Abstract

This study aims to identify the mediating role of the management accounting information system (MAIS) in the relationship between innovation strategy and the financial performance of industrial companies in Jordan. To achieve the objectives of the study, the prepared a questionnaire, where the number of questionnaires was distributed (374) randomly. Where (358) questionnaires were retrieved by (95.7%) of the total questionnaires sent electronically, and they were distributed to (the general manager, financial manager, chief accountant, internal auditors, and accountants. The study reached several results, most notably: There is no significant mediating role of MAIS on the relationship between management’s value orientation towards innovation and financial performance in Jordanian industrial companies. Moreover, there is a significant mediating role of MAIS in the relationship between riskiness and financial performance in Jordanian industrial companies. In view of these results, the study recommends to the Jordanian industrial companies’ management the importance of applying the modern MAIS because it has become a critical component, and it is difficult to achieve a competitive advantage and stay in the market without relying on systems.

1. Introduction

In global business competition, companies have to adapt themselves in terms of innovation to survive in such a fast-paced market (Ma et al., Citation2022). As the world of industry is becoming vast and influential as companies face more challenges and competition (Trubetskaya et al., Citation2022). Thus, companies seek to look for a competitive advantage that helps in improving financial performance, so innovation strategy is the catalyst that will better improve the performance of the company, reduce any regulatory and financial obstacles, and create a competitive advantage for the company in the markets (Grover & Dresner, Citation2022). Therefore, companies must implement strategies appropriately to build their competitive advantage (Hariyati & Tjahjadi, Citation2018). The MAIS also underwent several changes in the final decade of the 20th century as a result of the intense technological advancement that forces most businesses to develop their accounting systems in a creative way in order to obtain accounting information that is of high quality and timely. Hence, an urgent need to provide solutions that help provide accounting treatments for a potential or existing problem and work to improve its strategic plans, so objectives require a set of tools that help in developing an innovative strategy (Jelonek et al., Citation2022).

Since MAIS plays a crucial role in all organizations and sectors and is created to aid in the control and management of issues related to the economic and financial sectors of the organization, it is necessary to use it as a mediator between innovation strategy and financial performance. As a result, MAIS was created by technological advances for this strategic success. Moreover, the elements related to this system are aimed at identifying and collecting primary and systematic data and then transforming it into financial statements. This is to improve the decision-making process of managers and their employees and to inform decision-makers (Chen et al., Citation2022). Additionally, the study (Ahmad & Al-Shbiel, Citation2019) revealed that MAIS is crucial for enhancing company performance. In order to minimize expenses, make wise decisions, and develop an innovation strategy that enhances financial performance, businesses utilize MAIS as a structure to enhance the gathering, storage, and administration of their financial data by giving managers current information on internal processes (Muskat et al., Citation2021). Consequently, MAIS is a unit of a system designed for measuring and collecting financial and operational data, which work to direct motivational behaviors and administrative activities to achieve the strategic objectives of the organization through increasing and developing cultural values (Al Dabbas & Alkshali, Citation2021). Moreover, MAIS provides a vital role in enhancing organizational capacity and innovation capacity as well as enhancing the dynamic ability and improving the financial performance of the company (Mong Le et al., Citation2020). Recently, most companies are trying to drastically change their important policies and how they structure their businesses, commitments, and strategic framework to improve financial performance, so it is essential to emphasize that financial performance is a method through which companies seek to know the extent of their performance for while by achieving higher sales and profitability for the company and its shareholders through good management of current assets, non-current assets, property rights, financing, expenses, and revenues, as well as the main objective of which is able to provide shareholders and stakeholders with information that helps in making decisions. However, most companies in Jordan mainly practice financial accounting and focus little on management accounting (Naz et al., Citation2016).

In the development of MAIS, companies rely on the existence of many strategies according to specific standards to keep pace with the effects and rapid changes, side by side with competition in our time. Furthermore, the world has become characterized by innovation and change, technical innovations, and modern systems (Irfan et al., Citation2022). Considering technical developments and rapid changes, MAIS is no longer able to face the renewed problems and challenges posed by change (Enyi et al., Citation2019). A modern, unorthodox system capable of keeping up with development, innovation, and its impact on financial performance was designed using MAIS, which also served as a mediator between innovation strategy and financial performance. Accordingly, two theories have been relied on, the contingency theory, which is one of the theories commonly used in managerial accounting, and it is the optimal theory for the MAIS (Monehin & Diers-Lawson, Citation2022; Shenkar & Ellis, Citation2022). In addition, the resource-based viewpoint that seeks to explain the difference in firm performance between different firms in the same industry has been relied upon (Al-Abdallah & Al-Salim, Citation2021; Gerhart & Feng, Citation2021; Khanra et al., Citation2022). Therefore, the understanding and awareness of Jordanian industrial companies and their quest to apply modern accounting systems and develop continuously help to achieve efficiency, effectiveness, and competition, which directly affects the innovation strategy and financial performance. Accordingly, the study of the relationship between MAIS as a mediating variable and innovation strategy is side by side with the financial performance in the Jordanian industrial sector.

1.1. Study importance

This study is significant because it examines the evolution of MAIS and its mediating role in the relationship between innovation strategy and financial performance in Jordanian industrial companies. The impacts of this evolution are anticipated to enhance financial performance. Additionally, as the industrial sector helps to define the structure of the national economy, industrial enterprises need MAIS in order to carry out their duties effectively and efficiently by making diverse judgments in various administrative scenarios. Utilizing a contemporary MAIS that aids businesses in making wise selections about enhancing their innovation strategy and financial performance is crucial given the competitive situation in the Jordanian market (Alfawaire & Atan, Citation2021; Almahirah, Citation2022). Therefore, this study came to highlight the relationship of MAIS as a mediator between innovation strategy and financial performance in Jordanian industrial companies. It is considered one of the current topics, as there are not enough studies concerned with the MAIS and its relationship between innovation strategy and financial performance in the industrial sector.

2. Literature review and hypotheses

2.1. Contingency theory

The best theory for a MAIS is the contingency theory, which is one of the theories frequently used in management accounting (Araral, Citation2020). According to Christen and Lovaas (Citation2022), there isn’t an ideal design for a (MAIS), instead, they identify contingency variables including technology or environmental unpredictability, scale, strategy, or ideal design. Consider a scenario in which the (MAIS) deviates from the ideal design by offering either too little or too much information. In that instance, businesses could experience issues with low performance caused by incompatibility (Safari & Saleh, Citation2020). There is fit and has been described as the heart of contingency theory. There are four primary forms of fit: Selection fit, Interaction fit, Systems fit, and Mediating fit (Mong Le et al., Citation2020). The intermediate fit model is often associated with pathways between contextual variables, aspects of the managerial accounting variable, and organizational outcomes (McAdam et al., Citation2019). This ergonomic model has been used in previous studies (Gunarathne & Lee, Citation2021; Monehin & Diers-Lawson, Citation2022; Shenkar & Ellis, Citation2022; Soewarno & Tjahjadi, Citation2020). Additionally, earlier mediation models for the (MAIS) variable might clarify how mediating variables shape the association between innovation strategy and financial performance (Krishnan et al., Citation2021). The importance of examining the link between the use of management accounting information and performance to direct and indirect effects through the mediating variable that captures the overall effects of the use of management accounting information performance was confirmed by Mong Le et al. (Citation2020). In order to investigate the mediating role of (MAIS) on the relationship between innovation strategy and financial performance, a median model was constructed for this study.

