Abstract

Retail banking services of Vietnamese commercial banks are developing along with economic growth, improving the repurchase behavior of customers helps banks maintain a competitive edge in the market. Therefore, the research was conducted on factors affecting satisfaction and intention to repurchase retail banking (RB) services. This study builds and validates the Structured Equation Model (SEM) to assess the causal effect of factors such as service quality, brand reputation and customer trust on customer satisfaction and repurchase intention RB services of commercial banks in Vietnam. Survey results of 605 customers have shown that 6 factors affect positively the intention of individual customers to repurchase banking services. In the transition from satisfaction to intention to repurchase the services, there are two moderating variables included in the study, which are switching costs and commitment from the relationship. The research results can be suggestions to help customers improve their intention to use the services again at Vietnamese commercial banks.

1. Introduction

RB services can be generalized as banking services provided to individuals and small and medium-sized enterprises through a network of branches, either directly or indirectly. In Vietnam, developing banking services in the direction of applying technology to make non-cash payments, manage customer relationships and cross-sell products through measuring customer behavior is a current trend. According to statistics from the Vietnam Retail Banking Forum 2022, in 2021, consumer loans of financial institutions reached nearly 8,7 billion USA, making an increase of nearly 6% compared to 2020; personal deposit products became more diversified and flexible; and on-cash payment activities also achieved high growth rates.

In the period of digital transformation, commercial banks in Vietnam are oriented to promote retail banking services due to great potential of the domestic market. After the prolonged pandemic, the demand for RB services is increasing because they bring convenience, safety and economy to customers in the process of payment and use of their income (Vietnam Banking Report, Citation2022). Banking services are useful for speeding up the cash flow process, taking advantage of the capital of all economic sectors, limiting cash payments, bringing financial benefits and save time for both commercial banks as well as customers.

The repurchase intention (RI) of a product or service of customers can be influenced by satisfaction with their past experiences. Frequency of past behavior is a feature of habit and an important feature of satisfaction for habit formation is the learned association between a particular behavior and a satisfactory outcome (Verplanken & Orbell, Citation2003). When customers are satisfied, they will put their trust in the brand, which leads to their intention to use services repeatedly when necessary.

In the past, there were studies on customer satisfaction leading to intention to repurchase RB products and services (Hellier et al., Citation2003; E.E. Izogo, Citation2016; H Wang et al., Citation2018, etc.) to evaluate the relationship between customer satisfaction and repurchase intention RB services in many countries. The intention to use the services again has also been studied by many authors (Jaewon Choi et al., Citation2011; Lavenja & Hatammimi, Citation2015; Tun & Phyo, Citation2020; Jeffry et al., Citation2021, etc.) to determine the factors affecting the behavior of re-using services after the first transaction. These studies not only have theoretical significance, but also have practical significance for commercial banks in the current fierce competition.

Consequently, the aim of this research is to (1) identify the influence of service quality, brand reputation and customer trust on customer satisfaction and repurchase intention in retail banking in Vietnam’s financial market (2) test the moderating effect of switching cost and commitment from relationships in the transition from satisfaction to repurchase intention RB services. The next section is about literature review analyses of related papers, followed by a part of the data results. Finally, this article concludes with finding discussion and future implications. This study contributes and advances the literature by extending the connection between customer satisfaction and repurchase intention in the effect of switching cost and commitment from relationships in a particular Asian market where businesses value the important roles of relationship marketing. The results of the study will help managers know what factors affect satisfaction and intention to repurchase services and the importance of these factors, thereby offering some solutions and suggestions to improve the quality of RB in Vietnam and customer experience in using the banking services.

2. Literature review

2.1. Theoretical background

According to Kotler (Citation1991), satisfaction reflects customers’ post-purchase assessment of product and service quality compared to pre-purchase expectation. Crosby & Stephens, Citation1987a) determined 3 aspects of customer satisfaction in the service including “Satisfaction with employees, satisfaction with core services, and satisfaction with the organization”. Upon focusing attention on services, satisfaction can be defined as the result of a comprehensive assessment of all aspects that make up the relationship between customers and service provider. For enterprises, customer satisfaction is an essential factor that contributes to the company’s profitability through the purchasing process. Studies have demonstrated the importance of customer satisfaction to RI. More specifically, satisfied consumers are more likely to repurchase in the future than dissatisfied customers (Currás-Pérez & Sánchez-García, Citation2012). Moreover, when customers are satisfied, they will share with others about their good experiences, which is the basis for enterprises to gain more and more customers.

