Abstract

The purpose of this paper is to review existing literature on the consequences of International Financial Reporting Standards (IFRS) adoption in Europe with a specific focus on different enforcement environments. Following prior studies, we adopt the critical review approach. We begin the review in Europe and then provide a comparative analysis among four countries based on their enforcement environment. Academic papers were collected from high-quality ranked journals. The literature was analysed on different streams, including comparability, audit services liquidity and earning management. Our critical review indicates that the consequences of IFRS adoption depend on the country’s enforcement environment. If a country has strong enforcement, then the consequences of IFRS adoption are more pronounced for both positive and negative consequences. This was the case for the UK and Germany. If a country has a weak enforcement environment, the consequences are less pronounced, as was the case for Spain and Italy. The consequences of IFRS adoption include increased comparability, audit fees, liquidity, earnings management and investment. If a country is to realise the benefits of IFRS adoption fully, it is not sufficient to just adopt the standards; there must be a strong enforcement environment. The paper makes suggestions for further research in the context of IFRS consequences.

1. Introduction

Prior studies highlight the difference in accounting quality across countries even after IFRS adoption due to legal and political systems (Soderstrom & Sun, Citation2007). Hence, the consequences of IFRS are less likely to be the same even for countries with similar economic environments (Brüggemann et al., Citation2013). Therefore in this paper, we review the consequences of IFRS in Europe in the light of varying enforcement environments. The enforcement environment is defined by capital market structures, and legal and political institutions have been found to significantly influence how firms benefit from adopting IFRS (Wieczynska, Citation2016).

IFRS has three main objectives. First, the standards seek to improve transparency and quality of financial information by improving the comparability of companies from different countries. Second, to reduce the information gap that is evident between those that provide capital and those that the capital providers have entrusted their money to and therefore increase accountability of management. Third, improve economic efficiency and capital allocation by enabling investors to identify opportunities and risks (IFRS Foundation, Citation2021).

Following the above-mentioned objectives of IFRS, this paper synthesises the findings on the benefits of IFRS in Europe among countries with varying enforcement environments. The literature referenced how the strength of a country’s enforcement environment affects the pronounced benefits of IFRS adoption to a firm (Christensen et al., Citation2013; Kim et al., Citation2012; Yip & Young, Citation2012). Therefore, we analyse two countries with strong enforcement environments and two with weaker enforcement. For this reason, we chose the UK, Germany, Spain and Italy. A stronger regulatory environment yields greater benefits from IFRS adoption (Gastón et al., Citation2010; Wieczynska, Citation2016). For example, De Fuentes and Sierra-Grau (Citation2015) found that regulatory restrictions in Spain meant non-audit fees did not increase as expected. This increase was evident in other jurisdictions, such as the UK (El Guindy & Trabelsi, Citation2020).

Although there are benefits that result from IFRS adoption, such as increased comparability (Wang, Citation2014; Yip & Young, Citation2012), decreased forecasting errors (Byard et al., Citation2011; Horton et al., Citation2013), and decreased cost of equity for adopting firms (Daske et al., Citation2013; Li, Citation2010). IFRS adoption does not always have positive consequences. Negative consequences include increased earnings management (Ahmed et al., Citation2013; Callao & Jarne, Citation2010; Iatridis, Citation2012; Ahmed et al., Citation2013; Callao & Jarne, Citation2010; Iatridis, Citation2012) and decreased value relevance of accounting information (Christensen et al., Citation2015; Gastón et al., Citation2010).

Our findings indicate that for a country to realise the benefits of IFRS adoption fully, it is necessary to ensure that enforcement of the standards will be strong. Countries wishing to adopt IFRS should follow the blueprint of Germany, which has a two-tier enforcement system centred around naming and shaming perpetrators (Hitz et al., Citation2012) or the UK, which is also considered to have a strong enforcement environment of IFRS (El Guindy & Trabelsi, Citation2020). Spain is considered to have weaker enforcement of IFRS; therefore, the benefits of IFRS adoption are less pronounced than the UK and Germany (Cordazzo, Citation2013; Gastón et al., Citation2010). Italy also has a weak enforcement environment (Bischof, Citation2009; Wieczynska, Citation2016).

This paper complements other literature reviews on the consequences of IFRS adoption (Brüggemann et al., Citation2013; De George et al., Citation2016; Houqe, Citation2018; Márquez-Ramos, Citation2011; Soderstrom & Sun, Citation2007). However, it is significantly different from these existing studies and provides new insights into the consequences of IFRS adoption in several ways. First, we bring an up-to-date analysis from 2010 to 2020 of IFRS consequences in Europe. Most of the existing reviews were done in the earlier days of IFRS adoption, where the benefits were not evident. For example, Soderstrom and Sun’s (Citation2007) studies cover only 2005, when IFRS was largely voluntary.

Second, we depart from existing studies by focusing on the enforcement environment of the country. By comparing and contrasting countries with differing enforcement levels, we highlight how enforcement affects the benefits of IFRS adoption. Our review also emphasises that it is not enough to adopt the standards. There must be an active effort to fully implement and integrate them into a country’s legal system (Silva et al., Citation2021).

Third, unlike prior studies that are limited to single or few benefits, our review of the consequences covers almost all benefits of IFRS adoption as claimed by the IFRS Foundation (IFRS Foundation, Citation2022). For example, Márquez-Ramos (Citation2011) focused on trade and foreign direct investment, while Soderstrom and Sun (Citation2007) reviewed only accounting quality. Our study, therefore, provides a more comprehensive review of the consequences of IFRS adoption in Europe.

Overall our paper provides up-to-date information on the consequences of IFRS adoption in Europe from the enforcement perspective. Based on the existing literature, we have made some suggestions for future research. This analysis is beneficial to researchers to understand what has been done and areas for potential research.

The structure of the paper is as follows. Section 2 presents the background of IFRS and its history. Section 3 discusses the methodology behind the research design of the paper. Section 4 contains the results, and Section 5 covers the findings and discussion of literature relevant to IFRS consequences. Section 6 concludes the paper with suggestions for future research.