2.2. Resource-based view

The resource-based perspective aims to explain why different businesses operating in the same sector perform differently from one another (Khanra et al., Citation2022). The literature is largely resource-based (Mong Le et al., Citation2020). Additionally, the study contends that since businesses have unique, priceless, and irreplaceable resources, they may distinguish themselves from rivals in the same industry by putting innovative value creation strategies in place. This will provide a durable competitive edge (Al-Abdallah & Al-Salim, Citation2021). Some research has advocated the potential for innovation by drawing on the resource-based view (Maina & Mburugu, Citation2020). Furthermore, (MAIS) represents distinct resources and competencies and can be crucial for achievement, a competitive edge, and an improvement in financial performance (Gerhart & Feng, Citation2021; Soewarno & Tjahjadi, Citation2020).

2.3. The relationship between innovation strategy and MAIS

A high-value orientation of industrial companies will certainly provide innovation, ideas, products, and innovative projects more than industrial companies with a low orientation towards innovation, but these ideas, products, and projects may result in greater risk and uncertainty (Abba et al., Citation2018; Alshirah et al., Citation2021; Hadid & Al-Sayed, Citation2021). Therefore, Industrial companies need more information to decide if there is uncertainty in their work, and tension is high, extensive MAIS becomes necessary to assess potential competitors’ actions and customer needs (Luo, Citation2022). Miftah and Julina (Citation2020) stressed that MAIS has an impact on all corporate departments, particularly data about innovation strategy. The supply of timely information is helpful for industrial organizations to make decisions for changes and competitive markets and integrated and aggregated information has an increasingly essential function in coordination and decision-making (Ghasemi et al., Citation2016).

Also, Miftah and Julina (Citation2020) tested the indirect Impact of Innovation on MAIS as a Mediating Variable. The managers in the Riau Province-based Crude Palm Oil (CPO) sector served as the samples. SEM-PLS was used to process the data once it was obtained through surveys. According to the findings, innovation has an impact on a company’s performance. Impacts of innovation and business performance are mediated by MAIS. For the first time, particularly in Indonesia, a study on MAIS as a nested variable in the palm oil industry was carried out. The innovations introduced by the company through a good MAIS will improve the company’s performance in producing the CPO. Moreover, several factors have been proposed for the innovation strategy, including (Management orientation towards innovation, innovation capability, and riskiness; Karabulut, Citation2015; Mong Le et al., Citation2020).

2.3.1. Management value orientation towards innovation

As a result, management’s value orientation toward innovation represents management’s opinions on creative and innovative working practices (Mong Le et al., Citation2020). Miftah and Julina (Citation2020) emphasized that MAIS helps the management of these companies in facing the obstacles of competition in the market and monitoring performance in a competitive environment. Similarly, (Mohedano-Suanes et al., Citation2021) figured out that the implementation of the innovation strategy in companies needs a positive work environment by the companies’ management. Furthermore, Ashal et al. (Citation2021) conducted a study on the effect of strategic leadership orientation on organizational performance in Jordanian telecom enterprises. While the study advised Jordanian telecom businesses to understand the value of strategic directions to enhance organizational performance. They must also guarantee that an environment that values learning and innovation plays a key role in enhancing organizational success. Last but not least, they need to make sure that a culture of learning and innovation is in place to optimize the influence of strategic direction on organizational performance. Moreover, Muangmee et al. (Citation2021) emphasized on the implementation of the innovation strategy and improving financial performance may fail even if the work climate is positive and if the management does not develop the innovation strategy.

An innovation-based strategic orientation is related to the sub-construct of “innovation orientation,” which is used to describe the overall dominating strategy that characterizes an organization’s competitive posture and strategic focus (Farooq et al., Citation2021). This research incorporates systematically examined material to promote an all-encompassing viewpoint on innovation orientation. It provides an updated conceptualization of the innovation orientation and discusses internal organizational variables as well as external factors that can support the development of creative businesses. In order to achieve innovation and increase financial performance, it is necessary for management to support the implementation of an ambitious innovation strategy and foster a creative culture among personnel (Muangmee et al., Citation2021). The study’s findings are also in line with those of Al-Sa’di et al. (Citation2017) that advised managers of Jordanian manufacturing firms to enhance and adopt operating processes by putting a greater emphasis on process innovation and technological systems than on product innovation. Although product innovation may have an impact on other performance factors, such as financial and market factors, it has not been demonstrated to have a substantial impact on organizational performance. According to Migdadi et al. (Citation2017), managers in Jordanian businesses should pay special attention to innovation because it is a crucial part of enhancing overall company performance and sustaining competitiveness. This result is in line with Alshourah (Citation2021), where supplier management was unable to demonstrate a meaningful relationship between the strategy for product innovation and the operational procedures. It has important ramifications because developing thorough and efficient aspects of overall quality management, as well as product and process innovation in manufacturing companies, is essential to fending off intense rivalry and innovation in the Jordanian industrial organizations’ sector. In the same context, AlTarawneh et al. (Citation2021) discovered that the application of modern accounting systems in industrial companies is weak. As a result, they made several recommendations, the most crucial of which is the requirement to create a contemporary technological environment to link modern accounting systems with different accounting systems in Jordanian industrial companies, as well as to carry out studies and research in the advanced methods and modern systems of the strategy and linking it to the. The findings showed that a contextual component that influences MAIS is management’s orientation towards innovation. Thus, the following hypothesis was proposed:

H1: There is a significant relationship at (α ≤ 5%) between Management’s value orientation towards innovation and MAIS.

2.3.2. Innovation capability

Considering this, the study focuses on the ability of companies to bring about change, where the Innovation Capability is related to the company’s Innovation capability and introduce new competitive processes, ideas, and products into the company (Mong Le et al., Citation2020). According to Rajapathirana and Hui (Citation2018), organizational performance may be broken down into several hierarchical constructs that represent both financial and operational performance, including the market share and quality. Numerous studies have examined the relationship between innovation and corporate performance. The most important connection is between innovation and organizational performance. There are frequently inconsistent outcomes, according to an earlier study. Their findings alternate between positive and negative ones. Innovative performance plays the role of a mediator between performance kinds and aspects. The performance of the organization is strongly and directly impacted by innovation. Innovative performance serves as a mediator for the direct positive influence of the financial, market, and production performance, which are all favorably correlated with innovation. The main metric for measuring an organization’s performance is its innovation strategy. In addition, there is a positive impact of digital systems on the performance of the institution and its Innovation capability, and indicated that the Innovation capability had a positive impact on the performance of the institution (Al-Husban et al., Citation2021). Moreover, it has been demonstrated that Innovation capability plays a mediating role in the relationship between digital systems and enterprise performance in the Jordanian industrial sector. In addition, AlTarawneh et al. (Citation2021) found that the Innovation capability plays a mediating role in improving organizational performance, which recommended company managers support organizational activities that lead to the creation of new products and services that fit the general context of customer development and recognizing the importance of acquiring the company flexibly, returning resources that can be reallocated to meet the changes in the business environment, and adopting modern business models based on stimulating collaborative work and adopting Creative ideas. ALI et al. (Citation2020) confirmed that product and marketing innovation capabilities have a significant impact on the financial performance of SMEs, while organizational and process innovation capabilities positively affect the operational performance of SMEs in Jordan. Alnaim et al. (Citation2022) found in their study that there is a positive relationship between innovation and corporate financial performance, with corporate information systems playing a positive mediating role in the relationship between innovation and corporate financial performance. In short, the innovation of corporate information systems is one of the key factors that must be taken into account by the industrial sector wishing to maintain its survival in the current competitive market.

