Abstract

Drawn the socio-emotional wealth perspective, this paper investigates the relationship among CEO power, innovative investment and family board involvement in family enterprises. Secondary data on listed Chinese family small- and medium-sized enterprises from 2015 to 2019 was accessed via the China Stock Market and Accounting Research database and analysed using hierarchical multiple regression. The findings suggest a significant positive effect of CEO power on innovative investment in Chinese family SMEs. This study also found the moderating effect of family board involvement could inhibit the positive relationship between CEO power and family SMEs’ innovativeinvestment. Further, compared with hiring external professional managers as CEO, the inhibitory moderating effect of family board involvement is more significant when a family member is appointed as a CEO in family SMEs. In order to better adapt to the increasingly competitive market environment, the findings of this paper suggest that internal family board members should appropriately reduce their influence on the CEO power to stimulate Chinese family SMEs to conduct more innovative investment for their long-term prosperity.

According to estimates, family-owned enterprises account for between 65% and 80% of firms worldwide (Bent & Seaman, Citation2017). Family small- and medium-sized enterprises (SMEs) tend to play an significant role in supporting the economic stability of many countries and regions, especially in emerging markets (Ahmad & Yaseen, Citation2018). In China, the success of family enterprises is becoming increasingly necessary for the developing country’s economy (Yang et al., Citation2020). However, similar to the situation in many other countries, the rate of failure is notably high. Based on statistics, about 68% of Chinese family SMEs bankrupt within their first five years of operations, and only 13% of these firms have a lifespan that exceeds 10 years (Zhu et al., Citation2012).

With intensifying competition in the global markets, innovative/R&D investment has received much attention as one of the core factors that could assist family firms in remaining competitive against rival firms (Fuetsch & Suess-Reyes, Citation2017). Previous empirical studies demonstrated that a firm’s higher level of innovative investment could positively influence a family firm’s financial performance (Sher & Yang, Citation2005) as well as its stainable competitive advantage (Lee & Hsieh, Citation2010). Thus, family firms’ R&D investment has become an increasingly frontier topic in past decades (Gomez–Mejia et al., Citation2014; Luo et al., Citation2019; Sun, Citation2019). Previous studies widely recognised that stronger CEO power could effectively stimulate a firm’s innovative investment as innovative strategies plays an important role in assisting firms in achieving long-term financial success, thus bringing more compensation to CEOs (Barker & Mueller, Citation2002; Lewellyn & Muller‐Kahle, Citation2012; Sheikh, Citation2018). This study assumes that the relationship between CEO power and innovative investment deserves further investigation due to the unique involvement of family members in the top management team and family CEOs’ family-oriented non-financial pursuits (Gómez-Mejía et al., Citation2007).

Previous studies contended that family firms’ non-financial goals like preserving family control over the firm (Luo et al., Citation2019; Sciascia et al., Citation2015), creating and maintaining a positive family business identity (Zellweger et al., Citation2010) and the intergenerational vision (Carney et al., Citation2019) could significantly reduce family firms’ risky innovative investment. Further, Matzler et al. (Citation2015) empirical study has investigated how the three dimensions of family involvement (ownership, management and governance) will affect a family firm’s R&D input, and reflected that the family participation in general manager team will negatively impact the family firm’s innovative input. However, considering the huge differences between the general managers and the CEO in terms of their authority and status in a firm (Lewin & Stephens, Citation1994), the influence of family firms’ CEO power on family firms’ R&D intensity still remains unclear. While some studies have noted that having a family member as the CEO might result in less firm resources used to conduct R&D projects (Duran et al., Citation2016; Lodh et al., Citation2014), the mere presence of family members on the position of CEO does not automatically imply that the family CEO exert his/her actual influence on the family firm (Zellweger et al., Citation2010). To address this, this study tries to employ four dimensions of CEO power (see Table ) to investigate how family CEOs’ actual influence on the business can affect innovative strategies.

Table 1. CEO power dimension and explanation

Table 2. Measurement of variables

Table 3. Descriptive statistics

Table 4. Correlation coefficients

Table 5. Regression results for the effect of CEO power on R&D investment, and the moderating effect of family board involvement

Table 6. Regression analysis based on different sources of CEO

Different with ordinary managers, as chief planners and architects of an enterprise, the CEOs tend to play a significant role in various decisions-making process (e.g., investment strategies; Crossland et al., Citation2014; Sheikh, Citation2018). From the perspective of stewardship theory (Miller & Le Breton-Miller, Citation2006; Y.-M. Chen et al., Citation2016), some empirical studies suggested that both family and professional CEOs in family firms tend to exert their power to support firms’ innovative investment to enhance firms’ innovative capability, and accordingly increase a firm’s long-term competitiveness in the competitive marketplace (Chen, Citation2014; Sheikh, Citation2018). However, in the distinctive context of family business, this study proposed that the positive effect of CEO power on innovative investment may be inhibited due to following reasons:

Firstly, some internal family CEOs may not be able to exercise their influence on the business independently due to their potential lack of skills/knowledges. Due to socio-emotional wealth (SEW) perspective (Gómez-Mejía et al., Citation2007), some internal family members who are not competent or lack of skills/knowledges are still appointed in the key positions including CEO position in order to maintain family control on the firms (Gibb Dyer, Citation2006). Under this situation, the CEO’s decision-making and behaviours might be closely monitored and adjusted by other internal stakeholders like board directors. Secondly, according to Sheikh (Citation2018) study, the degree of CEOs’ power differs greatly in different firms due to various types of power distribution in a family firm, which implies that not all CEOs can enjoy a high degree of power in their firms. It is not uncommon that the family board directors have the potential to influence family CEOs’ works in the process of making key decisions, especially when the CEOs and board directors are bonded together through kinship and a shared family identity and a common history (Jacob, Citation2009; Zellweger et al., Citation2012). Under this situation, the family board directors’ possible pessimism towards R&D activities (due to SEW preservation) may influence a CEO’s decision-making process. Further, due to agency theory, the simultaneous presence of family board directors and family CEOs in the family firm might lead to a series of altruistic behaviours like free riding costs (Schulze et al., Citation2003) that might reduce the amount of innovative investment. Based on above reasoning, it tends to be meaningful to apply “family board involvement” as a moderating variable in this study to investigate how it will interfere the relationship between CEO power and family firms’ R&D intensity. By such, this study answers the call of Frank et al. (Citation2017) and Weismeier-Sammer et al. (Citation2013) studies to investigate how family-employee bond (one of the subscales of “familiness” construct) could affect a family firm’s innovation.