2. Background to IFRS in Europe

In 1973 the International Accounting Standards Committee (IASC) was set up by professional accounting bodies in Australia, Canada, France, Germany, Japan, Mexico, Netherlands, UK/Ireland, and the US. The IASC adopted International Accounting Standards for international listings IFRS Foundation, Citation2021). This was because capital markets were becoming more international and necessitated a common set of international accounting standards (Whittington, Citation2005)

In 1989, a conceptual framework was issued by the IASC, the Framework for the Preparation and Presentation of Financial Statements IFRS Foundation, Citation2021). In 1990, the IASC issued a Statement of Intent Comparability of Financial Statements to reduce the number of alternative accounting standards (IASC, Citation1990). The IASC also issued its initial set of International Accounting Standards (IAS), with thirty-one standards.

The Standards Interpretations Committee (SIC) was formed in 1996. This committee produced interpretations of the standards issued IFRS Foundation, Citation2021). In 2000, the IASC produced a full range of accounting standards that were internationally agreed upon following a call from the G7.

The International Accounting Standards Board (IASB) was formed in 2000 following a restructuring of the IASC. This coincided with the formation of the IFRS Foundation. In 2001, the IASB adopted IASC Standards IFRS Foundation, Citation2021). The IASB aimed to reduce diversity in accounting standards and financial reporting worldwide. This strategy was operationalised through the International Financial Reporting Standards (Whittington, Citation2005).

Before the mandatory adoption of IAS in Europe, its adoption was already underway as countries such as Germany and Switzerland had permitted listed companies to adopt the standards instead of local GAAP (Whittington, Citation2005). A watershed moment in the history of IAS occurred in 2002 when a law introduced in Europe required listed firms to issue financial statements in compliance with IFRS (IFRS Foundation, Citation2021; Whittington, Citation2005). This was to increase comparability and enable sound economic decisions to be made by market participants (IASC Foundation, Constitution 2(a)).

One of the stated objectives of the law was to reduce the barriers to cross-border securities trading by making cross-border company accounts easier to compare (Regulation (EC) No. 1606/2002, para. 1). There was also the goal of integrating European and global capital markets (Armstrong et al., Citation2010). Harmonisation achieves this as the costs of foreign investors to understand a foreign company’s financial statements are decreased as the financial statements are issued in an accounting standard investors are familiar with (Barth et al., Citation1999).

In 2002, the IASB and the US Financial Accounting Standards Board (FASB) signed the ‘Norwalk Agreement. The objective of this agreement was to have better convergence between IFRS and US GAAP (IFRS Foundation, Citation2021). The following year IFRS 1 was issued by the IASB. In addition to this, there was a reform of existing IASs.

In 2004, the IASB issued its second standard, IFRS 2. IFRS 3–6 followed based on reforms of existing standards. In 2005, IFRS 7 was issued due to concerns about financial instruments (IFRS Foundation, Citation2021). This is one of the most significant accounting changes in recent decades (Cascino & Gassen, Citation2015). In 2006, convergence between US FASB and IASB was accelerated, and IFRS 8 was issued to reduce the gap between IFRS and US GAAP IFRS Foundation, Citation2021). The adoption of IFRS worldwide is one of the most significant accounting changes in recent decades (Cascino & Gassen, Citation2015).

During the financial crisis, the US FASB and IFRS coordinate a response in the shape of a Financial Crisis Advisory Group (ibid). In 2009, IFRS 9 was published along with IFRS for SMEs. G20 leaders voice their support for the IASB, strengthening the movement towards a global set of accounting standards. In 2011, there were three more standards issued. The IASB and FASB jointly issued converged requirements relating to fair value measurement, offsetting requirements, and presentation of OCI (IFRS Foundation, Citation2021)

In 2013, the IASB underwent a first full review, and the IFRS Foundation published progress charts to document the progress each jurisdiction is making. In 2014, IFRS 9 was revised, and IFRS 15 was issued jointly with the FASB. European Securities Markets Authority (ESMA) issued a Statement of Protocols in association with the IFRS Foundation. Also, the International Integrated Reporting Council (IIRC) and the IFRS Foundation co-author a declaration of common intent. The IFRS Foundation issued a mission statement in 2015 that IFRS standards should bring transparency, accountability and efficiency to financial markets. Also, there are numerous 10-year reviews published in 2015 regarding the use of IFRS in various jurisdictions.

3. Methodology

3.1. Boundaries of the review

This review and synthesis are limited to studies conducted in European countries. Given our objective of analysing the benefits of IFRS adoption, we further restrict our review to papers focusing on the consequences of IFRS. Given the vast amount of literature on the consequences of IFRS in Europe (Silva et al., Citation2021), it was difficult to narrow down the specific countries and topics. Therefore we focused on more occurring themes such as comparability, audit services, earnings management, and impact on accounting figures. At the outset, academic literature on the consequences of IFRS with an emphasis on Europe was reviewed. The academic literature was then analysed on major topics at the European level and then single-country basis.

3.2. Selection of articles

Consistent with prior studies (Ahmed et al., Citation2013; De George et al., Citation2016; Houqe, Citation2018), we source articles from prominent accounting journals based on Chartered Association of Business Schools (CABS) journal rankings. Following prior studies (Ahmed et al., Citation2013; Houqe, Citation2018; Tawiah & Boolaky, Citation2019), we searched for relevant articles using several combinations of keywords. These included IFRS, adoption, consequences, Europe, and enforcement. A staged review of the literature was then conducted, which involved an initial review of the abstract, introduction and conclusion.

Having deemed an article relevant, it was reviewed in more depth. When relevant articles on IFRS consequences were found, these articles were reviewed, and their bibliographies were scanned to identify literature relevant to IFRS adoption and its consequences in Europe (De George et al., Citation2016). Following this, the review was expanded to individual countries in CABS-ranked journals. The UK, Germany, Spain and Italy were chosen due to the varied and significant amount of individual studies based on IFRS adoption and its consequences in these countries.

It was difficult to identify much literature on the consequences of IFRS adoption in Spain from CABS-ranked journals, which is why articles from the Spanish Journal of Finance and Accounting were used. Also, if there were not enough academic articles from previously mentioned sources, Google Scholar was used to identify more relevant literature. However, the academic journal was cross-referenced with the Scimago Journal Ranking and CABS list to ensure it was not poorly ranked. Table presents the main findings of the papers included in this review (Musah et al., Citation2021, Citation2022, Citation2022).

