate cash flow management policies to reduce the risk of financial distress.

PUBLIC INTEREST STATEMENT

The study evaluates the influence of cash flow on the financial distress of private listed enterprises on the Vietnamese stock market from 2010 to 2020. The results show that the cash flow from operating activities and the cash flow from financial activities have negative relationships with financial distress. However, the cash flow from investing activities has a positive relationship. Based on experimental results, the study proposes some recommendations on cash flow forecasting, building an optimal budget model to help business managers have appropriate cash flow management policies to reduce the risk of financial distress.

1. Introduction

Financial distress is more common in today’s competitive environment (Kamaluddin et al., Citation2019). Firms experiencing financial distress may face difficulties such as non-continuation of financing by creditors, delays in viable projects, or possible bankruptcy (Arnold, Citation2013; Khaliq et al., Citation2014). Therefore, studying financial hardship is critical.

Many researchers approved the relationship between cash flow and financial distress (Murty & Misra, Citation2004; Rodgers, Citation2011; Ward, Citation1994; Yap et al., Citation2012). Revenue and profit are necessary, but cash flow is more important to a business (Schellenger & Cross, Citation1994). Cash flows provide essential information to identify cash-generation ability, the quality of net profits, investment trends as well as the need to mobilize external funding sources, debt repayment capacity, the ability to divide the interest to the owners, the ability to self-finance, and many other financial issues (Horne & Wachowicz, Citation2008). The cash flow statement makes it easy to compare the operating aspects of enterprises’ financial information. Furthermore, it cannot be significantly manipulated under management’s diverse decisions about homogenous transactions.

The private sector plays a prominent role in driving the market forward and sustaining the momentum of reform. In Vietnam, the private sector has been a necessary driving force for national innovation and development (Jaax, Citation2020). By 2021, this sector contributed over 40% of GDP, 30% of the state budget, and attracted about 85% of Vietnam’s labor force.Footnote1 However, the development quality of this sector still has some limitations. Many private enterprises in developing countries face common difficulties such as accessibility to technology, poor management, slow productivity growth, and low conversion rate (Kokko & Thang, Citation2014). The productivity growth rate of the private sector is still low, only equal to 34% of the labor productivity of the state-owned enterprises, and about 69% of the labor productivity of the foreign-invested sector.Footnote2

In the context of rapidly escalating Covid-19 outbreaks, the resilience of businesses in general and the private sector, in particular, are increasingly declining. The cash flow of Vietnamese enterprises is seriously short. That led to financial difficulties for private enterprises and partly leads to private enterprises facing financial distress. Therefore, studying the effect of cash flow on the financial distress of private enterprises listed on the Vietnamese stock market is a topic interested by both scientists and administrators in the situation of businesses heavily affected by the Covid-19 pandemic.

2. Literature review

2.1. Theoretical basis

Trade-off theory. According to the theory, a company must consider the trade-off between the benefits of tax savings and the risk of financial distress when it makes debt decisions. If it maintains a low level of debt utilization and the risk of financial distress is not significant, the company value will increase because of the contribution of tax savings. In that case, its value will continue to rise accompanied by an increase in debt use. If the cost of financial distress becomes substantial and outweighs the contribution of tax savings from interest, the company value will decrease accompanied by an increase in debt use (Arnold, Citation2013; Brealey et al., Citation2008).

Signaling theory. The theory explains that encouraging companies provide information as positive signals to external parties. It is because information can be an essential factor for investors and traders. Information of all forms as notes or descriptions of past, present, or future conditions is valuable. Based on signal theory, Utami (Citation2016) indicated that a high value of a company’s cash flows over a long period can be a positive signal of its ability to pay its debts. Conversely, if the cash flow value is too small, even long-term loss, it is a negative signal. In that case, creditors will be doubtful about the company’s ability to repay its debts. Creditors will no longer entrust their credit because the company is considered to be in financial trouble or financial distress.

Liquid asset theory. According to the theory, it is predicted to enter bankruptcy of a company whenever the current year’s profit or net cash flow is negative or lowers its debt service level. One reason is a company with positive cash flows can raise capital and borrow from capital markets. In contrast, other companies with negative or insufficient cash inflows cannot borrow from capital markets (Isayas & McMillan, Citation2021). As a result, they are in a state of technical insolvency. Technical insolvency exists when a company can not meet its current financial obligations, presenting a lack of liquidity (Altman & Hotchkiss, Citation2006).

Cash management theory. Based on the theory, accurately predicting cash flows is challenging, and there is no perfect similarity between cash inflows and outflows. An imbalance between cash inflows and outflows will be a signal of a failure in a company’s cash management function, which can ultimately cause financial distress for the company (Aziz & Dar, Citation2006).