Furthermore, only a corporation has the innovation capability can innovation take place (Pei et al., Citation2022). Innovation capability is regarded as one of the most important assets that businesses can have to maintain their competitive edge and carry out their complete strategy. It is a product of the firm’s primary process and cannot be distinguished from the other practices (Robb et al., Citation2022). It is implicit, unchangeable, and strongly tied to experiential learning and internal experiences (Mazzucchelli et al., Citation2021). Innovation-capable companies can swiftly introduce new products and adapt new processes, which is a crucial aspect in sustaining the current level of competition. The combination of resources and assets can be used to explain innovation performance. Moreover, (Muskat et al., Citation2021) emphasized that companies need to adopt internal innovation processes to stay connected with their changing external environment. As confirmed by (Lütjena et al., Citation2019) that the importance of aligning the strategic factors of internal and external innovation capacity. Moreover, this success requires a flexible and high-quality MAIS for timely decision-making (Muskat et al., Citation2021). Thus, the following hypothesis was proposed:

H2: There is a significant relationship at (α ≤ 5%) between Innovation capability and MAIS.

2.3.3. Riskiness

Implementing the innovation strategy within the corporate structure needs reliable information, so companies need reliable information to implement the innovation strategy (Soewarno & Tjahjadi, Citation2020). (Karabulut, Citation2015) stressed that expecting the success of a new product in the market is very difficult, as riskiness has a role in encouraging the behavior of market opportunities by converting them into innovative products. Companies can boost their competitive edge if they approach innovations with a high level of riskiness. Abu Afifa and Saleh (Citation2021) claimed that these findings support the use of advanced management accounting systems (MASs) rather than conventional systems in businesses in order to enhance information quality and control levels and lower risks through the application of enterprise risk management in Jordanian industrial companies. According to Al-Nimer et al. (Citation2021), there is a positive relationship between corporate riskiness management and financial performance in Jordanian companies.

The results of the study by Karabulut (Citation2015) showed that riskiness has a favorable impact on financial success. As a result, organizations should adopt an innovation strategy to outperform their rivals and assist managers in keeping track of performance in a challenging, competitive climate. As a result, MAIS has a significant impact on predicting the difficulties that may arise while implementing alternatives in various processes including planning, controlling, and making decisions (Soewarno & Tjahjadi, Citation2020). Depending on is sighted by Yang et al. (Citation2018), enterprise riskiness management practices significantly affect small and medium-sized companies’ competitive advantage and performance, and the advised the importance of implementing companies’ riskiness management practices to gain competitive advantage, superior performance, and effectiveness to gain competition. Thus, the following hypothesis was proposed:

H3: There is a significant relationship at (α ≤ 5%) between Riskiness and MAIS.

2.4. The relationship between MAIS and financial performance

The efficient integrated MAIS provides highly flexible information, and it provides quality and consistent financial reports promptly for decision-making (Al-Waeli et al., Citation2020). Several studies have focused on this organism, as mentioned (Onodi et al., Citation2021). There is a noticeably positive relationship between the financial performance and the profitability of commodity companies through the impact of MAIS, as they used the survey study designed for this study is a good way, and it distributed 100 questionnaires to the employees of specific companies. Moreover, Afifa and Saleh (Citation2021) conducted a study on Jordanian industrial companies and found that management accounting systems have a significant impact on financial performance (FP).

In addition, Mong Le et al. (Citation2020) presented a study on the management approach to managing accounting information that had a significant impact on innovation and improving the financial performance of companies in Vietnam. It was one of the first studies that focused on the aspect of financial performance. At the same time, 200 managers with high and medium experience were collected from small and medium-sized Vietnamese companies through survey questionnaires. Moreover, other studies with similar frameworks were conducted in different countries. For example, Maina and Mburugu (Citation2020) conducted a similar study on 488 12-category industrial firms in Kenya in other sectors using descriptive and inferential statistics in the study. Although it was conducted on a larger sample and with a larger period, its results supported the idea of a positive relationship between the impact of accounting information systems and financial performance. In contrast, Ganyam and Ivungu (Citation2019) found that the use of survey design to examine this relationship by most firms was represented in developed countries. Furthermore it, Al-Khasawneh et al. (Citation2020) found that there is a strong positive impact of modern management accounting techniques on operational and financial performance in the Jordanian industrial companies listed on the Amman Stock Exchange.

Therefore, it is recommended to focus on the literature gap and fill this area (Ganyam & Ivungu, Citation2019). Moreover, managers enhance information system accounting to stay at a competitive advantage and improve the financial performance of companies under technological technology. In particular, Malek and Mahdi (Citation2019) indicated the identification of methods of administrative accounting tools to ascertain the extent of their application to the tax operations of banking services in Sudanese banks and their application problems. The study results included Banks operating in Sudan that have internal expertise that enables the application of modern methods in managerial accounting for banking services.

Furthermore, the result of (Kalbouneh et al., Citation2011) was not identical, which aimed to measure the extent of the effect of using a computerized accounting information system on the financial performance of the Jordanian industrial companies on Amman stock exchange, which indicated that the financial performance was not affected by using the accounting information system. (Kalbouneh et al., Citation2011) recommended using other variables and larger sample size for a more extended period. Moreover, (Liem & Hien, Citation2020) confirmed that the use of MAIS has a positive impact on the financial performance of the company. Where managers can obtain and process information through MAIS, which supports managers in forecasting changes that occur in the internal and external environment from the diversity of customer needs and facing competitors, and providing new products continuously (Liem & Hien, Citation2020). In addition, Setyani et al. (Citation2022) emphasized that MAIS is used to compare results with other competitors to help make decisions that contribute to improving financial performance and enhancing company performance.

Moreover, (Al-Salem & Malkawi, Citation2021) indicated in a study that applied in Jordanian companies that the effectiveness of these accounting systems lies in applying within these companies and developing the capabilities of their users to improve the expected performance. In addition, the result showed that AIS mediates the relationship between business strategy and financial performance (Melhem et al., Citation2021). At the same time, the delivery of information to management is very important and needs a timeless MAIS for project management (Alsufy, Citation2019). According to (Alsufy, Citation2019) timeless speed is more important than accuracy because timeless information allows decisions and pricing management without fear of unexpected risks. In addition, information must be provided on time to make wrong financing decisions. Some factors improve financial performance and profitability in industrial companies, the most important of which is organizational performance management (Onodi et al., Citation2021). Thus, the hypothesis was proposed:

H4: There is a significant relationship at (α ≤ 5%) between MAIS and financial performance.

2.5. The mediating role of the use of MAIS in the relationship between innovation strategy and financial performance

One of the main factors in strengthening the market share of companies is the innovation strategy that gives companies a competitive advantage over others (Chaudhry et al., Citation2020). Three innovation strategies affect the company’s performance: These dimensions include market performance, financial performance, and customer performance. Moreover, innovation strategy has a significant effect on performance, so well-performing companies have an easy financing option. This increases process innovations and product improvement. However, similar innovations in creating a product may reduce its effectiveness (Saeidi & Othman, Citation2017). Accordingly, several studies have confirmed that innovation processes greatly help in enhancing financial performance (Chaudhry et al., Citation2020; Fuzi et al., Citation2019).

Moreover, suppose companies are to sustain in an environment characterized by rapid change. In that case, they must innovate, and one of the main drivers of the company’s succeeds and improves financial performance (Mong Le et al., Citation2020(. So, the companies’ orientation towards the MAIS has a mediating role in the innovation strategy and financial performance. In addition, depending on the appropriate intermediate form of the contingency theory (Abba et al., Citation2018; Al-Baghdadi et al., Citation2021, Citation2020), all researchers defined the role of the mediator for MAIS. In light of this, MAIS can deliver thorough, integrated, aggregated, and timely MAIS that complements company culture and innovation strategy, hence improving financial performance.