Table 1. List of sample papers

4. Results

Table contains the details of the papers used in the review. This includes the authors’ names, sample countries, topics, journal and main findings. We observed that most of the papers are from multiple countries across Europe. The majority of papers were published between 2010 and 2016. Papers on the United Kingdom and Germany, considered strong enforcement countries, are published in top-tier journals like European Accounting Review, Contemporary Accounting Review and British Accounting Review.

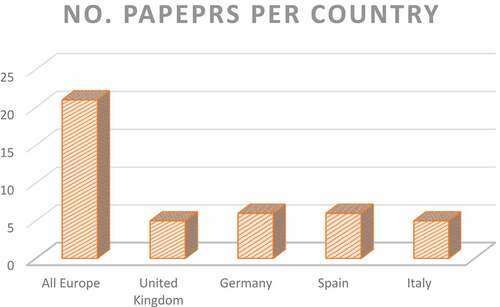

We present the number of papers per sample country in Figure . The bar chart in Figure shows that our review includes six papers each on Germany and Spain, followed by five each on the United Kingdom and Italy, signalling a balance collection between countries with varying enforcement environments. The papers on Europe as a single sample were over 20 and were dominated by the core EU countries. We observed that papers from multiple countries were published in high-ranking journals compared with single-country papers.

Figure 1. Number of papers per country.

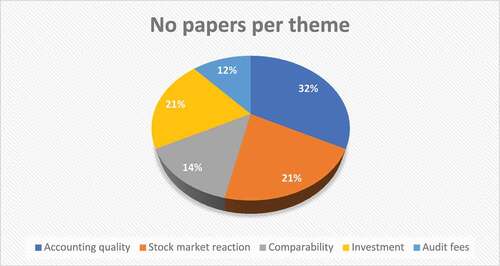

In Figure , we present the number of papers according to topics. As stated earlier, we group the papers under five main topics or themes: accounting quality, stock market reaction, comparability, investment and audit services. The pie chart of Figure indicates that 32% of the sample papers research the benefit of IFRS in improving accounting quality. This is unsurprising, given that the main objective of the IFRS is to improve accounting information and transparency. The next dominating themes were stock market reactions and investment, which are 21% of the total sample papers. Interestingly, the comparability theme appears to be less research; even though it is one of the key objectives of promoting the global adoption of IFRS.

Figure 2. Number of papers per theme.

In Table , we present the summary of the effect of the different themes among the four sample countries. We observed that adopting IFRS has increased accounting quality and comparability in United Kingdom and Germany, while it has mixed to no effect in Spain and Italy. On the contrary, we see that the benefit of IFRS on investment is similar for Germany and Italy. Similarly, the adoption of IFRS increases audit fees in the United Kingdom and Spain.

Table 2. Comparison among the sample countries on themes

5. Findings and discussion

5.1. Europe

This section analyses findings in studies concentrated on Europe. The consequences of IFRS adoption depend on a country’s enforcement and regulatory environment (Christensen et al., Citation2013). There are greater benefits seen in countries that adopt IFRS and have strong enforcement and regulatory systems than in countries that adopt IFRS and have weak enforcement and regulatory environments (Kim et al., Citation2012; Yip & Young, Citation2012).

5.2. Accounting quality

Under this theme, we consider studies on accounting information, earnings management, and transparency. Financial reporting quality is improved with IFRS adoption (Armstrong et al., Citation2010; Chen et al., Citation2010). However, Byard et al. (Citation2011) argued that a one size fits all approach in terms of IFRS adoption may not be the best option. If a firm’s domestic accounting standards are more informative, then adopting IFRS would lead to a negative impact as a firm would now be reporting less information, and analysts’ information would have less quality.

Ahmed et al. (Citation2013) found that income smoothing increased due to IFRS adoption. Callao and Jarne (Citation2010) found that the mandatory adoption of IFRS increased earnings management as discretionary accruals increased. IFRS enables opportunistic behaviour by management as more management discretion is needed due to increased subjective judgements. Before IFRS, more rigid accounting standards did not allow such subjective accounting choices. Therefore, there is a greater risk of earnings management (Callao & Jarne, Citation2010).

5.3. Stock market reaction

There is a negative market reaction to IFRS adoption if the company is situated in a country with poor enforcement and regulations. This illustrates that it is not enough for companies to adopt IFRS; the enforcement rules are taken into account by investors in determining whether this is a worthwhile exercise (Armstrong et al., Citation2010). Aharony et al. (Citation2010) also found that there was a positive market reaction to the adoption of IFRS.

Another benefit that can be seen in strong regulatory environments is that forecasting errors from analysts and forecast dispersion decrease due to the mandatory adoption of IFRS (Byard et al., Citation2011; Horton et al., Citation2013). This is evident in countries with accounting standards that were significantly different from IFRS and strong enforcement regimes. If a company is domiciled in a country with weak enforcement but also has significant differences in its domestic accounting standard compared to IFRS, there is a decrease in forecasting errors and forecast dispersion. These results lead to the conclusion that strong enforcement is needed for IFRS to be most beneficial (Byard et al., Citation2011).

Mandatory adoption of IFRS can impact a firm’s liquidity in capital markets (Christensen et al., Citation2013; Daske et al., Citation2013). Christensen et al. (Citation2013) found that IFRS impacted liquidity only when there were substantial positive changes in the reporting enforcement. If changes were not made and the regulatory environment was already strong, there was no effect on firms’ liquidity. Daske et al. (Citation2013) found that increased liquidity is evident for firms that adopt IFRS in line with a strategy to increase transparency. There was no increase in liquidity for firms that only adopted IFRS in name.

5.4. Comparability

One benefit of IFRS adoption is increased comparability, which is also a stated objective of the Financial Accounting Standards Board (FASB, Citation1980). Increased comparability between firms that have adopted IFRS results from an increase in the quality of information and accounting convergence (Ozkan et al., Citation2012; Wang, Citation2014; Yip & Young, Citation2012). If there is a strong enforcement environment, the benefits of IFRS adoption are more pronounced than in countries with weak environments (Yip & Young, Citation2012). However, Brüggemann et al. (Citation2013) found that mandatory IFRS adoption does not conclusively lead to increased comparability or transparency regarding financial statements. Moreover, Callao and Jarne (Citation2010) found that IFRS adoption leads to decreased earnings comparability and transparency.