Repurchase intention is the process of purchasing individual goods or services from the same company (Hellier et al., Citation2003), and the reason for repurchase is primarily based on previous purchase experience. According to Rosenberg and Czepiel (Citation1984), the cost of creating a new customer is said to be about six times higher than the cost of keeping an existing customer. Therefore, if commercial banks do not focus on maintaining existing customers, it will cost a lot more to find new customers. It is for this reason that companies need to refocus their efforts on retaining existing customers or getting them to repurchase, rather than focusing entirely on acquiring new customers (DeSouza, Citation1992). For retail banking, the intention to repurchase services not only helps banks save costs but also demonstrates the strength of the bank’s brand and is an opportunity for banks to upsell and cross-sell other products and services.

There are two directions of analyzing the correlation between satisfaction and intention to repurchase services: first, satisfaction acts as an independent variable and second, satisfaction acts as an intermediate variable. The author included in the research model a number of factors affecting customer satisfaction and chose satisfaction as an intermediate variable affecting the intention of customers to repeat use of retail banking services in Vietnamese commercial banks.

2.2. Relationship between satisfaction and repurchase intention

There are many local and international studies that have shown the relationship between service quality, customer satisfaction and RI. Several studies have examined the direct and indirect relationships between quality, perception, satisfaction, and post-purchase outcomes, such as customer perception, perceived ease of use and usefulness, social influence and RI (Lavenja & Hatammimi, Citation2015).; Satisfaction has also been found to be a predictor of behavioral repurchase intention (Zeithaml, Citation1988). Anderson and Sullivan (Citation1993) showed that service satisfaction has a strong influence on RI. Thus, satisfaction is an antecedent affecting RI in the future service environment (Anderson & Sullivan, Citation1993; Patterson & Spreng, Citation1997).

High satisfaction will reduce perceived benefits of alternative services and lead to higher loyalty (Anderson & Sullivan, Citation1993), and loyalty will lead to service repurchase behavior. Empirical studies have confirmed that satisfied customers are more likely to have RI and use word of mouth more actively.

2.3. Research hypothesis

Based on the overall analysis of the above-mentioned studies, it can be seen that Service Quality, Brand Reputation and Customer Trust are the main factors to form Satisfaction of Customers using RB services in Vietnam. Satisfaction along with the factors of Switching Cost and Commitment from Relationships will have a direct impact on RI of customers. Accordingly, the author chose the research model approach through intermediate variables with the main reference being the research model of Megdadi et al. (Citation2013) due to the similarities in the area of research on RB services.

The study selected the factors affecting the intention of customers to repurchase retail banking services including (1) Satisfaction, (2) Service quality, (3) Brand reputation, (4) Customer Trust, (5) Switching Costs, (6) Commitment from Relationships. The proposed research model is as follows:

2.3.1. Variables in the model include

Independent variables affecting customer satisfaction include: Service quality, reputation and customer trust.

The independent variable of satisfaction affects the dependent variable of repurchase intention.

The moderating variables affecting the conversion from customer satisfaction to repurchase intention include: switch cost and commitment from relationships.

2.3.2. Research hypotheses include

Hypothesis H1: Service quality influences positively satisfaction;

Hypothesis H2: Reputation influences positively satisfaction;

Hypothesis H3: Customer trust influences positively satisfaction;

Hypothesis H4: Customer satisfaction influences positively repurchase intention;

Hypothesis H5: Switch cost has an influence on conversion from customer satisfaction to repurchase intention;

Hypothesis H6: Commitment from relationships has an influence on conversion from customer satisfaction to repurchase intention.

Service quality: Lehtinen and Lehtinen (Citation1982) supposed that service quality must be assessed over two aspects including the service delivery process and the service results. Grönroos (Citation1984) also suggested two elements of service quality, namely technical quality, which represents what the customer receives, and functional quality, which describes how the service is delivered. Parasuraman et al. (Citation1985) defined service quality as “the comprehensive evaluation or attitude towards the overall perfection of the service”. In short, service quality is the set of characteristics of an object, giving the object the ability to satisfy stated or implied requirements, reflecting the effectiveness of the core activities of the enterprise and directly affecting customer satisfaction, thereby leading to the intention to repurchase the products.

Brand Reputation: The concept of brand reputation is often associated with the definition of brand value (Aaker, Citation1994) or a business’s reputation for its customers (Herbig et al., Citation1994). Brand reputation can be thought of as the result of a company’s historical relationship with the environmental context in which it operates. Acccording to Yoon et al. (Citation1993) “Data on the brand reputation of enterprises and customers will be a source of information for customers to appreciate the quality of the company’s products and services compared to available alternatives”. Thus, brand reputation is a factor that contributes to customer satisfaction with products and services and can influence the buying behavior of customers. Researched brand reputation includes belief and social value that the brand brings to customers.