Additionally, numerous theoretical and empirical research has demonstrated the beneficial effects of the dominant role of MAIS in the relationship between innovation and financial performance (Ali & Oudat, Citation2021). The corporation believes that the capacity for innovation is a strength that creates a competitive advantage and improved financial performance based on Resource Theory (Soewarno & Tjahjadi, Citation2020).

In a study conducted by (Pasch, Citation2019). It was found that there is a positive effect between innovation strategy and its use of MAIS; where the study contributed to understanding how companies follow the strategy of innovation and product differentiation through successful innovators can explore competitive products through MAIS that supports facing technology, competition, and decision-making (Pasch, Citation2019). According to the resource-based theory, a company’s Innovation capability to use limited, distinctive, and innovative resources will determine its competitive advantage and financial performance (Chaudhry et al., Citation2020). Additionally, (Otley, Citation2016) confirmed that the innovation strategy used by businesses contributes to improved financial performance. Thus, there is enough evidence to support the existing views that innovation improves business success and raises financial performance. This means that the theories and books that are currently available provide enough evidence to support the claim that innovation improves a company’s performance.

A similar study conducted by (Maina & Mburugu, Citation2020; Soewarno & Tjahjadi, Citation2020) on companies in Indonesia emphasized in their study that innovation strategy is a vital resource to develop financial performance and gain competitive advantage, as the financial strengthening of companies needs to adapt to the business environment using innovation through better management of environmentally oriented operations, customer management, and management Process innovation.

According to (Güngör et al. Citation2020), the Ensured that the main objective of companies is to improve innovation strategy and maximize value, so financial performance plays an essential role in achieving this goal for the economies of companies and countries, as it is an assessment of many companies, managers, suppliers, employees, and important competitors of many interest groups. Furthermore, Nizar (Citation2020) analyzed 50 companies within the Colombo Stock Exchange in Sri Lanka and the results showed a positive relationship between supporting management decisions and improving financial performance. The findings indicated that these systems are being used more frequently in Sri Lanka. As a result, the majority of empirical studies (Güngör et al., Citation2020; Mong Le et al., Citation2020; Nizar, Citation2020; Soewarno & Tjahjadi, Citation2020) showed that there is a positive association between the Innovation capability to implement an innovation strategy and financial performance. Thus, the following hypotheses were proposed:

H5: There is a significant mediating role of MAIS at (α ≤ 5%) on the relationship between Management’s value orientation towards innovation and financial performance.

H6: There is a significant mediating role of MAIS at (α ≤ 5%) on the relationship between Innovation capability and financial performance.

H7: There is a significant mediating role of MAIS at (α ≤ 5%) on the relationship between Riskiness and Financial performance.

3. Study methodology

3.1. Study method

The study follows a quantitative approach to determine the mediating role of the MAIS in the relationship between innovation strategy and financial performance in Jordanian industrial companies; where the data studied, analyzed, and variables are discussed in order to deal with testing hypotheses and show the results and recommendations of the research.

The descriptive-analytical approach was used in this study, which is one of the field studies, to determine the MAIS mediating role in the relationship between innovation strategy and financial performance in Jordanian industrial enterprises. The questionnaire and study model were developed by addressing studies that addressed the same research topic for the current study within the past two years (Enyi et al., Citation2019; Mong Le et al., Citation2020; Onodi et al., Citation2021; Soewarno & Tjahjadi, Citation2020). The study examines a questionnaire to identify the mediating role of the MAIS in the relationship between innovation strategy and financial performance.

The study developed a questionnaire to measure the relationship between the variables for each component of the innovation strategy, Management accounting information system, and financial performance, as follows:

Innovation strategy: the management’s orientation towards innovation, innovation capacity, and riskiness.

Management accounting information system: integration management, sales management system, management reporting system, budget management system, timeliness.

Financial performance: organizational performance.

However, the poll has been translated into Arabic because it must be carried out in a nation that does not know English. All terms have been translated as accurately as possible to allow the study to compare the results of this survey to those from other surveys that were similar to it (MAIS.IS.FP) and to ensure the validity and reliability of the translated questionnaire. Appendix No. 2 displays the questionnaire form. Six accounting scholars with expertise in auditing and accounting information systems pretested the questionnaire. This process aids in giving the best input on the questionnaire’s layout and content.

Structural Equation Modeling (SEM) was used in this study since it is one of the most effective statistical tools that analyze a variety of connected interactions between several independent and dependent variables simultaneously. Structured equation modeling (SEM) can be divided into two categories: covariance-based structural equation modeling (CB-SEM) and variance-based structural equation modeling (VB-SEM). Based on the study’s goal and the way the data are distributed, one type is preferred over the other. If the objective is the comparison of different theories or the validation of one theory, CB-SEM is used. Another name for variance-based structural equation modeling is partial least squares-based structural equation modeling (PLS-SEM). If the research is exploratory and the goal is to make a forecast, this is the preferred strategy. Additionally, the number of indicators per construct might be one or more, although CB-SEM requires three or more indicators. The main goals of VB-SEM are to maximize the variance explained in the dependent constructs and to evaluate the data’s quality in light of the properties of the measurement model (Hair et al., Citation2017). Due to the exploratory nature of the investigation and the fact that our data satisfy the prerequisites listed earlier, the PLS-SEM was used in this analysis.

3.2. Study model

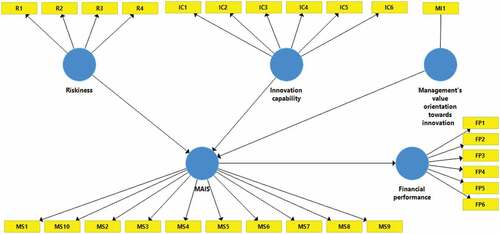

A research model was created based on prior studies in order to fulfill the study’s aim and accomplish its unique objectives (Enyi et al., Citation2019; Karabulut, Citation2015; Mong Le et al., Citation2020; Onodi et al., Citation2021). As a result, Figure illustrates the correlations between these factors.

Figure 1. The study model.

The respondent views the concept of “ Management’s orientation towards innovation” as being limited in scope, one-dimensional, and straightforward. Therefore, the ideal measuring strategy is to use a single-item construct. As stated by Rossiter (Citation2002, p. 313) “when an attribute is judged to be concrete, there is no need to use more than a single item … to measure it in the sale” and he then provided evidence demonstrating that a single item predictor had similar predictive validity to a multi-item scale (Diamantopoulos et al., Citation2012). PLS-SEM can easily handle single-item constructs with no identification issues (without additional requirements or constraints). Finally, for the single-item construct, the direction of the relationships between the construct and the indicator doesn’t matter as the construct and item are identical (Hair et al., Citation2017).

3.3. The study population and sample

The study sample consisted of (358) questionnaires distributed to (the general manager, financial manager, chief accountants, internal auditors, and accountants) in the Jordanian industrial companies, who were chosen randomly. Thus, the number of distributed questionnaires reached (374). Where (358) questionnaires were retrieved at a rate of (95.7%) of the total questionnaires sent electronically, all of which were subjected to statistical analysis. Thus, the sample settled on (358) respondents working in these industrial companies.

It is clear to us that the response rate is high, so it gives credibility to the study and results, as the low response rate leads to the weak statistical ability of the collected data. Especially if the studied community is large, it leads to reduce the credibility of the results. This result is consistent with (Sammut et al., Citation2021), that higher response rates provide strength and statistical confidence for the sample. Additionally, higher response rates are associated with outcomes that are more credible with important stakeholders (Lee, Citation2021).

3.4. Study tool

According to the variables used in this study, a questionnaire was created. Evaluation expressions were then used to determine the responses of the study sample on a five-point Likert scale (strongly agree, agree, neutral, disagree, and strongly disagree), and the questionnaire was distributed to the study participants. Testing the questionnaire in several ways:

Face Validity: To assess the questionnaire’s suitability as a tool for data collection, it was given to a group of academics from Jordanian universities. The suggested changes were made to the questionnaires after they had been retrieved, then the modified version was distributed to the study sample.

