?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The study examines the extent to which value added tax (VAT) receipts could cause industrial sector performance. Several studies on the influence of VAT on economic expansion have been conducted without specific focus on industry output. This study uses secondary data from 2010 to 2021 to evaluate the causation effect of VAT proceeds on industry productivity in Nigeria. The dependent variable employed is the manufacturing output while the independent factors include: import VAT, domestic VAT and the aggregate VAT receipts. The study applies Pairwise Granger Causality Tests which show that the local VAT returns and the aggregate VAT collection exhibit positive and strong causation effects on manufacturing output. We also test for relationship among the study elements, the results also show the existence of strong connection among the study variables. We conclude that VAT is indeed a growth factor to the industry performance in the country. Among all the proposals made in this study, there is need for the government to technologically improve the supply chain in order to boost VAT revenue collection and enhance infrastructural provision that will benefit the industrial sector for a more efficient productivity. It is very crucial for the government to checkmate unofficial industries that prevent the flow of VAT revenue into the government treasury.

1. Introduction

Value Added Tax (VAT) is a sort of indirect tax whereby an amount of funding is charged at every phase of a product’s or service’s production and delivery. VAT is a utilization tax that is levied when items are bought and care is provided. VAT is a multi-stage tax paid by the end customer (Omodero, Citation2020). According to Okoye and Gbegi (Citation2013), the Value Added Tax system was created in 1954 by Maurice Laure, then Joint Director of the French Tax Agency. However a German businessman Wilhelm Van Siemens suggested the notion in 1918, but value added tax scheme was applied for the very first time on 10 April 1954. Since then, other governments throughout the world have embraced the value added taxation system.VAT is presently administered in Nigeria by Federal Inland Revenue Service and the statue governing it the Value Added Tax Act Cap V1, LFN 2004 (as modified). The implementation of VAT in Nigeria by Decree 102 of 1993 signals the end of the Sales Tax Decree No. 7 of 1986. The Decree went into force on 1 December 1993, and began operative in Nigeria on 1 January 1994. Until the modification in 2021 based on the provisions of the Finance Act, 2020, VAT was paid at a flat rate of 5% on specified items of goods and services in Nigeria. As postulated by Schoeman et al. (Citation2022), cash flow from taxes such as VAT can be enhanced by either broadening the economic base, such as by obtaining more enrolled taxpayers, or by raising the percentage. Nigeria adopted the option of increasing VAT rate from 5% to 7.5%.

With the exception of those explicitly excluded by the VAT Act, all products and services (whether manufactured in the nation or supplies from abroad) attract VAT levy at the rate of 7.5 percent. Non-oil export earnings; passenger planes and service parts shipments; specified charitable efforts; manufacturing equipment used for strong mineral resources industry; export earnings; farm machinery; heavy trucks; basic foodstuffs; postal; housing rental costs; cosmetics and healthcare consumables; training and related items; a restricted number of economic amenities; books and magazines are exempt from the zero-rate regime. VAT periodic documents must be submitted by all liable individuals no sooner than the 21st day succeeding the month of operation (Federal Inland Revenue Service [FIRS], Citation2022).The Nigerian VAT policy requires three types of taxpayers to subtract VAT at the origin and deposit it straight to the tax administration. All of those are Nigerian firms that conduct VATable operations with non-resident corporations within the nation; governmental agencies, legislative authorities, and other governmental entities; and energy companies (FIRS, Citation2022).

The role of VAT in economic growth has been extensively researched. While some researchers believe that VAT increases industrial prosperity (Ayoub & Mukherjee, Citation2019; Demi et al., Citation2021; Inimino et al., Citation2018; Lan et al., Citation2020; Ma et al., Citation2022; Nasiru et al., Citation2016), others argue that it causes inflation and other economic problems (Alavuotunki et al., Citation2019; Bansal & Abdulla, Citation2020; Kalinin, Citation2022; Malkina, Citation2021; Sarwar et al., Citation2021; Stoilova, Citation2017; Timuno & Eita, Citation2021). There is no specific study that evaluates the impact of VAT on manufacturing outputs. The industrial output referred to in this study is primarily the manufacturing sector’s contribution to the GDP. However, the output used in this study does not include the productivity of the mining and quarrying industry segments. This study is thus uniquely designed to fill this obvious void. The majority of Nigerian manufacturing firms acquire products and services both locally and internationally. VAT expenditure is incurred both domestically and through importation during the process. The study’s goal is to highlight how manufacturing output responds to both import and domestic VAT. This paper is divided into five segments: the overview, the review of related literature phase, the methods used, the analysis of data, and the conclusion.

