Abstract

This paper investigates the relative effect of re-enforced tax ethics education (RTEE), religious commitment and professional experience on ethical decision-making (EDM). Survey data from 356 tax accountants were analysed using the partial least square structural equation modelling technique. The study found that intra-religious commitment predicts EDM, but inter-personal religious commitment does not predict EDM. Further, all three examined variables concurrently influence EDM, but RTEE is the most influential EDM variable. The findings of this study should energise tax practice organisations to re-enforce tax ethics education among their officers and guide the assignment of officers to ethically sensitive tax engagements. The paper contributes to Kant’s theory of morality.

PUBLIC INTEREST STATEMENT

The Ghana statistical service’s survey of people’s experiences and views on corruption listed tax workspace among the top three most corrupt institutions in Ghana. This finding partly motivated this study, considering that the tax workspace is dominated by ethically educated professionals. This study found that membership in professional tax association provides a re-enforcement of ethics and leads to improvement in ethical decision-making. Gatekeepers in the field of taxation should encourage and motivate professionals in other disciplines to acquire and maintain membership in tax profession association. Relatedly, tax organizations should encourage programs that re-enforce tax ethics education among their employees. Further, the study found that ethical decision-making improves as tax officer accumulate more experience. The study recommends that experienced, and chartered tax professionals should be assigned to ethically sensitive engagements. Finally, the study found that individuals could manifest a form of godliness but not be inclined to act ethically;thus religious stereotyping in tax team composition decisions may produce undesirable efffects.

1. Introduction

There is a plethora of literature on the respective influences of religiosity (Goel & Misra, Citation2020; Tariq et al. (Citation2019), ethics education (Kakos, Citation2019; Parks-Leduc et al., Citation2021) and professional experience (Barrainkua & Espinosa-Pike, Citation2018) on ethical decision-making (EDM). There are, however, compelling reasons to study the concurrent and relative influence of these variables on EDM. The extant literature captured the influence of the variables (religiosity, work experience, and ethics education) on EDM in isolation. Including these variables concurrently in an EDM model is pertinent for understanding variations in ethical behaviour among highly religious, ethically educated, and experienced professionals. This study fetches this important perspective to the EDM literature. It explains why ethical scandals may persist in workspaces dominated by highly religiousFootnote1 and ethically exposed professionals.

There is also the case for revisiting the individual influence of religious variables on EDM. The findings in extant literature are inconsistent. One school of thought evinces a positive relationship between religious variables and ethical behaviour proxies (Fathallah et al., Citation2020; Sidani & Khalil, Citation2020; Nambukara-Gamage & Rahman, Citation2020; Tittle & Welch, Citation1983). Another taxonomy of studies reported “no/weak” influence (Agle & Van Buren, Citation1999; Shariff, Citation2015). Contemporary studies conceptualised religious variables as religious commitment, yet the results are still inconsistent. Goel and Misra (Citation2020) extracted two components of religious commitment—intrinsic and extrinsic—and found that only intrinsic religious commitment influence EDM. However, Tariq et al. (Citation2019) suggest that both intrinsic and extrinsic commitment positively predict EDM. With a unique sample of ethics education “haves”, this study contributes to the contemporary debate on which component of religious commitment influences EDM and to what extent.

Another reason for this study is to capture the relative effect of re-enforced ethics education (RTEE) on EDM. Existing literature focused on the EDM effect of ethics education and overly relied on samples comprising ethics education “haves” and ethics education “have-nots (Cloninger & Selvarajan, Citation2010; Kakos, Citation2019; Parks-Leduc et al., Citation2021; Remišová et al., Citation2019). Beyond positing contradicting results, the literature is constrained in explaining how much RTEE contributes to explaining variations in EDM among ethical education “haves”. This perspective is pertinent in guiding organisational policy on sustained and continuous ethics education. The study on EDM is pertinent in an era where emerging discipline-specific professional bodies continue to question the sufficiency of ethics education offered by generalised professional bodies. In Ghana, for instance, the Chartered Institute of Taxation-Ghana (CITG) argues that accounting professionals who work in the tax workspace should further obtain CITG membership as this provides re-enforcement of their tax ethics. The claim that re-enforced tax ethics education (RTEE) offers an additional layer towards EDM is supported by theories of re-enforced learning (Croker et al., Citation2015). However, it is primarily not empirically tested within the given context.

Finally, this study examines the relative effect of professional experience on EDM. Literature on the influence of professional experience on EDM is scarce. The extant literature links work experience to EDM (Arlow, Citation1991; Barrainkua & Espinosa-Pike, Citation2018; Wittmer, Citation2019). In accounting/taxation practice, professional experience is a critical factor in work team composition and promotion. Thus, context-specific evidence on the relationship between professional experience and EDM is pertinent.

This paper investigates the relative and concurrent influences of religious commitment, RTEE, and professional experience on EDM. Specific research objectives (RO) are to:

RO1: re-examine the influence of two components of religious commitment (i.e., intra-religious and inter-personal religious commitment) on the EDM of tax accountants in Ghana.

RO2: establish the relative effect of religious commitment, RTEE, and professional experience on the EDM of tax accountants.