2.2. Cash flow and financial distress

The first studies on financial distress were reported by Beaver (Citation1966) and Edward (Citation1968), creating the basis for the development of probabilistic predictive models by Martin (Citation1977), Ohlson (Citation1980), Zavgren (Citation1985), and Lau (Citation1987). Researchers have different definitions of financial distress. Financial distress is the dynamic process of corporate failure when an enterprise has difficulty in fulfilling its commitments to creditors or is unable to do so (Fawzi et al., Citation2015; Le Maux & Morin, Citation2011). Financial distress occurs when a company has negative cash flows from operating, investing, and financing activities (Jantadej, Citation2006), and defaults on debt due to insufficient cash flow (Le Maux & Morin, Citation2011). When a business suffers financial distress, it begins to liquidate its assets, operates under the protection of the Court (Foster & Ward, Citation1997), and possibly file for bankruptcy (Bae, Citation2012; Grice & Dugan, Citation2001; Hossain et al., Citation2018; Khaliq et al., Citation2014).

Businesses are in financial distress if they face serious cash flow problems (Fawzi et al., Citation2015; Jooste, Citation2007). In the financial reporting system, three segments of cash flows represent different aspects of cash generation, investment trends, and external financing. These are operating cash flow, investing cash flow, and financing operating cash flow. Financial distress is identified by operating cash flow in deficit, cash flows from investing and financing activities in surplus, or operating and financing cash flows negative, but cash flow from investing activities positive (Kordestani et al., Citation2011). By empirical research based on data selected companies from Istanbul Stock Exchange, Sayari and Mugan (Citation2013) demonstrated that operating cash flow has a negative relationship with the financial distress index, in contrast, cash flow from financing activities has a positive relationship. Besides that, the cash flow from investing activities is not statistically significant. Operating cash flow is the basis for determining a company’s financial health (Gentry et al., Citation1990). If a company’s operating cash flow increases, its financial and credit health, potentially reducing credit risk. Net operating asset growth and change in asset turnover have a significant influence on explaining future profitability (Dickinson, Citation2011; Jooste, Citation2007; Kordestani et al., Citation2011; Sayari & Mugan, Citation2013).

Empirical research by Shamsudin and Kamaluddin (Citation2015) examined eight cash flow patterns as an alternative to predict financial distress. The cash flow patterns derived from positive and negative signs of cash flow components consist of operating, investing, and financing activities. The study results confirmed that two types of cash flow patterns explain financial distress in severity. First, the operating cash flow is surplus, and cash flows from investing and financing activities are in deficit. Second, the cash flows from operating, investing, and financing activities are in deficit. Besides, the operating and investing cash flows are both surpluses while financing cash flow is deficit, or operating and financing cash flows surplus while investing cash flow deficit, which also explain the financial distress of enterprises.

In the current state of the art of financial distress, accounting-based models and structural models are superior (Karas & Režňáková, Citation2020). The structural model approach requires data from capital markets, so its application will be limited to apply to some private enterprises or an underdeveloped capital market. Therefore, with a sample of 4350 small and medium enterprises in the Czech Republic, Karas and Režňáková (Citation2020) used the accounting-based distress model and incorporated the relationship between cash flows and financial distress. From a theoretical point of view, there is a strong connection between lack of cash flows and business difficulties. The authors concluded that financial distress occurs when there is a shortage of cash flows. And, cash flow indicators are easily affected by the earnings management behavior of the business. Cash flow from operating activities plays a crucial role in the risk of corporate financial distress, especially when considering the relationship between cash flow fluctuations and short-term debt. The results of the sample analysis also confirmed those points of view.

Research results of Romadhina et al. (Citation2022) show that cash flow from operating activities is significant against financial distress. The higher the company’s cash flow, the more its business continuity can be ensured. If the company has low operating cash flows, creditors will doubt whether that company can pay its current obligations.

The study to determine the relationship between cash flow and financial distress of manufacturing firms in Malaysia (CitationRoslan et al.,) shows that operating cash flow is a significant factor in the financial distress of manufacturing companies in Malaysia. Financial cash flow has a negative relationship with financial distress. However, with a sample of 84 delisted firms for a period between the years from 2001 to 2014, cash flow from investing and financing activities is not important in determining financial distress in Malaysia.

Enterprise size is a factor affecting the financial distress of a business. Small sized enterprises are more susceptible to financial difficulties than large sized enterprises. It is explained by their poor market experience, limited connectivity, and limited financial resources (Freixas et al., Citation2000; Honjo, Citation2000). It is the most fundamental determinant use of public debt of a business (Denis & Mihov, Citation2003; Isayas & McMillan, Citation2021). However, the study by Kamaluddin et al. (Citation2019) based on 150 data from the consumer and industrial product firms listed on Bursa Malaysia concluded that there is no relationship between firm size and the level of financial difficulties.