2. Literature review

2.1. Concept of a tax system

Tax is a mandatory commitment to the public treasury made by businesses, private citizens, and other entities in conformity with the laws. Levy has two primary roles. Taxation generates a significant and consistent revenue stream to match the government’s fiscal necessities. The legally required phenomenon of taxation with a broad impact is an essential priority for the authority to galvanize monetary capacity from the financial system in a prompt and adequate manner. Taxation is also used to maintain economic stability. The state controls the behavior of both companies and people through taxation, guiding consumption and regulating production (Nguyen, Citation2019).The tax system is generally divided into two parts: direct tax and indirect tax. A direct tax is one that is levied explicitly on the tax paying citizens and firms who incur the tax liability, thus the tax liability cannot be moved to others (Nguyen, Citation2019; Omodero et al., Citation2021). The state collects tax from middlemen in the case of an indirect tax. The utmost wielder of financial impact is not the taxable person. The consequences of indirect and direct taxes on the economic system vary considerably because of distinctions in collection techniques, earnings foundations, and the move of fiscal tax liability. The right mix of direct and indirect taxes will maximize the beneficial impact of taxes on the financial system. Thus, an acceptable tax plan fosters economic growth, whereas an irrational tax structure constrains businesses and obfuscates societal consumption pattern (Nguyen, Citation2019).Mawejje and Munyambonera (Citation2016) unearthed that the agricultural and unofficial industries are the most significant barriers to tax income effectiveness, whereas innovation costs, trade openness, and manufacturing industry expansion are highly linked with tax receipts achievement.

2.2. VAT and industrial productivity

VAT is a multiphase tax levied at different phases of importation, manufacturing, and transmission based on a proportion of the additional benefit of the products sold or delivered services at each phase (Alizadeh & Motallabi, Citation2015). Payment in each stage of the shipments, manufacturing, and supply chain is transmitted to the following phase component of the channel, so that the end user of the product or service bears the entire cost.In terms of benefits, it is expected that the economical collection technique will produce a consistent revenue stream; whereas household budget cuts can also be whittled down because VAT gives good funds to be invested (Sarwar et al., Citation2021).A few authors also highlight VAT as a component that can help stimulate the economy.According to Feher et al. (Citation2019), VAT has emerged as the most essential tax because it has proven to be an immensely important expansionary fiscal tool for EU member countries and was among the most efficient tax in reducing budget shortfalls during the financial meltdown.Miki (Citation2011) recognised a transition in the first pattern of consumption and GDP growth when the VAT rate was changed.According to Dwivedi and Sinha (Citation2016), the West Bengal state government’s major source of income is value added tax, which accounts for nearly 62% of the state’s own taxes collected.

Jalata (Citation2014) investigated whether VAT enhances productivity expansion and discovered that, from 2003 to 2012, VAT massively raised the economy of the nation. Alizadeh and Motallabi (Citation2015) examined the link between value added tax and the dimensions of present administration, as measured by current market price to GDP, and the magnitude of government building projects, as measured by building costs to GDP of Iran. In this context, periodic time statistics from 2008 to 2014 were adapted using the Ardl approach. According to the findings of the study, there is a significant and positive association between value added tax and the volume of existing and building projects of authorities. This tax has a greater impact on the amount of the existing building projects of government than the dimension of the current one.

Simionescu and Albu (Citation2016) explored the impact of the conventional VAT rate on income progress in Central and Eastern European countries between 1995 and 2015. The research showed that the VAT rate had a positive impact on the economy. A reciprocal Granger causality existed between productivity expansion and VAT rate. Just in Hungary did the Bayesian linear models demonstrated a favorable influence of VAT rate on GDP rate. When VAT rates were raised, other countries’ GDP rates fell in the near term.Nasiru et al. (Citation2016) study concluded that value-added tax had an optimistic navigation connotations between the VAT and productivity expansion. They also make some recommendations that focus on the significance of VAT receipts and its contributions to economic growth. Adegbie et al. (Citation2016) examined the impact of VAT on the Nigerian economy from its inception to the present in order to determine the urgency of its systemic change and to determine the relationship that existed between them. VAT was found to have a positive correlation with GDP.

Chan et al. (Citation2017) probed the effect of public expenditure performance on productivity expansion in 115 countries with a VAT structure. The VAT framework was discovered to strengthen the effect of productive governmental spending on economic growth, and the VAT system’s mediating roles was again improved by the administration’s liberal democracies and lawmaking power. Kalaš and Milenkovič (Citation2017) also discovered a substantial association between value-added tax and GDP.According to (Hassan, Citation2015; Inimino et al., Citation2018), VAT has a beneficial impact on economic growth. Ayoub and Mukherjee (Citation2019) researched this correlations in China and discovered a beneficial connection. Asllani and Statovci (Citation2018) investigated the impact of changes in VAT rates for specific types of products on Kosovo’s redistribution of income. According to the results of the assessment, the VAT decline from 16% to 8% on basic products and the VAT rise from 16% to 18% on luxury items had a massive influence on income and Productivity growth in Kosovo.Sowole and Adekoyejo (Citation2019) looked into the efficacy of Nigeria’s Consumption tax in order to assess its economic development effects. Using simple linear regression method, the analyze data revealed a positive association between VAT and GDP.