The study context and sample reflect specific contexts in Africa and Asia where workspaces dominated by highly religious persons (Ghana Statistical Service, Citation2021; Goel & Misra, Citation2020) continue to record tax ethics-related scandals (Addo, Citation2021). Furthermore, the study sample comprised tax accountants, a lowly represented perspective in accounting EDM literature. The study also draws and contributes to the Kantian theory of morality by establishing intra-religious commitment, RTEE and professional experience as factors that individually and collectively influence individuals’ scheme of interpretation and imbibement of the moral rules.

The remainder of the paper is structured as follows: a review of the relevant theoretical and empirical literature, the study methodology, results and a discussion of the finding and conclusion.

2. Literature review

2.1. Concept definition and theoretical review

2.1.1. EDM

Rest’s (Citation1986) conceptualised EDM as a cognitive process through which individuals imbibe ethics in their decision-making. According to Rest (Citation1986), the cognitive process comprises four independent stages: ethical issue recognition, ethical judgment, ethical intention, and actual ethical behaviour. At the ethical issue recognition stage, the decision-maker constructs ethical reality and evaluates the importance of ethical dimensions in a given situation (Lincoln & Holmes, Citation2008). In the second stage, the decision-maker applies his/her cognitive valuation of rules, principles, or norms to determine the rightness or otherwise of an intended decision. The ethical intention stage involves the willingness and mental fortitude of the decision-maker to take a purported “right” course of decision amid conflicting influences, other convenient alternatives and in the presence of external stress. The fourth stage involves unambiguous and absolute enforcement of the actual decision.

Rest (Citation1979) contends that the four stages are relatively distinct and that progress in one stage does not imply progress in the others. Musbah et al. (Citation2016) agree that the ethical issue recognition stage and the ethical intention stage are independent but contend that the ethical judgment stage predicts the ethical intention stage. Following prior studies in business (Hirth-Goebel & Weißenberger, Citation2019; Jaijairam, Citation2017; Kashif et al., Citation2017; Valentine & Godkin, Citation2019), this current study conceptualises EDM to comprise ethical issue recognition and ethical intention.

2.1.2. Kant’s theory of morality

Kantian theory of morality (Sullivan, Citation1989) provides a rich theoretical lens for understanding the influences of religious commitment, RTEE, and professional experience on EDM. We draw on Kant’s postulations on the interplay among moral rules, freedom, and autonomy. Kant argues that institutions/logics of life (i.e., religion, ethical norms of professional bodies) could be a source of moral rules that provide a moral reference for individuals (Reath, Citation2020; Wood, Citation2020). Although moral rules provide a frame of morality, individuals’ moral actions are influenced by their obligation to interpret the moral rules (autonomy) and freewill imbibement (freedom) of the moral rules (Sullivan, Citation1989).

Following Kantian’s theory of morality, this study argues that religious commitments, RTEE, and professional influence may provide a source of moral rules. However, their depth and direction of influence largely depend on how well each variable influences individuals’ interpretation and imbibements of the espoused moral rules. For instance, a low level of imbibement of a moral rule will predict a low influence on Rest’s (Citation1986) EDM scale, and extensive reflection on the moral rules may predict EDM at higher stages on the EDM scale.

2.2. Conceptual framework

In line with Kantian’s theory of morality and Rest’s EMD framework, the study holds that religious commitment, professional membership, and experience are institutional logics with unique moral rules. The study also postulates that individual decision-makers are autonomously responsible for interpreting moral rules offered by these three institutional logics. The results of these autonomous interpretations could either produce an intrinsic rational interest to act ethically or yield a mere extrinsic manifestation of moral rules. Further, it is postulated that an individual’s depth intrinsic imbibement of the moral rules predicts EDM; but the mere extrinsic manifestation of the moral rules will not predict EDM. Figure presents the summary of theoretical postulations, as inspired by Kantian’s theory of morality.

Figure 1. Conceptual framework.

Based on this conceptual framework, a positive association between the variables of interest (religious commitment, professional membership, and professional experience) should be interpreted as a high level of influence of the respective variables on the individuals’ scheme of interpretation and imbibement of the moral rules espoused by those institutions.

2.3. Empirical review and development of hypothesis

The literature has not captured the simultaneous and relative influence of the three variables (religious commitment, RTEE, and professional experience) on EDM. The literature, however, captures the relationships in isolation.

A taxonomy of studies linked religious disposition/affiliations and ethical behaviour proxies and reported inconsistent results (Agle & Van Buren, Citation1999; Fathallah et al., Citation2020; Shariff, Citation2015). Shariff (Citation2015) found that religion does not influence pro-social behaviour, while Fathallah et al. (Citation2020) concluded that religious affiliation influences ethical behaviour proxies. Agle and Van Buren (Citation1999) found a weak relationship between Christian religious affiliation and pro-social behaviour. Sulaiman et al. (Citation2021) also sought to understand how Islamic religiosity influences EDM. The study found that only conscience mediates the relationship between Islamic religiosity and EDM. Another taxonomy of studies conceptualised religious variables in greater depth as religiosity (Alteer et al., et al., Citation2013), religious commitment or spirituality (Nambukara-Gamage & Rahman, Citation2020). Nambukara-Gamage and Rahman (Citation2020) and Longenecker et al. (Citation2004) found that religious variable positively predicts ethical behaviour. Goel and Misra (Citation2020) and Tariq et al. (Citation2019) examined the relationship between two perspectives of religious commitment and EDM. While Goel and Misra (Citation2020) found that only intra-personal religious commitment (a person’s metaphysical belief) positively and significantly influences attitude towards business ethics, Tariq et al. (Citation2019) disagree. Tariq et al. (Citation2019) found that both intra- and interpersonal religious commitment positively influence EDM.