Tool Reliability Test: Given that 60% is the accepted threshold for generalizing the findings of such research (Malhotra, (Citation2004)0), the level of reliability of this tool according to Cronbach’s alpha is (80.8%). The reliability coefficients for each variable in the current investigation are displayed in Table below.

Convergent Validity: This is based on how well different measures of the same concept agree with one another (Hair et al., Citation2014). Convergent validity is evaluated using the following criteria: (1) Average Variance Extracted (AVE) at cut-offs (>0.50), (2) Composite Reliability at cut-offs (>0.60), and (3) the convergent validity results are displayed in Table :

Table 1. Construct Reliability and Validity

Table demonstrates that while all AVE values are lower than 0.5, all Composite reliability values are better than 0.60, except Management’s value orientation toward innovation. However, according to Shrestha (Citation2021), the constructs are still valid if AVE is less than 0.5, composite reliability is better than 0.6, and convergent validity is still sufficient.

Regarding the “Management’s orientation towards innovation,” the construct is equal to its measure, so the indicator loading is 1.00, making reliability and convergent validity assessments inappropriate (The construct has sufficient reliability), as mentioned by Hair et al. (Citation2017).

4. Data analysis and hypothesis testing

4.1. Descriptive analysis of the study variables

4.1.1. First: Descriptive analysis of the independent variable dimensions (Innovation strategy)

The first dimension of the study tool consists of the independent variable consisting of (11) statements. The means, standard deviations, and degrees of the agreement for each statement were as follows:

The mean of the sample members’ responses to the independent variable dimension of innovation strategy ranged between (3.32 and 4.12), with high and medium relative relevance, according to Table , which displays the values of the means, standard deviations, and the term’s relative importance.; where the phrase No. (1) from the (MVOTI) section, which stated “The extent of the administration’s desire to experiment new ideas” on the highest rank among the phrases with a mean of (4.12) and a standard deviation of (1.062) which means the respondents give the highest agreement for the extent of the administration’s desire to experiment new ideas; while the lowest rank was for the statement No. (3) From the (Riskiness) section, which states: “Innovation activities are seen as a very risky and not accepted approach” with mean value (3.32), medium relative importance, and a standard deviation (1.23) which means the respondents give the lowest agreement for the statement of innovation activities that are seen as a very risky and not accepted approach. The overall mean of all representations of the independent variable’s dimension was (3.779), which had a significant relative significance. This suggests that high- and medium-term innovation strategies are of importance to Jordanian industrial businesses.

Table 2. Descriptive Analysis of Independent Variables

4.1.2. Second: descriptive analysis of the mediating variable dimensions (MAIS)

The median variable dimension consisted of (10) statements, including the means, standard deviations, and degrees of the agreement for each statement were as follows:

According to Table , which displays the values of means, standard deviations, and the relative importance of the term the median variable dimension (MAIS), the sample members’ responses to this dimension had a mean that ranged from (3.780 to 4.030), with a high relative relevance; where the phrase No. (1) from the (Integration management) department, which stated “Defines cost and price information for the divisions of business unit” The highest rank among the phrases with a mean value (4.030) and a standard deviation of (0.990) which means the respondents give the highest agreement for the statement of Defines cost and price information for the divisions of the business unit; while the lowest rank was for phrase No. (3) also, the (Integration management) section states that “Information is provided on the impact of decisions throughout the business unit, and the impact of the decision of other individuals in the area of responsibility” with a mean value of (3.780) and significant High relativity and standard deviation (1.112) which means the respondents give the lowest agreement for the statement of Information is provided on the impact of decisions throughout the business unit, and the impact of the decision of other individuals in the area of responsibility. The median variable dimension’s total expressions reached the general arithmetic mean with a high degree of relative importance, which was (3.927). This suggests that the MAIS is of great importance to Jordanian industrial businesses.

Table 3. Descriptive Analysis of Mediating Variable Statements (MAIS)

4.1.3. Third: descriptive analysis of the dependent variable dimension (financial performance)

The dependent variable dimension consisted of (6) statements, in which the means, standard deviations, and degrees of the agreement for each statement were as follows:

The values of the means, standard deviations, and relative weights of the expressions for the dependent variable’s financial performance dimension are displayed in Table . It is evident from the information provided above that the sample members’ responses on this dimension ranged in mean from (3.490–4.180), with high and medium relative importance; where statement No. (1) Occurred, which stated “Emphasizing appropriate and adequate follow-up of clients to achieve growth” on the highest rank among the statements with an arithmetic mean of (4.180) and a standard deviation of (1.061) which means the respondents give the highest agreement for the statement of Emphasizing appropriate and adequate follow-up of clients to achieve growth. However, the lowest rank was for statement No. (4), which states “There is no budget for training and retraining of sales-force in an organization.” With a mean value (3.490), medium relative importance, and a standard deviation (1.164) which means the respondents give the lowest agreement for the statement. company has no funds for training and retraining salespeople. Regarding the overall mean of all expressions for the dependent variable dimension, it came in at 3.920 with a significant relative value. This indicates the interest of Jordanian industrial companies in their financial performance well, but there is an average value of (3.490), which shows the companies’ need to allocate funds for preparing and implementing training programs. Therefore, companies need skilled employees to introduce a mixture of distinctive products, these need to create a detailed plan in which all organizational goals and problems within the company are defined to contribute to setting budget priorities effectively. Moreover, this does not apply only to sales departments, and it is necessary to communicate with the heads of departments in the company, obtain weaknesses, and determine the type of training that contributes to the development of employee skills.

Table 4. Descriptive Analysis of Dependent Variable Statements (Financial Performance)

4.2. Assessment of the measurement model

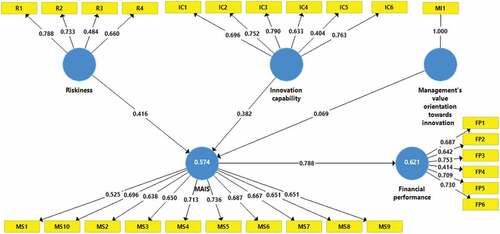

All items have their factor loading examined in order to exclude any that have low loads. Depending on the sample size, factor loading must be adjusted; for example, if there are more than 350 observations, the factor loading must be more than 30. (Gkatzelis et al., Citation2021). Since there were 358 final observations in this investigation, the cut-off factor loading of 0.30 is the most suitable. Figure displays the measurement model.

Figure 2. Measurement model.

All paragraphs are higher than 30, so none of the paragraphs will be deleted. To better display the factors loadings, they have been formulated in Table . Moreover, according to model (2), the independent variables influence the mediating variable with a percentage of (0.574), and the amount of the difference (0.43) are other variables that affect the mediating variable that was not used in the research. In addition, the mediating variable affected the relationship between the independent variable and the dependent variable with a ratio of (0.621). Thus, the median variable raised the degree of the relationship by (0.047). The following Table shows the results of Model No. (2) More clearly.

Table 5. Findings of Cross-Loadings criterion

Table 6. Findings of Fornell-Larcker Criterion

There are no cross-loadings between variables because Table demonstrates that each variable is substantially linked with and belongs to its respective concept. Because of this, and depending on the sample size, a variable with more than a substantial loading is not detected, these components stand for different and unique conceptions. Reducing the number of significant loads in each row of the factor matrix is the objective (i.e., to make each variable associated with only one factor).

The condition for discriminant validity was met since all loadings of an indicator on its assigned latent variable were larger than their loading on all other latent variables, according to a criterion provided by Fornell and Larcker (Citation1981) as shown in Table .