Obaretin and Uwaifo (Citation2020) looked into the influence of Value Added Tax on Nigerian industrial prosperity from 1994 to 2018. The repeated measures configuration was used in the analysis. The findings revealed that VAT had a significant and favorable effect on Nigeria’s economic progress. According to Bansal and Abdulla (Citation2020), the VAT implementation can significantly raise tax receipts, allowing the authorities to spend more on innovation to enhance economic growth. Nevertheless, VAT has a productive long-term effect on economic growth because it minimizes government debt while increasing GDP by 2%. Aside from these direct effects, VAT has an indirect impact on the economy as Lan et al. (Citation2020) discovered that replacing business taxes with value-added taxes in China encourages R&D investment and industry upgrading, which inevitably helps to foster fiscal expansion. Stoilova and Patonov (Citation2020) investigated the effect of fiscal policy on economic growth in Bulgaria from 1995 to 2018. The research found that value-added tax receipts appeared to be growth-promoting.

Nguyen et al. (Citation2020) assessed the impact of tax system on productivity expansion in Vietnam’s geographical areas. The study postulated that tax system was evaluated by the yearly increase of taxes collected in 63 Vietnamese cities and counties in three categories: consumption tax, income tax, and real estate taxes over an 11-year period from 2007 to 2017. The GMM regression analysis found that consumption and income taxes had a beneficial effect on the economy in Vietnam’s municipalities, while property tax had no statistically significant influence. According to Al-Ubaydli (Citation2020), VAT is one of the most effective strategies for supporting the financial system without laying off workers or thawing pay.

Furthermore, because a diverse variety of products and services are not subject to taxation, in an economic crisis, VAT will be the less distressing indicator (Sarwar et al., Citation2021). Demi et al. (Citation2021) confirmed that VAT influenced nominal GDP indirectly and constructively, and that there was a significant connection between VAT income and GDP growth rate, with virtually a 10% modification in VAT earnings causing a rise of at least 1.03% in the GDP growth rate. Even so, Guo and Shi (Citation2021) demonstrated that VAT decline assisted China in recovering from the latest COVID-19 zoonotic disease. According to Guo and Shi (Citation2021), VAT relieves fiscal pressures and VAT reductions aid in the recovery from an economic recession. Ma et al. (Citation2022) found that converting business taxes to VAT curtailed the tax pressure on firms in numerous districts of China.

2.3. VAT challenges and economic expansion

The value added tax (VAT) is very important in the global economy. As a result, any tax modification will have an instantaneous impact on the economy. VAT increases will have a negative impact on the economy and reduce societal engagement for venture creation. Increases in the VAT rate may have an inverse impact on the gathering of personal revenue taxes and import tariffs due to increased financial stress and intensification of inflation, relatively low demand, and lower consumption levels due to rising price increases (Semenova, Citation2020). Tax reform may have severe repercussions, including an increment in the tax liability, higher costs for the vast bulk of commodities and services, reduced consumer demand, an uptick in inflation, a worse predicament for small and medium-sized businesses, and a steady decline in productivity expansion (Semenova, Citation2020).VAT challenges in both administration and its economic consequences have been proved in previous studies. According to Harkushenko (Citation2022), even technological advances are not a best antidote for resolving all VAT administration issues. VAT is regressive, affecting low-income earners who pay the same price for goods and services as higher-income earners.

As claimed by Hajdúchová et al. (Citation2015), earnings from the value added tax in the Slovak republic increased from 1993 to 2015; nevertheless, cash flow from other forms of taxes was bigger than VAT earnings. Stoilova (Citation2017) used regressions on pooled panel data to examine the impact of taxation on productivity expansion in the EU-28 member countries from 1996 to 2013. The test discovered that implementing VAT had an adverse influence on the EU-28 economic systems and deduced that a tax structure premised on preferential consumption taxes, personal income taxes, and real estate taxes is more favorable to economic expansion.

Using recently released macro data, Alavuotunki et al. (Citation2019) looked at the effect of the emergence of the value-added tax on disparity and income growth. The research provided both traditional nation fixed effect regressions and dynamic panel analyses, in which VAT introduction was instated by using past values from neighboring countries’ VAT structures as a tool. The analysis indicated that, contrary to previous research, the VAT’s earnings implications were negative. The findings also revealed that the VAT implementation accelerated wealth disparity while leaving consumption disproportion unchanged. Owino (Citation2019) investigated the impact of value added tax/sales tax on economic expansion in Kenya from 1973 to 2010. The model was estimated using the ordinary least squares approach. The quantitative findings revealed a positive but insignificant relationship between values added tax and economic growth in Kenya. The study posits it that a positive but insignificant correlation between VAT Revenue and GDP indicates that there are some issues impeding its effectiveness. According to the study, the effect of value added tax on the financial system is insignificant to sway productivity expansion.