Financial leverage has a negative relation to financial distress (Kristanti et al., Citation2016). Companies with financial difficulties often have to take on large amounts of debt. When a company borrows money, it promises to make a series of interest payments and repay the money it borrowed. Therefore, corporate financial difficulties will increase when there is an increase in financial leverage (Gathecha, Citation2016; Isayas & McMillan, Citation2021).

Research on the influence of cash flow fluctuations on corporate financial distress in Vietnam has been studied recently. Research by Nguyen (Citation2020) examined the impact of cash flow fluctuations on the capital structure of listed companies. The test results show there is a negative relationship between cash flow volatility and the capital structure of listed companies in Vietnam during the research period. High cash flow volatility can reduce the use of total debt because of worries about the risk of financial distress, or bankruptcy. Bui and Mai (Citation2021) studied the relation of financial distress with the cash flow of listed non-financial enterprises in Vietnam from 2014 to 2018 using the GLS method. Their research results showed that cash flow from operating activities has a negative impact on financial distress, but cash flows from investing and financing activities have a positive impact on financial distress. Analyzing the data of 505 non-financial companies listed in the Vietnam joint stock market in the period 2015–2020, Le and Nguyen (Citation2022) confirm that operating cash flow has a negative impact on financial distress. Not only that, operating cash flow plays a role in reducing the negative impact of financial leverage on financial distress.

3. Research model and method

To study the impact of cash flow on the financial distress of private enterprises listed on the Vietnamese stock market from 2010 to 2020, the authors use the quantile regression method. It is for a detailed analysis of the impact of cash flow on the financial distress of private enterprises listed on the Vietnamese stock market in each quantile. The quantile regression was developed by Koenker and Bassett (Citation1978) and has been widely applied in the world. The quantile regression method differs from other methods in that instead of determining the marginal effect of the independent variable on the mean of the dependent variable. Quantile regression determines the marginal effect of the independent variable on the dependent variable in each quantile of that dependent variable. It shows details about the relationship between the dependent variable and the independent variables on each conditional quantile of the dependent variable. It is stable because the parameter tests do not rely on the standardization of the error. Besides that, the quantile regression is suitable when the model has variable variance (Hao & Naiman, Citation2007). The basic quantiles of the distribution function of financial distress variables are choose for analysis including quantiles 0.1; 0.25; 0.5; 0.75; 0.9. The quantile regression has some advantages over OLS regression and allows the researcher to consider the entire variation of the dependent variable based on the change of quantile θ (0,1). The assumption in the quantile regression is not strict as in OLS regression, and the condition of normal distribution and homogeneity of variance is not necessary (Hao & Naiman, Citation2007). There are no studies on the relationship between cash flows and financial distress using quantile regression in Vietnam. Therefore, the authors use the quantile regression method to examine the differences in cash flow effects on each quantile of financial distress in this study.

Research data are private enterprises listed on Hanoi Stock Exchange and Ho Chi Minh City Stock Exchange. The authors select a research sample consisting of enterprises that satisfy the following conditions: (1) enterprises without state capital contribution; (2) excluding finance, banking, and insurance enterprises due to industry specificity; and (3) the selected enterprises have the full financial statements in the period 2010–2020 with all the financial statements audited and accepted in reasonableness and truthfulness under the principle of materiality. The final research data includes 263 listed private non-financial enterprises in 11 years from 2010 to 2020. The sample of observations accounts for more than 70% of the total observations of enterprises listed on the Ho Chi Minh and Hanoi Stock Exchange, so it is guaranteed to represent the overall study.

The data in this study are collected from the financial statements of 263 private non-financial enterprises listed on the Vietnamese stock market from 2010 to 2020 provided by FinPro.

Based on an overview of the research literature, the authors derive from the research model of Sayari and Mugan (Citation2013) to propose the following research model:

To estimate the relationship between cash flow and corporate financial distress, the study measures financial distress and the volatility of cash flows as follows:

Many studies have used indicators such as Altman’s Z Score (Altman, Citation1968), Ohlson’s O index (Ohlson, Citation1980), and Zmijewski’s index (Zmijewski, Citation1984) to measure corporate financial distress. According to Kim and Upneja (Citation2014), Zmijewski’s index is the most commonly used because it is not sensitive to different states of financial distress and is also insensitive to different business sectors. Therefore, the study measured the dependent variable -FD- according to Zmijewski’s model with the following determination:

where FD with a negative value indicates relatively stronger financial health, and less likely to occur financial distress, while a positive value of FD shows the opposite result; or generalized that an increase in FD indicates a higher probability of financial distress. NI is profit after tax, TA is total assets, TL is liabilities, CA is current assets, and CL is current liabilities.