As can be seen in Table , each indicator has a higher loading on its assigned latent variable than it does on other variables. This indicates that a measure’s conceptual dissimilarity from another measure’s underlying construct is indicated by the degree to which it diverges from (i.e., does not correlate with) that other measure. Consequently, this aim. The axis must cross with itself to the highest degree because it knows whether the respondents, for example, interpreted the financial performance, that it explains the financial performance using the questionnaire, or explains the risks, for example.

4.3. Assessment of the structural model

4.3.1. Hypothesis testing

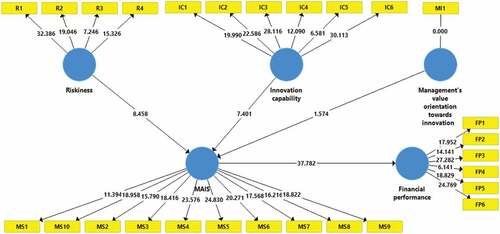

The bootstrapping technique of (Preacher & Hayes, Citation2008) was used to test the study hypothesis and the mediation effect of MAIS. As shown in Figure , the structural model aims to examine the mediating role of the MAIS in the relationship between innovation strategy and financial performance in Jordanian industrial companies.

Figure 3. Structural model.

SmartPLS 3.3 software was used to evaluate the study hypothesis, and the results are displayed in Table as follows for paths A (Independent Variables -> Mediator Variable) and B (Mediator Variable -> Dependent Variable):

Table 7. Specific indirect effects and Hypothesis Testing

Management’s value orientation towards innovation -> MAIS has a path coefficient of (0.069, p > 0.05) according to the findings of path A in Table , indicating that there is no significant relationship between Management’s value orientation toward innovation and MAIS. The null hypothesis, claims that “there is no significant relationship between Management’s value orientation towards innovation and Management accounting information system.”

According to the results of path A in Table , Innovation capability -> MAIS has a (β = 0.382, p < 0.05), which means there is a significant relationship between Innovation capability and MAIS. Accordingly, the second hypothesis was accepted which states “there is a significant relationship between Innovation capability and Management accounting information system”.

According to the results of path A in Table , Riskiness -> MAIS has a (β = 0.416, p < 0.05), which means there is a significant relationship between Riskiness and MAIS, so the third hypothesis was accepted which states “there is a significant relationship between Riskiness and Management accounting information system”.

According to the results of path B in Table , MAIS -> Financial Performance has a (β = 0.788, p < 0.05), which means there is a significant relationship between the MAIS and (FP), hence the fourth hypothesis was accepted which states “there is a significant relationship between Management accounting information system and Financial Performance.”

The result of the Indirect-Effect Hypothesis testing Path C (With Mediation) is shown in Table as follows:

Table 8. Indirect Effect Hypothesis Testing Path C (Mediation)

According to the results in Table , Management’s value orientation towards innovation -> MAIS -> Financial performance have a (β = 0.054, p > 0.05), which means there is no significant mediating role of MAIS on the relationship between Management’s value orientation towards innovation and financial performance. Thus, the first hypothesis was rejected, and the null hypothesis was accepted which states “there is no significant mediating role of management accounting information system on the relationship between Management’s value orientation towards innovation and financial performance”.

According to the results Table , Innovation capability -> MAIS -> Financial performance have a (β = 0.301, p < 0.05) which means there is a significant mediating role of MAIS on the relationship between Innovation capability and financial performance. Accordingly, the second hypothesis was accepted which states “there is a significant mediating role of management accounting information system on the relationship between Innovation capability and financial performance.”

According to the results in Table , Riskiness -> MAIS -> Financial performance have a (β = 0.328, p < 0.05), which means there is a significant mediating role of MAIS on the relationship between riskiness and financial performance, so the third hypothesis was accepted which states “there is a significant mediating role of management accounting information system on the relationship between riskiness and financial performance.

4.3.2. Predictive relevance q2, explanatory power r2, and the effect size f2

To examine the Predictive Relevance Q2, Explanatory Power R2, and the Effect Size f2 the PLS Algorithm and Blindfolding techniques are used as seen in Table .

Table 9. Predictive relevance (Q2) and Explained variance (R2) for endogenous constructs

Table shows that the mediating role of the MAIS in the relationship between innovation strategy and financial performance in Jordanian industrial companies has an explanatory power of (62.1), and the relationship between innovation strategy and MAIS in Jordanian industrial companies has an explanatory power of 57.4%. Hair and Alamer (Citation2022) argued that the explanatory power of the R2 of more than 10% is acceptable.

show the Effect sizes , according to Hanna et al. (Citation2021) guidelines, f2 ≥ 0.02, f2 ≥ 0.15, and f 2 ≥ 0.35 represent small, medium, and large effect sizes, respectively. Accordingly, there is a large effect size of each relationship in the study model. The highest largest effect size is for the MAIS; where the lowest smallest effect size is for the Management’s value orientation towards innovation.

Table 10. Effect sizes (f2)

Additionally, Stone-Geisser’s Predictive relevance is measured by Q-square, which indicates whether a model is predictively relevant or not (> 0 is good). The predictive relevance of the endogenous constructs is further established by Q2. In this study, the Q2 values are higher than zero, indicating that the study model has a predictive significance. Q2 values over zero show that values are well rebuilt and that the model has predictive relevance.

5. Discussion

There is no significant relationship between Management’s value orientation towards innovation and MAIS in Jordanian industrial companies, and the unwillingness of the management of these companies to introduce MAIS in the work environment leads to uncertainty and lack of information that affects decision-making about innovation. In addition, the senior management in industrial companies does not focus a lot on the direct supervision of the development of MAIS. And the departments are committed to the pre-established plans for the development of accounting systems, regardless of the requirements that are imposed on the improvement of their systems in line with the changes that take place in technological development. The impact of strategic leadership orientation on organizational performance in Jordanian telecom enterprises was also the subject of a study by Ashal et al. (Citation2021). While the study suggested that in order to enhance organizational performance, Jordanian telecom enterprises must understand the significance of strategic directions. They must also make sure that a culture of innovation and learning plays a key role in enhancing organizational performance. Finally, they must make sure that a culture of learning and innovation is present in order to optimize the influence of strategic direction on organizational performance. In addition, managers in Jordanian companies should focus additionally on innovation as it is an important component of achieving improved overall company performance and sustainable competitiveness (Migdadi et al., Citation2017). In the same context, AlTarawneh et al. (Citation2021) found that the application of modern accounting systems in industrial companies is weak, as he made several recommendations, the most important of which is the need to provide a modern technological environment to link modern accounting systems with various accounting systems in Jordanian industrial companies, and to conduct studies and research In the advanced methods and modern systems of the strategy and linking it to the accounting systems, in general, to accommodate environmental variables and improve financial performance.

There is a statistically significant relationship between innovation capability and the MAIS in Jordanian industrial companies. Moreover, the innovation capability is to identify new ideas and transform them into products or services; side by side with the continuous improvement of the capabilities and resources of companies to research and discover new products that meet customer needs. This result is consistent with Al-Husban et al. (Citation2021) that there is a positive impact of digital systems on the performance of the institution and its Innovation capability, and also indicated that the Innovation capability had a positive impact on the performance of the institution. Moreover, it has been demonstrated that Innovation capability plays a mediating role in the relationship between digital systems and enterprise performance in the Jordanian industrial sector. In addition, AlTarawneh et al. (Citation2021) found that the Innovation capability plays a mediating role in improving organizational performance, Where recommended company managers support organizational activities that lead to the creation of new products and services that fit the general context of customer development and recognizing the importance of acquiring the company flexibly, returning resources that can be reallocated to meet the changes in the business environment, and adopting modern business models based on stimulating collaborative work and adopting Creative ideas. In addition, Mong Le et al. (Citation2020) found that the innovation capability is linked to the company’s Innovation capability and introduces new competitive processes, ideas, and products to stay in touch with the changing external environment. As emphasized (Soewarno & Tjahjadi, Citation2020), the success of innovation requires flexibility and high quality of MAIS for timely decision-making.