5.5. Investment

IFRS adoption also increases foreign ownership in local companies (Florou & Pope, Citation2012; Yu & Wahid, Citation2014). The market reacts to mandatory IFRS adoption by increasing ownership in foreign mutual funds (DeFond et al., Citation2011; Yu & Wahid, Citation2014). This increase is more pronounced for companies in countries with strong implementation credibility of IFRS. In contrast, domestic ownership of domestic mutual funds does not increase with the mandatory implementation of IFRS. This is due to domestic investors already being familiar with local accounting standards and, therefore, no new information being published per IFRS (DeFond et al., Citation2011).

5.6. Audit fees

In strong regulatory environments, IFRS adoption leads to higher audit fees for firms adopting the standards (Khlif & Achek, Citation2016; Kim et al., Citation2012). This increase in audit fees for the adopters is driven by the increased complexity of evaluating the principle-based standards of IFRS. The IFRS-related premium is less pronounced in countries with strong regulatory environments (Kim et al., Citation2012) Khlif and Achek (Citation2016) found that firms are more likely to switch auditors following IFRS adoption.

5.7. Individual country analysis—The United Kingdom

For the purposes of this analysis, the UK is perceived to be a strong regulatory and enforcement environment (El Guindy & Trabelsi, Citation2020; Seetharaman et al., Citation2002; Wieczynska, Citation2016). Firms that are listed on the London stock exchange and the Alternative Investment Market (AIM) are mandated to issue their financial statements in accordance with IFRS (El Guindy & Trabelsi, Citation2020).

5.8. Accounting quality

Iatridis (Citation2012) explored whether there were differences in the IFRS transition process for hedgers and non-hedgers. The adoption of IFRS is positively and significantly related to the equity, earnings, leverage and liquidity of hedgers. Non-hedgers suffered a negative effect on these accounting figures. The firms that used hedging in advance of IFRS adoption had favourable benefits when IFRS was implemented due to accounting for some of the volatility resulting from fair value measurements in IFRS (Iatridis, Citation2012).

In the IFRS era, more firms use hedging instead of discretionary accruals to smooth income. Therefore, IFRS adoption decreases income smoothing as a method of earnings management. This is the opposite of what was found in a European context regarding IFRS adoption, as Ahmed et al. (Citation2013) observed that income smoothing increased, and Callao and Jarne (Citation2010) noted that earnings management increased. For firms that did not hedge, liquidity significantly decreased due to taking no effective measures to plan for the implementation of IFRS (Iatridis, Citation2012). Therefore, the consequences of IFRS adoption in the UK are similar to the European consequences as IFRS impacts liquidity (Christensen et al., Citation2013; Daske et al., Citation2013).

In another paper, Iatridis (Citation2012) found that firms which provided voluntary IFRS disclosures had the most significant positive impact on equity and earnings. Firms that did not voluntarily adopt IFRS negatively impacted leverage and liquidity. This is similar to what Daske et al. (Citation2013) and Christensen et al. (Citation2013) found in a European context in that IFRS adoption can impact a firm’s liquidity. Moreover, Brochet et al. (Citation2013) found that the above-average returns of insiders were reduced following the adoption of IFRS because privately held information was reduced. Therefore, the quality of financial reporting is improved as more information is published about a firm, enabling investors to make more informed decisions. Also, Iatridis (Citation2012) found a connection between voluntary IFRS disclosures before adoption and value relevance. This resulted from reduced information asymmetry, similar to Brochet et al. (Citation2013), as IFRS disclosures contain higher quality information and are more informative for investors in making decisions.

5.9. Comparability

Accounting standards in the UK were similar pre-2005 to IFRS. This means that benefits can be attributed to something other than changes in the quality of the core information being published. Brochet et al. (Citation2013) found that the introduction of IFRS decreased information asymmetry. Mandatory IFRS adoption increased the information set that was available to the public and therefore reduced the information set that was held privately. This helped investors determine a firm’s performance and valuation and increased comparability with IFRS-complying foreign firms (Brochet et al., Citation2013). Brochet et al. (Citation2013) “s research is similar to Wang’s (Citation2014) and Yip and Young’s (Citation2012), as the latter research papers also found that IFRS adoption results in increased comparability in Europe. This being said, it is in contrast with Brüggemann et al. (Citation2013)”s findings that IFRS does not result in increased comparability.

5.10. Audit fees

El Guindy and Trabelsi (Citation2020) investigated whether IFRS adoption had an impact on audit and non-audit fees for firms in the UK. It was found that first-time adopters of IFRS were being charged higher audit fees. This is similar to what Kim et al. (Citation2012) found in relation to higher audit fees as a consequence of IFRS for European companies. As well as this, audit and non-audit fees were significantly increased under both Big 4 and non-Big 4 firms. This increase was sustained over time (El Guindy & Trabelsi, Citation2020). The size of the audit firm charging the fee was irrelevant as Big 4 and non-Big 4 audit firms were charging the premium. This was the case in both audit and non-audit services. The premium is evident whether the audit tenure is a short or long-term due to the increase in audit effort and risk, which increases the audit liability (El Guindy & Trabelsi, Citation2020).

5.11. Germany

Germany has a strong regulatory and enforcement environment (Daske et al., Citation2013; Hitz et al., Citation2012; Wieczynska, Citation2016). Germany also has a two-tier enforcement system in place. This was established in 2005, post-EU mandatory adoption of IFRS. This system has a private body, the DPR, whose role is to investigate whether firms comply with IFRS. If errors are found, BaFin, the German securities regulator, is contacted and will issue a disclosure (Hitz et al., Citation2012). The largest stock exchange in Germany is the Frankfurt Stock Exchange, where all firms must comply with IFRS (IFRS Foundation, Citation2016a).