There are various ways to calculate cash flow volatilities such as the annual standard deviation of operating cash flow on total assets (Karimli, Citation2018); or the standard deviation of returns before taxes, interest and depreciation on total net assets (Keefe & Yaghoubi, Citation2016). In this study, the independent variables related to each cash flow, including OCF is operating cash flow normalized by the total assets. This independent variable is expected to have a negative impact on FD (Jooste, Citation2007; Kordestani et al., Citation2011; Sayari & Mugan, Citation2013); ICF is the net investment cash flow normalized by total assets and expected to have a negative effect on FD (Dickinson, Citation2011; Kordestani et al., Citation2011); FCF is the net cash flow from financing activities normalized by total assets and is expected to have a positive effect on FD (Kordestani et al., Citation2011; Sayari & Mugan, Citation2013; Shamsudin & Kamaluddin, Citation2015). In addition, the research model has two control variables, including (i) AGE calculated from the established year to the study year and (ii) SIZE measured by the logarithm of net sales.

The variables of the model are described in the following table:

4. Results and discussion

4.1. Descriptive statistics

The variables of the model are described in . Descriptive statistics of the variables are shown in .

Table 1. Description of the model variables

Table 2. Descriptive statistics

Table presents descriptive statistics with mean, median, and standard deviation as well as minimum and maximum values of the variables in the model. The results of the descriptive statistical analysis show differences in financial distress, cash flows, and other factors affecting the financial distress of private enterprises listed on the Vietnamese stock market. FD of listed private enterprises has the average of −3.34, the minimum value of −82, and the maximum value of 29.83. It shows a wide disparity in the financial distress of listed private enterprises in the 2010–2020 decade. The negative FD indicates relatively better financial health, and less likelihood of financial distress meanwhile the positive FD indicates the opposite. It means the more increasing FD values, the higher the probability of financial distress. That proves that Vietnamese private enterprises were seriously affected by the global financial crisis in the 2011–2014 period and the Covid-19 pandemic from 2019–2020. The consequence of this situation is that many private enterprises fell into financial distress.

For the independent variables, operating cash flow has an average of 0.46, the minimum is approximately −40, and the maximum of 186. It indicates there is a huge difference in the operating cash flows of listed private companies from 2010 to 2020. Investing cash flows has the lowest difference with the value ranges of ICF from −47.5 to 18.4, the average value of −0.36. The financial cash flow has an average value of −0.058, a minimum value of −155, and the maximum value of 78. So, there is a big difference in the financial cash flow of the listed private companies.

For control variables, the average age of the listed companies is 13.65. SZ is different among the listed private enterprises, the value ranges from 13.97 to 32.00, and the mean value is 26.49.

4.2. Correlation coefficient matrix

Table shows the correlation coefficient between the dependent and independent variables. The correlation coefficient between the independent variables is not greater than 0.8, so there is no multicollinearity between the variables (Cohen, Citation1988). Investing cash flow (ICF) and enterprise age (AGE) are variables correlated positively with FD. Meanwhile, operating cash flow (OCF) and financial cash flow (FCF) negatively correlated with variable FD. The correlation analysis results show that the possibility of multicollinearity between the independent variables in the model is not high.

Table 3. The correlation coefficient matrix among variables

4.3. Correlation regression analysis results

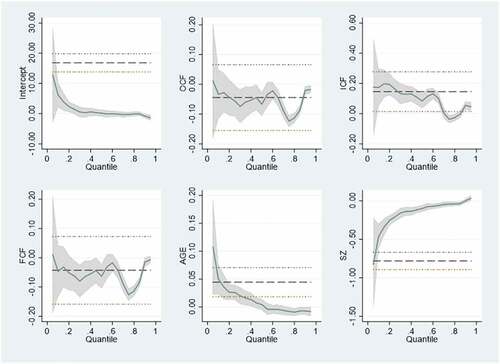

presents the results of quantile regression with quantiles 0.1; 0.25; 0.5; 0.75; and 0.9. Representation of variables on quantiles is illustrated in .

Table 4. Quantile regression results

Figure 1. Representation of variables on quantiles.

At the 0.1 quantiles of the FD, financial cash flow and enterprise’s age positively relate to financial distress, but enterprise size relates negatively. With a significance level of 5%, the ICF has the same effect as the FD with a 0.173 regression coefficient. It means that if the cash flow from financial activities increases, the risk of financial distress also increases. At a 1% significance level, AGE has a positive impact on financial distress, but the magnitude of the effect is tiny. SZ has a negative relationship with financial distress, or the bigger the company, the lower probability of financial distress.

At the 0.25 quantiles level of the FD, financial cash flow and enterprise’s age positively relate to financial distress; however, operating cash flow, investing cash flow, and enterprise size have negative relationships with financial distress. By a significance level of 10%, the OCF has a negative impact on the FD with a regression coefficient of 0.0553, and the FCF has a negative influence with a regression coefficient of 0.0622. That means the increase in operating and financing cash flows helps to reduce the corporate financial distress risk. With a statistical significance of 1%, the ICF has a positive effect on the FD with a regression coefficient of 0.162. It shows that when the financial cash flow increases, the risk of financial distress also increases. At a 1% significance level, AGE has a positive relationship with financial distress, but the magnitude of the effect is low. Furthermore, SZ negatively impacts financial distress, or the larger firm, the lower probability of financial distress.