Bogari (Citation2020) assessed the economic and social consequences of implementing a value-added tax in the Kingdom of Saudi Arabia. A descriptive and analytical methodology was applied to meet the objective. The survey looked at 287 Saudi nationals working in both the private and government organizations. The findings demonstrate that the implementation of the value-added tax increased the country’s monetary capacity while also confirming that the intervention had a negative social consequence and encountered numerous difficulties. Bansal and Abdulla (Citation2020) carried out a research in Bahrain and discovered that VAT had a deleterious short-term implication since it raises inflation and lessens the number of international investors. Wadesango (Citation2020) discovered that personal character traits, VAT technical requirement, and ecological factors such as the advanced nation’s economic political and socioeconomic predicament all had an impact on VAT acquiescence. Most SMEs’ failure to comply was a survival strategy in the face of challenging economic times. The increased costs of setting up such a complicated structure were so intense for SMEs that any efforts to conform projected the comparatively tiny company’s business demise.

Sarwar et al. (Citation2021) believe that despite the anticipation that VAT deployment is beneficial to the government’s recovery from an economic slump because more income will be accessible, but some problems could occur as a result of the VAT. Regrettably, VAT causes inflation of consumer costs (Sarwar et al., Citation2021). In Saudi Arabia, Sarwar et al. (Citation2021) discovered that the implications of labor became bad after VAT, but the consequence of investment and financial progression became substantial by Vision 2030 rapid industrialization. Price of crude coefficients were significant and harmful for both return and volatility. Capital accumulation and bilateral trade had different outcomes; positive shocks had negative sign. Trade liberalization, on the other hand, had a major and beneficial quotient after Perception 2030.

Santiago and Morozumi (Citation2021) investigated whether, in the perspective of OECD countries, a revenue-neutral uptick in VAT, counterbalanced by a reduction in income taxes, could have various impacts on long-run expansion contingent upon how the VAT is created. The analysis found that a revenue-neutral increase in VAT enhanced advancement when it was raised through an increase in C-efficiency, but not when it was raised through an increase in the standard VAT rate, which is tried to apply to the majority of taxed consumption. Kristjánsdóttir (Citation2021) wondered if higher VAT affected tourism demand in Europe. The results suggested that a VAT growth had no effect on tourist inflows to Europe. Furthermore, in contrast to prior European data analysis, the results of the study did not prove that ‘nearer to competency” tourist industry in Europe seems to be more tax responsive than “still on the expansion route” regions of the world.

Timuno and Eita (Citation2021) used the Autoregressive Distributive Lag method to evaluate the consequences of fiscal policy on sectoral total factor production (TFP) increase in Botswana between 1984 and 2016. The results indicated that concentrating on accumulated TFP expansion obscures particular concerns unique to a variety of industries. Natural resource tax, numerous different tax receipts, and social care spending, for example, were discovered to have a significant long-run beneficial impact on Output growth in the primary industry only, with a detrimental effect in the secondary and tertiary segments. Furthermore, both the value-added tax and the non-mining taxation reduced Output growth throughout all areas of the economy. Malkina (Citation2021) examined the impact of the 2020 bubonic plague on Russian provincial tax receipts, as well as the aspects that contribute to the persistence of provincial tax structures to infectious disease upheavals. It was discovered that territories with a bigger percentage of individual income tax and real estate taxes in tax collections, a greater portion of commerce and manufacturing sectors, public circle, and social policy in overall value added, a greater level of financial inclusion, and a greater proportion of small businesses in transaction value have the slightest downturn or even expansion in taxes collected.

In regards to the consequences of initiatives to ensure tax compliance, Kalinin (Citation2022) postulated a justification for the amount of VAT payouts in 2019 increasing at a quicker speed than the rapid expansion in value created. The 2% uptick in the basic rate of taxation resulted in a decrease in the return on revenue mobilization endeavours. A five-year timeframe of rapidly surpassing tax receipts growth ended almost concurrently with the VAT rate hike. The inquiry reached a conclusion that the financial system, even with a fairly insignificant boost in the rate of taxation, diminishes the government’s capacity to obtain extra revenue. Schoeman et al. (Citation2022) identified that while modifications in the VAT rate do not have a serious influence on taxpayer enrollment choices, the amplitude of the adjustment in the VAT rate could be impactful on signing up adoptions, whether pertaining to obligatory or spontaneous certification. More specifically, the larger the intensity of the VAT percentage decline (increment), the further presumably it is that payers will enroll (deactivate) for Tax reasons, implying that the enormity of VAT rate fluctuations will have a repercussions on VAT registration choices and thus on tax acquiescence more broadly.

3. Materials and methods

From 2010 to 2021, this study investigates the relationship between VAT returns and industrial sector performance in Nigeria. Given its descriptive and interactional quantitative testing methods, the study takes a cross-sectional approach. Secondary sources are used to collect data for both the dependent and independent factors. Manufacturing output is the dependent variable, and the data are from the Central Bank of Nigeria Statistical Bulletin. The independent variables are: import VAT, domestic VAT, and total VAT. All data used for predictor variables have all been obtained from the Federal Inland Revenue Service (FIRS) and the Organization for Economic Cooperation and Development (OECD) databases. The datasets are collected in the local currency, but after confirming their suitability, the variables are log transformed to ensure the correct outcome of the statistical analysis. The unit root is used to establish stability, while the correlation matrix depicts the relationship between the variables for both the reliant and autonomous elements. We also show the data trend for the time period covered by this study. The Pairwise Granger Causality Test contributes to the study’s specific objectives by confirming the causation effects of the variables.