To contribute to this emerging phase of literature, this study tests the following hypotheses:

H1a. There is a positive relationship between inter-personal religious commitment and EDM

H1b. There is a positive relationship between intra-religious commitment and EDM.

On the influence of ethics education on EDM, Kakos (Citation2019) argues that ethics cannot be taught and does not influence ethical behaviour. Other studies provide evidence to the contrary (Cloninger & Selvarajan, Citation2010; Remišová et al., Citation2019; Winston, Citation2007; Yoder & Denhardt, Citation2019). The studies found varying degrees of relationship between ethics education and ethical behaviour proxies. While some researchers (Remišová et al., Citation2019) hold that ethics education holds a pervasive influence on ethical behaviour, others (Cloninger & Selvarajan, Citation2010; Winston, Citation2007) contend that the level of influence does not transcend beyond Rest’s (Citation1986) first stage of EDM. Although theories of re-enforced learning suggest that re-enforced ethics education improves ethical behaviour, there is only a handful from the empirical perspectives. Balotsky (Citation2012) found that re-enforced ethics education led to an improved ethical outlook in sampled MBA students. Zegwaard and Campbell (Citation2014) attribute improved ethical development to re-enforced ethical learning from the graduate ethics curriculum.

Extant literature reports a conflicting relationship between work experience and EDM (or its proxies). Fang et al., (Citation2018) reported a positive relationship between work experience and EDM. This relationship is supported by Phatshwane (Citation2013), who found that managers with higher work experience are more ethical than managers with fewer years of work experience. Jain (Citation2020) likewise confirmed a positive relationship between work experience and ethical attitude among businesspersons. The positive association between work experience and EDM aligns with Kohlberg’s (Citation1969) theory of moral development. Arlow (Citation1991) reported a negative relationship between work and pro-social behaviour, suggesting that as individuals spend more time on a role, they are likely to “normalise” routine ethical issues that confront them.

From the review, the relationship between work experience and EDM is not definitive among business groups in general. Further, the specific influence of professional experience (as opposed to general work experience) is sparse in the literature.

To advance a comprehensive understanding of the collective relationship between religious commitment, RTEE, professional experience and EDM, the following hypotheses are tested:

H2a. Religious commitment, RTEE, and professional experience collectively predict ethical issue recognition stage EDM.

H2a. Religious commitment, RTEE, and professional experience collectively predict ethical intention stage EDM.

3. Methodology

3.1. Research design, sample, and data

This study adopts a quantitative design and a cross-sectional survey method. A sample of 450 tax accountants were contacted for the study. Of the 450 contacted, 356 responded to the survey instrument, yielding a response rate of 79.11%. According to J.F. Hair et al. (Citation2017a), the sample size should be at least ten times higher than the number of indicators of the construct with the highest number of indicators in the model. In this study, the intrapersonal religious commitment construct has the highest indicators (6). Following J.F. Hair et al. (Citation2017a), the study’s sample of 356 exceeds the minimum sample size of 60.

Self-administered questionnaires were used for data collection. The initial questionnaire was given to three tax accountants for review and comments, and sixty-three professional accounting students participated in a pilot study. The outcome of the pilot study informed the further revision of the data collection instrument. The instrument has three sections. The first section collected background information (i.e., age, experience, level of education, religion and affiliation, and professional status). The second section had a vignette that captured the ethical dilemmas of two fictional tax accountants. The respondents were requested to read and respond to statements from the vignettes. The third section collected data on religious commitment based on the adapted Worthington et al.’s (Citation2003) RC-10 items. The outcome of the pilot study informed the adaptations (appendix 1).

3.2. Measurement of variables

EDM and religious commitment are latent variables, with observable variables measured on a 7-point Likert scale, with 1 being strongly disagreed and 7 strongly agree. RTEE is a dummy variable, and professional experience is a continuous variable.

3.2.1. EDM

EDM is conceptualised as ethical issue recognition and ethical intention. The questionnaire has four ethical vignettes, which captured four ethical dilemmas of two fictional tax accountants (appendix 2). The vignettes are self-constructed, but items for measuring ethical issue identification and ethical intention were adapted from Musbah et al. (Citation2016). For each of the four vignettes, the respondents were expected to react to statements on a 7-point Likert scale to measure the EDM proxies. To measure ethical issue recognition, the respondents reacted to a statement, “I consider the ethical issue(s) in this scenario as important”. The respondent was requested to respond to a statement about whether he/she would take the same decision if he/she were the fictional tax Officer in each given vignette to measure ethical intention.

3.2.2. Re-enforced tax ethics education

The object here is to categorise respondents as having re-enforced tax ethics education through professional membership in taxation or not having such re-enforced tax ethics education. The respondents were asked to indicate whether they are qualified tax accountants within the meaning of the Chartered Institute of Taxation Act, 2016 (Act 916). For analysis purposes, respondents with RTEE status are coded as “1”, and those who do not have RTEE status as 0.