Customer trust: Trust is an important factor for relationships between customers with businesses in general and with commercial banks in particular. Morgan and Hunt (Citation1994) argued that trust is the faith in a trading partner, reliability and honesty generally accepted. Trust is at the core of successful transactions and the premise of building a lasting relationship. When customers are satisfied with the service provided by a certain brand, they will be able to “forgive” non-standard banking services and ready to use them again upon guarantee of change and improvement (Moorman et al., Citation1992). On the contrary, if customers do not have faith in the bank where they use the services, worries about the risk of losing personal information or poor service quality will increase, and they will not intend to use the services or even start using the Thus, enterprises, especially commercial banks, need to build customer trust, as this is a necessary condition for customer satisfaction and thereby leads to intention to repurchase services.

Switching costs: According to Barroso and Picón (Citation2012), switching costs include three categories: (i) Customer costs related to habits, efforts, time, commitment, expertise and psychological risks; (ii) Company expenses related to reference, search, study, research, communication; (iii) Industry costs associated with shifting to other attractive, competitive alternatives. In terms of direction, switching costs can be classified as positive and negative. Positive switching costs are relational and financial switching costs that add value to customers, while negative switching costs add no value or benefits to customers (Jones et al., Citation2007 Izogo, Citation2013). In fact, customers using retail banking services in Vietnam still face many barriers when switching to other banks such as: the difference between service capacity and organizational structure; financial constraints, i.e. loss of preferential interest rates; the time constraints of opening and depositing new accounts; or obstacles of spending more time and efforts getting to know new bank tellers. Therefore, the study selected switching cost as a moderating variable that affects the conversion from satisfaction to service re-use intention.

Commitment from relationships: There is a growing recognition of the importance of developing and maintaining the long-term relationships between businesses and customers (Examples: Berry & Parasuraman, Citation1991; Sheth & Paravatiyar, Citation1994). Relationships have been emphasized by some studies as an important variable closely associated with trust, satisfaction and service repurchase (Example: Cronin & Taylor, Citation1992; Crosby & Stephens, Citation1987b). The relationship between commercial banks and individual customers is developed through the relationship between bank employees and customers, and can also be the relationship between partners, acquaintances, friends or other social relationships. Relationships are the foundation for a beneficial and emotional commitment when individual customers choose a commercial bank to use the services, thus influencing their decision to borrow money or maintain their savings at that bank or switch to another bank. Based on the characteristics of Vietnamese customers who value social relationships, the author included the factor of commitment from relationships in the study as a moderating variable between satisfaction and RI services and products—this is also a new aspect of the subject compared to previous studies conducted in the Vietnamese market.

3. Methodology

3.1. Measurement scale

From the proposed research model, the author built a scale inherited from the following scholars: Lada et al. (Citation2009), Kassim and Abdullah (Citation2010), Yonggui Wang et al. (Citation2003), Megdadi et al. (Citation2013), Sharma and Patterson (Citation1999), Ruiz et al. (Citation2015), Moorman et al. (Citation1992) and Hellier et al. (Citation2003). Next, the author conducted qualitative research through interviews with 10 experts in the areas of finance, banking and marketing; combined with a focus group discussion with 10 customers who have used retail banking services at commercial banks and who are living and working in Hanoi to come up with a complete scale.

The scale of this research includes 33 observed variables, therefore the sample size should be at least a multiple of 5 of 33, that is 165 observations (Hair et al., Citation1998). The author selected a size of 605 samples to improve the research quality. The data was collected by surveying individual customers who made transactions at the bank’s branches in the cities of Vietnam from 14 February 2022 to 31 March 2022.

3.2. Measurement and methodology

There are two main parts in the final questionnaire. One part is related to hypothesis factors impacting on the RI of customers, the other part is about customers’ demographic and behaviour information. All of the measures in the study employed a 5-point Likert rating scale, which corresponds to 1 = strongly disagree, 2 = somewhat disagree, 3 = neither agree nor disagree, 4 = somewhat agree, and 5 = strongly agree. After collecting data, it was analyzed in descriptive statistics. Then the authors conducted the reliability and validity test, exploratory factor analysis (EFA), confirmatory factor analysis (CFA), and structural equation modeling (SEM).