At the 0.5 quantiles level of FD, financial cash flow is positively related to financial distress, in which operating cash flow, investing cash flow, and SZ is negative. At the significance level of 1%, the OCF has a negative influence on the FD with a regression coefficient of 0.0667. The FCF has a negative relationship with a regression coefficient of 0.0633 at the 5% significance level. It indicates that when operating and financial cash flow increase, the risk of corporate financial distress can reduce. At a statistical significance of 1%, the ICF has a positive influence on the FD with a regression coefficient of 0.0836. That means the financial distress increases when the financial cash flow increases. At the 1% significance level, SZ negatively relates to financial distress.

At the 0.75 quantiles level of the FD, all variables in the model (including operating cash flow, investing cash flow, financial cash flow, age, and size) have an opposite influence on financial distress. With a significance level of 1%, the OCF, ICF, and FCF have a negative influence on the FD-the sequential regression coefficients of 0.124; 0.0376; 0.126. It means that the increase in operating cash flow, investing cash flow, and financing cash flow increase contribute to reducing the risk of corporate financial distress. At the 5% significance level, AGE has a reverse relationship with financial distress, but the magnitude of the effect is tiny. SZ has a reverse relationship with financial distress, which means the bigger the firm size, the lower the probability of financial distress.

At the 0.9 quantiles of the FD, financial cash flow and enterprise age are the two variables that have an impact on the financial distress of listed private enterprises. At the 1% significance level, the ICF has a positive effect on the FD with a regression coefficient of 0.055, which means that when the cash flow from financial activities increases, the risk of financial distress also increases. At the 10% significance level, AGE has a positive effect on financial distress, but the impact level is not significant.

For the OCF, operating cash flow has a negative relationship with the probability of financial distress of private enterprises listed on the Vietnamese stock market with different levels of statistical significance at 0.25; 0.5; and 0.75 percentiles. It shows that operating cash flow increases, and the FD decreases; which means an increase in operating cash flow will reduce the possibility of financial distress in listed private companies. The research results are consistent with the studies of Sayari and Mugan (Citation2013), Kordestani et al. (Citation2011), Jantadej (Citation2006), Karas and Režňáková (Citation2020), and Bui and Mai (Citation2021), and Jantadej (Citation2006) stated that financial distress occurs when a business has negative cash flows from operating activities. When the company has a surplus and increased operating cash flow, it will make the enterprise perform well it will make company perform well in its financial obligations under the contract with creditors, thereby minimizing the possibility of falling into distress. The Covid-19 pandemic caused a serious cash inflows shortage for Vietnamese private enterprises, leading to financial difficulties. Some Vietnamese private enterprises had negative business cash flows in the period 2010–2020, especially in 2020.

For the ICF, the cash flow from investing activities has a reverse influence on the probability of financial distress of the private enterprises listed on the Vietnamese stock market with 0.75 quantiles. It shows that an increase in the investing cash flow reduces the probability of financial distress in the listed private enterprises at 0.75 quantiles. That result is supported by the study of Kordestani et al. (Citation2011), Jantadej (Citation2006). At the 0.1; 0.25; 0.5; and 0.9 quantile levels, the investing cash flow positively relates to the financial distress of the listed private enterprises. The greatest impact is at the 0.1 quantiles with a regression coefficient of 0.173 and a decreasing regression coefficient at the remaining quantiles. The result shows that the increasing investing cash flow rises the financial distress of listed private enterprises. This result is consistent with the research result of Bui and Mai (Citation2021). It can explain that enterprises have an increased cash flow from investing activities, which means investments shrink because they have sold off fixed assets or recovered financial investments. Proceeds from investment activities can be used to cover shortfalls in business operations, repay loans, or pay dividends. That may stem from inefficient investment and failure to manage financial risks well, leading to an increase in the possibility of financial distress for listed private enterprises.

For the FCF, cash flow from financial activities negatively influences the probability of financial distress of private enterprises listed on the Vietnamese stock market at the 0.25; 0.5; and 0.75 quantiles, and the biggest impact is at the 0.75 quantiles with the regression coefficient of 0.126. It shows that the increased cash flow from financial activities reduces the likelihood of financial distress of the listed enterprises, in contrast to the studies of Sayari and Mugan (Citation2013) and Kordestani et al. (Citation2011). The result explains that listed enterprises have increased cash flow from financial activities which means they increase long-term capital sources for investment, production, and business expansion, creating many opportunities to profit and improve competitiveness, helping to reduce the risk of financial distress.