There is a significant relationship between Riskiness and MAIS in Jordanian industrial companies; where those companies have a desire to invent new products and services in the markets. Still, there is a fear of riskiness arising from the application of the innovation strategy and uncertainty within this environment, which is caused by a lack of information systems in companies. Thus, the modern MAIS plays a major role in predicting the challenges and riskiness that occur by analyzing this riskiness and transforming it into activities that help companies to enhance the procedures that contribute to the innovation of new products and services in the markets. These findings were in accordance with Abu Afifa and Saleh (Citation2021) who supported the adoption of advanced management accounting systems (MASs) as opposed to conventional systems by businesses in order to enhance information quality and control levels and lower Riskiness by putting enterprise Riskiness management into place in Jordanian industrial companies. In addition, the result was consistent with Karabulut (Citation2015), and Pasch (Citation2019), where innovation riskiness positively affected financial performance, as the expectation of the success of a new product in the market is very difficult, and riskiness plays a role in encouraging the behavior of market opportunities by converting into innovative products.

There is a significant relationship between MAIS and financial performance in Jordanian industrial companies. The study that industrial companies have the most important components of MAIS; which contributes to providing internal and external information to decision-makers; help in making effective decisions. In addition, the importance of the MAIS lies in linking all the company’s departments through this management accounting system in order to transfer information and data between these departments by analyzing and forecasting the needs of customers, facing competitors, and providing new products that contribute to improving financial performance. Depending on that, this result was consistent with Al-Khasawneh et al. (Citation2020), where the results showed that there is a strong positive impact of MMAT on operational and financial performance in the Jordanian industrial companies listed on the Amman Stock Exchange. In addition, Liem and Hien (Citation2020) stressed on the use of MAIS has a positive impact on the financial performance of the company; where managers can obtain and process information through MAIS that supports managers in forecasting changes that occur in the internal and external environment from the diversity of customer needs and facing competitors, and constantly providing new products. Moreover, Setyani et al. (Citation2022), emphasized that MAIS is used to compare results with other competitors to help make decisions that contribute to improving financial performance and enhancing the performance of Certain Company.

There is no significant mediating role of MAIS at (α ≥ 5%) on the relationship between Management’s value orientation towards innovation and financial performance in Jordanian industrial companies. Therefore, according to the study results, those industrial companies in Jordan still face many problems in the application of MAIS due to the weak technical capabilities of the users of the systems in Jordanian industrial companies. In addition, the unwillingness of the management of these companies to introduce MAIS into the work environment. Consequently, these results in uncertainty and lack of information that influence innovation and financial performance decision-making. In addition, the study result is consistent with Al-Sa’di et al. (Citation2017), where managers of Jordanian manufacturing companies recommended the need to improve and adopt operating processes by focusing on process innovation and technology systems rather than product innovation. While product innovation may affect other aspects of performance, such as financial and market aspects, it has not been found to significantly affect organizational performance. Accordingly, (Al-Salem & Malkawi, Citation2021) indicated in a study applied in Jordanian companies that the effectiveness of these accounting systems lies in applying within these companies to develop the capabilities of their users to improve the expected performance. This finding is consistent with Alshourah (Citation2021) where supplier management didn’t show a significant relationship between product innovation strategy and operational processes. There are significant implications that building comprehensive and effective dimensions of total quality management and product and process innovation in manufacturing enterprises is critical to counteracting high competition and innovation in the industrial organization’s sector.

There is a significant mediating role of MAIS in the relationship between Innovation capability and financial performance in Jordanian industrial companies. The application of the Innovation capability in companies starts from the stage of preparing employees with experience, and efficiency, and giving the necessary powers that make them feel responsible and able to develop and innovation. Consequently, the introduction of a new product or service in the market distinguished from other competitors by its quality contributes to increasing revenues and improving financial performance. Therefore, the result was consistent with some studies conducted in Jordanian companies, which confirmed that innovation processes greatly help in improving financial performance (ALI et al., Citation2020; Marei, Citation2022; Zulkiffli et al., Citation2022). Also, confirmed by Alnaim et al. (Citation2022) who found that there is a positive relationship between innovation and corporate financial performance, with corporate information systems playing a positive mediating role in the relationship between innovation and financial performance of Jordanian companies. In addition, Lütjena et al. (Citation2019) emphasized the importance of aligning strategic factors with internal and external innovation capabilities. Moreover, Otley (Citation2016) confirmed that the innovation strategy that occurs in companies helps in enhancing financial performance.

There is a significant mediating role of MAIS in the relationship between Riskiness and Financial performance in Jordanian industrial companies. The Jordanian market is turbulent, and there is a desire among companies to innovate new products and services in the markets, but the uncertainty and fear of these companies make them outside the scope of innovation and competition. As a result, the result was consistent with Alsufy (Citation2019) who considered that timeless speed is more important than accuracy because timeless information allows decisions and pricing management without fear of unexpected riskiness. According to Al-Nimer et al. (Citation2021), there is a positive relationship between corporate riskiness management and financial performance in Jordanian companies. In addition, Yang et al. (Citation2018) confirmed that enterprise riskiness management practices significantly affect the competitive advantage and performance of small and medium companies.

6. Conclusions

This study aimed to examine the mediating role of the MAIS in the relationship between innovation strategy and financial performance. The study used measurable quantitative variables, and it used the descriptive-analytical method. To achieve the objectives of the research, a questionnaire was developed to determine (the mediating role of MAIS) in the relationship between innovation strategy and financial performance. The studied community consisted of all industrial companies in Jordan for the year 2021. The number of distributed questionnaires was (374). Where (358) questionnaires were retrieved by (95.7%) of the total questionnaires sent electronically, and all these questionnaires were subjected to statistical analysis using the programs (SPSS 25) and (Smart PLS 3.3). The association between management’s value orientation toward innovation, innovation capability, riskiness, and MAIS was then evaluated separately by the study. The findings showed that the value orientation of management toward innovation does not significantly influence MAIS, but that there is a substantial association between innovation capability and riskiness and MAIS. After that, it evaluated the relationship of MAIS on financial performance separately, and the results indicated an important relationship between MAIS and financial performance. The study then assessed the mediation role of MAIS in the relationship between financial performance and (management’s value orientation towards innovation, innovation capability, and riskiness). Additionally, the findings showed that MAIS had no discernible mediation effects in the relationship between management’s value orientation toward innovation and financial performance. As opposed to this, the findings showed that MAIS plays a significant mediating role in the relationship between (innovation capability, riskiness), and financial performance.

7. Recommendations

Finally, the study made the following recommendations based on the study results, firstly the management of Jordanian industrial companies must apply MAIS because systems have become a critical component, and it is difficult to achieve a competitive advantage and stay in the market without relying on information systems, and this will increase costs for companies, but in return, it improves financial performance. In addition, Managers of companies need to apply and develop appropriate guidelines for MAIS and link these systems to all company departments in an integrated manner to provide financial and non-financial reports to contribute to directing resources, and energy, and reducing costs to face competitors in the markets.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Qais Yaser Saleh

Qais Saleh completed his bachelor’s degree in Accounting and Business Law from Al al-Bayt University, and his master’s degree in Accounting and Finance at the Faculty of Economics and Administrative Sciences from the Hashemite University. His research interests focus on management accounting, management control and performance measurement, cost management, industrial sector and costing systems, quality costing and process development, accounting information technology and innovation strategy. Furthermore, Qais Saleh has over 6 years of experience in business development and growth while developing short- and long-term financial plans, budgets, and forecasts for industrial companies. Experienced in the day-to-day operations of companies, along with managing employees to increase productivity and compliance.