4. Results and findings

4.1. Descriptive analysis

The statistical results described in show:

Table 1. Overall respondent’s demographic

In regards to respondents, 68% of them have a time of using banking services over 3 years. This is understandable because RB services in Vietnam have been developed for more than 10 years, besides, after nearly 3 years of the Covid 19 pandemic, people have used RB increasingly. The number of simultaneous users of 2 banks accounts for the largest proportion (41%), this is the result of interbank connections and promotion campaigns of commercial banks promoting customers to open more banking accounts.

In terms of respondents’ demographic, more than half of them are officers and freelancers, the group with average income from 10 to under 20 million is the largest (35.7%); 63% of them are middle-aged citizens (from 30 to 49 years old). In general, people using RB services are middle-aged and middle-income. They live in big cities in Vietnam such as Hanoi, Danang, Ho Chi Minh city, Hai Phong and Can Tho (94.5%).

4.2. General research model testing

The results from evaluation of the distribution form of the scale show that the Min and Max of the observed variables are in the range of 1 to 5 with the mean values of all the variables greater than 3 and the standard deviations of the variables all smaller than 1 except for variable SC5. In particular, the mean value of the observed variables of Service Quality and Satisfaction is relatively high, showing that individual customers’ satisfaction with RB services at commercial banks in Vietnam is quite high.

According to Hoàng Trọng (Citation2008), variables that have greater than 0.3 item-total correlations will be accepted; the other ones having smaller than 0.3 item-total correlations will be eliminated from the analysis data. Below is a summary of the reliability and total variance of the scales:

The analysis results in show that the coefficients of Cronbach’s Alpha of all variables are greater than 0.6. The total variance extracted of the research variables are > 50%, therefore, the scales are reliable. This shows that the scale has high reliability, ensuring consistency.

Table 2. Summary of reliability and total variance extracted from the scales

To assess the overall fit of the model, the following criteria were used: Chi—square (Chi squared—CMIN); Chi—Square adjusted to degrees of freedom (CMIN/df); Goodness of Fit Index (GFI); TLI (Tucker & Lewis Index); Comparative Fit Index (CFI); RMSEA (Root Mean Square Error Approximation) index. The model is considered suitable when the Chi-Square test has a P > 0.05 value.). In this study, because the research sample N = 605 > 200, it will use the criteria of Kettinger et al. (Citation1995) that accept CMIN/df < 5; GFI, TLI, CFI > 0.9 (Bentler, Citation1990); RMSEA < 0.08, case RMSEA < 0.5 is considered very good.

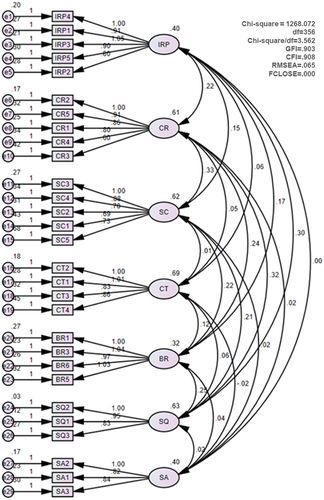

After CFA analysis (), the results show that 4 observed variables BR2, BR4, SA4 and SA5 are not eligible to be included in the analytical model because the results of the Pattern Matrix analysis show these 4 observed variables have the load factor less than 0.5. The results of the CFA test after removal of 4 observed variables show that Chi square/df = 3.562; GFI = 0.903; CFI = 0.908; RMSEA = 0.065. This proves that the critical theoretical scale fits the market data.

Figure 1. CFA analysis.

In addition, to comprehensively evaluate the quality and reliability of the scale, the author conducted an assessment of the Composite Reliability—C.R. and the Average Variance Extracted—A.V.E. According to Hair et al., Citation1998), if C.R > 0.7 and A.V.E > 0.5, it can be concluded that the observed variable is correlated with other observed variables in the same factor and the scale is considered as a convergent value. If the square root of A.V.E is larger than the correlations between the two concepts, it can be concluded that the observed variable has no correlation with other observed variables in other factors and the scale is considered discriminant. The below is the result of calculating C.R and A.V.E.

Table 3. Synthetic results of C.R and A.V.E of scales

Thus, after performance of the scale test, it can be concluded that the scale obtained in the formal quantitative research is eligible to serve as a basis for testing the research model and testing the research hypotheses set out.