In addition, the research results also show that the AGE positively influences the FD at the 0.1 and 0.25 quantiles. But at the 0.75 and 0.9 quantiles, the relationship between the AGE and the FD is inverse. However, the impact is not significant. While the bigger the size of the enterprise, the lower the probability of financial distress at 0.1; 0.25; 0.5; and 0.75 quantiles. Large-scale enterprises have a lot of potential in capital, reputation, and competitiveness, which helps their operating activities have many advantages and contributes to minimizing the distress.

5. Conclusion and recommendations

The study shows empirical evidence of the impact of cash flow on the financial distress of private enterprises listed on the Vietnamese stock market. By approaching the quantile regression method, the research determines a negative relationship between operating cash flow with the probability of financial distress with different statistical significance at the 0.25; 0.5; and 0.75 quantile levels. At the 0.1; 0.25; 0.5; and 0.9 quantiles, investment cash flow positively relates to the financial distress of the listed private enterprises, with the biggest impact at the 0.1 quantiles. Cash flow from financing activities negatively influences the probability of financial distress of the private enterprises listed at the 0.25; 0.5; and 0.75 quantiles, with the biggest impact at the 0.75 quantiles. Besides that, large-scale private enterprises are less likely to experience financial distress.

This research provides empirical evidence for listed private enterprises to have appropriate business strategies, contribute to reducing the risk of financial distress and develop sustainably. To reduce the risk of financial distress for listed private enterprises, they have to manage cash flow effectively. To manage cash flow, private enterprises need to forecast cash flows and build their optimal budget models. Because cash flow forecast is essential in the financial plan, listed enterprises must have a plan to raise capital and use capital in the case of cash flow shortage and cash flow surplus.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Thuy Duong Phan

Our research focuses on cash flows in Vietnam. Cash flow analysis is more popular because it is significant to manipulate or regulate cash flow. Using cash flow as a measure to evaluate a business comes from the fact that cash flow is less dependent on the accountant's subjectivity, so it is difficult to distort the cash flow numbers. So, we plan to examine the relationship between cash flow, financial distress, and capital structure. We help to improve the cash flow management of Vietnamese enterprises. This study is an important part of our plan to provide the relationship between cash flow and financial distress.

Notes

References

- Altman, E. I. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. The Journal of Finance, 23(4), 589–13. https://doi.org/10.2307/2978933

- Altman, E. I., & Hotchkiss, E. (2006). Corporate financial dis- tress and bankruptcy (3rd ed.). John Wiley & Sons, Inc.

- Arnold, G. (2013). Corporate financial management (pp. 849–902). Pearson.

- Aziz, M. A., & Dar, H. A. (2006). Predicting corporate bankruptcy: Where we stand? Corporate Governance. The International Journal of Business in Society, 6(3), 11–17. https://doi.org/10.1108/14720700610649436

- Bae, J. K. (2012). Predicting financial distress of the South Korean manufacturing industries. Expert Systems with Applications, 39(10), 9159–9165. https://doi.org/10.1016/j.eswa.2012.02.058

- Beaver, W. H. (1966). Financial ratios as predictors of failure. Journal of Accounting Research, 4(3), 71–111. https://doi.org/10.2307/2490171.

- Brealey, R. A., Myers, S. C., & Allen, F. (2008). Principles of Corporate Finance (Ninth ed.). Mc Graw – Hill International Edition.

- Bui, K. D., & Mai, T. T. N. (2021). Financial distress and cash flow of listed non-financial enterprises in Vietnam. Banking Science & Training Review, 1, 61–70. https://scholar.google.com/scholar?hl=vi&as_sdt=0%2C5&q=Kiệt+quệ+tài+ch%C3%ADnh+và+dòng+tiền+của+các+doanh+nghiệp+phi+tài+ch%C3%ADnh+niêm+yết+tại+Việt+Nam’&btnG=

- Cohen, J. (1988). Set correlation and contingency tables. Applied Psychological Measurement, 12(4), 425–434. https://doi.org/10.1177/014662168801200410

- Denis, D. J., & Mihov, V. T. (2003). The choice among bank debt, non-bank private debt, and public debt: Evidence from new corporate borrowings. Journal of Financial Economics, 70(1), 3–28. https://doi.org/10.1016/S0304-405X(03)00140-5

- Dickinson, V. (2011). Cash flow patterns as a proxy for firm life cycle. The Accounting Review, 86(6), 1969–1994. https://doi.org/10.2308/accr-10130

- Edward, A. (1968). Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. Journal of Finance, 23(4), 589–609. https://doi.org/10.2307/2978933

- Fawzi, N. S., Kamaluddin, A., & Sanusi, Z. M. (2015). Monitoring distressed companies through cash flow analysis. Procedia Economics and Finance, 28, 136–144. https://doi.org/10.1016/S2212-5671(15)01092-8