The variables are measured as displayed in Table below:

Table 1. Variable dimension and sources

3.1. Model specification

The econometric model employed to show the linear relationship is specified as follows:

Where,

Y = Manufacturing/Industrial Sector output;

X = VAT proceeds from both local and international business transactions;

β = Coefficient;

= Error term.

The above model adapted from Stoilova and Patonov (Citation2020) but modified can be specifically applied to this study as:

Where:

LOG = Logarithm form of variables;

MFGY = Manufacturing/Industrial Sector productivity;

IVAT = Value Added Tax revenue from the country’s Imports;

DVAT = Value Added Tax from local operations;

TVAT = Aggregate Value Added Tax returns.

= Coefficient of the parameter estimate

= intercept

= Error term

On the a priori, we anticipate; β1 > 0, β2 > 0, β3 > 0.

3.2. Model for granger causality testing

The model below explains the operation of the granger causality function applied in this study. We hypothesized that manufacturing VAT proceeds do not have causality effects on manufacturing outputs (y(t) does not Granger-cause x(t)). To test this hypothesis, these equations test to see if y(t) Granger-causes x(t):

From Equationequation 3(3)

(3) , we show that Y(Manufacturing/Industrial sector outputs) does not granger cause X or that Y does not have causality effect on X (VAT proceeds).

Similarly, Equationequation 4(4)

(4) also suggests that X (VAT receipts) does not granger cause Y (Manufacturing sector productivity).

4. Data processing and interpretation of results

This section contains the results of the data analysis as well as an explanation of each individual result of the analysis. The section discusses the dataset’s trend analysis, unit root test, correlational analysis, and granger causality result and explanation.

5. Trend analysis

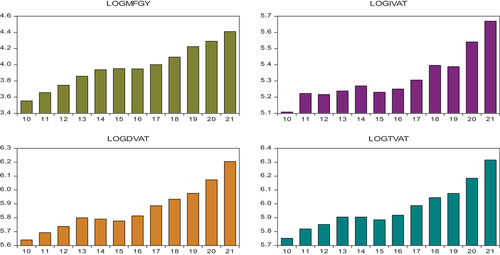

Figure depicts the data movement from 2010 to 2021. One important point to note is that all of the variables increased significantly in the year 2021. The VAT proceeds suffered a major setback in 2010 while attempting to gradually increase; the domestic and import VAT proceeds shrank substantially again in 2015, thereby affecting the total VAT increase. Aside from 2016, the manufacturing sector has been steadily improving since 2011, following a major decline in 2010. The expansion continued from 2017 to 2021. This increase demonstrates that the Nigerian industrial sector is improving as a result of the introduction of new technologies and the low level of the country’s VAT rate. It should be noted that Nigeria has one of the lowest VAT rates in the world (Omodero, Citation2020), so industries operating in the country can benefit from this important factor.

Figure 1. Trend of data from 2010–2021.

Table shows the unit root result, which validates that the datasets used in this study are stable and do not have the potential to produce erroneous results. Unit root confirmation tools include Levin, Lin & Chut, Im, Pesaran, and Shin W-stat, Augmented Dickey Fuller (ADF)—Fisher Chi-square, and Phillip Peron (PP)—Fisher Chi-square. With a probability of 0.00, which is less than 0.05, the various unit root apparatus used in this test confirm that there is no unit root challenge with the datasets.

Table 2. Unit root

We used the descriptive statistics in Table to verify the nature of the datasets before using them for evaluation. The results show that the mean values of MFGY, IVAT, DVAT, and TVAT are 3.97, 5.32, 5.86, and 5.97, respectively. Following the position of the mean values and the standard deviation values of 0.25 for MFGY and 0.16 for all predictor variables, it can be deduced that the data spread is low and is clustered around the mean area. The Kurtosis results indicate that the variables have values close to 3, indicating that the data distribution is normal. To corroborate the regularity of the data allocation, the Jarque Bera p-values for MFGY, IVAT, DVAT, and TVAT are 0.86, 0.34, 0.57, and 0.51, respectively. These values are greater than 0.05, indicating that the datasets used in this study are evenly distributed. The findings also show that the datasets are constructively and equitably skewed.

Table 3. Summary statistics

Table depicts the correlation matrix and shows the kind of connection that exists between the variables. The findings indicate that import VAT, domestic VAT, and total VAT have a very strong and positive correlation with manufacturing sector output. That is, the coefficient of correlation between import VAT (LOGIVAT) and manufacturing output (LOGMFGY) is 0.93, indicating a very strong link. Similarly, DVAT has a 0.97 correlation with MFGY, indicating a very important connection between domestic VAT and manufacturing contribution to GDP. The same outcome can be seen for the total VAT relationship with manufacturing output, which shows a 0.96 correlation. Looking at the relationship between the predictor variables, there is a strong link between them. The implication is that the industrial sector does not regard VAT compliance as a threat to their operations and performance. That is, IVAT has a 98% correlation with DVAT, while total VAT has a 99% correlation with both IVAT and DVAT. This indicates that both the domestic VAT and the import VAT contribute significantly to the country’s government revenue.