The method of linear structural model (SEM) analysis was used to test the research model. In addition, the same testing criteria were applied as in the CFA analysis mentioned above. The SEM analysis results are shown as below:

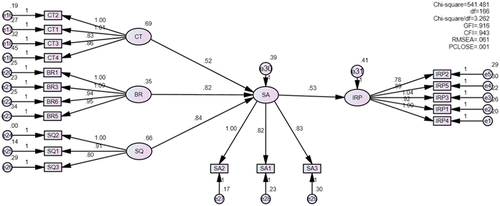

Results of testing the relevance of the research model by SEM analysis () are as follows: Chi-Square/df = 3,262; GFI = 0.916; CFI = 0.943, RMSEA = 0.061. This result shows that the model, if not affected by the regulatory variable, is completely consistent with the data of the market.

Figure 2. SEM analysis results of the theoretical research model without the influence of the moderator variables.

All impacts in the research theoretical model without the influence of the moderating variable have the significance level of P-value < 0.05. Based on the analysis results in , the factors affecting satisfaction of customers using RB services are trust, brand reputation and service quality. The most influential factor is service quality (Beta = 0.835), followed by reputation (Beta = 0.841) and finally customer trust (Beta = 0.516). Satisfaction has a proportionate relationship with repurchase intention at a strong degree (Beta = 0.527).

Table 4. Model testing results without impacts of moderating variables

This study used Hayes’s (Citation2013) linear regression analysis technique in SPSS 22.00 software. Commitment from relationships and switching costs are pure moderators, which means they only cause change to the transition from satisfaction to repurchase intention. To test the influence of the two moderators on the impact of satisfaction on repurchase intention, first, the author will perform the test for each moderator separately, and later test the concurrent influence of the two above-mentioned variables on customers’ repurchase intention.

4.2.1. Satisfaction affects repurchase intention under the influence of the moderating variable for switching costs

shows that the regression coefficient for Int_1 (XW) being b3 = 0.0510 and t(598) = 2.3173 has statistical significance (p = 0.0208 < 0.05). Therefore, the effect of satisfaction on behavioral repurchase intention is governed by switching costs. This result allows us to conclude: Switching costs have an impact on the transition from satisfaction to repurchase intention of individual customers using RB services with commercial banks.). In consistent with prior researches, Switching cost is considered one of the economic variables affecting the behavior of customers using banking services, it is also considered a competitive factor in banks (Fejza-Ademi et al., Citation2022).

Satisfaction affects repurchase intention under the influence of the moderating variable for commitment from relationships

Table 5. Results of regression to test hypothesis H5

From the , we can see that the regression coefficient for Int_1 (XW) being b3 = −0.0696 and t(596) = −2.9031 has statistical significance (p = 0.0038 < 0.05). Therefore, the effect of satisfaction on behavioral repurchase intention is governed by commitment from relationships. This result allows us to conclude that: Commitment from relationships has an impact on the transition from satisfaction to repurchase intention of individual customers using RB services at commercial banks. Therefore, our results are in line with Esat and Durguti and Kryeziu (Citation2021), whose results show that marketing relationships have an influence on customer behavior and thereby affect the profitability indicators of commercial banks.A summary of the results of the analysis is shown in below:

Table 6. Results of regression to test hypothesis H6

Table 7. Summary of hypothesis testing results

5. Discussion & implications

5.1. Discussion

The results of SEM analysis of the research model show that the factors of overall service quality, reputation and social responsibility are all significant at P-value < 0.05 and adjusted Beta weight > 0, which proves that the above factors have a positive impact on satisfaction of customers using RB services.

Apart from that, the factor having the strongest impact is service quality factor (Beta = 0.835), followed by brand reputation factor (Beta = 0.841), and customer trust factor (Beta = 0.527). This result is consistent with the actual situation, and commercial banks need to improve the overall quality of services first. Besides, it is necessary to build a better brand image and take into consideration social responsibility activities.

The analysis results show that customer satisfaction has a positive influence on customers’ repurchase intention. The influence of satisfaction on repurchase intention is stronger than the influence of the factors for trust, reputation and service quality on satisfaction. This means that in order to improve the repurchase intention of individual customers using RB services at commercial banks, it is necessary to improve their satisfaction in transactions.

The analysis results also show that the impact of switching costs and commitment from relationships has an impact on customers’ transition from satisfaction to repurchase intention. Commercial banks in Vietnam can take advantage of this to raise the barrier to switching or enhance the establishment of good relationships with individual customers, thereby positively affecting their repurchase intention.

5.2. Implications

The research results show that satisfaction is a factor that directly and strongly influences customers’ repurchase intention. In order to improve customer satisfaction, commercial banks are also required to consistently build up the elements constituting customer satisfaction.