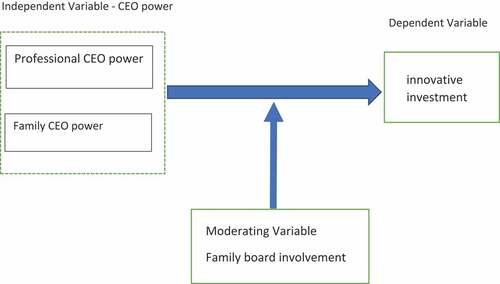

According to above reasoning, this study proposes that the decision-making process of external professional CEO and internal family CEO are likely to be diverse due to the interference of family board directors. In other words, the risk appetite of family firms may vary depending on both CEO source and family board directors’ involvement. Thus, the investigation regarding how different CEO power (actual influence instead of mere presence) in family business could affect firms’ innovative investment tends to be meaningful via employing family board involvement as the moderating variable. By taking Chinese-listed family SMEs from 2015 to 2019 as research samples, this paper aims to investigate the relationship between CEO power and innovative/R&D investment under the Chinese family SME context and explore how the family board involvement could interfere above relationship. The research model of this study is presented as below Figure .

Figure 1. Research model of this study.

1. Literature review and hypothesis

1.1. CEO power and R&D investment

A company’s R&D expenditure always plays an important and positive role in influencing a firm’s productivity growth (Wakelin, Citation2001). Besides, a significant positive relationship between innovative investment and firm performance has also been widely supported (Belderbos et al., Citation2004). Successful innovative decision and investment will enhance enterprises’ core competitiveness in the competitive market environment (Driver & Guedes, Citation2012). However, most R&D projects have no immediate tangible returns since the duration of payback period is often quite long (Coad & Rao, Citation2010). Further, compared with carrying out those conservative firm strategies, the failure rate of innovative investment tend to be much higher (Tishler, Citation2008). Thus, whether to carry out innovative investment is a major problem faced by family enterprises. Since CEO is the main decision-maker in a small- and medium-sized enterprise (Thong, Citation1999; Thong & Yap, Citation1995), family SME’s CEO power will undoubtedly affect family SMEs’ decision-making towards innovative/R&D projects.

On the basis of incentive theory (Killeen, Citation1981), companies tend to grant the CEOs more authority and power to make decisions, thereby motivating CEOs to serve the firm and stimulate CEO’s creativity and motivation (Combs et al., Citation2007). Meanwhile, other family managers with social and human capital will be more motivated to allocate various resources into innovative program when the CEO is powerful and influential in the firm (Chen, Citation2014). Further, Daily and Johnson (Citation1997) study suggested that the greater the power of the CEO, the less influenced he/she is influenced by those board directors. Thus, the powerful and influential CEO would be able to choose companies’ innovative strategies as their expectation.

From the perspective of stewardship theory, Davis et al. (Citation1997) suggested that the CEO in family firms tend to focus on achieving organisation’s pursuits like sales growth and maximizing shareholders’ wealth; this has become a way for the CEO to realize their personal value. Further, according to Lin (Citation2005) study, CEOs’ pro-organisational behaviour could be best facilitated when they are given sufficient authority and discretion. Therefore, if the family business grants the CEO sufficient autonomy and maintain a relationship of mutual trust with the CEO, the CEO will behave as an ideal “steward” aiming at maximizing the interests of shareholders. In order to achieve this goal, the CEO will be more inclined to implement innovative strategies and increase R&D investment to enhance the competitiveness of family business. Based on above discussion, the first hypothesis of this paper could be proposed:

Hypothesis 1: The CEO power is positively related to the level of innovative investment.

1.2. The moderating role of family board involvement

The board of directors tend to play an important role in family enterprises. Firstly, the board of directors could exert significant influence in the formulation of business strategies (Kelly & Gennard, Citation2007). Secondly, the board of directors could have sufficient power to hire, appoint and supervise senior managers including the CEO (Borokhovich et al., Citation1996; Tian et al., Citation2011). In family firms, the participation of family members in the board become the main way to influence family firms’ decision-making process and supervise/monitor the CEO behaviours (Corbetta & Salvato, Citation2004). Besides, Voordeckers et al. (Citation2007) study noted that the participation of family members in the board of family firms could maintain the family’s control over the enterprise, and thus improve the efficiency of corporate governance. Based on this, this study supposes that the influence of family board involvement cannot be neglected while investigating the relationship between CEO power and innovative investment under a family business context.

Many existing studies noted that the family board involvement should be negative to family firms’ R&D strategies (Adams et al., Citation2006; Matzler et al., Citation2015; Munari et al., Citation2010). From the perspective of socio-emotional wealth (SEW), the gain or loss the socio-emotional wealth becomes the primary referencing point for family board directors to make strategic decisions (Gómez-Mejía et al., Citation2007). Family board directors tend to restrict the entry of external talents into the top management team of the business in order to maintain family control over the family firms (Lionzo & Rossignoli, Citation2013), which is not conducive to the flow of innovative thinking into family business. Further, Jiang et al. (Citation2020) indicated that family directors always avoid or minimise risky innovative investments in order to effectively perpetuate family inheritance in the future. As the involvement of family board deepens, the family’s control over the business becomes higher, and the directions of firms’ business strategies will be closer to the expectation of the family (Bammens et al., Citation2008).

Although a CEO is the highest planner of family firms’ business operation, his/her decision-making could still be interfered by family board directors (Sheikh, Citation2018). With the degree of family board directors’ participation becomes deeper, the CEOs in family firms could face more decision-making resistance from the family board directors, thus accordingly reducing risky innovative investments. Based on above, the second hypothesis of this paper could be proposed:

Hypothesis 2: The family board involvement could inhibit the positive relationship between CEO power and R&D investment

1.3. The interact effect of family CEO and family board involvement

According to existing studies in regard with CEO source (Kang & Kim, Citation2016; Lin & Hu, Citation2007), the sources of CEOs in family business usually fall into two categories: (a) the internal family members serve as CEOs, such as the children and brothers of the founders; (b) a non-family professional manager serve as the CEO. This study supposes that the inhibiting effect of family board involvement (see hypothesis 2) on the relationship between CEO power and R&D investment may differs under different CEO sources. Westphal (Citation1999) study suggested that the kinship and social ties between CEOs and board directors could enhance the mutual trust and loyalty, resulting in a more collaborative working relationship, which encourages CEOs to solicit board directors’ advice on strategic issues. Considering a family CEO and family board members are from the same family background, and share a same family social network, this study proposes that an internal family CEO may be inclined to align his/her strategic decision with other family board directors.