Table 4. Correlation matrix

The study previously hypothesized that VAT proceeds, which include import VAT, domestic VAT, and total VAT, have a causal effect on manufacturing output at a 5% level of significance. The granger causality test results in Table clearly show that domestic VAT and total VAT receipts have causal effects on industrial sector performance at the 0.01 level of significance. The findings show that local VAT and aggregate VAT proceeds significantly boost the manufacturing sector. This is largely due to VAT being such an indirect levy on products throughout the supply chain that is ultimately borne by the end users of the products. The burden is not felt by the manufacturers because they do not directly bear the liability; rather, the industries in the country experience significant growth as a result of their compliance. This finding is consistent with the views of numerous authors who believe that VAT promotes economic growth and industry productivity (Ayoub & Mukherjee, Citation2019; Demi et al., Citation2021; Inimino et al., Citation2018; Lan et al., Citation2020; Ma et al., Citation2022; Nasiru et al., Citation2016). However, the findings of some authors who discovered that VAT represses the economy and causes a decline in industry outputs (Alavuotunki et al., Citation2019; Bansal & Abdulla, Citation2020; Kalinin, Citation2022; Malkina, Citation2021; Sarwar et al., Citation2021; Stoilova, Citation2017; Timuno & Eita, Citation2021) have been refuted. Thus, based on the outcome of this analysis, the null hypothesis is declined.

Table 5. Pairwise granger causality tests

6. Conclusion and implications

This study has been empirically examined, and the results show that none of the VAT classes have a causality effect on each other, and import VAT has no causal effect on manufacturing sector performance. Surprisingly, the study also reveals that the output of the manufacturing sector does not result in VAT receipts, confirming that the VAT liability is borne primarily by the final consumers, despite the fact that the manufacturing sector initiates the supply chain. On that note, the primary goal of this study was pursued, and this claim was tested using the null hypothesis that VAT proceeds do not have causality effect on manufacturing output. The end result demonstrates that total VAT and local VAT returns contribute positively and significantly to Nigeria’s industrial sector growth. This is a robust result with policy implications. One of the most significant policy implications is that the government must ensure that the supply chain is technologically improved in order to boost VAT administration at all levels of the supply chain. Secondly, there is need for sensitization and training of all industry operators on how to calculate VAT returns and remit same to the relevant tax authority accordingly. Industries operating unofficially should be checked by the relevant security agencies for probing. Above all, the government should ensure VAT revenue are adequately applied to provide infrastructures that will enhance industry operations in the country.

Acknowledgements

The authors would like to express their heartfelt appreciation to the administration of Covenant University Nigeria for their financial backing of the public access of this article.

Disclosure statement

The authors state that there are no present or future conflicts of interest related to this study.

Additional information

Funding

Notes on contributors

Cordelia Onyinyechi Omodero

Cordelia Onyinyechi Omodero (Ph.D, ACA) is a full-time lecturer in the Accounting Department of Covenant University Ota, Ogun State, Nigeria. She is a professional accountant and an Associate Member of The Institute of Chartered Accountants of Nigeria (ICAN), with extensive experience in taxation and public finance. She has published numerous innovative research works in the fields of taxation, accounting education, environmental sustainability, fiscal devolution, capital market analysis, and public sector finance.

Sylvester Eriabie

Eriabie, Sylvester (Ph.D.) is a Senior Lecturer in Covenant University Ota’s Accounting Department in Ogun State, Nigeria. Financial accounting, management accounting, and forensic studies are among his research interests. He has several works published to his name and has attended numerous conferences both locally and internationally.

References

- Adegbie, F. F., Olajumoke, J., & Danjuma, K. J. (2016). Assessment of value added tax on the growth and development of Nigeria economy: Imperative for reform. Accounting and Finance Research, 5(4), 163–13. http://dx.doi.org/10.5430/afr.v5n4p163

- Alavuotunki, K., Haapanen, M., & Pirttilä, J. (2019). The effects of the value-added tax on revenue and inequality. The Journal of Development Studies, 55(4), 490–508. https://doi.org/10.1080/00220388.2017.1400015

- Alizadeh, M., & Motallabi, M. (2015). Studying the effect of value added tax on the size of currentGovernment and construction government. Procedia Economics and Finance, 36(1), 334–336. https://doi.org/10.1016/S2212-5671(16)30045-4

- Al-Ubaydli, O. (2020). Saudi Arabia reaps the benefit of establishing VAT. Alrabia News 2020.