5.12. Accounting quality

Kim and Lin (Citation2019) examined accrual anomaly pre- and post-IFRS adoption. The authors find that the anomalies present in pre-IFRS adoption were no longer evident post-IFRS adoption. This meant that earnings management had decreased following IFRS adoption. The authors concluded that the decreased accrual anomaly was due to the enforcement improvements brought by IFRS adoption (Kim & Lin, Citation2019). Ernstberger et al. (Citation2012) examined the effective enforcement and regulation had on the consequences of IFRS adoption. New laws helped to increase the likelihood of firms publishing inaccurate financial statements being caught and reinforcing the sanctions brought on the companies and their auditors. Stronger financial reporting enforcement rules resulted in a decrease in earnings management. This was also accompanied by an increase in the quality of earnings information (Ernstberger et al., Citation2012). In contrast, Christensen et al. (Citation2015) found that voluntary IFRS adoption leads to less earnings management, but mandatory IFRS adoption did not have the same effect, and therefore, the authors of this paper could not conclude that IFRS adoption reduced earnings management. Similarly, Ahmed et al. (Citation2013) and Callao and Jarne (Citation2010) found that in European countries which were that earnings management did not decrease as a result of IFRS adoption.

Christensen et al. (Citation2015) explored whether IFRS adoption brought benefits to firms and compared voluntary adopters prior to 2005 with mandatory adopters in 2005 (Christensen et al., Citation2015). The authors found that benefits arising from IFRS adoption relating to accounting information quality were concentrated in firms that voluntarily adopted the standards prior to mandatory adoption. For these firms, there was less earnings management, increased value relevance, and decreased time to recognise losses.

However, for mandatory adopters of IFRS, there were no such benefits in the quality of accounting information, and therefore the authors conclude that mandatory IFRS adoption does not produce increased accounting quality in isolation (Christensen et al., Citation2015). The authors disagree with the literature stating that IFRS adoption in European countries results in an improved quality of financial reporting (Armstrong et al., Citation2010; Brochet et al., Citation2013).

5.13. Stock market reaction

Hitz et al. (Citation2012) found that investors reacted negatively to a firm being publicly named for non-compliance with IFRS by the German regulator. This evidence shows that the capital market punishes firms that do not comply with IFRS. Investors’ reaction depends on the degree of the accounting infringement, whether there is a threat of litigation and whether a firm intends to appeal the decision (Hitz et al., Citation2012). Furthermore, Ernstberger et al. (Citation2012) found an increase in the share price following IFRS adoption. These findings complement the findings of Armstrong et al. (Citation2010) and Aharony et al. (Citation2010) that investors value IFRS adoption.

5.14. Spain

For this analysis, Spain is considered a weak regulatory and enforcement environment (Gastón et al., Citation2010; Hope, Citation2003). Firms listed on the Spanish stock exchange are mandated to issue their financial statements per IFRS (IFRS Foundation, Citation2016b).

5.15. Accounting quality

Gastón et al. (Citation2010) referenced the regulatory environment of Spain in this study. These authors found that, for first-time adopters of IFRS, there was a significant impact on financial ratios and accounting figures for listed firms that previously used local accounting standards. If Spain had a stronger regulatory environment, the impact on these figures would have been more significant, as was the case in the UK with a reduction in privately held information (Brochet et al., Citation2013).

Another consequence of IFRS in Spain was that the standards had a negative impact on the relevance of financial information post-adoption. This is compared to the relevance of financial information for firms using local GAAP. With the introduction of IFRS, it was thought this would bring more relevant financial information. This was not the case; therefore, one of the objectives of IFRS implementation has not been met (Gastón et al., Citation2010). This is comparable to what was found in Germany by Christensen et al. (Citation2015) in that mandatory IFRS adoption did not account for an increase in the value relevance of the financial statements.

The increase in the quality of financial reporting information used by analysts for earnings forecasts is directly attributable to the transition from Spanish GAAP to IFRS. Analysts use financial statements as the basis for their predictions, and as there was an increase in the quality of their forecasts, this meant an increase in the quality of the financial statements (Garrido-Miralles & Sanabria-García, Citation2014).

It was found that the benefits arising from IFRS adoption in relation to a decrease in errors in analysts’ earnings forecasts and dispersion were mainly concentrated in firms that were audited by the Big 4. This is due to a firm with a Big 4 auditor being more incentivised to produce financial information that is more reliable and less open to interpretation (Garrido-Miralles & Sanabria-García, Citation2014). These findings contradict what Byard et al. (Citation2011) argued in a European context. They argued that there would be less information reported by companies, and analysts’ reports would decrease in quality. This is not the case in Spain, according to Garrido-Miralles and Sanabria-García (Citation2014).

5.16. Stock market reaction

Sanabria-García and Garrido-Miralles (Citation2020) concluded that IFRS adoption increased the volume of shares being traded for adopting companies. This implies that investors have increased investment in these companies due to an increase in comparability following IFRS adoption. This is due to lower investor costs in interpreting the financial statements, increased accuracy in the financial statements, and higher investor confidence (Sanabria-García & Garrido-Miralles, Citation2020). This complements the research of DeFond et al. (Citation2011), who found increased foreign ownership in local firms post-IFRS adoption. Ernstberger et al. (Citation2012) also found an increased demand for shares in IFRS-adopting companies in Germany.

5.17. Audit fees

De Fuentes and Sierra-Grau (Citation2015) built a model on audit and non-audit fees. The model ran predictions post-IFRS implementation to see if there was an IFRS premium. The authors found a constant rate of growth in the real audit fee. The authors also found that the audit fees charged in Spain were higher than in any other country (De Fuentes & Sierra-Grau, Citation2015). This complements the findings of Kim et al. (Citation2012), who found that the IFRS audit premium is highest in countries with weaker enforcement. IFRS premiums were evident due to the cost of an audit now being higher. The increase in audit fees accrued throughout the IFRS adoption process. The same premium was not seen in non-audit services. This was due to the introduction of regulatory restrictions on firms that jointly provide audit and non-audit services (De Fuentes & Sierra-Grau, Citation2015). Kim et al. (Citation2012) also found the IFRS premium in European countries. This was also evident in the UK (El Guindy & Trabelsi, Citation2020). This being said, El Guindy and Trabelsi (Citation2020) found evidence for an IFRS premium for both audit and non-audit services in a strong enforcement environment, whereas De Fuentes and Sierra-Grau (Citation2015) only found evidence for audit services in a weak enforcement environment.

5.18. Italy

Listed companies in Italy could voluntarily adopt IFRS from 2005. It was made mandatory in 2006. Italian firms are listed on the Borsa Italiana (Cordazzo, Citation2013). Italy is considered to have a weak enforcement environment (Bischof, Citation2009; Wieczynska, Citation2016).