- Foster, B. P., & Ward, T. J. (1997). Using cash flow trends to identify risks of bankruptcy. The CPA Journal, 67(9), 60. https://scholar.google.com/scholar?hl=vi&as_sdt=0%2C5&q=Foster%2C+B.+P.%2C+%26+Ward%2C+T.+J.+%281997%29.+Using+cash+flow+trends+to+identify+risks+of+bankruptcy.+The+CPA+Journal%2C+67%289%29%2C+60&btnG=

- Freixas, X., Parigi, B. M., & Rochet, J. C. (2000). Systemic risk, interbank relations, and liquidity provision by the central bank. Journal of Money, Credit, and Banking, 32(3), 611–638. https://doi.org/10.2307/2601198

- Gathecha, J. W. (2016). Effect of firm characteristics on financial distress of non-financial listed firms at Nairobi Securities Exchange. Kenya (Doctoral dissertation, Kenyatta University).

- Gentry, J. A., Newbold, P., & Whitford, D. T. (1990). Profiles of cash flow components. Financial Analysts Journal, 46(4), 41–48. https://doi.org/10.2469/faj.v46.n4.41

- Grice, J. S., & Dugan, M. T. (2001). The limitations of bankruptcy prediction models: Some cautions for the researcher. Review of Quantitative Finance and Accounting, 17(2), 151–166. https://doi.org/10.1023/A:1017973604789

- Hao, L., & Naiman, D. Q. (2007). Quantile regression (No. 149). Sage.

- Honjo, Y. (2000). Business failure of new firms: An empirical analysis using a multiplicative hazards model. International Journal of Industrial Organization, 18(4), 557–574. https://doi.org/10.1016/S0167-7187(98)00035-6

- Horne, J. C. V., & Wachowicz, J. M. (2008). Fundamentals of financial management (13th ed.). Prentice Hall.

- Hossain, M. A., Hossain, M. S., & Jahan, N. (2018). Predicting continuance usage intention of mobile payment: An experimental study of Bangladeshi customers. Asian Economic and Financial Review, 8(4), 487–498. https://doi.org/10.18488/journal.aefr.2018.84.487.498

- Isayas, Y. N., & McMillan, D. (2021). Financial distress and its determinants: Evidence from insurance companies in Ethiopia. Cogent Business & Management, 8(1), 1951110. https://doi.org/10.1080/23311975.2021.1951110

- Jaax, A. (2020). Private sector development and provincial patterns of poverty: Evidence from Vietnam. World Development, 127, 104747. https://doi.org/10.1016/j.worlddev.2019.104747

- Jantadej, P. (2006). Using the combinations of cash flow components to predict financial distress. The University of Nebraska-Lincoln.

- Jooste, L. (2007). An evaluation of the usefulness of cash flow ratios to predict financial distress. Acta Commercii, 7(1), 1–13. https://doi.org/10.4102/ac.v7i1.2

- Kamaluddin, A., Ishak, N., & Mohammed, N. F. (2019). Financial distress prediction through cash flow ratios analysis. International Journal of Financial Research, 10(3), 63–76. https://doi.org/10.5430/ijfr.v10n3p63

- Karas, M., & Režňáková, M. (2020). Cash flows indicators in the prediction of financial distress. Engineering Economics, 31(5), 525–535. https://doi.org/10.5755/j01.ee.31.5.25202

- Karimli, T. (2018). The impact of cash flow volatility on corporate debt decisions. Central European University.

- Keefe, M. O. C., & Yaghoubi, M. (2016). The influence of cash flow volatility on capital structure and the use of debt of different maturities. Journal of Corporate Finance, 38, 18–36. https://doi.org/10.1016/j.jcorpfin.2016.03.001

- Khaliq, A., Altarturi, B. H. M., Thaker, H. M. T., Harun, M. Y., & Nahar, N. (2014). Identifying financial distress firms: A case study of Malaysia’s Government Linked Companies (GLC). International Journal of Economics, Finance and Management, 3(3), 141–150.