As mentioned in last part, family board directors are usually reluctant to carry out risky innovative strategies in order to preserve their family firms’ socio-emotional wealth (Matzler et al., Citation2015; Patel & Chrisman, Citation2014). Under this situation, those internal family CEOs’ decision-making processes are more likely be affected by family board directors’ mind, and accordingly reduce their willingness to invest in R&D projects that are highly risky and full of uncertainty. Meanwhile, the nepotism and altruism could be formed when the CEO position and board directors’ position are both occupied by internal family members (Miller et al., Citation2015). Under this situation, a series of excessive costs like free riding costs and perquisites may occur (Schepers et al., Citation2014), which will potentially reduce family businesses’ resources/funding which could have been invested in those innovative/R&D projects. Based on above, the third hypothesis of this study could be proposed:

Hypothesis 3: Compared with having a professional manager as the CEO, the inhibiting effect of family board involvement on the relationship between CEO power and innovative investment is more reflected in those family firms with a family member serving as the CEO.

The research model of this study is presented as

2. Data and methods

2.1. Data source and sample

This paper collected and analysed data from listed Chinese family SMEs recorded in Chinese Stock Market & Accounting Research (CSMAR) database. CSMAR is a high-quality database and has been widely used in past Chinese business studies (Chi et al., Citation2010; Li et al., Citation2014; Truong, Citation2011) since it has consolidated a comprehensive collection of statistics regarding Chinese listed enterprises. In this paper, Chinese firms listed in the 2015–2019 SME board were sampled. The study population of this study includes 1536 listed firms in Chinese SME board. The sampling process is as below: (a) Selecting the firms whose actual controllers are families (Campopiano et al., Citation2014); (b) Excluding those enterprises where the controlling shareholders’ equity is less than 5% (Choi et al., Citation2015); (c) Screening the listed family enterprises across different industries according to the criteria of Chinese SMEs. For instance, in manufacturing industry, the employee number in the chosen company should be between 20 and 1000 (Prange & Zhao, Citation2018); (d) Since R&D investment is not mandatory data for public disclosure, the enterprises with insufficient data required for this study were excluded during the sampling process. By above process, this study obtained 1079 firm-year observations.

3. Measurement

3.1. Independent variable

CEO power is used as the independent variable in this study. Finkelstein (Citation1992) divided the power of top management team into four dimensions including structural power, ownership power, expert power and prestige power. Based on prior studies (Korkeamäki et al., Citation2017; Victoravich et al., Citation2011; Yang & Liu, Citation2017), this study selected four dummy variables corresponding to above four dimensions to measure a firm’s CEO power. Specifically, each sample firm’s CEO power is measured by the average of the four dummy variables in this study. Below Table showed the classification and interpretation of dummy variables. In this study, the CEO information was manually collected and consolidated through the prospectus of sample listed family firms. In China, the prospectuses of listed firms are required to be open to public, and they can be accessed via the China Securities Regulatory Commission (CSRC) website (http://www.csrc.gov.cn). CSRC is the only government agency responsible for enforcing security laws and regulations in Chinese stock market (Chen et al., Citation2005).

3.2. Dependent variable

In this paper, the innovative input of family SMEs is the dependent variable, and it is measured as the ratio of a firm’s R&D expenditure to total sales (Coad & Rao, Citation2010; Kim, Citation2018; Zantout & Tsetsekos, Citation1994). Matzler et al. (Citation2015) suggested that R&D spending could be considered as an appropriate indicator to measure a firm’s innovative capability.

3.3. Moderating variables

Family board involvement is the moderating variable in this study. To be consistent with prior studies (Matzler et al., Citation2015), the degree of family board involvement is measured as the ratio of the number of family members sitting on the firm’s board to the total number of board directors. As the same way of collecting the CEO information, the number of family members in the board and the total number of board directors are both manually collected from sample family firms’ prospectuses.

3.4. Control variables

There are many factors affecting enterprises’ R&D investment, and control variables can effectively control the influence of other factors on family SMEs’ innovative investment. Following prior studies, this study controlled the following variables: firm size, firm age, financial leverage, return on assets and sales growth (Haider & Fang, Citation2018; Kotlar et al., Citation2014; Matzler et al., Citation2015). The firm size is computed as the natural logarithm of the sample firms. The firm age is measured as the difference between the date of the recorded statistics in the database and the year when the enterprise was established. The financial leverage is measured as the asset-liability ratio. The sales growth is measured as the logarithm of current sales minus last year’s sales divided by last year’s sales. In addition, this study also controlled the industry and year as dummy variables. The measurements of all kinds of variables are concluded in below Table .

4. Analysis and results

4.1. Descriptive statistics and correlation coefficients

In this part, the descriptive statistic and correlations of variables are provided in Tables , respectively. Table depicts a basic statistical summary of all variables, including mean value, standard deviation, minimum value and maximum value. The datasets include 1079 firm-year observations. The average ratio of family members on the board to all board members is 31%. The average innovative/R&D investment of sample firms is 5.2%, the maximum value is 26.15%, and the minimum value is 0.07%. It can be seen that the intensity of innovative investment of sample firms varies greatly.

The correlation coefficients showed in Table reveal that CEO power is positively associated with a family firm’s innovative investment (r = 0.22, p < 0.01), which initially confirm the hypothesis 1 of this study. In addition, it can be seen that the family board involvement could have a negative influence on a family firm’s innovative expenditure (r = −0.06, p < 0.05). All the correlations are less than 0.5, which indicates that multicollinearity is not a problem in this study.

4.2. Regression results

This study firstly investigates the influence of CEO power on a family firm’s innovative investment, then investigates the moderating effect of family board involvement on above relationship, and finaly tests if the CEO source could influence the results. Below Table reports a set of hierarchical multiple regression analysis results. Model 1 is the baseline model, which includes all the control variables. Model 2 adds the CEO power as the independent variable. The regression results of Model 2 reveal that the influence of CEO power on innovative investment is posituve and significant (β = 0.69, p < 0.01), indicating that the stronger CEO power will enhance a family SMEs’ innovative investment. Therefore, the hypthesis 1 of this study is well supported.

For the purpose of testing the moderating effect of family board involvement on the relationship between CEO power and innovatiev investment, the interation term (Power×Fb) is entered at Model 3. The regression results in Model 3 showed that the interation term (Power ×Fb) has a significant influence on a family SMEs’ innovative expenditure (β = −0.15, p < 0.01). This result indicates that the family board involvement could weaken the postive relationship between CEO power and R&D investment. Thus, the hypothesis 2 of this study is supported.