3.2.3. Professional experience

Professional experience is a continuous variable measured as the number of years the respondent has accumulated as a professional accountant. The data was collected in continuous form, but responses were ranged every five years for sample characteristics description purposes.

3.2.4. Religious commitment

Two perspectives of religious commitment were measured: intra-religious commitment and inter-personal religious commitment. The reflective indicators for measuring each construct were adapted from Worthington et al. (Citation2003). The original instrument of Worthington et al. (Citation2003) comprised ten items: six items for intra-personal religious commitment and four items for inter-personal religious commitment. The adaptations (appendix 1) were informed by the outcome of the pilot study.

3.3. Empirical estimation strategy

A structural equation model (SEM) was used for data analysis. SEM provides a platform for using latent (observable) indicators to measure an unobservable construct (Nitzl, Citation2016). Again, SEM comes in handy for studies that study relationship-direct, mediation and moderation systems in a single model (Hair et al., Citation2012). The study used partial least squares structural equation model (PLS-SEM) instead of an alternative, covariance-based SEM. PLS-SEM is preferred for this study because PLS-SEM maximises explained variance of the endogenous latent variables (Hair et al., Citation2012).

4. Empirical analysis

4.1. Sample characteristics

The demographic composition of this study’s sample follows trends observed in the accounting profession and the study’s geographical space. The study sample comprises 65% males and 35% females, which holds a semblance of the gender composition of the accounting profession in Ghana. The sample comprises highly religious persons, with almost every participant expressing affiliation to a religious group. The majority (66%) are affiliated with Christianity, and 26% expressly affiliate with the Islamic religion (26%). The sample comprises highly educated tax accountants; 94% of the sample hold at least a university degree, and the remaining 6% hold a tertiary diploma. This is expected because this study sampled only professional accountants, who in most cases have tertiary academic qualification. Other descriptive statistics of the sample are contained in Table .

Table 1. Sample characteristics

Most respondents hold a professional qualification in taxation, indicating that they have achieved a reinforced tax ethics education associated with membership in the tax profession. The remaining 29%, although qualified accountants, have not achieved RTEE associated with membership in the tax profession.

4.2. Descriptive characteristics of variables of interest

The coefficient of variation for all the indicators and all variables falls below Papatsouma et al.’s (Citation2019) maximum threshold of 3, indicating normally distributed data. Table provides detailed descriptive characteristics of the variables of interest.

Table 2. Descriptive of latent variables of interest

The indicators for the proxies of EDM (EDM.EIR, EDM.EInt) have a score above the median score of 4. The sample recorded a lower score for ethical intention than the score for ethical issue recognition. This is primary evidence that the sample exhibit some attrition on the EDM scale.

4.3. Diagnostics of indicators

We used the indicator loading to check indicator reliability, the composite reliability (CR) statistics to confirm internal consistency, and the average variance extracted (AVE) to test convergent validity. The variance inflation factor (VIF) was used to confirm the non-existence of collinearity. We also tested for discriminant validity using the Fornell-Larcker criterion and the Heterotrait-Monotrait Ratio (HTMT).

4.3.1. Indicator reliability, internal consistency, and convergent validity

The indicator loadings of the latent variables are compared with a threshold value of 0.50 to confirm indicator reliability. Indicators are deemed reliable when loading exceeds the minimum threshold (Hair et al., Citation2014). To conclude on internal consistency, the constructs should have composite reliability (CR) of at least 0.7 (Hair et al., Citation2014; Straub, Citation1989). To show convergent validity for a construct, Fornell and Larcker (Citation1981) suggested an “extracted minimum average variance (AVE) of 0.5”. An AVE value of less than 0.50 means that more volatility exists, on average, in the products than the variance defined by the construct. The results for these three diagnostics are presented in Table .

Table 3. Indicator reliability, internal consistency, and convergent validity

The indicators for the constructs are reliable (i.e., indicators for the latent variables achieved factor loadings higher than the minimum threshold of 0.50). CR of all the constructs is higher than the minimum threshold of 0.70, indicative of internal consistency. The AVE values are greater than the 0.50 threshold for all constructs. Thus, it is safe to conclude that the model achieves convergent validity.

4.3.2. Discriminant validity

The Fornell-Larcker criterion is a technique for assessing discriminant validity (Hair et al., Citation2016). According to Fornell and Larcker (Citation1981), the square roots of the AVE of each construct should be higher than the correlations of that construct with all other constructs to ensure a good discriminant validity outcome. Based on the Fornell-Larcker criterion, the condition for discriminant validity has been adhered to for all the constructs. The figures in bold are larger than other correlation values among the latent variables (when glanced at vertically and horizontally) in Table .

Table 4. Discriminant validity- Fornell-Larcker criterion

The HTMT provides a further test of discriminant validity. According to Teo et al. (Citation2008), an HTMT value lower than 0.90 for a paired construct connotes discriminant validity for the paid construct. Table provides the HTMT results for the two models.

Table 5. Discriminant validity- HTMT criterion

4.3.3. Collinearity

The final set of diagnostics was a collinearity test. Variance inflation factor (VIF) was used to test for collinearity. As a rule of thumb, VIF below 6 suggests that the model’s paired variables are not collinear (Hair et al., Citation2021). Table provides the respective test results for the three models in this study.

Table 6. Variance Inflation Factor

The VIF for all the modelled relationships is below the maximum threshold of 5, confirming that the model is not affected by collinearity issues.