Satisfaction should be improved through improving service quality of RB. As service quality is reflected through human resources, commercial banks need to focus on improving the service providing capacity of staff who are in direct contact with customers (tellers, fund officers, personal financial advisors) through professional training and upskilling. Besides, commercial banks need to focus on the points of interaction with customers such as: completing the process of responding to customers’ requests, questions and complaints; implementing interactive activities such as events, attractive games, etc. This is the point of contact with customers that has been built and applied by many banks around the world, especially in the retail sector.

In order to improve customer satisfaction through brand reputation, commercial banks need to invest reasonably in communication for brand advertising in particular and communication for banking services in particular. In addition, it is also necessary to take into account the financial potential and the network of the banks as well as to apply modern technology solutions to improve customer experience.

Customer satisfaction can be improved through increasing trust in the bank. As technology develops, the issues that need to be addressed by the bank to improve customer trust include ensuring customer information security, accurate transactions from the first time and no errors or frauds during the transaction process. Customer trust is also demonstrated through the high homogeneity of the quality of RB transactions, including transactions at transaction points and online transactions.

Switching costs and commitment from customer relationships are also two factors that have a positive impact on the transition from customer satisfaction to repurchase intention. Banks need to raise the barrier to switching by providing more services to customers and creating more promotions for additional benefits for users. Besides, the increase in commitment from relationships with customers also means retaining the tellers because customers remain faithful to the bank partly because of the close relationships with the bank staff.

In addition to the recommendations to commercial banks, the research team also made a number of recommendations to the State bank on the issuance of regulations and policies to manage and support commercial banks in improving their customers’ repurchase intention as well as to collaborate with other relevant agencies in proposing measures to reduce the procedures and time for approval of promotional programs, gratitude programs for individual customers using RB services of commercial banks, in order to create favorable conditions for commercial banks.

6. Limitation and further research

6.1. Limitation

In addition to the achieved results, the study still has some limitations in terms of sample size when only focusing on a few large cities of Vietnam such as Hanoi, Ho Chi Minh city, Da Nang, Hai Phong and Can Tho. As a result, the research results may not be completely consistent with many other localities, especially remote areas.

Besides, it is inevitable that the difference in qualifications and opinions of the respondents affects the research results to a certain extent. In addition, the author has not been able to research in detail and fully all the models and schools of study related to the factors included in the author’s model and there are also factors which the author has not studied yet and which may influence the results of the study.

6.2. Further research

This study was conducted on the group of individual customers using RB services. However, from a modern point of view and the actual context in commercial banks, households and micro enterprises (with a size of less than 15 staff) are also considered individual customers because of similarities in the process of decision-making, and this can be an extended research orientation for the subject.

In addition to the suggestions for improvement as mentioned earlier, in fact, customers when using RB services at commercial banks do not gain the satisfaction as expected, probably due to difficulties in various aspects such as: poor technology, unsatisfactory personnel, legal environment in Vietnam, etc. Therefore, the next studies can take these issues into consideration.

Acknowledgements

Thank VNU University of Economics and Business, Hanoi for financing the Research Project number KT.20.03. This paper has been extracted from this research.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Aaker, D. A. (1994). Measuring brand equity across products and markets. California Management Review, 38(3), 102–20. https://doi.org/10.2307/41165845

- Anderson, E. W., & Sullivan, M. W. (1993). The antecedents and consequences of customer satisfaction for firms. Marketing Science, 12(2), 125–143. https://doi.org/10.1287/mksc.12.2.125

- Barroso, C., & Picón, A. (2012). Multi-dimensional analysis of perceived switching costs. Industrial Marketing Management, 41(3), 531–543. http://dx.doi.org/10.1016/j.indmarman.2011.06.020

- Bentler, P. M. (1990). Comparative fit indexes in structural models. Psychological Bulletin, 107(2), 238–246. https://doi.org/10.1037/0033-2909.107.2.238

- Berry, L. L., & Parasuraman, A. (1991). Marketing services: Competing through quality. The Free Press.