In below Table , a set of regression analysis were conducted to test if the moderating effect of family board involvement differs under different source of CEO. Specifically, Model 4 and Model 5 in Table tested the influence of professioanl CEO power and family CEO power on a family SMEs’ innovative investment, respectively. The results show that both family CEO power and professional CEO power positively affect a family firm’s innovative investment (β = 0.69, p < 0.01, β = 0.33, p < 0.05, repectively).

Further, Model 6 and Model 7 in Table tested the moderating effect of family board involvement under different CEO sources. The results in Model 6 show that the interaction term “CEO power ×Fb” did not have a significant influence on family firm’s innovative investment (β = −0.02, ns), which indicates the moderating effect of family board involvement on the relationship between CEO power and R&D expenditure is relatively weak when an external professional manager is appointed as the CEO of the family firms. The results in Model 7 reveal that the interaction term “CEO power ×Fb” has a significant influence on a family firm’s innovative investment (β = −0.07, p < 0.01), which means the moderating effect of family board involvement is significant when a family member is appointed as the CEO of the family firms.

Based on above, it could be concluded that the positive effect of CEO power on innovative investment will be inhibited by family board involvement if a family firm’s CEO is an internal family member. Thus, the hypothesis 3 of this study is supported.

5. Discussion

The empirical results provide strong evidence to confirm the three hypotheses proposed by this study. Firstly, the positive relationship between CEO power and innovative investment under the Chinese family SME context. The confirmation of hypothesis 1 strongly supports the viewpoint of stewardship theory (Davis et al., Citation1997), which implies the CEO, whatever internal or external, tend to behave as a dedicated steward in the fmaily enterprise when he/she has more authority and power in the CEO positon. Both family and professioanl CEO tend to exert their power to conduct more innovative investment, and maximize their unility to achieve organizationl success rather than personal interests. Further, the finding regarding positive impact of external/professional CEOs’ power on R&D expenditure challenges the viewpoint of principle-agency theory (Block, Citation2012; Fong, Citation2010) which imples the agency conflict between shareholders and external managers will neagtively affect a firm’s innovative investment. Besides, the positive relationship between CEO power and innovative investment can also be linked to previous findings based on incentive theory (Francis et al., Citation2011; Hagendorff & Vallascas, Citation2011; Lin et al., Citation2011). For instance, Francis et al. (Citation2011) study found that the CEO who received abundant compensation and equity compared to other executives is more likely to make risky innovative strategies which could bring huge long-term success to the companies.

Secondly, the hypothesis 2 regarding the moderating effect of family board involvement is confirmed. This result is in line with previous studies’ findings based on socio-emotional wealth perspective (Gómez-Mejía et al., Citation2007), and provides further evidence that family firms’ priority of preserving socio-emotional wealth could inhibt firms’ risk-taking behaviors. If family members are involved in the board of a family firm, they are more likely to put the achievement of non-economic/socio-emotional goals (e.g., family identification and reputation) at the first position (Deephouse & Jaskiewicz, Citation2013), and thus tend to prevent conducting risky innovative startegies/investments that may be more in line with a family firm’s long-term economic interests.

Thirdly, the findings of this study also support the hypothesis 3 which is an extension of hypothesis 2. The inhibiting effect of family board involvement on the relationship between CEO power and innovative investment is mainly reflected while a famiy member serving as the CEO. This results confirm a potential negative effect of family social ties on a family firm’s decision-making. Some prior studies noted that internal family social capital usually has a positive influence on family cohesivess (Salvato & Melin, Citation2008), and also enhace family firms’ competitiveness (Chang et al., Citation2009). However, this paper provides a promsing perspective and a evidence to prove that family ties/cohesiveness could potentially hinder a family firm’s strategic adaptation since the interact effect of family CEO and family board involvement will significantly reduce a family firm’s innovative investments, which may bring huge success to the family firms in the long term. The confirmation of H3 of this study is in line with existing studies (Shi & Wu, Citation2021; Van den Heuvel et al., Citation2006) that contend that the altruistic behaviours due to family board involvement will reduce family firms’ cash flow used to conduct R&D projects.

Further, the empirical evidence regarding H3 could be explained by the supervisory role of family board directors. Anderson and Reeb (Citation2004) study suggested that having independent board directors is necessary for a family-owned business, because a board dominated by internal family members will be less effective in monitoring the behaviors of family top managers/CEOs. Although many existing studies based on agency theory suggested that family networks bind the family members together and boost loyalty among family members, which may lead to a willingness of some family CEOs to abandon “on the job” consumption (James, Citation1999; Sanchez-Ruiz et al., Citation2019), some other studies argued that the altruism and nepotism among internal family members may lead to excessive company-paid private consumption (Kappes & Schmid, Citation2013), thereby increasing agency costs and reduing the resources used to conduct R&D projects. The findings from this empirical study well supports the latter view. Thus, in a part of family firms where the internal family CEOs’ opportunistic behaviors and resource abuse are severe, the potential fundings/resources that might be used for developing long-term innovative strategies will be eroded due to the weak supervision of internal family board directors.

6. Conclusions and contributions

This paper provides promising insight related to the relationship between CEO power and innovative investment under a context of family SMEs, and innovatively investigates how the family board involvment affects the relationship between CEO power and innovative investment under different CEO sources. Using sample firms listed on the Chinese SME board, this empirical study confirmed the positve effect of CEO power on Chines family SMEs’ innovative investment, as well as the inhibiting effect of family board involvement on above relationship. Besides, this study also found the interaction of family CEO power and family board involvement will have a neagtive impact on a family firm’s innovative investment.

The theoretical contributions of this study are as following: Firstly, this study provides a promising research model among three variables including CEO power, innovative investment and family board involvement, investigating how family board involvement affects the relationship between CEO power and innovative investment under a family SME context. As a result, the inhibiting effect of family board involvement differs under different CEO sources. Unlike previous studies that widely employed mere presence of family CEO as the antecedent of innovative investment, by applying the four dimensions of CEO power (see, Table ), this study tries to answer Weismeier-Sammer et al. (Citation2013) call to investigate family CEO’s actual influence on innovative strategies. Therefore, this study opens a promising avenue to explore how those unique features of family businesses-familiness construct (Frank et al., Citation2017; Zellweger et al., Citation2010) can influence innovative investment.