- Kim, S. Y., & Upneja, A. (2014). Predicting restaurant financial distress using decision tree and AdaBoosted decision tree models. Economic Modelling, 36, 354–362. https://doi.org/10.1016/j.econmod.2013.10.005

- Koenker, R., & Bassett, G.,sJr. (1978). Regression quantiles. Econometrica: Journal of the Econometric Society, 46(1), 33–50. https://doi.org/10.2307/1913643

- Kokko, A., & Thang, T. T. (2014). Foreign direct investment and the survival of domestic private firms in Viet Nam. Asian Development Review, 31(1), 53–91. https://doi.org/10.1162/ADEV_a_00025

- Kordestani, G., Bakhtiari, M., & Biglari, V. (2011). Ability of combinations of cash flow components to predict financial distress. Business: Theory and Practice, 12(3), 277–285. https://doi.org/10.3846/btp.2011.28

- Kristanti, F. T., Rahayu, S., & Huda, A. N. (2016). The determinant of financial distress on Indonesian family firm. Procedia-Social and Behavioral Sciences, 219, 440–447. https://doi.org/10.1016/j.sbspro.2016.05.018

- Lau, A. H. L. (1987). A five-state financial distress prediction model. Journal of Accounting Research, 25(1), 127–138. https://doi.org/10.2307/2491262

- Le Maux, J., & Morin, D. (2011). Black and white and red all over: Lehman Brothers’ inevitable bankruptcy splashed across its financial statements. International Journal of Business and Social Science, 2(20), 39-65. https://www.academia.edu/49493014/Cash_flows_ratios_as_predictors_of_corporate_failure

- Le, H. V., & Nguyen, H. B. (2022). Financial leverage, operating cash flows and financial distress of listed non-financial companies in Vietnam. Banking Science & Training Review, 238, 24-35.

- Martin, D. (1977). Early warning of bank failure: A logit regression approach. Journal of Banking & Finance, 1(3), 249–276. https://doi.org/10.1016/0378-4266(77)90022-X

- Murty, A. V. N., & Misra, D. P. (2004). Cash flow ratios as indicators of corporate failure. Finance India, 18(3), 1315–1325.. https://scholar.google.com/scholar_lookup?title=Cash%20Flow%20Ratios%20as%20Indicators%20of%20Corporate%20Failure&publication_year=2004&author=A.V.%20Murty&author=D.P.%20Misra.

- Nguyen, H. Y. (2020). CEOs, cash flow fluctuations and capital structure of listed companies in Vietnam. Journal of Asian Business and Economic Studies – JABES, (6), 44–71. http://jabes.ueh.edu.vn/Content/ArticleFiles/02b38b0e-ca93-4b36-8d39-96ed70c756cd/JABES-2020-10-V109.pdf

- Ohlson, J. A. (1980). Financial ratios and the probabilistic prediction of bankruptcy. Journal of Accounting Research, 18(1), 109–131. https://doi.org/10.2307/2490395

- Rodgers, C. S. (2011). Predicting corporate bankruptcy using multivariant discriminate analysis (MDA), logistic regression and operating cash flows (OCF) ratio analysis: A cash flow-based approach. Golden Gate University.

- Romadhina, A. P., Fitriani, M. N., & Andhitiyara, R. (2022). The effect of cash flow and currency exchange rate on financial distress. Jurnal Akuntansi Dan Perpajakan Jayakarta, 3(2), 146–167. https://doi.org/10.53825/japjayakarta.v3i02.111

- Roslan, N. H., RUS, R. M., & Rozzani, N. Determinants of cash flows towards financial distress prediction among manufacturing companies in Malaysia. https://doi.org/10.37602/IJSSMR.2022.5113

- Sayari, N., & Mugan, F. N. C. S. (2013). Cash flow statement as an evidence for financial distress. Universal Journal of Accounting and Finance, 1(3), 95–103. https://doi.org/10.13189/ujaf.2013.010302

- Schellenger, M., & Cross, J. N. (1994). FASB 95, Cash Flow and bankruptcy. Journal of Economics and Finance, 18(3), 261–274. https://doi.org/10.1007/BF02920486

- Shamsudin, A., & Kamaluddin, A. (2015). Impending Bankruptcy: Examining cash flow pattern of distress and healthy firms. Procedia Economics and Finance, 31, 766–774. https://doi.org/10.1016/S2212-5671(15)01166-1

- Utami, E. R. (2016). “The influence of ownership structure and cash flow on financial distress. Essay. Faculty of Economics and Business, Diponegoro University. Semarang.

- Ward, T. J. (1994). Cash flow information and the prediction of financially distressed mining, oil and gas firms: A comparative study. Journal of Applied Business Research (JABR), 10(3), 78–86. https://doi.org/10.19030/jabr.v10i3.5927

- Yap, B. C. F., Munuswamy, S., & Mohamed, Z. (2012). Evaluating company failure in Malaysia using financial ratios and logistic regression. Asian Journal of Finance & Accounting, 4(1), 330–344. http://dx.doi.org/10.5296/ajfa.v4i1.1752

- Zavgren, C. V. (1985). Assessing the vulnerability to failure of American industrial firms: A logistic analysis. Journal of Business Finance & Accounting, 12(1), 19–45. https://doi.org/10.1111/j.1468-5957.1985.tb00077.x

- Zmijewski, M. E. (1984). Methodological issues related to the estimation of financial distress prediction models. Journal of Accounting Research, 22, 59–82. https://doi.org/10.2307/2490859