4.4. PLS-SEM results

PLS-SEM results for the study are presented in Table .

Table 7. Influences of religious commitment, RTEE and ProfExp on EDM

The results in Table show the relationships for study objective 1 (RO1) and study objective (RO2) respectively.

The path diagram for the two respective study objectives is presented in Figures below.

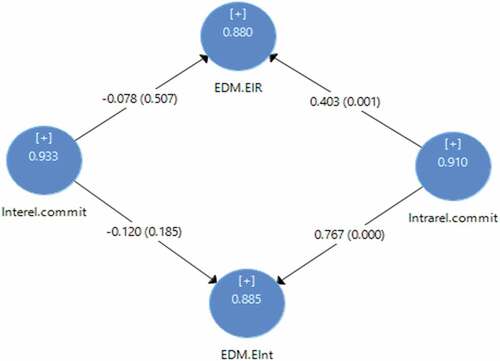

Figure 2. Religious commitment EDM.

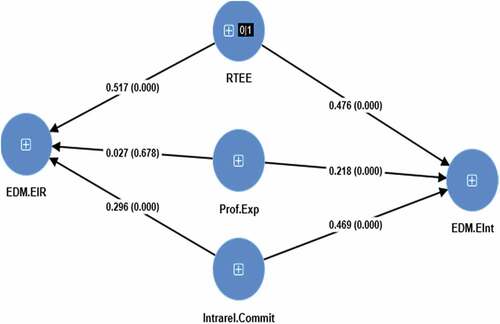

Figure 3. Intrarel.Commit, RTEE, ProfExp and EDM.

The hypotheses for the study are tested at a 95% confidence level. The threshold for the acceptance of the hypothesis is a p-value of 0.05. The hypothesis is rejected when the p-value exceeds the critical value of 0.05. The results of the hypothesis testing are produced in Table .

Table 8. Hypothesis

4.5. Discussion of findings

4.5.1. Does religious commitment predicts EDM?

The study’s first objective (RO1) is to re-examine religious commitment’s influence on the EDM of Ghana’s tax accountants. The results show that intra-religious commitment predicts EDM at both ethical issue recognition and ethical intention stages of EDM. Inter-personal religious commitment does not predict ethical EDM. From Kant’s theory perspective, the results mean that intrinsic manifestation of one’s religious belief (i.e., participation in religious activities, sharing of religious doctrines, financial commitments for religious purposes, etc.) have an insignificant level of influence on the individual’s scheme of interpretation and imbibement of moral rules espoused by religion. On the other hand, individuals’ level of metaphysical imbibement of religious norms positively influences their level of interpretation and propensity to act ethically.

Empirically, the findings of this study on religious commitment support Goel and Misra’s (Citation2020) finding that in the context of ethical behaviour, intra-religious commitment matters, not inter-personal religious commitment. The study’s finding does not support Tariq et al.’s (Citation2019) finding, with holds that both intra-religious and interpersonal religious commitment positively influence EDM.

Specifically, this paper provides that the extrinsic manifestation of shared religious values is “sand” in the wheels of EDM, while intra-religious commitment is “grease” in the wheels of EDM.

4.5.2. Relative effect of religious commitment, RTEE and professional experience on EDM

The study’s second objective (RO2) is to establish the relative effect of religious commitment, RTEE and professional experience on EDM. The findings are that only intra-religious commitment and RTEE influence EDM at the ethical issue recognition stage of EDM. At the ethical intention stage, however, all three examined variables influence EDM. RTEE has the most significant influence on EDM, followed by intra-religious commitment. Professional experience holds the slightest influence on EDM.

From Kantian’s theoretical perspective, the positive and significant relationship between the three variables of influence and EDM connotes that the variables do not merely serve as sources of “moral rules”. Beyond serving as a source of moral rules, the variables (i.e., RTEE, intra-religious commitment, professional experience) influence individual members’ construction of the meaning of “moral rules” and the imbibement of moral choices. For instance, the positive and significant association between RTEE status and EDM proxies suggests that RTEE that comes with membership in a tax professional body (i.e., CITG) influences EDM. In other words, professional qualification in tax is essential because it perhaps aligns the epistemological perspectives of the members towards EDM.

The findings of this paper support the argument for tax accountants to strive for a professional qualification in taxation, irrespective of whether they belong to other professions. This study does not support Goel and Misra (Citation2020) that there is no significant relationship between professional status and attitude towards ethics. Sample characteristic differences could account for the contrasting results of this study and Goel and Misra’s (Citation2020) study.

The paper finds that professional experience does not predict EDM at the ethical issue recognition stage but predicts EDM at the ethical intention stage of EDM. The “no relationship” finding between professional experience and EDM’s ethical issue recognition stage implies that experience is not an ethical sensitising device. In other words, individuals’ level of ethical sensitivity neither improves nor deteriorates with their experience level. It is pertinent to note that professional experience is an EDM influential variable, considering that the relationship between professional experience and ethical intention is significant and a relative measure of EDM. The paper confirms the findings of Jain (Citation2020), Fang and Foucaut (Citation2018), and Phatshwane (Citation2013) but is inconsistent with the findings of Arlow (Citation1991). In summary, this paper holds that more experienced professionals will likely exhibit improved EDM than new and inexperienced professionals.