5.19. Accounting quality

Cordazzo (Citation2013) investigated the differences between Italian GAAP and IFRS. There were performance benefits to be gained by Italian firms by switching to IFRS from Italian GAAP. There were significant positive impacts on net income and equity. In addition, adopting IFRS in Italy significantly improved the accounting systems in the country (Cordazzo, Citation2013). Cordazzo’s (Citation2013) research can be compared to that of Garrido-Miralles and Sanabria-García (Citation2014) in that both authors find significant differences between the local GAAP and IFRS.

Cordazzo and Rossi (Citation2020) found that IFRS resulted in intangible assets becoming less value relevant due to the transition from Italian GAAP. In addition, Palea (Citation2014) found that Italian GAAP-prepared separate financial statements were more value relevant than IFRS-prepared ones. This was due to IFRS consolidated statements containing all the information that a separate IFRS-prepared financial statement would have, therefore having no incremental value. This is similar to the effects of IFRS elsewhere, as Gastón et al. (Citation2010) found that IFRS made financial statements less value-relevant and Christensen et al. (Citation2015) observed that mandatory IFRS adoption did not account for an increase in the value relevance of the financial statements.

5.20. Comparability

Overall, Cascino and Gassen (Citation2015) found that mandatory IFRS adoption brings a marginal increase in the level of comparability for Italian firms when compared to cross-border companies. If there were a high compliance incentive for the adopting firm, there would be a significant increase in comparability. However, IFRS adoption makes firms less comparable to those that prepare their financial statements using Italian GAAP. These findings are similar to Callao and Jarne’s (Citation2010) that IFRS adoption leads to decreased earnings comparability.

5.21. Audit fees

Wieczynska (Citation2016) explored whether IFRS adoption affected a firm switching auditor. It was found that firms were more likely to migrate from local accounting firms to global accounting firms for auditing purposes. This is due to a perceived specialist knowledge in the area of IFRS. Similarly, Bassemir (Citation2018) and Iatridis (Citation2012) found that IFRS-adopting firms were more likely to be audited by a large audit firm in Germany and the UK. Also, Khlif and Achek (Citation2016) found that firms were more likely to switch auditors following IFRS adoption. It was found that firms in Italy were less likely to switch auditors than firms in Germany or the UK. This is another difference in the consequences of IFRS adoption between countries with strong enforcement and countries with enforcement (Wieczynska, Citation2016).

6. Conclusions and future research

This paper has analysed the consequences of IFRS adoption in Europe between 2010 and 2020, with particular attention to the enforcement environment of the country. The results of this analysis are that the main benefits of IFRS adoption were increased comparability (Wang, Citation2014; Yip & Young, Citation2012), a decrease in forecasting errors (Byard et al., Citation2011; Horton et al., Citation2013), a decrease in the cost of equity for adopting firms (Daske et al., Citation2013; Li, Citation2010), all of which were intended consequences (IFRS Foundation, Citation2022). There were also unintended consequences of IFRS adoption. These included an increase in earnings management (Ahmed et al., Citation2013; Callao & Jarne, Citation2010; Iatridis, Citation2012) and a decrease in the value relevance of accounting information (Christensen et al., Citation2015; Gastón et al., Citation2010). Depending on the strength of a country’s regulatory and enforcement environment, the consequences of IFRS adoption vary (Gastón et al., Citation2010; Wieczynska, Citation2016). The different enforcement environment means that not all countries have harnessed the full benefits of IFRS adoption (De Fuentes & Sierra-Grau, Citation2015; El Guindy & Trabelsi, Citation2020).

A limitation of this research is that only the consequences of IFRS adoption in Europe and the UK, Germany, Italy and Spain are analysed. Other European countries could have been analysed, but due to the volume of literature on IFRS adoption, it was impossible to examine more countries (Silva et al., Citation2021). Also, having mainly focused on CABS-ranked journals, relevant research in lesser-ranked journals might have been missed.

The implication for research is that countries that are using IFRS must realise that the strength of their enforcement environment plays a role in the benefits realised from IFRS (Christensen et al., Citation2013; Kim et al., Citation2012; Yip & Young, Citation2012). There are negative effects that can be realised if the enforcement environment is not strong enough. The findings indicate that three main areas of the consequences of IFRS adoption in Europe would benefit from future research.

First, researching the effects IFRS adoption has on audit fees in individual countries would contribute to existing literature. Kim et al. (Citation2012) explored European consequences of audit fees, but there was no research on audit fees based in Italy and Germany like in the UK (El Guindy & Trabelsi, Citation2020) and Spain(De Fuentes & Sierra-Grau, Citation2015).

Second, there is a lack of research on enforcing IFRS and its consequences (Silva et al., Citation2021). Therefore, having found that the level of enforcement determined the consequences of IFRS adoption (Gastón et al., Citation2010; Wieczynska, Citation2016), it is clear that more research is necessary on what impact enforcement has on accounting quality in European countries (Silva et al., Citation2021).

Third, much of the research on IFRS adoption consequences is based on large companies (Ahmed et al., Citation2013; El Guindy & Trabelsi, Citation2020; Wieczynska, Citation2016). There is a lack of research on the consequences of IFRS for SMEs (Gassen, Citation2017). Therefore, it is necessary to research this topic to the same extent as the consequences of large companies adopting IFRS.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Aharony, J., Barniv, R., & Falk, H. (2010). The impact of mandatory IFRS adoption on equity valuation of accounting numbers for security investors in the EU. European Accounting Review, 19(3), 535–19. https://doi.org/10.1080/09638180.2010.506285

- Ahmed, K., Chalmers, K., & Khlif, H. (2013). A meta-analysis of IFRS adoption effects. The International Journal of Accounting, 48(2), 173–217. https://doi.org/10.1016/j.intacc.2013.04.002

- Armstrong, C. S., Barth, M. E., Jagolinzer, A. D., & Riedl, E. J. (2010). Market Reaction to the Adoption of IFRS in Europe. The Accounting Review, 85(1), 31–61.

- Barth, M. E., Clinch, G., & Shibano, T. (1999). International accounting harmonisation and global equity markets. Journal of Accounting and Economics, 26(1), 201–235.