- Choi, J., Lee, H. J., & Kim, Y. (2011). The influence of social presence on customer intention to reuse online recommender systems: the roles of personalization and product type. International Journal of Electronic Commerce, 16(1), 129–154. https://doi.org/10.2753/JEC1086-4415160105

- Cronin, J., Jr, & Taylor, S. A. (1992). Measuring service quality: A reexamination and extension. Journal of Marketing, 56(3), 55‐68. https://doi.org/10.1177/002224299205600304

- Crosby, L. A., & Stephens, N. (1987a). Effects of relationship marketing on satisfaction, retention, and prices in the life insurance industry. Journal of Marketing Research, 24(4), 404–411. https://doi.org/10.1177/002224378702400408

- Crosby, L. A., & Stephens, N. (1987b). Effects of relationship marketing on relationship satisfaction, retention, and prices in the life insurance industry. Journal of Marketing Research, 24(4), 404–411. https://doi.org/10.2307/3151388

- Currás-Pérez, R., & Sánchez-García, I. (2012). Satisfaction and loyalty to a website: the moderating effect of perceived Risk. EsicMarket Economic and Business Journal, 141, 183–207. https://ssrn.com/abstract=2168310

- DeSouza, G. (1992). Designing a Customer Retention Plan. Journal of Business Strategy, 13(2), 24–28. https://doi.org/10.1108/eb039477

- Durguti, E., & Kryeziu, N. (2021). Importance of corporate governance: evidence from kosovo’s banking sector. Croatian Economic Survey, 23(2), 5–32. https://doi.org/10.15179/ces.23.2.1

- Fejza-Ademi, V., Avdullahi, A., Tmava, Q., & Durguti, E. (2022). Analysis of the banking sector competition in Kosovo. Studia Universitatis Vasile Goldiș Arad, Seria Științe Economice, 32(2), 84–101. https://doi.org/10.2478/sues-2022-0010

- Grönroos, C. (1984). A service quality model and its marketing implications. European Journal of Marketing, 18(4), 36–44. https://doi.org/10.1108/EUM0000000004784

- Hair, J. F., Jr., Anderson, R. E., Tatham, R. L., & Black, W. C. (1998). Multivariate data analysis (5th) ed.). Prentice Hall.

- Hayes, A. F. (2013). Introduction to mediation, moderation, and conditional process analysis: A regression based approach. In The Guilford press (third edition).

- Hellier, P. K., Geursen, G. M., Carr, R. A., & Rickard, J. A. (2003). Customer repurchase intention: A general structural equation model. European Journal of Marketing, 37(11/12), 1762–1800. https://doi.org/10.1108/03090560310495456

- Herbig, P., Milewicz, J., & Golden, J. (1994). A model of reputation building and destruction. Journal of Business Research, 31(1), 23‐31. https://doi.org/10.1016/0148-2963(94)90042-6

- Hoàng Trọng, C. N. (2008). Analyze data with SPSS. In University of economics Ho Chi Minh City Vol. l. https://sachvui.com/ebook/phan-tich-du-lieu-nghien-cuu-voi-spss-tap-1-hoang-trong-chu-nguyen-mong-ngoc.857.html

- Izogo, E. E. (2013). An empirical assessment of customer switching behaviour in the Nigerian telecom industry. African Journal of Business and Economic Research, 8(1), 61–82. https://hdl.handle.net/10520/EJC134624

- Izogo, E. E. (2016). Antecedents of attitudinal loyalty in a telecom service sector: The Nigerian case. International Journal of Quality & Reliability Management, 33(6), 747–768. https://doi.org/10.1108/IJQRM-06-2014-0070

- Jeffry, Z. C. N., Ni Nyoman Kerti Yasa, I. P. G. S., & Wayan Ekawati, N. (2021). Antecedent behaviour and its implication on the intention to reuse the internet banking and mobile services. International Journal of Data and Network Science, 5(3), 451–464.

- Jones, M. A., Reynolds, K. E., Mothersbaugh, D. L., & Beatty, S. E. (2007). The positive and negative effects of switching costs on relational outcomes. Journal of Business Research, 9(4), 335–355. https://doi.org/10.1177/1094670507299382

- Kassim, N., & Abdullah, N. A. (2010). The effect of perceived service quality dimensions on customer satisfaction, trust, and loyalty in e‐commerce settings: A cross cultural analysis. Asia Pacific Journal of Marketing and Logistics, 22(3), 351‐71. https://doi.org/10.1108/13555851011062269

- Kettinger, W. J., Lee, C. C., & Lee, S. (1995). Global measures of information services quality: A cross-national study. Decision Sciences, 26(5), 569–588. https://doi.org/10.1111/j.1540-5915.1995.tb01441.x

- Kotler, P. (1991). Marketing management: Analysis, planning, implementation, and control (7th edition) (pp. 756). Prentice-Hall.