References

- Abba, M., Yahaya, L., & Suleiman, N. (2018). Explored and critique of contingency theory for management accounting research. Journal of Accounting and Financial Management, 4(5).

- Abu Afifa, M. M., & Saleh, I. (2021). Management accounting systems effectiveness perceived environmental uncertainty and enterprise risk management: Evidence from Jordan. Journal of Accounting and Organizational Change, 17(5), 704–28. https://doi.org/10.1108/JAOC-10-2020-0165

- Afifa, M. M. A., & Saleh, I. (2021). Management accounting systems effectiveness perceived environmental uncertainty and companies’ performance: The case of Jordanian companies. International Journal of Organizational Analysis, 30(2), 259–288. https://doi.org/10.1108/IJOA-07-2020-2288

- Ahmad, M. A., & Al-Shbiel, S. O. (2019). The effect of accounting information system on organizational performance in Jordanian industrial SMEs: The mediating role of knowledge management. International Journal of Business and Social Science, 10(3), 99–104. https://doi.org/10.30845/ijbss.v10n3p9

- Al-Abdallah, G. M., & Al-Salim, M. I. (2021). Green product innovation and competitive advantage: An empirical study of chemical industrial plants in Jordanian qualified industrial zones. Benchmarking, An International Journal., 28(8), 2542–2560. https://doi.org/10.1108/BIJ-03-2020-0095

- Al-Baghdadi, E. N., Alrub, A. A., & Rjoub, H. (2021). Sustainable business model and corporate performance: The mediating role of sustainable orientation and management accounting control in the United Arab Emirates. Sustainability, 13(16), 8947. https://doi.org/10.3390/su13168947

- Al Dabbas, M. M., & Alkshali, S. J. (2021). The impact of competitive intelligence on project success in Jordanian construction companies. European Journal of Social Sciences, 61(4), 233–249.

- Alfawaire, F., & Atan, T. (2021). The effect of strategic human resource and knowledge management on sustainable competitive advantages at Jordanian universities: The mediating role of organizational innovation. Sustainability, 13(15), 8445. https://doi.org/10.3390/su13158445

- Al-Husban, D., Almarshad, M., & Altahrawi, M. (2021). Digital leadership and organization’s performance: The mediating role of innovation capability. International Journal of Entrepreneurship, 25(5).

- ALI, H., Hao, Y., & Aijuan, C. (2020). Innovation capabilities and small and medium enterprises’ performance: An exploratory study. The Journal of Asian Finance, Economics and Business, 7(10), 959–968. https://doi.org/10.13106/jafeb.2020.vol7.no10.959

- Ali, B. J., & Oudat, M. S. (2021). Accounting information system and financial sustainability of commercial and islamic banks: A review of the literature. Journal of Management Information & Decision Sciences, 24(5).

- Al-Khasawneh, S. M., Endut, W. A., & Nik Mohd Rashid, N. N. (2020). Relationship between modern management accounting techniques and organizational performance of industrial sector listed in amman stock exchange. International Journal of Management, Accounting and Economics, 7(5), 212–234.

- Almahirah, M. S. Z. (2022). The effectiveness of the strategic activities of production and operations management in achieving the total quality of products in the Jordanian pharmaceutical production company. Journal of Positive School Psychology, 2907–2916.

- Alnaim, M. M. A., Sulong, F., Salleh, Z., & Alsheikh, G. A. A. (2022). Conceptual paper on corporate environmental performance as mediating between innovation and financial performance in Jordanian industrial sector. Strategic Management Journal, 21(S2), 1–9.

- Al-Nimer, M., Abbadi, S. S., Al-Omush, A., & Ahmad, H. (2021). Risk management practices and firm performance with a mediating role of business model innovation. Observations from Jordan. Journal of Risk and Financial Management, 14(113), 1–20. https://doi.org/10.3390/jrfm14030113

- Al-Sa’di, A. F., Abdallah, A. B., & Dahiyat, S. E. (2017). The mediating role of product and process innovations on the relationship between knowledge management and operational performance in manufacturing companies in Jordan. Business Process Management Journal, 23(2), 349–376. https://doi.org/10.1108/BPMJ-03-2016-0047

- Al-Salem, S., & Malkawi, M. (2021). The impact of structural characteristics on the effectiveness of information systems “A field study in the Jordanian industrial shareholding companies”. The Jordan Journal of Applied Science, 7(1).

- Alshirah, M., Lutfi, A., Alshirah, A., Saad, M., Ibrahim, N. M. E. S., & Mohammed, F. (2021). Influences of the environmental factors on the intention to adopt cloud-based accounting information system among SMEs in Jordan. Accounting, 7(3), 645–654. https://doi.org/10.5267/j.ac.2020.12.013

- Alshourah, S. (2021). Assessing the influence of total quality management practices on innovation in Jordanian manufacturing organizations. Uncertain Supply Chain Management, 9(1), 57–68. https://doi.org/10.5267/j.uscm.2020.12.001

- Alsufy, F. (2019). The effect of speed and accuracy in accounting information systems on financial statements content in Jordanian commercial banks. International Journal of Business and Management, 14(8).

- AlTarawneh, I. M., Al-Thnaibat, H., & Almomani, S. N. (2021). The impact of strategic management accounting techniques on achieving competitive advantage in the Jordanian public industrial companies. Academy of Accounting and Financial Studies Journal, 25(2), 1–15.

- Al-Waeli, A. J., Hanoon, R. N., Ageeb, H. A., & Idan, H. Z. (2020). Impact of accounting information system on financial performance with the moderating role of internal control in Iraqi industrial companies: An analytical study. Jour of Adv Research in Dynamical & Control Systems, 12(8), 246–261. https://doi.org/10.5373/JARDCS/V12I8/20202471

- Araral, E. (2020). Why do cities adopt smart technologies? Contingency theory and evidence from the United States. Cities, 106, 102873. https://doi.org/10.1016/j.cities.2020.102873

- Ashal, N., Alshurideh, M., Obeidat, B., & Masa’deh, R. (2021). The impact of strategic orientation on organizational performance: Examining the mediating role of learning culture in Jordanian telecommunication companies. Academy of Strategic Management Journal, 21, 1–29.

- Azwardi, P. C., Azwardi, P. C., Azwardi, P. C., Azwardi, P. C., & Azwardi, P. C. (2021). The role of accounting information system afflication in reliability financial reporting. Ilomata International Journal of Tax and Accounting, 2(1), 97–112. https://doi.org/10.52728/ijtc.v2i1.208

- Chaudhry, N., Asad, H., Karami, M., Ch, M., & Hussian, R. (2020). Environmental innovation and financial performance: Mediating role of environmental management accounting and firm’s environmental strategy. Pakistan Journal of Commerce and Social Sciences 2020, 14(3), 715–737.

- Chen, L., Li, T., Jia, F., & Schoenherr, T. (2022). The impact of governmental COVID‐19 measures on manufacturers’ stock market valuations: The role of labor intensity and operational slack. Journal of Operations Management.. https://doi.org/10.1002/joom.1207

- Christen, C. T., & Lovaas, S. R. (2022). The dual-continuum approach: An extension of the contingency theory of strategic conflict management. Public Relations Review, 48(1), 102145. https://doi.org/10.1016/j.pubrev.2021.102145