Secondly, sicne the CEO’s tendency to condcut more innovative investment will be diminished when the CEO and board directors come from the same family group, this study contributes to the literature regarding the dark side of SEW (Kellermanns et al., Citation2012). Specifically, this study questioned the positive influence of family social network which is considered as one of the components of SEW (Berrone et al., Citation2012). Many exsiting studies emphasized the positive effect of family social network on a family firm’s long-term development since family members usually share common history, culture and family background, which makes the information exchange more efficiently within family firms (Adler & Kwon, Citation2002; Herrero, Citation2018; Nahapiet & Ghoshal, Citation1998). However, the empirical findings of this study reveal that a family firm’s R&D activities/programs will be reduced by family board involvement if a family member is appointed as the CEO, which implies a negative firm outcome caused by family social ties between family CEO and family board directors. Thus, based on the results from prior studies and this study, family social capital has been proved to be a ‘double-edge sword’for a family firm’s long-term development.

Besides, the confirmation of H1 and H3 of this study offers an insight to effectively challenge the traditional viewpoint regarding principal-agency conflicts (Claessens et al., Citation2000; Fang et al., Citation2017) under a family SME context. In contrast to those family CEOs whose decision-making process can be interfered by board directors, the finding of this study demonstrated that those external hired professional CEOs will conduct more innovative investment as their power grows in family firms, and this positive effect cannot even be interfered by internal family board directors. Consistent with stewardship theory, this finding implies that the professional CEOs in family firms are more likely to put organisation’s long-term objectives ahead of their personal interests. If they were given sufficient authority and discretion, external hired professional CEOs will try to maximize shareholders’ benefits, and assist family firms to achieve long-term prosperity. Besides, this findings also consolidated organisational identity theory in a family business context. A stronger organisational identity implies that the organisation might becomes an extension of employees’ self, thus creating the sense of “oneness” which will positively affect employees’ attitudes and actions toward their work (Ashforth & Mael, Citation1996). In the context of family business, the findings of this study is in line with Zellweger et al. (Citation2010) research which condent that non-family managers will behave as a loyal and dedicated steward once they embrace the beliefs and long-term goals of the family, indicating that a strong family business identity has been established.

As for the practical implication, the finding of this paper could effectively help more family firms, especially those Chinese family SMEs to achieve success. The inhibiting effect of family board involvement on the relationship between family CEO power and innovativeinvestment implies that the resource abuse caused by family nepotism cannot be neglected by Chinese family SMEs. In addition, since the finding showed that family board involvement will significantly weaken the positive effect of CEO power on innovative startegies, the degree of the involvement of family board directors should be kept relatively lower than before.

7. Limitations and future directions

Some limitations in this paper should be noted: Firstly, this study only selected Chinese listed family SMEs as the research sample, which imples the results obtained from this study may not be generalisable to larder-sized enterprise. Secondly, this empirical study only focus on Chinese family firms, which indicates the results could only apply to the family business in China but not to family enterprises in other countries. Further, this study uses R&D spendings as the only dependent variable. Although R&D investment is commonly used in previous studies to indicate a firm’s competitiveness and innovative capability (Chen, Citation2014; Matzler et al., Citation2015), some more dependent variables (e.g R&D output and other financial firm performance) could be applied into the theoretical model of this study in future studies. Besides, this study only selected four dummy variables corresponding to four CEO power dimensions (ownership power, prestige power, expert power and structual power) to measure a sample family firms’ CEO power, more dimensions/variables related with CEO power could be comprehensively explored in future research to enrich the study of antecedent of family firms’ innovative strategies.

Disclosure statement

On behalf of all authors, the corresponding author states that there is no conflict of interest.

Additional information

Funding

References

- Adams, R., Bessant, J., & Phelps, R. (2006). Innovation management measurement: A review. International Journal of Management Reviews, 8(1), 21–16. https://doi.org/10.1111/j.1468-2370.2006.00119.x

- Adler, P. S., & Kwon, S.-W. (2002). Social capital: Prospects for a new concept. Academy of Management Review, 27(1), 17–40. https://doi.org/10.5465/amr.2002.5922314

- Ahmad, Z., & Yaseen, M. R. (2018). Moderating role of education on succession process in small family businesses in Pakistan. Journal of Family Business Management, 8(3), 293–305. https://doi.org/10.1108/JFBM-12-2017-0041

- Anderson, R. C., & Reeb, D. M. (2004). Board composition: Balancing family influence in S&P 500 firms. Administrative Science Quarterly, 49(2), 209–237. https://doi.org/10.2307/4131472

- Ashforth, B. E., & Mael, F. A. (1996). Organizational Identity and Strategy as a Context for the Individual. Advances in Strategic Management, 13(2), 19–64. https://doi.org/10.1177/0149206308316059

- Bammens, Y., Voordeckers, W., & Van Gils, A. (2008). Boards of directors in family firms: A generational perspective. Small Business Economics, 31(2), 163–180. https://doi.org/10.1007/s11187-007-9087-5

- Barker, V. L., III, & Mueller, G. C. (2002). CEO characteristics and firm R&D spending. Management Science, 48(6), 782–801. https://doi.org/10.1287/mnsc.48.6.782.187

- Belderbos, R., Carree, M., & Lokshin, B. (2004). Cooperative R&D and firm performance. Research Policy, 33(10), 1477–1492. https://doi.org/10.1016/j.respol.2004.07.003

- Bent, R., & Seaman, C. (2017). The role of family values in the integrity of family business Marc, Orlitzky. In Integrity in business and management (pp. 109–122). Routledge.

- Berrone, P., Cruz, C., & Gomez-Mejia, L. R. (2012). Socioemotional wealth in family firms: Theoretical dimensions, assessment approaches, and agenda for future research. Family Business Review, 25(3), 258–279. https://doi.org/10.1177/0894486511435355

- Block, J. H. (2012). R&D investments in family and founder firms: An agency perspective. Journal of Business Venturing, 27(2), 248–265. https://doi.org/10.1016/j.jbusvent.2010.09.003

- Borokhovich, K. A., Parrino, R., & Trapani, T. (1996). Outside directors and CEO selection. Journal of Financial and Quantitative Analysis, 31(3), 337–355. https://doi.org/10.2307/2331395

- Campopiano, G., De Massis, A., & Chirico, F. (2014). Firm philanthropy in small-and medium-sized family firms: The effects of family involvement in ownership and management. Family Business Review, 27(3), 244–258. https://doi.org/10.1177/0894486514538450

- Carney, M., Zhao, J., & Zhu, L. (2019). Lean innovation: Family firm succession and patenting strategy in a dynamic institutional landscape. Journal of Family Business Strategy, 10(4), 100247. https://doi.org/10.1016/j.jfbs.2018.03.002