- Asllani, G., & Statovci, B. (2018). Effect of the change in value added tax on the fiscal stability of Kosovo. EKONOMSKI PREGLED, 69(4), 423–438. https://hrcak.srce.hr/file/302266 10.32910/ep.69.4.4

- Ayoub, Z., & Mukherjee, S. (2019). Value added tax and economic growth: An Empirical Study of China perspective. Signifikan Jurnal Ilmu Ekonomi, 8(2), 235–242. https://doi.org/10.15408/sjie.v8i2.10155

- Bansal, A., & Abdulla, A. A. A. A. (2020). Role of value added tax in the economic development of Kingdom of Bahrain. Journal of Critical Reviews, 7(3), 17–24. http://dx.doi.org/10.31838/jcr.07.03.03

- Bogari, A. (2020). The economic and social impact of the adoption of value-added tax in Saudi Arabia. International Journal of Economics, Business and Accounting Research, 4(2), 62–74. https://jurnal.stie-aas.ac.id/index.php/IJEBAR/article/view/991

- Chan, S.-G., Ramly, Z., & Karim, M. Z. A. (2017). Government spending efficiency on economicGrowth: Roles of value-added tax. Global Economic Review, 46(2), 162–188. https://doi.org/10.1080/1226508X.2017.1292857

- Demi, A., Xhaferri, S., Uku, S., Shahini, S., & Lushi, A. (2021). The impact of fiscal policies on Albanian economic growth: The case of value-added tax [Special issue]. Journal of Governance & Regulation, 10(4), 311–325. https://doi.org/10.22495/jgrv10i4siart11

- Dwivedi, H. K., & Sinha, S. K. (2016). Trends in collection of value added tax in West Bengal: A commentary. South Asian Journal of Macroeconomics and Public Finance, 5(2), 238–248. https://doi.org/10.1177/2277978716671066

- Feher, A., Condea, B. V., & Harangus, D. (2019). Impact of harmonization on the implicit tax rate of consumption. Prague Economic Papers, 28(4), 449–464. https://doi.org/10.18267/j.pep.705

- FIRS (2022). The relevant documents required for filing VAT returns. Federal Inland Revenue Service. https://www.firs.gov.ng/value-added-tax-vat-faq/#

- Guo, Y. M., & Shi, Y. R. (2021). Impact of the VAT reduction policy on local fiscal pressure in China in light of the COVID-19 pandemic: A measurement based on a computable general equilibrium model. Economic Analysis and Policy, 69(1), 253–264. https://doi.org/10.1016/j.eap.2020.12.010

- Hajdúchová, I., Sedliaciková, M., & Viszlai, I. (2015). Value-added tax impact on the state budget expenditures and incomes. Procedia Economics and Finance, 34(1), 676–681. https://doi.org/10.1016/S2212-5671(15)01685-8

- Harkushenko, O. N. (2022). Prospects of VAT administration improvement in digitalized world: Analytical review. Journal of Tax Reform, 8(1), 6–24. https://doi.org/10.15826/jtr.2022.8.1.105

- Hassan, B. (2015). The role of value added tax in the economic growth of Pakistan. Journal of Economics and Sustainable Development, 6(13), 174–183. https://core.ac.uk/download/pdf/234647134.pdf

- Inimino, E. E., Otubu, O. P., & Akpan, J. E. (2018). Value added tax and economic growth in Nigeria. International Journal of Research and Innovation in Social Sciences, 2(10), 211–219.

- Jalata, D. M. (2014). The role of value added tax on economic growth of Ethiopia. Science Technology and Arts Research Journal, 3(1), 156–161. https://doi.org/10.4314/star.v3i1.26

- Kalaš, B., & Milenkovič, N. (2017). The role of value added tax in the economy of Serbia. Ekonomika, 63(2), 69–78. https://doi.org/10.5937/ekonomika.1702069K

- Kalinin, A. M. (2022). Increasing the VAT rate in Russia from the position of the laffer curve. Studies on Russian Economic Development, 33(1), 353–358. https://doi.org/10.1134/S1075700722030042

- Kristjánsdóttir, H. (2021). Tax on tourism in Europe: Does higher value-added tax (VAT) impactTourism demand in Europe? Current Issues in Tourism, 24(6), 738–741. https://doi.org/10.1080/13683500.2020.1734550

- Lan, F., Wang, W., & Cao, Q. (2020). Tax cuts and enterprises’ R&D intensity: Evidence from a natural experiment in China. Economic Modelling, 89(1), 304–314. https://doi.org/10.1016/j.econmod.2019.10.031

- Ma, J., Leontyeva, Y. V., & Domnikov, A. Y. (2022). Analyze the impact of the transition from business tax to VAT on the tax burden of transport enterprises in various regions of China. Journal of Tax Reform, 8(2), 199–211. https://doi.org/10.15826/jtr.2022.8.2.117

- Malkina, M. Y. (2021). How the 2020 pandemic affected tax revenues in Russian regions? Equilibrium. Quarterly Journal of Economics and Economic Policy, 16(2), 239–260. https://doi.org/10.24136/eq.2021.009

- Mawejje, J., & Munyambonera, E. F. (2016). Tax revenue effects of sectoral growth and public Expenditure in Uganda. South African Journal of Economics, 84(4), 538–554. https://doi.org/10.1111/saje.12127

- Miki, B. (2011). The effect of the VAT rate change on aggregate consumption and economic growth. Working Paper Series No. 297. Center on japanese economy and business. https://academiccommons.columbia.edu/doi/10.7916/D8862QBH.