5. Conclusion and limitations

This paper investigated the relative influences of religious commitment, re-enforced tax ethics education (RTEE), and professional experience on EDM. Tax accountants were sampled, and PLS-SEM was utilised to analyse the data. The study found that RTEE, intra-religious commitment and professional experience individually and collectively influence EDM.

This paper contributes to Kantian’s theory of morality on two fronts. First, the study affirms Kantian’s proposition that the rational intrinsic interest explains an individual’s ethical behaviour. This study supports the Kantian postulation that intrinsic religious commitment is grease in the wheels of EDM, and the extrinsic manifestation of religious values is sand in the wheels of EDM. Secondly, the study proved that membership in a professional body does not only provide a source of moral rules to members. Specifically, the study evinces that such associations provide an additional layer towards EDM.

Regarding policy implications, the study’s results will energise tax professional bodies to insist on tax-specific professional qualifications for tax officers who handle ethics-sensitive portfolios. Again, gatekeepers in the tax workspace should strengthen protocols for admission and maintenance of membership as a tax practitioner. Policymakers in tax organisations should champion programs that re-enforce tax ethics among officers. Furthermore, tax practice firms should prioritise professional experience when assigning their officers to ethically sensitive tax engagements. Finally, policymakers should look beyond extrinsic manifestations of religious values when leveraging religiosity to enhance ethicality in organisations. Religious stereotyping, where “loud” religious manifestations are wrongly equated to ethicality has been disproven by this study. The finding of this study suggests the possibility of people manifesting godliness but not being committed to ethical behaviour.

The focus on tax accountants can be gleaned as a limitation of the study. The tax workspace is multidisciplinary, and the need to extend tax ethics studies to cover other professionals cannot be overemphasised.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Holy Kwabla Kportorgbi

Holy Kwabla Kportorgbi is a lecturer at the department of Accounting and Finance of Ghana Institute of Management and Public Administration (GIMPA). He is also a PhD candidate at University of Ghana Business School. His PhD thesis in on ethical decision-making. His current research interest is in the areas of tax ethics, tax compliance and tax policy, and financial reporting.

Teddy Ossei Kwakye

Teddy Ossei Kwakye Dr is a senior lecturer at the Department of Accounting at the University of Ghana Business School. Teddy’s research focuses on addressing strategic management accounting, corporate governance, financial and socio-environmental reporting, and ethics.

Francis Aboagye-Otchere

Francis Aboagye-Otchere Dr is a senior lecturer at the Department of Accounting at the University of Ghana Business School. His research areas are corporate governance, corporate social responsibility, environmental accounting, and ethics. He has extensive experience in university level teaching, executive and adult training, organizational and financial restructuring, design, redesign and improvement of business processes.

Notes

1. The study context is described as highly religious as 95% of the study context’s population profess affiliation to one of three dominant religious groups, namely Christianity, Islam, and Traditional African religions (Ghana Statistical Service, Citation2021)

References

- Addo, A. (2021). Controlling petty corruption in public administrations of developing countries through digitalisation: An opportunity theory informed study of Ghana customs. The Information Society, 37(2), 99–20. https://doi.org/10.1080/01972243.2020.1870182

- Agle, B. R., & Van Buren, H. J. (1999). God and mammon: The modern relationship. Business Ethics Quarterly, 9(4), 563–582. https://doi.org/10.2307/3857935

- Alteer, A. M, Yahya, S.B, Haron, M.H. (2013). The Mediating Impact of Ethical Orientation on the Religiosity and Undergraduate Auditing Student’ Ethical Sensitivity Relationship. International Journal of Finance and Accounting, 2(8), 472–477.

- Arlow, P. (1991). Personal characteristics in college students’ evaluations of business ethics and corporate social responsibility. Journal of Business Ethics, 10(1), 63–69. https://doi.org/10.1007/BF00383694

- Balotsky, E. R. (2012). Just how much does business ethics education influence practitioner attitudes? An empirical investigation of a multi-level ethical learning model. Journal of Business Ethics Education, 9, 101–128. https://doi.org/10.5840/jbee201296

- Barrainkua, I., & Espinosa-Pike, M. (2018). The influence of auditors’ professionalism on ethical judgement: Differences among practitioners and postgraduate students. Revista de Contabilidad, 21(2), 176–187. https://doi.org/10.1016/j.rcsar.2017.07.001

- Cloninger, P. A., & Selvarajan, T. T. (2010). Can ethics education improve ethical judgment? An empirical study. SAM Advanced Management Journal, 75(4), 4. https://www.proquest.com/openview/37aa45faa4d7f1be6affb12a433648e3/1?pq-origsite=gscholar&cbl=40946

- Croker, A., Fisher, K., & Smith, T. (2015). When students from different professions are co-located: The importance of interprofessional rapport for learning to work together. Journal of Interprofessional Care, 29(1), 41–48. https://doi.org/10.3109/13561820.2014.937481

- Fang, J., Jin, B, Slavin, N.S. (2018). Ethics - when the East Meets the West. Journal of Leadership, Accountability & Ethics, 15(2 http://digitalcommons.www.na-businesspress.com/JLAE/JLAE15-2/FangJ_15_2.pdf).