- Chang, E. P., Memili, E., Chrisman, J. J., Kellermanns, F. W., & Chua, J. H. (2009). Family social capital, venture preparedness, and start-up decisions: A study of Hispanic entrepreneurs in New England. Family Business Review, 22(3), 279–292. https://doi.org/10.1177/0894486509332327

- Chen, H. L. (2014). Board capital, CEO power and R&D investment in electronics firms. Corporate Governance: An International Review, 22(5), 422–436. https://doi.org/10.1111/corg.12076

- Chen, G., Firth, M., Gao, D. N., & Rui, O. M. (2005). Is China’s securities regulatory agency a toothless tiger? Evidence from enforcement actions. Journal of Accounting and Public Policy, 24(6), 451–488. https://doi.org/10.1016/j.jaccpubpol.2005.10.002

- Chen, Y.-M., Liu, -H.-H., Yang, Y.-K., & Chen, W.-H. (2016). CEO succession in family firms: Stewardship perspective in the pre-succession context. Journal of Business Research, 69(11), 5111–5116. https://doi.org/10.1016/j.jbusres.2016.04.089

- Chi, J., Wang, C., & Young, M. (2010). Long-run outperformance of Chinese initial public offerings. Chinese Economy, 43(5), 62–88. https://doi.org/10.2753/CES1097-1475430505

- Choi, Y. R., Zahra, S. A., Yoshikawa, T., & Han, B. H. (2015). Family ownership and R&D investment: The role of growth opportunities and business group membership. Journal of Business Research, 68(5), 1053–1061. https://doi.org/10.1016/j.jbusres.2014.10.007

- Claessens, S., Djankov, S., & Lang, L. H. (2000). The separation of ownership and control in East Asian corporations. Journal of Financial Economics, 58(1–2), 81–112. https://doi.org/10.1016/S0304-405X(00)00067-2

- Coad, A., & Rao, R. (2010). Firm growth and R&D expenditure. Economics of Innovation and New Technology, 19(2), 127–145. https://doi.org/10.1080/10438590802472531

- Combs, J. G., Ketchen, D. J., Jr, Perryman, A. A., & Donahue, M. S. (2007). The moderating effect of CEO power on the board composition–firm performance relationship. Journal of Management Studies, 44(8), 1299–1323. http://doi.org/10.1111/j.1467-6486.2007.00708.x

- Corbetta, G., & Salvato, C. A. (2004). The board of directors in family firms: One size fits all? Family Business Review, 17(2), 119–134. https://doi.org/10.1111/j.1741-6248.2004.00008.x

- Crossland, C., Zyung, J., Hiller, N. J., & Hambrick, D. C. (2014). CEO career variety: Effects on firm-level strategic and social novelty. Academy of Management Journal, 57(3), 652–674. https://doi.org/10.5465/amj.2012.0469

- Daily, C. M., & Johnson, J. L. (1997). Sources of CEO power and firm financial performance: A longitudinal assessment. Journal of Management, 23(2), 97–117. https://doi.org/10.1177/014920639702300201

- Davis, J. H., Schoorman, F. D., & Donaldson, L. (1997). Toward a stewardship theory of management. Academy of Management Review, 22(1), 20–47. https://doi.org/10.2307/259223

- Deephouse, D. L., & Jaskiewicz, P. (2013). Do family firms have better reputations than non‐family firms? An integration of socioemotional wealth and social identity theories. Journal of Management Studies, 50(3), 337–360. https://doi.org/10.1111/joms.12015

- Driver, C., & Guedes, M. J. C. (2012). Research and development, cash flow, agency and governance: UK large companies. Research Policy, 41(9), 1565–1577. https://doi.org/10.1016/j.respol.2012.04.003

- Duran, P., Kammerlander, N., Van Essen, M., & Zellweger, T. (2016). Doing more with less: Innovation input and output in family firms. Academy of Management Journal, 59(4), 1224–1264. https://doi.org/10.5465/amj.2014.0424

- Fang, H. C., Memili, E., Chrisman, J. J., & Penney, C. (2017). Industry and information asymmetry: The case of the employment of non‐family managers in small and medium‐sized family firms. Journal of Small Business Management, 55(4), 632–648. https://doi.org/10.1111/jsbm.12267

- Finkelstein, S. (1992). Power in top management teams: Dimensions, measurement, and validation. Academy of Management Journal, 35(3), 505–538. http://doi.org/10.5465/256485

- Fong, E. A. (2010). Relative CEO underpayment and CEO behaviour towards R&D spending. Journal of Management Studies, 47(6), 1095–1122. https://doi.org/10.1111/j.1467-6486.2009.00861.x

- Francis, B. B., Hasan, I., & Sharma, Z. SSRN (2011). Incentives and innovation: Evidence from CEO compensation contracts. Bank of Finland Research Discussion Paper(17).

- Frank, H., Kessler, A., Rusch, T., Suess–Reyes, J., & Weismeier–Sammer, D. (2017). Capturing the familiness of family businesses: Development of the family influence familiness scale (FIFS). Entrepreneurship Theory and Practice, 41(5), 709–742. https://doi.org/10.1111/etap.12229

- Fuetsch, E., & Suess-Reyes, J. (2017). Research on innovation in family businesses: Are we building an ivory tower? Journal of Family Business Management, 7(1), 44–92. https://doi.org/10.1108/JFBM-02-2016-0003

- Gibb Dyer, W., Jr. (2006). Examining the “family effect” on firm performance. Family Business Review, 19(4), 253–273. https://doi.org/10.1111/j.1741-6248.2006.00074.x

- Gomez–Mejia, L. R., Campbell, J. T., Martin, G., Hoskisson, R. E., Makri, M., & Sirmon, D. G. (2014). Socioemotional wealth as a mixed gamble: Revisiting family firm R&D investments with the behavioral agency model. Entrepreneurship Theory and Practice, 38(6), 1351–1374. https://doi.org/10.1111/etap.12083

- Gómez-Mejía, L. R., Haynes, K. T., Núñez-Nickel, M., Jacobson, K. J., & Moyano-Fuentes, J. (2007). Socioemotional wealth and business risks in family-controlled firms: Evidence from Spanish olive oil mills. Administrative Science Quarterly, 52(1), 106–137. https://doi.org/10.2189/asqu.52.1.106

- Hagendorff, J., & Vallascas, F. (2011). CEO pay incentives and risk-taking: Evidence from bank acquisitions. Journal of Corporate Finance, 17(4), 1078–1095. https://doi.org/10.1016/j.jcorpfin.2011.04.009