- Nasiru, M. G., Haruna, M. A., & Abdullahi, M. A. (2016). Evaluating the impact of value added tax on the economic growth of Nigeria. Journal of Accounting and Taxation, 8(6), 59–65. https://doi.org/10.5897/JAT2016.0226

- Nguyen, H. H. (2019). Impact of direct tax and indirect tax on economic growth in Vietnam. The Journal of Asian Finance, Economics and Business, 6(4), 129–137. https://doi.org/10.13106/JAFEB.2019.VOL6.NO4.129

- Nguyen, M.-L. T., Huy, D. T. N., Hang, N. P. T., Bui, T. N., & Tran, H. X. (2020). Interrelation of tax Structure and economic growth: A case study. Journal of Security and Sustainability Issues, 9(3), 1177–1188. http://doi.org/10.9770/jssi.2020.9.4(5)

- Obaretin, O., & Uwaifo, F. N. (2020). Value added tax and economic development in Nigeria. Accounting and Taxation Review, 4(1), 148–157. http://www.atreview.org/admin/12389900798187/ATR%204_1_%20148-157.pdf

- Okoye, E.I., & Gbegi, D.O. (2013). Effective value added tax: An imperative for wealth creation in Nigeria. Global Journal of Management and Business Research, 13(1), 90–100. doi:10.2139/ssrn.2238854

- Omodero, C. O. (2020). The consequences of indirect taxation on consumption in Nigeria. Journal of Open Innovation: Technology Market, and Complexity, 6(4), 1–13. https://doi.org/10.3390/joitmc6040105

- Omodero, C. O., Okafor, M. C., & Nmesirionye, J. A. (2021). Personal income tax revenue and Nigeria’s aggregate earnings. Universal Journal of Accounting and Finance, 9(4), 783–789. https://doi.org/10.13189/ujaf.2021.090424

- Owino, O. B. (2019). An empirical analysis of value added tax on economic growth, evidence from Kenya data set. Journal of Economics, Management and Trade, 22(3), 1–14. https://doi.org/10.9734/JEMT/2019/46167

- Santiago, A.-O., & Morozumi, A. (2021). The value-added tax and growth: Design matters. International Tax and Public Finance, 28(1), 1211–1241. https://doi.org/10.1007/s10797-021-09681-2

- Sarwar, S., Streimikiene, D., Waheed, R., Dignah, A., & Mikalauskiene, A. (2021). Does the vision 2030 and value added tax leads to sustainable economic growth: The case of Saudi Arabia? Sustainability, 13(19), 1–20. https://doi.org/10.3390/su131911090

- Schoeman, A. H. A., Evans, C. C., & Perez, H. D. (2022). To register or not to register for value-added tax? How tax rate changes can influence the decisions of small businesses in South Africa. Meditari Accountancy Research, 30(7), 213–236.

- Semenova, G. (2020). Impact of VAT raise on Russian economy. E3S Web of Conferences, 210. Article No. 13028. Innovative Technologies in Science and Education (ITSE-2020). https://doi.org/10.1051/e3sconf/202021013028.

- Simionescu, M., & Albu, -L.-L. (2016). The impact of standard value added tax on economic growth in CEE-5 countries: Econometric analysis and simulations. Technological and Economic Development of Economy, 22(6), 850–866. https://doi.org/10.3846/20294913.2016.1244710

- Sowole, O. E., & Adekoyejo, M. O. (2019). Influence of value added tax on economic development (The Nigeria perspective). Journal of Accounting and Management, 9(3), 35–43. https://dj.univ-danubius.ro/index.php/JAM/article/view/122

- Stoilova, D. (2017). Tax structure and economic growth: Evidence from the European Union. Contaduria y Administracion, 62(3), 1041–1057. https://doi.org/10.1016/j.cya.2017.04.006.

- Stoilova, D., & Patonov, N. (2020). Fiscal policy and growth in a small emerging economy: The case of Bulgaria. Society and Economy, 42(4), 386–402. https://doi.org/10.1556/204.2020.00015

- Timuno, S. O. M., & Eita, J. H. (2021). The impact of fiscal policy on total factor productivity growth in a developing: Evidence from Botswana. Studies in Economics and Econometrics, 45(4), 243–259. https://doi.org/10.1080/03796205.2022.2053298

- Wadesango, N. (2020). The impact of value added tax on small and medium enterprises in a Developing country. Academy of Accounting and Financial Studies Journal, 24(2), 1–12. https://www.abacademies.org/articles/the-impact-of-value-added-tax-vat-on-small-and-medium-enterprises-in-a-developing-country-9874.html