- Fathallah, R., Sidani, Y., & Khalil, S. (2020). How religion shapes family business ethical behaviors: An institutional logics perspective. Journal of Business Ethics, 163(4), 647–659. https://doi.org/10.1007/s10551-019-04383-6

- Fornell, C., & Larcker, D. F. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Ghana Statistical Service. (2021). 2021 population & housing census: National analytical report. Ghana Statistics Service.

- Goel, P., & Misra, R. (2020). It’s not inter-religiosity but intra-religiosity that really matters in attitude towards business ethics: Evidence from India. International Journal of Ethics and Systems, 36(2), 167–184. https://doi.org/10.1108/IJOES-10-2018-0153

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2017a). A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). Sage.

- Hair, J. F., Jr, Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2021). A primer on partial least squares structural equation modeling (PLS-SEM). Sage publications.

- Hair, J. F., Hult, G. T. M., Ringle, C. M., Sarstedt, M., & Thiele, K. O. (2016). Mirror, mirror on the wall: A comparative evaluation of composite-based structural equation modeling methods. Journal of the Academy of Marketing Science, 45(5), 616–632. https://doi.org/10.1007/s11747-017-0517-x

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2012). Partial least squares: The better approach to structural equation modeling? Long Range Planning, 45(5–6), 312–319. https://doi.org/10.1016/j.lrp.2012.09.011

- Hair, J. F., Jr, Sarstedt, M., Hopkins, L., & Kuppelwieser, V. G. (2014). Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. European Business Review. https://www.emerald.com/insight/content/doi/10 .1108/EBR-10-2013-0128/full/html

- Hirth-Goebel, T. F., & Weißenberger, B. E. (2019). Management accountants and ethical dilemmas: How to promote ethical intention? Journal of Management Control, 30(3), 287–322. https://doi.org/10.1007/s00187-019-00288-7

- Jaijairam, P. (2017). Ethics in Accounting. Journal of Finance and Accountancy, 23, 1–13. https://www.researchgate.net/profile/Paul-Jaijairam/publication/321167489_Ethics_in_Accounting/links/5a12cef4aca27287ce2a9b50/Ethics-in-Accounting.pdf

- Jain, B. K. (2020). Business decisions and attitudes towards business ethics of traders in Nepal. International Journal of Business Ethics in Developing Economies, 9(2), 17. https://www.researchgate.net/profile/Bandana-Jain/publication/349847492_Business_Decisions_and_attitudes_towards_Business_ethics_of_traders_in_nepal/links/6043985f4585154e8c8085cd/Business-Decisions-and-attitudes-towards-Business-ethics-of-traders-in-nepal.pdf

- Kakos, S. I. (2019). Against the fallacy of education as a source of ethics. In International Multidisciplinary Scientific Conference on the Dialogue between Sciences & Arts, Religion & Education (Vol. 3, No. 3, pp. 33–41). Ideas Forum International Academic and Scientific Association.

- Kashif, M., Zarkada, A., & Thurasamy, R. (2017). The moderating effect of religiosity on ethical behavioural intentions. Personnel Review, 46(2), 429–448. https://doi.org/10.1108/PR-10-2015-0256

- Khalil, S., & Sidani, Y. (2020). The influence of religiosity on tax evasion attitudes in Lebanon. Journal of International Accounting, Auditing and Taxation, 40, 100335. https://doi.org/10.1016/j.intaccaudtax.2020.100335

- Kohlberg, L. (1969). Stages and sequence: The cognitive-development mental approach to socialization. In McNally, R (Ed.) Handbook of socialization theory and research (pp. 347).

- Lincoln, S. H., & Holmes, E. K. (2008). A need to know: An ethical decision-making model for research administrators. The Journal of Research Administration, 39(1), 41–47. https://eric.ed.gov/?id=EJ888517

- Longenecker, J. G., McKinney, J. A., & Moore, C. W. (2004). Religious intensity, evangelical Christianity, and business ethics: An empirical study. Journal of Business Ethics, 55(4), 371–384. https://doi.org/10.1007/s10551-004-0990-2

- Musbah, A., Cowton, C. J., & Tyfa, D. (2016). The role of individual variables, organisational variables and moral intensity dimensions in Libyan management accountants’ ethical decision making. Journal of Business Ethics, 134(3), 335–358. https://doi.org/10.1007/s10551-014-2421-3

- Nambukara-Gamage, B., & Rahman, S. (2020). Ethics in accounting practices and its influence on business performance. International Journal of Social Sciences, 6(1), 331–348. https://pdfs.semanticscholar.org/8cbb/84d163b5ed4508e0a3a59ea9fd0b524011f9.pdf

- Nitzl, C. (2016). The use of partial least squares structural equation modelling (PLS-SEM) in management accounting research: Directions for future theory development. Journal of Accounting Literature, 37(1), 19–35. https://doi.org/10.1016/j.acclit.2016.09.003

- Papatsouma, I., Mahmoudvand, R., & Farmakis, N. (2019). Evaluating the goodness of the sample coefficient of variation via discrete uniform distribution. Statistics, Optimization & Information Computing, 7(4), 642–652. https://doi.org/10.19139/soic-2310-5070-798

- Parks-Leduc, L., Mulligan, L., & Rutherford, M. A. (2021). Can ethics be taught? Examining the impact of distributed ethical training and individual characteristics on ethical decision-making. Academy of Management Learning & Education, 20(1), 30–49. https://doi.org/10.5465/amle.2018.0157

- Phatshwane, P. M. D. (2013). Ethical perceptions of managers: A preliminary study of small and medium enterprises in Botswana. American International Journal of Contemporary Research, 3(2), 41–48. https://www.aijcrnet.com/journals/Vol_3_No_2_February_2013/5.pdf

- Reath, A. (2020). Kant’s theory of moral sensibility: Respect for the moral law and the influence of inclination. In Pasternack, L. (Ed.) Immanuel Kant: Groundwork of the metaphysic of morals in focus (pp. 211–233). Routledge.