- Lada, S., Tanakinjal, G. H., & Amin, H. (2009). Predicting intention to choose halal products using theory of reasoned action. International Journal of Islamic and Middle Eastern Finance and Management, 2(1), 66–76. https://doi.org/10.1108/17538390910946276

- Lavenja, C., & Hatammimi, J. (2015). Factors affecting the intention to reuse mobile banking service. International Journal of Research in Business and Social Science, 4(4), 2147–4478. https://doi.org/10.20525/ijrbs.v4i4.15

- Lehtinen, U., & Lehtinen, J. R. (1982) Service quality: A study of quality dimensions. Working Paper. Service Management Institute, Helsinki.

- Moorman, C., Deshapande, R., & Zaltman, G. (1992). Factors affecting trust in market research relationships. Journal of Marketing, 57(1), 81–101. https://doi.org/10.1177/002224299305700106

- Morgan, R. M., & Hunt, S. D. (1994). The commitment-trust theory of relationship marketing. Journal of Marketing, 58(3), 20–38. https://doi.org/10.1177/002224299405800302

- Parasuraman, A., Zeithaml, V. A., & Berry, L. L. (1985). A conceptual model of service quality and its implications for future research. Journal of Marketing, 49(4), 41–50. https://doi.org/10.1177/002224298504900403

- Patterson, P. G., & Spreng, R. A. (1997). Modelling the relationship between perceived value, satisfaction and repurchase intentions in a business‐to‐business, services context: An empirical examination. International Journal of Service Industry Management, 8(5), 414–434. https://doi.org/10.1108/09564239710189835

- Rosenberg, L. J., & Czepiel, J. A. (1984). A marketing approach for customer retention. Journal of Consumer Marketing, 1(2), 45–51. https://doi.org/10.1108/eb008094

- Ruiz, B., García, J. A., & Revilla, A. J. (2015). Antecedents and consequences of bank reputation: A comparison of the United Kingdom and Spain. International Marketing Review, 33(6), 781–805. https://doi.org/10.1108/IMR-06-2015-0147

- Sharma, N., & Patterson, P. G. (1999). The effect of communication effectiveness and quality of service on customer engagement, professional services. Journal of Marketing Services, 13(2), 151–170. https://doi.org/10.1108/08876049910266059

- Sheth, J., & Paravatiyar, A. (1994). Relationship marketing theory, methods and applications. In Center for relationship marketing. Emroy University, Atlanta, USA.

- Tun, M., & Phyo. (2020). Factors influencing intention to reuse mobile banking services for the private banking sector in Myanmar. ASEAN Journal of Management & Innovation, 7(1), 63–78. https://doi.org/10.14456/ajmi.2020.5

- Verplanken, B., & Orbell, S. (2003). Reflections on past behavior: A self-report index of habit strength. Journal of Applied Social Psychology, 33(6), 1313–1330.

- Vietnam Banking Report. (2022), https://fiinresearch.vn/Store/ReportDetails?id=165025

- Wang, H., Du, R., & Olsen, T. (2018). Feedback mechanisms and consumer satisfaction. Trust and Repurchase Intention in Online Retail, Information Systems Management, 201–219. https://doi.org/10.1080/10580530.2018.1477301

- Wang, Y., Lo, H. P., & Hui, Y. V. (2003). The antecedents of service quality and product quality and their influences on bank reputation: Evidence from the banking industry in China. An International Journal, 13(1), 72–83. https://doi.org/10.1108/09604520310456726

- Yoon, E., Guffey, H. J., & Kijewski, V. (1993). The effects of information and company reputation on intentions to buy a business service. Journal of Business Research, 27(3), 215‐28. https://doi.org/10.1016/0148-2963(93)90027-M

- Younes , Megdadi, A. , Arab, Jaber, R. A. Aljaber. (2013). An examine proposed factors affecting customer loyalty toward the financial services of Jordanian commercial banks: Empirical study. International Journal of Business and Social Science, 4(10), 142–149. https://doi.org/10.13106/jafeb.2021.vol8.no2.0497

- Zeithaml, V. A. (1988). Consumer perceptions of price, quality and value: a means-end model and synthesis of evidence. Journal of Marketing, 52(3), 2–22. https://doi.org/10.1177/002224298805200302

Appendices

1. Questionnaire

Part 1: Customer opinions about bank X

Bank X that appears in the comments below is the bank with which you repurchase its products many times.

Please give your opinion in the comments below with levels ranging from Strongly Disagree to Strongly Agree.

Please give your opinion about Bank X and retail banking services of Bank X

What is your opinion on the Service Quality of Bank X?

What is your opinion on your satisfaction with Bank X?

What is your opinion on the brand reputation of bank X?

What is your opinion on customer trust in bank X?

What is your opinion on switching cost in bank X?

What is your opinion on commitment from relationships with bank X?

Part 2: Demographic questions