- Bassemir, M. (2018). Why do private firms adopt IFRS? Accounting and Business Research, 48(3), 237–263. https://doi.org/10.1080/00014788.2017.1357459

- Bischof, J. (2009). The effects of IFRS 7 adoption on bank disclosure in Europe. Accounting in Europe, 6(2), 167–194. https://doi.org/10.1080/17449480903171988

- Brochet, F., Jagolinzer, A. D., & Riedl, E. J. (2013). Mandatory IFRS adoption and financial statement comparability. Contemporary Accounting Research, 30(4), 1373–1400.

- Brüggemann, U., Hitz, J.-M., & Sellhorn, T. (2013). Intended and unintended consequences of mandatory IFRS adoption: A review of extant evidence and suggestions for future Research. European Accounting Review, 22(1), 1–37. https://doi.org/10.1080/09638180.2012.718487

- Byard, D., Li, Y., & Yu, Y. (2011). The effect of mandatory IFRS adoption on financial analysts. Information Environment. Journal of Accounting Research, 49(1), 69–96.

- Callao, S., & Jarne, J. I. (2010). Have IFRS affected earnings management in the European Union? Accounting in Europe, 7(2), 159–189. https://doi.org/10.1080/17449480.2010.511896

- Cascino, S., & Gassen, J. (2015). What drives the comparability effect of mandatory IFRS adoption? Review of Accounting Studies, 20(1), 242–282. https://doi.org/10.1007/s11142-014-9296-5

- Chen, H., Tang, Q., Jiang, Y., & Lin, Z. (2010). The role of international financial reporting standards in accounting quality: Evidence from the European Union. Journal of International Financial Management & Accounting, 21(3), 220–278. https://doi.org/10.1111/j.1467-646X.2010.01041.x

- Christensen, H. B., Hail, L., & Leuz, C. (2013). Mandatory IFRS reporting and changes in enforcement. Journal of Accounting and Economics, 56(2, Suppl. 1), 147–177.

- Christensen, H. B., Lee, E., Walker, M., & Zeng, C. (2015). Incentives or standards: What determines accounting quality changes around IFRS adoption? European Accounting Review, 24(1), 31–61. https://doi.org/10.1080/09638180.2015.1009144

- Cordazzo, M. (2013). The impact of IFRS on net income and equity: Evidence from Italian listed companies. Journal of Applied Accounting Research, 14(1), 54–73. https://doi.org/10.1108/09675421311282540

- Cordazzo, M., & Rossi, P. (2020). The influence of IFRS mandatory adoption on value relevance of intangible assets in Italy. Journal of Applied Accounting Research, 21(3), 415–436. https://doi.org/10.1108/JAAR-05-2018-0069

- Daske, H., Hail, L., Leuz, C., & Verdi, R. (2013). Adopting a Label: Heterogeneity in the economic consequences around IAS/IFRS adoptions. Journal of Accounting Research, 51(3), 495–547. https://doi.org/10.1111/1475-679X.12005

- DeFond, M., Hu, X., Hung, M., & Li, S. (2011). The impact of mandatory IFRS adoption on foreign mutual fund ownership: The role of comparability. Journal of Accounting and Economics, 51(3), 240–258. https://doi.org/10.1016/j.jacceco.2011.02.001

- de Fuentes, C., & Sierra-Grau, E. (2015). IFRS adoption and audit and non-audit fees: Empirical evidence from Spanish listed companies. Spanish Journal of Finance and Accounting/Revista Española de Financiación Y Contabilidad, 44(4), 387–426.

- De George, E. T., Li, X., & Shivakumar, L. (2016). A review of the IFRS adoption literature. Review of Accounting Studies, 21(3), 898–1004. https://doi.org/10.1007/s11142-016-9363-1

- DiFabio, C. (2018). Voluntary application of IFRS by unlisted companies: Evidence from the Italian context. International Journal of Disclosure and Governance, 15(2), 73–86. https://doi.org/10.1057/s41310-018-0037-z

- El Guindy, M. N., & Trabelsi, N. S. (2020). IFRS adoption/reporting and auditor fees: The conditional effect of audit firm size and tenure. International Journal of Accounting & Information Management, 28(4), 639–666. https://doi.org/10.1108/IJAIM-09-2019-0107

- Ernstberger, J., Stich, M., & Vogler, O. (2012). Economic consequences of accounting enforcement reforms: The case of Germany. European Accounting Review, 21(2), 217–251. https://doi.org/10.1080/09638180.2011.628096

- FASB. (1980). Concepts Statements. https://fasb.org/page/PageContent?pageId=/standards/concepts-statements.html

- Fitó, A., Gómez, F., & Moya, S. (2012). Choices in IFRS Adoption in Spain: Determinants and Consequences. Accounting in Europe, 9(1), 61–83. https://doi.org/10.1080/17449480.2012.664390

- Florou, A., & Pope, P. F. (2012). Mandatory IFRS adoption and institutional investment decisions. The Accounting Review, 87(6), 1993–2025. https://doi.org/10.2308/accr-50225

- Garrido-Miralles, P., & Sanabria-García, S. (2014). The impact of mandatory IFRS adoption on financial analysts’ earnings forecasts in Spain/El efecto de la aplicación obligatoria de las IFRS sobre los pronósticos de los analistas financieros en ESPAÑA. Revista Española de Financiación y Contabilidad, 43(2), 111–131. https://doi.org/10.1080/02102412.2014.911587

- Gassen, J. (2017). The effect of IFRS for SMEs on the financial reporting environment of private firms: An exploratory interview study. Accounting and Business Research, 47(5), 540–563. https://doi.org/10.1080/00014788.2017.1314105

- Gastón, S. C., García, C. F., Jarne, J. I. J., & Laínez Gadea, J. A. (2010). IFRS adoption in Spain and the United Kingdom: Effects on accounting numbers and relevance. Advances in Accounting, 26(2), 304–313. https://doi.org/10.1016/j.adiac.2010.08.003

- Hitz, J.-M., Ernstberger, J., & Stich, M. (2012). Enforcement of accounting standards in Europe: Capital-market-based evidence for the two-tier mechanism in Germany. European Accounting Review, 21(2), 253–281. https://doi.org/10.1080/09638180.2011.641727