- Haider, J., & Fang, H.-X. (2018). CEO power, corporate risk taking and role of large shareholders. Journal of Financial Economic Policy, 10(1), 55–72. https://doi.org/10.1108/JFEP-04-2017-0033

- Herrero, I. (2018). How familial is family social capital? Analyzing bonding social capital in family and nonfamily firms. Family Business Review, 31(4), 441–459. https://doi.org/10.1177/0894486518784475

- Jacob, M. A. (2009). The shared history: Unknotting fictive kinship and legal process. Law & Society Review, 43(1), 95–126. https://doi.org/10.1111/j.1540-5893.2009.00368.x

- James, H. S. (1999). Owner as manager, extended horizons and the family firm. International Journal of the Economics of Business, 6(1), 41–55. https://doi.org/10.1080/13571519984304

- Jiang, F., Shi, W., & Zheng, X. (2020). Board chairs and R&D investment: Evidence from Chinese family-controlled firms. Journal of Business Research, 112(2), 109–118. https://doi.org/10.1016/j.jbusres.2020.02.026

- Kang, H. C., & Kim, J. (2016). Why do family firms switch between family CEOs and non-family professional CEO? Evidence from Korean Chaebols. Review of Accounting and Finance, 15(1), 45–64. https://doi.org/10.1108/RAF-03-2015-0032

- Kappes, I., & Schmid, T. (2013). The effect of family governance on corporate time horizons. Corporate Governance: An International Review, 21(6), 547–566. http://doi.org/10.1111/corg.12040

- Kellermanns, W., Eddleston, K., & Zellweger, T. (2012). Extending the socioemotional wealth perspective: A look at the dark. Entrepreneurship Theory and Practice, 36(6), 1175–1182. https://doi.org/10.1111/j.1540-6520.2012.00544.x

- Kelly, J., & Gennard, J. (2007). Business strategic decision making: The role and influence of directors. Human Resource Management Journal, 17(2), 99–117. https://doi.org/10.1111/j.1748-8583.2007.00038.x

- Killeen, P. R. (1981). Incentive theory. Nebraska symposium on motivation,

- Kim, H. (2018). evidence on the optimal level of research & development (R&D) expenses for KOSPI-listed firms in the domestic capital market. Journal of International Trade & Commerce, 14(1), 147–165. http://doi.org/10.16980/jjtc.14.1.201802.147

- Korkeamäki, T., Liljeblom, E., & Pasternack, D. (2017). CEO power and matching leverage preferences. Journal of Corporate Finance, 45(3), 19–30. https://doi.org/10.1016/j.jcorpfin.2017.04.007

- Kotlar, J., De Massis, A., Fang, H., & Frattini, F. (2014). Strategic reference points in family firms. Small Business Economics, 43(3), 597–619. https://doi.org/10.1007/s11187-014-9556-6

- Lee, J.-S., & Hsieh, C.-J. (2010). A research in relating entrepreneurship, marketing capability, innovative capability and sustained competitive advantage. Journal of Business & Economics Research (JBER), 8(9), 26–38. https://doi.org/10.19030/jber.v8i9.763

- Lewellyn, K. B., & Muller‐Kahle, M. I. (2012). CEO power and risk taking: Evidence from the subprime lending industry. Corporate Governance: An International Review, 20(3), 289–307. https://doi.org/10.1111/j.1467-8683.2011.00903.x

- Lewin, A. Y., & Stephens, C. U. (1994). CEO attitudes as determinants of organization design: An integrated model. Organization Studies, 15(2), 183–212. https://doi.org/10.1177/017084069401500202

- Li, M. L., Chui, C. M., & Li, C. Q. (2014). Is pairs trading profitable on China AH-share markets? Applied Economics Letters, 21(16), 1116–1121. https://doi.org/10.1080/13504851.2014.912030

- Lin, Y. F. (2005). Corporate governance, leadership structure and CEO compensation: Evidence from Taiwan. Corporate Governance: An International Review, 13(6), 824–835. https://doi.org/10.1111/j.1467-8683.2005.00473.x

- Lin, S. H., & Hu, S. Y. (2007). A family member or professional management? The choice of a CEO and its impact on performance. Corporate Governance: An International Review, 15(6), 1348–1362. https://doi.org/10.1111/j.1467-8683.2007.00650.x

- Lin, C., Lin, P., Song, F. M., & Li, C. (2011). Managerial incentives, CEO characteristics and corporate innovation in China’s private sector. Journal of Comparative Economics, 39(2), 176–190. https://doi.org/10.1016/j.jce.2009.12.001

- Lionzo, A., & Rossignoli, F. (2013). Knowledge integration in family SMEs: An extension of the 4I model. Journal of Management & Governance, 17(3), 583–608. https://doi.org/10.1007/s10997-011-9197-y

- Lodh, S., Nandy, M., & Chen, J. (2014). Innovation and family ownership: Empirical evidence from I ndia. Corporate Governance: An International Review, 22(1), 4–23. https://doi.org/10.1111/corg.12034

- Luo, J.-H., Li, X., Wang, L. C., & Liu, Y. (2019). Owner type, pyramidal structure and R&D investment in China’s family firms. Asia Pacific Journal of Management, 5, 1–27. http://doi.org/10.1007/s10490-019-09702-z

- Matzler, K., Veider, V., Hautz, J., & Stadler, C. (2015). The impact of family ownership, management, and governance on innovation. Journal of Product Innovation Management, 32(3), 319–333. https://doi.org/10.1111/jpim.12202

- Miller, D., & Le Breton-Miller, I. (2006). Family governance and firm performance: Agency, stewardship, and capabilities. Family Business Review, 19(1), 73–87. https://doi.org/10.1111/j.1741-6248.2006.00063.x

- Miller, D., Wright, M., Breton-Miller, I. L., & Scholes, L. (2015). Resources and innovation in family businesses: The Janus-face of socioemotional preferences. California Management Review, 58(1), 20–40. http://doi.org/10.1525/cmr.2015.58.1.20

- Munari, F., Oriani, R., & Sobrero, M. (2010). The effects of owner identity and external governance systems on R&D investments: A study of Western European firms. Research Policy, 39(8), 1093–1104. https://doi.org/10.1016/j.respol.2010.05.004

- Nahapiet, J., & Ghoshal, S. (1998). Social capital, intellectual capital, and the organizational advantage. Academy of Management Review, 23(2), 242–266. https://doi.org/10.5465/amr.1998.533225

- Patel, P. C., & Chrisman, J. J. (2014). Risk abatement as a strategy for R&D investments in family firms. Strategic Management Journal, 35(4), 617–627. https://doi.org/10.1002/smj.2119

- Prange, C., & Zhao, Y. (2018). Strategies for internationalisation: How Chinese SMEs deal with distance and market entry speed Noemie, Dominguez. In Key success factors of SME internationalisation: A Cross-Country Perspective. Emerald Publishing Limited, 205–224.