- Remišová, A., Lašáková, A., & Kirchmayer, Z. (2019). Influence of formal ethics program components on managerial ethical behavior. Journal of Business Ethics, 160(1), 151–166. https://doi.org/10.1007/s10551-018-3832-3

- Rest, J. R. (1979). Revised manual for the defined issues test: An objective test of moral judgment development. Minnesota Moral Research Projects.

- Rest, J. R. (1986). Moral development: Advances in research and theory. Praeger.

- Shariff, A. F. (2015). Does religion increase moral behaviour? Current Opinion in Psychology, 6, 108–113. https://doi.org/10.1016/j.copsyc.2015.07.009

- Straub, D. W. (1989). Validating instruments in MIS research. MIS Quarterly, 13(2), 147–169. https://doi.org/10.2307/248922

- Sulaiman, R., Toulson, P., Brougham, D., Lempp, F., & Haar, J. (2021). The role of religiosity in ethical decision-making: A study on Islam and the Malaysian workplace. Journal of Business Ethics, 1–17. https://link.springer.com/article/10 .1007/s10551-021-04836-x

- Sullivan, R. J. (1989). Immanuel Kant’s moral theory. Cambridge University Press.

- Tariq, S., Ansari, N. G., & Alvi, T. H. (2019). The impact of intrinsic and extrinsic religiosity on ethical decision-making in management in a non-Western and highly religious country. Asian Journal of Business Ethics, 8(2), 195–224. https://doi.org/10.1007/s13520-019-00094-3

- Teo, T. S. H., Srivastava, S. C., & Jiang, L. (2008). Trust and electronic government success: An empirical study. Journal of Management Information Systems, 25(3), 99–132. https://doi.org/10.2753/MIS0742-1222250303

- Tittle, C. R., & Welch, M. R. (1983). Religiosity and deviance: Toward a contingency theory of constraining effects. Social Forces, 61(3), 653–682. https://doi.org/10.2307/2578128

- Valentine, S., & Godkin, L. (2019). Moral intensity, ethical decision making, and whistleblowing intention. Journal of Business Research, 98, 277–288. https://doi.org/10.1016/j.jbusres.2019.01.009

- Winston, M. D. (2007). Ethical leadership and ethical decision making: A meta-analysis of research related to ethics education. Library & Information Science Research, 29(2), 230–251. https://doi.org/10.1016/j.lisr.2007.04.002

- Wittmer, D. P. (2019). Ethical decision-making. In Cooper, T.L. (Ed.) Handbook of administrative ethics (pp. 481–507). Routledge.

- Wood, A. W. (2020). Kant and religion. Cambridge University Press.

- Worthington, E. L., Jr., Wade, N. G., Hight, T. L., Ripley, J. S., McCullough, M. E., Berry, J. W., O’Connor, L., Bursley, K. H., O’Connor, L., & Schmitt, M. M. (2003). The religious commitment inventory–10: Development, refinement, and validation of a brief scale for research and counselling. Journal of Counselling Psychology, 50(1), 84–96. https://doi.org/10.1037/0022-0167.50.1.84

- Yoder, D. E., & Denhardt, K. G. (2019). Ethics education in public administration and affairs: Preparing graduates for workplace moral dilemmas. In Cooper, T.L. (Ed.) Handbook of administrative ethics (pp. 59–77). Routledge.

- Zegwaard, K. E., & Campbell, M. (2014). Students’ perceptual change of professional ethics after engaging in work-integrated learning. In 17th New Zealand Association for Cooperative Education Conference (pp. 47–49). New Zealand Association for Cooperative Education.

Appendix

Appendix 1: Adaptation of RC 10

Appendix 2:

Tax ethics vignette

The scenarios that you are about to read are hypothetical and are meant for this research only

Nimo and Kaiza have been friends. Their friendship dates to their university days when they were roommates. Nimo works with Ghana Revenue Authority (GRA) and on one occasion, led a team for tax audit at a company (Freeze Ltd). Kaiza is a senior consultant at a private tax practice firm, and in charge of managing tax affairs of Freeze Ltd. Nimo and Kaiza did not disclose to their long-standing friendship to their respective superiors.

Nimo suspected that Freeze Ltd operates an undisclosed bank account. Kaiza is aware that Freeze Ltd operates a secret bank account but remained quiet when Freeze’s officials denied the allegation. Nimo’s team did not probe the issue further.

Nimo-led team assessed Freeze Ltd.’s tax liability as Ghc450,000. After the field audit, Nimo held a review meeting with his supervisor. At the review meeting, Nimo’s supervisor said, “let the working papers reflect a tax position of GHC80,000; when Freeze Ltd is happy, we are happy as a team” Nimo compiled and reviewed the working papers to reflect a tax position of GHC80,000.