- Hope, O. -K. (2003). Disclosure Practices, Enforcement of Accounting Standards, and Analysts’ Forecast Accuracy: An International Study. Journal of Accounting Research, 41(2), 235–272. https://doi.org/10.1111/1475-679X.00102

- Horton, J., Serafeim, G., & Serafeim, I. (2013). Does mandatory IFRS adoption improve the information environment?*. Contemporary Accounting Research, 30(1), 388–423. https://doi.org/10.1111/j.1911-3846.2012.01159.x

- Houqe, N. (2018). A review of the current debate on the determinants and consequences of mandatory IFRS adoption. International Journal of Accounting & Information Management, 26(3), 413–442. https://doi.org/10.1108/IJAIM-03-2017-0034

- IASC. (1990). Statement of Intent Comparability of Financial Statements. https://www.ifrs.org/content/dam/ifrs/about-us/our-history/1990-soi.pdf

- Iatridis, G. (2012). Hedging and earnings management in the light of IFRS implementation: Evidence from the UK stock market. The British Accounting Review, 44(1), 21–35. https://doi.org/10.1016/j.bar.2011.12.002

- IFRS Foundation. (2016a). Jurisdictional Profile: Germany. https://www.ifrs.org/content/dam/ifrs/publications/jurisdictions/pdf-profiles/germany-ifrs-profile.pdf

- IFRS Foundation. (2016b). Jurisdictional Profile: Spain.

- IFRS Foundation. (2021). IFRS Foundation Constitution (pp. 28).

- IFRS Foundation. (2022). IFRS - The use of IFRS® Standards around the world. https://www.ifrs.org/use-around-the-world/

- Khlif, H., & Achek, I. (2016). IFRS adoption and auditing: A review. Asian Review of Accounting, 24(3), 338–361. https://doi.org/10.1108/ARA-12-2014-0126

- Kim, J. H., & Lin, S. (2019). Accrual anomaly and mandatory adoption of IFRS: Evidence from Germany. Advances in Accounting, 47, 100445. https://doi.org/10.1016/j.adiac.2019.100445

- Kim, J.-B., Liu, X., & Zheng, L. (2012). The impact of mandatory IFRS adoption on audit fees: theory and evidence. The Accounting Review, 87(6), 2061–2094. https://doi.org/10.2308/accr-50223

- Li, S. (2010). Does mandatory adoption of international financial reporting standards in the European Union reduce the cost of equity capital? The Accounting Review, 85(2), 607–636. https://doi.org/10.2308/accr.2010.85.2.607

- Márquez-Ramos, L. (2011). European accounting harmonization: Consequences of IFRS adoption on trade in goods and foreign direct investments. Emerging Markets Finance and Trade, 47(sup4), 42–57. https://doi.org/10.2753/REE1540-496X4705S403

- Musah, M., Kong, Y., Mensah, I. A., Li, K., Vo, X. V., Bawuah, J., Agyemang, J. K., Antwi, S. K., & Donkor, M. (2021). Trade openness and CO2 emanations: A heterogeneous analysis on the developing eight (D8) countries. Environmental Science and Pollution Research, 28(32), 44200–44215. https://doi.org/10.1007/s11356-021-13816-7

- Musah, M., Owusu-Akomeah, M., Boateng, F., Iddris, F., Mensah, I. A., Antwi, S. K., & Agyemang, J. K. (2022). Long-run equilibrium relationship between energy consumption and CO2 emissions: A dynamic heterogeneous analysis on North Africa. Environmental Science and Pollution Research, 29(7), 10416–10433. https://doi.org/10.1007/s11356-021-16360-6

- Ozkan, N., Singer, Z., & You, H. (2012). Mandatory IFRS adoption and the contractual usefulness of accounting information in executive compensation. Journal of Accounting Research, 50(4), 1077–1107. https://doi.org/10.1111/j.1475-679X.2012.00453.x

- Palea, V. (2014). Are IFRS value-relevant for separate financial statements? Evidence from the Italian stock market. Journal of International Accounting, Auditing and Taxation, 23(1), 1–17. https://doi.org/10.1016/j.intaccaudtax.2014.02.002

- Sanabria-García, S., & Garrido-Miralles, P. (2020). Impact of IFRS on non-cross-listed Spanish companies: Financial analysts and volume of trade. European Research on Management and Business Economics, 26(2), 78–86. https://doi.org/10.1016/j.iedeen.2020.04.001

- Seetharaman, A., Gul, F. A., & Lynn, S. G. (2002). Litigation risk and audit fees: Evidence from UK firms cross-listed on US markets. Journal of Accounting and Economics, 33(1), 91–115. https://doi.org/10.1016/S0165-4101(01)00046-5

- Silva, A., Jorge, S., & Rodrigues, L. L. (2021). Enforcement and accounting quality in the context of IFRS: Is there a gap in the literature? International Journal of Accounting & Information Management, 29(3), 345–367. https://doi.org/10.1108/IJAIM-08-2020-0126

- Soderstrom, N. S., & Sun, K. J. (2007). IFRS adoption and accounting quality: A Review. European Accounting Review, 16(4), 675–702. https://doi.org/10.1080/09638180701706732

- Tawiah, V., & Boolaky, P. (2019). A review of literature on IFRS in Africa. Journal of Accounting & Organizational Change, 16(1), 47–70. https://doi.org/10.1108/JAOC-09-2018-0090

- Wang, C. (2014). Accounting standards harmonisation and financial statement comparability: Evidence from transnational information transfer. Journal of Accounting Research, 52(4), 955–992.

- Whittington, G. (2005). The adoption of international accounting standards in the European Union. European Accounting Review, 14(1), 127–153. https://doi.org/10.1080/0963818042000338022

- Wieczynska, M. (2016). The “Big” Consequences of IFRS: How and when does the adoption of IFRS benefit global accounting firms? The Accounting Review, 91(4), 1257–1283. https://doi.org/10.2308/accr-51340

- Yip, R. W. Y., & Young, D. (2012). Does mandatory IFRS adoption improve information comparability? The Accounting Review, 87(5), 1767–1789. https://doi.org/10.2308/accr-50192

- Yu, G., & Wahid, A. S. (2014). Accounting standards and international portfolio holdings. The Accounting Review, 89(5), 1895–1930. https://doi.org/10.2308/accr-50801