- Salvato, C., & Melin, L. (2008). Creating value across generations in family-controlled businesses: The role of family social capital. Family Business Review, 21(3), 259–276. https://doi.org/10.1177/08944865080210030107

- Sanchez-Ruiz, P., Daspit, J. J., Holt, D. T., & Rutherford, M. W. (2019). Family social capital in the family firm: A taxonomic classification, relationships with outcomes, and directions for advancement. Family Business Review, 32(2), 131–153. https://doi.org/10.1177/0894486519836833

- Schepers, J., Voordeckers, W., Steijvers, T., & Laveren, E. (2014). The entrepreneurial orientation–performance relationship in private family firms: The moderating role of socioemotional wealth. Small Business Economics, 43(1), 39–55. https://doi.org/10.1007/s11187-013-9533-5

- Schulze, W. S., Lubatkin, M. H., & Dino, R. N. (2003). Toward a theory of agency and altruism in family firms. Journal of Business Venturing, 18(4), 473–490. https://doi.org/10.1016/S0883-9026(03)00054-5

- Sciascia, S., Nordqvist, M., Mazzola, P., & De Massis, A. (2015). Family ownership and R&D intensity in small‐and medium‐sized firms. Journal of Product Innovation Management, 32(3), 349–360. https://doi.org/10.1111/jpim.12204

- Sheikh, S. (2018). The impact of market competition on the relation between CEO power and firm innovation. Journal of Multinational Financial Management, 44(3), 36–50. https://doi.org/10.1016/j.mulfin.2018.01.003

- Sher, P. J., & Yang, P. Y. (2005). The effects of innovative capabilities and R&D clustering on firm performance: The evidence of Taiwan’s semiconductor industry. Technovation, 25(1), 33–43. https://doi.org/10.1016/S0166-4972(03)00068-3

- Shi, Y., & Wu, Z . (2021). Familial altruism and reputation risk: Evidence from China. China Finance Review International, 3(2), 123–129. http://doi.org/10.1108/CFRI-01-2021-0016

- Sun, K. (2019). The construction of quantitative research on evaluation of independent innovation ability of small and medium-sized industrial enterprises. 2019 International conference on robots & intelligent system (ICRIS) Haikou, China (IEEE)

- Thong, J. Y. (1999). An integrated model of information systems adoption in small businesses. Journal of Management Information Systems, 15(4), 187–214. https://doi.org/10.1080/07421222.1999.11518227

- Thong, J. Y., & Yap, C.-S. (1995). CEO characteristics, organizational characteristics and information technology adoption in small businesses. Omega, 23(4), 429–442. https://doi.org/10.1016/0305-0483(95)00017-I

- Tian, J., Haleblian, J., & Rajagopalan, N. (2011). The effects of board human and social capital on investor reactions to new CEO selection. Strategic Management Journal, 32(7), 731–747. https://doi.org/10.1002/smj.909

- Tishler, A. (2008). How risky should an R&D program be? Economics Letters, 99(2), 268–271. https://doi.org/10.1016/j.econlet.2007.07.006

- Truong, C. (2011). Post-earnings announcement abnormal return in the Chinese equity market. Journal of International Financial Markets, Institutions and Money, 21(5), 637–661. https://doi.org/10.1016/j.intfin.2011.04.002

- Van den Heuvel, J., Van Gils, A., & Voordeckers, W. (2006). Board roles in small and medium‐sized family businesses: Performance and importance. Corporate Governance: An International Review, 14(5), 467–485. https://doi.org/10.1111/j.1467-8683.2006.00519.x

- Victoravich, L., Buslepp, W. L., Xu, T., & Grove, H. (2011 (SSRN)). CEO power, equity incentives, and bank risk taking. Available at SSRN 1909547.

- Voordeckers, W., Van Gils, A., & Van den Heuvel, J. (2007). Board composition in small and medium‐sized family firms. Journal of Small Business Management, 45(1), 137–156. https://doi.org/10.1111/j.1540-627X.2007.00204.x

- Wakelin, K. (2001). Productivity growth and R&D expenditure in UK manufacturing firms. Research Policy, 30(7), 1079–1090. https://doi.org/10.1016/S0048-7333(00)00136-0

- Weismeier-Sammer, D., Frank, H., & von Schlippe, A. (2013). Untangling ‘familiness’ A literature review and directions for future research. The International Journal of Entrepreneurship and Innovation, 14(3), 165–177. https://doi.org/10.5367/ijei.2013.0119

- Westphal, J. D. (1999). Collaboration in the boardroom: Behavioral and performance consequences of CEO-board social ties. Academy of Management Journal, 42(1), 7–24. http://doi.org/10.5465/256871

- Yang, S.-L., & Liu, X.-F. (2017). The empirical study on CEO power and investment efficiency. 3rd Annual international conference on management, economics and social development (ICMESD 17) Guangzhou, China (Atlantis Press)

- Yang, J., Ma, J., & Doty, D. H. (2020). Family involvement, governmental connections, and IPO underpricing of SMEs in China. Family Business Review, 33(2), 175–193. https://doi.org/10.1177/0894486520905180

- Zantout, Z. Z., & Tsetsekos, G. P. (1994). The wealth effects of announcements of R&D expenditure increases. Journal of Financial Research, 17(2), 205–216. https://doi.org/10.1111/j.1475-6803.1994.tb00186.x

- Zellweger, T. M., Eddleston, K. A., & Kellermanns, F. W. (2010). Exploring the concept of familiness: Introducing family firm identity. Journal of Family Business Strategy, 1(1), 54–63. https://doi.org/10.1016/j.jfbs.2009.12.003

- Zellweger, T. M., Kellermanns, F. W., Chrisman, J. J., & Chua, J. H. (2012). Family control and family firm valuation by family CEOs: The importance of intentions for transgenerational control. Organization Science, 23(3), 851–868. https://doi.org/10.1287/orsc.1110.0665

- Zhu, Y., Wittmann, X., & Peng, M. W. (2012). Institution-based barriers to innovation in SMEs in China. Asia Pacific Journal of Management, 29(4), 1131–1142. https://doi.org/10.1007/s10490-011-9263-7